Embed Size (px)

Citation preview

Compliance Overview:

UDAAP

Complimentar

y

Preview

Compliance Overview: Unfair, Deceptive Page | 1 © 2014 insideARM.com and Abusive Acts or Practices

Copyright © 2014 insideARM.com. All rights reserved.

NOTICE:

This is not a free whitepaper. This report is offered for sale by insideARM.com. Purchase of this report

entitles the buyer to share this information only among his or her immediate team.

Site licenses or multiple copy discounts are available.

insideARM.com

Phone: 240.499.3834

E-mail: [email protected] | Website: www.insideARM.com

Complimentar

y

Preview

Compliance Overview: Unfair, Deceptive Page | 2 © 2014 insideARM.com and Abusive Acts or Practices

Legal Disclaimer

This information contained in this report is not intended to be legal advice and may not be used as legal

advice. Legal advice must be tailored to the specific circumstances of each case. Every effort has been

made to assure this information is up-to-date. It is not intended to be a full and exhaustive explanation

of the law in any area, however, nor should it be used to replace the advice of your own legal counsel.

Complimentar

y

Preview

Compliance Overview: Unfair, Deceptive Page | 3 © 2014 insideARM.com and Abusive Acts or Practices

Table of Contents

What is UDAAP? ............................................................................................................................................ 4

Common Terms and Acronyms ..................................................................................................................... 4

Who is Affected? ........................................................................................................................................... 4

Compliance ................................................................................................................................................... 5

Top 10 Compliance Tips ............................................................................................................................ 6

Vendor Management ................................................................................................................................ 7

Call Monitoring ......................................................................................................................................... 8

Internal Audits........................................................................................................................................... 9

Spotlight on: Banking Compliance ............................................................................................................ 9

Examples ..................................................................................................................................................... 11

Violations .................................................................................................................................................... 12

Timeline: High-Profile UDAAP Violations ................................................................................................ 12

Examinations ............................................................................................................................................... 13

Module 1: Entity Business Model ........................................................................................................... 14

Module 2: Communications in Connection with Debt Collection .......................................................... 15

Sample Checklists .................................................................................................................................... 16

CFPB Rules ................................................................................................................................................... 18

Appendix: Rules and Regulations ................................................................................................................ 20

Complimentar

y

Preview

Compliance Overview: Unfair, Deceptive Page | 4 © 2014 insideARM.com and Abusive Acts or Practices

What is UDAAP?

UDAAP stands for Unfair, Deceptive and Abusive Acts or Practices taking place in the debt collection

industry, or any other financial institution. It originates from Section 5 of the Federal Trade Commission

Act.

At first, the FTC Act only outlined UDAP: Unfair or Deceptive Acts or Practices. But the Dodd–Frank Wall

Street Reform and Consumer Protection Act – signed into law on July 21, 2010 – added “abusive” to the

alphabet soup. It also gave the newly-formed Consumer Financial Protection Bureau a directive to

supervise financial institutions and prevent UDAAP through rule-making, examination and enforcement.

The FDCPA, enacted in 1977, was a targeted call for the debt collection industry to treat consumers

honestly, fairly and with respect; in many ways, UDAAP is a broader version of the Fair Debt Collection

Practices Act. But being up-to-date on just FDCPA compliance is no longer enough; because of UDAAP,

collectors now have to actively prove that their practices don’t harm consumers.

