Embed Size (px)

Citation preview

TMX Equicom Toronto

April 2, 2014

Rob Dawson, Chief Financial Officer

Siren Fisekci, VP Investor and Corporate Relations

Forward-looking information

In the interest of providing you with information regarding Canadian Oil Sands Limited (the “Corporation”), including management’s assessment of the Corporation’s future plans and operations, certain statements and

graphs throughout this presentation contain “forward-looking information” under applicable securities laws. Forward-looking statements are typically identified by words such as “anticipate”, “expect”, “believe”, “plan”, “intend”

or similar words suggesting future outcomes. Forward-looking statements in this presentation include, but are not limited to, statements and graphs (collectively “statements”) with respect to: future dividends and any

increase or decrease from current payment amounts; the expected sales volume in 2014; the expected operating expenses in 2014; the expected cash flow from operations and cash flow from operations per share in 2014;

the expected realized selling price for the Corporation’s product in 2014; the estimated value and amount of reserves recoverable and the time frame to recover such reserves; the estimated resources; the expected impact

on cash flow from operations and cash flow from operations per share from increasing/decreasing crude oil prices; the expected impact on cash flow from operations from increasing Syncrude production; the expected

foreign exchange rate in 2014; the expected West Texas Intermediate (“WTI”) price in 2014; the expected average discount for synthetic crude oil (“SCO”) to WTI in 2014; the expected amount of total major project costs,

anticipated target in-service dates and estimated completion percentages for the Mildred Lake mine train replacements and the centrifuge plant at the Mildred Lake mine; the expectation that the major project spending will

taper off in 2015; the expected major project spending in 2014-2015; the estimate that regular maintenance capital costs for the next few years will be similar to 2014; the expectation that the Corporation will finance the

major projects primarily with existing cash balances and cash flow from operations; the belief that the Corporation is positioned to fund its 2014 capital program and support its dividend while maintaining net debt within the

targeted range; all expectations regarding net debt; the anticipated amount of current taxes in 2014; the expected increase in free cash flow in 2015 assuming continued strength in world crude oil prices; plans regarding

crude oil hedges in the future; the expected benefits of the management services agreement; the anticipated benefits in extraction and upgrading resulting from Syncrude’s reliability initiatives; the belief that the reliability

initiatives in place at Syncrude will lead to higher production levels; expectations regarding the Corporation’s cash levels; Crown royalties payable; the anticipated scope and economics of the Mildred Lake mine extension

(“MLX”) project; the expectation that the MLX project should allow the Mildred Lake mine and the Aurora North mine to operate into the 2030s and 2040s, respectively; the expectation that Syncrude will submit a regulatory

application for the MLX project in 2014; the timing of construction and spending for the MLX project; the expectation that the MLX project should be the most economic new mining production to come on stream in the next

ten years because it benefits from existing infrastructure and expectations regarding the timing of planned/announced market access pipelines, and all expectations regarding the SCO-WTI-Brent differentials.

You are cautioned not to place undue reliance on forward-looking statements, as there can be no assurance that the plans, intentions or expectations upon which they are based will occur. By their nature, forward-looking

statements involve numerous assumptions, known and unknown risks and uncertainties, both general and specific, that contribute to the possibility that the predictions, forecasts, projections and other forward-looking

statements will not occur. Although the Corporation believes that the assumptions and expectations represented by such forward-looking statements are reasonable and reflect the current views of the Corporation with

respect to future events, there can be no assurance that such assumptions and expectations will prove to be correct.

The factors or assumptions on which the forward-looking statements are based include, but are not limited to: the assumptions outlined in the Corporation’s guidance document as posted on the Corporation’s website at

www.cdnoilsands.com as of the date hereof and as subsequently amended or replaced from time to time, including without limitation, the assumptions as to production, operating expenses and oil prices; the successful and

timely implementation of capital projects; Syncrude’s major project spending plans; the ability to obtain regulatory and joint venture owner approval; our ability to either generate sufficient cash flow from operations to meet

our current and future obligations or obtain external sources of debt and equity capital; the continuation of assumed tax, royalty and regulatory regimes and the accuracy of the estimates of our reserves and resources

volumes.

