Embed Size (px)

Citation preview

Indonesia Automotive Outlook: 2012

Presented by

Vivek Vaidya

Vice President of Automotive & Transportation Practice, Asia Pacific

18th January 2012

Contents Contents

Indonesia Automotive Recap of 2011

Indonesia Automotive Outlook 2012

3

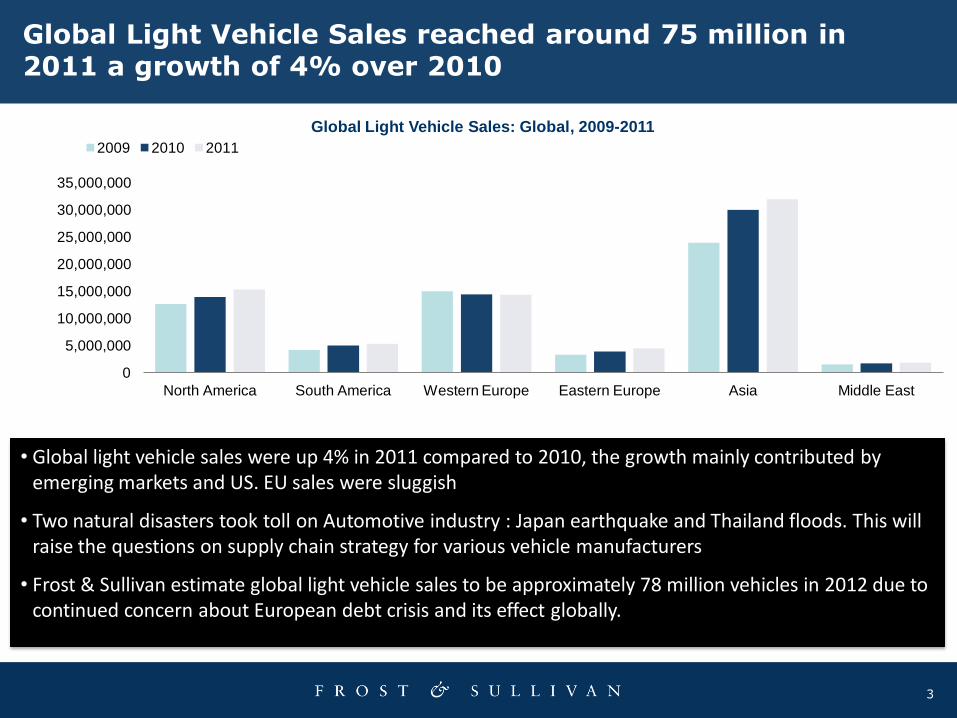

Global Light Vehicle Sales reached around 75 million in 2011 a growth of 4% over 2010

Global Light Vehicle Sales: Global, 2009-2011

• Global light vehicle sales were up 4% in 2011 compared to 2010, the growth mainly contributed by emerging markets and US. EU sales were sluggish

• Two natural disasters took toll on Automotive industry : Japan earthquake and Thailand floods. This will raise the questions on supply chain strategy for various vehicle manufacturers

• Frost & Sullivan estimate global light vehicle sales to be approximately 78 million vehicles in 2012 due to continued concern about European debt crisis and its effect globally.

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

North America South America Western Europe Eastern Europe Asia Middle East

2009 2010 2011

4

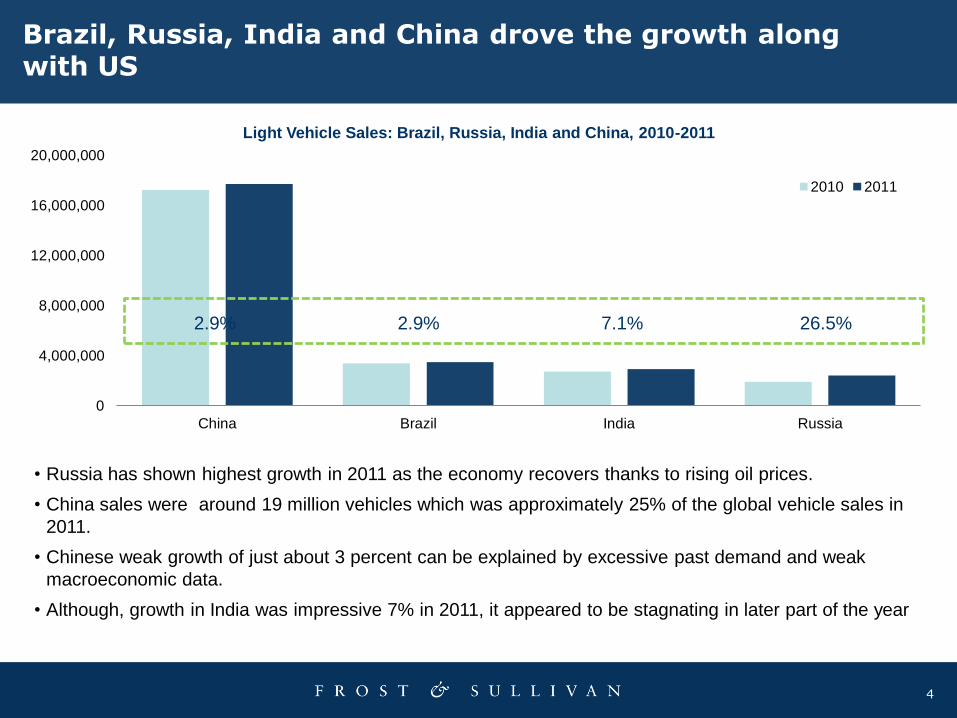

Brazil, Russia, India and China drove the growth along with US

0

4,000,000

8,000,000

12,000,000

16,000,000

20,000,000

China Brazil India Russia

2010 2011

Light Vehicle Sales: Brazil, Russia, India and China, 2010-2011

• Russia has shown highest growth in 2011 as the economy recovers thanks to rising oil prices.

