Embed Size (px)

Citation preview

25%

30%

35%

40%

45%

50%

1917

19

22

1927

19

32

1937

19

42

1947

19

52

1957

19

62

1967

19

72

1977

19

82

1987

19

92

1997

20

02

2007

20

12

Top

10%

Inco

me

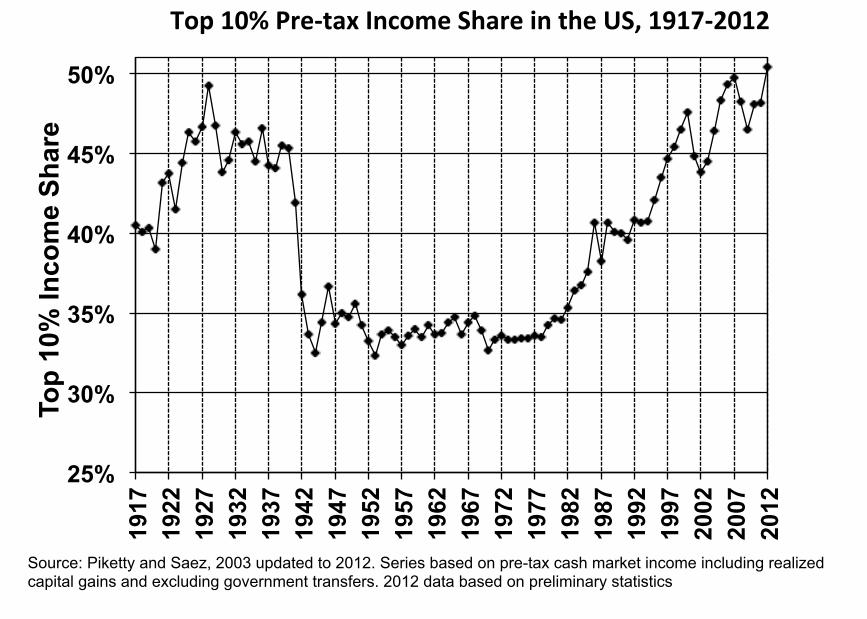

Shar

e Top 10% Pre-‐tax Income Share in the US, 1917-‐2012

Source: Piketty and Saez, 2003 updated to 2012. Series based on pre-tax cash market income including realized capital gains and excluding government transfers. 2012 data based on preliminary statistics

0%

5%

10%

15%

20%

25%

1913

19

18

1923

19

28

1933

19

38

1943

19

48

1953

19

58

1963

19

68

1973

19

78

1983

19

88

1993

19

98

2003

20

08

Shar

e of

tota

l inc

ome

for e

ach

grou

p

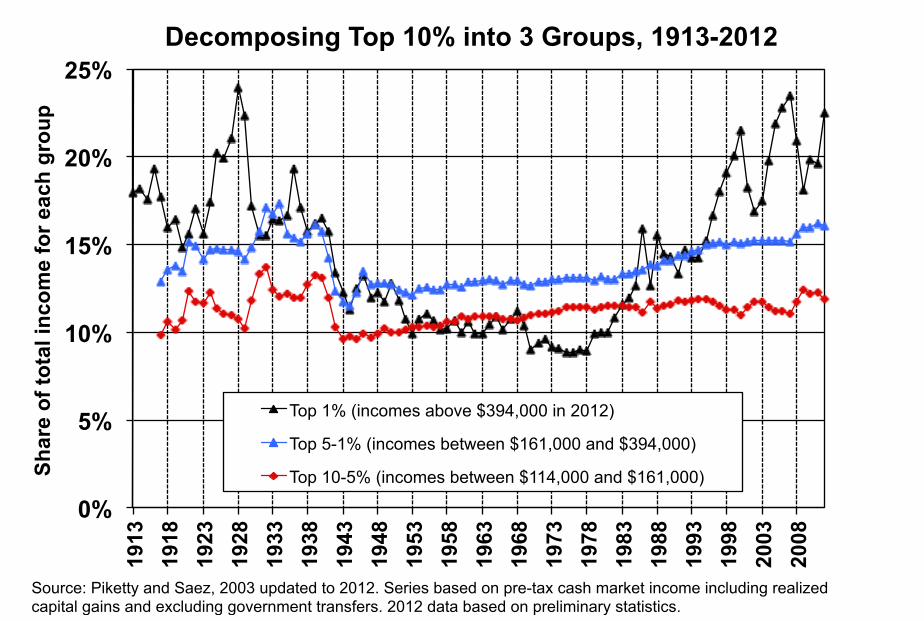

Decomposing Top 10% into 3 Groups, 1913-2012

Top 1% (incomes above $394,000 in 2012)

Top 5-1% (incomes between $161,000 and $394,000)

Top 10-5% (incomes between $114,000 and $161,000)

Source: Piketty and Saez, 2003 updated to 2012. Series based on pre-tax cash market income including realized capital gains and excluding government transfers. 2012 data based on preliminary statistics.

Public Finance and Public Policy Jonathan Gruber Third Edition Copyright © 2010 Worth Publishers

C H A P T E R 1 ■ W H Y S T U D Y P U B L I C E C O N O M I C S ?

11 of 24

The Congressional Budget Office: Government Scorekeepers � The methods and results derived from empirical economics

are central to the development of public policy at all levels of government.

� The Congressional Budget Office (CBO) provides Congress with the objective, timely, nonpartisan analyses needed for economic and budget decisions.

� The CBO increasingly plays a critical role as a “scorekeeper” for government policy debates.

� Legislative spending proposals that are to become law must first have their costs estimated by the analysts at the CBO.

It is not an overstatement to say that the economists who work at the CBO frequently hold the fate of a legislative proposal in their hands. The large price tag that the CBO assigned to the Clinton administration’s plan to reform health care in the United States in 1994 is often cited as a key factor in the defeat of that proposal.

