Embed Size (px)

Citation preview

Retail Investor Presentation

Long Gate S.C.

Ellicott City, MD

North America’s Largest Owner & Operator of

Neighborhood & Community Shopping Centers

The statements in this presentation, including targets and assumptions, state the Company’s and management’s hopes, intentions, beliefs,

expectations or projections of the future and are forward-looking statements. It is important to note that the Company’s actual results could

differ materially from those projected in such forward-looking statements. Factors that could cause actual results to differ materially from

current expectations include the key assumptions contained with this presentation, general economic conditions, local real estate

conditions, increases in interest rates, foreign currency exchange rates, increases in operating costs and real estate taxes. Additional

information concerning factors that could cause actual results to differ materially from those forward-looking statements is contained from

time to time in the Company’s SEC filings, including but not limited to the Company’s report on Form 10-K. Copies of each filing may be

obtained from the Company or the SEC.

Safe Harbor

Mesa Riverview

Mesa, AZ

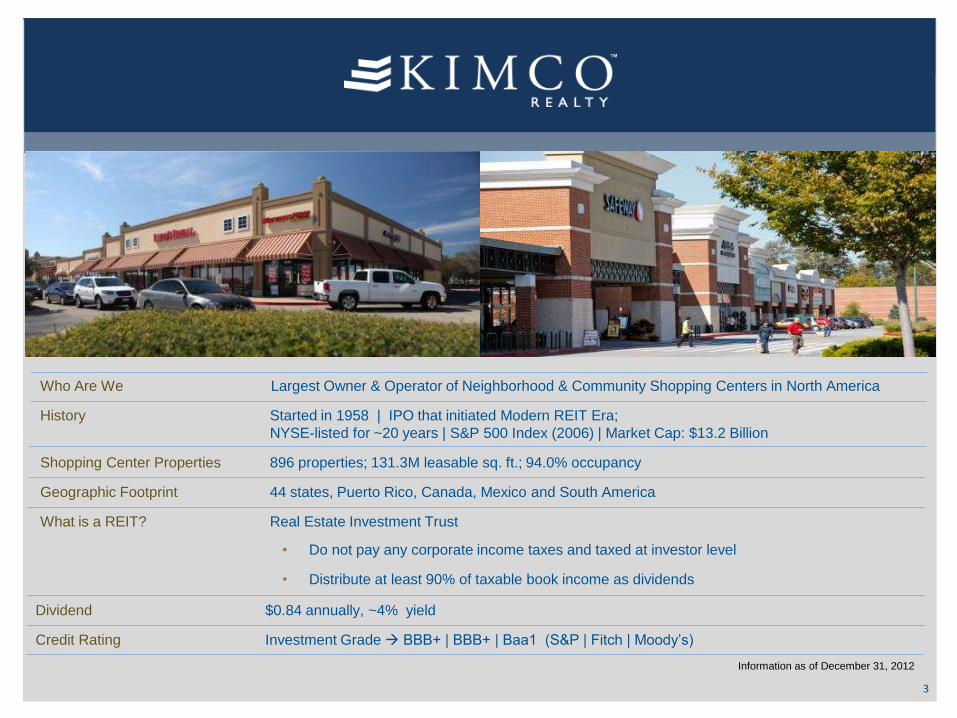

Who Are We Largest Owner & Operator of Neighborhood & Community Shopping Centers in North America

History Started in 1958 | IPO that initiated Modern REIT Era;

NYSE-listed for ~20 years | S&P 500 Index (2006) | Market Cap: $13.2 Billion

Shopping Center Properties 896 properties; 131.3M leasable sq. ft.; 94.0% occupancy

Geographic Footprint 44 states, Puerto Rico, Canada, Mexico and South America

What is a REIT? Real Estate Investment Trust

Information as of December 31, 2012

3

• Do not pay any corporate income taxes and taxed at investor level

• Distribute at least 90% of taxable book income as dividends

Dividend $0.84 annually, ~4% yield

Credit Rating Investment Grade BBB+ | BBB+ | Baa1 (S&P | Fitch | Moody’s)

