Embed Size (px)

Citation preview

The author is grateful for comments on earlier drafts of this paper from Piman Limpaphayom, Roy Kouwenberg, and Steen Thomsen. All remaining errors are my own.

Investment Policy at Family Firms: Evidence from Thailand J. Thomas Connelly Faculty of Commerce and Accountancy, Chulalongkorn University

[This version: 15 Jan 2014]

Abstract Using a unique, multi-year sample of publicly traded non-financial firms in Thailand, this study finds that firms’ ownership characteristics influence the level of investment. The results are from an emerging market, which features concentrated, family-dominated corporate ownership structures, including ownership pyramids. Firms with high family ownership have higher investment ratios and exhibit greater sensitivity to financial slack than low family ownership firms. However, with the use of a lower threshold to designate family ownership, the investment ratios and sensitivity to financial slack are not statistically different between firms with high or low family ownership. Both high and low family ownership firms exhibit higher investment ratios when facing growth opportunities. The investment ratios for both types of firms are more sensitive to growth opportunities than cash flow, in contrast with earlier findings for developed markets. Keywords: Family ownership; Investment-cash flow sensitivity; Capital investment; Financing constraints; Pyramids; Thailand JEL Classification: G31, G32 Corresponding Author: J. T. Connelly, Department of Banking and Finance, Faculty of Commerce and Accountancy, Chulalongkorn University, Phayathai Road, Bangkok 10330, Thailand. Telephone: +66-2-218-5674. Facsimile: +66-2-218-5676. E-mail: [email protected].

Investment Policy at Family Firms: Evidence from Thailand

Abstract Using a unique, multi-year sample of publicly traded non-financial firms in Thailand, this study finds that firms’ ownership characteristics influence the level of investment. The results are from an emerging market, which features concentrated, family-dominated corporate ownership structures, including ownership pyramids. Firms with high family ownership have higher investment ratios and exhibit greater sensitivity to financial slack than low family ownership firms. However, with the use of a lower threshold to designate family ownership, the investment ratios and sensitivity to financial slack are not statistically different between firms with high or low family ownership. Both high and low family ownership firms exhibit higher investment ratios when facing growth opportunities. The investment ratios for both types of firms are more sensitive to growth opportunities than cash flow, in contrast with earlier findings for developed markets. Keywords: Family ownership; Investment-cash flow sensitivity; Capital investment; Financing constraints; Pyramids; Thailand JEL Classification: G31, G32

1

Investment Policy at Family Firms: Evidence from Thailand 1. Introduction

A firm’s ownership characteristics can have a significant effect on the company’s

investment policy. Myers and Majulf (1984) articulate the ways that information

asymmetries can affect investment policy. For example, their model shows instances when

managers may make sub-optimal decisions and underinvest, forgoing value-creating projects.

The model also explains why financial slack may be valuable because financial slack will

give managers the flexibility to undertake investments without issuing new shares to secure

funds.

The effect of a firm’s ownership characteristics on its investment policy may be

accentuated for firms in an emerging market such as Thailand. Thai firms, like companies in

most emerging markets, have concentrated ownership structures that are quite often

dominated by families. At high levels of family ownership, the degree of information

asymmetry between the large family shareholders and the smaller outside shareholders can be

quite substantial. However, the high level of family ownership may also temper the effects of

the information disparity. Certainly the family owners –who are often the managers as well –

are in a position to know more about the investment opportunities facing the firm. Yet the

family owners would have an incentive to pursue an optimal investment policy. Should the

managers choose to over- or underinvest, their wealth as shareholders would be directly

affected. The effect on wealth could be large, as their ownership stake is large. The net

effect would be a reduction in the consequences of information symmetries, leading to pursuit

of an optimal investment policy.

2

At firms with lower levels of family ownership, information asymmetries between the

family owner-managers and minority shareholders could still be significant. Though their

ownership stake is smaller, the managers at these firms still control the investment decision.

At lower levels of family ownership, the owner-managers may be more prone to deviate from

an optimal investment policy in order to enjoy other benefits of control. The family

shareholders may be more likely to use their position to expropriate the minority

shareholders. This risk of expropriation would be most acute at firms which employ control-

enhancing structures like pyramidal ownership. In these instances, the net effect would be an

increase in the consequences of information asymmetries, leading to overinvestment.

