Embed Size (px)

Citation preview

Long-term economic growthGrowth and factors of production

Lecture 2Nicolas Coeurdacier

Understanding the World Economy

Master in Economics and Business

1. The neoclassical growth model

2. Do countries catch with economic leaders?

3. The Asian growth miracle?

Lecture 2 : Long-term economic growth

Growth and factors of production

0

5,000

10,000

15,000

20,000

25,00019

50

1953

1956

1959

1962

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

What makes countries rich ?

A Tale of Two Countries

The average income on a Japanese person

The average income on a Ghanaian person

Output per capita

(constant USD)

By 1996, Japan had 19 times the income of Ghana

• Three-quarters of Ghanaians have no access to health

care; all Japanese do.

• Forty percent of all Ghanaians do not have clean

drinking water; all Japanese do.

• Half of all Ghanaian women cannot read; all Japanese

women can.

• Ghanaian mothers are 91 times more likely to die in

childbirth than Japanese mothers.

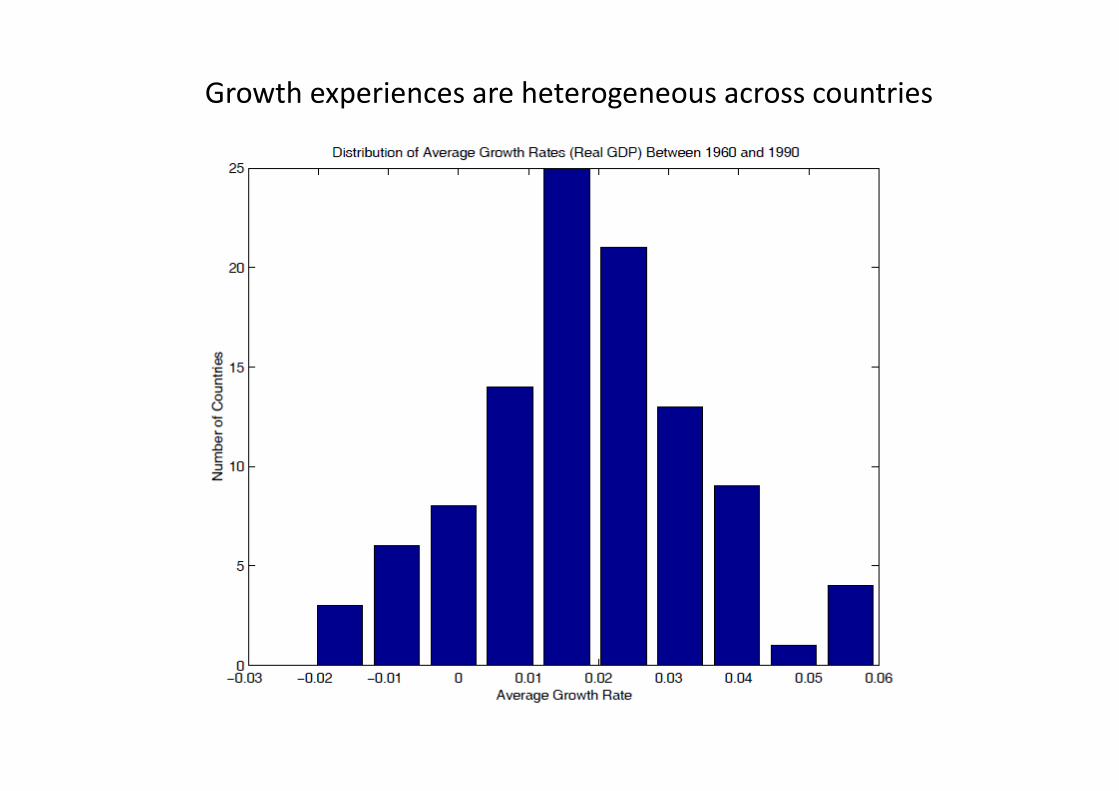

Growth experiences are heterogeneous across countries

What are the engines of economic growth?

• The full picture is complicated and involves many

different aspects. Next two lectures build up a

complete picture.

• Focus first on just one factor - capital accumulation.

Increases in the stock of physical capital (buildings and

machinery).

• Stress many other things important – not least how

efficiently this capital stock is used. Capital is just a

starting point.

Production function

OutputproducedOutput

produced

Buildings andmachinery

Buildings andmachinery

Labourinput

Labourinput

Technicalknowledge and

efficiency

Technicalknowledge and

efficiency

This lecture focuses on first input – capital accumulation

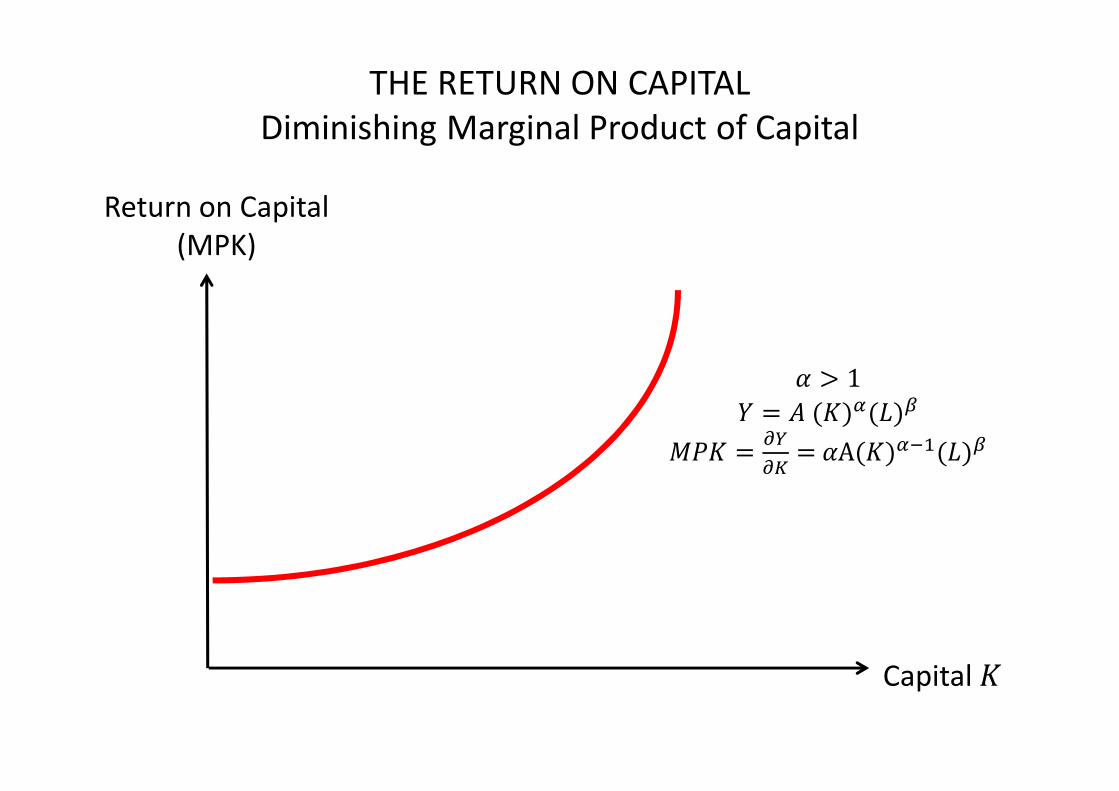

• How does increasing the capital stock lead to higher output?

