Embed Size (px)

Citation preview

1

SoK: Decentralized Exchanges (DEX) withAutomated Market Maker (AMM) Protocols

Jiahua Xu, Krzysztof Paruch, Simon Cousaert, Yebo Feng

Abstract—As an integral part of the decentralized finance(DeFi) ecosystem, DEX with AMM protocols have gained massivetraction with the recently revived interest in blockchain and dis-tributed ledger technology (DLT) in general. Instead of matchingthe buy and sell sides, AMMs employ a peer-to-pool methodand determine asset price algorithmically through a so-calledconservation function. To facilitate the improvement and devel-opment of AMM-based DEX, we create the first systematizationof knowledge in this area. We first establish a general AMMframework describing the economics and formalizing the system’sstate-space representation. We then employ our framework tosystematically compare the top AMM protocols’ mechanics,illustrating their conservation functions, as well as slippage anddivergence loss functions. We further discuss security and privacyconcerns, how they are enabled by AMM-based DEX’s inherentproperties, and explore mitigating solutions. Finally, we conducta comprehensive literature review on related work covering bothDeFi and conventional market microstructure.

Index Terms—decentralized finance, decentralized exchange,automated market maker, blockchain, Ethereum

I. INTRODUCTION

With the revived interest in blockchain and cryptocurrencyamong both the general populace and institutional actors, thepast year has witnessed a surge in crypto trading activity andaccelerated development in the decentralized finance (DeFi)space. Among all the prominent DeFi applications, decentral-ized exchanges (DEX) with automated market maker (AMM)protocols are in the ascendancy, with an aggregate value lockedexceeding $100 billion at the time of writing [1].

AMM-based DEX bear attractive features such as decentral-ization, automation and continuous liquidity. With traditionalorder-book-based exchanges, the market price of an asset isdetermined by the last matched buy and sell orders, ultimatelydriven by the supply and demand of the asset. In contrast, onan AMM-based DEX, a liquidity pool acts as a single coun-terparty for each transaction, with a so-called conservationfunction that prices assets algorithmically by only allowing theprice to move along predefined trajectories. AMMs implementa peer-to-pool method, where liquidity providers (LPs) con-tribute assets to liquidity pools while individual users exchangeassets with a pool or pools containing the input and the outputassets. Users obtain immediate liquidity without having tofind an exchange counterparty, whereas LPs profit from asset

J. Xu and S. Cousaert were with the Centre for Blockchain Technolo-gies, University College London, London, WC1E 6EA, UK. E-mail: [email protected] and [email protected].

K. Paruch was with the Vienna University of Economics and Business,Austria. E-mail: [email protected].

Y. Feng was with the Department of Computer and Information Science,University of Oregon, Eugene, OR, 97403 USA. E-mail: [email protected].

supply with exchange fees from users. Furthermore, by usinga conservation function for price setting, AMMs render mootthe necessity of maintaining the state of an order book, whichwould be costly on a distributed ledger.

AMMs benefit both LPs and exchange users with accessibleliquidity provision and exchange, especially for illiquid assets.Despite the apparent advantages, AMMs are often character-ized by high slippage and divergence loss, two implicit eco-nomic risks imposed on the funds of exchange users and LPsrespectively. Moreover, AMM-based DEX are associated withmyriads of security and privacy issues. Throughout the lastthree years, new protocols have been introduced to the marketone after another with incremental improvements, attemptingto tackle different issues which had been identified as weakspots in a previous version. On top of that, new use cases arebeing addressed, and new applications of AMM iterations areproposed to the market. While innovative in certain aspects,the various AMM protocols generally consist of the same setof composed mechanisms to allow for multiple functionalitiesof the system. As such, these systems are structurally similar,and their main differences lie in parameter choices and/ormechanism adaptations.

As one of the earliest DeFi application categories, AMM-based DEX also constitute the most fundamental and crucialbuilding blocks of the DeFi ecosystem. Their importanceprompts the emergence of studies covering various aspectsAMM-based DEX: economics [2], security [3]–[5], privacy[6], [7], etc. While there has arisen a large number of surveyson general DeFi [8], [9] as well as various DeFi applications[10], [11], there is a dearth of literature that systematicallystudies and critically examines DEX with AMM protocols ina comprehensive manner. To the best of our knowledge, thispaper fills this missing gap as the first SoK on AMM-basedDEX with examples of deployed protocols. We contribute tothe body of literature mainly by:

1) generalizing mechanisms and economics of AMM-basedDEX with a formalized state space modeling framework;

2) illustrating instantiations of our framework by comparingmajor AMM-based DEX with mathematical derivationand parameterized visualization on their conservationfunction, slippage and divergence loss functions;

3) positioning AMM-based DEX within the broader tax-onomy of DeFi, and examining their relationships andinteractions with other DeFi protocols;

4) establishing a taxonomy of security and privacy issuesconcerning AMM-based DEX, and exploring mitigationsolutions;

5) conducting a state-of-the-art literature review summariz-

arX

iv:2

103.

1273

2v5

[q-

fin.

TR

] 1

4 Ja

n 20

22

2

ing current research priorities as well as existing outputin AMM-based DEX and related fields, and identifyingpotential directions for future research.

The rest of the paper is structured as follows: in Section IIwe lay out fundamental concepts and components of AMMs;in Section III we formalize AMM mechanisms with a state-space representation; in Section IV we compare main protocolsin terms of conservation function, exchange rates, slippageand impermanent loss; in Section V we address issues relatedto security and privacy of AMM-based DEX; in Section VIwe indicate several avenues of future AMM research; inSection VII we present related work; in Section VIII weconclude.

II. AMM PRELIMINARIES

This section presents AMMs-based DEX’s main compo-nents, including different actors and assets, as well as theirgeneralized mechanism and economics.

A. Actors

1) Liquidity provider: A liquidity pool can be deployedthrough a smart contract with some initial supply of cryptoassets by the first LP. Other LPs can subsequently increasethe pool’s reserve by adding more of the type of assets thatare contained in the pool. In turn, they receive pool sharesproportionate to their liquidity contribution as a fraction of theentire pool [12]. LPs earn transaction fees paid by exchangeusers. While sometimes subject to a withdrawal penalty, LPscan freely remove funds from the pool [13] by surrendering acorresponding amount of pool shares [12].

2) Exchange user (Trader): A trader submits an exchangeorder to a liquidity pool by specifying the input and outputasset and either an input asset or output asset quantity; thesmart contract automatically calculates the exchange rate basedon the conservation function as well as the transaction fee andexecutes the exchange order accordingly.

Arbitrageurs compare asset prices across different marketsto execute trades whenever closing price gaps can extractprofits. AMMs such as DODO (see IV-A5) leverage on users’arbitrage behavior through their protocol design.

3) Protocol foundation: A protocol foundation consists ofprotocol founders, designers, and developers responsible forarchitecting and improving the protocol. The development ac-tivities are often funded directly or indirectly through accruedearnings such that the foundation members are financiallyincentivized to build a user-friendly protocol that can attracthigh trading volume.

B. Assets

Several distinct types of assets are used in AMM protocolsfor operations and governance; one asset may assume multipleroles.

1) Risk assets: Characterized by illiquidity, risk assets arethe primary type of assets AMM-based DEX are designedfor. Like centralized exchanges, an AMM-based DEX canfacilitate an initial exchange offering (IEO) to launch a newtoken through liquidity pool creation, a capital raising activitytermed “initial DEX offering (IDO)” that is particularly suit-able for illiquid assets. To be eligible for an IDO, a risk assetsometimes needs to be whitelisted, and must be compatiblewith the protocol’s technical requirements (e.g. ERC20 [14]for most AMMs on Ethereum).

2) Base assets: Some protocols require a trading pairalways to consist of a risk asset and a designated base asset.In the case of Bancor, every risk asset is paired with BNT,the protocol’s native token [15]. Uniswap V1 requires everypool to be initiated with a risk asset paired with ETH. Manyprotocols, such as Balancer and Curve, can connect two ormore risk assets directly in liquidity pools without a designatedbase asset.

3) Pool shares: Also known as “liquidity shares” and “LPshares”, pool shares represent ownership in the portfolio ofassets within a pool, and are distributed to LPs. Shares accruetrading fees proportionally and can be redeemed at any timeto withdraw funds from the pool.

4) Protocol tokens: Protocol tokens are used to representvoting rights on protocol governance matters and are thus alsotermed “governance tokens” (see II-D1c). Protocol tokens aretypically valuable assets that are tradeable outside of the AMMand can incentivize participation when e.g. rewarded to LPsproportionate to their liquidity supply. AMMs compete witheach other to attract funds and trading volume. To bootstrapan AMM in the early phase with incentivized early poolestablishment and trading, a feature called liquidity miningcan be installed where the native protocol’s tokens are mintedand issued to LPs and/or exchange users.

C. Fundamental AMM dynamics

1) Invariant properties: The functionality of an AMMdepends upon a conservation function which encodes a desiredinvariant property of the system. As an intuitive example,Uniswap’s constant product function determines trading dy-namics between assets in the pool as it always conservesthe product of value-weighted quantities of both assets inthe protocol—each trade has to be made in a way such thatthe value removed in one asset equals the value added inthe other asset. This weight-preserving characteristic is onedesired invariant property supported by the design of Uniswap.

2) Mechanisms: An AMM typically involves two types ofinteraction mechanism: asset swapping of assets and liquidityprovision/withdrawal. Interaction mechanisms have to be spec-ified in a way such that desired invariant properties are upheld;therefore the class of admissible mechanisms is restricted tothe ones which respect the defined conservation function, ifone is specified, or conserve the defined properties otherwise.

