Embed Size (px)

Citation preview

Inflation To Nudge Up To 9.4%

FDC Economic Bulletin

Financial Derivatives Company Ltd.

: 01-7739889 www.fdcng.com

October 09, 2015

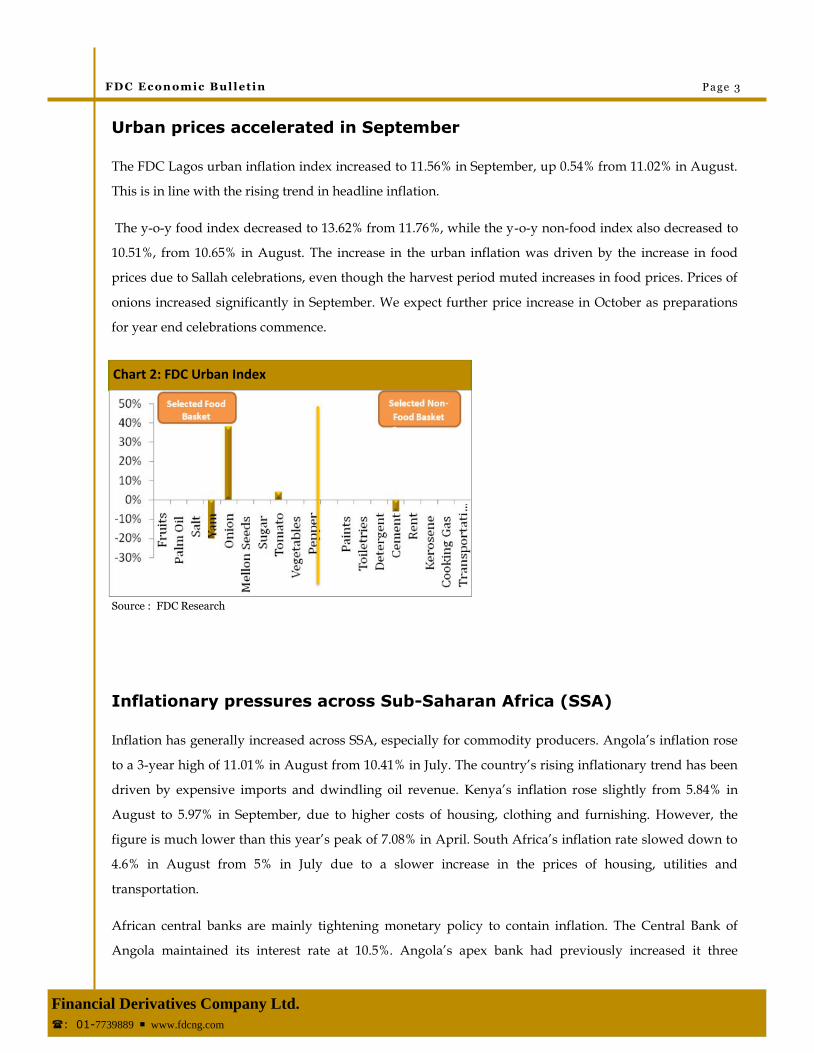

The CBN in its communiqué in July 2015 said that the inflationary pressures in Nigeria were transient in

nature. Ever since then headline inflation has increased again.

Our forecast for September headline inflation is 9.4%, which is 0.1% higher than the level in August. If

this forecast is accurate, it will mean that headline inflation has increased in 8 out of the 9 months so far

in 2015. Is the inflationary trend now more structural than transient? The primary catalysts of price

inflation in Nigeria are cost-push factors. These are being intensified by the restriction of dollars for some

critical inputs. However, this increasing inflationary trend is happening at a time when the price of diesel

has dropped by 33% from N160 to N108. Diesel is the fuel used by transporters of goods from the farms

to the markets.

Despite a favourable harvest of food items such as tubers and cereals, there was a modest uptick in

September’s price levels, mainly due to the increase in the prices of imported food items such as milk,

wheat and sugar. Furthermore, increased demand for livestock products due to the Eid-el-Kabir

celebrations led to higher inflationary pressures from the food index.

The recent release of the President’s ministerial list will help ease investor uncertainty. Though the new

cabinet did not stir up much enthusiasm, the stable environment created by revealing the President’s

team will help foster positive investor sentiment.

