Embed Size (px)

Citation preview

Economic Outlookfor the Global Food and Beverage Market

Christopher Shanahan

Food Industry Research Analyst

Chemicals, Materials and Food

February 26th, 2009

2

Agenda

• The economic recession and its

impact of economy on food and

beverage industry

• What will catalyze the turnaround?

• Emerging trends in food & beverage

industry

• Case studies of successful

companies resilient to the recession

3

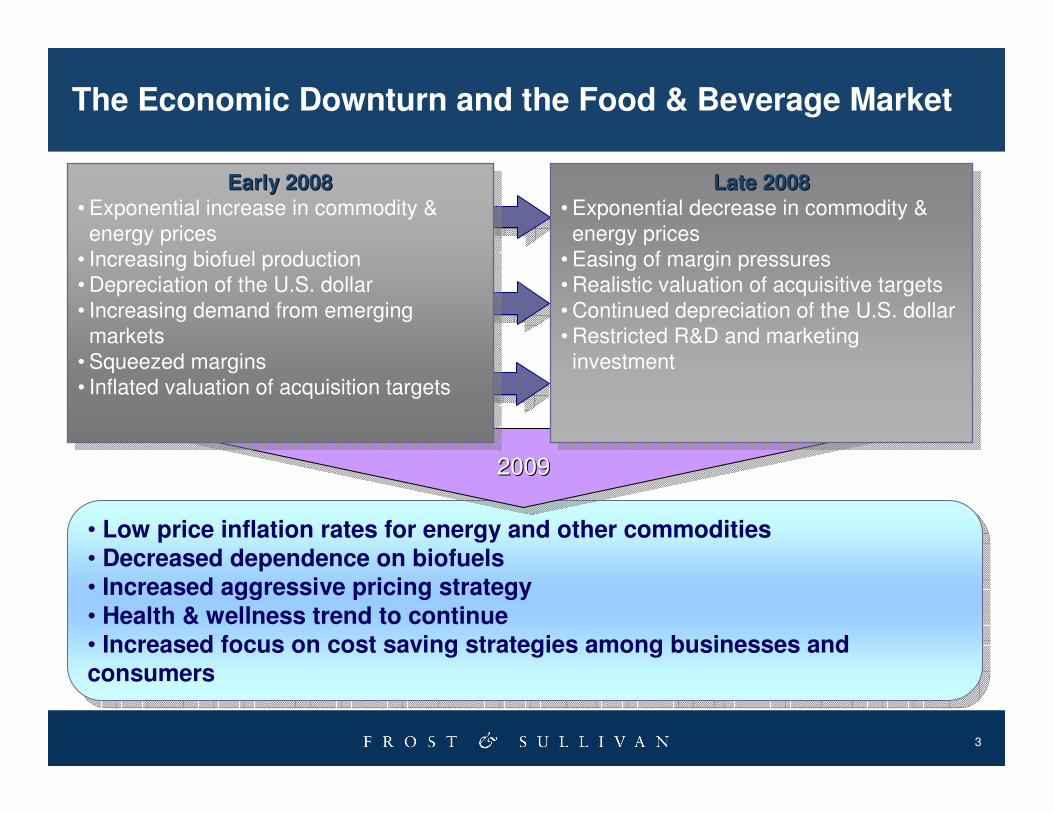

The Economic Downturn and the Food & Beverage Market

• Low price inflation rates for energy and other commodities• Decreased dependence on biofuels• Increased aggressive pricing strategy

• Health & wellness trend to continue • Increased focus on cost saving strategies among businesses and consumers

• Low price inflation rates for energy and other commodities• Decreased dependence on biofuels• Increased aggressive pricing strategy

• Health & wellness trend to continue • Increased focus on cost saving strategies among businesses and consumers

