Embed Size (px)

Citation preview

NONASH EC SP 5/96

^km.ms]

AUSTRALIA

MONASH UNIVERSITY

RAISING PRICES WHEN DEMAND IS FALLING:

WHO'S KINKY NOW, BUSINESS OR ECONOMICS?

Michael Bradfield

Economics, Dalhousie University Visiting Fellow, Monash University

Seminar Paper No. 5/96

FOR LIMITED DISTRIBUTION ONLY

DEPARTMENT OF ECONOMICS

SEMINAR PAPERS

; . , !? •>> ( > 0 I !;M^.^:AS>.... t.r...:. ^.^^.

• ' ' • ^ 1

1 " 5 '^uJ — -JosrmP C2£:;;:'-^2 :.:.^.:^xi.

iCOfiSh T.SS Raising Prices When Demand is Falling -Who's Kinky Now, Riisiness or Economics?

Michael Bradfield Economics, Dalhousie University

Visiting Fellow, Monash University

Abstract: Short run price rises in particular industries are often "explained" in unconvincing, if not bizarre, ways: to protect profits or margins in the face of falling demand or of rising fixed costs, to recoup losses in other markets, to refiect rising costs due to falling output and the concomitant loss of economies of scale. Despite their currency, these explanations are inconsistent with marginal cost analysis applied to either perfectly competitive or various forms of imperfect markets.

This paper discusses the richness of kinked demand curve analysis as originally developed (not as mis-represented in the literature) for dealing with price changes. It uses an extension of the kinked demand curve analysis - a version of the sliding kink of Cyert and DeGroot (1971) or "conscious parallelism" coined by Hamburger (1967) -to make apparently perverse business decisions explicable, if not predictable.

Microeconomics relies on marginal analysis, even if marginal cost is not always equated to marginal revenue, as in the case of the kinked demand curve. Nonetheless, the real world often provides examples of firm behaviour which runs counter to marginal analysis of short run behaviour:

1. The private banks, when they incurred massive losses from loans to third world dictators in the '80s and to first world speculators in the '90s, raised interest rates and

. service charges against their other customers "to recoup their losses". 2. In the face of the deepening of the recession in the early '90s, firms in many industries, as diverse as advertising and pulp and paper, raised their prices to "protect" profits or margins. 3. Various industries use rising fixed costs, such as interest rates or research and development expenditures, as the justification for price increases. 4. In the oil crisis of 1973, many industries raised their prices by much more than warranted by the increases in the energy costs which were used to justify those price increases; for many industries, profits rose during this period of rising costs and prices. 5. Firms which face falling demand sometimes raise prices, explaining that the loss of economies of scale forces this regrettable move.

The media carry these explanations of price increases without any suggestion that something is amiss. Neither academic nor "business" economists seem to question what is going on. Indeed, some even repeat the firms' rationalizations when asked to explain price trends.

Are firms' public pronouncements simply fig leaves covering their real intentions? Do firms feel under social pressure to offer a seemingly plausible rationale for their price increases? Do price increases refiect delayed responses to a number minor increases in costs (Nowotny and Walther, 1978)? Are movements to profit maximization jerky, and done when public acceptance is most likely? Are these examples simply anomalies of various types which require only ad hoc explanations or is there a theoretical explanation for these price increases and their rationales? Is it simply that "[ejconomists who are accustomed to thinking in terms of traditional demand curve analysis are likely to attribute this kind of [business behaviour] to

ignorance or perversity" (Sweezy, 1939: 569) on the part of the business community? At the risk of pumping more life into a body of literature which Stigler (1978) hoped

had become a corpse, this paper uses the kinked demand curve to analyse the above aberrations. We begin with a brief sketch of the development of the kinked demand curve and its predictions of price variability, as presented by its advocates, not its detractors. We then propose the "conjectural hitch" combining Hamburger's (1967) "conscious parallelism" with Cycrt and DeGroot's sliding kink (1971) to provide explanations for some anomalous behaviour.

THE KINKED DEMAND CURVE AND PRICE INSTABILITY

The literature following Stigler (1947) mis-represents the kinked demand analysis, claiming it was developed to explain 'perceived' price stability in oligopolies. However, Sweezy's original intent was to point out the policy and distributional implications of the kinked demand curve (Frecdman, 1995). He simply suggests, almost as a throw-away line, that the kinked demand curve "can be developed in such a way as to throw light on the much-debated problem of rigid prices, but to do so would be beyond the scope of this paper (572)." Thus, it is not true that "Sweezy...proposcd the model as an explanation of rigid oligopoly prices, which were taken as an empirical fact" (Cyert and DeGroot, 1971: 272). Similarly, Hall and Hitch (1939) intended to show that the process by which imperfectly competitive firms actually make their price decisions casts doubt on the applicability of marginal analysis.

Indeed, neither of the original kinked demand curve articles assumes only one, permanent kink. Sweezy states that at different times the kinked demand curve could be either concave or convex to the origin ~ what Efroymson (1943) labels the obtuse and refiex kinks, respectively. Hall and Hitch argue that the kink may shift, but the refiex curve is, at best, only implicit in their discussion (1939: 28; fn 2). Because of the possibility of multiple kinked demand curves, Sweezy (1939: 573) concludes that there are many possible "equilibriums". Hall and Hitch (1939; 27) are also unequivocal: "We may distinguish two main cases, which we shall call those of price stability and instability, since the terms equilibrium and dis-equilibrium have a connotation too precise to be warranted here."

