Embed Size (px)

Citation preview

International Monetary Economics

Master d’Affaires Publiques SciencesPo Spring 2013

Pierre-Olivier Gourinchas

Slide 1-2

Roadmap

§ Administrative Trivia § A quick recap on the global financial crisis § International Economics: What is it about? § Measurement:

• The National Income Accounts • National Income Accounting for the Open Economy • Three Interpretations of the Current Account

§ Balance of Payments Accounts

Slide 1-4

§ Course web page. • Available through the SciencesPo website.

§ Grading. • Class participation: 20%. • Group presentation: 35%. • Final exam: 45%.

Administrative Trivia

Slide 1-6

Administrative Trivia § Course material.

• International economics, Krugman Obstfeld and Melitz, Pearson, 9th edition.

• The Economist and The Financial Times: weekly readings.

• Additional material on the course web page.

Slide 1-7

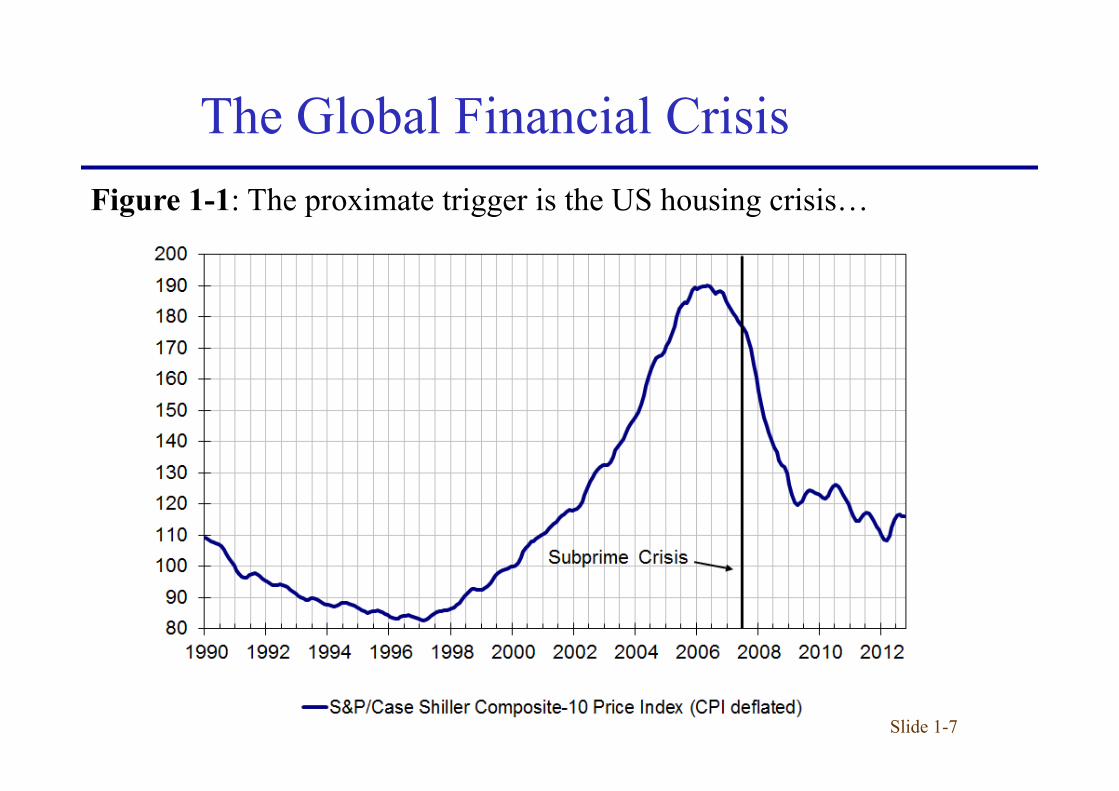

Figure 1-1: The proximate trigger is the US housing crisis…

The Global Financial Crisis

Slide 1-8

