Embed Size (px)

Citation preview

Growth Opportunities in the Turkish Passenger Growth Opportunities in the Turkish Passenger and Electric Vehicle Marketand Electric Vehicle Market

Mohamed Mubarak, Mohamed Mubarak, Program ManagerProgram Manager

Melih Nalcioglu, Melih Nalcioglu, Research ManagerResearch Manager

Automotive & TransportationAutomotive & Transportation

November 2, 2011November 2, 2011

Functional Expertise

� 6 years of experience in strategy consulting and research, having worked on more than 25 European and

Global projects.

- Manage the research and consulting operations in Frost & Sullivan, Turkey

- Managed over 15 strategic projects in last 2 years with Frost & Sullivan, ranging from diverse topics in,

- Market Assessment and Business Opportunity Analysis.

- Product Planning and Diversification Strategy

- New Business Model Planning and Growth Strategy Formation

- Pre-Due Diligence Evaluation

- Competitive Intelligence and Benchmarking

- Sustainable Mobility Concepts in Global Megacities

Industry Expertise

� Experience base covering broad range of industry sectors, leveraging long-standing working relationships with

leading industry participants’ Senior Management.

Today’s Presenter: Mohamed Mubarak

2

leading industry participants’ Senior Management.

� Before Frost & Sullivan, expertise in business development and product management in leading firms :

- Business Development Manager (IT Consulting), HCL Infosystems Ltd, India

- Marketing Executive, Mitsubishi Motors .(JV with Hindustan Motors in India)

What I bring to the Team

• Combined experience of consulting, research and business development.

• Deep industry knowledge of Automotive Industry

• Thought leadership in megacities and smart cities

• Ability to understand client issues and offer optimum solution.

• Presentation, client management and business development skills

Career Highlights

• Best Employee of the Year 2008, Frost & Sullivan.

• Best New Joinee of the Year 2006, HCL Infosystems Ltd.

Education

� Master of Business Administration in Marketing from University of Madras, India

� Bachelor of Engineering in Computer Science and Engineering from Crescent Engineering College, University

of Madras, India.

Mohamed Mubarak M Manager - Research

Frost & SullivanTürkiye

Functional Expertise

• 7 years+ experience in tailor made market research on cross industries in Turkey

• Market oppurtinity assestment

• Strategic partnership and due diligence

• Market entry strategy

Industry Expertise

• Strong track record in advising SME’s and larger companies, particularly in following sectors and industries

• Automotive & Transportation

• Healthcare

• Industrial Automation

Today’s Presenter: Melih Nalcioglu

• Environment & Building Technologies

• Food & Agriculture

What I bring to the Team

• Profound understanding of business processes in various industries

• Extensive experience working on Spanish and German consulting companies

• Extensive experience in approaching to the market from many different perspectives

Career Highlights

• 2011, April, Research Manager in Frost & Sullivan, Istanbul

• 2010 – 2011 Research Consultant in FM Consulting - German Consulting Company, Istanbul

• 2004 – 2010 Market Analyst in Copca (Acc1o) - Spanish Consulting Company, Istanbul

Education

• Bachelor’s degree in Business Administration, from Uludag University, Turkey

Melih NalciogluResearch Manager

Cross Industries

Frost & SullivanEMEA

Istanbul, Turkey

Agenda

Impact of Global Mega Trends on Automotive Industry

Turkish Passenger Vehicle Market – Top Level Analysis

Turkish Electric Vehicle Market – New Opportunity to

4

Turkish Electric Vehicle Market – New Opportunity to Grab

Key Conclusion

The Urbanisation and Mega Trends that will shape tomorrow’s mobility and transportation needs

Integrated Mobility

(smooth inter-modality –

metro, bus, vehicl

Mega Cities & Mega Regions (Over 50 cities by 2025 <10 millions inhabitants)

Vehicle Ownership/Sharing Trends (Over 10

million members of carsharing in Europe and North America by 2016)

Technology Developments

(Integration - mobile payment, cloud

computing, security)

5

Smart and Sustainable Cities (Over 100 smart and sustainable cities with state of the art mobility

& connectivity)

metro, bus, vehicle sharing, etc.)

computing, security)

New Economic Developments (Beyond BRIC – N11

Countries -Infrastructure developments)

Standardisation & Harmonisation (inter-

operability across systems)

Turkey – Urbanization Trend Urban sprawl in each city along with the emergence of mega-corridors will require city-specific sales strategy and dealership networks

Istanbul Megacity

360 Degree CEO Perspective of Turkish Automotive Market: Urbanization Trend, (Turkey), 2010 and 2025360 Degree CEO Perspective of Turkish Automotive Market: Urbanization Trend, (Turkey), 2010 and 2025

Marmara Megacorridor� Istanbul, Bursa, Yalova, Kocaeli and Sakarya

Ankara Greater City

Kocaeli

6

Izmir Metropolian

Ankara

Antalya

KonyaAdana

Şanlıurfa

Bursa

Aegean Megacorridor� Izmir, Manisa and Aydin

Çukurova Megacorridor� Gaziantep, Adana, Mersin and

Hatay

GaziantepMersin

Hatay

Legend Megacity Super City Emerging City

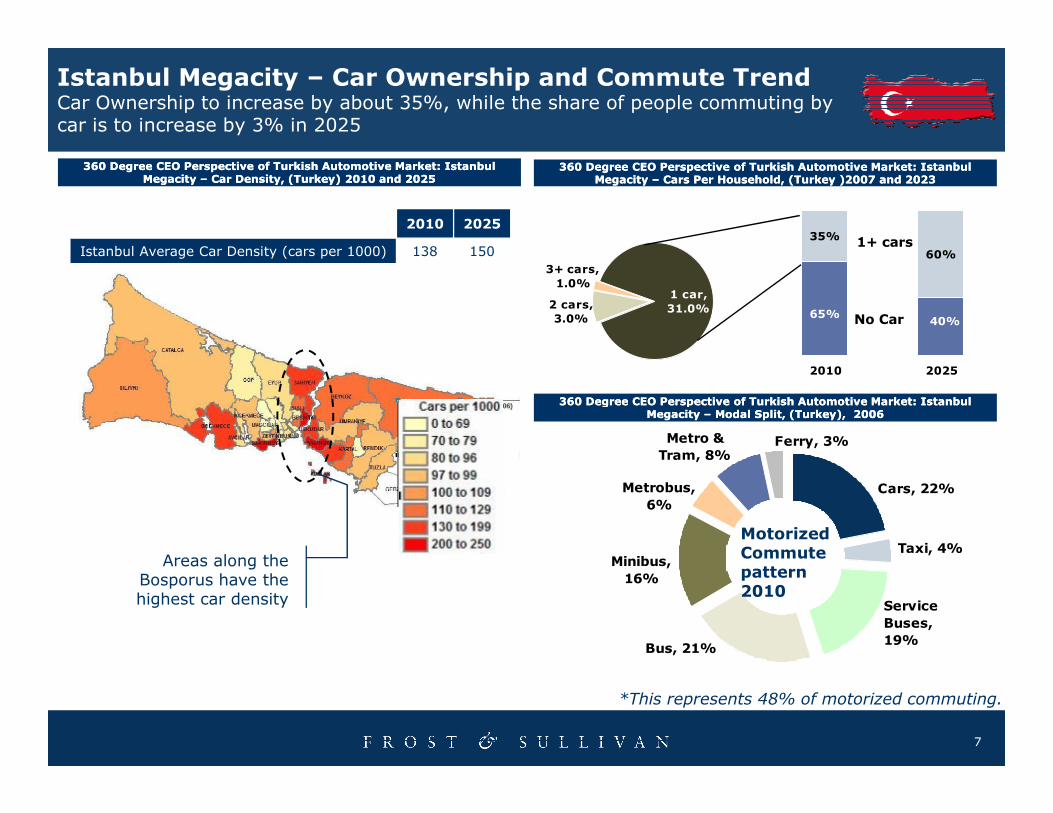

360 Degree CEO Perspective of Turkish Automotive Market: Istanbul 360 Degree CEO Perspective of Turkish Automotive Market: Istanbul Megacity Megacity –– Car Density, (Turkey) 2010 and 2025Car Density, (Turkey) 2010 and 2025

360 Degree CEO Perspective of Turkish Automotive Market: Istanbul 360 Degree CEO Perspective of Turkish Automotive Market: Istanbul Megacity Megacity –– Cars Per Household, (Turkey )2007 and 2023Cars Per Household, (Turkey )2007 and 2023

360 Degree CEO Perspective of Turkish Automotive Market: Istanbul 360 Degree CEO Perspective of Turkish Automotive Market: Istanbul

Istanbul Megacity – Car Ownership and Commute TrendCar Ownership to increase by about 35%, while the share of people commuting by car is to increase by 3% in 2025

3+ cars, 1.0%

2 cars, 3.0%

1 car, 31.0%

2010 2025

Istanbul Average Car Density (cars per 1000) 138 15035%

60%

65%40%

2010 2025

No Car

1+ cars

7

360 Degree CEO Perspective of Turkish Automotive Market: Istanbul 360 Degree CEO Perspective of Turkish Automotive Market: Istanbul Megacity Megacity –– Modal Split, (Turkey), 2006Modal Split, (Turkey), 2006

Areas along the Bosporus have the highest car density

Metro & Tram, 8%

Ferry, 3%

Metrobus, 6%

Minibus, 16%

Bus, 21%

Service Buses, 19%

Cars, 22%

Taxi, 4%Motorized Commute pattern 2010

*This represents 48% of motorized commuting.