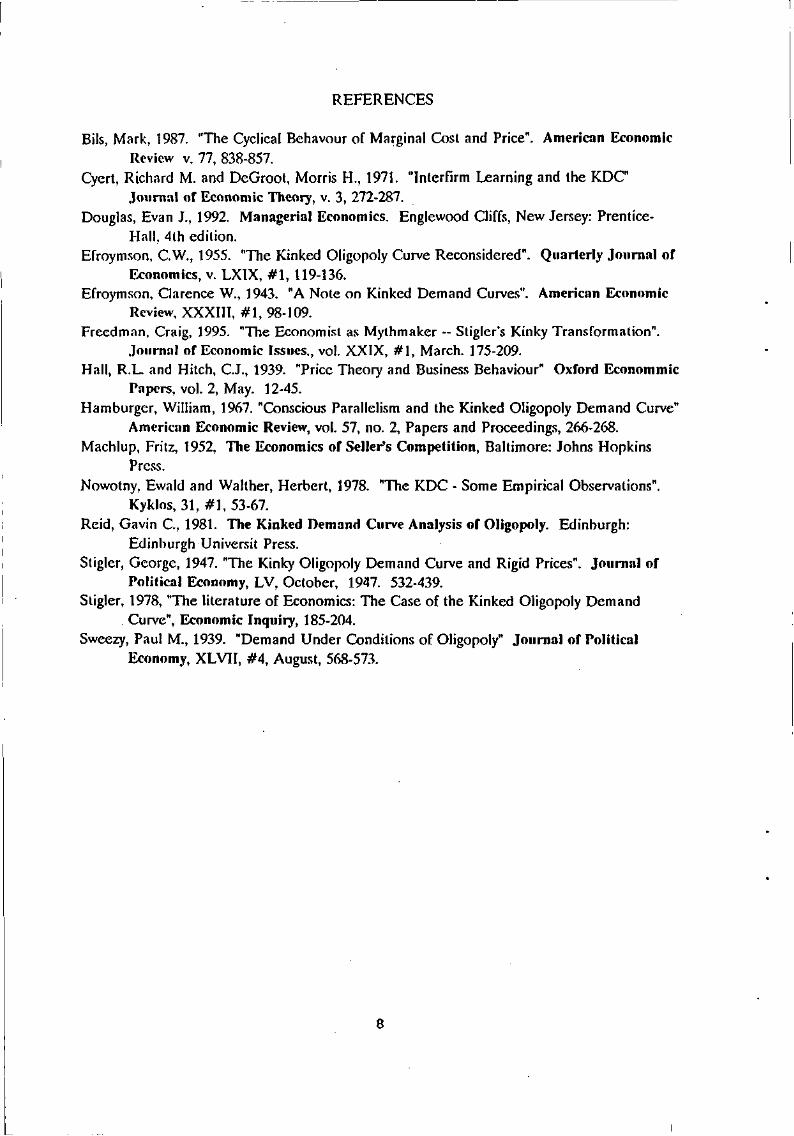

Figure 1 shows the "conventional" or obtuse kinked demand curve, CKM. It is composed of part of the ceteris paribus demand curve, CP (when competitors hold their prices), and part of the mutatis mutandis demand curve, FM, which suggests a fixed market share as each firm keeps its price in line with those of its competitors. When demand is not high enough for firms to be producing at capacity,' they are pessimistic (and risk averse?). Their conjecture of competitors' reactions generates the conventional kinked demand curve.

Both of the original articles suggest that firms may behave differently when producing at capacity compared to when demand is low. Efroymson (1943) develops this argument using Hall and Hitch's demand shifts, but with no reference to Sweezy although he speculated (570ff) about the conditions under which the refiex curve might be operative. When demand conditions are good, firms are producing high levels of output, at or close to their capacity. Efroymson argues this could generate optimism among all firms and perhaps expectations that other firms would raise their prices if someone leads the way. If they are already at

^ "Capacity" is not defined in the early kinked demand curve literature, but it seems to relate to businesses' concept of a normal output, not a technical definition such as a nearly vertical marginal cost curve.

capacity and have a backlog of orders, they may not see the need to cut prices should a competitor do so. (And if everyone is working at capacity, there is no reason to expect anyone to cut prices.) Sweezy (1939: 571) also notes that labour and material costs may be risiTig when demand is" growing, providing further justification for the change in expectation with respect to price cuts.

These changed expectations would mean that the demand curve would become the reflex kinked demand curve, fkp, in Figure 1. The increase in demand is indicated by the shift of the kink from K to k. The change in expectations is indicated by the shift to the reflex kink.

