Embed Size (px)

Citation preview

Advertising: Avoiding FairLending and UDAAP Pitfalls

Michelle AndersonSenior Manager

Ernst & [email protected]

Anjali GargAssociate

Mayer [email protected]

2

Speakers

Michelle AndersonSenior ManagerErnst & [email protected]

Anjali GargAssociateMayer [email protected]

3

• Advertisements are at the intersection of a number ofregulator concerns, including fair lending and theprohibition on unfair, deceptive, or abusive acts orpractices (“UDAAP”).

• As compliance professionals, you are at the vortex of themillion dollar question: is it possible to create acompliant, yet effective, advertisement?

• Recent enforcement actions demonstrate that institutionscannot rely on compliant disclosures to prevent UDAAP orfair lending risks associated with advertisements.

Introduction

4

What is an Advertisement?

• Print media

• Radio

• Television

• Brochures

• Direct mail

• Internet (websites, bannerads)

• Google Adwords

• Telemarketing scripts

• Any other consumer-facingsolicitations

5

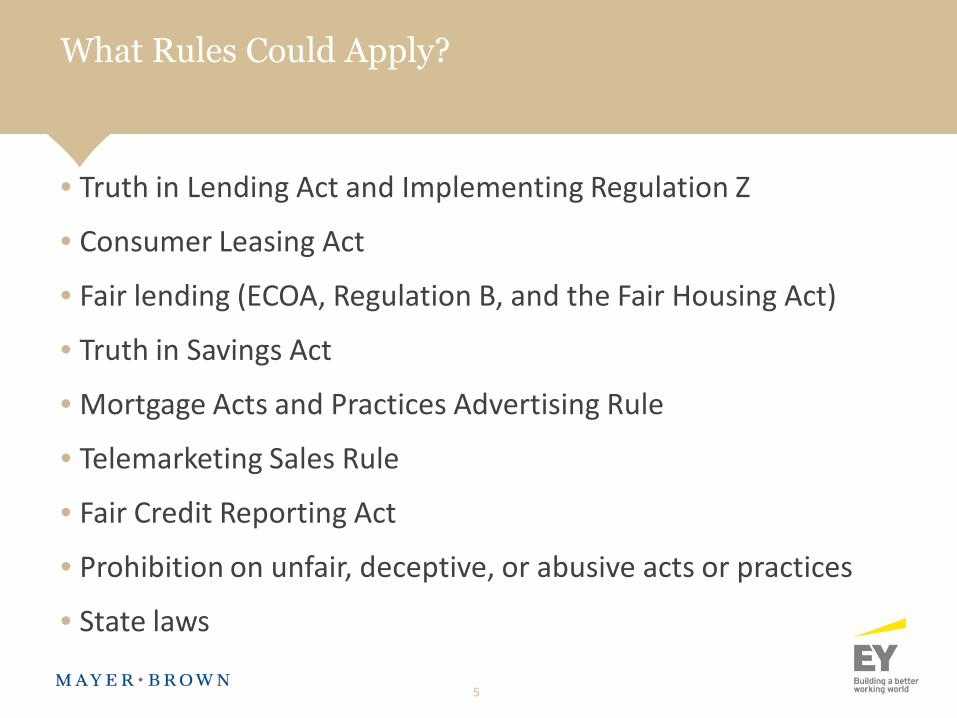

• Truth in Lending Act and Implementing Regulation Z

• Consumer Leasing Act

• Fair lending (ECOA, Regulation B, and the Fair Housing Act)

• Truth in Savings Act

• Mortgage Acts and Practices Advertising Rule

• Telemarketing Sales Rule

• Fair Credit Reporting Act

• Prohibition on unfair, deceptive, or abusive acts or practices

• State laws

What Rules Could Apply?

