Embed Size (px)

DESCRIPTION

It is two years since we started taking the emotional temperature of Ireland's recession. This month we report on progress towards an emotional recovery alongside economic recovery.

Citation preview

The Economic Recovery IndexAn Amárach Research Briefing

October Index Results

© Amárach Research 2009

April 2011 Results

The AIB Amárach Recovery Indicator

2

The Emotional Recovery

• We have been reporting our monthly

Recovery Indicator since April 2009.

• We set out two years ago to assess the

psychological impact of the recession and to

chart our ‘emotional progress’ towards recovery

alongside our ‘economic progress’.

• Our tracking research has shown the

remarkable emotional strength of the Irish

people, who have consistently reported

‘happiness’ and ‘enjoyment’ as their two most

frequently experienced emotions.

• But we are still in recession – and the path to

recovery still lies some way ahead.

• The next two years should nevertheless see us

make real progress along the path.

3

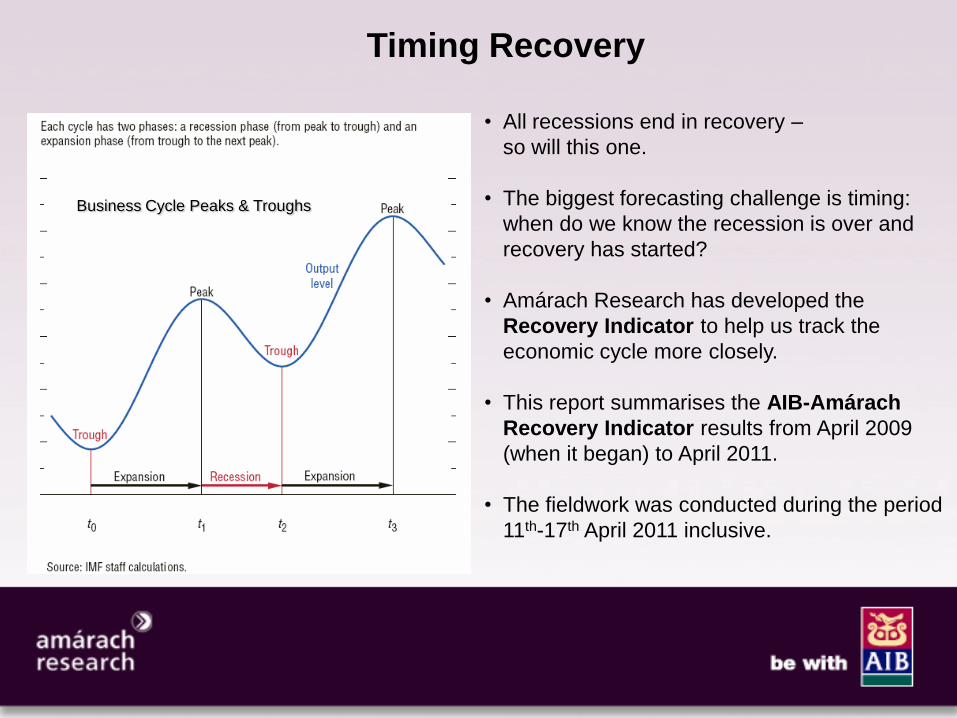

Timing Recovery

• All recessions end in recovery –

so will this one.

• The biggest forecasting challenge is timing:

when do we know the recession is over and

recovery has started?

• Amárach Research has developed the

Recovery Indicator to help us track the

economic cycle more closely.

• This report summarises the AIB-Amárach

Recovery Indicator results from April 2009

(when it began) to April 2011.

• The fieldwork was conducted during the period

11th-17th April 2011 inclusive.

