Embed Size (px)

Citation preview

Introduction to the Norwegian healthcaremarket

Tobias Bøggild-Damkvist 29.10.2015

2

Purpose of the workshopThe aim of the workshop is to give you…

• An introduction to the Norwegian healthcare market, and

• A chance to discuss needs and offerings as well as to ask question about the Norwegian healthcare sector

Please feel free to interrupt and ask questions at any time during the presentation. That’s how I can tailor the workshop to your expectations and needs

Agenda1. Introduction of the participants 2. The Norwegian healthcare regions – Strategic

agendas and needs3. Discussion about differences and similarities between

Finland and Norway4. National and regional procurement policy5. Group exercise: Matching your offers with Norwegian

needs and demand6. Q&A session about the Norwegian healthcare market

and how to approach it.7. Where to find more information? Overview of

resources available

1 A short introductionPlease state…1. Your name, position and company?2. What need do you meet in the healthcare market?3. What is your most important question about the

Norwegian healthcare market?

Example:• Tobias Bøggild-Damkvist, Partner at Epikon A/S• Epikon provides advisory services to healthcare executives in need of decision support• I would like to know what help innovative companies from Finland needin order to be able to paticipate in public procurement processes in Norway

5

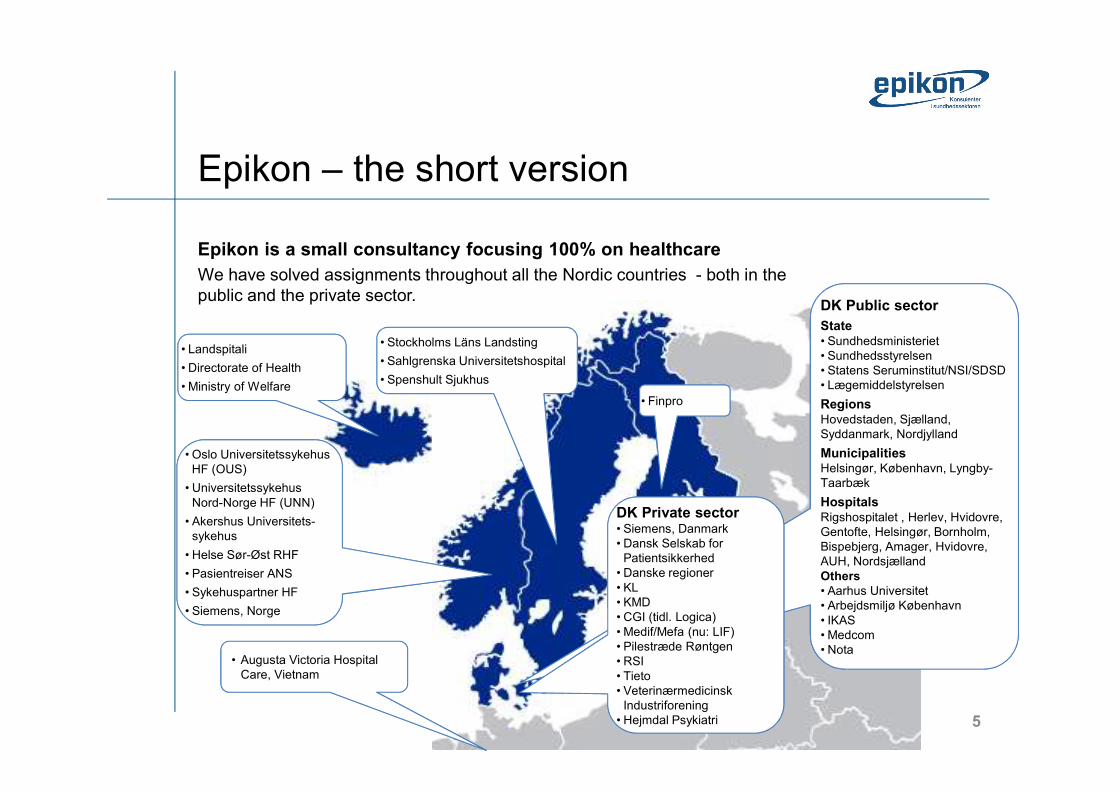

Epikon – the short versionEpikon is a small consultancy focusing 100% on healthcareWe have solved assignments throughout all the Nordic countries - both in the public and the private sector.

• Landspitali• Directorate of Health• Ministry of Welfare

•

•

• Oslo UniversitetssykehusHF (OUS)

• UniversitetssykehusNord-Norge HF (UNN)

• Akershus Universitets-sykehus

• Helse Sør-Øst RHF• Pasientreiser ANS• Sykehuspartner HF• Siemens, Norge

• Stockholms Läns Landsting• Sahlgrenska Universitetshospital• Spenshult Sjukhus

• Augusta Victoria Hospital Care, Vietnam

DK Public sectorState• Sundhedsministeriet • Sundhedsstyrelsen • Statens Seruminstitut/NSI/SDSD• Lægemiddelstyrelsen RegionsHovedstaden, Sjælland, Syddanmark, Nordjylland MunicipalitiesHelsingør, København, Lyngby-TaarbækHospitalsRigshospitalet , Herlev, Hvidovre, Gentofte, Helsingør, Bornholm, Bispebjerg, Amager, Hvidovre, AUH, NordsjællandOthers• Aarhus Universitet• Arbejdsmiljø København • IKAS • Medcom • Nota

DK Private

•

DK Private sector• Siemens, Danmark • Dansk Selskab for

Patientsikkerhed• Danske regioner • KL• KMD• CGI (tidl. Logica)• Medif/Mefa (nu: LIF) • Pilestræde Røntgen• RSI• Tieto• Veterinærmedicinsk

