Embed Size (px)

Citation preview

PART II

Firms CommercializingBiotechnology

Chapter 4

Firms CommercializingBiotechnology

Contents

PageIntroduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65Overview of U.S. and Foreign Companies Commercializing Biotechnology . . . . . . . . . . . 66

Pharmaceutical Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72Animal Agriculture Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79Plant Agriculture Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81Specialty Chemicals Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 83

U.S. and Foreign Support Firms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84Important Product Areas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 90

U.S. Firms Commercializing Biotechnology and Their Role in Competition. . . . . . . . . . . . 91New Biotechnology Firms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91Established U.S. Companies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 99Collaborative Ventures Between NBFs and Established U.S. Companies. . . . . . . . . . . . . 103Collaborative Ventures Between NBFs and Established Foreign Companies. . . . . . . . . . 108

Findings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 109Chapter preferences . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 111

Tables

Table No. Page4. Companies Commercializing Biotechnologyin the United States

and Their Product Markets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 675. Distribution of Sales by the Top 20 U.S.

and Foreign Pharmaceutical Companies, 1981 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 736.Introduction of New Pharmaceutical Products by Country of Origin

Between 1961 and 1983 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 747. Biotechnology R&D Budgets for Leading U.S. and Foreign Companies, 1982 . . . . . . . 748. Pharmaceutical R&D Expenditures by Country: 1964, 1973, and 1978, . . . . . . . . . . . 759. Diversification of Japanese Chemical, Food Processing, Textile,

and Pulp Processing Companies Into Pharmaceuticals . . . . . . . . . . . . . . . . . . . . . . . . . . 77IO. Japanese Joint Ventures in Pharmaceutical Applications of Biotechnology . . . . . . . . . 7811. Applications of Biotechnology to Plant Agriculture for Seven New

Biotechnology Firms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8212. Estimates of U.S. Monoclinal Antibody Markets, 1982 and 1990 . . . . . . . . . . . . . . . . . 9513. Equity Investments in New Biotechnology Firms by

Established U.S. Companies, 1977-83 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10014. Some Collaborative Ventures Between New Biotechnology Firms and

Established U.S .and Foreign Companies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ., ,. 104

Figures

Figure No. PageIO, Percentage of Firms in the United States Pursuing Applications of Botechnology

in Specific Industrial Sectors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71ll,Ernergence of New Biotechnology Firms, 1977-83. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9312. Aggregate Equity Investments in New Biotechnology Firms

by Established U.S. Companies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101

Chapter 4

Firms Commercializing Biotechnology

Introduction

Biotechnology has the technical breadth anddepth to change the industrial community of the21st century because of its potential to producesubstantially unlimited quantities of:

●

●

●

●

●

products never before available,products that are currently in short supply,products that cost substantially less thanproducts made by existing methods of pro-duction,products that are safer than those now avail-able, andproducts made with raw materials that maybe more plentiful and less expensive thanthose now used.

By virtue of its wide-reaching potential applica-tions, biotechnology lies close to the center ofmany of the world’s major problems—malnutri-tion, disease, energy availability and cost, andpollution. It is because of biotechnology’s promisethat the developed countries of the world havecommenced a competitive battle to commercializeits applications,

Nowhere in the world are efforts to commer-cialize biotechnology stronger than in the UnitedStates. * Large established U.S. companies in in-dustries ranging from pharmaceuticals to petro-leum have followed the lead in developing bio-technology that was set by entrepreneurial newbiotechnology firms (NBFs) in the United Stateswhose dedication to biotechnology is unmatchedanywhere. Major competitive challenges to theUnited States in current product markets, as wellas in new biotechnology markets yet to be de-fined, will be mounted by established companiesin the Federal Republic of Germany, United King-dom, Switzerland, and France—but the most for-midable challenge will come from established

● For a summary of activities in biotechnology in countries otherthan the United States, see Appendix B: Country Summaries.

companies in Japan. The Japanese consider bio-technology to be the last major technological rev-olution of this century (58). More immediate thanits promise of helping to alleviate some worldproblems, biotechnology offers Japan an impor-tant opportunity to revitalize its structurally de-pressed basic industries whose production proc-esses are reliant on imported petroleum,

This chapter provides an overview of U.S. andforeign private sector research and development(R&D) and commercialization efforts in biotech-nology to help answer the broader question be-ing addressed by this report: Will the UnitedStates be able to translate its present technologicallead into worldwide commercial success by secur-ing competitive shares of biotechnology-relatedproduct markets? The first section of the chapterprovides an overview of the types of companiesthat are commercializing biotechnology in theUnited States and the five foreign countries ex-pected to be the major competitors in the areaof biotechnology. This section briefly examinesthe four fields where biotechnology is being ap-plied most vigorously —pharmaceuticals, animalhealth, plant agriculture, and specialty chemicals.The second section analyzes and compares thestrength of the U.S. support base with that of thecompetitor countries, using three important prod-uct areas for comparison: biochemical reagents,instrumentation, and software. The third sectionanalyzes the respective roles of the firms apply-ing biotechnology in the United States—NBFs andestablished companies-in the domestic and inter-national development of biotechnology. It also de-scribes collaborative ventures between NBFs inthe United States and established U.S. and foreigncompanies that are seeking to commercialize bio-technology. The chapter concludes by summariz-ing major findings with respect to the role of NBFsand established companies in the U.S. commercial-ization effort.

65

.

66 Commercial Biotechnology: An International Analysis

Overview of U.S. and foreign companiescommercializing biotechnology

U.S. and foreign efforts to develop and commer-cialize biotechnology differ substantially in qhar-acter and structure. The manner in which theUnited States and other countries organize theirdevelopment efforts is important for two reasons:it can influence their respective commercial capa-bilities; and it will ultimately shape the characterof international competition.