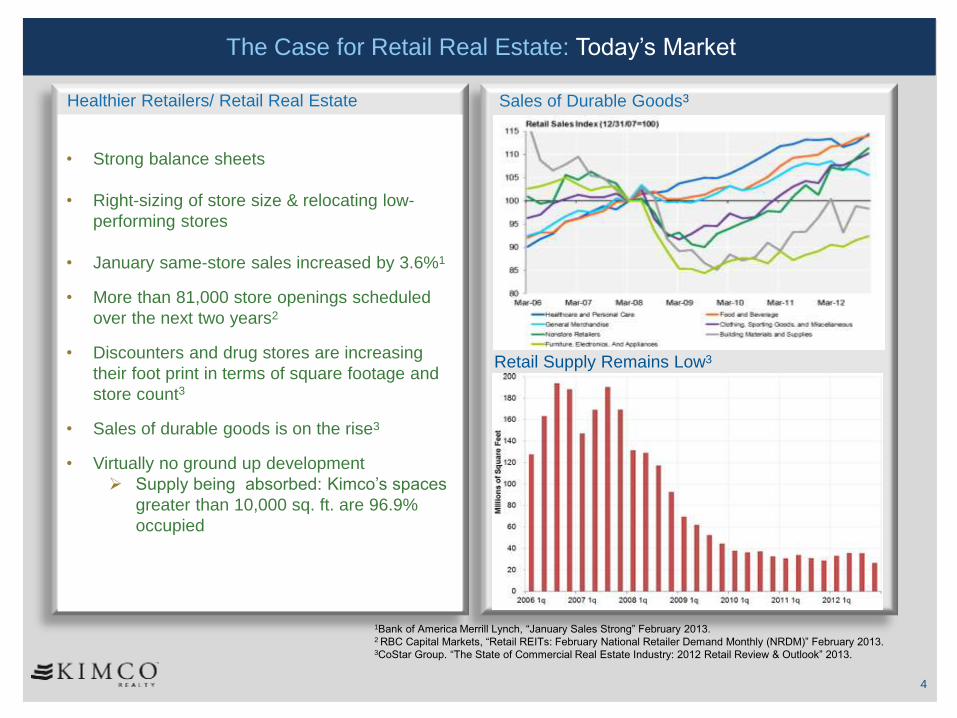

1Bank of America Merrill Lynch, “January Sales Strong” February 2013.

2 RBC Capital Markets, “Retail REITs: February National Retailer Demand Monthly (NRDM)” February 2013.

3CoStar Group. “The State of Commercial Real Estate Industry: 2012 Retail Review & Outlook” 2013.

• Strong balance sheets

• Right-sizing of store size & relocating low-

performing stores

• January same-store sales increased by 3.6%1

• More than 81,000 store openings scheduled

over the next two years2

• Discounters and drug stores are increasing

their foot print in terms of square footage and

store count3

• Sales of durable goods is on the rise3

• Virtually no ground up development

Supply being absorbed: Kimco’s spaces

greater than 10,000 sq. ft. are 96.9%

occupied

Retail Supply Remains Low3

Sales of Durable Goods3

The Case for Retail Real Estate: Today’s Market

Healthier Retailers/ Retail Real Estate

4

Millside Plaza

Delran, New Jersey

5

Shopping Center Portfolio

Westlake Shopping Center

Daly City, CA

Note: Amounts are shown on gross basis. Centers & square footage include properties not in

occupancy. Information as of December 31, 2012.

North American Footprint of Quality Assets

Canada United States Mexico

• 66 centers

• 12.4M sq. ft.

• $15.98 per sq. ft.

• 96.7% occupancy

• Top tenants:

TJ Maxx

Canadian Tire

Target

• 759 centers

• 106.2M sq. ft.

• $13.18 per sq. ft.

• 94.1% occupancy

• Top tenants:

TJ Maxx

Home Depot

Wal-Mart

• 56 centers

• 11.9M sq. ft.

• $9.97 per sq. ft.

• 89.7% occupancy

• Top tenants:

Wal-Mart

Cinepolis

HEB

Faubourg Boisbriand

Boisbriand, Quebec, Canada

Long Gate S.C.

