Embed Size (px)

Citation preview

MARKETVIEW

Occupier and investment markets

enjoy steady start to the year

Asia Pacific, Q1 2017

OFFICE

RETAIL

LOGISTICS

INVESTMENT

Q1 2017 CBRE Research © CBRE Inc. 2017 | 1

Quick Stats

Office q-o-q y-o-y

Rent +0.6% +2.1%

Capital value +0.7% +4.7%

Retail q-o-q y-o-y

Rent + 0.6% + 1.0%

Capital value +0.6% +3.1%

Logistics q-o-q y-o-y

Rent +0.2% +0.6%

Capital value +0.9% +5.6%

Investment* q-o-q y-o-y

Total volume -39% +6.2%

Cross-border -38% +33%

Source: CBRE Research, Q1 2017.

*Transactions include deals above US$10

million in the office, retail, mixed, industrial,

hotel and other commercial sectors

+4.4% in 2017F Q2 2017 +4.1% in 2017F

MARKETVIEW

ECONOMIC OUTLOOK IMPROVES

LOW INTEREST RATE ENVIRONMENT PERSISTS

Figure 1: Asia Pacific 2016 and 2017 GDP Forecast Growth (%, Y-o-Y)

Q1 2017 CBRE Research © CBRE Inc. 2017 | 2

ASIA PACIFIC Q1 2017

Table 1: Policy Interest Rate Changes

Source: Oxford Economics, April 2017.

Note on policy interest rates: Australia - Cash rate, China - 1 Yr lending

rate, Hong Kong – 3M HIBOR, India - Repo rate , Indonesia – 7-days

Repo rate, New Zealand - Official Cash Rate, Singapore – 3M SIBOR,

South Korea - Base rate, Taiwan – Discount Rate, Thailand -1-day repo

rate.

Source: CBRE Research, Various Central Banks and Monetary Authorities, Q1

2017.

ECONOMY

Market

End of

March

2017, %

Number of

rate cuts in

Q1 2017

Change

in Q1

2017

Australia 1.5 0 0 bps

China 4.35 0 0 bps

Hong Kong 1.02 0 -8 bps

India 6.25 0 0 bps

Indonesia 4.75 0 0 bps

New Zealand 1.75 0 0 bps

Singapore 0.97 0 -3 bps

South Korea 1.25 0 0 bps

Taiwan 1.375 0 0 bps

Thailand 1.5 0 0 bps

0

1

2

3

4

5

6

7

8

India

Vie

tnam

Chin

a

Philip

pin

es

Indonesia

Mala

ysia

New

Zeala

nd

Thailand

Austr

alia

Sin

gapore

Hong K

ong

South

Kore

a

Taiw

an

Japan

Asia

Pacific

2016E 2017F

MARKETVIEW

Figure 2: Office Net Absorption (‘000s sq. ft.)

© CBRE Inc. 2017 | 3

ASIA PACIFIC Q1 2017

Table 2: Major New Office Supply in Q1 2017

Figure 3: Vacancy Rate and Development Pipeline

Source: CBRE Research, Q1 2017.

Source: CBRE Research, Q1 2017.

Source: CBRE Research, Q1 2017.

Note: Q4 2016 vacancy rate are used for the Pacific markets.

OFFICE 0.0% y-o-y 0.7% q-o-q 0.6% q-o-q

Q1 2017 CBRE Research

LARGE PRE-COMMITMENTS DISTORT DEMAND

SUPPLY PIPELINE REMAINS SUBSTANTIAL

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Q1 Q2 Q3 Q4 Annual New Supply

Market Development Name Estimated Size

(sq. ft.)

Shanghai Shanghai Tower 2,150,000

Shenzhen PingAn IFC North Tower 1,560,000

Shanghai Landmark Center 1,160,000

Beijing CSCEC-1 540,000

Singapore GSH Plaza 282,000

Mumbai Zillion - Phase II 250,000

0

10

20

30

40

50

60

70

80

Hanoi

Jakart

a

Shanghai

Shenzhen

Mum

bai

HCM

C

Guangzhou

Pert

h

New

Delh

i

Bangalo

re

Taip

ei

Canberr

a

Beijin

g

Tokyo

Adela

ide

Seoul

Brisbane

Bangkok

Manila (

Makati)

Sin

gapore

Auckla

nd

Hong K

ong

Sydney

Wellin

gto

n

Melb

ourn

eVacancy &

develo

pm

ent pip

eline a

s %

of sto

ck

Development Pipeline end of Q1 2017 to end of 2018

Current Vacancy Rate (Q1 2017)

MARKETVIEW

Figure 4: Asia Pacific Vacancy Rate (%)

Q1 2017 CBRE Research © CBRE Inc. 2017 | 4

ASIA PACIFIC Q1 2017

Figure 5: Asia Pacific Office Rental and Capital Value Index

Figure 6: Strongest Grade A Rental Growth, Q-o-Q

Source: CBRE Research, Q1 2017.

Source: CBRE Research, Q1 2017.

Source: CBRE Research, Q1 2017.

VACANCY RATE SET TO INCREASE

RENTS RECORD SLIGHT GROWTH

0

2

4

6

8

10

12

14

16

H2

01

H2

02

H2

03

H2

04

H2

05

H2

06

H2

07

H2

08

H2

09

H2 1

0

H2

11

H2

12

H2

13

H2

14

H2 1

5

H2

16

Vacancy R

ate

(%

)

Asia

Pacific

Asia Pacific

50

75

100

125

150

175

200

225

250

275

200

1 Q

1

200

2 Q

1

200

3 Q

1

200

4 Q

1

200

5 Q

1

200

6 Q

1

200

7 Q

1

200

8 Q

1

200

9 Q

1

201

0 Q

1

201

1 Q

1

201

2 Q

1

201

3 Q

1

201

4 Q

1

201

5 Q

1

201

6 Q

1

201

7 Q

1

Index Q

1 2

00

1 =

100

Rental Value Index Capital Value Index

0%

1%

2%

3%

4%

Sydney Melbourne Shenzhen Hong Kong Bangkok

MARKETVIEW

CAUTION GUIDES RETAIL LEASING ACTIVITY

Figure 8: Y-o-Y Growth in Mainland Chinese Tourist Arrivals in Q1 2017

Q1 2017 CBRE Research © CBRE Inc. 2017 | 5

ASIA PACIFIC Q1 2017

Source: CBRE Research, Q1 2017.

