Embed Size (px)

Citation preview

1

Chapter 2

Aggregate Supply – Aggregate Demand and the Phillips Curve

EPP, 2011 Yann Algan

2

1. INTRODUCION

Questions

Impact of supply and demand shocks on the economy ?

Expectations, credibility and Public Policies

Relation between inflation, unemployment and fluctuations ?

3

Need a more general framework than the IS-LM model

Nominal rigidities • Prices on the product market are less rigid than wages • Need to integrate price adjustment and inflation

Natures of shocks • Fluctuations are not uniquely driven by demand shocks and shortage of demand • Role of supply shocks : ex stagflation

Synthesis • AS/AD framework: wage rigidities but price flexibility • Inflation and output fluctuations: Phillips curve

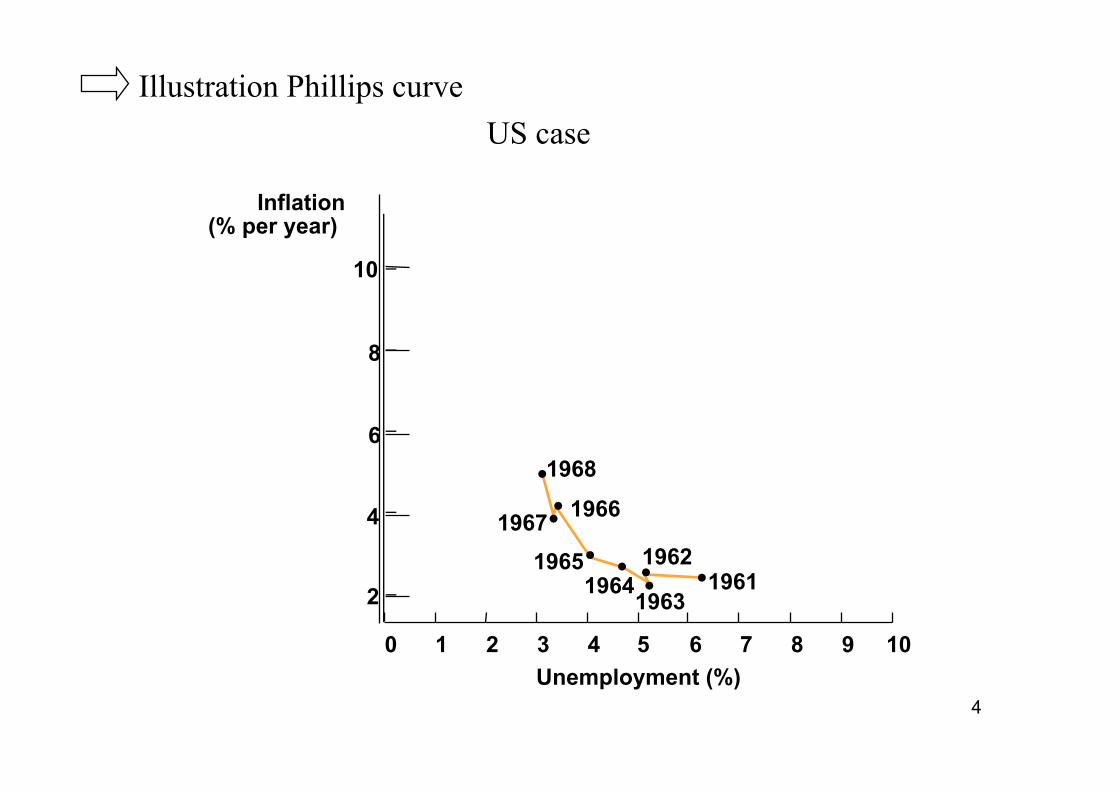

4

US case

Unemployment (%)

Inflation (% per year)

0 1 2 3 4 5 6 7 8 9 10 2

4

6

8

10

1968 1966

1961 1962 1963

1967 1965

1964

Illustration Phillips curve

5 Unemployment (%)

Inflation (% per year)

0 1 2 3 4 5 6 7 8 9 10 2

4

6

8

10

1973 1971 1969 1970 1968

1966

1961 1962 1963

1967 1965

1964

1972

6

2. Aggregate Supply

Framework for understanding the determinants of aggregate supply

Interplay between labor market and product market

Positive relationship between aggregate supply and prices

7

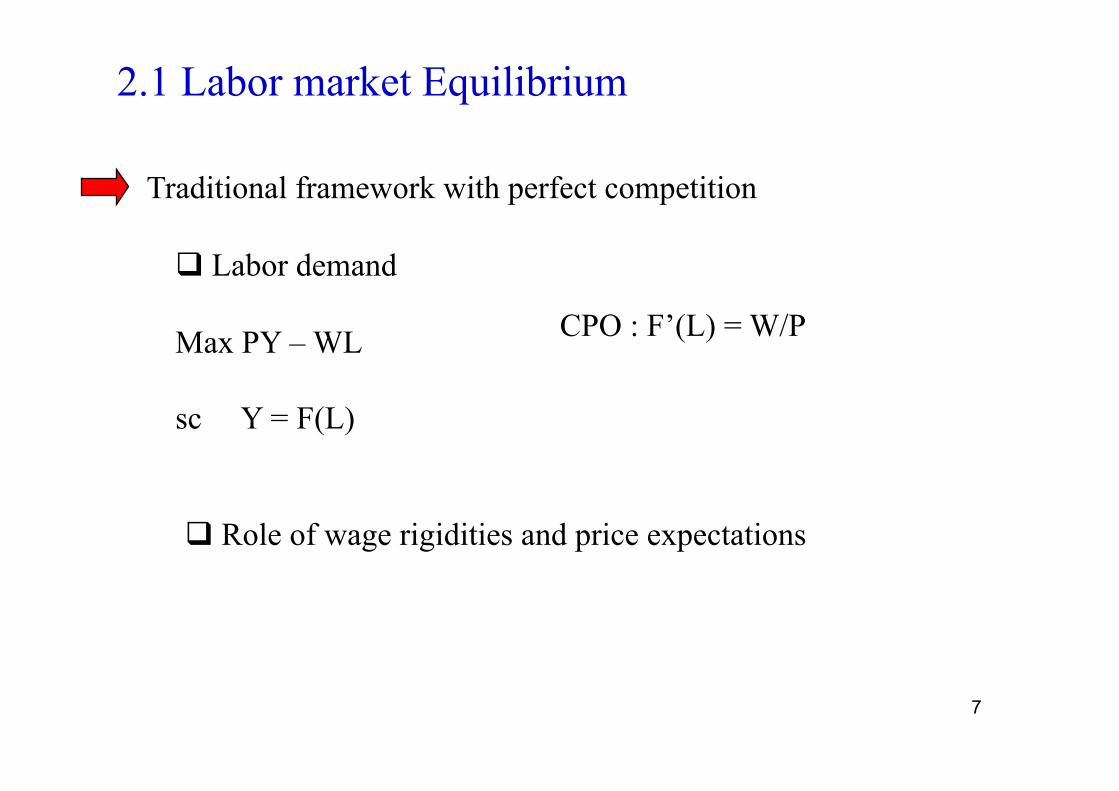

2.1 Labor market Equilibrium

Traditional framework with perfect competition

Labor demand

Max PY – WL

sc Y = F(L)

CPO : F’(L) = W/P

Role of wage rigidities and price expectations

8

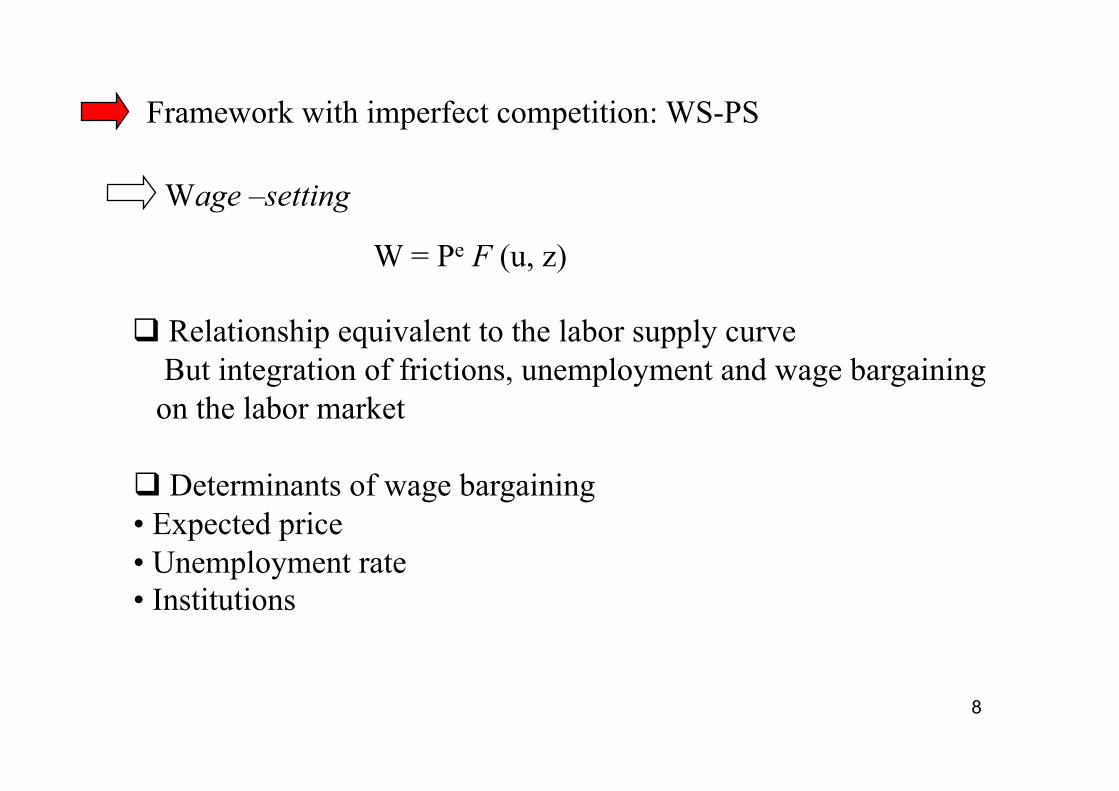

Wage –setting

Framework with imperfect competition: WS-PS

Determinants of wage bargaining • Expected price • Unemployment rate • Institutions

W = Pe F (u, z)

Relationship equivalent to the labor supply curve But integration of frictions, unemployment and wage bargaining on the labor market

9

Price-setting curve

P = (1 + µ) W

Relation PS equivalent to the labor demand … But integration of imperfect competition on the product market

10

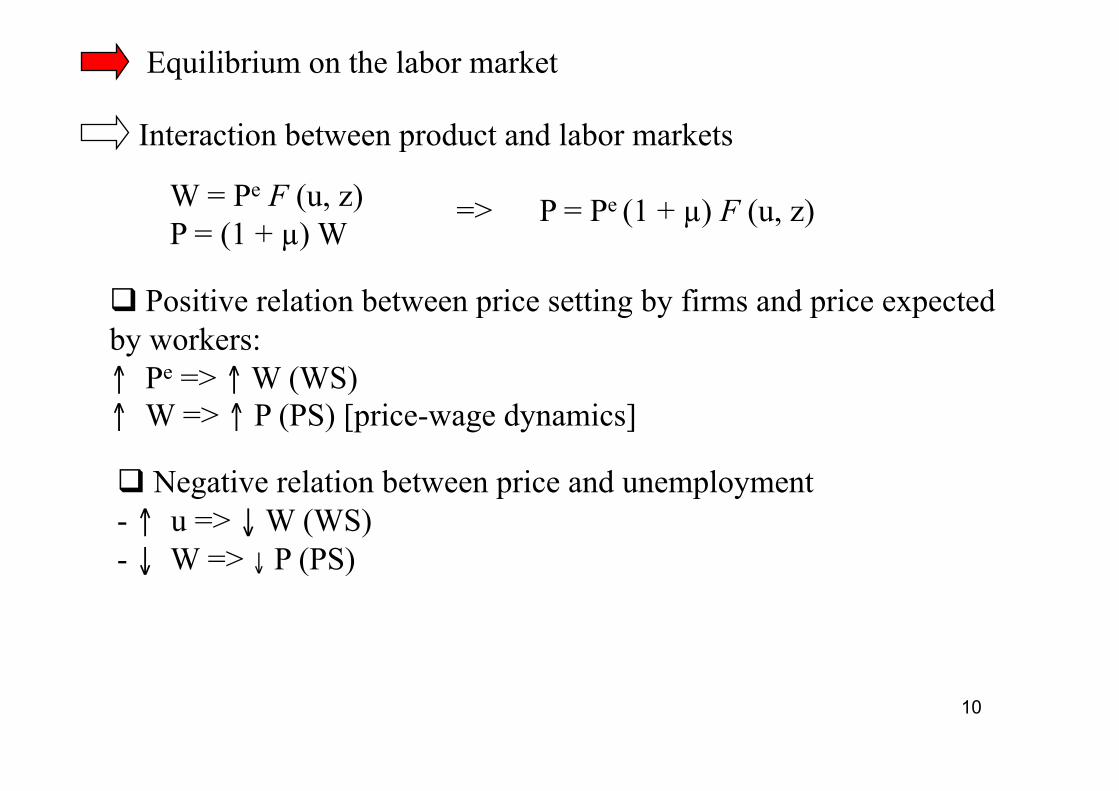

Equilibrium on the labor market

Interaction between product and labor markets

W = Pe F (u, z) P = (1 + µ) W

=> P = Pe (1 + µ) F (u, z)

Positive relation between price setting by firms and price expected by workers: ↑ Pe => ↑ W (WS) ↑ W => ↑ P (PS) [price-wage dynamics]

Negative relation between price and unemployment - ↑ u => ↓ W (WS) - ↓ W => ↓ P (PS)