The marginal product of capital (MPK) is the increase in output

that comes from increasing the capital stock leaving everything

else unchanged

• The MPK can be :

• decreasing (Solow neoclassical model) – each new machine

adds less than the last

• constant (Endogenous Growth I – AK) – each new machines

adds the same as the last

• increasing (Endogenous Growth II – Poverty Trap) – each new

machine adds more than the last

How does capital accumulation work?

THE RETURN ON CAPITAL

Diminishing Marginal Product of Capital

Capital �

Return on Capital

(MPK)

0 < � < 1

� = �(�)�( )���

��� =��

��= �A( /�)���

THE RETURN ON CAPITAL

Constant Marginal Product of Capital

Capital �

Return on Capital

(MPK)

� = 1

� = �K

��� =��

��= A

THE RETURN ON CAPITAL

Diminishing Marginal Product of Capital

Capital �

Return on Capital

(MPK)

� > 1

� = �(�)�( )�

��� =��

��= �A(�)���( )�

• Assumptions about MPK purely technological – no economics

involved.

• Different assumptions may be needed for different technologies.

• We stick on decreasing returns - neoclassical production function

with 0 < � < 1 and k =�

�= capital per capita:

��� =��

��= �A(�)���

Remark: Different assumptions lead to dramatically different

implications. What would cross country growth patterns look like if

MPK were initially increasing and then became decreasing?

The neoclassical MPK

} 1y∆

2} y∆

{k∆

{k∆

∆ > ∆1 2y y

Capital per worker �

Output per worker y

� = ���

The neoclassical production function

Will countries which invest more grow faster?

• Ultimately - No

• Short Term - Yes

• In long-run, investment affects only level not

growth of output.

• To show this we need to add some economics

to our technology assumption – need to

introduce investment.

Production: � = � (� )�( )

���

Capital accumulation:

� = (1 − ")� ��+$

"= depreciation rate; $ = investment

$ =Savings = constant fraction s of income:

$ = s� = &� (� )�( )

���

Thus, capital obeys to:

� = (1 − ")� ��+&� (� )�( )

���

The Solow growth model

� = (1 − ")� ��+&� (� )�( )

���

Assuming for now constant and � .

In per capita terms:

� = 1 − " � �� + &�(� )�

Steady-state is defined as: � = � �� = �∗

"�∗ = &�(�∗)�

Steady-state capital and output per worker:

�∗ = (()

*)�/(���); �∗ = �(�∗)�

The Solow growth model: steady state

Steady-state capital stock per worker

Capital per worker �

+ = &���

�∗

+ = "�Steady state

investment

per worker

� When capital stock is low:

Each new machine leads to a big increase in gross output

The amount of output needed to replace machines that have worn out is

low

As a result net output increases with the capital stock

� When capital stock is (too) high:

Each new machine leads to a small increase in gross output

Every period a substantial part of output is needed to replace machines

that have worn out

Eventually net output decreases with capital stock

� Key to these results is decreasing marginal return on capital.

Convergence to the steady state

Higher savings increase the steady-state capital stock

Steady state

investment

per worker

Capital per worker �

+ = &���

�∗

+ = "�

�∗∗

Higher &

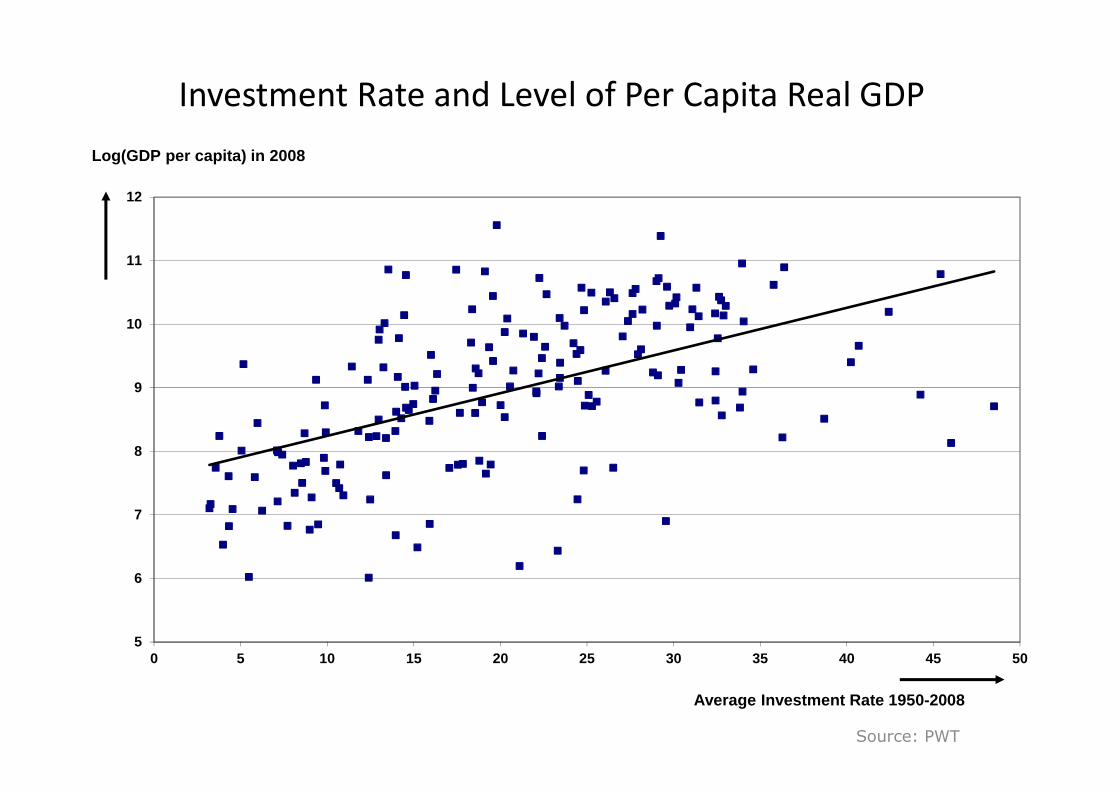

Source: PWT

Investment Rate and Level of Per Capita Real GDP

5

6

7

8

9

10

11

12

0 5 10 15 20 25 30 35 40 45 50

Log(GDP per capita) in 2008

Average Investment Rate 1950-2008

Savings or Investment?

• We are using investment and savings interchangeably

• If a country cannot borrow from overseas then its savings has

to equal investment.

• Most countries do not borrow much from overseas (as a % of

GDP) so savings and investment closely linked.

• When country borrows I > S but then it has to repay funds so

S>I. Therefore on average I = S

• When country can borrow abroad (I > S , convergence towards

steady-state can happen faster.