0%

10%

20%

30%

40%

50%

Coffee and

Restaurants

Specialist

Clothing

Luxury and

Business

Mid Range

Fashion

Value and

Denim

2014 2015 2016 Q1 2017

RETAIL 18% y-o-y 0.6% q-o-q 0.6% q-o-q

Figure 7: New Retail Entrants by Sector

-60%

-40%

-20%

0%

20%

40%

60%

80%

Vie

tnam

Hong K

ong

Sin

gapore

Japan

Austr

alia

New

Zeala

nd

Thailand

South

Kore

a

Taiw

an

2016 2017

Note on y-o-y growth: Hong Kong, Singapore and Australia are

cumulative growth of Jan-Feb 2017

Source: CEIC, April 2017.

Improved Slower Growth

MARKETVIEW

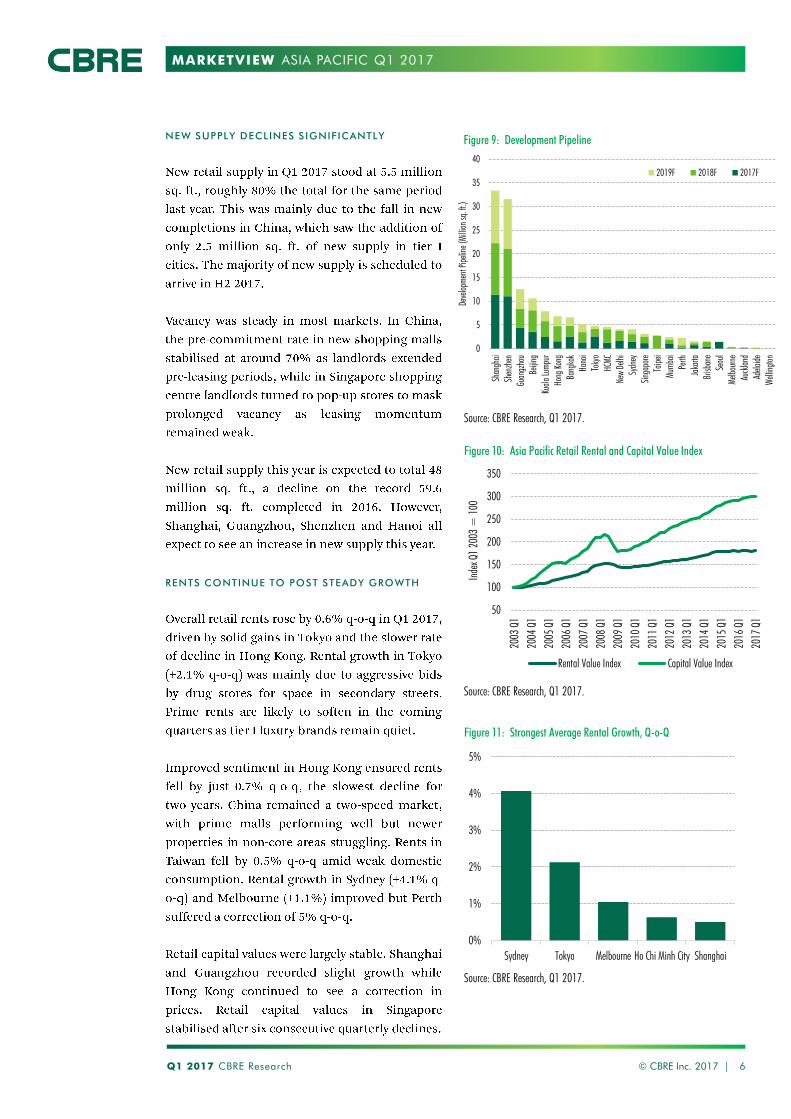

NEW SUPPLY DECLINES SIGNIFICANTLY

RENTS CONTINUE TO POST STEADY GROWTH

Figure 10: Asia Pacific Retail Rental and Capital Value Index

Q1 2017 CBRE Research © CBRE Inc. 2017 | 6

ASIA PACIFIC Q1 2017

Figure 11: Strongest Average Rental Growth, Q-o-Q

Figure 9: Development Pipeline

Source: CBRE Research, Q1 2017.

Source: CBRE Research, Q1 2017.

Source: CBRE Research, Q1 2017.

50

100

150

200

250

300

350

200

3 Q

1

200

4 Q

1

200

5 Q

1

200

6 Q

1

200

7 Q

1

200

8 Q

1

200

9 Q

1

201

0 Q

1

201

1 Q

1

201

2 Q

1

201

3 Q

1

201

4 Q

1

201

5 Q

1

201

6 Q

1

201

7 Q

1

Index Q

1 2

003 =

100

Rental Value Index Capital Value Index

0%

1%

2%

3%

4%

5%

Sydney Tokyo Melbourne Ho Chi Minh City Shanghai

0

5

10

15

20

25

30

35

40

Shanghai

Shenzhen

Guangzhou

Beijin

g

Kuala

Lum

pur

Hong K

ong

Bangkok

Hanoi

Tokyo

HCM

C

New

Delh

i

Sydney

Sin

gapore

Taip

ei

Mum

bai

Pert

h

Jakart

a

Brisbane

Seoul

Melb

ourn

e

Auckla

nd

Adela

ide

Wellin

gto

n

Develo

pm

ent Pip

eline (

Million s

q. ft

.)

2019F 2018F 2017F

MARKETVIEW

Source: CBRE Research, Q1 2017.

