Embed Size (px)

Citation preview

Mining Mining CompaniesCompanies

Lorna TamLorna Tam

Sandy GaoSandy Gao

Natalie KimNatalie Kim

JohnnyJohnny

Luka MiodragovicLuka Miodragovic

What is Mining?

Mining is the extraction of valuable minerals or other Mining is the extraction of valuable minerals or other geological materials from the earth. geological materials from the earth.

Materials recovered by mining include Materials recovered by mining include Coal , copper, gold, silver, diamonds, iron, precious Coal , copper, gold, silver, diamonds, iron, precious

metals, lead, limestone, nickel, and phosphate. metals, lead, limestone, nickel, and phosphate.

Any material that cannot be grown from agricultural Any material that cannot be grown from agricultural processes, or created artificially, is usually mined. processes, or created artificially, is usually mined.

Mining Industry

Two sectorsTwo sectors

Specialization in exploration for new resourcesSpecialization in exploration for new resources typically made up of individuals and small mineral typically made up of individuals and small mineral

resource companies dependent on public investmentresource companies dependent on public investment

Specialization in actual miningSpecialization in actual mining typically large and multi-national companies sustained typically large and multi-national companies sustained

by mineral production from their mining operations by mineral production from their mining operations

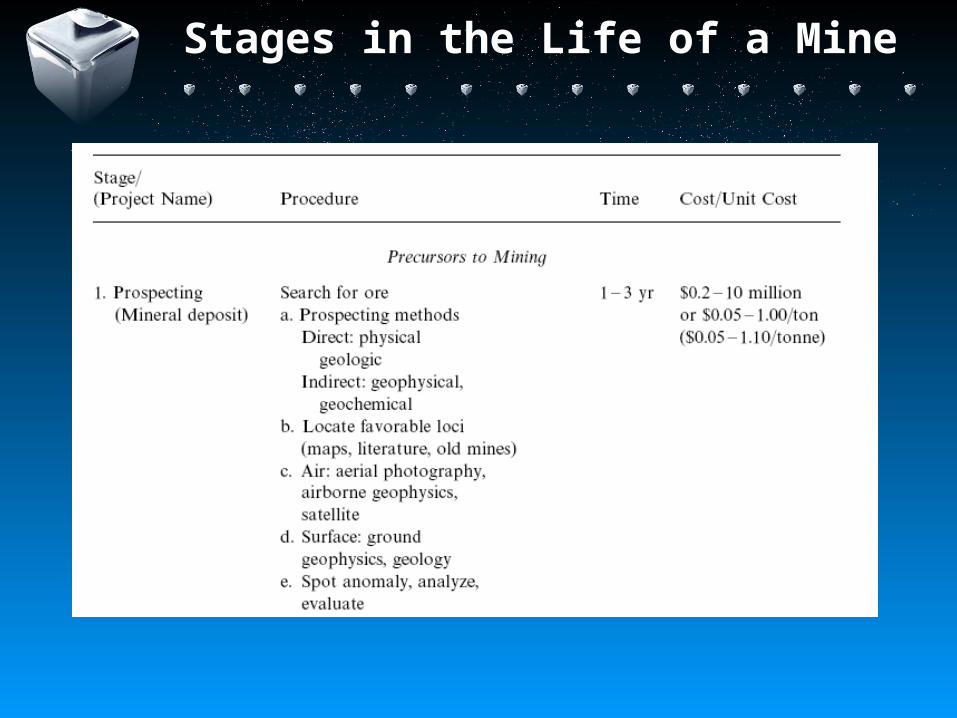

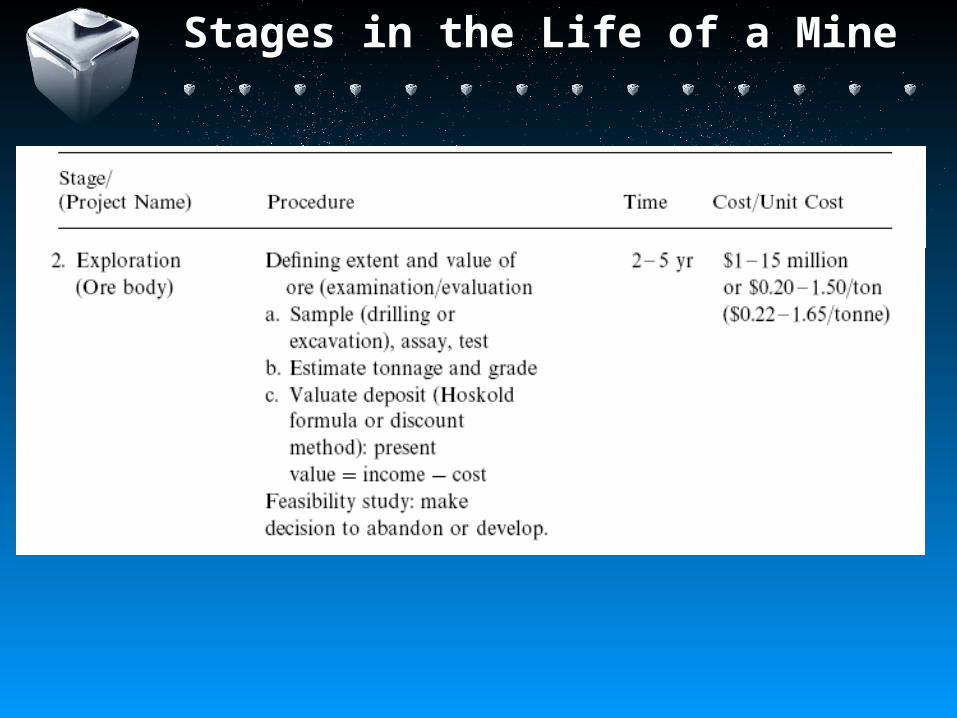

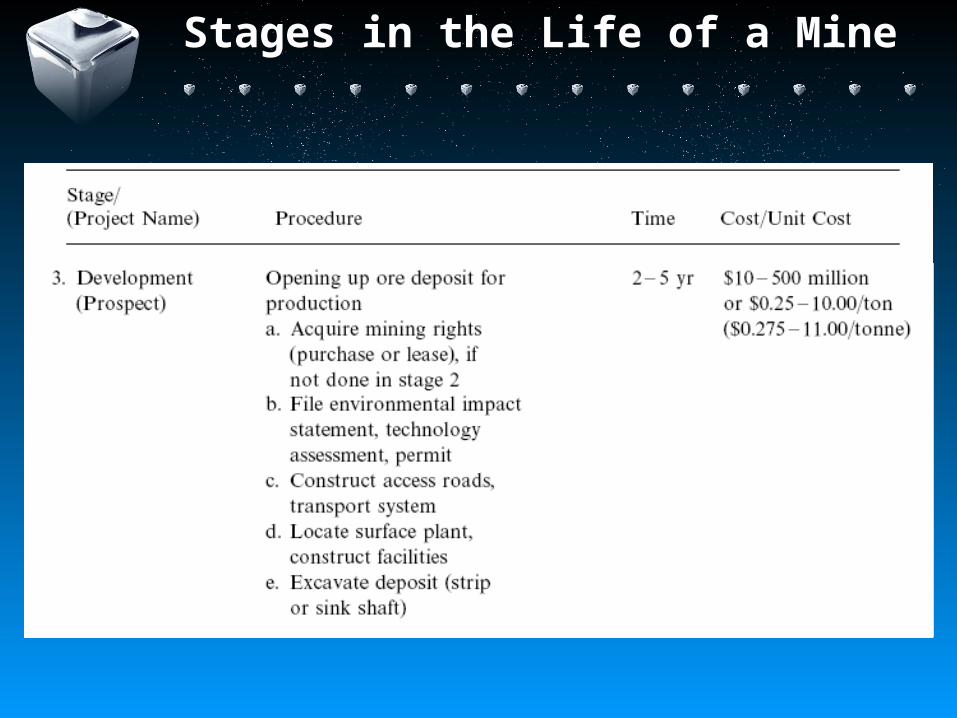

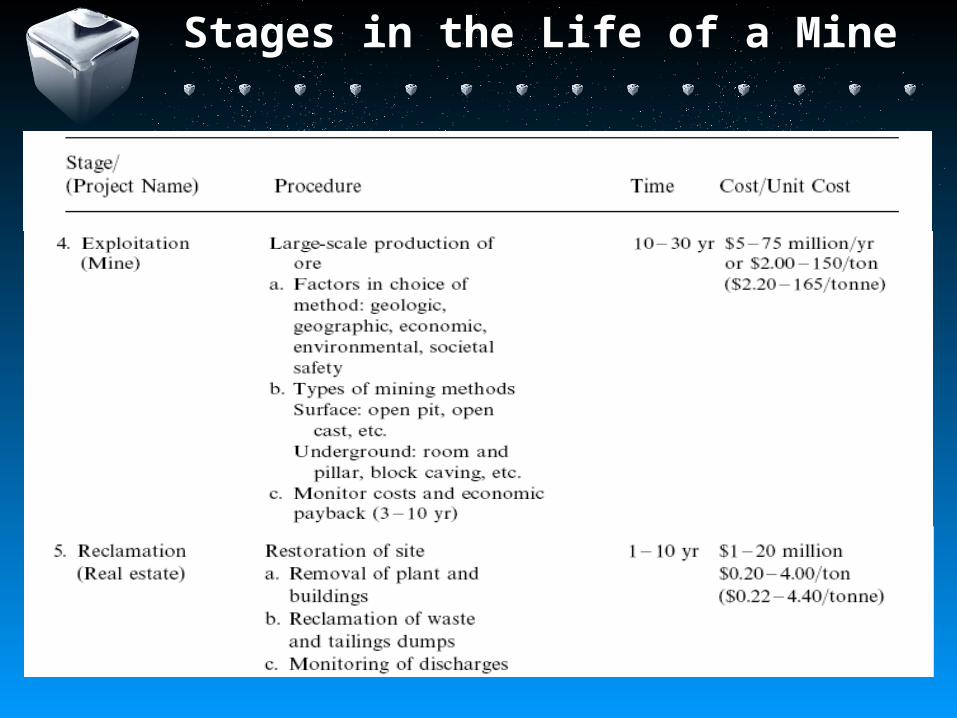

Stages in the Life of a Mine

Stages in the Life of a Mine

Stages in the Life of a Mine

Stages in the Life of a Mine

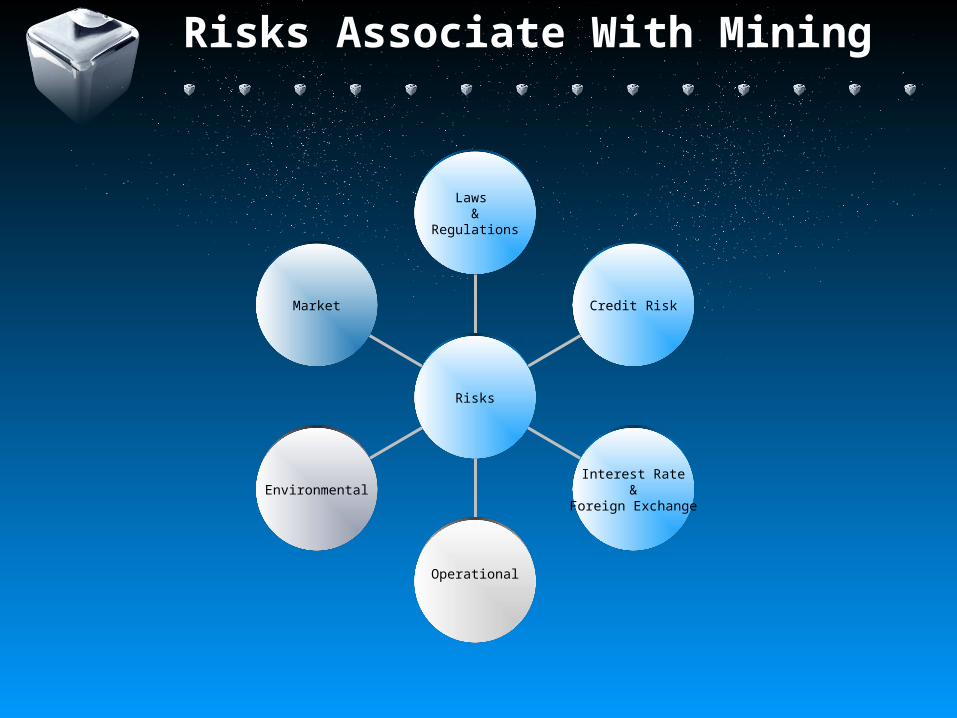

Laws &

Regulations

Credit Risk

Interest Rate&

Foreign Exchange

Operational

Environmental

Market

Risks

Risks Associate With Mining

Market Risk

Revenues are highly dependant on market prices

Prices are affected by: Growth and political conditions of consuming economies Currency exchange fluctuations Global supply and demand Availability and cost of substitute materials Speculative activities Production levels and costs of other mining countries

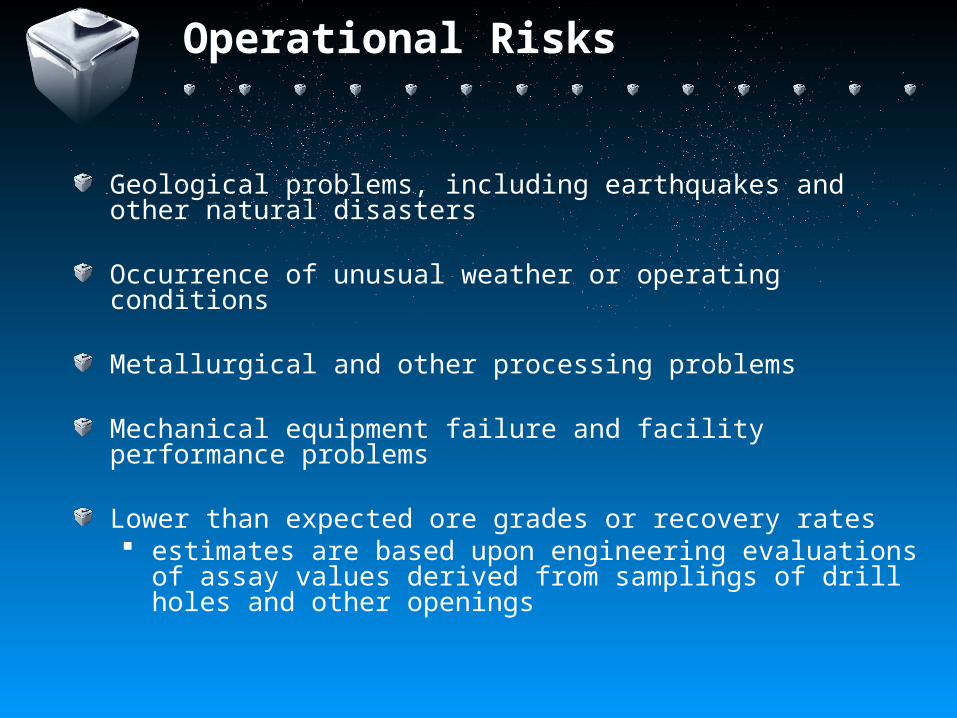

Operational Risks

Geological problems, including earthquakes and other natural disasters

Occurrence of unusual weather or operating conditions

Metallurgical and other processing problems

Mechanical equipment failure and facility performance problems

Lower than expected ore grades or recovery rates estimates are based upon engineering evaluations of

assay values derived from samplings of drill holes and other openings

Delays in the receipt of or failure to receive necessary government permit

Uncertainty of exploration and development

Energy represents a significant portion of the production costs of our operations Electricity, diesel fuel and natural gas

Labour disputes Occupational health Labour standards

Operational Risks

Ability to attract and retain skilled and experienced employees

Shortage of skills could limit ability to meet contractual requirements

Industrial accidentsLong term sales contracts Loss of any contracts require company to sell at

prevailing market prices, which might expose it to lower metal prices compared to contract prices

Default or modification of the sales contracts could prohibit additional loans or require the immediate repayment of outstanding loans depending on covenants of credit facilities

Operational Risks

Mine closure regulations Operations in the United States are subject to various

federal and state mine closure and mined-land reclamation laws (requirements of these laws vary depending upon the jurisdiction

Bureau of Land Management (BLM) regulates mining operations located on unpatented mining claims located on federal public lands

Mines are required to post increasing amounts of financial assurance to ensure the availability of funds to perform future closure and reclamation

Operational Risks

Operational Risk In Foreign Countries

Political instability and civil strife

Changes in foreign laws and regulations, including those relating to the environment, labor, tax, royalties on mining activities, and dividends or repatriation of cash and other property to the US

Foreign currency fluctuations

Import, export, and trade regulations

Insurance

Cost of insurance dramatically increased as a result of worldwide economic conditions

Liability for environmental damage or other hazards which may be uninsurable or for which it may elect not to insure because of premium costs

Environmental Laws and Regulations

Regulations include: Clean Air Act Clean Water Act Resource Conservation and Recovery Act Metals Mines Reclamation Act

Laws are continually changing and becoming more restrictiveObtain permits issued by federal, state and local regulatory agencies Some require periodic renewal or review of conditions

which they cannot predict if they could renew or new conditions imposed

Subject to claims for natural resource damages where the release of hazardous substances is alleged to have injured natural resources

Compliance with these laws and regulations imposes substantial costs and significant potential liabilities

Often impose liability with respect to divested or terminated operations, even if the operations were terminated or divested many years ago

Parties to pay for remedial action or to pay damages regardless of fault

Environmental Laws and Regulations

Credit and Interest Rate Risk

Credit Risk Default or modification of sales contracts could prohibit

additional loans or require the immediate repayment of outstanding loans depending on covenants of credit facilities

Interest Rate Risk Financing for operations from credit facilities are sensitive to

interest rates

Important to hedge against interest rate risk so cash flow is not affected for operations

Phelps Dodge

Phelps Dodge

Phelps Dodge (PD) is a producer of: Copper , Carbon black, Magnet wire, Continuous-cast

copper rodWorld’s major producer of copper and molybdenum

Consists of two divisions Phelps Dodge Mining Company (PDMC)

Integrated producer of copper and molybdenum Phelps Dodge Industries (PDI)

produces engineered products principally for the global energy sector

Acquisition of Phelps Dodge

Freeport-McMoRan bought out Phelps Dodge for $26 billion

Stockholders approved of the deal on March 21, 2007 98 percent of stockholder votes supported the merger

The largest publicly traded copper producer

Phelps Dodge shareholders are to receive $88 per share in cash and 0.67 of a share of Freeport stock (about $126.50 a share)

The buyout ends Phelps Dodge's 78-year run on the NYSE The new company will trade under the symbol of FCX

Future

If copper prices hold at the current rate of around $2.50 a pound, Freeport will be able to quickly pay off its debt. At existing prices, the new company will generate an estimated $6.5 billion in operating cash.

Will copper prices remain stable, allowing Freeport to quickly pay off the $17.5 billion in debt it took on to buy Phelps Dodge?

