Embed Size (px)

Citation preview

Page 1

IMPORTANT NOTICE: UK Value Investor provides information for investors who can make their own investment decisions without

advice. This newsletter does not contain financial advice and it should not be thought of as advice. If you think you need advice then

you should seek a regulated independent financial advisor. Please see the important notes on the back page.

Contents

FTSE 100: Valuation and Projection Page 2

Model portfolio: Monthly Review Page 3

Selling: Hill & Smith Holdings PLC (HILS) Page 19

Stock Screen Page 24

Appendices Back pages

Ideas for coping with bear market and recessions

Something rather unusual happened at the end of February. The FTSE 100’s earnings dipped

below its dividend payments, which means that the FTSE 100’s dividend is now uncovered.

Although this situation is unlikely to last for long, it does show that the current bear market

is not driven solely by investor sentiment. It is also backed up by aggressively declining

earnings and economic conditions, both of which are an additional cause for concern.

Back in 2003 when I found myself in a major bear market for the first time I did what many inexperienced

investors do: I panicked and sold pretty much all of my equity investments. Moving to cash made me feel

safe, but it also resulted in me missing out on a large part of the market’s subsequent recovery in 2003 and

2004. With another 13 years of experience under my belt I feel much better equipped for dealing with bear

markets and recessions, largely thanks to a greater understanding of and appreciation for history.

In almost every case, bear markets and recessions have been the best time to invest and the worst time to

sell out. Whether it’s the great depression of the 1930s, the great recessions of the 1970s or the global

financial crisis of 2009, they all have two things in common: 1) They are very unpleasant at the time and most

commentators think it’s the end of the world, or at least the end of equities, and 2) the returns generated by

the market after each crisis were far above average. Here are a few mental tricks which I use to stay focused

on the second point, rather than the first:

1) Don’t panic if a company cuts its dividend; 2) don’t panic if a company’s share price declines dramatically;

3) don’t panic if the whole market declines dramatically; 4) don’t watch the market or the value of your

shares every day or even every week; 5) When you do look at

your portfolio, focus primarily on the dividends paid out over

the last year, rather than today’s share prices; 6) remember

that this too shall pass, and that your portfolio’s value is likely

to be much higher in five or ten years’ time.

John Kingham, 1st March 2016

“Warren buys on bad news. This is why he has

made sure to miss good-news bull markets in

such popular industries as the Internet,

computers, biotechnology, cellular phones and

dozens of others that have seduced investors

through the years with promises of riches. He

shops when the stocks are unpopular and the

prices are cheap - when short-term doom and

gloom fog Wall Street’s eyes from seeing the

real long-term economic value.” - Mary Buffett,

The New Buffettology

March 2016

UK Value InvestorFor Defensive and Income-Focused Value Investors

John Kingham

Editor

Page 2

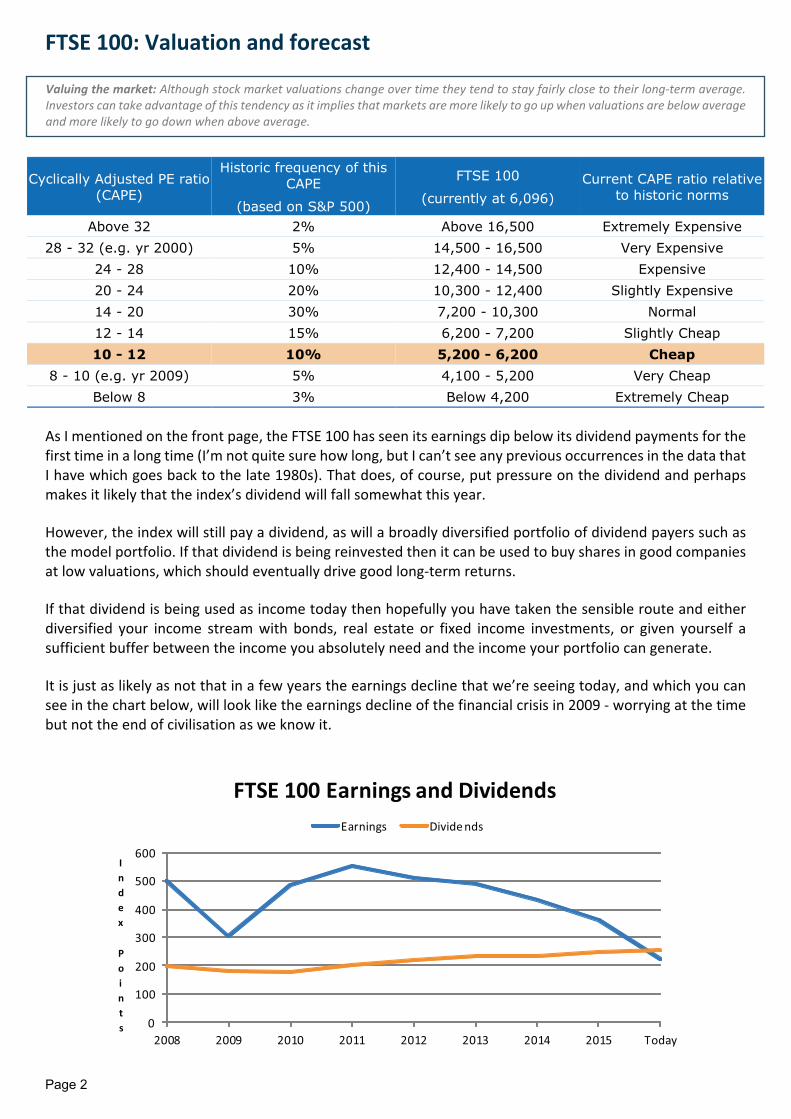

As I mentioned on the front page, the FTSE 100 has seen its earnings dip below its dividend payments for the

first time in a long time (I’m not quite sure how long, but I can’t see any previous occurrences in the data that

I have which goes back to the late 1980s). That does, of course, put pressure on the dividend and perhaps

makes it likely that the index’s dividend will fall somewhat this year.

However, the index will still pay a dividend, as will a broadly diversified portfolio of dividend payers such as

the model portfolio. If that dividend is being reinvested then it can be used to buy shares in good companies

at low valuations, which should eventually drive good long-term returns.

If that dividend is being used as income today then hopefully you have taken the sensible route and either

diversified your income stream with bonds, real estate or fixed income investments, or given yourself a

sufficient buffer between the income you absolutely need and the income your portfolio can generate.

It is just as likely as not that in a few years the earnings decline that we’re seeing today, and which you can

see in the chart below, will look like the earnings decline of the financial crisis in 2009 - worrying at the time

but not the end of civilisation as we know it.

FTSE 100: Valuation and forecast

Cyclically Adjusted PE ratio

(CAPE)

Historic frequency of this

CAPE

(based on S&P 500)

FTSE 100

(currently at 6,096)

Current CAPE ratio relative

to historic norms

Above 32 2% Above 16,500 Extremely Expensive

28 - 32 (e.g. yr 2000) 5% 14,500 - 16,500 Very Expensive

24 - 28 10% 12,400 - 14,500 Expensive

20 - 24 20% 10,300 - 12,400 Slightly Expensive

14 - 20 30% 7,200 - 10,300 Normal

12 - 14 15% 6,200 - 7,200 Slightly Cheap

10 - 12 10% 5,200 - 6,200 Cheap

8 - 10 (e.g. yr 2009) 5% 4,100 - 5,200 Very Cheap

Below 8 3% Below 4,200 Extremely Cheap

Valuing the market: Although stock market valuations change over time they tend to stay fairly close to their long-term average.

Investors can take advantage of this tendency as it implies that markets are more likely to go up when valuations are below average

and more likely to go down when above average.

0

100

200

300

400

500

600

2008 2009 2010 2011 2012 2013 2014 2015 Today

I

n

d

e

x

P

o

i

n

t

s

FTSE 100 Earnings and Dividends

Earnings Divide nds

Page 3

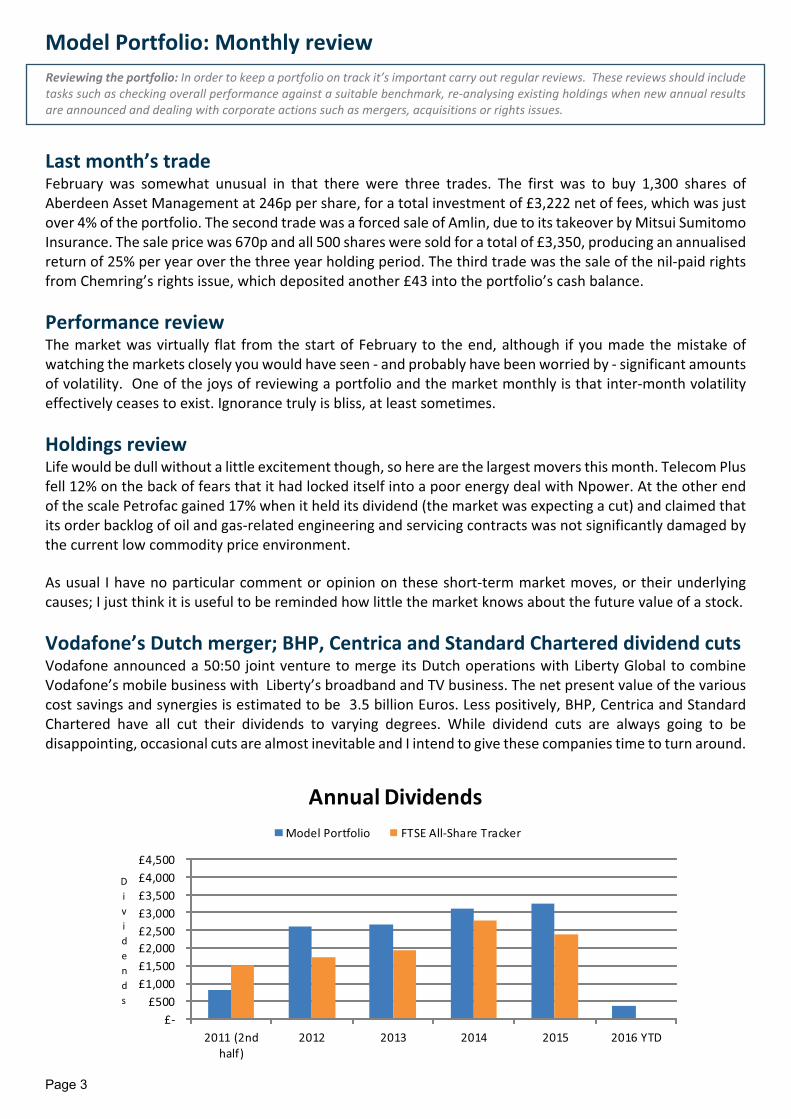

Model Portfolio: Monthly review

Last month’s tradeFebruary was somewhat unusual in that there were three trades. The first was to buy 1,300 shares of

Aberdeen Asset Management at 246p per share, for a total investment of £3,222 net of fees, which was just

over 4% of the portfolio. The second trade was a forced sale of Amlin, due to its takeover by Mitsui Sumitomo

Insurance. The sale price was 670p and all 500 shares were sold for a total of £3,350, producing an annualised

return of 25% per year over the three year holding period. The third trade was the sale of the nil-paid rights

from Chemring’s rights issue, which deposited another £43 into the portfolio’s cash balance.

Performance reviewThe market was virtually flat from the start of February to the end, although if you made the mistake of

watching the markets closely you would have seen - and probably have been worried by - significant amounts

of volatility. One of the joys of reviewing a portfolio and the market monthly is that inter-month volatility

effectively ceases to exist. Ignorance truly is bliss, at least sometimes.

Holdings reviewLife would be dull without a little excitement though, so here are the largest movers this month. Telecom Plus

fell 12% on the back of fears that it had locked itself into a poor energy deal with Npower. At the other end

of the scale Petrofac gained 17% when it held its dividend (the market was expecting a cut) and claimed that

its order backlog of oil and gas-related engineering and servicing contracts was not significantly damaged by

the current low commodity price environment.

As usual I have no particular comment or opinion on these short-term market moves, or their underlying

causes; I just think it is useful to be reminded how little the market knows about the future value of a stock.

Vodafone’s Dutch merger; BHP, Centrica and Standard Chartered dividend cutsVodafone announced a 50:50 joint venture to merge its Dutch operations with Liberty Global to combine

Vodafone’s mobile business with Liberty’s broadband and TV business. The net present value of the various

cost savings and synergies is estimated to be 3.5 billion Euros. Less positively, BHP, Centrica and Standard

Chartered have all cut their dividends to varying degrees. While dividend cuts are always going to be

disappointing, occasional cuts are almost inevitable and I intend to give these companies time to turn around.

Reviewing the portfolio: In order to keep a portfolio on track it’s important carry out regular reviews. These reviews should include

tasks such as checking overall performance against a suitable benchmark, re-analysing existing holdings when new annual results

are announced and dealing with corporate actions such as mergers, acquisitions or rights issues.