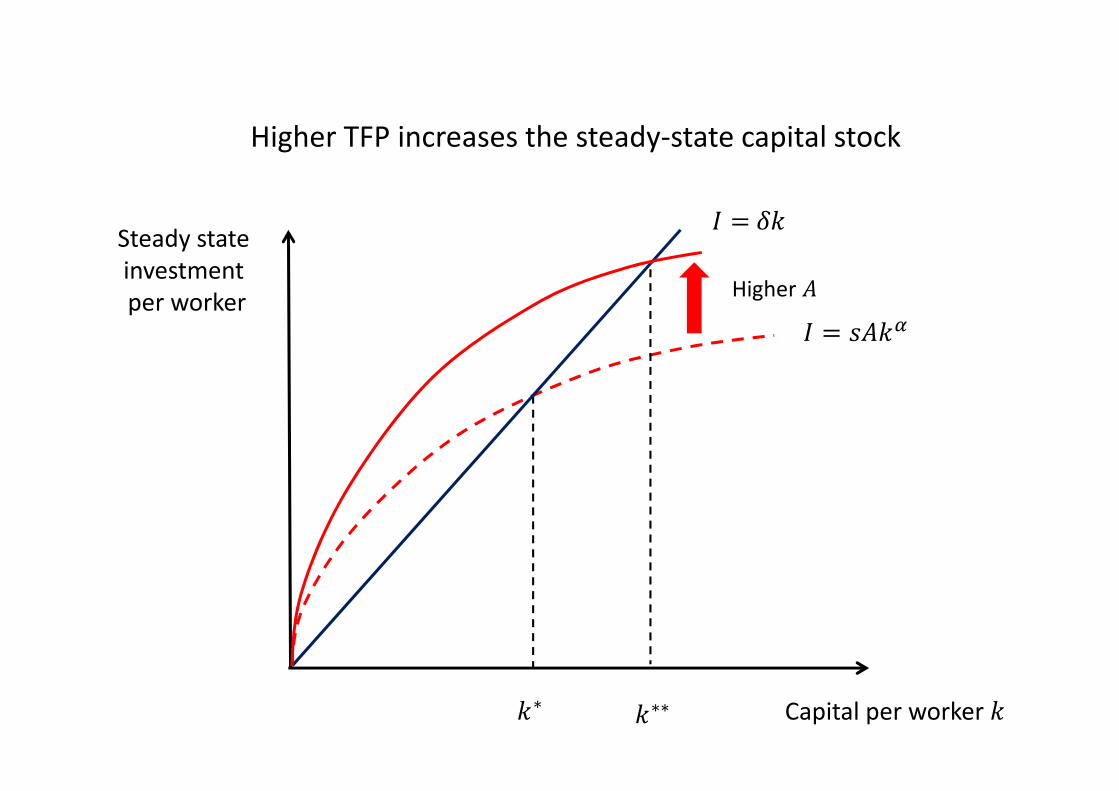

Higher TFP increases the steady-state capital stock

Capital per worker �

$ = &���

�∗

$ = "�

�∗∗

Higher �

Steady state

investment

per worker

� A high savings rate leads to high income but low consumption

� A low savings rate leads to low income but high consumption

Consumption per worker in the steady-state:

,∗ = (1 − &)�(�∗)� = (1 − &)(&�

")�/(���)

The “Golden rule” - level of savings that maximizes consumption

in the steady state. Simple calculations suggest that optimal rate

around 30-35% of GDP

Optimal consumption and welfare

- +

,∗ = (1 − &)�(�∗)� = (1 − &)(&�

")�/(���)

Optimal consumption and welfare

100%0%

,∗

&

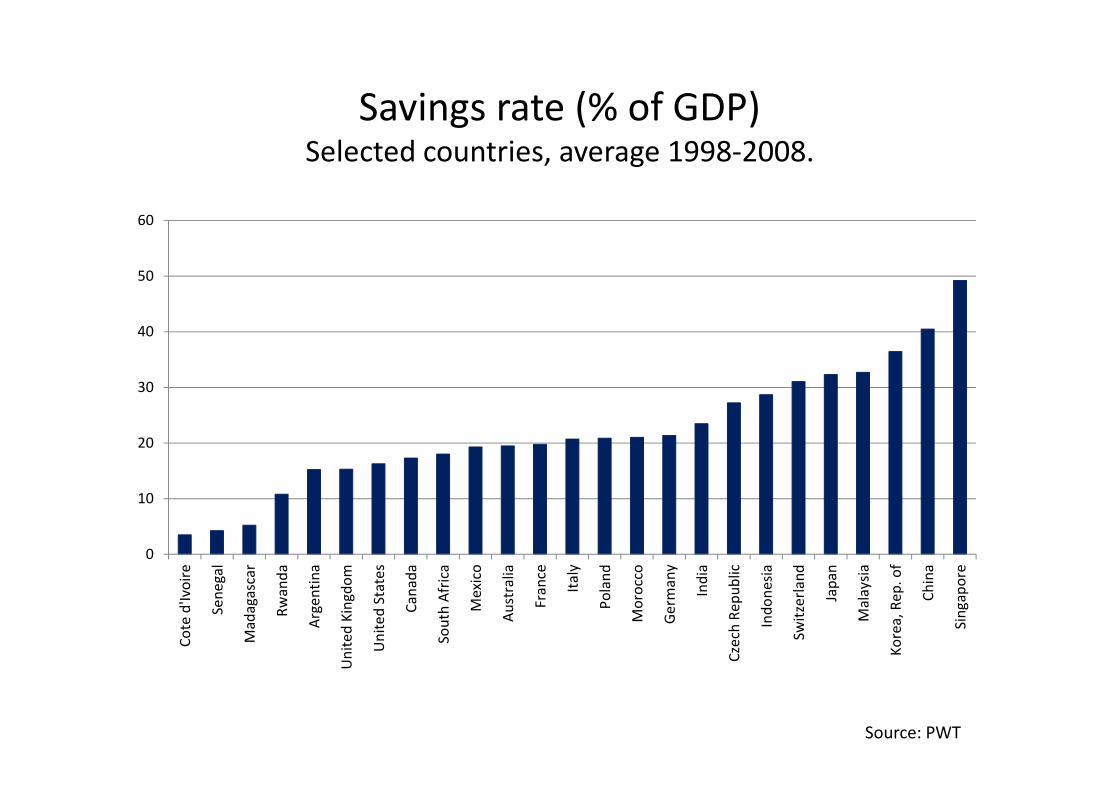

Savings rate (% of GDP) Selected countries, average 1998-2008.

Source: PWT

0

10

20

30

40

50

60

Co

te d

'Ivo

ire

Se

ne

ga

l

Ma

da

ga

sca

r

Rw

an

da

Arg

en

tin

a

Un

ite

d K

ing

do

m

Un

ite

d S

tate

s

Ca

na

da

So

uth

Afr

ica

Me

xico

Au

stra

lia

Fra

nce

Ita

ly

Po

lan

d

Mo

rocc

o

Ge

rma

ny

Ind

ia

Cze

ch R

ep

ub

lic

Ind

on

esi

a

Sw

itze

rla

nd

Jap

an

Ma

lay

sia

Ko

rea

, R

ep

. o

f

Ch

ina

Sin

ga

po

re

Steady-state: �∗ = (()

*)�/(���)

Dynamics: � = 1 − " � �� + &�(� )�

� = -(� ��)with�∗= -(�∗)

Convergence: � converges to �∗.

