Embed Size (px)

Citation preview

1

©2010 Foley & Lardner LLP • Attorney Advertising • Prior results do not guarantee a similar outcome • Models used are not clients but may be representative of clients • 321 N. Clark Street, Suite 2800, Chicago, IL 60654 • 312.832.4500

Avoiding the Bureau’s Crosshairs: Understanding UDAAP and

Strategic Management of the RiskPresented by:

Michael C. LuederMartin J. Bishop

©2010 Foley & Lardner LLP

2

Today’s Presenters

Michael C. LuederMilwaukee

Martin J. BishopChicago

2

©2010 Foley & Lardner LLP

3

UDAAP = FAIRNESSAre Your Consumer Finance Products and Services Fair?

Equal Outcomes?Equitable Treatment?Comparable Opportunities?Absence of Predictive Bias?

©2010 Foley & Lardner LLP

4

UDAAPSection 1031 of the Dodd-Frank Act empowers the Bureau “to prevent a covered person or service provider from committing or engaging in an unfair, deceptive, or abusive act or

practice under Federal law in connection with any transaction with a consumer for a consumer financial

product or service, or the offering of a consumer financial product or service.”

UNFAIR

DECEPTIVE

ABUSIVE

3

©2010 Foley & Lardner LLP

5

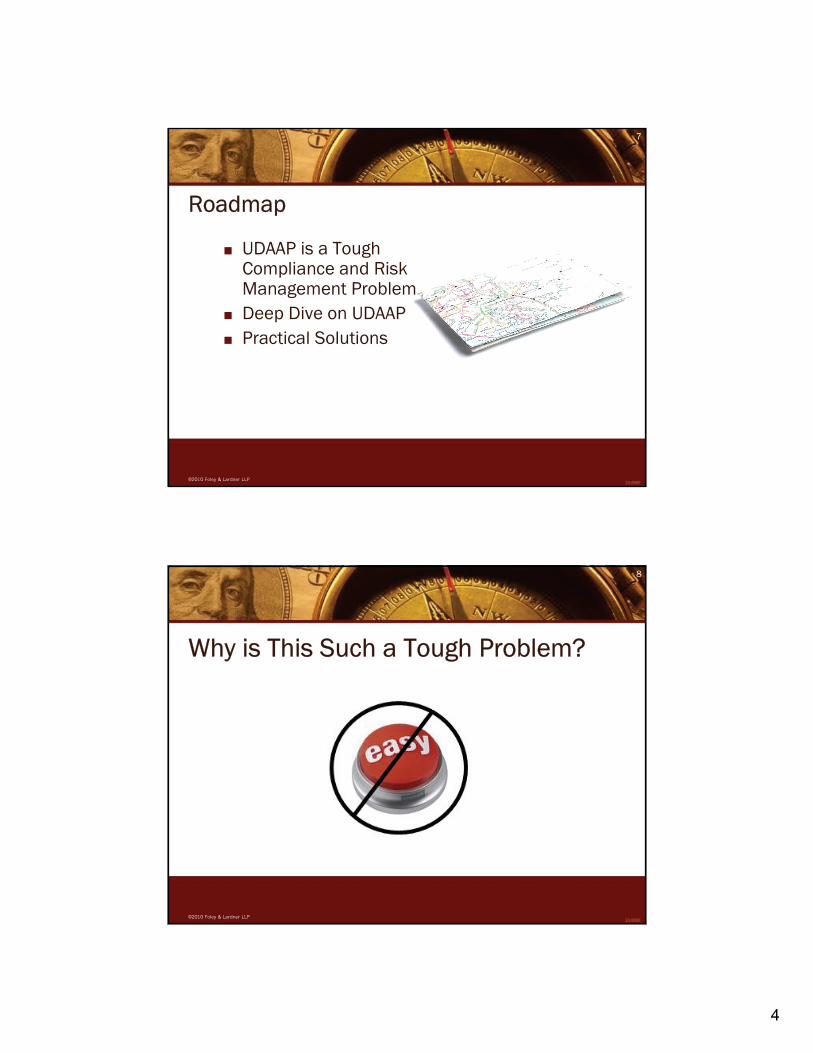

What is UDAAP?

