Embed Size (px)

Citation preview

A Service Provider Perspective on GBS Scope

….Doing more with Data and Analytics

Gary Plumpton

Traditional SSC approach may deliver less than expected ….……. And potentially less than Customers desire

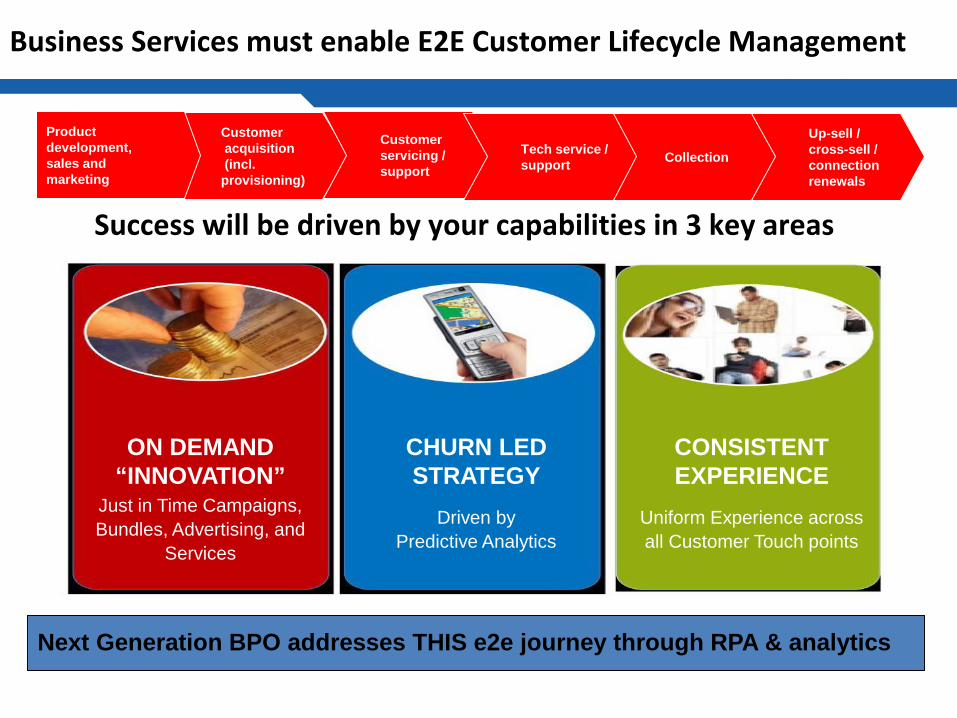

Business Services must enable E2E Customer Lifecycle Management…….. “Experience” is the true differentiator