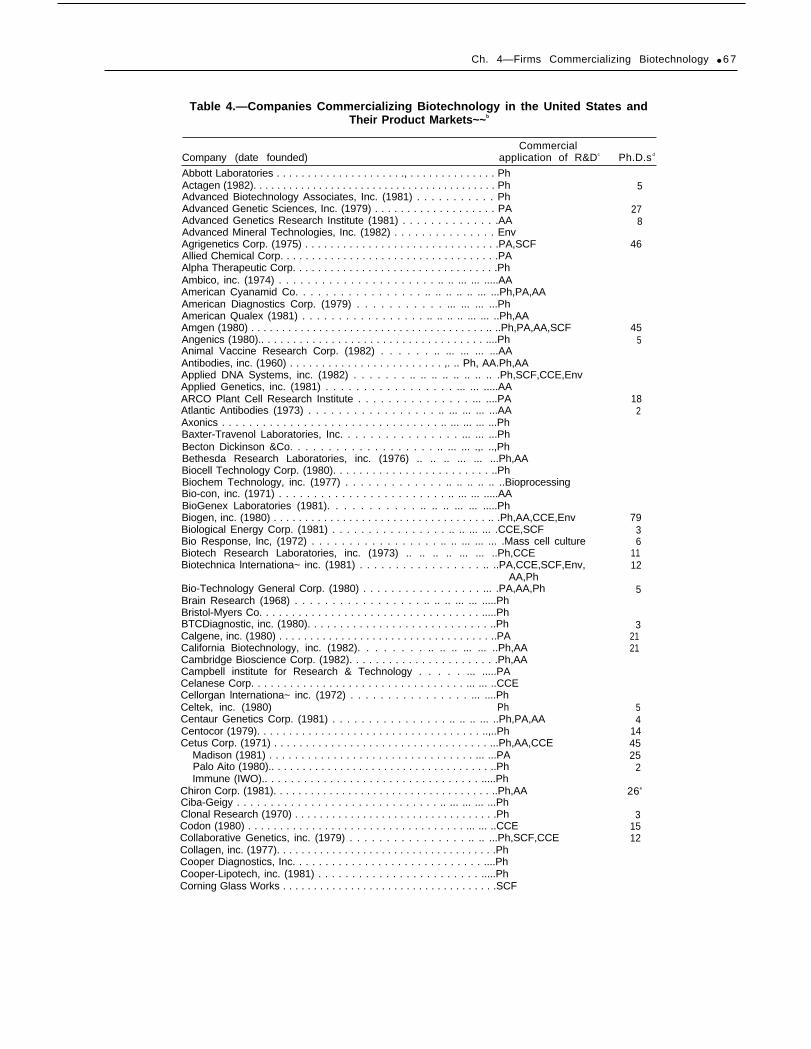

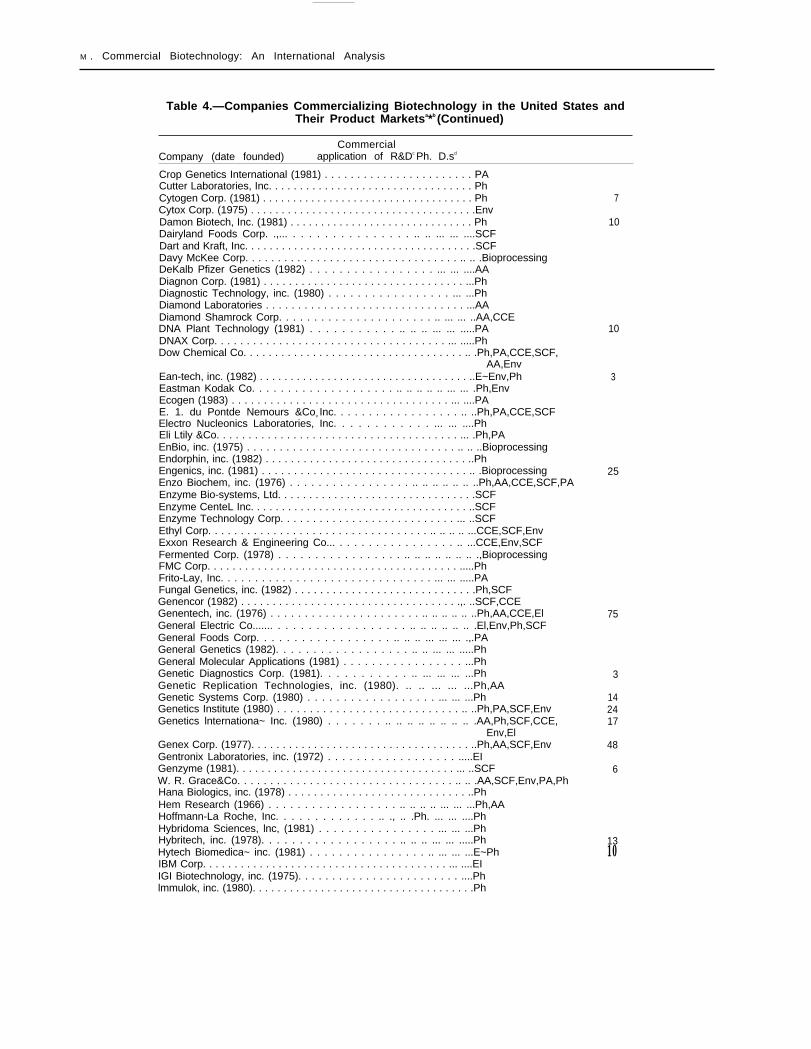

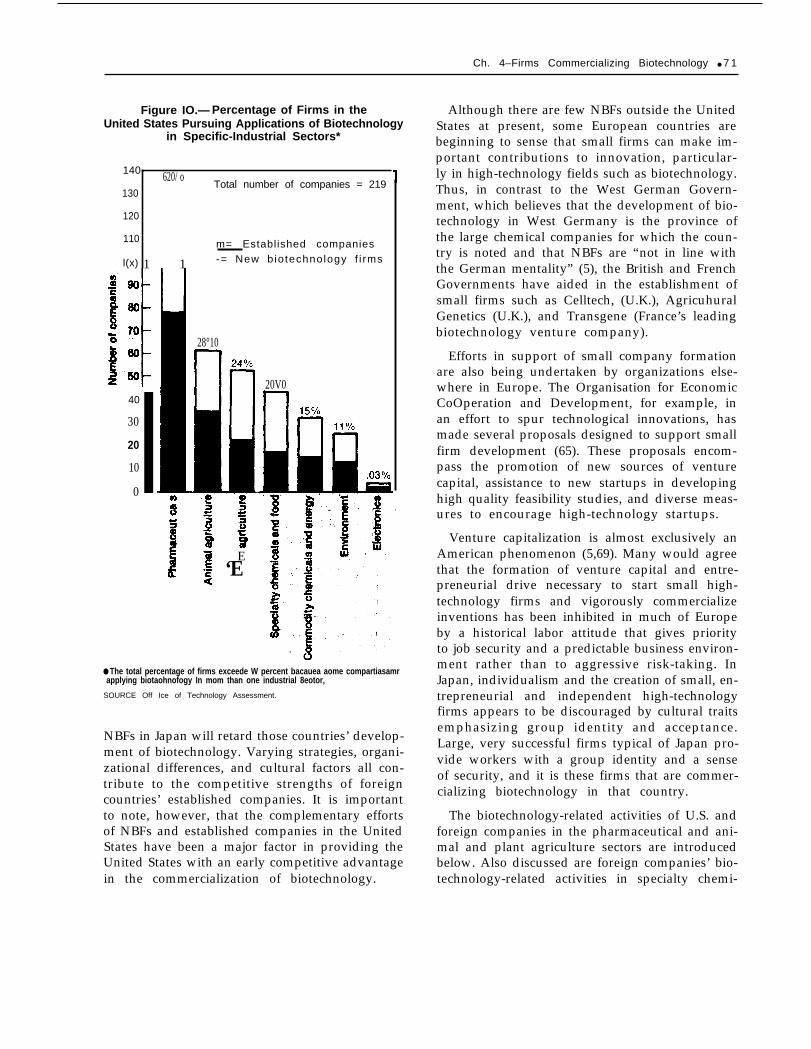

In the United States, two distinct sets of firmsare pursuing commercial applications of biotech-nology-NBFs and established companies. NBFs,as defined by this report, are entrepreneurial ven-tures started specifically to commercialize innova-tions in biotechnology. For the most part, theyhave been founded since 1976–the same year theU.S. firm Genentech was founded to exploit therecombinant DNA (rDNA) technology patented inthe United States by Cohen and Boyer, * Typical-ly, NBFs are structurally organized specifically toapply biotechnology to commercial product de-velopment. The established companies pursuingapplications of biotechnology are generally proc-essa-iented, multiproduct companies in tradition-al industrial sectors such as pharmaceuticals,energy, chemicals, and food processing. Thesecompanies have undertaken in-house biotechnol-ogy R&D in an effort to determine how andwhere best to apply biotechnology to existing ornew products and processes. Table 4 provides alist of NBFs and established companies currentlyapplying biotechnology in the United States andthe targeted commercial areas of their research.Figure 10 illustrates the percentage of U.S. firmspursuing biotechnology R&D in specific applica-tion areas.

Sixty-two percent (135) of the 219 U.S. compa-nies for whom commercial application areas are

● Two U.S. firms, Cetus and Agrigenetics, though established before1976, are considered to be NBFs. Cetus was founded to capitalizeon classical gerwtic techniques for product development, but showedearly interest in biotechnology and began aggressively pursuingproduct development with the new techniques. Agrigenetics wasformed in 1975 to link new genetic research with the seed business.Thus, the behavior and research focus of both Cetus and Agri-genetics place them in the new firm category despite their earlyfounding dates.

known* are pursuing applications of biotech-nology in the area of pharmaceuticals; 28 percentare pursuing applications in animal agriculture,and 24 percent in plant agriculture.** In the areaof specialty chemicals and food additives, com-modity chemicals and energy, the environment,and electronics, respectively, relatively fewer U.S.firms are pursuing commercial applications of bio-technology. In some of these sectors, conventionaltechnologies are working well or existing invest-ments in capital equipment are very substantial.In others, much uncertainty still surrounds thepotential of biotechnology or the research neededto develop applications of biotechnology is longterm.

In Japan, the Federal Republic of Germany,Switzerland, France, and the United Kingdom, * *biotechnology is being commercialized almost ex-clusively by established companies. Most Euro-pean nations and Japan, unlike the United States,tend, for different reasons, to emphasize the im-portance of large companies instead of small ones.Thus, the development of biotechnology in thesecountries is biased considerably toward the largepharmaceutical and chemical companies.

It should not be assumed that the small numberof NBFs in the European countries or the lack of

● This figure does not include the companies listed that are spe-cializing in bioprocessing, because the bioprocessing R&D may notbe associated with specific products. See Appendix D.’ Firms Com-mercializing Biotechnology in the United States for an explanationof how the list was obtained.

“ *These percentages add up to more than 100 percent becausemany of the fimns are engaged in more than one area of commer-cial application.

● ● ● In the United Kingdom, some NBFs, not including Celltech andAgricultural Genetics, are beginning to form on the periphery ofuniversities. Plant Science, Ltd., for example, is linked to the Univers-ity of Sheffield; Imperial Biotechnology, Ltd., is linked to the Im-perial College in London; IQ (Bio) was formed by some CambridgeUniversity biochemists; Boscot, Ltd., a joint venture between twoScottish institutions, was established by the University of Edinburghand Heriot-Watt University, and Cambridge Life Sciences pursuesbiosensors based on work at Southampton University. As an indica-tion of the increased number of NBFs forming in Britain, Biotech-nology Investments, Ltd., the venture fund managed by N.M. Roths-child (the bank) now has for the first time since the fund was es-tablished more proposals from British firms than from companiesin the United States (56).

Ch. 4—Firms Commercializing Biotechnology ● 6 7

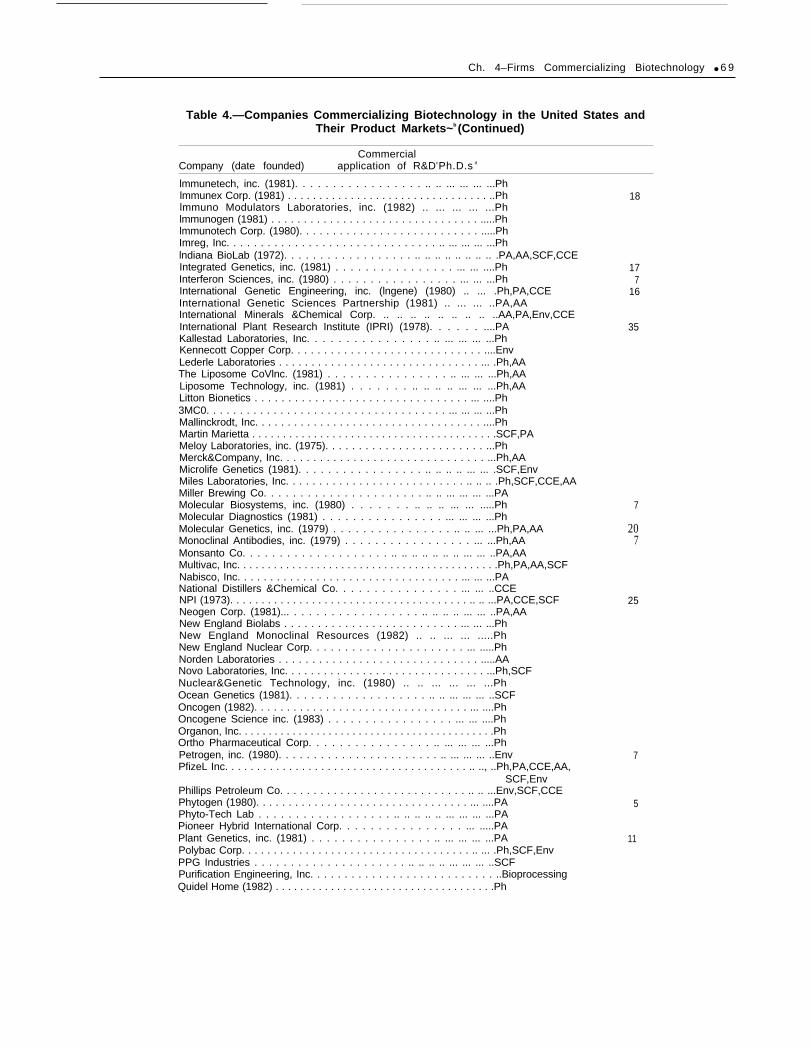

Table 4.—Companies Commercializing Biotechnology in the United States andTheir Product Markets~~b