11

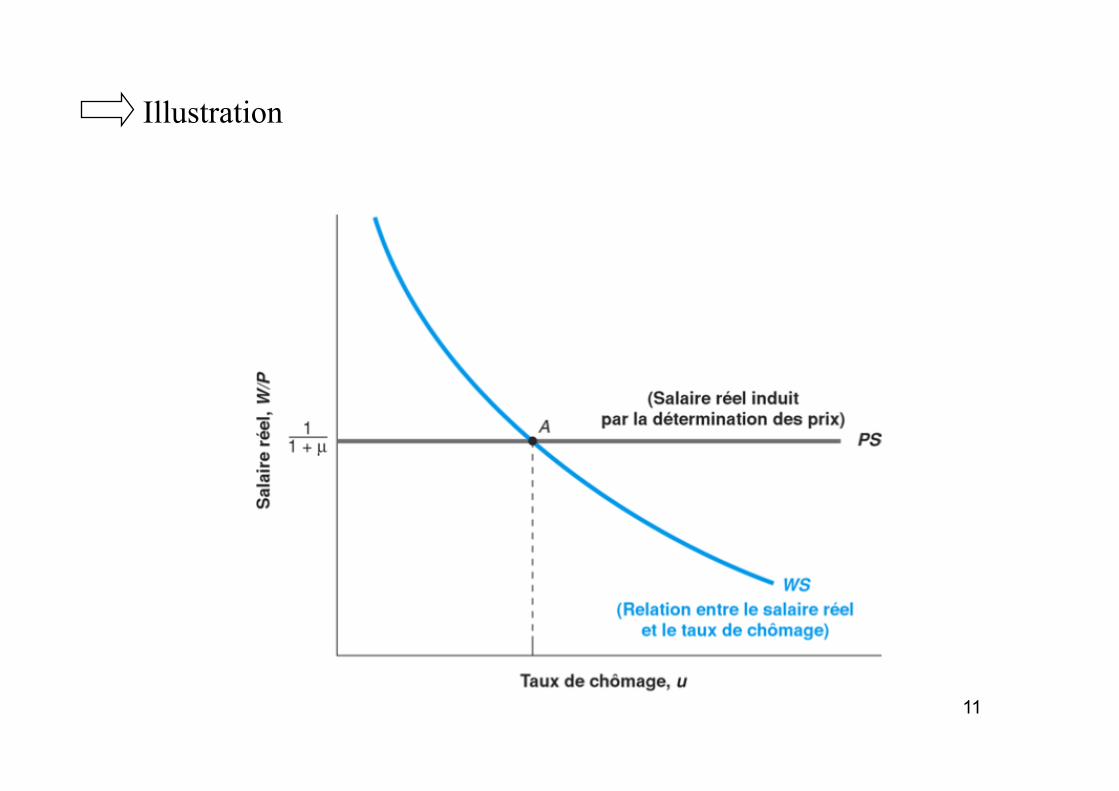

Illustration

12

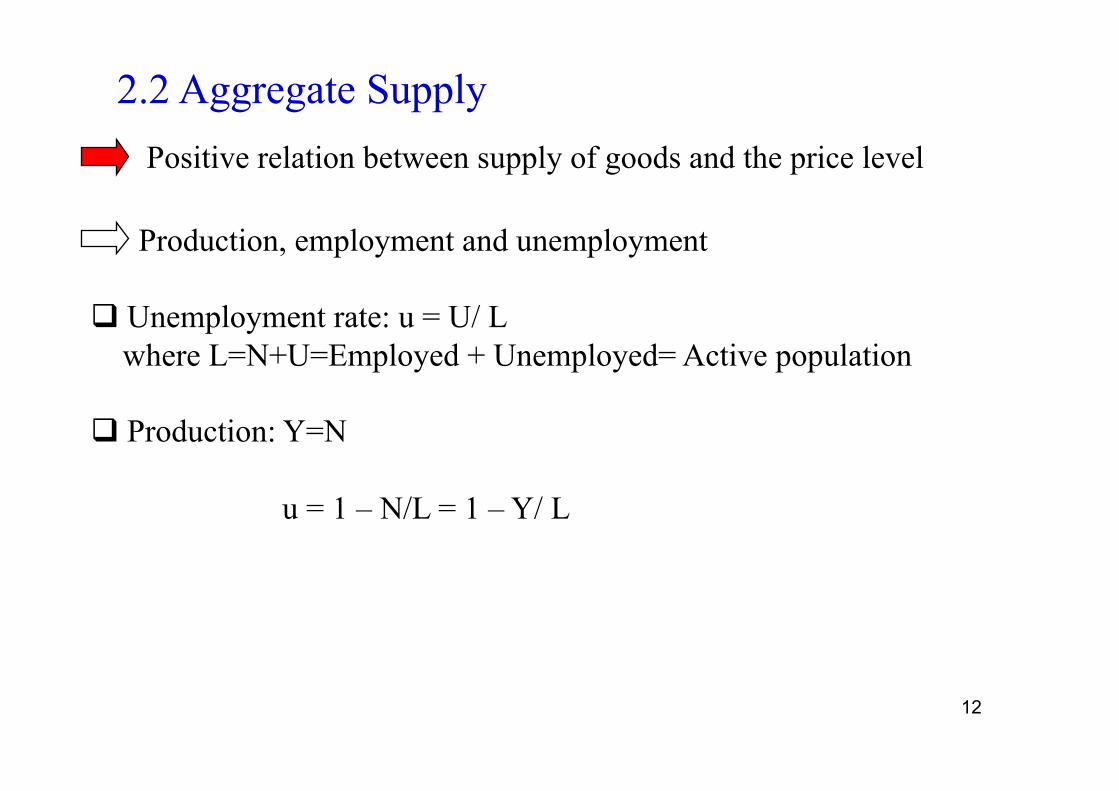

2.2 Aggregate Supply Positive relation between supply of goods and the price level

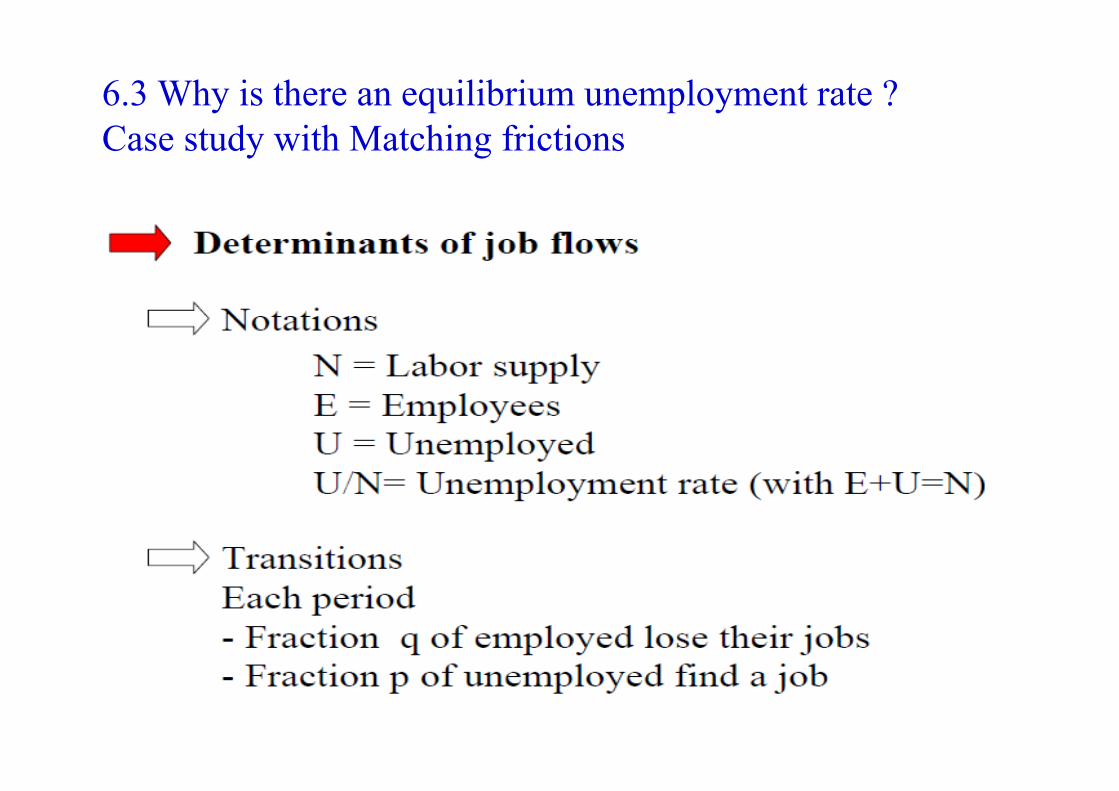

Unemployment rate: u = U/ L where L=N+U=Employed + Unemployed= Active population

Production: Y=N

u = 1 – N/L = 1 – Y/ L

Production, employment and unemployment

13

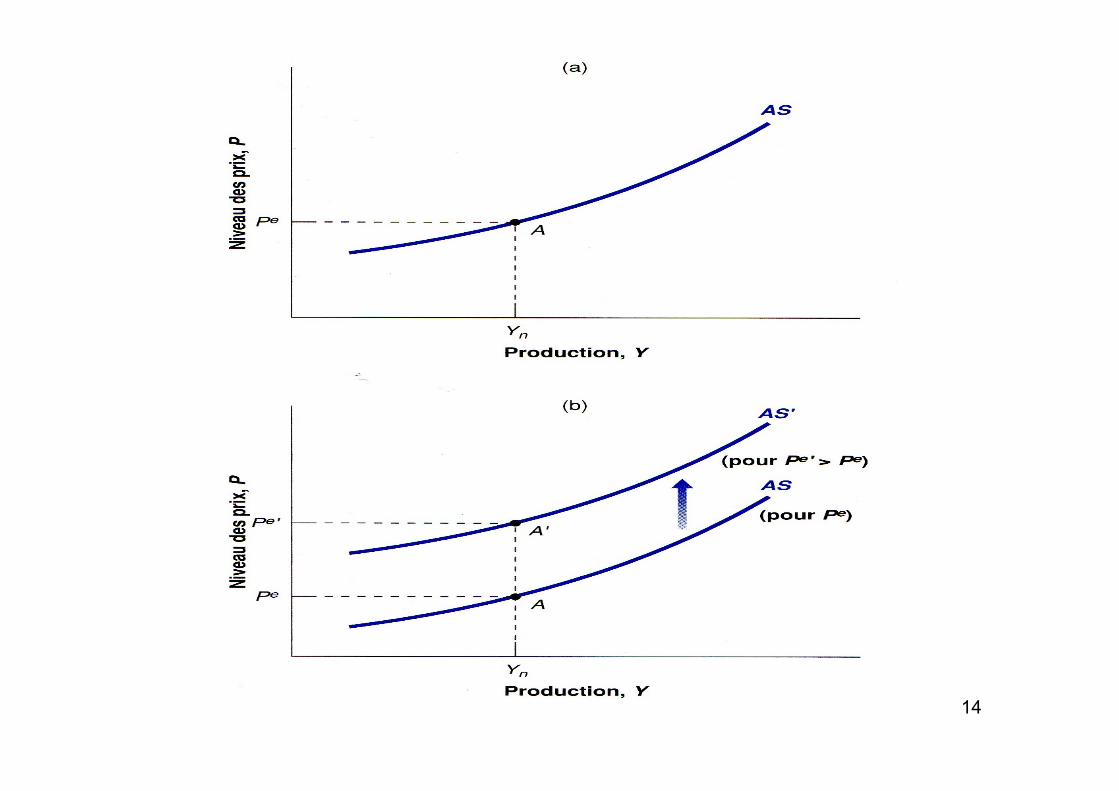

Aggregate supply

P = Pe (1 + µ) F (1-Y/L, z)

Positive relation between Y and P

• ↑ Y => ↑ N (cf. production function Y = N) • ↑ N => ↓ u • ↓ u => ↑ W (WS) • ↑ W => ↑ P (PS)

Implication : AS curve, for a given Pe, increases with P

14

15

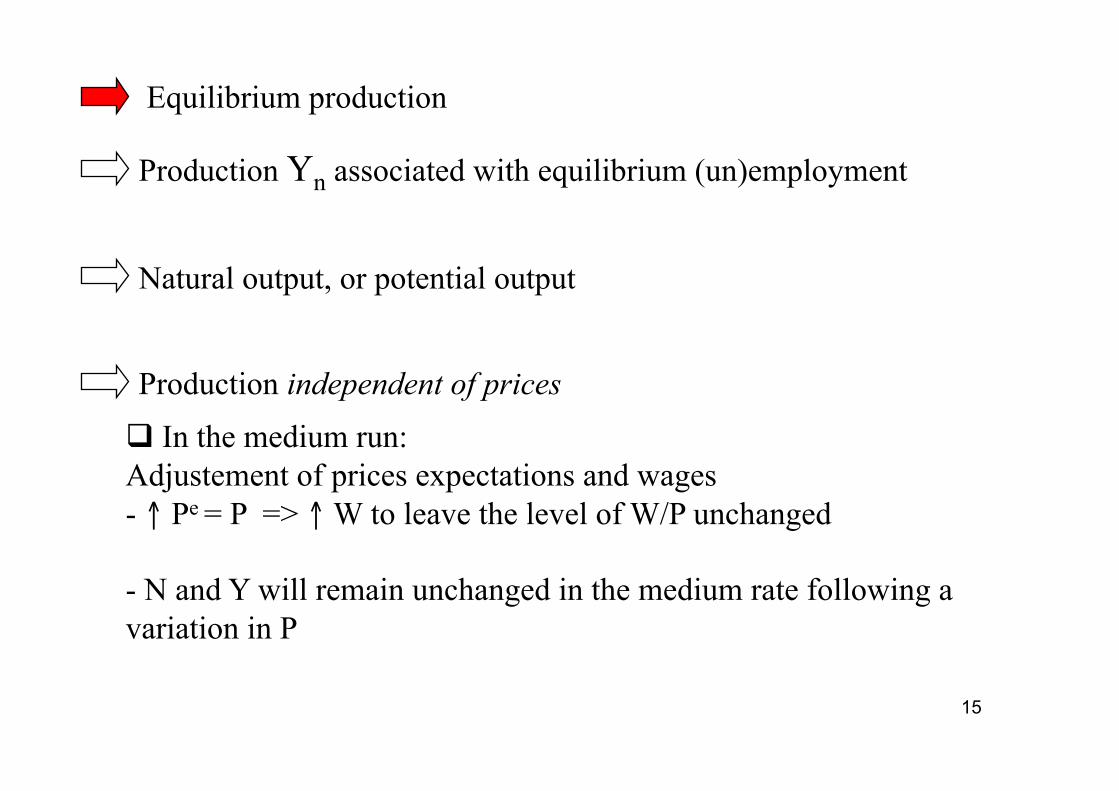

Equilibrium production

Production Yn associated with equilibrium (un)employment

Natural output, or potential output

In the medium run: Adjustement of prices expectations and wages - ↑ Pe = P => ↑ W to leave the level of W/P unchanged

- N and Y will remain unchanged in the medium rate following a variation in P

Production independent of prices

16

Equilibrium unemployement when P= Pe

Equalization

Structural unemployment rate: Real rigidities and frictions (mark-up, institutions…)

W = Pe F (u, z) P = (1 + µ) W

and P = Pe (WS) (PS)

In the short run, potential fluctuations of unemployment around the equilibrium unemployment. In the medium run: equilibrium unemployment independent of prices