If copper price plunges, the new company may end up on the rocks. Freeport is partially financing the buyout with $6 billion in junk-based bonds and $10 billion in bank loans.

Sales

US Mining Operations Majority of the copper from Phelps Dodge’s US mining

operations is cast into rod Rod sales to outside wire and cable manufacturers

constitute 74% of PDMC’s US sales in 2006South American Mines Production is sold as copper concentrate or as copper

cathode. Candelaria mine sells copper concentrate to copper Asian

smelters(Japan) under long-term contracts Ojos del Salado concentrate is sold to local Chilean

smelters. Sales prices are based on LME prices

Worldwide Competitors

Primary US producers

Numerous foreign producers, metal merchants, custom refiners and scrap dealers

Some major producers outside the US have cost advantages richer ore grades, lower labor costs and, in some cases, a lack

of strict regulatory requirements US mines has less political risk

Other materials that compete with copper Aluminum, plastics, stainless steel and fiber optics

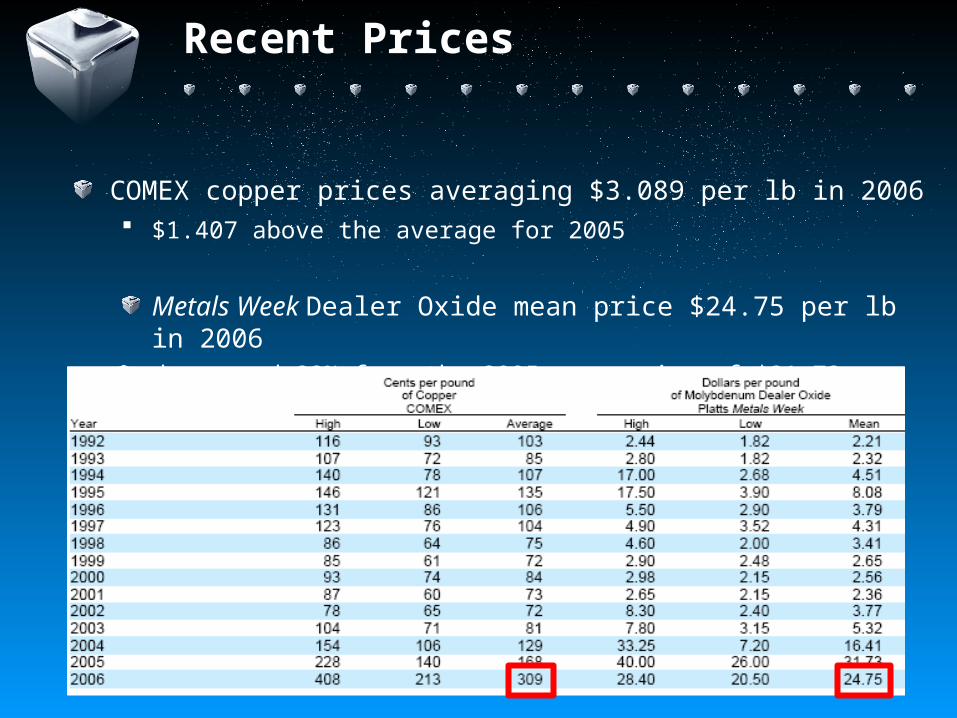

Recent Prices

COMEX copper prices averaging $3.089 per lb in 2006 $1.407 above the average for 2005

Metals Week Dealer Oxide mean price $24.75 per lb in 2006 decreased 22% from the 2005 mean price of $31.73 per lb

Copper and Molybdenum Price

Phelps Dodge’s reported ore reserves are economic at copper price of $2.02 per pound molybdenum price of $24.30 per pound

most-recent three-year historical average price

Phelps Dodge develops its business plans using a long-term average COMEX copper price of $1.05 per pound average molybdenum price of $5.00 per pound

The per lb COMEX copper price average $1.17(10 yr), $1.13(15 yr) and $1.12(20yr)

The per lb Metals Week molybdenum mean price $9.73(10yr), $7.88(15 yr) and $6.66(20yr)

Executives

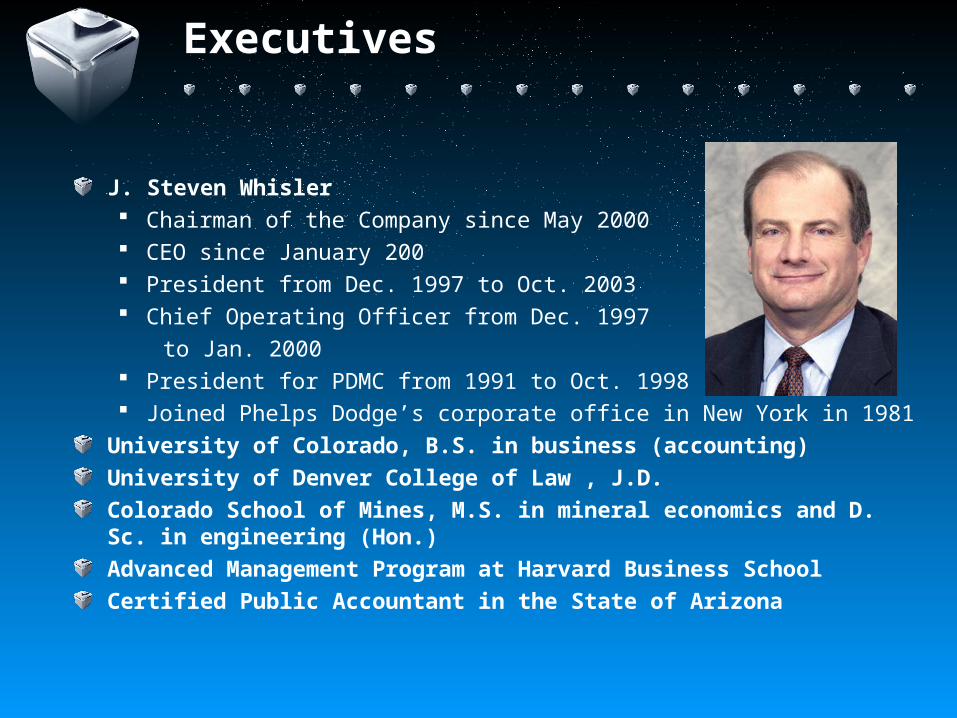

J. Steven Whisler Chairman of the Company since May 2000 CEO since January 200 President from Dec. 1997 to Oct. 2003 Chief Operating Officer from Dec. 1997

to Jan. 2000 President for PDMC from 1991 to Oct. 1998 Joined Phelps Dodge’s corporate office in New York in 1981

University of Colorado, B.S. in business (accounting) University of Denver College of Law , J.D. Colorado School of Mines, M.S. in mineral economics and D. Sc. in engineering (Hon.) Advanced Management Program at Harvard Business SchoolCertified Public Accountant in the State of Arizona

Executives

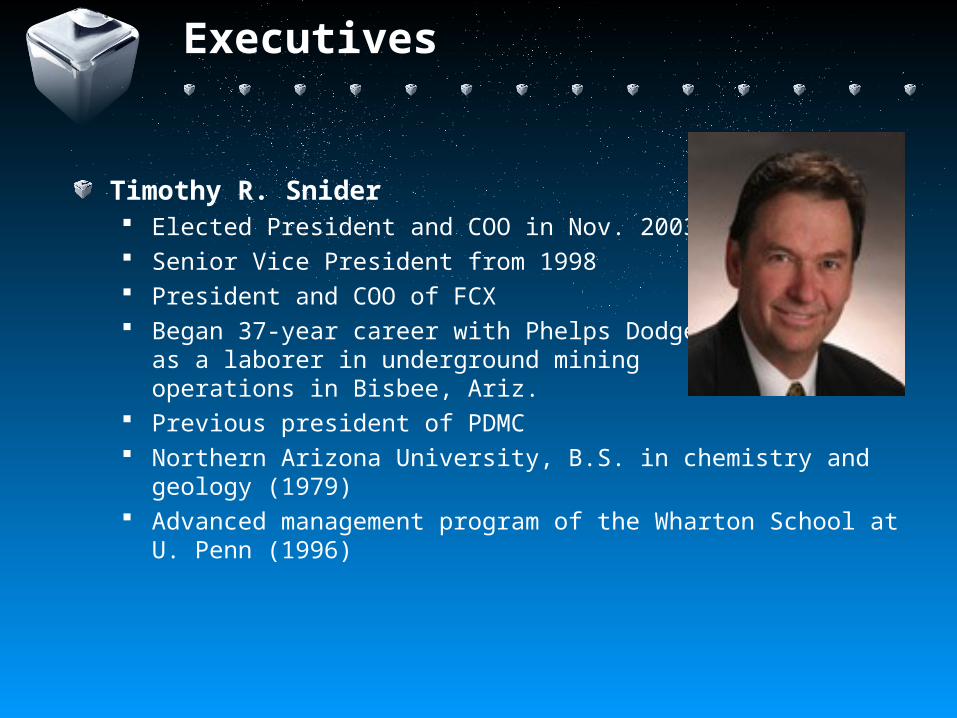

Timothy R. Snider Elected President and COO in Nov. 2003 Senior Vice President from 1998 President and COO of FCX Began 37-year career with Phelps Dodge

as a laborer in underground miningoperations in Bisbee, Ariz.

Previous president of PDMC Northern Arizona University, B.S. in chemistry and geology

(1979) Advanced management program of the Wharton School at U.

Penn (1996)

Executives

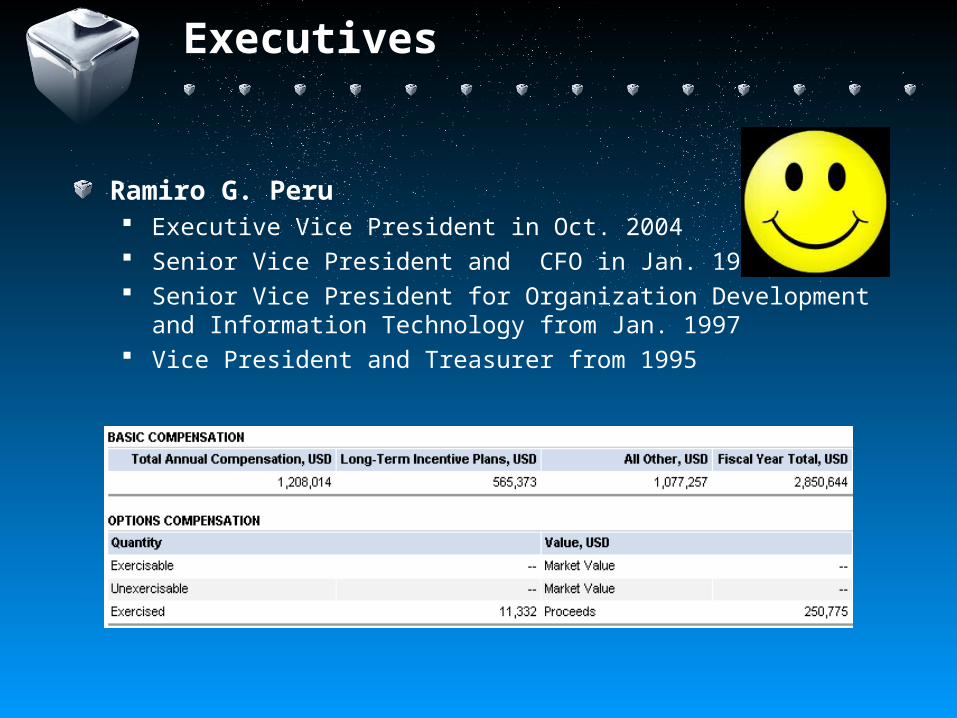

Ramiro G. Peru Executive Vice President in Oct. 2004 Senior Vice President and CFO in Jan. 1999 Senior Vice President for Organization Development and

Information Technology from Jan. 1997 Vice President and Treasurer from 1995

Executives

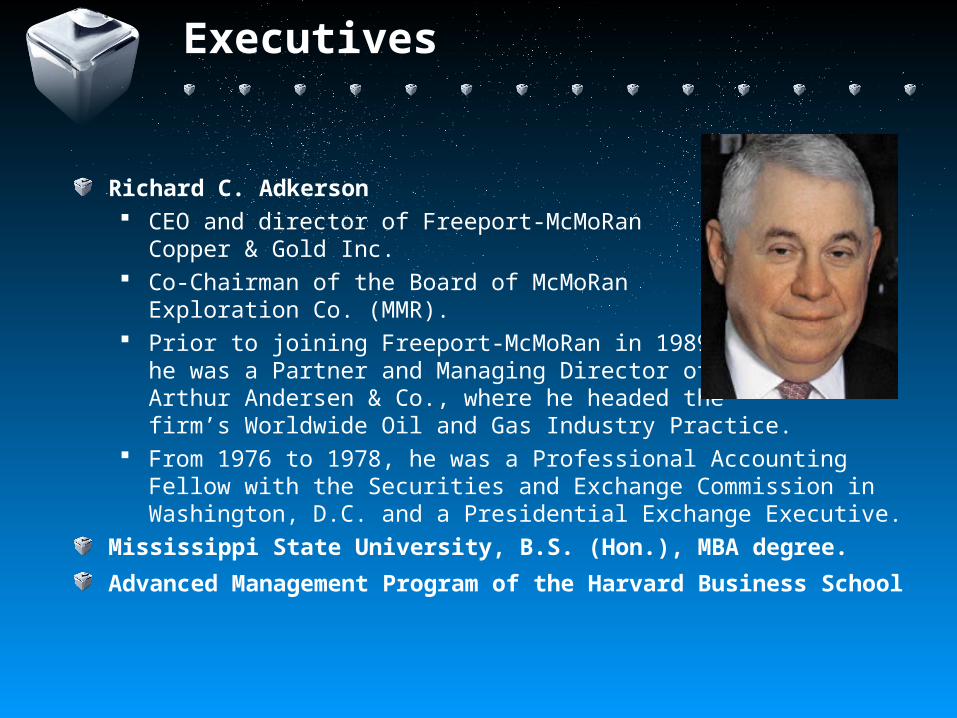

Richard C. Adkerson CEO and director of Freeport-McMoRan

Copper & Gold Inc. Co-Chairman of the Board of McMoRan

Exploration Co. (MMR). Prior to joining Freeport-McMoRan in 1989,

he was a Partner and Managing Director of Arthur Andersen & Co., where he headed the firm’s Worldwide Oil and Gas Industry Practice.

From 1976 to 1978, he was a Professional Accounting Fellow with the Securities and Exchange Commission in Washington, D.C. and a Presidential Exchange Executive.

Mississippi State University, B.S. (Hon.), MBA degree.