Industriforening• Hejmdal Psykiatri

• Finpro

6

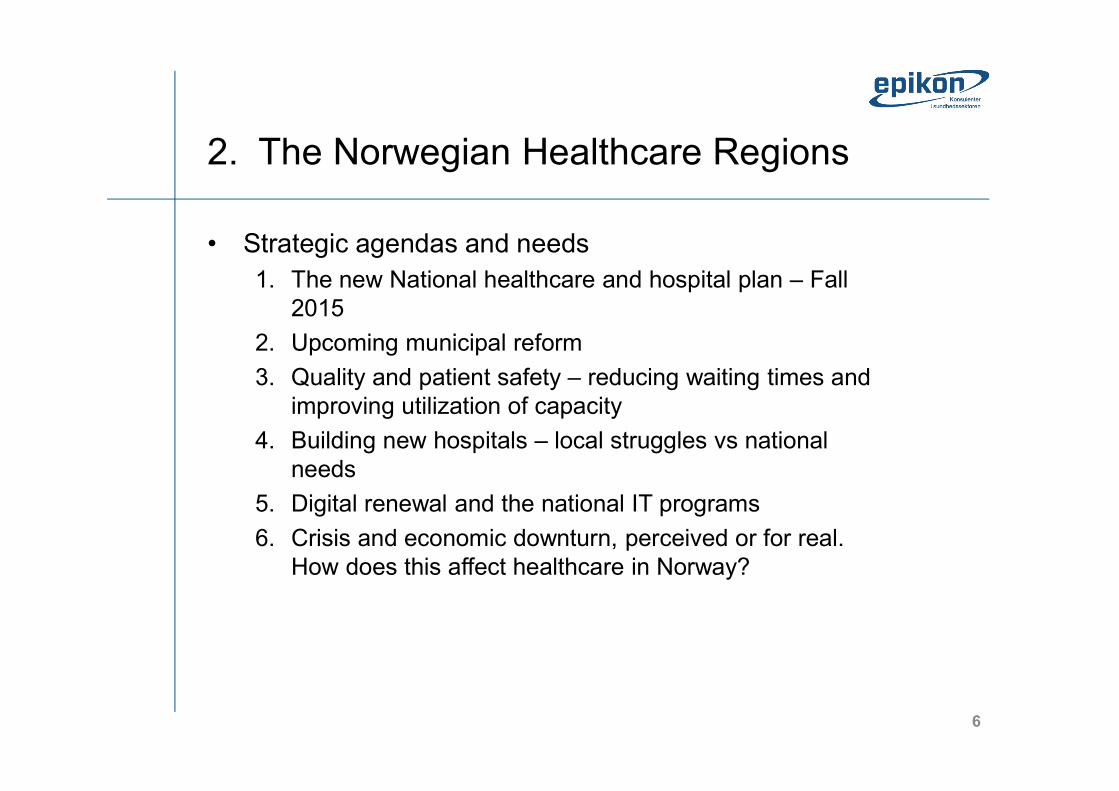

2. The Norwegian Healthcare Regions • Strategic agendas and needs

1. The new National healthcare and hospital plan – Fall 2015

2. Upcoming municipal reform3. Quality and patient safety – reducing waiting times and

improving utilization of capacity4. Building new hospitals – local struggles vs national

needs5. Digital renewal and the national IT programs6. Crisis and economic downturn, perceived or for real.

How does this affect healthcare in Norway?

7

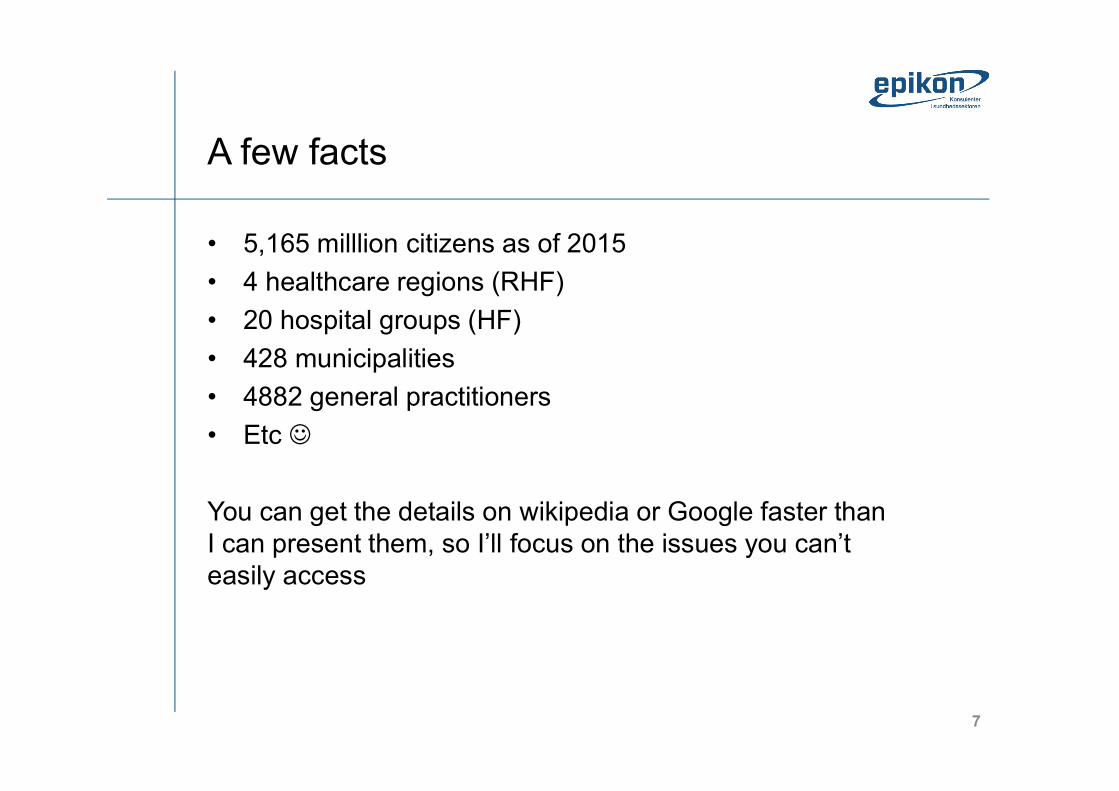

A few facts• 5,165 milllion citizens as of 2015• 4 healthcare regions (RHF)• 20 hospital groups (HF)• 428 municipalities• 4882 general practitioners• Etc

You can get the details on wikipedia or Google faster thanI can present them, so I’ll focus on the issues you can’teasily access

8

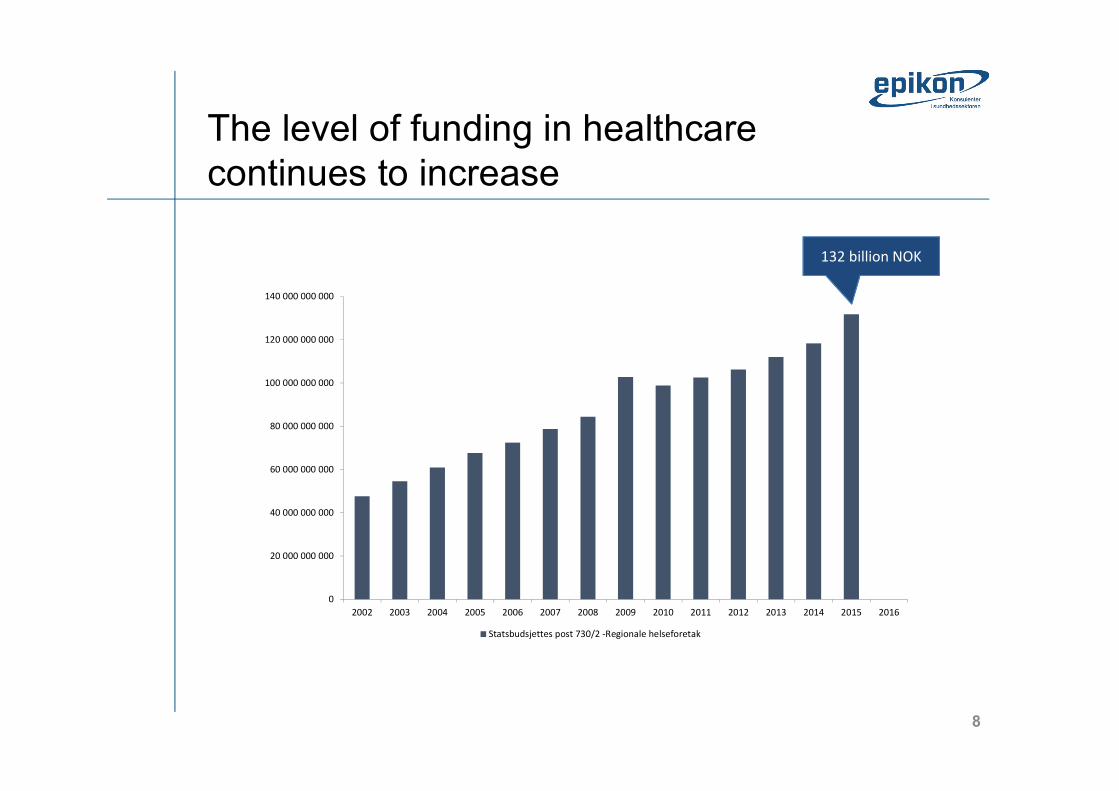

The level of funding in healthcarecontinues to increase

0

20 000 000 000

40 000 000 000

60 000 000 000

80 000 000 000

100 000 000 000

120 000 000 000

140 000 000 000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016Statsbudsjettes post 730/2 -Regionale helseforetak