Ellicott City, MD Magnocentro 26

Huixquilucan, EM

6

7

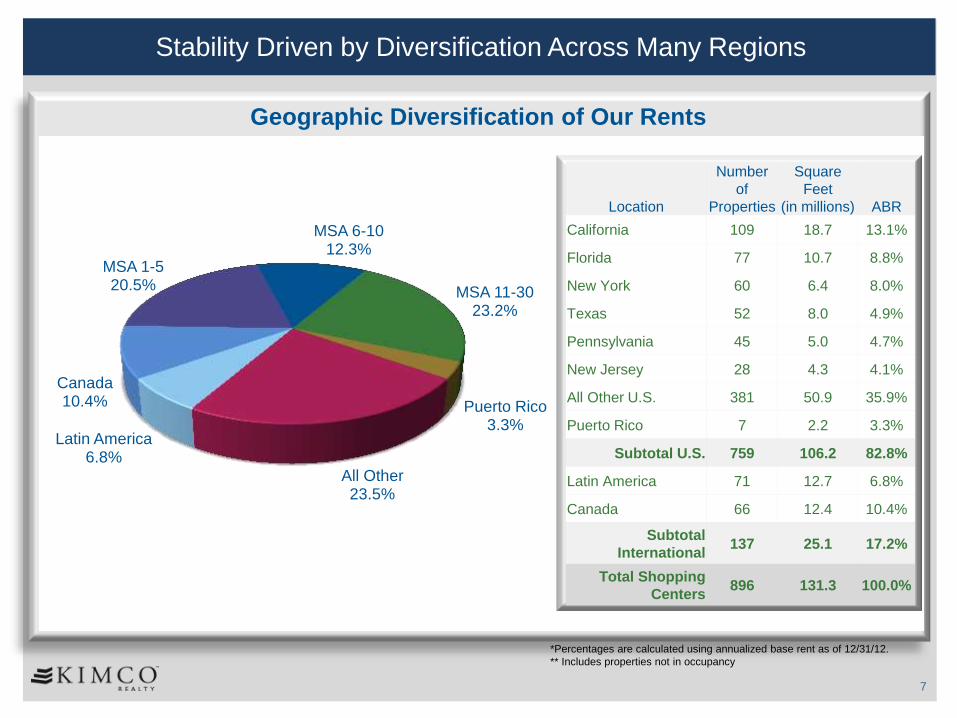

Stability Driven by Diversification Across Many Regions

Geographic Diversification of Our Rents

Latin America 6.8%

Canada 10.4%

MSA 1-5 20.5%

MSA 6-10 12.3%

MSA 11-30 23.2%

Puerto Rico 3.3%

All Other 23.5%

Location

Number

of

Properties

Square

Feet

(in millions) ABR

California 109 18.7 13.1%

Florida 77 10.7 8.8%

New York 60 6.4 8.0%

Texas 52 8.0 4.9%

Pennsylvania 45 5.0 4.7%

New Jersey 28 4.3 4.1%

All Other U.S. 381 50.9 35.9%

Puerto Rico 7 2.2 3.3%

Subtotal U.S. 759 106.2 82.8%

Latin America 71 12.7 6.8%

Canada 66 12.4 10.4%

Subtotal

International 137 25.1 17.2%

Total Shopping

Centers 896 131.3 100.0%

*Percentages are calculated using annualized base rent as of 12/31/12.

** Includes properties not in occupancy

* Percentages are calculated using annualized base rent as of 12/31/12.

Only 14 tenants with rent exposure greater than one percent

8

Tenant Overview

3.0%

2.9%

2.6%

2.0%

1.7%

1.6%

1.5%

1.5%

1.4%

1.2%

1.2%

1.2%

1.2%

1.1%

Well staggered lease maturity

with limited rollover in any given

year that averages about 8%

over the next 10 years.

Approx. 14,900 leases

with 8,400 tenants

Company Rating

S&P/ Moody’s

Home Depot A-/A3

TJX Companies A/A3

Wal-Mart AA/Aa2

Kmart/Sears

Holdings CCC+/B3

Bed Bath & Beyond BBB+/NR

Royal Ahold BBB/Baa3

Kohl’s BBB+/Baa1

Best Buy BB/Baa2

Petsmart BB+/NR

Costco A+/A1

Ross Stores BBB+//NR

Safeway BBB/Baa3

Michaels B/B2

Dollar Tree NR/NR

Solid tenant mix with good credit quality tenants

National Breath/Regional Depth- Experienced Management Team

9

Paul Puma, President

Southern Region

142 Properties

GLA: 22.7M sq. ft.

Occupancy: 93.1%

• Strong relationship network

• Knowledge of buyers/sellers

• Direct-market transaction opportunities

• Smoother approval process with local officials

Regional Presidents build portfolio value with:

• Experience: average 25 years in retail real estate

• Local market expertise

• Consumer preferences & trends

• Market-specific risk assessment

• Acquisitions & redevelopment opportunities

Localized Operating Approach

Rob Nadler, President

Central Region

167 Properties

GLA: 23.7M sq. ft.

Occupancy: 95.5%

Tom Simmons, President

Eastern Region

258 Properties

GLA: 28.0M sq. ft.

Occupancy: 95.8%

Conor Flynn, President

Western Region

192 Properties

GLA: 31.8M sq. ft.

Occupancy: 92.2 %

Note: GLA and occupancy shown on gross basis.