Agenda

Impact of Global Megatrends on Automotive Industry

Turkish Passenger Vehicle Market – Top Level Analysis

Turkish Electric Vehicle Market – New Opportunity to

8

Turkish Electric Vehicle Market – New Opportunity to Grab

Key Conclusion

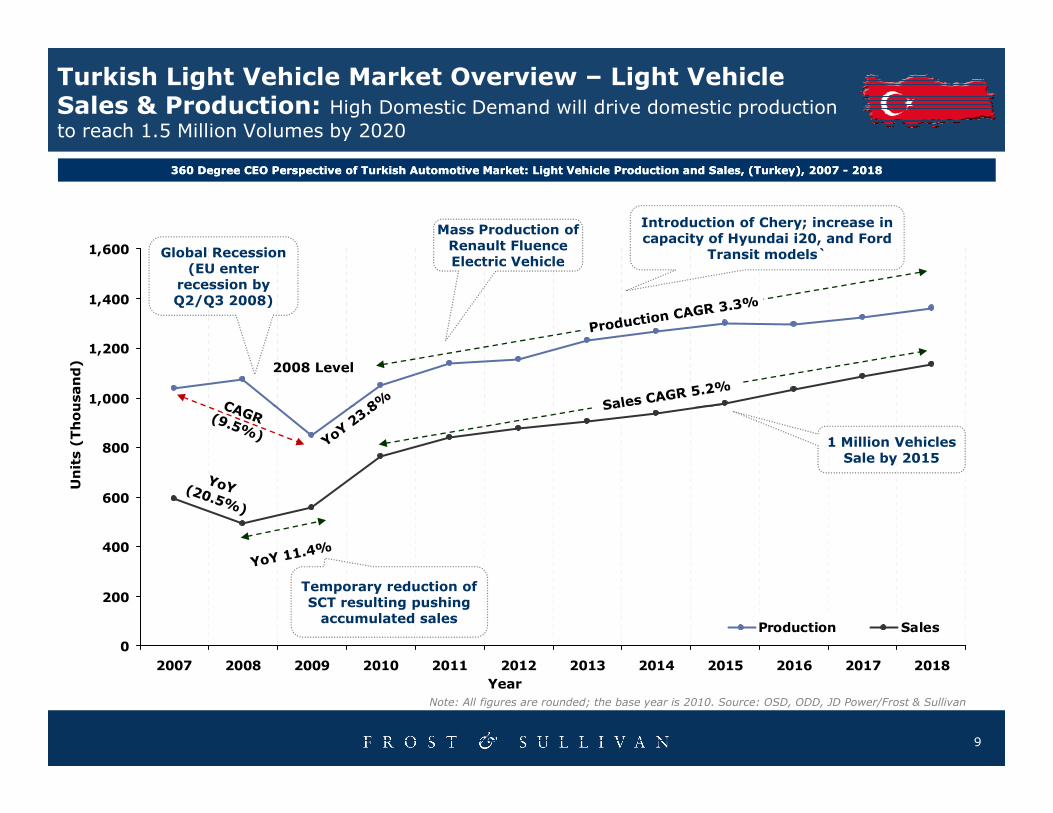

Turkish Light Vehicle Market Overview – Light Vehicle Sales & Production: High Domestic Demand will drive domestic production

to reach 1.5 Million Volumes by 2020

1,000

1,200

1,400

1,600

Units (Thousand) 2008 Level

Global Recession (EU enter

recession by Q2/Q3 2008)

Introduction of Chery; increase in capacity of Hyundai i20, and Ford

Transit models`

Mass Production of Renault Fluence Electric Vehicle

360 Degree CEO Perspective of Turkish Automotive Market: Light Vehicle Production and Sales, (Turkey), 2007 360 Degree CEO Perspective of Turkish Automotive Market: Light Vehicle Production and Sales, (Turkey), 2007 -- 20182018

9

0

200

400

600

800

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Production Sales

Units (Thousand)

YearNote: All figures are rounded; the base year is 2010. Source: OSD, ODD, JD Power/Frost & Sullivan

Temporary reduction of SCT resulting pushing accumulated sales

1 Million Vehicles Sale by 2015

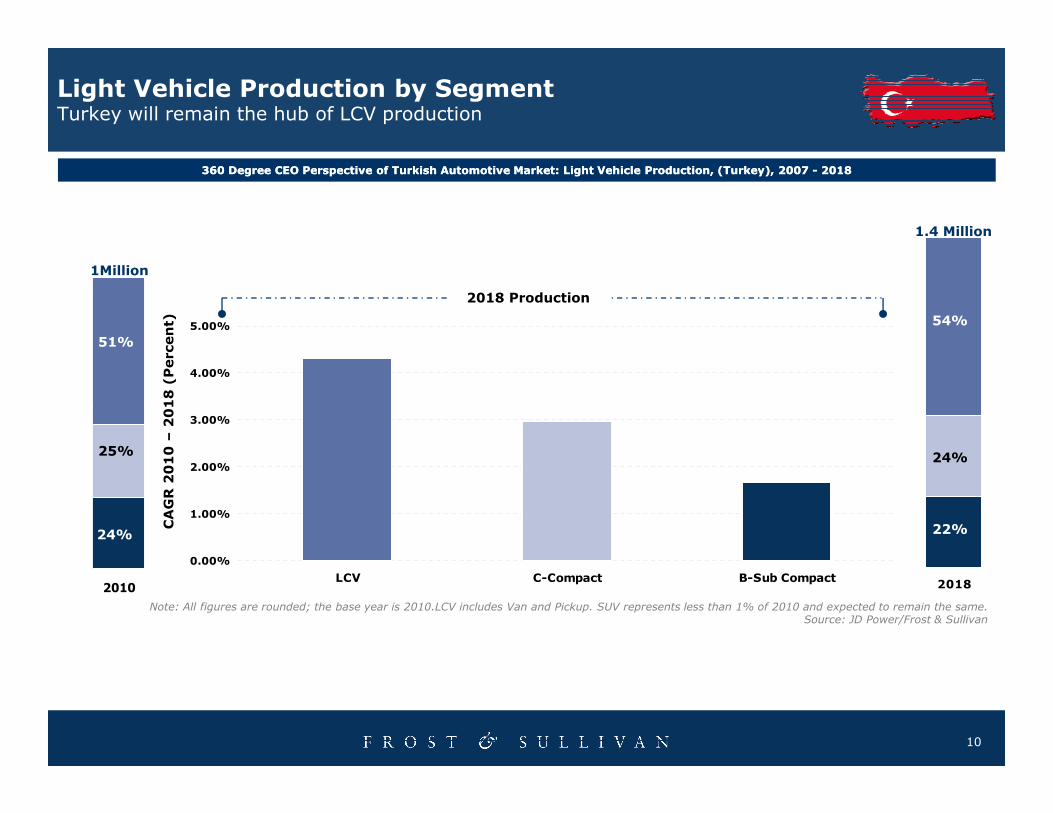

Light Vehicle Production by SegmentTurkey will remain the hub of LCV production

4.00%

5.00%

1Million

1.4 Million

2018 Production

360 Degree CEO Perspective of Turkish Automotive Market: Light Vehicle Production, (Turkey), 2007 360 Degree CEO Perspective of Turkish Automotive Market: Light Vehicle Production, (Turkey), 2007 -- 201820182018 (Percent)

51%

54%

10

0.00%

1.00%

2.00%

3.00%

LCV C-Compact B-Sub Compact2010 2018

CAGR 2010 –

2018 (Percent)

Note: All figures are rounded; the base year is 2010.LCV includes Van and Pickup. SUV represents less than 1% of 2010 and expected to remain the same. Source: JD Power/Frost & Sullivan

25%

24%

24%

22%

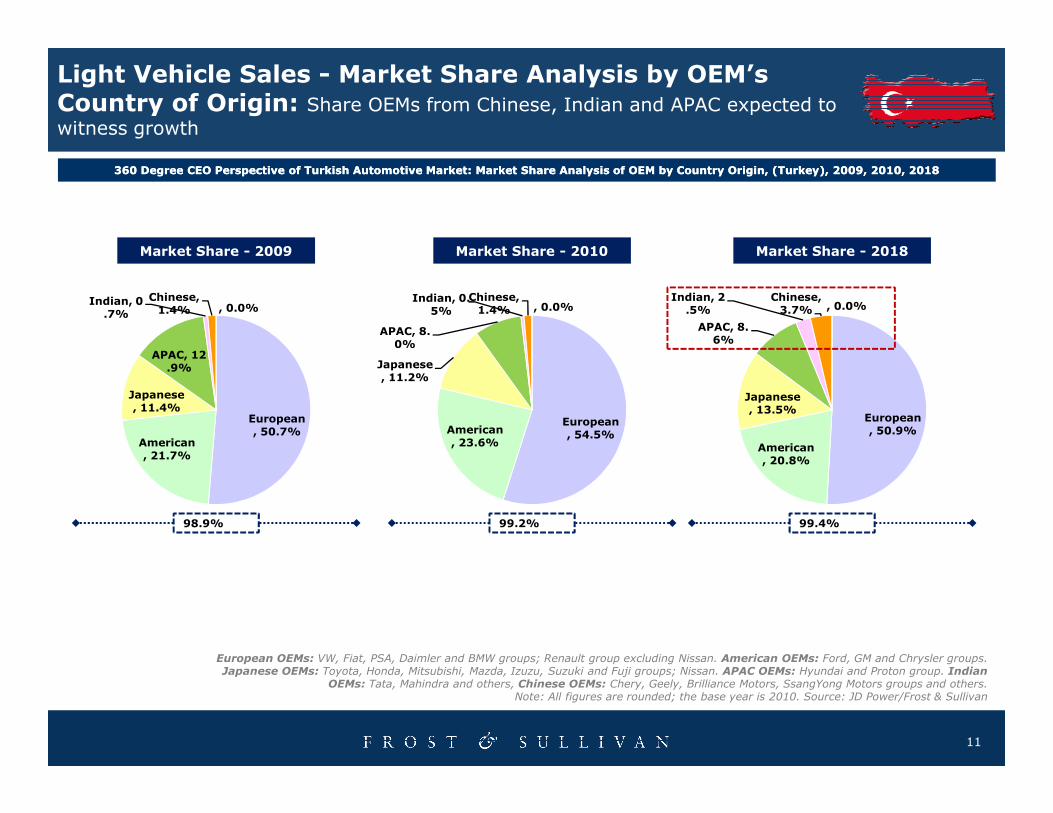

Light Vehicle Sales - Market Share Analysis by OEM’s Country of Origin: Share OEMs from Chinese, Indian and APAC expected to