132 billion NOK

9

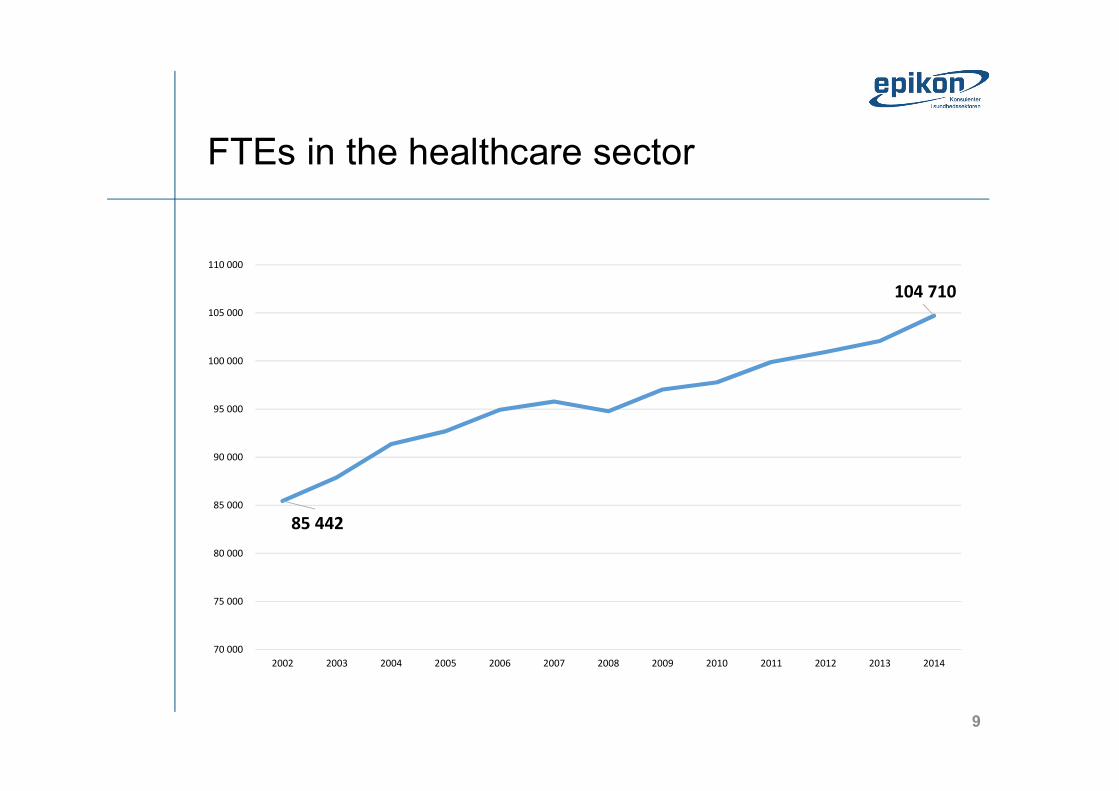

FTEs in the healthcare sector

85 442

104 710

70 000

75 000

80 000

85 000

90 000

95 000

100 000

105 000

110 000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

10

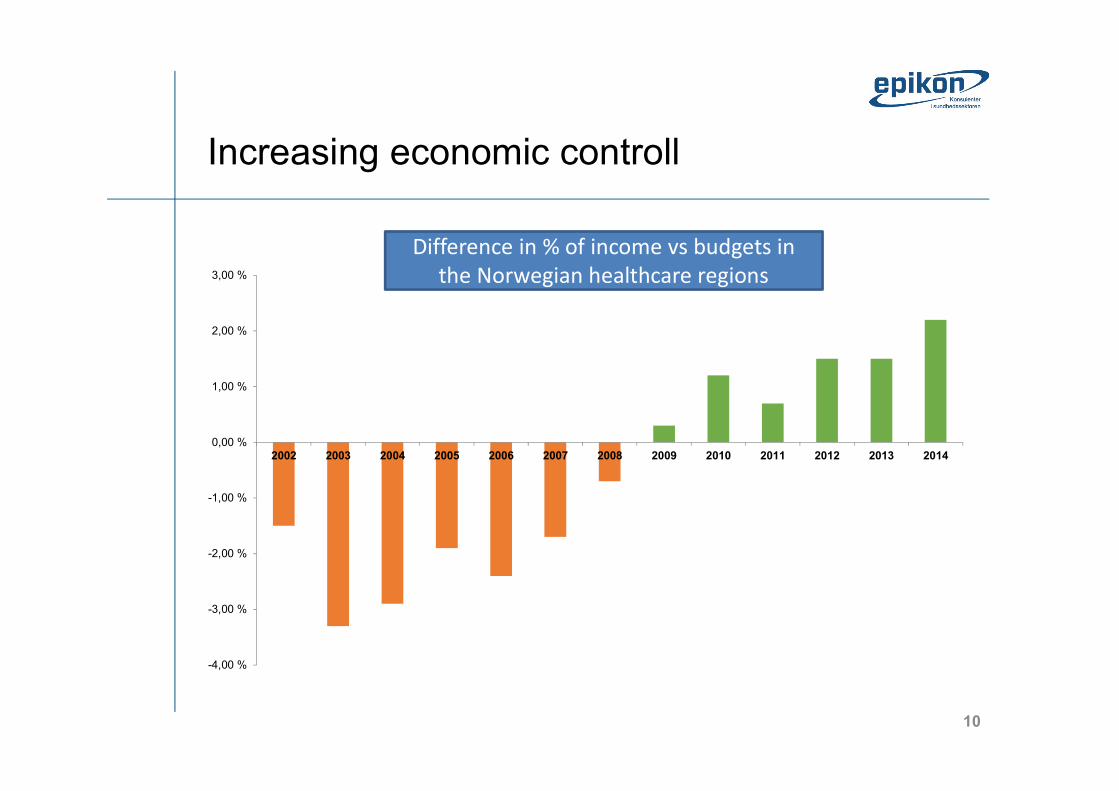

Increasing economic controll

-4,00 %

-3,00 %

-2,00 %

-1,00 %

0,00 %

1,00 %

2,00 %

3,00 %

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Avvik i prosent av inntekt mot eiers styringskravDifference in % of income vs budgets in the Norwegian healthcare regions