200920092009

Early 2008• Exponential increase in commodity &

energy prices

• Increasing biofuel production

• Depreciation of the U.S. dollar

• Increasing demand from emerging

markets

• Squeezed margins

• Inflated valuation of acquisition targets

Early 2008Early 2008• Exponential increase in commodity &

energy prices

• Increasing biofuel production

• Depreciation of the U.S. dollar

• Increasing demand from emerging

markets

• Squeezed margins

• Inflated valuation of acquisition targets

Late 2008• Exponential decrease in commodity &

energy prices

• Easing of margin pressures

• Realistic valuation of acquisitive targets

• Continued depreciation of the U.S. dollar

• Restricted R&D and marketing

investment

Late 2008Late 2008• Exponential decrease in commodity &

energy prices

• Easing of margin pressures

• Realistic valuation of acquisitive targets

• Continued depreciation of the U.S. dollar

• Restricted R&D and marketing

investment

4

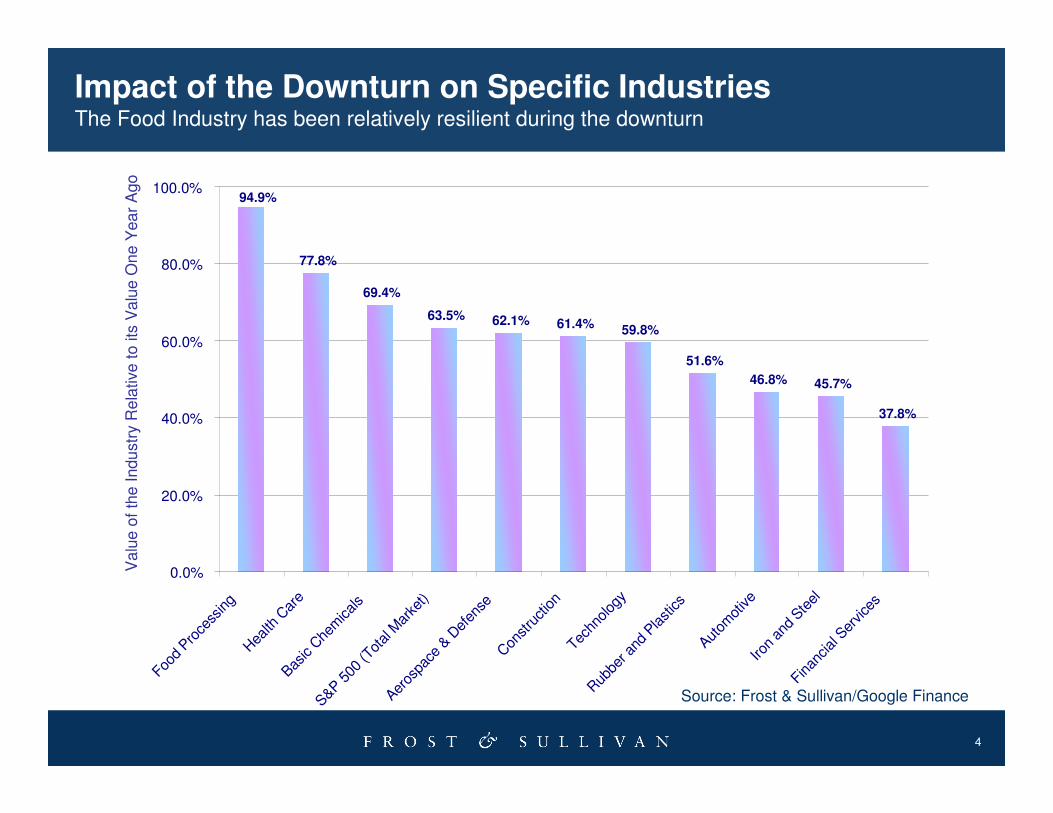

Impact of the Downturn on Specific IndustriesThe Food Industry has been relatively resilient during the downturn