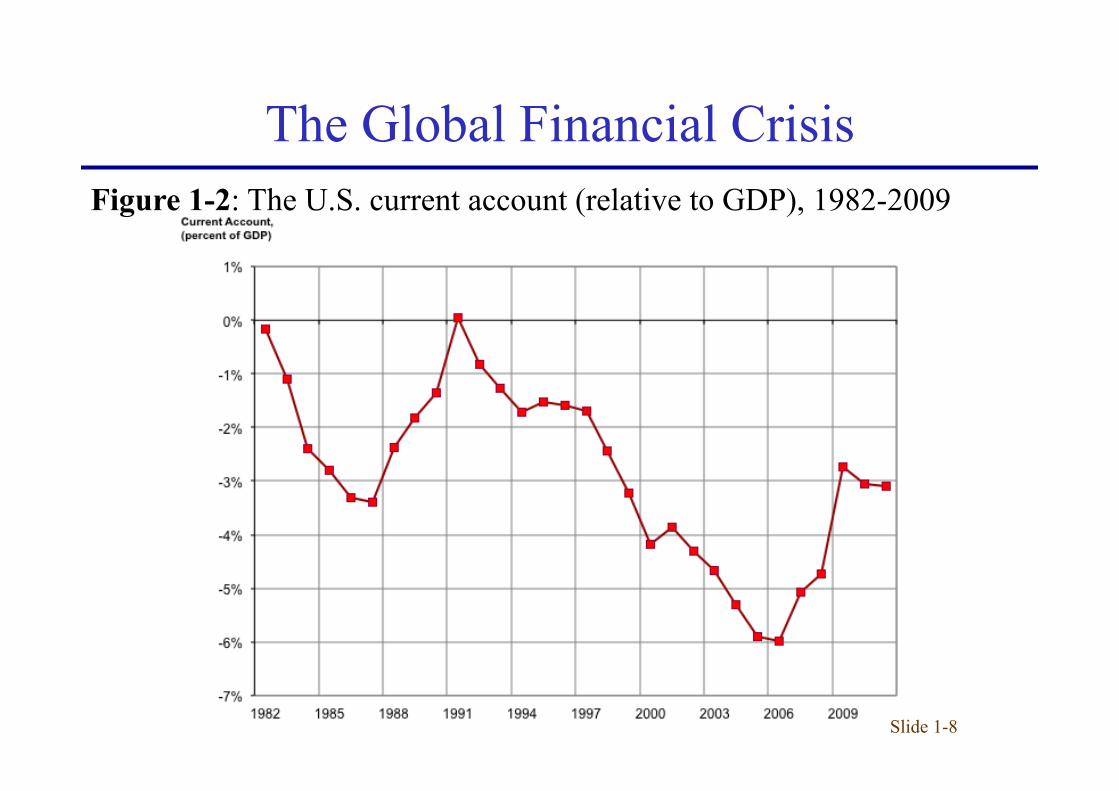

Figure 1-2: The U.S. current account (relative to GDP), 1982-2009

The Global Financial Crisis

Slide 1-9

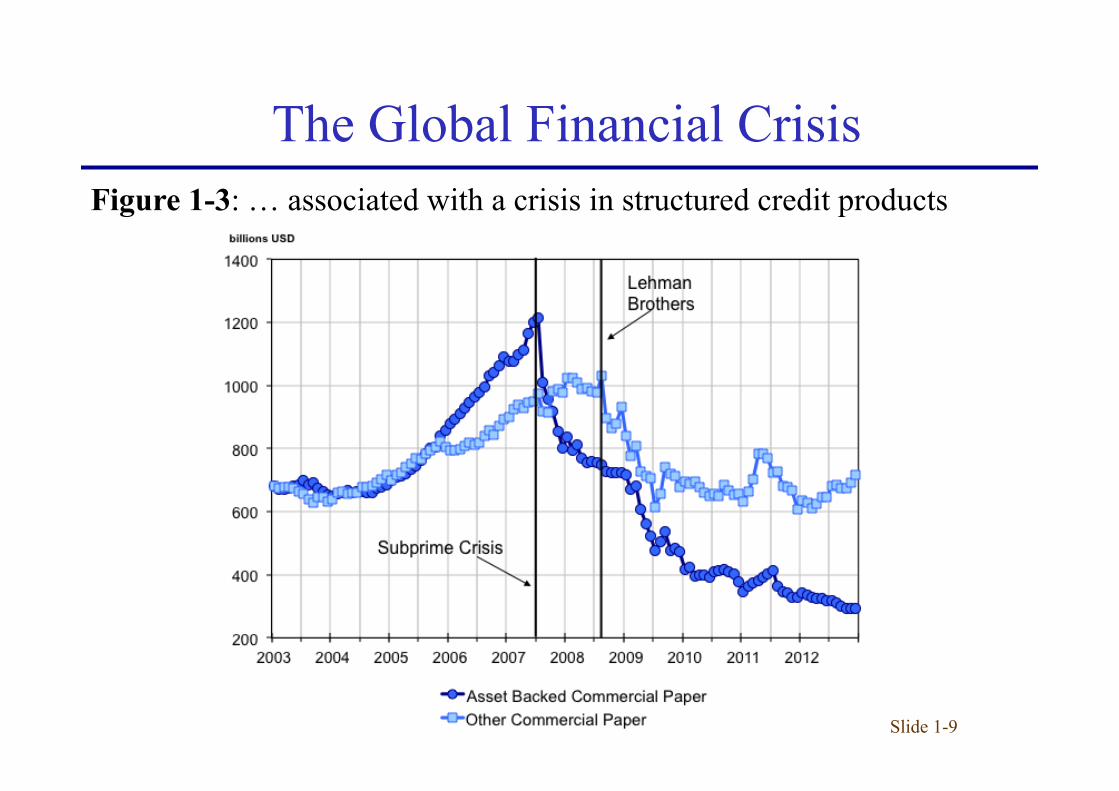

Figure 1-3: … associated with a crisis in structured credit products

The Global Financial Crisis

Slide 1-10

Figure 1-4: … and a sudden increase in counterparty risk…

The Global Financial Crisis

Slide 1-11

Figure 1-5a: … monetary policy responses in the US and in Europe

The Global Financial Crisis

Interest rates (percentage points)

Slide 1-12

Figure 1-5b: … followed by non-conventional monetary policies

The Global Financial Crisis

Slide 1-13

Figure 1-5c: … Balance Sheet of the US Federal Reserve (millions of $)

The Global Financial Crisis

Slide 1-14

Figure 1-6a: …while economic activity collapsed and rebounded…

The Global Financial Crisis

Slide 1-15

Figure 1-6b: … And world trade collapsed

The Global Financial Crisis

Slide 1-16

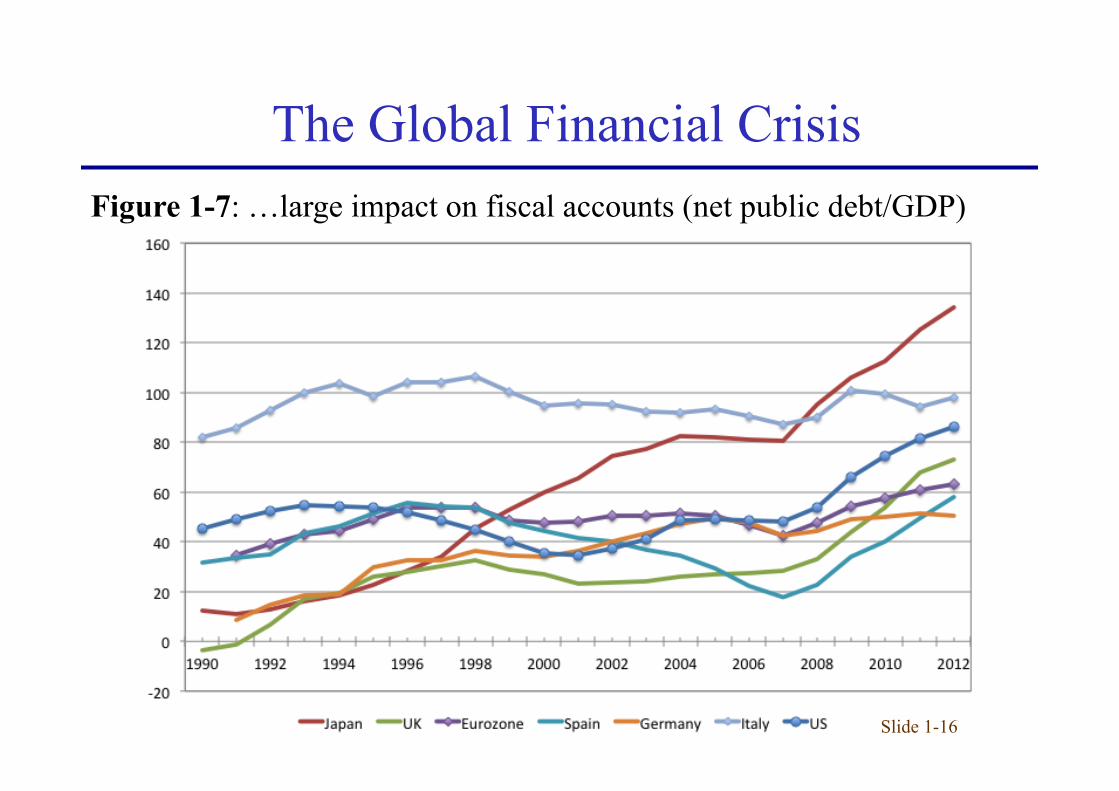

Figure 1-7: …large impact on fiscal accounts (net public debt/GDP)

