Embed Size (px)

DESCRIPTION

December 2007 issue of DARE Magazine

Citation preview

Vol 1

/Is

sue

03/D

ec 0

7 /Rs 30/-

babajob.comunique idea of the month/

entrepreneur of the month/Ajay Bijli, PVR

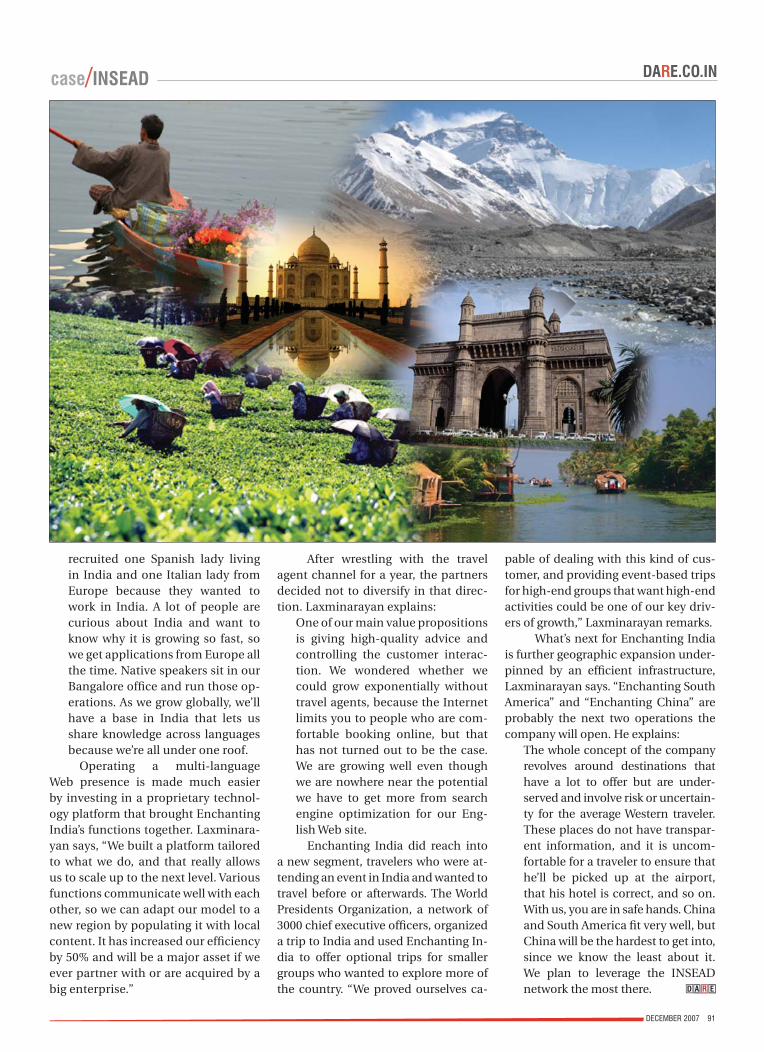

CASE STUDY -Enchanting India

Manage your team’s relationship network

How to get Angel funding

Windfall profi ts in carbon trading

5500 cr / year from parking lots

Opportunities in mobile apps

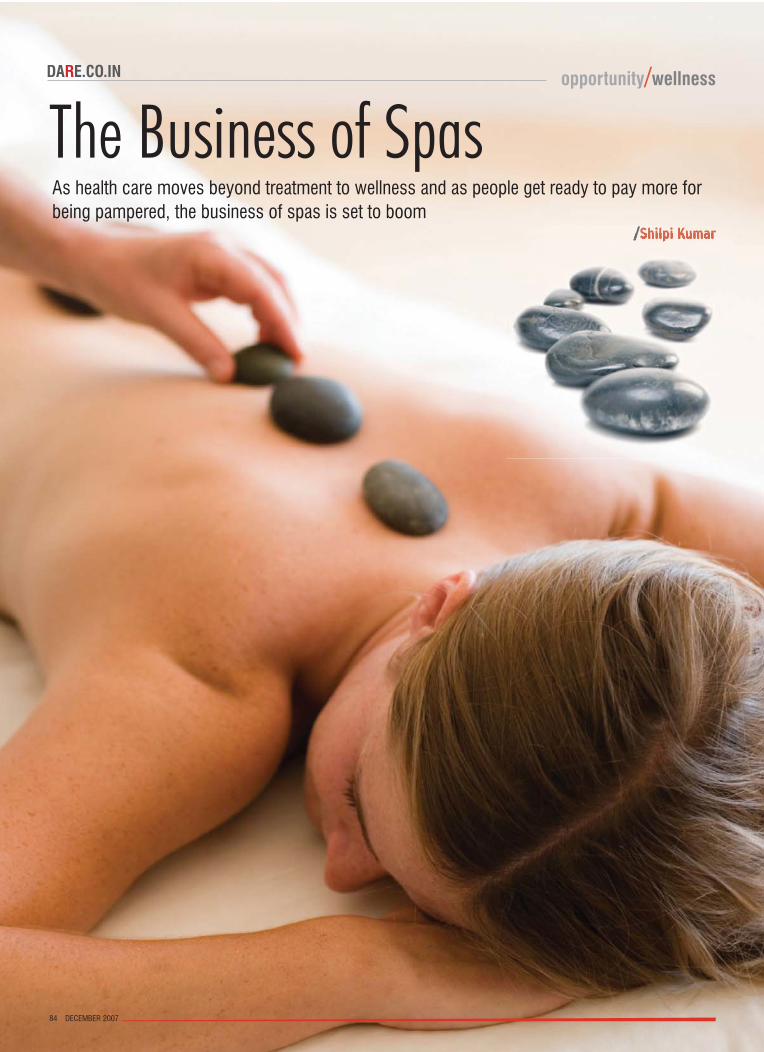

The business of Spas

apu

blic

atio

n

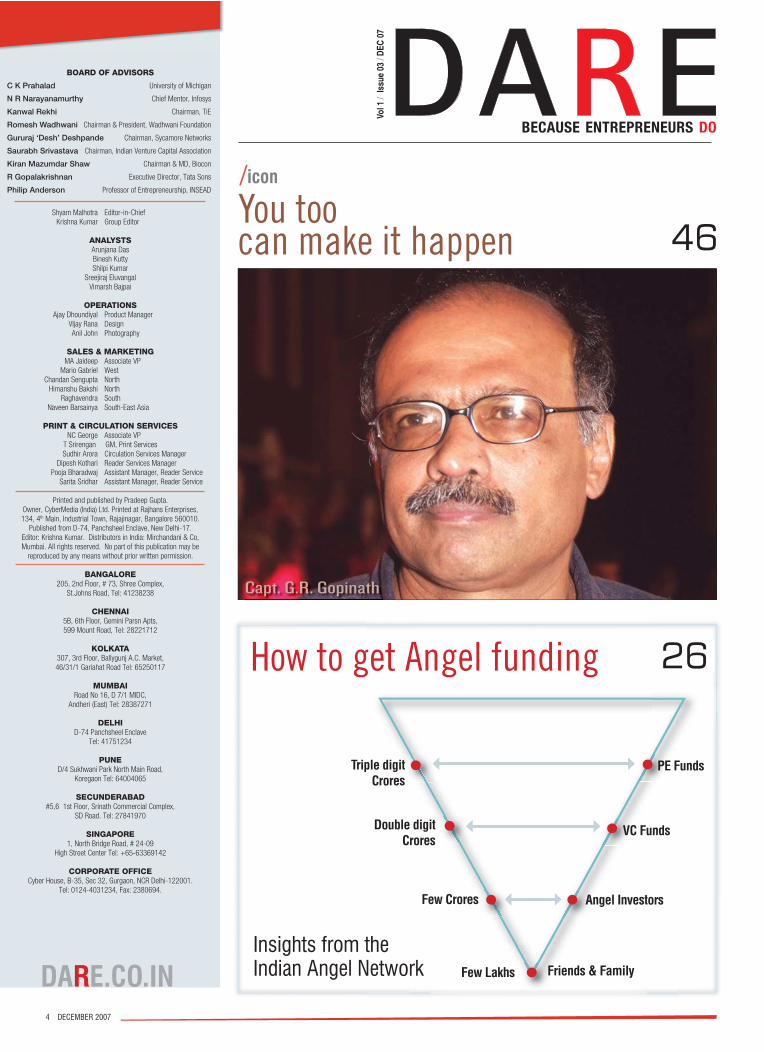

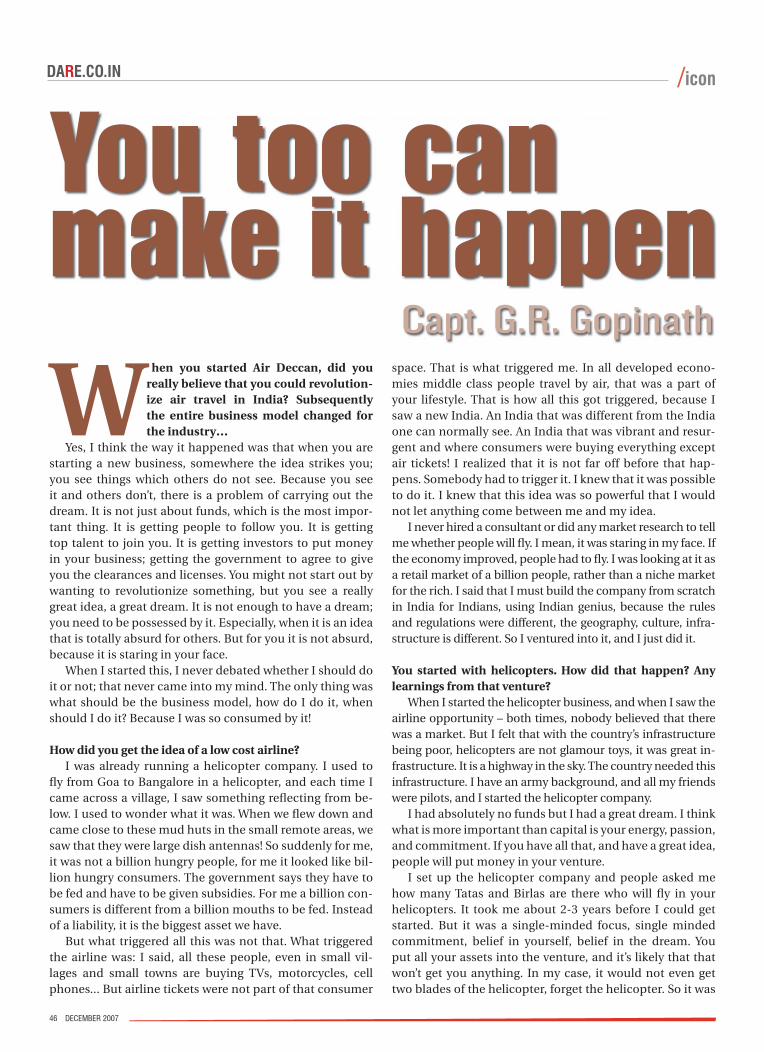

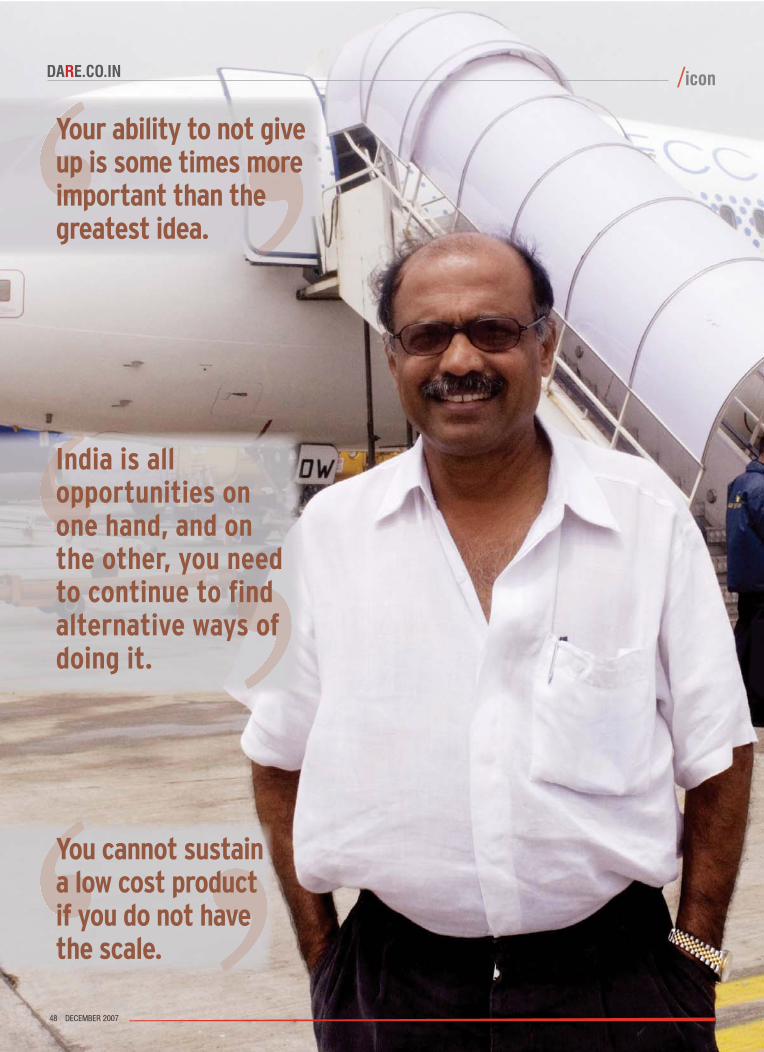

You too can makeit happen

Capt. G.R. Gopinath:

Can you win in China?Can you win in China?

Bala Deshpande, ICICI Ventureinvestor of the month/

4 DECEMBER 2007

You toocan make it happen

/icon

Shyam Malhotra Editor-in-Chief Krishna Kumar Group Editor

ANALYSTSArunjana DasBinesh KuttyShilpi Kumar

Sreejiraj EluvangalVimarsh Bajpai

OPERATIONS Ajay Dhoundiyal Product Manager VIjay Rana Design Anil John Photography

SALES & MARKETING MA Jaideep Associate VP Mario Gabriel West Chandan Sengupta North Himanshu Bakshi North Raghavendra South Naveen Barsainya South-East Asia

PRINT & CIRCULATION SERVICES NC George Associate VP T Srirengan GM, Print Services Sudhir Arora Circulation Services Manager Dipesh Kothari Reader Services Manager Pooja Bharadwaj Assistant Manager, Reader Service Sarita Sridhar Assistant Manager, Reader Service

Printed and published by Pradeep Gupta. Owner, CyberMedia (India) Ltd. Printed at Rajhans Enterprises, 134, 4th Main, Industrial Town, Rajajinagar, Bangalore 560010.

Published from D-74, Panchsheel Enclave, New Delhi-17. Editor: Krishna Kumar. Distributors in India: Mirchandani & Co, Mumbai. All rights reserved. No part of this publication may be

reproduced by any means without prior written permission.

BANGALORE205, 2nd Floor, # 73, Shree Complex,

St.Johns Road, Tel: 41238238

CHENNAI5B, 6th Floor, Gemini Parsn Apts, 599 Mount Road, Tel: 28221712

KOLKATA 307, 3rd Floor, Ballygunj A.C. Market, 46/31/1 Gariahat Road Tel: 65250117

MUMBAIRoad No 16, D 7/1 MIDC,

Andheri (East) Tel: 28387271

DELHID-74 Panchsheel Enclave

Tel: 41751234

PUNED/4 Sukhwani Park North Main Road,

Koregaon Tel: 64004065

SECUNDERABAD#5,6 1st Floor, Srinath Commercial Complex,

SD Road. Tel: 27841970

SINGAPORE1, North Bridge Road, # 24-09

High Street Center Tel: +65-63369142

CORPORATE OFFICECyber House, B-35, Sec 32, Gurgaon, NCR Delhi-122001.

Tel: 0124-4031234, Fax: 2380694.

BOARD OF ADVISORS

C K Prahalad University of Michigan

N R Narayanamurthy Chief Mentor, Infosys

Kanwal Rekhi Chairman, TiE

Romesh Wadhwani Chairman & President, Wadhwani Foundation

Gururaj ‘Desh’ Deshpande Chairman, Sycamore Networks

Saurabh Srivastava Chairman, Indian Venture Capital Association

Kiran Mazumdar Shaw Chairman & MD, Biocon

R Gopalakrishnan Executive Director, Tata Sons

Philip Anderson Professor of Entrepreneurship, INSEAD

46

DARE.CO.IN

How to get Angel funding 26

Vol 1

/ Is

sue

03 /

DEC

07

Triple digit Crores

Double digit Crores

Few Crores