Advanced Management Program of the Harvard Business School

Executive Compensation

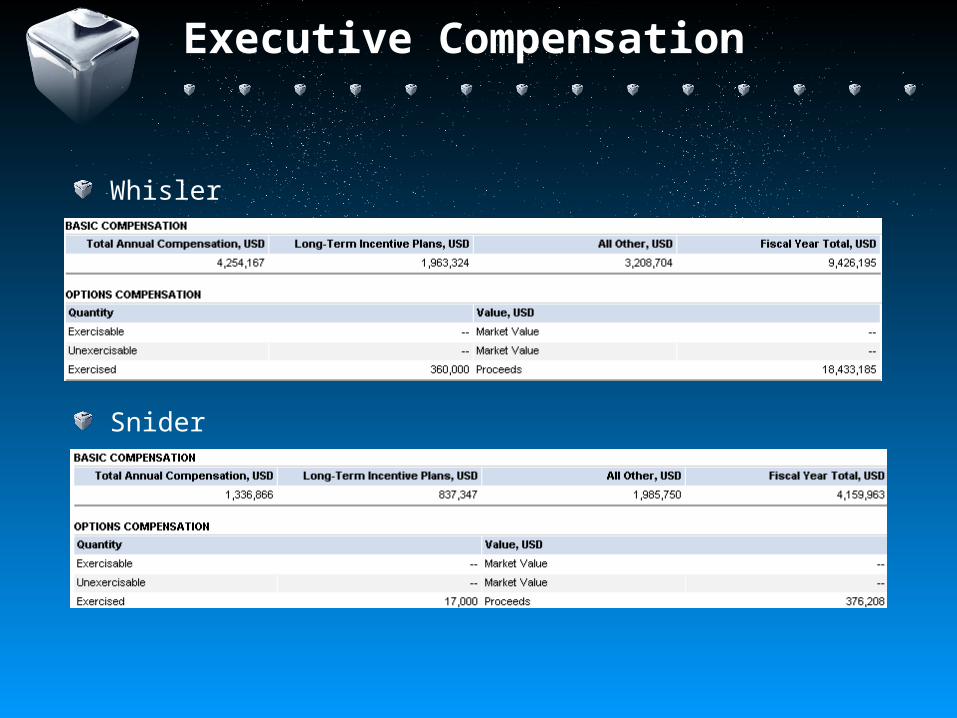

Whisler

Snider

Snider

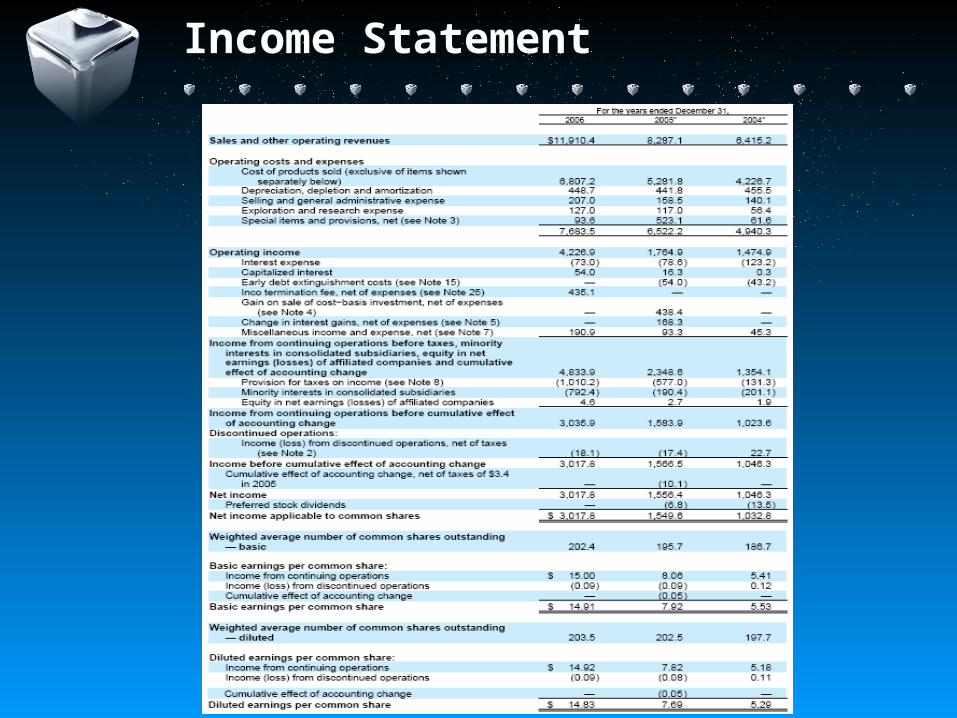

Income Statement

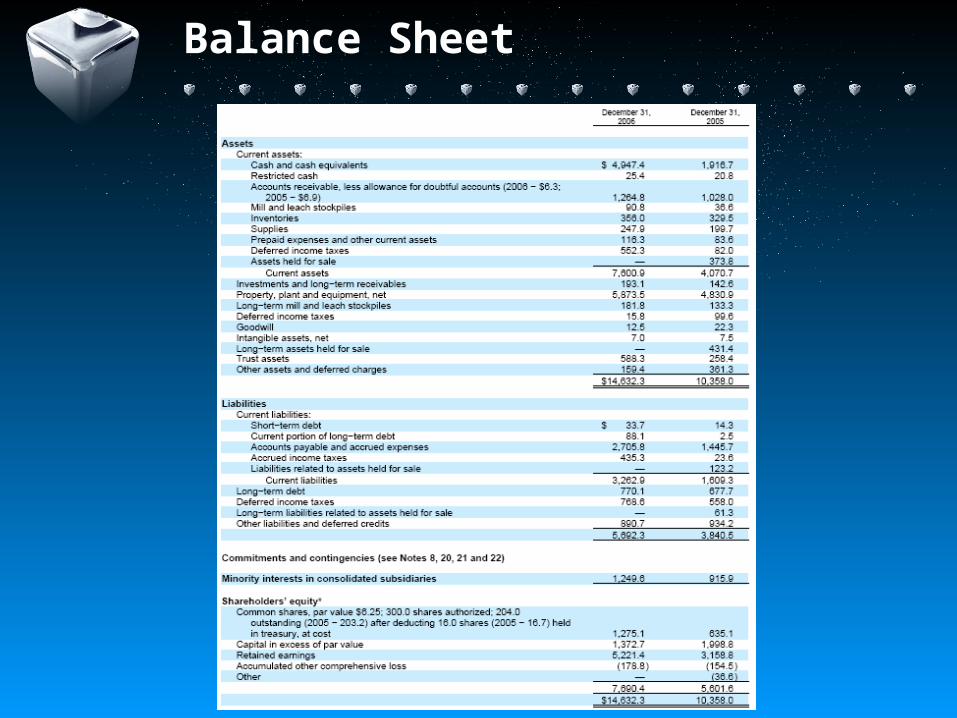

Balance Sheet

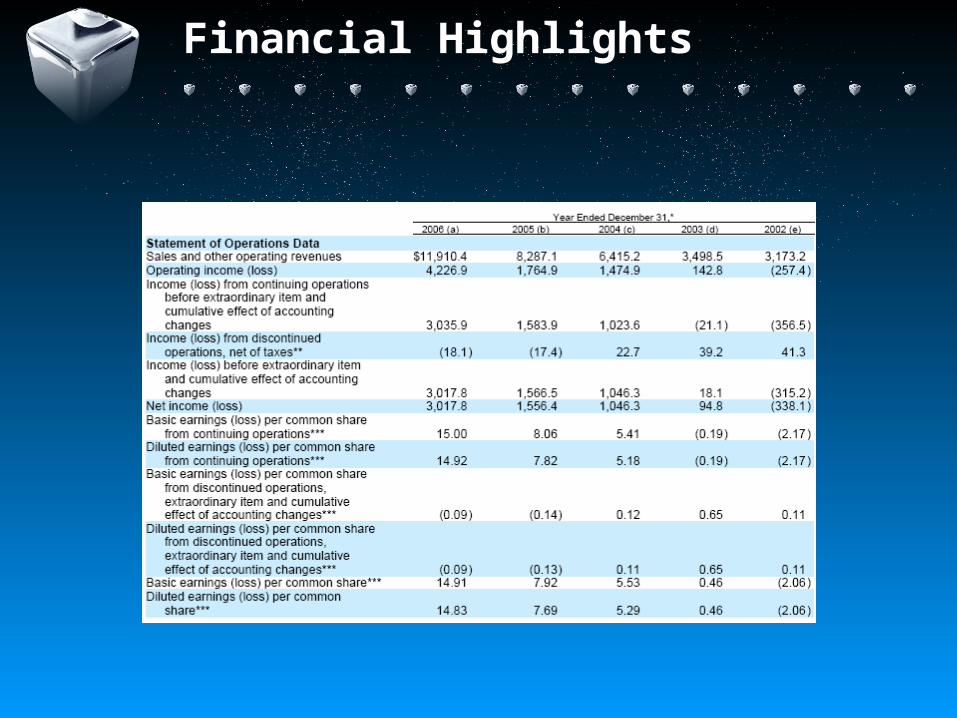

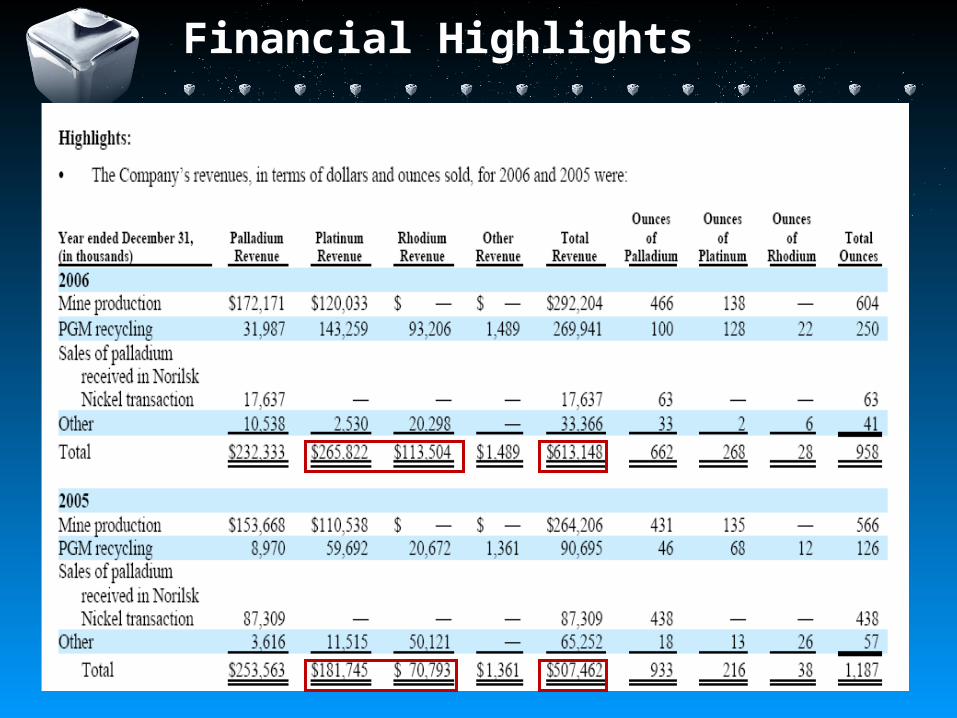

Financial Highlights

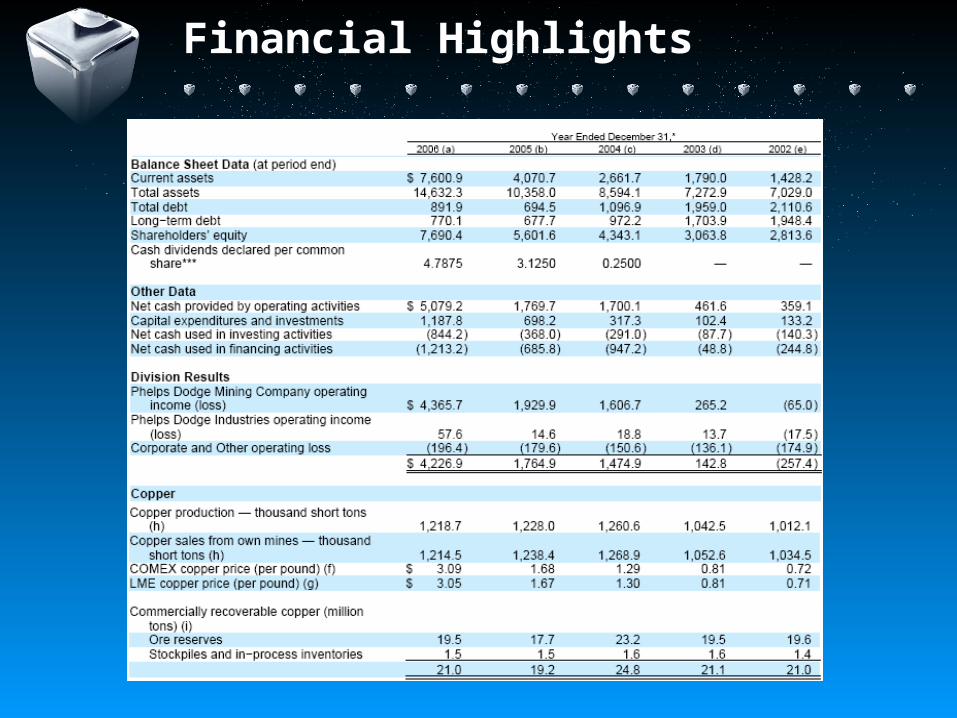

Financial Highlights

Risk Factors

Copper and Molybdenum Price Volatility

Increased Energy Costs

Copper price Protection Programs

Pressure on the Copper Production Costs

Mine Closure Regulations

Subject to Complex and Evolving Laws and Regulations

Uncertain level of Ore Reserves

Operational Risks

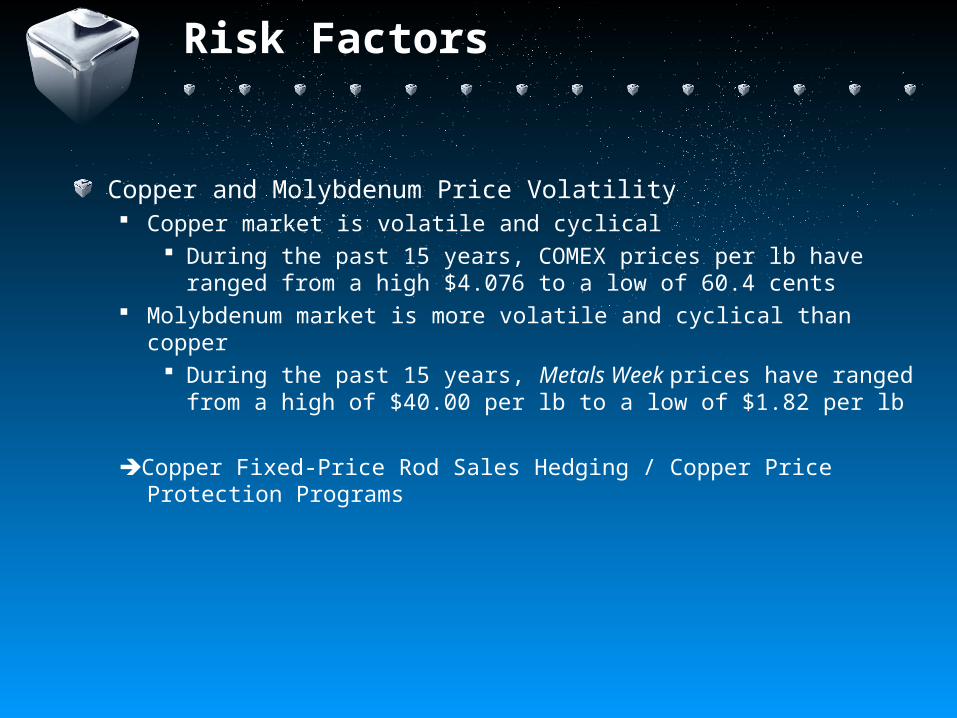

Risk Factors

Copper and Molybdenum Price Volatility Copper market is volatile and cyclical

During the past 15 years, COMEX prices per lb have ranged from a high $4.076 to a low of 60.4 cents

Molybdenum market is more volatile and cyclical than copper During the past 15 years, Metals Week prices have ranged

from a high of $40.00 per lb to a low of $1.82 per lb

Copper Fixed-Price Rod Sales Hedging / Copper Price Protection Programs

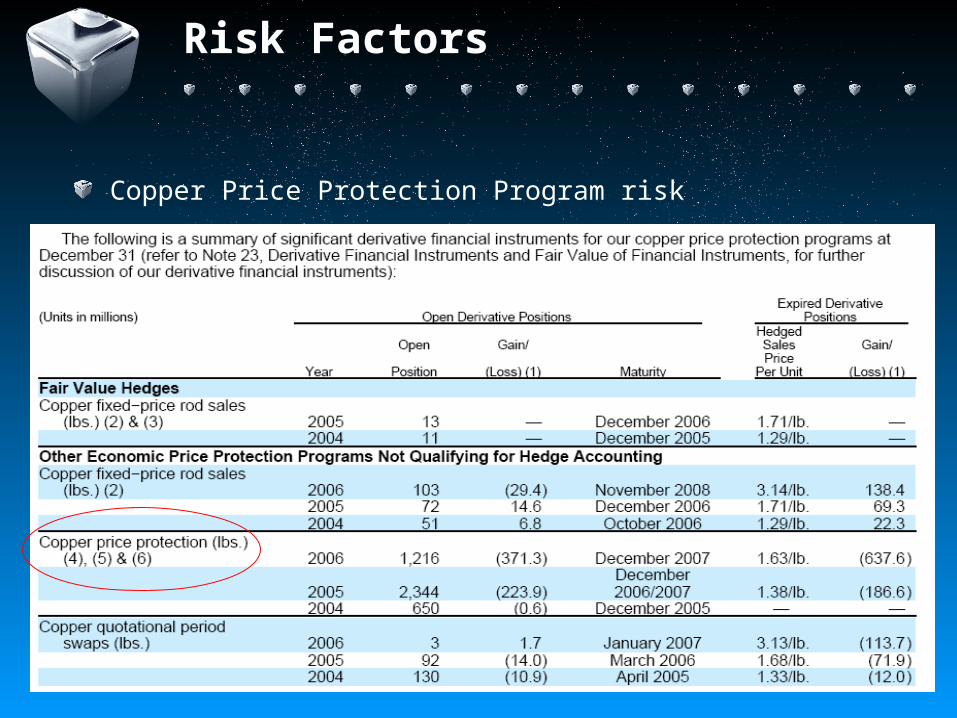

Risk Factors

Copper Price Protection Program risk

Risk Factors

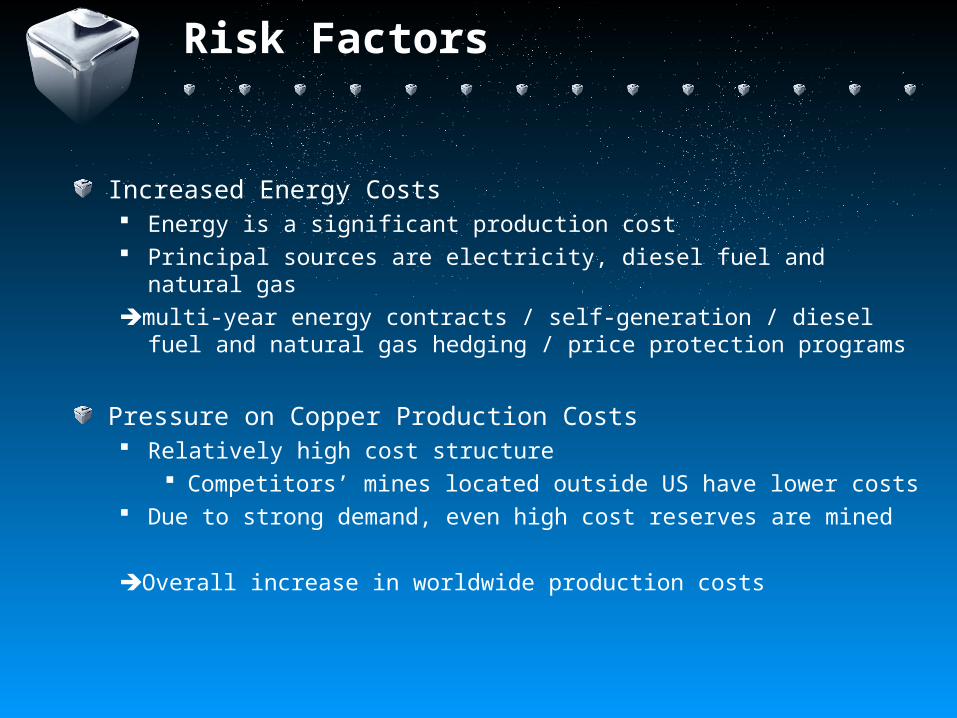

Increased Energy Costs Energy is a significant production cost Principal sources are electricity, diesel fuel and natural gasmulti-year energy contracts / self-generation / diesel fuel and

natural gas hedging / price protection programs

Pressure on Copper Production Costs Relatively high cost structure

Competitors’ mines located outside US have lower costs Due to strong demand, even high cost reserves are mined

Overall increase in worldwide production costs

Hedging Philosophy

“We do not purchase, hold or sell derivative financial instruments unless we have an exiting asset or obligation or we anticipate a future activity that is likely to occur and will result in exposing us to market risk. We do not enter into any instruments for speculative purposes. We use various strategies to manager our market risk, including the use of derivative instruments to limit, offset or reset or reduce our market exposure. Derivative financial instruments are used to manage well-defined commodity price, energy foreign exchange and interest rate risks from our primary business activities.”