witness growth

Japanese, 11.4%

APAC, 12.9%

Indian, 0.7%

Chinese, 1.4% , 0.0%

Market Share - 2009

Japanese, 11.2%

APAC, 8.0%

Indian, 0.5%

Chinese, 1.4% , 0.0%

Market Share - 2010

Japanese, 13.5%

APAC, 8.6%

Indian, 2.5%

Chinese, 3.7% , 0.0%

Market Share - 2018

360 Degree CEO Perspective of Turkish Automotive Market: 360 Degree CEO Perspective of Turkish Automotive Market: Market Share Analysis of OEM by Country Origin, Market Share Analysis of OEM by Country Origin, (Turkey), (Turkey), 2009, 2010, 20182009, 2010, 2018

11

European, 50.7%

American, 21.7%

, 11.4%

98.9%

European, 54.5%American

, 23.6%

99.2%

European, 50.9%

American, 20.8%

, 13.5%

99.4%

European OEMs: VW, Fiat, PSA, Daimler and BMW groups; Renault group excluding Nissan. American OEMs: Ford, GM and Chrysler groups. Japanese OEMs: Toyota, Honda, Mitsubishi, Mazda, Izuzu, Suzuki and Fuji groups; Nissan. APAC OEMs: Hyundai and Proton group. Indian

OEMs: Tata, Mahindra and others, Chinese OEMs: Chery, Geely, Brilliance Motors, SsangYong Motors groups and others.Note: All figures are rounded; the base year is 2010. Source: JD Power/Frost & Sullivan

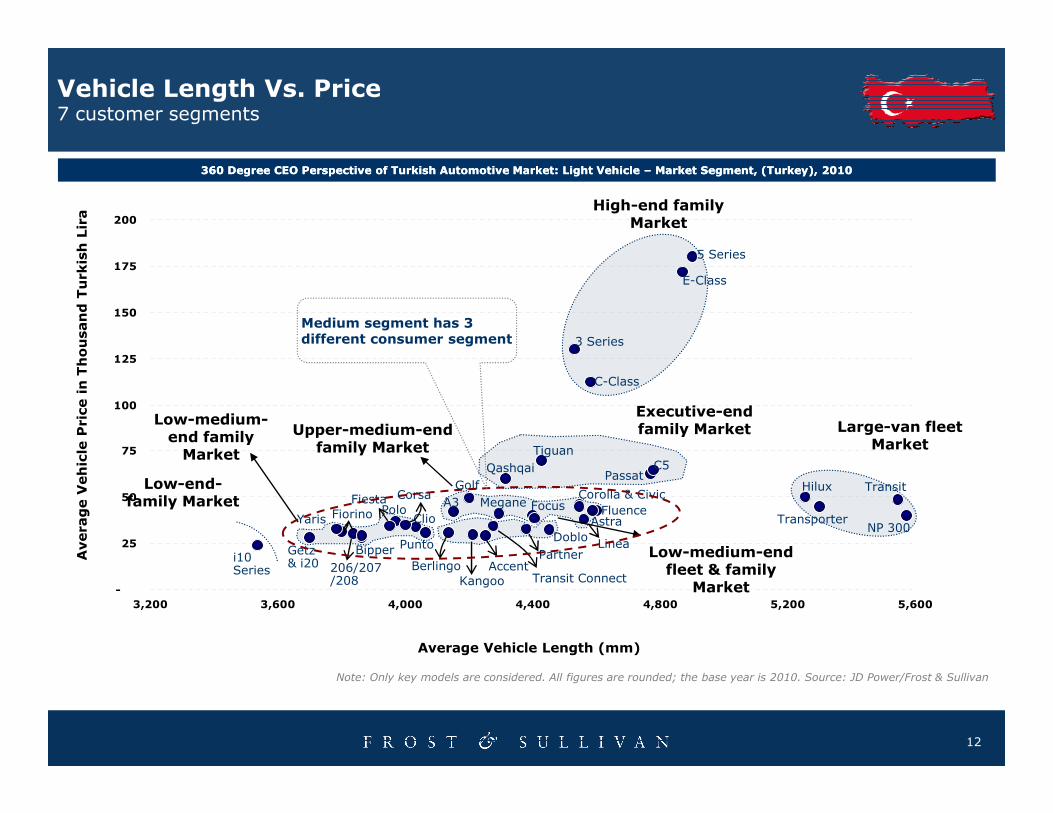

Vehicle Length Vs. Price7 customer segments

360 Degree CEO Perspective of Turkish Automotive Market: Light Vehicle 360 Degree CEO Perspective of Turkish Automotive Market: Light Vehicle –– Market Segment, (Turkey), 2010Market Segment, (Turkey), 2010

100

125

150

175

200

5 Series

E-Class

3 Series

C-Class

Average Vehicle Price in Thousand Turkish Lira

High-end family Market

Executive-end

Medium segment has 3 different consumer segment

12

-

25

50

75

100

3,200 3,600 4,000 4,400 4,800 5,200 5,600

Transit

i10 Series

Getz & i20

Yaris Fiorino

Bipper

FiestaPolo

Corsa

Clio

Punto

Berlingo

A3

Golf

Kangoo

NP 300Transporter

Hilux

C5Passat

FluenceAstra

Linea

Corolla & Civic

Tiguan

Qashqai

Megane

Doblo

Focus

Partner206/207/208

AccentTransit Connect

Average Vehicle Price in Thousand Turkish Lira

Average Vehicle Length (mm)

Note: Only key models are considered. All figures are rounded; the base year is 2010. Source: JD Power/Frost & Sullivan

Low-end-family Market

Low-medium-end family Market

Large-van fleet Market

Executive-end family MarketUpper-medium-end

family Market

Low-medium-end fleet & family

Market

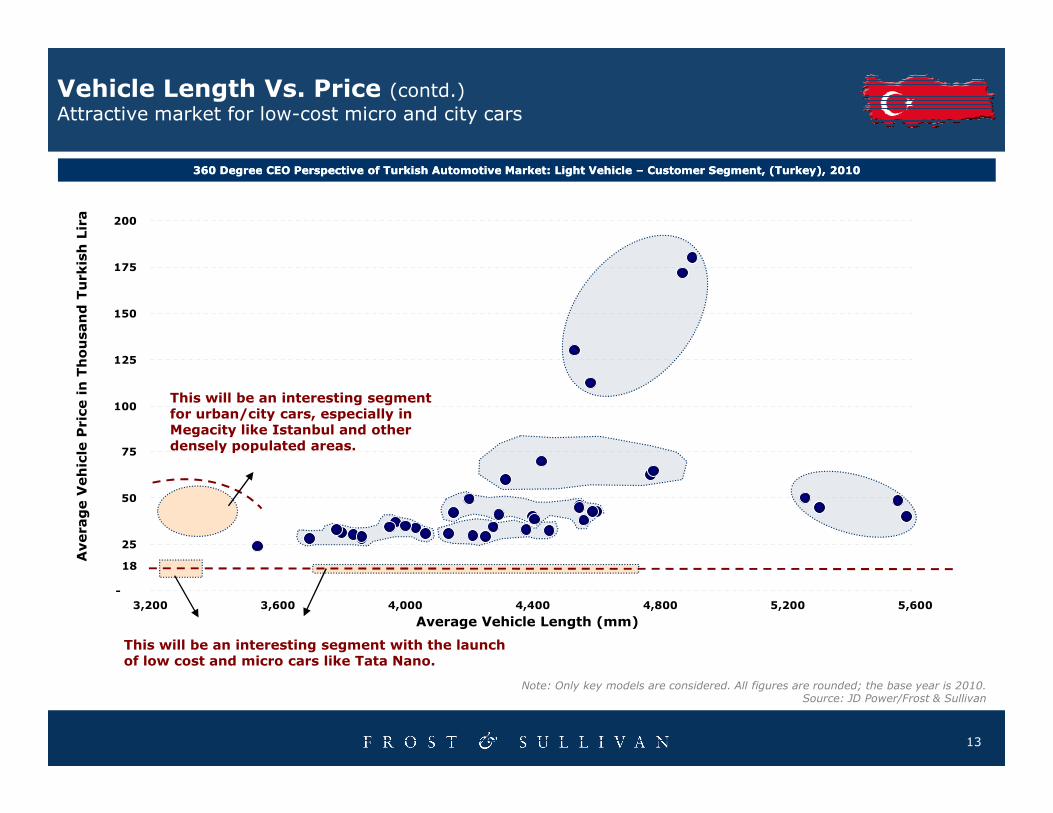

Vehicle Length Vs. Price (contd.)Attractive market for low-cost micro and city cars

360 Degree CEO Perspective of Turkish Automotive Market: Light Vehicle 360 Degree CEO Perspective of Turkish Automotive Market: Light Vehicle –– Customer Segment, (Turkey), 2010Customer Segment, (Turkey), 2010

100

125

150

175

200

Average Vehicle Price in Thousand Turkish Lira

This will be an interesting segment for urban/city cars, especially in

13

-

25

50

75

100

3,200 3,600 4,000 4,400 4,800 5,200 5,600

Average Vehicle Price in Thousand Turkish Lira

Average Vehicle Length (mm)

18

This will be an interesting segment with the launch of low cost and micro cars like Tata Nano.