• China sales were around 19 million vehicles which was approximately 25% of the global vehicle sales in

2011.

• Chinese weak growth of just about 3 percent can be explained by excessive past demand and weak

macroeconomic data.

• Although, growth in India was impressive 7% in 2011, it appeared to be stagnating in later part of the year

2.9% 2.9% 7.1% 26.5%

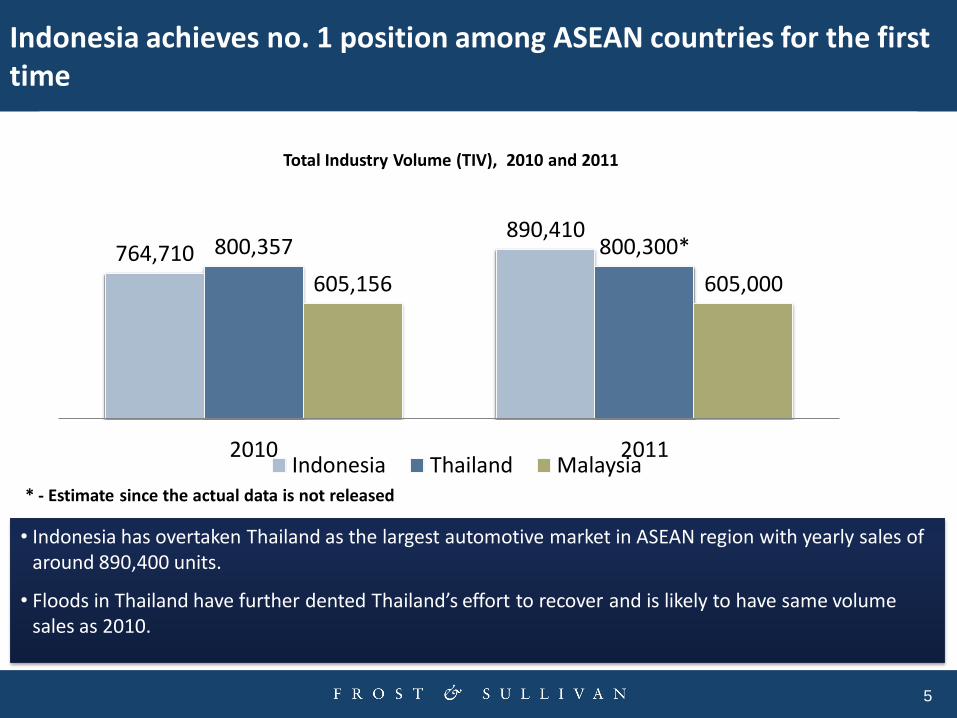

Indonesia achieves no. 1 position among ASEAN countries for the first time

5

764,710 890,410

800,357 800,300*

605,156 605,000

2010 2011 Indonesia Thailand Malaysia

Total Industry Volume (TIV), 2010 and 2011

• Indonesia has overtaken Thailand as the largest automotive market in ASEAN region with yearly sales of around 890,400 units.

• Floods in Thailand have further dented Thailand’s effort to recover and is likely to have same volume sales as 2010.

* - Estimate since the actual data is not released

0

20,000

40,000

60,000

80,000

100,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Un

its

Monthly Sales Trend (2009 – 2011)

2009

2010

2011 (f)

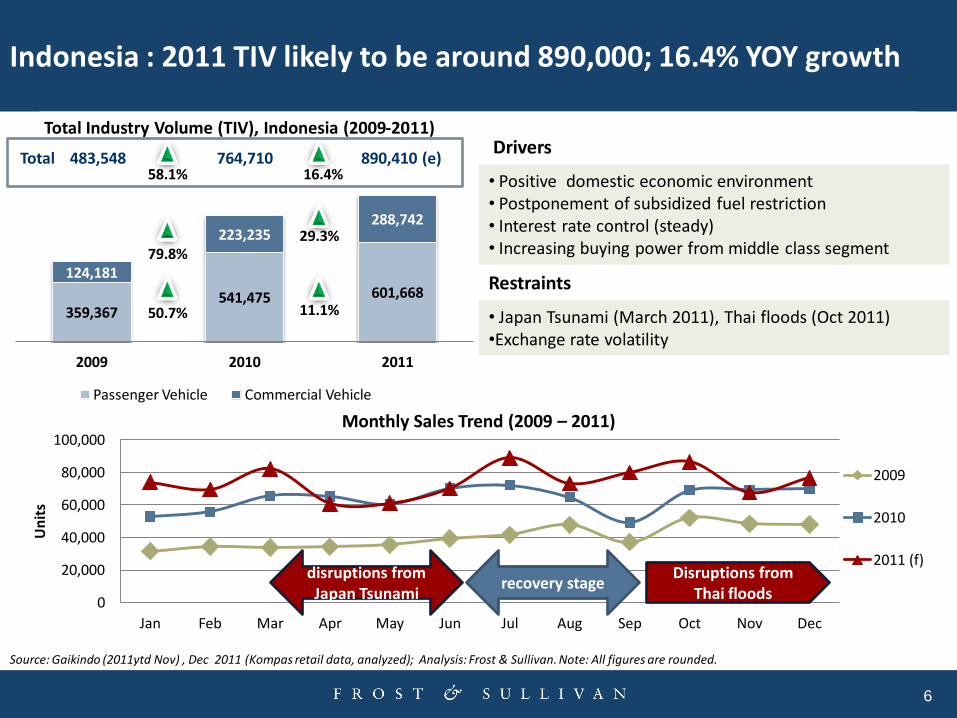

Indonesia : 2011 TIV likely to be around 890,000; 16.4% YOY growth

6

359,367 541,475 601,668

124,181

223,235 288,742

2009 2010 2011

Passenger Vehicle Commercial Vehicle

483,548 764,710 890,410 (e)

• Positive domestic economic environment • Postponement of subsidized fuel restriction • Interest rate control (steady) • Increasing buying power from middle class segment

Source: Gaikindo (2011ytd Nov) , Dec 2011 (Kompas retail data, analyzed); Analysis: Frost & Sullivan. Note: All figures are rounded.