Figure 12: Logistics Rental Growth (%)

LEASING DEMAND REMAINS SUBDUED

OVERSUPPLY CONFINED TO SELECTED AREAS

Q1 2017 CBRE Research © CBRE Inc. 2017 | 7

ASIA PACIFIC Q1 2017

LOGISTICS 17% y-o-y 0.9% q-o-q 0.2% q-o-q

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Shanghai Guangzhou Auckland Shenzhen Melbourne Tokyo Beijing Sydney Brisbane Singapore Hong Kong Perth

2017 Q1 2017F

MARKETVIEW

RENTAL GROWTH REMAINS LIMITED Figure 13: Asia Pacific Industrial Rental and Capital Value Index

Q1 2017 CBRE Research © CBRE Inc. 2017 | 8

Source: CBRE Research, Q1 2017.

Figure 15: Logistics Supply Comparison (Q1 Completions vs 2017F Future Supply, million sq. ft.)

Source: CBRE Research, Q1 2017.

ASIA PACIFIC Q1 2017

Figure 14: Logistics Development Pipeline

Note: Singapore records net supply

Source: CBRE Research, Q1 2017

0

5

10

15

20

25

30

Gre

ate

r…

Sydney

Shanghai

Sin

gapore

Melb

ourn

e

Brisbane

Guangzhou

Shenzhen

Beijin

g

Develo

pm

ent

Pip

eline (

million s

q. ft.)

2017F 2018F 2016

0

1

2

3

4

5

6

7

8

9

Greater Tokyo Sydney Shanghai Melbourne Shenzhen Beijing Guangzhou Perth

2017 Q1 Completions 2017F Future Supply

75

100

125

150

175

200

200

6 Q

1

200

7 Q

1

200

8 Q

1

200

9 Q

1

201

0 Q

1

201

1 Q

1

201

2 Q

1

201

3 Q

1

201

4 Q

1

201

5 Q

1

201

6 Q

1

201

7 Q

1

Index Q

4 2

00

5 =

100

Rental Value Index Capital Value Index

MARKETVIEW

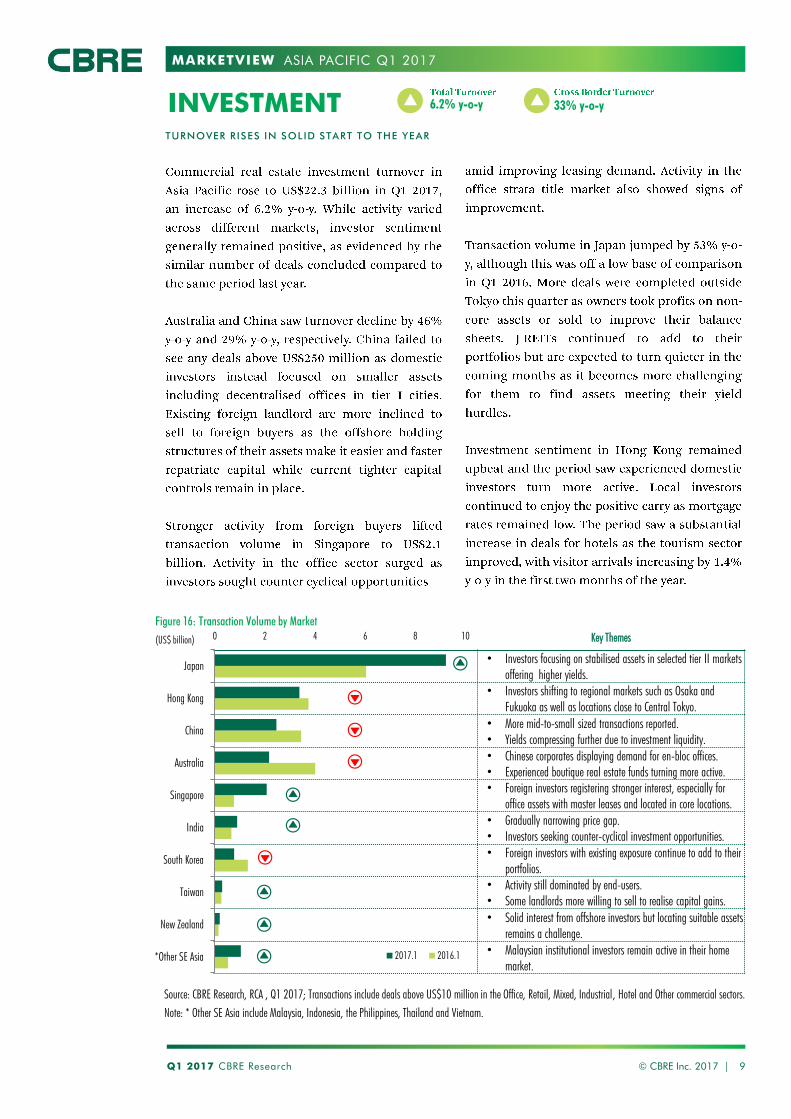

Key Themes

• Investors focusing on stabilised assets in selected tier II markets

offering higher yields.

• Investors shifting to regional markets such as Osaka and

Fukuoka as well as locations close to Central Tokyo.

• More mid-to-small sized transactions reported.

• Yields compressing further due to investment liquidity.

• Chinese corporates displaying demand for en-bloc offices.

• Experienced boutique real estate funds turning more active.

• Foreign investors registering stronger interest, especially for

office assets with master leases and located in core locations.

• Gradually narrowing price gap.

• Investors seeking counter-cyclical investment opportunities.

• Foreign investors with existing exposure continue to add to their

portfolios.

• Activity still dominated by end-users.

• Some landlords more willing to sell to realise capital gains.

• Solid interest from offshore investors but locating suitable assets

remains a challenge.

• Malaysian institutional investors remain active in their home

market.

Q1 2017 CBRE Research © CBRE Inc. 2017 | 9

ASIA PACIFIC Q1 2017

Source: CBRE Research, RCA , Q1 2017; Transactions include deals above US$10 million in the Office, Retail, Mixed, Industrial, Hotel and Other commercial sectors.

Note: * Other SE Asia include Malaysia, Indonesia, the Philippines, Thailand and Vietnam.