Some of the risks and other factors which could cause actual results or events to differ materially from current expectations expressed in the forward-looking statements contained in this AIF include, but are not limited to:

volatility of crude oil prices; volatility of the SCO to WTI differential; the impact that pipeline capacity and apportionment and refinery demand have on prices for SCO; the impacts of regulatory changes especially those

which relate to royalties, taxation, tailings, water and the environment; the impact of new technologies on the cost of oil sands mining; the impacts of rising costs associated with tailings and water management; the inability

of Syncrude to obtain required consents, permits or approvals, including without limitation, the inability of Syncrude to obtain approval to release water from its operations; the impact of Syncrude being unable to meet the

conditions of its approval for its tailings management plan under Directive 074; various events which could disrupt operations including fires, equipment failures and severe weather; unsuccessful or untimely implementation

of capital or maintenance projects; the impact of technology on operations and processes and how new complex technology may not perform as expected; the obtaining of required owner approvals from the Syncrude

Participants for expansions, operational issues and contractual issues; labour turnover and shortages and the productivity achieved from labour in the Fort McMurray area; uncertainty of estimates with respect to reserves

and resources; the supply and demand metrics for oil and natural gas; the variances of stock market activities generally; currency and interest rate fluctuations; volatility of natural gas prices; Canadian Oil Sands’ ability to

either generate sufficient cash flow from operations to meet our current and future obligations or obtain external sources of debt and equity capital; the inability of the Corporation to continue to meet the listing requirements

of the TSX; general economic, business and market conditions and such other risks and uncertainties described in the Corporation’s Annual Information Form dated February 20, 2014 and in the reports and filings made

with securities regulatory authorities from time to time by the Corporation which are available on the Corporation’s profile on SEDAR at www.sedar.com and on the Corporation’s website at www.cdnoilsands.com.

In this presentation we refer to additional GAAP and non-GAAP financial measures that do not have any standardized meaning as prescribed by Canadian Generally Accepted Accounting Principles (“GAAP”). We refer to

additional GAAP financial measures such as cash flow from operations, cash flow from operations on a per share basis and net debt. For more information on additional GAAP financial measures please refer to our 2013

Annual Management’s Discussion and Analysis which is available on the Corporation’s profile on SEDAR at www.sedar.com and on the Corporation’s website at www.cdnoilsands.com. In this presentation we also refer to

non-GAAP financial measures such as free cash flow, return on equity, enterprise value and earnings before interest and taxes. For more information on free cash flow and return on equity (referred to as return on average

shareholders’ equity in our 2013 Annual Report) please refer to our 2013 Annual Report, which is available on the Corporation’s profile on SEDAR at www.sedar.com and on the Corporation’s website at

www.cdnoilsands.com. Enterprise value and earnings before interest and taxes are discussed in this presentation.

Third party information: To the extent that information contained in this presentation, forward-looking or otherwise, has been derived from third party sources such as Bloomberg, First Energy, the US Department of

Energy, Environment Canada, the International Energy Agency, IHS CERA and the Canadian Association of Petroleum Producers, the Corporation makes no representations or warranties, express or implied, as to the

quality, accuracy and completeness of such information.