Data and Analytics within the GBS add value to the business

Opening Thoughts / Reflections on Yesterday

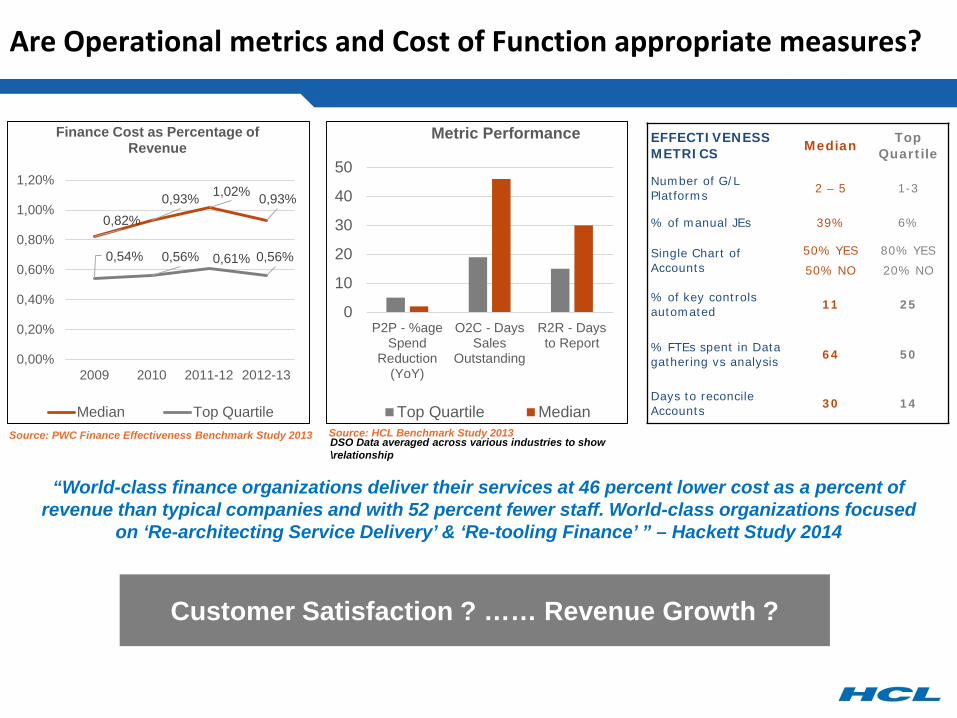

0,82%0,93% 1,02% 0,93%

0,54% 0,56% 0,61% 0,56%

0,00%

0,20%

0,40%

0,60%

0,80%

1,00%

1,20%

2009 2010 2011-12 2012-13

Finance Cost as Percentage of Revenue

Median Top QuartileSource: PWC Finance Effectiveness Benchmark Study 2013

Customer Satisfaction ? …… Revenue Growth ?

0

10

20

30

40

50

P2P - %ageSpend

Reduction(YoY)

O2C - DaysSales

Outstanding

R2R - Daysto Report

Metric Performance

Top Quartile MedianSource: HCL Benchmark Study 2013DSO Data averaged across various industries to show \relationship

“World-class finance organizations deliver their services at 46 percent lower cost as a percent of revenue than typical companies and with 52 percent fewer staff. World-class organizations focused

on ‘Re-architecting Service Delivery’ & ‘Re-tooling Finance’ ” – Hackett Study 2014

EFFECTIVENESS METRICS Median Top

Quartile

Number of G/L Platforms 2 – 5 1-3

% of manual JEs 39% 6%

Single Chart of Accounts

50% YES50% NO

80% YES20% NO

% of key controls automated 11 25

% FTEs spent in Data gathering vs analysis 64 50

Days to reconcile Accounts 30 14

Are Operational metrics and Cost of Function appropriate measures?

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Strategic relationship that provides business consulting, strategic planning and analysis that can include fundamental redesign of existing processes

Relationship enhances current capabilities by 'mining' and/or adding functionality to existing processes and

technologies

Relationship standardizes and/or consolidates existing processes in order to drive down costs and

achieve operational efficiencies

Current Status

Future Expectations

3 3.2 3.4 3.6 3.8 4 4.2

All (n=343)

1,000 - 4,999 (n=44)

5,000 - 9,999 (n=32)

10,000+ (n=76)

Ability to Transform your Business to a Cloud based model

Automation/Platform BPO Solutions

Analytics Capability

Talent

Global Delivery Infrastructure

This trend points towards a customer willingness to outsource higher value services to BPO providers.

Top 3 selection criteria to choose a provider:

1. Ability to transform business in to a cloud based model

2. Automation of Platform/BPO solutions3. Analytics capability

Top 3 outcomes from an outsourcing initiative:

1. Support/enhance Finance Transformation 2. Improve cash-flow and working capital 3. Globalize Finance Operations

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Other

Leverage BPO providers strengths in mobility services

Leverage BPO providers financial services skills/knowledge for my industry

Leverage BPO providers infrastructure to scale operations

Leverage providers financial services platform/technology

Access quality talent related to financial operations

Standardize processes across regional operations and Acquisitions

Leverage provider’s experience and solutions to infuse efficiency into Financial business processes