The Global Financial Crisis

Slide 1-17

Figure 1-8: …and a period of severe fiscal stress for Eurozone countries (yield on 10-year government debt. Percent)

The Eurozone Crisis

Slide 1-18

Figure 1-9: ‘Eurozone’ Current Account Imbalances, 1993-2013

The Eurozone Crisis

Slide 1-19

§ Understanding international linkages

§ Understand the relevant policy choices

§ Understanding ‘global imbalances’

§ Understanding exchange rates

What is International Macro About?

slide 1-20

§ Essential tool for studying the macroeconomics of open, interdependent economies.

§ National income accounting • Records all the expenditures that contribute to a

country’s income and output § Balance of payments accounting

• Keeps track of changes in a country’s indebtedness to foreigners and of the fortunes of its export- and import-competing industries

The National Income Accounts

slide 1-21

§ Gross Domestic product (GDP, notation Y) • The value of all final goods and services produced

domestically and sold on the market in a given time period.

• It is the basic measure of a country’s output.

The National Income Accounts

slide 1-22

§ GDP is calculated by adding up the market value of all expenditures on final output:

• Consumption (C)

• Investment (I)

• Government purchases (G)

• Net Exports (NX=EX-IM)

The National Income Accounts

slide 1-23

§ National Income Identity: Y = C + I + G + NX

§ In a closed economy:

§ Equivalent definitions of GDP: • Income Approach:

• Product approach:

The National Income Accounts

slide 1-24

§ Gross National Product (GNP, Q): • GDP measures economic activity within a

country’s borders • GNP measures the economic activity of the

nationals, independent of location • Difference is Net Factor Payments (NFP): • Net payments to national factors of production

located outside the borders

The National Income Accounts

slide 1-25

The National Income Accounts § Formally:

Q = Y + NFP

Q = C + I + G + CA

• CA = NX + NFP : Current Account

slide 1-26

The National Income Accounts § Figure 1-10: U.S. GNP and Its Components, 2011 (source: BEA)

slide 1-27

The National Income Accounts § Figure 1-11: U.S. Current Account, Net Exports and NFP, 2011

slide 1-29

§ The Current Account and the Trade Balance • The difference between exports of goods and services

and imports of goods and services plus NFP: CA = (EX – IM) + NFP

• Ignoring NFP: CA > 0 when EX > IM CA < 0 when EX < IM

Three Interpretations of the Current Account

slide 1-30

§ The Current Account and Domestic Absorption: CA balance is equal to the difference between national income and

domestic residents’ spending: CA = Q – (C+ I + G)

• CA balance is goods production less domestic demand. • CA balance measures the size and direction of international

borrowing

Three Interpretations of the Current Account

slide 1-31

§ Saving and the Current Account • National saving (S)

– The portion of output, Q, that is not devoted to household consumption, C, or government purchases, G S = S = S =

– A closed economy can save only by building up its capital stock:

– An open economy can save either by building up its capital stock or by acquiring foreign wealth

– A country’s CA surplus is referred to as its net foreign investment. CA = S - I

Three Interpretations of the Current Account

slide 1-32

§ Private and Government Saving • Private saving (Sp)

– The part of disposable income that is saved rather than consumed Sp = (Q – T) – C

– T : Taxes.

• Government saving (Sg) – T is the government's “income” (its net tax revenue) – The extent to which the government is borrowing to finance its

expenditures (opposite of government deficit) Sg = T-G

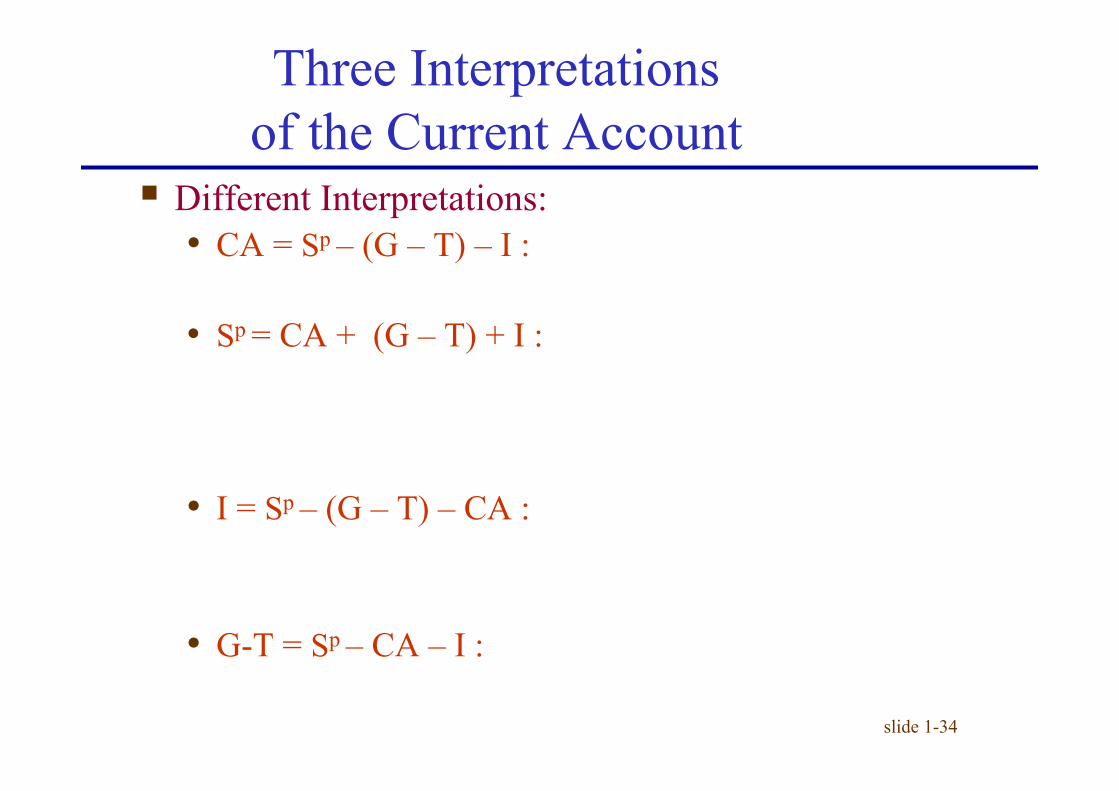

• National Saving (S) S = Sp +Sg = CA + I

– This is an identity: it must always hold!