Business Cycle Peaks & Troughs

4

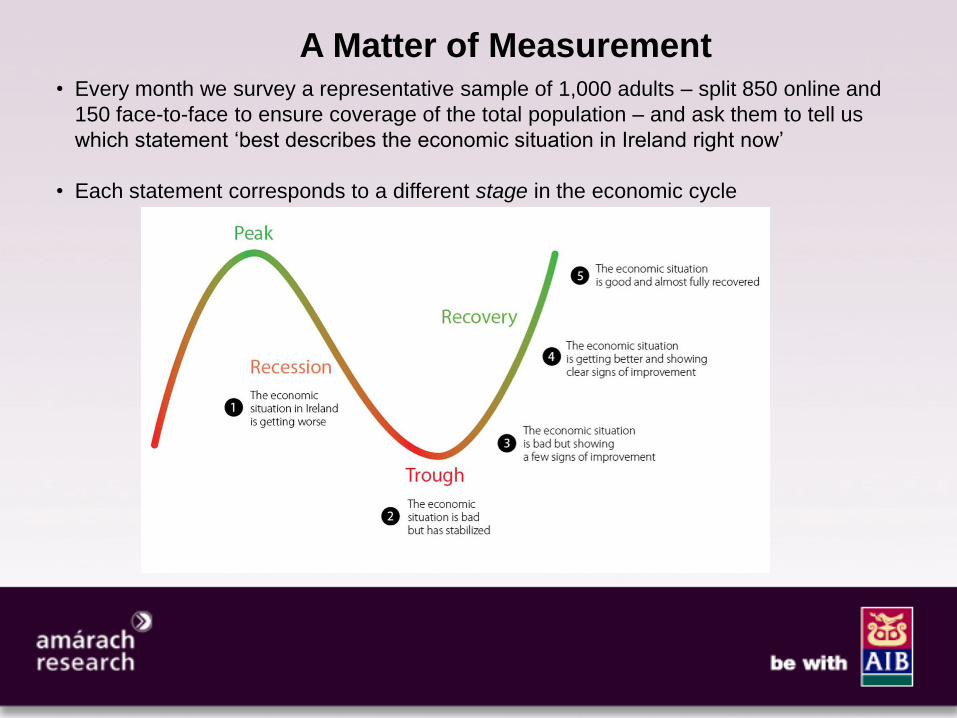

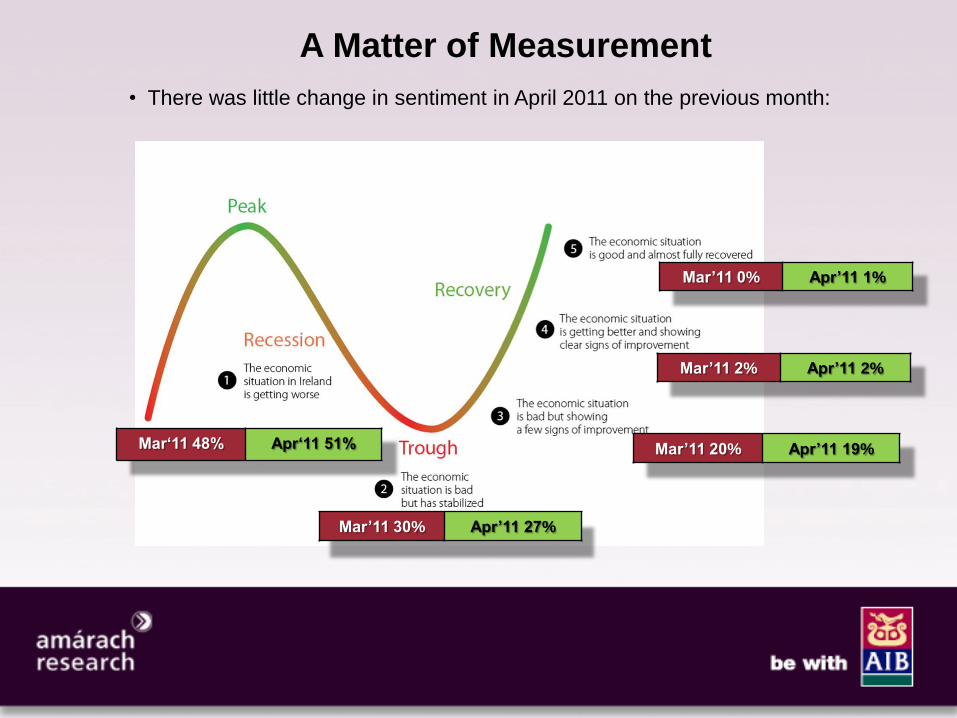

A Matter of Measurement• Every month we survey a representative sample of 1,000 adults – split 850 online and