Use analytics services to extract performance metrics

Globalize Financial Operations

Improve Cash Flow and Working capital

Achieve and/or enhance overall company’s financial transformation efforts

n=134

Source: IDC

CFO’s have begun to lay down wider expectations of BPO Vendors

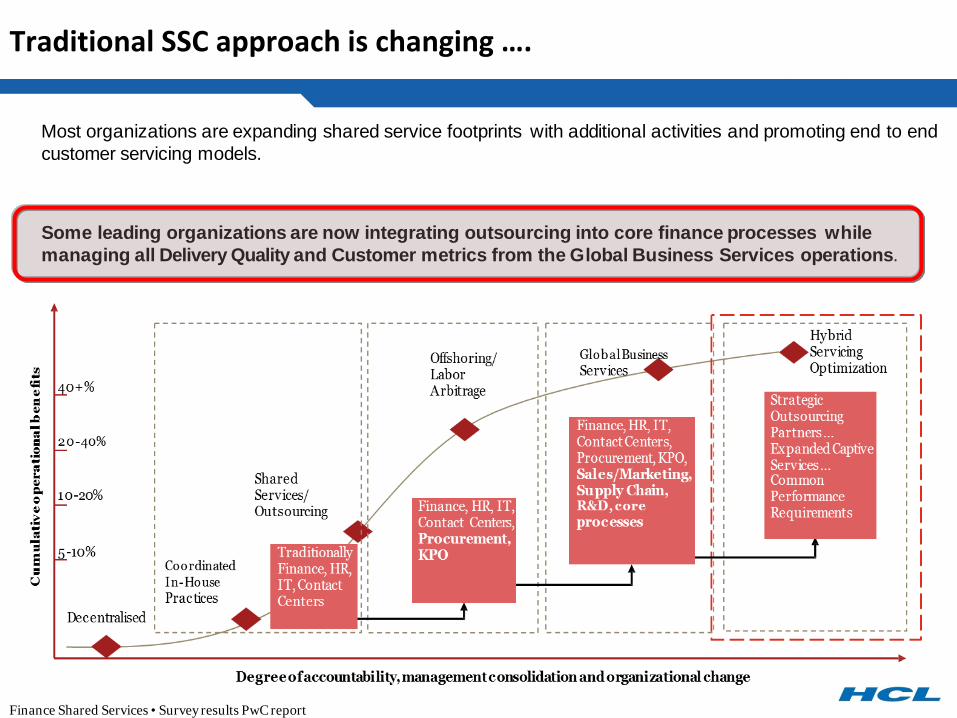

Most organizations are expanding shared service footprints with additional activities and promoting end to endcustomer servicing models.

Some leading organizations are now integrating outsourcing into core finance processes whilemanaging all Delivery Quality and Customer metrics from the Global Business Services operations.

Finance Shared Services • Survey results PwC report

Traditional SSC approach is changing ….