As � approaches �∗, the growth rate of � (and

output � ) decreases.

The further away from �∗ a country is, the faster

it grows.

The Solow growth model: dynamics

Dynamics of the capital stock per worker

�

� ��

� = -(� ��)

�∗

� = � ��

�∗

�.

45°

German GDP and capital growth 1936-1955

-50

-40

-30

-20

-10

0

10

20

3019

36

1937

1938

1939

1940

1941

1942

1943

1944

1945

1946

1947

1948

1949

1950

1951

1952

1953

1954

1955

GDP Growth

Change in Capital Stock

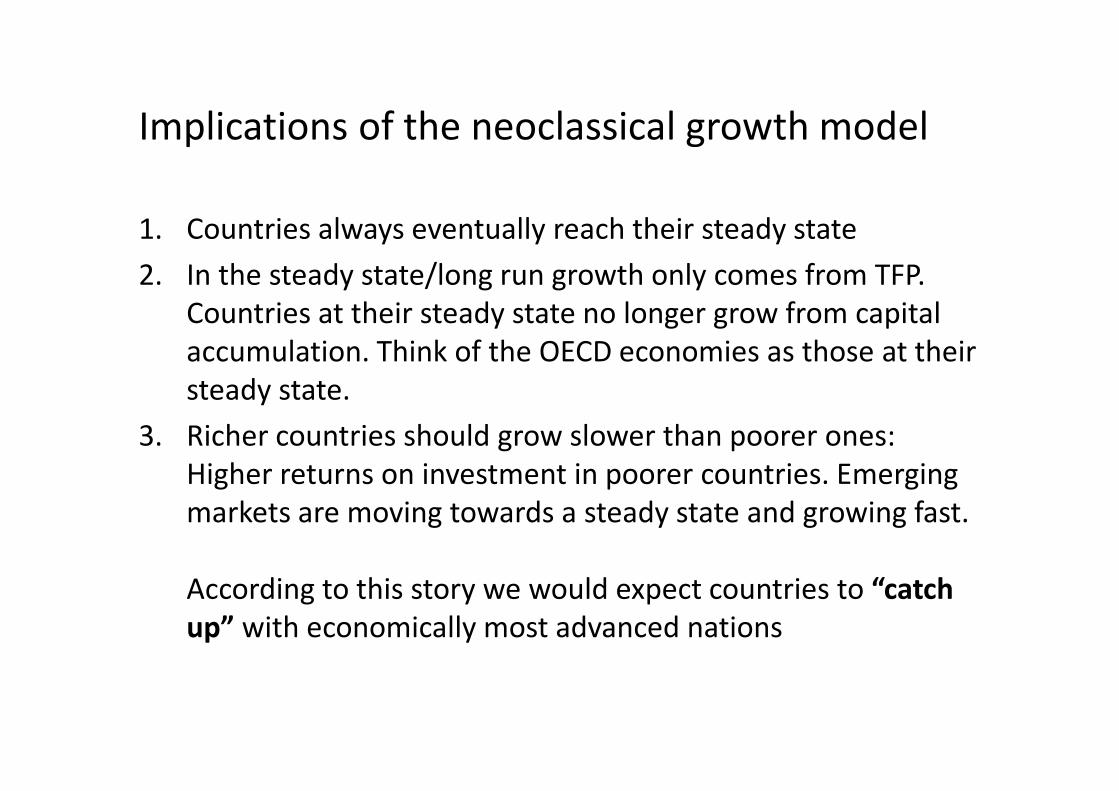

Implications of the neoclassical growth model

1. Countries always eventually reach their steady state

2. In the steady state/long run growth only comes from TFP.

Countries at their steady state no longer grow from capital

accumulation. Think of the OECD economies as those at their

steady state.

3. Richer countries should grow slower than poorer ones:

Higher returns on investment in poorer countries. Emerging

markets are moving towards a steady state and growing fast.

According to this story we would expect countries to “catch

up” with economically most advanced nations

Catch up amongst Europe’s big 4

Source: Maddison, GGDC and DataStream

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

11.018

6118

6618

7118

7618

8118

8618

9118

9619

0119

0619

1119

1619

2119

2619

3119

3619

4119

4619

5119

5619

6119

6619

7119

7619

8119

8619

9119

9620

0120

06

France

Germany

Italy

UK

Log output per capita (US $ 1990)

1. The neoclassical growth model

2. Do countries catch up with economic leaders?

3. The Asian growth miracle?

Lecture 2 : Long-term economic growth

Growth and factors of production

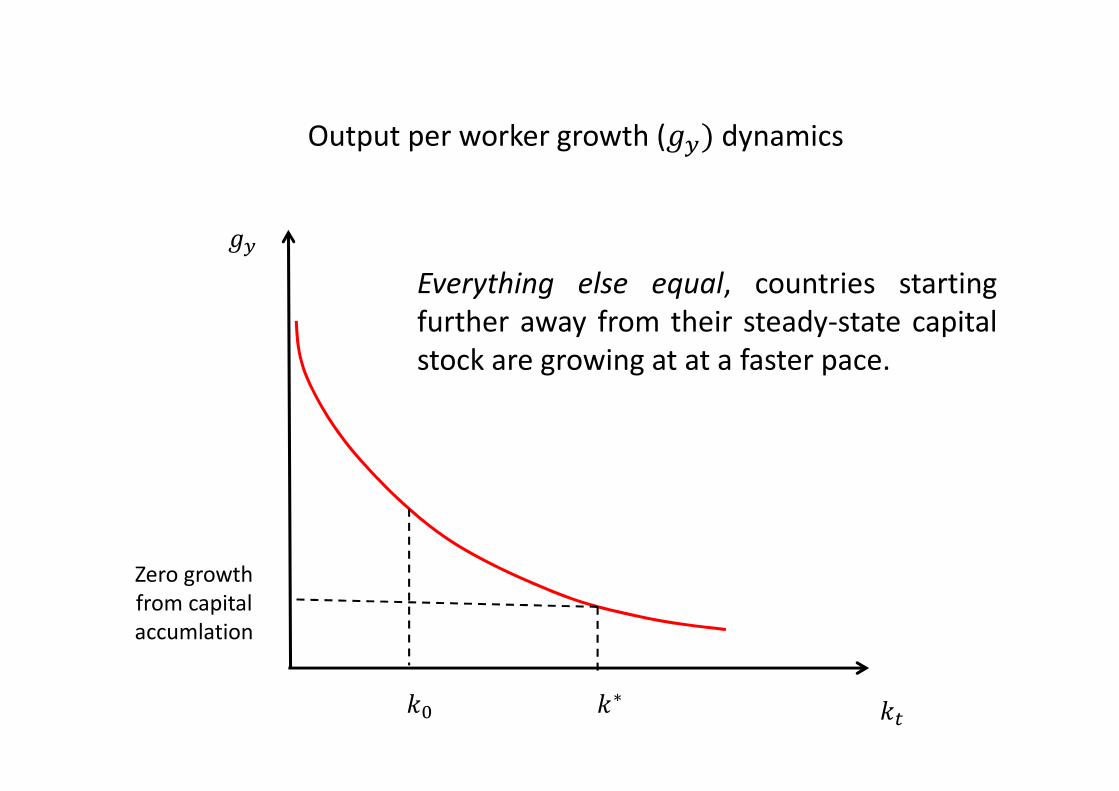

Output per worker growth (/0) dynamics

/0

� �∗�.

