8/13/2019 635264979128106250_Ajanta Pharma_Q3FY14 Result Update

http://slidepdf.com/reader/full/635264979128106250ajanta-pharmaq3fy14-result-update 1/4

‐

50.00

100.00

150.00

200.00

250.00

300.00

350.00

Ajanta Pharma Sensex

IndiaNivesh Research IndiaNivesh Securities Private Limited601 & 602, Sukh Sagar, N. S. Patkar Marg, Girgaum Chowpatty, Mumbai 400 007. Tel: (022) 66188800

Result UpdateJanuary 28, 2014

Ajanta Pharma Ltd.(Standalone)

IndiaNivesh Research is also available on Bloomberg INNS, Thomson First Call, Reuters and Factiva INDNIV.

STOCK INFO

Bse 532331

Nse AJANTPHARM

Bloomberg AJP IN

Reuters AJPH. BO

Sector Pharmaceutical

Face Value (Rs) 5

Equity Capital (Rs mn) 177

Mkt Cap (Rs mn) 32,002

52w H/L (Rs) 1,020/327

Avg Daily Vol (BSE+NSE) 64,567

SHAREHOLDING PATTERN %

(as on 31st Dec. 2013)

Promoters 73.60

FIIs 2.74

DIIs 0.04

Public & Others 23.62

Source: BSE

STOCK PERFORMANCE (%) 1m 3m 12m

AJANTA PHARMA -4.6 9.9 173.1

SENSEX 0.2 1.0 6.1

AJANTA PHARMA v/s SENSEX

Source: Capitaline, IndiaNivesh Research

Source: Capitaline, IndiaNivesh Research

CMP : Rs.904

Rating : BUY

Target : Rs.1,032

Rating : BUY

Target : Rs.1,032

Current Previous

Daljeet S. Kohli

Head of Research

Mobile: +91 77383 93371, 99205 94087

Tel: +91 22 66188826

Bhagwan Singh Chaudhary

Research Analyst

Mobile: +91 77383 93427

Tel: +91 22 66188835

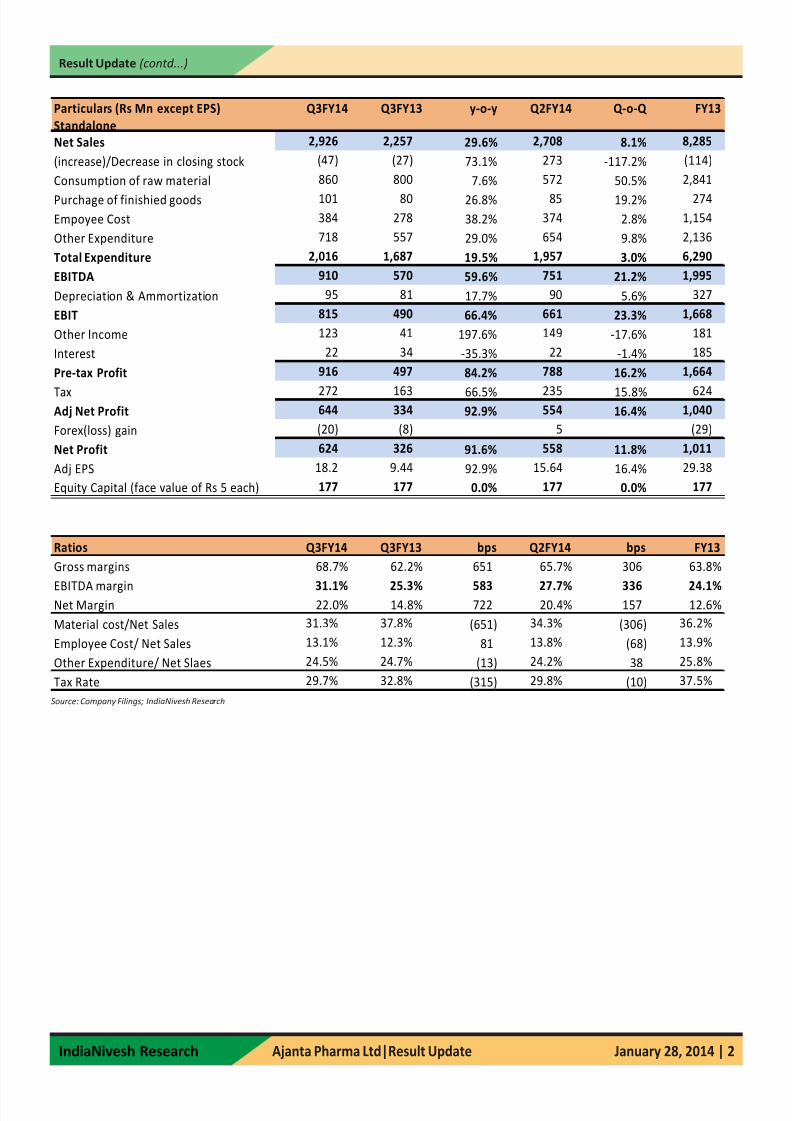

Robust revenue growth driven by exports as well as domestic business:

Ajanta Pharma reported another quarter of robust performance on account of healthy growth across the markets. Company’s total revenue grew ~29.6% y-o-y

(~8% sequentially) to Rs 2,926 mn in Q3 FY14 above our estimates. (INSPL est= Rs

2,776 mn) on account of ~36% revenue growth from domestic business (contributed

33% of total revenue) & ~26% revenue growth from exports.

Domestic business growth of ~36% y-o-y to Rs 970 mn was on account of 40% growth

in Ophthalmology, 33% in Dermatology, 48% in Cardiology segments.

On exports front company’s African business grew ~35% y-o-y to Rs 1150 mn &

Asian region grew 25% y-o-y to Rs 780 mn, while LAta declined 75% y-o-y to Rs 20

mn.

Favorable product mix led to expansion in margins:

Company’s gross margins increased 650 bps y-o-y (~300 bps q-o-q) to 68.7% level

mainly on account of favorable product mix from exports as well as from domestic

market. Inline with gross margins expansion, company’s EBITDA margins grew ~580

bps y-o-y (~330 bps q-o-q) to 31% level (V/s INSPL est=27.1%). Company’s EBITDA

grew ~59.6% y-o y (~21% q-o-q) to Rs 910 mn ( V/s INSPL est= Rs 751 mn).

Net profit grew ~93% y-o-y to Rs 644 mn in Q3FY14:

On account of improved operating leverage & higher other income (mainly linked

with higher exports incentives) Company’s net profit grew 93% y-o-y to Rs 644 mn

in Q3FY14 (V/s INSPL est= Rs 501 mn) in Q3FY14.

Company reported adj EPS of Rs 18.2 in Q3FY14 compared to Rs 9.44 in Q3FY13.