Three Interpretations of the Current Account

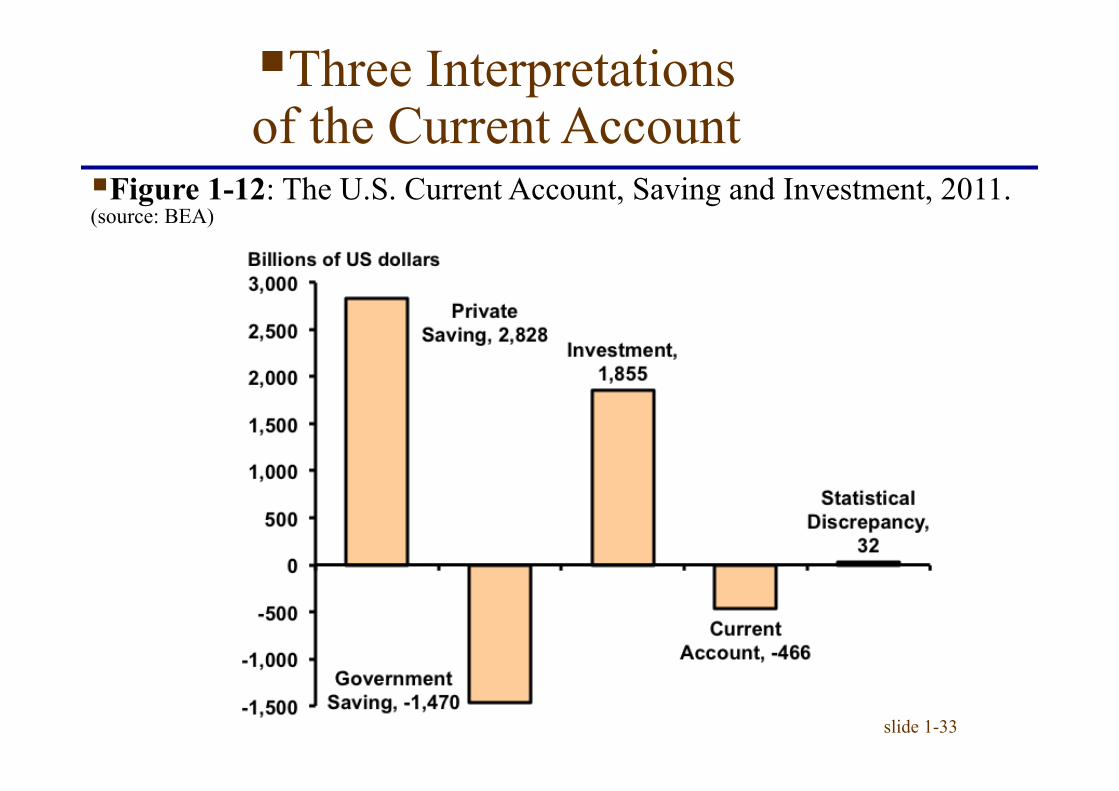

slide 1-33

§ Figure 1-12: The U.S. Current Account, Saving and Investment, 2011. (source: BEA)

§ Three Interpretations of the Current Account

slide 1-34

§ Different Interpretations: • CA = Sp – (G – T) – I :

• Sp = CA + (G – T) + I :

• I = Sp – (G – T) – CA :

• G-T = Sp – CA – I :

Three Interpretations of the Current Account

slide 1-35

Figure 1-13: The U.S. Current Account, Saving and Investment 1980-2011 (source BEA)

§ Three Interpretations of the Current Account

slide 1-36

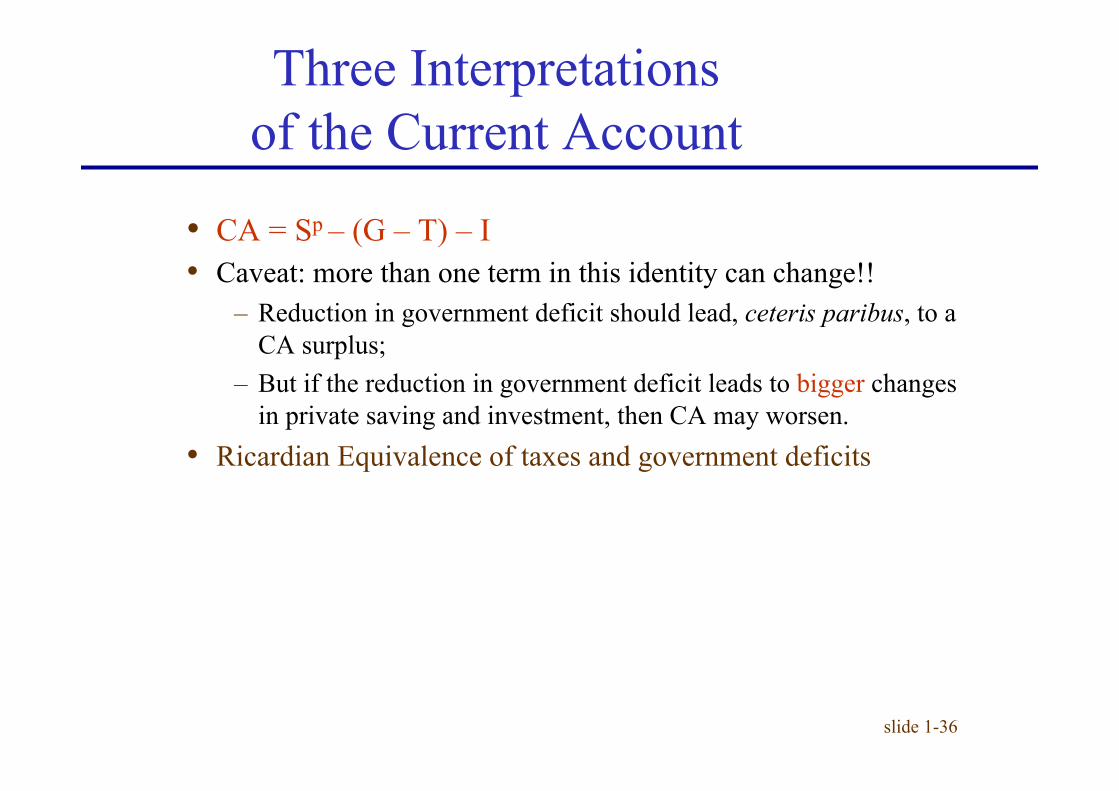

• CA = Sp – (G – T) – I • Caveat: more than one term in this identity can change!!