Why own COS

• Pure (100% light, sweet) crude oil investment in long-life resource

• Strong operating base with production upside potential

• High-quality, undeveloped leases for future development

• Well-positioned with financial strength and flexibility

• High dividend payout (current yield 6.2%*)

The definitive oil sands investment

* Based on March 26/14 stock price and dividend announced on Jan. 30/14, annualized

Syncrude: A high quality resource

• Strong, stable production base

• Integrated oil sands mining project

• No exposure to light/heavy differentials

• Proven technology

• Predictable reservoir recovery – over 90%

• Less exposure to natural gas prices and impact of potential CO2 legislation than SAGD projects

1.6

5.1

2.2

2.3

0 1 2 3 4 5 6 7

Prospective resources

Contingent resources

Probable - Undeveloped

Proved plus Probable - Producing

Large Syncrude reserve and resource base supports decades of production

Billions of Synthetic Crude Oil Barrels

1. All amounts gross to Syncrude. Canadian Oil Sands Limited, through its wholly-owned partnership, holds a 36.74% interest in the Syncrude Project. Based on independent reserves and resources estimates by GLJ Petroleum Consultants, Ltd. as of Dec. 31/13. See reserves and resources cautionary advisory in Canadian Oil Sands’ Annual Information Form dated Feb. 20/14 and the definitions and forward-looking information advisory.

2. Calculated as Proved Developed Producing Reserves of 2.0 billion barrels plus Probable Producing Reserves of 0.3 billion barrels. Probable Producing Reserves calculated as Total Probable Reserves of 923 million barrels (net to COS) less Probable Undeveloped Reserves of 812 million barrels (net to COS) equals 111 million barrels (net to COS) or 0.3 billion barrels (100% Syncrude).

3. Calculated as 812 million barrels (net to COS) grossed up to reflect 100% Syncrude.

4. Reserve Life Index (RLI) based on COS January 30, 2014 Guidance of approximately 105 million barrels per year of Syncrude production (38.6 million barrels net to COS).

• Mildred Lake

Extension

• Other leases

• Other leases

•Aurora South

• Mildred Lake

• Aurora North

RLI= 22 years 4 2

3

1

RLI= 21 years 4

Pure play oil sands investment

0% 20% 40% 60% 80% 100%

COS

Canadian Natural

Cenovus

Imperial

MEG

Suncor

Oil sands as % of total production

Source: FirstEnergy Capital Nov. 8/13 report

Our production is 100% light, sweet crude oil

Quality and location differentials

Cdn $/bbl Trailing 3-month

average

$40

$50

$60

$70

$80

$90

$100

$110

$120

$130

Trailing 3-Month Average

Brent

SCO

WTI

WCS

Bitumen

Kitimat

Hardisty

Edmonton

Burnaby

Cushing

Montreal

Houston

Sarnia

Patoka

Quebec City

Markets for COS’ Syncrude Production

Chicago

Syncrude

Current synthetic crude oil markets

Potential new markets

Sales volume (bbl/d)2 105,700

Operating expenses ($/bbl) 41.48

Cash flow from operations ($millions)3,4 1,158

Cash flow from operations ($/share)3 2.39 Realized selling price ($/bbl) 87.77

2014 Outlook

20141

1. 2014 Outlook as at Jan. 30/14. 2. Sales after crude oil purchases and transportation expense.

3. Additional GAAP measure. 4. 2014 CFFO includes $200 million in cash taxes.

Highly leveraged to increasing crude oil prices1

0.00

1.00

2.00

3.00

4.00

$70 $80 $90 $100 $110

Illustrative cash flow from operations ($/share)2

WTI (US$/bbl)

2014 estimate

All figures in Canadian dollars unless otherwise noted. 1. Every US $1.00/bbl WTI increase/decrease in crude oil price increases/reduces cash flow from operations/share by $0.05 after tax; see Jan. 30/14 Guidance for other

sensitivities; this assumes no other changes to operating expenses or other assumptions from the Jan. 30/14 Guidance; see the risk factors outlined in our Annual Information Form dated Feb. 21/13 as to other risks; for illustrative purposes only – COS is not expressing a particular view on crude oil prices.

2. Additional GAAP measure; assumes Jan. 30/14 Guidance of: $0.97 US$/Cdn$ FX, $5/bbl SCO discount to Cdn$WTI, $41.48/bbl operating expenses and sales of approximately 105,700 bbl/d net to COS.