CommercialCompany (date founded) application of R&Dc Ph.D.s d

Abbott Laboratories . . . . . . . . . . . . . . . . . . . . ., . . . . . . . . . . . . . . PhActagen (1982). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . PhAdvanced Biotechnology Associates, Inc. (1981) . . . . . . . . . . . PhAdvanced Genetic Sciences, Inc. (1979) . . . . . . . . . . . . . . . . . . . PAAdvanced Genetics Research Institute (1981) . . . . . . . . . . . . . .AAAdvanced Mineral Technologies, Inc. (1982) . . . . . . . . . . . . . . . EnvAgrigenetics Corp. (1975) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .PA,SCFAllied Chemical Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .PAAlpha Therapeutic Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .PhAmbico, inc. (1974) . . . . . . . . . . . . . . . . . . . . . . .. .. ... ... .....AAAmerican Cyanamid Co. . . . . . . . . . . . . . . . . .. .. .. .. .. ... ...Ph,PA,AAAmerican Diagnostics Corp. (1979) . . . . . . . . . . . ... ... ... ...PhAmerican Qualex (1981) . . . . . . . . . . . . . . . . . .. .. .. .. ... ... ..Ph,AAAmgen (1980) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. ..Ph,PA,AA,SCFAngenics (1980).. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ....PhAnimal Vaccine Research Corp. (1982) . . . . . . .. ... ... ... ...AAAntibodies, inc. (1960) . . . . . . . . . . . . . . . . . . . . . . . . ,. .. Ph, AA.Ph,AAApplied DNA Systems, inc. (1982) . . . . . . . .. .. .. .. .. .. .. .. .Ph,SCF,CCE,EnvApplied Genetics, inc. (1981) . . . . . . . . . . . . . . . . . ... ... .....AAARCO Plant Cell Research Institute . . . . . . . . . . . . . . . ... ....PAAtlantic Antibodies (1973) . . . . . . . . . . . . . . . . . .. ... ... ... ...AAAxonics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. ... ... ... ...PhBaxter-Travenol Laboratories, Inc. . . . . . . . . . . . . . . . ... ... ...PhBecton Dickinson &Co. . . . . . . . . . . . . . . . . . . .. ... ... .,. ..,PhBethesda Research Laboratories, inc. (1976) .. .. .. ... ... ...Ph,AABiocell Technology Corp. (1980). . . . . . . . . . . . . . . . . . . . . . . . ..PhBiochem Technology, inc. (1977) . . . . . . . . . . . . . .. .. .. .. .. ..BioprocessingBio-con, inc. (1971) . . . . . . . . . . . . . . . . . . . . . . . . .. ... ... .....AABioGenex Laboratories (1981). . . . . . . . . . . .. .. .. ... ... .....PhBiogen, inc. (1980) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. .Ph,AA,CCE,EnvBiological Energy Corp. (1981) . . . . . . . . . . . . . . . . .. .. ... ... .CCE,SCFBio Response, lnc, (1972) . . . . . . . . . . . . . . . . . .. .. ... ... ... .Mass cell cultureBiotech Research Laboratories, inc. (1973) .. .. .. .. ... ... ..Ph,CCEBiotechnica lnternationa~ inc. (1981) . . . . . . . . . . . . . . . . . .. ..PA,CCE,SCF,Env,

AA,PhBio-Technology General Corp. (1980) . . . . . . . . . . . . . . . . . ... .PA,AA,PhBrain Research (1968) . . . . . . . . . . . . . . . . . .. .. .. ... ... .....PhBristol-Myers Co. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .....PhBTCDiagnostic, inc. (1980). . . . . . . . . . . . . . . . . . . . . . . . . . . . ..PhCalgene, inc. (1980) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ..PACalifornia Biotechnology, inc. (1982). . . . . . . . .. .. .. ... ... ..Ph,AACambridge Bioscience Corp. (1982). . . . . . . . . . . . . . . . . . . . . . .Ph,AACampbell institute for Research & Technology . . . . . ... .....PACelanese Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ... ... ..CCECellorgan lnternationa~ inc. (1972) . . . . . . . . . . . . . . . . ... ....PhCeltek, inc. (1980) PhCentaur Genetics Corp. (1981) . . . . . . . . . . . . . . . . .. .. .. ... ..Ph,PA,AACentocor (1979). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ..,..PhCetus Corp. (1971) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ...Ph,AA,CCE

Madison (1981) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ... ...PAPalo Aito (1980).. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ..PhImmune (IWO).. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .....Ph

Chiron Corp. (1981). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ..Ph,AACiba-Geigy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. ... ... ... ...PhClonal Research (1970) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .PhCodon (1980) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ... ... ..CCECollaborative Genetics, inc. (1979) . . . . . . . . . . . . . . . . .. .. ...Ph,SCF,CCECollagen, inc. (1977). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .PhCooper Diagnostics, Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . ....PhCooper-Lipotech, inc. (1981) . . . . . . . . . . . . . . . . . . . . . . . . .....PhCorning Glass Works . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .SCF

5

278

46

455

182

7936

1112

5

32121

54

144525

2

26e

31512

M . Commercial Biotechnology: An International Analysis

Table 4.—Companies Commercializing Biotechnology in the United States andTheir Product Marketsa*b (Continued)

CommercialCompany (date founded) application of R&Dc Ph. D.sd

Crop Genetics International (1981) . . . . . . . . . . . . . . . . . . . . . . . PACutter Laboratories, Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . PhCytogen Corp. (1981) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . PhCytox Corp. (1975) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .EnvDamon Biotech, Inc. (1981) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . PhDairyland Foods Corp. .,... . . . . . . . . . . . . . . . .. .. ... ... ....SCFDart and Kraft, Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .SCFDavy McKee Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. .. .BioprocessingDeKalb Pfizer Genetics (1982) . . . . . . . . . . . . . . . . . ... ... ....AADiagnon Corp. (1981) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ...PhDiagnostic Technology, inc. (1980) . . . . . . . . . . . . . . . . . ... ...PhDiamond Laboratories . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ...AADiamond Shamrock Corp. . . . . . . . . . . . . . . . . . . . . . .. ... ... ..AA,CCEDNA Plant Technology (1981) . . . . . . . . . . . .. .. .. ... ... .....PADNAX Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ... .....PhDow Chemical Co. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. .Ph,PA,CCE,SCF,

AA,EnvEan-tech, inc. (1982) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ..E~Env,PhEastman Kodak Co. . . . . . . . . . . . . . . . . . . . .. .. .. .. .. ... ... .Ph,EnvEcogen (1983) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ... ....PAE. 1. du Pontde Nemours &Cov Inc. . . . . . . . . . . . . . . . . . .. ..Ph,PA,CCE,SCFElectro Nucleonics Laboratories, Inc. . . . . . . . . . . . ... ... ....PhEli Ltily &Co. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ... .Ph,PAEnBio, inc. (1975) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. .. ..BioprocessingEndorphin, inc. (1982) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ..PhEngenics, inc. (1981) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. .BioprocessingEnzo Biochem, inc. (1976) . . . . . . . . . . . . . . . . . .. .. .. .. .. .. ..Ph,AA,CCE,SCF,PAEnzyme Bio-systems, Ltd. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .SCFEnzyme CenteL Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ..SCFEnzyme Technology Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . ... ..SCFEthyl Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. .. .. .. ...CCE,SCF,EnvExxon Research & Engineering Co... . . . . . . . . . . . . . . . . .. ...CCE,Env,SCFFermented Corp. (1978) . . . . . . . . . . . . . . . . . .. .. .. .. .. .. .. .,BioprocessingFMC Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .....PhFrito-Lay, Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ... ... .....PAFungal Genetics, inc. (1982) . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Ph,SCFGenencor (1982) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .,. ..SCF,CCEGenentech, inc. (1976) . . . . . . . . . . . . . . . . . . . . . . .. .. .. .. .. ..Ph,AA,CCE,ElGeneral Electric Co....... . . . . . . . . . . . . . . . . . .. .. .. .. .. .. .El,Env,Ph,SCFGeneral Foods Corp. . . . . . . . . . . . . . . . . . .. .. .. ... ... ... .,.PAGeneral Genetics (1982). . . . . . . . . . . . . . . . . . .. .. ... ... .....PhGeneral Molecular Applications (1981) . . . . . . . . . . . . . . . . . ...PhGenetic Diagnostics Corp. (1981). . . . . . . . . . . .. ... ... ... ...PhGenetic Replication Technologies, inc. (1980). .. .. ... ... ...Ph,AAGenetic Systems Corp. (1980) . . . . . . . . . . . . . . . . . . ... ... ...PhGenetics Institute (1980) . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. ..Ph,PA,SCF,EnvGenetics lnternationa~ Inc. (1980) . . . . . . . .. .. .. .. .. .. .. .. .AA,Ph,SCF,CCE,

Env,ElGenex Corp. (1977). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ..Ph,AA,SCF,EnvGentronix Laboratories, inc. (1972) . . . . . . . . . . . . . . . . . . .....EIGenzyme (1981). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ... ..SCFW. R. Grace&Co. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. .. .AA,SCF,Env,PA,PhHana Biologics, inc. (1978) . . . . . . . . . . . . . . . . . . . . . . . . . . . . ..PhHem Research (1966) . . . . . . . . . . . . . . . . . . .. .. .. .. ... ... ...Ph,AAHoffmann-La Roche, Inc. . . . . . . . . . . . . .. ., .. .Ph. ... ... ....PhHybridoma Sciences, lnc, (1981) . . . . . . . . . . . . . . . . ... ... ...PhHybritech, inc. (1978). . . . . . . . . . . . . . . . . . .. .. .. ... ... .....PhHytech Biomedica~ inc. (1981) . . . . . . . . . . . . . . . . .. ... ... ...E~PhIBM Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ... ....EIIGI Biotechnology, inc. (1975). . . . . . . . . . . . . . . . . . . . . . . . ....Phlmmulok, inc. (1980). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Ph

7

10

10

3

25

75

3

142417

48

6

1310

Ch. 4–Firms Commercializing Biotechnology ● 6 9

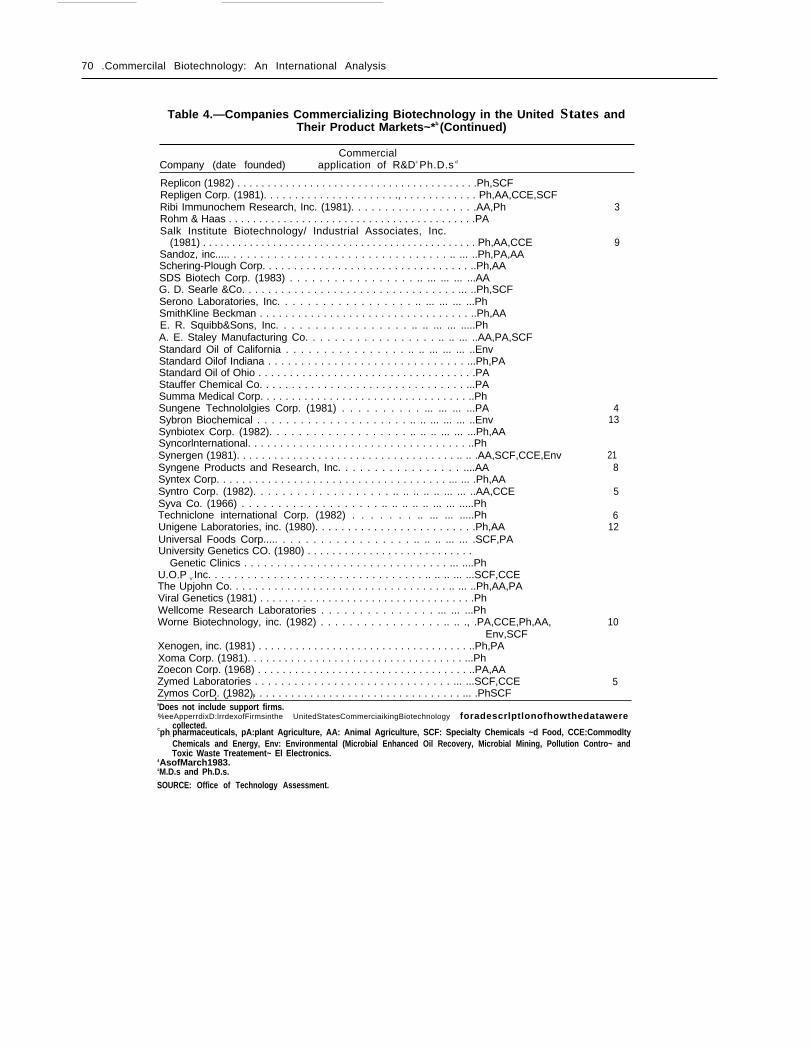

Table 4.—Companies Commercializing Biotechnology in the United States andTheir Product Markets~b (Continued)