£-

£500

£1,000

£1,500

£2,000

£2,500

£3,000

£3,500

£4,000

£4,500

2011 (2nd

half)

2012 2013 2014 2015 2016 YTD

D

i

v

i

d

e

n

d

s

Annual Dividends

Model Portfolio FTSE All-Share Tracker

Page 4

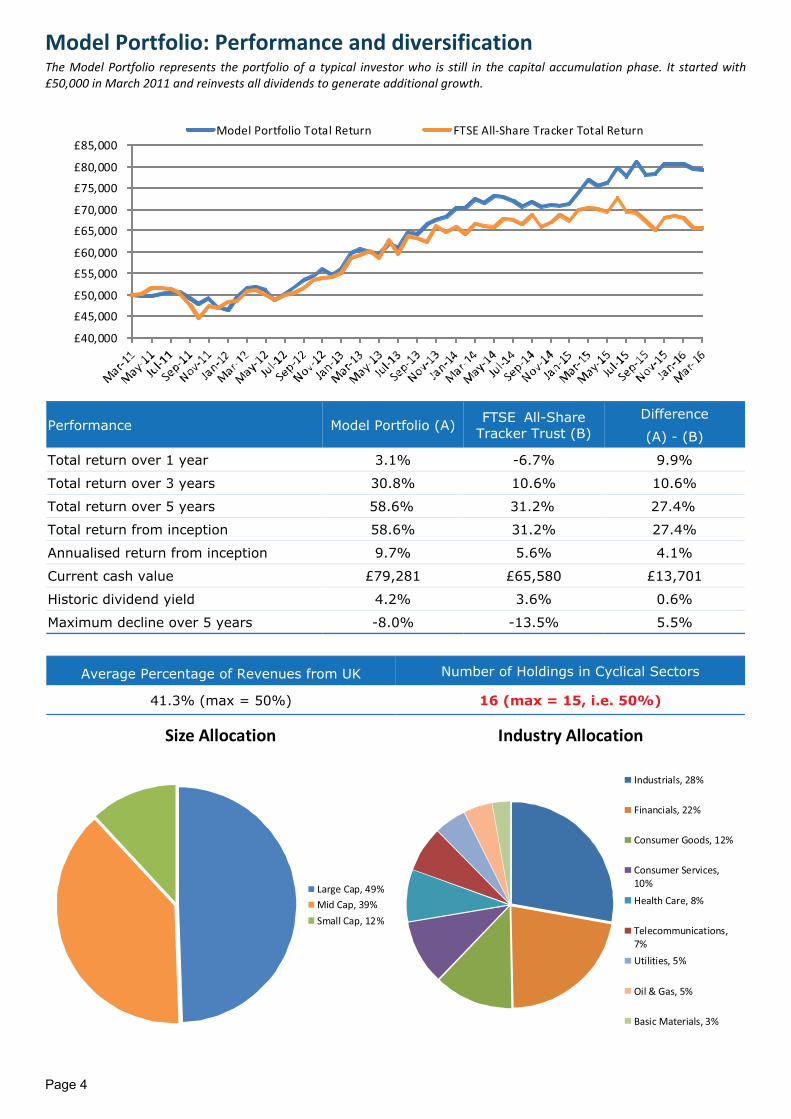

Model Portfolio: Performance and diversification

Average Percentage of Revenues from UK Number of Holdings in Cyclical Sectors

41.3% (max = 50%) 16 (max = 15, i.e. 50%)

Performance Model Portfolio (A)FTSE All-Share

Tracker Trust (B)

Difference

(A) - (B)

Total return over 1 year 3.1% -6.7% 9.9%

Total return over 3 years 30.8% 10.6% 10.6%

Total return over 5 years 58.6% 31.2% 27.4%

Total return from inception 58.6% 31.2% 27.4%

Annualised return from inception 9.7% 5.6% 4.1%

Current cash value £79,281 £65,580 £13,701

Historic dividend yield 4.2% 3.6% 0.6%

Maximum decline over 5 years -8.0% -13.5% 5.5%

The Model Portfolio represents the portfolio of a typical investor who is still in the capital accumulation phase. It started with

£50,000 in March 2011 and reinvests all dividends to generate additional growth.

£40,000

£45,000

£50,000

£55,000

£60,000

£65,000

£70,000

£75,000

£80,000

£85,000

Model Portfolio Total Return FTSE All-Share Tracker Total Return

Size Allocation

Large Cap, 49%

Mid Cap, 39%

Small Cap, 12%

Industry Allocation

Industrials, 28%

Financials, 22%

Consumer Goods, 12%

Consumer Services,

10%

Health Care, 8%

Telecommunications,

7%

Utilities, 5%

Oil & Gas, 5%

Basic Materials, 3%

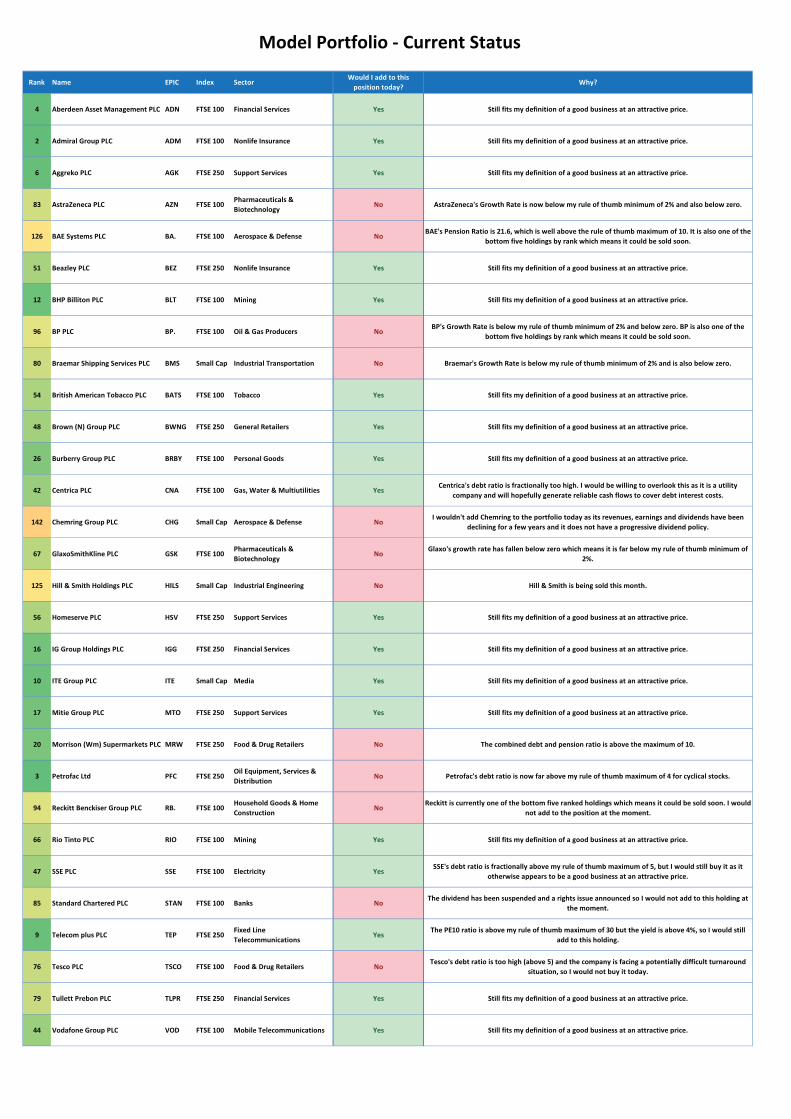

���������������� ������������������������������ ������������ ����� ������������������������ �

���� ����� ���� ��� ����� �����������

������������

�� ������

!������"#

$��%��

���

$��%��

&����'

����

���(��)����� *+�,����

���������

����

���������

�����������������

- .(./ 0�������$���1��2 0�� ,3���"## ���������������� 4"5(67 "7(89 :(7/ -.(8 ".(./ 8-/ :6/ #(# 96/ 9 4"-(8# #5;"";-#".

. -(#/ �������2� �, ,3���-:#<����=��1���>���� �����?�

�����)����49(9# ."6(-8 :(#/ ".(- "-(./ 58/ -8/ 5(" --/ -. 4".(8# #5;#.;-#"6

6 6(#/ 0)�������0���������������2 0�� ,3���"## ,������������ ���� 4-(6- "#(-. 9("/ ":(# -"(-/ 5:/ "./ #(# :-/ : 4-(67 #:;#-;-#"7

7 6(:/ 0��������2 0$+ ,3���-:# ��11������ ���� 49(99 "#(85 .("/ ".(- "5(5/ 99/ "7/ -(- :/ 6 49(5. #9;#";-#"7

8 6(./ 3�������1�����2 3�� ,3���-:# ,�����2����3���������������� 49(:# -"(": 6(5/ .#(. "5(6/ 99/ .7/ -(7 "##/ 8 45("7 #7;#:;-#":

"# -(5/ �3��$���1��2 �3� ������ �1 ����� 4"(.. ""(77 :(7/ ""(# 7(./ 5"/ -5/ -(" :/ 7 4"(9: #7;#.;-#":

"- "(-/ @���@��������2 @23 ,3���"## ������ 45("7 7("6 ""(:/ 6(: 7(#/ 7./ "5/ -(# "/ �;0 4"8("# "-;#8;-#""

"7 6(6/ �$�$���1�����������2 �$$ ,3���-:# ,������������ ���� 45(56 -"(:" .(7/ -:(6 ".(:/ 99/ -7/ #(# :#/ 9 47(#. #:;#8;-#"6

"5 .(:/ �����$���1��2 �3< ,3���-:# ��11������ ���� 4-(9# "-(7- 6(-/ ":(" 9(8/ 8-/ "-/ .(7 85/ �;0 4-(.9 "7;#8;-#""

-# "(5/ ���������A��B���1����������2 ��� ,3���-:# ,����?�������������� 4"(99 ".(#- 5(./ 8(5 8(6/ 58/ 5/ 6(: "##/ "7 4-(8. #5;#:;-#".

-7 .(9/ @��)���'�$���1��2 @�@! ,3���"## ���������$���� 4"-(78 "7(:8 -(9/ -6(- "7(:/ 9./ -7/ #(- "#/ -: 4".(5# #7;"";-#":

6- "(:/ ��������2 �0 ,3���"## $��>������?������������ 4-("" "-(-5 :(5/ 9(6 6(6/ 5"/ 8/ :(. 77/ -: 4.(-- "#;#9;-#"-

66 -(./ C�������$���1��2 C<� ,3���"## ��)����3���������������� 4-("8 8(95 :("/ "-(# .(8/ 8-/ 5/ -(# "5/ �;0 4-(#- #-;#7;-#""

65 .(-/ �����2 ��� ,3���"## ��������' 4".(98 ".(#" 7(6/ "6(7 :(./ 9./ 9/ :(- 85/ �;0 4".(.. #";"";-#""

69 .(9/ @��%��A�B�$���1��2 @��$ ,3���-:# $��������������� 4.(.- "-(85 6(./ ".(7 7(-/ 5:/ ""/ .(9 "##/ "5 4.(65 #5;"";-#"6

:" 6(./ @��D��'��2 @�E ,3���-:# ���������������� 4.(:8 ""(-9 -(9/ ":(" :(./ 58/ "5/ "(. "6/ -- 4.(-8 #6;#8;-#":

:6 .(:/ @������0��������3�)������2 @03� ,3���"## 3�)���� 4.8(": -6(:" .(8/ --(9 7(./ 58/ "5/ .(" ""/ -9 4..(-- #8;#8;-#".

:7 6(./ ������� ���2 ��C ,3���-:# ��11������ ���� 46(#: -.(## .("/ "8(. 7(./ 58/ "9/ "(8 :#/ "5 4-(7. #:;#9;-#".

77 "(6/ ����3�����2 ��< ,3���"## ������ 4"9(7# -.(56 5(5/ :(5 6(9/ :6/ ""/ -(. "/ "5 4-8(99 #5;#8;-#"-

75 .(7/ $��������+������2 $�+ ,3���"##���������������?�

@����������'4"6("# "9(7. :(5/ ":(9 #(6/ 5"/ "9/ 6(6 :/ -: 4"6(-5 #8;#";-#":

57 "(./ 3������2 3� < ,3���"## ,����?�������������� 4"(96 "7(-5 #(7/ 7(8 -("/ 75/ 9/ :(6 78/ -9 4.(## "";#7;-#"-

58 .(#/ 3��������)����2 32�� ,3���-:# ,������������ ���� 4.(65 8(#6 6(8/ 9(- -(5/ :6/ "6/ -(6 :#/ �;0 4.(:8 #:;#8;-#""

9# -(5/ @����������11������� ������2 @�� ������ �1 ����������3����1������ 46(-- "5(97 7(-/ "#(5 #(./ :9/ ":/ "(- 7"/ �;0 46(58 ".;#:;-#""

9. 6(#/ 0���E�������2 0E� ,3���"##���������������?�

@����������'46-(#6 -5(". 6(:/ "6(5 �"(:/ 5"/ -#/ -(# "5/ "8 46"(75 #7;#5;-#":

9: "("/ �������� ���������2 �30� ,3���"## @���� 46(.# �"-(76 -(-/ 6(8 �#(./ :6/ ""/ �;0 :/ 8 4"-(": #5;#5;-#"6

86 6(-/ ������@���������$���1��2 �@( ,3���"##����������$�����?������

���������477(#. -:(65 -("/ ."(: 5(6/ 9./ -"/ "(: 5/ -5 469("" #5;#-;-#"6

87 -(-/ @���2 @�( ,3���"## <���?�$������������ 4.(:# ":(55 5(7/ 7(" �-(9/ :9/ "#/ .(. -#/ �;0 46(86 #6;#.;-#""

"-: :(#/ �����?����������������2 ��2� ������ �1 ��������������������� 45(87 "9(:8 -(./ -.(7 5(6/ 99/ "#/ .(: 67/ -9 46(." #5;#7;-#".