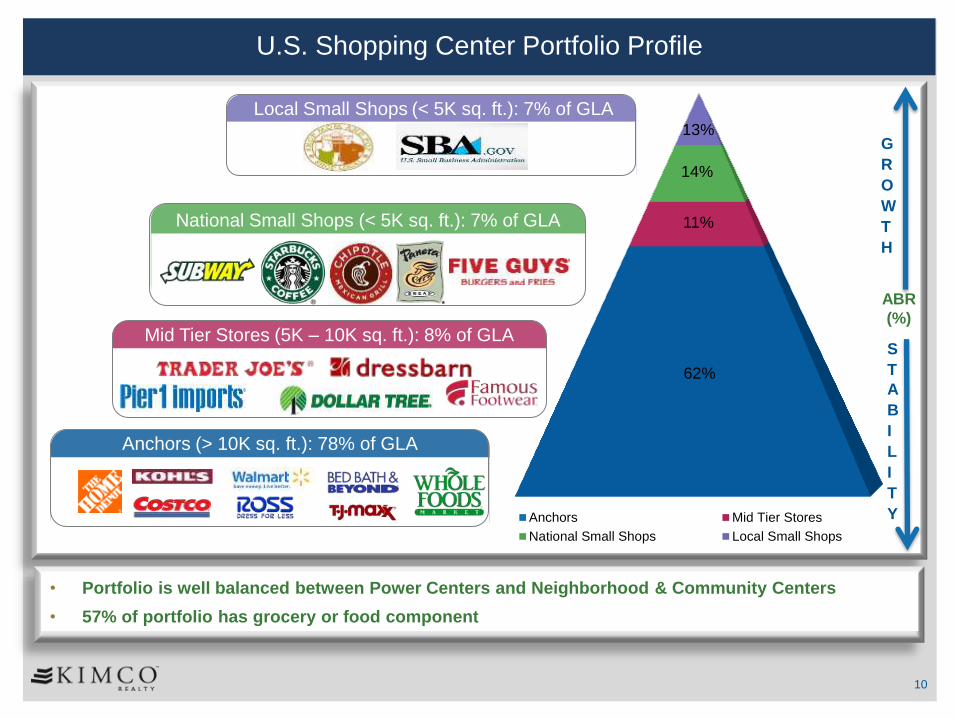

U.S. Shopping Center Portfolio Profile

10

Mid Tier Stores (5K – 10K sq. ft.): 8% of GLA

National Small Shops (< 5K sq. ft.): 7% of GLA

Anchors (> 10K sq. ft.): 78% of GLA

Local Small Shops (< 5K sq. ft.): 7% of GLA

G

R

O

W

T

H

ABR

(%)

• Portfolio is well balanced between Power Centers and Neighborhood & Community Centers

• 57% of portfolio has grocery or food component

S

T

A

B

I

L

I

T

Y

62%

11%

14%

13%

Anchors Mid Tier Stores

National Small Shops Local Small Shops

Timonium Square

Timonium, MD

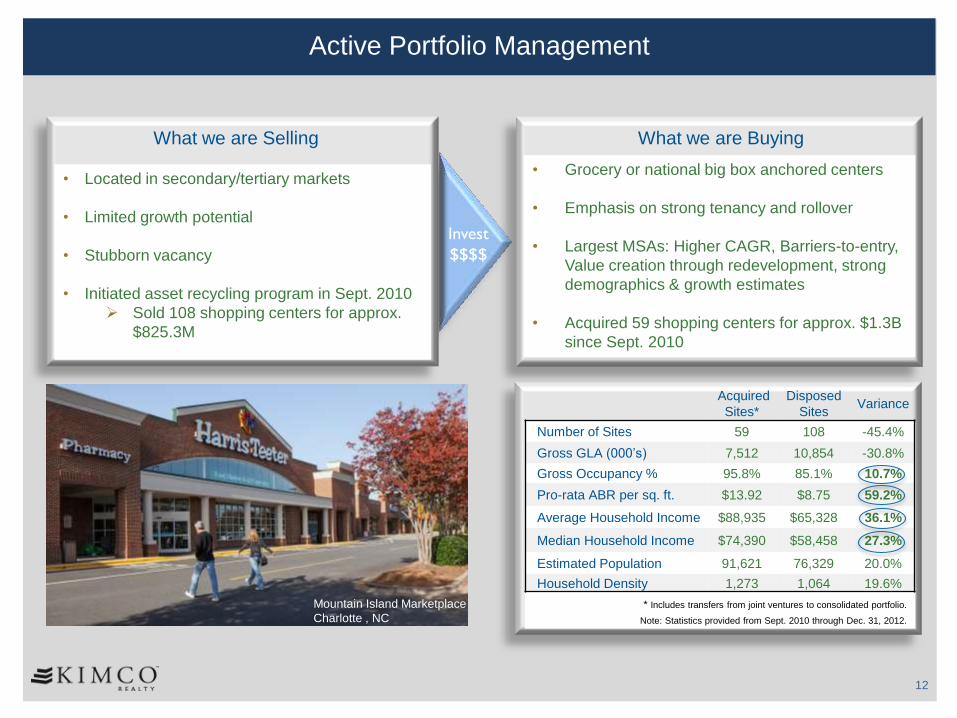

Active Portfolio Management

Active Portfolio Management

Invest

$$$$

• Located in secondary/tertiary markets

• Limited growth potential

• Stubborn vacancy

• Initiated asset recycling program in Sept. 2010

Sold 108 shopping centers for approx.

$825.3M

What we are Selling

• Grocery or national big box anchored centers

• Emphasis on strong tenancy and rollover

• Largest MSAs: Higher CAGR, Barriers-to-entry,

Value creation through redevelopment, strong

demographics & growth estimates

• Acquired 59 shopping centers for approx. $1.3B

since Sept. 2010

What we are Buying

Acquired

Sites*

Disposed

Sites Variance

Number of Sites 59 108 -45.4%

Gross GLA (000’s) 7,512 10,854 -30.8%

Gross Occupancy % 95.8% 85.1% 10.7%

Pro-rata ABR per sq. ft. $13.92 $8.75 59.2%

Average Household Income $88,935 $65,328 36.1%

Median Household Income $74,390 $58,458 27.3%

Estimated Population 91,621 76,329 20.0%

Household Density 1,273 1,064 19.6%

12

Mountain Island Marketplace

Charlotte , NC

* Includes transfers from joint ventures to consolidated portfolio.