UDAAP

UDAP

FEDERAL(Dodd-Frank, FTC Act, Reg. AA)

STATE(Mini-FTC Acts)

©2010 Foley & Lardner LLP

6

IF… THEN…

Abusive-Advantage outweighed by disadvantages-Increased risk of financial distress

Deceptive-Confusing-Leads to Misunderstandings-Leads to Mistakes in decision making

Unfair-Offensive to standards of fairness-High Costs

4

©2010 Foley & Lardner LLP

7

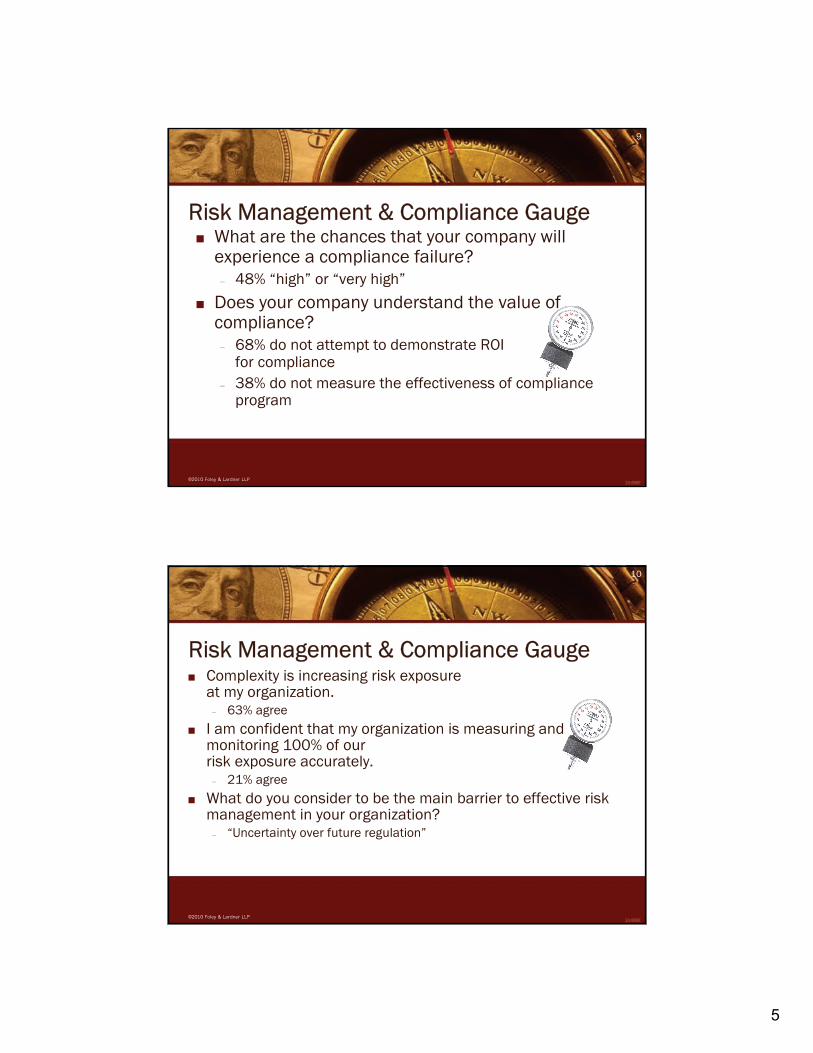

Roadmap

UDAAP is a Tough Compliance and Risk Management ProblemDeep Dive on UDAAPPractical Solutions

©2010 Foley & Lardner LLP

8

Why is This Such a Tough Problem?