"-7 :(-/ @0���'������2 @0( ,3���"## 0����1����?������� 4:("- "7(6" 6("/ "6(7 #(5/ 5:/ 8/ .(" -"/ �;0 4.(#9 -";#7;-#""

"6- #(7/ ��������$���1��2 �$ ������ �1 0����1����?������� 4"(-9 "6.(9- "(7/ 7(# �9(6/ :6/ 8/ 6(7 ":/ �;0 47(98 "9;#6;-#""

5(8/ ���

���������������� ����������

���� ���� ��� ����� �����������������������

�����������������

!"�������!��������#������$ !%� &'���()) &������������*���� +�� ������������������������#����"������������������*�������,

- !�������.������$ !%� &'���()) ���������������� +�� ������������������������#����"������������������*�������,

/ !##������$ !.0 &'���-1) ����������*���� +�� ������������������������#����"������������������*�������,

23 !���4�������$ !4� &'���())���������������5�

6���������#��� !���4�����7��.��8�����������8�"���8��������������"�����������-9����������"���8�:���,

(-/ 6!����������$ 6!, &'���()) !���������5�%����� ��6!�7������������������-(,/;�8��������8�����"�*���������������"�����������(),��������������������

"�����*��������#��"�������8�������������������"�����������,

1( 6��:�����$ 6�4 &'���-1) ���������������� +�� ������������������������#����"������������������*�������,

(- 6<��6��������$ 6$' &'���()) �����# +�� ������������������������#����"������������������*�������,

=/ 6���$ 6�, &'���()) >���5�.������������ ��6�7��.��8���������"���8��������������"�����������-9�����"���8�:���,�6�������������������

"�����*��������#��"�������8�������������������"�����������,

2) 6��������������#����*������$ 6�� ������ �� ����������'����������� �� 6������7��.��8���������"���8��������������"�����������-9�������������"���8�:���,

1 6������!��������'�"������$ 6!'� &'���()) '�"���� +�� ������������������������#����"������������������*�������,

2 6��8��?�@�.������$ 6��. &'���-1) .��������������� +�� ������������������������#����"������������������*�������,

-/ 6��"�����.������$ 6�6+ &'���()) ���������.���� +�� ������������������������#����"������������������*�������,

- ��������$ �! &'���()) .��;������5������������ +�� ������7����"�������������������������#�,���8�����"��8�����#����*���������������������������

������������8�������������#������������"����������8������*�����"������������,

( - ������#�.������$ <. ������ �� !���������5�%����� ����8�����7����� ������#���������������������������*�����;�������#��������*���������*��"����

��������#�������8�����������������������*�������#�����*����*������������,�

/A .��������0������$ .�0 &'���())���������������5�

6���������#���

.����7��#��8����������������"���8�:����8�������������������"���8��������������"�����������

-9,

(-1 <����5������<�����#���$ <�$� ������ �� ������������#�������# �� <����5���������"���#��������������,

1/ <������*���$ <�B &'���-1) ����������*���� +�� ������������������������#����"������������������*�������,

(/ �.�.�����<�����#���$ �.. &'���-1) &������������*���� +�� ������������������������#����"������������������*�������,

() �'��.������$ �'� ������ �� ����� +�� ������������������������#����"������������������*�������,

(A �����.������$ �'> &'���-1) ����������*���� +�� ������������������������#����"������������������*�������,

-) ���������?��@��������������$ ��� &'���-1) &����5�%��#��������� �� '������"�������"����������������������"�*���������������(),

3 �������$� �& &'���-1)>����C������;����*�����5�

%����"������ ������7����"�����������8�����"�*���������������"����������� ������������������,

= ������6���������.������$ �6, &'���())<���������.�����5�<����

�����������

���������������������������"�����*���������������#��8�������������������"�����������,���8�����

������������������������������,

// ����'�����$ ��> &'���()) �����# +�� ������������������������#����"������������������*�������,

A �����$ ��� &'���()) ��������� +�����7����"���������������������"�*���������������"�����������1;�"����8����������"����������

����8��������������"����#����"������������������*�������,

21 �������� ���������$ �'!� &'���()) 6���� ��'�����*����������"����������������������#������������������������8������������������������#���

��������,

= '�������������$ '�� &'���-1)&�����$����

'����������������+��

'�����()����������"�*���������������"�����������3)�"���������������"�*�� 9;������8����������

����������������#,

A/ '������$ '� > &'���()) &����5�%��#��������� ��'����7����"��������������#��?�"�*��1@�����������������������#������������������������������

�������;������8��������"���������,

A= '��������"����$ '$�� &'���-1) &������������*���� +�� ������������������������#����"������������������*�������,

B�������.������$ B>% &'���()) ��"����'���������������� +�� ������������������������#����"������������������*�������,

Page 7

Model Portfolio: Latest interim results

23rd Feb: BHP Billiton, Mining (cyclical), Large-Cap (£15.5bn)

“We are among the world’s largest producers of major commodities, including iron ore, metallurgical coal,

copper and uranium, and have substantial interests in conventional and unconventional oil and gas and

energy coal.” (www.bhpbilliton.com)

Revenue down 37% Dividend down 74%

Quotes from the interim results

“While we were prepared for lower prices across our commodities, the reduction over the last six months has

been more severe and synchronised than expected. The short to medium-term outlook for the sector

remains challenging. We expect prices will take time to recover and are likely to remain volatile, however this

environment should provide opportunities. We enter this downturn from a position of strength, with the

simplest portfolio of high-quality assets, sector-leading operating capabilities, rising capital flexibility as

current projects are completed and a strong balance sheet.“

“Our strong balance sheet remains a fundamental enabler of our strategy. It provides access to sufficient,

low-cost funding at all points in the cycle which provides optionality and insulates our operations from rising

volatility.“

“The adoption of a 50 per cent dividend payout ratio will re-phase distributions to shareholders and while

this payout level is in line with the average cash returned to shareholders since the merger, dividends will be

more closely linked to the performance of our business. At every reporting period, the Board will consider

cash returns in excess of the minimum implied by the new payout ratio.”

“The market level does not, as so many imagine, represent the consensus judgement of experts who

have carefully weighed the long-term evidence. The market is high because of the combined effect

of indifferent thinking by millions of people, very few of whom feel the need to perform careful

research on the long-term investment value of the aggregate stock market, and who are motivated

substantially by their own emotions, random attentions, and perceptions of conventional wisdom.

Their all-too-human behaviour is heavily influenced by news media that are interested in attracting

viewers or readers, with limited incentive to discipline their readers with the type of quantitative

analysis that might give them a correct impression of the aggregate stock market level.”

Professor Robert Shiller, Irrational Exuberance (2000 edition, written shortly before the bursting of

the dot-com bubble)

Page 8

Quotes from the annual results presentation

“The recent sharp fall in oil prices has had a big impact on our 2015 results – as it has for the whole industry.

The key in such times is to adapt and compete in the new environment. At BP, I believe we have a distinctive

track record of understanding, responding and adapting to change quickly and effectively. I believe our swift

response, the fundamental principles of our strategy, and the solid day-to-day delivery in our businesses are

all serving us well in this environment.”

“In BP we recognised early on, the need to focus on a set of clear priorities for the near term. You may recall

we called these priorities the 4 D’s – ongoing delivery in the business; a disciplined reset of our capital and

cash costs; completing our planned divestments; and most importantly, maintaining our dividend as the first

priority in our financial framework. In 2015, we did make good progress against these priorities.”

“We also reached a milestone - a significant one - in July with the announcement of the agreements in

principle with the United States government and five Gulf States to settle all federal and state claims arising

from the Deepwater Horizon oil spill. This leaves us able to focus more clearly on the future.”

“As we look forward in 2016 we continue to adapt to the changing circumstances. I am convinced we are

responding smartly; doing the right things and that, as we adapt, we are also learning and enhancing our

ability to adapt even further for what we expect to be a very tough year ahead. Our balance sheet was

strengthened by divestments after 2010 to provide flexibility for Deepwater Horizon uncertainties as well as

this sort of price volatility. And the rapid pace at which we are resetting the business is putting us well down

a path of rebalancing our financial framework. All of this is supporting our ongoing commitment to sustaining

the dividend.”

Revenue

Down 34%

10-Year average earnings

Down 5%

Dividend

Up 7%

Debt Ratio (max 4)

3.8

Pension Ratio (max 10)

5.8

Does it pass the buy tests?

No (growth rate too low)

Model Portfolio: Latest annual results

2nd Feb - BP, Oil & Gas Producers (cyclical), Large-Cap (£64.5bn)

“BP is one of the world's leading international oil and gas companies. We provide customers with fuel for

transportation, energy for heat and light, lubricants to keep engines moving, and the petrochemicals

products used to make everyday items as diverse as paints, clothes and packaging.” (www.bp.com)

0

50,000

100,000

150,000

200,000

250,000

300,000

0

10

20

30

40

50

60

70

80

90

100

2007 2008 2009 2010 2011 2012 2013 2014 2015

£

M

i

l

l

i

o

n

s

P

e

n

c

e

p

e

r

s

h

a

r

e

Normalised Earnings (left axis) Dividends (left axis) Revenue (right axis)

Page 9

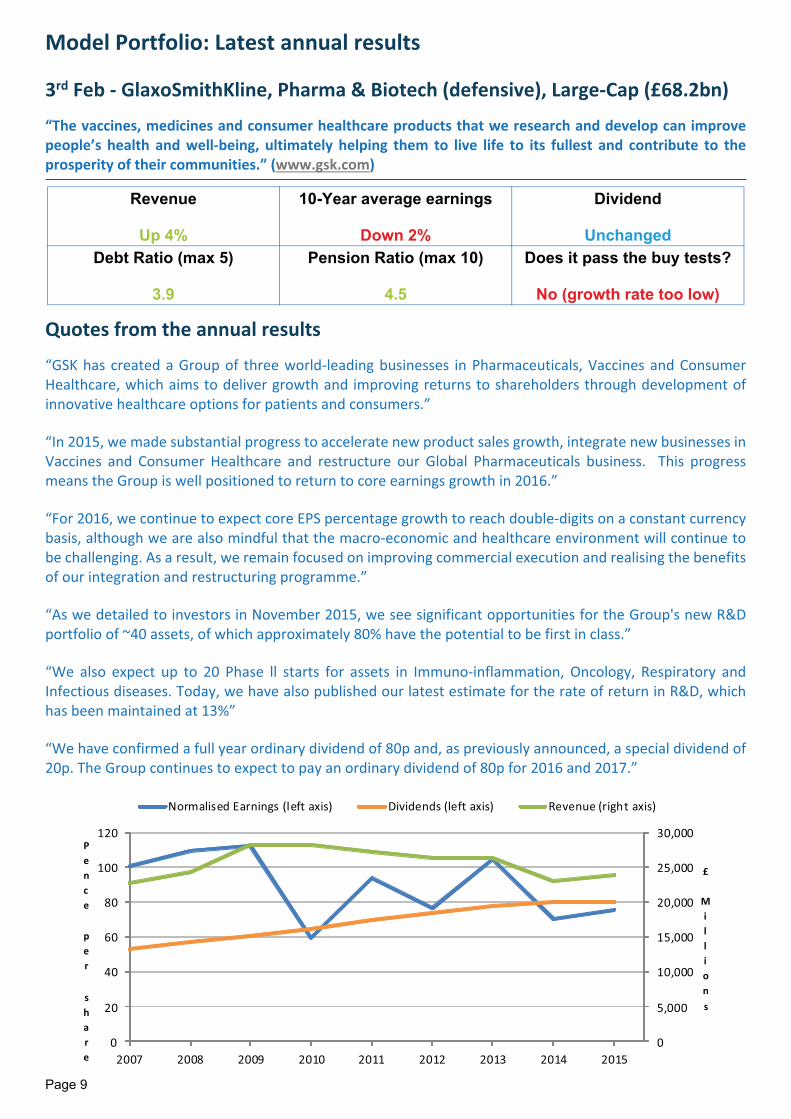

Quotes from the annual results

“GSK has created a Group of three world-leading businesses in Pharmaceuticals, Vaccines and Consumer

Healthcare, which aims to deliver growth and improving returns to shareholders through development of

innovative healthcare options for patients and consumers.”