Few Lakhs

PE Funds

VC Funds

Angel Investors

Friends & Family

Insights from the Indian Angel Network

Capt. G.R. Gopinath

/content DARE.CO.IN

DECEMBER 2007 5

Ajay Bijli, PVR entrepreneur of the month

No Parking! .......................................... 34Parking lots: A Rs 5,500 cr opportunity

Hiring for startups ......................76There are a number of things you can do to get the right people on board

Social Networks go local ...................... 96As networking sites prove to be a major pull for internet users, a host of Indian startups are eyeing the sector

Bala Deshpande, ICICI Venture

others/

I was very keen that my company should not become

a mom-and-pop operation. I should have a business that is something I enjoy,

and make it scalable

Windfall profi ts from carbon tradingProjects aimed at reducing pollution have now become revenue generators

case study/INSEADThis case study traces the evolution of Enchanting India, and its role in providing tailor-made travel experiences to foreign tourists

Philip Anderson ........ 20

Anurag Batra ........... 33

Rupin Jayal................... 54

blogs/columns

opportunity/

Networking for social change ............... 22Three entrepreneurs combine social networking with online job search for the benefi t of unskilled workers

unique idea of the month/

Investor of the month/

14

42

opportunity /Big Flora, Big Bucks ......................28

Get a green offi ce ..........................50

The Business of Spas ....................84

38

DARE.CO.INinteractive business models,

wiki profi les, business

graph of the day, idea pic of the day, sector spotlight, blogs,

news, discussion fora, keyword

based alerts, rss feeds, contacts,

mentoring, market trends,

webinars, newsletters, live chat,

opinion polls, leads, slideshows,

professional guidance, search, on demand,

archives, event calendar, research,

directories, faqs

campus /

coming soon

TiE /

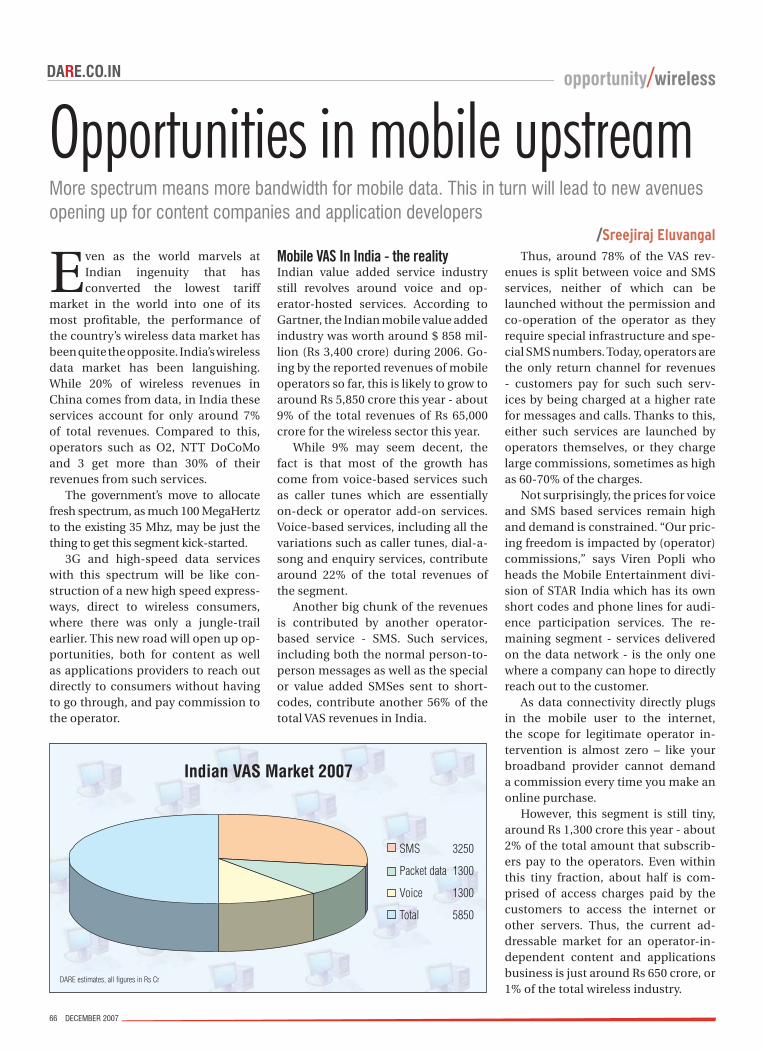

Mobile UpstreamMore spectrum means more bandwidth for mobile data. This in turn will lead to new avenues opening up for content companies and application developers

opportunity/

72

Run-up to TES 2007 ...................104

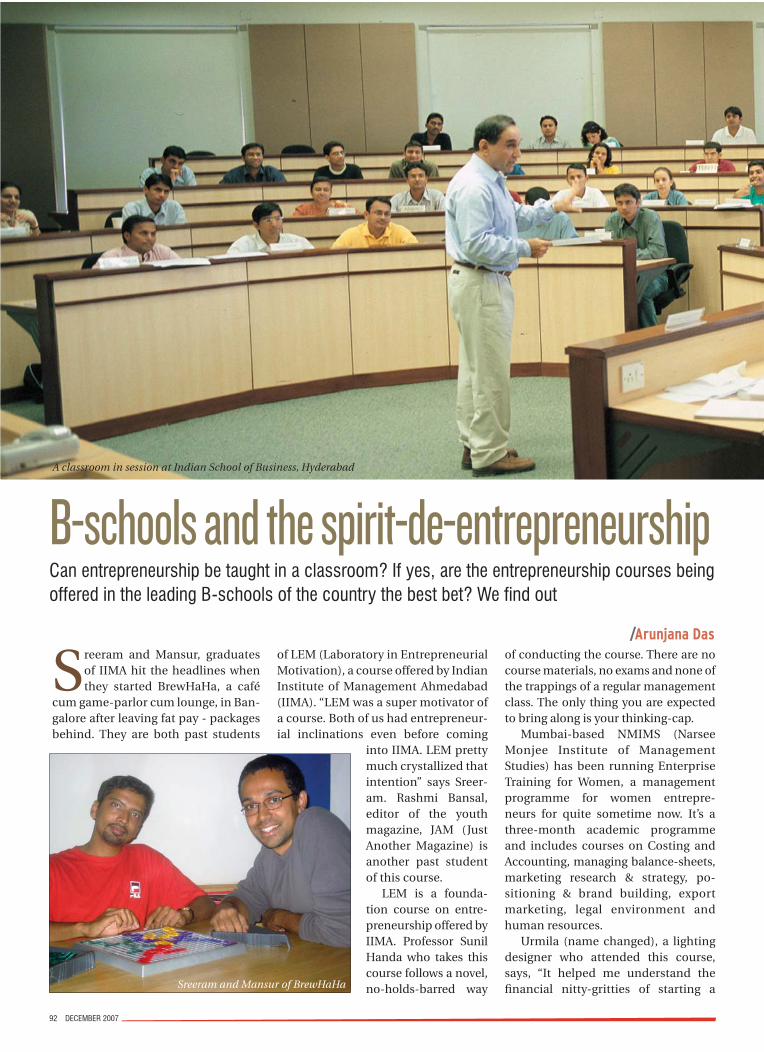

B-schools and the spirit-de-entrepreneurship ..........................92

66

When approaching us, an entrepreneur should come prepared to spend time and energy and also be very honest and open with us

DARE.CO.IN /news

8 DECEMBER 2007

newsnew

s

Medical tourism to grow to $2 bn by 2012Union Minister of Commerce &

Industry Kamal Nath has said that medical tourism has the potential to grow into a $2 billion industry by 2012. Speaking at the 4th India Health Summit on November 14, the minister said: “Large windows of opportunities

are opening up. To give just one example, Indian medical tourism was estimated at $350 million in 2006 and this has the potential to grow into a $2 billion industry by 2012”. Nath stressed on developing new infrastructure for the healthcare sector in view of the tremendous opportunities that are available for public-private partnership.