1.1

The Four Questions of Public Finance APPLICATION �

�

2A. Tax revenue/GDP in the US, UK, and Sweden

0%

10%

20%

30%

40%

50%

60%18

68

1878

1888

1898

1908

1918

1928

1938

1948

1958

1968

1978

1988

1998

2008

Tota

l Tax

Rev

enue

/GD

P

United States

United Kingdom

Sweden

Source: Kleven-Kreiner-Saez NBER WP 2009

Public Finance and Public Policy Jonathan Gruber Fourth Edition Copyright © 2012 Worth Publishers

C H A P T E R 1 ■ W H Y S T U D Y P U B L I C E C O N O M I C S ?

15 of 32

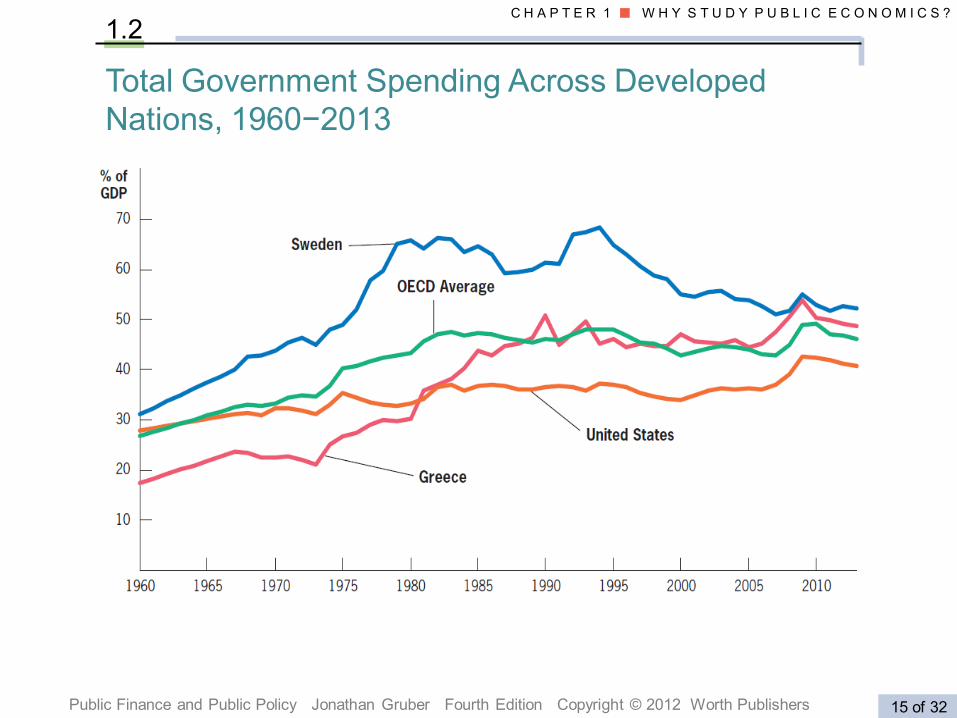

1.2

Total Government Spending Across Developed Nations, 1960−2013

Public Finance and Public Policy Jonathan Gruber Fourth Edition Copyright © 2012 Worth Publishers

C H A P T E R 1 ■ W H Y S T U D Y P U B L I C E C O N O M I C S ?

18 of 32

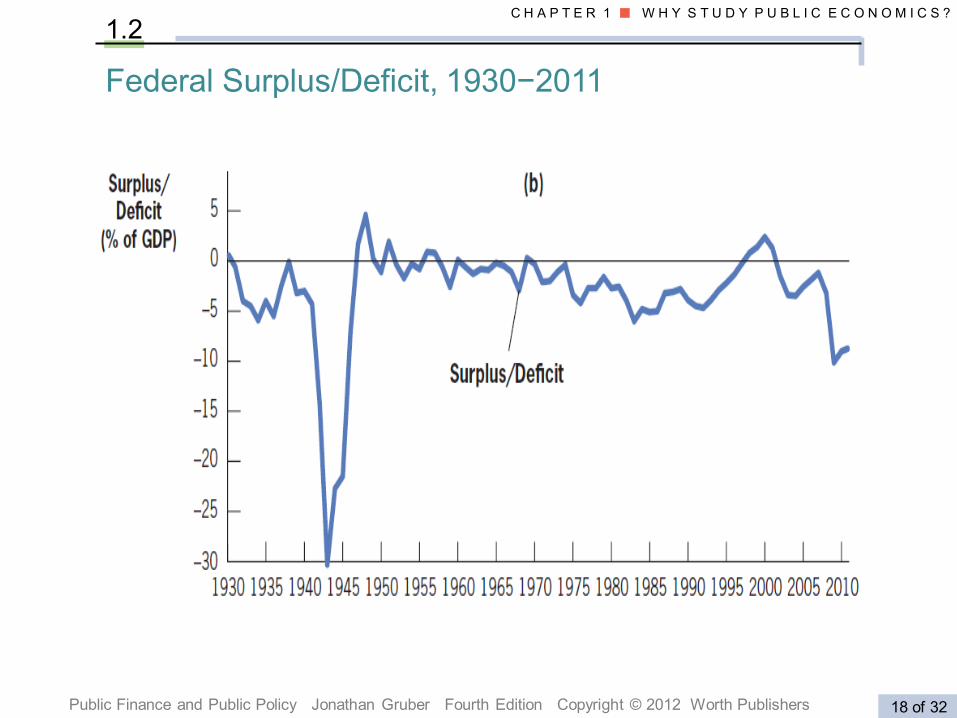

Federal Surplus/Deficit, 1930−2011

1.2

Public Finance and Public Policy Jonathan Gruber Fourth Edition Copyright © 2012 Worth Publishers

C H A P T E R 1 ■ W H Y S T U D Y P U B L I C E C O N O M I C S ?