Everything else equal, countries starting

further away from their steady-state capital

stock are growing at at a faster pace.

Zero growth

from capital

accumlation

Do countries converge?

• According to the Solow neoclassical growth model,

poorer countries (in terms of capital stock per worker

should) grow faster.

• Does it hold in the data?

• Investigate link between future growth and initial

income per capita.

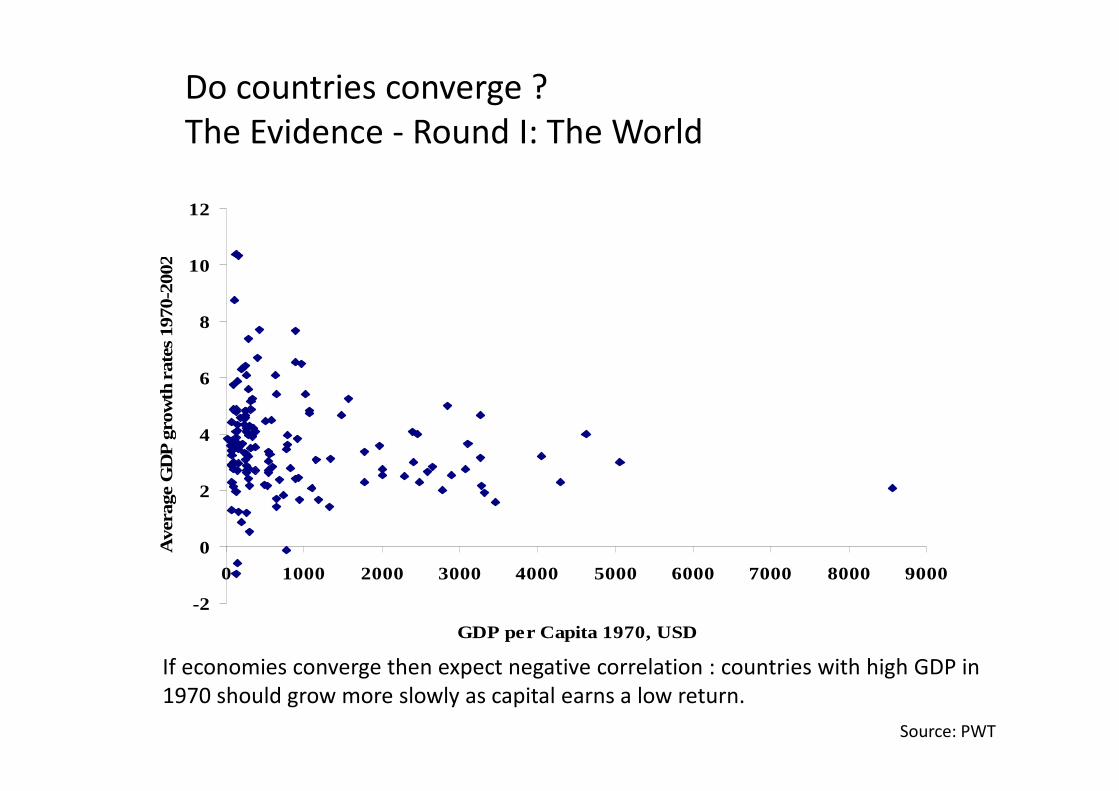

Do countries converge ?

The Evidence - Round I: The World

-2

0

2

4

6

8

10

12

0 1000 2000 3000 4000 5000 6000 7000 8000 9000

GDP per Capita 1970, USD

Ave

rage

GD

P g

row

th r

ates

197

0-20

02

If economies converge then expect negative correlation : countries with high GDP in

1970 should grow more slowly as capital earns a low return.

Source: PWT

Do economies converge?

The evidence - Round II: OECD

Evidence for convergence is much stronger

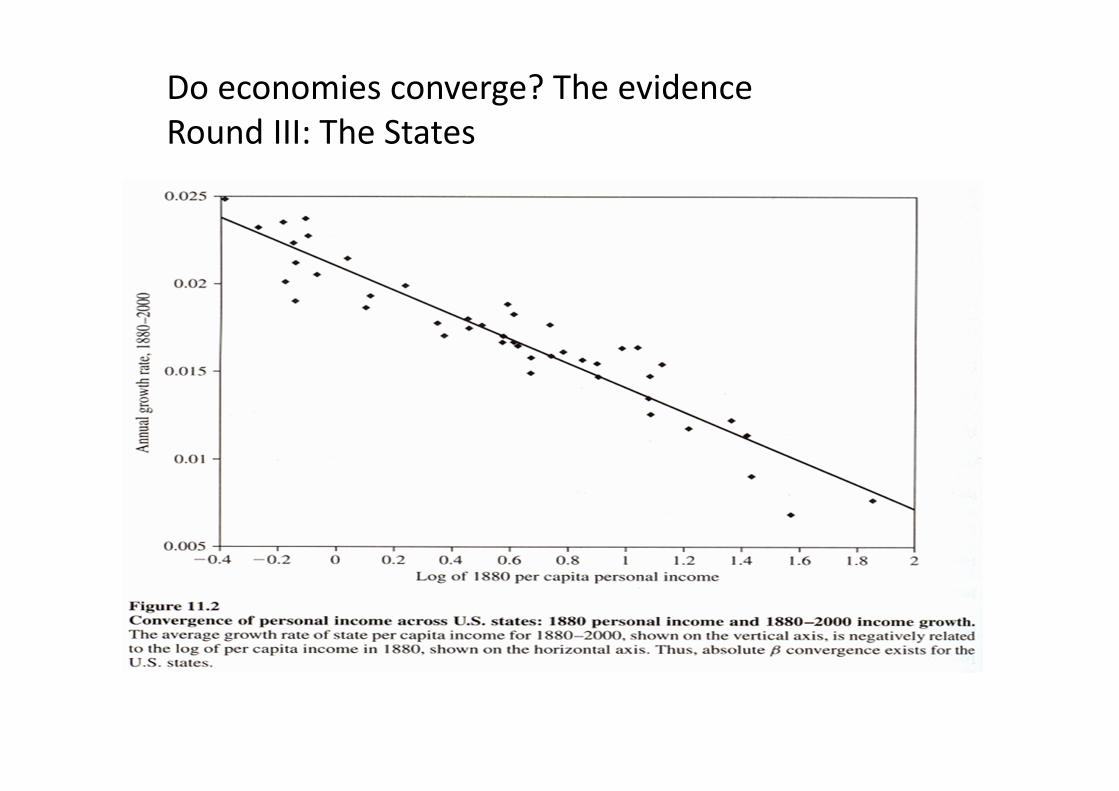

Do economies converge? The evidence

Round III: The States

Do economies converge?