Hedge Programs

Copper Fixed-Price Rod Sales HedgingCopper Price Protection ProgramsMetal Purchased HedgingGold and Silver Price Protection ProgramCopper Quotational Period Swap ProgramDiesel Fuel/Natural Gas Price Protection ProgramInterest Rate HedgingForeign currency Hedging

Fixed sales price instead of the COMEX average price

Enter copper futures and swap contracts

619M(2006), 492M(2005) and 381M(2004) lbs of copper sales were hedged

The sensitivity analysis of copper futures contracts to change in copper prices if copper prices dropped 10% at the end of 2006, copper

futures contracts would result in a net loss of $30M. All losses would have been offset by a gain in sales

Copper Fixed-Price Rod Sales Hedging

Protection against unanticipated copper price decreases

Purchase zero-premium copper collars and copper put options to protect 2005, 2006, and expected 2007 global copper production

These transactions do not qualify as hedge accounting treatment (SFAS No.133) Adjusted to fair market value based on the forward curve price

and implied volatility as of the last day of the recording period

Copper Price Protection

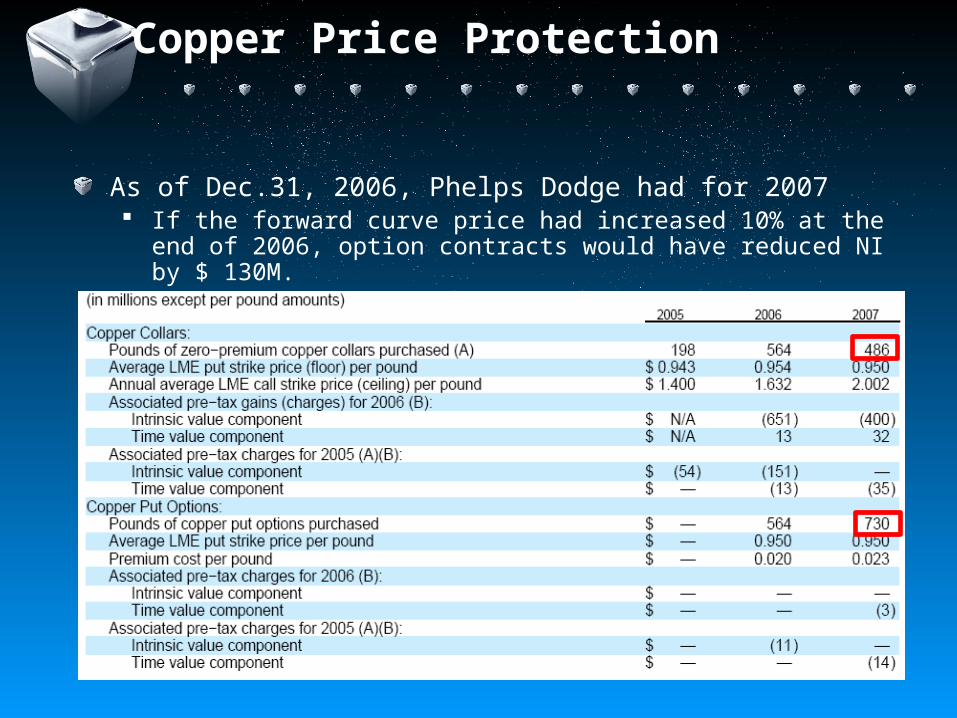

As of Dec.31, 2006, Phelps Dodge had for 2007 If the forward curve price had increased 10% at the end of

2006, option contracts would have reduced NI by $ 130M.

Copper Price Protection

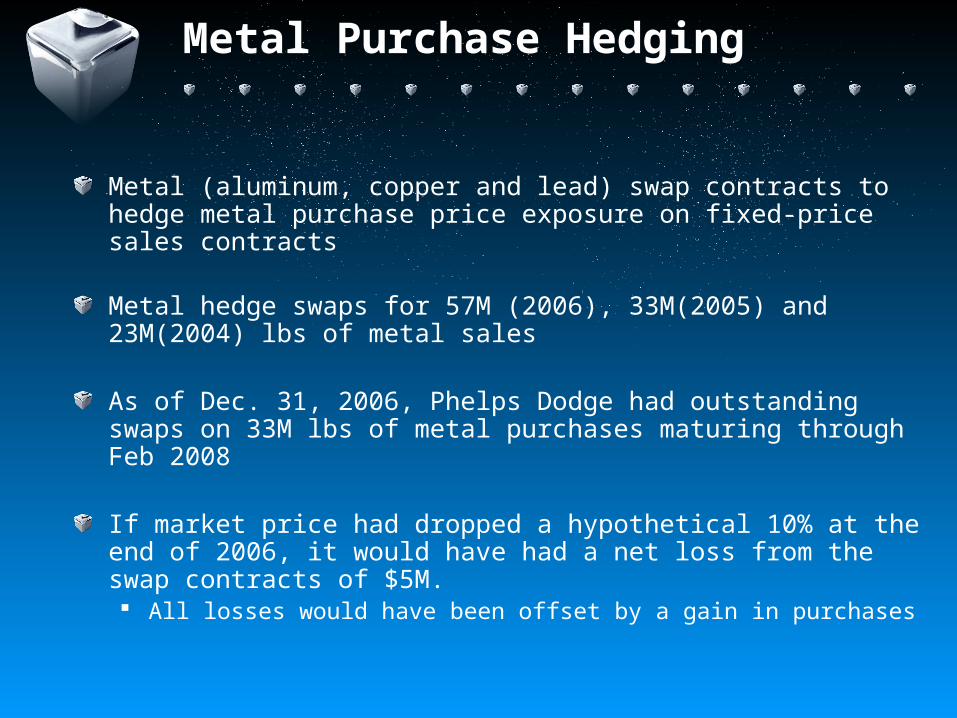

Metal (aluminum, copper and lead) swap contracts to hedge metal purchase price exposure on fixed-price sales contracts

Metal hedge swaps for 57M (2006), 33M(2005) and 23M(2004) lbs of metal sales

As of Dec. 31, 2006, Phelps Dodge had outstanding swaps on 33M lbs of metal purchases maturing through Feb 2008

If market price had dropped a hypothetical 10% at the end of 2006, it would have had a net loss from the swap contracts of $5M. All losses would have been offset by a gain in purchases

Metal Purchase Hedging

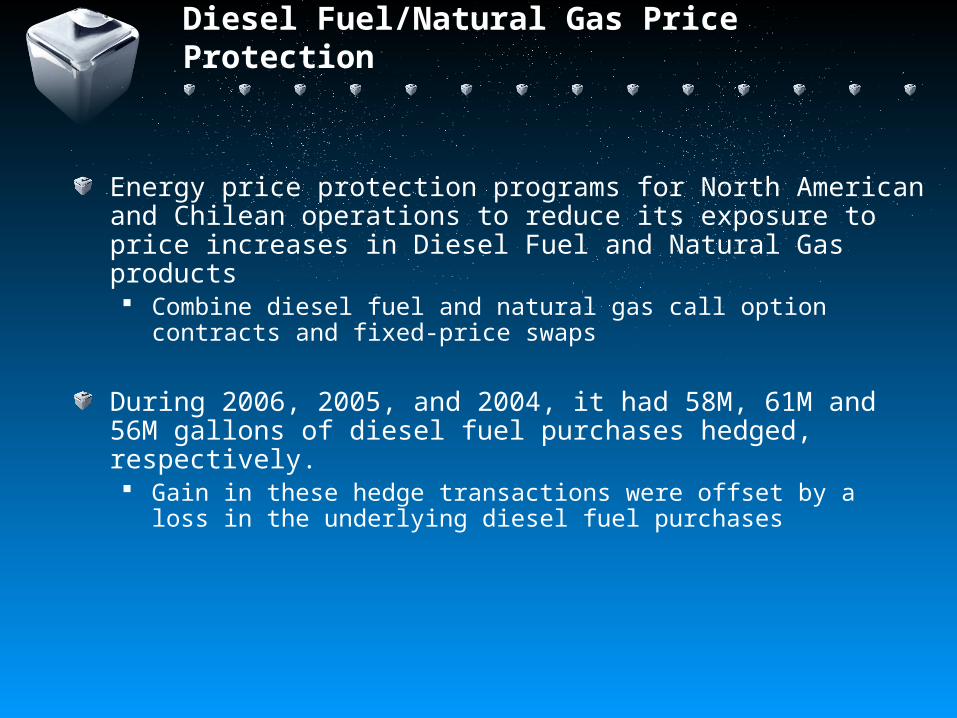

Energy price protection programs for North American and Chilean operations to reduce its exposure to price increases in Diesel Fuel and Natural Gas products Combine diesel fuel and natural gas call option contracts and

fixed-price swaps

During 2006, 2005, and 2004, it had 58M, 61M and 56M gallons of diesel fuel purchases hedged, respectively. Gain in these hedge transactions were offset by a loss in the

underlying diesel fuel purchases

Diesel Fuel/Natural Gas Price Protection

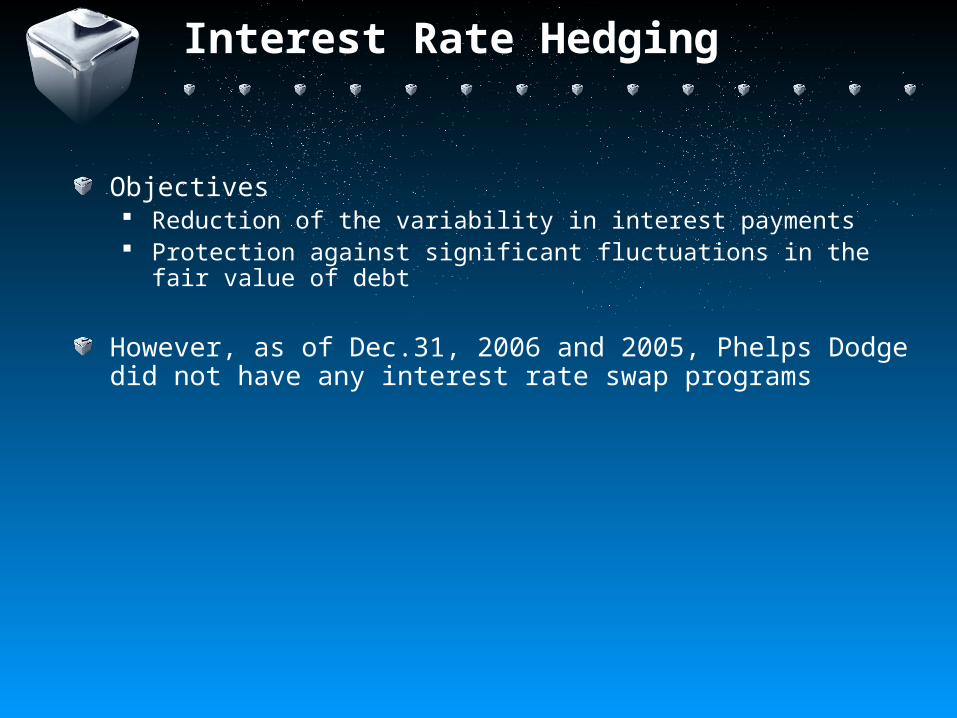

Objectives Reduction of the variability in interest payments Protection against significant fluctuations in the fair value of

debt

However, as of Dec.31, 2006 and 2005, Phelps Dodge did not have any interest rate swap programs

Interest Rate Hedging

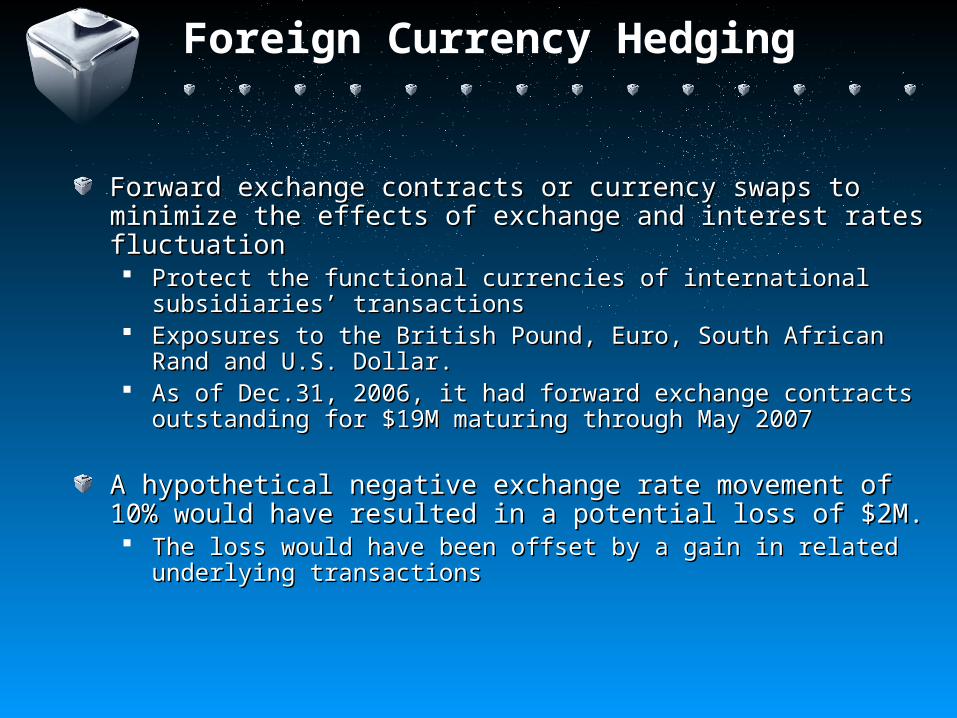

Forward exchange contracts or currency swaps to minimize Forward exchange contracts or currency swaps to minimize the effects of exchange and interest rates fluctuationthe effects of exchange and interest rates fluctuation Protect the functional currencies of international subsidiaries’ Protect the functional currencies of international subsidiaries’

transactionstransactions Exposures to the British Pound, Euro, South African Rand and Exposures to the British Pound, Euro, South African Rand and

U.S. Dollar. U.S. Dollar. As of Dec.31, 2006, it had forward exchange contracts As of Dec.31, 2006, it had forward exchange contracts

outstanding for $19M maturing through May 2007outstanding for $19M maturing through May 2007

A hypothetical negative exchange rate movement of 10% A hypothetical negative exchange rate movement of 10% would have resulted in a potential loss of $2M. would have resulted in a potential loss of $2M. The loss would have been offset by a gain in related underlying The loss would have been offset by a gain in related underlying