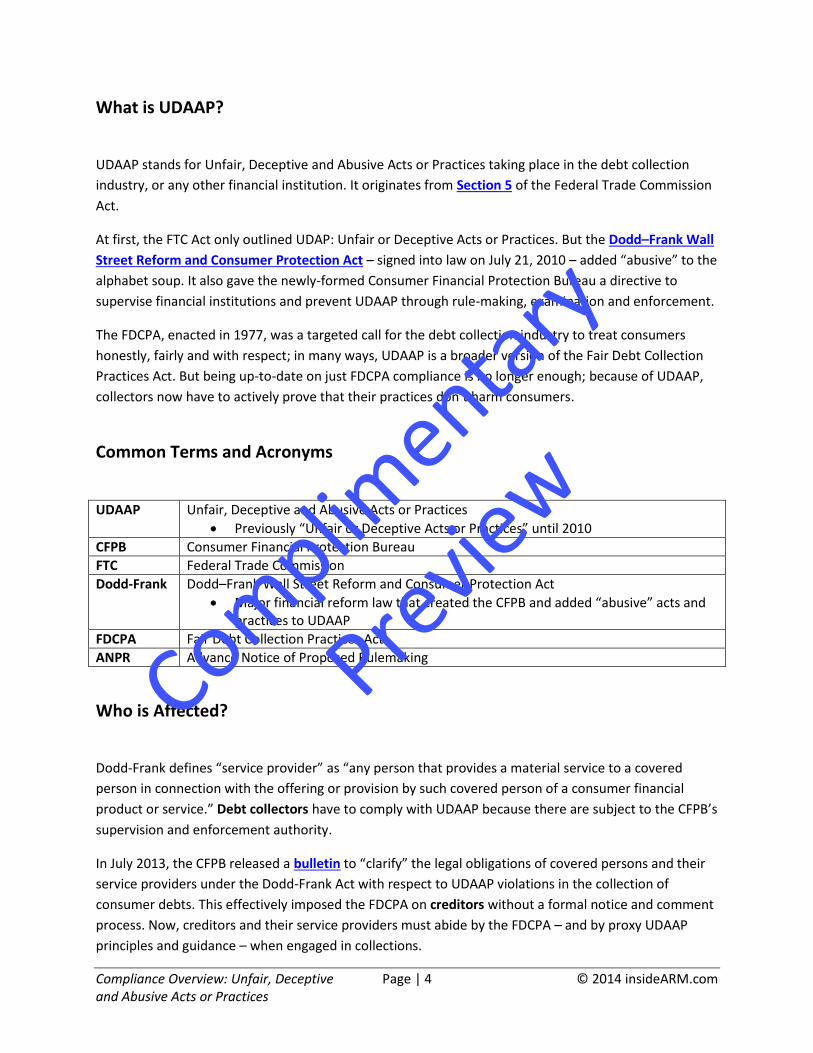

Common Terms and Acronyms

UDAAP Unfair, Deceptive and Abusive Acts or Practices

Previously “Unfair or Deceptive Acts or Practices” until 2010

CFPB Consumer Financial Protection Bureau

FTC Federal Trade Commission

Dodd-Frank Dodd–Frank Wall Street Reform and Consumer Protection Act

Major financial reform law that created the CFPB and added “abusive” acts and practices to UDAAP

FDCPA Fair Debt Collection Practices Act

ANPR Advance Notice of Proposed Rulemaking

Who is Affected?

Dodd-Frank defines “service provider” as “any person that provides a material service to a covered

person in connection with the offering or provision by such covered person of a consumer financial

product or service.” Debt collectors have to comply with UDAAP because there are subject to the CFPB’s

supervision and enforcement authority.

In July 2013, the CFPB released a bulletin to “clarify” the legal obligations of covered persons and their

service providers under the Dodd-Frank Act with respect to UDAAP violations in the collection of

consumer debts. This effectively imposed the FDCPA on creditors without a formal notice and comment

process. Now, creditors and their service providers must abide by the FDCPA – and by proxy UDAAP

principles and guidance – when engaged in collections.

Complimentar

y

Preview

Compliance Overview: Unfair, Deceptive Page | 5 © 2014 insideARM.com and Abusive Acts or Practices

Compliance

Any consumer product or service has the potential of being criticized for possible UDAAP violations.

UDAAP is a principle-based tool the CFPB uses on a case-by-case basis; the definitions of unfair,

deceptive and abusive acts and practices focus primarily on what a debt collector can’t do, putting the

onus for compliance on the collection agency itself.