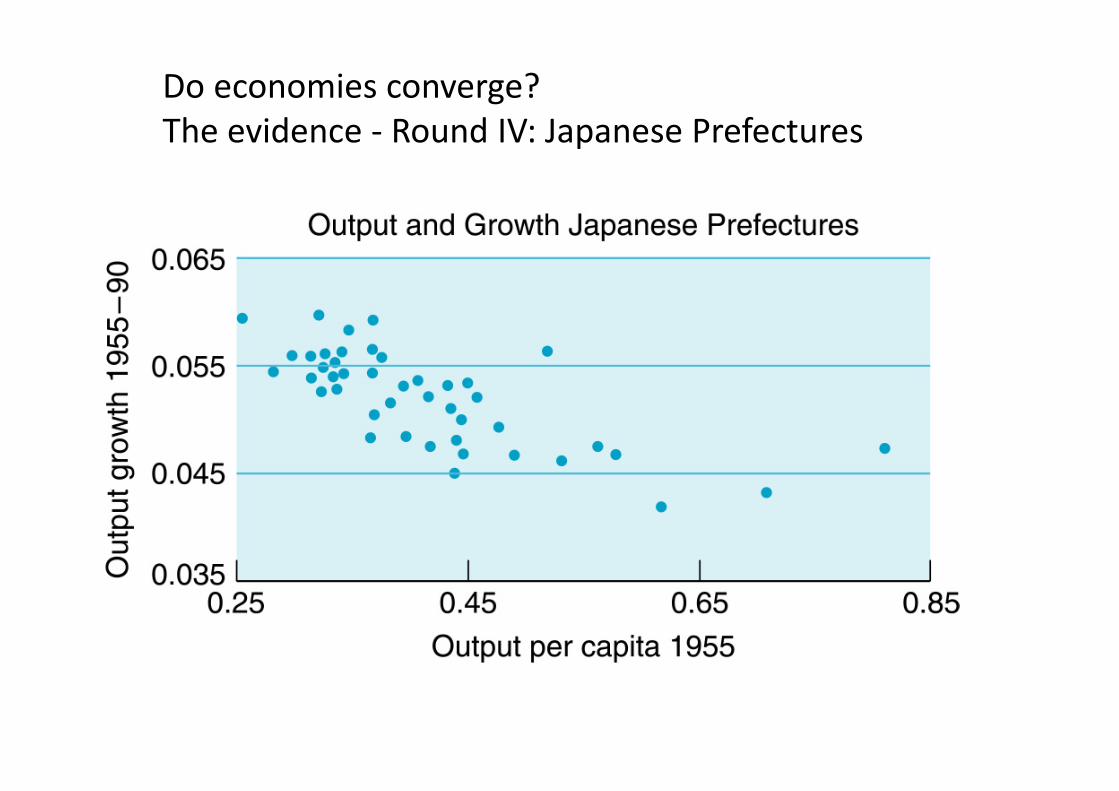

The evidence - Round IV: Japanese Prefectures

Do economies converge?

The evidence - Round V: European Regions

Do economies converge?

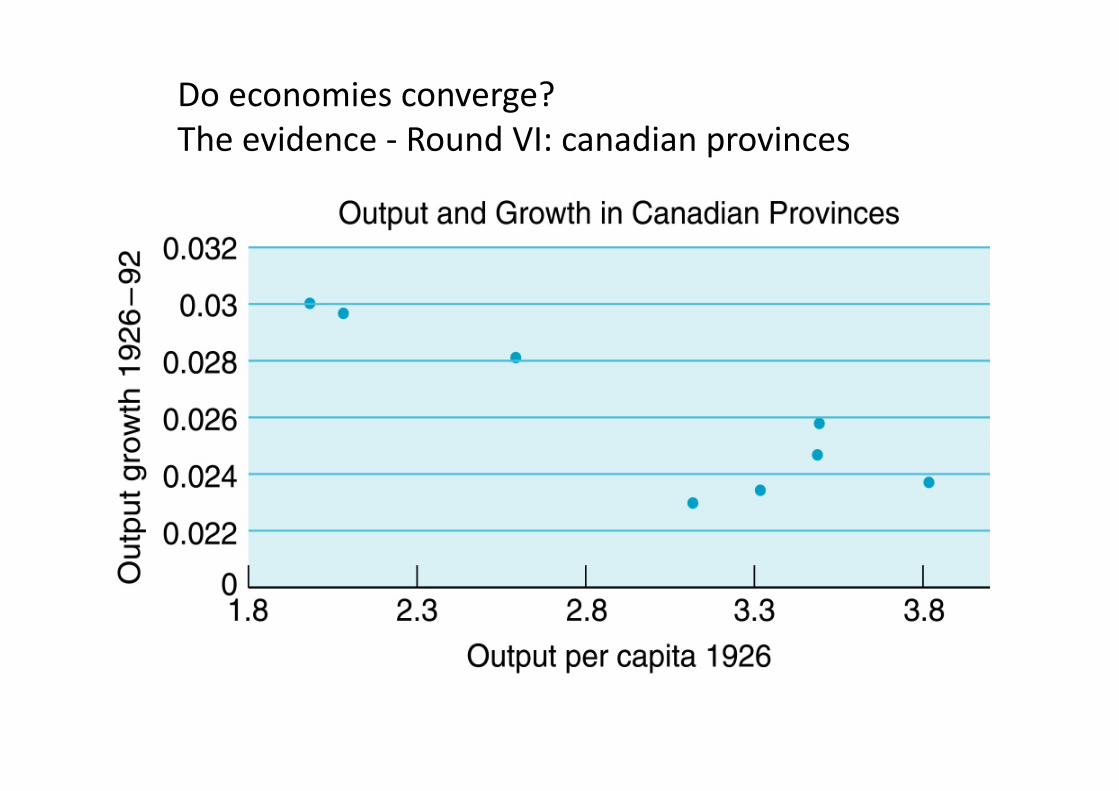

The evidence - Round VI: canadian provinces

The “Iron Law of Convergence”

• On average 2% of the gap between poor and rich

countries that are similar vanishes in a year.

• Very slow - takes 35 years to eliminate half of the

initial output gap.

Reconciling the evidence

•When we look at all economies no evidence of convergence.

• When we examine very similar countries strong evidence of

convergence.

• How can we explain this mixed evidence concerning

convergence?

- take into account that steady states can differ across

countries!

Conditional convergence

• Neoclassical Solow model does not predict convergence

unconditionally.

• Everything else equal, countries with lower capital stock

should grow faster.

• Countries with same steady-state should converge =

conditional convergence

• In particular, countries with lower TFP (or lower savings)

should not catch-up.

• Importance for growth is distance from steady-state which

can be different across countries.

Conditional convergence: an illustration

Which country should grow faster?