transactionstransactions

Foreign Currency Hedging

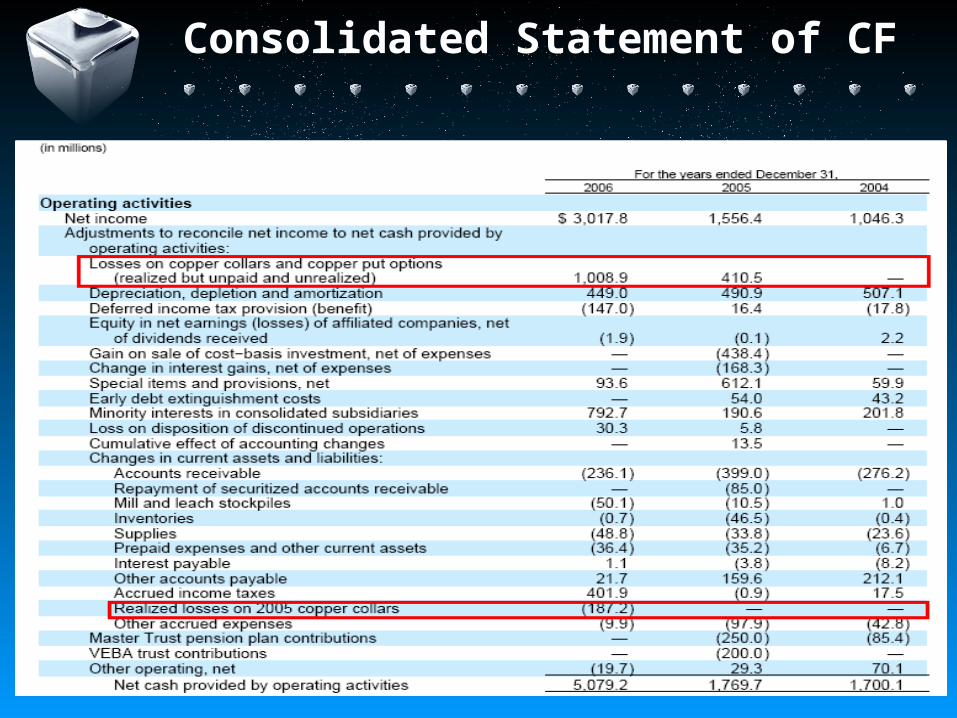

Consolidated Statement of CF

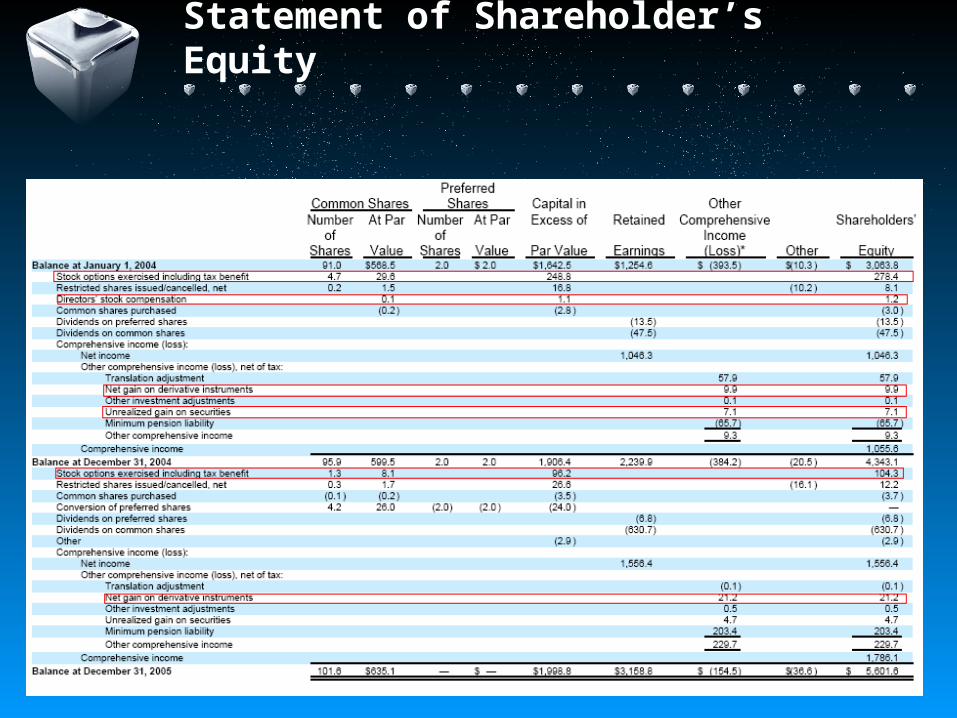

Statement of Shareholder’s Equity

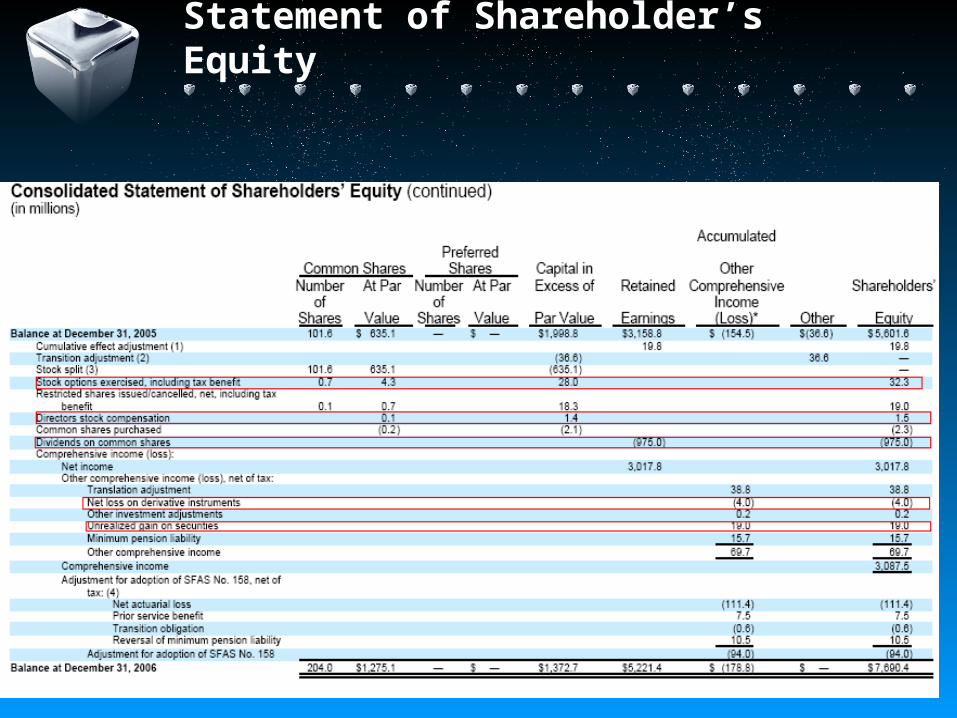

Statement of Shareholder’s Equity

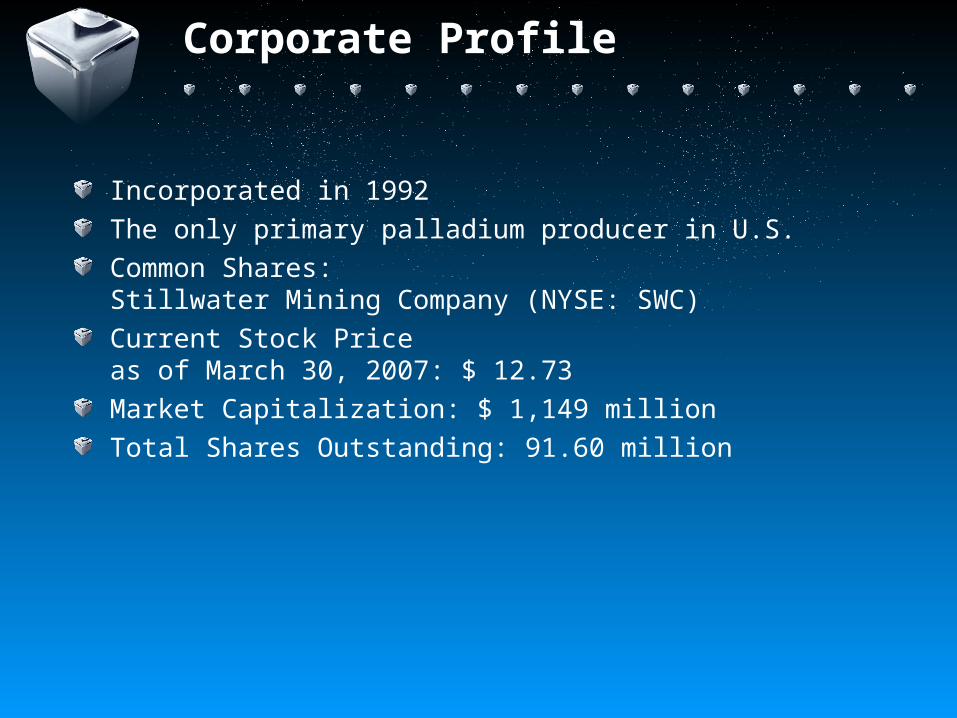

Incorporated in 1992 The only primary palladium producer in U.S. Common Shares:Stillwater Mining Company (NYSE: SWC)Current Stock Priceas of March 30, 2007: $ 12.73 Market Capitalization: $ 1,149 millionTotal Shares Outstanding: 91.60 million

Corporate Profile

Profile

One of the world's leading producers of platinum group metals (PGMs)The only significant primary producer of palladium in the Western Hemisphere Extraction: two mines in southern MontanaConcentration and refining: a site near Columbus, Montana, to a purity of 60% PGMs, then shipped to Johnson Matthey for final refining of palladium, platinum and other metals at a facility in New Jersey.

Profile

The Company's 28-mile long JM Reef in Montana is the highest grade ore-body containing platinum group metals (PGMs).

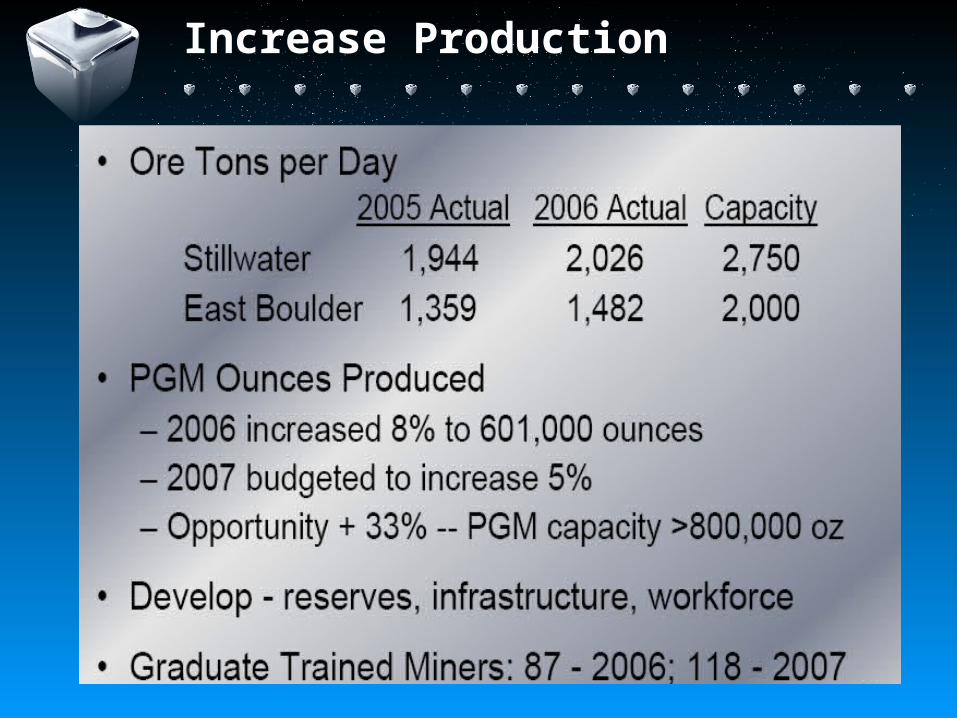

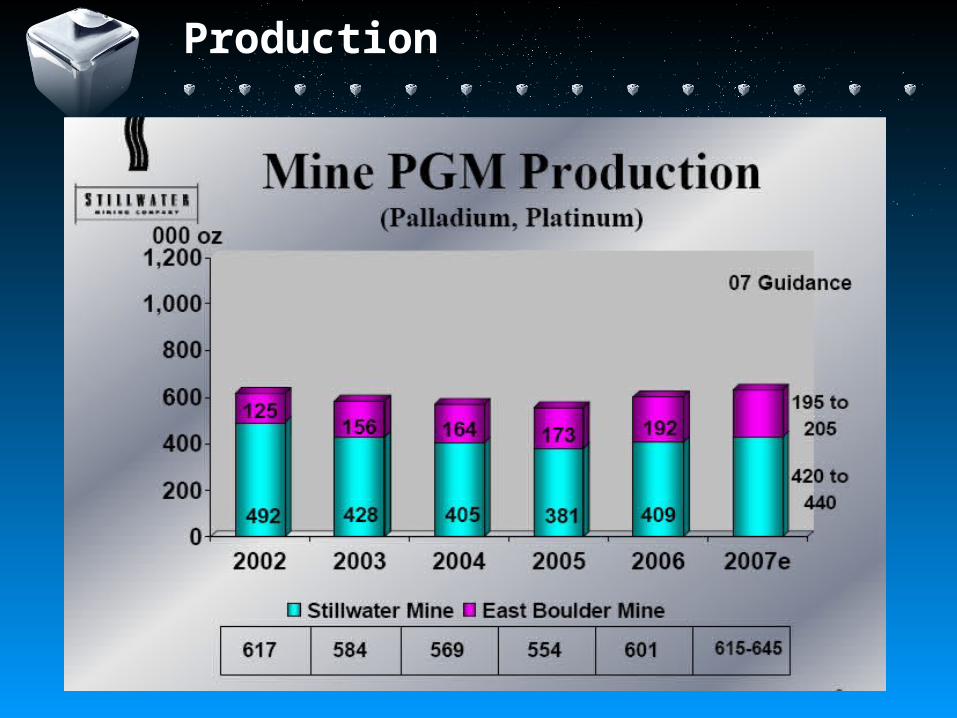

In 2006 the Company’s PGM production increased 8% to 601,000 ounces of PGMs.

In 2007 the company expects PGM production to increase by 5% and plan to increase its PGM capacity more than 800,000 ounces.

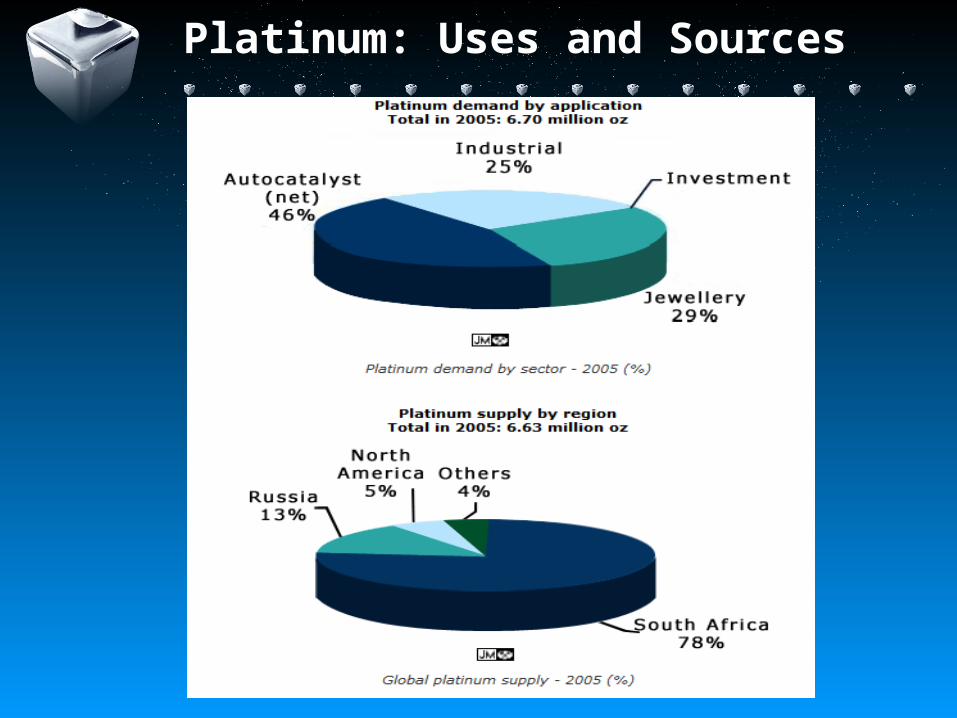

Platinum: Uses and Sources

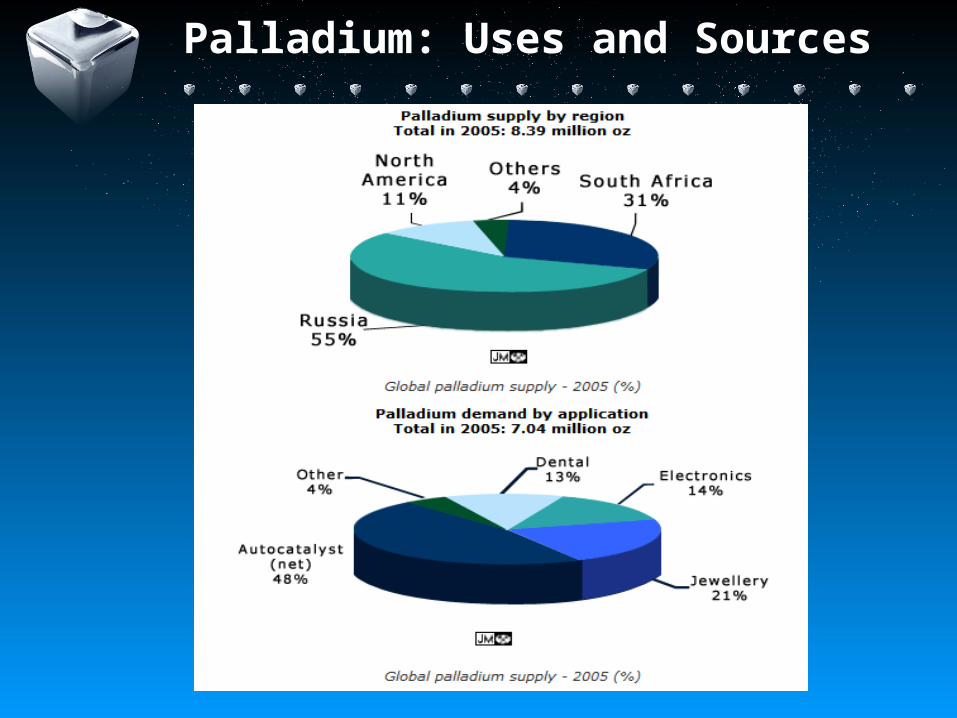

Palladium: Uses and Sources

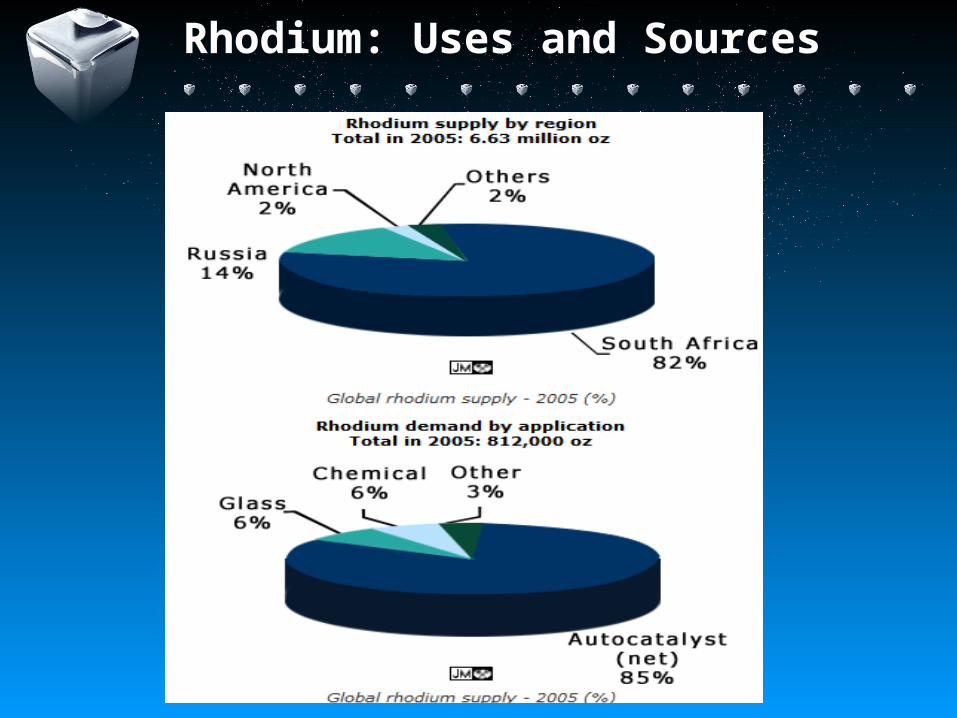

Rhodium: Uses and Sources

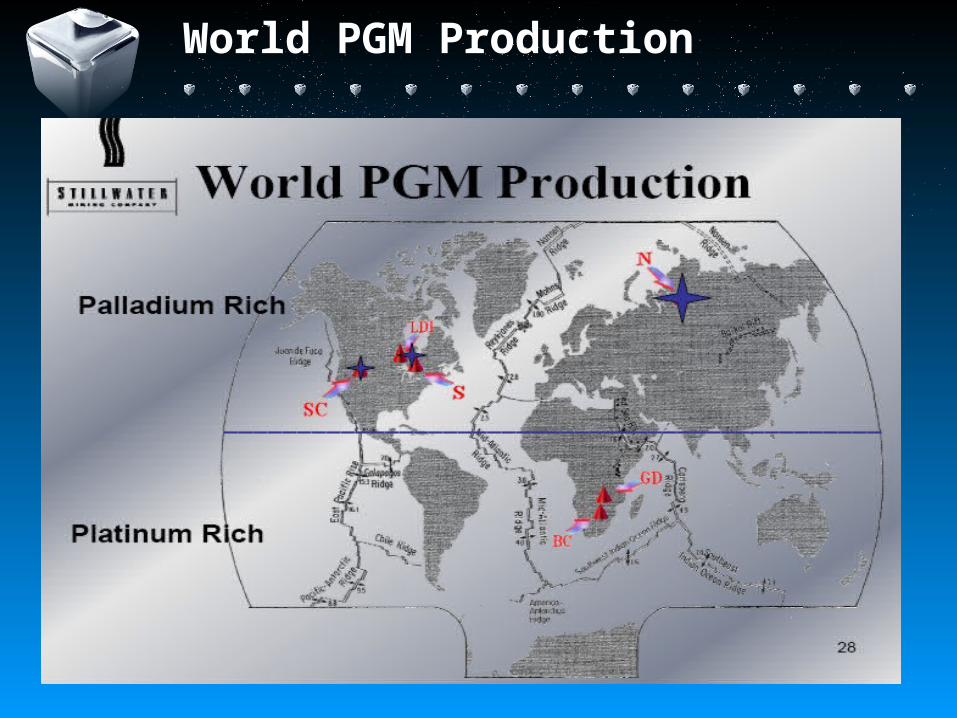

World PGM Production

Stillwater Properties

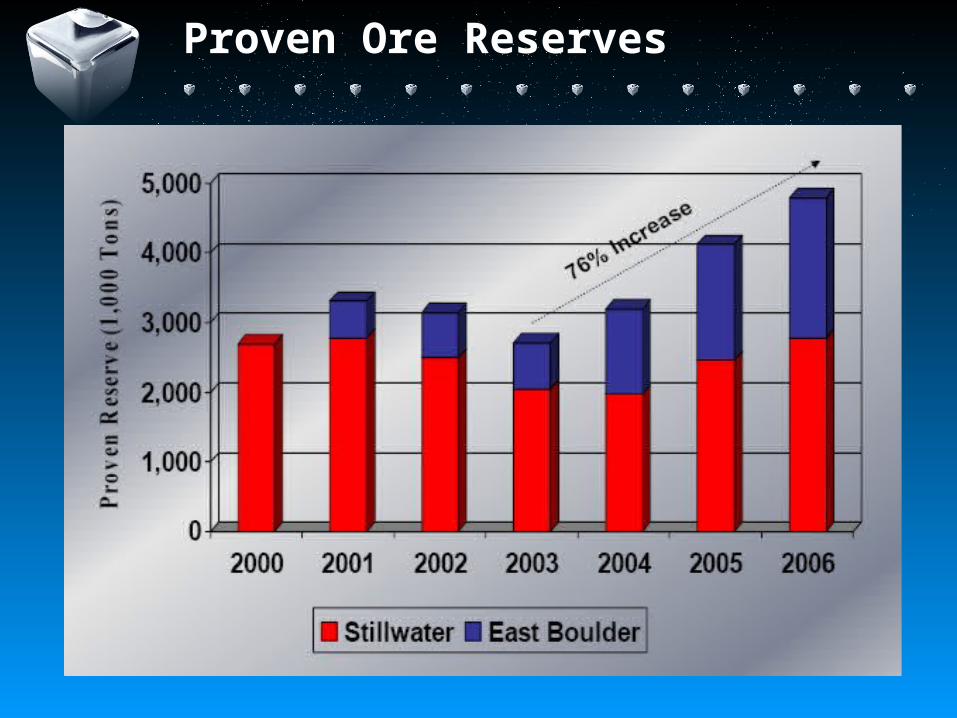

Proven Ore Reserves

Developed State

Upgrade infrastructure- 2006: Four major projects completed- 2007: smelter furnace addition