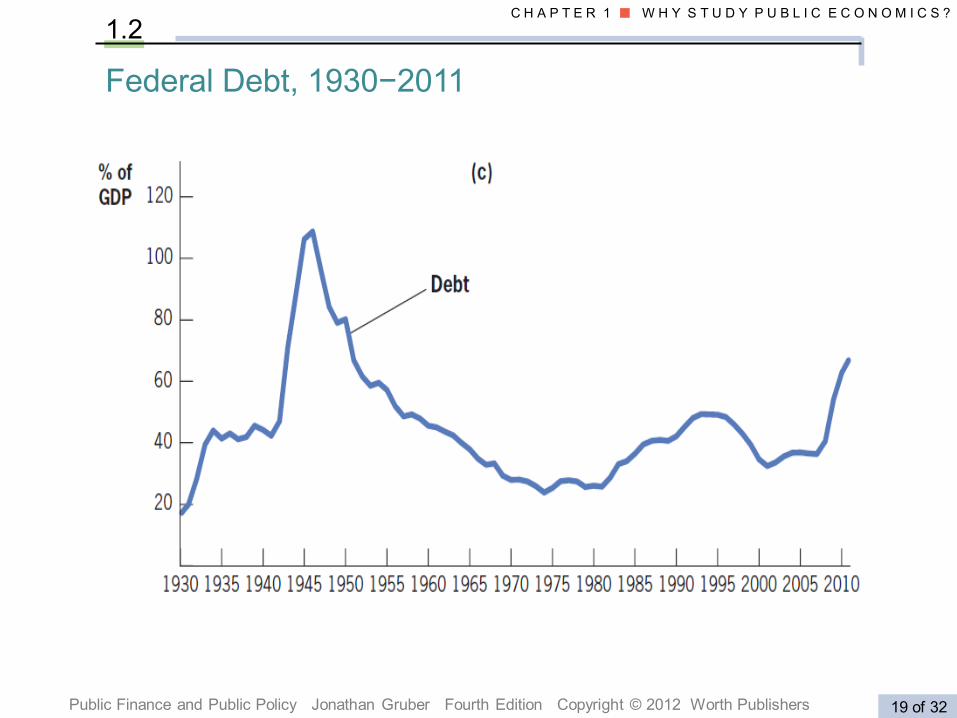

19 of 32

Federal Debt, 1930−2011

1.2

Public Finance and Public Policy Jonathan Gruber Fourth Edition Copyright © 2012 Worth Publishers

C H A P T E R 1 ■ W H Y S T U D Y P U B L I C E C O N O M I C S ?

20 of 32

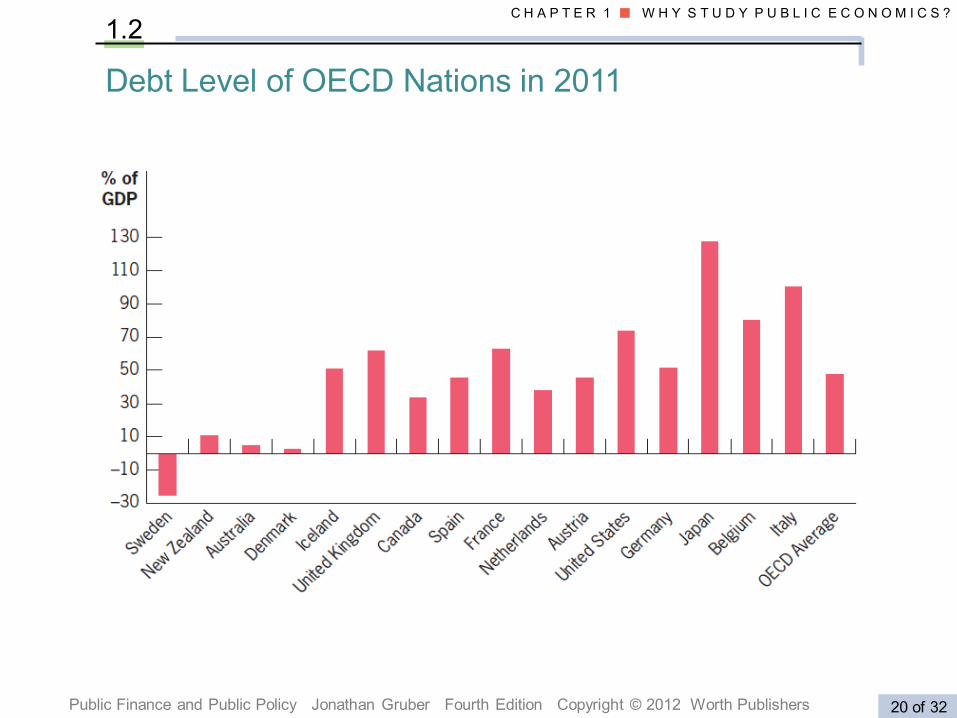

1.2

Debt Level of OECD Nations in 2011

Public Finance and Public Policy Jonathan Gruber Third Edition Copyright © 2010 Worth Publishers

C H A P T E R 1 ■ W H Y S T U D Y P U B L I C E C O N O M I C S ?

