Embed Size (px)

Citation preview

EIA’s Natural Gas Outlook Through 2025

Howard GruenspechtDeputy Administrator

Energy Information Administration([email protected])

forThe Fertilizer InstituteOutlook Conference

October 26, 2004Annapolis, MD

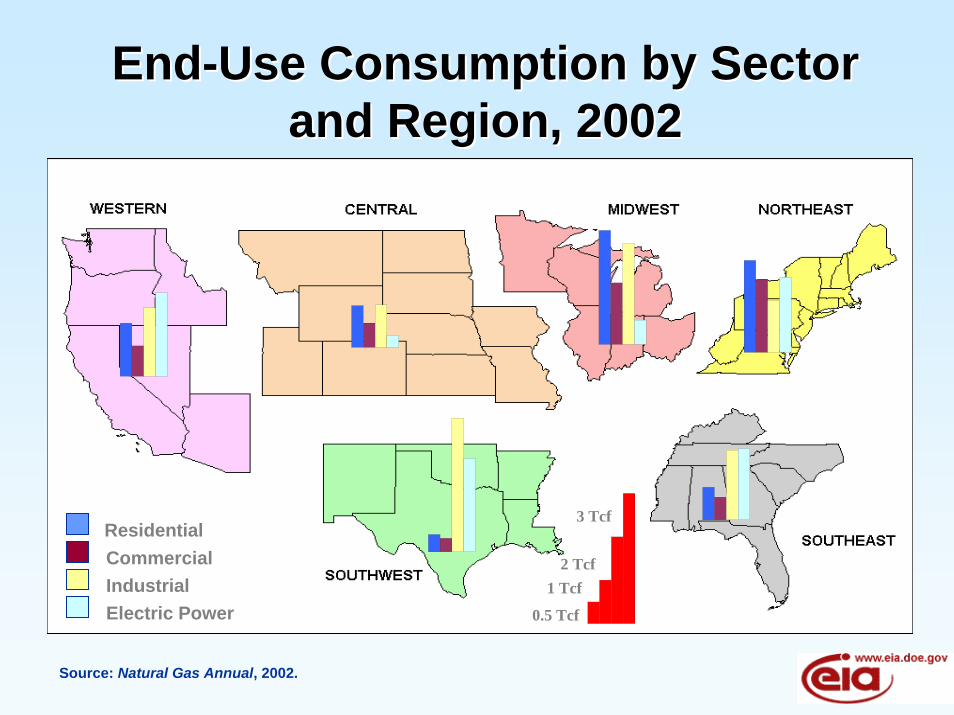

EndEnd--Use Consumption by Sector Use Consumption by Sector and Region, 2002and Region, 2002

Residential

Electric PowerIndustrialCommercial

0.5 Tcf

1 Tcf2 Tcf

3 Tcf

Source: Natural Gas Annual, 2002.

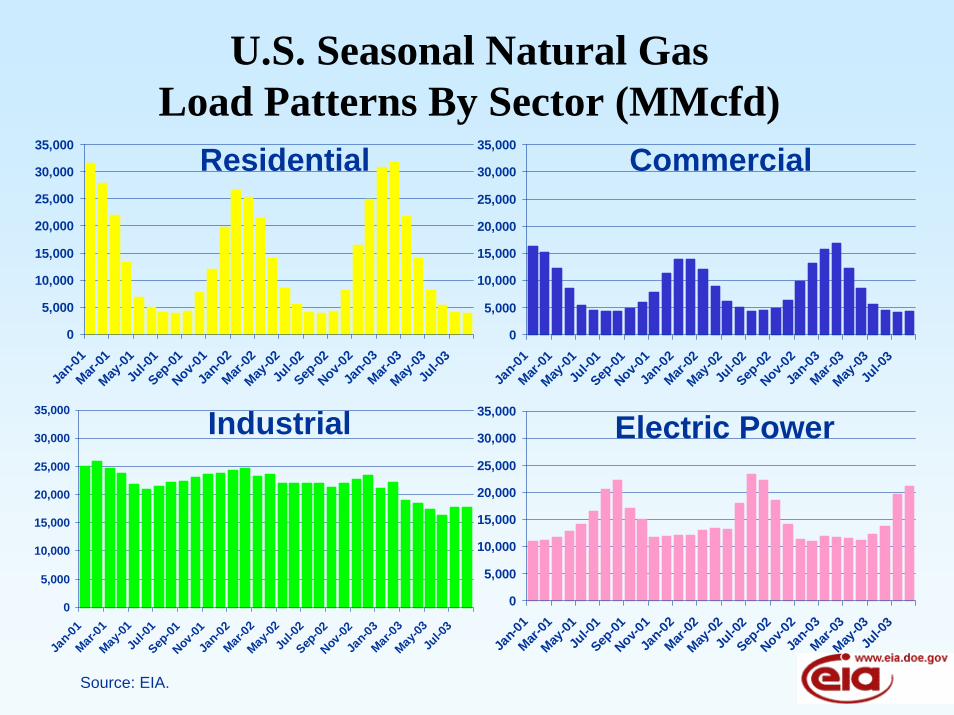

U.S. Seasonal Natural Gas Load Patterns By Sector (MMcfd)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Jan-0

1Mar-

01May

-01Ju

l-01

Sep-01

Nov-01

Jan-0

2Mar-

02May

-02Ju

l-02

Sep-02

Nov-02

Jan-0

3Mar-

03May

-03Ju

l-03

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Jan-0

1Mar-

01May

-01Ju

l-01

Sep-01

Nov-01

Jan-0

2Mar-

02May

-02Ju

l-02

Sep-02

Nov-02

Jan-0

3Mar-

03May

-03Ju

l-03

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Jan-01

Mar-01

May-01

Jul-0

1Sep

-01Nov

-01Ja

n-02

Mar-02

May-02

Jul-0

2Sep

-02Nov

-02Ja

n-03

Mar-03

May-03

Jul-0

3

Source: EIA.