“In 2015, we made substantial progress to accelerate new product sales growth, integrate new businesses in

Vaccines and Consumer Healthcare and restructure our Global Pharmaceuticals business. This progress

means the Group is well positioned to return to core earnings growth in 2016.”

“For 2016, we continue to expect core EPS percentage growth to reach double-digits on a constant currency

basis, although we are also mindful that the macro-economic and healthcare environment will continue to

be challenging. As a result, we remain focused on improving commercial execution and realising the benefits

of our integration and restructuring programme.”

“As we detailed to investors in November 2015, we see significant opportunities for the Group's new R&D

portfolio of ~40 assets, of which approximately 80% have the potential to be first in class.”

“We also expect up to 20 Phase ll starts for assets in Immuno-inflammation, Oncology, Respiratory and

Infectious diseases. Today, we have also published our latest estimate for the rate of return in R&D, which

has been maintained at 13%”

“We have confirmed a full year ordinary dividend of 80p and, as previously announced, a special dividend of

20p. The Group continues to expect to pay an ordinary dividend of 80p for 2016 and 2017.”

Revenue

Up 4%

10-Year average earnings

Down 2%

Dividend

Unchanged

Debt Ratio (max 5)

3.9

Pension Ratio (max 10)

4.5

Does it pass the buy tests?

No (growth rate too low)

Model Portfolio: Latest annual results

3rd Feb - GlaxoSmithKline, Pharma & Biotech (defensive), Large-Cap (£68.2bn)

“The vaccines, medicines and consumer healthcare products that we research and develop can improve

people’s health and well-being, ultimately helping them to live life to its fullest and contribute to the

prosperity of their communities.” (www.gsk.com)

0

5,000

10,000

15,000

20,000

25,000

30,000

0

20

40

60

80

100

120

2007 2008 2009 2010 2011 2012 2013 2014 2015

£

M

i

l

l

i

o

n

s

P

e

n

c

e

p

e

r

s

h

a

r

e

Normalised Earnings (left axis) Dividends (left axis) Revenue (right axis)

Page 10

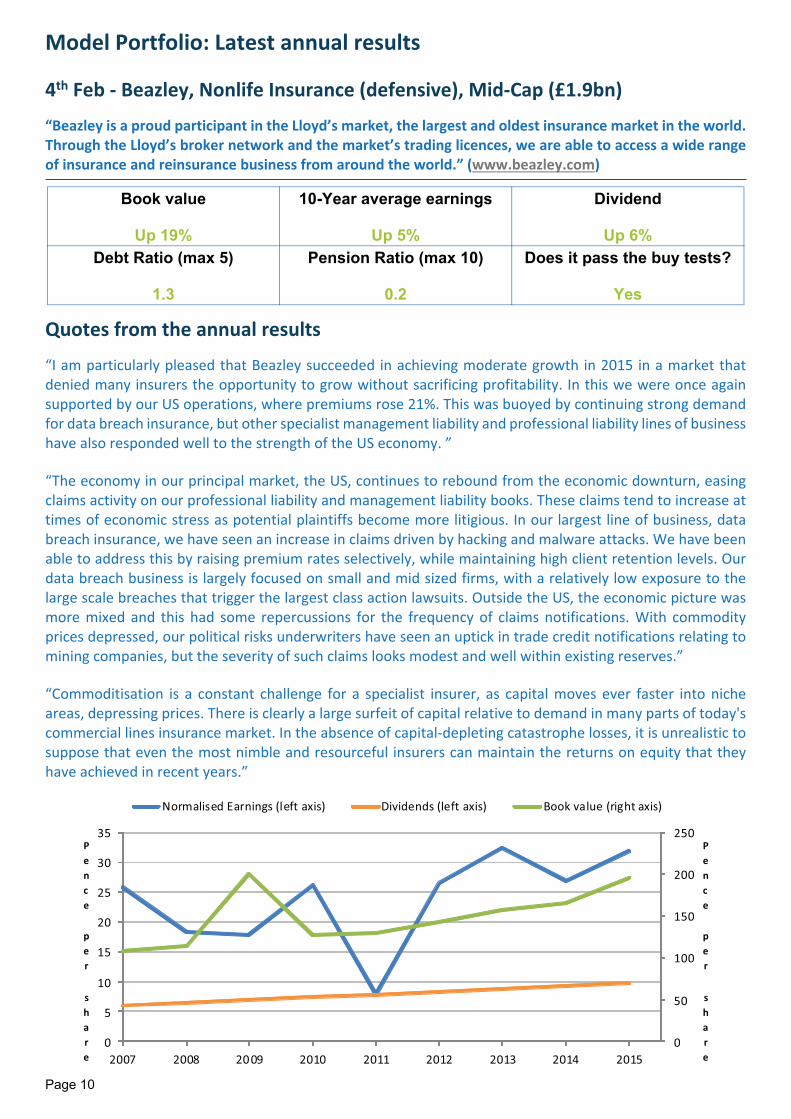

Quotes from the annual results

“I am particularly pleased that Beazley succeeded in achieving moderate growth in 2015 in a market that

denied many insurers the opportunity to grow without sacrificing profitability. In this we were once again

supported by our US operations, where premiums rose 21%. This was buoyed by continuing strong demand

for data breach insurance, but other specialist management liability and professional liability lines of business

have also responded well to the strength of the US economy. ”

“The economy in our principal market, the US, continues to rebound from the economic downturn, easing

claims activity on our professional liability and management liability books. These claims tend to increase at

times of economic stress as potential plaintiffs become more litigious. In our largest line of business, data

breach insurance, we have seen an increase in claims driven by hacking and malware attacks. We have been

able to address this by raising premium rates selectively, while maintaining high client retention levels. Our

data breach business is largely focused on small and mid sized firms, with a relatively low exposure to the

large scale breaches that trigger the largest class action lawsuits. Outside the US, the economic picture was

more mixed and this had some repercussions for the frequency of claims notifications. With commodity

prices depressed, our political risks underwriters have seen an uptick in trade credit notifications relating to

mining companies, but the severity of such claims looks modest and well within existing reserves.”

“Commoditisation is a constant challenge for a specialist insurer, as capital moves ever faster into niche

areas, depressing prices. There is clearly a large surfeit of capital relative to demand in many parts of today's

commercial lines insurance market. In the absence of capital-depleting catastrophe losses, it is unrealistic to

suppose that even the most nimble and resourceful insurers can maintain the returns on equity that they

have achieved in recent years.”

Book value

Up 19%

10-Year average earnings

Up 5%

Dividend

Up 6%

Debt Ratio (max 5)

1.3

Pension Ratio (max 10)

0.2

Does it pass the buy tests?

Yes

Model Portfolio: Latest annual results

4th Feb - Beazley, Nonlife Insurance (defensive), Mid-Cap (£1.9bn)

“Beazley is a proud participant in the Lloyd’s market, the largest and oldest insurance market in the world.

Through the Lloyd’s broker network and the market’s trading licences, we are able to access a wide range

of insurance and reinsurance business from around the world.” (www.beazley.com)

0

50

100

150

200

250

0

5

10

15

20

25

30

35

2007 2008 2009 2010 2011 2012 2013 2014 2015

P

e

n

c

e

p

e

r

s

h

a

r

e

P

e

n

c

e

p

e

r

s

h

a

r

e

Normalised Earnings (left axis) Dividends (left axis) Book value (right axis)

Page 11

Quotes from the annual results

“We delivered a strong pipeline and financial performance in 2015 as we begin the next phase in our strategic

journey. The Growth Platforms delivered an 11% rise in Product Sales that, along with the 7% increase in Core

EPS, demonstrated the underlying strength of our business. Our culture of innovation continued to drive R&D

productivity, with six regulatory approvals in the year. This momentum will continue in 2016 as we anticipate

six regulatory submissions and around ten major data readouts.”

“We strengthened the strategic importance of Oncology, bringing to patients next-generation therapies such

as Tagrisso in lung cancer and Lynparza in ovarian cancer, as well as a promising immuno-oncology pipeline.

Alongside this organic progress, we also continued to invest in our main therapy areas through key

agreements with Acerta Pharma, ZS Pharma, and Takeda.”

“As we face the transitional period of patent expiry for Crestor in the US, we're confident that our strong

execution on strategy, combined with the benefits of focused investments and new launches, keeps us on

track to return to sustainable growth in line with our targets.”

“[Full Year] 2016 [Constant Exchange Rate] guidance - a low to mid single-digit percentage decline in Total

Revenue and a low to mid single-digit percentage decline in Core EPS; includes dilutive effects from recent

transactions.”

“The Board reaffirms its commitment to the Company's progressive dividend policy.”

Revenue

Unchanged

10-Year average earnings

Down 2%

Dividend

Up 6%

Debt Ratio (max 5)

3.3

Pension Ratio (max 10)

2.9

Does it pass the buy tests?

No (growth rate too low)

Model Portfolio: Latest annual results

4th Feb - AstraZeneca, Pharma & Biotech (defensive), Large-Cap (£52.0bn)

“A global, innovation-driven biopharmaceutical business that focuses on the discovery, development and

commercialisation of prescription medicines, primarily in Respiratory, Inflammation and Autoimmunity,

Cardiovascular and Metabolic Disease and Oncology” (www.astrazeneca.com)

0

5,000

10,000

15,000

20,000

25,000

0

50

100

150

200

250

300

350

400

450

500

2007 2008 2009 2010 2011 2012 2013 2014 2015

£

M

i

l

l

i

o

n

s

P

e

n

c

e

p

e

r

s

h

a

r

e

Normalised Earnings (left axis) Dividends (left axis) Revenue (right axis)

Page 12

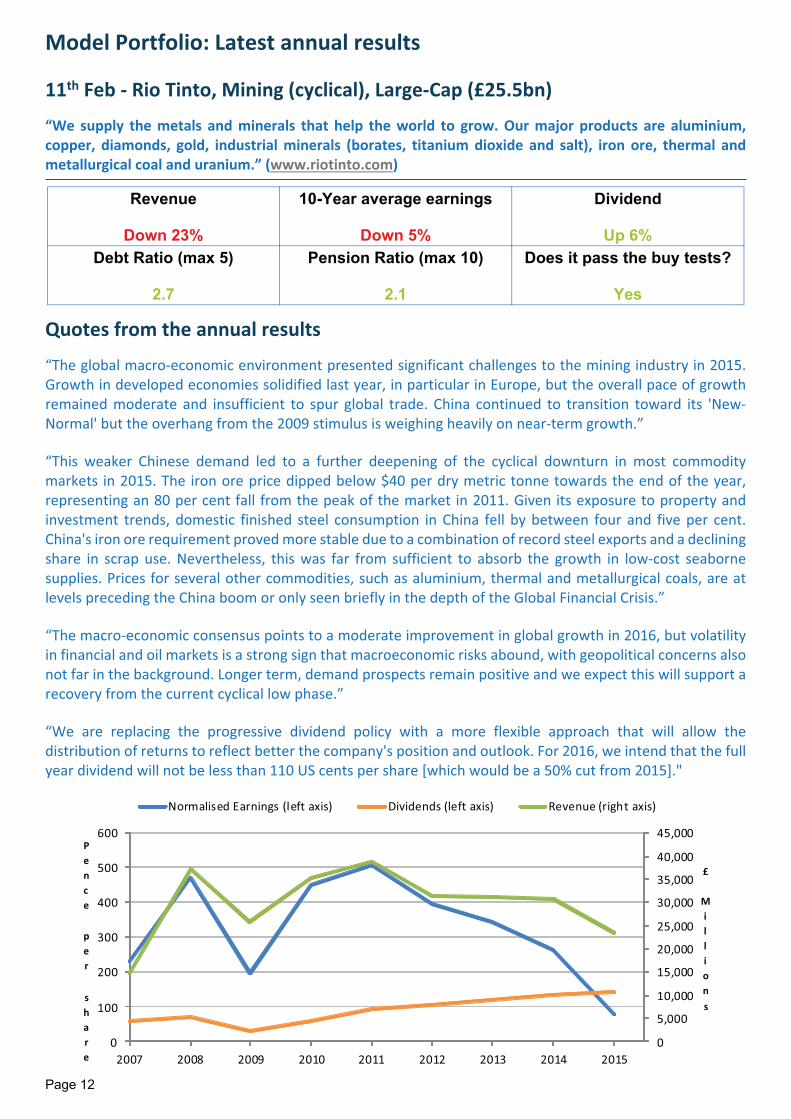

Quotes from the annual results

“The global macro-economic environment presented significant challenges to the mining industry in 2015.

Growth in developed economies solidified last year, in particular in Europe, but the overall pace of growth

remained moderate and insufficient to spur global trade. China continued to transition toward its 'New-

Normal' but the overhang from the 2009 stimulus is weighing heavily on near-term growth.”