FAIR LENDING ANDADVERTISING

7

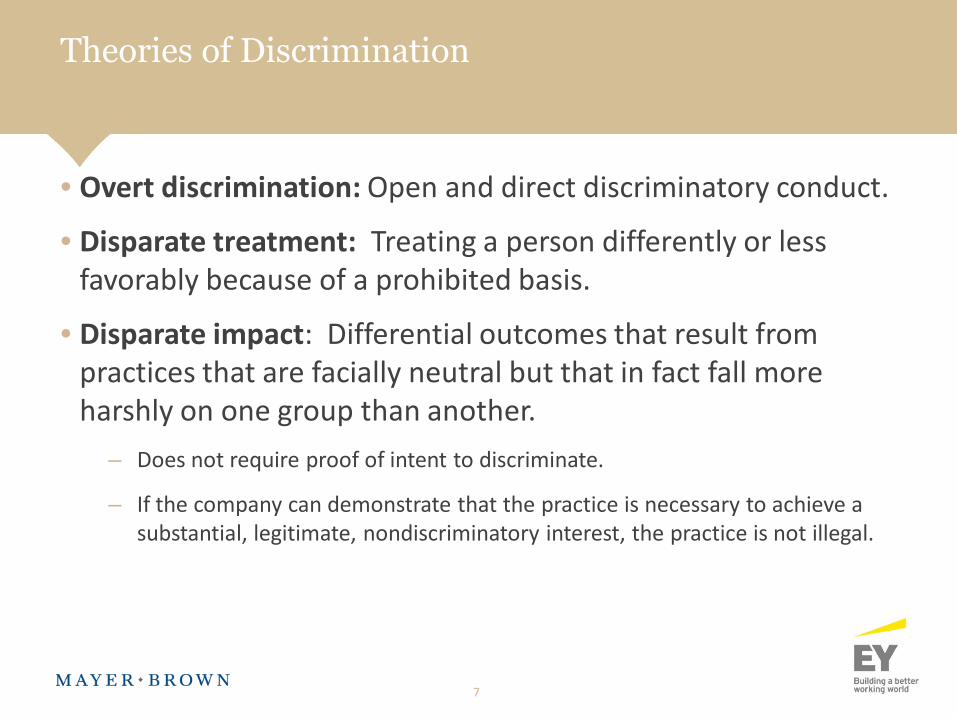

• Overt discrimination: Open and direct discriminatory conduct.

• Disparate treatment: Treating a person differently or lessfavorably because of a prohibited basis.

• Disparate impact: Differential outcomes that result frompractices that are facially neutral but that in fact fall moreharshly on one group than another.

– Does not require proof of intent to discriminate.

– If the company can demonstrate that the practice is necessary to achieve asubstantial, legitimate, nondiscriminatory interest, the practice is not illegal.