Note: Statistics provided from Sept. 2010 through Dec. 31, 2012.

Recent U.S. Acquisition Profile

GLA: 97,000 square feet

Anchor Tenants: Stop & Shop

Occupancy: 100%

Rent Per Sq. Ft.: $30.03

Demographics:

Total Population: 21,465

Avg. HH Income: $241,486

Med. HH Income: $207,457

Wilton Campus Shops in Wilton, Connecticut

Savi Ranch in Yorba Linda, California

GLA: 161,000 square feet

Anchor Tenants: Dick’s Sporting Goods,

Bed Bath & Beyond, Michaels

Occupancy: 100%

Rent Per Sq. Ft.: $15.11

Demographics:

Total Population: 61,263

Avg. HH Income: $150,071

Med. HH Income: $138,498

13

Recent U.S. Acquisition Profile

GLA: 79,000 square feet

Anchor Tenant: Harris Teeter

Occupancy: 97.1%

Rent Per Sq. Ft.: $14.98

Demographics:

Total Population: 29,157

Avg. HH Income: $114,506

Med. HH Income: $95,636

Davidson Commons in Davidson, North Carolina

GLA: 69,000 square feet

Occupancy: 100%

Rent Per Sq. Ft.: $31.49

Anchor Tenant: Whole Foods Market

Demographics:

Total Population: 48,741

Avg. HH Income: $152,318

Med. HH Income: $109,341

14

Devon Village in Devon, Pennsylvania

Redhawk Towne Center

Temecula , CA

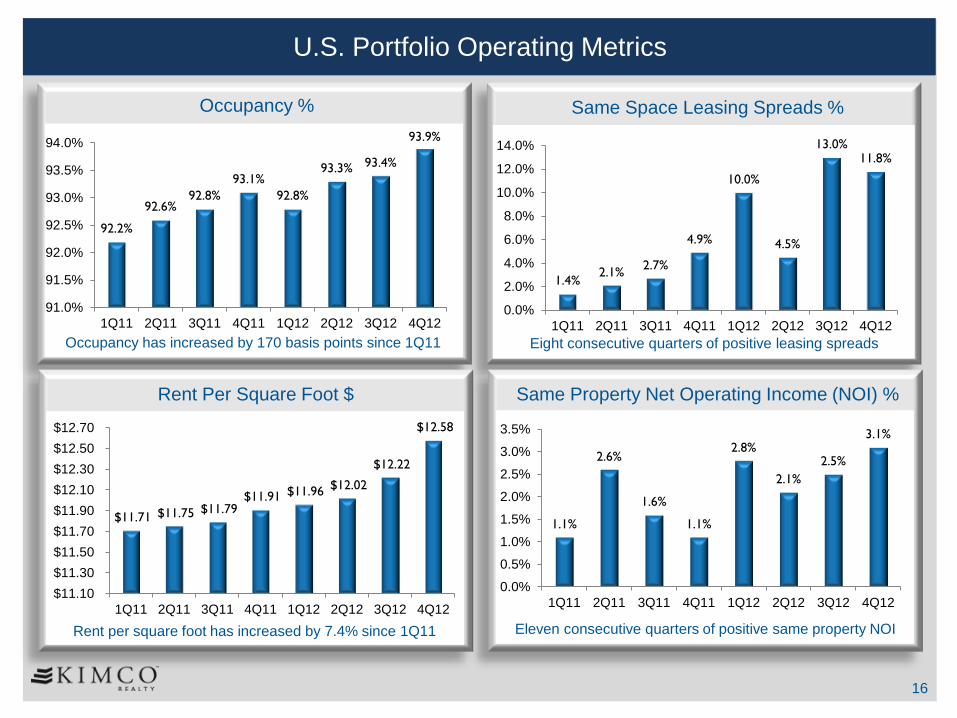

U.S. Portfolio Operating Metrics

16

U.S. Portfolio Operating Metrics

Occupancy %

92.2%

92.6% 92.8%

93.1%

92.8%

93.3% 93.4%

93.9%

91.0%

91.5%

92.0%

92.5%

93.0%

93.5%

94.0%

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12

Rent Per Square Foot $

$11.71 $11.75 $11.79 $11.91 $11.96

$12.02

$12.22

$12.58

$11.10

$11.30

$11.50

$11.70

$11.90

$12.10

$12.30

$12.50

$12.70

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12

Occupancy has increased by 170 basis points since 1Q11

Same Space Leasing Spreads %

1.4% 2.1%

2.7%

4.9%

10.0%

4.5%

13.0% 11.8%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12

Eight consecutive quarters of positive leasing spreads

Rent per square foot has increased by 7.4% since 1Q11

Same Property Net Operating Income (NOI) %

1.1%

2.6%

1.6%

1.1%

2.8%

2.1%

2.5%

3.1%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12

Eleven consecutive quarters of positive same property NOI

17

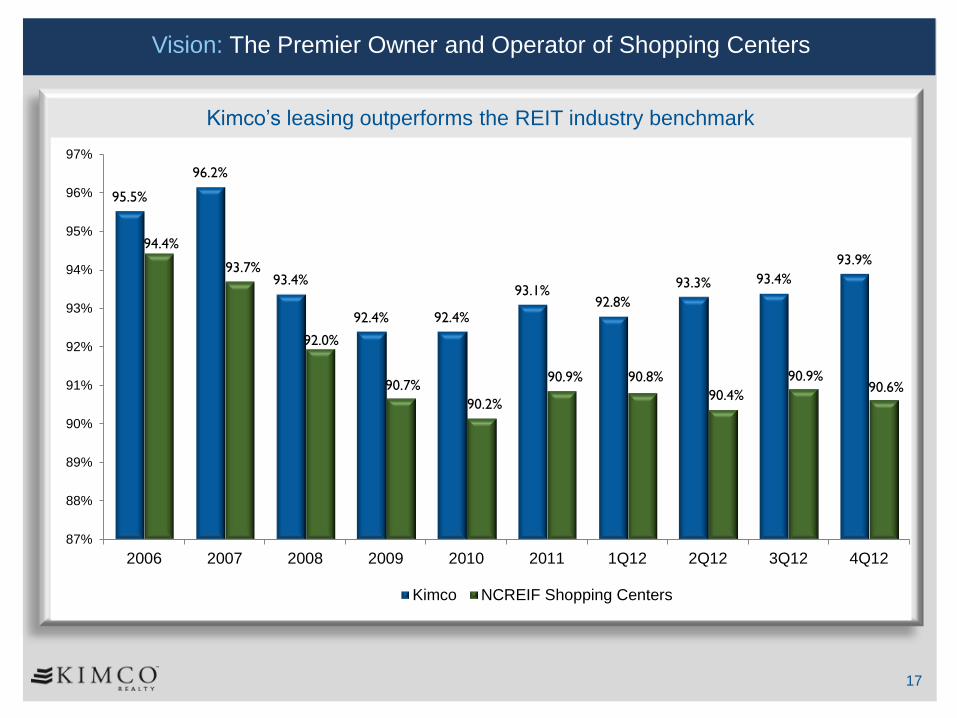

Vision: The Premier Owner and Operator of Shopping Centers

Kimco’s leasing outperforms the REIT industry benchmark

95.5%

96.2%

93.4%

92.4% 92.4%

93.1% 92.8%

93.3% 93.4%

93.9% 94.4%

93.7%

92.0%

90.7%

90.2%

90.9% 90.8%

90.4%

90.9% 90.6%

87%

88%

89%

90%

91%

92%

93%

94%

95%

96%

97%

2006 2007 2008 2009 2010 2011 1Q12 2Q12 3Q12 4Q12

Kimco NCREIF Shopping Centers

Corporate Responsibility Program

Towson Marketplace

Towson, MD

CORPORATE RESPONSIBILITY PROGRAM

R E T H I N K B u s i n e s s • R E N E W C o m m u n i t y • R E S T O R E E n v i r o n m e n t

Objective:

Improve Kimco’s economic, social & environmental performance through

a series of initiatives that enhance tenant satisfaction, reduce operating

expenses, mitigate business risks, & generate new sources of income.

Key Initiatives:

• NAREIT leader in The Light Group

• Participates in Global Real Estate Sustainability

Benchmark (GRESB) & Carbon Disclosure Project (CDP)

• CR Web Portal: www.KimcoCR.com

• Kimco Blog: blog.kimcorealty.com

• Twitter: twitter.com/KimcoCR

• Email: [email protected]