5

©2010 Foley & Lardner LLP

9

Risk Management & Compliance GaugeWhat are the chances that your company will experience a compliance failure?– 48% “high” or “very high”

Does your company understand the value of compliance?– 68% do not attempt to demonstrate ROI

for compliance– 38% do not measure the effectiveness of compliance

program

©2010 Foley & Lardner LLP

10

Risk Management & Compliance GaugeComplexity is increasing risk exposure at my organization.– 63% agree

I am confident that my organization is measuring and monitoring 100% of our risk exposure accurately.– 21% agree

What do you consider to be the main barrier to effective risk management in your organization?– “Uncertainty over future regulation”

6

©2010 Foley & Lardner LLP

11

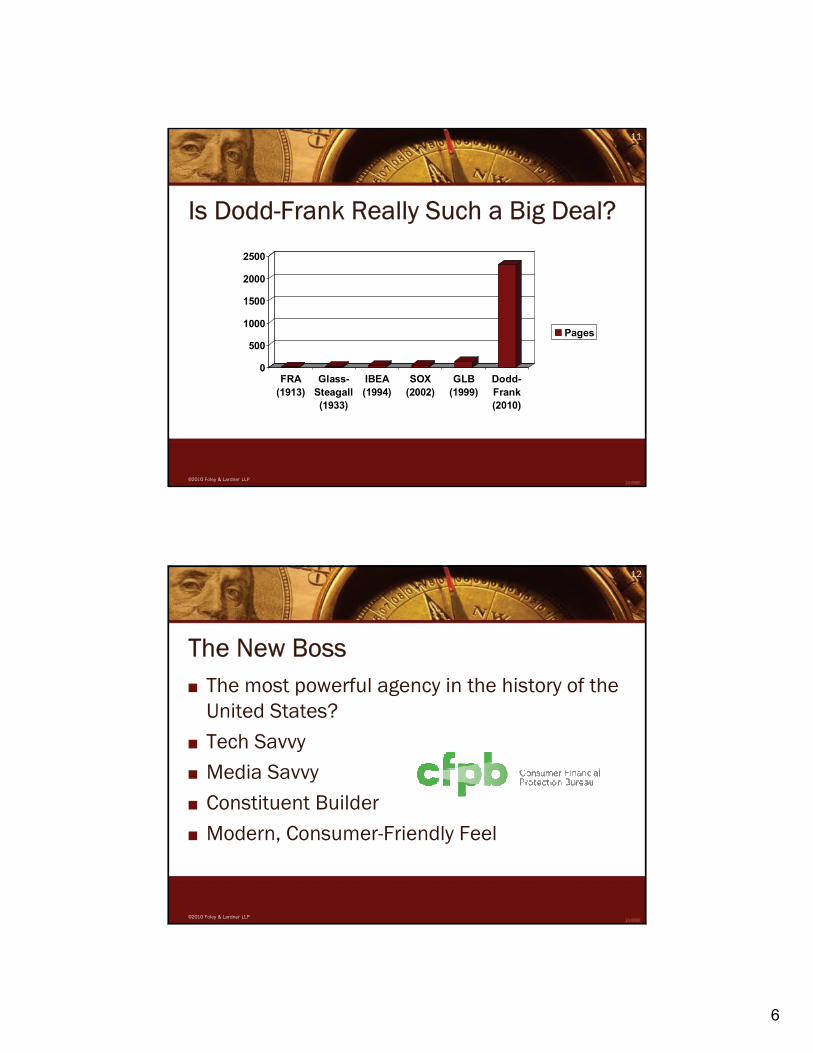

Is Dodd-Frank Really Such a Big Deal?

0

500

1000

1500

2000

2500

FRA(1913)

Glass-Steagall(1933)

IBEA(1994)

SOX(2002)

GLB(1999)

Dodd-Frank(2010)

Pages

©2010 Foley & Lardner LLP

12

The New BossThe most powerful agency in the history of the United States?Tech SavvyMedia SavvyConstituent BuilderModern, Consumer-Friendly Feel

7

©2010 Foley & Lardner LLP

13

Staying Power?The Next Election Will Lead to a Repeal of Dodd-Frank– Likely voters favor the 2010 Dodd-Frank Act by a 5 to 1

margin (71% vs. 14%).Congress Will Weaken the Leadership and Funding of the Bureau– Presented with information about

challenges in Congress to the law, 63% believe that policymakers should allow the law to be fully implemented.

©2010 Foley & Lardner LLP

14

Staying Power?Other More Experienced and Less Focused Regulators Will Have a More Prominent Role In Consumer Protection– Three-quarters (74%) of voters support the

existence of a single entity with the mission of protecting consumers from deceptive practices.