Theories of Discrimination

8

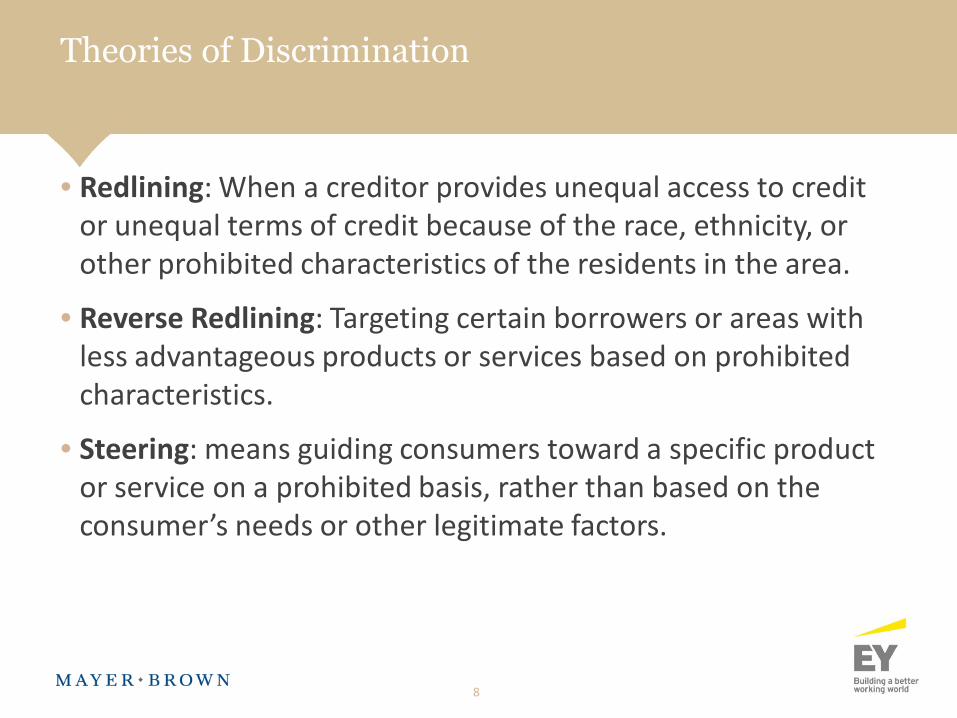

• Redlining: When a creditor provides unequal access to creditor unequal terms of credit because of the race, ethnicity, orother prohibited characteristics of the residents in the area.

• Reverse Redlining: Targeting certain borrowers or areas withless advantageous products or services based on prohibitedcharacteristics.

• Steering: means guiding consumers toward a specific productor service on a prohibited basis, rather than based on theconsumer’s needs or other legitimate factors.

Theories of Discrimination

9

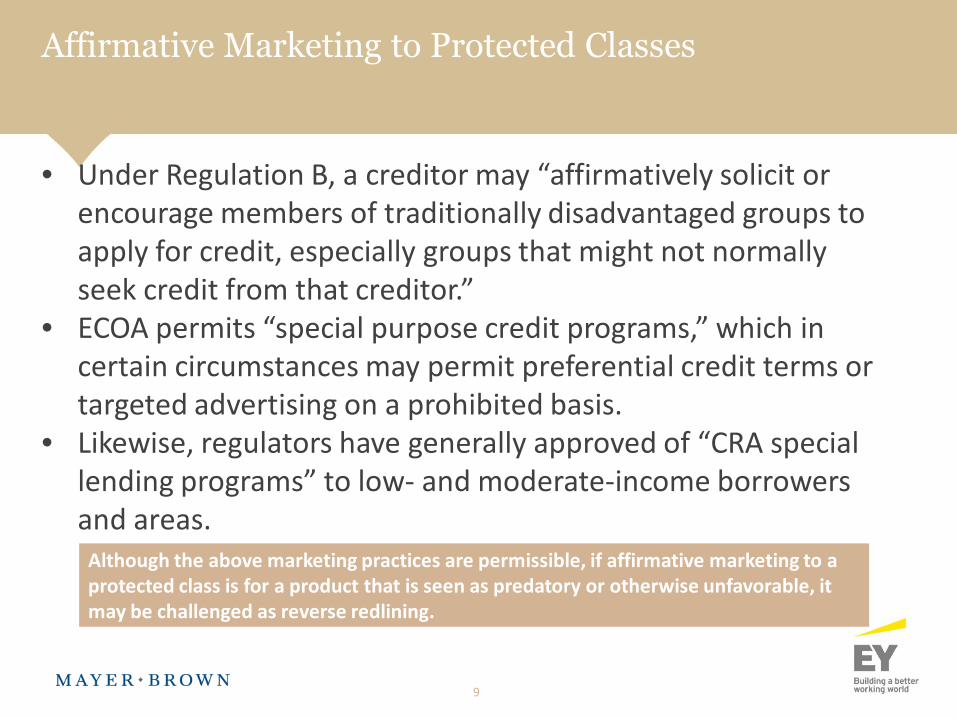

• Under Regulation B, a creditor may “affirmatively solicit orencourage members of traditionally disadvantaged groups toapply for credit, especially groups that might not normallyseek credit from that creditor.”

• ECOA permits “special purpose credit programs,” which incertain circumstances may permit preferential credit terms ortargeted advertising on a prohibited basis.

• Likewise, regulators have generally approved of “CRA speciallending programs” to low- and moderate-income borrowersand areas.

Affirmative Marketing to Protected Classes

Although the above marketing practices are permissible, if affirmative marketing to aprotected class is for a product that is seen as predatory or otherwise unfavorable, itmay be challenged as reverse redlining.

10

• Third party marketing companies can mine vast amounts of data fromsocial media about individuals that could potentially be used for marketingpurposes, including credit history of an individual’s online “friends,” one’srelationship status, online purchases, and organizations that an individual“likes.”

• Use of this information could present disparate treatment or disparateimpact risks.