50.7% 11.1%

79.8%

58.1%

29.3%

16.4% Total

disruptions from Japan Tsunami

recovery stage Disruptions from

Thai floods

• Japan Tsunami (March 2011), Thai floods (Oct 2011) •Exchange rate volatility

Restraints

Drivers Total Industry Volume (TIV), Indonesia (2009-2011)

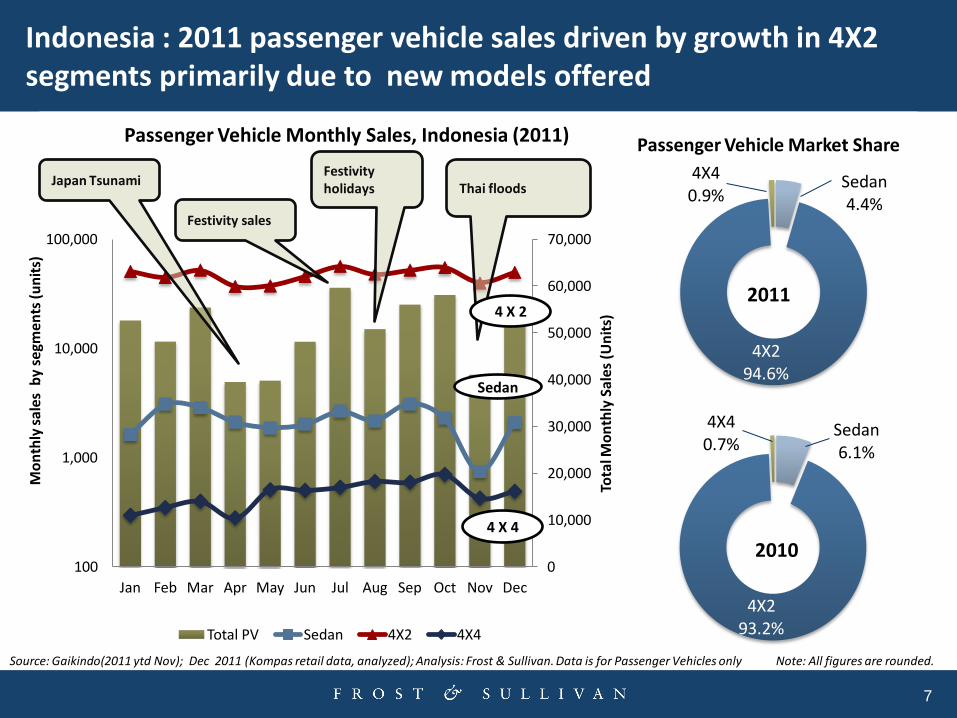

Sedan 4.4%

4X2 94.6%

4X4 0.9%

2011

Sedan 6.1%

4X2 93.2%

4X4 0.7%

2010

Indonesia : 2011 passenger vehicle sales driven by growth in 4X2 segments primarily due to new models offered

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

100

1,000

10,000

100,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec To

tal M

on

thly

Sal

es (

Un

its)

Mo

nth

ly s

ales

by

segm

ents

(u

nit

s)

Passenger Vehicle Monthly Sales, Indonesia (2011)

Total PV Sedan 4X2 4X4

7

Source: Gaikindo(2011 ytd Nov); Dec 2011 (Kompas retail data, analyzed); Analysis: Frost & Sullivan. Data is for Passenger Vehicles only Note: All figures are rounded.

Japan Tsunami Festivity holidays

Festivity sales

Thai floods

4 X 4

Sedan

4 X 2

Passenger Vehicle Market Share

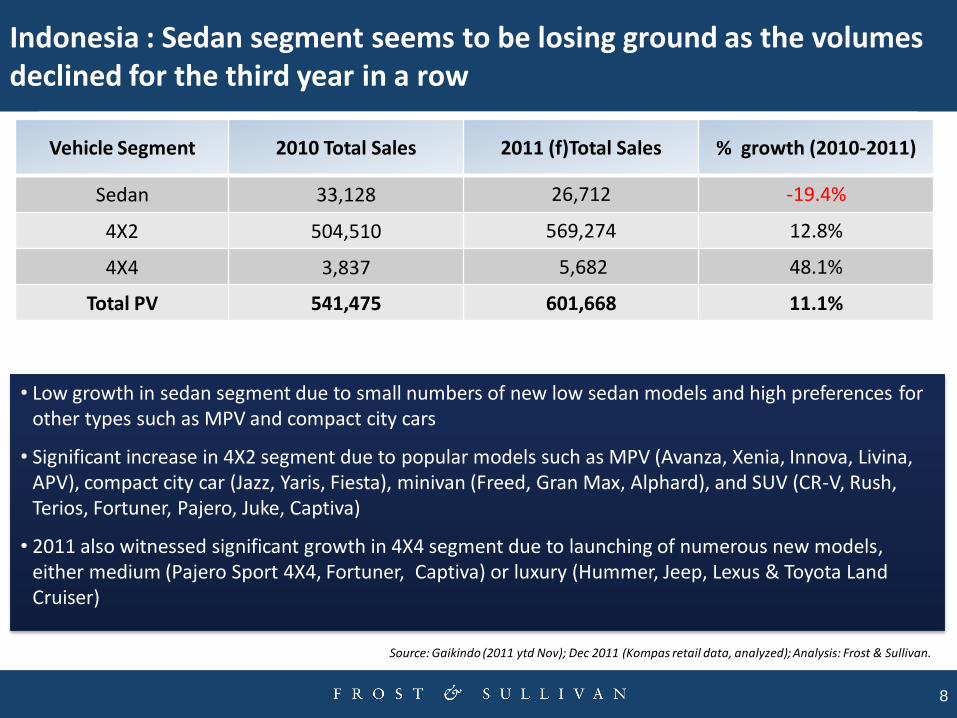

Indonesia : Sedan segment seems to be losing ground as the volumes declined for the third year in a row