D. Fundamental AMM economics

1) Rewards: AMM protocols often run several rewardschemes, including liquidity reward, staking reward, gover-

3

nance rights and security reward distributed to different actorsto encourage participation and contribution.

a) Liquidity reward: LPs are rewarded for supplyingassets to a liquidity pool, as they have to bear the opportunitycosts associated with funds being locked in the pool. LPsreceive their share of trading fees paid by exchange users.

b) Staking reward: On top of the liquidity reward in theform of transaction income, LPs are offered the possibilityto stake pool shares or other tokens as part of an initialincentive program from a certain token protocol. The ultimategoal of the individual token protocols (see e.g. GIV [16] andTRIPS [17]) is to further encourage token holding, whilesimultaneously facilitating token liquidity on exchanges andproduct usage. These staking rewards are given by protocolsother than the AMM.

c) Governance right: An AMM may encourage liquidityprovision and/or swapping by rewarding participants gov-ernance rights in the form of protocol tokens (see II-B4).Currently, governance issues such as protocol treasury man-agement [18] are proposed and discussed mostly on off-chaingovernance portals such as snapshot1, Tally2 and Boardroom3,where protocol tokens are used as ballots (see II-B4) to voteon proposals.

d) Security reward: Just as every protocol built on top ofan open, distributed network, AMM-based DEX on Ethereumsuffer from security vulnerabilities. Besides code auditing,a common practice that a protocol foundation adopts is tohave the code vetted by a broader developer community andreward those who discover and/or fix bugs of the protocolwith monetary prizes, commonly in fiat currencies, through abounty program [19].

2) Explicit costs: Interacting with AMM protocols incursvarious costs, including charges for some form of “value”created or “service” performed and fees for interacting withthe blockchain network. AMM participants need to anticipatethree types of fees: liquidity withdrawal penalty, swap fee andgas fee.

a) Liquidity withdrawal penalty: As introduced in Sec-tion III-B and further discussed in Section IV of this paper,withdrawal of liquidity changes the shape of the conservationfunction and negatively affects the usability of the pool byelevating slippage. Therefore, AMMs such as DODO [20] levya liquidity withdrawal penalty.

b) Swap fee: Users interacting with the liquidity poolfor token exchanges have to reimburse LPs for the supplyof assets and for the divergence loss (see II-D3b). Thiscompensation comes in the form of swap fees that are chargedin every exchange trade and then distributed to liquidity poolshareholders. A small percentage of the swap fees may also goto the foundation of the AMM to further develop the protocol.

c) Gas fee: Every interaction with the protocol is exe-cuted in the form of an on-chain transaction, and is thus subjectto a gas fee applicable to all transactions on the underlyingblockchain. In a decentralized network, validating nodes needto be compensated for their efforts, and transaction initiators

1https://snapshot.org/.2https://www.withtally.com/.3https://app.boardroom.info/.

must cover these operating costs. Interacting with more com-plex protocols results in a higher gas fee due to the highercomputational power needed for transaction verification.

3) Implicit costs: Two essential implicit costs native toAMM-based DEX are slippage for exchange users and di-vergence loss for LPs.

a) Slippage: Slippage is defined as the difference be-tween the spot price and the realized price of a trade. Insteadof matching buy and sell orders, AMMs determine exchangerates on a continuous curve, and every trade will encounterslippage conditioned upon the trade size relative to the poolsize and the exact design of the conservation function. Thespot price approaches the realized price for infinitesimallysmall trades, but they deviate more for bigger trade sizes. Thiseffect is amplified for smaller liquidity pools as every tradewill significantly impact the relative quantities of assets in thepool, leading to higher slippage. Due to continuous slippage,trades on AMMs must be set with some slippage tolerance tobe executed, a feature that can be exploited to perform e.g.sandwich attacks (see V-A3).

b) Divergence loss: For LPs, assets supplied to a proto-col are still exposed to volatility risk, which comes into playin addition to the loss of time value of locked funds. A swapalters the asset composition of a pool, which automaticallyupdates the asset prices implied by the conservation functionof the pool (Equation 3). This consequently changes the valueof the entire pool. Compared to holding the assets outsideof an AMM pool, contributing the same amount of assets tothe pool in return for pool shares can result in less valuewith price movement, an effect termed “divergence loss” or“impermanent loss” (see Section IV). This loss can be deemed“impermanent” because as asset price moves back and forth,the depreciation of the pool value continuously disappears andreappears and is only realized when assets are actually takenout of the pool. Well-devised AMMs charge appropriate swapfees to ensure that LPs are sufficiently compensated for thedivergence loss (see IV-C2).

Despite the fact that “impermanent loss” is a more widelyused term on the Internet, we adhere to the more accurateterm “divergence loss” in a scientific context. In fact, for themajority of AMM protocols, this “loss” only disappears whenthe current proportions of the pool assets equal exactly thoseat liquidity provision, which is rarely the case.

Since assets are bonded together in a pool, changes in pricesof one asset affect all others in this pool. For an AMM protocolthat supports single-asset supply, this forces LPs to be exposedto risk assets they have not been holding in the first place.

E. AMM-based DEX within DeFi

For brevity, we use “AMM” or “DEX” to refer to AMM-based DEX throughout the paper, unless indicated otherwise.Nevertheless, it is to be noted that the term “AMM” empha-sizes the algorithm of a protocol, whereas “DEX” emphasizesthe use case, or application, of a protocol. Within the contextof blockchain-based DeFi, there also exist orderbook-basedDEX such as Gnosis and dYdX that do not rely on AMMalgorithms. On the other hand, AMM algorithms are also

4

DeFi on Blockchain

AMM

Prediction marketDEX

Constant product

Lending platform

Constant summStable

DODO

BalancerUniswap

CurveProvidepriceoracle

Stablecoin

Augur

Gyroscope

Bancor

Derivative

Pods finance

NFTEulerBeats

OrderbookGnosis dYdX

Sushiswap

Constant power sum

YieldSpaceCompound

Aave

Constant functionLMSR

Application Algorithm Italic Protocol name

Figure 1: AMM-based DEX within the broader taxonomy ofDeFi on blockchain. AMM as an algorithm and DEX as anapplication are not mutually inclusive.

not exclusively employed by DEX. DeFi applications suchas lending platforms, non-fungible tokens (NFTs), stablecoinsand derivatives all have protocols that make use of differentAMM algorithms.

AMMs can also assume various forms (see VII-B2). Pre-diction markets for example commonly employs logarithmicmarket scoring rule (LMSR), whereas constant function mar-ket maker (CFMM) is the primary underpinning for DEX. Inparticular, constant sum and constant product are the mostrepresentative forms of CFMM, widely adopted by AMM-based DEX protocols. Figure 1 illustrates AMM-based DEXwithin the broader taxonomy of DeFi on blockchain.

The ensuing sections, III and IV, focus on CFMM mech-anisms which have been adopted by major DEX, with theirexact formulas derived in Appendix A. Appendix IV-D brieflypresents other DeFi applications with AMM implementations.

III. FORMALIZATION OF MECHANISMS

Overall, the functionality of an AMM can be generalizedformally by a set of few mechanisms. These mechanismsdefine how users can interact with the protocol and what theresponse of the protocol will be given particular user actions.

A. State space representation

The functioning of any blockchain-based system can bemodeled using state-space terminology. States and agentsconstitute the main system components; protocol activities aredescribed as actions (Figure 2); the evolution of the systemover time is modelled with state transition functions. This canbe generalized into a state transition function f encoded in theprotocol such that χ a−→

fχ′, where a ∈ A represents an action

imposed on the system while χ and χ′ represent the currentand future states of the system respectively.

Liquidity ProviderPool of AMM-based DEX

DEPOSIT action

Input: 10 Token A + 1 Token B Output: 4 LP Shares

Reserves Token A: 90 → 100 Token B: 9 → 10

Liquidity Shares Pool Tokens: 36 → 40

Claim LP Shares

Add Liquidity

Amount Token A

Amou

nt T

oken

B

Trader

SWAP action

Input: 90 Token A Output: 90 Token B

Token B Token A

(90, 9)

(100, 10)Liquidity Addition

Liquidity Withdrawal

Amount Token A

Amou

nt T

oken

B

(100, 10)

Sell Token B / Buy Token A

Buy Token B/ Sell Token A

(10, 100)

Liquidity ProviderPool of AMM-based DEX

WITHDRAW action

Input: 4 LP Shares Output: 10 Token A + 1 Token B

Reserves Token A: 100 → 90 Token B: 10 → 9

Liquidity Shares Pool Tokens: 40 → 36

Token SurrenderLP Shares

Pool of AMM-based DEX

Reserves Token A: 10 → 100 Token B: 100 → 10

Liquidity Shares

Pool Tokens: 40

Trader

SWAP action

Input: 90 Token B Output: 90 Token A

Token A Token B

Pool of AMM-based DEX

Reserves Token A: 10 → 100 Token B: 100 → 10

Liquidity Shares

Pool Tokens: 40

(a) Liquidity provision and withdrawal.

Liquidity ProviderPool of AMM-based DEX

DEPOSIT action

Input: 10 Token A + 1 Token B Output: 4 LP Shares

Reserves Token A: 90 → 100 Token B: 9 → 10

Liquidity Shares Pool Tokens: 36 → 40

Claim LP Shares

Add Liquidity

Amount Token A

Amou

nt T

oken

B

Trader

SWAP action

Input: 90 Token A Output: 90 Token B

Token B Token A

(90, 9)

(100, 10)Liquidity Addition

Liquidity Withdrawal

Amount Token A

Amou

nt T

oken

B

(100, 10)

Sell Token B / Buy Token A

Buy Token B/ Sell Token A

(10, 100)

Liquidity ProviderPool of AMM-based DEX

WITHDRAW action

Input: 4 LP Shares Output: 10 Token A + 1 Token B

Reserves Token A: 100 → 90 Token B: 10 → 9

Liquidity Shares Pool Tokens: 40 → 36

Token SurrenderLP Shares

Pool of AMM-based DEX

Reserves Token A: 10 → 100 Token B: 100 → 10

Liquidity Shares

Pool Tokens: 40

Trader

SWAP action

Input: 90 Token B Output: 90 Token A

Token A Token B

Pool of AMM-based DEX

Reserves Token A: 10 → 100 Token B: 100 → 10

Liquidity Shares

Pool Tokens: 40

(b) Token exchange.