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Jan-0

1Mar-

01May

-01Ju

l-01

Sep-01

Nov-01

Jan-0

2Mar-

02May

-02Ju

l-02

Sep-02

Nov-02

Jan-0

3Mar-

03May

-03Ju

l-03

Residential

Industrial

Commercial

Electric Power

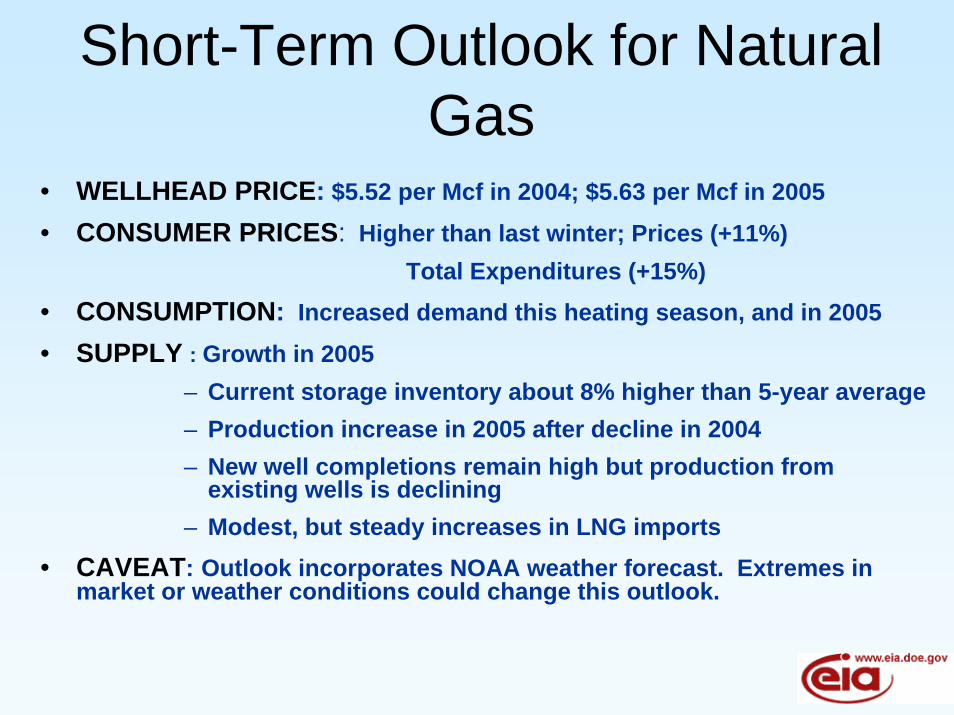

Short-Term Outlook for Natural Gas

• WELLHEAD PRICE: $5.52 per Mcf in 2004; $5.63 per Mcf in 2005

• CONSUMER PRICES: Higher than last winter; Prices (+11%)Total Expenditures (+15%)