11

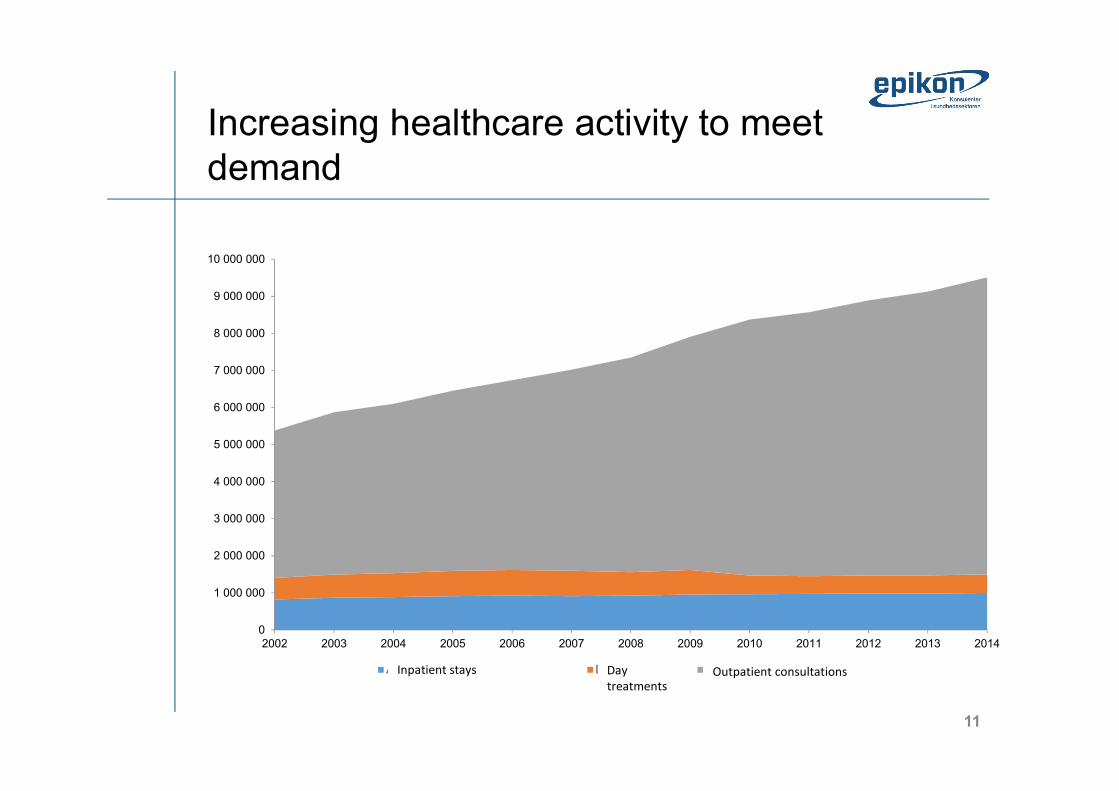

Increasing healthcare activity to meetdemand

0

1 000 000

2 000 000

3 000 000

4 000 000

5 000 000

6 000 000

7 000 000

8 000 000

9 000 000

10 000 000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014Antall utskrivninger - Døgnopphold Dagbehandling Polikliniske konsultasjonerOutpatient consultationsDay treatmentsInpatient stays

12

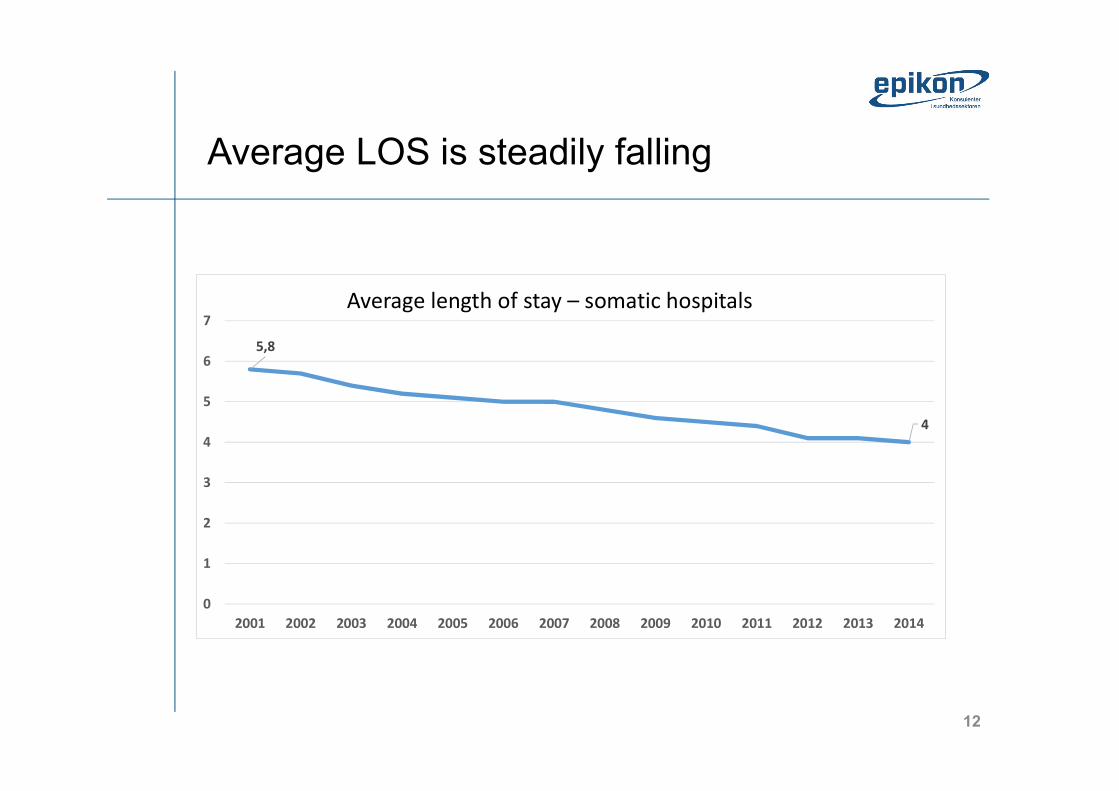

Average LOS is steadily falling

5,8

4

01234567

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Gjennomsnittlig liggetid ved somatiske sykehusAverage length of stay – somatic hospitals

13

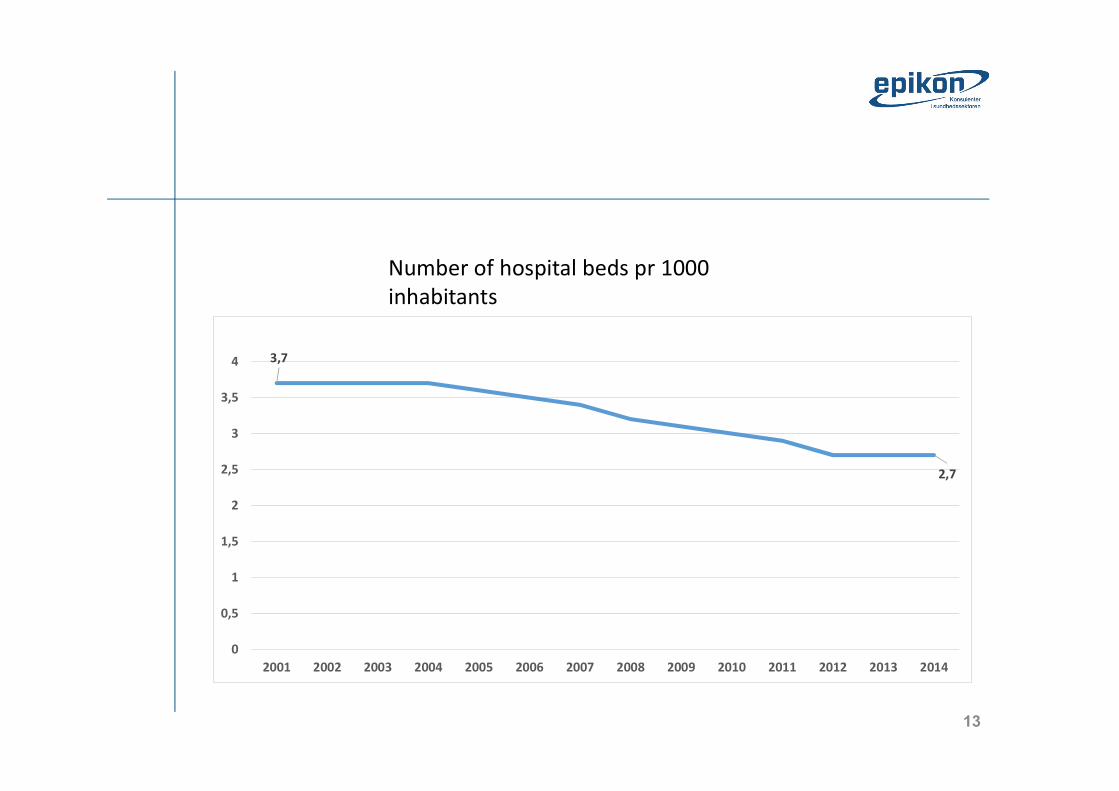

3,7

2,7

00,5

11,5

22,5

33,5

4

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Senger (per 1 000 innbyggere)