CommercialCompany (date founded) application of R&DcPh.D.s d

lmmunetech, inc. (1981). . . . . . . . . . . . . . . . . .. .. ... ... ... ...Phlmmunex Corp. (1981) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ..Ph 18lmmuno Modulators Laboratories, inc. (1982) .. ... ... ... ...Phlmmunogen (1981) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .....Phlmmunotech Corp. (1980). . . . . . . . . . . . . . . . . . . . . . . . . . . .....PhImreg, Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. ... ... ... ...Phlndiana BioLab (1972). . . . . . . . . . . . . . . . . . .. .. .. .. .. .. .. .. .PA,AA,SCF,CCEIntegrated Genetics, inc. (1981) . . . . . . . . . . . . . . . . ... ... ....PhInterferon Sciences, inc. (1980) . . . . . . . . . . . . . . . . . ... ... ...PhInternational Genetic Engineering, inc. (lngene) (1980) .. ... .Ph,PA,CCEInternational Genetic Sciences Partnership (1981) .. ... ... ..PA,AAInternational Minerals &Chemical Corp. .. .. .. .. .. .. .. .. ..AA,PA,Env,CCEInternational Plant Research Institute (IPRI) (1978). . . . . . ....PAKallestad Laboratories, Inc. . . . . . . . . . . . . . . . .. ... ... ... ...PhKennecott Copper Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . ....EnvLederle Laboratories . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ... .Ph,AAThe Liposome CoVlnc. (1981) . . . . . . . . . . . . . . . . .. ... ... ...Ph,AALiposome Technology, inc. (1981) . . . . . . . .. .. .. .. ... ... ...Ph,AALitton Bionetics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ... ....Ph3MC0. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ... ... ... ...PhMallinckrodt, Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ....PhMartin Marietta . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .SCF,PAMeloy Laboratories, inc. (1975). . . . . . . . . . . . . . . . . . . . . . . . ...PhMerck&Company, Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ...Ph,AAMicrolife Genetics (1981). . . . . . . . . . . . . . . . . .. .. .. .. ... ... .SCF,EnvMiles Laboratories, Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . .. .. .. .Ph,SCF,CCE,AAMiller Brewing Co. . . . . . . . . . . . . . . . . . . . . . .. .. ... ... ... ...PAMolecular Biosystems, inc. (1980) . . . . . . . .. .. .. ... ... .....PhMolecular Diagnostics (1981) . . . . . . . . . . . . . . . . ... ... ... ...PhMolecular Genetics, inc. (1979) . . . . . . . . . . . . . . . . .. .. ... ...Ph,PA,AAMonoclinal Antibodies, inc. (1979) . . . . . . . . . . . . . . . . . ... ...Ph,AAMonsanto Co. . . . . . . . . . . . . . . . . . . . .. .. .. .. .. .. .. ... ... ..PA,AAMultivac, Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Ph,PA,AA,SCFNabisco, Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ... ... ...PANational Distillers &Chemical Co. . . . . . . . . . . . . . . . ... ... ..CCENPI (1973). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. .. ...PA,CCE,SCFNeogen Corp. (1981)... . . . . . . . . . . . . . . . . . .. .. .. .. ... ... ..PA,AANew England Biolabs . . . . . . . . . . . . . . . . . . . . . . . . . . ... ... ...PhNew England Monoclinal Resources (1982) .. .. ... ... .....PhNew England Nuclear Corp. . . . . . . . . . . . . . . . . . . . . . ... .....PhNorden Laboratories . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .....AANovo Laboratories, Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ...Ph,SCFNuclear&Genetic Technology, inc. (1980) .. .. ... ... ... ...PhOcean Genetics (1981). . . . . . . . . . . . . . . . . . . .. .. ... ... ... ..SCFOncogen (1982). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ... ....PhOncogene Science inc. (1983) . . . . . . . . . . . . . . . . . ... ... ....PhOrganon, Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .PhOrtho Pharmaceutical Corp. . . . . . . . . . . . . . . . .. ... ... ... ...PhPetrogen, inc. (1980). . . . . . . . . . . . . . . . . . . . . . . .. ... ... ... ..EnvPfizeL Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. .., ..Ph,PA,CCE,AA,

SCF,EnvPhillips Petroleum Co. . . . . . . . . . . . . . . . . . . . . . . . . . . . .. .. ...Env,SCF,CCEPhytogen (1980). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ... ....PAPhyto-Tech Lab . . . . . . . . . . . . . . . . . . .. .. .. .. .. ... ... ... ...PAPioneer Hybrid International Corp. . . . . . . . . . . . . . . . ... .....PAPlant Genetics, inc. (1981) . . . . . . . . . . . . . . . . .. ... ... ... ...PAPolybac Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. ... .Ph,SCF,EnvPPG Industries . . . . . . . . . . . . . . . . . . . . . .. .. .. .. ... ... ... ..SCFPurification Engineering, Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . ..BioprocessingQuidel Home (1982) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Ph

177

16

35

7

207

25

7

5

11

70 .Commercilal Biotechnology: An International Analysis

Table 4.—Companies Commercializing Biotechnology in the United States andTheir Product Markets~*b (Continued)

CommercialCompany (date founded) application of R&Dc Ph.D.s d

Replicon (1982) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Ph,SCFRepligen Corp. (1981). . . . . . . . . . . . . . . . . . . . . ., . . . . . . . . . . . . Ph,AA,CCE,SCFRibi Immunochem Research, Inc. (1981). . . . . . . . . . . . . . . . . . .AA,PhRohm & Haas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .PASalk Institute Biotechnology/ Industrial Associates, Inc.

(1981) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Ph,AA,CCESandoz, inc..... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. ... ..Ph,PA,AASchering-Plough Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ..Ph,AASDS Biotech Corp. (1983) . . . . . . . . . . . . . . . . . .. ... ... ... ...AAG. D. Searle &Co. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ... ..Ph,SCFSerono Laboratories, Inc. . . . . . . . . . . . . . . . . . .. ... ... ... ...PhSmithKline Beckman . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ..Ph,AAE. R. Squibb&Sons, Inc. . . . . . . . . . . . . . . . . .. .. ... ... .....PhA. E. Staley Manufacturing Co. . . . . . . . . . . . . . . . . . .. .. ... ..AA,PA,SCFStandard Oil of California . . . . . . . . . . . . . . . . .. .. ... ... ... ..EnvStandard Oilof Indiana . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ...Ph,PAStandard Oil of Ohio . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .PAStauffer Chemical Co. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ...PASumma Medical Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ..PhSungene Technololgies Corp. (1981) . . . . . . . . . . ... ... ... ...PASybron Biochemical . . . . . . . . . . . . . . . . . . . . . .. .. ... ... ... ..EnvSynbiotex Corp. (1982). . . . . . . . . . . . . . . . . . . .. .. .. ... ... ...Ph,AASyncorlnternational. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ..PhSynergen (1981). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. .. .AA,SCF,CCE,EnvSyngene Products and Research, Inc. . . . . . . . . . . . . . . . . ....AASyntex Corp. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ... ... .Ph,AASyntro Corp. (1982). . . . . . . . . . . . . . . . . . . .. .. .. .. .. ... ... ..AA,CCESyva Co. (1966) . . . . . . . . . . . . . . . . . . . .. .. .. .. .. ... ... .....PhTechniclone international Corp. (1982) . . . . . . . .. ... ... .....PhUnigene Laboratories, inc. (1980). . . . . . . . . . . . . . . . . . . . . . . . .Ph,AAUniversal Foods Corp..... . . . . . . . . . . . . . . . . . .. .. .. ... ... .SCF,PAUniversity Genetics CO. (1980) . . . . . . . . . . . . . . . . . . . . . . . . . . .

Genetic Clinics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ... ....PhU.O.P V Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. .. .. ... ...SCF,CCEThe Upjohn Co. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. ... ..Ph,AA,PAViral Genetics (1981) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .PhWellcome Research Laboratories . . . . . . . . . . . . . . . ... ... ...PhWorne Biotechnology, inc. (1982) . . . . . . . . . . . . . . . . . .. .. ., .PA,CCE,Ph,AA,

Env,SCFXenogen, inc. (1981) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ..Ph,PAXoma Corp. (1981). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ...PhZoecon Corp. (1968) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ..PA,AAZymed Laboratories . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ... ...SCF,CCEZvmos CorD. (1982). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ... .PhSCF

3

9

413

218

5

612

10

5. , . r

aDoes not include support firms.%eeApperrdixD:lrrdexofFirmsinthe UnitedStatesCommerciaikingBiotechnology foradescrlptlonofhowthedatawere

collected.Cph: pharmaceuticals, pA:plant Agriculture, AA: Animal Agriculture, SCF: Specialty Chemicals ~d Food, CCE:CommodltyChemicals and Energy, Env: Environmental (Microbial Enhanced Oil Recovery, Microbial Mining, Pollution Contro~ andToxic Waste Treatement~ El Electronics.

‘AsofMarch1983.‘M.D.s and Ph.D.s.SOURCE: Office of Technology Assessment.

Ch. 4–Firms Commercializing Biotechnology ● 7 1

Figure IO.— Percentage of Firms in theUnited States Pursuing Applications of Biotechnology

in Specific-Industrial Sectors*

140- 620/o

1 1

Total number of companies = 219130

120

110 m= Established companies

l(x) -= New b io technology f i rms

40

30

20

10

0I28°10

20V0

E‘E

● The total percentage of firms exceede W percent bacauea aome compartiasamrapplying biotaohnofogy In mom than one industrial 8eotor,

SOURCE Off Ice of Technology Assessment.