150 face-to-face to ensure coverage of the total population – and ask them to tell us

which statement ‘best describes the economic situation in Ireland right now’

• Each statement corresponds to a different stage in the economic cycle

5

A Matter of Measurement

Mar‘11 48% Apr‘11 51%

Mar’11 30% Apr’11 27%

Mar’11 20% Apr’11 19%

Mar’11 2% Apr’11 2%

Mar’11 0% Apr’11 1%

• There was little change in sentiment in April 2011 on the previous month:

6

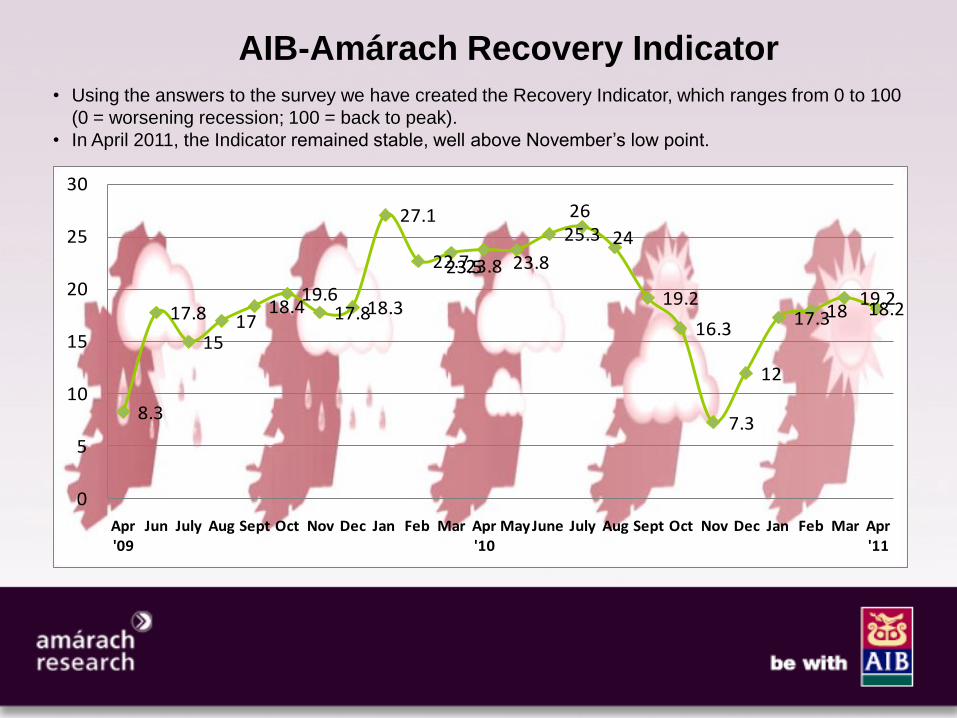

• Using the answers to the survey we have created the Recovery Indicator, which ranges from 0 to 100

(0 = worsening recession; 100 = back to peak).

• In April 2011, the Indicator remained stable, well above November’s low point.