• CONSUMPTION: Increased demand this heating season, and in 2005

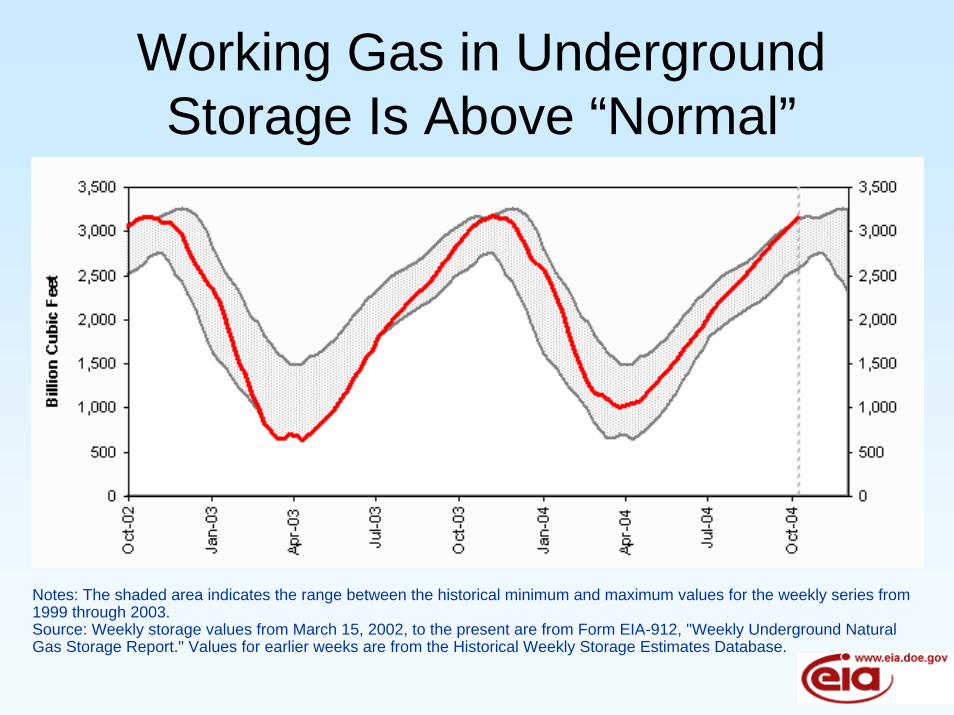

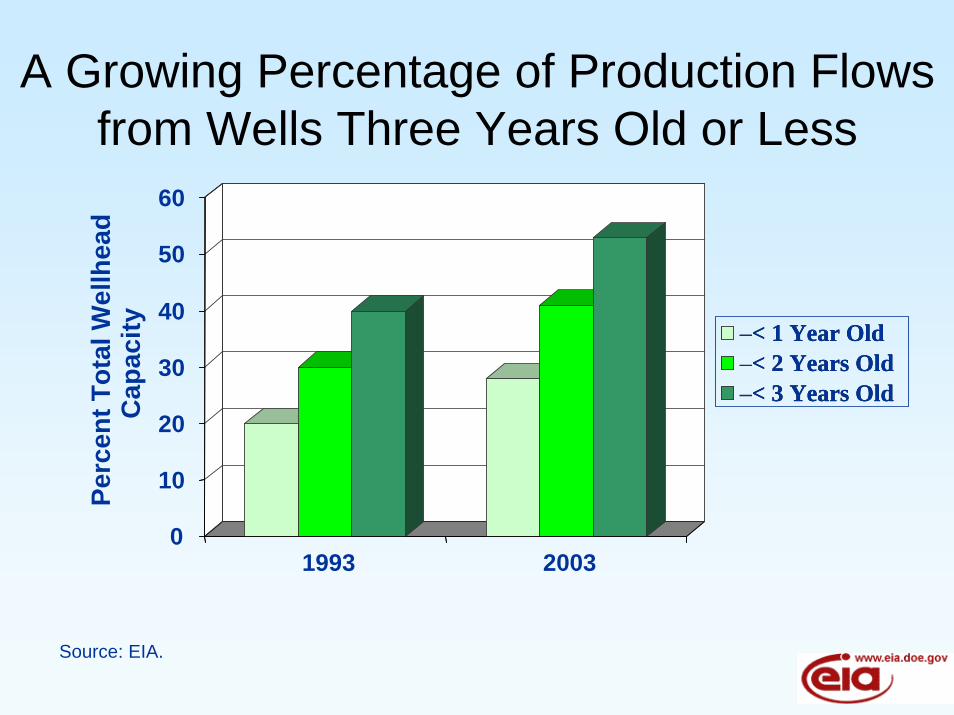

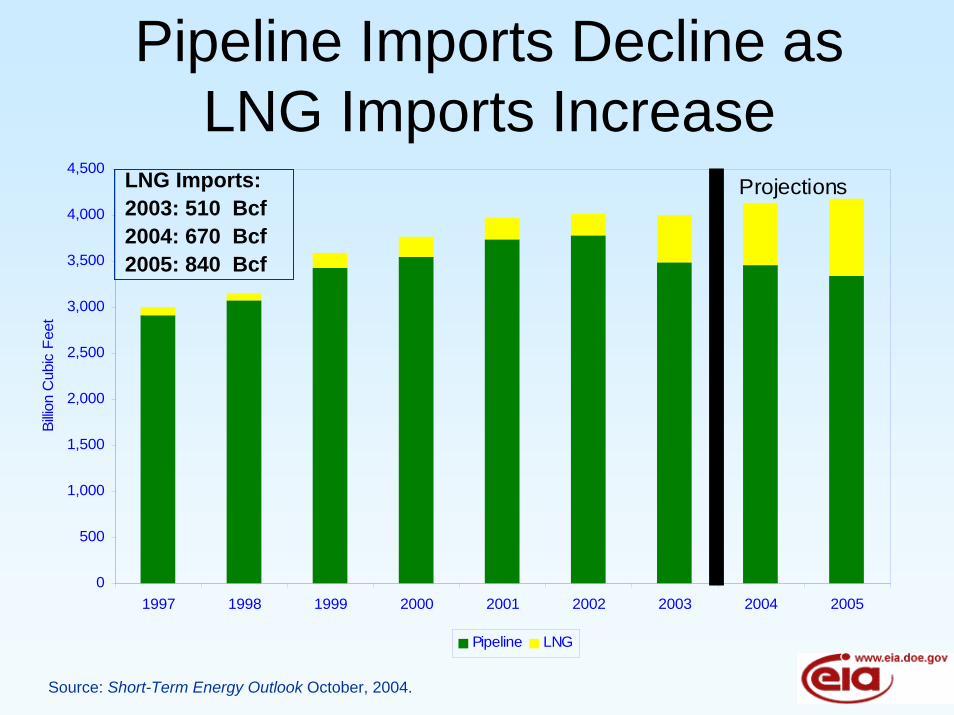

• SUPPLY : Growth in 2005– Current storage inventory about 8% higher than 5-year average– Production increase in 2005 after decline in 2004– New well completions remain high but production from

existing wells is declining– Modest, but steady increases in LNG imports

• CAVEAT: Outlook incorporates NOAA weather forecast. Extremes in market or weather conditions could change this outlook.

0.0

2.0

4.0

6.0

8.0

10.0

12.0Ja

n-99

May

-99

Sep

-99

Jan-

00

May

-00

Sep

-00

Jan-

01

May

-01

Sep

-01

Jan-

02

May

-02

Sep

-02

Jan-

03

May

-03

Sep

-03

Jan-

04

May

-04

Sep

-04

Jan-

05

May

-05

Sep

-05

Monthly

Dol

lars

per T

hous

and

Cub

ic F

eet

Projections

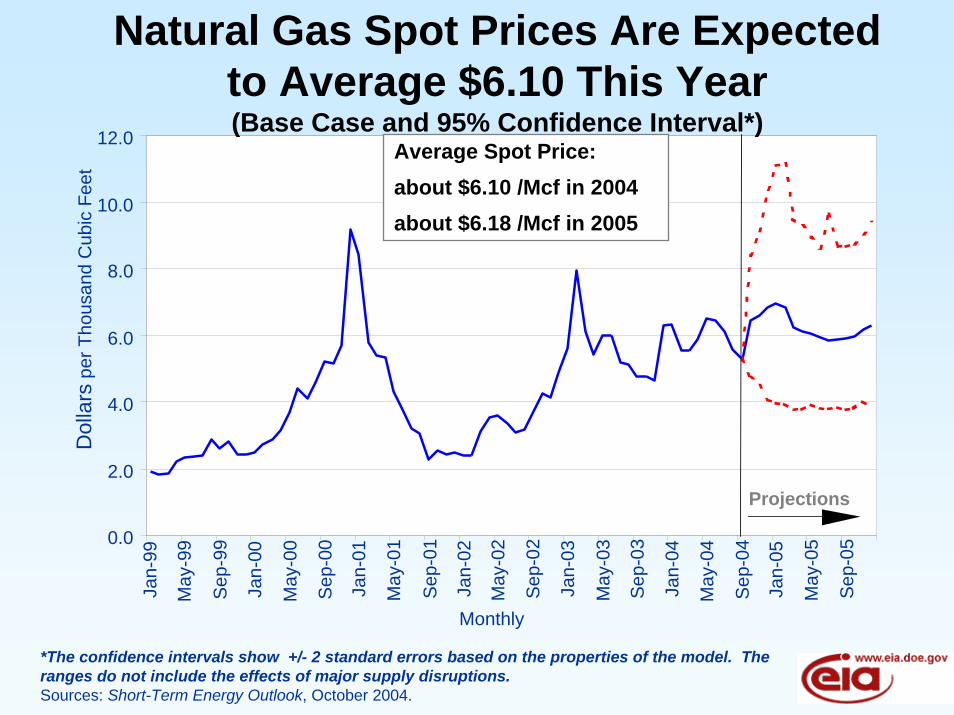

Natural Gas Spot Prices Are Expected to Average $6.10 This Year(Base Case and 95% Confidence Interval*)

Average Spot Price:about $6.10 /Mcf in 2004about $6.18 /Mcf in 2005

*The confidence intervals show +/- 2 standard errors based on the properties of the model. The ranges do not include the effects of major supply disruptions.Sources: Short-Term Energy Outlook, October 2004.

$0

$2

$4

$6

$8

$10

$12

$14

$16

Jan-96

Jan-97

Jan-98

Jan-99

Jan-00

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

Dol

lars

Per

Mcf

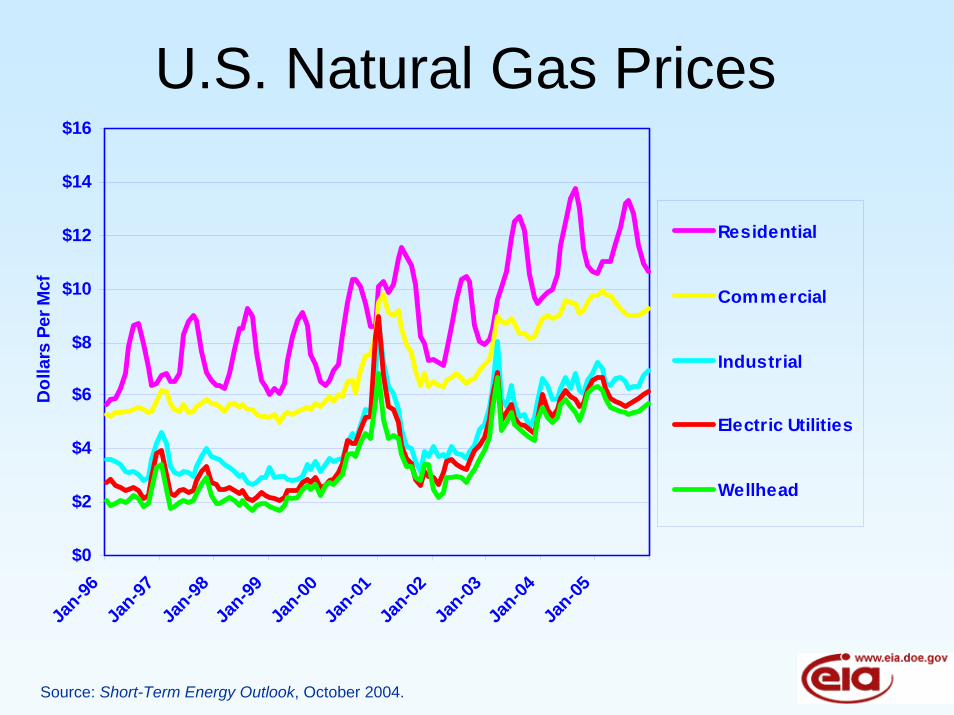

Residential

Commercial

Industrial

Electric Utilities

Wellhead

U.S. Natural Gas Prices

Source: Short-Term Energy Outlook, October 2004.