Va

lue

of

the

Indu

str

y R

ela

tive

to

its

Va

lue

One

Yea

r A

go

The Value of the Industry Today Relative to its Value One Year Ago

77.8%

69.4%

63.5% 62.1% 61.4% 59.8%

51.6%

46.8% 45.7%

37.8%

94.9%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Food

Proce

ssin

g

Hea

lth C

are

Basic

Che

mic

als

S&P 500

(Tot

al M

arke

t)

Aeros

pace

& D

efen

seC

onst

ruct

ion

Techn

olog

y

Rub

ber a

nd P

last

ics

Autom

otiv

eIro

n an

d Ste

el

Finan

cial

Ser

vice

s

Source: Frost & Sullivan/Google Finance

5

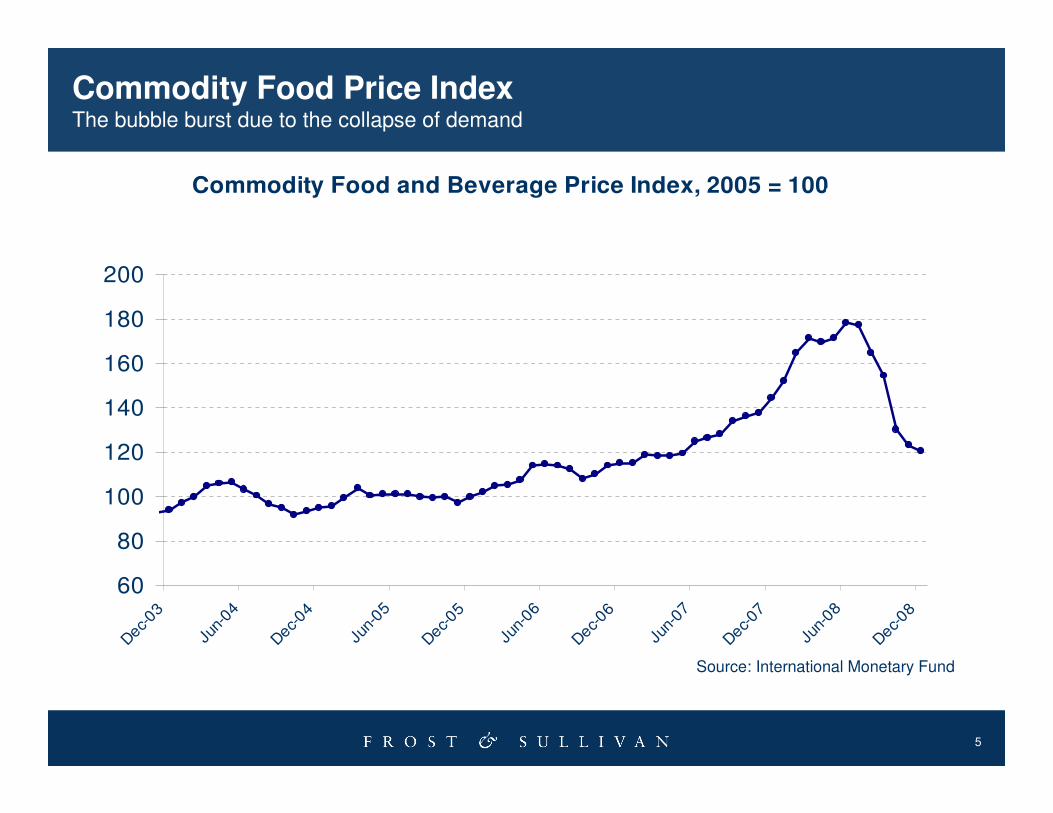

Commodity Food Price IndexThe bubble burst due to the collapse of demand

Commodity Food and Beverage Price Index, 2005 = 100,

includes Food and Beverage Price Indices

60

80

100

120

140

160

180

200

Dec-

03

Jun-

04

Dec-

04

Jun-

05

Dec-

05

Jun-

06

Dec-

06

Jun-

07

Dec-

07

Jun-

08

Dec-

08

Source: International Monetary Fund

6

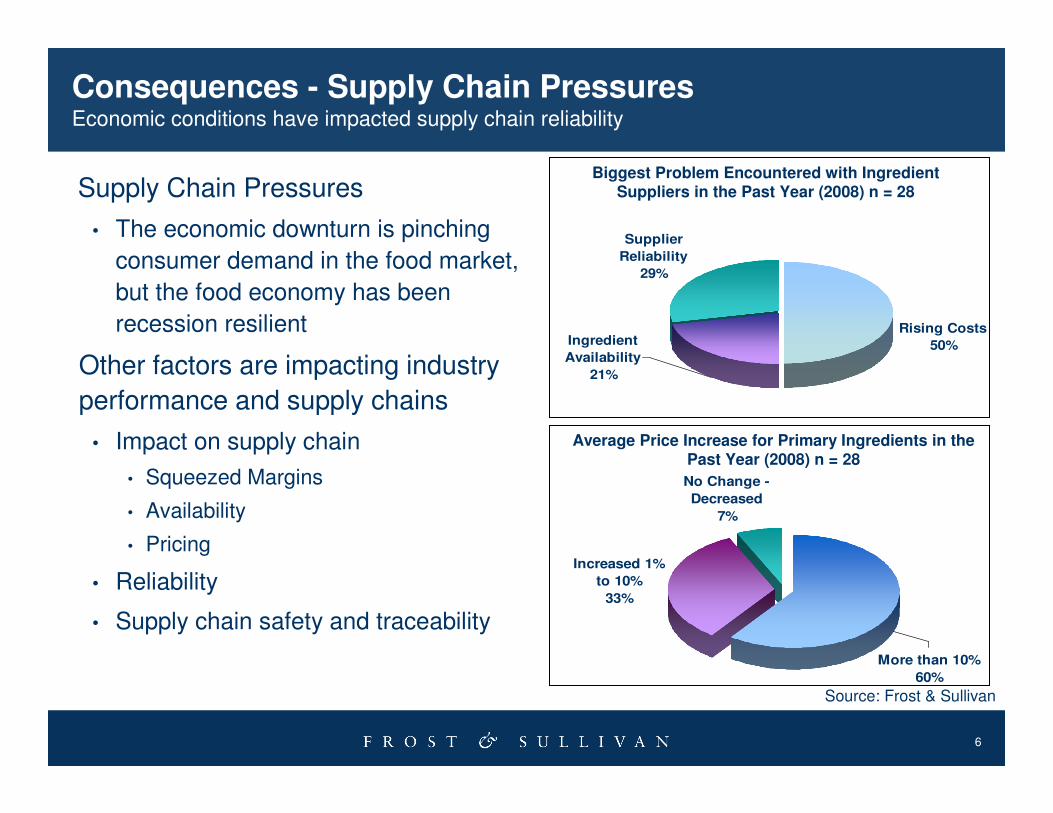

Consequences - Supply Chain PressuresEconomic conditions have impacted supply chain reliability

Rising Costs

50%

Supplier

Reliability

29%

Ingredient

Availability

21%

Increased 1%

to 10%

33%

No Change -

Decreased

7%

More than 10%

60%

Biggest Problem Encountered with Ingredient Suppliers in the Past Year (2008) n = 28

Average Price Increase for Primary Ingredients in the Past Year (2008) n = 28

Supply Chain Pressures

• The economic downturn is pinching

consumer demand in the food market,

but the food economy has been

recession resilient

Other factors are impacting industry

performance and supply chains

• Impact on supply chain

• Squeezed Margins

• Availability

• Pricing

• Reliability

• Supply chain safety and traceability

Source: Frost & Sullivan

7

Focus on the U.S. Organic FoodFrom double digit growth to no growth

• In the past, the organic food market had been

regarded as relatively recession proof.

However, there is beginning to evidence of

diminishing growth, suggesting market

maturity.