He said there were fi ve areas for government and organized industry action in the healthcare sector, i.e., to create low-cost, high-quality facilities, with a focus on underserved areas; second is to work towards creating standards for high-quality healthcare; third is to invest in training and developing healthcare manpower; fourth is to work with health insurers to improve coverage; and fi fth and most important is to create public-private part-nerships in healthcare.

According to the joint study by CII and McKinsey on this sector, Nath said: “During the 1990s, Indian health-care grew at a compound annual rate of 16%. Today the total value of the sector is more than $34 billion. This translates to $34 per capita, or roughly 6% of GDP. By 2012, India’s healthcare sector is projected to grow to nearly $40 billion”.

Revised guidelines for recognition of tour agentsThe Ministry of Tourism has said that initial recogni-

tion for all categories of travel trade viz., tour operators, travel agents, tourist transport operators, domestic tour operators & adventure tour operators shall now be given at the Headquarters for a period of fi ve years instead of three years as was given earlier. This is based on the in-spection report / recommendation of a Committee com-prising of Regional Director concerned and a member of TAAI / IATO, etc.

FDI proposals worth Rs 500 cr cleared

Finance Minister P Chidambaram has approved 22 Foreign Direct Investment (FDI) proposals worth Rs 511 crore, recommended by the Foreign Investment Promo-tion Board. The proposals are related to various minis-tries including Commerce, Food Processing Industries, and Information and Broadcasting. Some of the impor-tant proposals approved include the Rs 155.74 crore proposal of PTC India Financial Services for induction of foreign equity by Goldman Sachs and Macqarie.

There are no excuses. Your package must get from A to B on time. Period. But between A and B a lot of crazy things can happen. Precisely why we go all the way to monitor your shipment using a 24x7 track and trace system. This state-of-the-art technology allows us to proactively inform our customers in real time of any problems that may affect their delivery. It’s how our Quality Control Centre can maintain a contingency plan for every stage of delivery. And it’s why ‘fun runs’ remain just that, fun.

Contact DHL Express 24x7 at 30 300 345 & 1 800 111 345. www.allthewaydhl.com

Winner of Avaya GlobalConnect Customer Responsiveness Award 2006 in the logistics category.

ALL THE WAY

OUR LOCAL KNOWLEDGE TELLS US WHERE THETRAFFIC JAMS ARE EVEN WHEN THERE’S NO TRAFFIC.

DARE.CO.IN /news

10 DECEMBER 2007

225 TV channels allowed uplinking

The Ministry of Information & Broadcasting has per-mitted 149 news & current affairs TV channels and 106 non-news & current affairs TV channels to uplink from India, as on November 15, 2007. Five TV channels, up-linked from abroad, have also been permitted to down-link in India.

In addition to this, 52 TV channels, uplinked from abroad, have been provisionally permitted to downlink in India. The permissions are for op-eration on an all-India basis and are not State-wise. Out of the total 255 channels permitted to uplink from India, 123 channels have Indian ownership whereas 132 have varying components of foreign equity in the parent company.

Production by SSIs to grow 12.6% in 2006-07Based on the revised Index of Industrial Production

for the Small Scale Industries (SSIs) sector, with base year 2001-02, the rate of growth of production of SSIs in the country during 2004-05, 2005-06,and 2006-07 (projected) have been 10.9%, 12.3% and 12.6% respectively.

To assist the States/UTs and supplement their efforts in this regard, the Central Government implements sev-eral schemes/ programs for promotion and development of SSIs. These include facilitating availability of credit mainly through public sector banks/institutions, assis-tance for (a) technology upgradation, (b) marketing,(c) integrated infrastructural development,(d) comprehen-sive need-based development of clusters, and (iii) entre-preneurship development.

Govt for more pvt investment in renewable energyThe government is encouraging private investment in

renewable energy sector through a mix of fi scal and fi -nancial incentives that include capital/ interest subsidy, accelerated depreciation, nil/ concessional excise and customs duties, Minister of State in the Ministry of New and Renewable Sources, Vilas Muttemwar has said.

Further, as applicable to all new infrastructure proj-ects, profi ts earned from sale of renewable power are ex-empt from Income Tax for any 10 years out of the fi rst 15 years of project’s operation. This apart, preferential tariff for grid interactive renewable power is being given in most potential states. An amount of Rs 1,100 crore has been proposed to support Research and Development on different aspects of new and renewable energy technolo-gies during 11th Plan period.

Cabinet nod to export promotion scheme

The Cabinet Committee on Economic Affairs has gave its approval for implementation of a Centrally Sponsored Scheme on Marketing and Export Promotion during the 11th Five-year Plan period with an outlay of Rs 230 crore. The scheme will have two components: (i) Marketing Promotion and (ii) Handlooms Export Promotion.

Out of Rs 230 crore, Rs 205 crore has been earmarked for marketing promotion component and the balance Rs 25 crore will be for handlooms export promotion. It is expected that the marketing promotion component will benefi t more than 27 lakh handloom weavers increase their sales of products in the domestic market.

World Bank to provide $944 million support

India has signed three loan/credit agreements with the World Bank amounting to $944 million. The agreements are aimed at strengthening the Rural Credit Cooperatives Project for $600 million loan and credit; India Vocational Education Training Project for $280 million credit; and additional fi nancing for the Karnataka Community Based Tank Management Project for $64 million loan and credit.

India needs entrepreneurs to take on China

India needs more entrepreneurs to meet the challenge ahead and to take on China, Essar Group Chairman Sashi Ruia has said at the Indian Institute of Management, Ahmedabad. Even if “eight to ten” of those who gradu-ated from the IIMs would take on the challenge, it would do the country good, he said.

“Both Indians and Chinese are known for their entre-preneurship. However, the Chinese are ahead of India in producing steel, cement, cars, infrastructure and other areas,” Ruia said.

MSME growth rate higher than industrial sectorThe annual growth rate of Micro, Small & Medium En-

terprises has so far been consistently higher than that of the country’s industrial sector as a whole and their share in national exports is about 33%. The number of MSME has grown from 109 lakh in 2002-03 to 128 lakh in 2006-07 and their production has increased from Rs 3,14,850 crore to Rs 5,87,196 crore.

The government supports MSMEs through assistance for technological upgrade, accessing markets, improved infrastructure and better availability of credit. PVR to tap high-end consumers

PVR (Priya Village Roadshow) has come out with a new offering – PVR Premier, which is targeted at high-end ur-ban consumers in the metros, with premium offerings such as leather upholstered fully reclining seats and un-paralleled legroom in two Gold Class and four Premier Class auditoria.

With an investment of Rs 24 crore, the fi rst PVR Pre-mier theatre was launched recently in New Delhi.

DECEMBER 2007 11

FeedbackDARE.CO.IN

I need to confess that the entre-preneur in me was lying dormant till I picked up the fi rst issue of DARE at the Indian Magazine Congress last month. Here was a magazine which actually provoked you to take up the challenge. It made my decision of giving up a cushy and, as some people say, high profi le job so much easier.

The entrepreneur in me has wo-ken up now and I must tell you in all humility that DARE has contributed to this decision in some way. In a way which really can't be measured, but it certainly took away the ifs and buts in my thought process.

It has been a long but satisfying 11 years at Zee, the company which has made me what I am today.

I seek your blessings as I dare to be different and dare to take the plunge I have been so much waiting for.

Samir Ahluwalia,Editor, Zee Business

I have seen your statement: Solid waste management can fetch good rev-enue. I am working in the water, sani-tation and solid waste management (SWM) sector for the last 30 years.

My organization has done a study on the situation of SWM in Kerala on behalf of the World Bank. But the situ-ation is quite pathetic. There are lob-bies who are against SWM activities. These are dominated by politicians and businessmen. I would like to see the work on SWM being done by mu-nicipal corporations in India, prefer-ably in south India.

Dr K Balachandra KurupExecutive Director & Chief Executive

Socio Economic Unit Foundation, Trivandrum

Congratulations for giving a very good magazine-cum-guide for aspir-ing entrepreneurs and those in the startup stage of their business. It pro-vides tips and inspirational features that give its readers a framework for success.

Vivek DhariaCIO, KNP Sec Ltd

The organic farming and the VC funding articles made an interesting reading and the interview with Biocon lady was amazing... Thanks

Bal Govind

Hey ur magazine rocks ..its a in-formative ..attractive..n a sensible magazine with easy to understand lan-guage...good..

Deepa

Kudos to the Cyber Media team for bringing out an excellent mag for aspiring young entrepreneurs like me. wish you all the best.

Anish Achuthan

The article on VC is a real eye open-er. DARE should become a platform for exchange of entreprenurial spirit. Thumbs up DARE.

Gaurav

I am an entrepreneur and the latest issue rekindled the fi re in my belly and i have dared to think BIG.

BG Sreedhhar

Via SMS - DARE 56677

Within them, the club has the expe-rience and wisdom of more than fi ve decades of conception and execution of organic growth. The club has the sole motto of elevating SMEs in their quest for sustenance and growth.

Please visit our website www.tecin-dia.in, which will provide more infor-mation about us.

Every month we conduct program for the SME called inTECgrate with two topics.

Please fi nd enclosed the invite for the same.

I have read your DARE magazine and it is really interesting and infor-mative and that made me visit your Chennai offi ce.

K Gangadharan, Founder Trustee,The Entrepreneurs Club, Chennai

Thank you very much for sending me the fi rst issue of your magazine, which I found quite interesting. I have also received the next issue.

I would like to subscribe the same. Kindly let me know the subscription payable.

Dr R LakshmipathyPublisher, DINAMALAR

Can the next Google come out of India? Hyperbole aside, what are the real challenges of building successful and scalable technol-ogy startups in India?

Aparna, a graduate student at MIT/Sloan, is doing a research project investigating these issues. As part of her project, she is look-ing to interview entrepreneurs and India-focused early-stage in-vestors for their perspectives.

From an entrepreneur’s view, some of the issues she is exploring are -- hiring the early team, busi-ness models that have worked or not, nature of external mentors and advisers, importance of ac-cess to US entrepreneurs etc.

From an investor’s view, issues she is exploring are -- deal-fl ow challenges, relationships with incubators / angels / seed funds, ownership stake dynamics, nature and extent of portfolio company support.

To learn further or participate in the project, please write to her at [email protected].

Your subscription page does not look professional at all. India has been spelled incorrectly. Please amend that. As I am a designer, I cannot overlook these mistakes.

Anyhow, I will subscribe soon.

Sunny Kapoor

The Entrepreneurs Club is a not-for-profi t organization and registered as a trust. It is the brain child of three fi rst generation entrepreneurs.