8

Vehicle Segment 2010 Total Sales 2011 (f)Total Sales % growth (2010-2011)

Sedan 33,128 26,712 -19.4%

4X2 504,510 569,274 12.8%

4X4 3,837 5,682 48.1%

Total PV 541,475 601,668 11.1%

• Low growth in sedan segment due to small numbers of new low sedan models and high preferences for other types such as MPV and compact city cars

• Significant increase in 4X2 segment due to popular models such as MPV (Avanza, Xenia, Innova, Livina, APV), compact city car (Jazz, Yaris, Fiesta), minivan (Freed, Gran Max, Alphard), and SUV (CR-V, Rush, Terios, Fortuner, Pajero, Juke, Captiva)

• 2011 also witnessed significant growth in 4X4 segment due to launching of numerous new models, either medium (Pajero Sport 4X4, Fortuner, Captiva) or luxury (Hummer, Jeep, Lexus & Toyota Land Cruiser)

Source: Gaikindo (2011 ytd Nov); Dec 2011 (Kompas retail data, analyzed); Analysis: Frost & Sullivan.

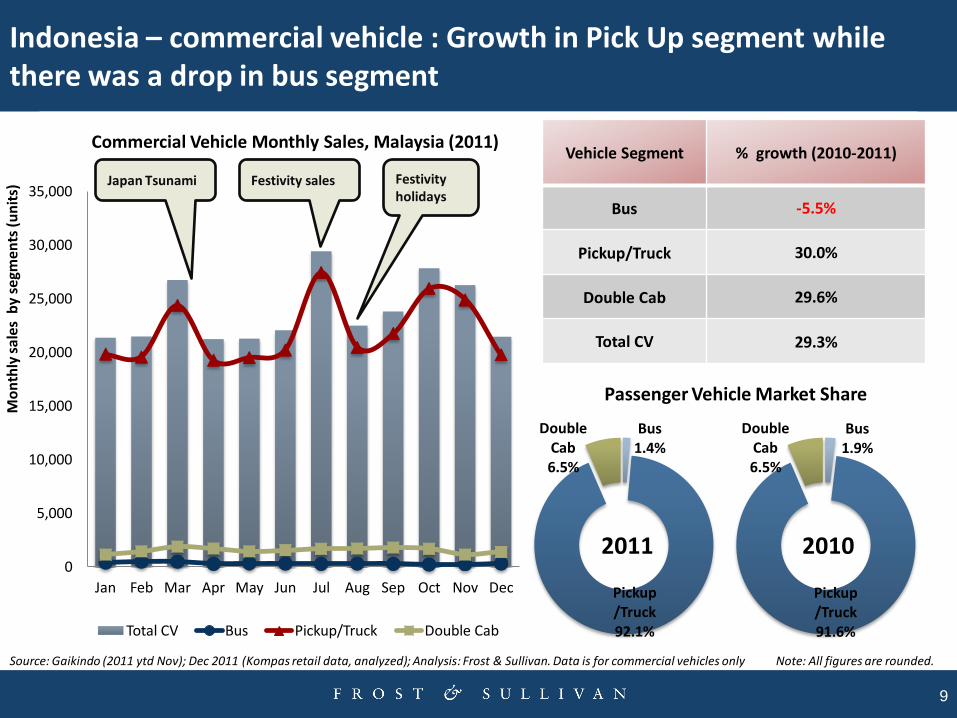

Bus 1.4%

Pickup/Truck 92.1%

Double Cab 6.5%

2011

Bus 1.9%

Pickup/Truck 91.6%

Double Cab 6.5%

2010

Indonesia – commercial vehicle : Growth in Pick Up segment while there was a drop in bus segment

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Mo

nth

ly s

ales

by

segm

ents

(u

nit

s)

Commercial Vehicle Monthly Sales, Malaysia (2011)

Total CV Bus Pickup/Truck Double Cab

9

Vehicle Segment % growth (2010-2011)

Bus -5.5%

Pickup/Truck 30.0%

Double Cab 29.6%

Total CV 29.3%

Source: Gaikindo (2011 ytd Nov); Dec 2011 (Kompas retail data, analyzed); Analysis: Frost & Sullivan. Data is for commercial vehicles only Note: All figures are rounded.