Contents

Some Practical Examples

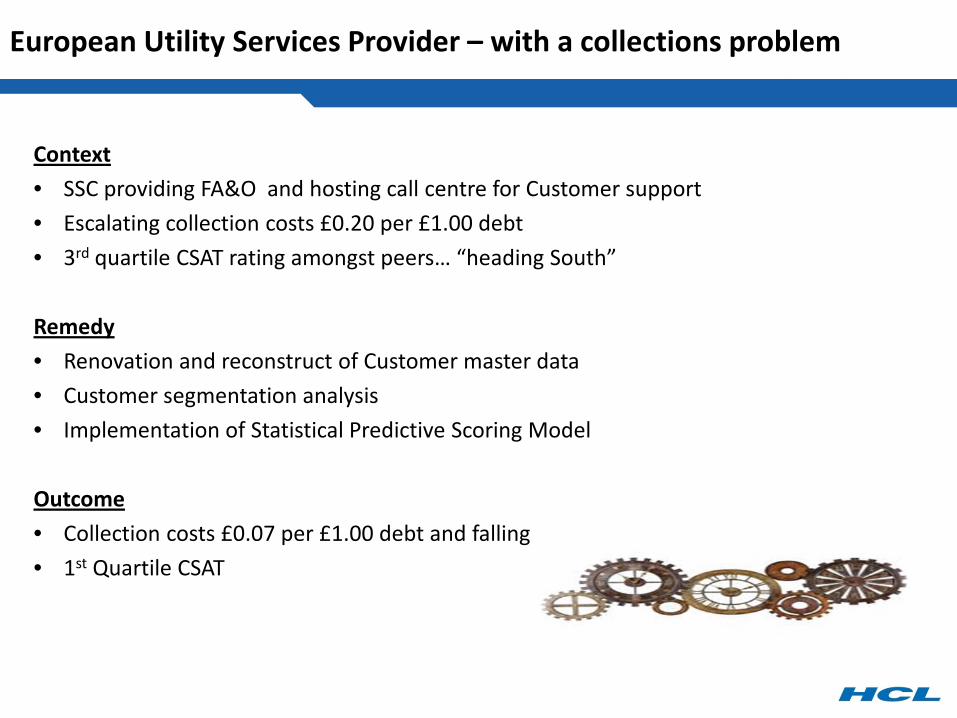

A leading European Utility Services Provider – with a collections problem

A Leading Automotive Manufacturer – with declining market share

Context• SSC providing FA&O and hosting call centre for Customer support• Escalating collection costs £0.20 per £1.00 debt• 3rd quartile CSAT rating amongst peers… “heading South”

Remedy• Renovation and reconstruct of Customer master data • Customer segmentation analysis• Implementation of Statistical Predictive Scoring Model

Outcome• Collection costs £0.07 per £1.00 debt and falling• 1st Quartile CSAT

European Utility Services Provider – with a collections problem

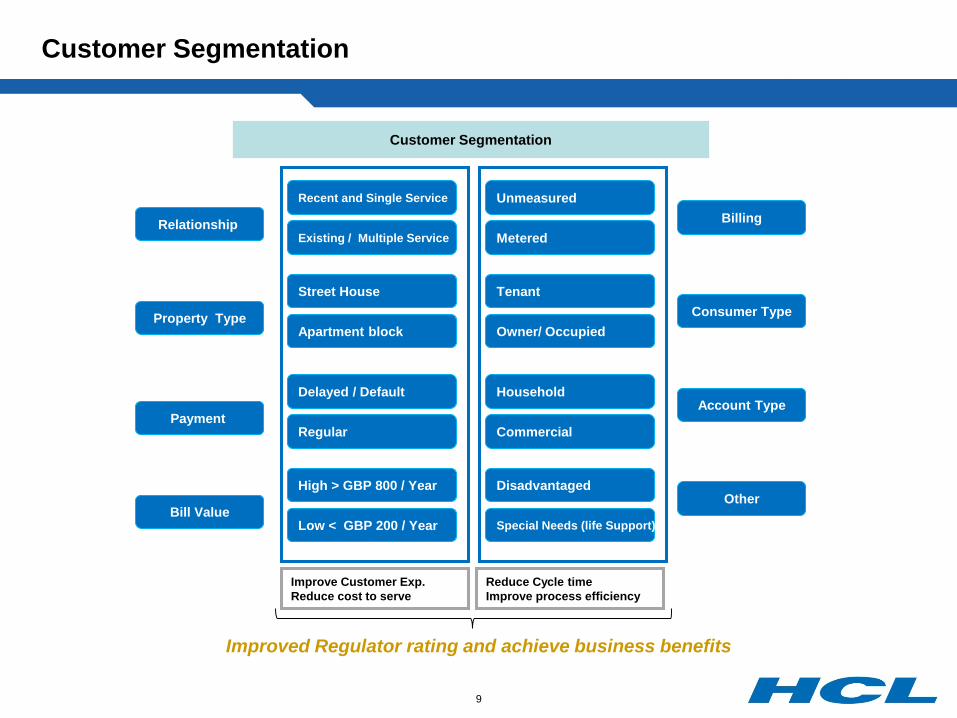

The use of Master Data - Customer Behavior analysis

Customer Behavior analysis can benefit all areas of Client business

Marketing / Sales PaymentsService Bill Generation Bill Overdue Collections

SPSM: Statistical Predictive

Scoring Model

Bill Generation and Pre Bill Overdue Reminder to customers

with High Score

Pre sales Strategies can be formed using the same patterns of

behavior recorded

• SPSM (Statistical Predictive Scoring Model): This model will be created using a statistical tool which will provide behavior pattern of Origin’s current customers

• Onboard the customer on the correct plan• Prevention of customer churn• Know your customer’s behavior• Select right mode of collection at the right time (SMS, Emails, Letters, Collector less collector. Etc.)

Data from our Mercantile collections.