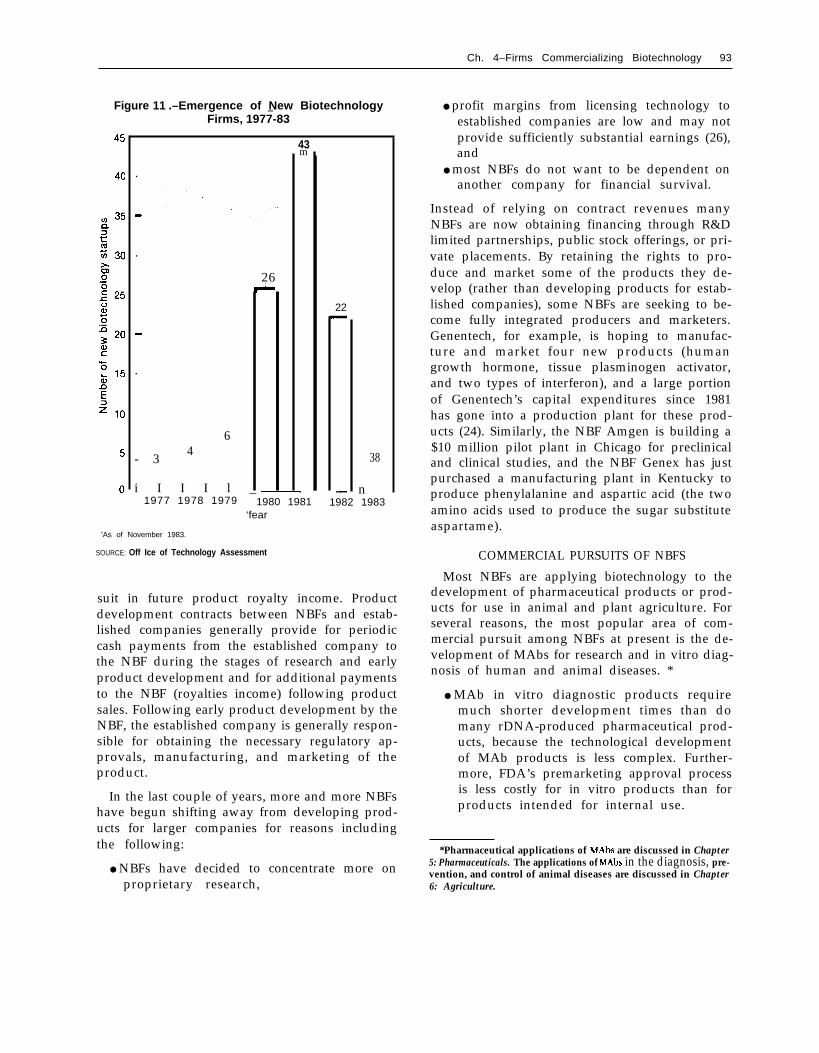

NBFs in Japan will retard those countries’ develop-ment of biotechnology. Varying strategies, organi-zational differences, and cultural factors all con-tribute to the competitive strengths of foreigncountries’ established companies. It is importantto note, however, that the complementary effortsof NBFs and established companies in the UnitedStates have been a major factor in providing theUnited States with an early competitive advantagein the commercialization of biotechnology.

Although there are few NBFs outside the UnitedStates at present, some European countries arebeginning to sense that small firms can make im-portant contributions to innovation, particular-ly in high-technology fields such as biotechnology.Thus, in contrast to the West German Govern-ment, which believes that the development of bio-technology in West Germany is the province ofthe large chemical companies for which the coun-try is noted and that NBFs are “not in line withthe German mentality” (5), the British and FrenchGovernments have aided in the establishment ofsmall firms such as Celltech, (U.K.), AgricuhuralGenetics (U.K.), and Transgene (France’s leadingbiotechnology venture company).

Efforts in support of small company formationare also being undertaken by organizations else-where in Europe. The Organisation for EconomicCoOperation and Development, for example, inan effort to spur technological innovations, hasmade several proposals designed to support smallfirm development (65). These proposals encom-pass the promotion of new sources of venturecapital, assistance to new startups in developinghigh quality feasibility studies, and diverse meas-ures to encourage high-technology startups.

Venture capitalization is almost exclusively anAmerican phenomenon (5,69). Many would agreethat the formation of venture capital and entre-preneurial drive necessary to start small high-technology firms and vigorously commercializeinventions has been inhibited in much of Europeby a historical labor attitude that gives priorityto job security and a predictable business environ-ment rather than to aggressive risk-taking. InJapan, individualism and the creation of small, en-trepreneurial and independent high-technologyfirms appears to be discouraged by cultural traitsemphasizing group identity and acceptance.Large, very successful firms typical of Japan pro-vide workers with a group identity and a senseof security, and it is these firms that are commer-cializing biotechnology in that country.

The biotechnology-related activities of U.S. andforeign companies in the pharmaceutical and ani-mal and plant agriculture sectors are introducedbelow. Also discussed are foreign companies’ bio-technology-related activities in specialty chemi-

72 . Commercial Biotechnology: An International Analysis

cals. Discussion of U.S. private sector activitiesin specialty chemicals, commodity chemicals, andthe environmental and electronics fields is re-served for the chapters in part III. It is importantto recognize that there is no “biotechnology indus-try.” Biotechnology is a set of technologies* thatcan potentially benefit or be applied to severalindustries.

The industrial sector in which the earliest ap-plications of biotechnology have occurred is thepharmaceutical sector. Because of the rapid dif-fusion of the new genetic techniques into phar-maceutical R&D programs, the pharmaceuticalsector is currently the most active in commer-cializing biotechnology. For this reason, the phar-maceutical sector serves as a model for the de-velopment of biotechnology in this chapter andin much of this report, It is important to recognizehowever, that the development of biotechnologyin other industrial sectors will differ from its de-velopment in the pharmaceutical sector. Regula-tory and trade barriers and a marketing and dis-tribution system unique to the pharmaceuticalsector limit the applicability of the model to otherindustrial sectors.

Pharmaceutical industry* *

The pharmaceutical industry is one of the mostsuccessful high-technology sectors of the worldeconomy (80). Because research is the foundationof competitive strength for modern pharmaceu-tical companies (55), and because pharmaceuticalsare the first products to which biotechnology hasbeen applied, the first and perhaps most intenseproving ground for U.S. competitive strength inbiotechnology will be in the area of pharmaceu-ticals.

U.S. COMPANIES

The first applications of biotechnology haveemerged in the area of pharmaceuticals for sev-eral reasons. First, rDNA and MAb technologieswere developed with public funds directed to-ward biomedical research. The first biotechnol-ogy products-MAb in vitro diagnostic kits, rDNA-

“See Chapter 3: The Technologies.“ ‘Applications of biotechnology to the area of pharmaceuticals

are discussed further in Chapter 5: Pharmaceuticals.

produced human insulin, and interferon—are adirect result of the biomedical nature of the basicresearch that led to these new technologies. Sec-ond, pharmaceutical companies have had yearsof experience with biological production methods,and this experience has enabled them to take ad-vantage of the new technologies. Finally, sincesome pharmaceutical products, such as large poly -peptides and antibiotics, can only be producedby biological methods, there are no competingproduction methods that might inhibit the applica-tion of biotechnology to their production.

Pharmaceuticals are profitable products be-cause they are low volume, high-value-addedproducts. * This and other financial considerationssuch as the following have led many U.S. com-panies to apply biotechnology to the phar-maceutical field.

● The time required to develop some phar-maceutical applications of biotechnology, inparticular MAb or DNA probe in vitro diag-nostic products for humans, is much lessthan that required to develop other industrialapplications (except possibly some animalhealth applications).Many of the pharmaceutical products beingdeveloped with biotechnology are replace-ments for or improvements in pharmaceuti-cal products already on the market, and theycan quickly generate income to finance thedevelopment of additional products.The pharmaceutical industry offers highrates of return on both sales and equity andis thus an attractive and profitable industrialsector into which firms might diversify.Many of the biotechnology pharmaceuticalmarkets may be relatively small. Small firmswith limited production and financial re-sources are able to compete more equallywith large firms in small product marketsrather than in large markets, because econ-omies of scale and costs of marketing in smallproduct markets are small.

“Value added is the value that a company adds to goods and serv-ices that it purchases from other companies. It is the difference be-tween the sales revenues and the cost of resources that it has pur-chased from other companies. For a “high-value+ idded” product,therefore, the difference between the resources expended to pro-duce the product and the sales revenues generated by the productis greater than average.

Ch. 4—Firms Commercializing Biotechnology ● 7 3

U.S. pharmaceutical companies are quite activeinternationally. Table 5 illustrates the distributionof sales by the top 20 U.S. and foreign pharma-ceutical companies in 1981. Sales by the U.S. com-panies listed represented almost 60 percent of thetotal pharmaceutical sales for the top 20 pharma-ceutical companies in the world. On the average,almost 42 percent of the sales by these U.S. com-panies were foreign sales. According to the Insti-tute for Alternative Futures, foreign sales ac-counted for roughly 43 percent of total U.S. pre-scription drug sales in 1980 (45), and U.S. phar-maceutical subsidiary sales in foreign countriesexceeded $10 billion in 1980. * Given establishedU.S. pharmaceutical companies’ strong exportperformance in the past, the U.S. posture in worldpharmaceuticals markets will be a subject of greatinterest as biotechnology develops.

Up until about 1976, the average participant inthe U.S. pharmaceutical industry could be de-scribed as a research-based, integrated, multina-tional company that spent (and still does) approx-imately 11.5 percent of its annual pharmaceuticalsales on R&D (67). Since about 1976, the profile

● This figure is from a survey of Pharmaceutical ManufacturersAssociation member companies that had not been published as thisreport went to press.