Figure 2: Stylized AMM mechanisms for liquidity providersand traders.

The object of interest is the state χ of the liquidity poolwhich can be described with

χ = (rkk=1,...,n, pkk=1,...,n, C,Ω) (1)

where rk denotes the quantity of token k in the pool, pkthe current spot price of token k, C the conservation functioninvariant(s), and Ω the collection of protocol hyperparameters.This formalization can encompass various AMM designs.

The most critical design component of an AMM is itsconservation function which defines the relationship betweendifferent state variables and the invariant(s) C. The conser-vation function is protocol-specific as each protocol seeks toprioritize a distinct feature and target particular functionalities(see Section IV).

The core of an AMM system state is the quantity of eachasset held in a liquidity pool. Their sums or products aretypical candidates for invariants. Examples of a constant-sum market maker include mStable [21]. Uniswap [22] rep-resents constant-product market makers, while Balancer [13]generalizes this idea to a geometric mean. The Curve [23]conservation function is notably a combination of constant-sum and constant-product (see Section IV).

5

B. Liquidity change and asset swap

Hyperparameter set Ω is determined at pool creation andshall remain the same afterwards. While this value of hy-perparameters might be changed through protocol governanceactivities, this does not and should not occur on a frequentbasis.

Invariant C, despite its name, refers to the pool variable thatstays constant only with swap actions but changes at liquidityprovision and withdrawal. In contrast, trading moves the priceof traded assets; specifically, it increases the price of the outputasset relative to the input asset, reflecting a value appreciationof the output asset driven by demand. Liquidity provision andwithdrawal, on the other hand, should not move the asset price.In particular, a pure liquidity provision and withdrawal activityrequires a proportional change in reserves (Equation (2)).

General rules of AMM-based DEX1) The price of assets in an AMM pool stays constant for

pure liquidity provision and withdrawal activities.2) The invariant of an AMM pool stays constant for pure

swapping activities.

Formally, the state transition induced by pure liquiditychange and asset swap can be expressed as follows.

(rkk=1,...,n, pkk=1,...,n, C,Ω)liquidity change−−−−−−→

f

(a · rkk=1,...,n, pkk=1,...,n, C′,Ω), where a > 0 (2)

(rkk=1,...,n, pkk=1,...,n, C,Ω)swap−−→f

(r′kk=1,...,n, p′kk=1,...,n, C,Ω) (3)

Note that protocol-specific intricacies may result in asset pricechange with liquidity provision/withdrawal, or invariant Cupdate with trading. This is a consequence of what is describedin Section II-C regarding each mechanism having to respectimposed system invariances.

The asset spot price can remain the same only when assetsare added to or removed from a pool proportionate to thecurrent reserve ratio (r1 : r2 : ... : rn). In any other case, achange of quantities in any pool would result in changes inrelative prices of assets. To manage to uphold the invariancesa disproportionate addition or removal can be treated as acombination of two actions: proportionate reserve change plusasset swap, such as with Balancer [13]. When only one asset isprovided instead of e.g. eight, the protocol would first executeseven trades to swap this one asset to arrive at a vector ofquantities in current proportions and next add this vector tothe liquidity pool. In other words, adding only one asset tothe liquidity pool is not an eligible state transition and has tobe treated accordingly. Consequently, this sequence of actionsis no longer a pure liquidity provision/withdrawal and wouldthus move the asset spot price.

Swap fees (see II-D2b) also cause invariant C to becomevariant through trading. Specifically, when swap fees are keptwithin the liquidity pool, a trading action can be decomposedinto asset swap and liquidity provision. This action is, there-fore, no longer a pure asset swap and would thus move the

Table I: Mathematical notations for pool mechanisms

Notation Definition Applicable protocols

Preset hyperparameters, Ωwk Weight of asset reserve rk BalancerA Slippage controller Uniswap V3, Curve, DODO

State variablesC or (C1, C2) Conservation function invariant(s) allrk Quantity of tokenk in the pool allpk Current spot price of tokenk all

Process variablesxi Input quantity added to tokeni re-

serve (removed if xi < 0)all

xo Output quantity removed fromtokeno reserve (added if xo < 0)

all

ρ Token value change all

FunctionsC Conservation function allZ Implied conservation function alliEo tokeno price in terms of tokeni allS Slippage allV Reserve value allL Divergence loss Uniswap, Balancer, Curve

value of C (see e.g. [24]). Also, as float numbers are not yetfully supported by Solidity [25]—the language for Ethereumsmart contracts, AMM protocols typically recalculate invariantC after each trade to avoid the accumulation of rounding errors.

C. Generalized formulas

In this section, we generalize AMM formulas necessaryfor demonstrating the interdependence between various AMMstate variables, as well as for computing slippage and diver-gence loss. Mathematical notations and their definitions canbe found in Table I.

1) Conservation function: An AMM conservation function,also termed “bonding curve”, can be expressed explicitly asa relational function between AMM invariant and reservequantities rkk=1,...,n:

C = C(rk) (4)

A conservation function for each token pair, say ri—ro,must be concave, nonnegative and nondecreasing [26] (seealso Figure 3). For complex AMMs such as Curve, it might beconvenient to express the conservation function (Equation 4)implicitly in order to derive exchange rates between two assetsin a pool:

Z(rk; C) = C(rk)− C = 0 (5)

Equation 5 contains a constant C, whose value is determinedby the initial liquidity provision (liquidity pool creation);afterwards, given the change in reserve quantity of one asset,the reserve quantity of the other asset can be solved.

2) Spot exchange rate: The spot exchange rate betweentokeni and tokeno can be calculated as the slope of the ri—rocurve (see examples in Figure 3) using partial derivatives ofthe conservation function Z.

iEo(rk; C) =∂Z(rk; C)/∂ro∂Z(rk; C)/∂ri

(6)

Note that iEo = 1 when i = o.

6

3) Swap amount: The amount of tokeno received xo (spentwhen xo < 0) given amount of tokeni spent xi (received whenxi < 0) can be calculated following the steps below.

Note that xi > −ri and xo > −ro. Their lower boundcorresponds to the case when the received asset is depletedfrom the pool, i.e. its new reserve becomes 0 (see alsoEquation 7 below). With common AMM protocols, xi, xotheoretically often do not have a upper bound: if the reservequantity is 1 unit, a trader can still sell 2 or more units intothe pool, but mostly accompanied with a high slippage (seeFigure 4 in the next section).

a) Update reserve quantities: Input quantity xi is simplyadded to the existing reserve of tokeni; the reserve quantityof any token other than tokeni or tokeno stays the same:

r′i := Ri(xi; ri) = ri + xi (7)r′j = rj , ∀j 6= i, o (8)

b) Compute new reserve quantity of tokeno: The newreserve quantity of all tokens except for tokeno is known fromthe previous step. One can thus solve r′o, the unknown quantityof tokeno, by plugging it in the conservation function:

Z(r′k; C) = 0 (9)

Apparently, r′o can be expressed as a function of the originalreserve composition rk, input quantity xi, namely,

r′o := Ro(xi, rk; C) (10)

c) Compute swapped quantity: The quantity of tokenoswapped is simply the difference between the old and newreserve quantities:

xo := Xo(xi, rk; C) = ro − r′o (11)

4) Slippage: Slippage measures the deviation between ef-fective exchange rate xi

xoand the pre-swap spot exchange rate

iEo, expressed as:

S(xi, rk; C) =xi/xo

iEo− 1 (12)

5) Divergence loss: Divergence loss describes the loss invalue of all reserves in the pool compared to holding thereserves outside of the pool, after a price change of an asset(see II-D3b). Based on the formulas for spot price and swapquantity established above, the divergence loss can generallybe computed following the steps described below. In thevaluation, we assign tokeni as the denominating currency forall valuations. While the method to be presented can be usedfor multiple token price changes through iterations, we onlydemonstrate the case where only the value of tokeno increasesby ρ, while all other tokens’ value stay the same. Tokeni isthe numeraire. Designating one of the tokens in the pool as anumeraire can also be found in DeFi simulation papers suchas [26].

a) Calculate the original pool value: The value of thepool denominated in tokeni can be calculated as the sum ofthe value of all token reserves in the pool, each equal to thereserve quantity multiplied by the exchange rate with tokeni:

V (rk; C) =∑j

iEj(rk; C) · rj (13)

Table II: Comparison table of discussed DEX: value locked,trade volume of the past 7 days, the market share by the last 30days volume, the governance token, the number of governancetoken holders and the fully diluted value, as on 21 September2021. Data retrieved from DeFi Pulse and Dune Analytics.

Protocol Value Trade Market Governance Governance Fully dilutedlocked ($bn) volume ($bn) (%) token token holders value ($bn)

Uniswap 6.15 11.4 66.7 UNI 269,923 21.1Sushiswap 3.92 2.9 14.2 SUSHI 71,007 2.4Curve 11.64 1.5 6.4 CRV 44,654 4.0Bancor 1.37 0.4 2.5 BNT 38,124 0.8Balancer 1.74 0.5 2.2 BAL 37,613 1.0DODO 0.07 0.4 2.1 DODO 11,330 1.2

b) Calculate the reserve value if held outside of the pool:If all the asset reserves are held outside of the pool, then achange of ρ in tokeno’s value would result in a change of ρin tokeno reserve’s value:

Vheld(ρ; rk, C) = V (rk; C) + [jEo(rk; C) · ro] · ρ

c) Obtain re-balanced reserve quantities: Exchangeusers and arbitrageurs constantly re-balance the pool throughtrading in relatively “cheap”, depreciating tokens for rela-tively “expensive”, appreciating ones. As such, asset valuemovements are reflected in exchange rate changes implied bythe dynamic pool composition. Therefore, the exchange ratebetween tokeno and each other tokenj (j 6= o) implied bynew reserve quantities r′k, compared to that by the originalquantities rk, can be expressed with Equation set 14. Atthe same time, the equation for the conservation function muststand (Equation 15).