Increase proven reserves- Key driver on production growth- Primary development, diamond drilling

Proven Ore Reserves

Transforming the Mines

Continue to Advance Safety systems

Increase Developed State of Mines

Expand selective mining methods

Increase production levels

Reduce operating costs

Increase Production

Production

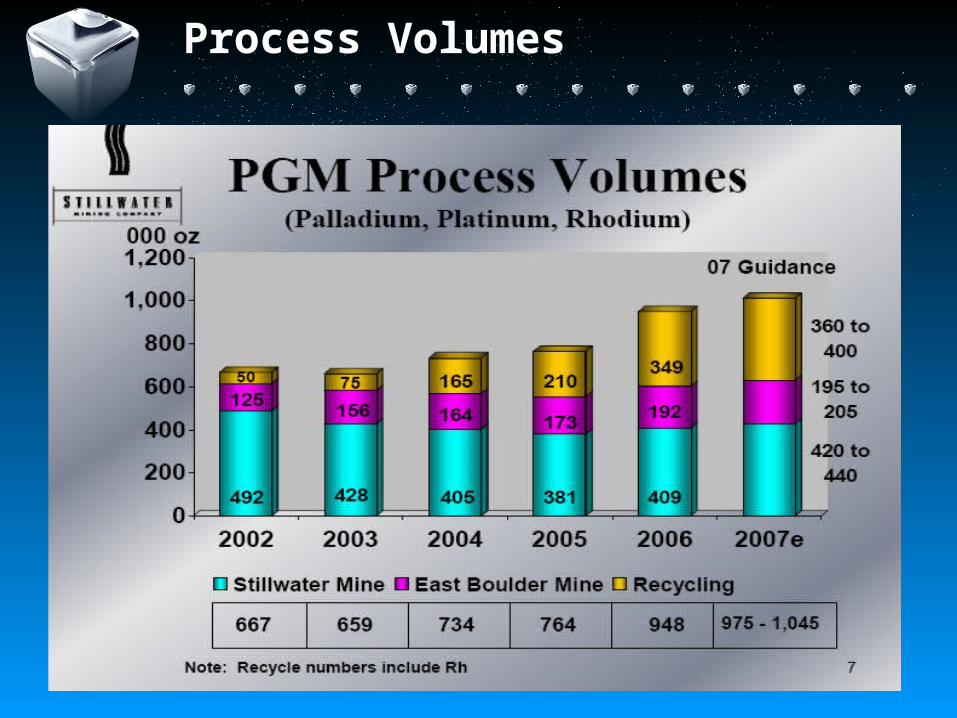

Process Volumes

Officers

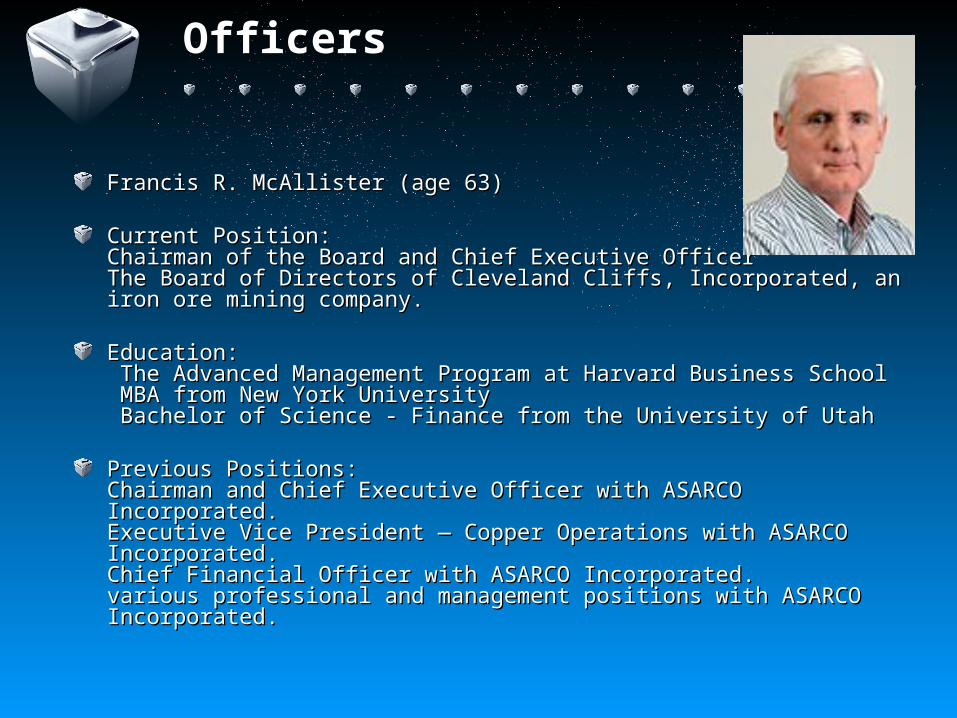

Francis R. McAllister (age 63) Francis R. McAllister (age 63)

Current Position:Current Position:Chairman of the Board and Chief Executive OfficerChairman of the Board and Chief Executive OfficerThe Board of Directors of Cleveland Cliffs, Incorporated, an iron ore The Board of Directors of Cleveland Cliffs, Incorporated, an iron ore mining company.mining company.

Education:Education: The Advanced Management Program at Harvard Business School The Advanced Management Program at Harvard Business School MBA from New York University MBA from New York University Bachelor of Science - Finance from the University of Utah Bachelor of Science - Finance from the University of Utah

Previous Positions:Previous Positions:Chairman and Chief Executive Officer with ASARCO Incorporated. Chairman and Chief Executive Officer with ASARCO Incorporated. Executive Vice President — Copper Operations with ASARCO Executive Vice President — Copper Operations with ASARCO Incorporated.Incorporated.Chief Financial Officer with ASARCO Incorporated.Chief Financial Officer with ASARCO Incorporated.various professional and management positions with ASARCO various professional and management positions with ASARCO Incorporated.Incorporated.

Officers

Gregory A. Wing (age 56)

Current Position: Chief Financial Officer

Education: M.B.A in Accounting and Finance from the University of California at BerkeleyBachelor of Arts in Physics from the University of California at Berkeley

Previous Positions:Vice President of Finance and Chief Financial Officer with Black Beauty Coal Company Manager of Financial Planning and Analysis with Pittsburg and Midway Coal Mining Company (a subsidiary of Chevron Corporation)Senior Analyst in Corporation Planning with Chevron Corporation