Number of hospital beds pr 1000 inhabitants

14

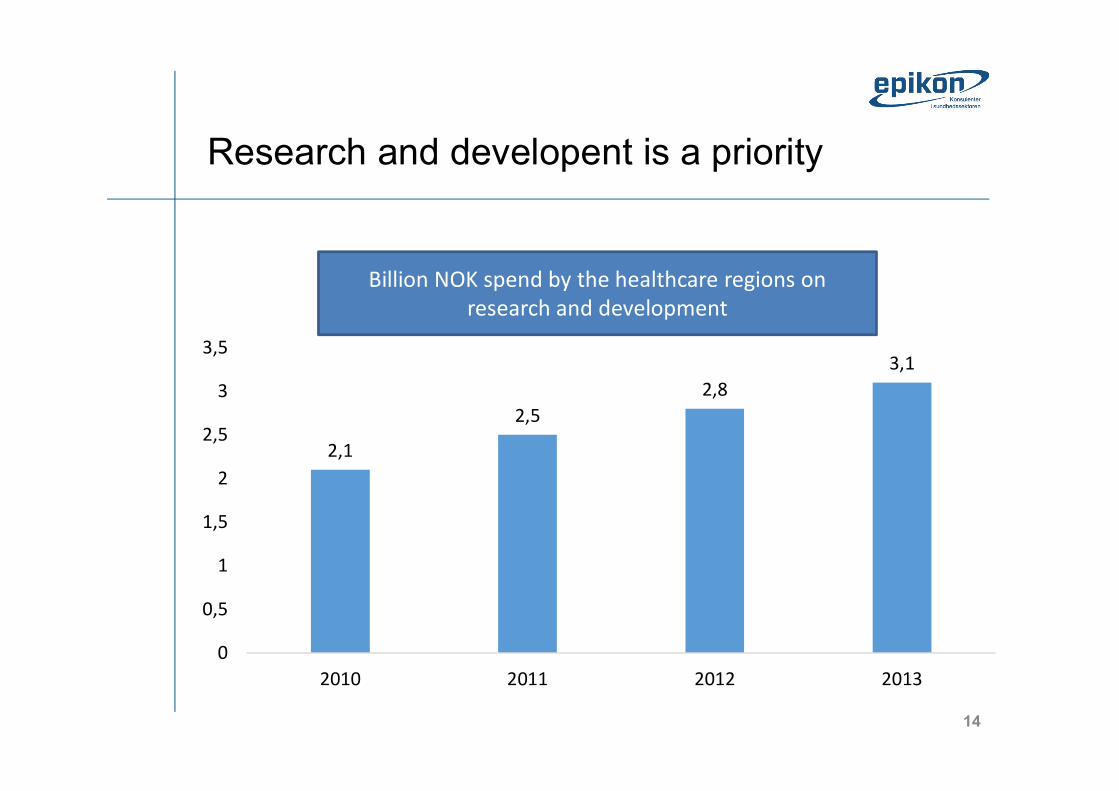

Research and developent is a priority

2,12,5

2,83,1

00,5

11,5

22,5

33,5

2010 2011 2012 2013

Ressursbruk i mrdBillion NOK spend by the healthcare regions onresearch and development

15

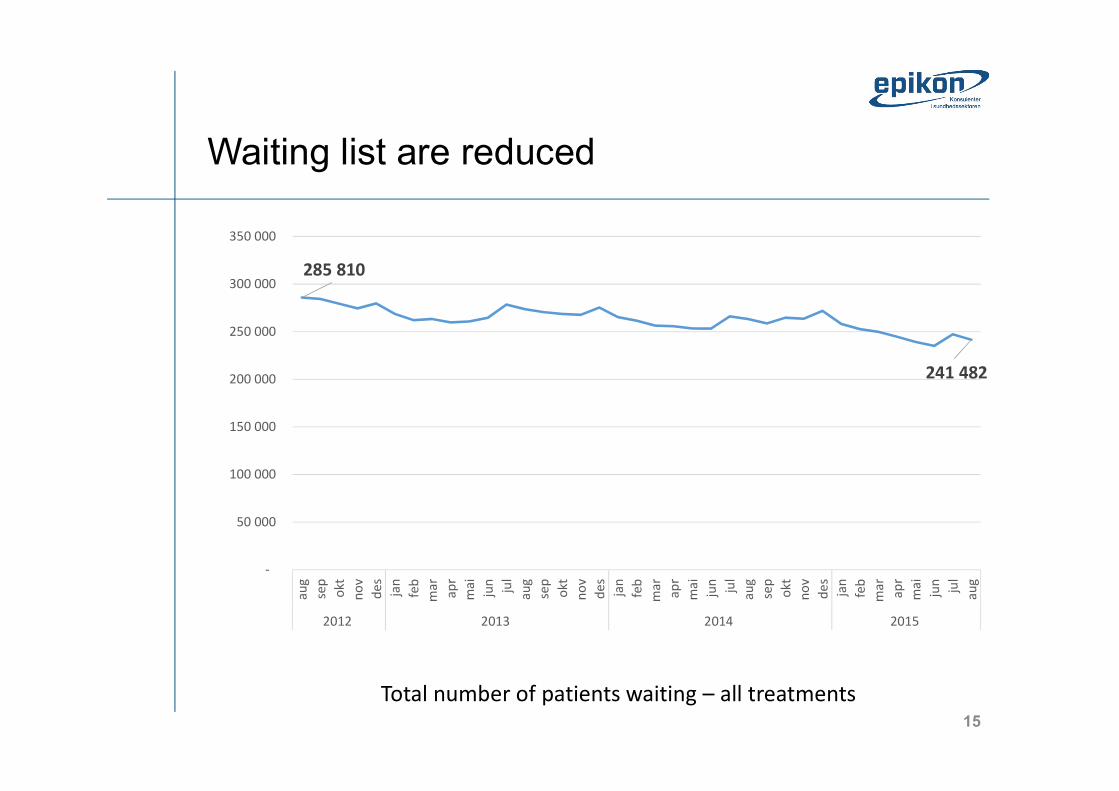

Waiting list are reduced

285 810

241 482

-

50 000

100 000

150 000

200 000

250 000

300 000

350 000

aug sep okt nov des jan feb mar apr mai jun jul aug sep okt nov des jan feb mar apr mai jun jul aug sep okt nov des jan feb mar apr mai jun jul aug

2012 2013 2014 2015

Total number of patients waiting – all treatments

16

The new National Health and Hospital Plan During the autumn of 2015 the government will present a national health and hospital plan, which seeks to outline the principles for the future hospital structure and criteria for different types of hospitals. The plan will be based on how the health service should look like from the patients’ perspective, and it seeks to reflect the users’ experience, expertise and viewpoints.

