Embed Size (px)

Citation preview

Fortis UK

FORTIS I 9/25/2009 I page 2

Agenda

1. Profile and track record(Introduction – overview of main topics)

2. The market and the competition

3. Strategic initiatives

4. Conclusion

FORTIS I I page 3

Profile – Fortis UK

Key financial data (Non-Life) Mission/strategy

Market Position/ Key competences Business mix

FY 08 H1 09GBP mio

Gross inflow

Operating costs

Net profit

Underwriting Combined ratio¹

759.6

146.3

51.7

100.7%

401.6

68.1

21.7

103.6%

To be the natural choice for insurance, in whatever way the consumer decides to purchase their insuranceDelivering on its promises through its dynamic and responsive team dedicated to customer satisfaction

This vision has to be achieved through the continued pursuit of the existing 3-axes for growth strategy:1. Manufacturing a wider range of products2. Distribution through owned and 3rd party routes to market3. Leveraging the combined capability of Fortis UK to

deliver cost effective solutions

Strong foothold in Personal Lines marketn⁰ 8 Personal Lines insurern⁰ 3 in private car insurance (# cars insured)n⁰ 4 in travel insurancen⁰ 5 Personal Lines intermediary (via RIAS)

A number of core strengths including Customer focused credentialsHigh levels of efficiency, with low unit costs of productionMulti-channel capabilities (to client and consumer)

(10%) Commercial Lines

(90%) Personal Lines

(25%) Affinities

(18%)Owned

(57%) Brokers

Product Mix (GWP) Distribution Mix (GWP)

¹ Excludes investment income

9/25/2009

FORTIS I I page 4

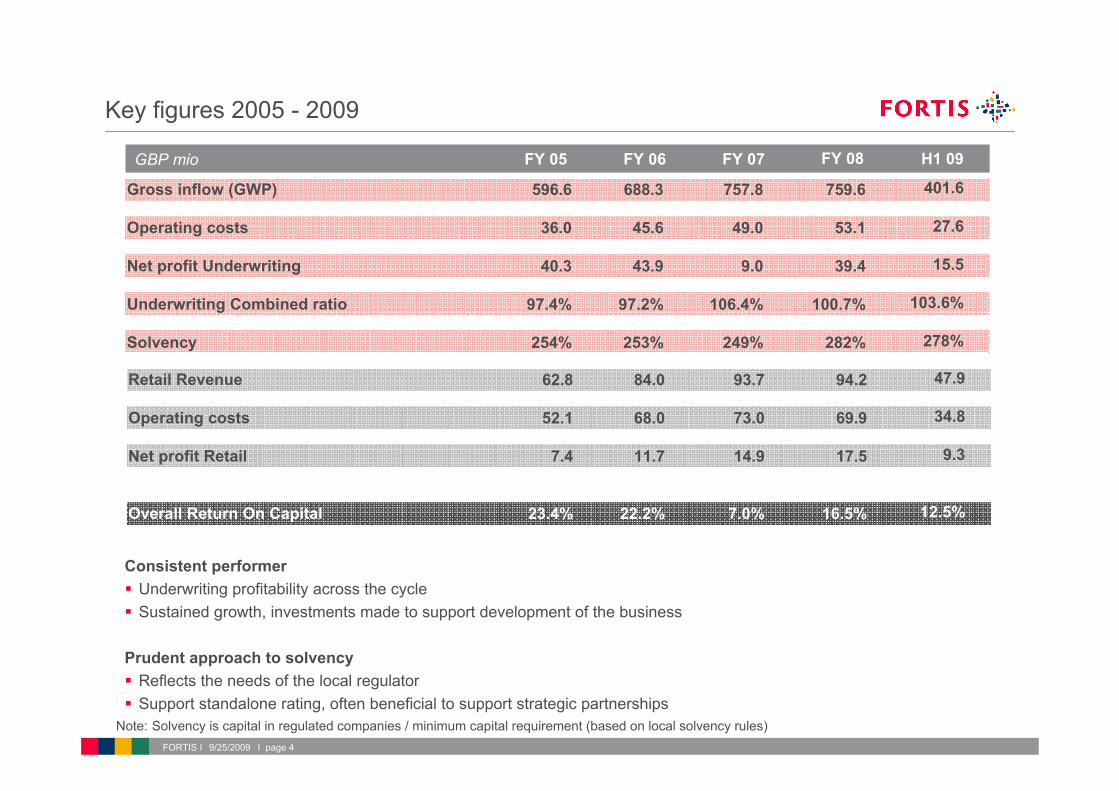

Key figures 2005 - 2009

FY 07FY 05 FY 08FY 06GBP mio

Gross inflow (GWP)