Capital per worker �

&�12��= &�345464��

�784564 �345464

Steady state

investment

per worker

�12

&�784564��

Initial conditions:

�784564 < �12 = �345464

�784564 < �345464 < �12

$ = "�

•Only when countries share the same steady state should we

see convergence. Explains why only see evidence for

convergence amongst similar countries.

• Explains why many African countries do not catch up with

Europe/U.S.

• Suggests that wealthier economies will persistently stay

wealthier, but within wealthier economies should see evidence

of catch up.

• The big question is what determines a countries steady state?

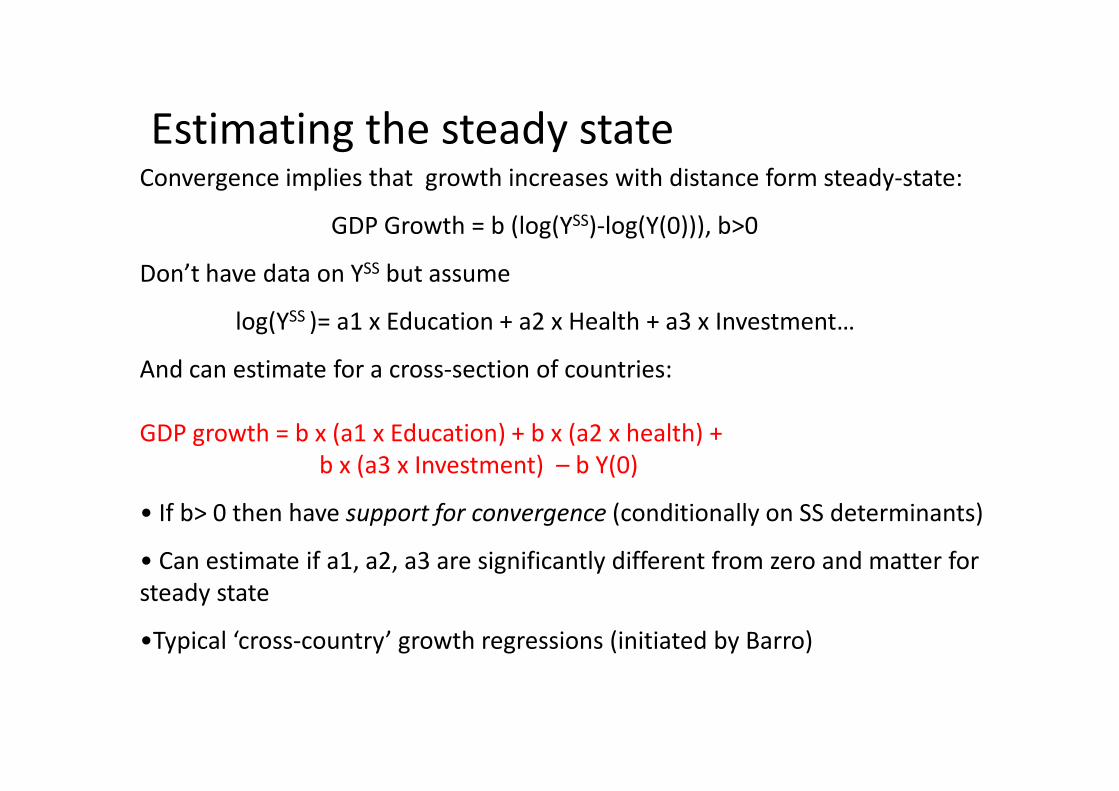

Conditional convergence

Convergence implies that growth increases with distance form steady-state:

GDP Growth = b (log(YSS)-log(Y(0))), b>0

Don’t have data on YSS but assume

log(YSS )= a1 x Education + a2 x Health + a3 x Investment…

And can estimate for a cross-section of countries:

GDP growth = b x (a1 x Education) + b x (a2 x health) +

b x (a3 x Investment) – b Y(0)

• If b> 0 then have support for convergence (conditionally on SS determinants)

• Can estimate if a1, a2, a3 are significantly different from zero and matter for

steady state

•Typical ‘cross-country’ growth regressions (initiated by Barro)

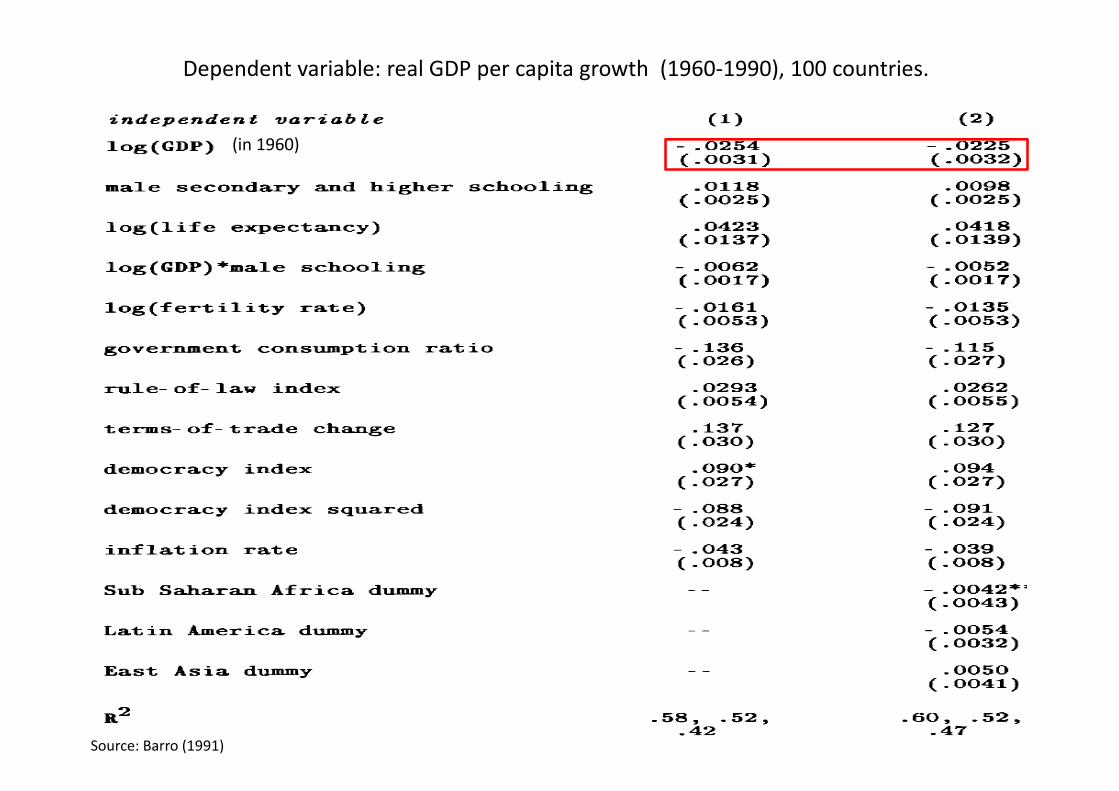

Estimating the steady state

Source: Barro (1991)

Dependent variable: real GDP per capita growth (1960-1990), 100 countries.