Source: Center For Responsible Lending, July 2011

8

©2010 Foley & Lardner LLP

15

Staying Power?More Bank Regulation is Disfavored?

Increased government regulation of banks and major financial institutions

DisapproveApprove

61% 37%

Source: USA Today/Gallup, Aug. 27-30, 2010

©2010 Foley & Lardner LLP

16

Deep Dive

9

©2010 Foley & Lardner LLP

17

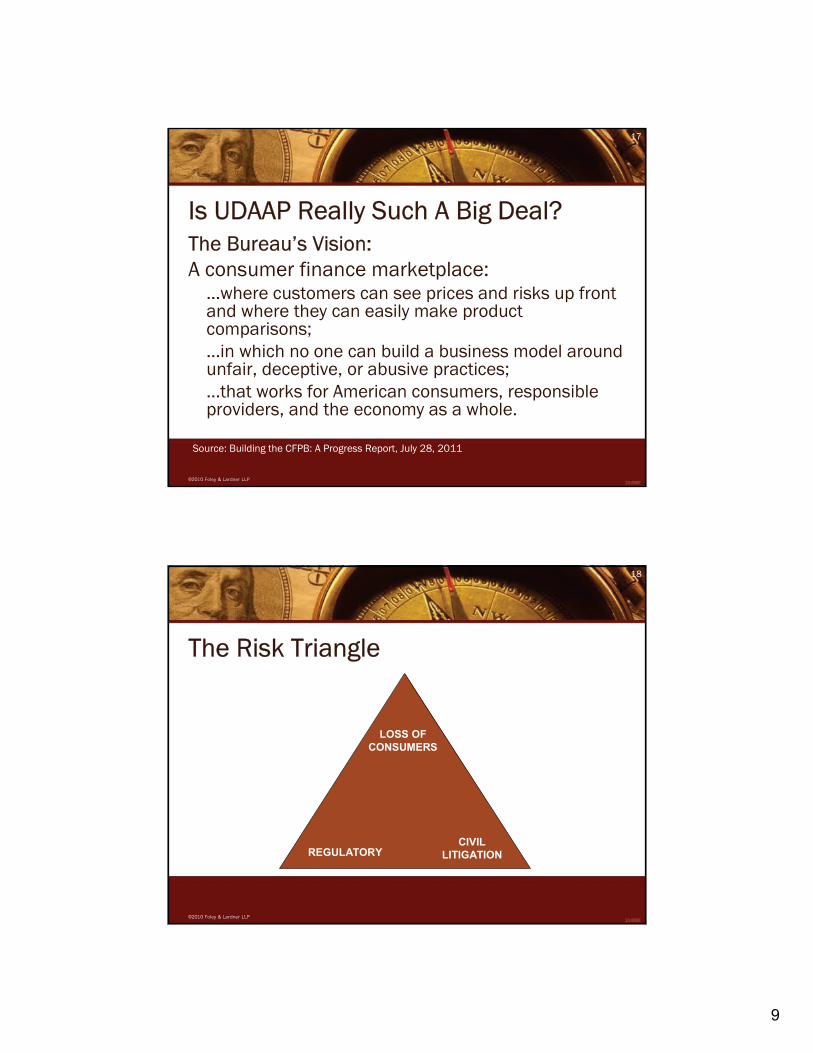

Is UDAAP Really Such A Big Deal?The Bureau’s Vision:A consumer finance marketplace:

…where customers can see prices and risks up front and where they can easily make product comparisons;…in which no one can build a business model around unfair, deceptive, or abusive practices;…that works for American consumers, responsible providers, and the economy as a whole.

Source: Building the CFPB: A Progress Report, July 28, 2011

©2010 Foley & Lardner LLP

18

The Risk Triangle

REGULATORYCIVIL

LITIGATION

LOSS OF CONSUMERS

10

©2010 Foley & Lardner LLP

19

Regulatory RisksInvestigation and DiscoveryAdministrative Hearings and Court LitigationRelief:– Rescission; Reformation; Refunds;

Restitution; Disgorgement; Damages; – Payment of Government Incurred Costs

Monetary Penalties– Violation (up to $5,000/day)– Reckless Violation (up to $25,000/day)– Knowing Violation (up to $1,000,000/day)

©2010 Foley & Lardner LLP

20

UnfairThe act or practice causes, or is likely to cause, substantial injury to consumers which is not reasonably avoidable by consumers; andSuch substantial injury is not outweighed by countervailing benefits to consumers or to competition.