ρ =jEo(r′k; C)jEo(rk; C)

− 1, ∀j 6= o (14)

0 = Z(r′k; C) (15)

A total number of n-equations (n − 1 with Equation set 14,plus 1 with Equation 15) would suffice to solve n unknownvariables r′kk=1,...,n, each of which can be expressed as afunction of ρ and rk:

r′k := Rk(ρ, rk; C) (16)

d) Calculate the new pool value: The new value of thepool can be calculated by summing the products of the newreserve quantity multiplied by the new price (denominated bytokeni) of each token in the pool:

V ′(ρ, rk; C) =∑j

iEj(r′k; C) · r′j (17)

e) Calculate the divergence loss: Divergence loss can beexpressed as a function of ρ, the change in value of an assetin the pool:

L(ρ, rk; C) =V ′(ρ, rk; C)Vheld(ρ; rk, C)

− 1 (18)

7

Table III: Overview of major existing AMM-based DEX on Ethereum, Solana, Polkadot, Tezos, EOS, Polygon and BinanceSmart Chain (BSC). CS: Constant sum, CP: Constant product, OP: Oracle price component, CC: Capital concentration, T:Time component.

AMM AMM add-ons

DEX Pool structure CP CS OP CC T Divergence loss compensation Chain Mainnet launch

Uniswap V1 [27] asset-pair # # # # — Ethereum 11/2018Uniswap V2 [28] asset-pair # # # # — Ethereum 05/2020Uniswap V3 [29] asset-pair # # # — Ethereum 05/2021Balancer V1 [13] multi-asset # # # — Ethereum 03/2020Balancer V2 [30] multi-asset # # # — Ethereum —Curve [23] multi-asset # # # — Ethereum 01/2020DODO [20] various # # # — Ethereum, BSC 09/2020Bancor V1 [31] asset-pair # # # # — Ethereum, EOS 06/2017Bancor V2 [32] asset-pair # # # — Ethereum, EOS 04/2020Bancor V2.1 [15] asset-pair # # # # Divergence loss insurance Ethereum, EOS 10/2020SushiSwap [33] asset-pair # # # # — Ethereum 08/2020Mooniswap [34] asset-pair # # # — Ethereum 08/2020mStable [21] asset-pair # # # # — Ethereum 07/2020Kyber 3.0 [35] multi-asset # # # Dynamic swap fee Ethereum, Tezos 03/2021Saber [36] multi-asset # # # — Solana 06/2021HydraDX [37] multi-asset # # — Polkadot —Uranium Finance [38] asset-pair # # # # — BSC 05/2021QuickSwap [39] asset-pair # # # # — Ethereum, Polygon 10/2020Burgerswap [40] asset-pair # # # # — BSC 10/2020

IV. COMPARISON OF AMM PROTOCOLS

AMM-based DEX are home to billions of dollars’ worth ofon-chain liquidity. Table II lists major AMM protocols, theirrespective value locked, as well as some other general metrics.Uniswap is undeniably the biggest AMM measured by tradevolume and the number of governance token holders, althoughit is remarkable that Curve has more value locked within theprotocol. The number of governance token holders of smallerprotocols as Bancor and Balancer is relatively high comparedto CRV token holders, as they do approximately a third of thevolume but have only slightly fewer governance token holders.

A. Major AMM protocols

This section focuses on the four most representative AMMs:Uniswap (including V2 and V3), Balancer, Curve, and DODO.These protocols were selected based on their market share [41]on the Ethereum blockchain and the representativeness in theiroverall mechanism.

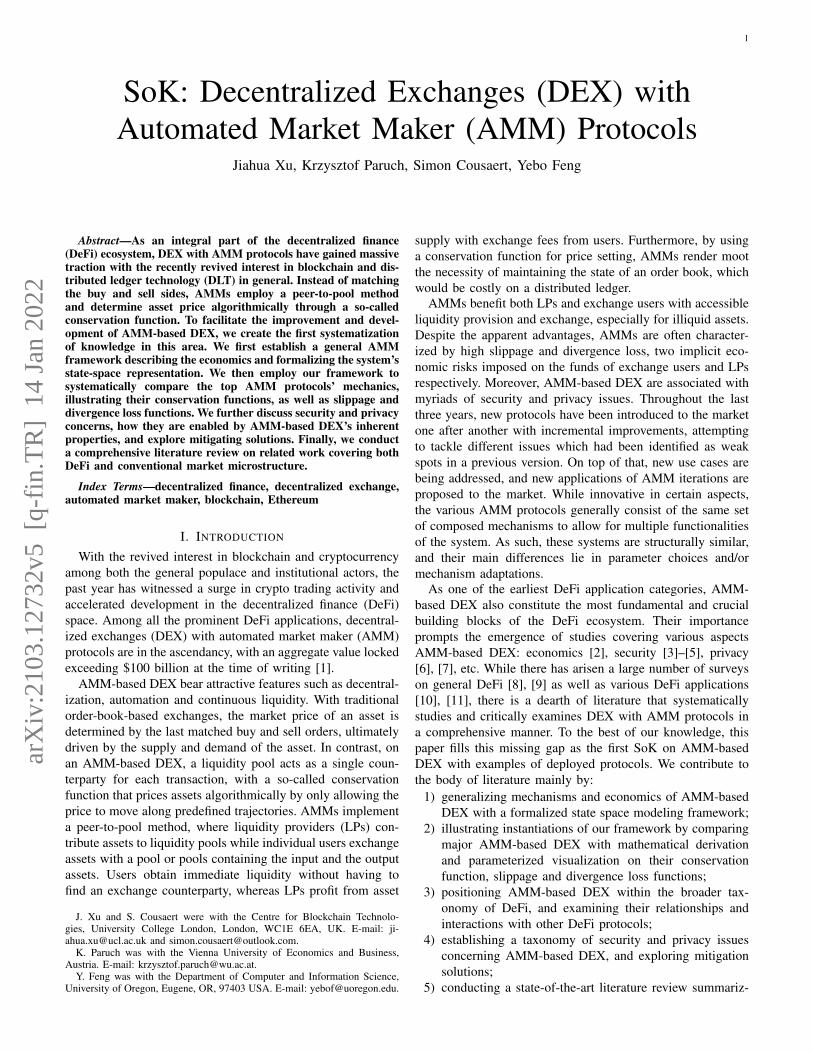

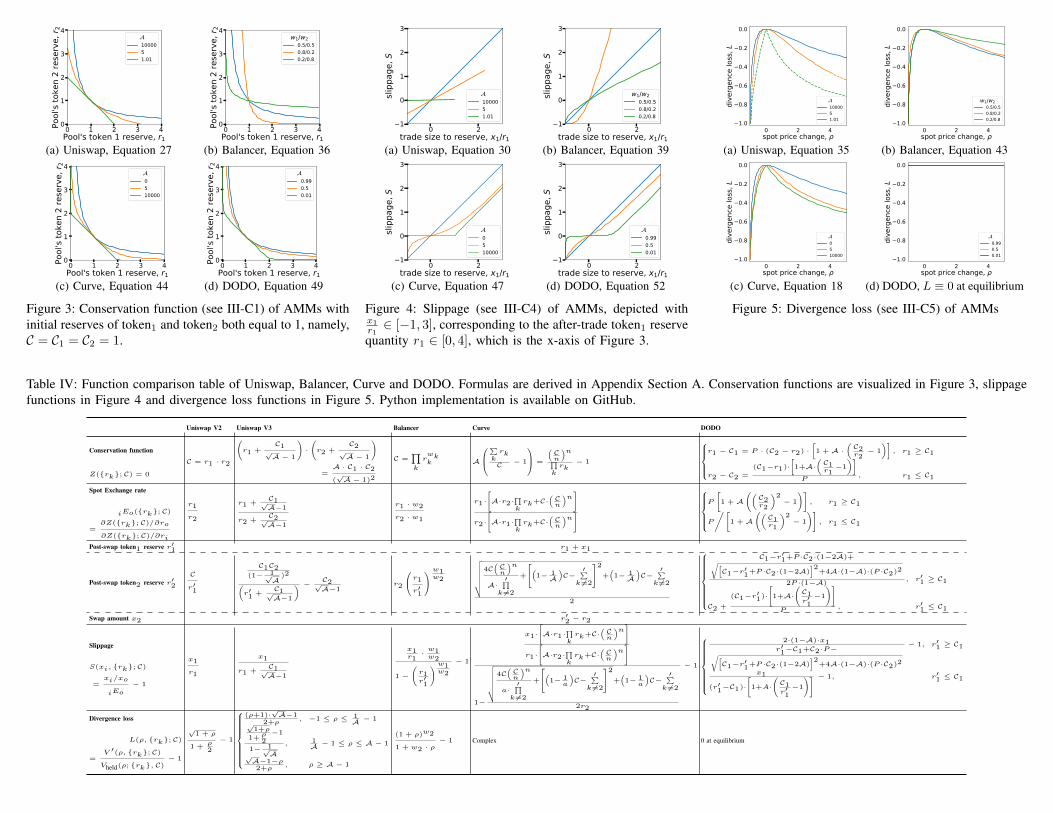

We describe the liquidity pool structures of those protocolsin the main text. We also derive the conservation function,slippage, as well as divergence loss of those protocols. Asummary of formulas can be found in Table IV. We referour readers to Appendix A for a detailed explanation andderivation of those formulas. The protocols’ conservationfunction, slippage, as well as divergence loss under differenthyperparameter values are plotted in Figure 3, Figure 4 andFigure 5, respectively. We always use token1 as price or valueunit; namely, token1 is the assumed numeraire.