DARE.CO.INblogs/edit

DECEMBER 2007 13

Our Performance ReportThe biggest impact we hoped to have was to infl uence people’s decisions on business. I am proud to report that it has started to happen.

Three months down the line, we thought that

like any other venture, we should take stock

of where we have reached. When we started,

we set two goals for ourselves. One was, of course, the

business plan. The other was what in my fi rst editorial,

I called “ a simple yardstick of success”. I had said: “If

even one entrepreneur will be able to say that what we

have carried, what we have done, has made him think

differently, has made a positive difference to his business

ambitions, then we have achieved our objective”

As you turn the pages, do stop for a minute at

feedback, where we carry your responses to our articles.

There you will fi nd evidence that we have made a small

but signifi cant step towards achieving this objective.

That leaves the business plan. Suffi ce to say that at

this point, we are ever so slightly ahead of the plan, both

in terms of number of copies and fi nances.

Another impact we have had, which we did not

quite expect, has been what I call the WOW- I – did-

not- know- that reaction. This has been the reaction to

our opportunity stories. For example, when we said that

downstream opportunities from corporate aircraft was

Rs 1,500 crore a year or that collecting and processing

household wastes was a Rs 6,000 crore a year opportunity,

the uniform reaction, even from established businesses

has been the same – WoW, I did not know that!

Thank you for the wonderful support you have given

us in getting going and I am sure that your support and

best wishes will be with us as we go forward.

/Krishna Kumar

blogs/edit

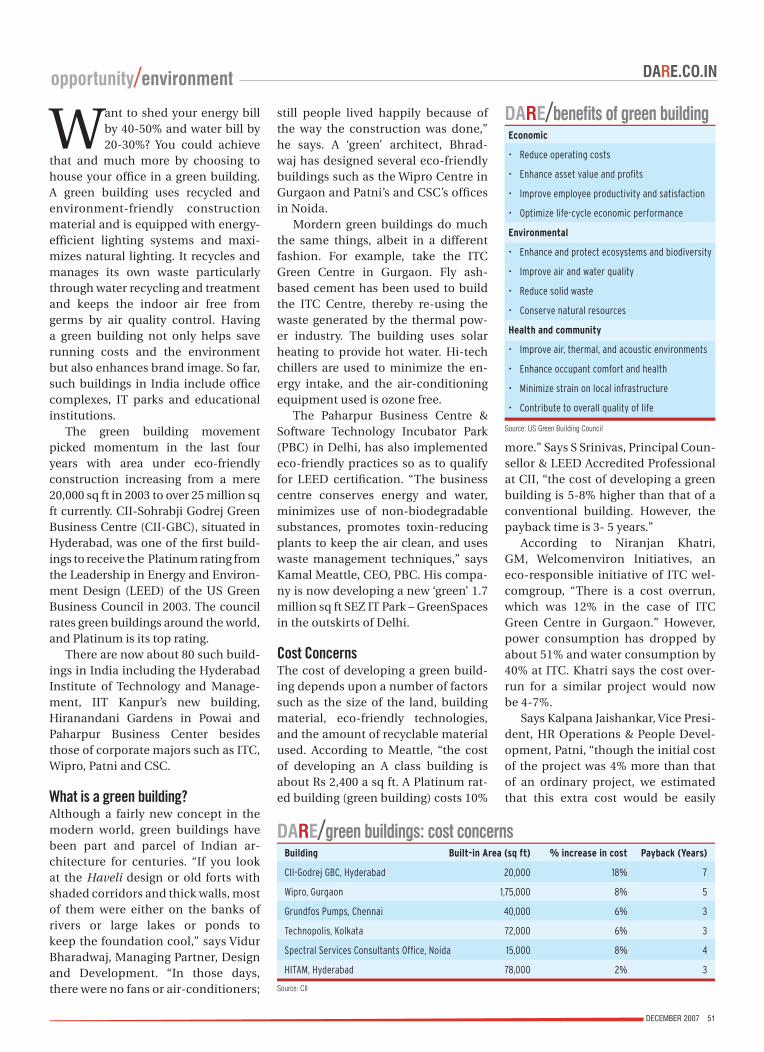

DARE.CO.IN opportunity/environment

14 DECEMBER 2007

Projects aimed at reducing pollution and mitigating climate change are no longer mere investments for a good cause. They have become revenue generators, thanks to the Kyoto Protocol, an agreement by world governments to limit dangerous emissions

/Vimarsh Bajpai

CDM Project Stages

DARE.CO.IN opportunity/environment

14 DECEMBER 2007

1. Project identifi cation

2. Preparation of project documentation applying an approved methodology for calculating emission reductions (Project Design Document)

3. Validation of project documentation by environmental an auditor accredited by Clean Development Mechanism Executive Board (CDMEB)

4. Host country approval

Windfallprofi tsfromcarbontrading

Windfallprofi tsfromcarbontrading

DARE.CO.INopportunity/environment

DECEMBER 2007 15

SRF, a refrigerant producer, took up a project in 2005 to re-duce the emission of HFC-23, a

greenhouse gas (GHG) generated as a byproduct at its factory in Bhiwadi, Rajasthan. This effort reduced the emission of 3.8 million tons of GHG every year. Good show, right? But what happened next is more of interest to us. The company traded this reduction at Euro 10 a ton of emission saved or per CER (Carbon Emission Reduction) units, earning $53.2 million a year!

At the other end of the spectrum, Karnataka-based NGO SKG Sangha has set up biogas and vermi-compost plants for 10,000 rural families in the state. This reduces carbon dioxide (CO2) emissions substantially. The NGO sells these emission savings as Voluntary Emission Reduction (VER) units directly to international buyers and not through regulatory mechanisms, thus raising money for its programs.

Welcome to the world of carbon trading, where otherwise non-remu-

Carbon Trading in a Nutshell

This is a unique trading system agreed upon by more than 170 countries in a bid to save our environment from further degradation. It is based on the premise that those who continue to pollute the environment should pay for their sins to those who make efforts to save it.

If you undertake a project to reduce pollution levels, you become eligible for selling the amount of greenhouse gas emissions saved as carbon credits. One credit equals to one ton of CO2 emission saved. Carbon credits are traded in the international market.

Credits earned through the Clean Development Mechanism are called Carbon Emission Reduction (CER) units. The process requires approval of the host country and registra-tion with the UN Executive Board. The CDM is time consuming and expensive compared to another process which generates Voluntary Emission Reduction (VER) units. VERs are tradable at climate exchanges like the Chicago Climate Exchange or sold directly to end buyers. VERs have a much lower market value than CERs.

Payments in the carbon market are made in the form of cash, equity, debt, convertible debt or warrants. Some parties pay in-kind, providing technologies to curb emissions.

nerative projects aimed at reducing pollution, specifi cally carbon dioxide and other greenhouse gases, become money-spinners. Both SRF and SKG Sangha are among the hundreds of ben-efi ciaries of the carbon trading busi-ness that Frost and Sullivan estimates to be worth $52 billion this year, and to touch $100 billion by 2010. Developing countries such as India are tapping the benefi ts of this market both through the highly regulated Clean Develop-ment Mechanism (CDM) or a more informal voluntary market.

The era of debate whether climate change is for real or not has drawn to an end and the fi ght to save environ-ment has achieved a critical mass. This year’s Nobel Peace Prize, jointly shared by climate change activist and former US Vice President Al Gore and the Intergovernmental Panel on Climate Change (IPCC), has only underscored the need to contain global warming, which if left unchecked, could cause the biggest catastrophe mankind has ever witnessed.

Opportunity: Reducing Emissions“The Clean Development Mechanism is a voluntary activity to reduce green house gas emissions and everyone is eligible whether it is a big corporate, an NGO or an individual. You become eligible if the project meets the CDM eligibility criteria,” says CDM expert Dhirendra Kumar, Group Coordinator, Winrock International. Bharti Gupta Ramola, Executive Director at PricewaterhouseCoopers feels that “early success in the CDM market has brought such projects within the investment decision-making process in a large number of medium and large corporations.”

While for Indian companies, car-bon trade has opened up a new rev-enue stream, for NGOs, this has be-come a means for making grass-root level projects self-sustaining in the long run. “We want money to imple-ment programs for poor rural women, and carbon trade has helped bring in funds," says D Vidya Sagar, President, SKG Sangha.

DARE.CO.INopportunity/environment

DECEMBER 2007 15

5. Acceptance of project by the CDMEB (Registration)

7. Verifi cation of generated emission reductions by an accredited verifi er

6. Project implementation, monitoring and reporting

8. Acceptance of verifi ed emission reductions and issuance of credits by the CDMEB (Certifi cation and Issuance)

9. End of contract period (May be post-2012)

DARE.CO.IN opportunity/environment

16 DECEMBER 2007

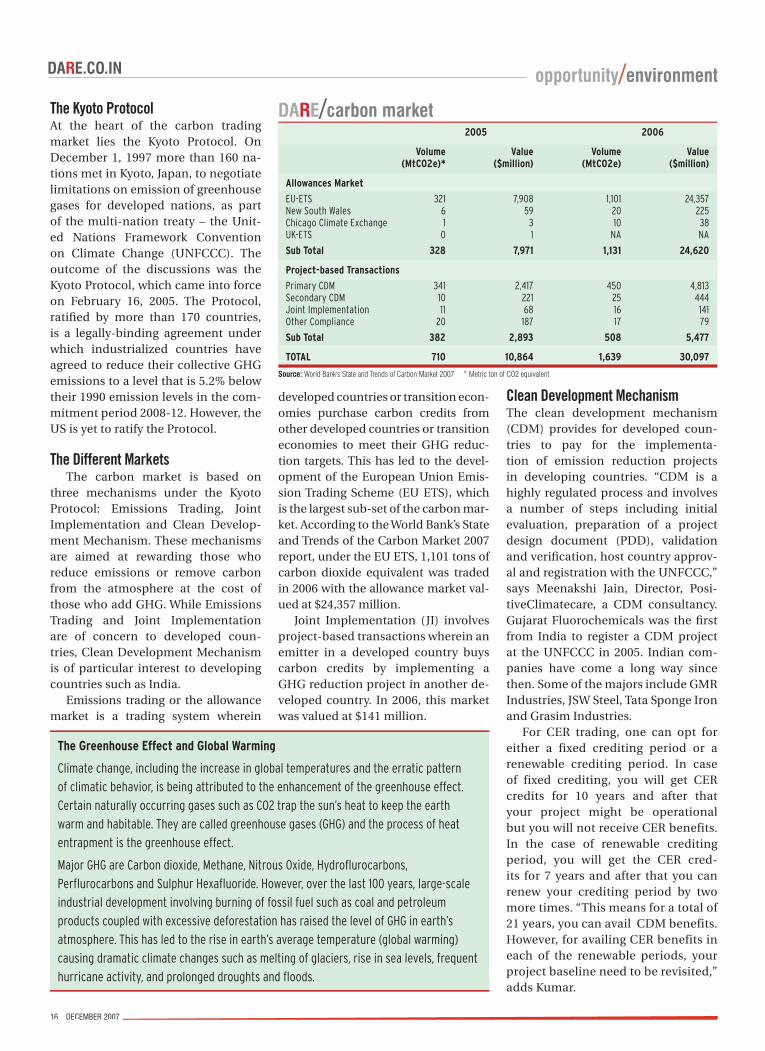

developed countries or transition econ-omies purchase carbon credits from other developed countries or transition economies to meet their GHG reduc-tion targets. This has led to the devel-opment of the European Union Emis-sion Trading Scheme (EU ETS), which is the largest sub-set of the carbon mar-ket. According to the World Bank’s State and Trends of the Carbon Market 2007 report, under the EU ETS, 1,101 tons of carbon dioxide equivalent was traded in 2006 with the allowance market val-ued at $24,357 million.