• Zero growth of the organic food market in 2008

• Organic market is set to grow again, but at a

much slower rate

• Falling demand will negatively impact organics'

price premium

• Willingness to pay extra is still positive but

decreasing

• Awareness of supply chain safety can be positive

for organic “organic’ growth

8

• Limited impact on the APAC food industry

• Asia shines despite economic gloom

• Growing consumer interest in health &

wellness

• APAC remains a vital sourcing ground for raw

materials and low cost production

• 2009 outlook among APAC food

manufacturers is gloomy

• High growth in APAC food markets will begin

to slow

What Does the Downturn Mean for APAC?Not much…yet

9

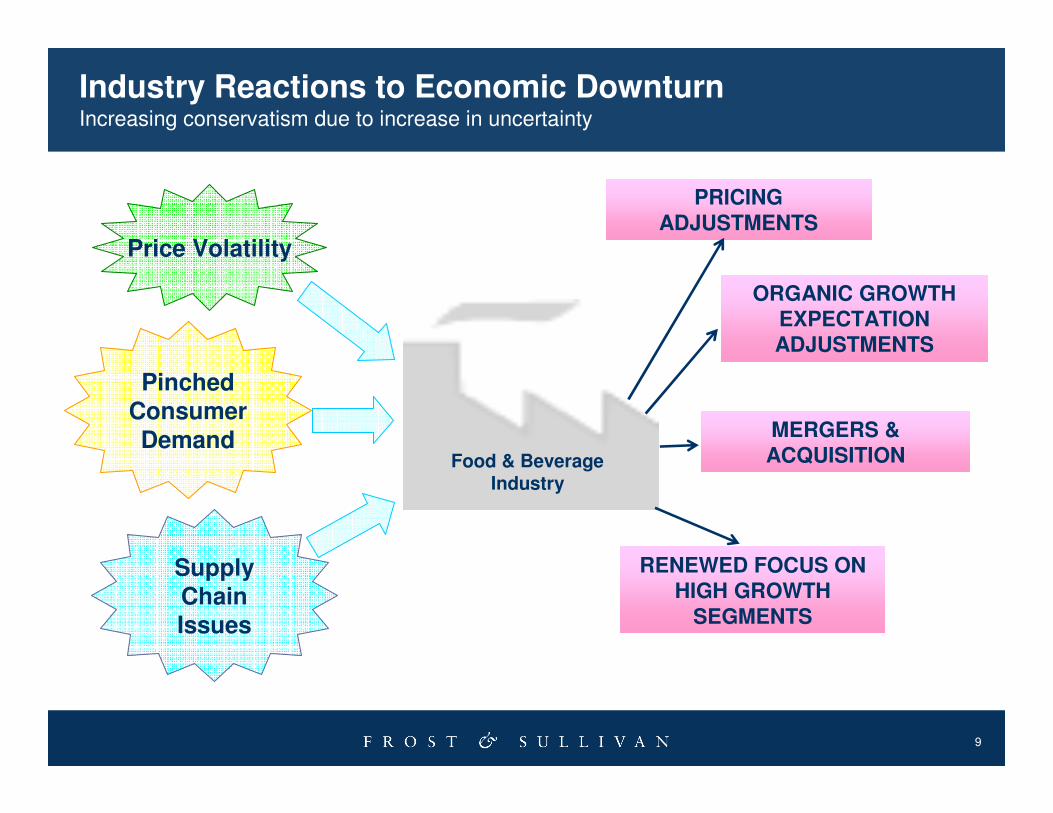

Industry Reactions to Economic DownturnIncreasing conservatism due to increase in uncertainty