– Reduction in government deficit should lead, ceteris paribus, to a CA surplus;

– But if the reduction in government deficit leads to bigger changes in private saving and investment, then CA may worsen.

• Ricardian Equivalence of taxes and government deficits

Three Interpretations of the Current Account

slide 1-37

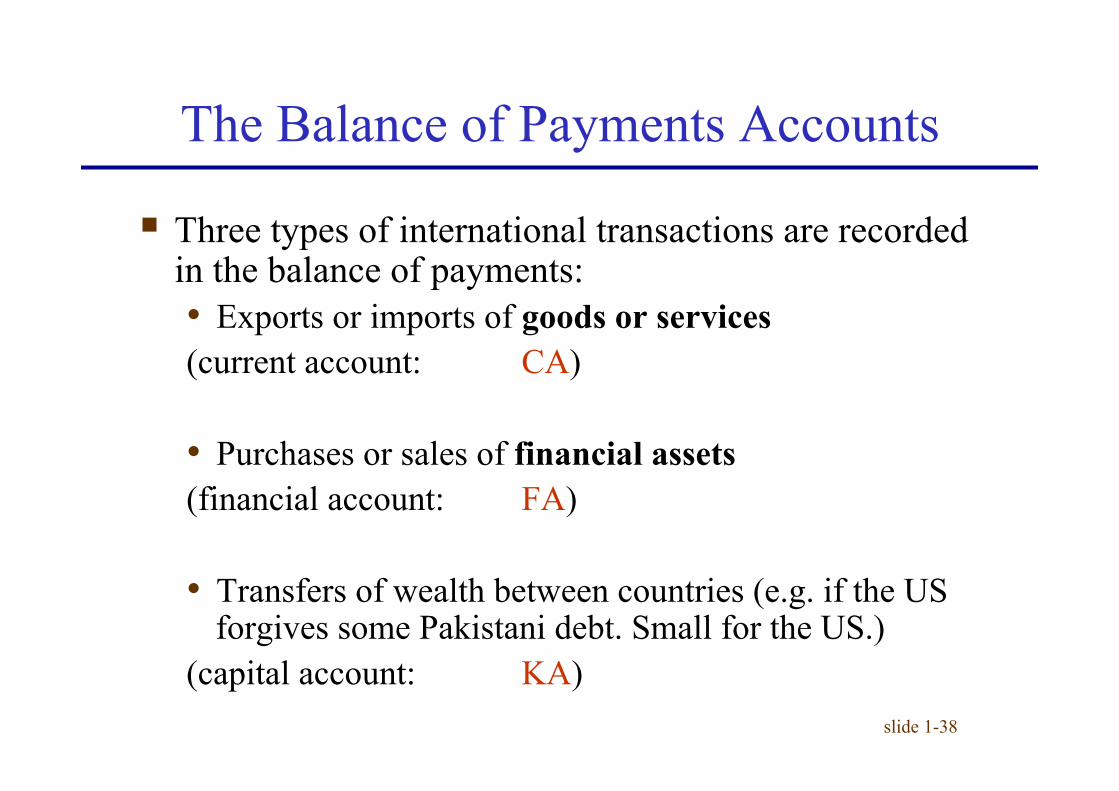

The Balance of Payments Accounts § A country’s balance of payments accounts keep track

of both its payments to and its receipts from foreigners. § Convention:

• Any payment to foreigners enters with as a debit.

• Any payment from foreigners enters as a credit.

slide 1-38

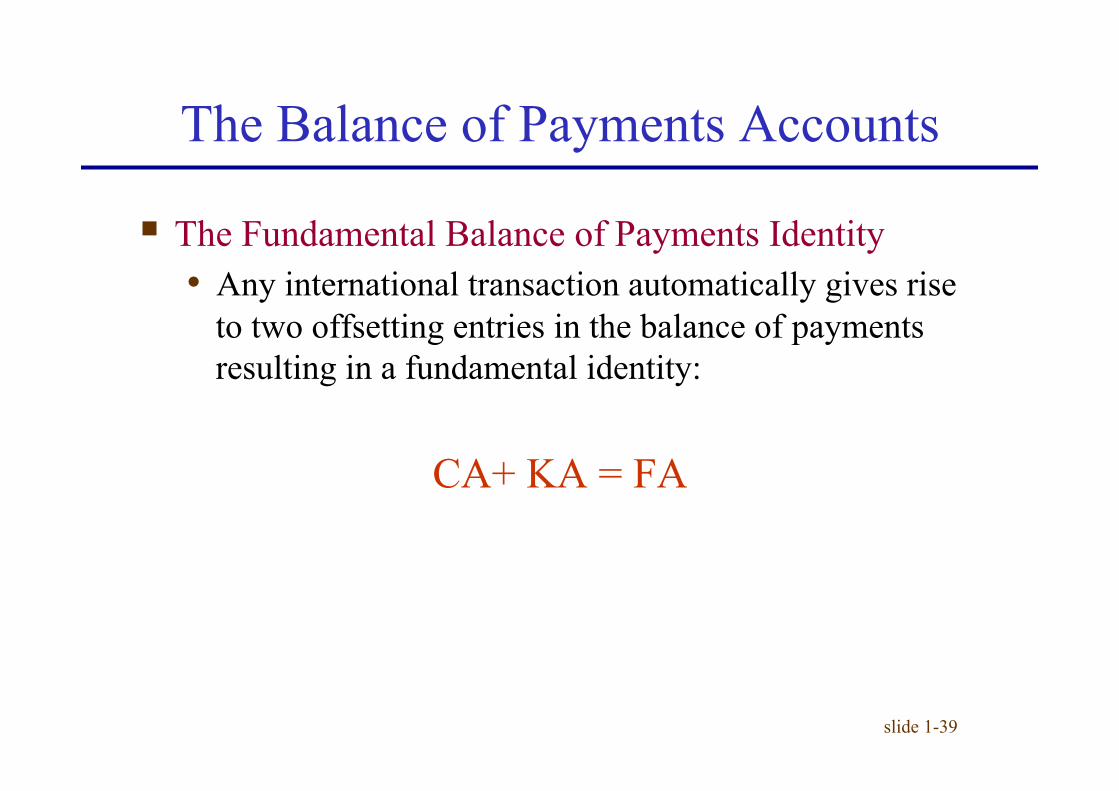

§ Three types of international transactions are recorded in the balance of payments: • Exports or imports of goods or services (current account: CA) • Purchases or sales of financial assets (financial account: FA) • Transfers of wealth between countries (e.g. if the US

forgives some Pakistani debt. Small for the US.) (capital account: KA)

The Balance of Payments Accounts

slide 1-39

§ The Fundamental Balance of Payments Identity • Any international transaction automatically gives rise

to two offsetting entries in the balance of payments resulting in a fundamental identity:

CA+ KA = FA

The Balance of Payments Accounts

slide 1-40

§ Examples of Paired Transactions • A U.S. citizen buys a $1000 tablet PC from a Chinese

company, and the Chinese company deposits the $1000 in its account at Citibank in New York.