Operating leverage

0

50

100

150

200

250

300

350

400

2007 2008 2009 2010 2011 2012 2013 2014F

Syncrude production

Thousand barrels per day

2014F based on Jan. 30/14 Outlook.

Average production of 287,000 bbl/d since 2007

2 million bbl change in 2014 Syncrude production impacts cash flow from operations by $40 million

Key reliability initiatives

Extraction

• Major projects in 2013/2014 renew and replace most crusher/conveyor systems

– Start-up of MLMR in Q4 2014 increases froth production capacity by ~20%

• Reduced solids content in bitumen feed

– Retrofitting centrifuges and reconfigured centrifuge bypass

Upgrading

• Replaced hydrogen plant exchangers (remaining 4th to be completed Q1 2014)

• Designing modifications to improve CO boiler performance

• Plan to improve run length of hydrotreaters

Premium product and competitive operating costs result in significant margin advantage

Average premium of $11/bbl translated to $2.4B total advantage since 2008

Realized price advantage vs. Competitor “A”

Operating cost advantage / disadvantage vs. Competitor “A”

Gross margin advantage

Source: Company “A” data based on publicly available information. Sales and operating costs are volume-weighted and use a four-quarter trailing average

Syncrude margin advantage over nearest competitor

$(5.00)

$-

$5.00

$10.00

$15.00

$20.00

Syncrude upgrader delivers significant value

$0

$20

$40

$60

$80

$100

$120

COS Mining & SAGD Peer

Typical SAGD Peer

Earnings before interest and taxes

Depreciation

Crown royalties

Other

Operating expenses and G&A

per bbl

1. COS data for the year ended December 31, 2013; Peer data updated periodically based on publicly available data as it becomes available: Cenovus Operating, MEG Net Operating Costs, Suncor Total Cash Operating Costs

2. SAGD based on average of Cenovus (Christina Lake and Foster Creek), MEG and Suncor In-situ 3. “Other” for COS and Suncor refers to non-production or development costs, MEG is share-based comp and R&D 4. COS operating expenses include Syncrude G&A 5. Earnings before interest and taxes is a non-GAAP financial measure and is calculated as net income plus tax expense plus

net finance expense plus foreign exchange gain (loss).

COS EBIT ~ $35/bbl

1, 4

1 1, 2

3

5

Compelling valuation relative to new mining projects

Project(s) Cost estimate/ Enterprise value1

Production capacity (bbl/d)

Product $ per flowing bbl

Syncrude (COS’ share)

$11.8 billion 128,000

Light, sweet synthetic

$92,000

Kearl Lake 2

(Imperial Oil) $12.9 billion 110,000

Bitumen $117,000

Horizon Phases 2/3 3

(CNRL) $12.5 billion - $14.0 billion

140,000

Light, sweet synthetic

$90,000 - $100,000

Fort Hills 4

(Suncor/Total/Teck) $15.1 billion 180,000 Bitumen $84,000

1. COS enterprise value based on market cap as at March 26/14 and net debt at December 31/13; non-GAAP measure. 2. Company estimate for cost and production capacity; includes pre-built infrastructure. 3. Company estimate for capital required for 140,000 bbl/d of growth from the Reliability-Tranche 2 and Phases 2A, 2B and 3. 4. Suncor estimate announced October 2013; includes capital spend to date.

At similar price, COS provides additional value through:

• Production today

• High quality synthetic product

• All of our reserves and resources

• High dividend payout

Investing in our business for sustained success

Major Capital Projects Total Costs 1

Total cost estimate

($B)

Total cost estimate

accuracy (% )

Estimated % complete @

12/31/132

Target in-service date

Mildred Lake mine train replacement 1.6 +15% /

-15% 80% Q4 2014

Centrifuge tailings management 0.7 +15% /

-15% 70% H1 2015

(1) Total project costs are net COS’ 36.74% working interest and include both capital and certain development expenses; costs exclude capitalized interest.

(2) The estimated percentage complete is based on hours spent as a percentage of total forecasted hours to project completion.