Working Gas in Underground Storage Is Above “Normal”

Notes: The shaded area indicates the range between the historical minimum and maximum values for the weekly series from 1999 through 2003. Source: Weekly storage values from March 15, 2002, to the present are from Form EIA-912, "Weekly Underground Natural Gas Storage Report." Values for earlier weeks are from the Historical Weekly Storage Estimates Database.

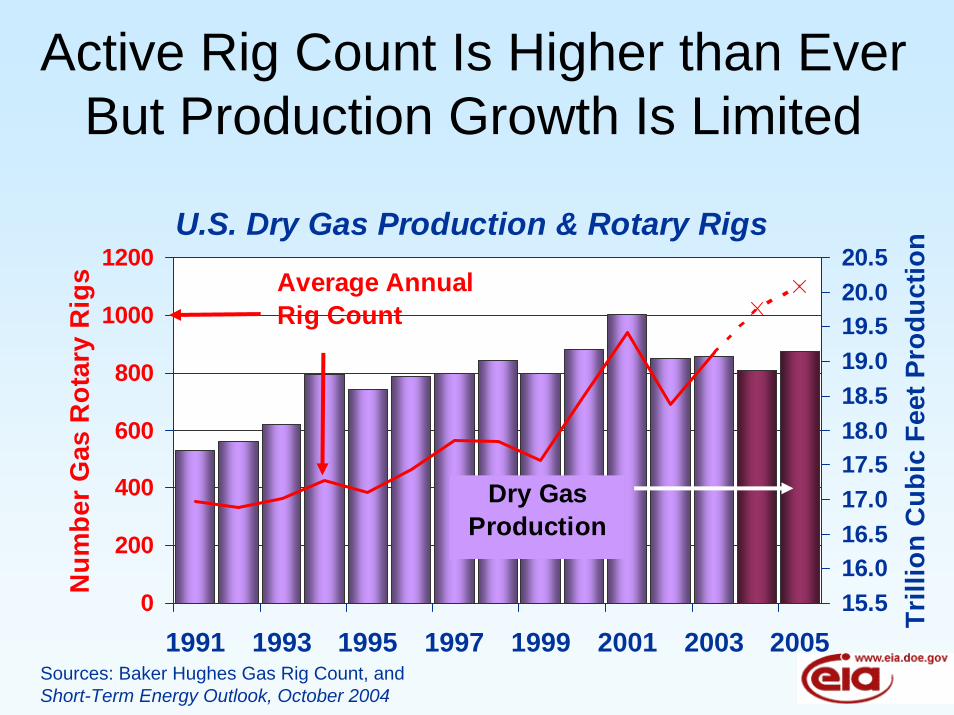

Active Rig Count Is Higher than Ever But Production Growth Is Limited

0

200

400

600

800

1000

1200

1991 1993 1995 1997 1999 2001 2003 2005

Num

ber

Gas

Rot

ary

Rig

s

15.516.016.517.017.518.018.519.019.520.020.5

Trill

ion

Cub

ic F

eet P

rodu

ctio

nU.S. Dry Gas Production & Rotary Rigs

Dry Gas Production

Average Annual Rig Count

Sources: Baker Hughes Gas Rig Count, andShort-Term Energy Outlook, October 2004

A Growing Percentage of Production Flows from Wells Three Years Old or Less

0

10

20

30

40

50

60

Perc

ent T

otal

Wel

lhea

d C

apac

ity

2003

–< 1 Year Old–< 2 Years Old–< 3 Years Old

1993

–< 1 Year Old–< 2 Years Old–< 3 Years Old

Source: EIA.

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

1997 1998 1999 2000 2001 2002 2003 2004 2005

Billio

n C

ubic

Fee

t

Pipeline LNG

Projections

Source: Short-Term Energy Outlook October, 2004.

Pipeline Imports Decline asLNG Imports Increase

LNG Imports:2003: 510 Bcf2004: 670 Bcf2005: 840 Bcf

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Perc

ent C

hang

e

0

10

20

30

40

50

60

70

80

90

Bill

ion

Cub

ic F

eet p

er D

ay

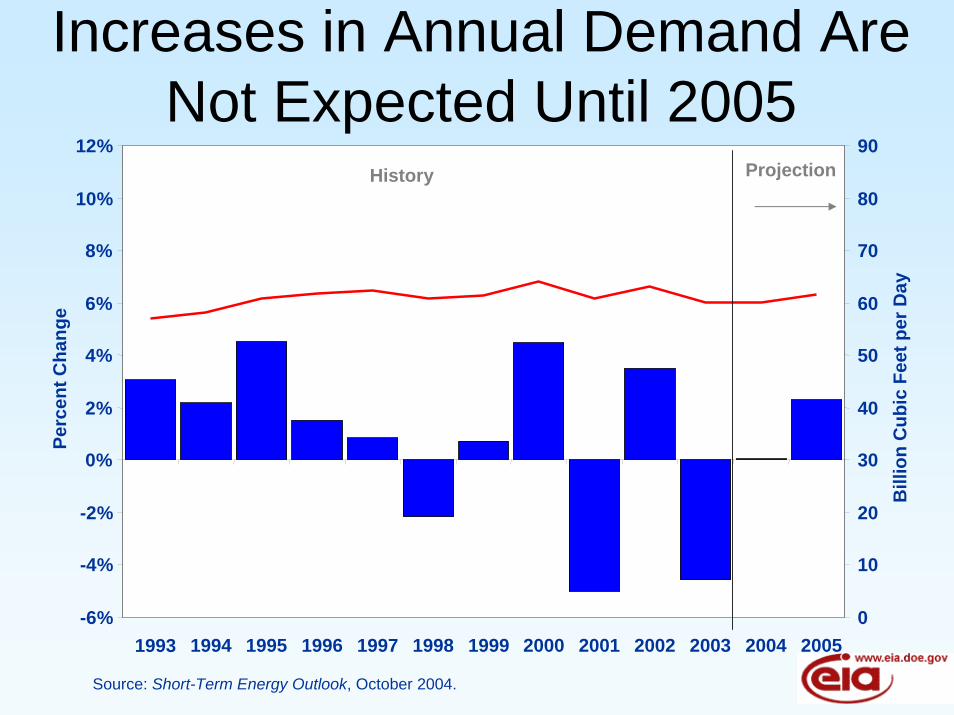

Increases in Annual Demand Are Not Expected Until 2005

History Projection

Source: Short-Term Energy Outlook, October 2004.