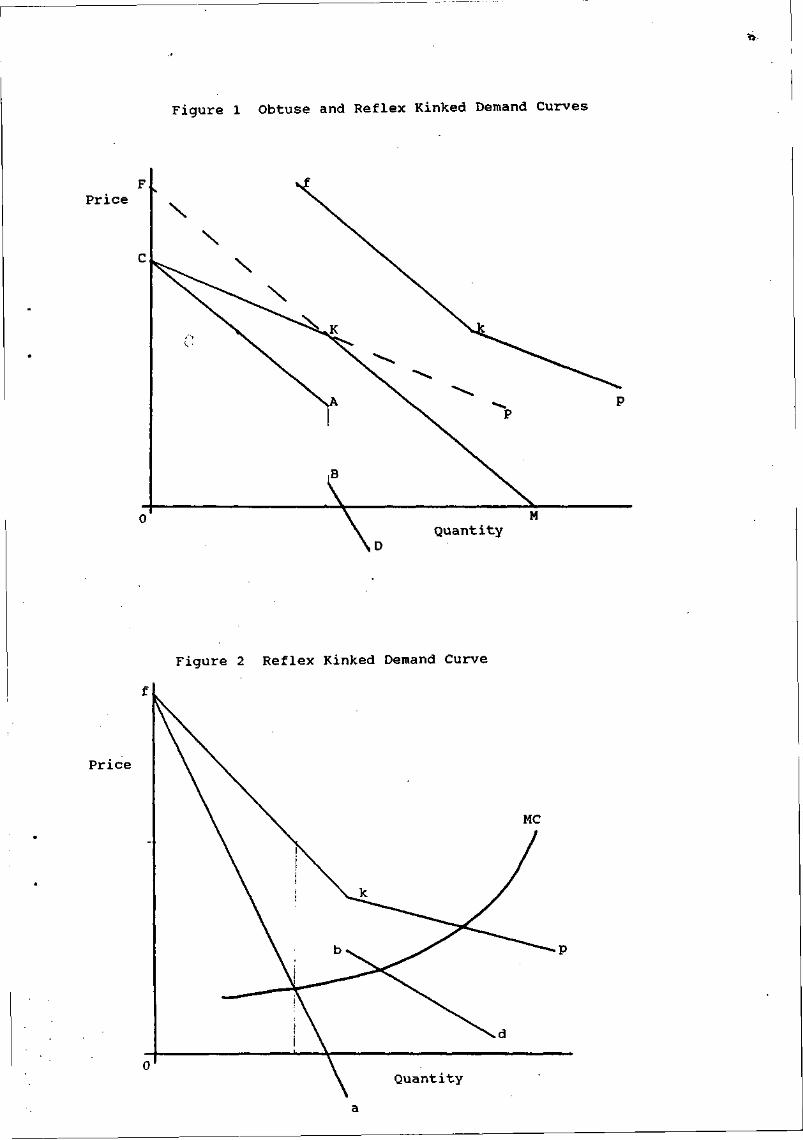

Figure 2 illustrates the discontinuous marginal revenue curve, fabd, generated by the reflex kink, fkp. If the marginal cost is as shown, MC, it not only goes through the ab gap in the marginal revenue curve but intersects both segments of the marginal revenue, fa and bd. Thus, two different prices are possible in this situation, although only one will generate maximum profits.^ Of course, different marginal cost and marginal revenue curves could generate an intersection of the marginal cost with either the fa or the bd segments of the marginal revenue curve and there would be only one profit maxmising price, again not at the kink.

Efroymson argues that boom conditions will lead to rising prices which will eventually push the level of production below capacity. This will create pessimism and a return to the obtuse kink and stable prices with unemployment. Prices would be stable during slumps in demand, but rising and unstable during periods of high demand. Efroymson concludes that these alternative kinks will generate cyclical pricing behaviour. "It is, I believe, obvious that reflex and obtuse demand curves are intimately linked to cyclical fluctuations, both in their origins and in their effects (Efroymson, 1943: 107)." However, he subsequently (1955) plays down the likely frequency of the reflex curve.

The kinked demand curve literature •also includes the possibility of changing expectations with changes in costs. Hall and Hitch (1939: 25) suggest that cost changes could generate a "re-evaluation" of the kinked price but they are not clear how they expect this to affect the kink. Sweezy, as noted, mentions increasing costs as part of the explanation for the shift from the obtuse to the reflex kink.

Machlup (1952: 473-474) is less careful and asserts that general cost increases will drive prices up. "If the firm knows that the rivals' costs also increase, the entire demand curve (with its kink) will be shifted upwards and selling prices will be raised." Neither Sweezy nor Hall and Hitch makes this clear distinction between firm-specific and industry cost increases. It is a useful distinction. Clearly a firm which faces rising input costs unique to itself will be inclined to view the kink as unmoved and absorb the extra costs as long as the marginal cost remains in the AB gap of the marginal revenue curve in Figure 1.

But an industry-wide increase in costs does not imply Machlup's "bodily upward shift of the kinked demand curve" (Reid, 1982:47). In the short run with the number of firms constant, the only way that the FM (fixed market share) demand curve can shift up would be if there were an increase in market demand for the industry's product. This would lead to an increase in demand for each firm's product. But an increase in demand does not occur when

^ Here Efroymson moves dramatically away from Hall and Hitch (1939: 18) who predict that maximum profits are "an accidental (or possibly evolutionary) by-product" of the application of "full cost" or markup pricing. Efroymson (1943: 99) points out that the kink is not tied to the assumption by Hall and Hitch of full cost pricing.

an industry's costs rise!- Nor does a general increase in industry costs suggest an upward shift in the ceteris

paribus demand curve, CP in Figure 1. This too implies an increase in demand for the product, an increase which would not be the result of rising industry, or firm, costs.