17

Definition

3. Aggregate Demand

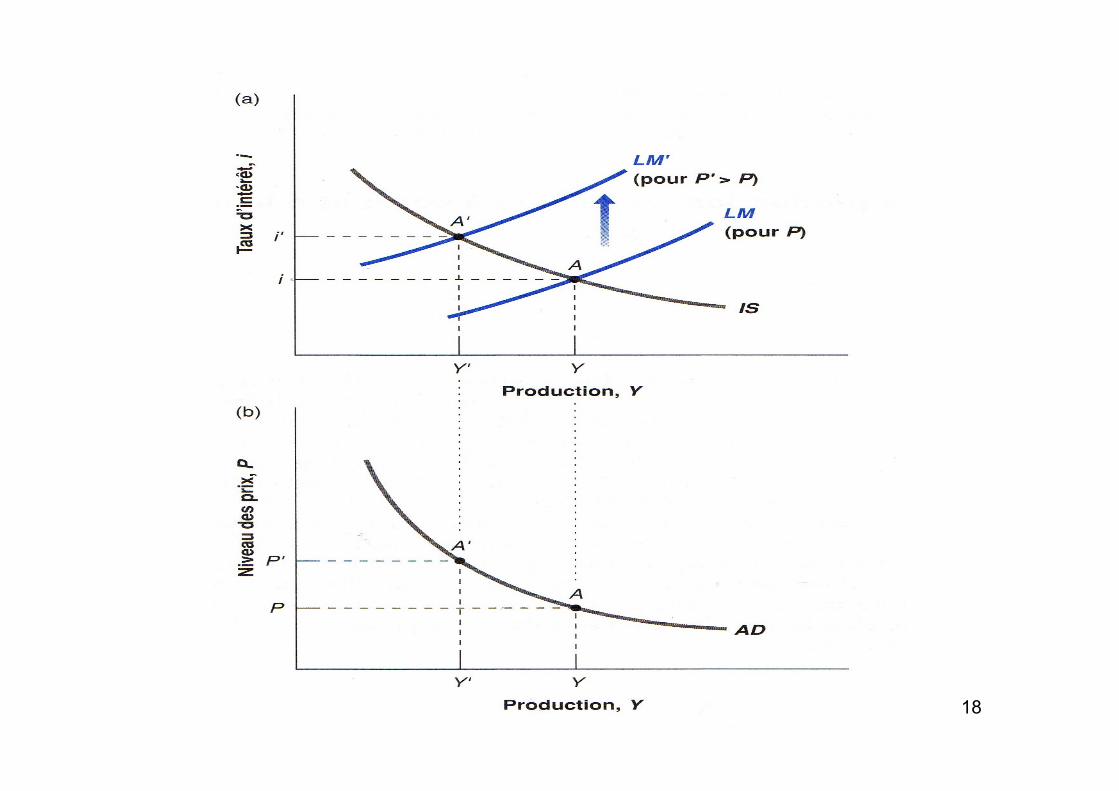

Demand on the product market consistent with money market equilibrium. Derived from the IS-LM side.

Integration of price effect on demand: decreasing relation between demand and prices

↑ P => ↓ M/ P => LM curve shifts upward ↑ i and ↓ de Y

Aggregate demand determinants

Y = Y(M/P, G, T) (+ , + , - )

LM IS

18

19

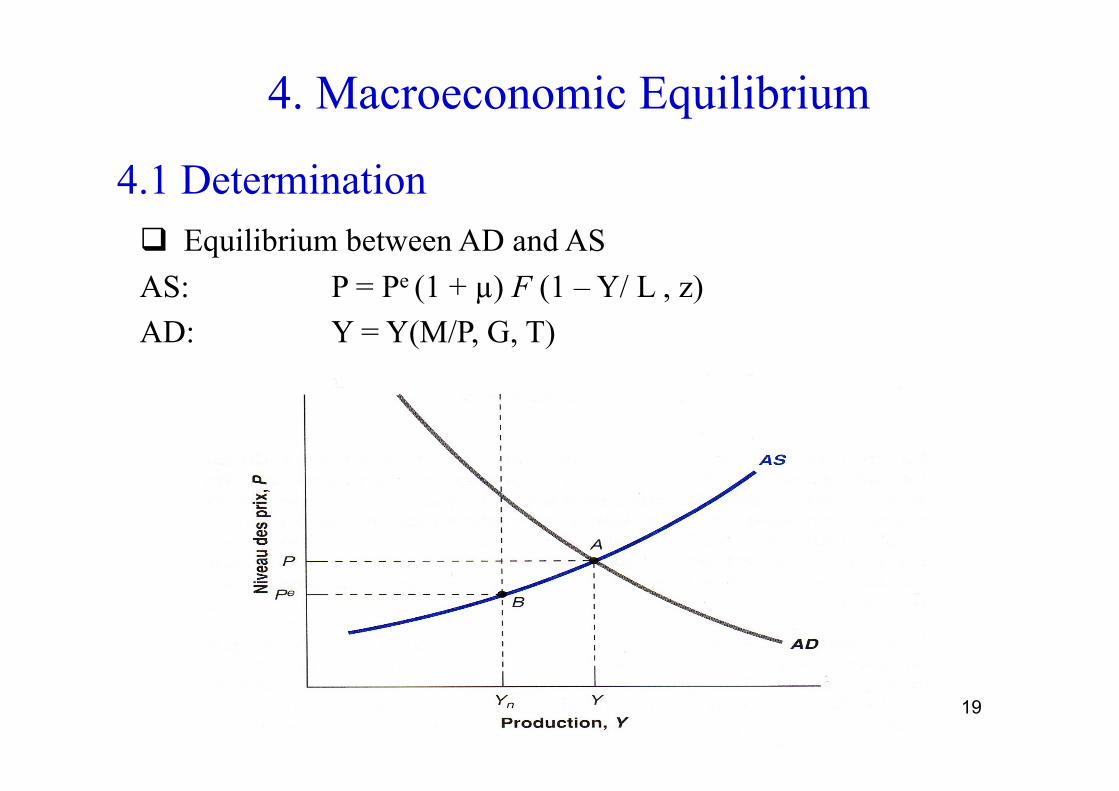

4. Macroeconomic Equilibrium

4.1 Determination Equilibrium between AD and AS AS: P = Pe (1 + µ) F (1 – Y/ L , z) AD: Y = Y(M/P, G, T)

20

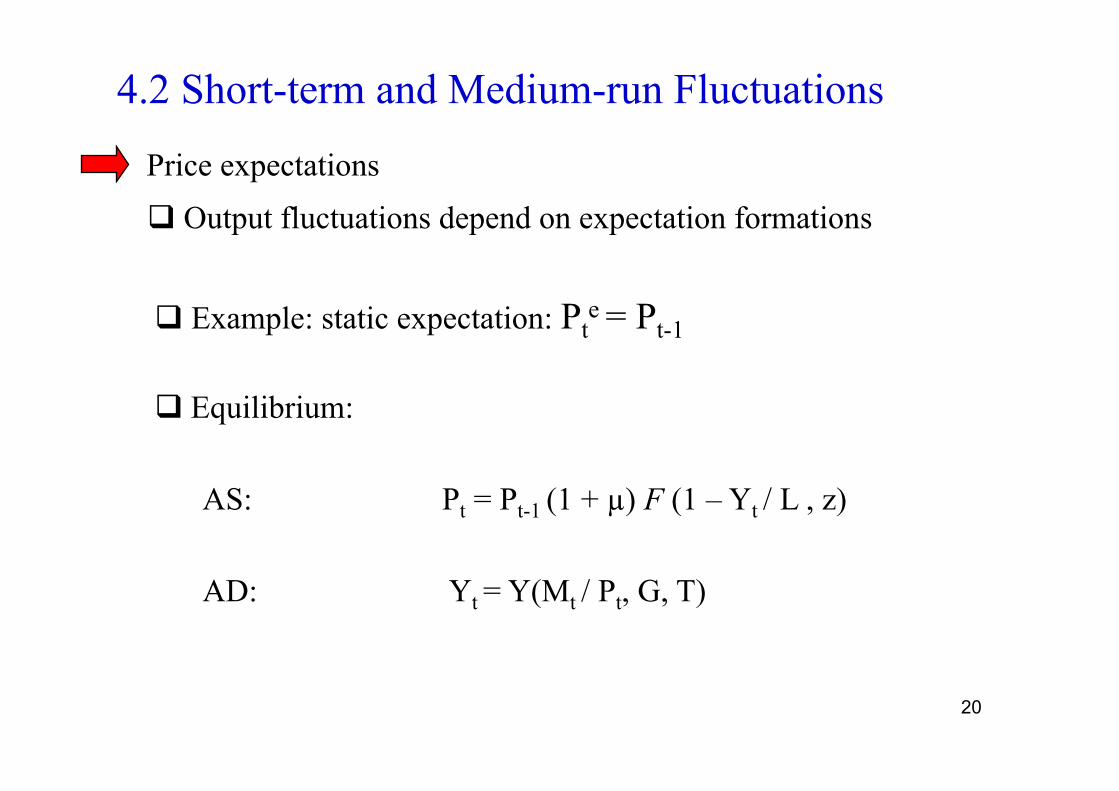

4.2 Short-term and Medium-run Fluctuations

Equilibrium:

AS: Pt = Pt-1 (1 + µ) F (1 – Yt / L , z)

AD: Yt = Y(Mt / Pt, G, T)

Price expectations

Output fluctuations depend on expectation formations

Example: static expectation: Pte = Pt-1

21

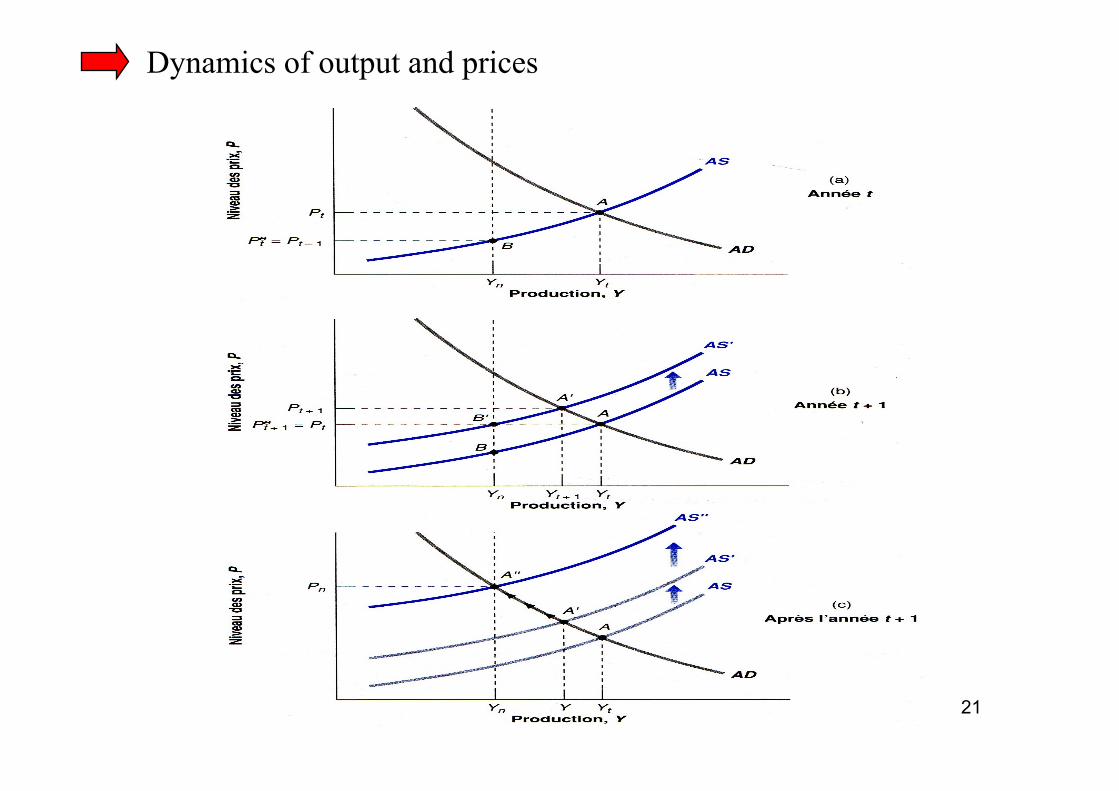

Dynamics of output and prices

22

In the short run, output can be higher or lower than potential output

But in the mid-term, output converges to its equilibrium level following adjustments of expectations and prices

Speed of the adjustment process depends on price and wage flexibility and on expectation formations

23

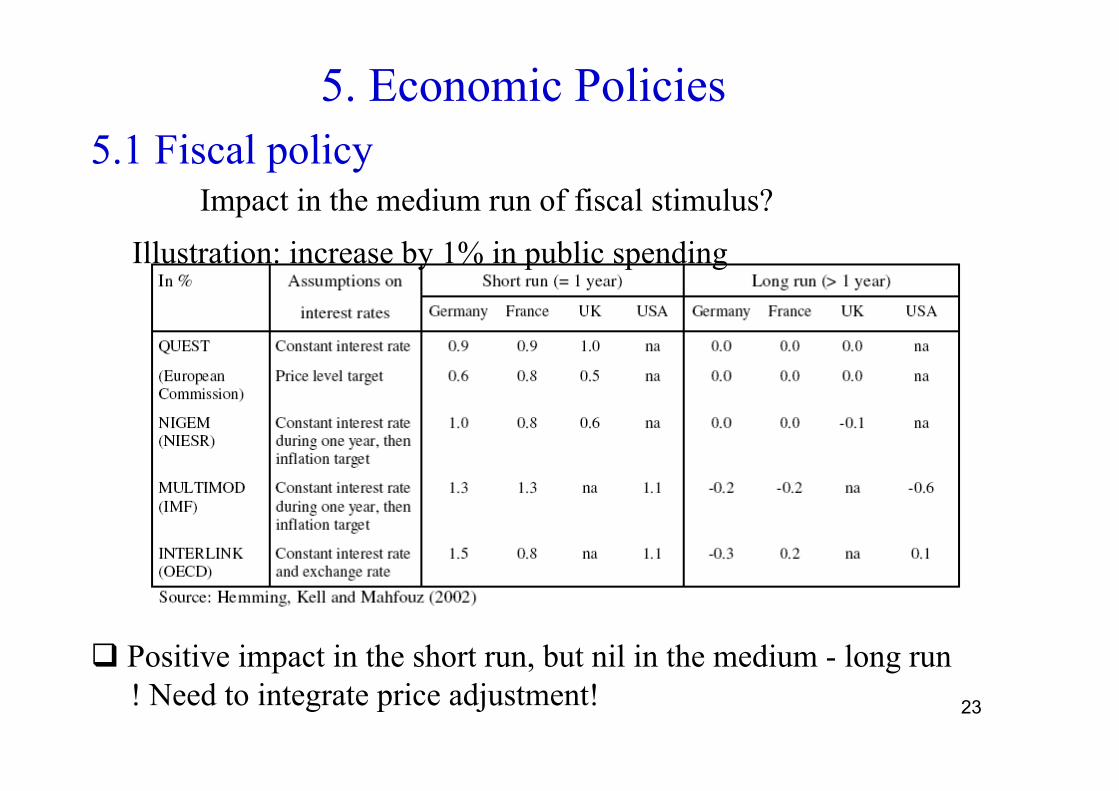

5. Economic Policies 5.1 Fiscal policy

Impact in the medium run of fiscal stimulus?