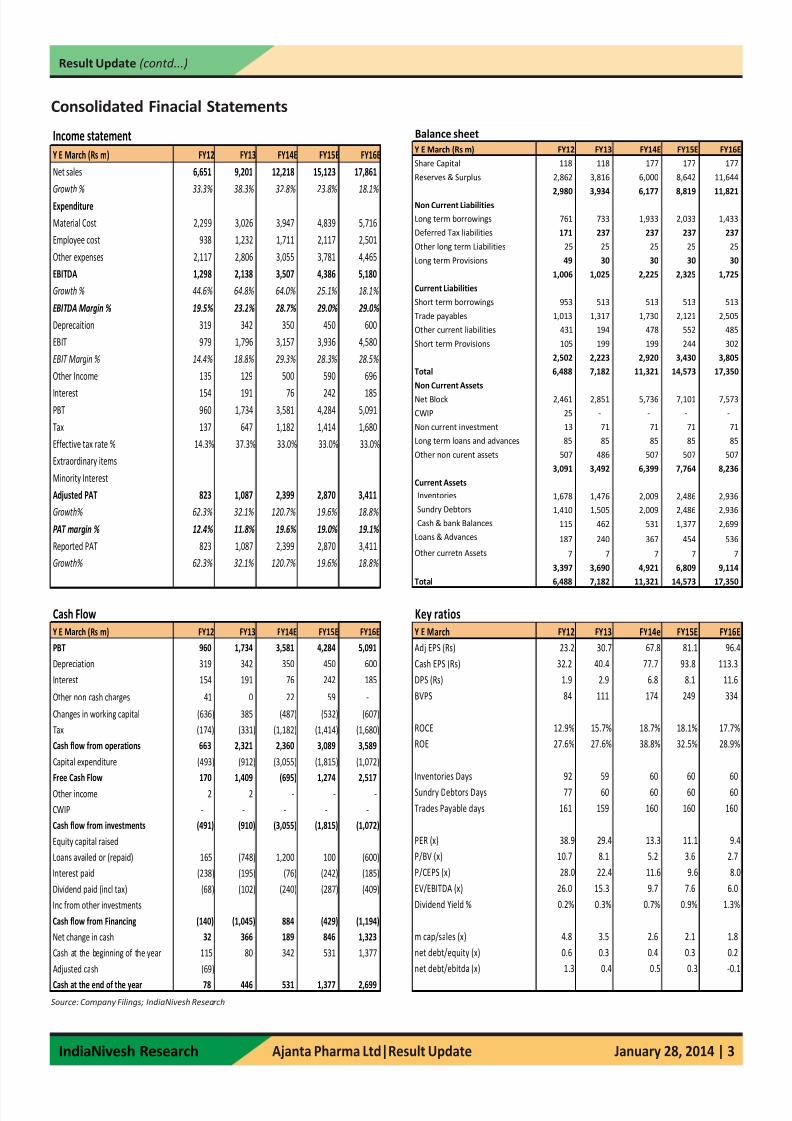

OutlookOn the back of strong growth momentum in domestic market as well as in the

exports in the last 5 years, (During FY08-13), company’s revenue has grown at 24.3%

CAGR & PAT at 38% CAGR. During the same period, benefiting from strategy of

focusing on branded formulations in domestic market, healthy ramp up in exports

business & due to healthy operating leverage, company’s EBITDA margins has

improved by ~650 bps from 16.6% in FY08 to 23.2% in FY13. We expect company’s

EBITDA margins to expand further from 23% level in FY13 to ~29% in FY15E on

account of better product mix & favorable operating leverage. We expect revenue/

net profit CAGR of 28%/60% CAGR during FY13-15E.

ValuationsSince June 2011, we had recommended buy rating on the stock at prevailing adj

market price of Rs 97 level (adjusting 1:1 split & 2:1 bonus issue). Our

recommendation was based on the continuity in robust performance and expansion

in P/E multiple to Industry level. In line with our expectations, company has

maintained robust performance & its valuations have expanded accordingly from

forward P/E multiple of 4-5x to 15x level.

At CMP of Rs 904, the stock is trading at P/E multiple of 13.3x of FY14E & 11.1x of

FY15E earnings estimates. Given continuous out-performance, capacity expansion,

entry into regulated markets & penetration in emerging markets, company’s outlook

seems robust. We believe that valuation gap is likely to narrow down further

between its closest peer of Ipca labs. We continue to maintain BUY rating on the

stock with the target price of Rs 1,032, (which translates to ~13x of FY15E).

Robust performance continues, maintain BUY with the target price of Rs 1,032

8/13/2019 635264979128106250_Ajanta Pharma_Q3FY14 Result Update

http://slidepdf.com/reader/full/635264979128106250ajanta-pharmaq3fy14-result-update 2/4

IndiaNivesh Research Ajanta Pharma Ltd|Result Update

Result Update (contd...)

January 28, 2014 | 2

Source: Company Filings; IndiaNivesh Research

Particulars (Rs Mn except EPS)

Standalone

Q3FY14 Q3FY13 y-o-y Q2FY14 Q-o-Q FY13

Net Sales 2,926 2,257 29.6% 2,708 8.1% 8,285

(increase)/Decrease in closing stock (47) (27) 73.1% 273 -117.2% (114)