Joint Implementation (JI) involves project-based transactions wherein an emitter in a developed country buys carbon credits by implementing a GHG reduction project in another de-veloped country. In 2006, this market was valued at $141 million.

Clean Development MechanismThe clean development mechanism (CDM) provides for developed coun-tries to pay for the implementa-tion of emission reduction projects in developing countries. “CDM is a highly regulated process and involves a number of steps including initial evaluation, preparation of a project design document (PDD), validation and verifi cation, host country approv-al and registration with the UNFCCC,” says Meenakshi Jain, Director, Posi-tiveClimatecare, a CDM consultancy. Gujarat Fluorochemicals was the fi rst from India to register a CDM project at the UNFCCC in 2005. Indian com-panies have come a long way since then. Some of the majors include GMR Industries, JSW Steel, Tata Sponge Iron and Grasim Industries.

For CER trading, one can opt for either a fixed crediting period or a renewable crediting period. In case of fixed crediting, you will get CER credits for 10 years and after that your project might be operational but you will not receive CER benefits. In the case of renewable crediting period, you will get the CER cred-its for 7 years and after that you can renew your crediting period by two more times. “This means for a total of 21 years, you can avail CDM benefits. However, for availing CER benefits in each of the renewable periods, your project baseline need to be revisited,” adds Kumar.

The Kyoto ProtocolAt the heart of the carbon trading market lies the Kyoto Protocol. On December 1, 1997 more than 160 na-tions met in Kyoto, Japan, to negotiate limitations on emission of greenhouse gases for developed nations, as part of the multi-nation treaty – the Unit-ed Nations Framework Convention on Climate Change (UNFCCC). The outcome of the discussions was the Kyoto Protocol, which came into force on February 16, 2005. The Protocol, ratifi ed by more than 170 countries, is a legally-binding agreement under which industrialized countries have agreed to reduce their collective GHG emissions to a level that is 5.2% below their 1990 emission levels in the com-mitment period 2008-12. However, the US is yet to ratify the Protocol.

The Different MarketsThe carbon market is based on

three mechanisms under the Kyoto Protocol: Emissions Trading, Joint Implementation and Clean Develop-ment Mechanism. These mechanisms are aimed at rewarding those who reduce emissions or remove carbon from the atmosphere at the cost of those who add GHG. While Emissions Trading and Joint Implementation are of concern to developed coun-tries, Clean Development Mechanism is of particular interest to developing countries such as India.

Emissions trading or the allowance market is a trading system wherein

The Greenhouse Effect and Global Warming

Climate change, including the increase in global temperatures and the erratic pattern

of climatic behavior, is being attributed to the enhancement of the greenhouse effect.

Certain naturally occurring gases such as CO2 trap the sun’s heat to keep the earth

warm and habitable. They are called greenhouse gases (GHG) and the process of heat

entrapment is the greenhouse effect.

Major GHG are Carbon dioxide, Methane, Nitrous Oxide, Hydrofl urocarbons,

Perfl urocarbons and Sulphur Hexafl uoride. However, over the last 100 years, large-scale

industrial development involving burning of fossil fuel such as coal and petroleum

products coupled with excessive deforestation has raised the level of GHG in earth’s

atmosphere. This has led to the rise in earth’s average temperature (global warming)

causing dramatic climate changes such as melting of glaciers, rise in sea levels, frequent

hurricane activity, and prolonged droughts and fl oods.

DARE/carbon market 2005 2006

Volume Value Volume Value (MtCO2e)* ($million) (MtCO2e) ($million)

Allowances Market

EU-ETS 321 7,908 1,101 24,357New South Wales 6 59 20 225Chicago Climate Exchange 1 3 10 38UK-ETS 0 1 NA NA

Sub Total 328 7,971 1,131 24,620

Project-based Transactions

Primary CDM 341 2,417 450 4,813Secondary CDM 10 221 25 444Joint Implementation 11 68 16 141Other Compliance 20 187 17 79

Sub Total 382 2,893 508 5,477

TOTAL 710 10,864 1,639 30,097

Source: World Bank's State and Trends of Carbon Market 2007 * Metric ton of CO2 equivalent

Carbon Trading1.indd 16 11/29/2007 11:03:07 AM

DARE.CO.INopportunity/environment

DECEMBER 2007 17

What is the reason behind the increasing participation of Indian companies in carbon trade (CDM and the voluntary market)? Is it just money or more

than that? The possibility of additional revenue stream through CDM has played a signifi cant role in making corporations look more closely at investments in low carbon technologies. We must however salute the spirit of Indian entrepreneurs who went ahead with potential projects long before Kyoto Protocol was ratifi ed and have maintained their faith in the carbon market despite facing hurdles. Extensive capacity building (including identifi cation of project opportunities, technology, CDM fi nancing sources, etc.) done by the Indian national CDM authority, CDM service providers, CDM fi nancing agencies and CDM champions within the organisations, particularly in the case of large organisations is another facilitating factor.

How are Indian companies benefi ting from the voluntary carbon market? Indian companies are using the additional opportunity provided by the voluntary mar-kets mainly in two ways: There are a large number of “early start” projects which have missed the UNFCCC deadline for retroactive claim of CERs. Once these projects are registered with the CDM

Executive Board, they receive CERs from after the date of registration. For the period prior to registration, the emission reductions (once verifi ed) are traded in the voluntary carbon markets. For a voluntary buyer, these represent good quality emission reductions as these arise from registered CDM projects.There are various small scale emission reduction projects, which due to higher pre-registration expenditure and the long lead time as-sociated with the regulatory process, cannot afford to go through the CDM process. These projects therefore look at voluntary market.There are also cases where UNFCCC approved methodologies are not available, but the identifi ed projects have GHG reduction potential and these then choose to sell in the voluntary carbon market.

Is the future of the voluntary carbon market brighter than that of the CDM, which is a highly regulated and expensive process? Reduction in carbon footprint is a global initiative and is here to stay. The voluntary carbon market can be considered as an additional opportunity for GHG reduction. The voluntary carbon markets, which were in nascent stages until last year have now started showing signs of development because of the growing interest from both buyer and seller sides. It is true that the long and expensive CDM pro-cess may force project implementers/investors to look at the voluntary carbon market route. But this should not be seen as a compari-son between the compliance and the voluntary market. The growth and robustness of the voluntary carbon market will be inextricably linked to that of the compliance carbon market. If anything, the voluntary carbon market will supplement the compliance carbon markets but will continue to derive its depth (and systems and procedures) from the compliance carbon markets.

How can an entrepreneur benefi t from carbon trade? The scope of carbon trading is very much defi ned in the Kyoto protocol, wherein any activity carried out by the investor results in GHG emission reduction beyond the business as usual scenario or the prevailing practices in the market is eligible for CDM due diligence and registration. Out of the six identifi ed GHGs in the protocol, carbon dioxide is the most common one and is generated in almost all the industries which consume energy in one form or the other and thus energy effi ciency and process change is one of the most common type of projects which can be taken up for GHG reduction. In addition to this, switching over to alternate fuels and cleaner technologies can also result in GHG emission reductions. With new trading avenues opening up, it is always possible to trade the emission reductions in voluntary markets if not in compliance markets under the Kyoto Protocol.

BHARTI GUPTA RAMOLA,EXECUTIVE DIRECTOR,PRICEWATERHOUSECOOPERS

Tough methodologies for verifi ca-tion of the projects have been a damp-ener in getting more projects registered for CERs. “Methodologies for some projects such as those related to affor-estation are so rigorous that only one such project, in China, has so far been registered for carbon credits,” says Ashutosh Pandey, Practice Head, Emer-gent Ventures, a CDM consultancy fi rm. “There are also cases where the UNFCCC approved methodologies are not available, but if the projects have

GHG reduction potential, they can choose to sell in the voluntary carbon market,” adds Ramola.

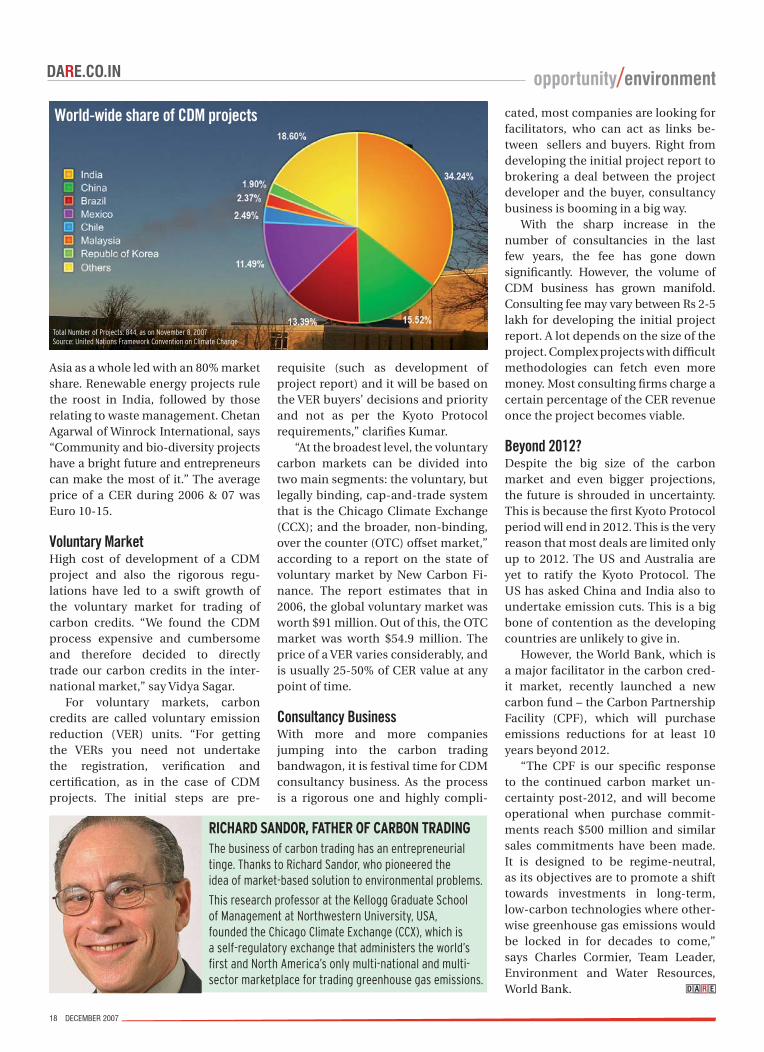

Asia dominates the seller side of the market while a majority of buyers are based out of Europe and Japan. As of November 8, 2007, a total number of 844 projects have been registered with the UNFCCC, out of which India led the pack with 288 projects, followed by China and Brazil. But despite hav-ing the maximum number of projects registered under the CDM, India lags

behind China on the number of carbon credits issued to it. “This is because most of the projects in China curb emissions of HFC, which is a more potent gas compared to CO2. This fetches more CERs,” says Pandey. Ac-cording to the World Bank report on State and Trends of Carbon market, in 2006, China dominated the CDM mar-ket on the supply side with a 61% mar-ket share of volumes transacted, down slightly from 73% in 2005. Next was In-dia at 12%, recovering from 3% in 2005.

DARE.CO.IN opportunity/environment

18 DECEMBER 2007

requisite (such as development of project report) and it will be based on the VER buyers’ decisions and priority and not as per the Kyoto Protocol requirements,” clarifi es Kumar.

“At the broadest level, the voluntary carbon markets can be divided into two main segments: the voluntary, but legally binding, cap-and-trade system that is the Chicago Climate Exchange (CCX); and the broader, non-binding, over the counter (OTC) offset market,” according to a report on the state of voluntary market by New Carbon Fi-nance. The report estimates that in 2006, the global voluntary market was worth $91 million. Out of this, the OTC market was worth $54.9 million. The price of a VER varies considerably, and is usually 25-50% of CER value at any point of time.