The Balance of Payments Accounts

slide 1-41

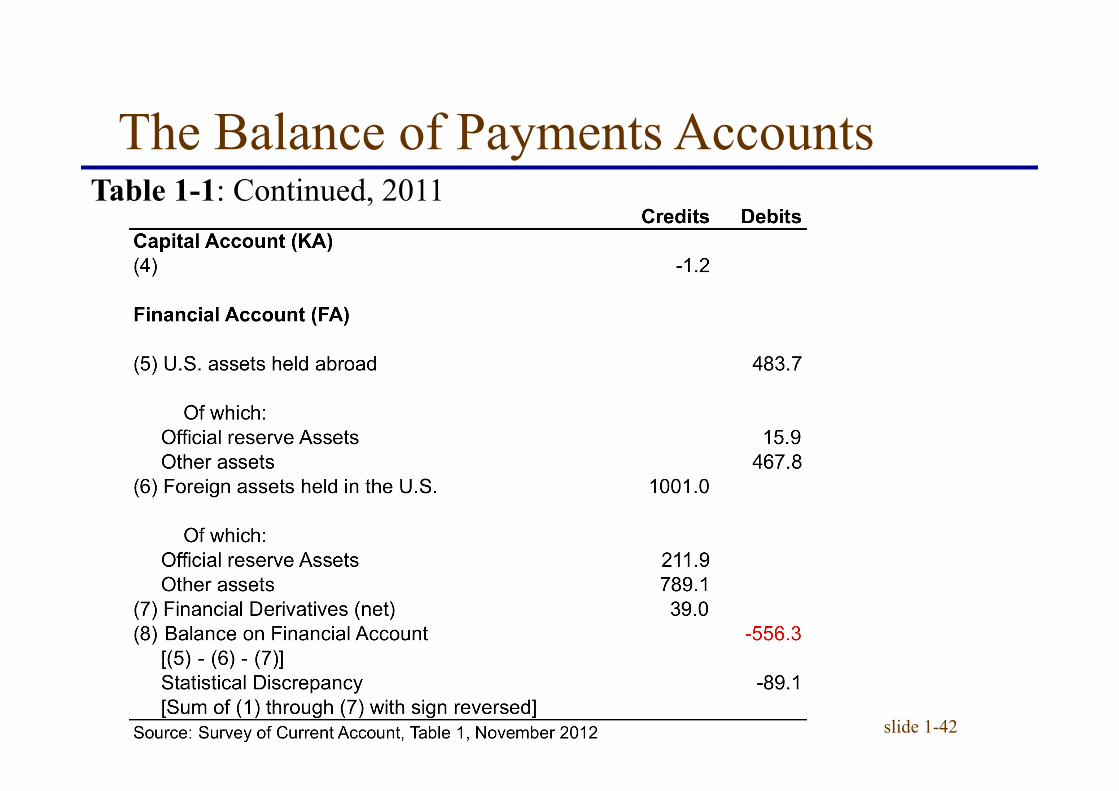

The Balance of Payments Accounts Table 1-1: U.S. Balance of Payments Accounts for 2011 (bn of dollars)

slide 1-42

The Balance of Payments Accounts Table 1-1: Continued, 2011

Slide 1-48

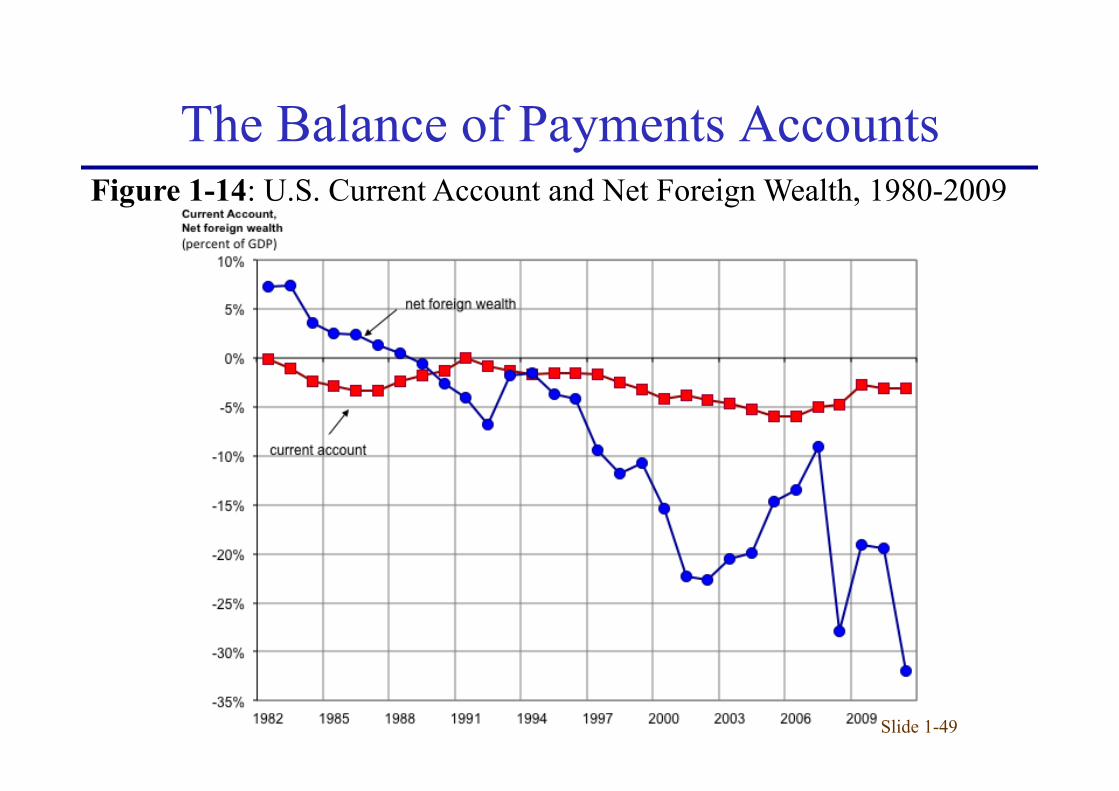

§ Is the United States the World’s Biggest Debtor? • At the end of 2011, the United States had a negative

net foreign wealth position far greater than that of any other single country.