“This weaker Chinese demand led to a further deepening of the cyclical downturn in most commodity

markets in 2015. The iron ore price dipped below $40 per dry metric tonne towards the end of the year,

representing an 80 per cent fall from the peak of the market in 2011. Given its exposure to property and

investment trends, domestic finished steel consumption in China fell by between four and five per cent.

China's iron ore requirement proved more stable due to a combination of record steel exports and a declining

share in scrap use. Nevertheless, this was far from sufficient to absorb the growth in low-cost seaborne

supplies. Prices for several other commodities, such as aluminium, thermal and metallurgical coals, are at

levels preceding the China boom or only seen briefly in the depth of the Global Financial Crisis.”

“The macro-economic consensus points to a moderate improvement in global growth in 2016, but volatility

in financial and oil markets is a strong sign that macroeconomic risks abound, with geopolitical concerns also

not far in the background. Longer term, demand prospects remain positive and we expect this will support a

recovery from the current cyclical low phase.”

“We are replacing the progressive dividend policy with a more flexible approach that will allow the

distribution of returns to reflect better the company's position and outlook. For 2016, we intend that the full

year dividend will not be less than 110 US cents per share [which would be a 50% cut from 2015]."

Revenue

Down 23%

10-Year average earnings

Down 5%

Dividend

Up 6%

Debt Ratio (max 5)

2.7

Pension Ratio (max 10)

2.1

Does it pass the buy tests?

Yes

Model Portfolio: Latest annual results

11th Feb - Rio Tinto, Mining (cyclical), Large-Cap (£25.5bn)

“We supply the metals and minerals that help the world to grow. Our major products are aluminium,

copper, diamonds, gold, industrial minerals (borates, titanium dioxide and salt), iron ore, thermal and

metallurgical coal and uranium.” (www.riotinto.com)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

0

100

200

300

400

500

600

2007 2008 2009 2010 2011 2012 2013 2014 2015

£

M

i

l

l

i

o

n

s

P

e

n

c

e

p

e

r

s

h

a

r

e

Normalised Earnings (left axis) Dividends (left axis) Revenue (right axis)

Page 13

Quotes from the annual results

“RB delivered excellent growth and margin expansion in 2015 as a result of our continued focus on our

Health, Hygiene and Home Powerbrand portfolio and supported by our culture of innovation and agility.

Despite a year of mixed market conditions, we achieved broad-based growth (+6% [like-for-like]), across both

developed and developing markets. This was led by an exceptional performance in Consumer Health, due to

both a strong flu season at the beginning of the year and outstanding performances from our innovations on

brands such as Scholl, Durex, Nurofen and Strepsils.

Our virtuous earnings model continued to deliver in 2015 and resulted in significant value creation for

shareholders. Strong gross margin expansion, combined with accelerated indirect cost savings from our

Supercharge programme, created room in our P&L to both increase our brand equity investment (BEI) and to

deliver exceptional operating margin expansion. We continue to expect Supercharge to lead to £150m in cost

savings over three years, but have achieved a significant portion of those savings within the first year.

In 2016, we expect that the macro environment will be tough, but remain confident that our strategic choices

across Powerbrands and Powermarkets will enable RB to deliver another year of growth and margin

expansion. We are targeting [like-for-like] net revenue growth of +4-5%. For operating margin, we reiterate

our medium term target of moderate margin expansion. We expect this to be supplemented in 2016 by part

of the remaining Project Supercharge efficiencies.”

“We intend to continue our current policy of paying an ordinary dividend equivalent to around 50% of

adjusted net income.”

Revenue

Unchanged

10-Year average earnings

Up 8%

Dividend

Unchanged

Debt Ratio (max 4)

1.4

Pension Ratio (max 10)

1.1

Does it pass the buy tests?

Yes

Model Portfolio: Latest annual results

15th Feb - Reckitt Benckiser, Household Goods (cyclical), Large-Cap (£42.1bn)

“RB is the global leader in consumer health and hygiene, with operations in approximately 60 countries and

sales in almost 200. Our purpose is to make a difference by giving people innovative solutions for healthier

lives and happier homes.” (www.rb.com)

0

2,000

4,000

6,000

8,000

10,000

12,000

0

50

100

150

200

250

300

2007 2008 2009 2010 2011 2012 2013 2014 2015

£

M

i

l

l

i

o

n

s

P

e

n

c

e

p

e

r

s

h

a

r

e

Normalised Earnings (left axis) Dividends (left axis) Revenue (right axis)

Page 14

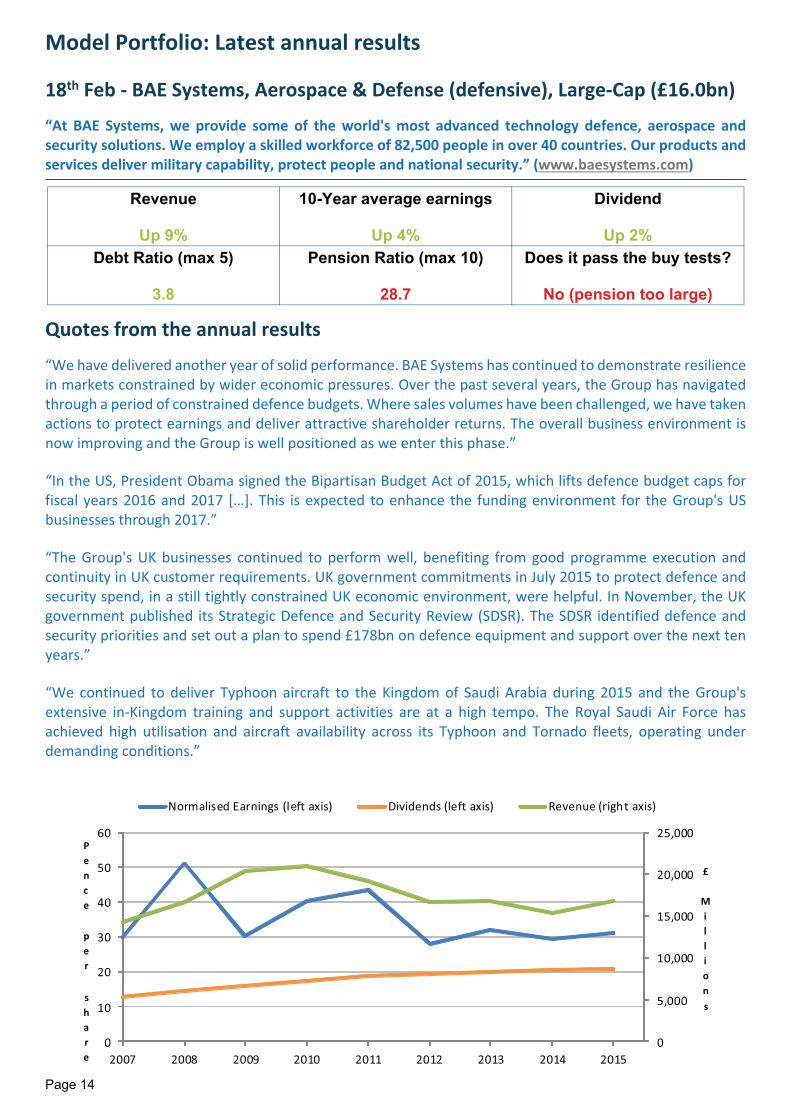

Quotes from the annual results

“We have delivered another year of solid performance. BAE Systems has continued to demonstrate resilience

in markets constrained by wider economic pressures. Over the past several years, the Group has navigated

through a period of constrained defence budgets. Where sales volumes have been challenged, we have taken

actions to protect earnings and deliver attractive shareholder returns. The overall business environment is

now improving and the Group is well positioned as we enter this phase.”

“In the US, President Obama signed the Bipartisan Budget Act of 2015, which lifts defence budget caps for

fiscal years 2016 and 2017 […]. This is expected to enhance the funding environment for the Group's US

businesses through 2017.”

“The Group's UK businesses continued to perform well, benefiting from good programme execution and

continuity in UK customer requirements. UK government commitments in July 2015 to protect defence and

security spend, in a still tightly constrained UK economic environment, were helpful. In November, the UK

government published its Strategic Defence and Security Review (SDSR). The SDSR identified defence and

security priorities and set out a plan to spend £178bn on defence equipment and support over the next ten

years.”

“We continued to deliver Typhoon aircraft to the Kingdom of Saudi Arabia during 2015 and the Group's

extensive in-Kingdom training and support activities are at a high tempo. The Royal Saudi Air Force has

achieved high utilisation and aircraft availability across its Typhoon and Tornado fleets, operating under

demanding conditions.”

Revenue

Up 9%

10-Year average earnings

Up 4%

Dividend

Up 2%

Debt Ratio (max 5)

3.8

Pension Ratio (max 10)

28.7

Does it pass the buy tests?

No (pension too large)

Model Portfolio: Latest annual results

18th Feb - BAE Systems, Aerospace & Defense (defensive), Large-Cap (£16.0bn)

“At BAE Systems, we provide some of the world's most advanced technology defence, aerospace and

security solutions. We employ a skilled workforce of 82,500 people in over 40 countries. Our products and

services deliver military capability, protect people and national security.” (www.baesystems.com)

0

5,000

10,000

15,000

20,000

25,000

0

10

20

30

40

50

60

2007 2008 2009 2010 2011 2012 2013 2014 2015

£

M

i

l

l

i

o

n

s

P

e

n

c

e

p

e

r

s

h

a

r

e

Normalised Earnings (left axis) Dividends (left axis) Revenue (right axis)

Page 15

Quotes from the annual results

“2015 provided a very challenging environment for Centrica. Commodity prices continued to fall during the

year, creating major challenges for our [Exploration & Production] and nuclear power businesses. However,

Centrica delivered a resilient financial performance against this backdrop, with increased adjusted operating

cash flow and a 9% reduction in net debt in the year. In addition, the actions we have taken since the start of

2015 on the dividend, capital expenditure and costs mean the Group is robust in this much lower oil and gas

price environment, and our current projections indicate we can more than balance sources and uses of cash

flow out to 2018 at flat real commodity prices of $35/bbl Brent oil, 35p/therm UK NBP gas and £35/MWh UK

power.“

“In July, we announced the conclusions of our fundamental and wide-ranging strategic review. We concluded

that Centrica’s strength lies in being a customer-facing energy and services business. This is where we have

distinctive positions and capabilities and where we can make the biggest difference and contribution going

forward, for our customers, our employees and our shareholders.”

“We remain confident we can deliver at least 3-5% per annum operating cash flow growth at flat real

commodity prices and are committed to delivering a progressive dividend in line with the sustainable

operating cash flow growth of the Group. I am encouraged with the progress we have made since July, as we

develop our customer-facing platforms for growth and we deliver on our major cost efficiency programme,

which is now underpinned in our business plans. Implementation of the strategy is on track, and I remain

excited about this next phase and continue to believe that Centrica has all the components necessary to

deliver a powerful investor proposition – one of returns and growth.”

Revenue

Down 5%

10-Year average earnings

Down 1%

Dividend

Down 11%

Debt Ratio (max 5)

4.9

Pension Ratio (max 10)

5.0

Does it pass the buy tests?

Yes (but only just)

Model Portfolio: Latest annual results

18th Feb - Centrica, Gas, Water & Multiutilities (defensive), Large-Cap (£10.7bn)

“We are a leading integrated energy company with customers at our core. Our scale is of great benefit to

the markets we are in as we secure the future energy needs of our customers.” (www.centrica.com)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

0

5

10

15

20

25

30

35

40

45

50

2007 2008 2009 2010 2011 2012 2013 2014 2015

£

M

i

l

l

i

o

n

s

P

e

n

c

e

p

e

r

s

h

a

r

e

Normalised Earnings (left axis) Dividends (left axis) Revenue (right axis)

Page 16

Quotes from the annual results

“2015 was a challenging year. While our 2015 financial results were poor, they are set against a backdrop of

continuing geo-political and economic headwinds and volatility across many of our markets as well as the

effects of deliberate management actions. Our share price performance has also been disappointing,

underperforming the wider equity market which has seen broad declines driven largely by the same

macroeconomic concerns. Our strategy, announced in November 2015, will address our performance issues

and reposition our business on a strengthened platform. We have made good progress in a number of areas,

though there is much work still to do during 2016 and beyond. The strategy’s three core priorities are to

secure our foundations, get lean and focused and invest and innovate in our franchise.”

“Given current market conditions and the early stage of implementation of our strategy, we expect the

financial performance of the Group to remain subdued during 2016. We will continue to take the necessary

and sometimes painful actions to reposition the Group for returns and disciplined growth. We will increase

the value of our franchise through the relentless focus on execution that we set out alongside our strategy

announced in November 2015. We will continue to balance support for strong, high-returning clients with

discipline on our tightened risk tolerances. We will continue to take out substantial costs and invest much of

these savings into the future of the Group. We will also retain a strong balance sheet which both protects us

from economic volatility and positions us for future opportunity when conditions allow.”

“The size of any future ordinary dividends will be a function of future earnings and our capital position

relative to regulatory and market expectations. Subject to these factors, the Board intends to declare a

dividend on Ordinary Shares in respect of the 2016 financial year.”