Consultancy BusinessWith more and more companies jumping into the carbon trading bandwagon, it is festival time for CDM consultancy business. As the process is a rigorous one and highly compli-

cated, most companies are looking for facilitators, who can act as links be-tween sellers and buyers. Right from developing the initial project report to brokering a deal between the project developer and the buyer, consultancy business is booming in a big way.

With the sharp increase in the number of consultancies in the last few years, the fee has gone down signifi cantly. However, the volume of CDM business has grown manifold. Consulting fee may vary between Rs 2-5 lakh for developing the initial project report. A lot depends on the size of the project. Complex projects with diffi cult methodologies can fetch even more money. Most consulting fi rms charge a certain percentage of the CER revenue once the project becomes viable.

Beyond 2012?Despite the big size of the carbon market and even bigger projections, the future is shrouded in uncertainty. This is because the fi rst Kyoto Protocol period will end in 2012. This is the very reason that most deals are limited only up to 2012. The US and Australia are yet to ratify the Kyoto Protocol. The US has asked China and India also to undertake emission cuts. This is a big bone of contention as the developing countries are unlikely to give in.

However, the World Bank, which is a major facilitator in the carbon cred-it market, recently launched a new carbon fund – the Carbon Partnership Facility (CPF), which will purchase emissions reductions for at least 10 years beyond 2012.

“The CPF is our specifi c response to the continued carbon market un-certainty post-2012, and will become operational when purchase commit-ments reach $500 million and similar sales commitments have been made. It is designed to be regime-neutral, as its objectives are to promote a shift towards investments in long-term, low-carbon technologies where other-wise greenhouse gas emissions would be locked in for decades to come,” says Charles Cormier, Team Leader, Environment and Water Resources, World Bank.

RICHARD SANDOR, FATHER OF CARBON TRADINGThe business of carbon trading has an entrepreneurial tinge. Thanks to Richard Sandor, who pioneered the idea of market-based solution to environmental problems.

This research professor at the Kellogg Graduate School of Management at Northwestern University, USA, founded the Chicago Climate Exchange (CCX), which is a self-regulatory exchange that administers the world’s fi rst and North America’s only multi-national and multi-sector marketplace for trading greenhouse gas emissions.

Asia as a whole led with an 80% market share. Renewable energy projects rule the roost in India, followed by those relating to waste management. ChetanAgarwal of Winrock International, says “Community and bio-diversity projects have a bright future and entrepreneurs can make the most of it.” The average price of a CER during 2006 & 07 was Euro 10-15.

Voluntary MarketHigh cost of development of a CDM project and also the rigorous regu-lations have led to a swift growth of the voluntary market for trading of carbon credits. “We found the CDM process expensive and cumbersome and therefore decided to directly trade our carbon credits in the inter-national market,” say Vidya Sagar.

For voluntary markets, carbon credits are called voluntary emission reduction (VER) units. “For getting the VERs you need not undertake the registration, verifi cation and certifi cation, as in the case of CDM projects. The initial steps are pre-

D A R E

World-wide share of CDM projects

Total Number of Projects: 844, as on November 8, 2007 Source: United Nations Framework Convention on Climate Change

25 years ago, India’s first IT magazine, Dataquest, was born.And that started CyberMedia’s journey as a specialty mediahouse dedicated to the knowledge industries. Our 15 publications, 12 websites, 100+ events, weekly TV programs, market research and media services are a testament to that.As India moves on its journey to become the knowledge capital of the world, CyberMedia will be at the forefront.Catalyzing the knowledge industries.

KNOWLEDGE

20 DECEMBER 2007

DARE.CO.IN blogs/INSEAD

An entrepreneurial team needs a lot of resources to launch a successful

business—money, ideas, em-ployees, infrastructure, custom-ers and so on. Most of these are acquired with the help of other people, so perhaps the most im-portant resource on which all others depend is your human

relationships. Who will help you? Who will make introduc-tions for you? Who will share with you useful information that you didn’t already know? Answers to questions like this help you fi gure out how much social capital you can use in order to grow your enterprise.

Few of us start businesses alone, so what matters is the total social capital of a venture’s top management team. INSEAD entrepreneurship professor, Bala Vissa, has spent years studying how successful teams use their social networks to leverage a young business, mostly using data gathered in India. In this month’s column I will share his key fi ndings with you and his advice on how to get the most out of your team’s web of social connections.

Professor Vissa started off asking under what conditions a team’s networks were, as a whole, worth more than the sum of the individual networks. To address this question, he studied 85 top management teams of young software companies from various regions in India, identifi ed with the help of NASSCOM and The Indus Entrepreneurs (TIE). He focused on one industry at fi rst, because the way people network often depends on the nature of the industry they occupy.

Professor Vissa was somewhat surprised to fi nd that different teams had very different patterns of social ties. In many teams, all the members were connected only to people who were very similar to themselves in terms of age, occupation, and social background. This is not uncommon, he says, because people tend to be most comfortable getting to know others who are like themselves. But the teams with the highest revenue growth were different: their members reached out to a very diverse web of people, many of whom were quite different from anyone on the team. Professor Vissa’s fi rst lesson for entrepreneurs: make the effort to build relationships with people who aren’t like you or anyone else in your venture’s top management. Look for people

Winning teams share a clear vision of what their business is all about/Philip Anderson

Manage your team’s relationship network

who are different in terms of age, area of expertise, and geographic location, and get to know people at companies with different positions in the supply chain, e.g. vendors, partners and customers.

Delving more deeply, he found that the teams who made the most effective use of their networks shared one thing in common: they shared a clear vision of what their business was all about and what were their key priorities going forward. That helped them agree on who to connect with, what data to share with outsiders, and what was worth learning from them. If each member of the management team explains in a different way to outsiders what the company does and what kind of help or information it needs, the team ends up with jigsaw puzzle pieces that don’t fi t together into a bigger picture. Only when they agree on their future direction and what kind of business they want to become can they pool ideas from many different sources and derive sensible insights. If they don’t agree, then data from different sources confl ict too much, creating confusion.

Is camaraderie and esprit de corps a good thing for a ven-ture team to build up? Professor Vissa’s research suggests that the answer is “maybe.” If a team contains a complete set of skills, such cohesion helps them get more from their relationships. But when there isn’t much diverse expertise in a team—for example, when everyone on the team has a technical background—they all tend to reach out to the same set of people. It’s easy to build cohesion in such cases, but different team members tend to keep reaching out to the same people, hearing the same stories, and reaching the same conclusions. They end up in too much of a comfort zone and never seem to build the diverse set of relation-ships they need in order to be exposed to new ideas, new people, and new opportunities. Instead, the same advice and the same information keeps re-circulating, and people fool themselves into believing that what they are learning from the outside world is consistent and logical, when actu-ally it only seems coherent because it comes from a narrow range of sources.

Diverse teams tend to have diverse social networks, but they also tend to have more confl ict because different people have different points of view, steeped in their different functional backgrounds. That’s why the best entrepreneurial teams combine people who have dissimilar expertise and backgrounds, but who pull together because

DECEMBER 2007 21

DARE.CO.INblogs/INSEAD

they are truly committed in spirit to one another and to their shared enterprise.

Professor Vissa then turned to examining how successful entrepreneurial team members manage to build useful networks. Even if you know that you should build a diverse set of relationships, it’s not clear how to do it or why some people are better than others at creating effective social relationships. In-depth interviews suggested that most people adopt one of two different networking styles: relational and transactional. Entrepreneurs who have a relational style typically reach out to a lot of new people and fi nd out a lot about the new people they meet, because they are interested in establishing a relationship. They are very good at converting professional relationships to personal relationships, and they are also very good at culling relationships, reducing their investment of time and energy in connections that are not mutually benefi cial. Those who have a relational style make a point of staying in touch with their contacts periodically, whether or not they need anything specifi c, to see what is new and to refresh the connection.

Entrepreneurs who have a transactional style differ in every one of these aspects. They typically reach out to a much smaller number of new people, preferring to spend time with those already familiar to them. They typically don’t fi nd out very much about new people they meet, be-cause they are focused on learning how those people can be useful to them. They tend to keep professional and personal relationships separate, and seldom thin down the number of ties they are maintaining. They typically get in touch with the people they know only when they have a specifi c reason to do so.

Because these two styles are so different, they affect the way entrepreneurs search for new customers, partners, vendors, or investors. When members of an entrepreneur-ial team have a transactional style, they gain new custom-ers or alliance partners by relying heavily on referrals from people they know. In contrast, people with a relational style are much more willing and able to strike up relationships when they encounter strangers. They have learned over time to be confi dent in their success forming new relation-

ships, so referrals are less important to them. Understand-ing your own style and that of your partners in an entrepre-neurial venture as well as the style of people you encounter, is key to ensuring that a team ends up with a diverse and helpful web of social ties, Professor Vissa suggests.

What should you do to get the most out of your team’s network? INSEAD’s Vissa offers four concrete pieces of advice.1. Reach out to people who have similar (or better) expe-

riences and accomplishments as you, not people who have the same social background you have. Networking with other successful entrepreneurs as opposed to other people from the same region that you hail from, usually produces better results.

2. Use a long time horizon; make sure you stay in touch with people whose help you might not need until well in the future. Don’t drop out of touch with people just because you don’t need their assistance or advice in the next 90 days.

3. Reach out to people who are both younger and older than you. Most people spend the great majority of their time with others who are about the same age. Older people are sources of sound advice while younger peo-ple are more attuned to what’s new and are better sourc-es of really novel ideas.

4. Finally, delegate enough of your operational tasks so you have time to reach out to new people to develop your business. Remember, your personal network today will likely become your venture’s network six months down the road.

When an entrepreneurial team comes together to grow a business, it’s easy to spend so much time thinking about products, markets, competitors, fi nancing, and other concerns that one neglects the resource that underpins all other resources: people. It’s a good idea to assess how the networks of your team members overlap so that you can get more resources from your overall web of connections than you would if every member of your team pursued the same relationships using the same style. D A R E

INSEAD Alumni Fund Professor of Entrepreneurship, Director, Rudolf and Valeria Maag International Center for Entrepreneurship and Director, 3i Venturelab

SMS “DARE <your comments, questions or suggestions>” to

56677

DARE.CO.IN /unique idea of the month

22 DECEMBER 2007

Sean Blagsvedt was working at Microsoft’s Research Labs in Bangalore two years ago when

he came across a research paper by professor Anirudh Krishna of the Duke University on the causes of poverty and its alleviation. Having moved to India when Microsoft was setting up the Lab in 2003, Sean’s job at the time consisted of communicating the ideas put out by the Ph.D researchers at the Labs to the company’s product team for implementation. But it was Krish-na’s paper that left the deepest impres-sion on Sean.

“I came to India because the move offered the chance to set up an orga-nization from scratch, with a great charter: to build applications for poor people,” says this 31-year-old from Oakland in the US. While Sean did fi g-ure out ways to convert some of the work done by the researchers at the labs into actual products, it was Krish-na’s ideas that, after a year-and-a-half, led him to quit his job and start his own venture - babajob.com.

Started three months ago, babajob offers users the opportunity to fi nd a new cook, gardener, driver, nanny, maid, offi ce boy etc. from the com-fort of their home. While mainstream sites like naukri.com and monster.com cater to the educated workforce, babajob tries to bring the benefi ts of the internet to the “sub 10k” job-mar-ket. “Nobody was paying attention to the market because the prospective employees - maids, drivers, garden-ers - did not have access to computers and the internet and could not register themselves online,” Sean points out. “Yet, this was a huge under-served market... (it is) nearly 50% of the job market?” he wonders.