16 of 24

Decentralization

Why Study Public Finance? Facts on Government in the United States and around the World

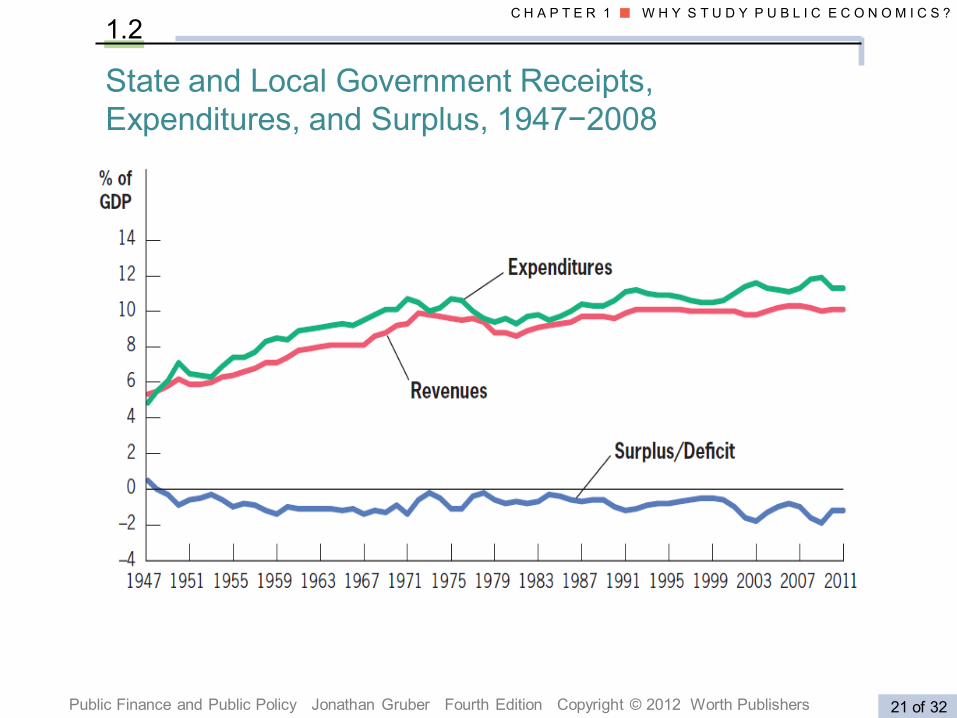

A key feature of governments is the degree of centralization across local and national government units—that is, the extent to which spending is concentrated at higher (federal) levels or lower (state and local) levels.

1.2

Public Finance and Public Policy Jonathan Gruber Fourth Edition Copyright © 2012 Worth Publishers

C H A P T E R 1 ■ W H Y S T U D Y P U B L I C E C O N O M I C S ?

21 of 32

1.2

State and Local Government Receipts, Expenditures, and Surplus, 1947−2008

Public Finance and Public Policy Jonathan Gruber Third Edition Copyright © 2010 Worth Publishers

C H A P T E R 1 ■ W H Y S T U D Y P U B L I C E C O N O M I C S ?

21 of 24

Distribution of Spending

1.2

The Distribution of Federal and State Expenditures, 1960 and 2007 • This figure shows the changing composition of federal and state spending over time, as a share of total spending. (a) For the federal government, defense spending has fallen and Social Security and health spending have risen. (b) For the states, the distribution has been more constant, with a small decline in education and welfare spending and a rise in health spending.

Public Finance and Public Policy Jonathan Gruber Third Edition Copyright © 2010 Worth Publishers

C H A P T E R 1 ■ W H Y S T U D Y P U B L I C E C O N O M I C S ?

22 of 24

Distribution of Revenue Sources

1.2

The Distribution of Federal and State Revenues, 1960 and 2008 • This figure shows the changing composition of federal and state revenue sources over time, as a share of total revenues. (a) At the federal level, there has been a large reduction in corporate and excise tax revenues and a rise in payroll tax revenues. (b) For the states, there has been a decline in property taxes and a rise in income taxes and federal grants.

20%

30%

40%

50%

60%

Tota

l tax

reve

nues

(% n

atio

nal i

ncom

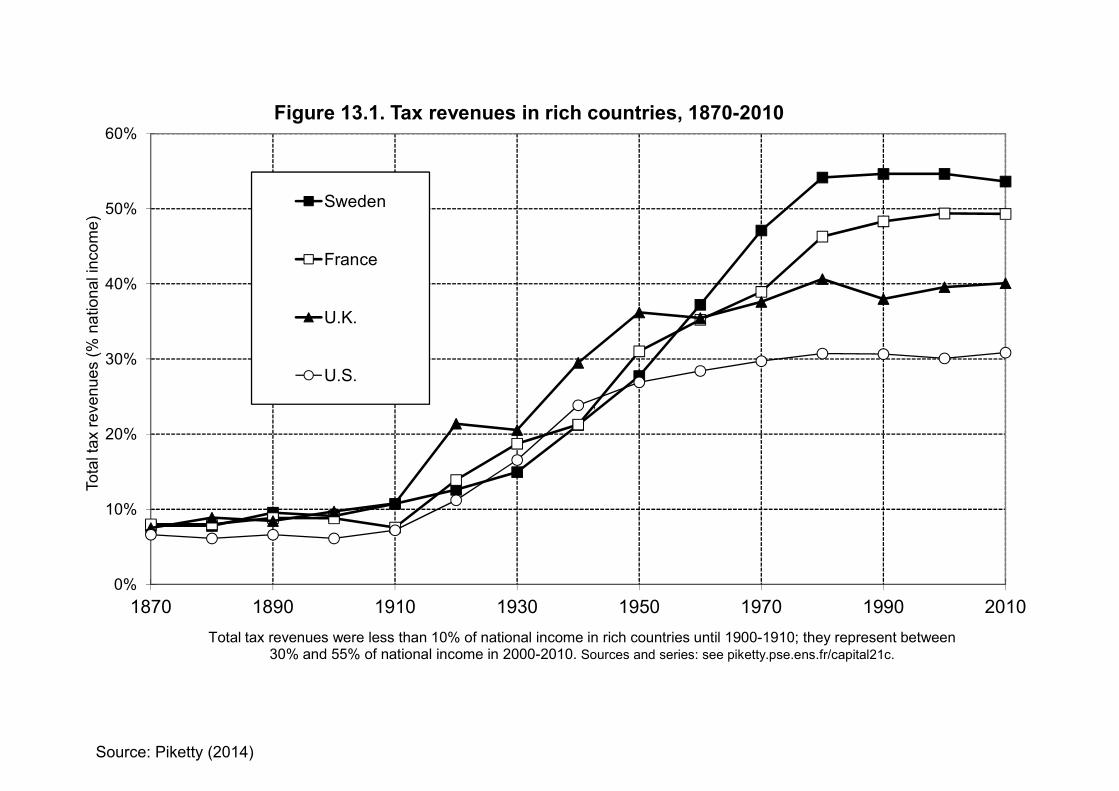

e)Figure 13.1. Tax revenues in rich countries, 1870-2010

Sweden

France

U.K.