Positive impact in the short run, but nil in the medium - long run ! Need to integrate price adjustment!

Illustration: increase by 1% in public spending

24

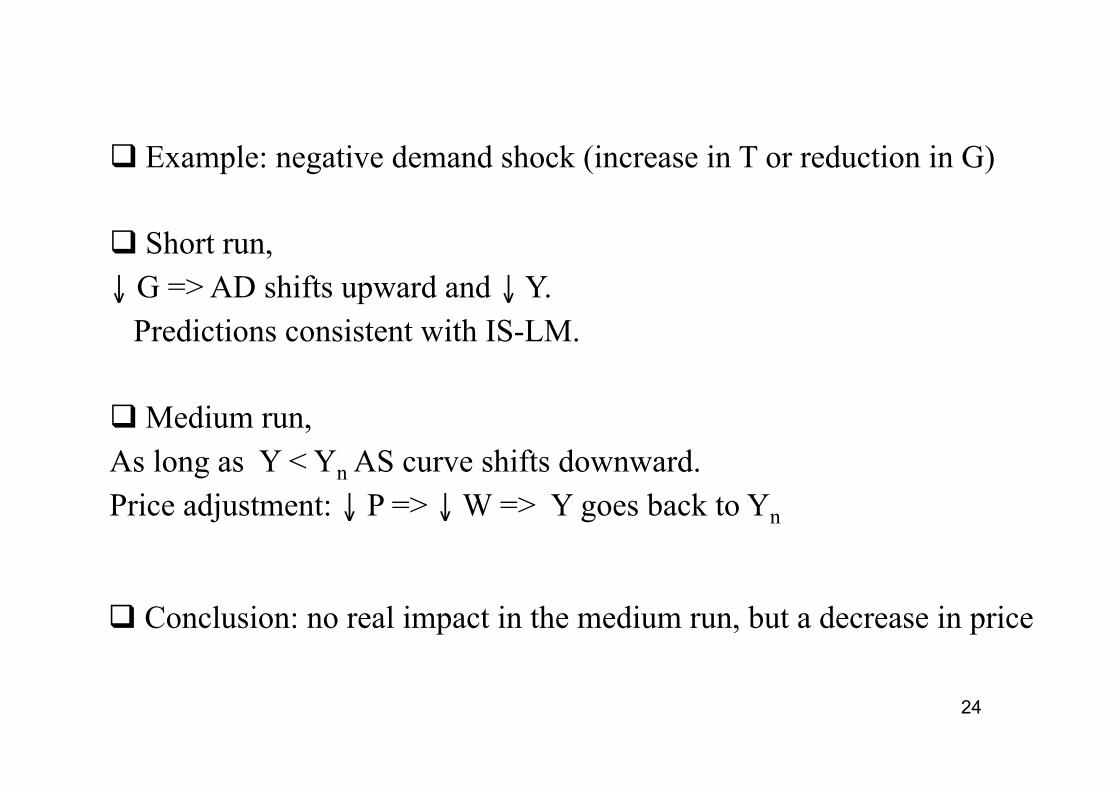

Example: negative demand shock (increase in T or reduction in G)

Short run, ↓ G => AD shifts upward and ↓ Y. Predictions consistent with IS-LM.

Medium run, As long as Y < Yn AS curve shifts downward. Price adjustment: ↓ P => ↓ W => Y goes back to Yn

Conclusion: no real impact in the medium run, but a decrease in price

25

26

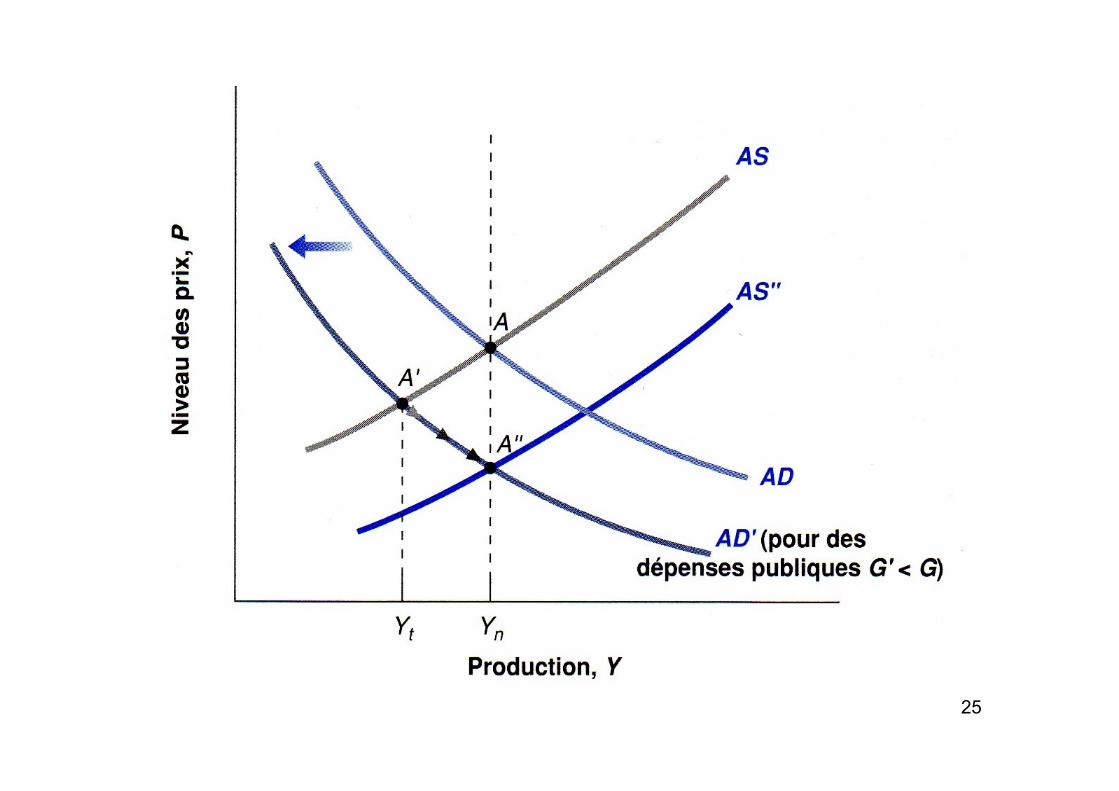

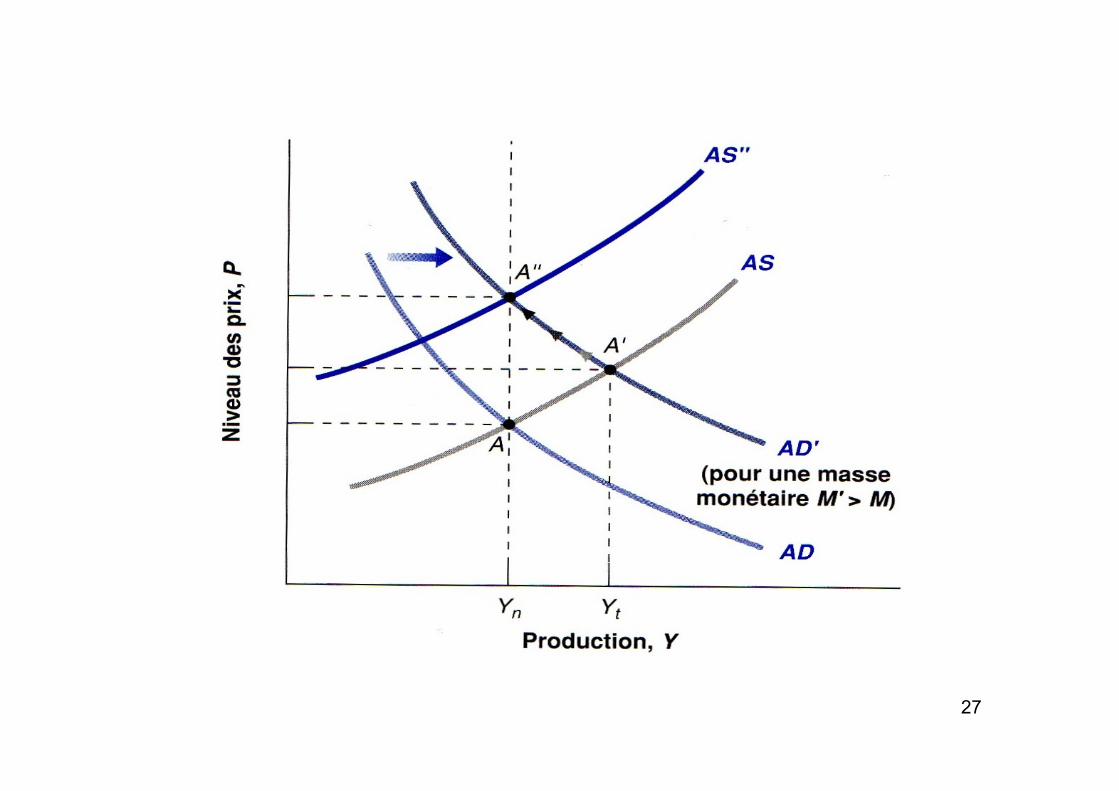

5.2 Monetary Policy

Assume production is at its equilibrium Y = Yn,,

Expansionary monetary policy: short-run impact ↑ M => ↑ AD => ↑ Y > Yn

Price adjustment in the medium run => ↑ P => ↑ W => AS shifts upward=> Y goes back to Yn

Conclusion: monetary policy is neutral in the medium run, price adjust in proportion to the increase in M

Estimates in the US • Peak in output after three quarters: + 1,8% of GDP, but vanishes after • 4 years latter, P increases by 1,5 % but Y has increased by 0,3% only

27

28

29

6. Phillips Curve

Questions

• Relations between inflation, unemployment an output

• Is there a trade-off between inflation and unemployment ?

• Credibility of monetary policy and Independance of Central Bank

30

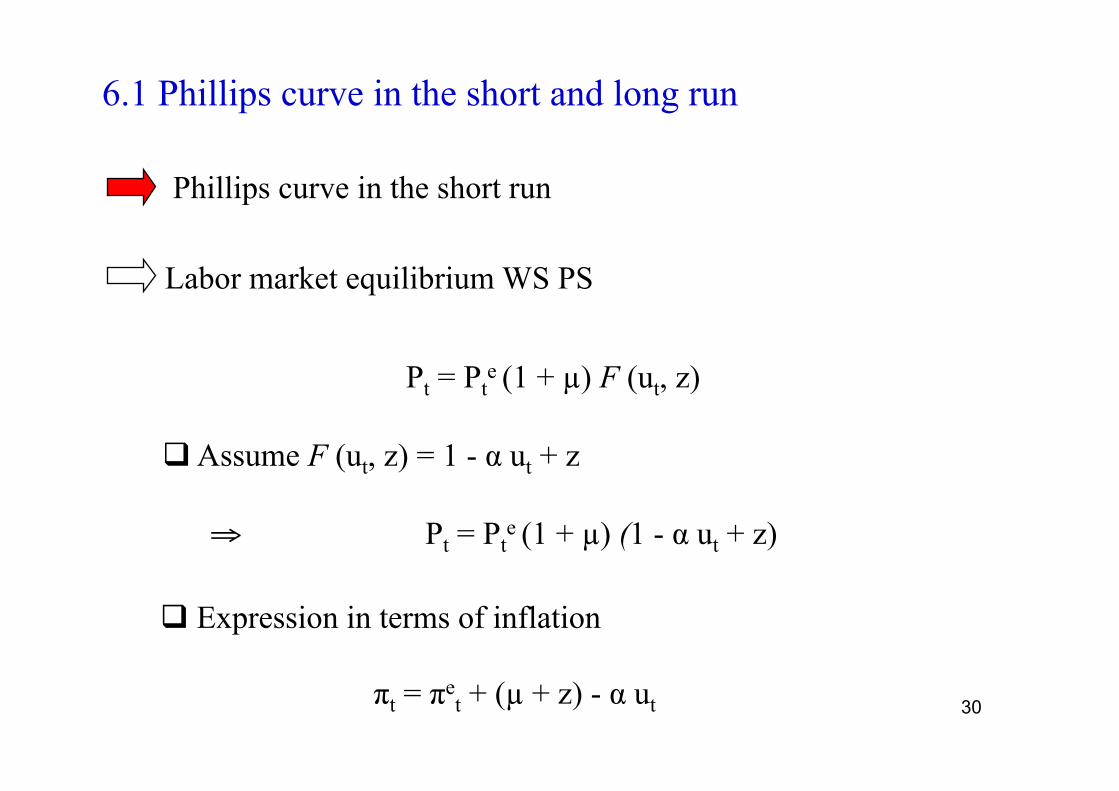

6.1 Phillips curve in the short and long run

Phillips curve in the short run

Pt = Pte (1 + µ) F (ut, z)

Labor market equilibrium WS PS

Assume F (ut, z) = 1 - α ut + z

⇒ Pt = Pte (1 + µ) (1 - α ut + z)