8.3

17.8

1517

18.419.6

17.818.3

27.1

22.723.523.8 23.8

25.326

24

19.2

16.3

7.3

12

17.31819.218.2

0

5

10

15

20

25

30

Apr '09

Jun July Aug Sept Oct Nov Dec Jan Feb Mar Apr '10

May June July Aug Sept Oct Nov Dec Jan Feb Mar Apr '11

AIB-Amárach Recovery Indicator

7

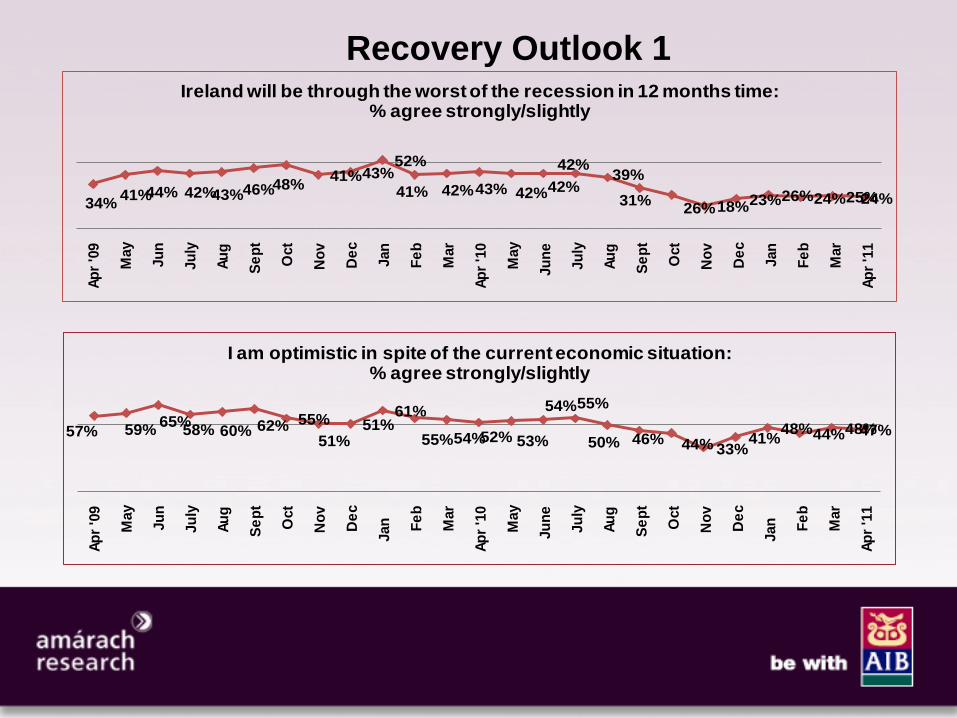

34%41%44% 42%43%46%48%

41%43%52%

41% 42%43% 42%42%

42%39%

31%26%18%23%26%24%25%24%

Ap

r '0

9

May

Ju

n

Ju

ly

Au

g

Se

pt

Oct

No

v

De

c

Jan

Fe

b

Mar

Ap

r '1

0

May

Ju

ne

Ju

ly

Au

g

Se

pt

Oct

No

v

De

c

Jan

Fe

b

Mar

Ap

r '1

1

Ireland will be through the worst of the recession in 12 months time: % agree strongly/slightly

57% 59%65%

58% 60% 62% 55%

51%51%

61%

55%54%52% 53%

54%55%

50% 46% 44% 33%41%

48%44%48%47%

Ap

r '0

9

May

Ju

n

Ju

ly

Au

g

Se

pt

Oct

No

v

De

c

Jan

Fe

b

Mar

Ap

r '1

0

May

Ju

ne

Ju

ly

Au

g

Se

pt

Oct

No

v

De

c

Jan

Fe

b

Mar

Ap

r '1

1

I am optimistic in spite of the current economic situation: % agree strongly/slightly