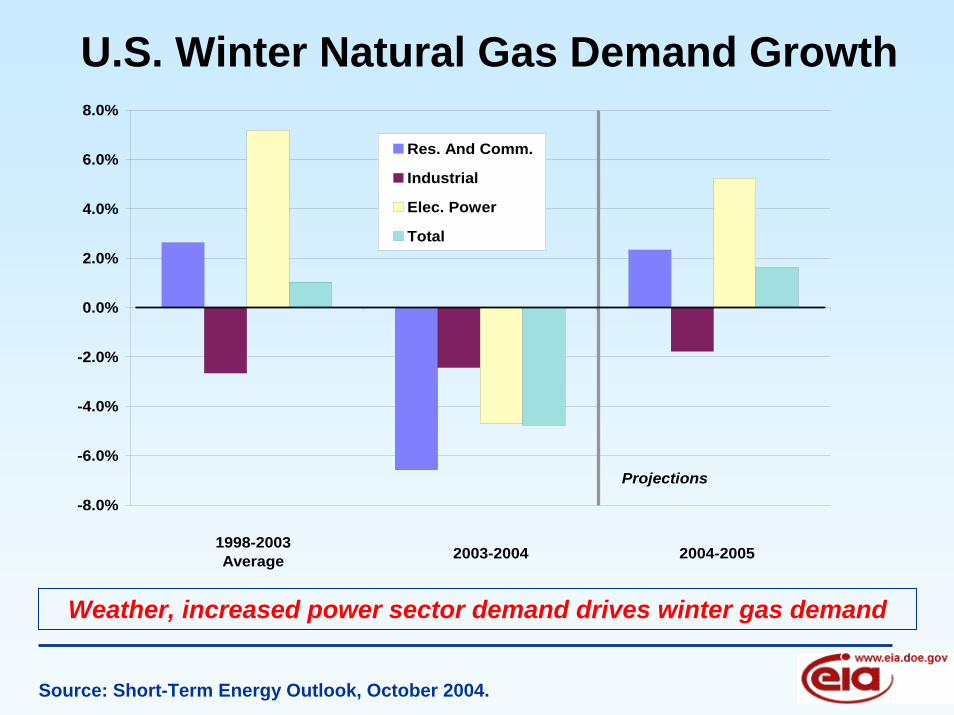

U.S. Winter Natural Gas Demand Growth

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

Res. And Comm.

Industrial

Elec. Power

Total

Projections

1998-2003Average 2003-2004 2004-2005

Weather, increased power sector demand drives winter gas demand

Source: Short-Term Energy Outlook, October 2004.

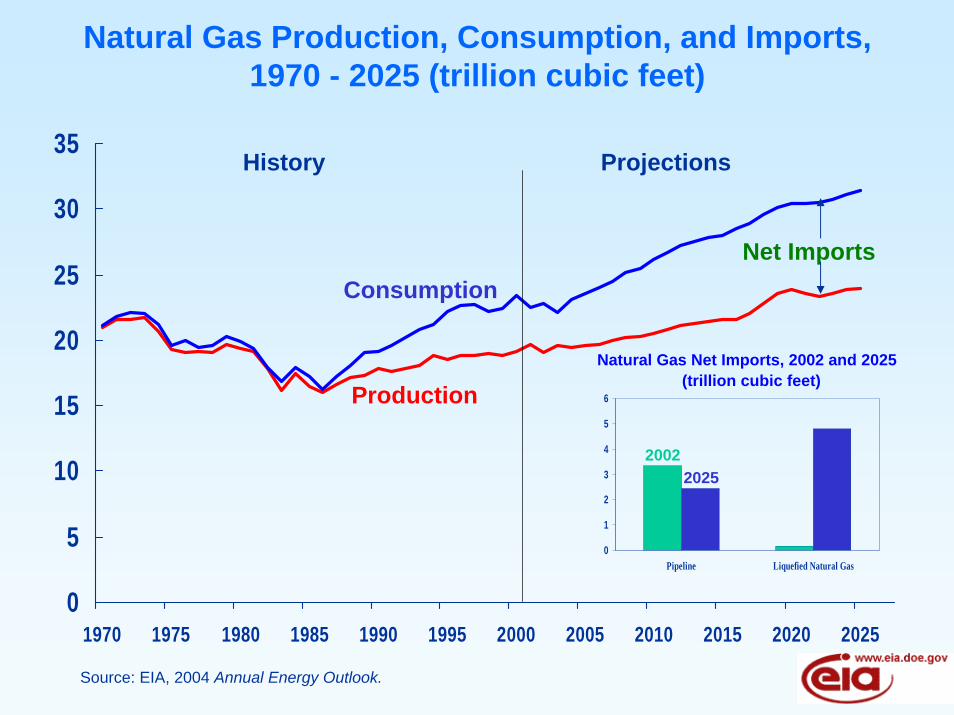

Natural Gas Production, Consumption, and Imports,1970 - 2025 (trillion cubic feet)

0

5

10

15

20

25

30

35

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025

Consumption

Production

Net Imports

History Projections

0

1

2

3

4

5

6

Pipeline Liquefied Natural Gas

Natural Gas Net Imports, 2002 and 2025(trillion cubic feet)

20022025

Source: EIA, 2004 Annual Energy Outlook.

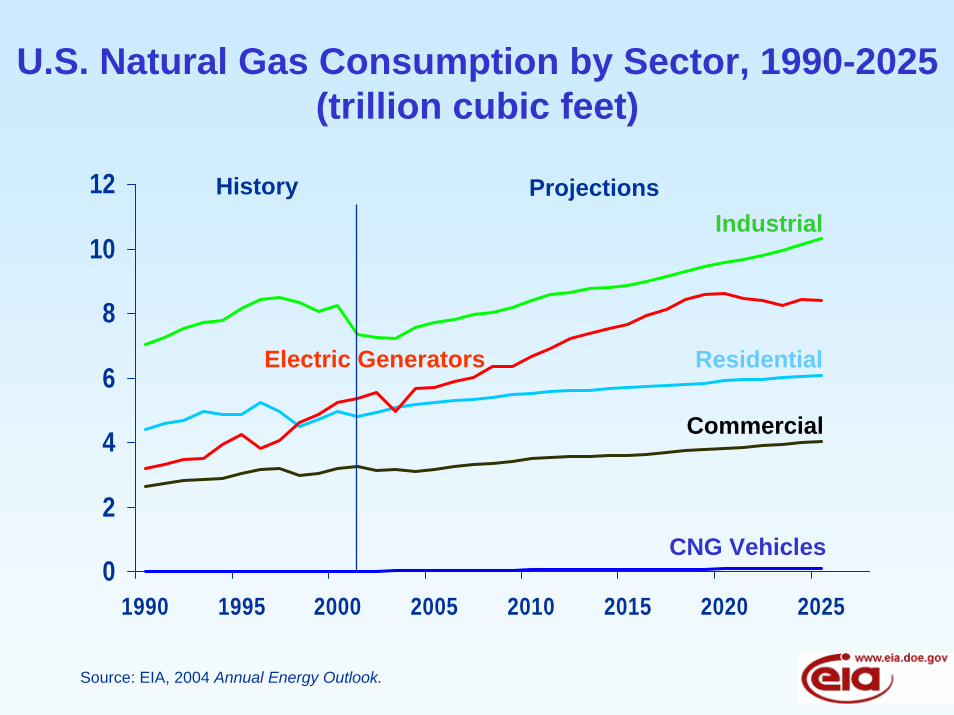

U.S. Natural Gas Consumption by Sector, 1990-2025(trillion cubic feet)

0

2

4

6

8

10

12

1990 1995 2000 2005 2010 2015 2020 2025

HistoryIndustrial

Electric Generators Residential

Commercial

CNG Vehicles

Projections

Source: EIA, 2004 Annual Energy Outlook.