Operating costs

Net profit Underwriting

Underwriting Combined ratio

Solvency

757.8

49.0

9.0

106.4%

249%

596.6

36.0

40.3

97.4%

254%

759.6

53.1

39.4

100.7%

282%

688.3

45.6

43.9

97.2%

253%

H1 09

401.6

27.6

15.5

103.6%

278%

Note: Solvency is capital in regulated companies / minimum capital requirement (based on local solvency rules)

Consistent performerUnderwriting profitability across the cycleSustained growth, investments made to support development of the business

Prudent approach to solvency Reflects the needs of the local regulatorSupport standalone rating, often beneficial to support strategic partnerships

Retail Revenue

Operating costs

Net profit Retail

Overall Return On Capital

62.8

52.1

7.4

23.4%

94.2

69.9

17.5(5.2)

16.5%

84.0

68.0

11.7

22.2%

47.9

34.8

9.3(3.1)

12.5%

93.7

73.0

14.9

7.0%

9/25/2009

FORTIS I

Fortis UK – a journey of evolution and innovation

2003Launch RIAS brand

2005Acquired OutRight and Affinity Solutions to strengthen capabilities in growing partnership market. Secured 10-year relationship Age Concern

2004Secured first affinitypartnership with Post Office to provide Travel insurance.

2000Acquired Northern Star

2001Completed integration of Northern Star with Bishopsgate to create Fortis Insurance

2002Strategic review completed of UK activities.

2006Acquisition of majority shares in distribution technology companies Text2Insure and InsureTECH. Voted General Insurer of the Year

2007New operations centre opened in Gloucester.

2008Extended into Life Protection market and rebranded OutRight to Fortis Insurance Solutions

From a single channel, mono line insurer……“ …to an insurer with a

broad range of solutions

I page 59/25/2009

FORTIS I

We deliver throughNeeds

Fortis UK – our business model today

Brokers & Intermediaries

Competitively priced products, delivered electronically, in the mainLarger intermediaries require underwriting aligned to their product designClear focus on good service at point of claimSome point of sale assistance for certain products e.g. Travel, Small BusinessAncillary products to help them increase their margins

A range of solutions including single insurer, lead insurer, panelMulti-channel interface with their customers e.g. telesales, internet, face to faceUnderwriting only through to the full value chain including systemsStandard and tailored products and servicesOpportunities to increase value and returns

Affinities, Brands & Financial Institutions

Direct Competitively priced products, value for moneyAligned to their chosen method of purchaseSolutions that can be tailored to their needs, sometimes with a choice of insurersGood levels of service across the relationship lifecycleA readily accessible and proactive claims service

Fortis Insurance LimitedText2InsureAffinity Solutions

Fortis Insurance LimitedFortis Insurance SolutionsText2InsureAffinity SolutionsInsureTECH

RIAS (> 50s)Fortis Insurance LimitedFortis Insurance SolutionsText2InsureInsureTECHAffinity Solutions

I page 69/25/2009

FORTIS I I page 7

A proven track record in terms of growth & profitability

Private Car Household Travel Commercial Van Other Protection8% Gross Written Premium CAGR (FY 05-08)

Further diversification of customer baseSuccessful new product launches (e.g. HouseGuard Extra) Entry new product markets (e.g. Van and Protection)

Brokers Owned Affinities

Manufacturing Retailing

Product Evolution (GWP GBP mio)

Distribution Evolution (GWP GBP mio)

Profit Before Tax Evolution (GBP mio)

0

200

400

600

800

FY 05 FY 06 FY 07 FY 08

0

200

400

600

800

FY 05 FY 06 FY 07 FY 08

0

20

40

60

80

FY 05 FY 06 FY 07 FY 08

Impact of severe weather events

About 7 mio customers thanks to deployment of multi-channel distribution model

> 1 mio direct policyholders via retail activities (RIAS, AutoDirect, CoverDirect)Further roll-out of Donedealinsurance.co.ukGrowing customer numbers across all channels