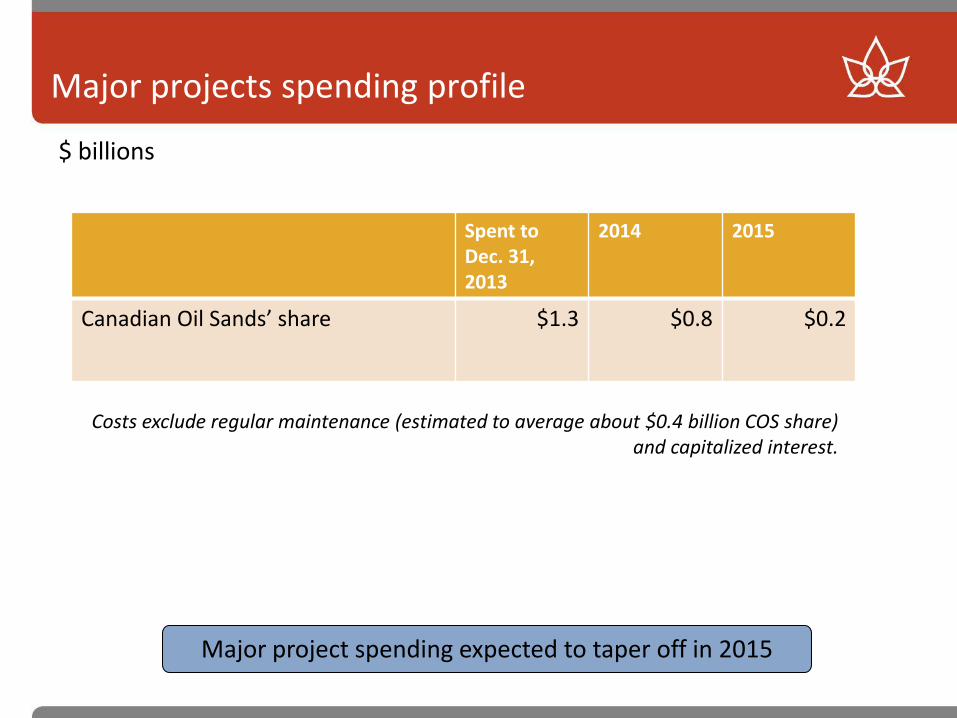

Major projects spending profile

Spent to Dec. 31, 2013

2014 2015

Canadian Oil Sands’ share $1.3 $0.8 $0.2

$ billions

Costs exclude regular maintenance (estimated to average about $0.4 billion COS share) and capitalized interest.

Major project spending expected to taper off in 2015

Mildred Lake Mine Train Replacement

Strong liquidity position to support capital program and healthy dividend

Based on COS’ 2014 Outlook dated Jan. 30/14; dividends assume quarterly $0.35 per share for 2014 (This is an illustrative assumption and COS is not expressing a view on its future dividends). Cash flow from operations is an additional GAAP measure. A portion of the cash balance at Dec. 31/13 will be used in 2014 to settle accounts payable of $500 million for taxes and Crown royalties.

$ millions

0

500

1000

1500

2000

Cash uses - 2014 estimate

Cash flow from operations - 2014

estimate

Cash balance @ Dec 31/13

Credit facility (undrawn)

Dividends

Capex

$1.8B

$1.2B

$0.8B

$1.5B

Managing a strong, efficient balance sheet

1. Non-GAAP measure

Net debt1, $ millions

0

500

1000

1500

2000

2005 2006 2007 2008 2009 2010 2011 2012 2013

Targeting net debt level of $1 to $2 billion

0

500

1000

1500

2000

2500

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

major projects capex

maintenance capex

capitalized interest

cash flow from operations

Positioned for strong free cash flow1,2

$ millions, net to Canadian Oil Sands

(1) Free cash flow is calculated as cash flow from operations less capital expenditures and is a non-GAAP measure. (2) Data for 2009 and prior years has not been adjusted for International Financial Reporting Standards “IFRS”. (3) Maintenance capex post 2014 based on an estimated $10/bbl; capital expenditures exclude capitalized interest post 2014.