The actual impact of an industry-wide increase in costs can be explained by what Douglas (1992: 376-377) calls, following Hamburger (1967), "conscious parallelism". It seems more appropriate to use a term such as "conjectural hitch" since conjectural change is implied by Hall and Hitch. The application of the conjectural hitch leads to explanations of the anomalies which opened this paper.

THE CONJECTURAL HITCH

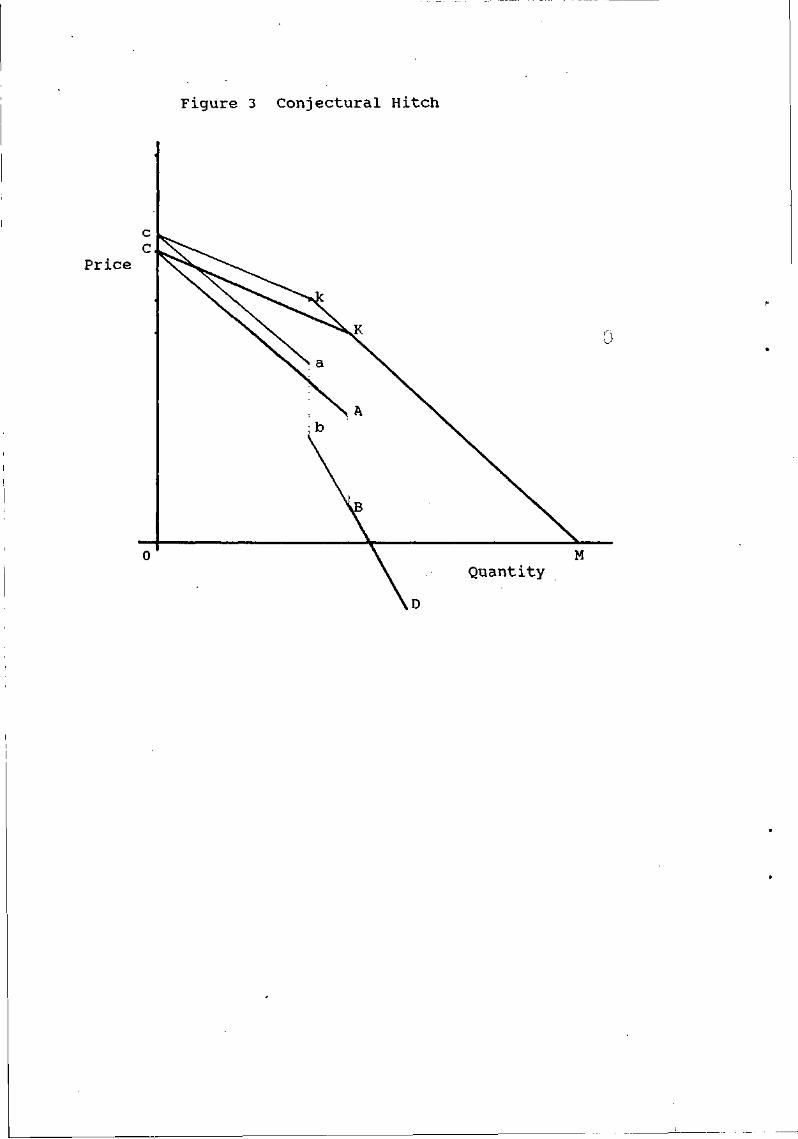

Let us assume a situation in which each firm in an industry is faced with an obtuse kinked demand curve such as CKM in Figure 3. The marginal cost curve is assumed to cut the marginal revenue curve in the AB gap and prices are stable.

If there is an increase in labour or material costs, the marginal cost curve shifts up. As long as the new marginal cost is still in the AB gap, prices will remain stable, ceteris paribus. But are other things likely to remain constant? If the increase in costs is pervasive in the industry, each firm will not only suffer declining profits but will know that its competitors are also experiencing a cost squeeze on their profits.

Given the general decline in industry profits, firms may change their conjecture about competitors' reactions to a price change. Each firm may want prices to rise "to offset the cost increases". If each firm recognizes that this is true for all firms, they may decide that some increase in price is acceptable to all. If one firm raises its price, all firms will follow, up to some limit (Cyert and DeGroot, 1971).

Tliis change in expectations creates a hitch in the conventional kinked demand analysis. Rather than a shift up in the mutatis mutandis demand curve, FM, as claimed by Machlup, there will be an extension of MK to a new point, such as k. Thus, the firm expects competitors are willing to follow an increase in price to the level determined by k. This is the "re-valuation" of the acceptable industry price posited by Hall and Hitch. Under the new conjecture, competitors will only follow to k; after that the firm raising its price is, once again, on its own. The kink has moved to k.

Thus the conjectural hitch creates a new demand curve, ckM, with its discontinuous marginal revenue curve, cabD. Prices will rise to k if the marginal cost curve cuts through ab, the new gap in the marginal revenue curve. However, if the marginal cost curve intersects the bD component of the marginal revenue curve, the price rise will be less than to k. Demand conditions could prevent the price from rising by the initial amount intended if the firms are profit maximising.

