Embed Size (px)

Citation preview

Pair Trade: Long SAP - Short Dassault Systèmes

Tuesday, October 30th 2012

Investment Case

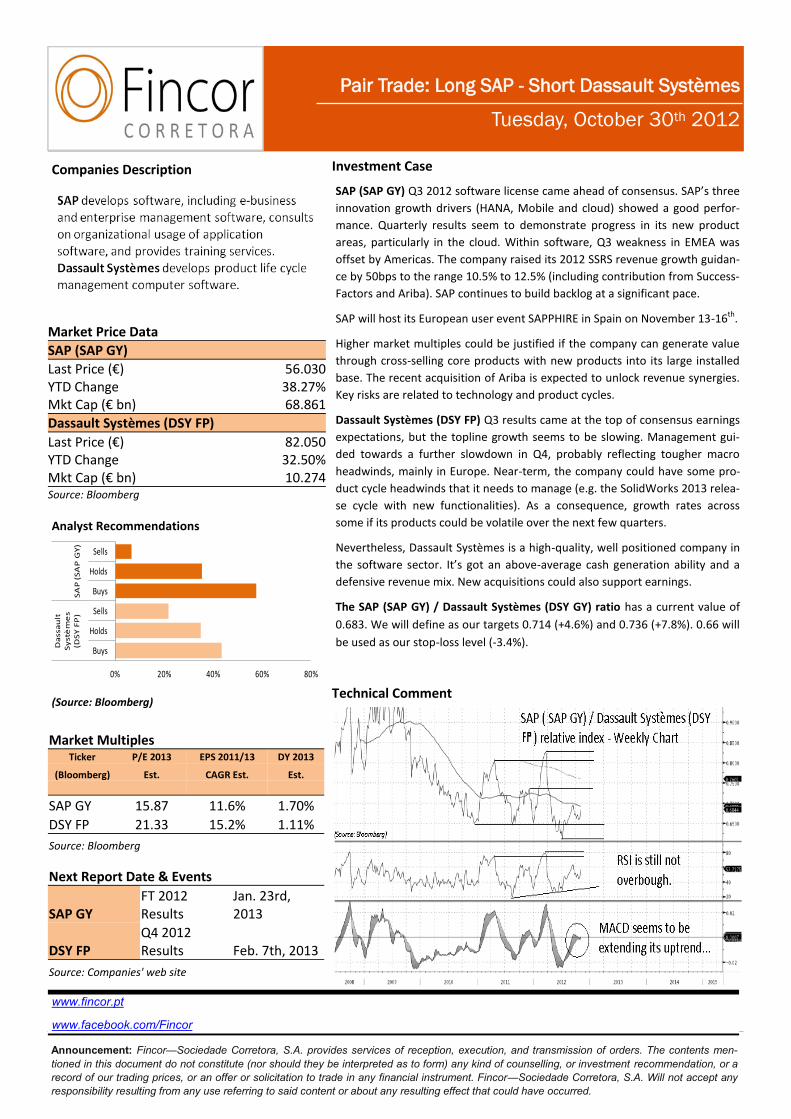

Technical Comment

Announcement: Fincor—Sociedade Corretora, S.A. provides services of reception, execution, and transmission of orders. The contents men-

tioned in this document do not constitute (nor should they be interpreted as to form) any kind of counselling, or investment recommendation, or a

record of our trading prices, or an offer or solicitation to trade in any financial instrument. Fincor—Sociedade Corretora, S.A. Will not accept any

responsibility resulting from any use referring to said content or about any resulting effect that could have occurred.

www.fincor.pt

www.facebook.com/Fincor

Companies Description

Analyst Recommendations

(Source: Bloomberg)

Market Multiples Ticker P/E 2013 EPS 2011/13 DY 2013

(Bloomberg) Est. CAGR Est. Est.

SAP GY 15.87 11.6% 1.70%

DSY FP 21.33 15.2% 1.11%

Source: Bloomberg

Market Price Data

SAP (SAP GY)

Last Price (€) 56.030 YTD Change 38.27% Mkt Cap (€ bn) 68.861

Dassault Systèmes (DSY FP)

Last Price (€) 82.050 YTD Change 32.50% Mkt Cap (€ bn) 10.274 Source: Bloomberg

Next Report Date & Events

SAP GY FT 2012 Results

Jan. 23rd, 2013

DSY FP Q4 2012 Results Feb. 7th, 2013

Source: Companies' web site

SAP (SAP GY) Q3 2012 software license came ahead of consensus. SAP’s three

innovation growth drivers (HANA, Mobile and cloud) showed a good perfor-

mance. Quarterly results seem to demonstrate progress in its new product

areas, particularly in the cloud. Within software, Q3 weakness in EMEA was

offset by Americas. The company raised its 2012 SSRS revenue growth guidan-

ce by 50bps to the range 10.5% to 12.5% (including contribution from Success-

Factors and Ariba). SAP continues to build backlog at a significant pace.

SAP will host its European user event SAPPHIRE in Spain on November 13-16th.

Higher market multiples could be justified if the company can generate value

through cross-selling core products with new products into its large installed

base. The recent acquisition of Ariba is expected to unlock revenue synergies.

Key risks are related to technology and product cycles.

Dassault Systèmes (DSY FP) Q3 results came at the top of consensus earnings

expectations, but the topline growth seems to be slowing. Management gui-

ded towards a further slowdown in Q4, probably reflecting tougher macro

headwinds, mainly in Europe. Near-term, the company could have some pro-

duct cycle headwinds that it needs to manage (e.g. the SolidWorks 2013 relea-

se cycle with new functionalities). As a consequence, growth rates across

some if its products could be volatile over the next few quarters.

Nevertheless, Dassault Systèmes is a high-quality, well positioned company in

the software sector. It’s got an above-average cash generation ability and a

defensive revenue mix. New acquisitions could also support earnings.

The SAP (SAP GY) / Dassault Systèmes (DSY GY) ratio has a current value of

0.683. We will define as our targets 0.714 (+4.6%) and 0.736 (+7.8%). 0.66 will

be used as our stop-loss level (-3.4%).

0% 20% 40% 60% 80%

Buys

Holds

Sells

Buys

Holds

Sells

Da

ssa

ult

S

yst

èm

es

(DS

Y F

P)

SA

P (

SA

P G

Y)