11

©2010 Foley & Lardner LLP

21

UnfairTaking Advantage“There is no limit to human inventiveness in this field.”“Substantial Inquiry:”– Small Harm to Many Consumers– Significant Risk of Concrete Harm

“Reasonably Avoidable”– Lack of Free and Informed Choice

©2010 Foley & Lardner LLP

22

Unfair

Case Study:Federal Trade Commission v. Neovi, Inc., et al. (“Qchex”)

12

©2010 Foley & Lardner LLP

23

UnfairWhat does the Bureau consider to be unfair?– Refusing to release a lien after a consumer makes

the final payment on a mortgage.– Dishonoring credit card convenience checks

without notice.– Processing payments for companies engaged in

fraudulent activities.

©2010 Foley & Lardner LLP

24

DeceptiveFTC: Material representation, omission or practice that, from the perspective of a consumer acting reasonably under the circumstances, is likely to mislead the consumer.

13

©2010 Foley & Lardner LLP

25

DeceptiveFraud, but less stringent.Actual deception not required.Misleading a consumer by words, silence, or action.Good faith is not a defense.

©2010 Foley & Lardner LLP

26

Case Study:Richard Cordray v. Mortgage Servicers

14

©2010 Foley & Lardner LLP

27

DeceptiveWhat Does the Bureau Consider to be Deceptive?– Failing the FTC’s 4 “P”s Test (Prominence,

Presentation, Placement, Proximity).– Inadequate disclosure of adequate lease terms in

television advertising.– Misrepresentation about loan terms.

©2010 Foley & Lardner LLP

28

AbusiveMaterial interference with the ability of a consumer to understand a term or condition of a consumer financial product or service; orTaking unreasonable advantage of --– A lack of understanding on the part of the consumer of the

material risks, costs, or conditions of the product or service;– The inability of the consumer to protect the interests of the

consumer in selecting or using a consumer financial product or service; or

– The reasonable reliance by the consumer on a covered person to act in the interests of the consumer.

15

©2010 Foley & Lardner LLP

29

AbusiveThe most-feared word in all of Dodd-Frank:– Unconscionability?– Suitability?– Age-Specific Products?– Financial Illiteracy?

©2010 Foley & Lardner LLP

30

AbusiveWhat does the Bureau Consider to be Abusive?– “Although abusive acts also may be unfair or

deceptive, examiners should be aware that the legal standards for abusive, unfair, and deceptive each are separate.”

16

©2010 Foley & Lardner LLP

31

Focus on Compliance RisksNature and Structure of ProductsConsumers to whom products are marketedIncentives and CompensationMarketing and AdvertisingCustomer RelationsCompliance ManagementBoard of Directors/ManagementAuthority and AccountabilityProduct Development and ModificationTrainingComplaint Management

©2010 Foley & Lardner LLP

32

Solutions!

17

©2010 Foley & Lardner LLP

33

Solutions to Manage the RiskBring Compliance and Legal into the RoomIncentivize Compliance and Ethical ConductFacilitate Informed Choice SuitabilityBe ProactiveFocus on Consumer Complaints

©2010 Foley & Lardner LLP

34

Solutions to Manage the RiskUDAAP Audit TrainingMonitoringPartner With Vendors Who Will Put “Skin in the Game”Analyze Revenue From Consumer Finance TransactionsStatement on Prohibition of Unfair, Deceptive, and Abusive Practices

18

©2010 Foley & Lardner LLP

35

Thank YouMartin J. BishopPartner, Vice Chair, Consumer Financial Services Practice, Foley & Lardner LLP321 North Clark Street, Suite 2800Chicago, IL 60654-5313Phone: 312-832-4500(312) [email protected]

Michael C. LuederPartner, Chair, Consumer Financial Services Practice, Foley & Lardner LLP777 E Wisconsin AvenueMilwaukee, WI 53202-5306(414) 297-5643 [email protected]