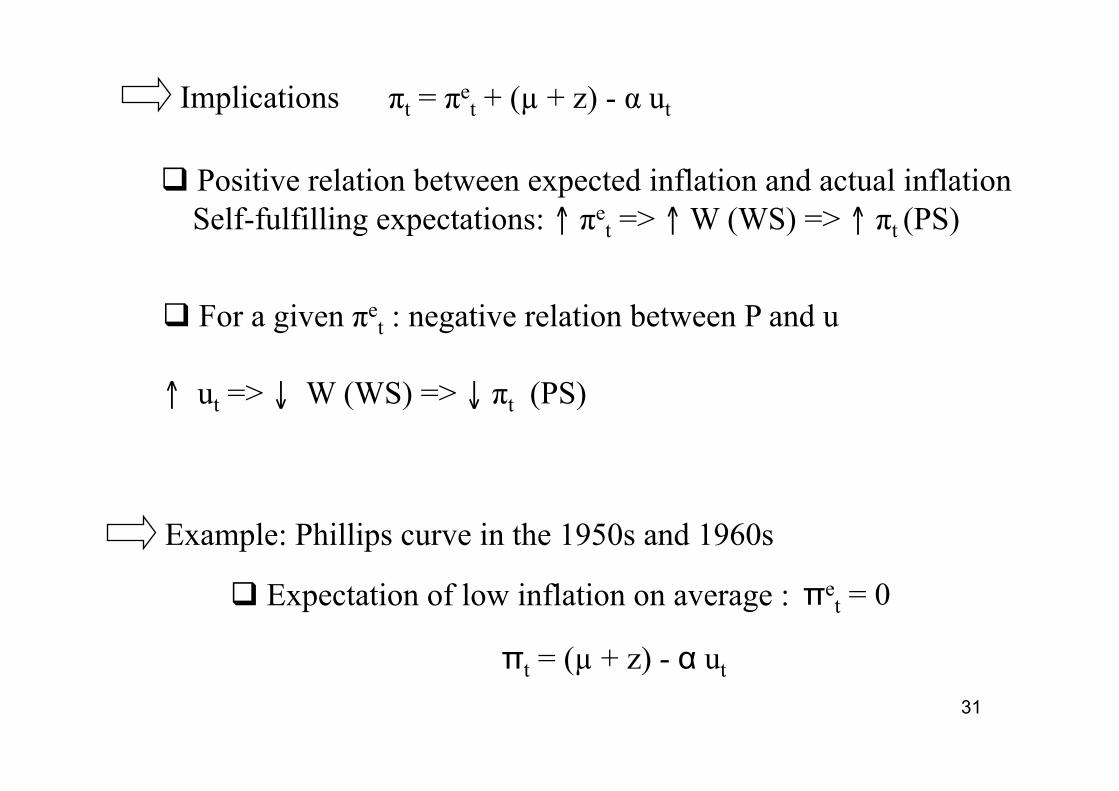

πt = πet + (µ + z) - α ut

Expression in terms of inflation

31

Implications

Positive relation between expected inflation and actual inflation Self-fulfilling expectations: ↑ πe

t => ↑ W (WS) => ↑ πt (PS)

πt = πet + (µ + z) - α ut

For a given πet : negative relation between P and u

↑ ut => ↓ W (WS) => ↓ πt (PS)

Example: Phillips curve in the 1950s and 1960s

Expectation of low inflation on average :

32

Trade off between inflation policy and unemployment

Phillips curve

0

(b) Phillips curve

Inflation

u 0

(a) AD-AS curves

P

AD

AD’

B

4

6

(Y= 8,000)

A

7

2

(Y= 7,500)

A

7,500

102

(u= 7%)

B

8,000

106

(u=4%)

AS in the SR

Y

33

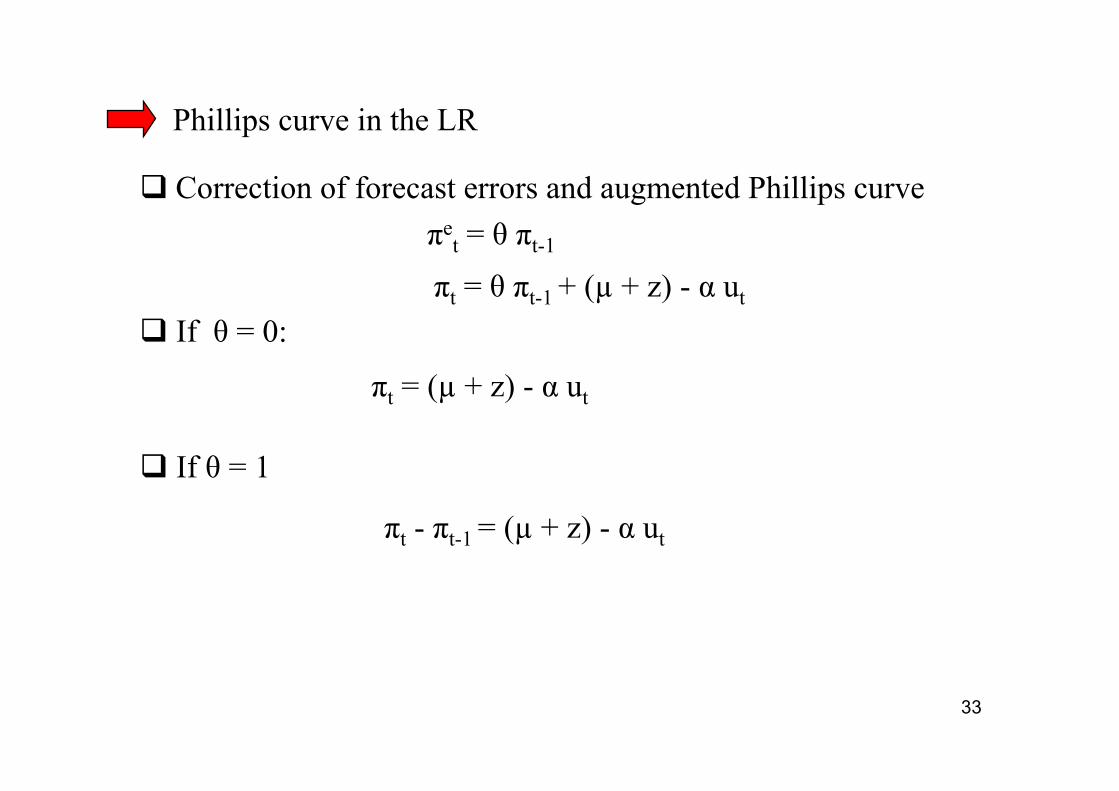

Phillips curve in the LR

Correction of forecast errors and augmented Phillips curve πe

t = θ πt-1

If θ = 1

πt = θ πt-1 + (µ + z) - α ut

If θ = 0:

πt = (µ + z) - α ut

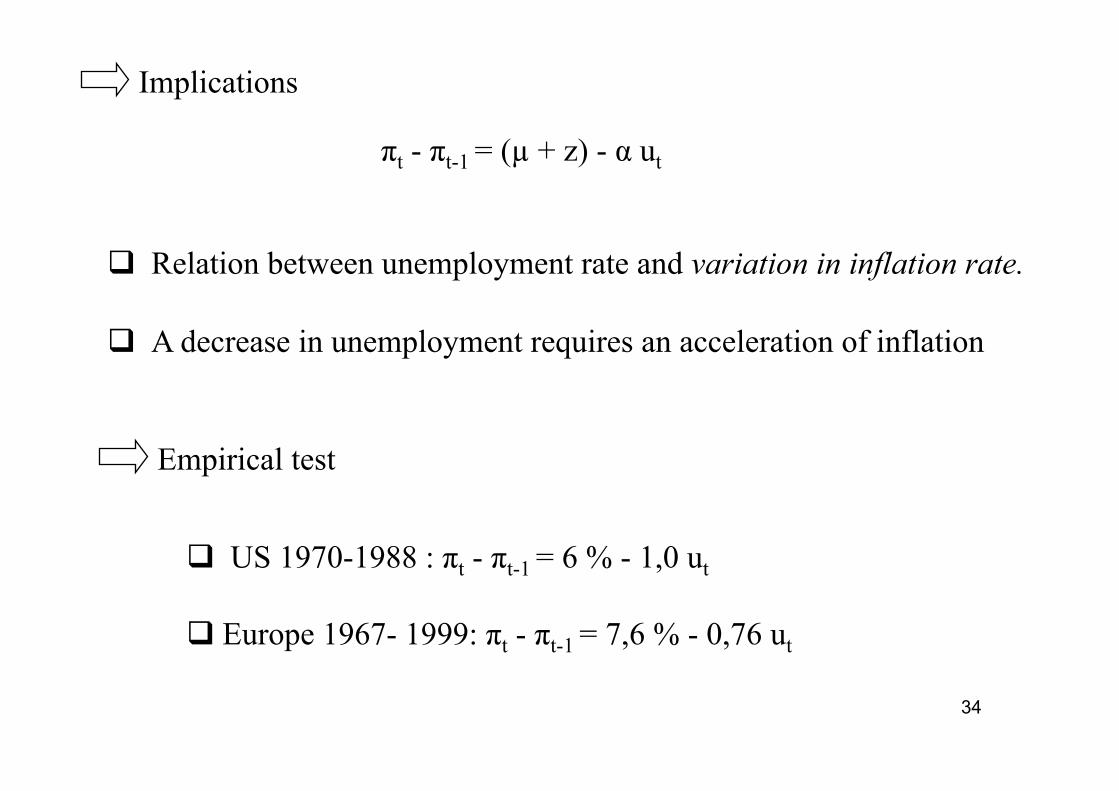

πt - πt-1 = (µ + z) - α ut

34

Relation between unemployment rate and variation in inflation rate.

A decrease in unemployment requires an acceleration of inflation

Implications

πt - πt-1 = (µ + z) - α ut

Empirical test

US 1970-1988 : πt - πt-1 = 6 % - 1,0 ut

Europe 1967- 1999: πt - πt-1 = 7,6 % - 0,76 ut

35

36

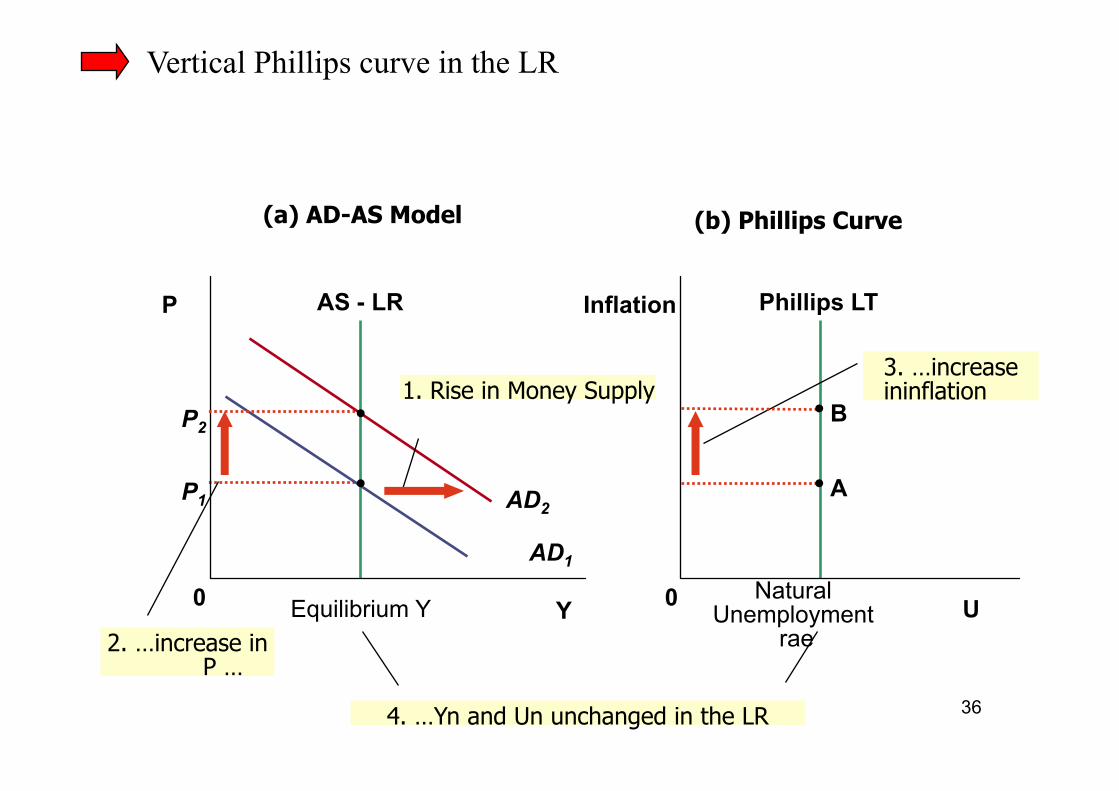

Vertical Phillips curve in the LR

Natural Unemployment

rae

Phillips LT

0

(b) Phillips Curve

Inflation

A

Equilibrium Y 0

P1

AD1

AS - LR

(a) AD-AS Model

P

4. …Yn and Un unchanged in the LR

P2

2. …increase in P …

Y U

1. Rise in Money Supply

AD2

B

3. …increase ininflation

37

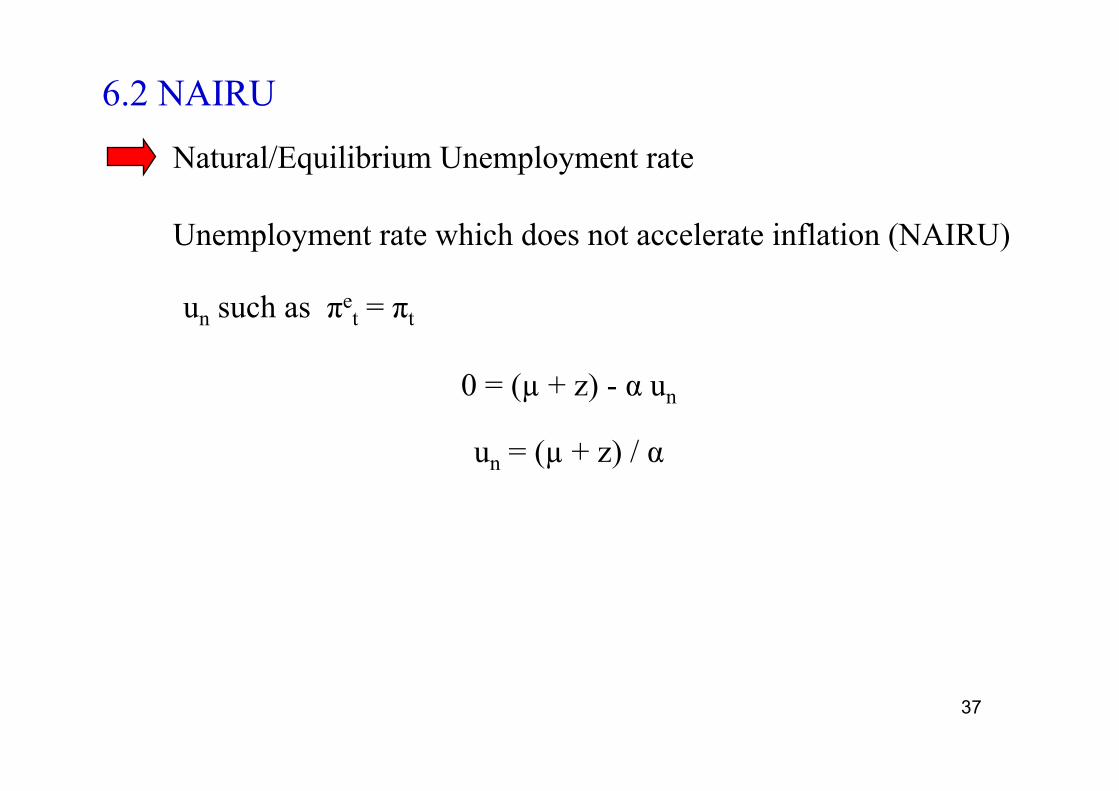

6.2 NAIRU

Natural/Equilibrium Unemployment rate

Unemployment rate which does not accelerate inflation (NAIRU)