Consumption of raw material 860 800 7.6% 572 50.5% 2,841

Purchage of finishied goods 101 80 26.8% 85 19.2% 274

Empoyee Cost 384 278 38.2% 374 2.8% 1,154

Other Expenditure 718 557 29.0% 654 9.8% 2,136

Total Expenditure 2,016 1,687 19.5% 1,957 3.0% 6,290

EBITDA 910 570 59.6% 751 21.2% 1,995

Depreciation & Ammortization 95 81 17.7% 90 5.6% 327

EBIT 815 490 66.4% 661 23.3% 1,668

Other Income 123 41 197.6% 149 -17.6% 181

Interest 22 34 -35.3% 22 -1.4% 185

Pre-tax Profit 916 497 84.2% 788 16.2% 1,664

Tax 272 163 66.5% 235 15.8% 624Adj Net Profit 644 334 92.9% 554 16.4% 1,040

Forex(loss) gain (20) (8) 5 (29)

Net Profit 624 326 91.6% 558 11.8% 1,011

Adj EPS 18.2 9.44 92.9% 15.64 16.4% 29.38

Equity Capital (face value of Rs 5 each) 177 177 0.0% 177 0.0% 177

Ratios Q3FY14 Q3FY13 bps Q2FY14 bps FY13

Gross margins 68.7% 62.2% 651 65.7% 306 63.8%

EBITDA margin 31.1% 25.3% 583 27.7% 336 24.1%Net Margin 22.0% 14.8% 722 20.4% 157 12.6%

Material cost/Net Sales 31.3% 37.8% (651) 34.3% (306) 36.2%

Employee Cost/ Net Sales 13.1% 12.3% 81 13.8% (68) 13.9%

Other Expenditure/ Net Slaes 24.5% 24.7% (13) 24.2% 38 25.8%

Tax Rate 29.7% 32.8% (315) 29.8% (10) 37.5%

8/13/2019 635264979128106250_Ajanta Pharma_Q3FY14 Result Update

http://slidepdf.com/reader/full/635264979128106250ajanta-pharmaq3fy14-result-update 3/4

IndiaNivesh Research Ajanta Pharma Ltd|Result Update

Result Update (contd...)