Net asset value

Down 19%

10-Year average earnings

Down 8%

Dividend

Down 82%

5-Yr CET1 Ratio (min 12%)

11.7%

Pension Ratio (max 10)

0.8

Does it pass the buy tests?

No (CET1 ratio too low)

Model Portfolio: Latest annual results

23rd Feb - Standard Chartered, Banks (cyclical), Large-Cap (£13.6bn)

“A leading international banking group committed to building a sustainable business over the long-term.

We operate in some of the world's most dynamic markets and have been for over 150 years. More than 90

per cent of our income and profits are derived from Asia, Africa and the Middle East.” (www.sc.com)

0

200

400

600

800

1,000

1,200

1,400

0

20

40

60

80

100

120

140

2007 2008 2009 2010 2011 2012 2013 2014 2015

P

e

n

c

e

p

e

r

s

h

a

r

e

P

e

n

c

e

p

e

r

s

h

a

r

e

Normalised Earnings (left axis) Dividends (left axis) Book Value (right axis)

Page 17

Quotes from the annual results

“Petrofac's core proposition is based on strong project execution, clear geographic focus, a disciplined

approach to bidding and a sustainable, cost-effective structure. These strengths have positioned Petrofac

well in a very challenging period for the oil and gas industry. Our results for 2015 were adversely affected by

the Laggan-Tormore project on Shetland. However, we faced up to the exceptional challenges we

encountered and honoured our commitment to our client. With the plant now successfully operational, these

issues are finally behind us.”

"We enter 2016 with a renewed focus on our core strengths. The Group's backlog stands at record year end

levels, giving us excellent revenue visibility for 2016 and beyond. We remain committed to reducing the

capital-intensity of the business and managing the [Integrated Energy Services] portfolio to maximise value.

Our balance sheet remains robust, our working capital position has improved and we remain dedicated to

delivering shareholder value.”

“We enter 2016 with a very cost-effective and sustainable structure. We are targeting further annualised

efficiency savings of up to US$90 million by the end of 2016, which will help us to protect margins and

maintain our strong competitive position, including US$25 million from de-layering and centralising back

office services as part of our recently implemented Group reorganisation.“

“We see continuing investment from our clients in our core onshore markets of the Middle East and North

Africa, in both key upstream and downstream projects. Our overall portfolio is in good shape, with embedded

margins consistent with guidance.”

Revenue

Up 15%

10-Year average earnings

Down 2%

Dividend

Up 3%(unchanged in USD)

Debt Ratio (max 4)

7.1

Pension Ratio (max 10)

0.0

Does it pass the buy tests?

No (debt ratio too high)

Model Portfolio: Latest annual results

24th Feb - Petrofac, Oil Equipment & Services (cyclical), Mid-Cap (£2.5bn)

“We design, build, operate and maintain oil and gas facilities, delivered through a range of innovative

commercial models, enabling us to respond to the distinct needs of each client and helping them to

transform the value of their assets across the oil and gas life cycle. ” (www.petrofac.com)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

0

20

40

60

80

100

120

140

2007 2008 2009 2010 2011 2012 2013 2014 2015

£

M

i

l

l

i

o

n

s

P

e

n

c

e

p

e

r

s

h

a

r

e

Normalised Earnings (left axis) Dividends (left axis) Revenue (right axis)

Page 18

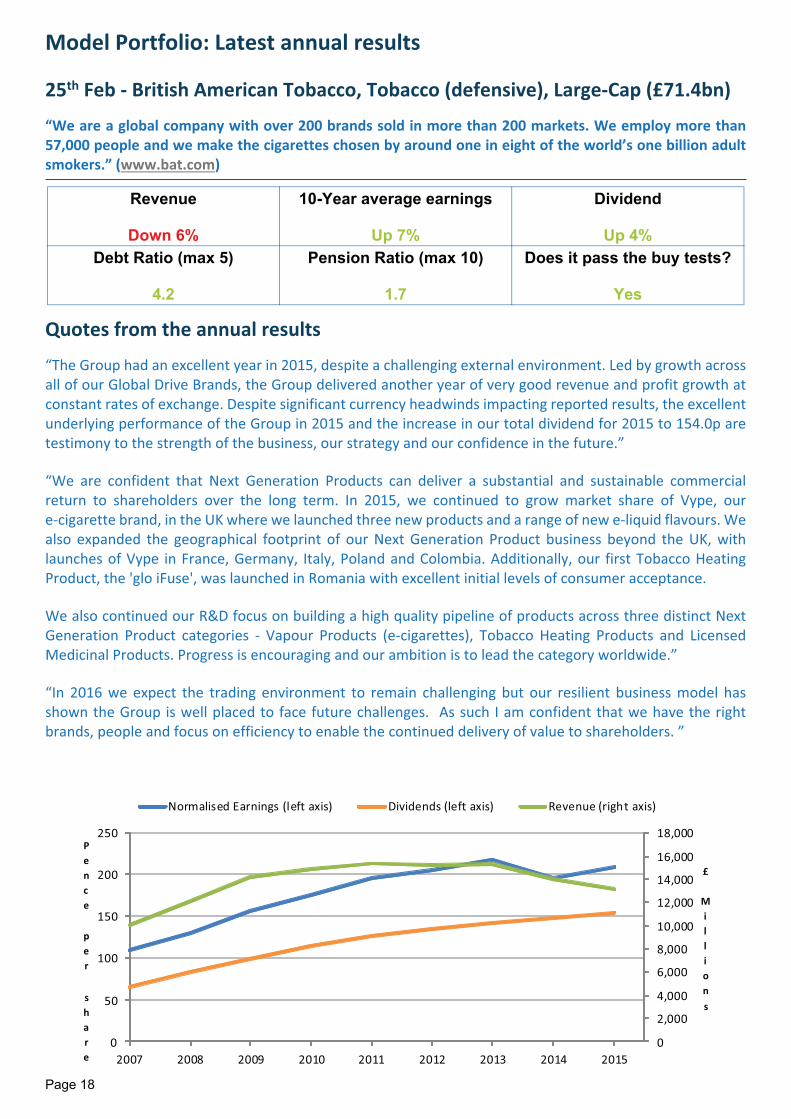

Quotes from the annual results

“The Group had an excellent year in 2015, despite a challenging external environment. Led by growth across

all of our Global Drive Brands, the Group delivered another year of very good revenue and profit growth at

constant rates of exchange. Despite significant currency headwinds impacting reported results, the excellent

underlying performance of the Group in 2015 and the increase in our total dividend for 2015 to 154.0p are

testimony to the strength of the business, our strategy and our confidence in the future.”

“We are confident that Next Generation Products can deliver a substantial and sustainable commercial

return to shareholders over the long term. In 2015, we continued to grow market share of Vype, our

e-cigarette brand, in the UK where we launched three new products and a range of new e-liquid flavours. We

also expanded the geographical footprint of our Next Generation Product business beyond the UK, with

launches of Vype in France, Germany, Italy, Poland and Colombia. Additionally, our first Tobacco Heating

Product, the 'glo iFuse', was launched in Romania with excellent initial levels of consumer acceptance.

We also continued our R&D focus on building a high quality pipeline of products across three distinct Next

Generation Product categories - Vapour Products (e-cigarettes), Tobacco Heating Products and Licensed

Medicinal Products. Progress is encouraging and our ambition is to lead the category worldwide.”

“In 2016 we expect the trading environment to remain challenging but our resilient business model has

shown the Group is well placed to face future challenges. As such I am confident that we have the right

brands, people and focus on efficiency to enable the continued delivery of value to shareholders. ”

Revenue

Down 6%

10-Year average earnings

Up 7%

Dividend

Up 4%

Debt Ratio (max 5)

4.2

Pension Ratio (max 10)

1.7

Does it pass the buy tests?

Yes

Model Portfolio: Latest annual results

25th Feb - British American Tobacco, Tobacco (defensive), Large-Cap (£71.4bn)

“We are a global company with over 200 brands sold in more than 200 markets. We employ more than

57,000 people and we make the cigarettes chosen by around one in eight of the world’s one billion adult

smokers.” (www.bat.com)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

0

50

100

150

200

250

2007 2008 2009 2010 2011 2012 2013 2014 2015

£

M

i

l

l

i

o

n

s

P

e

n

c

e

p

e

r

s

h

a

r

e

Normalised Earnings (left axis) Dividends (left axis) Revenue (right axis)

Page 19

“Hill & Smith Holdings PLC is an international group of companies with leading positions in the design,

manufacture and supply of infrastructure products and the provision of galvanizing services.”

(www.hsholdings.co.uk)

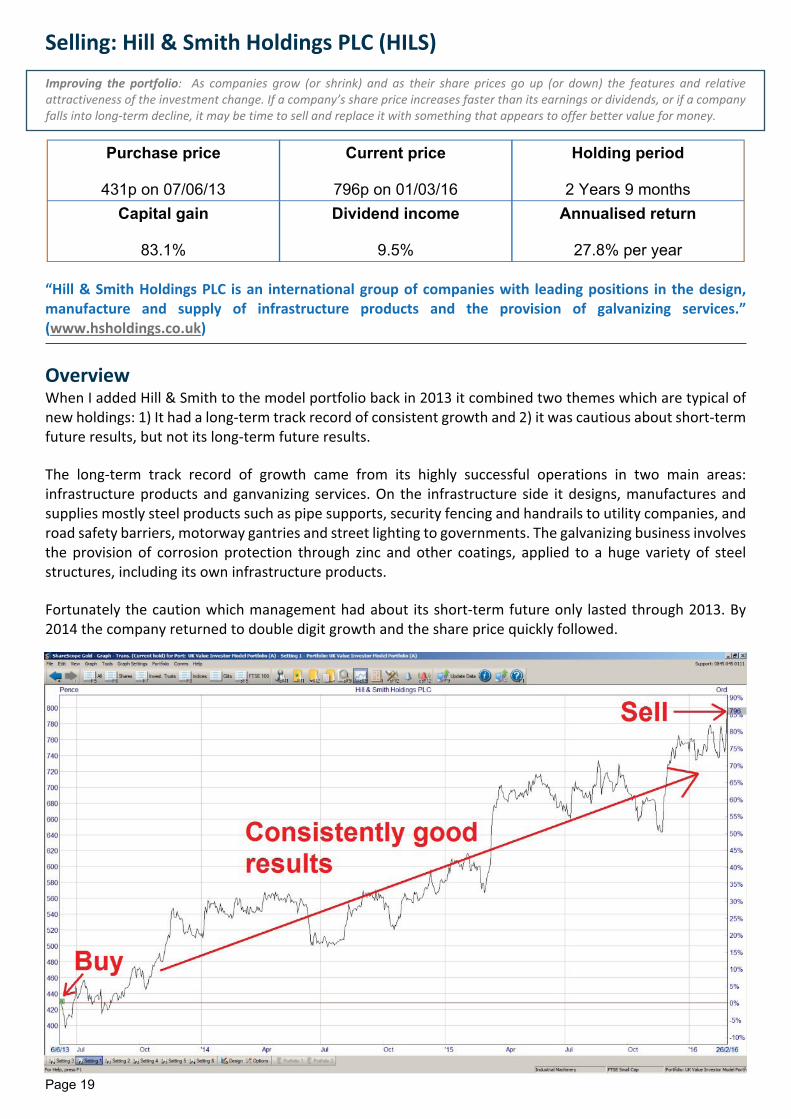

OverviewWhen I added Hill & Smith to the model portfolio back in 2013 it combined two themes which are typical of

new holdings: 1) It had a long-term track record of consistent growth and 2) it was cautious about short-term

future results, but not its long-term future results.

The long-term track record of growth came from its highly successful operations in two main areas:

infrastructure products and ganvanizing services. On the infrastructure side it designs, manufactures and

supplies mostly steel products such as pipe supports, security fencing and handrails to utility companies, and

road safety barriers, motorway gantries and street lighting to governments. The galvanizing business involves

the provision of corrosion protection through zinc and other coatings, applied to a huge variety of steel

structures, including its own infrastructure products.

Fortunately the caution which management had about its short-term future only lasted through 2013. By

2014 the company returned to double digit growth and the share price quickly followed.

Purchase price

431p on 07/06/13

Current price

796p on 01/03/16

Holding period

2 Years 9 months

Capital gain

83.1%

Dividend income

9.5%

Annualised return

27.8% per year

Selling: Hill & Smith Holdings PLC (HILS)

Improving the portfolio: As companies grow (or shrink) and as their share prices go up (or down) the features and relative

attractiveness of the investment change. If a company’s share price increases faster than its earnings or dividends, or if a company

falls into long-term decline, it may be time to sell and replace it with something that appears to offer better value for money.

Page 20

The company’s financial track record is exceptional. No, it isn’t the next Google or Microsoft, but it has grown

far faster than the average company and with much greater consistency. You would be hard pressed to even

spot the global financial crisis in the chart above, although of course that does have something to do with the

relatively defensive markets which it operates in, i.e. infrastructure for utilities and roads.