17

3 main areas that will receive special attention1. The patients’ healthcare - “There are no decisions to be taken about me, without me”

- With this it is meant to strive toward a health care system that is organized and adapted according to the patients’ needs.

- It seeks to move power and influence to the patient and its relatives. It seeks to empower the patient in a higher degree and it seeks to consider health care services from the patients’ perspective.

The new National Health and Hospital Plan

Key questions

- What is important for the individual patient?

- How can health services be most in line with individual patients’ values and wishes?

18

2. Future hospitals and hospital structure

- Hospitals in Norway are established according to where people historically have lived and worked

This structure is developed over 100 years – Much has changed since (age composition, disease picture, settlement patterns, medical diagnostics and treatments etc.)

Key questions

- Can the current structure work for tomorrows specialized health care? - To what extent should it be centralized or decentralized? - To what extent can disease and medical treatment be given outside the hospital? - Which structure is the best in light of the “the patients' healthcare?”

The new National Health and Hospital Plan 3 main areas that will receive special attention

19

3. Quality

- Facilitate for the specialized health care to increasingly be governed on the basis of quality objectives

- To a higher degree give the patients and public understandable and useful information about quality

- To deal with undesirable variations it seeks to give managers and employees relevant and fresh data that supports quality improvement and management (design quality measures)

Key question

- How can quality data be used to better measure, develop and manage the Norwegian specialist health care system?

The new National Health and Hospital Plan 3 main areas that will receive special attention

20

Upcoming Municipal ReformThere are 428 municipalities in Norway (vary significantly in population and size) More than 50% < 5000 inhabitants, and the 100 largest municipalities account for appx. 75% of the total population. Oslo the largest with appx. 640.000 inhabitants

Brief background

Large expansion in the municipalities' task portfolio for the last 50 years (kindergarten services, primary school starting at age 6, expansion of health and care services etc.)

Additional responsibilities through The Integration Reform of 2012 and the Norwegian Public Health Act

Municipalities not small on a European scale, but compared with Nordic neighbors they are relatively small

21

The aim and logic behindUpcoming Municipal Reform- The aim is bigger, and more capable municipalities with greater power and authority to “take on challenges of

tomorrow and meet the ever-increasing expectations of the citizens”

- The goal is a local democracy that can safeguard welfare and ensure value creation. More power to local politicians and more leeway for municipalities.

- Wants to make decisions as close to those they affect as possible – develop more comprehensive and coherent range of services for users.

- The reform aims to provide opportunities for a more professional administration and management and may better equip the municipalities to innovate both in revamping services as well as work methods

22

Reducing waiting times and improving utilization of capacityQuality and patient safety

A stated goal of the government is to ensure the quality and patient safety, and reduce waiting times while at the same time improve resource utilization

23

Goals intended to be achieved by

- Changed and improved systems, leadership and culture Avoid unwarranted variation, strengthen leadership in the sector and increasingly control on the basis of quality indicators.

- Getting a knowledge base with good, reliable, relevant and timely dataIdentification of knowledge gaps and deficiencies, and focus on sealing these.

- Good and clear managementClear demands to management at all levels at it is important for health and safety of both patients and staff

- Improved registration and updating of data, especially real-time dataOngoing effort to develop more and better quality indicators, including patient perceived quality, and improved systems to publicize and update information

- Residential treatment choices designed to reduce waiting times and enhance patients rights Utilize excess capacity and efficiency potential in the health service better, and cooperate with “all good forces” to provide good health services. Public hospitals are given more freedom and encouragement to become more efficient.

Quality and patient safety

24

Goals rooted in some legislative changes as of 1. Nov 2015

- When it comes to handling and assessment of referrals

Assessment deadline shortened from 30 to 10 working days. Also, patients requiring specialized medical care gets a legal deadline for last justifiable startup of health care

- Also a new scheme for deadline violations

The specialist health care is to contact HELFO if the deadline for commencement cannot be met. Today, patients themselves must contact HELFO. The specialist care must also notify HELFO if they expect to violate the deadline to arrange for a different treatment.

- Furthermore, patients get free treatment choices

Goal is to reduce waiting times, increase freedom of choice, and stimulate the public hospitals to become more efficient, buy more from private through tender, and

Quality and patient safety

25

Local vs. National needs – A subject of vigorous debateBuilding new hospitals

Everyone wants a capable hospital system, the proper “medicine” however, is heavily discussed.

The current structure – Most emergency rooms offer internal medicine treatment, surgery and anesthesia 24 hours a day. This is challenged by surgery being more specialized and centralized. An international trend due to both the medical and technological progress, often-used argument for this is that “practice makes perfect”

26

Three points of view- Arguments for centralization

“The current hospital structure is not appropriate for solving the defined duties. There are too many hospitals with emergency functions, resources are spread too wide and thin in small hospitals, which leads to poorer quality. Some tasks require a higher degree of expertise so they need to be centralized”.

- Arguments for keeping local hospitals

“The population must be ensured good emergency shelters wherever they live. The travel time, geography and weather condition require local hospitals with full emergency preparedness”.

- Professional representatives in favor of preserving local hospitals

“Need to keep local hospitals, firstly because of the needs of the citizens, but also the employees' working conditions. Safe, well-qualified and motivated employees provide the best services”.

Building new hospitals

27

Conditions that will affect development of the structure- The demographic change

More people become older and have more chronic diseases, and will need internal medical services closer to where they live

- International trends hitting Norway

Provision of surgery becomes more specialized to perform better. Advanced equipment and technology leads to a need for greater expertise. The general surgeon is replaced by more specialized surgeons who work in teams.

- The need for maintaining acute surgical expertise

Surgeons might not be able to maintain acute surgical expertise by daytime elective surgery

Building new hospitals

28

Digital renewal and national IT programsGood use of information technology is essential for achieving health political objectives. The goal is to make quality of services and work processes more efficient so that more time can be used on direct patient contact and treatment.

29

National initiatives at all levelsPatient perspective

- “Each patient should have the opportunity to be involved in processes and decisions about their own health”

- One important measure is “Helsenorge.no” (guidance on patient rights, upload/transmit data, initiate and participate in digital communication, book appointments, organize their own treatment etc.)

Health care workers

- “Ensure the best possible treatment through simple and secure access to the necessary information throughout the course of a treatment”

- Important measures for this goal is joint drug information, introduce E-prescription functionality in hospitals, national core journal (faster access to important health information) and more.

Other measures

- Also ongoing measures related to privacy and data protection, common standards and terminology, research and innovation, computer software for management bases etc.

Digital renewal and national IT programs

30

Crisis and economic downturnPerceived or for real? How does this affect health care in Norway?

31

Crisis and economic downturnPerceived or for real?