Increasing portion net profit generation viaretailing activities

Generated through margins created through commission and ancillary revenuesGWP generated via the distribution we own

9/25/2009

FORTIS I

With a strong reputation for service and partnership

A clear focus on the understanding and delivering to the needs of the client and the customer

High levels of customer service are hard coded into delivery at all points of contact

Increasingly recognised by its clients, customers and the market for its delivery and approach to doing business such as‒ Six times Insurance Times Motor Insurer of the Year‒ First ever insurer to achieve standard Gold Standard Award ‒ Institute of Insurance Brokers (IIB) ranking Fortis as the top

insurer in terms of service levels compared with 10 other major UK insurers

Fortis’s strong reputation for service has led it to become the ‘Intel inside’ of a number of well known insurance brands in the UK, partnerships developed on a clear understanding of‒ Strategic alignment‒ Open communication‒ Cultural values‒ Common and realistic objectives

Finalist FY 08

I page 89/25/2009

FORTIS I I page 9

Agenda

1. Profile and track record

2. The market and the competition

3. Strategic initiatives

4. Conclusion

9/25/2009

FORTIS I I page 10

Established market positions in chosen marketsPersonal Lines

Highly commoditised and competitive in the UK. Fortis is a strong performerFortis is an established player in the UK’s Personal Lines market competing against many UK based insurers Fortis progressively growing its market share

UK Personal Lines (GWP GBP mio)

0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000 4,500

Great LakesLVAllianzFortisAXAZurichRSALTSBAVIVARBS

Top Car Insurers (by # cars insured)

8,0000 1,000 2,000 3,000 4,000 5,000 6,000 7,000

Zurich

AXA

RSA

HBOS

Fortis

Aviva

RBS

Car insuranceHas provided Fortis with the solid platform on which to grow it’s market presence Fortis has delivered sustained growth over the past 10 years in a highly competitive marketNow insuring in excess 1.7 mio cars, Fortis has grown its market share through its focus on price, underwriting discipline throughout the market cycle and ability to distribute through a broad range of channels

Source: Datamonitor

Source: FSA Returns9/25/2009

FORTIS I I page 11

Delivering solutions aligned to customers needs

Personal Lines distribution has seen some significant changes with the development of the ‘direct’ challenge in late 1990s and the emergence of affinity distribution in recent years

Brokers have continued to have a role to play and many have consolidated their positions and taken the opportunity of internet comparison sites to further broaden their appeal

Fortis has been part of this market development with its strong and deepening relationships in the broker channel, the creation of its own direct operations and its successful expansion in the affinity partnership market

This evolution is driven by where the consumer chooses to buy their insurance and the solution that best suits their needs

Personal Lines Distribution by channelBrokers/Intermediaries Direct Affinities/Partnerships Agents/Others

Fortis Distribution by channelSource: ABI

0%

20%

40%

60%

80%

100%

FY 04 FY 05 FY 06 FY 07 FY 08

Brokers/Intermediaries Direct Affinities/Partnerships

0%

20%

40%

60%

80%

100%

FY 00 FY 01 FY 02 FY 03 FY 04 FY 05 FY 06 FY 07 FY 08

9/25/2009

FORTIS I I page 12

Leveraging operational efficiency to delivery competitive solutions

Personal Lines distribution has seen some Having clear, aligned and efficient routes to the customer are key to success in this highly competitive market

Key to Fortis’s success in the UK has been its efficient operations which enables it to deliver products and services at a cost few other insurers are able to achieve

Fortis is recognised as having the most efficient claims operations for both Motor and Household, and continues to have low unit costs of production in car insurance 0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 7.0% 8.0% 9.0%

FortisNFU Allianz HBOSRBSZurichAvivaHighwayRSAAXA

Ratio of motor claims management costs to net claims incurred

Ratio of household claims management costs to net claims incurredPrivate Car Unit Costs (Company/EMB analysis)

0%

20%

40%

60%

80%

100%

Forti

s

NFU

HBO

S

Hig

hway

AXA

RBS

RSA

Aviv

a

Zuric

h

CIS

Source: Datamonitor, FY 08 data

AvivaAllianzL&GMMALVAssurantRBSGroupamaNFUFortis

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0%

9/25/2009

FORTIS I I page 13

Agenda

1. Profile and track record

2. The market and the competition

3. Strategic initiatives

4. Conclusion

9/25/2009

FORTIS I

Recent trends in General Insurance Distribution

I page 14

Brokers Consolidation subdued during recession

Larger Personal Lines brokers become more active in the internet channel, challenging dominance direct writers