PRICING

ADJUSTMENTS

ORGANIC GROWTHEXPECTATION ADJUSTMENTS

MERGERS & ACQUISITION

RENEWED FOCUS ON HIGH GROWTH

SEGMENTS

Price Volatility

Pinched Consumer

Demand

Supply Chain Issues

Food & Beverage Industry

10

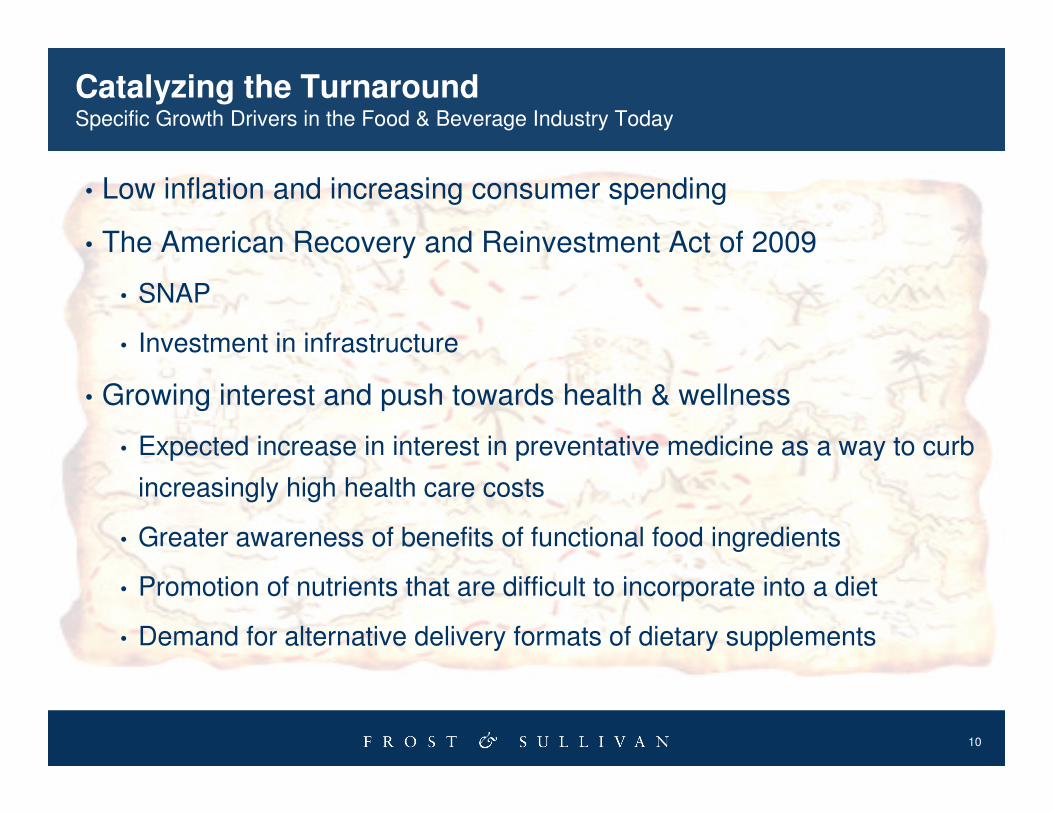

Catalyzing the TurnaroundSpecific Growth Drivers in the Food & Beverage Industry Today