un such as πet = πt

0 = (µ + z) - α un

un = (µ + z) / α

38

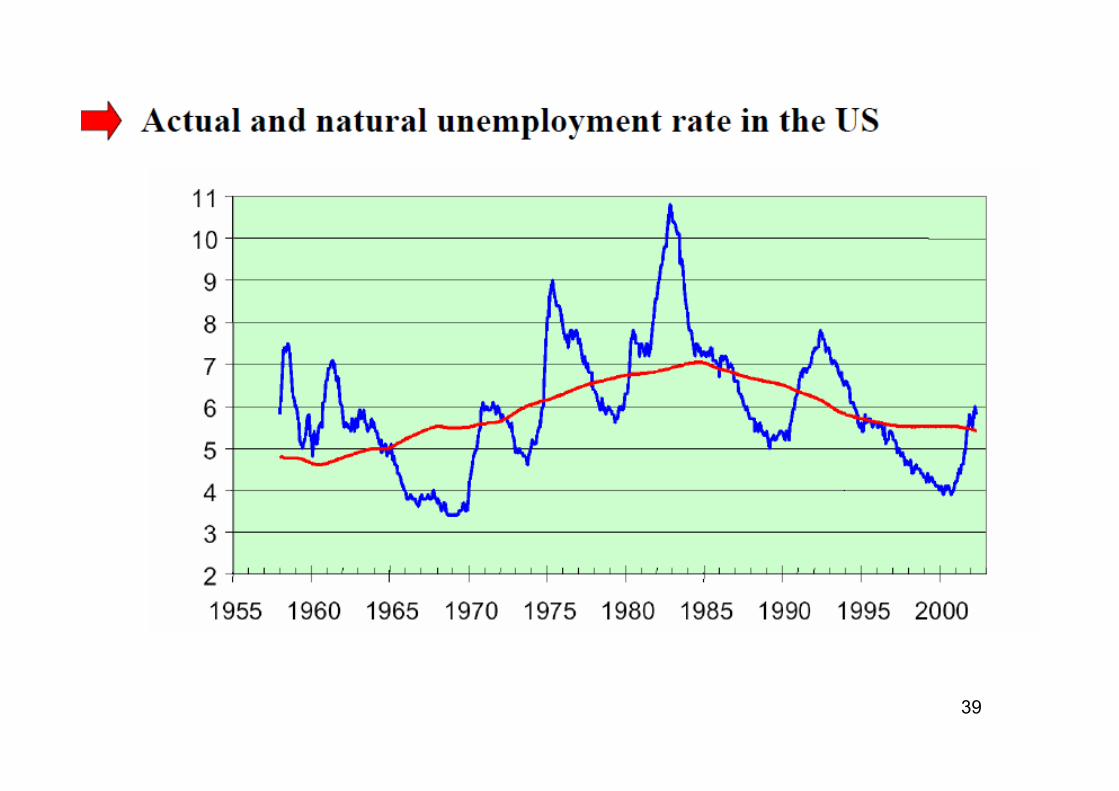

Augmented Phillips curve

NAIRU

⇒ Variation in inflation depends on unemployment gap

⇒ un NAIRU (Non-accelerating inflation rate Unemployment)