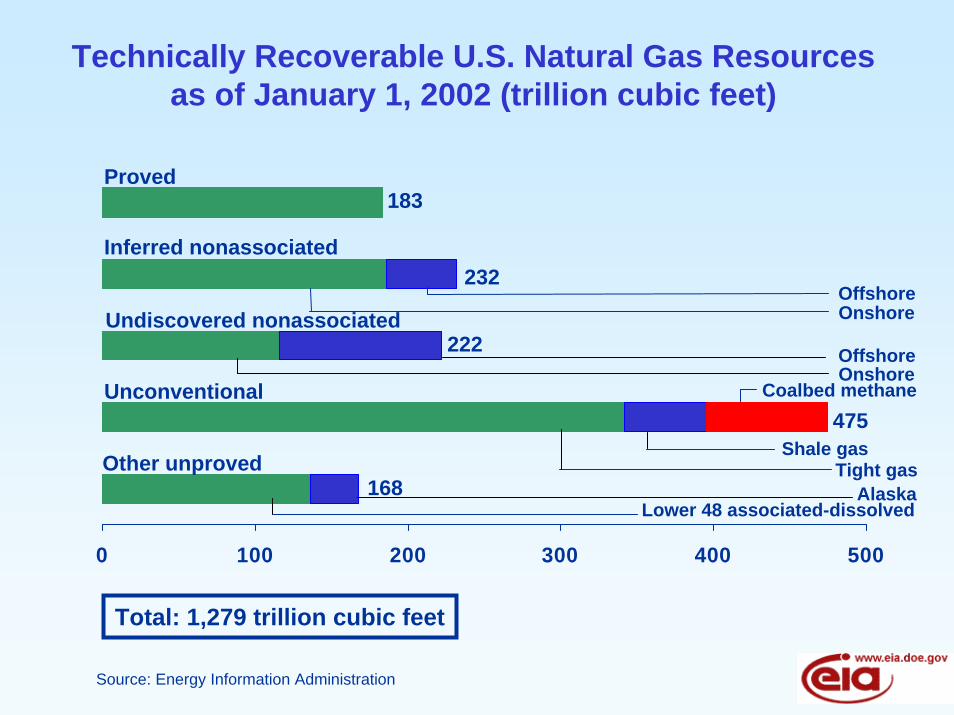

Technically Recoverable U.S. Natural Gas Resources as of January 1, 2002 (trillion cubic feet)

0 100 200 300 400 500

Undiscovered nonassociated

Inferred nonassociated

Unconventional

Other unproved

Proved

Offshore

Coalbed methane

Shale gasTight gas

AlaskaLower 48 associated-dissolved

Onshore

OffshoreOnshore

222

475

232

168

183

Total: 1,279 trillion cubic feet

Source: Energy Information Administration

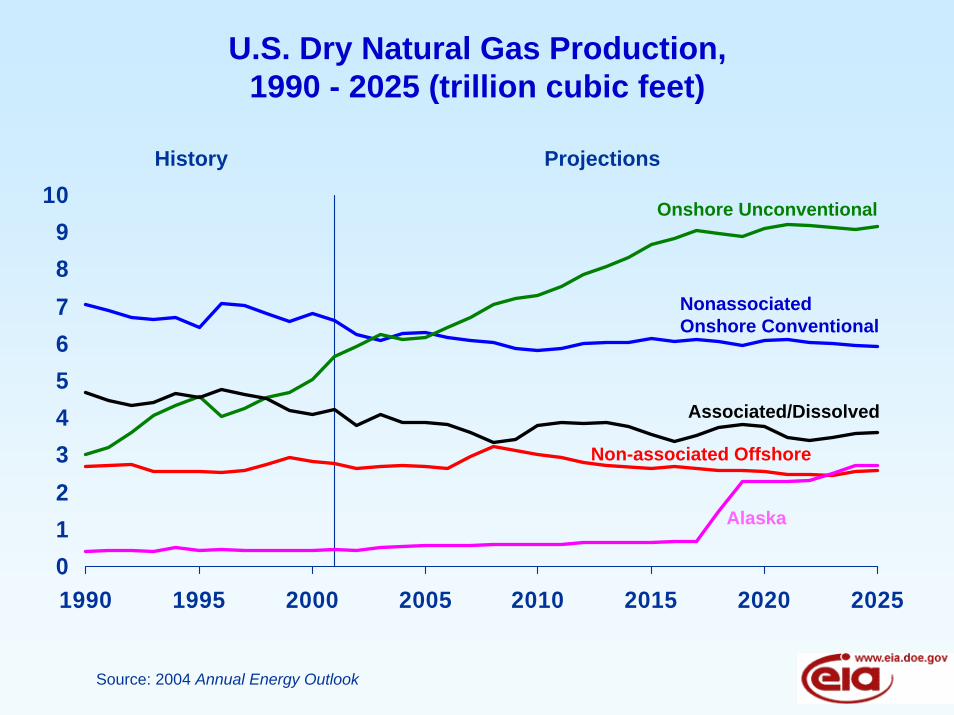

U.S. Dry Natural Gas Production, 1990 - 2025 (trillion cubic feet)

0123456789

10

1990 1995 2000 2005 2010 2015 2020 2025

History Projections

Associated/Dissolved

Non-associated Offshore

NonassociatedOnshore Conventional

Onshore Unconventional

Alaska

Source: 2004 Annual Energy Outlook

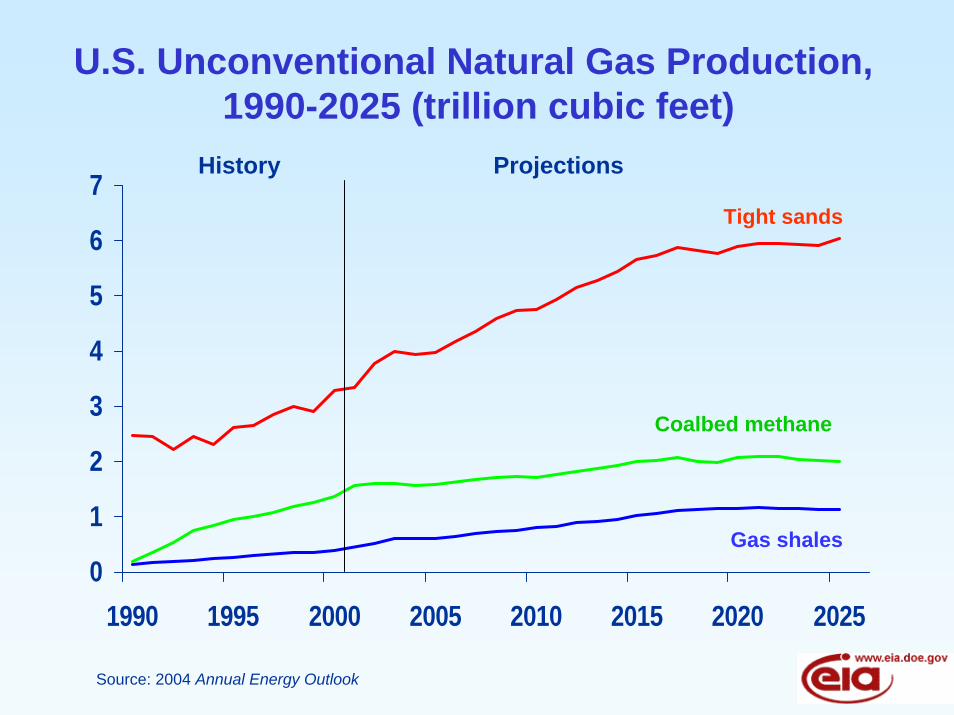

U.S. Unconventional Natural Gas Production,1990-2025 (trillion cubic feet)