• Low inflation and increasing consumer spending

• The American Recovery and Reinvestment Act of 2009

• SNAP

• Investment in infrastructure

• Growing interest and push towards health & wellness

• Expected increase in interest in preventative medicine as a way to curb

increasingly high health care costs

• Greater awareness of benefits of functional food ingredients

• Promotion of nutrients that are difficult to incorporate into a diet

• Demand for alternative delivery formats of dietary supplements

11

Emerging Trends in Food & Beverage Industry in 2009

• Food Product Customization

• Increased Food Health Regulation

• Multi-attribute Product Alternatives

• Food Safety and Traceability

• Simple Ingredients List

• Economic Slowdown and Changing

Diets

• Growing Consumer Interest in Local,

Environmentally-save, and Traditional

Foods

12

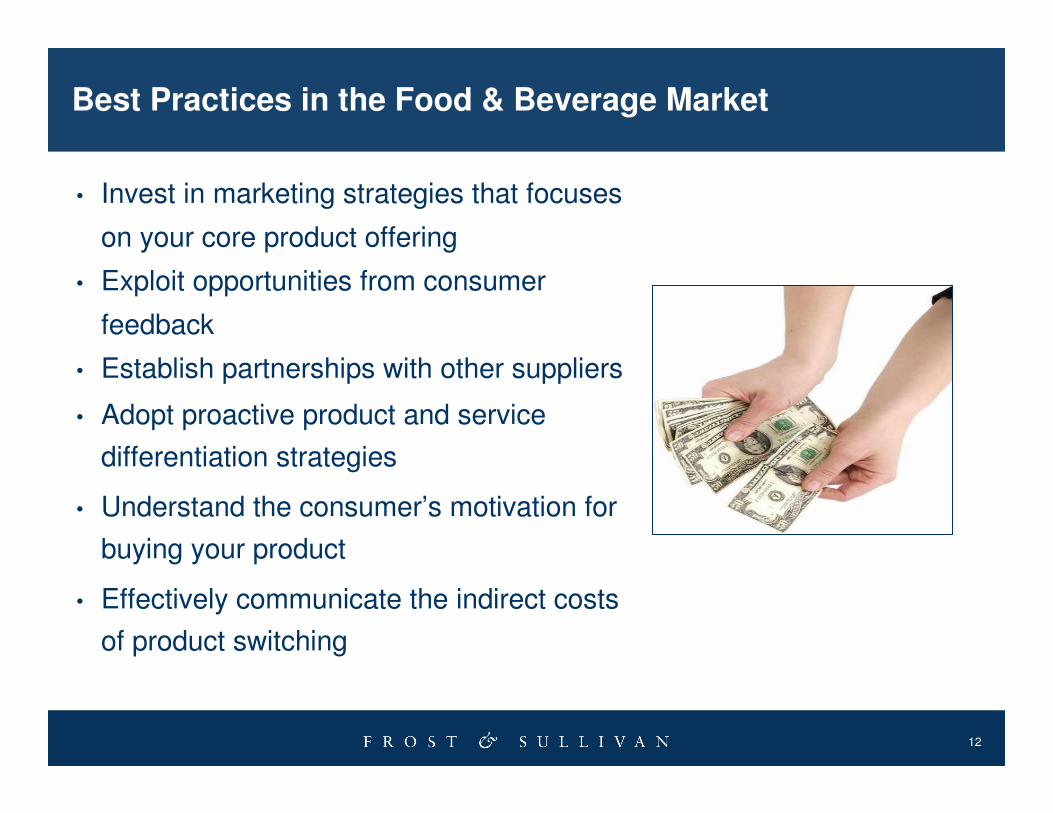

Best Practices in the Food & Beverage Market

• Invest in marketing strategies that focuses

on your core product offering

• Exploit opportunities from consumer

feedback

• Establish partnerships with other suppliers

• Adopt proactive product and service

differentiation strategies

• Understand the consumer’s motivation for

buying your product

• Effectively communicate the indirect costs

of product switching

13

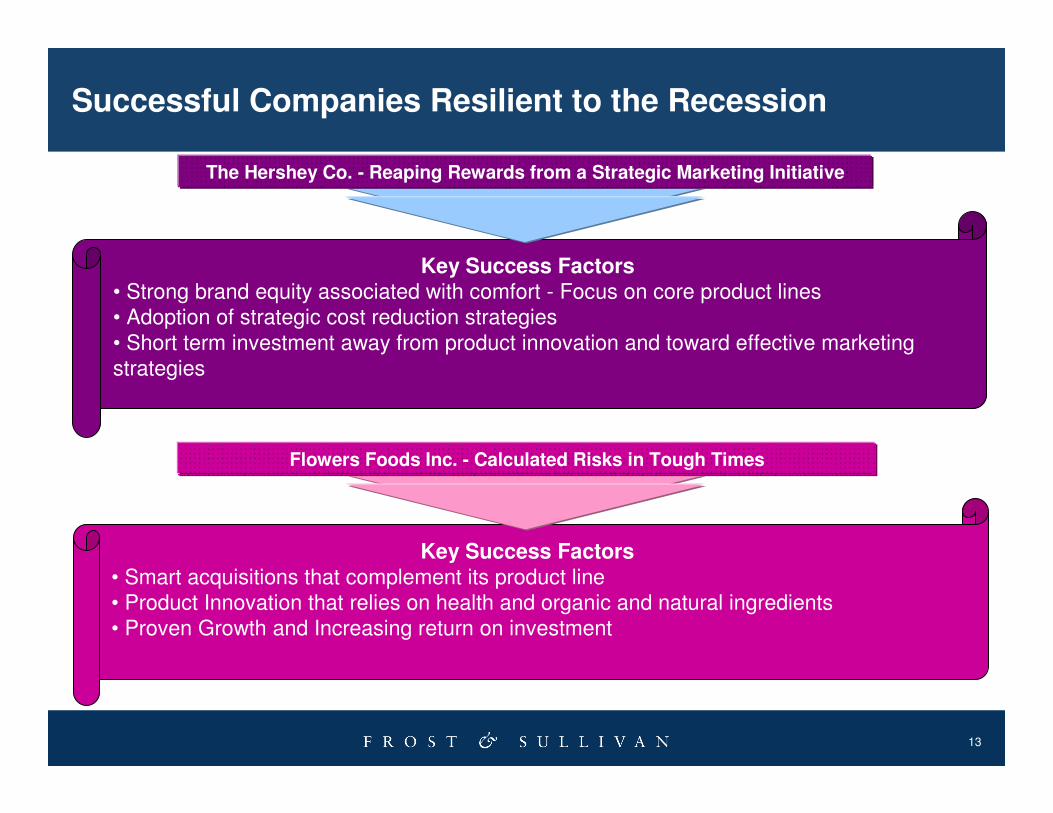

Successful Companies Resilient to the Recession

The Hershey Co. - Reaping Rewards from a Strategic Marketing Initiative

Key Success Factors• Strong brand equity associated with comfort - Focus on core product lines