8

Customer Segmentation

Customer Segmentation

Recent and Single Service

Existing / Multiple Service

Street House

Apartment block

Delayed / Default

Regular

High > GBP 800 / Year

Low < GBP 200 / Year

Unmeasured

Metered

Tenant

Owner/ Occupied

Household

Commercial

Disadvantaged

Special Needs (life Support)

Billing

Consumer Type

Account Type

Other

Relationship

Property Type

Payment

Bill Value

Improve Customer Exp.Reduce cost to serve

Reduce Cycle timeImprove process efficiency

Improved Regulator rating and achieve business benefits

9

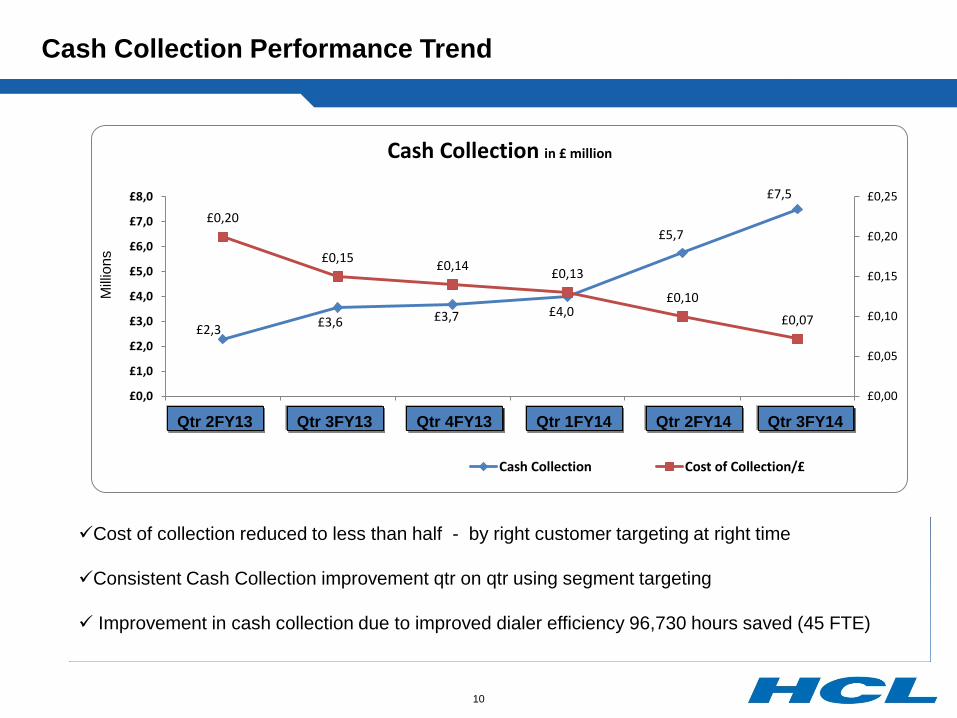

Cash Collection Performance Trend

Cost of collection reduced to less than half - by right customer targeting at right time

Consistent Cash Collection improvement qtr on qtr using segment targeting

Improvement in cash collection due to improved dialer efficiency 96,730 hours saved (45 FTE)