0

1

2

3

4

5

6

7

1990 1995 2000 2005 2010 2015 2020 2025

History Projections

Tight sands

Coalbed methane

Gas shales

Source: 2004 Annual Energy Outlook

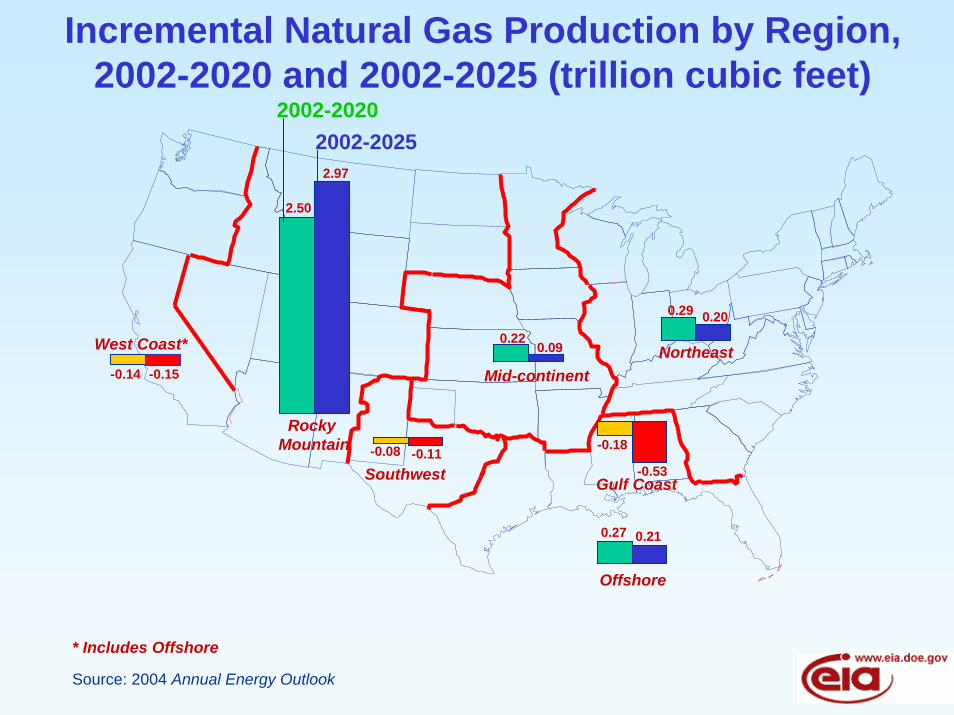

Incremental Natural Gas Production by Region,2002-2020 and 2002-2025 (trillion cubic feet)

Northeast

Gulf Coast

West Coast*

Rocky Mountain

Southwest

Mid-continent

Offshore

2.97

-0.08

0.09

0.20

0.21

-0.53

-0.15

0.29

-0.18

0.22

-0.11

2.50

0.27

-0.14

2002-20202002-2025

* Includes Offshore

Source: 2004 Annual Energy Outlook

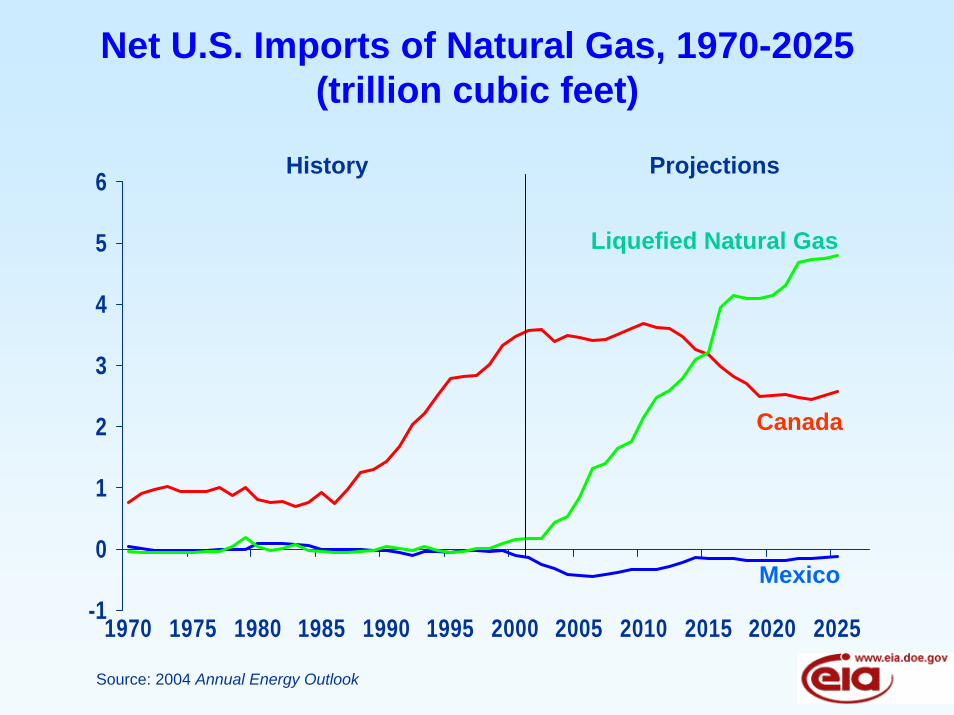

Net U.S. Imports of Natural Gas, 1970-2025(trillion cubic feet)