While the opportunity and the as-sociated problem was obvious, Sean,

Three entrepreneurs combine social networking with online job search for the benefi t of unskilled workers

/Sreejiraj Eluvangal

Netwoking for social changewho always had a thing for “mass”, scalable ideas, had got a valuable in-sight from Krishna’s research paper. The paper was based on a four-month-long study of people falling into and getting out of poverty in 35 villages in Rajasthan and put out a set of conclu-sions on how people, given the right environment, emerged out of poverty by themselves.

“The study basically said that the key to rising out of poverty was diver-sifi cation... that one of the members of the family had got a job, usually in a city. And the information about these jobs came through connections - you got a job because you knew someone who knew someone who knew of the job.. “ he explains.

It is this insight which forms the core idea of babajob. In its revenue

model, babajob too is based on the principle of the recruiter paying, while the job-seeker gets a free listing, like the other job portals. However, un-like the mainstream recruitment sites, babajob could not expects its prospec-tive job-seekers -- maids, drivers and gardeners -- to fi ll out forms and sign up on the net.

“On the one hand, information about job opportunities was crucial for these people, yet they could not be brought into the net because of problems like access to PCs, low lit-eracy levels etc.,” points out Sean. It was then that Sean, along with Vibhore Goyal, a 26-year-old programmer from the Labs who joined him in the ven-ture, decided to use one of the most widespread phenomena online, social networking, to solve the problem.

VIBHORE GOYAL, CTOPrior to Babajob.com, Vibhore worked as a developer for Microsoft Research India on a variety of projects. Vibhore’s areas of interest include Security & Networking and he holds a B. Tech. + M. Tech. in Electrical Engg. from IIT Bombay.

IRA WEISE, MDIra has founded a variety of companies as an experienced entrepreneur over the last 25 years, including 800-Software, one of the US’s fi rst mail order software companies, and the fi rst to offer free technical support and toll free order lines.

DARE.CO.IN/unique idea of the month

DECEMBER 2007 23

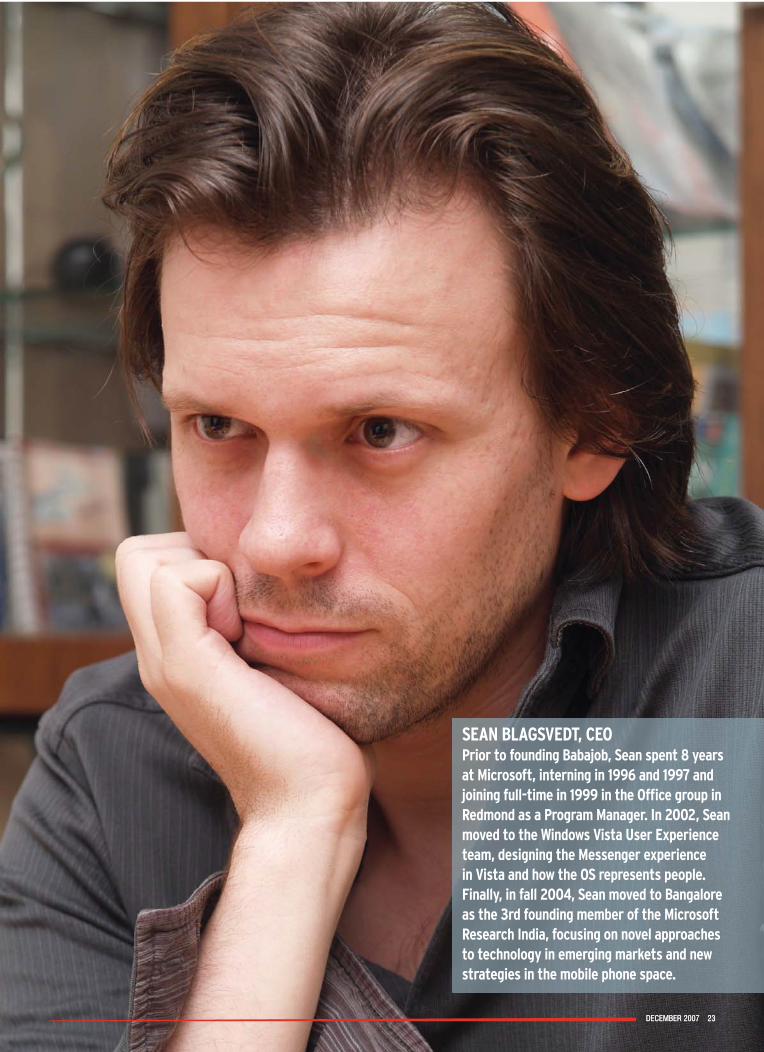

SEAN BLAGSVEDT, CEOPrior to founding Babajob, Sean spent 8 years at Microsoft, interning in 1996 and 1997 and joining full-time in 1999 in the Offi ce group in Redmond as a Program Manager. In 2002, Sean moved to the Windows Vista User Experience team, designing the Messenger experience in Vista and how the OS represents people. Finally, in fall 2004, Sean moved to Bangalore as the 3rd founding member of the Microsoft Research India, focusing on novel approaches to technology in emerging markets and new strategies in the mobile phone space.

DECEMBER 2007 23DECEMBER 2007 23

DARE.CO.IN /unique idea of the month

24 DECEMBER 2007

“We realized that tying it up around a social networking site would give us two advantages,” says Sean, “One was that all the members of the network could act as the last mile access for the less privileged job-seekers to the in-ternet, suggesting them and fi lling in their forms. Second is that it also solved another problem - that of trust. When it comes to household workers, people tend to prefer employ someone rec-ommended by someone within their friends-circle. So, social networking plus employee recommendation tied in very well,” he says. So Sean, along with Vibhore, built a social networking site - babalife, to go along with babajob.

Sean and stepfather Ira Weise have funded the project so far. Ira, a 58-year-old, is the veteran of three companies and brings his managerial experience to the team. “He was retired and was into remodelling houses with my mom when I pulled him in,” he smiles.

His third partner, Vibhore Goyal came from the Labs. He was taken into Sean’s team after being recommended to Microsoft as a “good hacker” by peo-ple at IIT Bombay and writes most of the code for the platform. Vibhore has brought to babalife a robust set of fea-tures like with customizable friendship levels, making it on-par with the best in the business as far as the technology is concerned.

The site has been on the beta mode so far, with around 70 low-skilled work-ers already placed and a data-base of around 1700 job-seekers. The plat-form gives free access to the database to potential employers. However, after browsing through the list of job-seek-ers, if they want to contact anyone of them, they will have to pay Rs 500 per job opening, plus a refundable deposit of Rs 300.

To encourage people to recom-mend and register job-seekers and potentially spinning off a new class of entrepreneurs, babajob pays Rs 200 to the person who fi lled up the details of anyone selected by an employer. As of now, it has made aware a handful of cy-ber-cafes in and around Indira Nagar of the potential earning opportunity and redirects many of its job-seeker

inquiries to such places. In addition to rewarding the persons and agents who fi ll up the forms, it also pays Rs 100 to anyone who refers a job-seekers to babajob. Both strategies are tailored to get around the handicap of the low-skilled workers’ twin handicaps - lack of awareness about online opportuni-ties and when aware, lack of access to the medium.

With the pay-out or shared model, Sean sees the platform growing into more than just an online phenome-non, with benefi ts being shared by the downstream partners such as cyber-ca-fes and fi eld workers. “Internet is just an aspect of it.. perhaps the interface with the ultimate customer. But a lot of oth-er things are required to make it work. For example, it depends on telephone connectivity, because the job-seeker has to be accessible to a potential em-ployer. Also, once someone becomes aware of babajob, he must be provided assistance to get himself registered,” he

points out.Since the jobs are usually in-house,

the need for security and trust-worthi-ness limits babajob’s ability to directly reach out to job-seekers and sign them on. The fi rm, however, has a fi eld staff of around 6 people who distribute fl i-ers and cards and try to get around the diffi culty of getting known people by maintaining a list of former employers and other references.

Sean feels building a well referenced job-seeker database is going to be his biggest challenge, not getting people to pay Rs 500 to hire someone. “We have only around 1,700 people now... I am waiting for the day when we can have at least 5,000 potential employees and then go to market and say, yes, I have so many people that you can hire..”

The site is currently in beta mode, with employer charges waived off. “I don’t think fi nding enough people willing pay Rs 500 to hire someone is going to be the problem. There are

DARE.CO.IN/unique idea of the month

DECEMBER 2007 25

many people, especially those who have shifted into the city from outside, desperately trying to fi nd someone to take care of their child or their old par-ents,” he points out, “Even now, when we have written on the website that it is

free, around 100 out of the 750 employ-ers who registered with us have paid.”

Presently, the three owners - Sean, Ira and Vibhore - do not draw salaries, while the remaining operations cost around Rs 2 lakh a month. Having been with Microsoft for eight years, Sean is depending on his savings to see the company through, besides some help from Ira. He has also sold his house in the US recently and expects the month-ly expenditure to stabilize around Rs 5 lakh after he recruits more people to spread the word.

Meanwhile, media coverage has en-sured that people from far fl ung corners of Bangalore are trying to get employees from the database, even as the database is still being formed. Sean says they have said no to external funding offers so far, including from many of the top VCs and angel investors in the country. “If it’s just money, then we don’t need it now... So, I ask them, why is your money better than ours?” he says.

While it is too early to talk of lessons learnt, Sean says the project is fi nding it

diffi cult to cope with the expectations raised. “We thought we could do one neighborhood at a time, but that was a mistake.. it is diffi cult keep things to a neighborhood on the internet,” he jokes, “We have had people from

London calling us and ask-ing, when are you coming to London!”

As of now, everybody is waiting to see what happens as site shifts into the pay mode by late November. Sean and Vibhore are also working

on creating babajob applications that will run on top of other social network-ing sites such as Orkut and Facebook, to take advantage of the large user-base that these platforms offer.

“I would say there is another six months before we fi nalize the business model, there are still some experiments to be done to see what works and what doesn’t. But I would be very dis-appointed if we haven’t expanded it to at least three more cities by then,” Sean predicts. D A R E

Sun Startup EssentialsJumpstart your Startup

For more information log on to:http:/in.sun.com/startup© 2007 Sun Microsystems, Inc. All Rights Reserved. For information on Sun's trademarks see: http://www.sun.com/suntrademarks. All other trademarks mentioned in this document are the property of their respective owners.

DARE.CO.IN funding/angel

26 DECEMBER 2007

It is unlikely that not too many have heard of Angel investing. For starters, the monies involved

are nowhere near as large as in VC or PE investing. Nor are the com-panies themselves large. And most Angels are individual entrepreneurs themselves who have made it good. Some are senior executives in large organizations.

For an entrepreneur starting a business, an Angel is the second port

of call, after you have used up your own and family funds (what they call friends, family and fools funding) and before you approach a VC. Typically, Angel investments are in the region of one to two million dollars and an Angel offers much more than funds – they offer you expertise and access to their networks and are also more involved in your day to day operations than VCs and PE funds.

Projects that are refused by VCs

as being too small for their portfolio would be better off getting Angel funding and reaching the right size to approach a VC.

There are also cases of more than one Angel investor getting together to invest in a company.

The Indian Angel Network is perhaps the fi rst organization of Angels in the country. We spoke to Padmaja Ruparel, Vice President of the network to understand how Angel investing works.

How to get Angel fundingfor a startup

Triple digit Crores

Double digit Crores

Few Crores

Few Lakhs

PE Funds

VC Funds

Angel Investors

Friends & Family

DARE.CO.INfunding/angel

DECEMBER 2007 27

Could you give us a brief idea about the Indian Angel Network; what it does?

Indian Angel Network is the fi rst and largest Angel network in India. IAN brings together successful entrepreneurs and CEOs who would like to invest in early stage companies and create disproportionate value for all the stakeholders. The members make fi nancial investments, but also provide strategic thinking and leverage their networks for the investee companies.