What is the limit for the price rise? The conjectural hitch may anticipate a willingness to increase prices by as much as costs have increased, or even more, if firms follow a markup over cost rule. This would establish an upper limit on the new kink. The lower limit is

^ Of course, such an upward shift in the mutatis mutandis demand curve would result if there were an economy-wide infiation in which all prices and incomes rose by the same amount, so that nothing changed in real terms.

determined by whether the marginal cost curve intersects the extended marginal revenue curve, bD, to the right of the new gap in the marginal revenue curve. If the marginal cost does intersect the new marginal revenue, bD, prices will not rise as high as k and k is likely to shift down to the profit maximising price, especially if the new price remains for some time.

Wherever the new kink is established, the effect of the general increase in variable input costs can be an increase in prices, even though the higher marginal cost still remains in the initial gap in the marginal revenue. Thus the conjectural hitch generates rising prices even in circumstances where the conventional kinked demand curve analysis would predict stable prices.

Once the possibility of a conjectural hitch is accepted, a number of anomalies may be explained. We begin with rising fixed costs and then examine falling demand.

Rising Fixed Costs

Let us remain with the scenario where firms can rationally expect to be faced by the kinked demand curve, CKM, in Figure 3. There is price stability (or "discipline" as firms in the market might express it) even though firms may be operating below capacity, may have excess inventories, and profits may be down.

Now consider an increase in fixed costs, for instance higher interest rates. The rising fixed costs would cut into profits; how can a firm protect its profits?

Firms will all face interest cost increases as their respective debts come up for renewal. Eventually, if firms are similarly leveraged, all firms will be suffering similar cost increases and profit declines.

Given their common dilemma, each firm in the industry may feel that all firms would like prices to rise to offset the increases in interest costs. This new conjecture about their competitors' preferences means that, again, some ri.se in price by one firm will be followed by other firms. This anticipated movement in parallel again means the demand curve in Figure 3 changes from CKM to something like ckM. The price rise in the industry will be generated by an increase in fixed costs, even though marginal cost has not moved out of the AB gap and no firm has left the industry, as would be the necessary in a perfectly competitive industry making long run adjustments to higher fixed costs.^

This type of fixed cost increase leading to price increases is at least implicit in the kinked demand curve literature from the beginning. Both Hall and Hitch and Machlup (1952) refer to cost increases raising prices, without specifying whether they mean any and all costs. TTie examples of cost increases they both present are of marginal costs, such as for labour or raw materials. However, under their "full cost" pricing assumption, it is reasonable to infer from Hall and Hitch that, in the long run at least, fixed costs would be fully passed on in higher prices. The conjectural hitch means that this can happen in the short run. Moreover, if the increase in price is successful in raising profit levels, although not necessarily or even likely to the original level, this short run strategy may preclude the need for a long run adjustment of some firms leaving the industry. The firms may be making normal or even excess profits, but not as excess as before the increase in fixed costs and the shift in the kink to k.

'' Of course, in a monopoly, the rise in fixed costs would have no effect on price at all, as long as at least normal profit,s were generated.

Falling Demand

Does the obtuse demand curve CKM represent the only possible firm conjecture in a slump? With falling sales and declining profits, firms will not want to lose further sales because of price cuts from competitors. Nor, in the conventional kinked demand curve analysis, are they likely to follow a price rise. Hence, Efroymson and others assume the obtuse curve, CKM, will prevail when demand has fallen.

But in a slump, each firm knows that all other firms are suffering from falling sales and declining profits. Each knows that all firms want to do something to improve profits. What if the decision-makers' experience is that raising prices has traditionally increased profits?

If the subjective conditions exist to make the firms believe that everyone wants a price rise to restore profits, then the kink shifts, for instance to k in Figure 3. This again generates the new kinked demand curve ckM and its discontinuous marginal revenue curve, cabD. Again, price could rise to k, but this will depend on whether the firm's marginal cost lies in the ab gap or intersects with either segment ca or bD of the new marginal revenue curve. In any case, the conjectural hitch generated by falling demand and declining profits will lead to an increase in price.

Rather than falling, the conjectural hitch generates a rise in price when demand falls! The firms' common conjecture that everyone needs and wants a price increase to restore profits generates a self-fulfilling prophecy. Output falls by more than the initial decline in demand and stagflation is generated. This effect is all the more likely if the fall in demand and profits were caused by an increase in interest rates. The increase in interest rates may have been instituted to fight inflation - real, incipient, or apprehended. Because of the conjectural hitch, the result is stagflation.

However, if the decision-makers of each firm took introductory economics, they might assume that when demand falls, price will fall, somewhere on the fixed market share portion of their existing demand curve. But if they assume their competitors would follow price cuts anywhere along KM, the kink would stay where it is, and price would not fall. This could well be the case if, for instance, firms believed the current demand slump to be temporary.

Of course, there are any number of variations on this theme. If the firm has the capacity to make secret price concessions (Sweezy, 1939: 570), it may feel the kink can be avoided for a time, and its demand curve becomes CP. Or it may feel that the other firms will be glad to cut price during the slump and hold it at the lower level so that the kink moves toward M along KM. This would shift the ceteris paribus part of the demand curve down and create the possibility of a new kink at a lower price. How much lower will again depend on the constraint imposed by the possible intersection of the marginal cost and marginal revenue curves.