Recovery Outlook 1

8

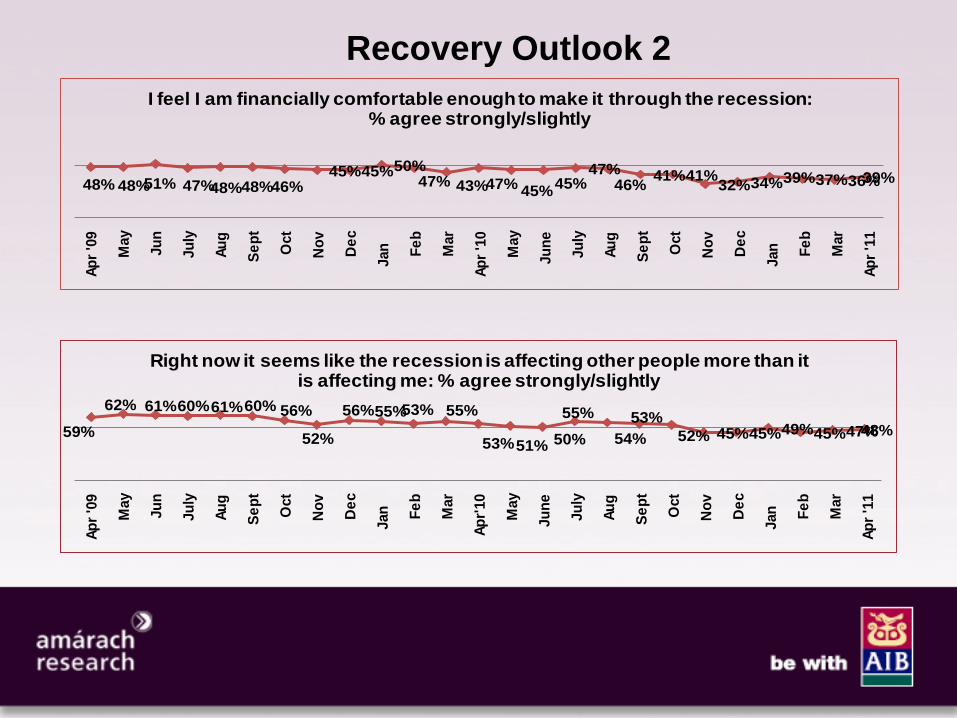

48% 48%51% 47%48%48%46%45%45%50%

47% 43%47% 45%45%

47%46%

41%41%32%34%39%37%36%39%

Ap

r '0

9

May

Ju

n

Ju

ly

Au

g

Se

pt

Oct

No

v

De

c

Jan

Fe

b

Mar

Ap

r '1

0

May

Ju

ne

Ju

ly

Au

g

Se

pt

Oct

No

v

De

c

Jan

Fe

b

Mar

Ap

r '1

1

I feel I am financially comfortable enough to make it through the recession: % agree strongly/slightly

Recovery Outlook 2

59%

62% 61%60%61%60% 56%

52%

56%55%53% 55%

53%51% 50%

55%

54%

53%

52% 45%45%49%45%47%48%

Ap

r '0

9

May

Ju

n

Ju

ly

Au

g

Se

pt

Oct

No

v

De

c

Jan

Fe

b

Mar

Ap

r'10

May

Ju

ne

Ju

ly

Au

g

Se

pt

Oct

No

v

De

c

Jan

Fe

b

Mar

Ap

r '1

1

Right now it seems like the recession is affecting other people more than it is affecting me: % agree strongly/slightly