What are the network’s activities?Our activities revolve around investing. We source and

vet deals and prepare them for presentation to the angels. The entrepreneur gets value from each interaction with the Network - be it the Secretariat or members. The vetting of propositions and reviewing the business model and strategy is done by the investor members themselves. This is invaluable as members, who are domain leaders, provide direct feedback and suggestions to entrepreneurs during the vetting process. IAN then hand holds entrepreneurs right through the investment process as well as any other help that the entrepreneur may want, post investment.

How does one become an Angel? Is it just by giving money to some entrepreneur?

The members of the Network have had prior entrepreneurial and/or strong operational experience that they wish to bring to early stage businesses. They share a passion to enable more early stage businesses to create scale and value. The Network believes that early stage businesses require more than just money to succeed. They require close mentoring and inputs on strategy as well as

execution. The success rate of early stage businesses can signifi cantly be enhanced if such guidance is available on a constant basis. Hence the network members collectively commit not just money, but also their time and expertise to investee companies. New members are proposed by existing members and membership is by invitation.

How does an entrepreneur identify an Angel to approach? What would the Angel need to know before investing?

An entrepreneur can approach the Indian Angel Network which connects him to this leading group of Angels. IAN members would need to know have a complete understanding of the business proposition, the potential and scalability of the product and service, the entrepreneurial team, the market targeting, client acquisition and retention strategies, delivery model, risks and how they would get mitigated and the overall business model.

What returns are typically expected from Angel investment?

Angels expect far higher returns than other investment options that are available in the market. As this is high risk - high gain investment for the Angels, they will expect a return which is much higher than other investment instruments (like real estate, mutual funds, public equity, etc)

What is the normal investment period? What are the exit options?

Usually Angels remain invested for about 3 to 5 years. Angel invested companies usually go in for a second round of funding or get merged with larger companies, which is when angels exit.

PADMAJA RUPARELVICE PRESIDENTINDIAN ANGEL NETWORK

DECEMBER 2007 27

D A R E

opportunity/ideaDARE.CO.IN

28 NOVEMBER 2007

Big Flora, Big BucksFloriculture exports sector is set to touch Rs 700 crore by 2010. Huge government subsidies, diverse geo-climatic conditions and a dearth of big players; the equation is perfect for your entry

/Arunjana Das

Sipping champagne on the French Riviera, you contemplate the huge bouquet of fresh fl owers that has

been arriving with room service every single morning of your French holiday. “What exotic beauties!” you think. Lit-tle would you know that those roses and chrysanthemums were grown virtually in your own backyard! Yes. France hap-pens to be just one of the many coun-tries to which India exports its fl oricul-ture products.

The message is simple. The world is saying it with fl owers; and India has a part to play.

The fl oriculture export market in India, which stands at around Rs 400 crore, is projected to grow upto Rs 700 crore by 2010. Floriculture is a broad term used for a wide range of fl ower products such as cutfl owers, fl owering and ornamental plants, bulbs, tubers, corms, rhizomes, chicory, orchids, mosses etc. Amongst these, cutfl owers

comprise the majority of fl oriculture exports, nearing 72% of the total value. Cutfl owers—both fresh and dried—command the maximum demand in the global export market. Its worldwide demand is growing at a rate of 6-10% per annum. Developed countries in Europe, the US, Japan, Singapore and Australia are the major importers since climatic conditions in these countries are unfavorable to year-round produc-tion of fl owers.

This leaves us with a wide fi eld to play in with many factors in favor. Good quality soil, suitable climate, abundant water supply, low labor cost and proximity to markets are a few of these. Given all this, it’s a pity that the number and size of the players in this segment have been pathetically small. And most of the players are unorganized small fl ower growers.

If you can afford to holiday on the French Riviera, you can surely start off a

fl oriculture-export chain. With an initial investment of around Rs 10-15 crore a unit and earnings many times over, it is a wonder that you haven’t started already!

The prospects are green, which explains why the government of India is doing its bit for this business. To promote fl oriculture exports in the country, it has given 100% export status to fl oriculture and provides several tax benefi ts to EOUs.

Under the Seed Policy announced in 2002, import of seed and plant ma-terial has been made duty-free, subject to EXIM guidelines. The Agricultural and Processed Food Products Export Development Authority (APEDA), established in 1986, grants subsidies for establishing cold storage, pre-cool-ing units, refrigerated vans and green houses and provides air freight subsidy for exports. It assists growers/ export-ers in improving the quality of fl owers and promotes effi cient post harvest measures, packaging and quality-up-gradation.

Why has organized fl oriculture not taken off in a big way? The reasons are many. Firstly, it is a capital intensive game. Secondly, it requires technical know-how. Thirdly, there is a lack of appropriate infrastructure.

But setting up a fl oriculture unit is not a Herculean task. You need to follow a set of guidelines. As for the

actual setting up of the fl ower farm, you need to consider factors such as the species of fl owers you wish to grow, climatic conditions of the place, soil quality, water availability, and air or land connectivity. Maharashtra, Kar-nataka, Tamil Nadu, Andhra Pradesh and the North-Eastern states score high on these counts. With appropri-ate infrastructure in place, states in northern and western India also come into the list.

Roses, Chrysanthemum, Gladiolus, Carnation, Gerbera, Dahlia, Poinsettia, Orchids, Lily

Forms of export

Cutfl owers are exported in two forms:

1. Fresh form for bouquets and ornamental purposes

2. Dried, dyed or bleached (as potpourri)

DARE/fl owers in demand

BIG IDEA/THE POTENTIAL FOR FLORICULTURE EXPORTS HAS BEEN UNDERLEVERAGED SO FAR

opportunity/agriDARE.CO.IN

28 DECEMBER 2007

opportunity/idea DARE.CO.IN

NOVEMBER 2007 29

Appropriate infrastructure com-prises anything from a simple green-house to one fi tted with sophisticated irrigation systems and automated cli-mate controller. The kind of infrastruc-ture that you set up depends on the site that you select and the fl owers you want to grow. For example, the green-house that you build in your farm will depend upon factors like intensity of sunlight, local temperatures, etc. Your climate control systems will largely depend on the same factors plus hu-midity of the place, rainfall, etc.

The actual process of cultivation needs to be done carefully. Different species of fl owers need different treat-ments and environments. For exam-

ple, roses and gerberas need a cool environment with suffi cient sunlight and high humidity, whereas carna-tions can survive in much cooler en-vironments. Also, the roses grown in the mountainous regions turn out to be bigger and better than those grown in the plains.

An effi cient post harvest manage-ment system ensures that once the produce is harvested, it’s checked for quality, graded, sorted, bunched and maintained in cold storage facilities at required temperatures. The entire concept behind post harvest manage-ment systems is to ensure that the fl owers are not destroyed, that your consumers get what they ask for—the

best quality fl owers, and you get the highest possible returns.

How much will you earn from it? Each hectare produces 15-20 lakh

fl owers. From 10 hectares, you’ll make a produce of, say, 1.5 – 2 crore fl ow-ers. Loose fl owers are usually traded by weight and the stemmed ones by dozen or stems. Roses and chrysanthe-mums are usually traded by weight or by the dozen. Gladiolus, carnation and gerberas are traded by the dozen where-as lilies and orchids are counted in stems. Roses, chrysanthemums sell for Rs 40-60/ kg, gladiolus and gerberas for Rs 50-100/ dozen and orchids and lilies for Rs 20-60/ stem. D A R E

opportunity/agri DARE.CO.IN

DECEMBER 2007 29

RFCL Leverages HP's Power of Portfoliofor a Leading Edge in the Life Sciences Space

Delhi-based RFCL, an ICICI Venture company, is a leading solutions and

services provider in the life sciences segment. The company has a presence in the pharma-ceuticals, biotechnology, R&D laboratories, food processing, in vitro diagnostic facilities in clinical labs, hospitals, nursing homes and animal healthcare sectors.

Prior to November 2005, RFCL was a part of Ranbaxy, a leading pharmaceutical player in India. After becoming an ICICI Venture company, the new entity is all set to emerge as a globally respected player in the fi eld of life sciences and laboratory solutions, creat-ing winning relationships to provide quality products and services.

The company has grown, at double the market growth rate over the last fi nancial year, and has drawn up an aggressive roadmap to sustain it over a three-year time frame.

Last year, RFCL also invested in an indig-enous multi-product manufacturing plant at Haridwar to produce diagnostic and animal healthcare products.

Tackling challenges the IT wayAs with any rapidly growing organisation, RFCL was faced with many challenges:

• Acquisition

• Growing need to consolidate multiple platforms

• Growth without trading off quality compliance

• Maintaining a healthy customer retention ratio

“Our assessment of the market determined that HP was the best choice to be our IT partner based on portfolio, technology and relationship management. The team managed to deliver a smooth, stress-free implementation with no cost or time overruns. HP’s understanding and the resulting consolidation exercise have helped us realise the goal of providing effective business solutions while ensuring IT capital investment optimisation.”

Ganesan RamaduraiSenior Manager

IS & Business Solutions, RFCL

• Growing need for CRM tracking

• A well informed and agile mobile sales force

• Scaling up current businesses and amalgamating new business across new product lines and geographies

Solution - HP puts it all togetherThe decision at RFCL was fi nally to consolidate on one platform – a 60-user scalable SAP environment on Windows, running on HP In-tegrity Servers with Storage on HP EVA 3000. Backup was on HP Ultrium 448 Tape drives.

All systems were customised from the ground up and HP front-ended the hybrid solution by managing the relationship with an implementation partner and facility management team.

HP SolutionCore SAP Production environment running

• Windows Cluster on HP Integrity rx2620 Servers with Intel Itanium 1.6Ghz, 6MB CPU

• SAP Development/QA environment on Windows on a single HP Integrity rx1620 Server with Intel Itanium 1.3Ghz, 3MB CPU

• Storage consolidation on an HP EVA 3000 with 146GB 10K FC hard drives

• HP Ultrium 448 Tape Drive for back up

• Blade infrastructure: HP Blade Servers with AMD Opteron processors

• HP ProLiant Servers for the Exchange messaging environment

Benefi ts – for company & customer The biggest benefi t to RFCL, was the ease of use and manageability of proven solutions. While on the customer side, it resulted in higher level of customer satisfaction.By partnering with HP and using the power of its portfolio of solutions – right from serv-ers and storage, to software, solution part-nership and IT management – RFCL needed to look no further for end-to-end support. On the one hand, the HP EVA technology provided RFCL with much-needed ease of use, virtualisation and ease of manageabili-ty while on the other hand its strong alliance with SAP provided RFCL with a great deal of comfort while making the choice of IT solu-tion partner and porting its hardware and software on the platform.Other benefi ts included balanced perform-ance of HP Integrity Servers and scalability and fl exibility of the HP BladeSystem.

The Road AheadGoing forward, RFCL is all set to bank on HP’s portfolio of solutions while adopting technology for providing effective solutions at a faster pace and continuing to address risk mitigation, ensuring business continuity and IT security - right through the cycle of its operations.While SAP is the backbone of business oper-ations, Communication Tools [MS Exchange] are also equally mission critical. Automation of other areas is also on the cards with the CRM project being ready to take off within the next few weeks.

Are you also interested in leveraging technology for better business outcomes? Would you like to explore what HP can do for you? Contact [email protected] 20 enquiries are eligible for an Early Bird gift!

© 2007 Hewlett-packard Development Company, L.P.The information contained herein is subject to change without notice

Clearing the way for successClearing the way for successverse business impact. Most important, as the volume of business increases, we are able to scale effortlessly.

How has investing in HP hardware and solutions helped your organization optimize IT spends?

Before we embark on any IT project, we do a clear evaluation of the need and how its related to our busi-ness objectives. Vendor evaluation too comes into the picture. Unless we have a clear roadmap we cannot op-timization IT spends.