(in 1960)

‘I JUST RAN TWO MILLION REGRESSIONS’

(Salah-i-Martin (1997))

Always significant Frequently significant Often significant Sometimes significant

Education – Primary school Enrolment

Regional dummies (Latin America, Sub Saharan Africa, Negative)

Exchange Rate

Overvaluation (Negative)

Government Consumption (Negative)

Investment Rule of Law Black market premiums (Negative)

Financial Sophistication

Health – Life Expectancy Political Rights Primary Products (% exports – Negative)

Inflation (Negative)

Religious dummies (confucian, Muslim, Protestant)

Ethnic Diversity (Negative)

Openness Civil Liberties

Degree of Capitalism Revolutions, Coups, Wars (Negative)

Religious dummies (Buddhism, Catholic)

Public Investment

1. The neoclassical growth model

2. Do countries catch with economic leaders?

3. The Asian growth miracle?

Lecture 2 : Long-term economic growth

Growth and factors of production

�Since the post-war period we have witnessed astonishing levels

of growth in the “Asian Tigers”.

� The press and political commentators:

� Bad for the West: Take our jobs

� Western leaders and CEO’s should look at the Tigers and

learn how to improve efficiency.

� Economists: No growth miracle. Just accumulation of inputs.

Asian Tigers: growth miracle?

Average Growth GDP per capita 1966-2009

Source : Penn WT 6.3 and DataStream.

0% 1% 2% 3% 4% 5% 6% 7%

Germany

Mexico

US

Canada

France

Brazil

Italy

Chile

Japan

Singapore

HongKong

China

Korea

Taiwan

Investment rates

0

10

20

30

40

50

60

7019

60

1963

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

Source : Penn World Table 6.3

% of GDP

Singapore

Hong Kong

China

Large amount of compulsory savings in Singapore

0

10

20

30

40

50

60

1982 1983 1984 1985 1986 1987 1988 1989 1990 1991

Employee

Employers

% of Wages

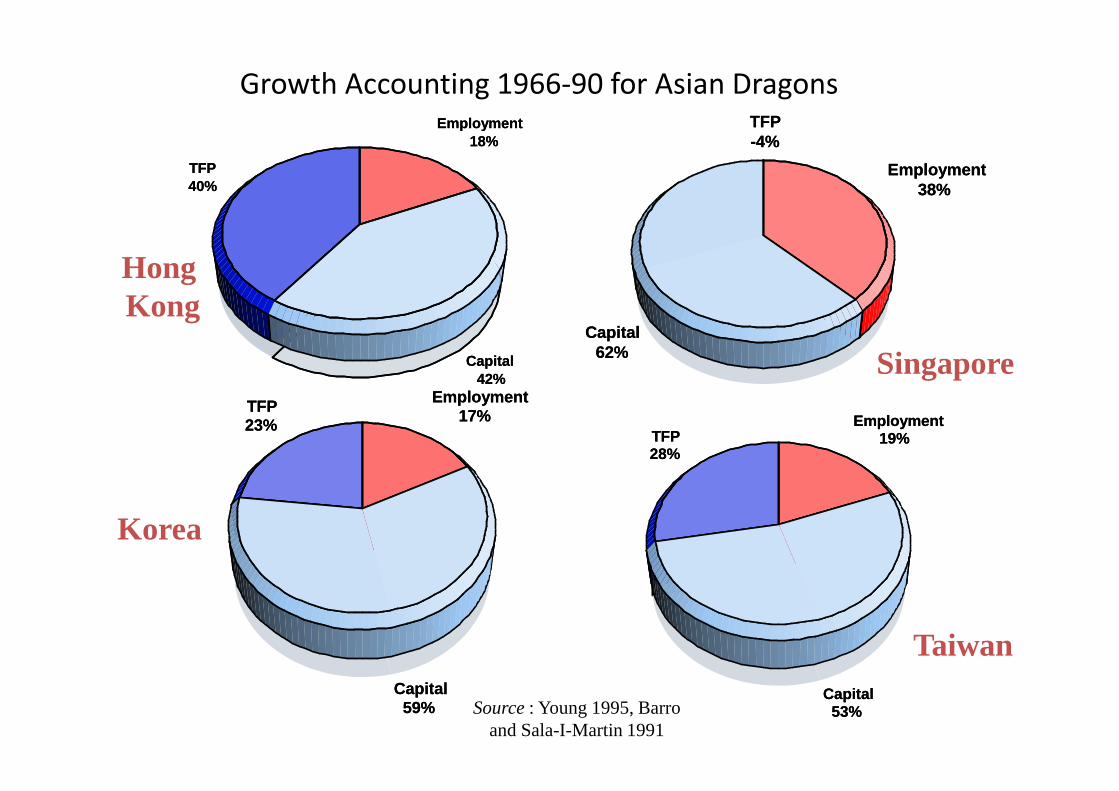

Source : Young 1995, Barro and Sala-I-Martin 1991

CPF Contributions

Growth Accounting 1966-90 for Asian DragonsEmployment

18%

Capital42%

TFP40%

Employment18%

Capital42%

TFP40%

Employment38%

Capital62%

TFP-4%

Employment38%

Capital62%

TFP-4%

Employment17%

Capital59%

TFP23%

Employment17%

Capital59%

TFP23% Employment

19%

Capital53%

TFP28%

Employment19%

Capital53%

TFP28%

Source : Young 1995, Barroand Sala-I-Martin 1991

Hong Kong

Singapore

Korea

Taiwan

� Some differences in the sources of growth. BUT: Increased capital stock MOST important factor for all of them.

� Krugman: “Perspiration rather than inspiration”!

� Too rapid development? No gains from the learning curve? Incorrect balance between innovation and experience?

� Does it matter?

� No: They got much richer anyway

� Yes: Some have paid for it - those that were young early on in the process: Low income, high savings

� Future? Need to shift from extensive to intensive margin

Asian Tigers: growth miracle?

• Countries show enormous differences in their standard of living. Further

some poor countries have shown rapid growth while others have

remained poor.

• The neoclassical (Solow) growth model focuses on explaining these

differences through capital accumulation, assuming diminishing marginal

product of capital. This assumption implies convergence. Countries with

high investment rates have a high steady state and are rich. At the steady

state all countries grow at the rate of technological progress.

• The neoclassical model relies on conditional convergence – conditional on

countries sharing the same steady state then poorer countries will grow

faster than rich ones.

• The steady state depends on many factors. Strong roles are found for

education, health and rate of investment but many other additional

variables are also found important. The analysis suggests that making a

country rich will involve a broad package of economic, social and political

policies – don’t look for magic ingredient X.

Summary

![Lecture 4 [0.3cm] Tax structures: production efficiency ...econ.sciences-po.fr/sites/default/files/file/laroque/lect4.pdf · Tax structures: production e ciency and ... Destructive](https://img.pdfslide.us/doc/110x75/5ab224fc7f8b9a284c8d458a/lecture-4-03cm-tax-structures-production-efficiency-econsciences-pofrsitesdefaultfilesfilelaroquelect4pdftax.jpg)