32

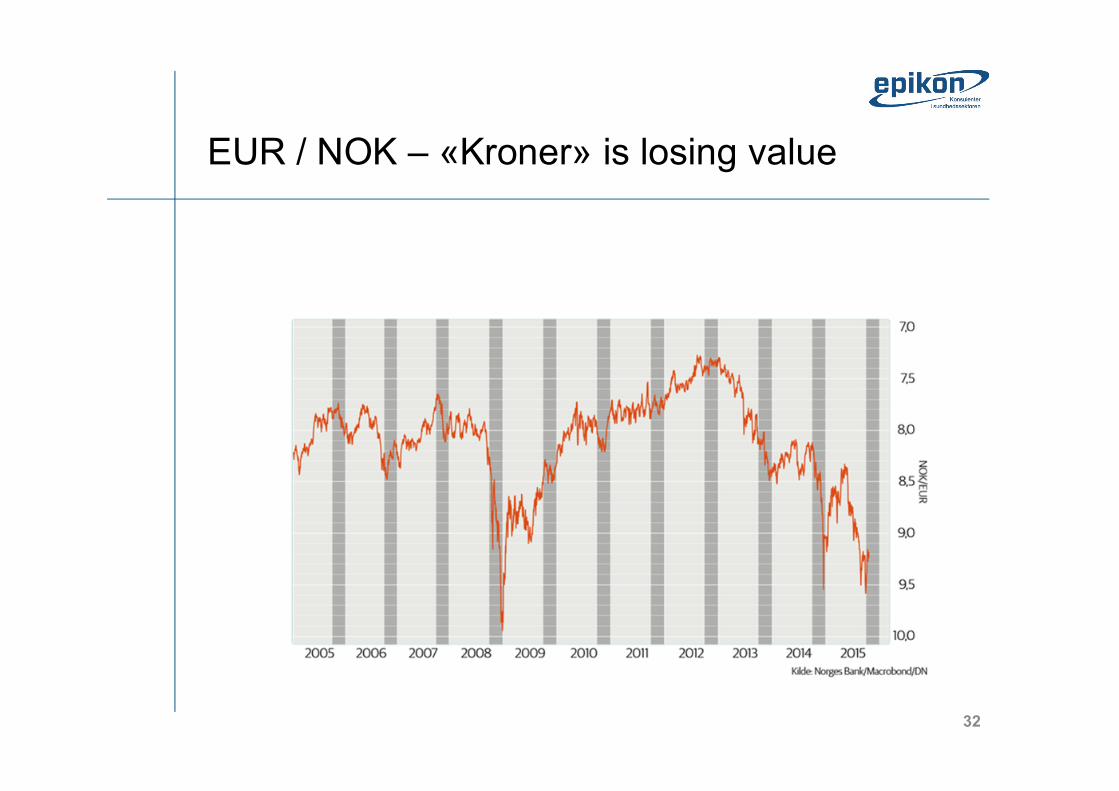

EUR / NOK – «Kroner» is losing value

33

Finland vs Norway• What do you think are the most

important similarities between Finland and Norway?

• What do you think are the most important differences?

• What possible advantages does this confer to Finish companies

34

National and regional procurement policy– The healthcare procurement organizations

• National: Hinas, Sykehusbygg HF, Nasjonal IKT, Innomedetc

• Regional: Helse Midt-Norge RHF – Seksjon for Innkjøp, Sykehuspartner HF Innkjøp, Helse Nord RHF Innkjøp, Helse Vest Innkjøp HF

• Hospital procurement – Innovation in healthcare

35

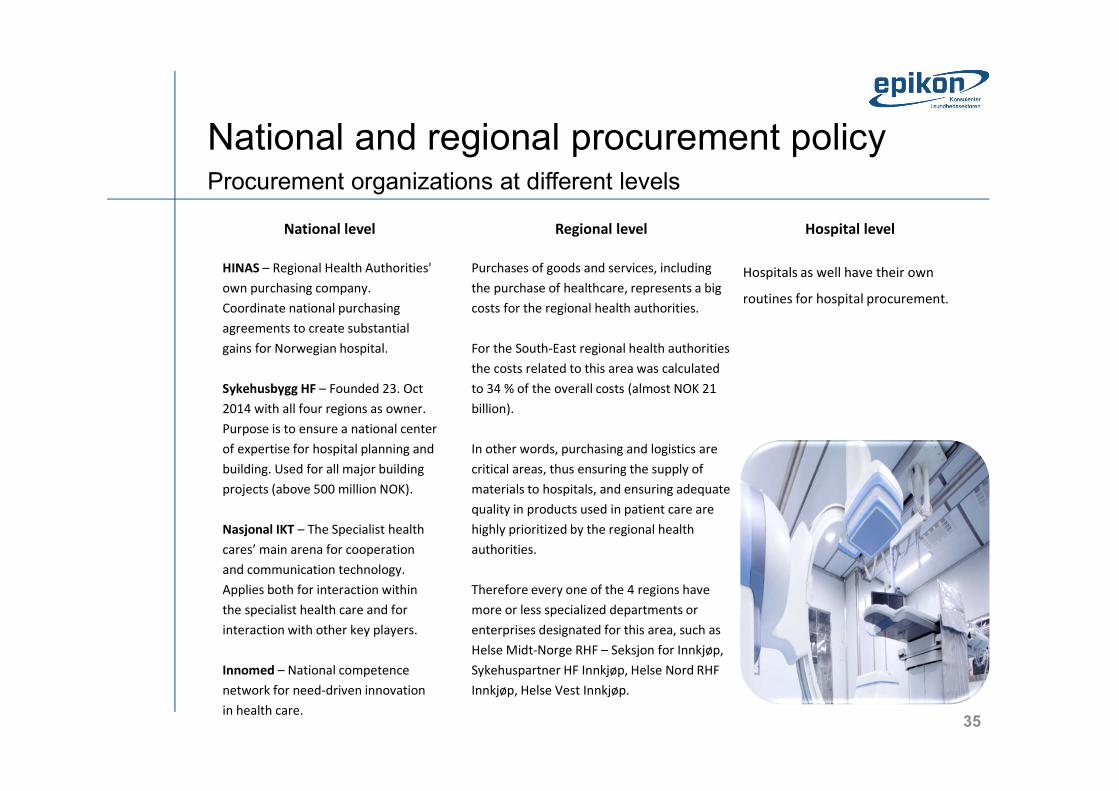

Procurement organizations at different levelsNational and regional procurement policy

National levelHINAS – Regional Health Authorities' own purchasing company. Coordinate national purchasing agreements to create substantial gains for Norwegian hospital.Sykehusbygg HF – Founded 23. Oct 2014 with all four regions as owner. Purpose is to ensure a national center of expertise for hospital planning and building. Used for all major building projects (above 500 million NOK). Nasjonal IKT – The Specialist health cares’ main arena for cooperation and communication technology. Applies both for interaction within the specialist health care and for interaction with other key players.Innomed – National competence network for need-driven innovation in health care.

Regional levelPurchases of goods and services, including the purchase of healthcare, represents a big costs for the regional health authorities. For the South-East regional health authorities the costs related to this area was calculated to 34 % of the overall costs (almost NOK 21 billion). In other words, purchasing and logistics are critical areas, thus ensuring the supply of materials to hospitals, and ensuring adequate quality in products used in patient care are highly prioritized by the regional health authorities. Therefore every one of the 4 regions have more or less specialized departments or enterprises designated for this area, such as Helse Midt-Norge RHF – Seksjon for Innkjøp, Sykehuspartner HF Innkjøp, Helse Nord RHF Innkjøp, Helse Vest Innkjøp.

Hospital levelHospitals as well have their own routines for hospital procurement.