£2,3 £3,6 £3,7 £4,0

£5,7

£7,5

£0,20

£0,15 £0,14 £0,13

£0,10

£0,07

£0,00

£0,05

£0,10

£0,15

£0,20

£0,25

£0,0

£1,0

£2,0

£3,0

£4,0

£5,0

£6,0

£7,0

£8,0

2009-10 2010-11 2011-12 2012-13 2013-14 2014-15

Cash Collection in £ million

Cash Collection Cost of Collection/£

Milli

ons

Qtr 2FY13 Qtr 3FY13 Qtr 4FY13 Qtr 1FY14 Qtr 2FY14 Qtr 3FY14

10

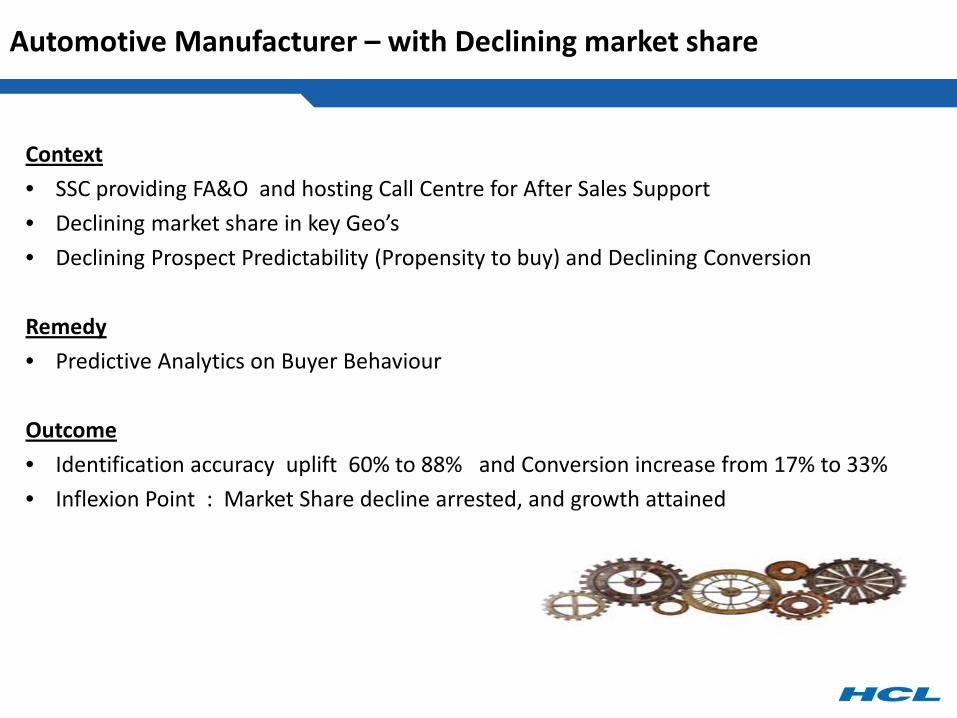

Context• SSC providing FA&O and hosting Call Centre for After Sales Support• Declining market share in key Geo’s• Declining Prospect Predictability (Propensity to buy) and Declining Conversion

Remedy• Predictive Analytics on Buyer Behaviour

Outcome• Identification accuracy uplift 60% to 88% and Conversion increase from 17% to 33%• Inflexion Point : Market Share decline arrested, and growth attained

Automotive Manufacturer – with Declining market share

Data Diagnostics Data Preparation Data Transformation

• Identifying common variables• Identifying primary key• Develop rules for identification

of key variable• create index variables if absent• Merge data using primary keys• Removal of duplicate variables• Removal of duplicate records• Creating new variables• Data cleansing

• Outlier detection & removal -Box-Cox plot

• Descriptive statistics• Graphical tests • Perform Multicollinearity Test &

Heteroscedasticity test• Correlation Analysis• Normality tests (P-P , Q-Q

plots, Anderson Darling)

• Selecting approapriate modeling technique(s) (Regression, Logistic, Cluster etc.)

• Model specification • Fit model• Diagnostic tests• Use simulation technique for

model suitability test on alternative scenarios

• Choosing a decision/classification rule(s)

• Acceptability• Predictability• Key Impact variables• Empirical Test• Final Model for deployment

• Redefine variables• Define coding criteria/

quantification of qualitative variables

• Innovating methods to use available data points

• Construct relevant scoring indices

• Prepare Index of Information Content (IIC)

• Checking data history• Checking duplicates & blanks• Identifying variables• Assess data consistency• Assess data completeness• Assess compatibility of different