U.S.,

0%

10%

1870 1890 1910 1930 1950 1970 1990 2010

Tota

l tax

reve

nues

(% n

atio

nal i

ncom

e)

Total tax revenues were less than 10% of national income in rich countries until 1900-1910; they represent between 30% and 55% of national income in 2000-2010. Sources and series: see piketty.pse.ens.fr/capital21c.

Source: Piketty (2014)

25%

30%

35%

40%

45%

50%

1917

1922

1927

1932

1937

1942

1947

1952

1957

1962

1967

1972

1977

1982

1987

1992

1997

2002

2007

2012

2017

% o

f nat

iona

l inc

ome

Share of pre-tax national income going to top 10% adults

Pre-tax

Source: Piketty, Saez, and Zucman (2018)

0

10,000

20,000

30,000

40,000

50,000

60,000 19

62

1966

1970

1974

1978

1982

1986

1990

1994

1998

2002

2006

2010

2014

Aver

age

inco

me

in c

onst

ant 2

014

dolla

rs

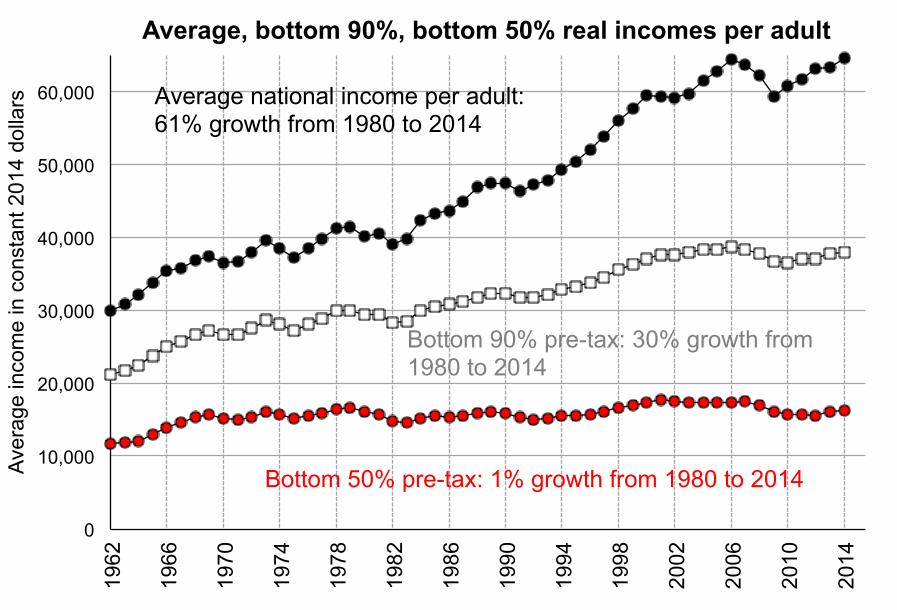

Average, bottom 90%, bottom 50% real incomes per adult

Average national income per adult: 61% growth from 1980 to 2014

Bottom 50% pre-tax: 1% growth from 1980 to 2014

Bottom 90% pre-tax: 30% growth from 1980 to 2014

10%

12%

14%

16%

18%

20%

22%

1962

1966

1970

1974

1978

1982

1986

1990

1994

1998

2002

2006

2010

2014

% o

f nat

iona

l inc

ome