3

Dividends reflect free cash flow over time (1,2)

(1) Includes distributions on trust units prior to Dec. 31/10 (2) Free cash flow (FCF) is cash flow from operations less capital expenditures and is a non-GAAP measure

Cumulative Dividends/FCF Annual Total Dividends

$ millions

$(1,000)

$-

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$(300)

$-

$300

$600

$900

$1,200

$1,500

$1,800

$2,100

$2,400

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Dividends

Cumulative Dividends

Cumulative FCF

Highest yield amongst peers

6.2%*

2.2%

3.5%

1.0%

0.0%

2.5%

2.9%

2.0%

COS

Canadian Natural

Cenovus

Imperial

MEG

Suncor

S&P/TSX

S&P 500 Average

Source: Bloomberg as at March 26/14 *Based on price as at March 26/14 and dividend announced Jan. 30/14, annualized.

Note: COS does not target a specific yield .

COS investment catalysts

1. Higher production through improved reliability

2. Completion of remaining major projects

• Mildred Lake Mine Replacement (MLMR)

• Tailings Centrifuge Project

3. Market access

• Narrowing of SCO-WTI-Brent differentials

4. Market view of long-term oil prices

These four catalysts

represent potential

upside to COS’ share

price

Plus, COS offers:

Higher oil prices and

lower CAD than

assumed in our

current guidance

Solid finance plan and

a strong balance

sheet

6.2% yield*

* Yield as at March 26, 2014

COS has significantly outperformed the market over the long-term

Source: Bloomberg

Average compound annual return

14%

10%

8%

-100%

0%

100%

200%

300%

400%

500%

600%

700%

Dec-0

3

Apr-

04

Aug-0

4

Dec-0

4

Apr-

05

Aug-0

5

Dec-0

5

Apr-

06

Aug-0

6

Dec-0

6

Apr-

07

Aug-0

7

Dec-0

7

Apr-

08

Aug-0

8

Dec-0

8

Apr-

09

Aug-0

9

Dec-0

9

Apr-

10

Aug-1

0

Dec-1

0

Apr-

11

Aug-1

1

Dec-1

1

Apr-

12

Aug-1

2

Dec-1

2

Apr-

13

Aug-1

3

Dec-1

3

10 Year Cumulative Return as of December 31, 2013

Canadian Oil Sands

S&P/TSX Oil & Gas

S&P/TSX Composite

Appendix

Syncrude supported by Management Services Agreement with ExxonMobil and Imperial Oil

Canadian Oil Sands (COS)

25%

Suncor

Sinopec

36.74%

12%

Nexen (CNOOC)

7.23%

Murphy Oil

Mocal

5%

Imperial Oil

XOM/IMO provide global best practices, proprietary systems and staff expertise

JV ownership structure

COS: a premier pure-play oil sands investment

• Ticker: COS on Toronto Stock Exchange

• Shares outstanding: 484.6 million

• 52 week high / low / close1: $22.59 / $18.62 / $21.59

• Market cap: $10.9 billion1

• Enterprise value: $11.8 billion2

• Quarterly dividend amount: $0.35 per share3

• High dividend payout: 6.2%4

All figures in Canadian dollars 1. As at March 26/14. 2. As at March 26/14 and net debt at Dec. 31/13; non-GAAP measure. 3. Paid on Feb. 28/14 to shareholders of record on Feb. 21/14. 4. Based on close price as at March 26/14 and dividend announced on Jan. 30/14, annualized.

Demonstrating strong return on shareholders’ equity

Average ROE of 24% since 2001

Return on Equity calculated as net income divided by average shareholders’ equity; Net income as per COS’ financial statements

Return on shareholders’ equity is a non-GAAP measure.