Note: Only key models are considered. All figures are rounded; the base year is 2010. Source: JD Power/Frost & Sullivan

for urban/city cars, especially in Megacity like Istanbul and other densely populated areas.

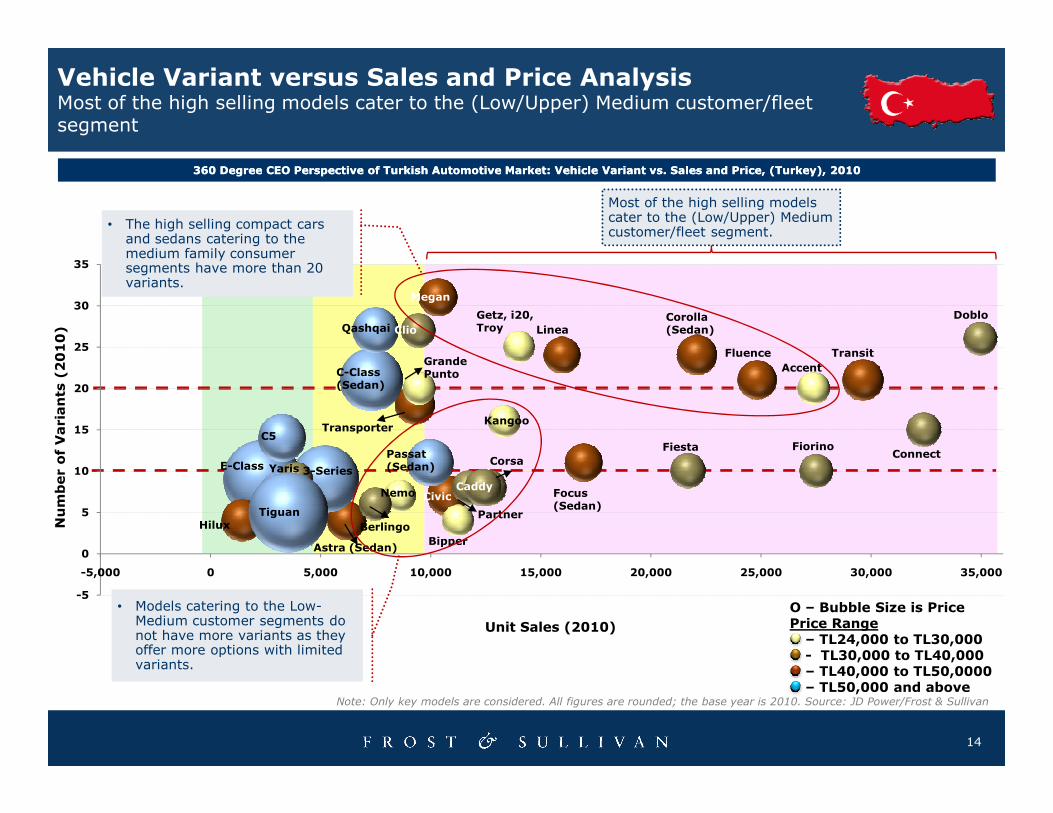

Vehicle Variant versus Sales and Price AnalysisMost of the high selling models cater to the (Low/Upper) Medium customer/fleet segment

20

25

30

35

Doblo

TransitAccent

Fluence

Corolla (Sedan)Linea

Getz, i20, Troy

Megan

Grande Punto

Qashqai

C-Class (Sedan)

Clio

Number of Variants (2010)

Most of the high selling models cater to the (Low/Upper) Medium customer/fleet segment.

360 Degree CEO Perspective of Turkish Automotive Market: Vehicle Variant vs. Sales and Price, (Turkey), 2010360 Degree CEO Perspective of Turkish Automotive Market: Vehicle Variant vs. Sales and Price, (Turkey), 2010

• The high selling compact cars and sedans catering to the medium family consumer segments have more than 20 variants.

14

-5

0

5

10

15

-5,000 0 5,000 10,000 15,000 20,000 25,000 30,000 35,000

Fiesta FiorinoConnect

TransporterKangoo

C5

E-Class 3-Series

Passat (Sedan)Yaris

HiluxTiguan

Astra (Sedan)

Berlingo

NemoCaddy

Corsa

Focus (Sedan)

Partner

Bipper

Civic

Number of Variants (2010)

Unit Sales (2010)

O – Bubble Size is PricePrice RangeO – TL24,000 to TL30,000O - TL30,000 to TL40,000O – TL40,000 to TL50,0000O – TL50,000 and above

• Models catering to the Low-Medium customer segments do not have more variants as they offer more options with limited variants.

Note: Only key models are considered. All figures are rounded; the base year is 2010. Source: JD Power/Frost & Sullivan

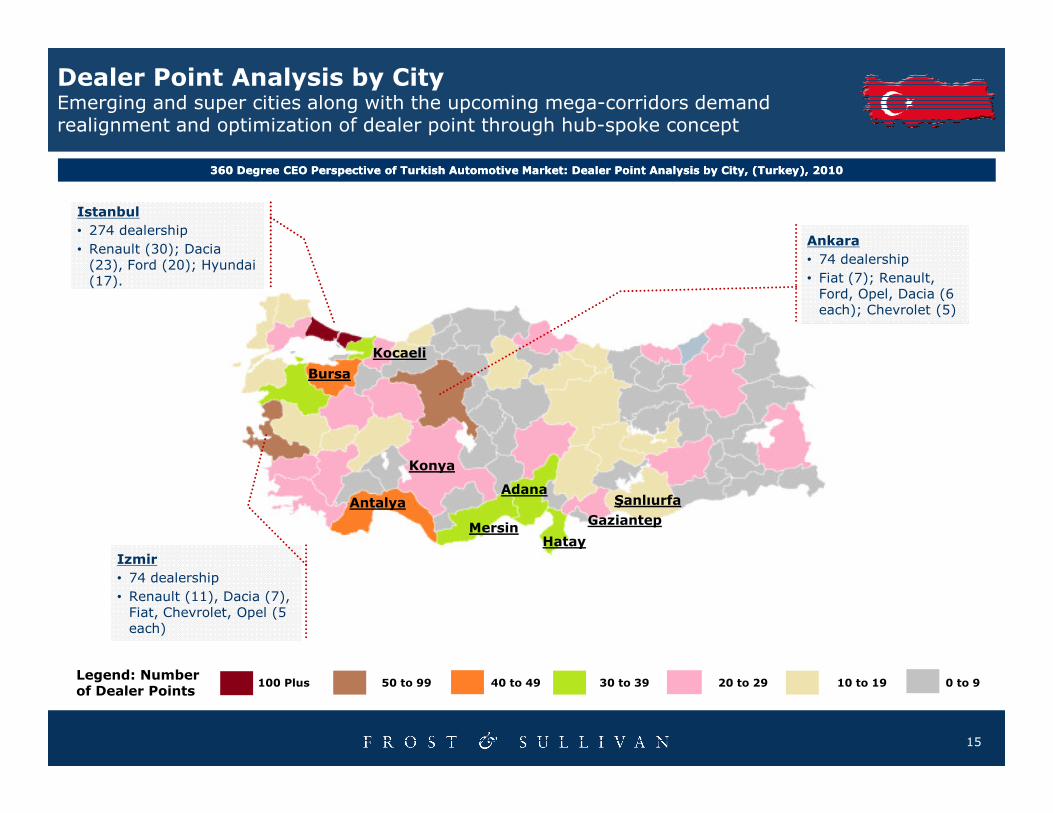

Dealer Point Analysis by CityEmerging and super cities along with the upcoming mega-corridors demand realignment and optimization of dealer point through hub-spoke concept

Bursa

Kocaeli

360 Degree CEO Perspective of Turkish Automotive Market: 360 Degree CEO Perspective of Turkish Automotive Market: Dealer Point Analysis by City, Dealer Point Analysis by City, (Turkey), 2010(Turkey), 2010

Ankara• 74 dealership

• Fiat (7); Renault, Ford, Opel, Dacia (6 each); Chevrolet (5)

Istanbul• 274 dealership

• Renault (30); Dacia (23), Ford (20); Hyundai (17).