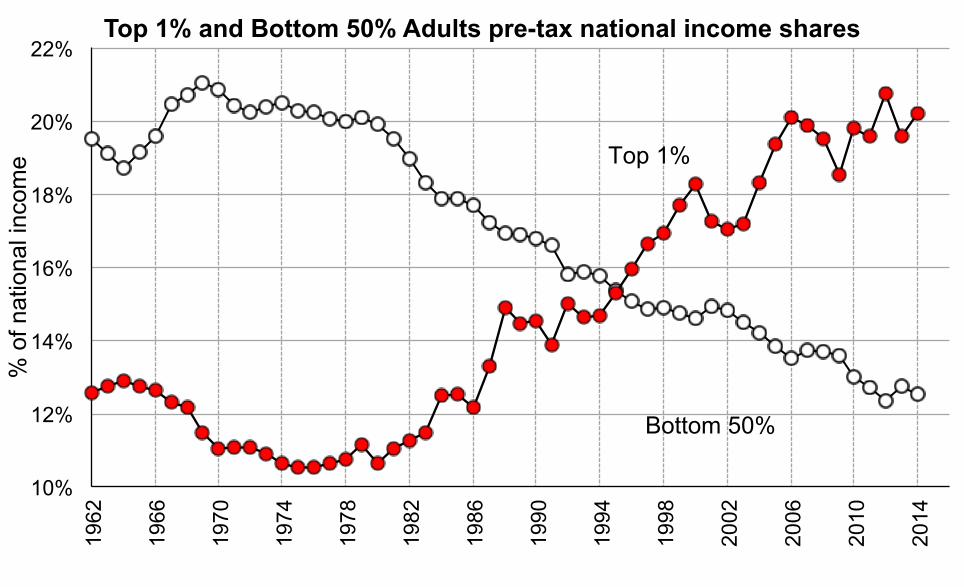

Top 1% and Bottom 50% Adults pre-tax national income shares

Bottom 50%

Top 1%

25%

30%

35%

40%

45%

50%

1917

1922

1927

1932

1937

1942

1947

1952

1957

1962

1967

1972

1977

1982

1987

1992

1997

2002

2007

2012

2017

% o

f nat

iona

l inc

ome

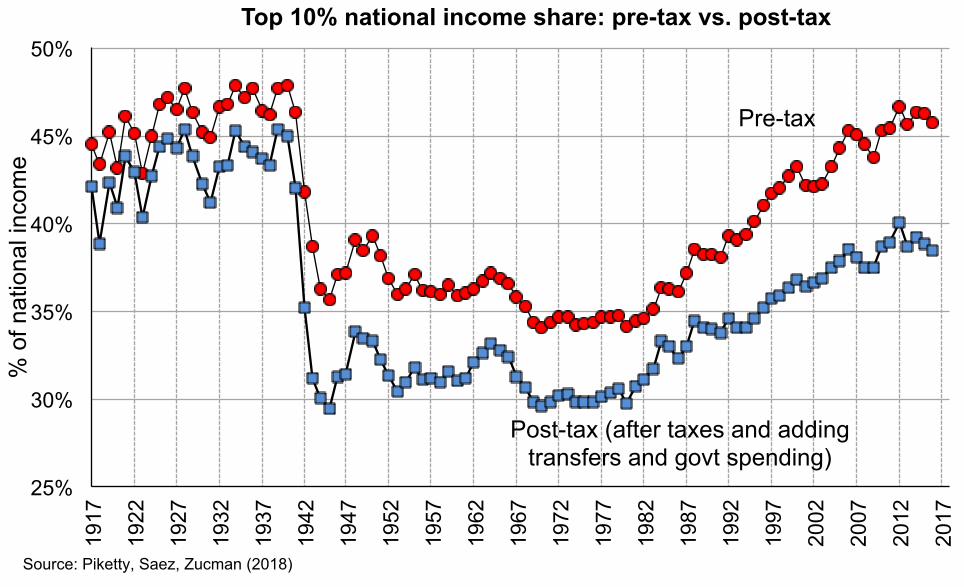

Top 10% national income share: pre-tax vs. post-tax

Pre-tax

Post-tax (after taxes and adding transfers and govt spending)

Source: Piketty, Saez, Zucman (2018)

0

10,000

20,000

30,000

40,000

50,000

60,000 19

62

1966

1970

1974

1978

1982

1986

1990

1994

1998

2002

2006

2010

2014

Aver

age

inco

me

in c

onst

ant 2

014

dolla

rs

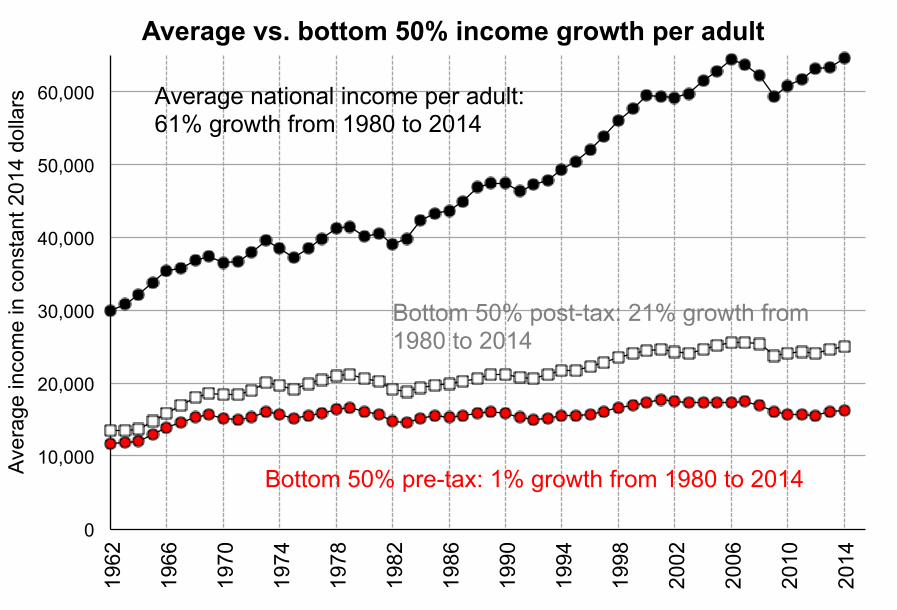

Average vs. bottom 50% income growth per adult

Average national income per adult: 61% growth from 1980 to 2014

Bottom 50% pre-tax: 1% growth from 1980 to 2014

Bottom 50% post-tax: 21% growth from 1980 to 2014

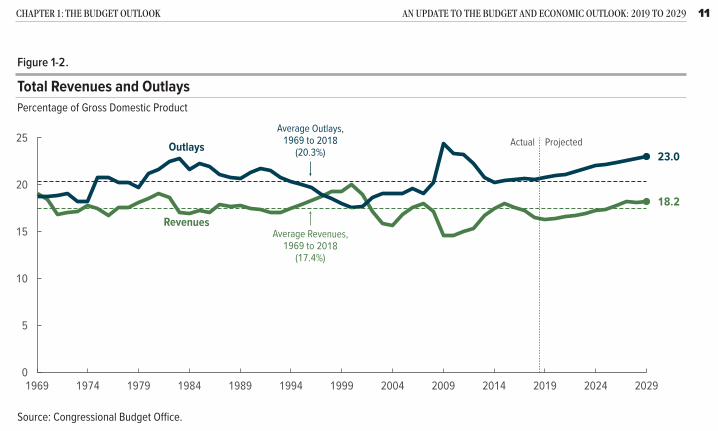

11chApteR 1: the BUdget oUtlook An UpdAte to the BUdget And economic oUtlook: 2019 to 2029

2017 tax act.) Federal outlays, adjusted to exclude shifts in the timing of certain payments, are projected to climb from 21.0 percent of GDP in 2020 to 23.0 percent in 2029 (see Figure 1-2).