$-

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

$35.00

$40.00

$45.00

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Pe

rce

nta

ge

Re

turn

Canadian Oil Sands' ROE

Return on Equity

Average ROE of 24%

Average Share Price

Bitumen production projects

2 mine train moves

2 new mine train builds

2 sustaining mine train builds

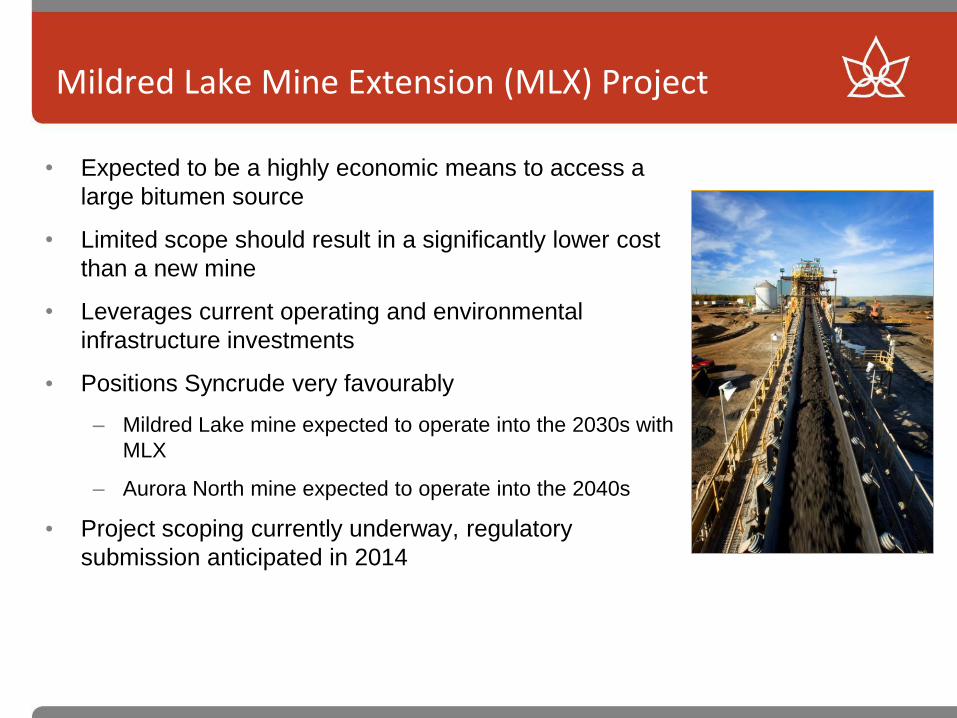

Mildred Lake Mine Extension (MLX) Project

• Expected to be a highly economic means to access a

large bitumen source

• Limited scope should result in a significantly lower cost

than a new mine

• Leverages current operating and environmental

infrastructure investments

• Positions Syncrude very favourably

– Mildred Lake mine expected to operate into the 2030s with

MLX

– Aurora North mine expected to operate into the 2040s

• Project scoping currently underway, regulatory

submission anticipated in 2014

A mine train processes oil sands ore

Surge bin

Crusher

Mix box

Hydrotransport

1

2

3

4

1 2

3

4

Access to Markets – Pipeline Expansions in Development

Source: CAPP

U.S. Oil Demand and Sources of Supply

Source: IEA Annual Energy Outlook 2012

Syncrude is a leader in sustainable oil sands development

Recognition

Reflects industry best practices

• Mining Association – Toward Sustainable Mining

• Canadian Association of Petroleum Producers – Responsible Canadian Energy Program

• Canadian Council for Aboriginal Business – Progress Aboriginal Relations Program

• Canadian Business for Social Responsibility

• Canadian Industry Program for Energy Conservation

Leading Research and Development

• Syncrude operates the industry’s only dedicated R&D centre

• Syncrude spends $60 million on R&D each year; one of Top 50 spenders in Canada

• Syncrude is a founding member of Canadian Oil Sands Network for Research and Development (CONRAD) and the Oil Sands Tailings Consortium (OSTC), which will be managed under the recently formed Canadian Oil Sands Industry Alliance (COSIA)