• The United States is the world’s biggest debtor. • However, the United States has the world’s largest

GNP.

The Balance of Payments Accounts

Slide 1-49

Figure 1-14: U.S. Current Account and Net Foreign Wealth, 1980-2009

The Balance of Payments Accounts

Slide 1-50

Table 1-2: International Investment Position of the United States at Year End, 2010 and 2011 (millions of dollars)

The Balance of Payments Accounts

(a) (b) (c ) (d) (a+b+c+d)

with DI positions at current cost -2,584.0 -517.3 -802.0 -23.0 -230.1 -1,572.4 -4,156.4 with DI positions at market value -2,923.9 -517.3 -1,284.0 -41.3 -172.3 -2,014.9 -4,938.8U.S. assets owned abroad with DI positions at current cost 16,646.1 483.7 -519.5 -28.9 -153.6 -218.3 16,427.8 with DI positions at market value 17,105.9 483.7 -1,163.9 -46.7 -132.9 -859.8 16,246.1Foreign owned assets in the U.S. with DI positions at current cost 19,230.1 1,001.0 282.5 -5.9 76.5 1,354.1 20,584.2 with DI positions at market value 20,029.8 1,001.0 120.1 -5.4 39.4 1,155.1 21,184.9

Source: Survey of Current Business, July 2012, excluding derivatives. DI: direct investment. Millions of USD.

Net international investment position of the U.S.

Position 2010

Changes in position in 2011 (decrease(-))

Position 2011

Attributable to:

TotalFinancial Flows

Valuation AdjustmentsPrice

changesExchange

rate Other

slide 1-51

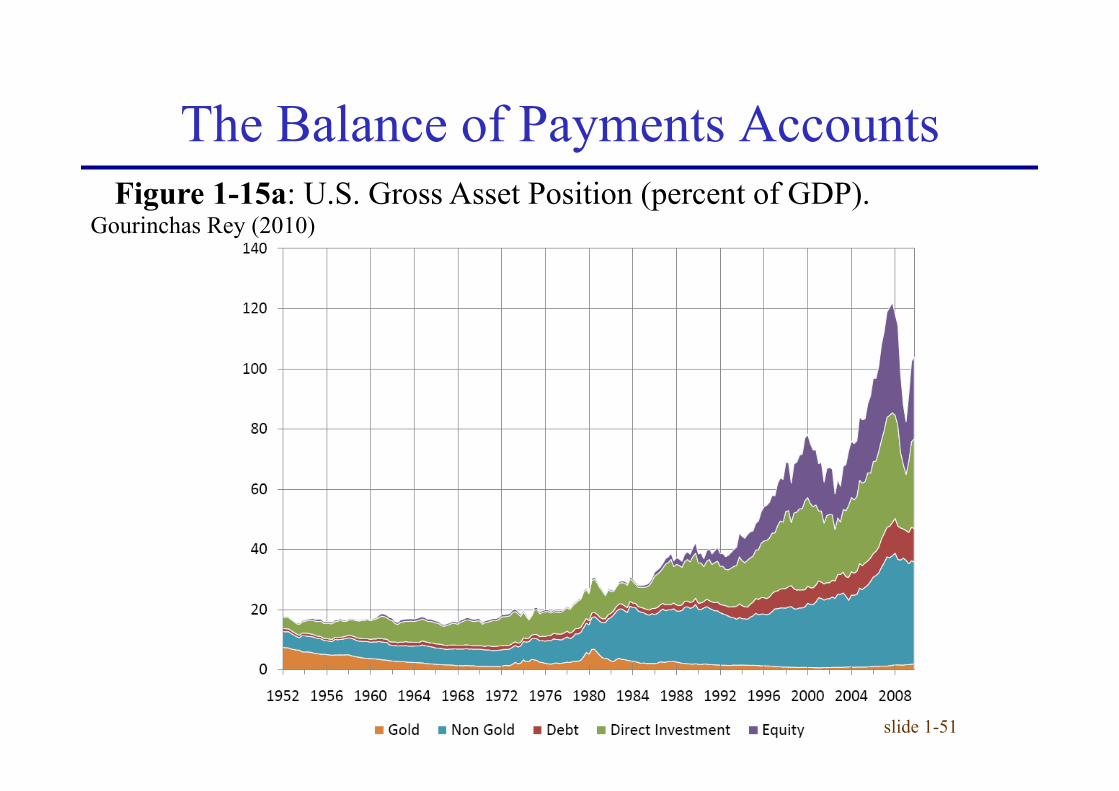

Figure 1-15a: U.S. Gross Asset Position (percent of GDP). Gourinchas Rey (2010)

The Balance of Payments Accounts

slide 1-52

Figure 1-15b: U.S. Gross Asset Position (percent of GDP). Gourinchas Rey (2010)

The Balance of Payments Accounts

slide 1-53

Table 1-3: Exorbitant Privilege? Gourinchas Rey (2007)

The Balance of Payments Accounts

slide 1-54

The Rise of Sovereign Assets

§ Sovereign Assets: • International Reserves (in the ORT) • Sovereign Wealth Funds

§ The rise of International Reserves • The counterpart of US CA deficits:

– Private capital inflows (especially before 2002) – But growing inflows from foreign central banks

• Over time, foreign, especially emerging, countries have accumulated vast “treasure chests” of US Treasury bills.