The table below shows Hill & Smith’s results compared to the FTSE 100 at the time of purchase.

The green highlighting shows that Hill & Smith had an above market-average growth rate and growth quality,

while post-tax profitability was only slightly below average (although the FTSE 100’s profitability of 10% is

only an estimate, and is deliberately likely to be on the high side).

On the valuation side, the company’s PE ratio and dividend yield were better than average, while its

longer-term PE10 and PD10 ratios (price to 10-year average earnings and dividends) were slightly worse than

the market average, although that is to be expected from a company with an above average growth rate.

However, relatively to other companies with consistent histories of double digit growth rates, Hill & Smith’s

valuation ratios and dividend yield were unusually attractive. The opportunity to buy a company with a long

history of double digit growth combined with a market-beating dividend yield seemed compelling, and so

after working through the usual company analysis process I added it to the model portfolio in June 2013 at

431 pence per share.

Buying an exceptional success story at a time of cautionHill & Smith Holdings is unusual in that it is a true “holding” company. The plc is made up of around 30

subsidiaries which are managed as individual companies, but which also have access to information, services

or products from other companies within the group.

To a large extent the role of the directors is to acquire fundamentally sound companies which are trading at

attractive prices, often because of operational issues which Hill & Smith can then hopefully sort out. This

sounds a lot like value investing, and it has produced results that any value investor would be proud of.

June 2013 Growth Quality Profitability PE Yield PE10 PD10

Hill & Smith 11.3% 88.0% 9.7% 12.3 3.5% 15.5 43.5

FTSE 100

(at 6,583)4.0% 74.0% 10.0% 12.9 3.4% 14.5 35.1

0

50

100

150

200

250

300

350

400

450

500

0

5

10

15

20

25

30

35

40

45

2004 2005 2006 2007 2008 2009 2010 2011 2012

£

M

i

l

l

i

o

n

s

P

e

n

c

e

p

e

r

s

h

a

r

e

Hill & Smith Holdings Results to 2012

Normalised Earnings (left axis) Dividends (left axis) Revenue (right axis)

Page 21

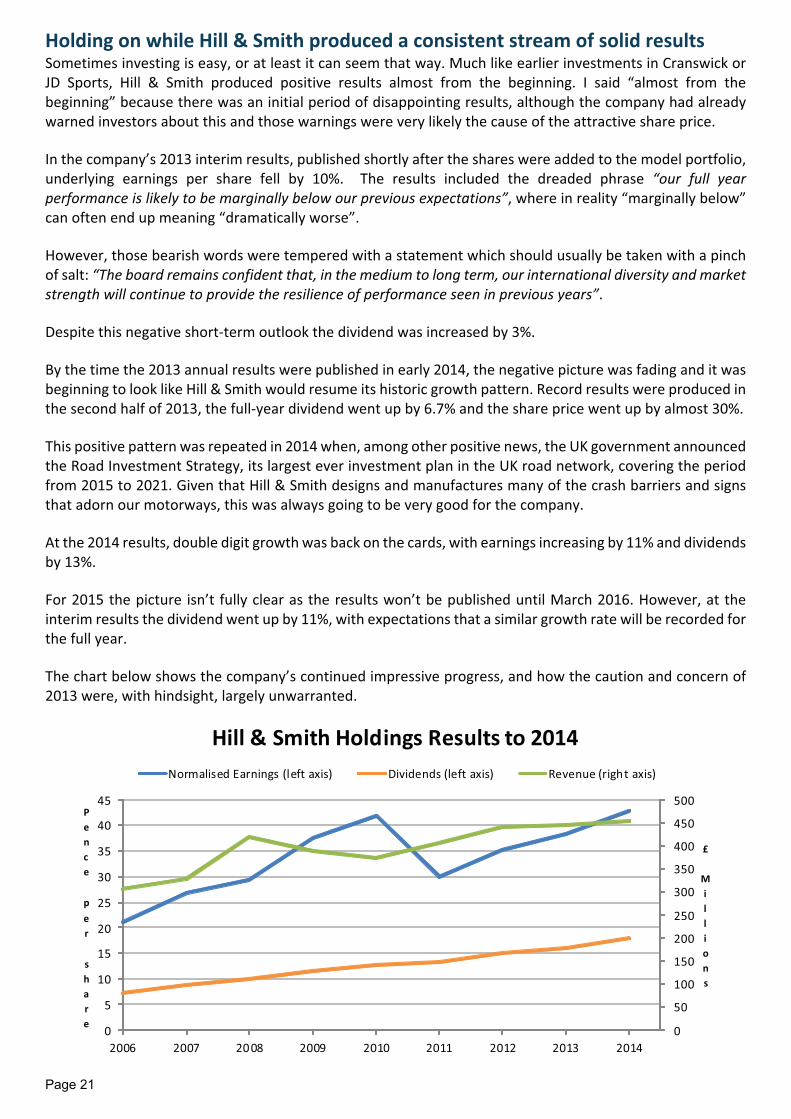

Holding on while Hill & Smith produced a consistent stream of solid resultsSometimes investing is easy, or at least it can seem that way. Much like earlier investments in Cranswick or

JD Sports, Hill & Smith produced positive results almost from the beginning. I said “almost from the

beginning” because there was an initial period of disappointing results, although the company had already

warned investors about this and those warnings were very likely the cause of the attractive share price.

In the company’s 2013 interim results, published shortly after the shares were added to the model portfolio,

underlying earnings per share fell by 10%. The results included the dreaded phrase “our full year

performance is likely to be marginally below our previous expectations”, where in reality “marginally below”

can often end up meaning “dramatically worse”.

However, those bearish words were tempered with a statement which should usually be taken with a pinch

of salt: “The board remains confident that, in the medium to long term, our international diversity and market

strength will continue to provide the resilience of performance seen in previous years”.

Despite this negative short-term outlook the dividend was increased by 3%.

By the time the 2013 annual results were published in early 2014, the negative picture was fading and it was

beginning to look like Hill & Smith would resume its historic growth pattern. Record results were produced in

the second half of 2013, the full-year dividend went up by 6.7% and the share price went up by almost 30%.

This positive pattern was repeated in 2014 when, among other positive news, the UK government announced

the Road Investment Strategy, its largest ever investment plan in the UK road network, covering the period

from 2015 to 2021. Given that Hill & Smith designs and manufactures many of the crash barriers and signs

that adorn our motorways, this was always going to be very good for the company.

At the 2014 results, double digit growth was back on the cards, with earnings increasing by 11% and dividends

by 13%.

For 2015 the picture isn’t fully clear as the results won’t be published until March 2016. However, at the

interim results the dividend went up by 11%, with expectations that a similar growth rate will be recorded for

the full year.

The chart below shows the company’s continued impressive progress, and how the caution and concern of

2013 were, with hindsight, largely unwarranted.

0

50

100

150

200

250

300

350

400

450

500

0

5

10

15

20

25

30

35

40

45

2006 2007 2008 2009 2010 2011 2012 2013 2014

£

M

i

l

l

i

o

n

s

P

e

n

c

e

p

e

r

s

h

a

r

e

Hill & Smith Holdings Results to 2014

Normalised Earnings (left axis) Dividends (left axis) Revenue (right axis)

Page 22

Selling after significant share price gains make the investment less compellingAs usual, once good news begins to flow consistently over a period of time, the market reacts. In this case the

market’s reaction was to re-rate Hill & Smith’s shares from a dividend yield of 3.5%, which was slightly above

the market average, to a yield today of 2.3%, which is a long way below the FTSE 100’s yield of 4.2%.

Of course, Hill & Smith has a very good chance of growing its dividend far faster than the market average, and

so today’s yield of 2.3% is perhaps entirely reasonable. But a stock which is trading at a reasonable price is

unlikely to make a good value investment. The market expects Hill & Smith’s future results to be excellent,

and so those results are already effectively baked into the valuation pie.

This has become especially noticeable recently as the FTSE 100 and other global indices have entered bear

market territory. As markets and individual stocks have been falling left, right and centre, Hill & Smith’s share

price has continued to grow. It is up more than 5% in 2016 and up almost more than 30% from the start of

2015.

This is good for Hill & Smith’s shareholders, but at some point the rising price and falling dividend yield mean

that most of the gains lie in the past, while ahead lies the risk that the shares will be re-rated downwards

again if the company hits even the slightest bump in the road.

In order to lock in the existing capital gains and avoid future downside risk I will be selling the entire Hill &

Smith investment in the next few days from both the model portfolio and my personal portfolio.

The proceeds will be reinvested into a new holding next month, and of course I hope that the next investment

can perform even remotely as well as this one.

Lower ranked stocks that were not sold Reason for not selling

BAE Systems, Chemring

The model portfolio currently holds 16 cyclical

sector stocks when my rule of thumb is to have 15

at most. Both of BAE and Chemring are in the

Aerospace & Defense sector, which is defined as

defensive, while Hill & Smith is in the cyclical

Industrial Engineering sector. Rather than selling a

defensive holding I wanted to remove one of the

cyclical holdings instead, otherwise the risk is that

next month the portfolio will end up with another

new cyclical stock, taking the total to 17 and

further above my preferred maximum of 15.

However, I still intend to sell Chemring (a major

underperformer) sooner rather than later.

IMPORTANT NOTICE: This analysis is to be used as information only and should not be thought of as investment advice.It is an example of one approach to making investment decisions. It should be used alongside other sources of informationrather than used in isolation. You should always perform your own analysis and factual verification before making investmentdecisions. If you need advice you should seek a regulated financial advisor. See the important notes on the last page.

Page 23

Readers’ Q & A

Interesting and/or helpful questions from readers

Q: Is it really reasonable to only look at the pension scheme liabilities when calculating the pension ratio,

without also looking at the value of assets that might balance out or negate those liabilities? Or do you

ignore these because the value of the assets in the pension scheme can vary a lot (e.g. as stock markets rise

and fall)?

A: I think that looking at the liabilities alone is a more sensible approach than looking at the pension surplus or deficit

(i.e. whether or not the pension assets exceed the pension liabilities).

As you point out, pension assets can change in value as the underlying investments change in value. Not only that,

pension liabilities can also change in value (typically upwards) when actuaries reappraise the expected remaining

lifetime of retirees. Given that both liabilities and assets are subject to change, the deficit or surplus can change

dramatically in a relatively short period of time. So for example a company with a £100m pension liability and pension

assets worth £101m has a £1m surplus. But if the liabilities increased to £110m while the assets fell to £90m it would

find itself with a £20m deficit, and possibly in a relatively short period of time. Whether or not a £20m deficit was a

problem would depend on how much profit the company typically made. If the company made £20m profit a year then

it might be a bit of a problem, but if the company only made £2m a year then fixing a £20m pension hole would be an

enormous problem which could require a rights issue to fix.

So pension scheme risk is closely related to the size of the pension deficit we could reasonably expect the scheme to

have at some point in the future, and that is determined primarily by the size of the pension liabilities.

Defensive Sectors! Aerospace & Defense

! Beverages

! Electricity

! Fixed Line Telecommunications

! Food & Drug Retailers

! Food Producers

! Gas, Water & Multiutilities

! Health Care Equipment & Services

! Mobile Telecommunications

! Non-life Insurance

! Personal Goods

! Pharmaceuticals & Biotechnology

! Tobacco

Cyclical Sectors! Automobiles & Parts

! Banks

! Chemicals

! Construction & Materials

! Electronic & Electrical Equipment

! Financial Services

! Forestry & Paper

! General Industrials

! General Retailers

! Household Goods & Home Construction

! Industrial Engineering

! Industrial Metals & Mining

! Industrial Transportation

! Leisure Goods

! Life Insurance

! Media

! Mining

! Oil & Gas Producers

! Oil Equipment, Services & Distribution

! Real Estate Investment & Services

! Software & Computer Services

! Support Services

! Technology Hardware & Equipment

Defensive and Cyclical sectors

The Model Portfolio aims to be at least 50% invested in defensive FTSE Sectors as defined in the Capita

Dividend Monitor. The definitions are repeated here:

��������������������� �������������������� ������������ ����� ������������������������ �

��� ���� ���� ���� ������������

�������������

��������

���������

��� ���

����

��� ���

!"���� ��������#$

�����

�����

����%&�

�� ���

� '����(�&����)��������*� '+() (,���-.� /����0"�1���2��������&�3���&����"��� 45$6� .$7 �-$�8 6$9 �.$�8 :58 �-8 6$� 4-�6

- '����������"1��*� '�+ (,������ ����#���&"���� 4�7$;6 �7$� .$68 -5$9 �5$58 9-8 .;8 �$� 4-;9

5 �����#���*�� �(� (,���-.� /����0"�1���2��������&�3���&����"��� 4:$:� 5�;$5 .$�8 �5$- �-$58 798 -98 7$� 4-65

; '�������'&&���+��%������*� '�� (,������ (��������������& 4-$;- ��$- :$�8 �.$� -�$-8 7.8 �58 �$� 4-7;

. ��������*� �/� (,���-.� ��"&�������%�����% 4�$6� �5$6 5$�8 -�$� �;$58 ���8 5�8 �$- 4::

6 '%%������*� '�< (,���-.� �"11�����������& 4:$:: ��$� 5$�8 �5$- �7$78 ::8 �68 -$- 4-5:

7 '&���������"1��*� '�=+ (,���-.� (��������������& 4-$-9 ��$: 7$58 ��$7 6$-8 7�8 5.8 �$� 4�7�

: ���&�����*� ��� ��������1 *�#���&"���� 45$-5 �;$6 .$78 �5$7 7$�8 :58 �.8 �>< 4-9

9 ,�������1�"&��*� ,�� (,���-.� (�����*���,�������"������& 4:$.� -�$� ;$78 5�$5 �7$;8 ::8 568 -$6 4-6

�� �,�����"1��*� �,� ��������1 +���� 4�$55 ��$7 .$68 ��$� 6$58 7�8 -78 -$� 45;

�� �� ������*� �'� (,���-.� �"11�����������& 47$;5 �-$9 .$-8 �:$: :$�8 ::8 5;8 �$� 45�

�- ?=��?��������*� ?*, (,������ +��% 47$�6 6$� ��$.8 ;$. 6$�8 658 �78 -$� 4927::

�5 @��������*� @�, (,���-.� ��������& 4�.$6� �.$9 5$�8 --$. �;$:8 9-8 --8 �$� 476

�; ���%����������"1��*� ��� (,���-.� ,������3�*��&"�� 4-$7� ��$7 5$98 �-$9 :$�8 9-8 �;8 .$; 4�;.