1) Uniswap V2: The Uniswap protocol prescribes that aliquidity pool always consists of one pair of assets. The pool’ssmart contract always assumes that the reserves of the twoassets have equal value. Uniswap implements a conservationfunction with a constant-product invariant.

2) Uniswap V3: Uniswap V3 enhances Uniswap V2 byallowing liquidity provision to be concentrated on a fractionof the bonding curve [29] (see A2a), thus virtually amplifyingthe conservation function invariant and reducing the slippage.

The slippage controller A determines the degree of liquidityconcentration. Specifically, A signifies how concentrated theliquidity should be provided around the initial spot price: whenA → ∞, the covered price range approaches (0,∞), and theLP’s individual conservation function approximates a UniswapV2 one (A = 10000 in Figure 3a); on the other extreme, whenA → 1, the liquidity only supports swaps close to the initialexchange rate, and the conservation function approximates aconstant-sum one (Figure 3a).

3) Balancer: The Balancer protocol allows each liquiditypool to have more than two assets [13]. Each asset reserve rkis assigned a weight wk at pool creation, where

∑k

wk = 1.

Weights are pool hyperparameters and do not change witheither liquidity provision/removal or asset swap. The weightof an asset reserve represents the value of the reserve as afraction of the pool value. Balancer can also be deemed ageneralization of Uniswap; the latter is a special case of theformer with w1 = w2 = 1

2 (Figure 3b).4) Curve: With the Curve protocol, formerly StableSwap

[23], a liquidity pool consists of two or more assets withthe same peg, for example, USDC and DAI, or wBTC andrenBTC. Curve approximates Uniswap V2 when its constant-sum component has a near-0 weight, i.e. A → 0 (Figure 3c).

5) DODO: DODO supports customized pools [42] wherea pool creator provides reserves on both sides of the tradingpair with arbitrary quantities, which determines the pool’sinitial equilibrium state. Unlike conventional AMMs suchas Uniswap, Balancer and Curve where the exchange ratebetween two assets in a pool is derived purely from theconservation function, DODO does it the other way around.Resorting to external market data as a major determinant of

8

the exchange rate, DODO has its conservation function (seeA5b) derived from its exchange rate formula (see A5a).

Specifically, the pool exhibits an arbitrage opportunity—namely a gap between the price offered by the pool and thatfrom the external market—as soon as the reserve ratio betweenthe two assets in the pool deviates from its equilibrium state.Price alignment by arbitrageurs always pulls the reserve ratioback to its equilibrium state set by the LP, thus eliminatingany divergence loss. Due to this feature, DODO differentiatesitself from other AMMs and terms their pricing algorithm as“proactive market maker”, or PMM.

In DODO, a higher slippage controller A ∈ (0, 1) resultsin a greater slippage around the market price—i.e. the equi-librium price. Specifically, when A → 1, the DODO bondingcurve resembles Uniswap V2 (A = 0.99 in Figure 3d); andwith a high slippage around the market price (Figure 4d), thepool exhibits a strong tendency to fall back to the equilibriumstate. When A → 0, the DODO bonding curve resembles aconstant sum one (A = 0.01 in Figure 3d); and with a near-flatslippage (Figure 4d), the algorithm’s force to pull the reserveratio back to equilibrium is at its weakest due to little arbitrageprofitability exhibited.

Summary: Each AMM has its quirks. Uniswap V2 imple-ments an rudimentary bonding curve that achieves a low gasfee; Uniswap V3 allows for concentrated liquidity provisionwhich improves capital efficiency; Balancer supports morethan 2 assets in a pool; Curve is suitable for swapping assetswith the same peg; DODO proactively reduces divergence lossby leveraging external price feeds.

Common AMMs can be predominantly seen as a general-ization, or an extension, of the most fundamental constant-product protocol that is applied by Uniswap V2. Whenhyperparameters such as reserve weights wk and slippagecontroller A are assigned with certain values, different AMMscan be reduced to the basic form equivalent to Uniswap V2(illustrated with blue curves in Figures 3, 4 and 5).

In other cases, AMMs assume different forms with a trade-off between slippage and divergence loss. Indeed, an AMMwith low slippage is in favor of traders but to the detrimentof LPs: given a range of price movement, traders wouldbe able to exchange assets in higher volume, whereas LPswould suffer a higher divergence loss. Seemingly with thecapability to achieve both low slippage and zero divergenceloss at equilibrium (when A → 0), DODO appears to be anexception. Nevertheless, it is to be noted that with low A,DODO’s PMM algorithm is less effective in restoring the poolto its equilibrium state (see IV-A5), thus still exposing LPs todivergence loss risks in non-equilibrated states.

Ultimately, users interacting with an AMM-based DEX,including both traders and LPs, form a zero-sum game. Theyshould understand the protocol design, and beware of embed-ded hidden costs such as slippage and divergence loss, whichimpose economic risks on their funds.

B. Other AMM-based DEXs

1) Sushiswap: Sushiswap is a fork of Uniswap V2 (seeV-A3f). Though the two mainly differ in governance token

structure and user experience, Sushiswap share the sameconservation function, slippage and divergence loss functionsas Uniswap.

2) Kyber Network: Currently in its 3.0 version, the DEXuses a Dynamic Market Maker (DMM) mechanism, whichallows for dynamic conservation functions based on amplifiedbalances, called “virtual balances” [43]. This is supposed toresult in higher capital efficiency for LPs and better slippagefor traders. Also, the trading fees are adjusted automaticallyto market conditions. A volatile market causes increased fees,to offset impermanent loss for LPs.

3) Bancor: While Bancor’s white paper [31] gives theimpression that a different conservation function is applied, acloser inspection of their transaction history and smart contractleads to the conclusion that Bancor is using the same formulaas Balancer (confirmed by a developer in the Bancor Discordcommunity). As the majority of Bancor pools consist of twoassets, one of which is usually BNT, with the reserve weightsof 50%–50%, Bancor’s swap mechanism is equivalent toUniswap. Bancor V2.1 now allows single-sided asset exposure,and provides divergence loss insurance [32] (see IV-C3).

C. Additional AMM features

1) Time component: A time component refers to the abil-ity to change traditionally fixed hyperparameters over time.Balancer V1 and V2 implement this (Table III), by allowingliquidity pool creators to set a scheme that changes the weightsof two pool assets over time. This implementation is called aLiquidity Bootstrapping Pool (see IV-D4).

2) Dynamic swap fee: Dynamic fees are introduced byKyber 3.0 to reduce the impact of divergence loss for LPs.The idea is to increase swap fees in high-volume marketsand reduce them in low-volume markets. This should resultin more protection against divergence loss, as during periodsof sharp token price movements during a high-volume market,LPs absorb more fees. In low-volume and -volatility markets,trading is encouraged by lowering the fees.

3) Divergence loss insurance: Popularized by Bancor V2.1,LPs are insured against divergence loss after 100 days in thepool, with a 30-day cliff at the beginning. Bancor achievesthis by using an elastic BNT supply that allows the protocolto co-invest in pools and pay for the cost of impermanent losswith swap fees from its co-investments [44]. This insurancepolicy is earned over time, 1% each day that liquidity is stakedin the pool.

9

0 1 2 3 4Pool's token 1 reserve, r1

0

1

2

3

4

Pool

's to

ken

2 re

serv

e, r 2

1000051.01

(a) Uniswap, Equation 27

0 1 2 3 4Pool's token 1 reserve, r1

0

1

2

3

4

Pool

's to

ken

2 re

serv

e, r 2 w1/w2

0.5/0.50.8/0.20.2/0.8

(b) Balancer, Equation 36

0 1 2 3 4Pool's token 1 reserve, r1

0

1

2

3

4

Pool

's to

ken

2 re

serv

e, r 2

0510000

(c) Curve, Equation 44

0 1 2 3 4Pool's token 1 reserve, r1

0

1

2

3

4

Pool

's to

ken

2 re

serv

e, r 2

0.990.50.01

(d) DODO, Equation 49

Figure 3: Conservation function (see III-C1) of AMMs withinitial reserves of token1 and token2 both equal to 1, namely,C = C1 = C2 = 1.

0 2trade size to reserve, x1/r1

1

0

1

2

3

slipp

age,

S

1000051.01

(a) Uniswap, Equation 30

0 2trade size to reserve, x1/r1

1

0

1

2

3

slipp

age,

S

w1/w20.5/0.50.8/0.20.2/0.8

(b) Balancer, Equation 39

0 2trade size to reserve, x1/r1

1

0

1

2

3

slipp

age,

S

0510000

(c) Curve, Equation 47

0 2trade size to reserve, x1/r1

1

0

1

2

3

slipp

age,

S

0.990.50.01

(d) DODO, Equation 52

Figure 4: Slippage (see III-C4) of AMMs, depicted withx1

r1∈ [−1, 3], corresponding to the after-trade token1 reserve

quantity r1 ∈ [0, 4], which is the x-axis of Figure 3.

0 2 4spot price change,

1.0

0.8

0.6

0.4

0.2

0.0

dive

rgen

ce lo

ss, L

1000051.01

(a) Uniswap, Equation 35

0 2 4spot price change,

1.0

0.8

0.6

0.4

0.2

0.0

dive

rgen

ce lo

ss, L

w1/w20.5/0.50.8/0.20.2/0.8

(b) Balancer, Equation 43

0 2 4spot price change,

1.0

0.8

0.6

0.4

0.2

0.0

dive

rgen

ce lo

ss, L

0510000

(c) Curve, Equation 18

0 2 4spot price change,

1.0

0.8

0.6

0.4

0.2

0.0

dive

rgen

ce lo

ss, L

0.990.50.01

(d) DODO, L ≡ 0 at equilibrium

Figure 5: Divergence loss (see III-C5) of AMMs

Table IV: Function comparison table of Uniswap, Balancer, Curve and DODO. Formulas are derived in Appendix Section A. Conservation functions are visualized in Figure 3, slippagefunctions in Figure 4 and divergence loss functions in Figure 5. Python implementation is available on GitHub.