Some acts and practices currently receiving a lot of attention in the debt collection industry are:

Check/debit processing orders

Loan payment processing

Debt settlement services

Industry experts agree that collection agencies must be proactive in their UDAAP compliance, instead of

simply waiting until they get a notice of a CFPB investigation.

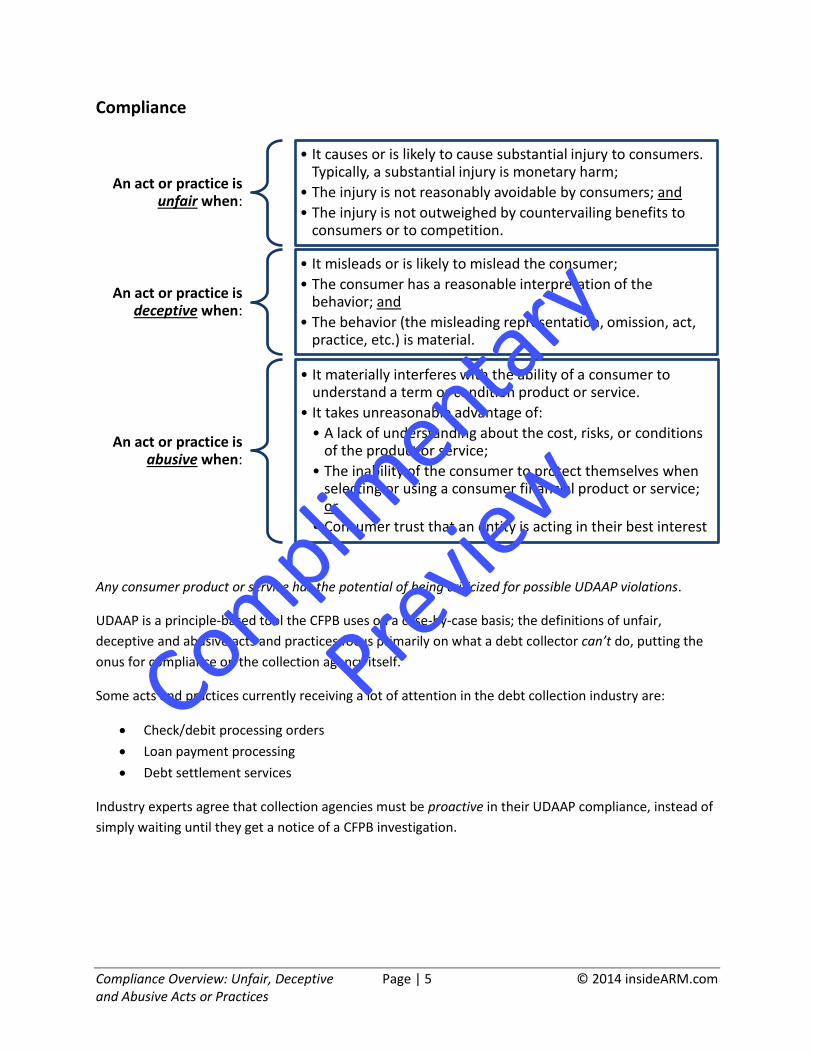

An act or practice is unfair when:

• It causes or is likely to cause substantial injury to consumers. Typically, a substantial injury is monetary harm;

• The injury is not reasonably avoidable by consumers; and

• The injury is not outweighed by countervailing benefits to consumers or to competition.

An act or practice is deceptive when:

• It misleads or is likely to mislead the consumer;

• The consumer has a reasonable interpretation of the behavior; and

• The behavior (the misleading representation, omission, act, practice, etc.) is material.

An act or practice is abusive when:

• It materially interferes with the ability of a consumer to understand a term or condition product or service.

• It takes unreasonable advantage of:

• A lack of understanding about the cost, risks, or conditions of the product or service;

• The inability of the consumer to protect themselves when selecting or using a consumer financial product or service; or

• Consumer trust that an entity is acting in their best interest

Complimentar

y

Preview