Passenger Vehicle Market Share

Japan Tsunami Festivity holidays

Festivity sales

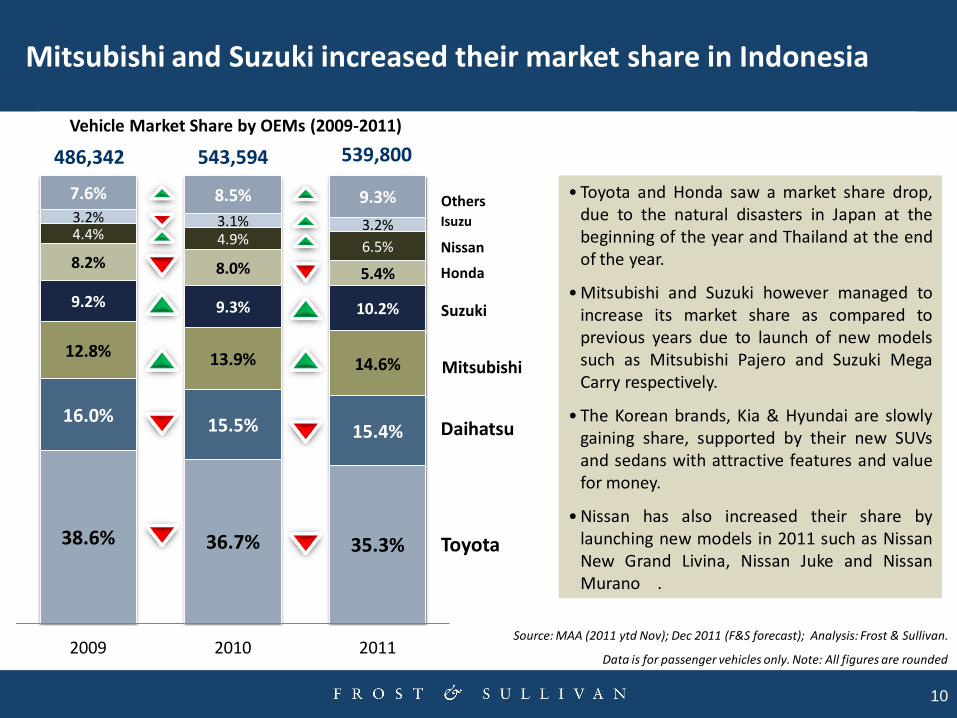

Mitsubishi and Suzuki increased their market share in Indonesia

38.6% 36.7% 35.3%

16.0% 15.5% 15.4%

12.8% 13.9% 14.6%

9.2% 9.3% 10.2%

8.2% 8.0% 5.4%

4.4% 4.9% 6.5%

3.2% 3.1% 3.2%

7.6% 8.5% 9.3%

2009 2010 2011

Vehicle Market Share by OEMs (2009-2011)

10

Toyota

Daihatsu

Mitsubishi

Suzuki

Honda

Nissan

Isuzu

Others

486,342 543,594 539,800

• Toyota and Honda saw a market share drop, due to the natural disasters in Japan at the beginning of the year and Thailand at the end of the year.

• Mitsubishi and Suzuki however managed to increase its market share as compared to previous years due to launch of new models such as Mitsubishi Pajero and Suzuki Mega Carry respectively.

• The Korean brands, Kia & Hyundai are slowly gaining share, supported by their new SUVs and sedans with attractive features and value for money.

• Nissan has also increased their share by launching new models in 2011 such as Nissan New Grand Livina, Nissan Juke and Nissan Murano .

Source: MAA (2011 ytd Nov); Dec 2011 (F&S forecast); Analysis: Frost & Sullivan.

Data is for passenger vehicles only. Note: All figures are rounded

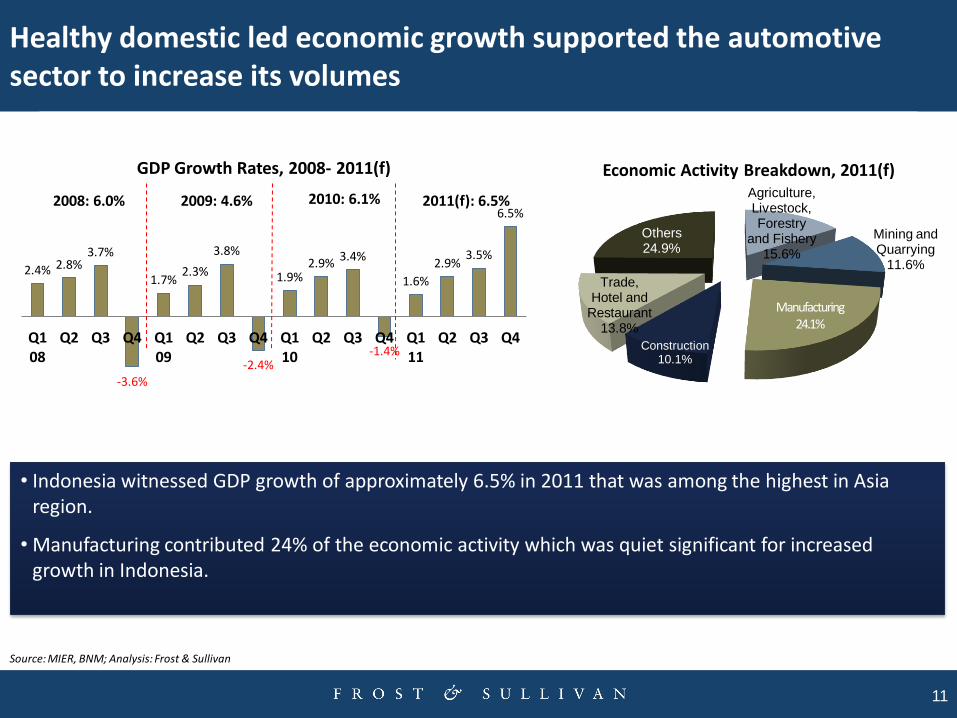

Healthy domestic led economic growth supported the automotive sector to increase its volumes

11

2.4% 2.8% 3.7%

-3.6%

1.7% 2.3%

3.8%

-2.4%

1.9% 2.9%

3.4%

-1.4%

1.6%

2.9% 3.5%

6.5%

Q1 08

Q2 Q3 Q4 Q1 09

Q2 Q3 Q4 Q1 10

Q2 Q3 Q4 Q1 11

Q2 Q3 Q4

GDP Growth Rates, 2008- 2011(f)

2008: 6.0% 2009: 4.6% 2010: 6.1% 2011(f): 6.5% Agriculture, Livestock, Forestry

and Fishery 15.6%

Mining and Quarrying

11.6%

Manufacturing 24.1%

Construction 10.1%

Trade, Hotel and

Restaurant 13.8%

Others 24.9%

Economic Activity Breakdown, 2011(f)

Source: MIER, BNM; Analysis: Frost & Sullivan

• Indonesia witnessed GDP growth of approximately 6.5% in 2011 that was among the highest in Asia region.

• Manufacturing contributed 24% of the economic activity which was quiet significant for increased growth in Indonesia.