January 28, 2014 | 3

Source: Company Filings; IndiaNivesh Research

Consolidated Finacial Statements

Income statement

Y E March (Rs m) FY12 FY13 FY14E FY15E FY16E

Net sales 6,651 9,201 12,218 15,123 17,861

Growth % 33.3% 38.3% 32.8% 23.8% 18.1%

Expenditure

Material Cost 2,299 3,026 3,947 4,839 5,716

Employee cost 938 1,232 1,711 2,117 2,501

Other expenses 2,117 2,806 3,055 3,781 4,465

EBITDA 1,298 2,138 3,507 4,386 5,180

Growth % 44.6% 64.8% 64.0% 25.1% 18.1%

EBITDA Margin % 19.5% 23.2% 28.7% 29.0% 29.0%

Deprecaition 319 342 350 450 600

EBIT 979 1,796 3,157 3,936 4,580

EBIT Margin % 14.4% 18.8% 29.3% 28.3% 28.5%

Other Income 135 129 500 590 696

Interest 154 191 76 242 185

PBT 960 1,734 3,581 4,284 5,091

Tax 137 647 1,182 1,414 1,680

Effective tax rate % 14.3% 37.3% 33.0% 33.0% 33.0%

Extraordinary items

Minority Interest

Adjusted PAT 823 1,087 2,399 2,870 3,411

Growth% 62.3% 32.1% 120.7% 19.6% 18.8%

PAT margin % 12.4% 11.8% 19.6% 19.0% 19.1%

Reported PAT 823 1,087 2,399 2,870 3,411

Growth% 62.3% 32.1% 120.7% 19.6% 18.8%

Balance sheet

Y E March (Rs m) FY12 FY13 FY14E FY15E FY16E

Share Capital 118 118 177 177 177

Reserves & Surplus 2,862 3,816 6,000 8,642 11,644

2,980 3,934 6,177 8,819 11,821

Non Current Liabilities

Long term borrowings 761 733 1,933 2,033 1,433

Deferred Tax liabilities 171 237 237 237 237

Other long term Liabilities 25 25 25 25 25

Long term Provisions 49 30 30 30 30

1,006 1,025 2,225 2,325 1,725

Current Liabilities

Short term borrowings 953 513 513 513 513

Trade payables 1,013 1,317 1,730 2,121 2,505

Other current liabilities 431 194 478 552 485

Short term Provisions 105 199 199 244 302

2,502 2,223 2,920 3,430 3,805

Total 6,488 7,182 11,321 14,573 17,350

Non Current Assets

Net Block 2,461 2,851 5,736 7,101 7,573

CWIP 25 - - - -

Non current investment 13 71 71 71 71

Long term loans and advances 85 85 85 85 85

Other non curent assets 507 486 507 507 507

3,091 3,492 6,399 7,764 8,236

Current Assets

Inventories 1,678 1,476 2,009 2,486 2,936

Sundry Debtors 1,410 1,505 2,009 2,486 2,936

Cash & bank Balances 115 462 531 1,377 2,699

Loans & Advances 187 240 367 454 536

Other curretn Assets 7 7 7 7 7

3,397 3,690 4,921 6,809 9,114

Total 6,488 7,182 11,321 14,573 17,350

Cash Flow

Y E March (Rs m) FY12 FY13 FY14E FY15E FY16E

PBT 960 1,734 3,581 4,284 5,091

Depreciation 319 342 350 450 600

Interest 154 191 76 242 185

Other non cash charges 41 0 22 59 -

Changes in working capital (636) 385 (487) (532) (607)

Tax (174) (331) (1,182) (1,414) (1,680)

Cash flow from operations 663 2,321 2,360 3,089 3,589

Capital expenditure (493) (912) (3,055) (1,815) (1,072)

Free Cash Flow 170 1,409 (695) 1,274 2,517

Other income 2 2 - - -

CWIP - - - - -

Cash flow from investments (491) (910) (3,055) (1,815) (1,072)

Equity capital raised

Loans availed or (repaid) 165 (748) 1,200 100 (600)

Interest paid (238) (195) (76) (242) (185)

Dividend paid (incl tax) (68) (102) (240) (287) (409)

Inc from other investments

Cash flow from Financing (140) (1,045) 884 (429) (1,194)

Net change in cash 32 366 189 846 1,323

Cash at the beginning of the year 115 80 342 531 1,377

Adjusted cash (69)

Cash at the end of the year 78 446 531 1,377 2,699

Key ratios

Y E March FY12 FY13 FY14e FY15E FY16E

Adj EPS (Rs) 23.2 30.7 67.8 81.1 96.4

Cash EPS (Rs) 32.2 40.4 77.7 93.8 113.3

DPS (Rs) 1.9 2.9 6.8 8.1 11.6

BVPS 84 111 174 249 334

ROCE 12.9% 15.7% 18.7% 18.1% 17.7%

ROE 27.6% 27.6% 38.8% 32.5% 28.9%

Inventories Days 92 59 60 60 60

Sundry Debtors Days 77 60 60 60 60

Trades Payable days 161 159 160 160 160

PER (x) 38.9 29.4 13.3 11.1 9.4

P/BV (x) 10.7 8.1 5.2 3.6 2.7

P/CEPS (x) 28.0 22.4 11.6 9.6 8.0

EV/EBITDA (x) 26.0 15.3 9.7 7.6 6.0

Dividend Yield % 0.2% 0.3% 0.7% 0.9% 1.3%

m cap/sales (x) 4.8 3.5 2.6 2.1 1.8

net debt/equity (x) 0.6 0.3 0.4 0.3 0.2

net debt/ebitda (x) 1.3 0.4 0.5 0.3 -0.1

8/13/2019 635264979128106250_Ajanta Pharma_Q3FY14 Result Update

http://slidepdf.com/reader/full/635264979128106250ajanta-pharmaq3fy14-result-update 4/4

Recommended

![Result Update Presentation Q1 FY 16 [Company Update]](https://img.pdfslide.us/doc/110x75/577cb2961a28aba7118c175a/result-update-presentation-q1-fy-16-company-update.jpg)

![Financial Result Updates [Company Update]](https://img.pdfslide.us/doc/110x75/577c78191a28abe0548eb963/financial-result-updates-company-update.jpg)