CSR Reporting • Syncrude publishes a bi-annual sustainability report

www.syncrudesustainability.com • Also publishes an annual Aboriginal Review

A responsible developer of the oil sands

Achievements at Syncrude

Reduced water intensity by 60% since the early 1980s

Recycle ~85% of water used

Responsible for ~70% of all reclaimed land in oil sands mining industry

Returned 3,400 hectares to nature

Planted nearly 7 million trees

One of Canada’s largest employers of Aboriginal peoples (~9% of workforce)

Conducted over $1.7 billion in business with Aboriginal companies since 1992

Over $6 million/year donated to community projects and initiatives

Oil sands industry GHG emissions are 3.5% of those of the U.S. coal industry

Source: U.S. DOE/EIA, Environment Canada 2009, CAPP

“Wells-to-wheels” CO2 emissions

Source: IHS CERA Special Report – Oil Sands Dialogue: Oil Sands, Greenhouse Gases, and US Oil Supply: Getting the Numbers Right, November 2012

Average oil

sands is

only 9%

more GHG

intensive

than

average

U.S. barrel

Environmental regulations

• GHG – Provincial regulations require 12% reduction in emission intensity over 2003 - 2005 average for

large emitters

• If not met, the emitter may:

– Pay $15/tonne levy into Climate Change and Emissions Management Fund

– Purchase Alberta based offset credits

– Purchase emission performance credits from a different Alberta facility.

– Federal government targeting 17% reduction by 2020 from 2005 levels

• Land – Alberta law requires land reclamation to productivity equal to or better than original

– Directive 074 - requirements to reduce tailings and accelerate reclamation

• Water – All existing and approved oil sands projects restricted to withdraw less than 3% of average

annual flow of Athabasca River

– Further restrictions during low flow periods; actual usage by industry less than 1% of average annual flow

Syncrude Crown royalty terms*

• Greater of 25% net bitumen revenue less capital and operating costs, or 1% of

gross bitumen revenue*

– Previously based on Synthetic Crude Oil (upgraded from bitumen) revenues

and costs

• Repay $1.25 billion plus interest over 25 years for previously deducted

upgrader growth capital

– Payments deferred during 1% royalty periods

• Pay an additional $975 million in royalties as per schedule:

– Amount will be prorated to extent Syncrude daily average bitumen production over 6-

year period less than 345 KBPD

* Terms and rates effective Jan. 1/09 to Dec. 31/15. The royalty agreements are available on the Corporation’s profile at www.sedar.com. Effective Jan. 1/16 New Royalty Framework rates apply.

2010 2011 2012 2013 2014 2015 Total

$75 mm $75 mm $100 mm $150 mm $225 mm $350 mm $975 mm

All figures gross to Syncrude

2014 Crown Royalty Calculation

1. Bitumen revenue is based on an SCO yield of 87% and a bitumen price equal to 60% of C$WTI. 2. Royalty rate is the greater of 25% of net revenue or 1% of revenue. 3. As part of the transition to the generic royalty regime, Syncrude is obligated to pay additional Crown Royalties of $975 million over 2010-

2015. The $57 million shown above is COS’ share of the 2014 expense based on accrual accounting; actual cash payments are per the schedule on previous slide. In any given year, the difference will be reflected as a change in Crown royalty payable.

See COS’ 2012 Annual MD&A dated Feb. 20/14 for further discussion on Crown royalties.

Based on 2014 Outlook provided Jan. 30/14

SCO % Mining Bitumen

Revenue1 3,386 2,469

Operating expenses (1,600) 80% (1,280)

Non-production costs (181) 80% (145)

Capital expenditures (1,014) 85% (862)

Net revenue 182

Crown royalty2 46

Upgrader growth capital recapture payment 25

Additional Crown royalty expense3 57

Total Crown royalty 128

Crown royalty (per bbl) $3.32