Phillips curve with natural unemployment rate

α un = µ + z =>

39

40

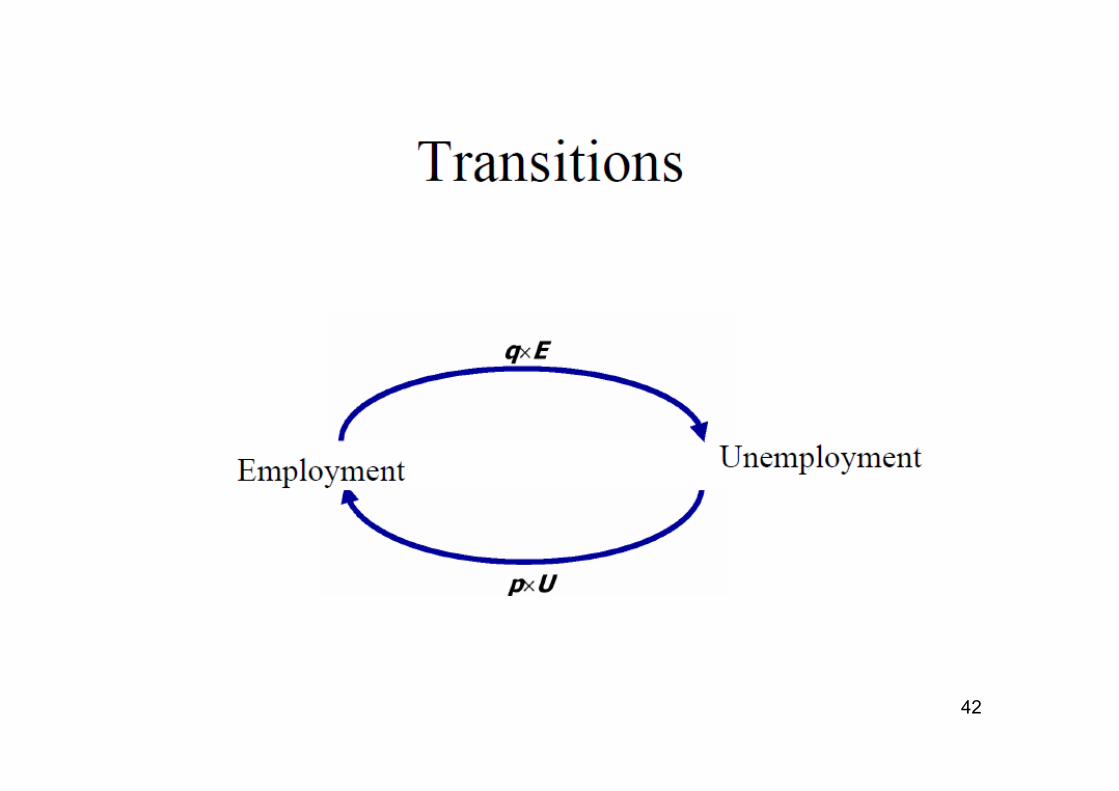

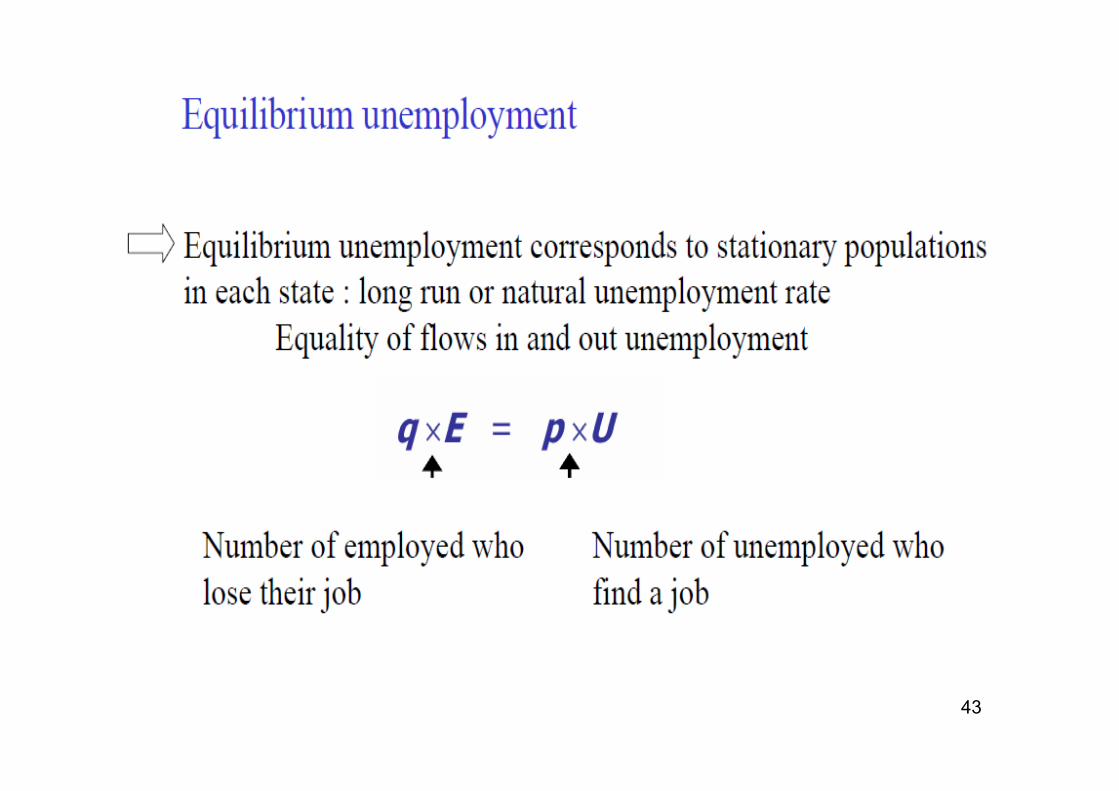

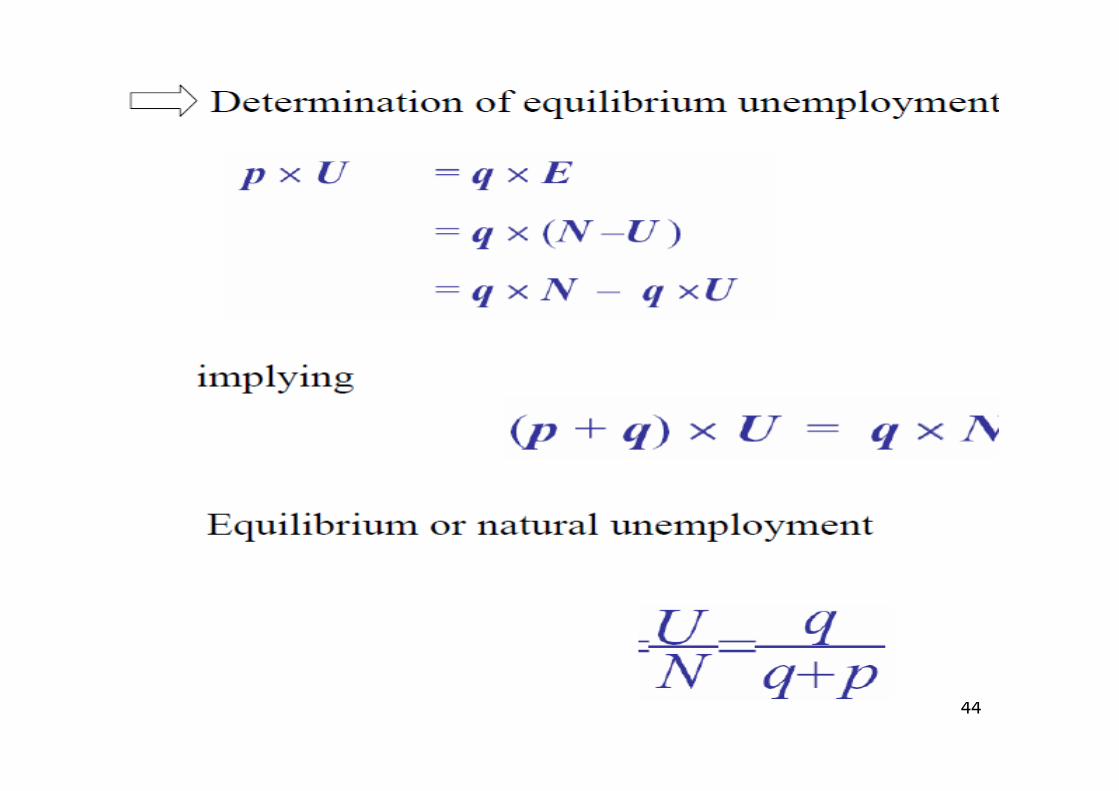

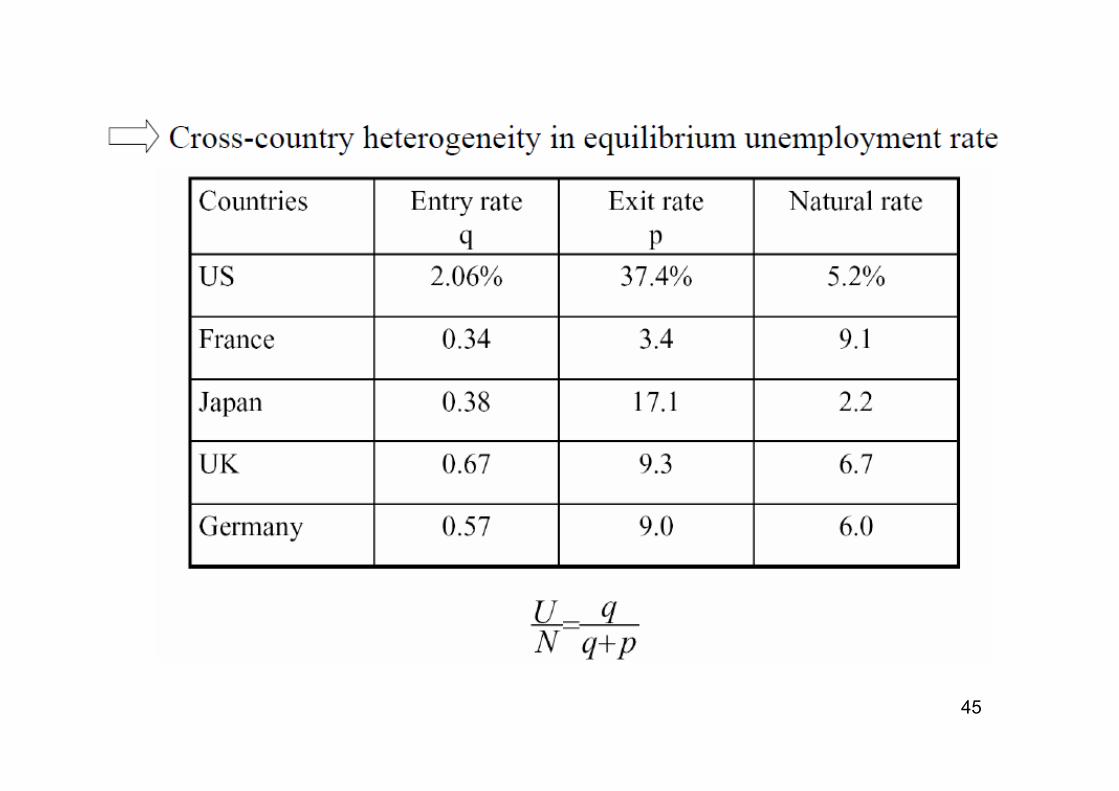

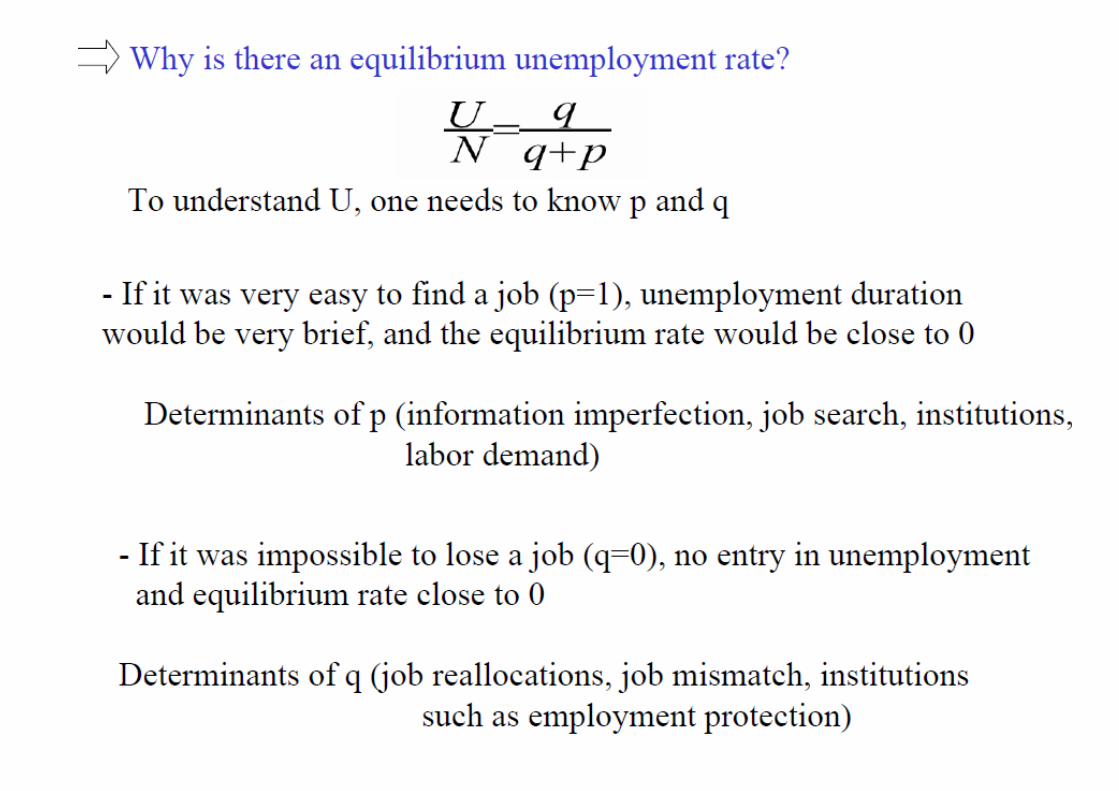

6.3 Why is there an equilibrium unemployment rate ? Case study with Matching frictions

41

42

43

44

45

46

47

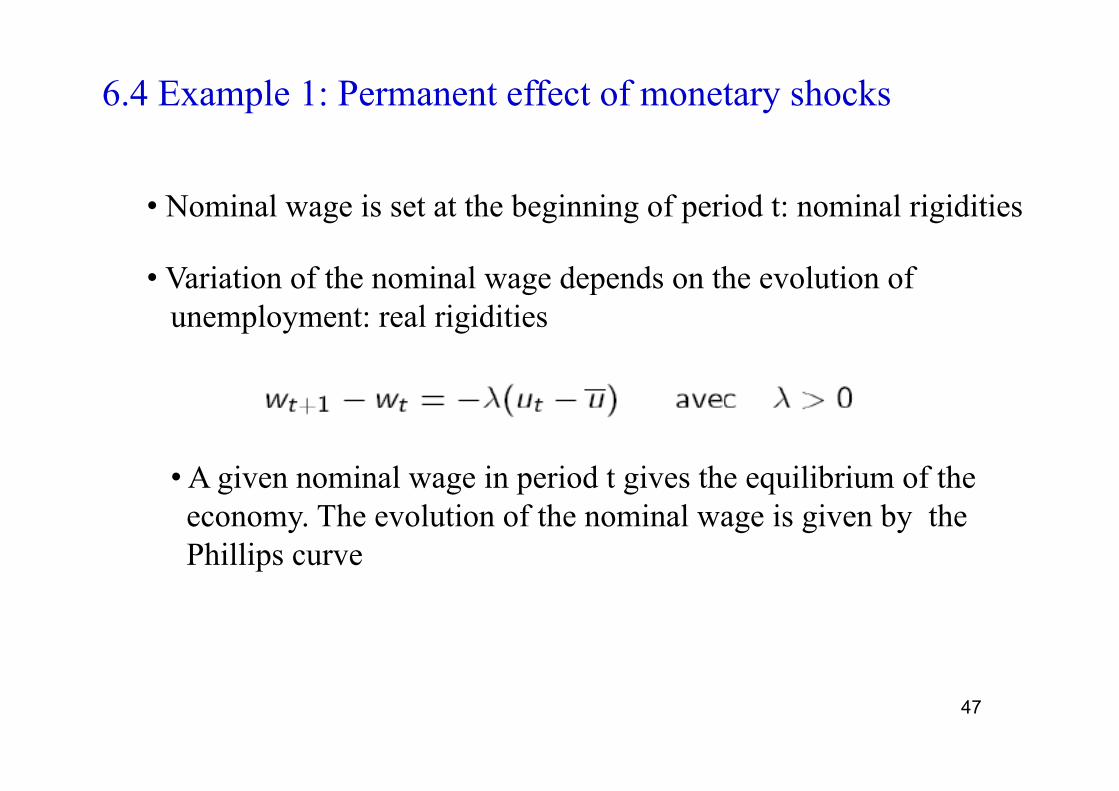

6.4 Example 1: Permanent effect of monetary shocks

• Nominal wage is set at the beginning of period t: nominal rigidities

• Variation of the nominal wage depends on the evolution of unemployment: real rigidities

• A given nominal wage in period t gives the equilibrium of the economy. The evolution of the nominal wage is given by the Phillips curve

48

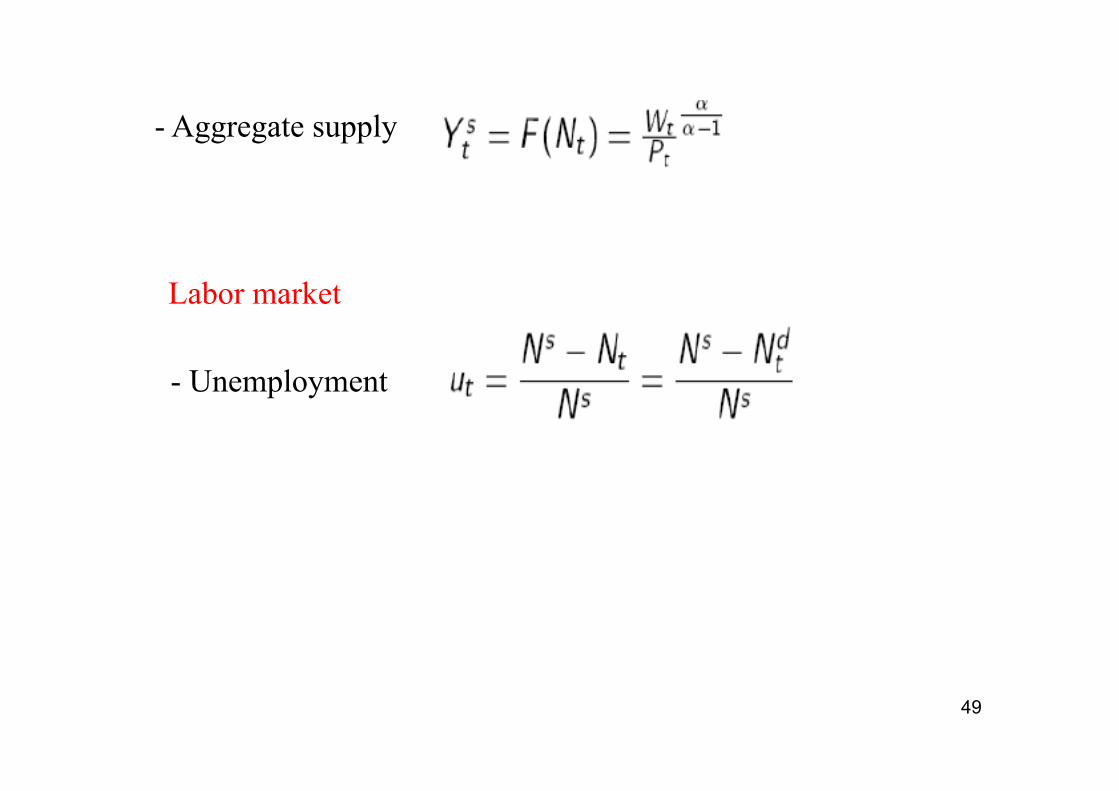

• Aggregate demand

• Aggregate supply

- Production

- Flexible prices Labor demand is given by the maximization of the profit

Equilibrium on the good market

49

- Aggregate supply

- Unemployment

Labor market

50

Macroeconomic equilibrium

Log linear representation

Find the equilibrium for a given period and determine the law of motion of the equilibrium

51

• Equilibrium price: equality between AD and AS

• Equilibrium output: Substitute equilibrium price in AD or AS

• Law of motion of output

52

• Law of motion of unemployment

- Using the definition of output

- From the equilibrium price equation and the definition of inflation

53

• Equilibrium unemployment

Stationary solution such that

Equilibrium unemployment given by

• Implications:

- Monetary policy can have a long run impact on unemployment

- Impact depends on the adjustment of wages (impact nil if immediate adjustment of wages to unemployment)

54

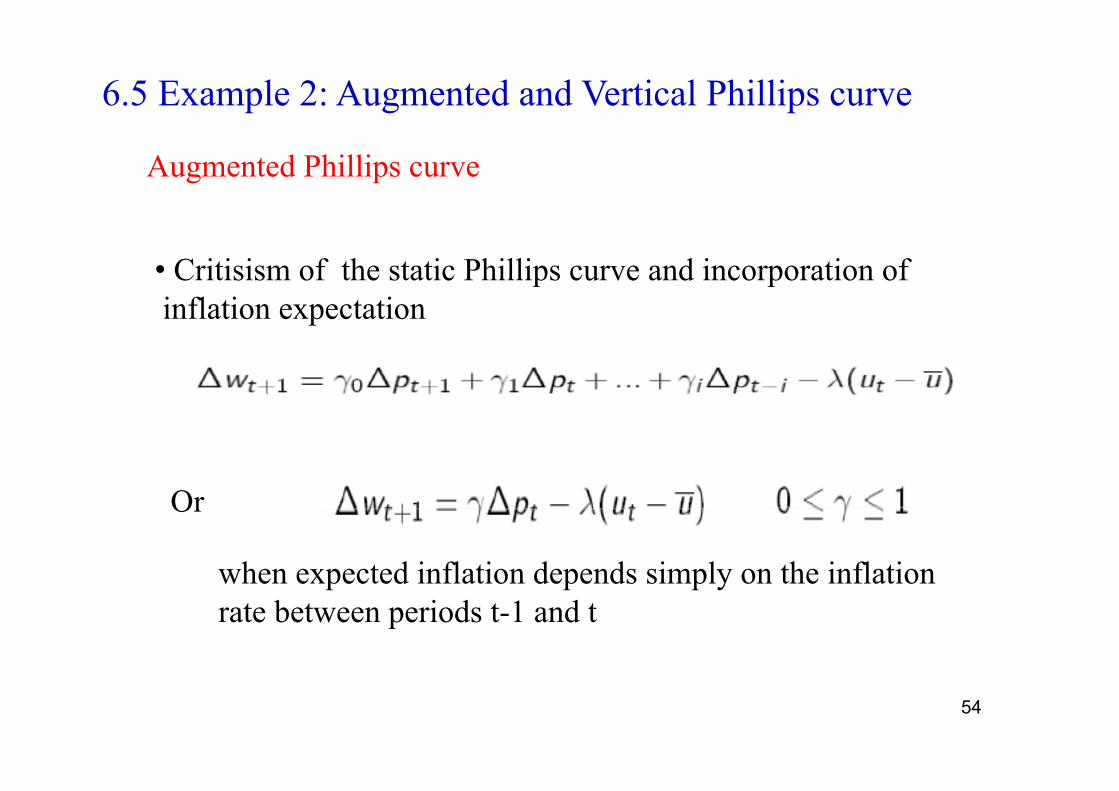

6.5 Example 2: Augmented and Vertical Phillips curve

Augmented Phillips curve

• Critisism of the static Phillips curve and incorporation of inflation expectation

Or

when expected inflation depends simply on the inflation rate between periods t-1 and t

55

• Nominal rigidities: wage growth depends on past inflation and not on the current one