15

Konya

Antalya

Mersin

Adana

Hatay

Gaziantep

Şanlıurfa

Izmir• 74 dealership

• Renault (11), Dacia (7), Fiat, Chevrolet, Opel (5 each)

100 Plus 50 to 99 40 to 49 30 to 39 20 to 29 10 to 19 0 to 9Legend: Number of Dealer Points

Agenda

Impact of Global Megatrends on Automotive Industry

Turkish Passenger Vehicle Market – Top Level Analysis

Turkish Electric Vehicle Market – New Opportunity to

16

Turkish Electric Vehicle Market – New Opportunity to Grab

Key Conclusion

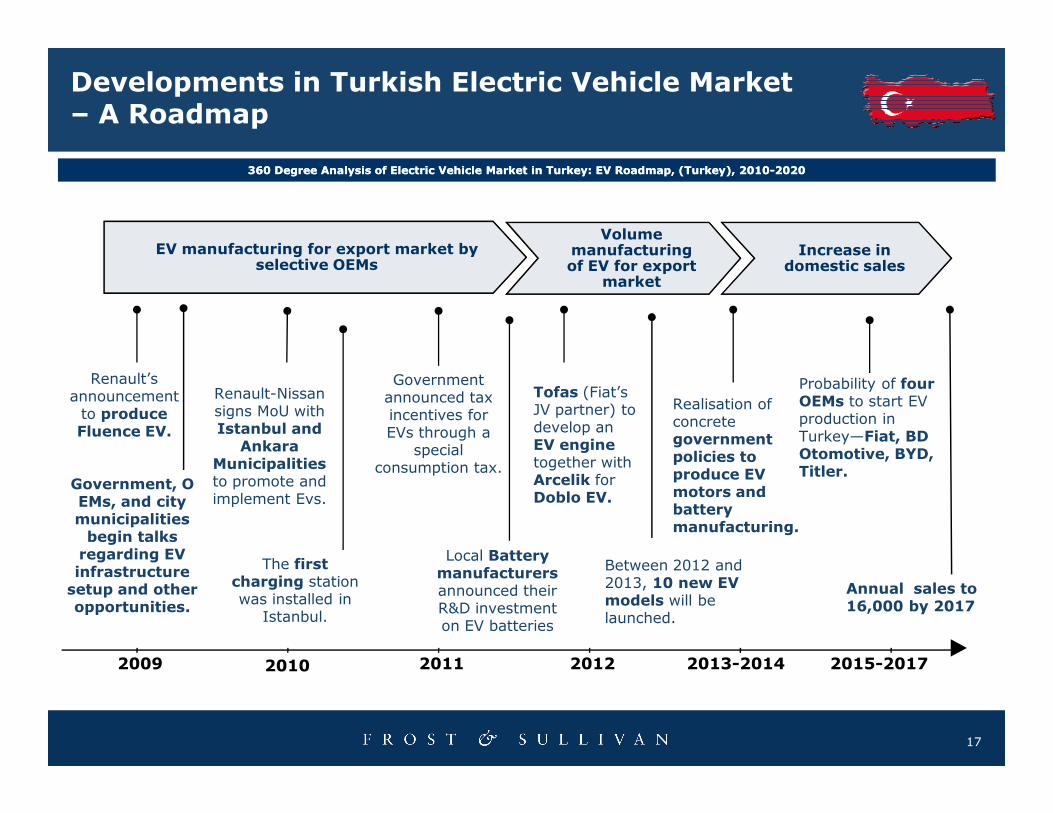

Developments in Turkish Electric Vehicle Market – A Roadmap

Increase in domestic sales

Volume manufacturingof EV for export

market

EV manufacturing for export market by selective OEMs

Renault’s announcement to produce

360 Degree 360 Degree Analysis of Electric Vehicle Market in TurkeyAnalysis of Electric Vehicle Market in Turkey: : EV EV Roadmap,Roadmap, (Turkey), 2010(Turkey), 2010--20202020

Renault-Nissan signs MoU with

Government announced tax incentives for

Tofas (Fiat’s JV partner) to Realisation of

Probability of four OEMs to start EV

17

2009 2010 2011 2012 2013-2014 2015-2017

to produce Fluence EV.

Government, OEMs, and city municipalities begin talks regarding EV infrastructure setup and other opportunities.

signs MoU with Istanbul and

Ankara Municipalities to promote and implement Evs.

incentives for EVs through a

special consumption tax.

JV partner) to develop an EV engine together with Arcelik for Doblo EV.

Realisation of concrete government policies to produce EV motors and battery manufacturing.

OEMs to start EV production in Turkey—Fiat, BD Otomotive, BYD, Titler.

Annual sales to 16,000 by 2017

Between 2012 and 2013, 10 new EV models will be launched.

Local Battery manufacturers announced their R&D investment on EV batteries

The first charging station was installed in

Istanbul.

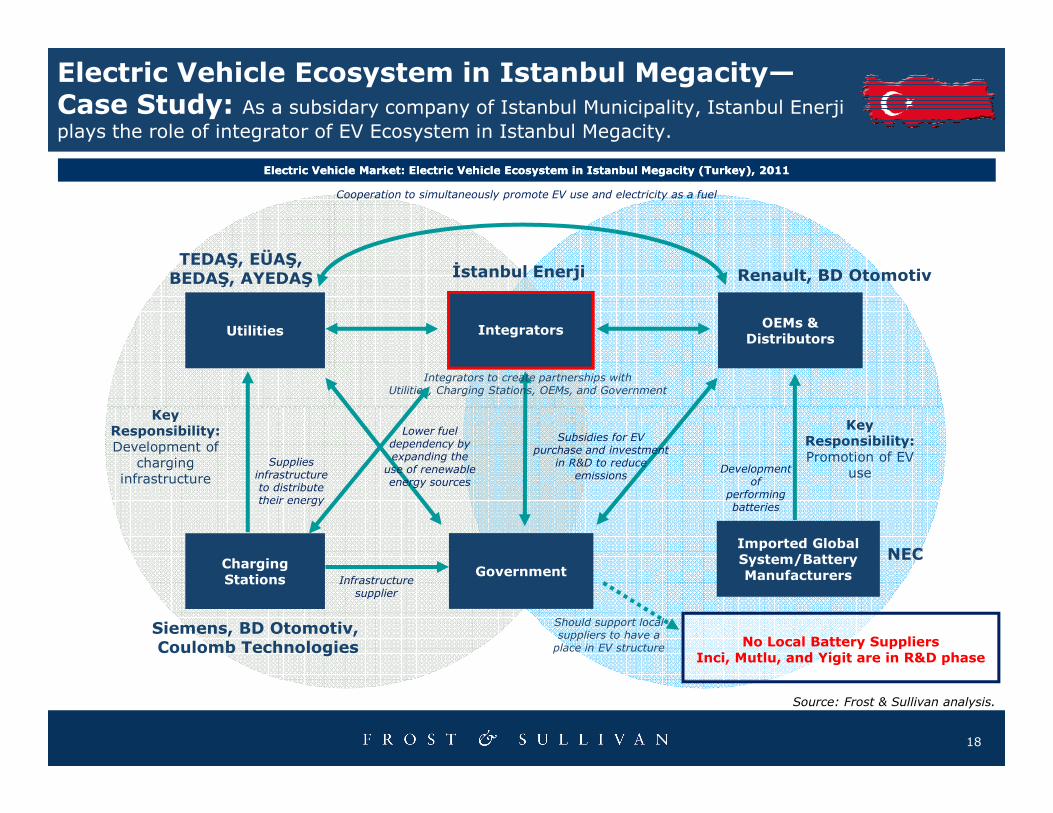

Electric Vehicle Ecosystem in Istanbul Megacity—Case Study: As a subsidary company of Istanbul Municipality, Istanbul Enerji

plays the role of integrator of EV Ecosystem in Istanbul Megacity.

Utilities Integrators OEMs & Distributors

Integrators to create partnerships with Utilities, Charging Stations, OEMs, and Government

Key

Cooperation to simultaneously promote EV use and electricity as a fuel

Electric Vehicle MarketElectric Vehicle Market:: Electric Vehicle Ecosystem in Istanbul Megacity (TurkeyElectric Vehicle Ecosystem in Istanbul Megacity (Turkey), ), 20120111

Renault, BD Otomotivİstanbul EnerjiTEDAŞ, EÜAŞ, BEDAŞ, AYEDAŞ

18

Imported Global System/Battery ManufacturersGovernment

Charging Stations

No Local Battery Suppliers Inci, Mutlu, and Yigit are in R&D phase

Lower fuel dependency by expanding the

use of renewable energy sources

Subsidies for EV purchase and investment

in R&D to reduce emissions

Development of

performing batteries

Supplies infrastructure to distribute their energy

Infrastructure supplier

Key Responsibility: Development of

charging infrastructure

Key Responsibility:Promotion of EV

use

Should support local suppliers to have aplace in EV structure

Source: Frost & Sullivan analysis.