Figure 16: Transaction Volume by Market

INVESTMENT 6.2% y-o-y 33% y-o-y

TURNOVER RISES IN SOLID START TO THE YEAR

0 2 4 6 8 10

*Other SE Asia

New Zealand

Taiwan

South Korea

India

Singapore

Australia

China

Hong Kong

Japan

(US$ billion)

2017.1 2016.1

MARKETVIEW

0%

20%

40%

60%

80%

0

2

4

6

8

2013.1 2014.1 2015.1 2016.1 2017.1

US$

Billion

Chinese Capital Other Capital Sources

Chinese as % to total (RHS)

Q1 2017 CBRE Research © CBRE Inc. 2017 | 10

ASIA PACIFIC Q1 2017

Figure 18: Total capital raised by APAC focused real estate funds

Source: CBRE Research, Q1 2017.

Table 3: Largest Transactions in Q1 2017

CHINESE OUTBOUND INVESTMENT SLOWS

FUND RAISING ACTIVITY WEAKENS

Market Property Name SectorPrice

(US$ mil)Buyer Seller

Singapore 70% stake in TripleOne Somerset Office 630 Shun Tak61% from Perennial Real Estate

9% from Unified Elite Ltd

Japan TOC Minato Mirai Mixed 600 Hulic TOC Co. Ltd

Singapore GSH Plaza Office & Retail 570 Fullshare Holdings Plaza Ventures Pte Ltd

India RMZ Equinox Business Park Office 370 RMZ Corporation Equinox Realty

Hong Kong Newton Place Hotel Hotel 296 Domestic Investor Henderson Land

Source: CBRE Research, Q1 2017.

Figure 17: Cross-border investment in Asia Pacific

0

2

4

6

8

10

12

14

16

18

20

2012 2013 2014 2015 2016 Q1 2017

US$

billion

Source: CBRE Research, Q1 2017.

MARKETVIEW

OFFICE

RETAIL

LOGISTICS

INVESTMENT

ASIA PACIFIC Q1 2017

Q1 2017 CBRE Research © CBRE Inc. 2017 | 11

OUTLOOK

MARKETVIEW

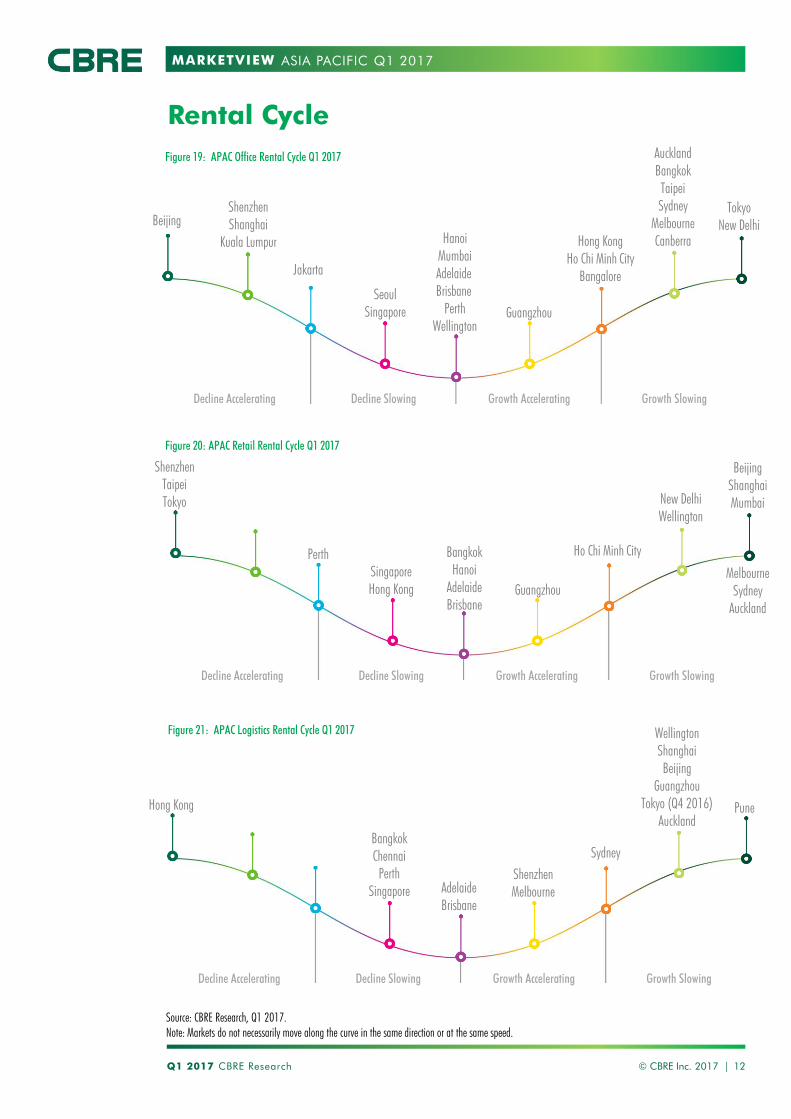

Rental Cycle

ASIA PACIFIC Q1 2017

Source: CBRE Research, Q1 2017.

Note: Markets do not necessarily move along the curve in the same direction or at the same speed.