This paper makes several contributions to the literature. Few studies have examined

the extent to which ownership characteristics affect firms’ investment policies, especially in

emerging markets. Next, I use a unique time series dataset of firm ownership patterns after

the 1997 Asian financial crisis. I also examine the effects that growth opportunities and

financial constraints have on the investment decision for firms with high levels and with low

levels of family ownership.

I find firms with high family ownership show higher levels of investment than low

family ownership firms. However, this distinction depends on the level of family ownership

and the absence of a control-enhancing (pyramidal) ownership structure. These results imply

family firms follow an investment policy more close to optimal when their ownership stake is

high. Firms with growth opportunities have higher investment ratios, no matter if the level of

family ownership is high or low. I find a weak positive association between financial slack

and the investment ratio. However, this association does not hold for lower levels of family

ownership or firms with a control-enhancing pyramidal ownership structure.

3

2. Motivation and Theory

Myers and Majulf (1984) create a model connecting the investment decision and the

financing decision, specifically when a firm is contemplating issuing new equity to fund a

new investment opportunity. The model makes two important assumptions. First, managers

have information that other investors do not have. A second vital assumption is that

managers act in the interest of the old stockholders, the existing owners of the firm, who own

shares before a new project is undertaken and before the firm finances the new project with

additional equity. Based on these two assumptions, Myers and Majulf (1984) show instances

where managers may make a sub-optimal decision and decide not to invest in a value-

creating project. The authors make an example of an investment in a positive NPV project.

The project lowers the value of the shares held by the old shareholders, since the old

shareholders do not capture the increase in value created by the new, positive NPV project.

The gains go to the new shareholders. Thus, the old shareholders would not want the firm to

undertake the investment if the investment requires the issuance of new shares to new

stockholders. The model also explains why firms prefer to have financial slack (cash,

marketable securities, or unused borrowing capacity). Slack is valuable, as it permits firms to

take investment opportunities without issuing shares.

Myers and Majulf (1984) note two instances where slack would not be valuable. The

first instance occurs if a firm were able to communicate privately and preferentially to the old

shareholders rather than the new shareholders.1 Another instance would be if the old

shareholders would agree to purchase, and then hold, the newly issued shares, eliminating the

conflict between old and new shareholders.

1 Myers and Majulf (1984, p. 195) note that this action “…would be difficult and also illegal”.

4

The two instances where financial slack would not be valuable are precisely the

conditions that apply at family owned and managed firms. At a family firm, the managers are

insiders, they are shareholders, and they have information that outside shareholders do not

have. Also, the owner-managers may be extremely reluctant to sell shares to outsiders and

thus compromise their control. Potential purchasers of the new shares, knowing that the

insiders would only be selling if the shares are overvalued, would demand a discount. The

discount would further discouraging insiders from selling new shares. For these reasons,

financial slack would be more valuable at firms where family ownership is high, but less

valuable at firms where family ownership is lower.

Since Thai firms are quite often family owned and managed, the owner-managers

would indeed know more about the firm and its investment opportunities – the first

assumption made by Myers and Majulf (1984). In addition, the owner-managers would act in

the interest of themselves, the existing owners of the firm, according to the second

assumption. For example, secondary equity offerings are rare for Thai public companies.

Firms more commonly undertake a rights offering to the existing shareholders as a means to

secure new additional equity capital.

At a family owned and managed firm, the family owners often have much of their

wealth tied up in the firm, and the wealth may not be especially liquid. Their own money is

at risk. Thus, they would not make decisions that would impair their wealth. For example, if

the family owner-managers overinvest by accepting value-destroying, negative NPV projects,

they reduce their own wealth because they have reduced the value of the company.

Similarly, if the family owner-managers underinvest, they have refused to fund positive NPV

projects that would increase the value of their firm, missing opportunities to increase their

wealth. At higher levels of family ownership, family members would have a greater

5

incentive to pursue an optimal investment policy, since their investment decisions have a

larger direct effect on their wealth. Conversely, as family ownership declines,

overinvestment would become more of a problem than underinvestment because the family

typically does not own all of a firm’s shares. Minority shareholders may have sizeable stakes

in aggregate. Since the family owner-managers do control the investment decision, their

investment decisions may bring other private benefits of control (increasing the firm size, for

example, or consumption of perks, or the opportunity to divert assets) that they alone can

enjoy. For this reason, a less-than-optimal investment policy would be the more likely

outcome at firms with lower levels of family ownership.