data sources

Exploratory AnalysisModel DevelopmentFinal Model Validation

Model Implementation

Dat

a So

urce

MSC

RM

, aC

RM

Approach to Model Development

12

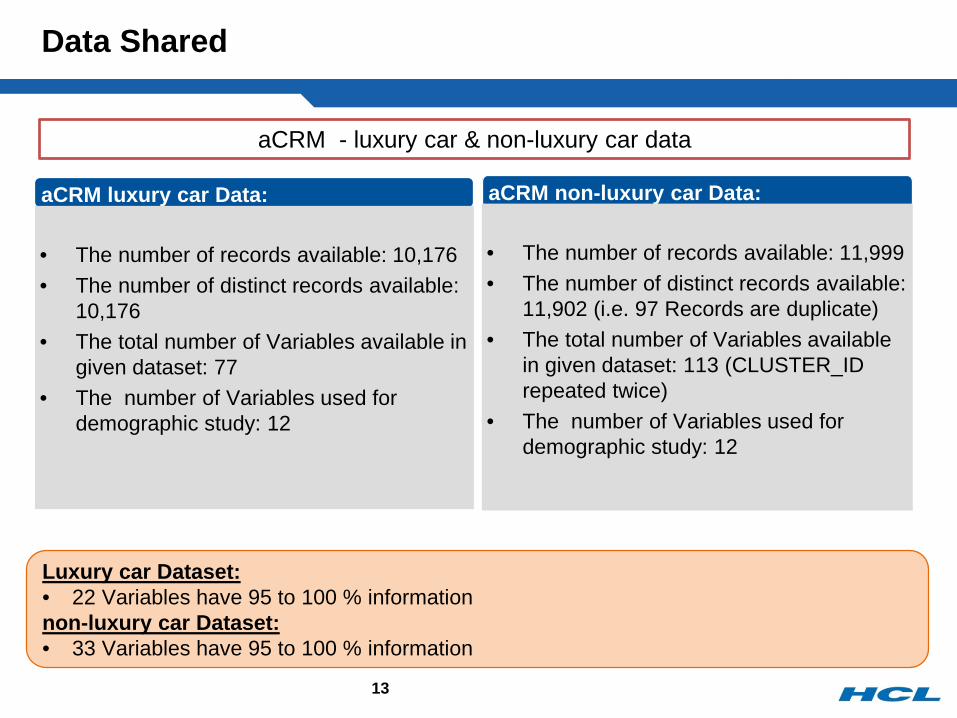

aCRM luxury car Data:

Data Shared

13

• The number of records available: 10,176• The number of distinct records available:

10,176• The total number of Variables available in

given dataset: 77• The number of Variables used for

demographic study: 12

aCRM - luxury car & non-luxury car data

aCRM non-luxury car Data:

• The number of records available: 11,999• The number of distinct records available:

11,902 (i.e. 97 Records are duplicate)• The total number of Variables available

in given dataset: 113 (CLUSTER_ID repeated twice)

• The number of Variables used for demographic study: 12

Luxury car Dataset:• 22 Variables have 95 to 100 % informationnon-luxury car Dataset:• 33 Variables have 95 to 100 % information

Models for Different Scenario and Visibility

Sno Variables Total observations Percentages Scenario-1 Scenario-2 Scenario-3 Scenario-4 Scenario-5 Scenario-61 Resi_city 20683 99.2 yes yes yes yes yes yes2 Resi_state 19359 89.6 yes yes yes3 Gender 18977 87.82 yes yes4 Pincode 17374 96.05 yes yes yes yes yes yes5 Occupation 14711 68.08 yes yes yes yes yes6 Marital_status 4153 19.22 yes yes7 Profession 1320 6.12 yes8 Employer 778 3.71 yes9 Qualification 449 2.08 yes

10 Designation 428 2.23 yes11 Fmly_size 223 1.03

TOTAL 21608

Number of Observation

used 129 9949 17094 11989 2821 10681Overall

Prediction 88% 64% 72% 67% 60% 65%Prediction Within luxury segment 93% 72% 70% 72% 81% 72%

We have tried all possible Scenarios to develop models based on :• Data Content• Availability• Prediction

Model Implemented: Logistic Regression

Predictive efficacy varies from 60% to 88%14

86(67%)

13(10%)

30(23%)

129

Model with Higher Prediction

Category Top decile customers

Middle layer

Bottom Layer

Number of Customers

Direction Must Target;Do multiple follow ups

Can be targeted;Single follow up Do not target

• Overall Prediction

88 %

• Prediction luxury category

93 %

Predicted TotalNot to

purchase luxury sedan

To purchase luxury sedan

Actual

NON_luxury car Purchased 22 7 29

Luxury sedan Purchased 8 92 100

Total 30 99 12915

Business Services must enable E2E Customer Lifecycle Management……..Post Digitisation “Experience” is the true differentiator

Data and Activity Based Analytics within the GBS identify value creation opportunities

If / What …. Not what / if ??