NEC

Siemens, BD Otomotiv, Coulomb Technologies

AnkaraBursa

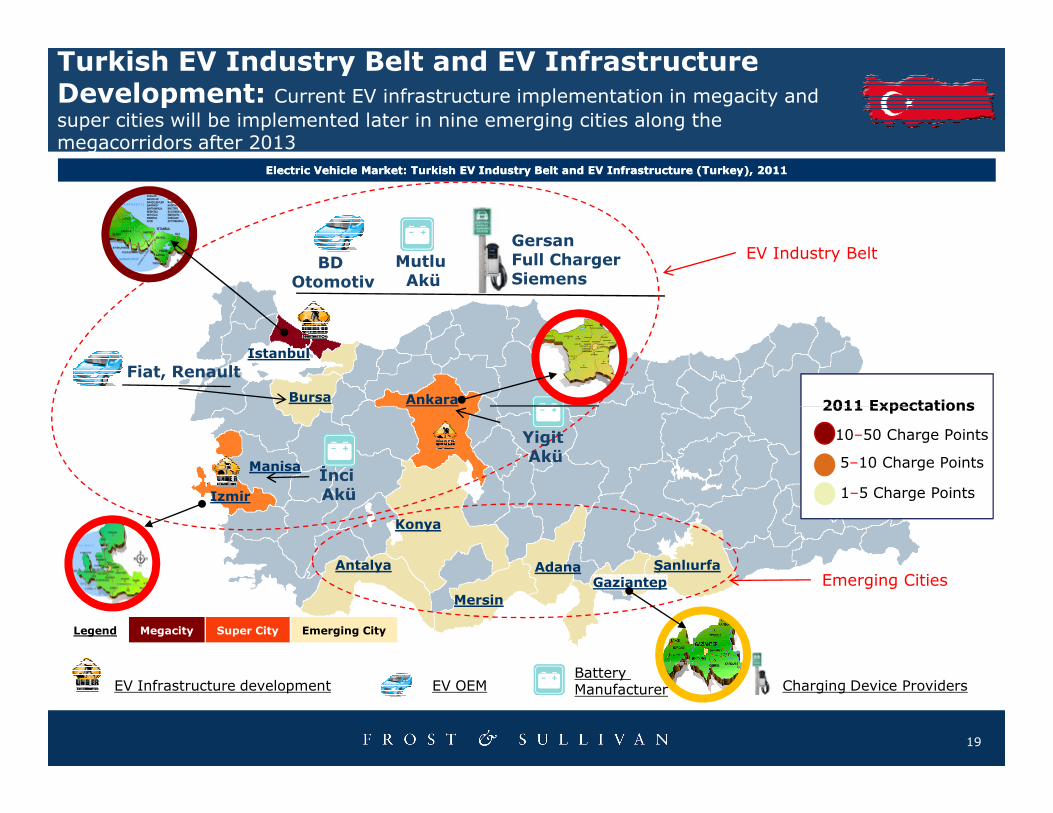

Turkish EV Industry Belt and EV Infrastructure Development: Current EV infrastructure implementation in megacity and

super cities will be implemented later in nine emerging cities along the megacorridors after 2013

Electric Vehicle MarketElectric Vehicle Market:: Turkish EVTurkish EV Industry Belt and EV Infrastructure (Industry Belt and EV Infrastructure (TurkeyTurkey), ), 20120111

Istanbul

EV Industry Belt

2011 Expectations

Fiat, Renault

BD Otomotiv

Mutlu Akü

GersanFull ChargerSiemens

19

Antalya

Konya

Adana Şanlıurfa

Manisa

EV Infrastructure development

Izmir

EV OEMBattery Manufacturer Charging Device Providers

Emerging Cities

Legend Megacity Super City Emerging City

Mersin

10–50 Charge Points

5–10 Charge Points

1–5 Charge Points

2011 Expectations

Gaziantep

Yigit Akü

İnci Akü

0

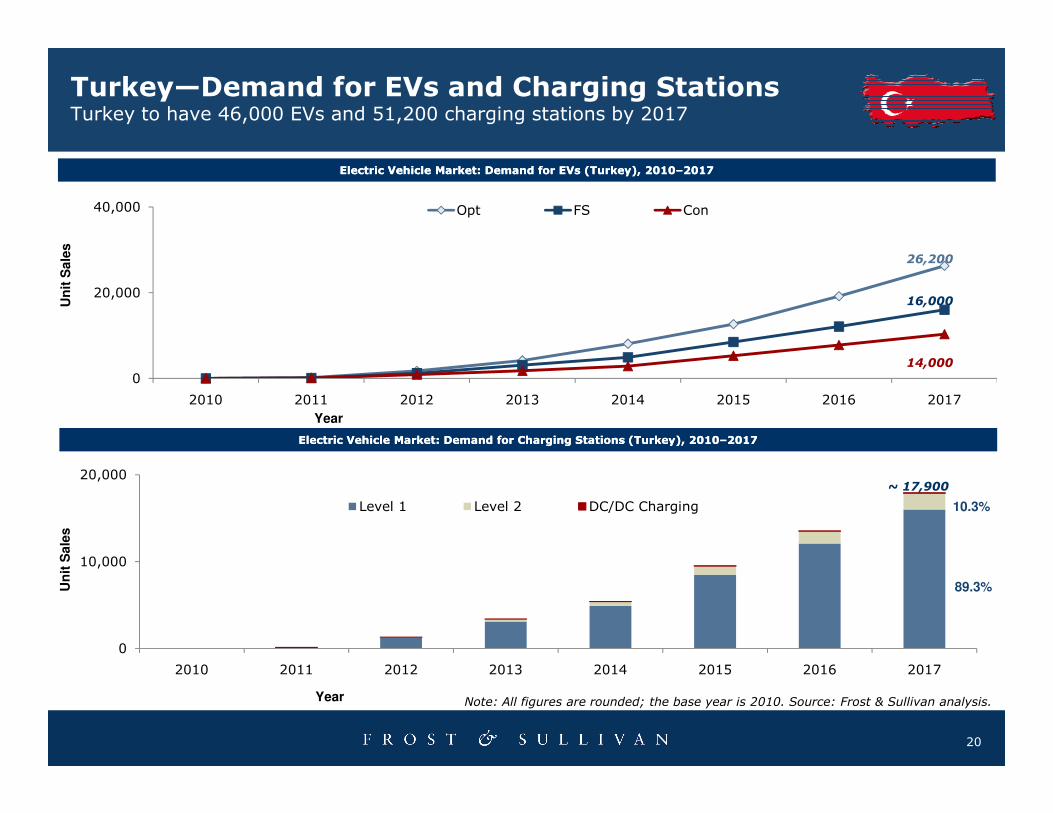

20,000

40,000

2010 2011 2012 2013 2014 2015 2016 2017

Opt FS Con

Turkey—Demand for EVs and Charging StationsTurkey to have 46,000 EVs and 51,200 charging stations by 2017

Electric Vehicle MarketElectric Vehicle Market:: Demand for EVsDemand for EVs (Turkey(Turkey), ), 20102010––20120177

Un

it S

ale

s

16,000

26,200

14,000

20

0

10,000

20,000

2010 2011 2012 2013 2014 2015 2016 2017

Level 1 Level 2 DC/DC Charging

2010 2011 2012 2013 2014 2015 2016 2017

Un

it S

ale

s

Year

Year

~ 17,900

89.3%

10.3%

Electric Vehicle MarketElectric Vehicle Market:: Demand for Charging StationsDemand for Charging Stations (Turkey(Turkey), ), 20102010––20120177

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan analysis.

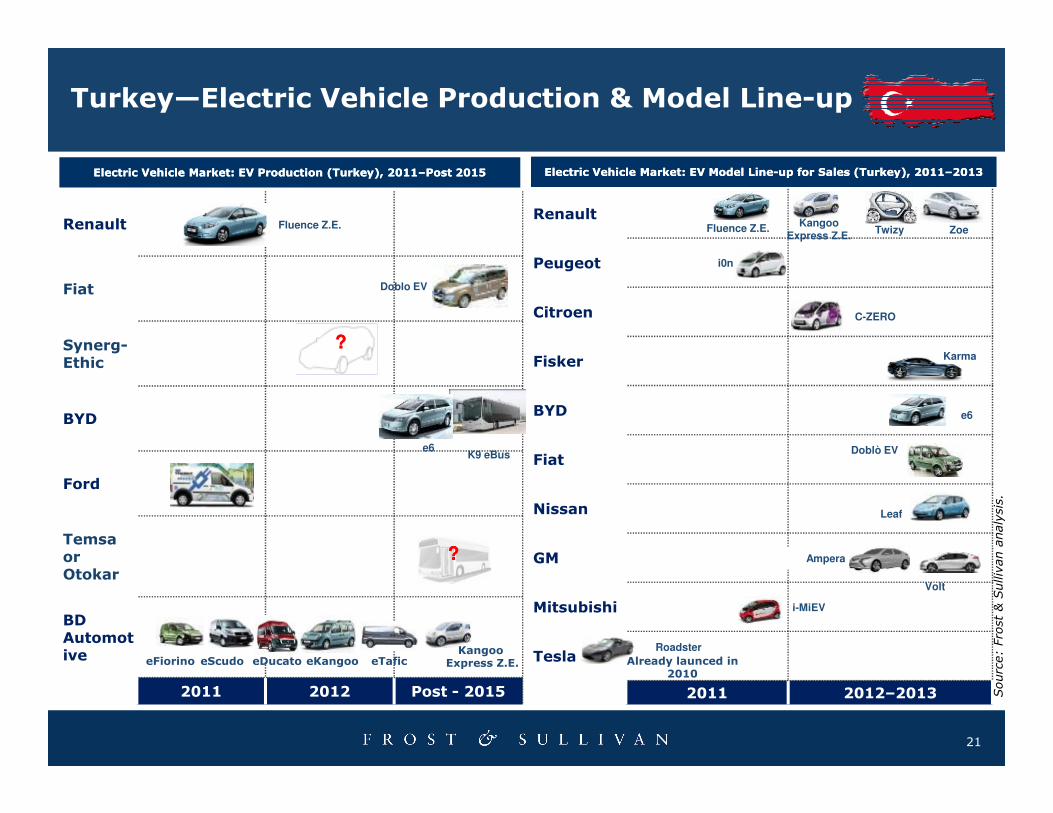

Turkey—Electric Vehicle Production & Model Line-up

Renault

Peugeot

Citroen

Fisker

BYD

Renault

Fiat

Synerg-Ethic

Fluence Z.E.

Doblo EV

??