On the other hand. Hall and Hitch (1939: 28; fn 2), take the position that a rise in demand so that firms are working at capacity "will remove the kink in the demand curve and make its elasticity above the old price similar to its elasticity below it" . In the context of the current discussion, Hall and Hitch are suggesting that high demand may generate a "conjectural hitch" extending the mutatis mutandis demand curve, rather than generating the refiex curve as predicted by both Sweezy and Efroymson.

The conjectural hitch suggests an asymmetry in firm reactions. If demand has been increasing, the obtuse kink of demand curve CKM may shift to the right and prices remain stable. If interest rales are increased to fight infiation, this could lead firms to change their

conjecture about their competitors' reactions and generate the reflex kink of fkp in Figure 1. From Figure 2-, this will generate a jump in prices. Thus the high interest rate policy, intended to fight inflation, causes it.

IMPLICATIONS

The kinked demand curve analysis can predict a variety of price reactions to changing conditions - or even to the same market conditions. The ambiguities reflect the complexity of market conditions and of changing expectations with changes in those, and other, conditions. Cyert and DeGroot (1971:286) note that "in the real world, it would be possible at one instant of time to have the kink prevail and at another instant of time to have it fail to prevail." The variations and permutations of the kinked demand curve, once the conjectural hitch enters, are more numerous than just an "on-off proposition^ The possibilities for contrasting outcomes provide a micro rationale for the sunspols of the macro economy. The conjectural hitch with falling demand could explain the countercyclical nature of margins (Bils, 1987).

While providing reduced capacity for prediction, the conjectural hitch introduces increased capacity for explanation. This should be an acceptable trade-off since the two-handed economist who admits she cannot predict but can suggest alternative scenarios will be more useful than the economist who points confidently but incorrectly in one direction. In some ways, the policy implications revive earlier attitudes. To the extent that the conjectural hitch is operative, attempts to use interest rates to remove inflationary pressures may only add to them, even if the higher interest rates are successful in slowing the economy. Industry reactions which are normally expected to occur in the long run become short run responses. Also, with the conjectural hitch, reducing wages may not lead to price reductions or even price stability if firms feel they have "earned" higher profits.

REFERENCES

Bils, Mark, 1987. "The Cyclical Behavour of Marginal Cost and Price". American Economic Review v. 77, 838-857.

Cyert, Richard M. and DeGroot, Morris H., 1971. "Interfirm Learning and the KDC" .Journal of Economic Theory, v. 3, 272-287.

Douglas, Evan J., 1992. Managerial Exronomics. Englewood Cliffs, New Jersey: Prentice-Hall, 4lh edition.

Efroymson, C.W., 1955. "The Kinked Oligopoly Curve Reconsidered". Qnarterly Journal of

Economics, v. LXIX, # 1 , 119-136. Efroymson, Clarence W., 1943. "A Note on Kinked Demand Curves". American Economic

Review, XXXIII, # 1 , 98-109. Freedman, Craig, 1995. "The Economist as Mythmaker ~ Stigler's Kinky Transformation".

Journal of Economic Issues., vol. XXIX, # 1 , March. 175-209. Hall, R.L. and Hitch, C.J., 1939. "Price Theory and Business Behaviour" Oxford Econommic

Papers, vol. 2, May. 12-45. Hamburger, William, 1967. "Conscious Parallelism and the Kinked Oligopoly Demand Curve"

American Economic Review, vol. 57, no. 2, Papers and Proceedings, 266-268. Machlup, Fritz, 1952, The Economics of Seller's Competition, Baltimore: Johns Hopkins

Press. Nowotny, Ewald and Walther, Herbert, 1978. "The KDC - Some Empirical Observations".

Kyklos, 31, # 1 , 53-67. Reid, Gavin C, 1981. The Kinked Demand Curve Analysis of Oligopoly. Edinburgh:

Edinburgh Universit Press. Stigler, George, 1947. "The Kinky Oligopoly Demand Curve and Rigid Prices". Journal of

Political Economy, LV, October, 1947. 532-439. Stigler, 1978, "The literature of Economics: The Case of the Kinked Oligopoly Demand

Curve", Economic Inquiry, 185-204. Sweezy, Paul M., 1939. "Demand Under Conditions of Oligopoly" Journal of Political

Economy, XLVII, #4, August, 568-573.

Figure 1 Obtuse and Reflex Kinked Demand Curves

Price

Figure 2 Reflex Kinked Demand Curve

Price

Quantity

Figure 3 Conjectural Hitch

Price

Quantity

MONASH UNIVERSITY, DEPARTMENT OF ECONOMICS, SEMINAR PAPERS

5/96 Michael Bradfield, Raising Prices when Demand is Falling: Who's Kinky Now, Business or Economics? 4/96 Kerry Anne McGeary, The Effert of Preventive Care on the Demand for Health Services in a Developing

Country 3/96 Robert Rice, The Urban Informal Sertor: Theory, Charatteristics, and Growth from 1980 to 1990 with a

Special Emphasis on Indonesia 2/96 Jurg Niehans, Adam Smith and the Welfare Cost of Optimism 1/96 Yew-Kwang Ng, The Paradox of Interpersonal Cardinal Utility: A Proposed Solution

