Embed Size (px)

Citation preview

Limited English Proficiency

Fair Lending and UDAAP Impact

Brad BlowerVice President, Principal ComplianceLeader, Consumer Practices

American Express

Stephanie RobinsonPartner

Mayer [email protected]

2

Speakers

Brad BlowerVice President, PrincipalCompliance Leader,Consumer PracticesAmerican Express

Stephanie RobinsonPartnerMayer [email protected]

3

• Who is a Limited English Proficiency (LEP) individual?

• Opportunities

• Regulatory and enforcement trends signaling focus onLEP consumer support

• Risks

• State foreign-language disclosure laws

• What should I do?

• Questions

Overview

4

• According to LEP.gov, a federal interagency website, LEPindividuals are:

– “Individuals who do not speak English as their primary languageand who have a limited ability to read, speak, write, orunderstand English.”

Who is a Limited English Proficiency (LEP)Individual?

5

• The foreign born represent a significant source of housingdemand.

• Net international immigration increased over 40% from 2011to 2014.

• 63.2 million US residents in 2014 spoke a language other thanEnglish at home and over 40 percent of those residents speakEnglish less than “very well.”

• Increase in immigration will cause uptick in LEP individuals’demand for financial products and services.

• Lenders have an opportunity to serve a growing, andpotentially underserved, market.

Opportunities

6

• Executive Order 13166, “Improving Access to Services forPersons with Limited English Proficiency.”

• DOJ Guidance, LEP Guidance to Recipients, 67 Fed. Reg.41455 (June 18, 2002)

• HUD Guidance, 72 Fed. Reg. 50121 (Jan. 22, 2007)

• HUD Rule on Affirmatively Furthering Fair Housing, 80Fed. Reg. 42272 (July 16, 2015)

• CFPB Language Access Plan, 79 Fed. Reg. 60840 (October8, 2014)

• CFPB Exam Manual–Mortgage Servicing module

Regulatory and Supervisory Focus on LEP ConsumerSupport

7

• Litigation and enforcement

– Fair lending laws.

• Fair Housing Act, 42 U.S.C. § 3601, et seq.

• Equal Credit Opportunity Act, 15 U.S.C. § 1691, et seq.

– Unfair, Deceptive, or Abusive Acts or Practices (UDAAP)

– State foreign-language disclosure laws

– CFPB enforcement actions

• Synchrony consent order

Risks

8

• Arizona

– Requiring a variety of financial services providers to give Spanish-language notices and disclosures.See Ariz. Rev. Stat. §§ 6-631 (consumer loan lenders), 6-1257 (deferred presentment companies), 6-1411 (premium finance companies), and 44-1362 (check cashers).

• California

– California lenders negotiating loans in Spanish, Korean, Chinese, Tagalog or Vietnamese are requiredto provide certain disclosures in those languages. See Cal. Civ. Code §§ 1632.5.

• Connecticut

– Drawee of a dishonored check required to demand payment from the drawer in both Spanish andEnglish. See Conn. Gen. Stat. § 52-565a(g).

• Delaware

– Requirement that lenders of short-term, closed-end consumer loans must provide loan applicationsin Spanish and English, with a conspicuously displayed written disclosure of certain consumerinformation. See 5 Del. Code §§ 978(b), 2235A.

State Foreign-Language Disclosure Laws

9

• Illinois

– Disclosure and translation requirements for non-English-language transactions involving retail sales.See 815 ILCS 505/2N.

• Kansas and Nebraska

– Requiring notice of cancellation of rights in Spanish in door-to-door solicitations. See K.S.A. § 50-640(b); Neb. Rev. Stat. § 69-1604(3).

• New York

– Licensed check cashers required to post fee schedules in English and Spanish. See 3 N.Y.C.R.R.400.5(a)(1).

State Foreign-Language Disclosure Laws (cont.)

WHAT SHOULD I DO?

11

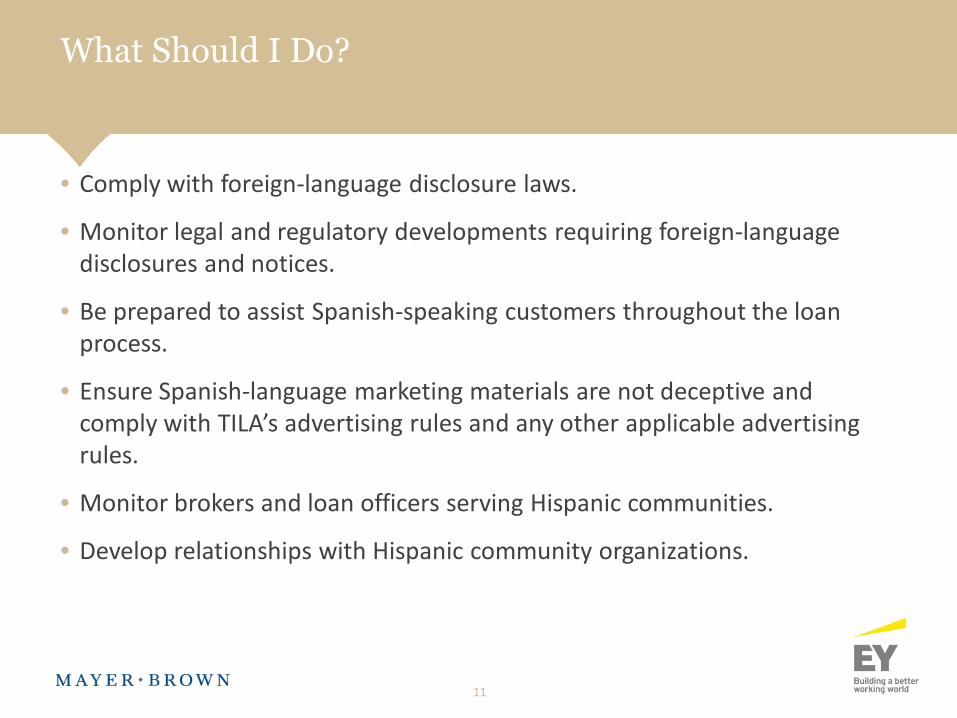

• Comply with foreign-language disclosure laws.

• Monitor legal and regulatory developments requiring foreign-languagedisclosures and notices.

• Be prepared to assist Spanish-speaking customers throughout the loanprocess.

• Ensure Spanish-language marketing materials are not deceptive andcomply with TILA’s advertising rules and any other applicable advertisingrules.

• Monitor brokers and loan officers serving Hispanic communities.

• Develop relationships with Hispanic community organizations.

What Should I Do?

QUESTIONS

Mayer Brown is a global legal services provider comprising legal practices that are separate entities (the "Mayer Brown Practices"). The Mayer Brown Practices are: Mayer Brown LLP and Mayer Brown Europe–Brussels LLP, both limited liability partnerships established in Illinois USA;Mayer Brown International LLP, a limited liability partnership incorporated in England and Wales (authorized and regulated by the Solicitors Regulation Authority and registered in England and Wales number OC 303359); Mayer Brown, a SELAS established in France; Mayer BrownJSM, a Hong Kong partnership and its associated legal practices in Asia; and Tauil & Chequer Advogados, a Brazilian law partnership with which Mayer Brown is associated. Mayer Brown Consulting (Singapore) Pte. Ltd and its subsidiary, which are affiliated with Mayer Brown, providecustoms and trade advisory and consultancy services, not legal services. "Mayer Brown" and the Mayer Brown logo are the trademarks of the Mayer Brown Practices in their respective jurisdictions.