9

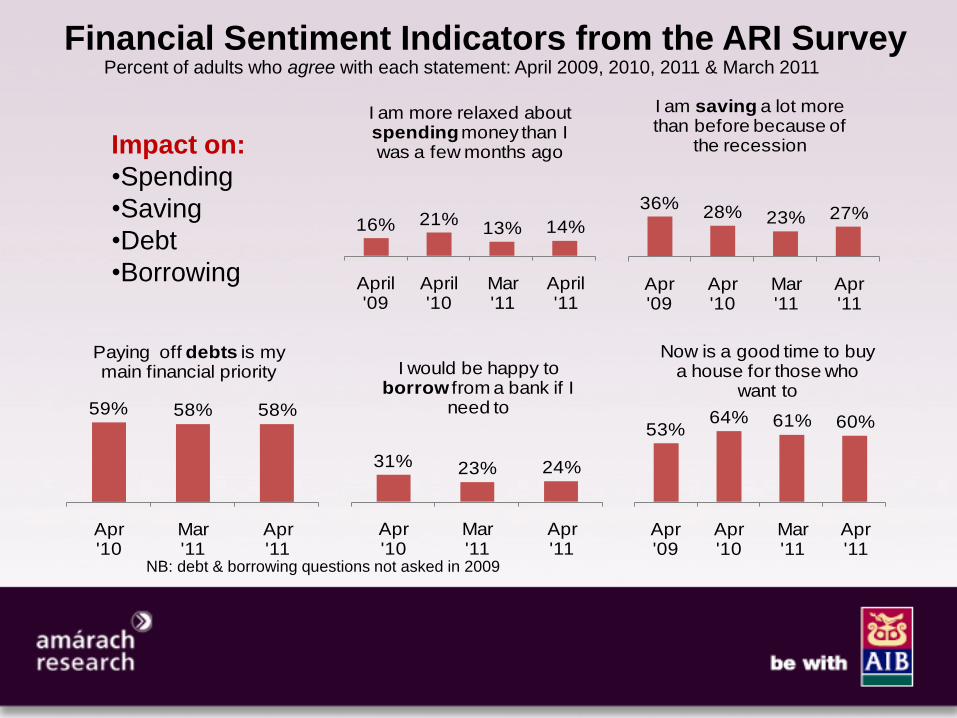

Percent of adults who agree with each statement: April 2009, 2010, 2011 & March 2011

16% 21%13% 14%

April '09

April '10

Mar '11

April '11

I am more relaxed about spendingmoney than I was a few months ago

53%64% 61% 60%

Apr '09

Apr '10

Mar '11

Apr '11

Now is a good time to buy a house for those who

want to

36%28% 23% 27%

Apr '09

Apr '10

Mar '11

Apr '11

I am saving a lot more than before because of

the recession

31% 23% 24%

Apr '10

Mar '11

Apr '11

I would be happy to borrow from a bank if I

need to 59% 58% 58%

Apr '10

Mar '11

Apr '11

Paying off debts is my main financial priority

Impact on:

•Spending

•Saving

•Debt

•Borrowing

Financial Sentiment Indicators from the ARI Survey

NB: debt & borrowing questions not asked in 2009

10

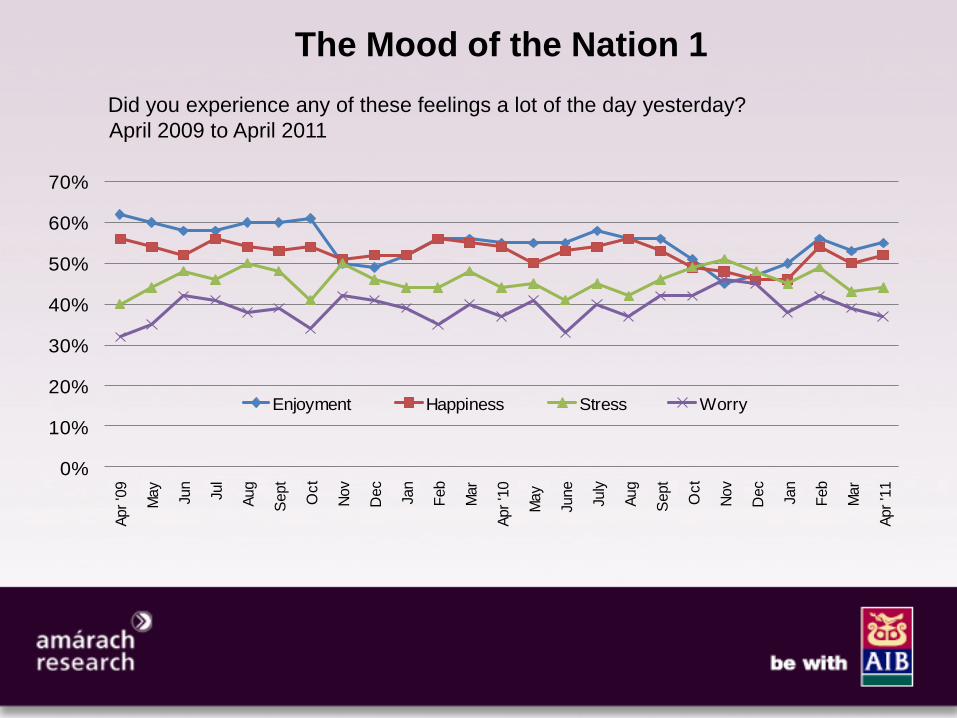

The Mood of the Nation 1

Did you experience any of these feelings a lot of the day yesterday?