Some key launches in 2011

12

Suzuki Mega Carry

Feb ’11

Honda New Full Size Accord

Feb ’11

Nissan New Grand Livina

Feb ’11

Nissan All New Elgrand Feb ‘11

Hyundai H1 (facelift)

Mar ‘11

BWM 520d

Mar ‘11

Toyota Grand New Innova

Jul ‘11

Daihatsu New Sirion

Jul ‘11

Mazda8 Jul ‘11

Hyundai Sonata Jul ‘11

KIA All New Picanto Jul ‘11

Nissan Murano Sep ‘11

Q1 2011 Q2 2011 Q3 2011 Q4 2011

Chevrolet New Captiva

Jul ‘11

Mitsubishi Pajero Sport

Dakar Apr ‘11

Honda All New Jazz (facelift)

May ‘11

KIA All New Sportage

May ‘11

Mercedes Benz ML300 May ‘11

Nissan Juke

Jun ‘11

Audi A8 L

Apr ‘11

Toyota All New Avanza

(Veloz) Nov ‘11

Daihatsu All New Xenia

Nov ‘11

KIA All New Rio

Dec ‘11

BMW X1

Oct ‘11

BMW 116i

Nov ‘11

Mercedes E 300 Connect

Oct ‘11

Contents Contents

Indonesia Automotive Recap of 2011

Indonesia Automotive Outlook 2012

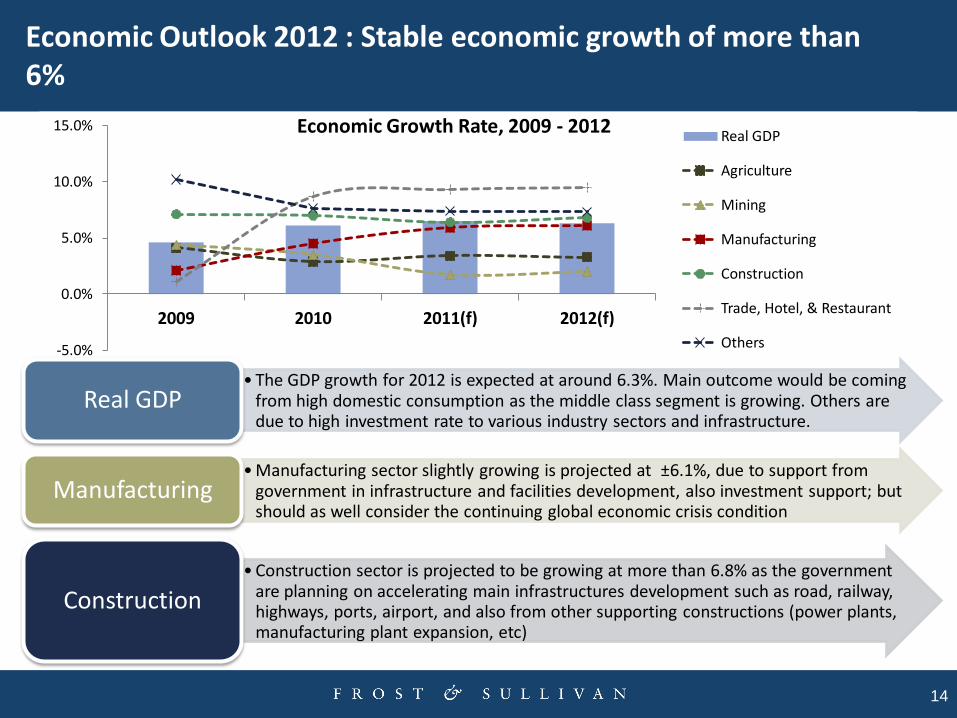

Economic Outlook 2012 : Stable economic growth of more than 6%

14

-5.0%

0.0%

5.0%

10.0%

15.0%

2009 2010 2011(f) 2012(f)

Real GDP

Agriculture

Mining

Manufacturing

Construction

Trade, Hotel, & Restaurant

Others

Economic Growth Rate, 2009 - 2012

• The GDP growth for 2012 is expected at around 6.3%. Main outcome would be coming from high domestic consumption as the middle class segment is growing. Others are due to high investment rate to various industry sectors and infrastructure.

Real GDP

• Manufacturing sector slightly growing is projected at ±6.1%, due to support from government in infrastructure and facilities development, also investment support; but should as well consider the continuing global economic crisis condition

Manufacturing

• Construction sector is projected to be growing at more than 6.8% as the government are planning on accelerating main infrastructures development such as road, railway, highways, ports, airport, and also from other supporting constructions (power plants, manufacturing plant expansion, etc)