Uniswap V2 Uniswap V3 Balancer Curve DODO

Conservation function

Z(rk; C) = 0

C = r1 · r2

(r1 +

C1√A− 1

)·(r2 +

C2√A− 1

)

=A · C1 · C2(√A− 1)2

C =∏k

rwkk A

∑krk

C − 1

=

(Cn

)n∏krk− 1

r1 − C1 = P · (C2 − r2) ·

[1 +A ·

(C2r2− 1

)], r1 ≥ C1

r2 − C2 =

(C1−r1)·[1+A·

(C1r1−1

)]P

, r1 ≤ C1

Spot Exchange rate

iEo(rk; C)

=∂Z(rk; C)/∂ro

∂Z(rk; C)/∂ri

r1

r2

r1 +C1√A−1

r2 +C2√A−1

r1 · w2

r2 · w1

r1·[A·r2·

∏krk+C·

(Cn

)n]

r2·[A·r1·

∏krk+C·

(Cn

)n]P

[1 +A

((C2r2

)2− 1

)], r1 ≥ C1

P

/[1 +A

((C1r1

)2− 1

)], r1 ≤ C1

Post-swap token1 reserve r′1

Post-swap token2 reserve r′2

Swap amount x2

r1 + x1

C

r′1

C1C2(1− 1√

A)2(

r′1 +C1√A−1

) − C2√A−1

r2

r1r′1

w1w2

√√√√√√√4C(Cn

)nA·′∏

k 6=2

+

(1− 1A)C−

′∑k 6=2

2+(1− 1A)C−

′∑k 6=2

2

C1−r′1+P ·C2·(1−2A)+√[

C1−r′1+P ·C2·(1−2A)]2

+4A·(1−A)·(P ·C2)2

2P ·(1−A), r′1 ≥ C1

C2 +

(C1−r′1)·[1+A·

(C1r′1−1

)]P

, r′1 ≤ C1r′2 − r2

Slippage

S(xi, rk; C)

=xi/xo

iEo− 1

x1

r1

x1

r1 +C1√A−1

x1r1· w1w2

1 −(r1r′1

)w1w2

− 1

x1·[A·r1·

∏krk+C·

(Cn

)n]

r1·[A·r2·

∏krk+C·

(Cn

)n]

1−

√√√√√√√4C(Cn

)na·′∏

k 6=2

+

(1− 1a

)C−

′∑k 6=2

2+(1− 1

a

)C−

′∑k 6=2

2r2

− 1

2·(1−A)·x1r′1−C1+C2·P−√[

C1−r′1+P ·C2·(1−2A)]2

+4A·(1−A)·(P ·C2)2

− 1, r′1 ≥ C1

x1

(r′1−C1)·[1+A·

(C1r′1−1

)] − 1, r′1 ≤ C1

Divergence loss

L(ρ, rk; C)

=V ′(ρ, rk; C)

Vheld(ρ; rk, C)− 1

√1 + ρ

1 +ρ2

− 1

(ρ+1)·√A−1

2+ρ, −1 ≤ ρ ≤ 1

A − 1√

1+ρ

1+ρ2

−1

1− 1√A

, 1A − 1 ≤ ρ ≤ A− 1

√A−1−ρ2+ρ

, ρ ≥ A− 1

(1 + ρ)w2

1 + w2 · ρ− 1 Complex 0 at equilibrium

10

D. Other DeFi protocols with AMM implementationsAMMs form the basis of other DeFi applications (see

Figure 1) that implement existing or invent newly designedbonding curves, facilitating the functionalities of these imple-menting protocols. In this section, we present a few examplesof projects that use AMM designs under the hood.

1) Gyroscope: Gyroscope [45] is a stablecoin backed bya reserve portfolio that tries to diversify DeFi tail risks. GyroDollars can be minted for a price near $1 and can be redeemedfor an amount worth of near $1 in reserve assets, as determinedthrough a new AMM design that balances risk in the system.

Gyroscope includes a Primary-market AMM (P-AMM),through which Gyro Dollars are minted and redeemed, and aSecondary-market AMM (S-AMM) for Gyro Dollar trading.Similar to Uniswap V3, where a price range constraint isimposed. The P-AMM yields a mint quote and a redeem quotethat serves as a price range constraint for the S-AMM to decideupon concentrated liquidity ranges [46].

2) EulerBeats: EulerBeats [47] is a protocol that issueslimited edition sets of algorithmically generated art and music,based on the Euler number and Euler totient function. Theproject uses self-designed bonding curves to calculate burnprices of music/art prints, depending on the existing supply.The project thus implements a form of AMM to mint and burnNFTs price-efficiently.

3) Pods Finance: Pods [48] is a decentralized non-custodialoptions protocol that allows users to create calls and or putsand trade them in the Options AMM. Users can participateas sellers and buy puts and calls in a liquidity pool or actas LPs in such a pool. The specific AMM is one-sided andbuilt to facilitate an initially illiquid options market and priceoption algorithmically using the Black-Scholes pricing model.Users can effectively earn fees by providing liquidity, even ifthe options are out-of-the-money, reducing the cost of hedgingwith options.

4) Balancer Liquidity Bootstrapping Pool: Liquidity Boot-strapping Pools (LBPs) are pools where controllers can changethe parameters of the pool in controlled ways, unlike im-mutable pools described in section Section IV. The idea ofan LBP is to launch a token fairly, by setting up a two-tokenpool with a project token and a collateral token. The weightsare initially set heavily in favor of the project token, thengradually “flip” to favor the collateral coin by the end of thesale. The sale can be calibrated to keep the price more orless steady (maximizing revenue) or declining to the desiredminimum (e.g., the initial offering price) [49].

5) YieldSpace: The YieldSpace paper [50] introduces anautomated liquidity provision for fixed yield tokens. A formulacalled the “constant power sum invariant” incorporates timeto maturity as input and ensures that the liquidity provisionoffers a constant interest rate—rather than price—for a givenratio of its reserves. fyTokens are synthetic tokens that areredeemable for a target asset after a fixed maturity date [51].The price of a fyToken floats freely before maturity, and thatprice implies a particular interest rate for borrowing or lendingthat asset until the fyToken’s maturity. Standard AMMprotocols as discussed in Section IV are capital-inefficient. Byintroducing the concept of a constant power sum formula, the

writers want to build a liquidity provision formula that worksin “yield space” instead of “price space”.

6) Notional Finance: Notional Finance [52] is a protocolthat facilitates fixed-rate, fixed-term crypto-asset lending andborrowing. Fixed interest rates provide certainty and minimizerisk for market participants, making this an attractive protocolamong volatile asset prices and yields in DeFi. Each liquiditypool in Notional refers to a maturity, holding fCash tokensattached to that date. For example, fDai tokens represent afixed amount of DAI at a specific future date. The shape of theNotional AMM follows a logit curve, to prevent high slippagein normal trading conditions. Three variables parameterizethe AMM: the scalar, the anchor, and the liquidity fee [53].The first and second mentioned allowing for variation inthe steepness of the curve and its position in a xy-plane,respectively. By converting the scalar and liquidity fee to afunction of time to maturity, fees are not increasingly punitivewhen approaching maturity.

7) Gnosis Custom Market Maker (CMM): The GnosisCMM [54] allows users to set multiple limit orders at customprice brackets and passively provide liquidity on the GnosisProtocol. The mechanism used is similar to the Uniswap V3structure, although it allows for even more possibilities tomarket makers by allowing them to choose price upper andlower limits and a number of brackets within that price range.Uniswap V3 allows LPs to solely choose the upper and lowerlimits. Because users deposit funds to the assets at differentprice levels specifically, this specific application behaves morelike a central limit order book than an AMM pool.

E. AMMs on Layer 2 solutions

The growth and success of DeFi on Ethereum have puta strain on the Ethereum network’s ability to process trans-actions, leading to increasing gas [55]. As the EthereumNetwork becomes busier, user experience decreases becauseof increasing gas prices and decreasing transaction speed.Users aim to outbid each other by increasing the gas prices.Also, transaction speed decreases, which results in poor userexperience for certain types of decentralized applications(dApps). And as the network gets busier, gas prices increaseas transaction senders aim to outbid each other. In an attemptto prevent these consequences, “layer 2 solutions” (L2) arebeing developed. These solutions handle transactions outsideof the Ethereum network, but still rely on the decentralizedsecurity model of the mainnet [56]. Examples of layer 2technologies include Plasma, Sidechains, Optimistic Rollupsand ZK-Rollups. For a more comprehensive reading on thistopic, we direct the reader to [57]. Examples of Ethereum layer2 solutions are Polygon [58], Arbitrum [59], Optimism [60]and Starknet [61].

Characteristics of layer 2 solutions, such scaling and secu-rity, have been well-documented across different sources [62][63] [64] and are out of scope for this SoK. The advantagesand disadvantages of transacting on layer 2 solutions are notspecifically related to AMMs, but to all protocols on thesetechnologies. Therefore, we focus on the security issues anduser experience of interacting with AMMs on layer 2.

11

Implicit Economic RiskIn

fras

truc

ture

La

yer

Mid

dlew

are

Laye

rA

pplic

atio

n La

yer

Reentrancy AttackOthers

Block TS ManipulationTrans Seq Manipulation

Others

Smart Contract

3

Smart Contract

n...