36

Summing up the healthcare market• Procurement is being centralized in order to increase

buying power. This is supported by national organizations and regional logistics systems. However, the hospitals are quite independent especially with smaller procurements

• The EØS agreement ensures that all EU procurement rules are in effect and Norway generally adheres to «gold-plated standards»

• Language is a barrier. Most tenders in healthcare are required to be submitted in Norwegian

• “Bygde-politik” ie local politics pays an important role in healthcare. Local investments and jobs are highly valued at a policy level, but plays less role in the actual procurements

37

Focus on innovation in healthcare• All four of the Norwegian regions have strategies for

innovation in healthcare with the following in common: – All have established innovation-labs, tech clusters,

incubators, idea clinics and similar– Great variations on organisation and funding– Twin focus on healthcare improvement and regional

business development– Emphasis om collaboration with universities and to some

extent on commercial partners– Focus on innovation in procurement – primarily on a

policy level• Possible entrances as well as gatekeeping competitors

38

Group exercise• Matching your offers with Norwegian needs and

demand– Identification of relevant entry points– Discussion of market entry strategies

• Discuss with the person next to you – What is your ideal Norwegian customer? – What characterizes this customer?– Size, organization, maturity, issues, competences or lack

thereof • Are you offering a new(better/cheaper/safer etc)

solution to a known need or are you introducing solutions that require new customer understanding of their needs?

39

Market entry strategiesWhich market entry strategy havee you been considering?

Discuss the classic approaches with the person next to you

– Direct exporting– Indirect exporting (agent or distributor)– Joint ventures– Strategic alliance or partnering– Direct investment / local company

40

Q&A session• What do you need to know about the

Norwegian healthcare market and how to approach it?

41

Overview of ressourcesNational authorities• https://www.regjeringen.no/en/dep/hod/id421/• https://helsedirektoratet.no/English

National, regional and municipal associations• http://www.nasjonalikt.no/no/english/• http://sjukehusbygg.no/ national hospital building trust, in Norwegian only)• https://helsenorge.no/other-languages/english (the Norwegian healthcare portal)• http://www.spekter.no/Stottemeny/Om-Spekter/Om-Spekter/Information-in-English/• http://www.ks.no

English presentations of the four Norwegian regions• http://www.helse-sorost.no/omoss_/english_/• http://www.helse-nord.no/?lang=en_US• http://www.helse-vest.no/en/Sider/default.aspx• http://www.helse-midt.no/EN/

The national procurement organisations• https://doffin.no/en (Norwegian national notification database for public procurement)• http://hinas.no/index.php/omhinas/visjon (national healthcare procurement organization, only in Norwegian)

42

Thank you for your attention

Tobias Bøggild-Damkvist------------------------------------------------------Epikon – Konsulenter i sundhedssektorenPartner, cand.merc.(fil)Ole Maaløes Vej 3 - 2200 Kbh N - Danmark+45 2063 7324 / +47 468 22 059 - [email protected]

Please contact me if you have any questions about theNorwegian or the Danish healthcare market. Epikon can assist clients with:- Market research- Networking and introductions to clients and partners in thehealthcare sector- Bid managemt and writing of tenders

Epikon - the short version–

Who we are?• Epikon is a consulting company 100% devoted to the

healthcare sector• Our consultants know the healthcare sector in-depth

and have solved assignments for numerous public and private organizations in the Nordic countries

• Epikon believes in the value of long-lasting customer relations and we are proud to help our customers with high quality counselling, sparring, project management and facilitation

• We want to create the best solutions to the challenges and opportunities facing the healthcare sector - in close cooperation with our clients

Healthcare IT

Business Cases

Business Intelligence

Proces optimization

Sourcing and procurement

43

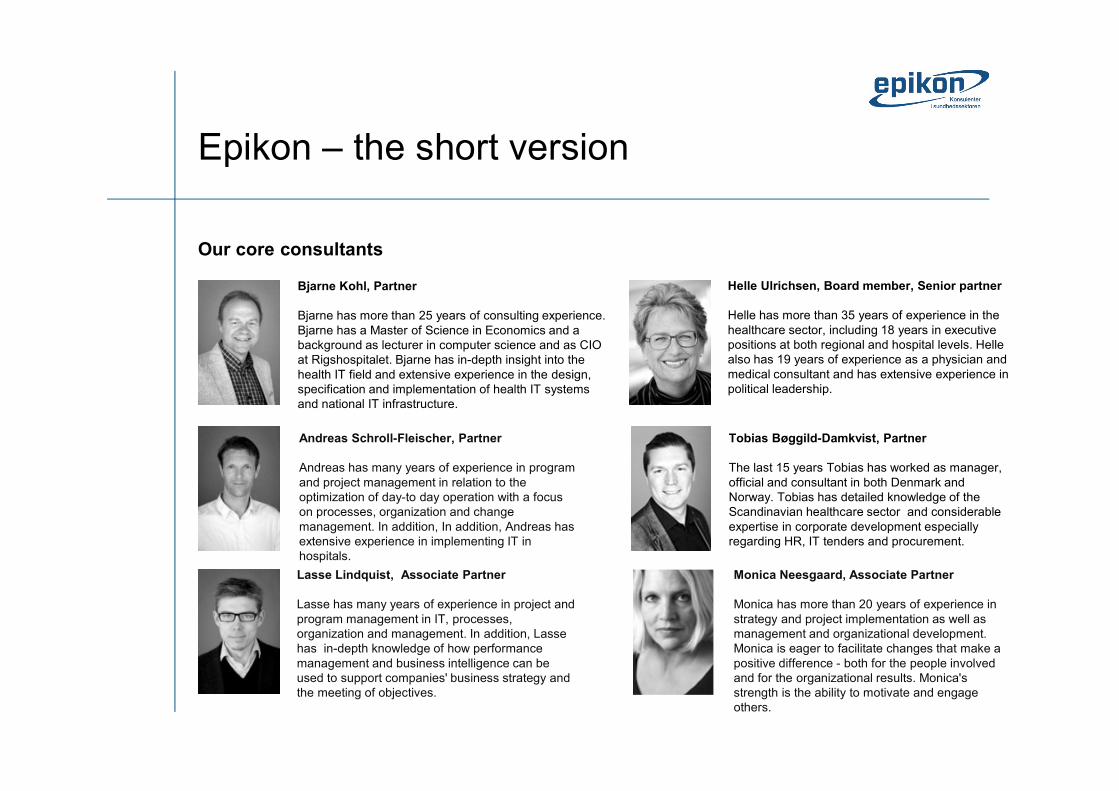

Monica Neesgaard, Associate PartnerMonica has more than 20 years of experience in strategy and project implementation as well as management and organizational development. Monica is eager to facilitate changes that make a positive difference - both for the people involved and for the organizational results. Monica's strength is the ability to motivate and engage others.

Epikon – the short versionOur core consultants

Andreas Schroll-Fleischer, PartnerAndreas has many years of experience in program and project management in relation to the optimization of day-to day operation with a focus on processes, organization and change management. In addition, In addition, Andreas has extensive experience in implementing IT in hospitals.

Bjarne Kohl, PartnerBjarne has more than 25 years of consulting experience. Bjarne has a Master of Science in Economics and a background as lecturer in computer science and as CIO at Rigshospitalet. Bjarne has in-depth insight into the health IT field and extensive experience in the design, specification and implementation of health IT systems and national IT infrastructure.

Helle Ulrichsen, Board member, Senior partnerHelle has more than 35 years of experience in the healthcare sector, including 18 years in executive positions at both regional and hospital levels. Helle also has 19 years of experience as a physician and medical consultant and has extensive experience in political leadership.

Tobias Bøggild-Damkvist, PartnerThe last 15 years Tobias has worked as manager, official and consultant in both Denmark and Norway. Tobias has detailed knowledge of the Scandinavian healthcare sector and considerable expertise in corporate development especially regarding HR, IT tenders and procurement.

Lasse Lindquist, Associate PartnerLasse has many years of experience in project and program management in IT, processes, organization and management. In addition, Lasse has in-depth knowledge of how performance management and business intelligence can be used to support companies' business strategy and the meeting of objectives.