Deficits are projected to average 4.7 percent of GDP over the 2020–2029 period. Over the past 50 years, deficits have averaged 2.9 percent of GDP; and in years when the unemployment rate has been below 6 percent, deficits averaged just 1.5 percent of GDP.

Primary deficits—that is, deficits excluding net outlays for interest—are projected to decrease over time, averag-ing 2.7 percent of GDP from 2020 through 2024 and 2.2 percent from 2025 through 2029. At the same time, because of projected increases in interest rates and fed-eral borrowing, net interest outlays grow steadily, from 1.8 percent of GDP in 2020 to 2.6 percent in 2029 (see Figure 1-3 on page 14).

Those deficits are projected to boost federal debt held by the public, which consists mostly of the securities that the Treasury issues to raise cash to fund federal activities and pay off the government’s maturing liabilities. The

net amount that the Treasury borrows by issuing those securities (calculated as the amounts that are sold minus the amounts that have matured) is influenced primarily by the annual budget deficit.

Consequently, under current law, debt held by the public would increase in upcoming years. In CBO’s baseline, after accounting for all of the government’s borrowing needs, debt held by the public rises from $17.8 trillion at the end of 2020 to $29.3 trillion at the end of 2029 (see Table 1-3 on page 15). As a percentage of GDP, that debt would increase from 79 percent in 2019 to 95 per-cent by the end of the projection period (see Figure 1-4 on page 16). At that point, such debt would be the largest since 1946 and more than twice the 50-year average.

Outlays Over the coming decade, CBO projects, federal outlays would grow at an average annual rate of 5 percent, reach-ing $7.1 trillion in 2029 (adjusted to exclude the effects of timing shifts). Outlays for Social Security, Medicare, and net interest account for about two-thirds of that $2.7 trillion increase.

Figure 1-2 .

Total Revenues and OutlaysPercentage of Gross Domestic Product

●

●

18.2

23.0ProjectedActual

0

5

10

15

20

25

1969 1974 1979 1984 1989 1994 1999 2004 2009 2014 2019 2024 2029

Outlays

Average Outlays,1969 to 2018

(20.3%)

Average Revenues,1969 to 2018

(17.4%)

Revenues

Source: Congressional Budget Office.

When October 1 (the first day of the fiscal year) falls on a weekend, certain payments that would have ordinarily been made on that day are instead made at the end of September and thus are shifted into the previous fiscal year. All projections presented here have been adjusted to exclude the effects of those timing shifts. Historical amounts have been adjusted as far back as the available data will allow.

0%5%

10%15%20%25%30%35%40%45%

Average tax rates by income group in 2018 (% of pre-tax income)

Corporate & property taxesConsumption taxes

Payroll taxesIndividual income taxes

Estate tax

Source: Saez and Zucman (2019)

0%

10%

20%

30%

40%

50%

60%

1870 1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010

Use

s of

fisc

al re

venu

es a

s %

nat

iona

l inc

ome

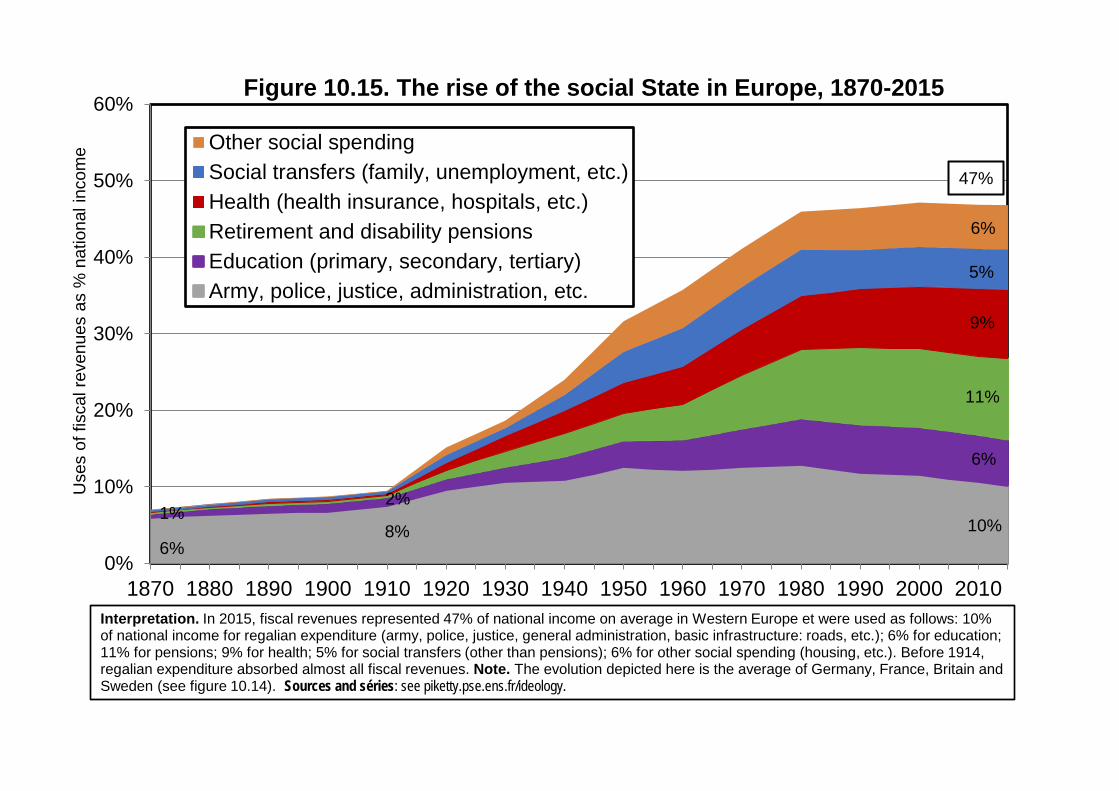

Figure 10.15. The rise of the social State in Europe, 1870-2015

Other social spendingSocial transfers (family, unemployment, etc.)Health (health insurance, hospitals, etc.)Retirement and disability pensionsEducation (primary, secondary, tertiary)Army, police, justice, administration, etc.