• “Digital divide” issues.

• Advertising or offering special products or discounts through social media,mobile, or other online channels could present fair lending issues inasmuchas groups have different levels or types of online or mobile access.

Social Media

UDAAP AND ADVERTISING

12

• An otherwise compliant disclosure does not eliminate UDAAPrisk.

– Written disclosures may be insufficient to correct a misleadingstatement or representation, particularly where the consumer isdirected away from qualifying limitations in the text or is counseledthat reading the disclosures is unnecessary.

– Likewise, oral disclosures or fine print are generally insufficient tocure a misleading headline or prominent written representation.

– A deceptive act or practice cannot be cured by subsequent truthfuldisclosures.

• Target markets and distribution practices can also createUDAAP and fair lending risks.

It’s Not Just About the Disclosures

13

• A practice is deceptive if:

– A representation, omission, act, or practice misleads or is likelyto mislead the consumer.

– A consumer’s interpretation of the representation, omission,act, or practice is reasonable under the circumstances.

– The misleading representation, omission, act, or practice ismaterial.

Deception

14

• Is the statement prominent enough for the consumer tonotice?

• Is the information presented in an easy-to-understandformat that does not contradict other informationprovided and is presented at a time when the consumer’sattention is not distracted elsewhere?

• Is the placement of the information in a location whereconsumers can be expected to look or hear?

• Is the information in close proximity to the claim itqualifies?

Likely to Mislead

15

• Regulators consider a misrepresentation, omission, orpractice “material” if it is likely to affect a consumer’schoice of or conduct regarding a product.

• Certain items are presumed material, such as the price orcost of a product or service.

Materiality

BEST PRACTICES

17

• Consider whether the target audience creates fair lendingor UDAAP risks.

– Are only certain existing customers being targeted for theadvertisement based on a prohibited characteristic?

– Are the advertisements only being distributed in certain mediamarkets based on a prohibited characteristic (e.g., television orradio ads)?

– Are the advertisements steering consumers toward lessfavorable products or services?

Step Away from the Ad: Target Audience

18

• Does the advertisement create confusion about theproduct or service being offered?

• Tell it like it is: If it is a lease, call it a lease. If it is a loan,call it a loan.

• Don’t forget the net impression.

• Recent example:

– The CFPB filed a complaint in August 2015 against a companythat advertised what the CFPB considers to be a loan product asa “pension buyout” and “pension advance” and actively deniedthat the product was a loan.

Explain the Product

19

• All media:

– Font size and color matter.

– Evaluate how effective the ad directs the consumers to thedisclosures.

– Beware of the block of text.

• TV: consider how long the disclosures appear on thescreen.

• Radio and TV: listen for the cadence and speed of oraldisclosures.

• Don’t forget the net impression.

Clearly and Conspicuously Disclose Terms andConditions

20

• Ensure that the advertised features and terms aregenerally available to consumers.

– Would most consumers be ineligible for the advertised terms?

• Consider whether the advertised claims are substantiated.

• Avoid:

– Creating a false sense of urgency

– Displaying results that are not typical

– Advertising false promotions

• Don’t forget the net impression.

Honor the Advertisements

21

• Fair lending considerations:

– Do not use words, symbols, models, or other forms ofcommunication in advertising that express, imply, or suggest adiscriminatory preference or a policy of exclusion.

– Evaluate the diversity of your stock photos.

• UDAAP considerations:

– Avoid images that imply affiliation with or endorsement by thegovernment, unions, universities, celebrities, etc.

– Be careful with creative formatting that could confuse aconsumer into thinking your advertisement is not anadvertisement.

Be Careful with Images

22

• Many elements of the “net impression” may beoutsourced by your institution:

– Telemarketing

– Inbound call handling

– Development of creative content

• Failed oversight or inadequate training and monitoringcreate additional risks.

• Consider including call monitoring, training, mysteryshopping, and reviews of consumer-facing materials aspart of your vendor management oversight program.

Don’t Forget the Vendors

23

• Claims matter: Evaluate the net consumer experiencefrom the point of solicitation to the point of sale, andeverything in between.

• Images matter: Consider the diversity of the images andwhether the images imply an inaccurate term, feature, orendorsement.