26/95 J. Boymal, The Economics of Alcohol Addirtion 25/95 N. Haralambopoulos, The Monetary Transmission Mechanism 24/95 X. Yang and S. Ng, Specialisation and Division of Labour: A Survey 23/95 Wenli Cheng and Yew-Kwang Ng, Intra-Firm Branch Competition for a Monopolist 22/95 Joel M Guttman, Rational Artors, Tit-for-Tat Types, and the Evolution of Cooperation 21/95 Stephen King & Rohan Pitchford, Economic Theories of Privatisation and Corporatisation 20/95 Anne O. Krueger, Free Trade Agreements Versus Customs Unions. 19/95 Andrew Comber, Estimates of the Elasticity of Substitution between Imported and Domestically Produced

Goods in New Zealand. 18/95 Peter Hartley and Chris Jones, Asset Demands of Heterogeneous Consumers with Uninsurable Idiosyncratic

Risk. 17/95 Yew-Kwang Ng, Non-Neutrality of Money Under Non-Perfert Competition: Why Do Economists Fail to See

the Possibility? 16/95 Yew-Kwang Ng, Relative-Income and Diamond Efferts: A Case for Burden-Free Taxes and Higher Public

Expenditures. 15/95 Wen Mei, Per Capita Resource, Division of Labor, and Produrtivity. 14/95 Deborah A. Cobb-Clark, Clinton R. Shiells & B. Lindsay Lowell, Immigration Reform: The Efferts of

Employer Sanrtions and Legalization on Wages. 13/95 Murray C. Kemp & Hans-Werner Sinn, A Simple Model of Privately Profitable But Socially Harmful

Speculation. 12/95 Harold O. Fried, Suthathip Yaisawamg, Hospital Mergers and Efficiency. 11/95 Yew-Kwang Ng, From Separability to Unweighted Sum: A Case for Utilitarianism. 10/95 Gerald T. Garvey, Michael S. McCony, Peter L. Swan, Stock Market Liquidity and Optimal Management

Compensation: Theory and Evidence 9/95 Siang Ng, Specialisation, Trade, and Growth 8/95 X Yang, Economies of Specialization and Downward Sloping Supply Curves: An Infra-Marginal Analysis 7/95 Viv Hall, Economic Growth Performance and New Zealand's Economic Reforms 6/95 Farzana Naqvi, Social Welfare Efferts of Taxes on Energy Produrts in Pakistan: A Computable General

Equilibrium Approach 5/95 Mei Wen, An Analytical Framework of Producer-Consumers, Economies of Specialization and Transartion

Costs 4/95 Marc Lavoie, Interest Rates in Post-Keynesian Models of Growth and Distribution 3/95 Marcus Berliant and Miguel Gouveia, On the Political Economy of Income Taxation 2/95 Russell Smyth, Estimating the Deterrent Effert of Punishment using New South Wales Local Court Data 1/95 Rod Maddock, The Access Regime and Evaluation of the Hilmer Report

30/94 Barry A. Goss and S. Gulay Avsar, Price Determination in the Australian (Non-Storble) Line Cattle Maiicet 29/94 D.K. Fausten & Robert D. Brooks, The Balancing Item in Australian Balance of Payments Accounts: An

Impressionistic View. 28/94 Sugata Maijit & Hamid Beladi, A Game Theoretic Analysis of South-South Cooperation. 27/94 Sugata Marjit, Transferring Personalised Knowledge or Guru's Dilemma. 26/94 Richard H. Snape, Globalisation and Intemationalisation of the Australian Economy: Trade and Trade Policy. 25/94 Eric O'N Fisher, Crowding Out in a Model of Endogenous Growth. 24/94 Yew-Kwang Ng, Ranking Utility Streams of Infinite Length: the Immunity of Utilitarianism from some Recent

Attadcs. 23/94 Krueger, Anne O & Roderick Duncan, The Political Economy of Controls: Complexity. 22/94 Xiangkang Yin, A Micro-Macroeconomic Analysis of the Chinese Economy with Imperfert Competition. 21/94 Brendon Riches, Price Wars and Petroleum: A 'strurture Condurt' Analysis. 20/94 Xiaokai Yang, An EquiUbrium Model of Hierarchy. 19/94 Ronald W. Jones & Tapan Mitra, Share Ribs and Income Distribution. 18/94 Dagobert Brito & Peter Hartlq', In Defence of Contributory Negligence. 17/94 Michihiro Ohyama and Ronald W. Jones, Technology Choice, Overtaking and Comparative Advantage. 16/94 Xiaokai Yang, Two Notes on New Growth Models. 15/94 Xiaokai Yang, The Nature of Capital, Investment, and Saving. 14/94 Walter Y. Oi, Towards a Theory of the Retail Firm. 13/94 Matthew W. Peter & George Verikios, Quantifying the Effert of Immigration on Economic Welfare in

Australia. 12/94 Xiaokai Yang, A Theory of the Socialist Economic System and the Differences Between the Economic Reforms

in China and Russia.

11 /94 Xiaokai Yang, Learning Through the Division of Labour and Interrelationship between Trade and Productivity Progress.