�. A���� ���*�� A�� ��������1 ����������3�������������0"�1��� 4�.$6. �.$- ;$-8 -�$. �;$68 798 --8 �$� 4�:

�6 ������"1�=����%&��*� ��� (,���-.� (��������������& 47$7; -�$. 5$68 -.$; �5$.8 ::8 -68 �$� 4�:

�7 +��������"1��*� +,/ (,���-.� �"11�����������& 4-$:� �-$6 ;$-8 �.$� :$98 9-8 �-8 5$6 47:

�: B<�+�������"1��*� B<+ ��������1 ��"&������,��&1������� 4-$:6 9$5 7$68 �-$. .$;8 678 �:8 �$7 4�;

�9 @��������&�"���&��*� @�� (,���-.� +��% 4-$.5 �$- �.$98 �$� �.$98 678 58 �5$� 4:65

-� +����&��C)�D��"1��������&��*� +�) (,���-.� (����3���"%���������& 4�$:: �5$� 7$58 9$7 9$;8 798 78 ;$. 4..9

-� ���� ���*� ��)� ��������1 ��"&�������%�����% 4�;$:- 6$9 -$98 ��$7 ��$;8 7�8 �:8 �$; 4�-

-- �� ��*� �<� (,������ +���� 4��$5; --$7 5$-8 -.$. ��$�8 9-8 -�8 7$7 4�2�-6

-5 ��������������&����(������*� ��( (,���-.� (��������������& 4-$.- :$- ;$98 7$. ��$58 7.8 98 5$: 4�-.

-; )�������"1��*� )��� (,���-.� ��"&�������%�����% 49$55 -5$- 5$-8 9$9 �-$;8 7�8 ��8 5$. 45��

-. E������*�� ��,���1&�����"1��*� E*, (,���-.� ����#���&"���� 47$9: �5$7 5$68 �9$5 :$.8 798 5-8 �>< 4��;

-6 ?"����� ����"1��*� ?�?� (,������ ���&��������& 4�-$69 �6$6 -$:8 -;$- �6$.8 :58 -68 �$- 45�;

-7 '��#�%�&����*� '�,/ (,������ +��% 4;$:; ��$6 -$:8 7$5 �;$68 .:8 �58 -$- 469;

-: �����%����*� ��' ��������1 ����������3�������������0"�1��� 4;$5� ��$: 5$.8 �9$- �7$�8 :58 �-8 �$7 4��

-9 '&��� �C*�"��D�=����%&��*� '*� ��������1 ���������������& 4�$-. ��$5 :$�8 �.$5 7$78 .:8 -�8 �$� 4�6

5� �+���*� �+� (,���-.� ��"&�������%�����% 4:$7- �-$- ;$58 �.$5 6$�8 :58 �78 �$- 4-��

5� ���*���"���*� �*'� ��������1 �"11�����������& 4;$-5 9$5 .$98 :$5 �$78 .�8 ;68 -$9 4;:

5- ��&��"�������"1�C,��D��*� �,� (,���-.� ,������3�*��&"�� 4.$;� �:$� -$:8 -.$. ��$�8 ���8 �98 �$9 4.�

55 ��� ��#�*�������&��������"1��*� �*�� ��������1 (��������������& 4-$:6 ��$� :$;8 ��$. .$�8 ;68 ;68 �$� 47

5; (�����*� (��� ��������1 ��"&�������%�����% 4�$-; 9$: 9$78 6$- :$;8 678 :8 .$� 4;7

5. ��"��������*� ��B (,������ *�#���&"���� 4�-$;6 �5$9 5$�8 -�$6 ��$.8 :58 �:8 �>< 4�2:�7

56 ?��������*� ?�'+ ��������1 �"11�����������& 4�$:: ��$� .$78 ��$. 9$.8 798 :8 ;$; 4--

57 �"�������"1��*� ��*+ (,���-.� ���������������& 49$95 -�$9 -$-8 5-$9 �:$�8 ���8 5.8 �$� 4:�

5: ��1������*� ��*+ (,���-.� �"11�����������& 47$�. �:$� -$68 5�$5 �6$;8 9-8 �78 �$6 456

59 ��������*� �/? (,���-.� '���&1����3���#�&� 4-$.9 -:$- ;$�8 �7$. 9$78 798 �58 7$7 4�::

;� ���&�� ��*� ��) (,���-.� ����������3�������������0"�1��� 4�7$;. ��$; -$78 -;$: �:$-8 798 �78 �$� 47.

;� =�&������������*� =�� ��������1 *�#���&"���� 4�$�6 9$5 :$58 9$� 6$-8 .:8 5-8 �>< 4�5

;- ���������*� ��' (,������ ��&2�)�����3�+"���"�������& 4-$�� �-$5 .$78 :$; ;$;8 7�8 98 .$5 4�25-.

;5 +�F��&�CE��D��*� +�G� ��������1 �"11�����������& 4;$6� �5$. 5$.8 ��$5 ;$.8 7�8 �58 ;$6 45-

;; @���#������"1��*� @/� (,������ +������,�������"������& 4-$�9 9$9 .$�8 �-$� 5$98 9-8 78 -$� 492979

;. �����H&���FF��B<�3���*��*� �/+ (,���-.� ,������3�*��&"�� 4��$;- ;�$; �$78 65$� �9$;8 ���8 598 �$6 45.

;6 *�%���3�����������"1��*� *��� (,������ *�#���&"���� 4-$-6 �-$. .$�8 �:$9 ��$�8 678 �78 �>< 4:9;

;7 �����*� ��� (,������ ���������� 4�5$:9 �5$� 6$;8 �;$6 .$58 :58 :8 .$- 4�2�79

;: ?�� �C�D����"1��*� ?)�� (,���-.� ���������������& 45$5- �5$� ;$58 �5$6 6$-8 7.8 ��8 5$: 476

;9 �������*� ��� (,���-.� '���&1����3���#�&� 4-$�. ��$9 -$68 �7$6 �5$-8 :58 �-8 �$: 467

.� '��������"1��*� '@@ (,���-.� ��#� ����3����1"�����������& 4�.$�. --$6 -$�8 -.$� �5$98 :58 -�8 �$� 4;;

.� ?��F�� ��*� ?�G (,���-.� ����#���&"���� 45$.9 ��$5 -$:8 �.$� .$58 798 �78 �$5 4�5�

.- '���&�C)��D��*� ',< (,���-.� �"11�����������& 4�-$:9 �5$5 -$:8 �.$9 .$-8 798 �98 �$5 4:7

.5 +���&����"1��*� +�� ��������1 �"11�����������& 4;$�5 �6$. -$.8 -�$5 �-$-8 9-8 ��8 -$9 4-�

.; ?����&��'�������,��������*� ?',� (,������ ,������ 459$�. -;$. 5$98 --$: 6$58 798 �78 5$� 4529-.

.. =��#���&����"1��*� =(� (,���-.� ���������������& 45$99 �-$� ;$�8 �-$� �$.8 7�8 �.8 �$5 467

.6 =���&������*� =�@ (,���-.� �"11�����������& 4;$�. -5$� 5$�8 �9$5 6$58 798 �:8 �$9 475

.7 ���1"���������*� ��� (,���-.� ��#� ����3����1"�����������& 4:$-. �7$6 -$58 -5$9 ��$;8 9-8 �58 �$- 46�

.: �"����� ��&���"���������&�����*� ��+ (,���-.� +���� 49$�� 9$7 -$68 �:$6 :$58 7.8 �78 �$� 476

.9 �1�����������%�����%��*� ��A (,���-.� ��"&�������%�����% 45�$�: --$; -$-8 -:$9 ��$�8 968 �78 �$9 496

6� ���&�"� �CED��*� �?�� (,������ (����3���"%���������& 4-$.5 ��$� .$-8 ��$. 6$;8 7.8 .8 .$- 4.55

6� ������*� �A, (,������ ���������������& 467$7� �6$; -$-8 -7$7 ��$98 :58 ;-8 �$7 4.��

6- ���� ��� ���?��#�����*� ��? (,���-.� ,������3�*��&"�� 4��7$7� ;6$5 �$;8 69$9 �:$-8 9-8 5:8 �$� 497

65 ��������(�������*� �(* ��������1 �"11�����������& 4�$�; :$� 9$�8 :$� -$68 ;-8 �58 .$5 4.7

6; ?����C'��D��*� ?'� (,���-.� ?�����%�& 4.$�; �:$� -$;8 -:$- 9$-8 968 �68 �$6 4-7

6. �������"1��*� ��� ��������1 �"11�����������& 4�$7; ��$6 ;$98 �-$� 7$-8 :58 :8 5$� 45�

66 ����,�����*� ��/ (,������ +��% 4�:$6� -5$7 7$78 .$7 ;$:8 .;8 ��8 -$5 472��;

67 ����������<�����*� ��< (,������ ��������"�����&�3�?���������% 4�;$�� �:$6 .$78 �.$: �$;8 7�8 �:8 ;$; 4;2-9:

6: ���%����*� ��� (,������ ?�����%�& 4�:$6. �9$- 5$�8 -5$; 7$58 ::8 �58 ;$5 4-25:�

69 ������������������*� ���' (,���-.� ��������& 4-9$:5 --$9 -$58 5�$6 �.$;8 :58 �78 �$5 4�7�

7� +�����(��"&�������������*� +��/ (,���-.� ��#� ����3����1"�����������& 4�;$6- -�$- -$�8 59$- -�$98 798 ;;8 �-$: 4:5

7� =�&����*�� =�A (,���-.� ����#���&"���� 4��$6� �.$; -$58 -�$; 9$58 798 �.8 �>< 4�67

7- ����������*� �**� (,���-.� �"11�����������& 4-$7� ��$6 6$.8 9$5 .$�8 7�8 78 ;$. 4�;.

75 �1�����&��*� �A� (,���-.� ����������3�������������0"�1��� 4�7$:: �:$- -$:8 -�$; ��$�8 798 �-8 �$- 4�-:

7; *�������&��*� *'� (,���-.� ,������3�*��&"�� 4�$55 -66$� -$58 6$� 7$:8 ;-8 -�8 5$. 4�5:

7. (�&����CE���&D�3���&��*� (�E ��������1 ��"&������,��&1������� 49$75 ��$- -$58 -�$6 �5$�8 ���8 :8 -$7 45�

76 ,�&����*� ,��/ (,������ (����3���"%���������& 4�$:; �6$5 �$68 6$9 -$�8 678 :8 .$; 4-255;

77 ?���������������������"1��*� ?'? (,������ �"11�����������& 49$-5 �:$� -$68 -.$5 �5$68 ::8 ��8 :$; 4�:7

7: �����������"1��*� �,�< (,������ �"11�����������& 4-9$-. -5$5 �$78 55$. �6$:8 9-8 �;8 ;$� 4�:-

79 ,"�������������*� ,*�� (,���-.� (��������������& 45$;7 9$� ;$98 :$- -$78 .;8 �;8 -$; 49-

:� ?����������11�%��������&��*� ?+� ��������1 ��"&������,��&1������� 4;$-- �7$9 6$-8 ��$7 �$58 .:8 �.8 �$- 4:

:� ?��������*� ?@�� (,���-.� ?�����%�& 46$9. �.$5 5$58 -�$5 :$;8 798 �-8 6$5 49�

��������������������� �������������������� ������������ ����� ������������������������ �

��� ���� ���� ���� ������������

�������������

��������

���������

��� ���

����

��� ���

!"���� ��������#$

�����

�����

����%&�

�� ���