April 2009 to April 2011

0%

10%

20%

30%

40%

50%

60%

70%

Apr

'09

May

Jun

Jul

Aug

Sept

Oct

Nov

Dec

Jan

Feb

Mar

Apr

'10

May

June

July

Aug

Sept

Oct

Nov

Dec

Jan

Feb

Mar

Apr

'11

Enjoyment Happiness Stress Worry

11

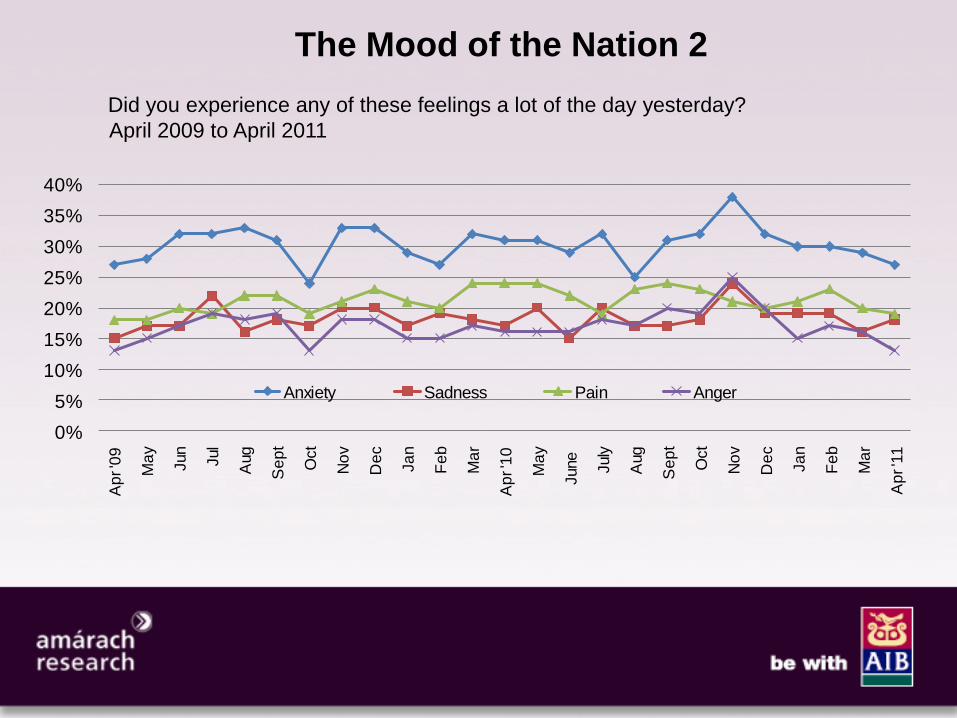

The Mood of the Nation 2

Did you experience any of these feelings a lot of the day yesterday?

April 2009 to April 2011

0%

5%

10%

15%

20%

25%

30%

35%

40%

Ap

r '0

9

Ma

y

Jun

Jul

Aug

Se

pt

Oct

No

v

De

c

Ja

n

Fe

b

Ma

r

Ap

r '1

0

Ma

y

June

July

Aug

Se

pt

Oct

No

v

De

c

Ja

n

Fe

b

Ma

r

Ap

r '1

1

Anxiety Sadness Pain Anger

12

Taking Stock

• Irish consumers are now planning for the long

haul – emotionally and economically.

• Their financial focus is on debt reduction, as well

as on precautionary savings to see them

through to recovery.

• Nevertheless, consistently between a third and

half of all adults feel some degree of ‘insulation’

from the full consequences of the recession.

• Couple that with continuing emotional

robustness and it could reasonably be argued

that recovery in consumer markets may bounce

back more strongly than expected one people

feel the worst is behind them.

• But we’re not there yet...

13

Amárach Contact Details

Gerard O’Neill - Chairman

Amárach Research

11 Kingswood Business Centre

Citywest Business Campus

Dublin 24

T. (01) 410 5200

W. www.amarach.com

B. www.amarach.com/blog