Source : NBS, FDC Research

Chart 1: Headline Inflation Rate

Urban prices accelerated in September

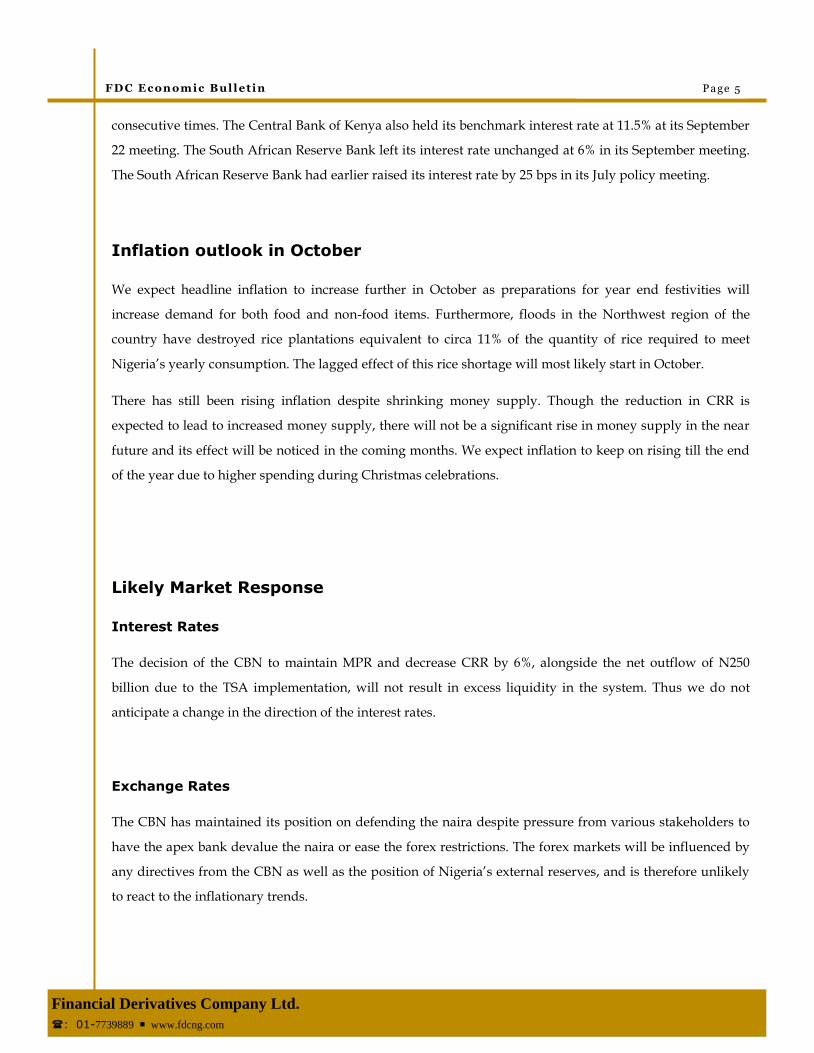

The FDC Lagos urban inflation index increased to 11.56% in September, up 0.54% from 11.02% in August.

This is in line with the rising trend in headline inflation.

The y-o-y food index decreased to 13.62% from 11.76%, while the y-o-y non-food index also decreased to

10.51%, from 10.65% in August. The increase in the urban inflation was driven by the increase in food

prices due to Sallah celebrations, even though the harvest period muted increases in food prices. Prices of

onions increased significantly in September. We expect further price increase in October as preparations

for year end celebrations commence.

Inflationary pressures across Sub-Saharan Africa (SSA)

Inflation has generally increased across SSA, especially for commodity producers. Angola’s inflation rose

to a 3-year high of 11.01% in August from 10.41% in July. The country’s rising inflationary trend has been

driven by expensive imports and dwindling oil revenue. Kenya’s inflation rose slightly from 5.84% in

August to 5.97% in September, due to higher costs of housing, clothing and furnishing. However, the

figure is much lower than this year’s peak of 7.08% in April. South Africa’s inflation rate slowed down to

4.6% in August from 5% in July due to a slower increase in the prices of housing, utilities and

transportation.

African central banks are mainly tightening monetary policy to contain inflation. The Central Bank of

Angola maintained its interest rate at 10.5%. Angola’s apex bank had previously increased it three

FD C E c on om ic Bul l et in Page 3

Financial Derivatives Company Ltd.

: 01-7739889 www.fdcng.com

Source : FDC Research

Chart 2: FDC Urban Index

consecutive times. The Central Bank of Kenya also held its benchmark interest rate at 11.5% at its September

22 meeting. The South African Reserve Bank left its interest rate unchanged at 6% in its September meeting.

The South African Reserve Bank had earlier raised its interest rate by 25 bps in its July policy meeting.

Inflation outlook in October

We expect headline inflation to increase further in October as preparations for year end festivities will

increase demand for both food and non-food items. Furthermore, floods in the Northwest region of the

country have destroyed rice plantations equivalent to circa 11% of the quantity of rice required to meet

Nigeria’s yearly consumption. The lagged effect of this rice shortage will most likely start in October.

There has still been rising inflation despite shrinking money supply. Though the reduction in CRR is

expected to lead to increased money supply, there will not be a significant rise in money supply in the near

future and its effect will be noticed in the coming months. We expect inflation to keep on rising till the end

of the year due to higher spending during Christmas celebrations.

Likely Market Response

Interest Rates

The decision of the CBN to maintain MPR and decrease CRR by 6%, alongside the net outflow of N250

billion due to the TSA implementation, will not result in excess liquidity in the system. Thus we do not

anticipate a change in the direction of the interest rates.

Exchange Rates

The CBN has maintained its position on defending the naira despite pressure from various stakeholders to

have the apex bank devalue the naira or ease the forex restrictions. The forex markets will be influenced by

any directives from the CBN as well as the position of Nigeria’s external reserves, and is therefore unlikely

to react to the inflationary trends.

FD C E c on om ic Bul l et in Page 5

Financial Derivatives Company Ltd.

: 01-7739889 www.fdcng.com

Stock Market

The influential governor of Kaduna state recently called for a reduction in interest rates in order to aid

economic growth. As an influential and leading member of the APC, his views are likely to be a critical input

into the policy direction of the country. If the CBN yields to the sentiment of lower interest rates, stock prices

will spike in response. Whilst conventional logic will suggest interest rate increases at a time of higher

inflation, it is likely that this might be a countercyclical accommodative policy to stimulate growth.

FD C E c on om ic Bul l et in Page 6

Financial Derivatives Company Ltd.

: 01-7739889 www.fdcng.com

Important Notice

This document is issued by Financial Derivatives Company. It is for information purposes only. It does not constitute any offer, recommendation or

solicitation to any person to enter into any transaction or adopt any hedging, trading or investment strategy, nor does it constitute any prediction of

likely future movements in rates or prices or any representation that any such future movements will not exceed those shown in any illustration. All

rates and figures appearing are for illustrative purposes. You are advised to make your own independent judgment with respect to any matter con-

tained herein.