Construction

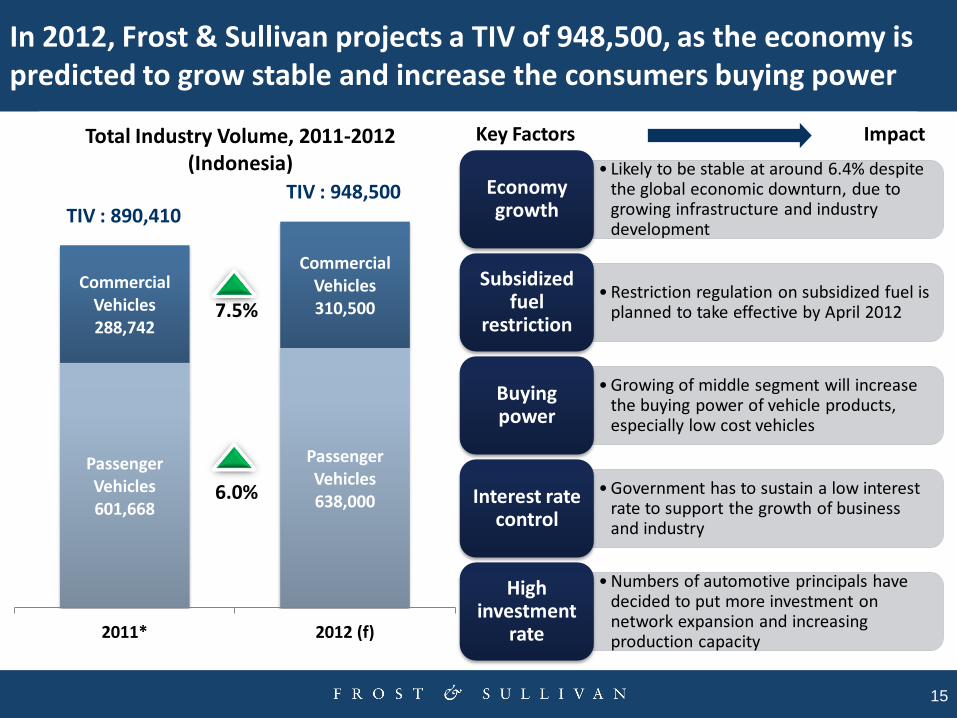

Passenger Vehicles 601,668

Passenger Vehicles 638,000

Commercial Vehicles 288,742

Commercial Vehicles 310,500

2011* 2012 (f)

Total Industry Volume, 2011-2012 (Indonesia)

In 2012, Frost & Sullivan projects a TIV of 948,500, as the economy is predicted to grow stable and increase the consumers buying power

15

6.0%

7.5%

TIV : 890,410 TIV : 948,500

Key Factors Impact

• Likely to be stable at around 6.4% despite the global economic downturn, due to growing infrastructure and industry development

Economy growth

• Restriction regulation on subsidized fuel is planned to take effective by April 2012

Subsidized fuel

restriction

• Growing of middle segment will increase the buying power of vehicle products, especially low cost vehicles

Buying power

• Government has to sustain a low interest rate to support the growth of business and industry

Interest rate control

• Numbers of automotive principals have decided to put more investment on network expansion and increasing production capacity

High investment

rate

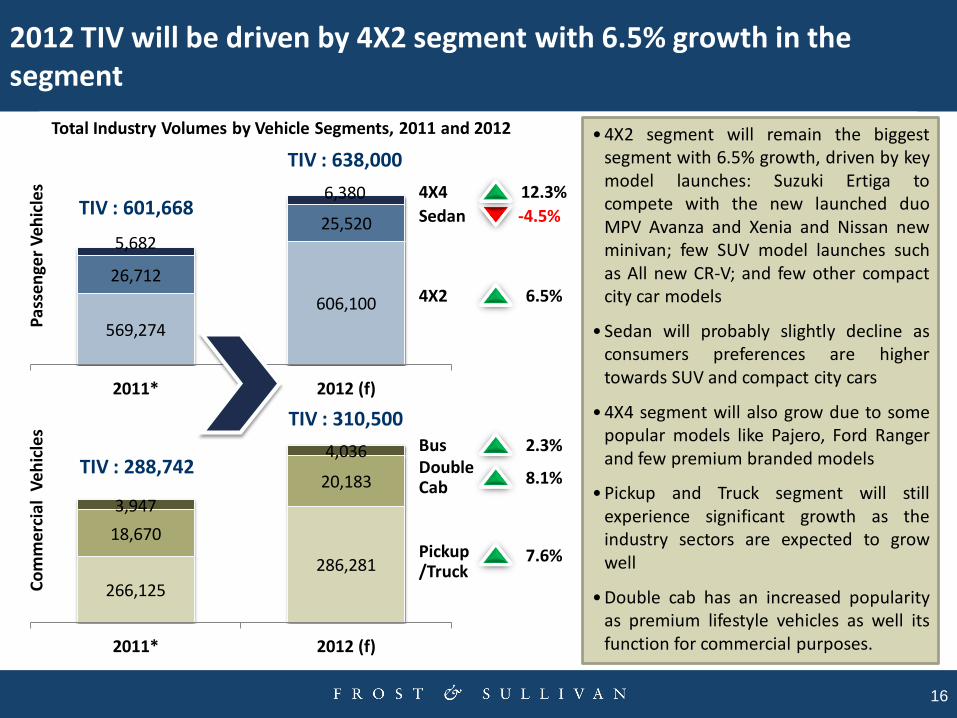

569,274

606,100

26,712

25,520 5,682

6,380

2011* 2012 (f)

266,125

286,281

18,670

20,183

3,947

4,036

2011* 2012 (f)

2012 TIV will be driven by 4X2 segment with 6.5% growth in the segment

16

Total Industry Volumes by Vehicle Segments, 2011 and 2012

TIV : 601,668

TIV : 638,000

7.6%

8.1%

6.5%

-4.5%

12.3%

• 4X2 segment will remain the biggest segment with 6.5% growth, driven by key model launches: Suzuki Ertiga to compete with the new launched duo MPV Avanza and Xenia and Nissan new minivan; few SUV model launches such as All new CR-V; and few other compact city car models

• Sedan will probably slightly decline as consumers preferences are higher towards SUV and compact city cars

• 4X4 segment will also grow due to some popular models like Pajero, Ford Ranger and few premium branded models

• Pickup and Truck segment will still experience significant growth as the industry sectors are expected to grow well

• Double cab has an increased popularity as premium lifestyle vehicles as well its function for commercial purposes.

4X2

Pas

sen

ger

Ve

hic

les

Co

mm

erci

al V

ehic

les

Sedan

4X4

Pickup/Truck

Double Cab

Bus 2.3% TIV : 288,742

TIV : 310,500

New launches supporting the growth in 2012

17

2012 will witness the launch/facelift of around 25-30 new models in Indonesia that will further increase the sales volumes growth.

Japanese OEMs mainly Toyota, Honda and Suzuki are likely to be the front runners in terms of new model introduction by launching close to 15-20 models in 2012.