Program Overview

Additional Information/Resources

Westlake Shopping Center

Daly City, CA

North Brunswick Plaza

North Brunswick, NJ

19

• KimCares

• KEYS

• FastTRACK Franchise

• Redevelopment

• Utility Management

• Lighting and Irrigation Efficiency

• Integrated Waste Management

• Tenant Energy Services

Hamden Mart

Hamden, CT

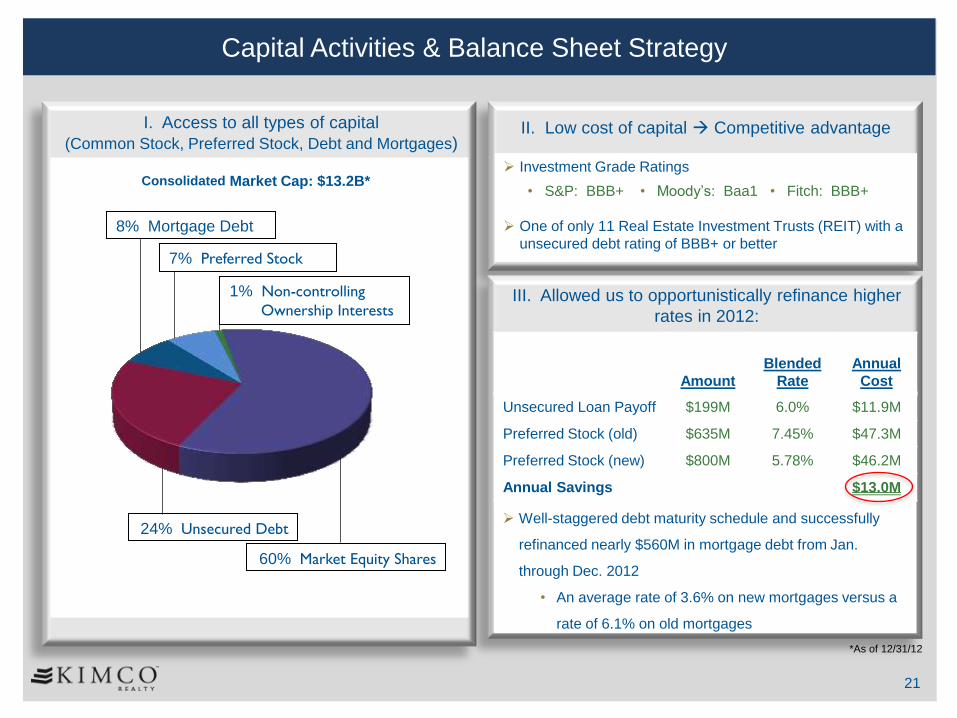

Capital Structure & Dividend Summary

60% Market Equity Shares

24% Unsecured Debt

8% Mortgage Debt

7% Preferred Stock

1% Non-controlling

Ownership Interests

Consolidated Market Cap: $13.2B*

*As of 12/31/12

21

I. Access to all types of capital

(Common Stock, Preferred Stock, Debt and Mortgages)

Capital Activities & Balance Sheet Strategy

II. Low cost of capital Competitive advantage

Investment Grade Ratings

• S&P: BBB+ • Moody’s: Baa1 • Fitch: BBB+

One of only 11 Real Estate Investment Trusts (REIT) with a

unsecured debt rating of BBB+ or better

III. Allowed us to opportunistically refinance higher

rates in 2012:

Well-staggered debt maturity schedule and successfully

refinanced nearly $560M in mortgage debt from Jan.