-1

0

1

2

3

4

5

6

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025

History Projections

Canada

Liquefied Natural Gas

Mexico

Source: 2004 Annual Energy Outlook

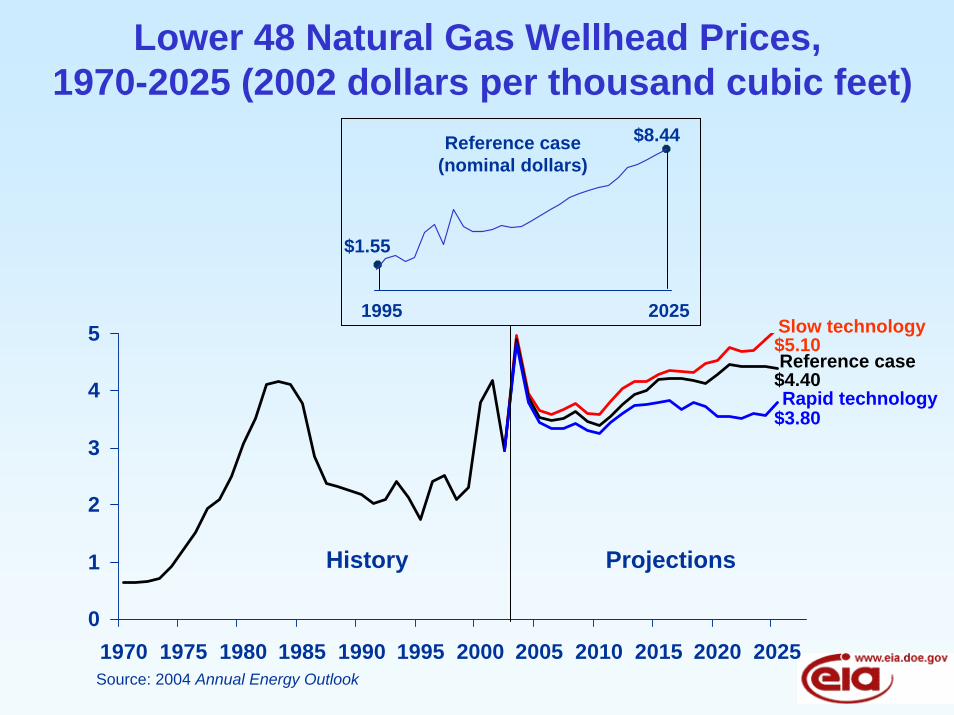

Lower 48 Natural Gas Wellhead Prices,1970-2025 (2002 dollars per thousand cubic feet)

0

1

2

3

4

5

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025

1995 2025

Reference case(nominal dollars)

$1.55

$8.44

History Projections

$4.40

Slow technology

Reference case

Rapid technology$3.80

$5.10

Source: 2004 Annual Energy Outlook

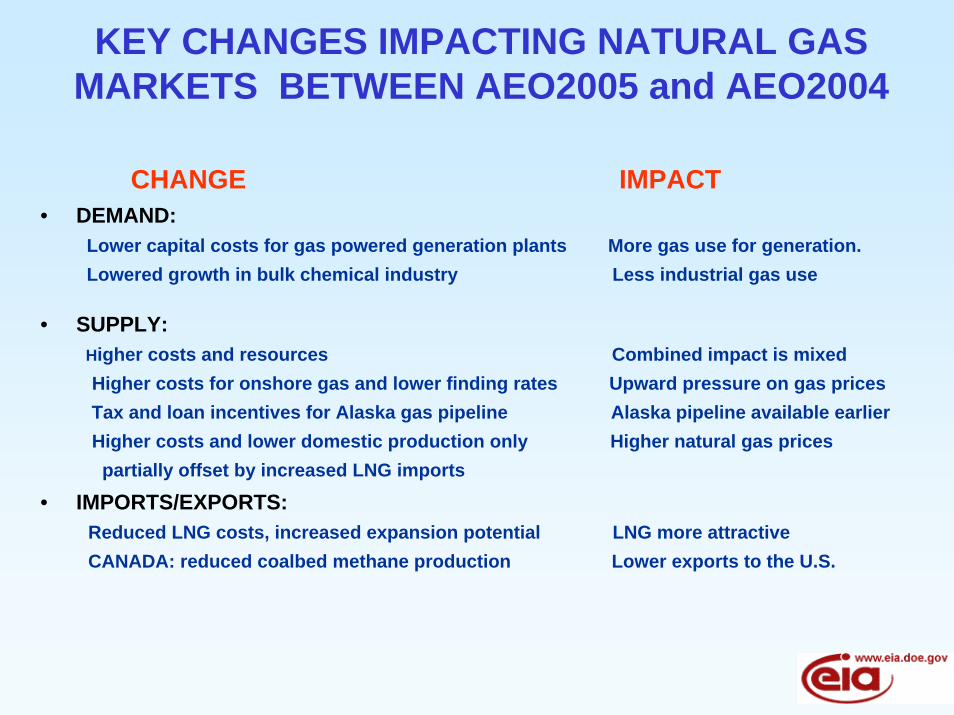

KEY CHANGES IMPACTING NATURAL GAS MARKETS BETWEEN AEO2005 and AEO2004

CHANGE IMPACT• DEMAND:

Lower capital costs for gas powered generation plants More gas use for generation.Lowered growth in bulk chemical industry Less industrial gas use

• SUPPLY:Higher costs and resources Combined impact is mixedHigher costs for onshore gas and lower finding rates Upward pressure on gas pricesTax and loan incentives for Alaska gas pipeline Alaska pipeline available earlierHigher costs and lower domestic production only Higher natural gas pricespartially offset by increased LNG imports

• IMPORTS/EXPORTS: Reduced LNG costs, increased expansion potential LNG more attractiveCANADA: reduced coalbed methane production Lower exports to the U.S.

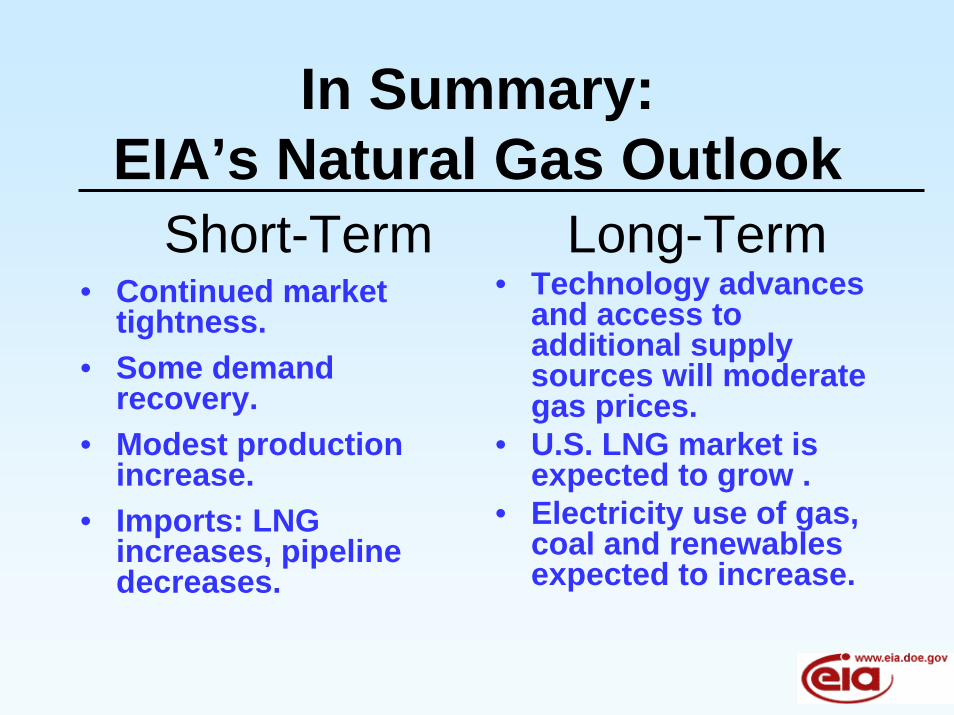

In Summary:EIA’s Natural Gas Outlook

Short-Term• Continued market

tightness. • Some demand

recovery.• Modest production

increase. • Imports: LNG

increases, pipeline decreases.

Long-Term• Technology advances

and access to additional supply sources will moderate gas prices.

• U.S. LNG market is expected to grow .

• Electricity use of gas, coal and renewablesexpected to increase.

www.eia.doe.gov