Financial Highlights

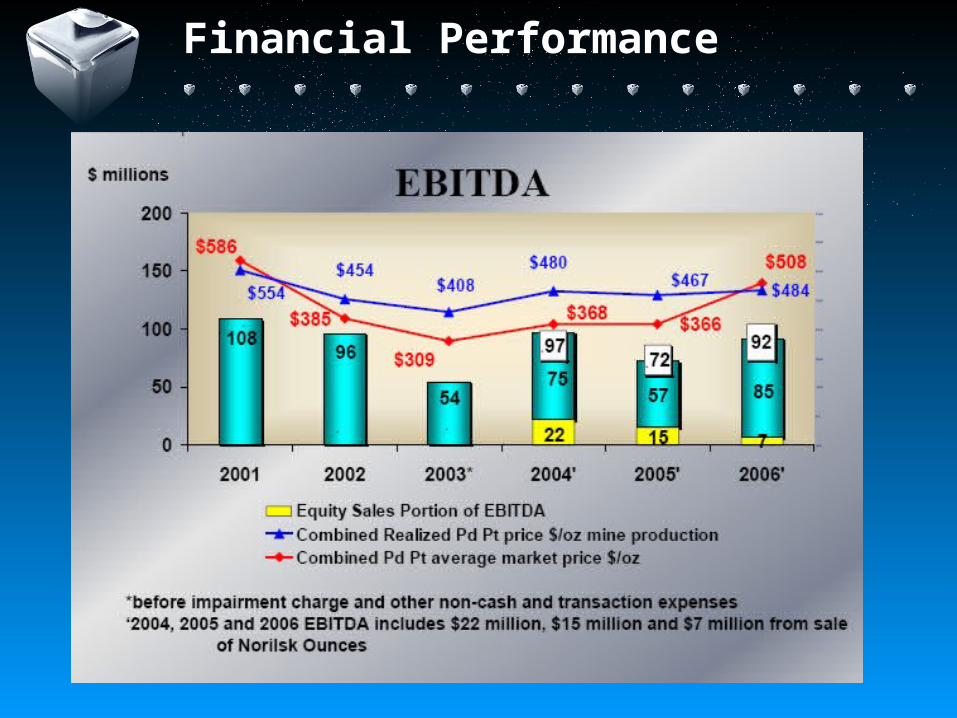

Financial Performance

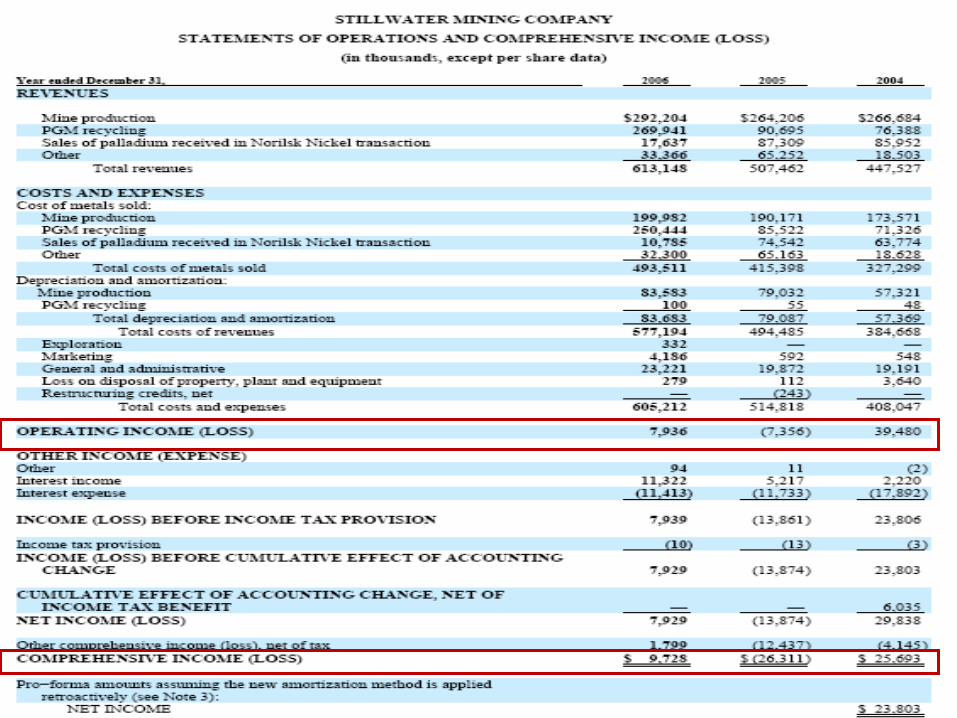

Income Statement

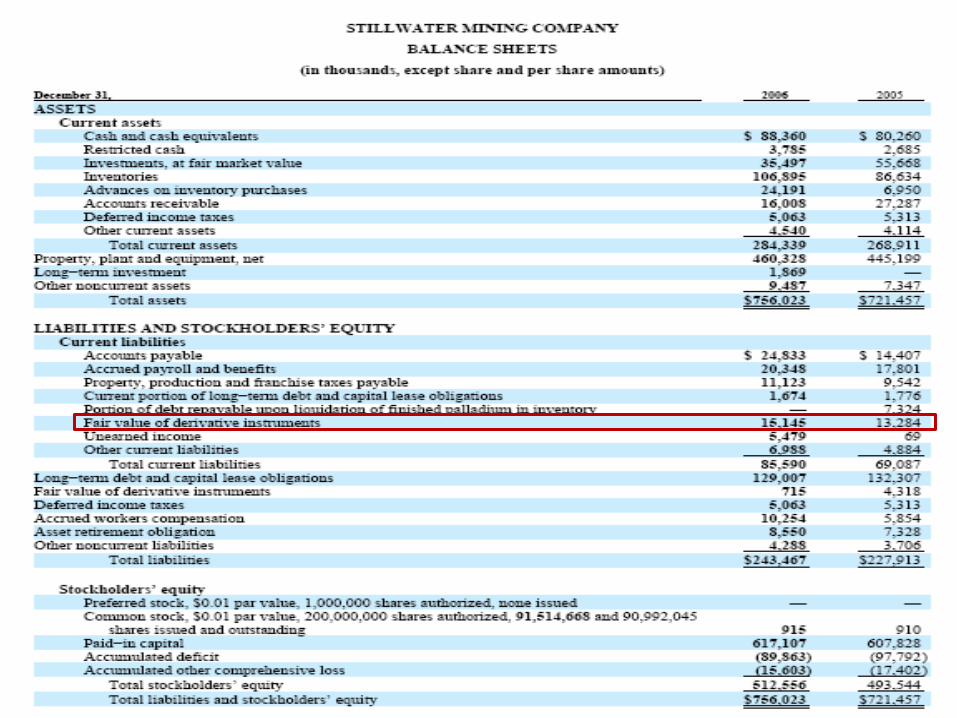

Consolidated Balance Sheets

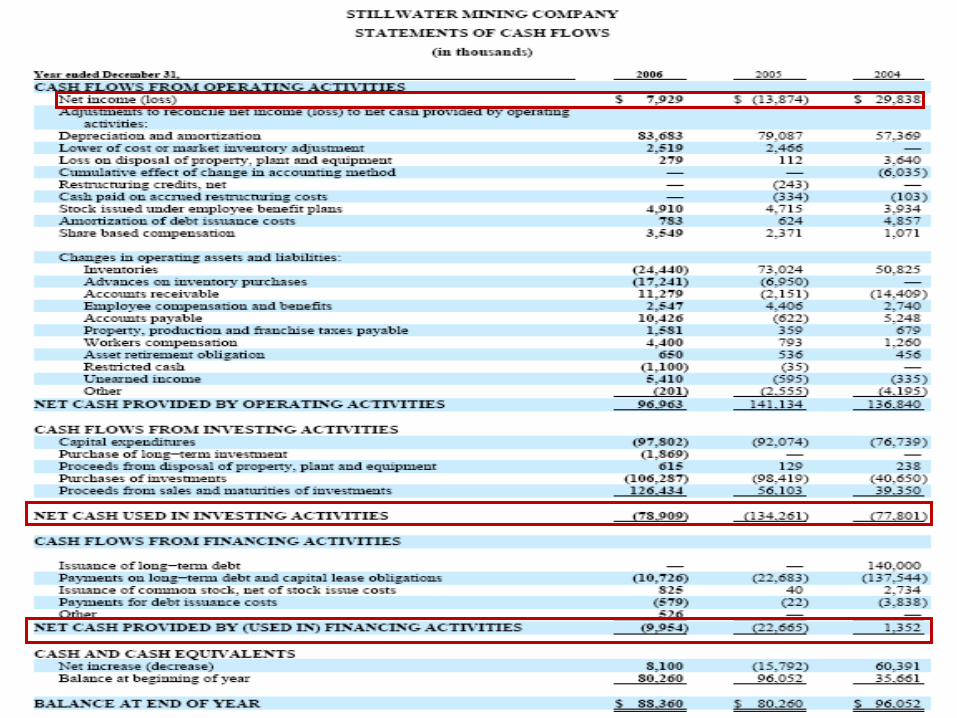

Statements Of Cash Flows

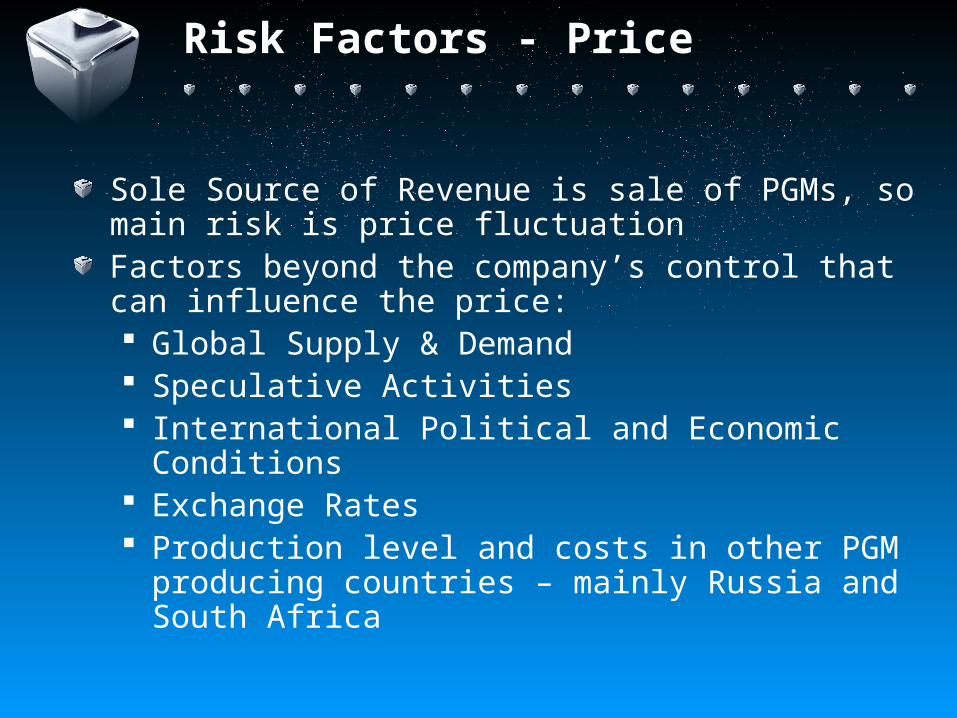

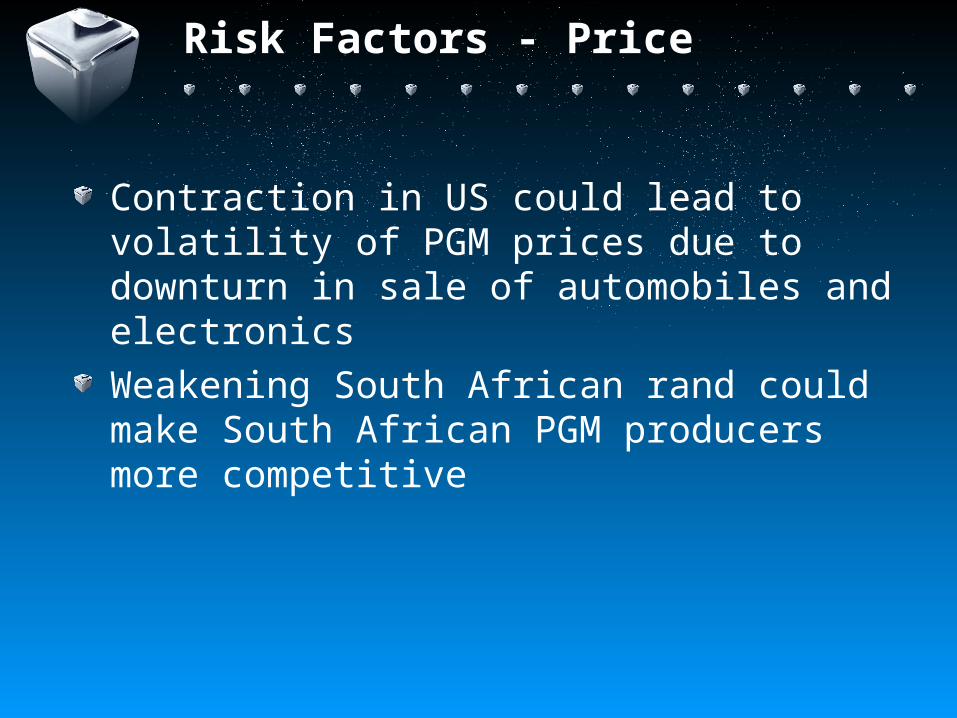

Risk Factors - Price

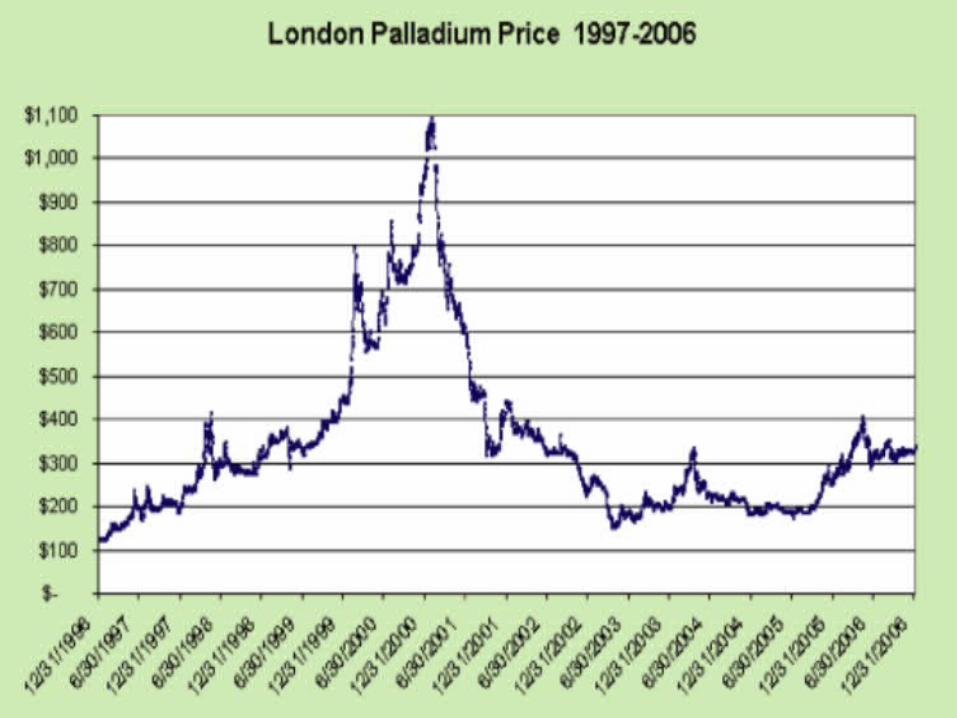

Sole Source of Revenue is sale of PGMs, so main risk is price fluctuationFactors beyond the company’s control that can influence the price: Global Supply & Demand Speculative Activities International Political and Economic Conditions Exchange Rates Production level and costs in other PGM

producing countries – mainly Russia and South Africa

Risk Factors - Price

Contraction in US could lead to volatility of PGM prices due to downturn in sale of automobiles and electronicsWeakening South African rand could make South African PGM producers more competitive

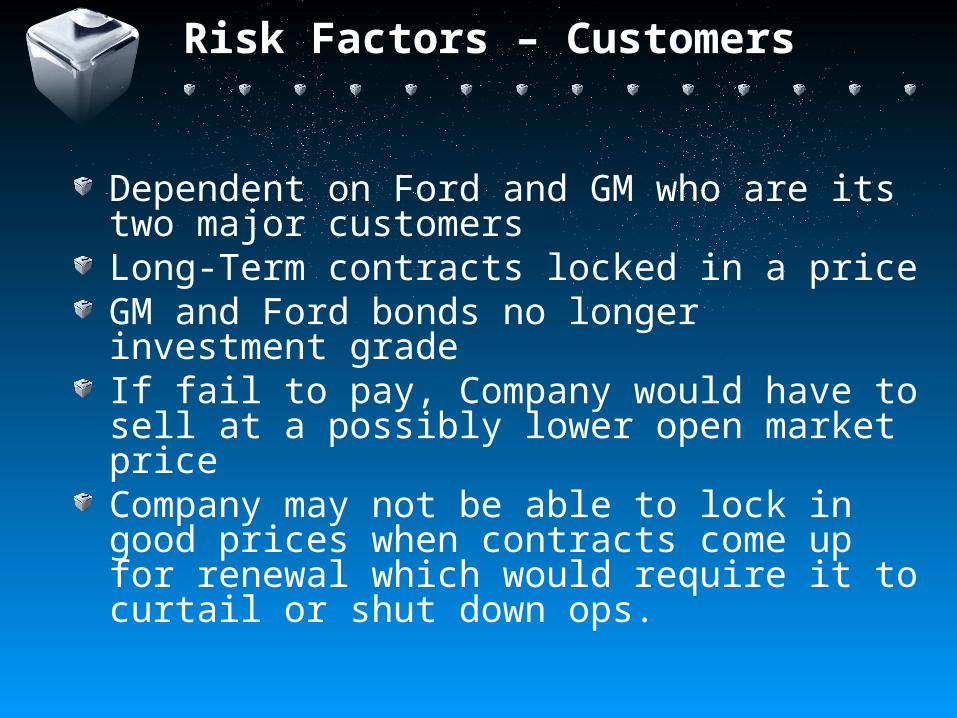

Risk Factors – Customers

Dependent on Ford and GM who are its two major customersLong-Term contracts locked in a priceGM and Ford bonds no longer investment gradeIf fail to pay, Company would have to sell at a possibly lower open market priceCompany may not be able to lock in good prices when contracts come up for renewal which would require it to curtail or shut down ops.

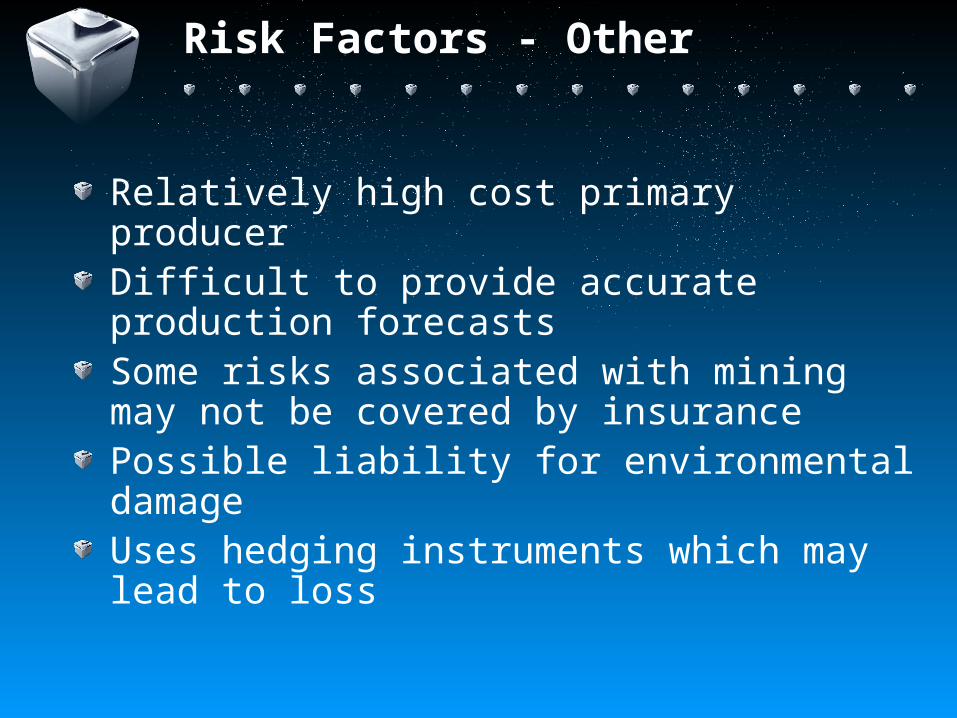

Risk Factors - Other

Relatively high cost primary producerDifficult to provide accurate production forecastsSome risks associated with mining may not be covered by insurancePossible liability for environmental damageUses hedging instruments which may lead to loss

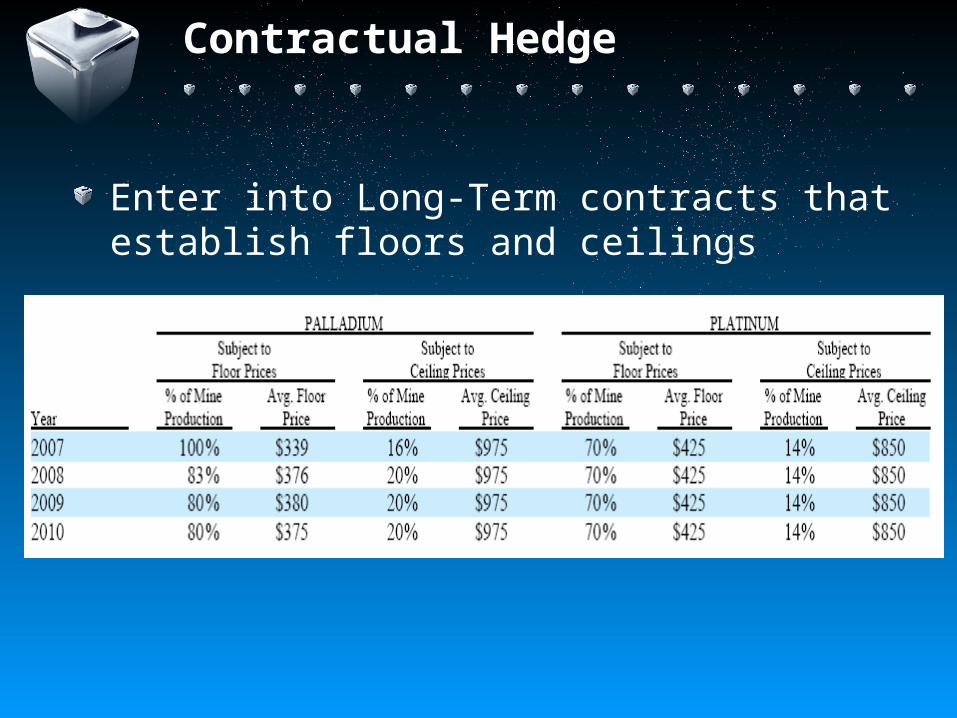

Contractual Hedge

Enter into Long-Term contracts that establish floors and ceilings

Derivatives Usage

Fixed Forwards, Cashless Put and Call Collar Options and Financially Settled ForwardsUsed to Hedge Metal Prices and Interest Rate RiskLoss of $15.8 million in 2006Highly Effective Hedges – Fair Value of Derivatives offset changes in the hedged transaction very well due to high correlation between hedged transaction and financial instrument

Commodity Price Risk

Financially Settled Forwards accounted as cash flow hedgesFinancially Settled Forward contracts cover half of its anticipated platinum sales until June 2008.Hedged 113,500 ounces of platinum sales at an average price of approximately $988/ounce.