10/94 Sugata Marjit & Heling Shi, Non-Cooperative, Cooperative and Delegative R & D 9/94 Richard H. Snape, Which Regional Trade Agreement? 8/94 Richard H. Snape, Trade and Multilateral Trade Agreements: Effects on the Global Environment 7/94 Bany A. Goss & Jane M. Fry, Expectations and Forecasting in the US Dollar/British Pound Market. 5/94 Ronald W. Jones & Sugata Marjit, Labour-Market Aspects of Enclave-Led Growth. 5/94 David Henderson, Economic Liberalism: Australia in an International Setting. 4/94 Reinhard Tietz, Simplification and Complexity: The Dilemma of Economic Theory. 3/94 Ian WUls & Jane Harris, Government Versus Private Quality Assurance for Australian Food Exports. 2/94 Yew-Kwang, Ng & Jianguo Wang, A Case for Cardinal Utility and Non-Arbitrary Choice of Commodity Units. 1/94 Yew-Kwang, Ng, Why Does the Real Economy Adjust Sluggishly? Interfirm Macroeconomic Externality and

Continuum of Quasi-Equilibria.

12/93 Yew-Kwang, Ng, Towards Welfare Biology: Evolutionary Economics of Animal Consciousness and Suffering. 11/93 Yew-Kwang Ng, The Necessity, Feasibility and Adequacy of Cost-Benefit Analysis Where Life or Other "Non-

Economic" Factors are Concerned. 10/93 John Freebaim, Microeconomic Reform: Progress and Effectiveness. 9/93 K. Abayasiri-Silva & G.M. Richards, Non-Neutrality of Money in Imperfectly Competitive Macroeconomic

Models. 8/93 Xiaokai Yang, Economic Organisms and Application of Topology and Graph Theory in Economics. 7/93 Dietrich K. Fausten & Sugata Marjit, The Persistence of International Real Interest Differentials in the

Presence of Perfect Financial Arbitrage. 6/93 Barry A. Goss & S. Gulay Avsar, A Simultaneous, Rational Expectations Model of the Australian Dollar/U.S.

Dollar Market. 5/93 Xiaokai Yang & Robert Rice, An Equilibrium Model Endogenizing the Emergence of a Dual Structure

Between the Urban and Rural Sectors. 4/93 Xiaokai Yang, An Expanded Dixit-Stiglitz Model Based on the Tradeoff Between Economies of Scale and

Transaction Costs. 3/93 Sugata Marjit, On the Participation of Local Capital in a Foreign Enclave - a General Equilibrium Analysis

(published December 1993) 2/93 Sugata Marjit & Hamid Beladi, Foreign Capital Accumulation and Welfare in a Small Economy: Does

Employment Matter? 1/93 Dietrich K. Fausten, Exploratory Estimates of the Influence of Economic Activity on German Portfolio

Investment Abroad.

17/92 Blair R. Comley, The Australian Film Industry as an Infant Industry. 16/92 Yew-Kwang Ng, Complex Niches Favour Rational Species. 15/92 Yew-Kwang Ng, Population Dynamics and Animal Welfare. 14/92 Yew-Kwang Ng, Happiness Surveys: Ways to Improve Accuracy and Comparability. 13/92 Richard H. Snape, How Should Australia Respond to NAFTA? 12/92 Richard H. Snape, Background and Economics of GATTs Article XXTV. 11/92 Richard Snape, Economic Aspeas of APEC. 10/92 Richard Snape, Bilateral Initiatives: Should Australia Join? 9/92 Xiaokai Yang, The Pricing Mechanism that Coordinates the Division of Labor. 8/92 Xiaokai Yang & Jeff Borland, Specialization and Money as a Medium of Exchange. 7/92 He-ling Shi & Xiaokai Yang, A Theory of Industrialization. 6/92 Xiaokai Yang & Jeff Borland, Specialization, Product Development, Evolution of the Institution of the Firm,

and Economic Growth. 5/92 Ian Wills, Implementing Sustainable Development: Systems and Signalling Problems. 4/92 Ian Wills, Pollution Taxes Versus Marketable Permits: A Policy Maker's Guide. 3/92 Ian Wills, Do Our Prime Farmlands Need Saving? 2/92 Dietrich K. Fausten, Financial Integration and Net International Capital Movements. 1/92 John Freebaim, An Overview of the Coalition's Tax Package.

12/91 G A. Meagher, The International Comparison Project as a Source of Private Consumption Data for a Global Input/Output Model.

11/91 GA. Meagher, Applied General Equilibrium Modelling and Social Policy: A Study of Fiscal Incidence. 10/91 Dietrich K. Fausten, The Ambiguous Source of International Real Interest Difi^erentials in Integrated Financial

Markets. 9/91 Richard H. Snape, Discrimination, Regionalism, and GATT. 8/91 Richard H. Snape, The Environment: International Trade and GATT. 7/91 Yew-Kwang Ng & Jianguo Wang, Relative Income, Aspiration, Environmental Quality, Individual and Political

Myopia: Why May the Rat-Race for Material Growth be Welfare-Reducing? 6/91 Yew-Kwang Ng, Polish and Publish: The Economics of Simultaneous Submission. 5/91 Yew-Kwang Ng & He-Ling Shi, Work Quality and Optimal Pay Structure: Piece vs. Hourly Rates in Employee

Remuneration. 4/91 Bany A. Goss, S. Gulay Avsar & Siang Choo Chan, Price Determination in the U.S. Oats Market: Rational

vs. Adaptive Expectations.