Figure 20: APAC Retail Rental Cycle Q1 2017

Figure 19: APAC Office Rental Cycle Q1 2017

Q1 2017 CBRE Research © CBRE Inc. 2017 | 12

Figure 21: APAC Logistics Rental Cycle Q1 2017

Decline Accelerating Decline Slowing Growth Accelerating Growth Slowing

Decline Accelerating Decline Slowing Growth Accelerating Growth Slowing

Perth Bangkok

Hanoi

Adelaide

Brisbane

Guangzhou

Ho Chi Minh City

New Delhi

Wellington

Beijing

Shanghai

Mumbai

Melbourne

Sydney

Auckland

Hong Kong

Bangkok

Chennai

Perth

Singapore Adelaide

Brisbane

Shenzhen

Melbourne

Wellington

Shanghai

Beijing

Guangzhou

Tokyo (Q4 2016)

Auckland

Pune

Sydney

Singapore

Hong Kong

Shenzhen

Taipei

Tokyo

Decline Accelerating Decline Slowing Growth Accelerating Growth Slowing

Seoul

Singapore

Hanoi

Mumbai

Adelaide

Brisbane

Perth

Wellington

Guangzhou

Hong Kong

Ho Chi Minh City

Bangalore

Auckland

Bangkok

Taipei

Sydney

Melbourne

Canberra

Tokyo

New Delhi

Shenzhen

Shanghai

Kuala Lumpur

Beijing

Jakarta

MARKETVIEW

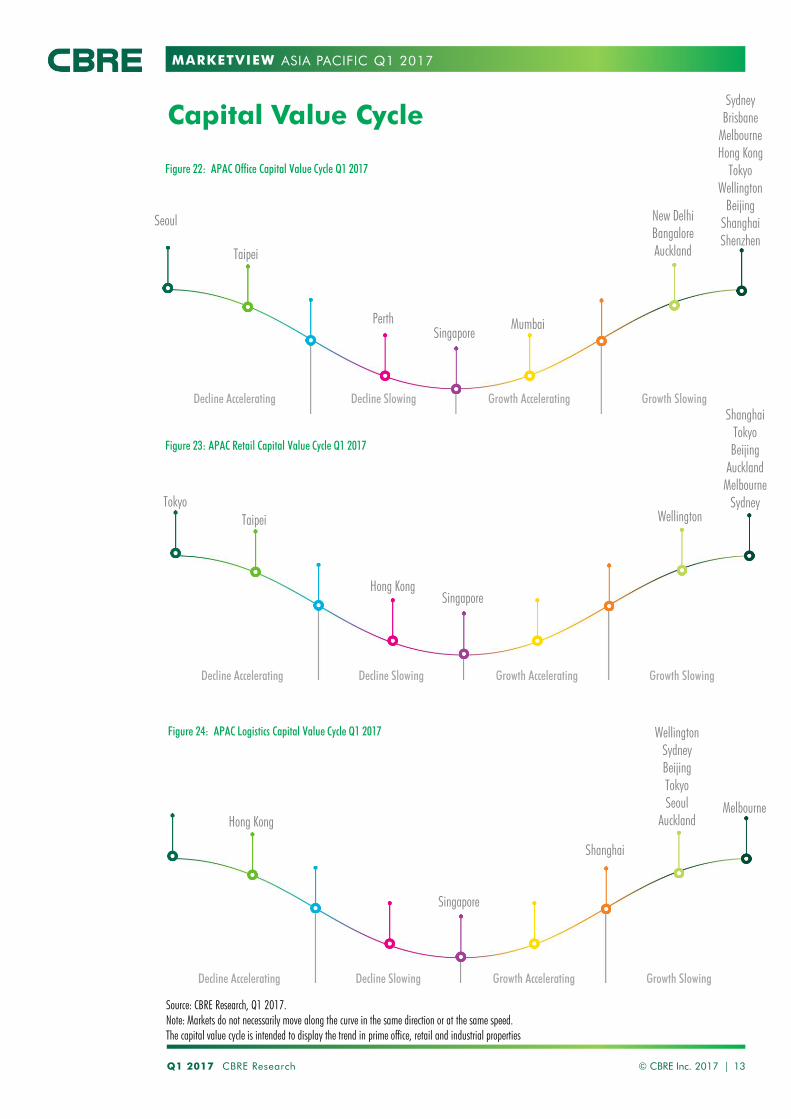

Capital Value Cycle

ASIA PACIFIC Q1 2017

Source: CBRE Research, Q1 2017.

Note: Markets do not necessarily move along the curve in the same direction or at the same speed.

The capital value cycle is intended to display the trend in prime office, retail and industrial properties