AMM-based DEX

Malicious / Benign Nodes

Smart Contract 1, 2, 3

Smart Contract

1, 2

Attack

Call

Vampire Attack

Rug Pool Oracle Attack

Sandwich Attack Frontrunning Backrunning

Privacy Concern

Transaction Inspection Identity Tracing

Behavioral Model Infer

Enable

Slippage Divergence Loss

Lead to

Figure 6: Architectural layers of an AMM-based DEX with itsimplicit economic risks, attacks, privacy concerns, and theirrelationships

Daian et al. [?] note that abstraction achieved by layer 2exchange systems is not sufficient to prevent sandwich attacksand a report of Delphi Digital [65] concludes that there isstill front-running risk when a protocol wants to aggregateliquidity across layer 1 and layer 2 pools. The front-runningand sandwich attacks does not seem to be solved by layer 2solutions. [66] proposes a simple solution for front-runningattacks on Optimistic Rollups technology.

One of the most important advantages of deploying aprotocol on layer 2 is the reduction in gas fees. This dra-matically enhances the user experience, and opens up waysto introduce new forms of decentralized exchanges. Oneexample is ZKSwap [67], allowing users to trade with zerogas fees. Sushiswap and Curve have deployed their contractson Polygon and QuickSwap is a fork of Uniswap on that samelayer 2 solution [68]. As a result, users are now able to use thesame products on layer 2 solutions, with drastically reducescosts and allows faster transactions. In 2021, dYdX launchedits order book-based DEX on StarkEx [69].

In sum, AMMs on layer 2 solutions result in faster trans-actions and a reduction of costs due to zero or decreased gascosts, ultimately enhancing the user experience.

V. SECURITY AND PRIVACY CONCERNS

The previous sections focus on implicit economic costs—including slippage and divergence loss—imposed on the fundsof users interacting with AMM-based DEX. Besides thoserisks, security and privacy matters are also to be taken intoaccount when using AMM-based DEX.

In particular, as a complex, distributed system with a varietyof software and hardware components interacting with eachother, AMM-based DEX are prone to exhibit attack interfaces[70]–[73]. With conventional exchanges, the success of marketmanipulation is uncertain as each trade must be agreed uponbetween the sell and buy sides. In contrast, AMM-based DEXare subject to atomic, risk-free exploits on the protocol’stechnical structure such as its algorithmic pricing scheme [8].Built on top of public blockchain infrastructures featuringtransparency and traceability, AMM-based DEX also exposetheir users to privacy risks.

In this section, we define a taxonomy (illustrated in Fig-ure 6) to enumerate potential security and privacy concerns ofAMM-based DEX, expounding their root causes and possiblemitigation solutions.

A. Associated attacks

We identify three classes of attacks according to the archi-tectural layer on which they occur: infrastructure-layer attacks,middleware-layer attacks, and application-layer attacks. Some-times, a certain attack (e.g. frontrunning) can target multiplelayers simultaneously. We present known historical attacksaffecting AMMs in Table V.

1) Infrastructure-layer attacks: The proper operation ofDEX is based upon healthy and stable blockchain infras-tructures (i.e., validators, network, full nodes, etc.). However,since the birth of the blockchain systems, various attacks havethreatened their normal operations, potentially affecting therobustness and user experience of DEX.

a) Block timestamp manipulation: A timestamp fieldis set by miners during the validation process. However,malicious miners can manipulate the block timestamps withinconstraints to win rewards from certain smart contracts [74],or to tamper with the execution order of DEX transactionspacked in different blocks [75].

To mitigate the negative impact of such manipulation, DEXcontracts should be timestamp independent [76]. For example,smart contract engineers should avoid using block timestampsas program inputs or make sure a contract function can toleratevariations by a certain time period (e.g. 15 seconds [77]) andstill maintain integrity [78]. Besides, DEX should choose to bebuilt on a blockchain that applies rigorous constraints to thetimestamps of committed blocks or uses external timestampauthorities to assert a block creation time [79].

b) Transaction sequence manipulation: While transac-tions within a block share the same timestamp, miners canorder transactions, and choose to include or exclude certaintransactions at their discretion. Malicious miners can abusetheir “power” to prioritize transactions in their favor, profitingfrom miner extractable value (MEV). This can be furtherfacilitated by open-source software such as Flashbots [10].

To prevent transaction sequence manipulation, DEX shouldfirst be built upon reputable, frequently-used blockchain sys-tems, as they feature high miner/validator participation, mak-ing transaction sequence manipulation difficult. Besides, thisattack can be mitigated through an enforced transaction se-quencing rule that relies on a trusted third party to assignsequential numbers to transactions [80]. We also discuss howDEX and its transactions can practice transaction sequencingfrom application-layer in V-A3c, and how privacy-preservingblockchain and DEX are resistant to this attack in V-B.

c) Other infrastructure-layer attacks: Aiming to perturboperations of blockchain systems [81], many other attacks donot target AMM-based DEX specifically, but can indirectlyaffect the service of DEX. For example, attackers can launchspam or distributed denial-of-service (DDoS) attacks towardsthe blockchain system [82], [83], thereby increasing the la-tency or even hindering the accessibility of DEX services;

12

blockchain denial-of-service (BDoS) attacks exploit the rewardmechanism to discourage miner participation, thereby causinga blockchain to a halt with significantly fewer resources [84];the 51% attack [81], the most classic blockchain attack, is ableto tamper with the blockchain in any way by controlling morethan 50% of the network’s mining hash rate; network attackscan destroy the network connections between the users andthe blockchain system through domain name server (DNS) hi-jacking [85] or border gateway protocol (BGP) hijacking [86].

In short, AMM-based DEX should be built upon distributedledgers with active service, community maintenance, and up-grades, as well as modular security designs. Only by ensuringeach module of the blockchain system and the interactionsbetween them are secure, can the relative security of the entireblockchain system be ensured.

2) Middleware-layer attacks: An AMM-based DEX usu-ally consists of various smart contracts, in which each servesas a middleware that bridges some application-layer functionswith blockchain infrastructures, and collectively support oper-ations of the DEX. However, the smart contracts and complexcollaborations between them can also lead to potential systemvulnerabilities [92]. Attackers can exploit such attack inter-faces to steal tokens from a DEX or even paralyze it.

a) Reentrancy attack: Reentrancy attack can happenwhen two or more entities (e.g. smart contract, side-chain) callor execute certain functions in specific sequences or frequen-cies. Ever since July 2016, reentrancy attacks have capturedthe attention of the crypto industry, when the DecentralizedAutonomous Organization (DAO), an Ethereum smart con-tract, was executed maliciously with such an attack, causing a$50 million economic loss in tokens [90]. Afterwards, despitethe emergence of various proposals addressing the reentrancyproblems [91]–[93], reentrancy attacks persist, and becameparticularly threatening to AMM-based DEX. In January 2019,an audit identified a reentrancy vulnerability in Uniswap [94],which was then exploited by hackers to steal $25 million worthof tokens in April 2020 [95] Hackers performed this attackby leveraging a subtle interaction between two contracts thatwere secure in isolation, and a third malicious contract [96].In March 2021, $3.8 million worth of tokens were stolenfrom DODO through a series of attacks, which began withreentrancies via the init() function in a liquidity pool smartcontract, followed by frontrunning and honeypot attacks [97].

The security community has proposed a variety of ap-proaches to tackle reentrancy attacks [98]. For example, Rodleret al. [99] protect existing smart contracts on Ethereum in abackwards compatible way based on run-time monitoring andvalidation; Das et al. [100] propose Nomos, a reentrancy-awarelanguage that enforces security using resource-aware sessiontypes; Cecchetti et al. [96] formalize a general definition ofreentrancy and leverage information flow control to solve thisproblem in general. However, with the increasing complexityof AMM, it can become more difficult for developers to reasonabout the reentrant interface, thus making reentrancy attacksa more intractable problem for AMM-based DEX.

b) Other middleware-layer attacks: On the middlewarelayer, there are many other attacks and threats that can affectnormal operations of smart contracts [105], such as replay

attack [106], exception mishandling [107], integer under-flow/overflow attacks [108], etc. These threats are not specifi-cally targeted at DEX, but can potentially be harmful to DEXoperation. The security community has proposed a variety ofapproaches to secure smart contract from these threats, suchas Smartshield [109], Zether [110], and NeuCheck [111]. Still,to fundamentally resolve middleware-layer attacks, smart con-tract developers must strictly abide by software developmentspecifications and conduct comprehensive security tests.

3) Application-layer attacks:a) Oracle attack: A flash loan is a feature provided by

lending platforms where an uncollateralized borrow positioncan be created as long as the borrowed funds can be repaidwithin one transaction. Flash loans can be used to repay atdiscount debts that are liquidable without having to acquireborrowed assets in the first place.

In this kind of attack, adversaries manipulate lending plat-forms that use a DEX as their sole price oracle (see Figure 1).

Attack Algorithm 1 Flash-loan-funded price oracle attack1: Take a flash loan to borrow xA tokenA from a lending platform,

whose value is equivalent to xB tokenB at market price.2: Swap xA tokenA for xB −∆1 tokenB on an AMM, pushing the

new price of tokenA in terms of tokenB down to xB−∆2xA

, where∆2 > ∆1 > 0 due to slippage.

3: Borrow xA + ∆3 tokenA with xB −∆1 tokenB as collateral ona lending platform that uses the AMM as their sole price oracle.To temporarily satisfy overcollateralization, xB−∆2

xA< xB−∆1

xA+∆3.

4: Repay the flash loan with xA tokenA.

Following Attack algorithm 1, an attacker profits with ∆3

tokenA less any transaction fees incurred. Utilizing continuousslippage native to an AMM-based DEX (see III-C4), the attacktemporarily distorts the price of tokenA relative to tokenB .After the prices are arbitraged back, the attack would leavethe loan taken from step 3 undercollateralized, jeopardizingthe safety of lenders’ funds on the lending platform. Examplesof such attacks are exploits on Harvest finance [112], ValueDeFi [113] and Cheese bank [114].