Table 5.–Distribution of Sales by the Top 20 U.S.

of the participants has changed considerably. Ap-proximately 70 new US. companies have enteredthe pharmaceutical field just to apply biotechnol-ogy. Many of these NBFs are wagering their exist-ence on the success of commercial pursuits of bio-technology in nascent pharmaceutical productmarkets. In total, about 135 U.S. companies—78NBFs and 57 established companies—are knownto be pursuing pharmaceutical product and proc-ess development using biotechnology. *

Since the early 1960’s, the U.S. share of worldpharmaceutical research, innovation, production,sales, and exports has declined, as has the numberof U.S. companies actively participating in thevarious ethical drug markets compared to the

● The high level of US. firms’ interest in pharmaceutical applica-tions of biotechnology is in part a reflection of the large numberof old and new firms producing MAbs. Many companies includedin table 4 are using hybridoma technology to produce MAbs forthe markets traditionally addressed by the pharmaceutical industry.In some cases, OTA did not have sufficient information to deter-mine the specific application for MAbs. For example, some com-panies indicated that they were engaged in the production of MAbs,but would not specify their intended use (i.e., research, separationand purification, diagnostic or therapeutic products for humans,animals, or plants). Because a majority of firms producing MAbsare manufacturing MAbs for pharmaceutical use, OTA placed firmsfor whom data were incomplete in the pharmaceutical sector, eventhough hybridoma technolo~v is also essential to fundamental mo-lecular research on plants, animals, and bacterial systems.

and Foreign Pharmaceutical Companies, 1981

1981 totalPercent of Percent of pharmaceutical Share of

Home sales in sales in other sales pharmaceuticalCompany country home country countries (millions of dollars) sales

American Home Products . . . . . . . . .Merck. . . . . . . . . . . . . . . . . . . . . . . . . . .Bristol-Myers . . . . . . . . . . . . . . . . . . . .Warner Lambert . . . . . . . . . . . . . . . . . .Smith Kline Beckman . . . . . . . . . . . . .Pfizer . . . . . . . . . . . . . . . . . . . . . . . . . . .Eli Lilly . . . . . . . . . . . . . . . . . . . . . . . . .Johnson & Johnson . . . . . . . . . . . . . .Upjohn . . . . . . . . . . . . . . . . . . . . . . . . . .Abbott . . . . . . . . . . . . . . . . . . . . . . . . . .Schering-Plough . . . . . . . . . . . . . . . . .

U s .U s .U s .U s .U s .U s .U s .U s .U s .U s .U s .

Hoechst. . . . . . . . . . . . . . . . . . . . . . . . . F.R.G,Bayer . . . . . . . . . . . . . . . . . . . . . . . . . . . F.R.G.Boehringer-lngleheim . . . . . . . . . . . . . F.R.G.

Ciba-Geigy , . . . . . . . . . . . . . . . . . . . . . Switz.Sandoz. . . . . . . . . . . . . . . . . . . . . . . . . . Switz.Hoffmann-La Roche . . . . . . . . . . . . . . Switz.

Takeda. . . . . . . . . . . . . . . . . . . . . . . . . . Japan

Rhone-Poulenc. . . . . . . . . . . . . . . . . . . France

660/053715559436256626551

282437

253

94

41

440/047294541573844383549727663

989597

6

59

$2,3032,2662,1902,0451,7821,7771,6641,3081,2421,182

924 I

2,5552,4001,197 /1,8911,5151,629 [1,195 )1,008 )

580/o

190/0

160/0

40/03Y0

SOURCE: Adapted from Arthur D. Little, estimates based on publicly available company data.

25-561 0 - 84 - 6

74 . Commercial Biotechnology: An International Analysis

number of foreign firms (80). At least one studyhas suggested that substantially fewer U.S.-orig-inated new chemical entities will appear on themarket in the mid to late 1980’s than are appear-ing today because of a decline in self-originatedinvestigational new chemical entities since themid-1970’s (83). Table 6 indicates the number ofnew pharmaceutical products introduced by theUnited States, four European countries, and Japanin the period 1961-80 and each year since. As thefigures in that table show, the United States andFrance were the leaders in 1961-80, with 23.6 and18.1 percent of new product introductions, re-spectively. They were followed by West Germany,Japan, Switzerland, and the United Kingdom. Theworld leader for the years 1981-83 is Japan, withan average of 27 percent of new product intro-ductions. Although the United States had an aver-age of only 16 percent of new product introduc-tions for the years 1981-83, the drive by NBFs andestablished U.S. companies to apply biotechnologyto the development and production of pharma-ceuticals could help reverse the downward trendin U.S. innovation and thereby contribute to thecompetitive strength of U.S. companies in worldpharmaceutical markets.

FOREIGN COMPANIES

Established European and Japanese companies,following the lead of NBFs and established compa-nies in the United States, are now vigorously pur-suing pharmaceutical applications of biotechnol-ogy. * On average, European companies’ biotechnol-

“Japanese companies are though to have begun making a seriouscommitment to biotechnolo~v as early as late 1981 (7o). West Ger-man companies were among the last European companies to begincommercializing biotechnology and did not intensify their R&.D ef-forts in biotechnology until late 1982. Other European countrieshave paralleled the Japanese in their date of entry into biotech-nolog,v.

ogy R&D budgets lag somewhat behind the budgetsof established U.S. companies and some U.S NBFsas well (see table 7). As biotechnology processes gainwider acceptance in the pharmaceutical industry,however, European manufacturers-e.g., theWest German companies Bayer AG and Hoechst,the Swiss companies Hoffmann-La Roche, CibaGeigy, Sandoz, and the French company RhonePoulenc—are expected to challenge U.S. compa-nies, if for no other reasons than their prevail-ing strength in bioprocessing, their strength ininternational pharmaceutical markets (see table5)* and their intentions to maintain this strength,

*Although no British pharmaceutical companies appear in table5, British companies such as Beecham, Welkome, Glaxo, and ICIare important international manufacturers of biologically produc-ed products and are applying biotechnology to product develop-ment. Additionally, Beecham and Glaxo are amcmg the world’s largestproducers of biologically made products (48).

Table 7.–Biotechnoiogy R&D Budgets for LeadingU.S. and Foreign Companies, 1982s

Biotechnology R&DCompany b budget (millions of dollars)

Hoechst (F. R.G.). . . . . . . . . . . $42C

Schering A.G. (F, R. G.) . . . . . . 4.2Hoffmann-La Roche (Switz.) . 59Schering-Plough (U.S.). . . . . . 60Eli Lilly (U. S.) ... , . . . . . . . . . 60Monsanto (U. S.) . . . . . . . . . . . 62DuPont (U. S.) . . . . . . . . . . . . . 120Genentech (U.S.)* . . . . . . . . . 32Cetus (U.S.)* . . . . . . . . . . . . . . 26Genex (U.S.)* . . . . . . . . . . . . . 8.3Biogen (U.S.)* . . . . . . . . . . . . . 8.7Hybritech (U.S.)* . . . . . . . . . . 5Sumitomo (Japan) . . . . . . . . . 6 +Ajinomoto (Japan) . . . . . . . . . 6 +Suntory (Japan). . . . . . . . . . . . 6 +Takeda (Japan) . . . . . . . . . . . . 6 +Eif-Aquitaine (France) . . . . . . 4 +aBiotechnology R&D figures for Brltlsh companies not available.bCompanie9 with asterisks are NBFs.C1983 figure.SOURCE: Off Ice of Technology Assessment.

Table 6.—introduction of New Pharmaceutical Products by Country of OriginBetween 1961 and 1983

Number of new products introduced by year

Country 1961-80 1981 1982 1983 (est.)

Japan . . . . . . . . . . . . . . . . . . . . . 155 (10.30/0) 15 (23.10/’0) 9 (23.1 0/0) 17 (35.40!0)West Germany. . . . . . . . . . . . . . 201 (13.40/0) 8 (12.30/o) 1 ( 2.60/o) 7 (14.60/o)United States. . . . . . . . . . . . . . . 353 (23.60/o) 9 (13.9”/0) 9 (23.1 ~0) 6 (12.5Yo)France . . . . . . . . . . . . . . . . . . . . 271 (18.1 0/0) 3 (4.60/o) 5 (12.80/o) 5 (10,4!40)United Kingdom . . . . . . . . . . . . — ( — ) 3 (4.60/o) – ( – ) 3 ( 6.20/o)Switzerland . . . . . . . . . . . . . . . . 109 ( 7.3”/0) 6 ( 9.20/o) 4 (10.2%0) –( – )aNurnbOrS In parentheses indicate share of total rwmbr of new pharmaceutical products introduced for the Years indicated.

SOURCE: Nomura Research Institute, “Trends of Biotechnology in Japan,” Tokyo, July 19s3.

Ch. 4—Firms Commercializing Biotechnology . 75

and their increasing shares of worldwide pharma-ceutical R&D expenditures as compared to U.S.companies. (Pharmaceutical R&D expenditures bycountry for the years 1964, 1973, and 1978 areshown in table 8).

The average European company’s involvementin biotechnology is largely characterized byresearch contracts with universities and researchinstitutes rather than by investments in new in-house biotechnology facilities. * Some of the largepharmaceutical companies of Switzerland have,however, begun to make substantial investmentsin biotechnology facilities. Hoffmann-La Roche,for example, spent $59 million on biotechnologyR&D in 1981 (26) and ranks eleventh in world-wide pharmaceutical sales (28). CibaGeigy, whichcommands 3.1 percent of the global drug market,is building a $19.5 million biotechnology centerin Switzerland and a $7 million agriculturalbiotechnology laboratory in North Carolina(11,12).

West German chemical and pharmaceuticalcompanies have been among the last foreign com-panies to move into biotechnology. Many of thecompanies have signed contracts with universitiesinstead of investing in facilities to support theirresearch (10). Some West German companies, in-cluding Schering AG and Boehringer Ingleheim,however, are making significant contributions tothe German biotechnology effort. Schering AG,for example, in a joint agreement with the Stateof Berlin is establishing a $10.7 million instituteof ‘(genetic engineering,” which is regarded as an

● Many of the established U.S. companies have made substantialinvestments in new in-house facilities. See section below on“Established Companies.”

important step for biotechnology research in Ger-many (29).

In terms of total sales, pharmaceutical com-panies in the United Kingdom are not among theworld’s top 20, and historically, the UnitedKingdom has been slow to commercialize the re-sults of much of its basic research. It is impor-tant to note, however, that some British pharma-ceutical companies (e.g., Glaxo and Beecham) pos-sess substantial bioprocessing knowledge, a ca-pability that may provide them with a competitiveadvantage as biotechnology develops. Further-more, some British pharmaceutical companieshave made in-house investments in biotechnology.ICI and Wellcome appear to be among the moststrongly committed of the British pharmaceuticalcompanies commercializing biotechnology. ICI,for example, has the world’s largest continuousbioprocessing plant and is considered an inter-national leader in bioprocessing technology. Thiscompany recently developed a new biodegradablethermoplastic polyester, Biopol@, formed by a ge-netically manipulated microorganism. AlthoughBiopol@ is not a pharmaceutical, it does give someindication of ICI’s innovative capacity in the bio-technology field.