Closing Thoughts / Reflections on Tomorrow

ON DEMAND“INNOVATION”

Just in Time Campaigns,Bundles, Advertising, and

Services

CHURN LEDSTRATEGY

Driven byPredictive Analytics

Uniform Experience acrossall Customer Touch points

CONSISTENTEXPERIENCE

Success will be driven by your capabilities in 3 key areas

Collection

Customer acquisition (incl. provisioning)

Customer servicing / support

Tech service /support

Product development,sales and marketing

Up-sell / cross-sell / connection renewals

Next Generation BPO addresses THIS e2e journey through RPA & analytics

Business Services must enable E2E Customer Lifecycle Management

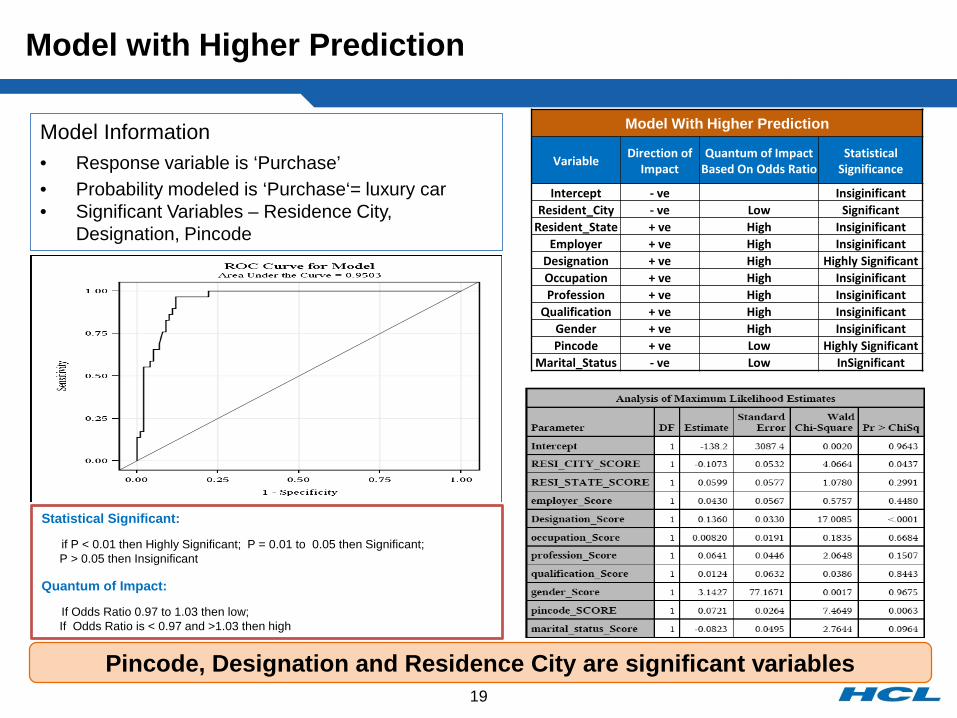

Model with Higher Prediction

Model Information• Response variable is ‘Purchase’• Probability modeled is ‘Purchase‘= luxury car• Significant Variables – Residence City,

Designation, Pincode

Model With Higher Prediction

Variable Direction of Impact

Quantum of Impact Based On Odds Ratio

Statistical Significance

Intercept - ve InsiginificantResident_City - ve Low Significant

Resident_State + ve High InsiginificantEmployer + ve High Insiginificant

Designation + ve High Highly SignificantOccupation + ve High InsiginificantProfession + ve High Insiginificant

Qualification + ve High InsiginificantGender + ve High InsiginificantPincode + ve Low Highly Significant

Marital_Status - ve Low InSignificant

Pincode, Designation and Residence City are significant variables

Statistical Significant:

if P < 0.01 then Highly Significant; P = 0.01 to 0.05 then Significant; P > 0.05 then Insignificant

Quantum of Impact:

If Odds Ratio 0.97 to 1.03 then low; If Odds Ratio is < 0.97 and >1.03 then high

19