This broken design can generally be fixed by either provid-ing time-weighted price feeds, or using external decentralizedoracles. The first solution ensures that a price feed cannot bemanipulated within the same block, while the second solutionaggregates price data from multiple independent data providersthat add a layer of security behind the aggregation algorithm,making sure that prices are not easily manipulated [115].

b) Rug pull: A rug pull involves the abandonment ofa project by the project foundation after collecting investor’sfunds [150]. One way of doing this, is to lure people intobuying the coin with no value through a DEX, subsequentlyswapping this coin for ETH or another cryptocurrency withvalue, as shown in Attack algorithm 2. DEX allow users todeploy markets without audit and for free (barring the gascosts), which makes them an excellent target to scam investors.One method is to create a coin with the same name as anexisting one. This attracts a lot of attention since everyonewants to pick up the coin at the lowest price possible. Thecoin is being bought up, and the original LP swaps his fakecoin for ETH. In other cases, the creators of the scam token

13

Table V: Overview of the attacks in different layers and losses experienced by AMM-based DEX.

Attacks Literature Affected AMMs Estimated Loss Attack Time

Infrastructure-layerattacks

Block timestamp manipulation [74], [75], [78], [79], [87], [88] — —Transaction sequence manipulation [41], [80] — —Other infrastructure-layer attacks [81]–[86], [89] — —

Middleware-layerattacks

Reentrancy attack [90]–[103] Uniswap V1 [104] 25.00m 04/2020Other middleware-layer attacks [105]–[111] — —

Application-layerattacks

Oracle attack [112]–[117] Curve [118] 30.00m 11/2020QuickSwap [119] 2.40m 07/2021Burgerswap [120] 7.20m 05/2021DODO [121] 0.70m 03/2021

Rug pull [80], [122]–[129] Uranium Finance [130], [131] 50.00m 04/2021SushiSwap [132] 13.00m 08/2020

Frontrunning [?], [3], [5], [77], [80], [133]–[135] Various [136] 280.00m each month worldwideDODO [121] 0.70m 03/2021

Backrunning [3], [5], [137]–[140] — —Sandwich attacks [3], [5], [141] Various [142] 0.12m each month worldwideVampire attack [33], [143]–[146] Uniswap V2 [147] 1000.00m 08/2020

Uniswap V2 [148] 4300.00m 09/2020Uniswap V2 [149] 239.00m 09/2021

reach out to several prominent people, creating false hype.Once potential buyers see that major players have purchasedthe token, they start buying themselves, before realizing thatthe token cannot be swapped back for ETH. Sometimes, theattackers let people trade the coin back for ETH, but only fora short period since they are running the risk of losing money.[122] research data on scam tokens on Uniswap and confirmthat rug pulls commonly find their victims through DEX.

In August 2020, an rug puller extracted 3 ETH by imitatingthe well-known AMPL token [123] with a scam token TMPL.The token’s transaction history shows the provision of 150ETH and TMPL tokens to a Uniswap V2 pool by the attacker,who removed 153.81 ETH only 35 minutes later [124].

Attack Algorithm 2 Rug Pull1: Mint a new coin XYZ.2: Create a liquidity pool with xXYZ XYZ and xETH ETH (or any

other valuable cryptocurrency) on an AMM, and receive LPtokens.

3: Attract unwitting traders to buy XYZ with ETH from the pool,effectively changing the composition of the pool.

4: Withdraw liquidity from the pool by surrendering LP tokens, andobtain xXYZ −∆1 XYZ and xETH + ∆2 ETH, where ∆1,∆2 > 0.

To protect themselves from being rugged, investors shouldexercise caution and always confirm a project’s credibilitybefore investing in its IDO [125], [126]. Usually, reputableIDOs feature high liquidity and a pool lock [127] that disableswithdrawal for a fixed period, so that LPs are unable to quicklyempty the pool once it has absorbed a sufficient amount ofvaluable assets from investors [128].

c) Frontrunning: Frontrunning is often enabled throughaccess to privileged market information about upcoming trans-actions and trades [80]. Since all transactions are visiblefor a very short period of time before being committed toa block, it is possible for a user to observe and react toa transaction while it is still in the mempool. Those whoplace their trade immediately before someone else’s are calledfrontrunners [80], [129]. Frontrunners attempt to get the bestprice of a new coin before selling them onto the market. Theycan buy up a great portion of the supply of a new token to

create exorbitant prices. Due to the hype, this does not stopretail traders from further buying. The frontrunner, who is theseller with the most significant supply, can swap the purchasedtoken for popular coins (e.g. ETH) paid by retail traders. Forexample, a considerable amount of IDOs on Polkastarter arefrontran on Uniswap [133].

Frontrunning can also be achieved through transactionsequence manipulation (see V-A1b) and by exploiting thegeneral mining mechanism. Most mining software, includingthe vanilla Go-Ethereum (geth), the most popular command-line interface for running Ethereum node, sorts transactionsbased on their gas price and nonce [?], [5], [80]. This featurecan be exploited by malicious users of DEX who broadcasta transaction with a higher gas price than the target one todistort transaction ordering and thus achieve frontrunning.

Normal exchange users can set a low slippage tolerance toavoid suffering from a price elevated by front-runners. How-ever, an overly low slippage tolerance may lead a transaction tofail, especially when the trade size is large, resulting in a wasteof gas fee [134]. DEX can enforce transaction sequencingto fundamentally solve frontrunning. Some exchanges, suchas EtherDelta [77] and 0xProject [135], utilize centralizedtime-sensitive functionalities in off-chain order books [80]. Inaddition, transactions can specify the sequence by includingthe current state of the contract as the only state to executeon [80], thereby preventing some types of frontrunning attacks.Frontrunning can further be tackled by addressing privacyissues (see V-B) and transaction sequence manipulation onthe infrastructure layer (see V-A1b).

d) Backrunning: Backrunners place their trade immedi-ately after someone else’s trade. The attacker needs to fill upthe block with a large number of cheap gas transactions todefinitively follow the target’s transaction. Compared to fron-trunning which only requires a single high valued transactionand is detrimental to the user being frontrun, backrunning isdisastrous to the whole network by hindering the throughputwith useless transactions [137].

Backrunning attacks can be mitigated through anti-BDoSsolutions such as A2MM [3]. Theoretically, defense solutionsof application-layer distributed denial-of-service (L7 DDoS)

14

Figure 7: Two sandwich price attacks (see Attack algorithm 3),marked with orange on 30 September 2021, with theSTARL/ETH pair on Uniswap V2. The first attack, con-ducted at 10:16:46 by 0xa405e8...f802, resulted in a profit of0.0310743 ETH; the second attack, conducted at 10:19:52 by0x1d6e8b...932d, resulted in a profit of 0.0308927 ETH.

attacks [138]–[140] can also be adopted to tackle backrunningproblems, as they all aim to secure usability of web servicesto legitimate users. In addition, backrunning can be addressedby confidentiality-enhancing solutions that hide the content ofa transaction before it is committed to a block (see V-B).

e) Sandwich attacks: Combining front- and back-running, an adversary of a sandwich attack places his ordersimmediately before and after the victim’s trade transaction.The attacker uses front-running to cause victim losses, andthen uses back-running to pocket benefits. While there areendless examples of sandwich attacks, Zhou et al. [5] detailtwo types that can occur on an AMM: an LP attacking an ex-change user (see Attack algorithm 4 Sandwich LP attack), andone exchange user attacking another (see Attack algorithm 3Sandwich price attack). The latter is particularly common.Figure 7 shows two examples of such attacks on UniswapV2 within a time frame of 3 minutes.

Attack Algorithm 3 Sandwich price attack1: UserA wishes to purchase xA XYZ whose spot price is P1 on an

AMM with gas fee g1.2: UserB observes the mempool and sees the transaction.3: UserB front-runs by buying xB XYZ with a higher gas fee g2 >

g1 on the same AMM.4: UserB and UserA’s transactions are executed sequentially at

respective average price of PB and PA, pushing XYZ’s spot priceup to P2, where P2 > PA > PB > P1 due to slippage.

5: UserB back-runs by selling xB XYZ at an average price of P ′B ,with P2 > P ′B > PB due to slippage.

Attack Algorithm 4 Sandwich LP attack1: UserA places a transaction order to buy xA tokenA with tokenB

with a pool containing rA tokenA and rB tokenB with gas feeg1.

2: LPB observes the mempool and sees the transaction.3: LPB front-runs by withdrawing liquidity k rA tokenA and k rB

tokenB with a higher gas fee g2 > g1.4: LPB and UserA’s transactions are executed sequentially, resulting

in a new composition of the pool with (1 − k)rA + xA tokenA

and (1 − k)rB − xB tokenB .5: LPB back-runs by re-providing k rA tokenA and k· (1−k)rB−xB

(1−k)rA+xAtokenB .

6: LPB back-runs by selling (1 − (1−k)rB−xB(1−k)rA+xA

) tokenB for sometokenA

Considering swap fee (see II-D2b), gas fee (see II-D2c) andslippage (see II-D3a), sandwich attacks are only profitable ifthe size of the target trade exceeds a certain threshold, a valuethat depends on the DEX’s design and the pool size. DEXcan thus prevent sandwich attacks by disallowing transactionsabove the threshold [3]. Naturally, sandwich attacks can alsobe curbed by deterring either frontrunning (see V-A3c) orbackrunning (see V-A3d).

f) Vampire attack: A vampire attack targets an AMM bycreating a more attractive incentive scheme for LPs, therebysiphoning out liquidity from the target AMM [143] to thedetriment of the protocol foundation (see II-A3).

In September 2020, Sushiswap gained $830 million ofliquidity through a vampire attack [144], where Sushiswapusers were incentivized to provide Uniswap LP tokens intothe Sushiswap protocol for rewards in SUSHI tokens [33]. Amigration of liquidity from Uniswap to protocol Sushiswapwas executed by a smart contract that took the Uniswap LPtokens deposited in Sushiswap, redeeming them for liquidityon Uniswap which was then transferred to Sushiswap andconverted to Sushiswap LP tokens.