Figure 22: APAC Office Capital Value Cycle Q1 2017

Q1 2017 CBRE Research © CBRE Inc. 2017 | 13

Figure 24: APAC Logistics Capital Value Cycle Q1 2017

Decline Accelerating Decline Slowing Growth Accelerating Growth Slowing

Decline Accelerating Decline Slowing Growth Accelerating Growth Slowing

Decline Accelerating Decline Slowing Growth Accelerating Growth Slowing

Sydney

Brisbane

Melbourne

Hong Kong

Tokyo

Wellington

Beijing

Shanghai

Shenzhen

New Delhi

Bangalore

Auckland

Mumbai

Shanghai

Tokyo

Beijing

Auckland

Melbourne

Sydney

WellingtonTaipei

Melbourne

Wellington

Sydney

Beijing

Tokyo

Seoul

Auckland

Singapore

Taipei

Figure 23: APAC Retail Capital Value Cycle Q1 2017

Hong Kong

Perth

Singapore

Tokyo

Singapore

Hong Kong

Seoul

Shanghai

MARKETVIEW ASIA PACIFIC Q1 2017

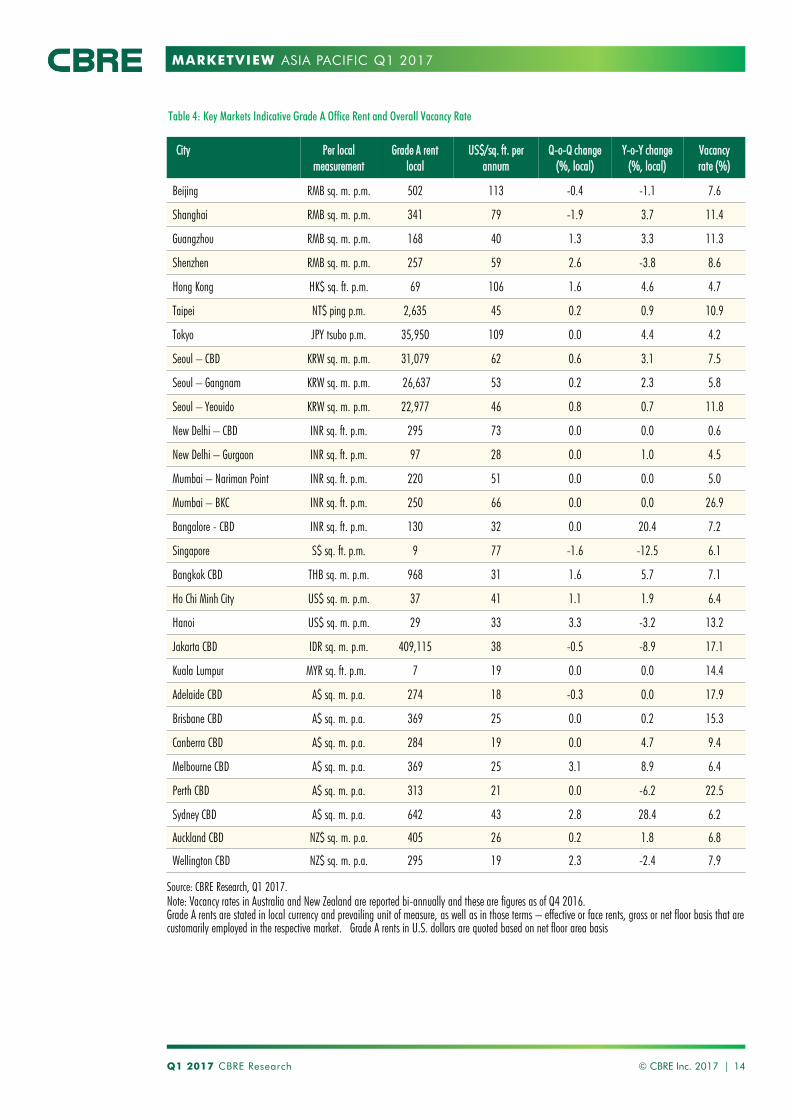

Table 4: Key Markets Indicative Grade A Office Rent and Overall Vacancy Rate

© CBRE Inc. 2017 | 14

Source: CBRE Research, Q1 2017.

Note: Vacancy rates in Australia and New Zealand are reported bi-annually and these are figures as of Q4 2016.

Grade A rents are stated in local currency and prevailing unit of measure, as well as in those terms – effective or face rents, gross or net floor basis that are

customarily employed in the respective market. Grade A rents in U.S. dollars are quoted based on net floor area basis

Q1 2017 CBRE Research

City Per local

measurement

Grade A rent

local

US$/sq. ft. per

annum

Q-o-Q change

(%, local)

Y-o-Y change

(%, local)

Vacancy

rate (%)

Beijing RMB sq. m. p.m. 502 113 -0.4 -1.1 7.6

Shanghai RMB sq. m. p.m. 341 79 -1.9 3.7 11.4

Guangzhou RMB sq. m. p.m. 168 40 1.3 3.3 11.3

Shenzhen RMB sq. m. p.m. 257 59 2.6 -3.8 8.6

Hong Kong HK$ sq. ft. p.m. 69 106 1.6 4.6 4.7

Taipei NT$ ping p.m. 2,635 45 0.2 0.9 10.9

Tokyo JPY tsubo p.m. 35,950 109 0.0 4.4 4.2

Seoul – CBD KRW sq. m. p.m. 31,079 62 0.6 3.1 7.5

Seoul – Gangnam KRW sq. m. p.m. 26,637 53 0.2 2.3 5.8

Seoul – Yeouido KRW sq. m. p.m. 22,977 46 0.8 0.7 11.8

New Delhi – CBD INR sq. ft. p.m. 295 73 0.0 0.0 0.6

New Delhi – Gurgaon INR sq. ft. p.m. 97 28 0.0 1.0 4.5

Mumbai – Nariman Point INR sq. ft. p.m. 220 51 0.0 0.0 5.0

Mumbai – BKC INR sq. ft. p.m. 250 66 0.0 0.0 26.9

Bangalore - CBD INR sq. ft. p.m. 130 32 0.0 20.4 7.2

Singapore S$ sq. ft. p.m. 9 77 -1.6 -12.5 6.1

Bangkok CBD THB sq. m. p.m. 968 31 1.6 5.7 7.1

Ho Chi Minh City US$ sq. m. p.m. 37 41 1.1 1.9 6.4

Hanoi US$ sq. m. p.m. 29 33 3.3 -3.2 13.2

Jakarta CBD IDR sq. m. p.m. 409,115 38 -0.5 -8.9 17.1

Kuala Lumpur MYR sq. ft. p.m. 7 19 0.0 0.0 14.4

Adelaide CBD A$ sq. m. p.a. 274 18 -0.3 0.0 17.9

Brisbane CBD A$ sq. m. p.a. 369 25 0.0 0.2 15.3

Canberra CBD A$ sq. m. p.a. 284 19 0.0 4.7 9.4

Melbourne CBD A$ sq. m. p.a. 369 25 3.1 8.9 6.4

Perth CBD A$ sq. m. p.a. 313 21 0.0 -6.2 22.5

Sydney CBD A$ sq. m. p.a. 642 43 2.8 28.4 6.2

Auckland CBD NZ$ sq. m. p.a. 405 26 0.2 1.8 6.8

Wellington CBD NZ$ sq. m. p.a. 295 19 2.3 -2.4 7.9

MARKETVIEW ASIA PACIFIC Q1 2017

City TypePer local

measurement

Average rent

local

US$/sq. ft. per

annum

Q-o-Q change

(%, local)

Y-o-Y change

(%, local)