through Dec. 2012

• An average rate of 3.6% on new mortgages versus a

rate of 6.1% on old mortgages

Amount

Blended

Rate

Annual

Cost

Unsecured Loan Payoff $199M 6.0% $11.9M

Preferred Stock (old) $635M 7.45% $47.3M

Preferred Stock (new) $800M 5.78% $46.2M

Annual Savings $13.0M

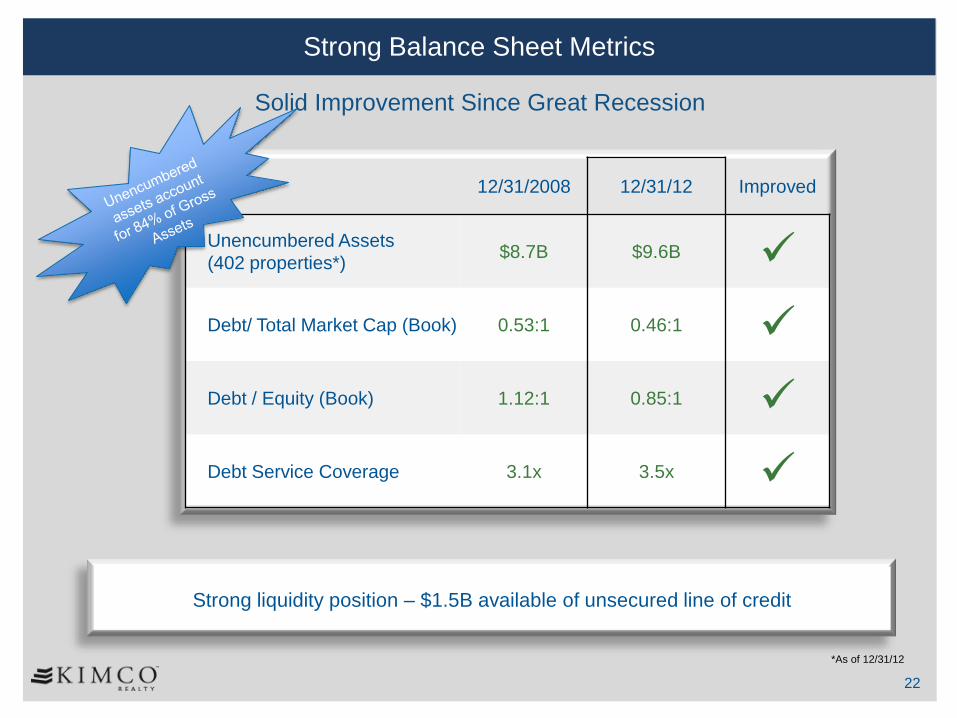

Strong Balance Sheet Metrics

12/31/2008 12/31/12 Improved

Unencumbered Assets

(402 properties*) $8.7B $9.6B

Debt/ Total Market Cap (Book) 0.53:1 0.46:1

Debt / Equity (Book) 1.12:1 0.85:1

Debt Service Coverage 3.1x 3.5x

*As of 12/31/12

22

Strong liquidity position – $1.5B available of unsecured line of credit

Solid Improvement Since Great Recession

23

Dividend & Total Return Thesis

Source: NAREIT and Bloomberg.

*Total return on investment including reinvestment of dividends through Feb. 28, 2013. Statistics for return since IPO are based on closing prices as of Nov. 30, 1991

12.5%

6.0%

$0.14

$0.15

$0.16

$0.17

$0.18

$0.19

$0.20

$0.21

$0.22

Q110 Q210 Q310 Q410 Q111 Q211 Q311 Q411 Q112 Q212 Q312 Q412 Q113

Dividend Growth

Total Return Analysis

$100,000 invested at IPO would be $1.5M today Kimco outperforms these major indices over a one-year period

13.5%

11.7% 10.3%

9.0%

0%

5%

10%

15% Since IPO

KIM NAREIT Equity Index DJIA S&P500

23.1%

15.1%

11.5% 13.4%

0%

5%

10%

15%

20%

25% One Year Period

KIM NAREIT Equity Index DJIA S&P500

• Paid quarterly cash dividend since

Initial Public Offering in Nov. 1991

• Annual dividend of $.084 provides

yield of ~4% (12/31/12)

• In 2012, approximately 23% of our

dividend distribution was treated as

a return of capital

10.5%

International platform with

incremental earnings from Canadian

and Latin America portfolios provides

further diversification of rental and

tenant base

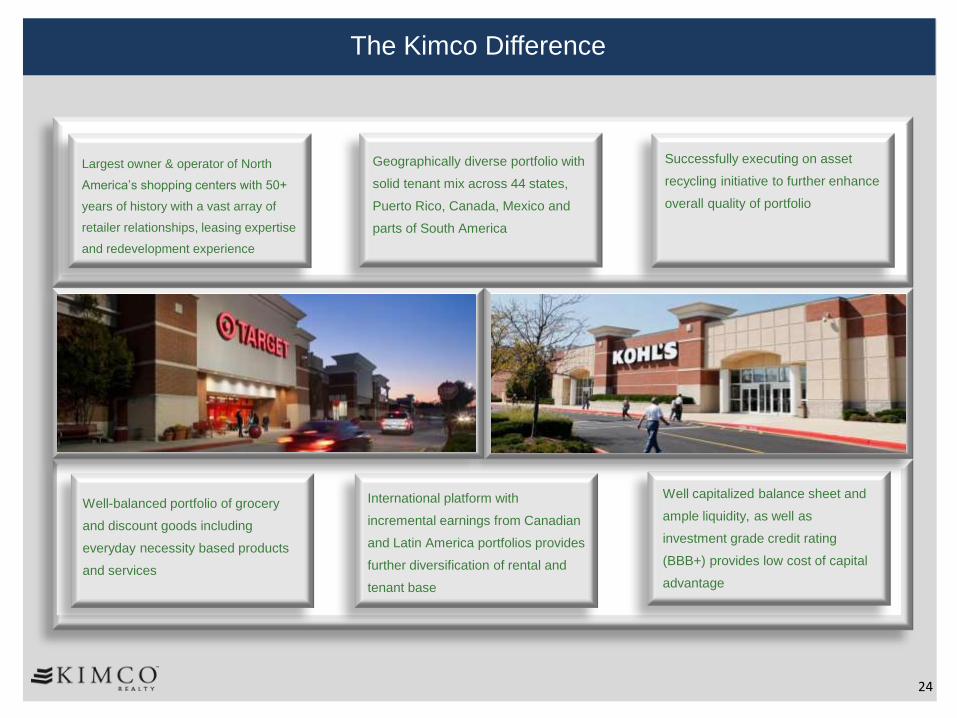

The Kimco Difference

Well capitalized balance sheet and

ample liquidity, as well as

investment grade credit rating

(BBB+) provides low cost of capital

advantage

Well-balanced portfolio of grocery

and discount goods including

everyday necessity based products

and services

24

Largest owner & operator of North

America’s shopping centers with 50+

years of history with a vast array of

retailer relationships, leasing expertise

and redevelopment experience

Geographically diverse portfolio with

solid tenant mix across 44 states,

Puerto Rico, Canada, Mexico and

parts of South America

Successfully executing on asset

recycling initiative to further enhance

overall quality of portfolio

Q&A