The pharmaceutical and chemical companies ofFrance appear less aggressive than British com-panies in developing biotechnology expertise.Three major French companies have R&D pro-grams in biotechnology-Elf Aquitaine (67-percentGovernmentawned), Rhone Poulenc (l00)-percentGovernment-owned), and Roussel Eclaf (40-per-cent Government-owned and a Hoechst subsid-iary). Of these three, Elf Aquitaine has committedthe most to biotechnology. It owns Sanofi, a phar-

Table 8.-Pharmaceutical R&D Expenditures by Country: 1984, 1973, and 1978

1964 1973 1978Level World share Level World share Level World share

(millions of dollars) (percentage) (millions of dollars) (percentage) (millions of dollars) (percentage)

United States . . . . . . . . $282 60% $640 34% $1,159 28%Federal Republic of Germany 40 310 16 750 18Switzerland ., . . . . . . . . . . . 38 : 244 13 7ooa 17Japan ... ., ., 27 6 236 13 641 15France ... ., . . . . . . . . . . . 28 6 166 9 328 8U n i t e d K i n g d o m . . 29 6 105 6 332 8a EstimatedNote Data are m current dollars and represent expenditures for both human and veterina~ research

SOURCE National Academy of Sciences, The CompetWe Status of the U S Pharmaceutical Industry Washington, O C , 1983

76 . Commercial Biotechnology: An International Analysis

maceutical company that is applying biotechnol-ogy to human and animal health in areas includingdiagnostics, neuropeptides, serums, vaccines, andantibiotics, and has established Elf-Bioindustriesand E1f-Bioresearch to develop biotechnology inthe foodstuffs and agriculture sectors. To supportsome of its new biotechnology R&D, Elf is cur-rently building a $10 million “genetic engineer-ing” plant (5). Rhone Poulenc is the world’s secondlargest producer of animal health products (84)and is considered to be the second most com-mitted of the three French companies activelycommercializing biotechnology (50). To supportits biotechnology effort, in 1980, Rhone Poulencestablished a small specialty biotechnology sub-sidiary named Genetica.

Despite the efforts of companies such as Elf andRhone Poulenc, the initial hesitation France ex-pressed in the early stages of biotechnology de-velopment has put French companies at a distinctdisadvantage internationally, particularly vis-a-visU.S. companies. The French Government has aformal policy designed to promote biotechnology,but it is not clear that whatever impetus thispolicy provides will be great enough to compen-sate for France’s slow entry into biotechnology.Historically, the French Government’s plans topromote national champions (e.g., the Plan Calcul,the Concord) have failed. As the pace of biotech-nology commercialization quickens, a strong pri-vate sector effort may be necessary in order tolaunch France into a more competitive position.

Overall, Europe is considered to be fartherbehind the United States in the application of bio-technology to product-related research areas thanin fundamental research (23). Strong commercial-ization efforts by the major chemical companiesof West Germany or by the pharmaceutical com-panies of Switzerland or the United Kingdom,however, could significantly improve West Ger-many’s, Switzerland’s, or the United Kingdom’scurrent competitive positions in the commer-cialization of pharmaceutical applications of bio-technology.

Some would argue that large companies havean inertia that is difficult or impossible to change,making rapid changes in research policy and di-rection impracticable (5). To the extent that large

companies pursuing pharmaceutical applicationsof biotechnology in Europe lack the dynamismand flexibility to compete with the combined ef-forts of NBFs and established companies in theUnited States, Europe could initially beat a com-petitive disadvantage. If the timing of market en-try for therapeutic and diagnostic products be-comes the most important factor in competitionfor market share and market acceptance, how-ever, the marketing strength of the Europeanmultinationals could help balance competition inpharmaceuticals between the United States andEurope.

The potential competitive challenge that will bemounted by Japan in the area of pharmaceuticalsis more difficult to estimate than the challengefrom the European countries for two reasons: 1)Japanese pharmaceutical companies such as Ta-keda, Sumitomo Chemical, Mitsubishi Chemicalstraditionally have not had a significant presencein world pharmaceutical markets (55); and 2) pres-ent Japanese commercialization efforts, most be-ing proprietary, are difficult to assess either quan-titatively or qualitatively. One set of factors char-acterizing Japanese efforts to apply biotechnologyto pharmaceutical development suggests a ratherformidable challenge facing U.S. companies in fu-ture biotechnology-related pharmaceutical mar-kets, while a different set of factors suggests lessof a future challenge. Each set of factors is dis-cussed in turn below.

Factors that suggest that Japan will have inter-national competitive advantages in the applicationof biotechnology to pharmaceutical developmentinclude the following:

● The application of biotechnology to pharma-ceuticals in Japan has stimulated the involve-ment in pharmaceuticals of many Japanesecompanies from a broad variety of bioproc-ess-based industries. Table 9 shows the diver-sification of Japanese chemical, food process-ing, and textile and pulp processing com-panies into pharmaceuticals.

A 1982 Keidanren* survey of 132 Japanese com-panies using biotechnology found that 83 percent

“Keidanren, the Japan Federation of Economic Organizations, isa national organization composed of about 700 of the largest

—

Ch. 4—Firms Commercializing Biotechnology 77

Table 9.—Diversification of Japanese Chemical,Food Processing, Textile, and Pulp Processing

Companies Into Pharmaceuticals

Company Pharmaceutical field of entry

Chemical companies:Sunstar. . . . . . . . . . . . . . . . . .Hitachi Chemical . . . . . . . . .Hokko Chemical Industry . .Mitsubishi Chemical

Industries . . . . . . . . . . . . . .

Denki Kagaku Kogyo . . . . . .Sumitomo Chemical . . . . . . .

Daicel . . . . . . . . . . . . . . . . . . .Mitsubishi Petrochemical

Industries . . . . . . . . . . . . . .Chisso . . . . . . . . . . . . . . . . . .Mitsui Toatsu Chemical . . .

Food processing companies:Ajinomoto . . . . . . . . . . . . . . .Suntory. . . . . . . . . . . . . . . . . .

Meiji Seika Kaisha . . . . . . . .Sanraku-Ocean . . . . . . . . . . .Kikkoman Shoyu . . . . . . . . . .

Takara Shuzo . . . . . . . . . . . . .Meiji Milk Products ., . . . . .

Yakult Honsha. . . . . . . . . . . .

Kyowa Hakko Kogyo . . . . . .

Kirin-Seagrams . . . . . . . . . . .Kirin Brewery. ., . . . . . . . . . .Sapporo Breweries ... , . . . .Toyo JO ZO . . . . . . . . . . . . . . .Morinaga & Co. . . . . . . . . . . .

Snow Brand Milk Co. . . . . . .

Textile and pulp companies:Asahi Chemical Industry . . .Toray Industries . . . . . . . . . .Teiji Limited . . . . . . . . . . . . .Kirin-Seaarams . . . . . . . . . . .

Antibiotics, interferonAntibiotics, vaccinesAntibiotics

Physiologically activeagents, anticancer drugs,diagnostic reagents,monoclinal antibodies

Physiologically active agentsMonoclinal antibodies,

interferon, growthhormone

Anticancer drugs

Diagnostic reagentsDiagnostic reagentsUrokinase

AntibioticsAntibiotics, interferon,

anticancer drugs, drugsfor treatment of highblood pressure

Antibiotics, interferonAntibioticsPhysiologically active

agents, antibiotics,immune suppressors

Physiologically active agentsPhysiologically active

agents, interferonPhysiologically active

agents, anticancer drugs,diagnostic reagents forliver cancer

Physiologically activeagents, interferon

InterferonAnticancer drugsAnticancer drugsImmune suppressorsDiagnostic reagents for liver

cancer, drugs fortreatment of high bloodpressure

Interferon

InterferonInterferonInterferonInterferon

SOURCE: Office of Technology Assessment.

Japanese companies. It enjoys the regular and active participationof the top business leaders working closely with a large professionalstaff to forge agreements on behalf of business as a whole. It oftensurveys its members on issues of economic importance.

of the 60 companies that responded were pursu-ing applications in the area of pharmaceuticals(70), compared to only 62 percent of U.S. com-panies (see table 4). Intensified competition is ex-pected to push technical advances in the area ofpharmaceuticals along in Japan at a rate that iscomparable to or greater than the rate in theUnited States. Among the companies using bio-technology in Japan, it is already a widely ac-cepted view that Japan can catch up with theUnited States within 5 years. This point is verywell illustrated by the Nikkei Sangyo Shirnbun(Japan Industrial Daily) survey undertaken in June1981. According to the survey, 48 percent of the128 responding firms thought Japan could catchup to the United States in the commercial develop-ment of biotechnology in 5 years, and 24 percentestimated that catching up would take only 2 to3 years (57).

● The Government of Japan, which has tar-geted the pharmaceutical industry for inter-national expansion, has improved the en-vironment for pharmaceutical innovation,and thus, for the application of biotechnol-ogy.

The Japanese Government through targeting ofthe pharmaceutical industry, changes in patentlaws to prevent imitation, and pricing policies inthe Government-administered national health in-surance system has begun an effort to coordinatetrade, pricing, and health care policies to promotepharmaceutical innovation and overseas expan-sion (74). These Government efforts are expectedto facilitate the application of biotechnology in theJapanese pharmaceutical industry.

● Joint pharmaceutical research projects andcollaborative arrangements among compa-nies, sometimes in conjunction with Govern-ment research institutions, promote biotech-nology transfer throughout Japanese indus-try and accelerate the pace of technical ad-vances. Table 10 provides a list of some Japa-nese joint ventures in pharmaceuticals de-rived from the Keidanren survey of 1982.

As early as 1979, the Japanese Ministry of Healthset up a study group between Green Cross andToray Industries to speed the development ofinterferon, because the Ministry had concluded

78 . Commercial Biotechnology: An International Analysis

Table 10.–Japanese Joint Ventures in Pharmaceutical Applications of Biotechnology

Companies Product area

Otsuka PharmaceuticallHayashibara/MochidaPharmaceutical . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Production of alpha, beta, and gamma interferon

Yamanouchi PharmaceuticallAjinomoto . . . . . . . . . . . . . . . . Large-scale production of thrombolytic agentYoshitomo Pharmaceutical/Takeda Chemical. . . . . . . . . . . . Large-scale production of thrombolytic agentAjinomotolMorishita Pharmaceutical . . . . . . . . . . . . . . . . . . . R&D on pharmaceuticalsYoshitomi Pharmaceutical Industries, Ltd./Yuki Gosei Kogyo Co., Ltd. . . . . . . . . . . . . . . . . . . . . . . . . . . . Developing rDNA products for circulatory systemTakara Shuzo/Taiho Pharmaceutical . . . . . . . . . . . . . . . . . . . Development of heart drugs using rDNAToray lndustrieslKyowa Hakko KogyolGan Kenkyu Kai

(Cancer Research Association) . . . . . . . . . . . . . . . . . . . . . . Development of beta and gamma interferon by rDNAAsahi Chemical lndustrylDainippon Pharmaceutical/Tokyo

University . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . R&D on alpha and gamma interferonToray lndustrieslDaiichi Seiyaku Co., Ltd. . . . . . . . . . . . . . . Using rDNA to produce gamma interferonAjinomoto~akeda Chemical Industries, Ltd. . . . . . . . . . . . . Development of interleukin-2Asahi Chemical Industries Co., Ltd./Dainippon Pharmaceutical Co. . . . . . . . . . . . . . . . . . . . . . . . . Development of tissue necrotic factorSOURCE: Office of Technology Assessment.

that the separate approach being taken was costlyboth in terms of funds expended and time taken(73). Many other examples of technical collabo-ration in biotechnology in Japan can be cited, andmany more Japanese companies have intentionsto cooperate with one another in research or de-velopment and/or in commercialization in the fu-ture. In 1981, a scientist from the FermentationResearch Institute of Japan’s Ministry of Interna-tional Trade and Technology acknowledged thatalmost half of the companies who work or intendto work in “genetic engineering” will cooperateor have already cooperated in some biotechnologyactivities (79). Joint ventures such as those listedin table 10 might provide Japanese companieswith commercial advantages for two reasons: 1)each firm participating in the venture brings dif-ferent resources and expertise to the project,thereby making the group effort more efficient;and 2) the intention of some of the joint venturesis to secure patents in fields not yet pre-emptedby foreign competition (e.g., new host-vector sys-tems and sophisticated sensors for bioprocessing)or to undertake joint clinical testing (70).