Fluence Z.E.

i0n

Kangoo Express Z.E.

Twizy

C-ZERO

Zoe

Electric Vehicle MarketElectric Vehicle Market:: EV EV ProductionProduction (Turkey(Turkey), 201), 20111––Post Post 20152015 Electric Vehicle MarketElectric Vehicle Market:: EV Model EV Model LineLine--up up for for SalesSales (Turkey(Turkey), 201), 20111––20132013

Karma

21

BYD

Fiat

Nissan

GM

Mitsubishi

Tesla

2011 2012–2013

BYD

Ford

Temsaor Otokar

BD Automotive

2011 2012 Post - 2015

e6K9 eBus

eFiorino eScudo eDucato eKangoo eTaficKangoo

Express Z.E.

??

e6

i-MiEV

Ampera

Roadster

Volt

Leaf

Doblò EV

Already launced in 2010

Source: Frost & Sullivan analysis.

Agenda

Impact of Global Megatrends on Automotive Industry

Turkish Passenger Vehicle Market – Top Level Analysis

Turkish Electric Vehicle Market – New Opportunity to

22

Turkish Electric Vehicle Market – New Opportunity to Grab

Key Conclusion

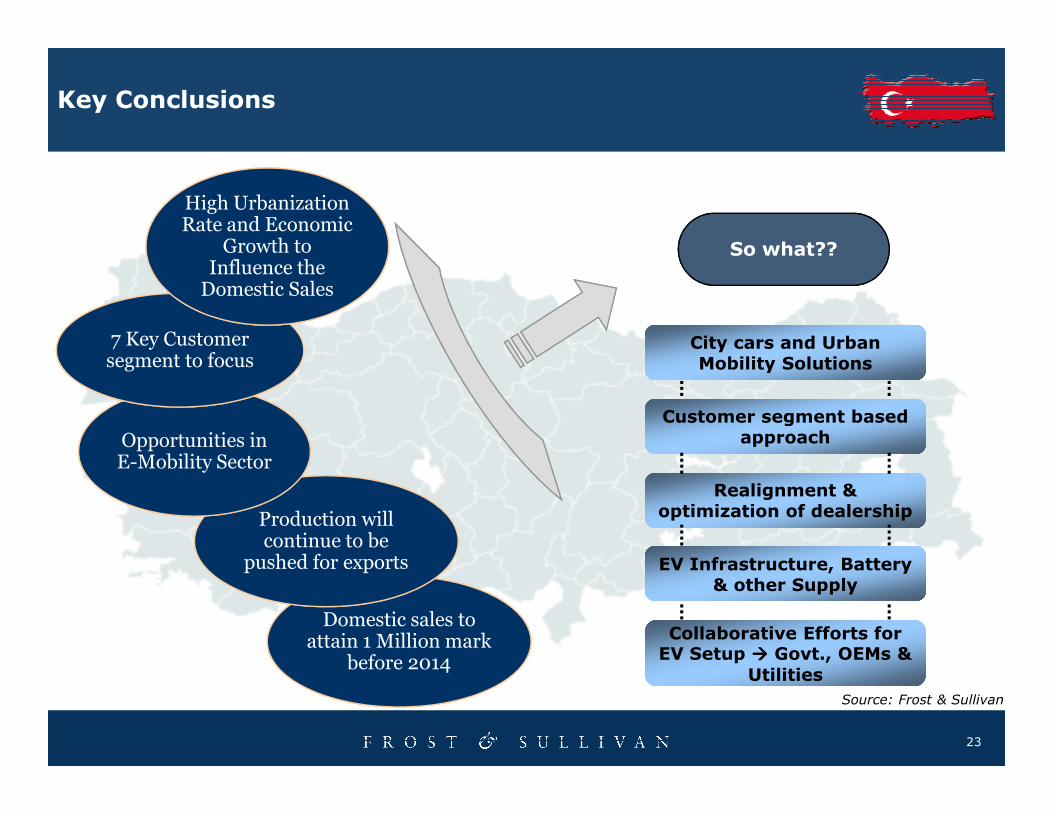

Key Conclusions

7 Key Customer segment to focus

High Urbanization Rate and Economic

Growth to Influence the Domestic Sales

City cars and Urban Mobility Solutions

Customer segment based

So what??

23

Domestic sales to attain 1 Million mark

before 2014

Production will continue to be

pushed for exports

Opportunities in E-Mobility Sector

Customer segment based approach

Realignment & optimization of dealership

EV Infrastructure, Battery & other Supply

Collaborative Efforts for EV Setup ���� Govt., OEMs &

UtilitiesSource: Frost & Sullivan

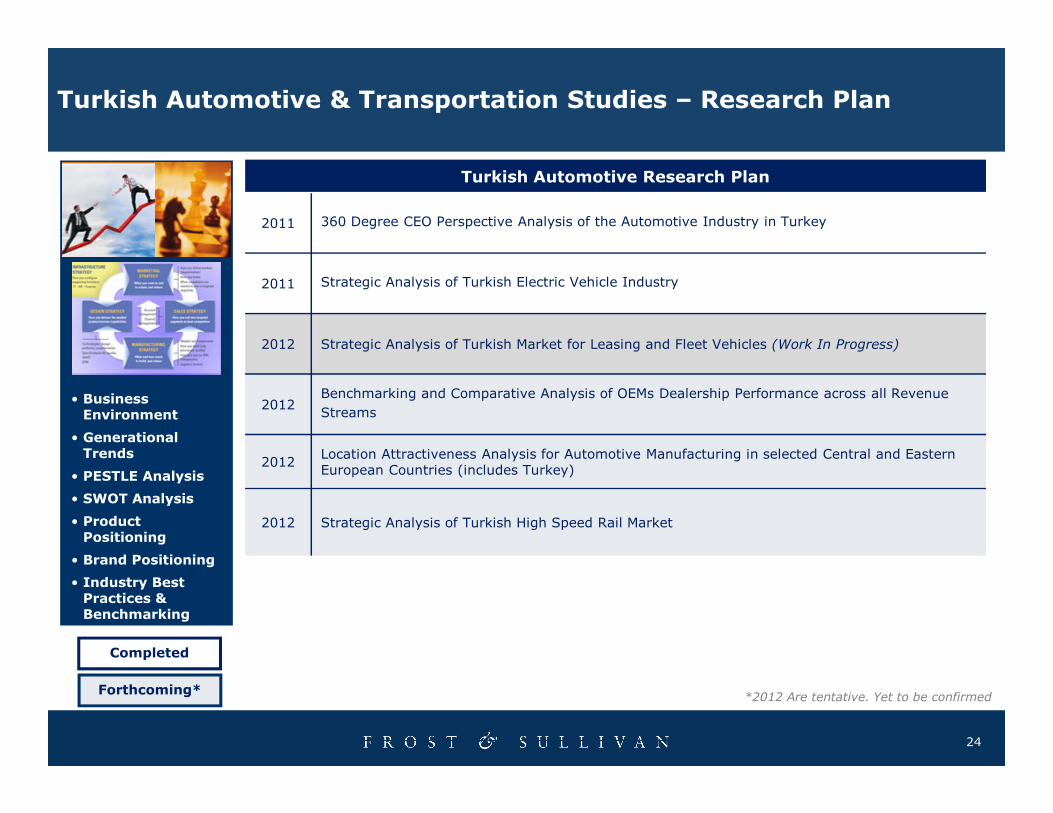

Turkish Automotive & Transportation Studies – Research Plan

• Business Environment

Turkish Automotive Research Plan

2011 360 Degree CEO Perspective Analysis of the Automotive Industry in Turkey

2011 Strategic Analysis of Turkish Electric Vehicle Industry

2012 Strategic Analysis of Turkish Market for Leasing and Fleet Vehicles (Work In Progress)

2012Benchmarking and Comparative Analysis of OEMs Dealership Performance across all Revenue

Streams

24

Environment

• Generational Trends

• PESTLE Analysis

• SWOT Analysis

• Product Positioning

• Brand Positioning

• Industry Best Practices & Benchmarking

2012Streams

2012Location Attractiveness Analysis for Automotive Manufacturing in selected Central and Eastern European Countries (includes Turkey)