Control-enhancing structures like pyramids make it much easier for controlling

shareholders to take advantage of the minority owners through expropriation actions like

transfers of assets or funds through related-party transactions. However, these control-

enhancing structures are somewhat rare for Thai firms. Thus, the family owners ideally

would follow an optimal investment strategy, suppressing the inclination to overinvest and

destroy firm value, and suppressing the temptation to underinvest, for the same reasons. The

costs of pursuing a less-than-optimal investment policy, and the resultant wealth destruction

or foregone increases in value, would fall disproportionately on the dominant (controlling)

owners.

In contrast, managers at firms with low family ownership may have little or no

ownership of the company they manage. Managers at these firms may be risk-averse and

prefer to underinvest, or not to invest at all, to reduce the variability of profits and to increase

job security. The managers would bear little or none of the consequences their decision to

forego investment opportunities. Firms with low family ownership may also be subject to

greater monitoring by the shareholders or creditors. Greater monitoring, for example, may

6

take the form of creditors place restrictions on the firm, such as loan covenants or limits on

capital expenditures. Given the absence of an active market for corporate control in the Thai

stock market, the managers could underinvest with relative impunity.

Based on the discussion above, I can make clear theoretical predictions about the

relation between firm type and the investment ratio, growth opportunities, and the effect of

financing constraints. I expect firms with high family ownership to follow an optimal

investment policy. Firms with low family ownership, on the other hand, may exhibit signs of

underinvestment. Thus, I predict low family ownership firms will have investment ratios less

than the ratios at high family ownership family firms. I will interpret lower investment ratios

at low family ownership firms as a sign of underinvestment.

Next, I expect that the relation between the investment ratio and growth opportunities

is positive among high family ownership firms. This implies that high family ownership

firms invest to capture the full benefits of the growth opportunities they possess. I do not

expect a significant relation between the investment ratio and growth opportunities among

low family ownership firms, based on the expectation that managers at low family ownership

firms will underinvest. Lastly, I predict no relation between the investment ratio and

financing constraints at high family ownership firms. Financial slack, in the form of cash or

unused borrowing capacity, can be thought of as the opposite of a financing constraint. At

high family ownership firms, slack is not valuable because the owners are the managers and

possess knowledge of the value of investment opportunities. The value of a potential

investment does not have to be communicated to outside equity investors, thus preserving

control and confidentiality. As noted earlier, financial slack may be more valuable to low

family ownership firms.2 For low family ownership firms, I expect a negative relation

2 The information asymmetry argument (Myers and Majluf, 1984) expresses a relation between investment policy and financing constraints. At low family ownership firms, managers have information that other

7

between the investment ratio and financing constraints; that is, the relation between the

investment ratio and financial slack is positive.

Theoretical Prediction for Variables of Interest Concerning:

Type of firm

Degree of Information Asymmetry

Investment Ratio Growth Opportunities

Financial Slack

High Family Ownership

Lower Investment policy is optimal

Positive relation with investment

ratio

No relation with

investment ratio

Low Family Ownership

Higher Investment policy is not optimal;

underinvestment

No relation with investment ratio

Positive relation with investment

ratio

3. Prior Empirical Research

There are just a few studies examining the connection between a dominant owner or

family ownership and the investment policies of firms.

Goergen and Renneboog (2001) use UK firms to evaluate whether the availability of

internal funds influences the investment spending of firms. The authors document no

positive relation between internally generated funds and investment for the random sample of

UK firms covering a six-year period. However, the authors note interesting differences in

their subsamples. For example, financially constrained firms underinvest, judging from the

strong positive relation between investment spending and the amount of internally generated

funds at these companies. Ownership moderates this relation. The authors also show firms

with higher levels of managerial ownership have less underinvestment.

investors do not have, and managers may act in the interest of the existing owners of the firm. The authors suggest this could lead to underinvestment.

8

Andres (2008) uses a sample of German public company covering 1997 to 2004 to

determine the influence of founding family ownership on investment policy. Family firms

show investment patterns that are less sensitive to the availability of cash and more sensitive

to investment opportunities compared with other types of firms.

These two studies for developed markets arrive at consistent conclusions that

ownership characteristics influence investment expenditures. This conclusion is supported by

Wei and Zhang (2008), who examine the sensitivity of investment cash flows for eight East

Asian nations in 1993-1996, the four years immediately preceding the Asian Financial Crisis.