Ford, Hyundai, Proton and BMW are the other OEMs that are each likely to introduce more than 2-3 new models and make their mark in Indonesia automotive market in 2012.

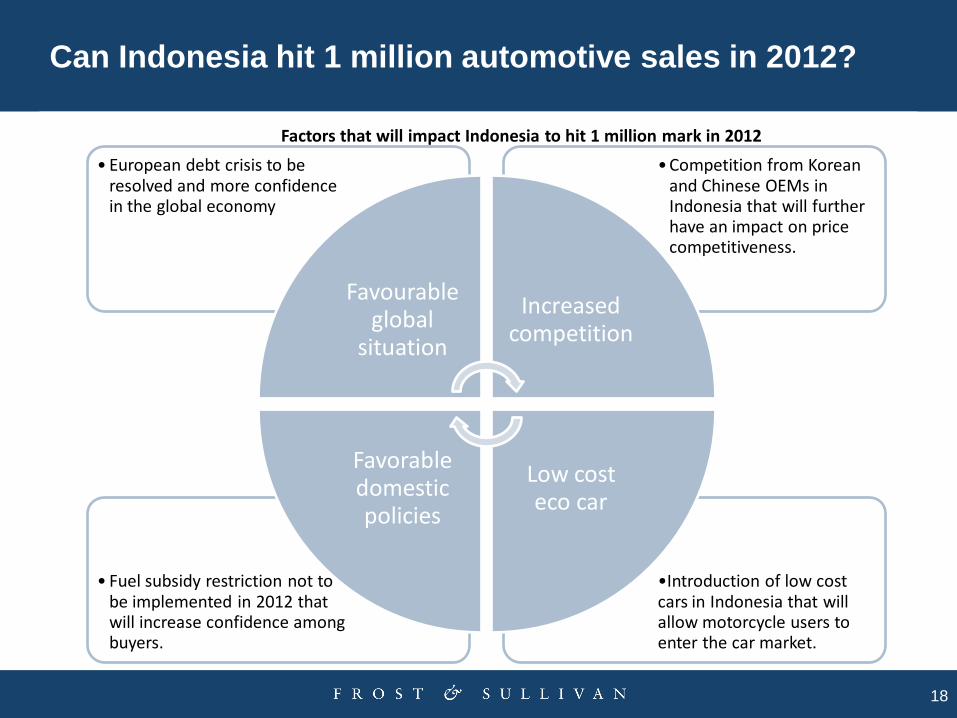

Can Indonesia hit 1 million automotive sales in 2012?

18

•Introduction of low cost cars in Indonesia that will allow motorcycle users to enter the car market.

• Fuel subsidy restriction not to be implemented in 2012 that will increase confidence among buyers.

• Competition from Korean and Chinese OEMs in Indonesia that will further have an impact on price competitiveness.

• European debt crisis to be resolved and more confidence in the global economy

Favourable global

situation

Increased competition

Low cost eco car

Favorable domestic policies

Factors that will impact Indonesia to hit 1 million mark in 2012

Conclusions

19

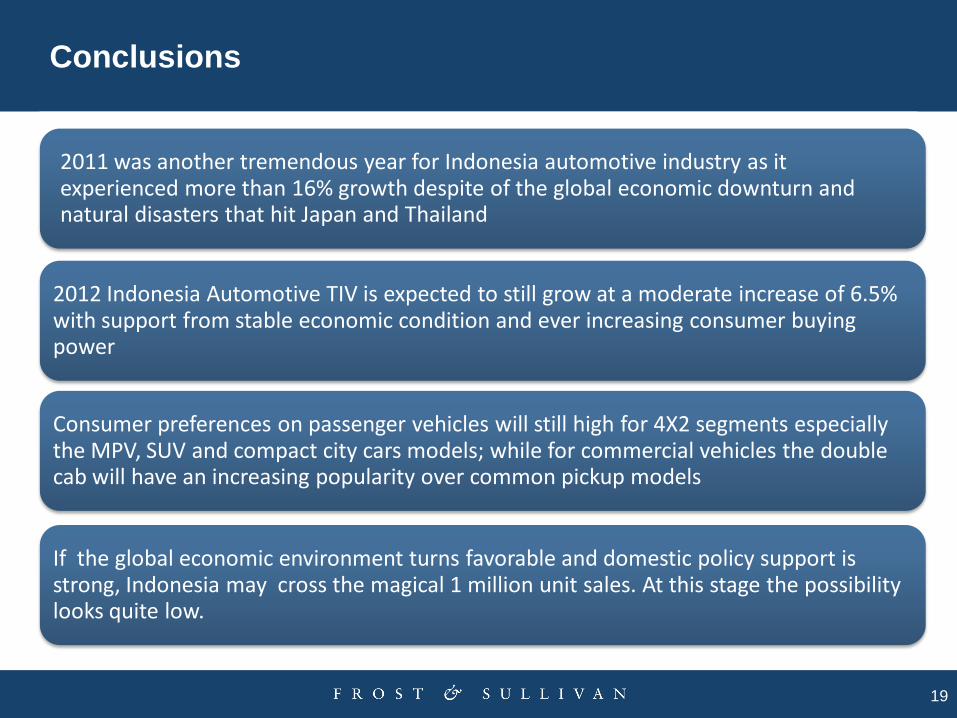

2011 was another tremendous year for Indonesia automotive industry as it experienced more than 16% growth despite of the global economic downturn and natural disasters that hit Japan and Thailand

2012 Indonesia Automotive TIV is expected to still grow at a moderate increase of 6.5% with support from stable economic condition and ever increasing consumer buying power

Consumer preferences on passenger vehicles will still high for 4X2 segments especially the MPV, SUV and compact city cars models; while for commercial vehicles the double cab will have an increasing popularity over common pickup models

If the global economic environment turns favorable and domestic policy support is strong, Indonesia may cross the magical 1 million unit sales. At this stage the possibility looks quite low.