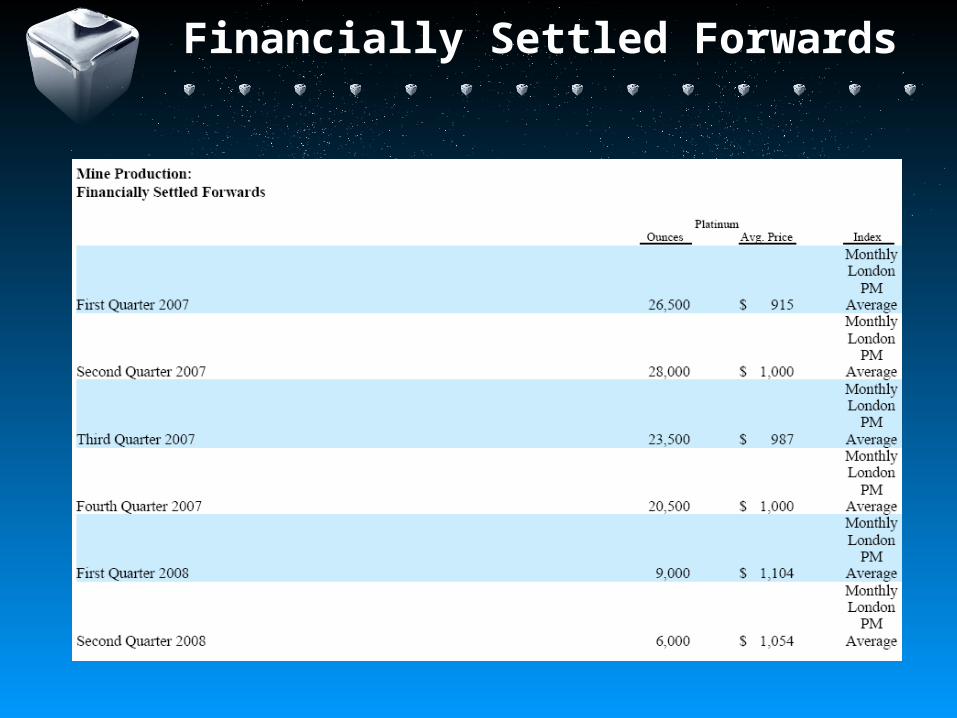

Financially Settled Forwards

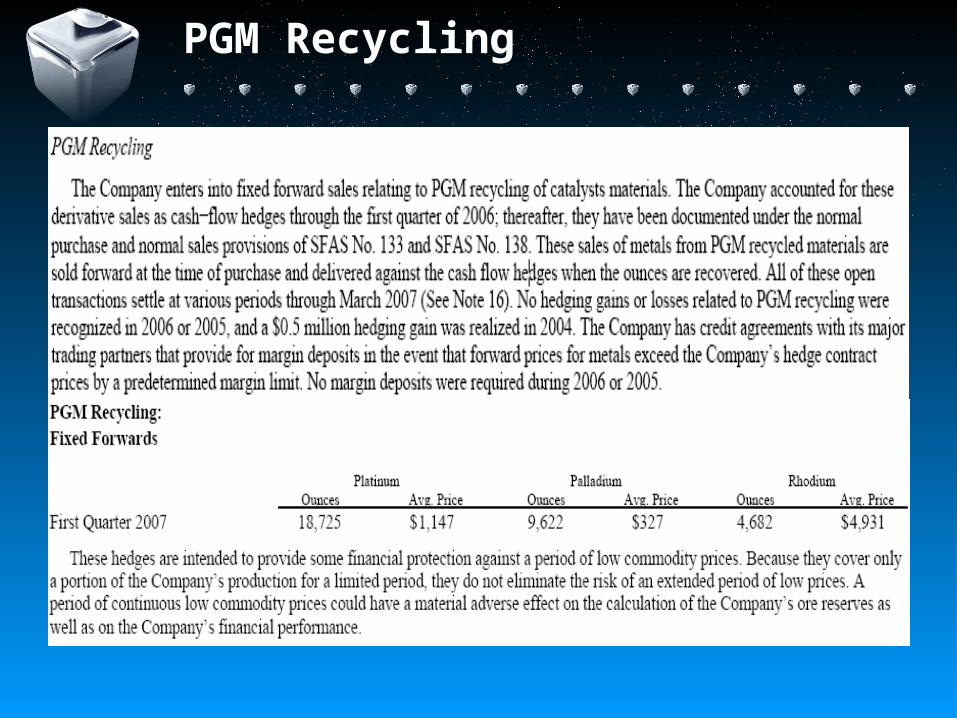

PGM Recycling

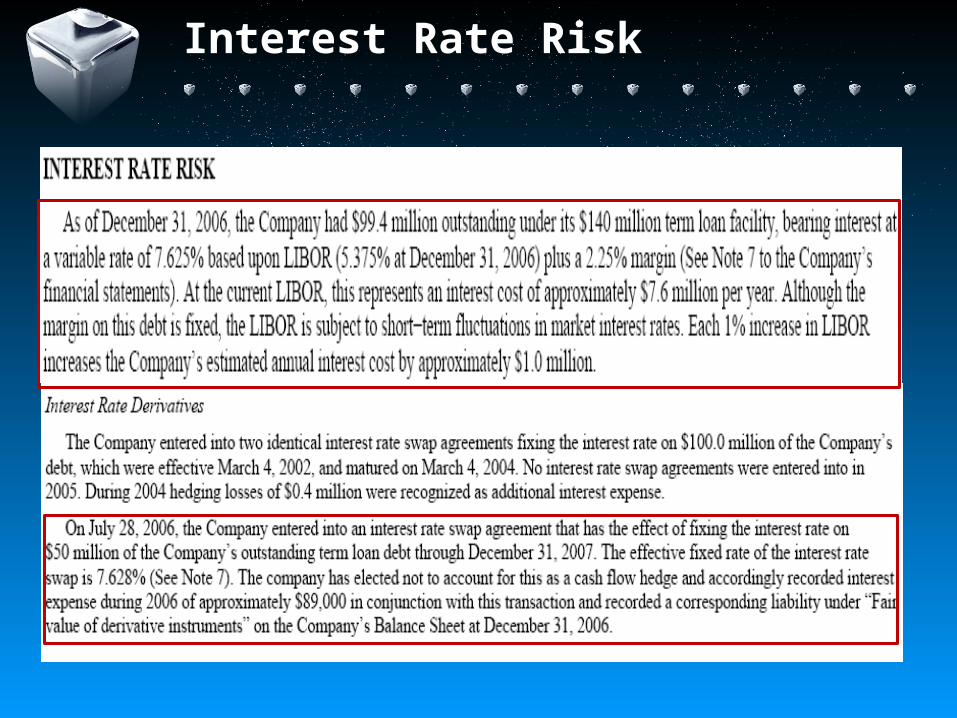

Interest Rate Risk

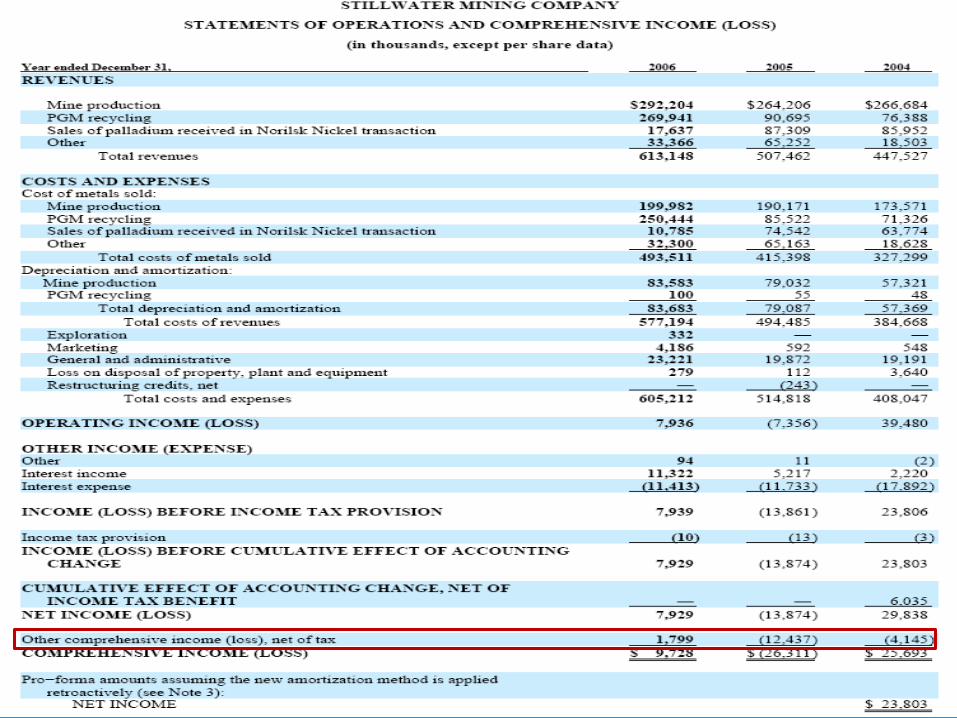

Other Comprehensive Income

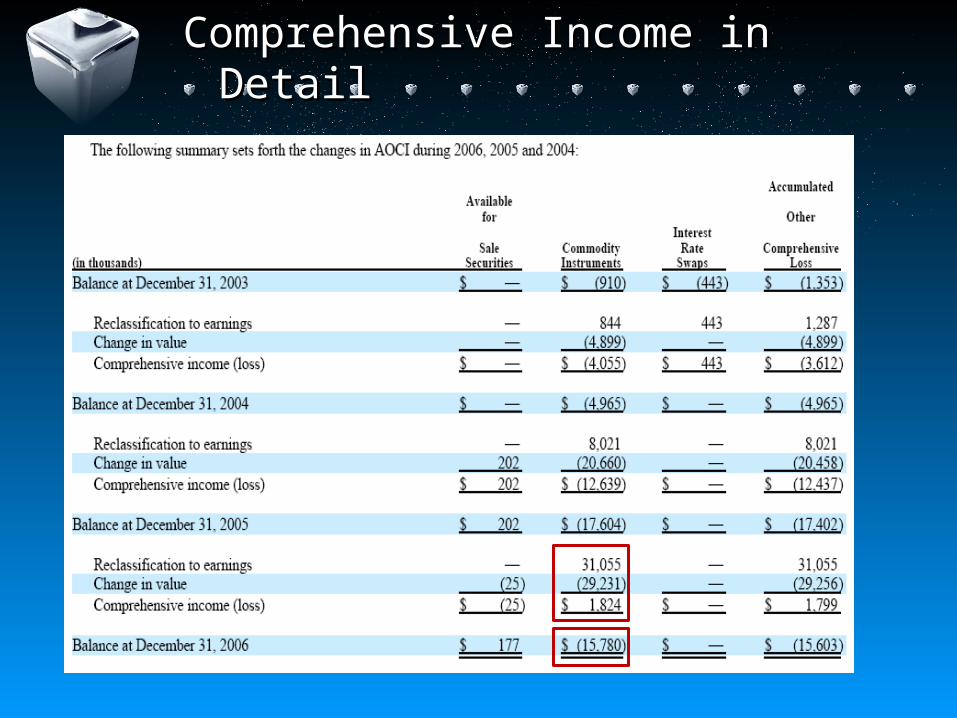

Contains $31.1 million of realized hedging losses offset by $29.3 million change in fair value of derivatives held$25,000 difference is the unrealized loss on investments held for sale

Comprehensive Income in DetailComprehensive Income in Detail

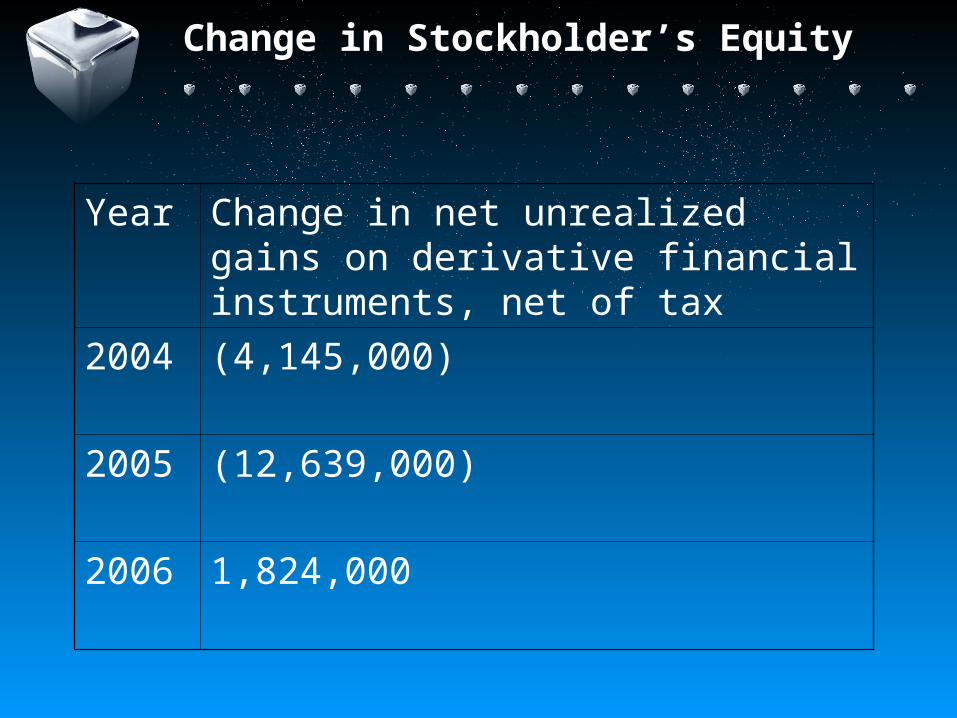

Change in Stockholder’s Equity

Year Change in net unrealized gains on derivative financial instruments, net of tax

2004 (4,145,000)

2005 (12,639,000)

2006 1,824,000

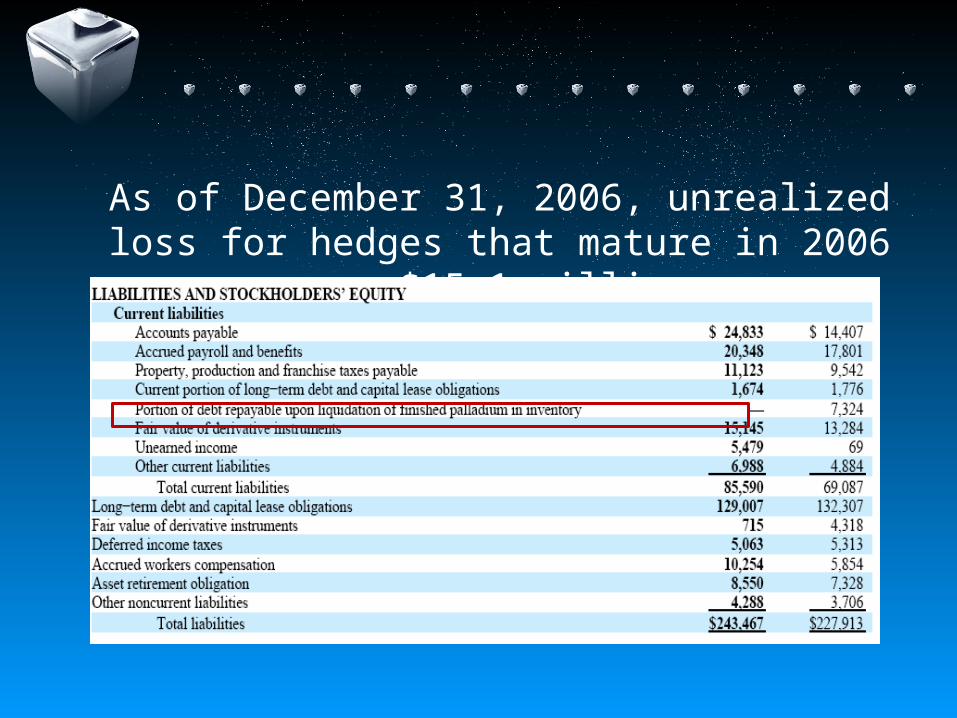

As of December 31, 2006, unrealized loss for hedges that mature in 2006 was $15.1

million

Fair Value

Stillwater classifies it as the price to sell an asset or to pay to transfer a liability (exit price) not the price paid to acquire an asset or assume liability (entry price)Derivatives must be recognized on the balance sheet, and, if the derivative is not designated as a hedging instrument, changes in the fair value must be recognized in the earnings in the period of the hedge

Stock Options

Estimated at the date of grant using the Black-Scholes option pricing modelThe effect of stock options on diluted weighted average shares outstanding was 85,341 in 2006Options expire 10 years after the grantMay consist of incentive stock options (ISOs) or non-qualified stock options (NQSOs), stock appreciation rights (SARs), nonvested shares or other stock-based awards, with the exception that non-employee directors may not be granted SARs and only employees of the Company may be granted ISOs.

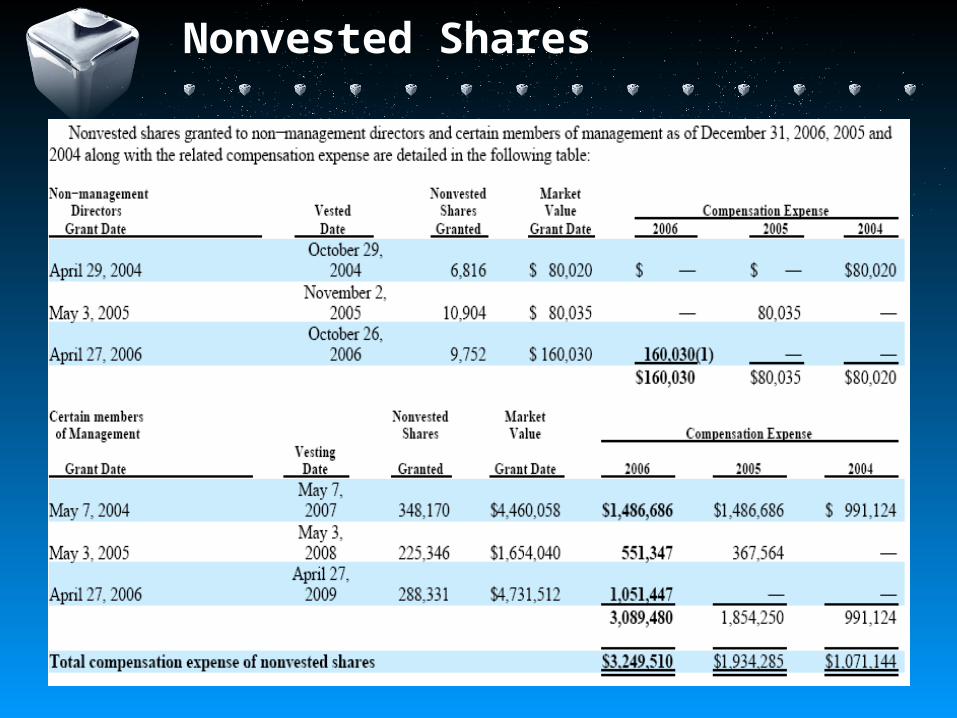

Nonvested Shares

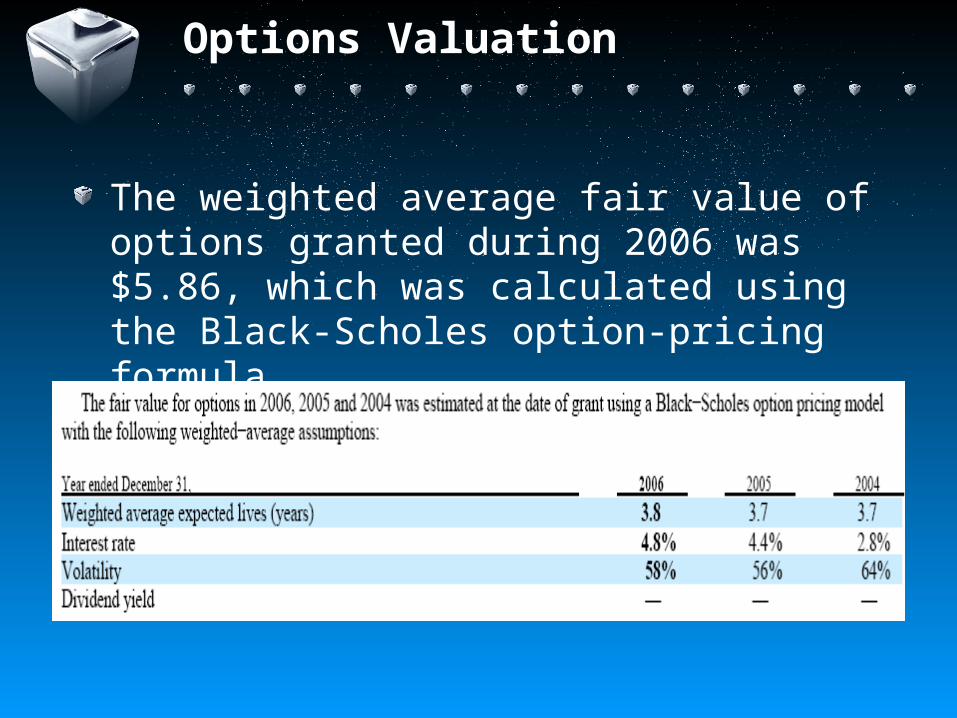

Options Valuation

The weighted average fair value of options granted during 2006 was $5.86, which was calculated using the Black-Scholes option-pricing formula.

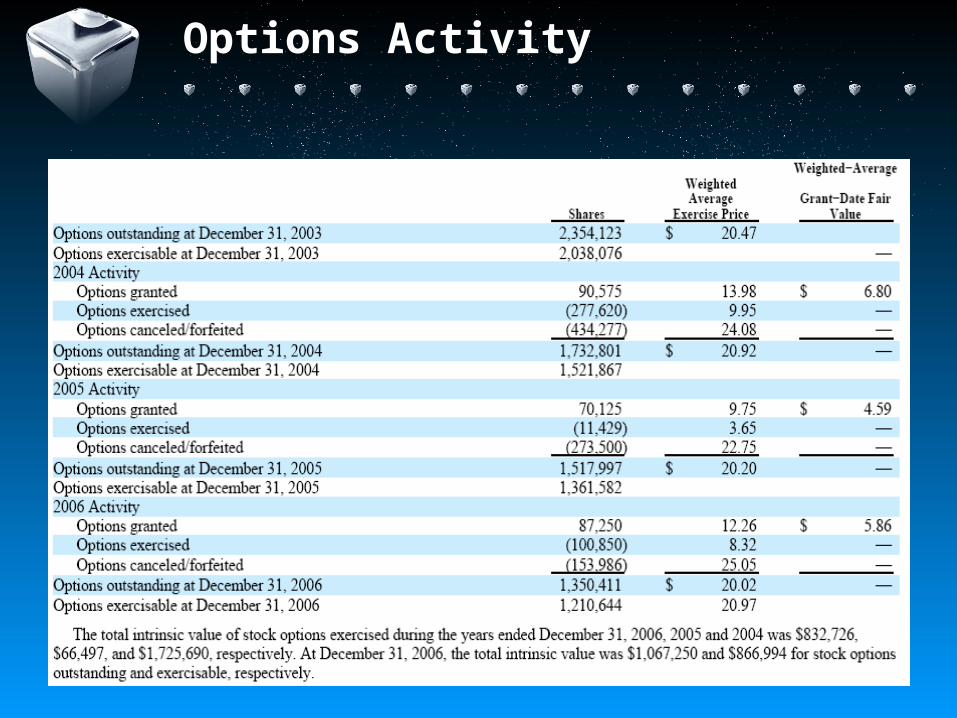

Options Activity

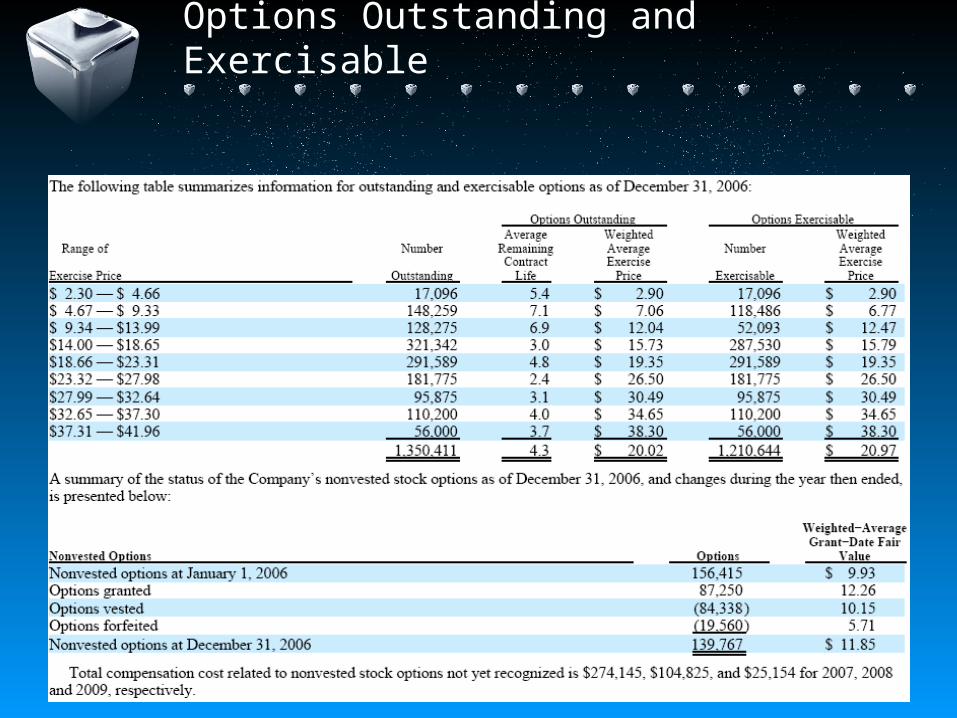

Options Outstanding and Exercisable