Beijing Shopping Centre RMB sq. m. p.day 35 173 0.1 1.4

Shanghai Shopping Centre RMB sq. m. p.day 41 202 0.5 1.9

Guangzhou Shopping Centre RMB sq. m. p.day 39 190 0.2 2.7

Shenzhen Shopping Centre RMB sq. m. p.day 24 119 -0.1 0.4

Hong Kong High Street HK$ sq. ft. p.m. 504 778 -0.7 -7.1

Taipei High Street NT$ sq. m. p.m. 5,493 201 -0.5 0.2

Tokyo* High Street JPY tsubo p.m. 400,000 1,210 0.0 0.0

Singapore Shopping Centre S$ sq. ft. p.m. 25 217 -0.6 -2.7

Bangkok Shopping Centre THB sq. m. p.m. 2,180 71 0.0 0.0

Ho Chi Minh City Shopping Centre US$ sq. m. p.m. 56 279 0.6 8.6

Hanoi Shopping Centre US$ sq. m. p.m. 30 234 -1.2 -9.4

New Delhi Shopping Centre INR sq. ft. p.m. 1,250 153 0.0 0.0

New Delhi High Street INR sq. ft. p.m. 1,500 278 0.0 0.0

Mumbai Shopping Centre INR sq. ft. p.m. 750 111 0.0 7.1

Sydney High Street A$ sq. m. p.a. 5,342 379 4.1 18.0

Melbourne High Street A$ sq. m. p.a. 3,808 270 1.1 1.1

Adelaide High Street A$ sq. m. p.a. 2,033 144 0.0 0.0

Brisbane High Street A$ sq. m. p.a. 3,155 224 0.0 0.0

Perth High Street A$ sq. m. p.a. 3142 223 -5.3 -10.9

Auckland High Street NZ$ sq. m. p.a. 4,500 292 0.0 12.5

Wellington High Street NZ$ sq. m. p.a. 2,684 174 0.0 7.9

Table 5: Key Markets Indicative Retail Rent

© CBRE Inc. 2017 | 15

Source: CBRE Research, Q1 2017.

* Prime Rent - The prime retail rents represent the typical “achievable” open market headline rent which an international retail chain would be expected to

pay for a ground floor retail unit (either high street or shopping centre depending on the market) of up to 200 sq. m. of the highest quality and

specification and in the best location in a given market. The quoted rents reflect the level at which relevant transactions are being completed in the market

at the time but need not be exactly identical to any of them, particularly if deal flow is very limited or made up of unusual one-off deals. In these

circumstances, the quoted figure will be more hypothetical, based on expert opinion of market conditions, but the same criteria on building size and

specification apply. The figures exclude any leasing incentives or “key money” (premium, or initial payment, to secure the right to occupy the unit).

Note: All markets measure the relative performance of retail properties of similar quality with the exception of Vietnam, which tracks the overall market movement.

Q1 2017 CBRE Research

MARKETVIEW ASIA PACIFIC Q1 2017

City TypePer local

measurement

Prime rent

local

US$/sq. ft. per

annum

Q-o-Q change

(%, local)

Y-o-Y change

(%, local)

Beijing≠

Logistics RMB sq. m. p.m. 40.5 6.6 0.5 0.7

Shanghai≠

Logistics RMB sq. m. p.m. 44.0 7.1 1.5 6.5

Guangzhou≠

Logistics RMB sq. m. p.m. 35.9 5.8 0.8 2.9

Shenzhen≠

Logistics RMB sq. m. p.m. 43.4 7.0 0.7 6.7

Chengdu≠

Logistics RMB sq. m. p.m. 24.5 4.0 -3.2 -10.7

Tianjin≠

Logistics RMB sq. m. p.m. 29.1 4.7 0.0 0.2

Wuhan≠

Logistics RMB sq. m. p.m. 29.3 4.7 -0.7 2.6

Hong Kong Warehouse HK$ sq. ft. p.m. 12.4 19.2 -0.6 -1.2

Chennai Logistics INR sq. ft. p. m. 28.0 5.0 0.0 7.7

Pune Logistics INR sq. ft. p. m. 28.0 5.0 0.0 0.0

Greater Tokyo* Logistics JPY tsubo p.m. 6320.0 19.1 0.5 1.1

SingaporeWarehouse

(ground floor)S$ sq. ft. p.m. 1.6 14.0 -0.6 -4.7

Sydney Warehouse A$ sq. m. p.a. 124.6 8.8 0.3 5.7

Melbourne Warehouse A$ sq. m. p.a. 84.0 6.0 0.6 1.2

Brisbane Warehouse A$ sq. m. p.a. 113.0 8.0 0.0 -0.9

Adelaide Warehouse A$ sq. m. p.a. 75.0 5.3 1.4 1.4

Perth Warehouse A$ sq. m. p.a. 95.8 6.8 -2.7 -9.2

Canberra Warehouse A$ sq. m. p.a. 95.0 6.7 0.0 0.0

Auckland Warehouse NZ$ sq. m. p.a. 137.4 8.9 0.8 3.0

Wellington Warehouse NZ$ sq. m. p.a. 107.0 7.0 7.9 21.4

Table 6: Key Markets Indicative Logistics Rent

Q1 2017 CBRE Research © CBRE Inc. 2017 | 16

Source: CBRE Research, Q1 2017.

Logistics rents - Average rental values are derived from a basket of prime logistics properties located in major industrial zones in each market.