• Omissions matter: If the absence of certain informationwould impact the effectiveness of the ad, then themissing information is probably material.

Bottom Line: Net Impression

COMPLIANCE MANAGEMENTFOR ADVERTISING

25

• The CFPB filed a consent order against an online payment platform,claiming the company misled customers related to the security of itsonline payment system and security practices. No actual breach ofcustomer data was reported, rather the CFPB’s complaint wasagainst the company’s deceptive marketing.

• The following claims were made by the online payment platform:

– Respondent represented to consumers that its network andtransactions were “safe” and “secure.”

– Product claimed to “empower anyone with an internetconnection to safely send money to friends or businesses.”

– Safer [than credit cards] and less of a liability for bothconsumers and merchants.”

Case Study–Dwolla

26

• The consent order is the CFPB’s first data security penalty. Specifically, theCFPB stated the following:

– “From its launch until at least September 2012, respondent did notadopt or implement reasonable and appropriate data-security policiesand procedures.”

– “From its launch until at least October 2013, respondent did notadopt or implement a written data-security plan to govern thecollection, maintenance, or storage of consumers’ personalinformation”

– “Until at least December 2012, respondent’s employees received littleto no data security training on their responsibilities for handling andprotecting the security of consumers’ personal information.”

Enforcement Actions

27

• Under the consent order, the following enforcement actions weretaken against the company:

– Refrain from misleading consumers on in its data securitypractices

– Provide training for employees on data security practices and fixany security issues

– Pay civil money penalties of $100,000 to the CFPB

• Customers made decisions to select the online payment providerbased on claims made on its website.

• Conducting testing to ensure marketed claims are well supported inan institution’s control environment is critical.

Key Impacts

28

• Significant reliance and lack of oversight of vendors forcreative development and marketing execution

• Lack of end-to-end review of marketing materials toassess overall “net impression”

• Use of trigger words (e.g. fixed, guaranteed, savings, “pre-approved”, and “lifetime rates”, “free trial period offers”,“up to” and “free”)

Fair Lending and UDAAP Common MarketingProgram Pitfalls

29

• Increasing use of digital marketing without appropriatecontrols

• Lack of end-to-end testing to determine if benefitsmarketed/offered can be supported by Operations

• Placement of images

• Language preference considerations

Fair Lending and UDAAP Common MarketingProgram Pitfalls

30

• A strong risk assessment process focused on an institution’smarketing practices is a critical element of understandingexisting risks.

• In assessing the inherent risk faced by an organization, it isimportant to consider:

– The use of geography in marketing campaigns

– Use of third parties

– Factors used in marketing models

– Customer segmentation

– Channel differences

– Use of foreign language in marketing activities

Managing Risk in Marketing Programs

31

• Depending on the level and nature of the inherent risk, fairlending controls should include:

– Involvement of fair lending, UDAAP compliance along with Legal andbusinesses throughout marketing life cycle (e.g., new productconsiderations, review of campaigns and marketing collateral)

– Disparate impact analyses

– Redlining analyses

– Consideration of impact of language preference

– Review of key risk indicators (e.g., early cancellation levels, complaintsvolume)

– Evaluation of third party fair lending programs

Managing Risk in Marketing Programs

QUESTIONS

Mayer Brown is a global legal services provider comprising legal practices that are separate entities (the "Mayer Brown Practices"). The Mayer Brown Practices are: Mayer Brown LLP and Mayer Brown Europe–Brussels LLP, both limited liability partnerships established in Illinois USA;Mayer Brown International LLP, a limited liability partnership incorporated in England and Wales (authorized and regulated by the Solicitors Regulation Authority and registered in England and Wales number OC 303359); Mayer Brown, a SELAS established in France; Mayer BrownJSM, a Hong Kong partnership and its associated legal practices in Asia; and Tauil & Chequer Advogados, a Brazilian law partnership with which Mayer Brown is associated. Mayer Brown Consulting (Singapore) Pte. Ltd and its subsidiary, which are affiliated with Mayer Brown, providecustoms and trade advisory and consultancy services, not legal services. "Mayer Brown" and the Mayer Brown logo are the trademarks of the Mayer Brown Practices in their respective jurisdictions.