• : measure of the indexation of wages on prices in the long run

56

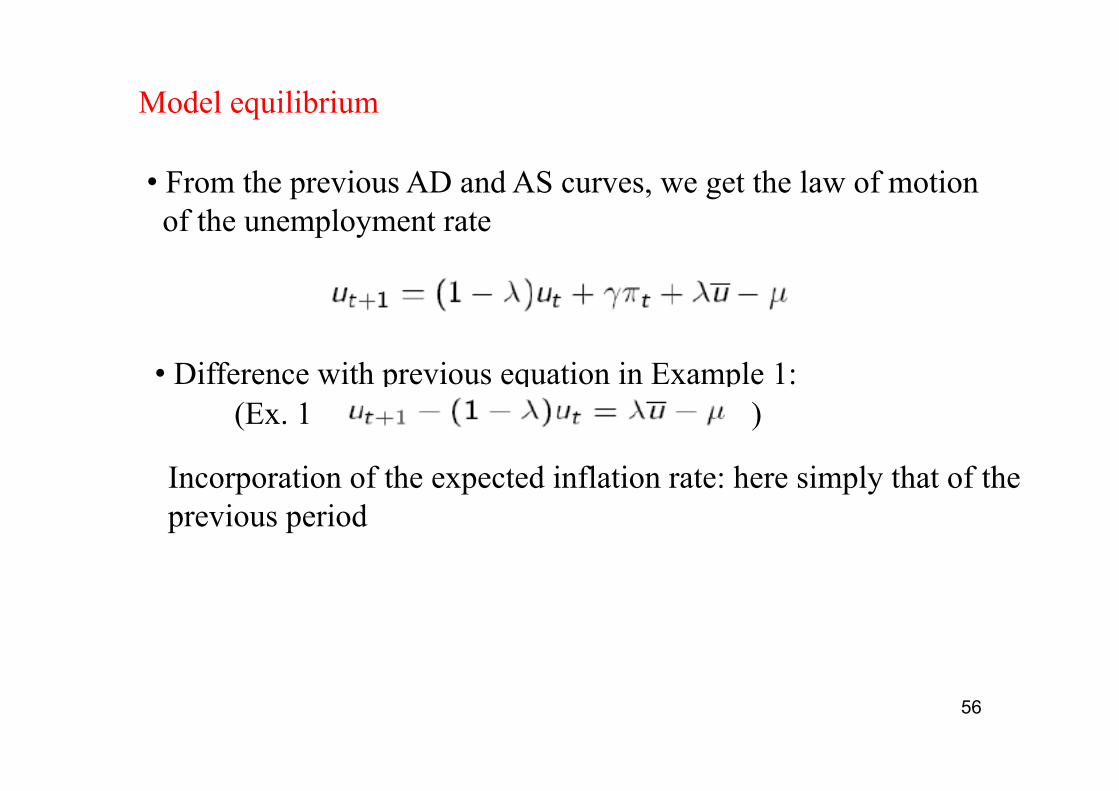

Model equilibrium

• From the previous AD and AS curves, we get the law of motion of the unemployment rate

• Difference with previous equation in Example 1: (Ex. 1 )

Incorporation of the expected inflation rate: here simply that of the previous period

57

• From the previous structure of the model in Ex. 1, and taking into account the new equation for wage formation:

Law of motion of the inflation rate

58

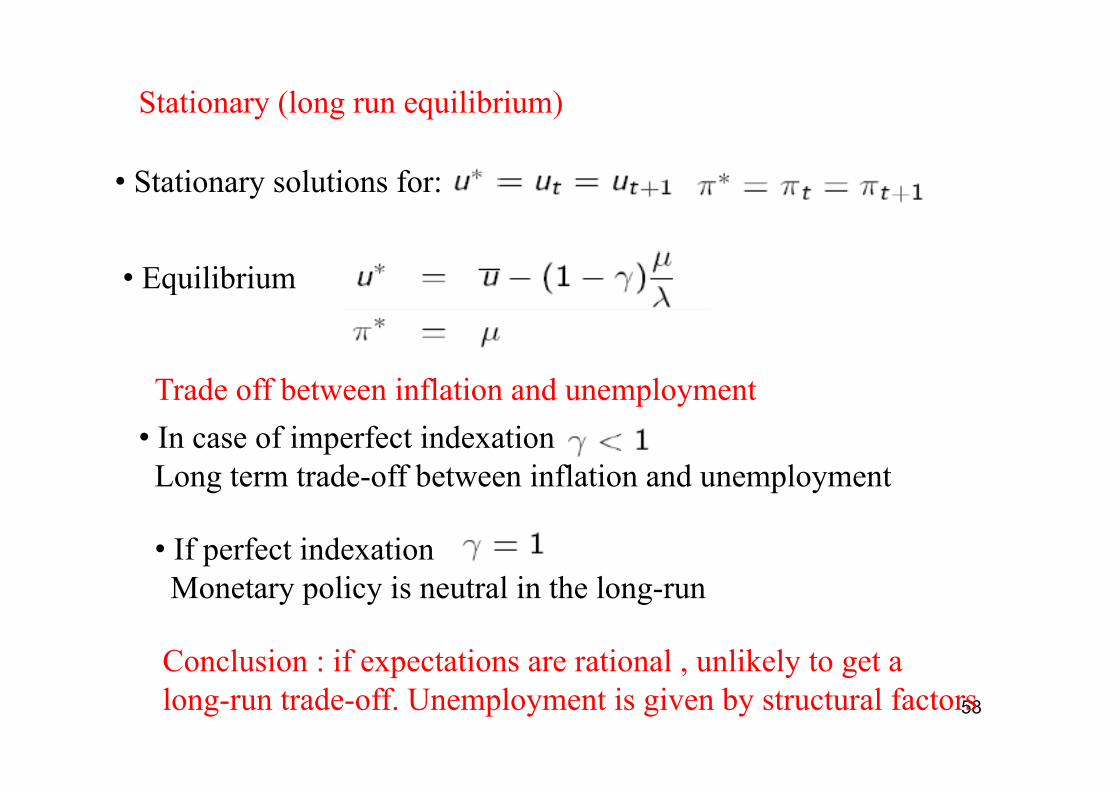

Stationary (long run equilibrium)

• Stationary solutions for: :

• Equilibrium

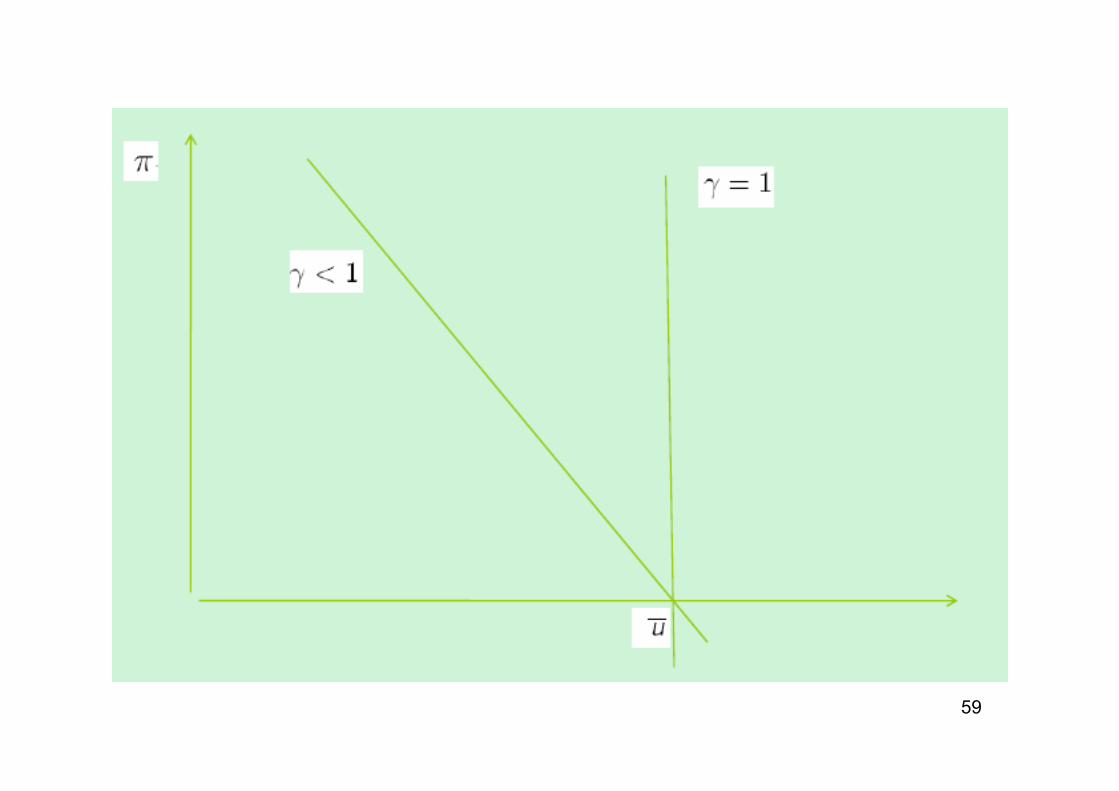

• In case of imperfect indexation Long term trade-off between inflation and unemployment

• If perfect indexation Monetary policy is neutral in the long-run

Trade off between inflation and unemployment

Conclusion : if expectations are rational , unlikely to get a long-run trade-off. Unemployment is given by structural factors

59

60

7. Credibility of Economic Policies

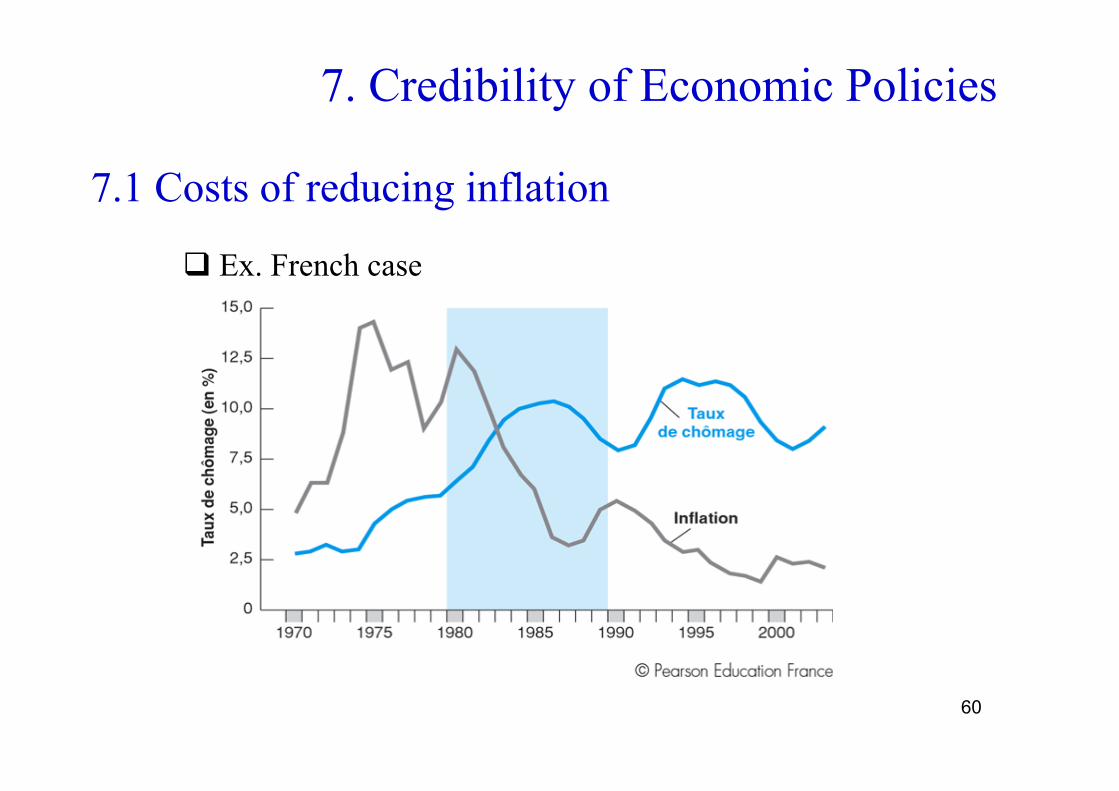

7.1 Costs of reducing inflation

Ex. French case

61

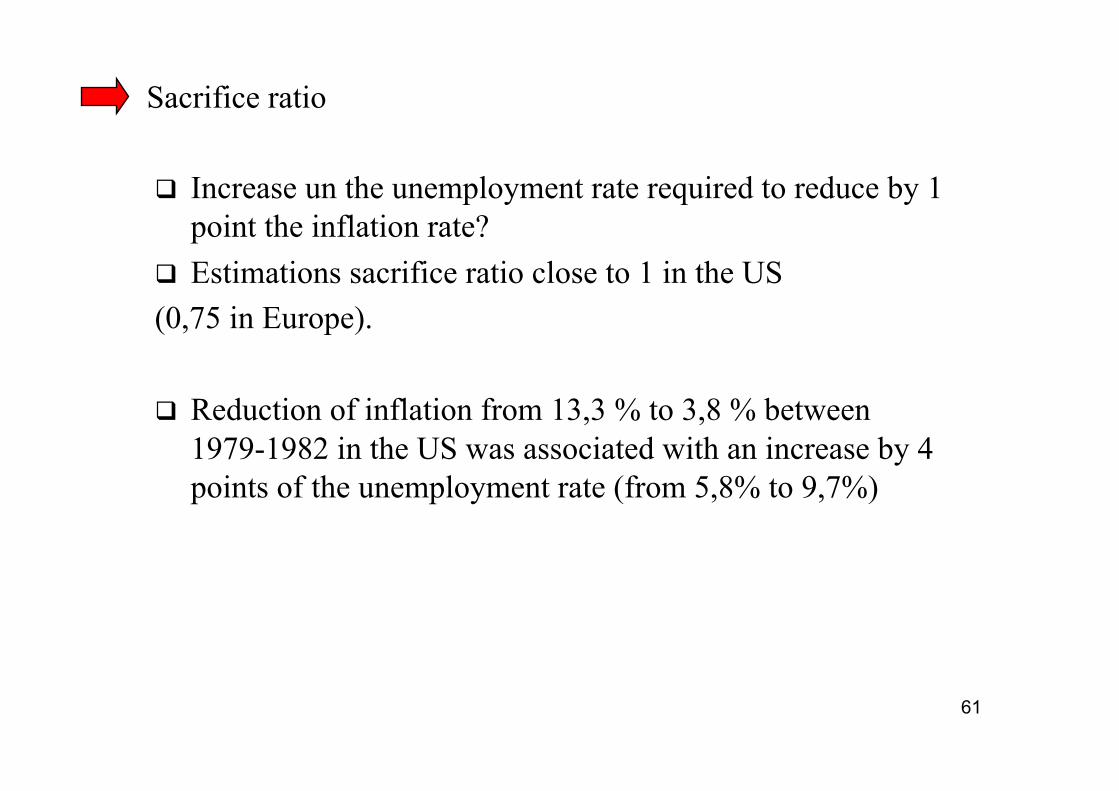

Increase un the unemployment rate required to reduce by 1 point the inflation rate?

Estimations sacrifice ratio close to 1 in the US (0,75 in Europe).

Reduction of inflation from 13,3 % to 3,8 % between 1979-1982 in the US was associated with an increase by 4 points of the unemployment rate (from 5,8% to 9,7%)

Sacrifice ratio

62

Anticipations and the Lucas ’ critic

7.2 Anticipations, Credibility and Central Bank independence

The sacrifice ratio could be lower if the monetary authorities were credible in their willingness to reduce inflation

Problem of credibility and up-ward inflation bias

63

Barro-Gordon solution: independence of Central Bank

64

Evolution index of Central Bank Independence

CONCLUSION: Financial crisis and Monetary Policy, Should we rethink the optimal monetary policy (see text Blanchard et al. (2010))