*Greater Tokyo – effective rents≠

like-for-like rental change

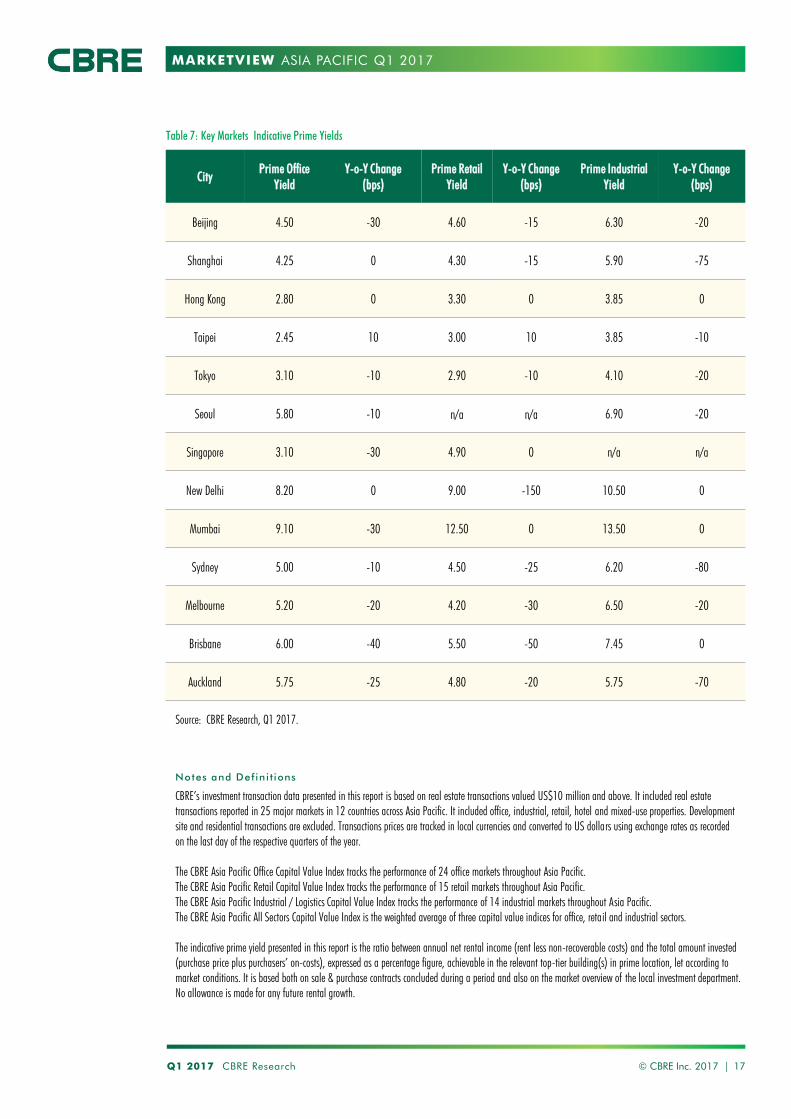

MARKETVIEW ASIA PACIFIC Q1 2017

CityPrime Office

Yield

Y-o-Y Change

(bps)

Prime Retail

Yield

Y-o-Y Change

(bps)

Prime Industrial

Yield

Y-o-Y Change

(bps)

Beijing 4.50 -30 4.60 -15 6.30 -20

Shanghai 4.25 0 4.30 -15 5.90 -75

Hong Kong 2.80 0 3.30 0 3.85 0

Taipei 2.45 10 3.00 10 3.85 -10

Tokyo 3.10 -10 2.90 -10 4.10 -20

Seoul 5.80 -10 n/a n/a 6.90 -20

Singapore 3.10 -30 4.90 0 n/a n/a

New Delhi 8.20 0 9.00 -150 10.50 0

Mumbai 9.10 -30 12.50 0 13.50 0

Sydney 5.00 -10 4.50 -25 6.20 -80

Melbourne 5.20 -20 4.20 -30 6.50 -20

Brisbane 6.00 -40 5.50 -50 7.45 0

Auckland 5.75 -25 4.80 -20 5.75 -70

Table 7: Key Markets Indicative Prime Yields

Q1 2017 CBRE Research © CBRE Inc. 2017 | 17

Source: CBRE Research, Q1 2017.

Notes and Defini t ions

CBRE’s investment transaction data presented in this report is based on real estate transactions valued US$10 million and above. It included real estate

transactions reported in 25 major markets in 12 countries across Asia Pacific. It included office, industrial, retail, hotel and mixed-use properties. Development

site and residential transactions are excluded. Transactions prices are tracked in local currencies and converted to US dollars using exchange rates as recorded

on the last day of the respective quarters of the year.

The CBRE Asia Pacific Office Capital Value Index tracks the performance of 24 office markets throughout Asia Pacific.

The CBRE Asia Pacific Retail Capital Value Index tracks the performance of 15 retail markets throughout Asia Pacific.

The CBRE Asia Pacific Industrial / Logistics Capital Value Index tracks the performance of 14 industrial markets throughout Asia Pacific.

The CBRE Asia Pacific All Sectors Capital Value Index is the weighted average of three capital value indices for office, retail and industrial sectors.

The indicative prime yield presented in this report is the ratio between annual net rental income (rent less non-recoverable costs) and the total amount invested

(purchase price plus purchasers’ on-costs), expressed as a percentage figure, achievable in the relevant top-tier building(s) in prime location, let according to

market conditions. It is based both on sale & purchase contracts concluded during a period and also on the market overview of the local investment department.

No allowance is made for any future rental growth.

MARKETVIEW

CBRE GLOBAL RESEARCH

This report was prepared by the CBRE Asia Pacific Research Team, which forms part of CBRE Global Research – a network of preeminent researchers who

collaborate to provide real estate market research, econometric forecasting and consulting solutions to real estate investors and occupiers around the globe.

Disclaimer

All materials presented in this report, unless specifically indicated otherwise, is under copyright and proprietary to CBRE. Information contained herein, including

projections, has been obtained from materials and sources believed to be reliable at the date of publication. While we do not doubt its accuracy, we have not

verified it and make no guarantee, warranty or representation about it. Readers are responsible for independently assessing the relevance, accuracy, completeness

and currency of the information of this publication. This report is presented for information purposes only, exclusively for CBRE clients and professionals, and is not

to be used or considered as an offer or the solicitation of an offer to sell or buy or subscribe for securities or other financial instruments. All rights to the material

are reserved and none of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party

without prior express written permission of CBRE. Any unauthorised publication or redistribution of CBRE research reports is prohibited. CBRE will not be liable for

any loss, damage, cost or expense incurred or arising by reason of any person using or relying on information in this publication.

GLOBAL RESEARCH

ASIA PACIFIC Q1 2017

ASIA PACIFIC RESEARCH

![EMEA Corporate Occupier Conditions – Autumn 2015 [Infographic]](https://img.pdfslide.us/doc/110x75/58743d391a28ab0e6c8b5df9/emea-corporate-occupier-conditions-autumn-2015-infographic.jpg)