2012 Strategic Analysis of Turkish High Speed Rail Market

Completed

Forthcoming**2012 Are tentative. Yet to be confirmed

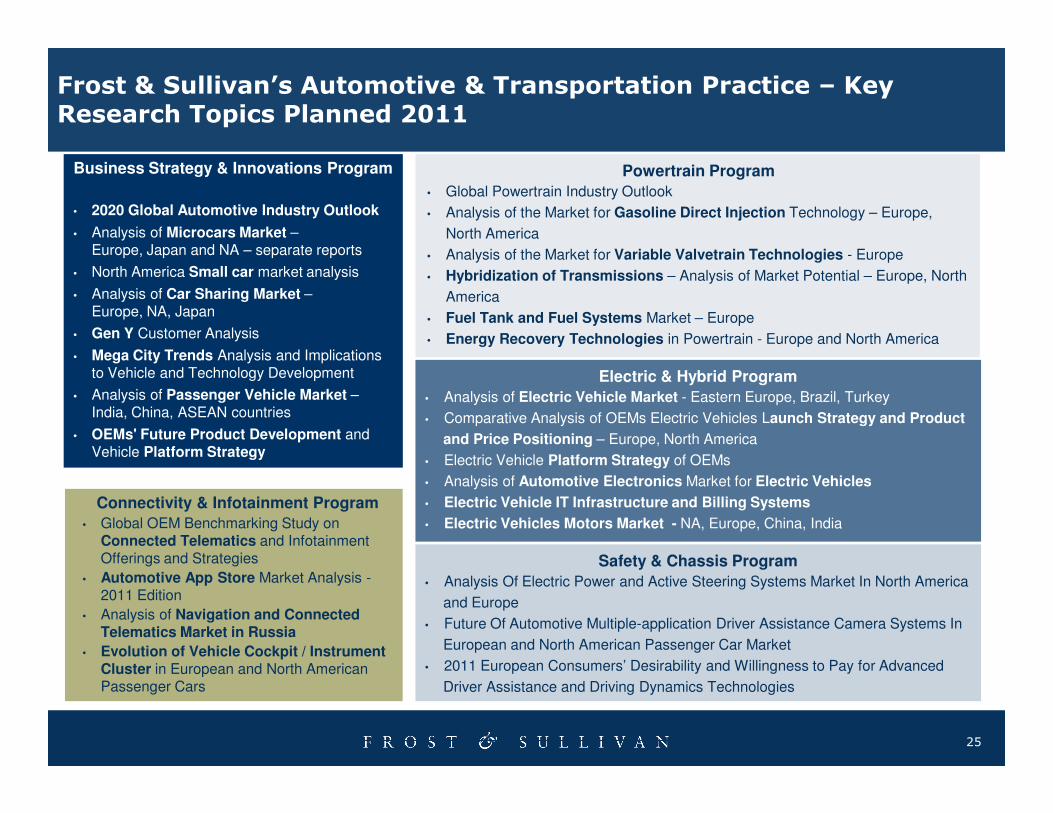

Frost & Sullivan’s Automotive & Transportation Practice – Key Research Topics Planned 2011

Powertrain Program

• Global Powertrain Industry Outlook

• Analysis of the Market for Gasoline Direct Injection Technology – Europe,

North America

• Analysis of the Market for Variable Valvetrain Technologies - Europe

• Hybridization of Transmissions – Analysis of Market Potential – Europe, North

America

• Fuel Tank and Fuel Systems Market – Europe

• Energy Recovery Technologies in Powertrain - Europe and North America

Business Strategy & Innovations Program

• 2020 Global Automotive Industry Outlook

• Analysis of Microcars Market –Europe, Japan and NA – separate reports

• North America Small car market analysis

• Analysis of Car Sharing Market –Europe, NA, Japan

• Gen Y Customer Analysis

• Mega City Trends Analysis and Implications to Vehicle and Technology Development

• Analysis of Passenger Vehicle Market –India, China, ASEAN countries

Electric & Hybrid Program

• Analysis of Electric Vehicle Market - Eastern Europe, Brazil, Turkey

25

Safety & Chassis Program

• Analysis Of Electric Power and Active Steering Systems Market In North America

and Europe

• Future Of Automotive Multiple-application Driver Assistance Camera Systems In

European and North American Passenger Car Market

• 2011 European Consumers’ Desirability and Willingness to Pay for Advanced

Driver Assistance and Driving Dynamics Technologies

Connectivity & Infotainment Program

• Global OEM Benchmarking Study on Connected Telematics and Infotainment Offerings and Strategies

• Automotive App Store Market Analysis -2011 Edition

• Analysis of Navigation and Connected Telematics Market in Russia

• Evolution of Vehicle Cockpit / Instrument Cluster in European and North American Passenger Cars

India, China, ASEAN countries

• OEMs' Future Product Development and Vehicle Platform Strategy

• Comparative Analysis of OEMs Electric Vehicles Launch Strategy and Product

and Price Positioning – Europe, North America

• Electric Vehicle Platform Strategy of OEMs

• Analysis of Automotive Electronics Market for Electric Vehicles

• Electric Vehicle IT Infrastructure and Billing Systems

• Electric Vehicles Motors Market - NA, Europe, China, India

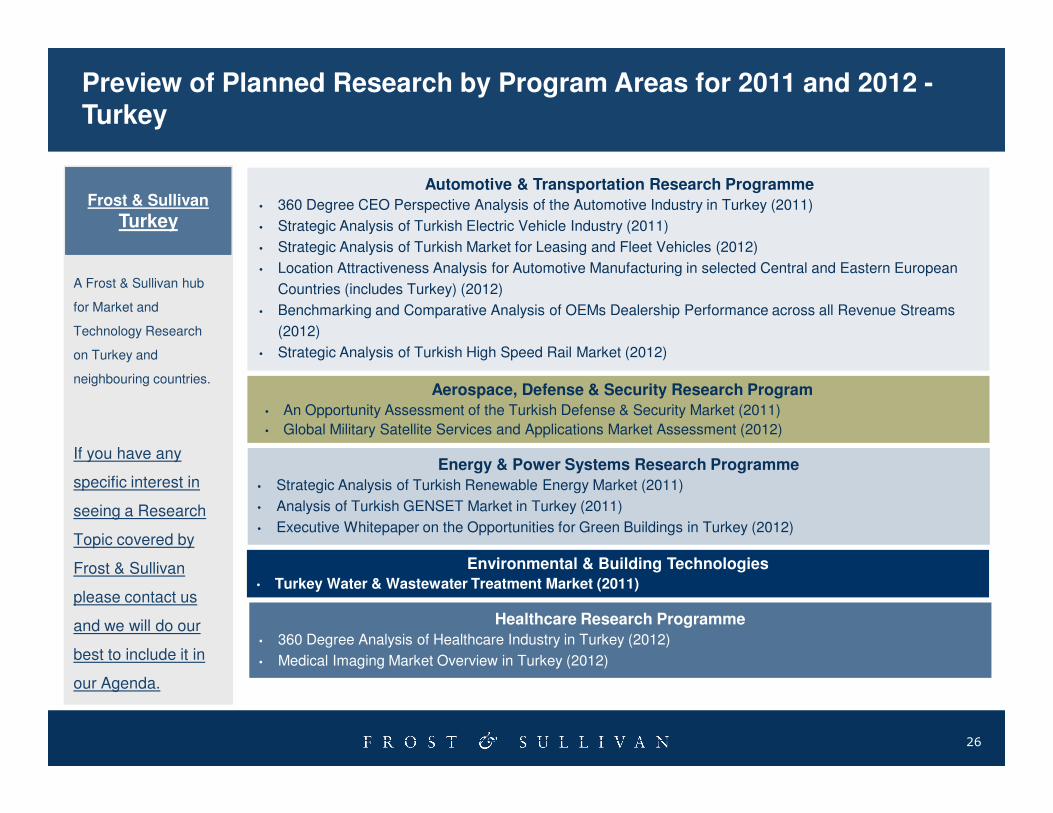

Preview of Planned Research by Program Areas for 2011 and 2012 -Turkey

Automotive & Transportation Research Programme

• 360 Degree CEO Perspective Analysis of the Automotive Industry in Turkey (2011)

• Strategic Analysis of Turkish Electric Vehicle Industry (2011)

• Strategic Analysis of Turkish Market for Leasing and Fleet Vehicles (2012)

• Location Attractiveness Analysis for Automotive Manufacturing in selected Central and Eastern European

Countries (includes Turkey) (2012)

• Benchmarking and Comparative Analysis of OEMs Dealership Performance across all Revenue Streams

(2012)

• Strategic Analysis of Turkish High Speed Rail Market (2012)

Aerospace, Defense & Security Research Program

• An Opportunity Assessment of the Turkish Defense & Security Market (2011)

Frost & Sullivan

Turkey

A Frost & Sullivan hub

for Market and

Technology Research

on Turkey and

neighbouring countries.

26

• An Opportunity Assessment of the Turkish Defense & Security Market (2011)

• Global Military Satellite Services and Applications Market Assessment (2012)

Environmental & Building Technologies

• Turkey Water & Wastewater Treatment Market (2011)

Healthcare Research Programme

• 360 Degree Analysis of Healthcare Industry in Turkey (2012)

• Medical Imaging Market Overview in Turkey (2012)

Energy & Power Systems Research Programme

• Strategic Analysis of Turkish Renewable Energy Market (2011)

• Analysis of Turkish GENSET Market in Turkey (2011)

• Executive Whitepaper on the Opportunities for Green Buildings in Turkey (2012)

If you have any

specific interest in

seeing a Research

Topic covered by

Frost & Sullivan

please contact us

and we will do our

best to include it in

our Agenda.

Next Steps

� Request a proposal for Growth Partnership Services or Growth Consulting Services to support you and your team to accelerate the growth of your company. ([email protected])

� Join us at our annual Growth, Innovation, and Leadership 2012: A Frost & Sullivan Global Congress on Corporate Growthoccurring 9 – 10 May, 2012 (www.gil-global.com)

27

� Register for Frost & Sullivan’s Growth Opportunity Newsletter and keep abreast of innovative growth opportunities (www.frost.com/news)

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

What would you like to see from Frost & Sullivan?

28

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by “Rating” this presentation.

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter

http://www.facebook.com/FrostandSullivan

http://www.linkedin.com/companies/4506

29

http://twitter.com/frost_sullivan

http://www.linkedin.com/companies/4506

http://www.slideshare.net/FrostandSullivan

For Additional Information

Katja FeickCorporate Communications

Automotive & Transportation

+49 (0) 69 [email protected]

Cyril Cromier

Sales Director

Europe

+33 1 42 81 22 44

30

Melih Nalcioglu

Research Manager

Automotive & Transportation

+90 212 249 56 39

Mohamed Mubarak

Program Manager

Automotive & Transportation

+90 212 244 69 41