Strong hold over Commercial Lines distribution

Increased focus on alternative income streams, e.g. claims management, upsell and cross-sell

Channel maintained leadership position within Personal Lines but little growth since the emergence aggregators and decision by RBS and Aviva not to transact own large direct businesses via aggregator channel

Zurich, AXA and RSA investing further to grow their own direct businesses primarily through the internet

Remains limited growth of direct channel within Commercial Lines

Direct

AggregatorsWork with consolidators to protect revenues but also build closer strategic partnerships leading to new opportunities e.g. Towergate

Align pricing to purchase channel. Fortis has long standing approach to secure returns in first year, enabling brokers to aligning their returns in more competitive channels

Successfully expanding Commercial Lines product range and broker partnerships e.g. Giles

Introduced new products and propositions to support alternative income streams e.g. Fortis LegalGuard

RIAS established as 2nd largest > 50s specialist, with telesales and internet presence. Soon to be testing in aggregator channel

Recognising dominance of aggregator channel for Car and Household, internet only brands (AutoDirect and CoverDirect) well established present on all leading aggregators. Aggregator only proposition DoneDealinsurance being rolled out across product range

Infrastructure in place for Commercial Lines will support direct channel if consumers demand warrant investment

Fortis response……Market Development……

9/25/2009

FORTIS I

Fortis response……Market Development……

Recent trends in General Insurance Distribution

I page 15

AggregatorsAggregators

Developed capabilities to sell successfully through the aggregator channel using both owned and affinity brands

Invested in products and infrastructure to support higher levels of traffic and consumer demands for products to meet their demands and needs

Good working partnerships established with leading aggregators

Through InsureTECH, have build the capability to build aggregator platforms e.g. MoneyExtra

Broad range of partnerships across a number of market sectors. Chosen partner for a number of trusted brands including Post Office, M&S, Tesco and John Lewis

Strong growth in the affinity market as Fortis has become one of the leading solutions providers. Represents c. 25% of GWP income

Increasingly successful in establishing good relationships with prospective partners and entering new sectors e.g. motor manufacturers with new Toyota deal

Highly competitive channel

Increasing levels of transparency enabling consumers to fully understand what drives risk price

Rationalisation of the market expected; Brand awareness essential to success

Leading aggregators now becoming more well known than the insurance brands/companies who use them

Turbulence around financials services brands (e.g. banks) positively impacting trust in quality non-financial brands e.g. M&S, Post Office, Tesco

Market share in c.15% of Motor and Household markets.

Large affinity deals continue to offer opportunities as they come up for renewal e.g. Ford, GM and Toyota recently changed their respective insurance solutions providers

Partnerships(affinities)

9/25/2009

FORTIS I

Fortis UK Strategy focuses on 3-axes growth strategy …

Continued development of our multi-channel platform, based on flexibility and easy adaptability to new market dynamics

A focus on major distribution channels driven by the needs of the consumer

Combination of own distribution and third party providers

In-depth adaptation of pricing policy and product lines in order to widen appeal both to business partners and end customers.

Capitalise on existing capabilities with a focus on support systems allowing greater speed and control over manufacturing and operational delivery

MAN

UFAC

TURI

NG

Products

Channels

Customers

RETAILING

COMBINED CAPABILITY

I page 169/25/2009

FORTIS I

… To be realised by actions aligned to our axes of growth….

I page 17

Manufacturing

Retailing

Combined Capability

Continued development of a high quality and profitable range of Personal & Commercial lines products to support multi-channel strategyImproving existing products to widen appeal and introduction of new productsOngoing investment in underwriting excellence and rating techniquesContinued focus on low unit cost of production and high levels of customer service

Design and delivery of a broad range of tailored insurance solutions for the >50s market through our RIAS brandContinued development and growth of internet based propositionsResearch & development of propositions to continue to reflect the insurance and purchase preferences of consumersContinue to invest in retail margins through service efficiency and value adding products

Continued building of broad range of capabilities to satisfy the existing and emerging needs of our multi-channel approach Further improve operational effectiveness through partnership with key suppliers of products & servicesFocus on ensuring the ‘whole is greater than the sum of the parts’