They find a positive relation between capital expenditures (investment) and cash flow, and a

positive relation between capital expenditures and growth opportunities. They also examine

the way in which the control rights of the largest shareholder (owning 50 percent of the

outstanding shares) affect the relation between investment and cash flow. The authors find

that increases in the cash flow rights of the largest shareholder reduce the sensitivity of

capital expenditures to cash flow. Wei and Zhang (2008) also find as managers become more

entrenched (measured by a greater deviation between the cash flow rights and voting rights),

the sensitivity of capital expenditures to cash flow increases.

However, two studies for other emerging markets arrive at different conclusions.

Prasetyantoko (2007) observes no difference in the sensitivity to financial constraints

between firms in the tradable versus non-tradable sectors of the Indonesian stock market.

The author also notes no difference in firm investment and liquidity (measured by cash flow)

between these two types of firms. Pallathitta, Kabir and Qian (2011) separate a sample of

Indian businesses into group-affiliated and non-affiliated firms. The authors make the

assumption that group-affiliated firms should have easier access to funds and thus investment

should be less sensitive to cash flow. They find a strong positive relation between investment

9

and cash flow sensitivity, but the relation is indistinguishable between group-affiliated and

non-affiliated firms.

Fazzari, Hubbard, and Petersen (1988) find that financing factors affect firms’

investment decisions. They use investment cash flow sensitivity as a measure of financing

constraint. Kaplan and Zingales (1997) return to this issue, examining the relation between

investment-cash flow sensitivities and financing constraints for firms previously studied

Fazzari, Hubbard, and Petersen. Kaplan and Zingales (1997) find that firms appearing less

financially constrained have higher investment-cash flow sensitivities, and conclude that

sensitivities cannot be used to show financial constraints. The debate continued in a series of

papers (see Fazzari, Hubbard, and Petersen (2000) and Kaplan and Zingales (2000) for

dissections of each other’s work). Cleary (1999) strives to resolve the debate by using

financial statement information to classify firms based on the level of financing constraint.

Cleary (1999) finds that investment decisions are related to financial factors, supporting the

findings of Kaplan and Zingales (1997).

3. Data and Methodology

3.1 Identification of High Family Ownership versus Low Family Ownership Firms

Family ownership is common among Thai public companies, even though the total

amount of family ownership may be significantly below 25 percent of the shares, the legally-

designated threshold for control. For example, a family could own 12 percent of the shares,

yet retain a significant amount of influence over the firm’s policies, by virtue of occupying

key management positions, or holding seats on the board of directors. There are arguably

very few true widely-held firms in Thailand, where widely-held means small, atomistic

10

shareholdings, as described by Berle and Means (1932). Appendix 1 gives a more detailed

description of the extent of family ownership among publicly-traded non-financial firms in

Thailand.

I divide my sample into high family ownership and low family ownership firms, using

an ownership classification scheme similar to the method described by La Porta, Lopez-de-

Silanes, and Shleifer (1999) and other researchers, such as Claessens, Djankov, and Lang,

(2000) and Claessens, Djankov, Fan, and Lang, (2002). The designation of high family

ownership is set at 25 percent of the outstanding shares, since this is the threshold for control

according to Thai law.3

For each sample firm in each sample year, the ownership of the voting rights4

determines whether a firm has high or low family ownership. I examine the list of the top ten

shareholders, plus annual reports and other outside references, to determine if a firm has an

ultimate controller. An ultimate controller is a shareholder owning 25 percent or more of the

equity.5 I trace ownership of the shares upwards through networks of companies, both private

and public.6 If family members own 25 percent of the shares, either directly or indirectly, I

classify the company as a ‘high family ownership’ firm. If a firm does not have a family

owning 25 percent of the shares, I classify the firm as a ‘low family ownership’ firm.

3 The threshold used to designate family ownership varies in the literature. In early studies, the ownership threshold or cutoff value may be set by the researchers or set by law. For example, other researchers have used 20 percent ownership of the voting rights to determine the extent of family control, or even lower levels. See for example La Porta, Lopez-de-Silanes, and Shleifer (1999), Claessens, Djankov, and Lang (2000), Claessens, Djankov, Fan, and Lang (2002), Vilalonga and Amit (2006), and Wei and Zhang (2008). Wiwattanakantang (2001) notes that 25 percent ownership designates control of a Thai firm, consistent with Thai law. In more recent studies, researchers consider a family firm to be on where a founder or family shareholder manages the company or sits on the board. Researchers also use lower cutoff values to establish family ownership. For example, Anderson, Duru, and Reeb (2012) set a minimum family ownership threshold of 5 percent. 4 Thai law requires one share, one vote. 5 Individual family members and family-controlled affiliated firms are grouped as “family”. Shareholders with the same last name are counted as family, as are shareholders with known familial relationships (spouses, children, and other relatives), even if the last names are different. Corporations, either public or private, that are part of a family-controlled network are included in the family ownership tally. 6 I eliminate from the sample firms that have the state, a foreign corporation, a widely-held domestic financial institution, or another type of institution (such as a charitable foundation) as an ultimate controller.