● Japan’s share of world pharmaceutical R&Dexpenditures has been increasing steadilysince 1964 (see table 8) as has its share of theworldwide total of newly introduced pharma-ceuticals (see table 6).

In 1981, Japanese companies ranked first in termsof the largest number of major new drugs intro-duced into world markets, being responsible for15 (23 percent) of the 65 newly introduced phar-

maceuticals (see table 6). In 1982, Japanese com-panies again accounted for roughly 23 percentof the new pharmaceutical products introduced.They also accounted for over 16 percent of allU.S. patents issued for pharmaceutical andmedicinal products and for 38 percent of all U.S.pharmaceutical and medicinal patents granted toforeign firms (14).

● Japanese companies applying biotechnologyto pharmaceutical development (in contrastto U.S. companies) appear to be dedicatingrelatively more research effort to the laterstages of commercialization (i.e., bioprocess-ing) and cancer treatment. Seventy-five per-cent of all Japanese medical and drug com-panies are engaged in MAb research, and alarge proportion of the MAb R&D is targetedtoward developing a “magic bullet” for cancertreatment, monitoring bioprocesses, and re-covering pioteins (70).

Factors that suggest that the Japanese may nothave significant advantages in future biotechnol-ogy-related pharmaceutical markets include thefollowing:

● Barriers to entering foreign pharmaceuticalmarkets are high, and Japanese companiesat present have neither distribution channelsin place nor a sufficient sales force to per-mit aggressive marketing of pharmaceuticalproducts in Western markets.

Japanese companies’ lack of distribution channelsin Western pharmaceutical markets is one fac-

Ch. 4—Firms Commercializing Biotechnology ● 7 9

tor that has limited Japanese companies’ abilityto penetrate these markets. It is expected that themode by which Japanese companies will pene-trate these markets in the future will be throughjoint ventures with U.S. or European companiesthat allow Japanese companies to take advantageof existing distribution channels. * Although Japa-nese companies tend to seek opportunities to pen-etrate foreign markets directly through manufac-turing subsidiaries rather than through licensingcontracts, only two Japanese companies haveestablished equity joint ventures with U.S. firms * *and only three have established U.S. subsidiaries. * * *However, the international expansion of Japan’spharmaceutical industry has only just begun.

Almost half of the Japanese companies nowusing biotechnology - expect to “catch up”technologically to the United States in 5 years.These companies therefore intend to set theirown R&D and commercialization targetsbeyond the 5-year catch-up period at consid-erable commercial risk.

The intention of Japanese companies to catch upto U.S. companies and to set their own R&D tar-gets is a unique phenomenon. In the past, evenin high- technology fields such as computers andelectronics, the R&D and commercialization tar-gets have been demonstrated in advance by U.S.and Western European companies, so Japanesecompanies have not had to worry about the mar-ketability of their R&D and commercialization ef-forts. By selecting the best technology availableand refining it, Japanese companies have beenable to minimize the time required to catch upwith the front runners and sometimes surpassthem at the product marketing stage (70). Giventhe lack of established commercial targets in bio-technology and considering the barriers to enter-ing foreign pharmaceutical markets mentioned

● In support of this expectation is a study by the Japanese Pro-ductivity Center in 1982 of the potential for Japanese drug firmsin the United States. The study estimated that the establishmentof a U.S. subsidiary by a Japanese company would require an in-vestment of about $80 million over a 4-year period. The study recom-mended that Japanese companies form joint ventures with U.S. com-panies rather than establish a Japanese company or purchase a U.S.company (75).

* *Takeda with Abbott (U. S.) and Fujisawa with SmithKline (U.S.).* ● *The three U.S. subsidiaries are Daiichi Pharmaceutical Corp.,

Otuska Pharmaceutical, and Alpha Therapeutics (subsidiary of GreenCross),

above, it cannot be assumed that the Japanese willbe major competitors in biotechnology-relatedpharmaceutical markets.

Japan’s traditional bioprocess-based indus-tries, including pharmaceuticals, rely large-ly on conventional microbiology, genetics,and bioprocess feedstocks. These traditionalapproaches in bioprocessing could be chal-lenged by new biotechnology (4 I).

Japan is considered to be behind the United Statesin fundamental biology. This weakness in funda-mental biology could reduce the potential compet-itive threat of Japanese companies applying bio-technology to pharmaceutical development.

● Biotechnology R&D investments by Japanesecompanies are still low in comparison to theinvestments by U.S. companies.

Although Japan’s aggregate investment in phar-maceutical R&D has increased steadily since 1964,investments by individual Japanese companies inbiotechnology R&D are still low compared to in-vestments by NBFs and established companies inthe United States (see table 7). According to theNikkei SazIgyo Shiznbun survey (June 1981) andthe Keidanren survey (1982), only 5 Japanesecompanies spent more than $6 million per year ,on biotechnology R&D. The average R&D ex-penditure of 49 of the 60 Japanese companies thatresponded to the Keidanren survey was under$1 million. Although it is difficult to translate R&Dinvestment into commercial success, on a quan-titative basis, Japan falls far behind the UnitedStates in terms of industrial expenditures on bio-technology research.

Animal agriculture industry*

U.S. COMPANIES

The animal agriculture industry encompassescompanies engaged in the manufacture of prod-ucts, the prevention and control of animal dis-eases, animal husbandry, growth promotion, andgenetic improvement of animal breeds. The com-panies that dominate the production of most ani-mal health products are established U.S. and

● Applications of biotechnology to animal agriculture are discussedfurther in Chapter 6: Agriculture.

80 ● Commercial Biotechnology: An International Analysis

foreign pharmaceutical and chemical compa-nies. ” Most of these companies have global mar-keting and distribution networks and undertakeanimal drug production as a diversification oftheir principal activities. In recent years, the ad-vent of biotechnology, the rising industrializationof animal agriculture, and changing dietary habitsin foreign countries have increased the demandsfor improvements in old products and for com-pletely new products. NBFs may have a major roleto play in expanding animal health markets.

Sixty-one companies in the United States areknown to be pursuing animal health related appli-cations of biotechnology, as shown in table 4.Thirty-four (56 percent) of these companies areNBFs. Of special note is the role new firms ap-pear to be playing in three major segments of theindustry-diagnostic products, growth promo-tants, and vaccines. possible explanations for whysome NBFs might be interested in these three ani-mal health markets include the following:

●

●

●

●

Recombinant DNA methods used to makehuman vaccines are suited to making safeand effective animal vaccines against bothviral and bacterial infections, just as the MAbor DNA probe technology used to producehuman products is suited to making passivevaccines or diagnostic products for ani-mals. * *The markets for many animal health prod-ucts (e.g., vaccines or diagnostic products) arerelatively small and therefore allow NBFs tocompete equally with larger companies with-out suffering from scale disadvantages.The commercial introduction of veterinaryvaccines can generally be achieved morequickly than can that of human therapeuticproducts. The regulatory process allowing

● Major U.S. producers of animal health products include Syntex,Pfizer, Eli Lilly, Upjohn, SmithKline Beckman, American Cyanamid,Merck, Johnson & Johnson, Tech America, and Schering-Plough.Major foreign producers include Burmn@s-Wellcome (U.K.), Rhone-Merieux (France), Hoechst AG (F.R.G.), Bayer AC (F.R.G,), Connaught(Canada), Beecham (U.K.), Solvay (Belgium), Boehringer Ingleheim(F. R.G.), Intervet (Netherlands), and Elf Aquitaine (France).

● *The NBFs Chiron and Cetus both became involved in the vet-erinary products business as extensions of their research in the fieldof human health care (17,20). The NBF Monoclinal Antibodies, Inc.,as a spinoff from research on detection kits for human pregnancyand ovulation, is developing an ovulation detection kit for large ani-mals which will be useful in animal breeding management.

veterinary vaccines to enter the market typi-cally can be completed in about 1 year (17).Thus, the lower costs of commercializationfor veterinary vaccines in comparison tohuman pharmaceuticals and the potential forshort-term product revenues may reduceNBFs’ financial need to collaborate extensive-ly with established companies. *Some veterinary vaccine research (e.g., on fe-line leukemia vaccines) could serve a~ a mod-el for developing human vaccines for simi-lar viruses that could launch some NBFs intothe more profitable human pharmaceuticalmarkets.

The fact that 34 of the 61 U.S. companies pur-suing applications of biotechnology in animalagriculture are NBFs suggests the evolution of anexpanding animal health market in which NBFssuch as Molecular Genetics, Inc. (MGI), Amgen,Chiron, Bio-Technology General and Cetus per-ceive opportunities. In contrast to human phar-maceutical products, animal vaccines and diag-nostic products are in many cases being devel-oped by NBFs independently of established U.S.or foreign companies.

In the development of animal growth promot-ants, however, established U.S. companies aremore involved. The market for animal growthpromotants is the second fastest growing marketin the animal health field, and because it may bethe most significant commercial development area(26), it is also one of the most competitive. Globalsales for growth promotants are expected toreach $515 million by 1985 (84). Several estab-lished U.S. companies, including American Cyana-mid, Eli Lilly, Monsanto, and Norden (a subsidiaryof SmithKline Beckman), have displayed interestin the field by sponsoring research contracts withNBFs such as MGI, Biotechnica International,Genentech, and Genex. Other established U.S.companies have shown interest by conducting ini-tial evaluations of growth promotants developedby NBFs, as Eli Lilly did in the case of a productdeveloped by the NBF Biotechnology General.

In an effort to expand their own technical capa-bilities and reach new product markets, some es-

“Collaborative ventures between NBFs and established U.S. andforeign companies are discussed further below.

Ch. 4–Firms Commercializing Biotechnology ● 8 1