9/25/2009

FORTIS I

….with continued exploration into the Protection market

0

20

40

60

80

100

Q107 Q207 Q307 Q407 Q108 Q208 Q308 Q408 Q109

I page 18

02004006008001,0001,200

FY 00 FY 01 FY 02 FY 03 FY 04 FY 05 FY 06 FY 07 FY 08

New Annual Premiums (GBP 000's)IFA Direct Sales Bancassurers Non-intermediated

New Annual Premiums sold via IFAs (%)

FortisLegal & General AVIVAScottish Equitable

Friends ProvidentRoyal LondonAXA Sun Life BUPA

LV=Zurich Other

Based on Non-Life model, research undertaken as to whether there is a natural extension into the UK Protection market

Applying the same principlesIntroduce a range of products aligned to client and consumer needsMulti-channel distributionEstablish strong service credentialsLow cost efficient operations

From a greenfield start, we entered UK market in August FY 08

Achievements so far include:Launched innovative products, securing 5* ratingsCreated a point of sale system which has market leading straight through processing rates linked to an automated underwriting systemHave had early successes with our multi-channel approach Built a business receiving > 500 applications per day Written >GBP 9 mio new annual premiums since launch, selling >30,000 policies

Our research will continueLinked to multi-channel distributionHow we align further with the needs of the client and consumer (products and services)Further improve operational efficiency and effectiveness

9/25/2009

FORTIS I

Growth of Tesco Personal Finance (mio customers)

Fortis and Tesco – one of the largest partnerships in the UK

9/25/2009 I page 19

Tesco is the UK’s largest general retailer generating sales of GBP >59 bn (08), net profit before tax of GBP 2.9 bn*

Tesco Personal Finance (TPF) launched in 1997 and by end 08 reported underlying profit of GBP 244mio (insurance representing over 65%).

End 08, TPF had in the region of 6 mio customers, c. 2.5 mio relating to insurance generating GBP 500 mio GWP including 1.1 mio car and over 440k household customers

Fortis & Tesco will create Tesco Insurance, leveraging Fortis’s existing skills, capabilities and operations in the core areas of underwriting, product development and claims‒ GBP 100 mio capital investment‒ An initial period of 5-years ‒ Management team and Board consist of Fortis and Tesco

senior executives

This partnership and the planned organic growth of Fortis UK, will potentially position Fortis as:‒ A top 6 General Insurer‒ 3rd or 4th largest Personal Lines insurer‒ 2nd largest car insurer (by volume of cars)‒ A leading affinity insurer in the UK insuring in excess of 12

mio customers

Tesco insurance is expected to be operational by the end of 2010

* Reported sales and profit for 53 weeks ending 28 February 2009

0

1

2

3

4

5

6

2001 2008

FORTIS I I page 20

Agenda

1. Profile and track record

2. The market and the competition

3. Strategic initiatives

4. Conclusion

9/25/2009

FORTIS I

Fortis UK - rising to a number of market challenges

I page 21

Customer Service

Efficiency

People

Continued demand for higher standards of service and efficiencyThe annual renewal cycle is a natural opportunity to switch to other insurance providers. Pricing capabilities should lead to competitive propositions throughout their relationship, reflecting their demands, needs and their chosen channel of purchaseIn parallel, work more closely with clients and customers to deepen knowledge of the needs and the relationship with Fortis

Continued investment in employees to support ongoing growth including working with industry and educational bodies, nationally and locally Focus on developing our Fortis family, in order to identify how we can further improve our role as an employer & develop them as employeesAmbition is to be recognised as a quality employer within the UK

Fortis’ service up, cost down ethos will continue to deliver service above market norms at a very competitive costPropositions should benefit from a service experience that adds value to the customer’relationship and that creates more marginProgressively establish strategic partnerships to provide cost and service leverage across our operationsOur focus on efficiency and effectiveness will continue to avoid significant cost reductions our competitors find necessary

9/25/2009

FORTIS I

Key messages

• Large market with potential for growth of market share

• Successful development & implementation of a multi-channel distribution model

• Proven track record of consistent profitable underwriting results

• Recognised low cost market leader with award winning high quality service

• Strategy of a broader range of products via multi-channel distribution should result in delivering excess CAGR compared to market norms

• Growth will be delivered profitably, with a continued focus of managing underwriting excellence and margins to deliver market competitive CORs

9/25/2009