6%

10%

11%

Interpretation. In 2015, fiscal revenues represented 47% of national income on average in Western Europe et were used as follows: 10% of national income for regalian expenditure (army, police, justice, general administration, basic infrastructure: roads, etc.); 6% for education; 11% for pensions; 9% for health; 5% for social transfers (other than pensions); 6% for other social spending (housing, etc.). Before 1914, regalian expenditure absorbed almost all fiscal revenues. Note. The evolution depicted here is the average of Germany, France, Britain and Sweden (see figure 10.14). Sources and séries: see piketty.pse.ens.fr/ideology.

9%

8%

6%

5%

2%

6%

1%

47%

0%

10%

20%

30%

40%

50%

60%

1870 1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010

Tota

l tax

reve

nues

as

% n

atio

nal i

ncom

e

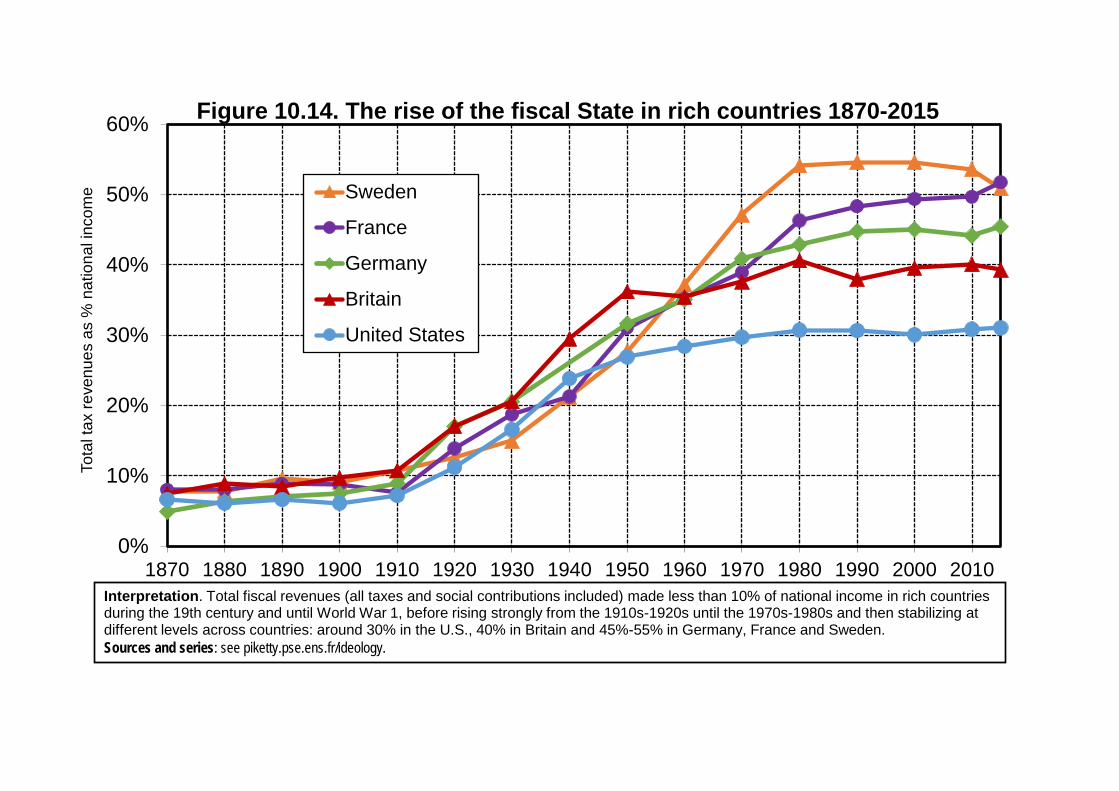

Figure 10.14. The rise of the fiscal State in rich countries 1870-2015

Sweden

France

Germany

Britain

United States

Interpretation. Total fiscal revenues (all taxes and social contributions included) made less than 10% of national income in rich countriesduring the 19th century and until World War 1, before rising strongly from the 1910s-1920s until the 1970s-1980s and then stabilizing at different levels across countries: around 30% in the U.S., 40% in Britain and 45%-55% in Germany, France and Sweden. Sources and series: see piketty.pse.ens.fr/ideology.et

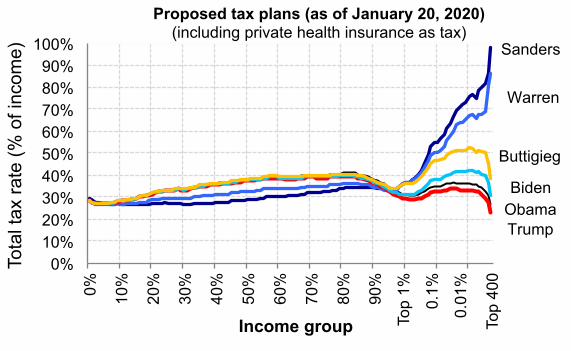

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

100%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Top

1%

0.1%

0.01

%

Top

400

Tota

l tax

rate

(% o

f inc

ome)

Income group

Proposed tax plans (as of January 20, 2020) (including private health insurance as tax)

Sanders

Warren

Biden

Trump

Buttigieg

Obama

![Gini Coefficient California pre-tax income, 2000, Gini=62.1%saez/course131/taxintro_ch17_new_attach.pdfFigure 1: Gini coefficient 6RXUFH .RSF]XN 6DH] 6RQJ4-( :DJHHDUQLQJVLQHTXDOLW\](https://img.pdfslide.us/doc/110x75/5f9d687763df8333422405c5/gini-coefficient-california-pre-tax-income-2000-gini621-saezcourse131taxintroch17newattachpdf.jpg)