0%#

2%#

4%#

6%#

8%#

10%#

12%#

14%#

16%#

18%#

2000# 2001# 2002# 2003# 2004# 2005# 2006# 2007# 2008# 2009# 2010# 2011#

Rest#of#the#World# China# Japan# Russia# World#

slide 1-55

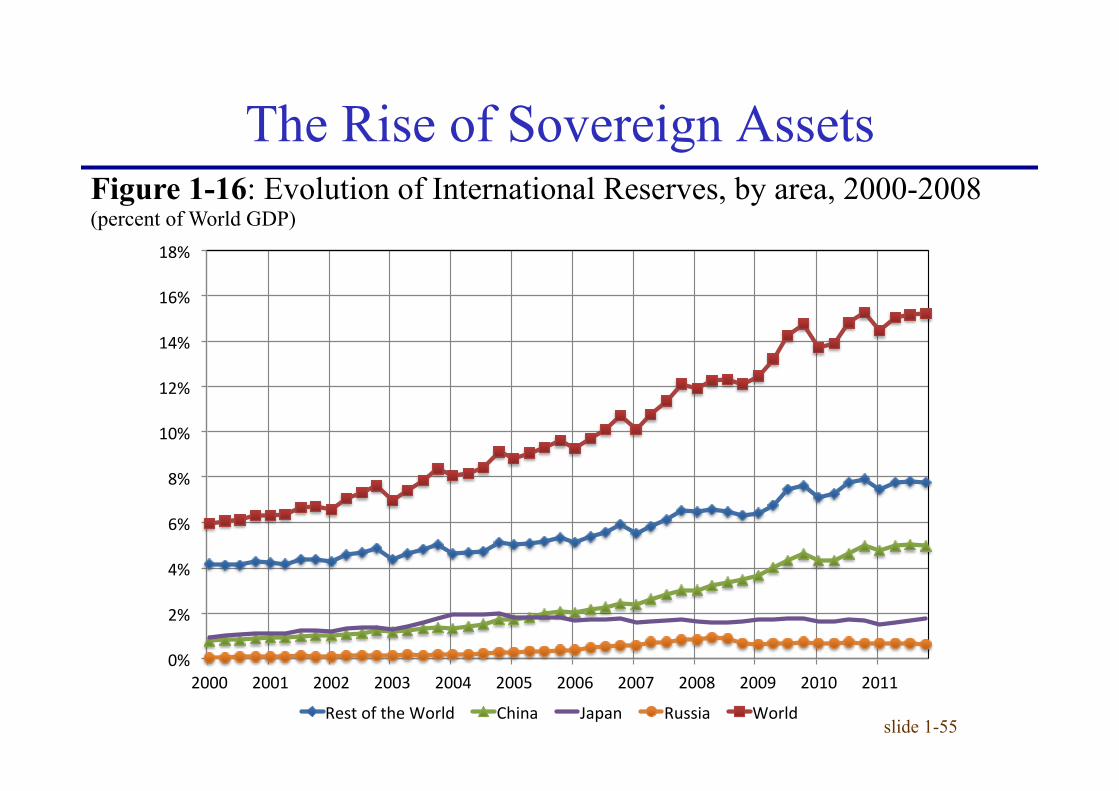

Figure 1-16: Evolution of International Reserves, by area, 2000-2008 (percent of World GDP)

The Rise of Sovereign Assets

slide 1-56

The Rise of Sovereign Assets

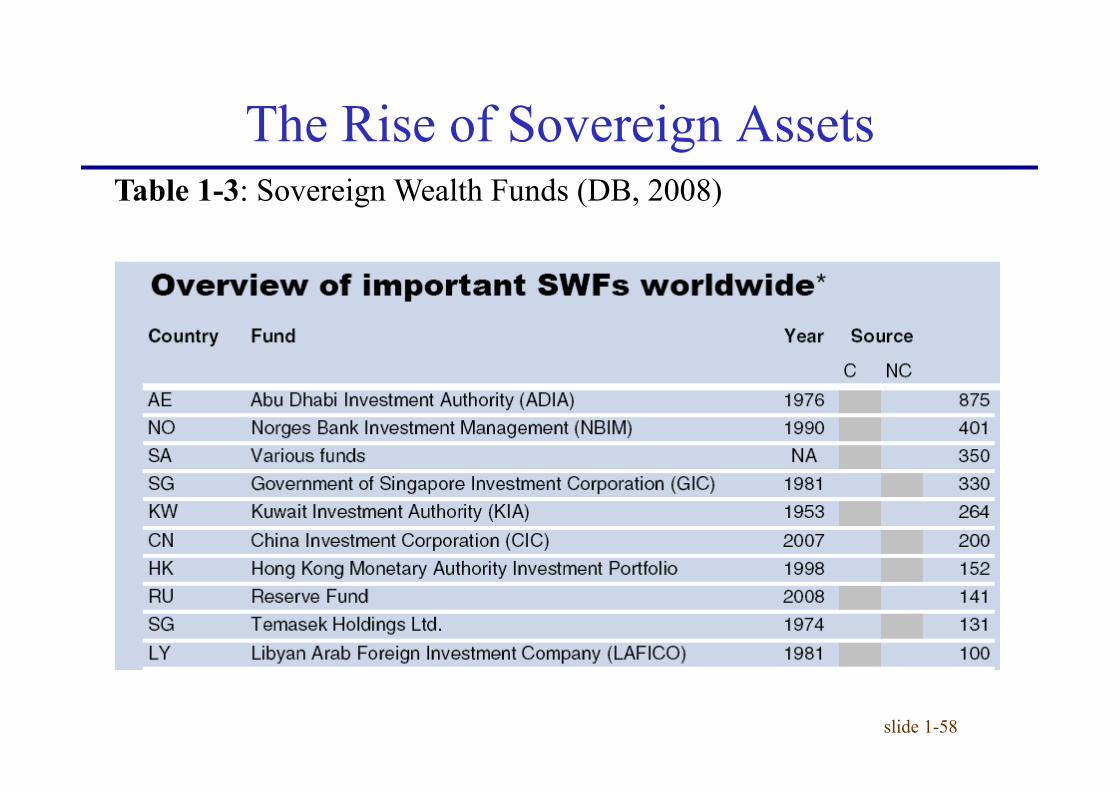

§ Why do countries accumulate reserves?

slide 1-57

The Rise of Sovereign Assets

§ The problem: • Typically, Central Banks invest in safe, liquid assets

(US Treasury bills and the like) • The financial return on these is quite low. • In addition, oil and commodity producing countries

want to invest in a diversified, high-return portfolio of assets (long horizon).

§ The answer: Sovereign Wealth Funds: • Financial vehicles owned by States which invest public

funds in a wide range of assets. • Examples: GIC (Singapore), Abu Dhabi Investment

Authority (UAE) etc…

slide 1-58

Table 1-3: Sovereign Wealth Funds (DB, 2008)

The Rise of Sovereign Assets

![Lecture 4 [0.3cm] Tax structures: production efficiency ...econ.sciences-po.fr/sites/default/files/file/laroque/lect4.pdf · Tax structures: production e ciency and ... Destructive](https://img.pdfslide.us/doc/110x75/5ab224fc7f8b9a284c8d458a/lecture-4-03cm-tax-structures-production-efficiency-econsciences-pofrsitesdefaultfilesfilelaroquelect4pdftax.jpg)