• Adoption of strategic cost reduction strategies

• Short term investment away from product innovation and toward effective marketing

strategies

Flowers Foods Inc. - Calculated Risks in Tough Times

Key Success Factors

• Smart acquisitions that complement its product line

• Product Innovation that relies on health and organic and natural ingredients

• Proven Growth and Increasing return on investment

14

Next Steps

Register for Frost & Sullivan’s Growth Opportunity Newsletter and keep abreast of innovative growth opportunities(www.frost.com/news)

Register for the next Chairman’s Series on Growth:

Growth Acceleration System: The Architecture for Building A Successful Growth Strategy

(March 3rd) (http://www.frost.com/growth)

Join us at our 5th Annual Customer Contact Executive MindXchange April 19-22 2009, Bonita Springs, FL (www.frost.com/ccs)

Request a proposal for a Growth Partnership Service to support you and your team to accelerate the growth of your company. ([email protected])1-877-GoFrost (1-877-463-7678)

Follow Frost & Sullivan on-line at:

� http://twitter.com/Frost_Sullivan

� http://www.facebook.com/people/Frost-Sullivan/1131686497

15

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

Emerging Trends?

Strategic Recommendations?

Other?Please inform us by taking our survey.

What would you like to see from Frost & Sullivan?

16

For Additional Information

To leave a comment, ask the analyst a question, download a copy,

or receive the free audio segment that accompanies this

presentation, please contact Stephanie Ochoa, Analyst Briefing

Coordinator, at (210) 247-2421 or via email,