11

I repeat the classification methodology using a lower cutoff value to determine the

high family ownership and low family ownership firms. I use the lower cutoff value (family

ownership of 10 percent of the shares) as a robustness check.

3.2 Identification of pyramidal ownership structures

The “wedge” is measured as the ratio of the cash flow (or ownership) rights divided

by the voting (or control) rights. This variable is frequently used by researchers as a proxy

for the extent of agency problems in firms. I employ the wedge as a proxy for the degree of

information asymmetry at family firms. An ownership “wedge” arises through the use of a

pyramidal ownership structure.7 I hypothesize the wedge will have a negative relation with

investment. A smaller wedge value means a wider deviation between the cash flow rights

and voting rights. The wider deviation implies the information asymmetries grow more

severe as the wedge value declines. The owner-managers of a family firm would be less

likely to overinvest and destroy the wealth they have built up in their firms; their personal

fortunes would suffer. However, control-enhancing structures, like pyramidal shareholdings,

permit the controlling shareholders to take advantage of smaller shareholders more easily.

Combining these two points, the differences in information will be higher when the owners

employ control-enhancing structures, as shown by smaller values for the wedge. As the

values of the wedge gets smaller, the degree of information asymmetry rises. Firms with

pyramidal ownership structures are more likely to overinvest, shown by higher investment

ratios. Thus, I predict a negative sign for the wedge. In contrast, firms with wedge values

7 The “wedge” is defined as the ratio of the cash flow rights divided by the voting rights. The “wedge” is determined by first finding the chain of control for a firm. If a firm does not have a chain of control, that is, the shareholders own their shares directly rather than through a network of affiliated public or private companies, the cash flow rights are equal to the voting rights. For firms with a chain of control, the cash flow rights are measured as the product of the family’s ownership percentages at each level in the chain of control. The voting or control rights for a firm are the smallest ownership percentage along the chain of control. This is the method used by La Porta et al. (1999).

12

equal to one will have less information asymmetries, despite differences in the level of family

ownership. These firms will not overinvest and thus exhibit lower investment ratios.

Due to data availability, I use only a single year (2005) of values for the wedge

variable. I extend this single year to cover all ten years in my sample (2001 – 2010).

Anecdotal evidence and a visual inspection of the data show ownership characteristics, such

as the use of pyramidal shareholdings, are static for most firms.

Early research, such as a study by Claessens et al. (2000), find that Thai firms rarely

employ ownership pyramids before the 1997 Asian financial crisis. However, a more recent

paper by Connelly et al. (2012) documents that by 2005, well after the Asian financial crisis

of 1997, the incidence of pyramidal ownership structures by Thai firms had increased. By

2005, more Thai firms used ownership pyramids to enhance their owners’ control rights.

3.3 Empirical methods

Equation 1 is an augmented version of the equation tested in Cleary (1999) and Cleary

(2005).

Capex Ratioi,t = β1 + β2 High Family Ownership Dummyi,t + β3 Growth Opportunitiesi,t

+ β4 High Family Ownershipi,t * Growth Opportunities i,t + β5 Financing

Constraintsi,t + β6 High Family Ownership Dummyi,t * Financing

Constraintsi,t + β7 Cash Flowi,t + β8 Wedgei,t + β9 Profitabilityi,t

+ β10 Sizei,t + β11 Leveragei,t + Yeari,t + Industryi,t + εi,t Eqn. (1)

13

From the theoretical background, the expected signs are:

Type of firm

Invest-ment Ratio

Growth Oppor-tunities

Financing Constraints

Cash Flow

Profit-ability

Size Lever-age

Wedge

High Family Owner

ship

( + ) ( + ) ( - ) ( + ) ( + ) ( + ) ( - ) ( - )

Low Family Owner

ship

Base category No relation No relation ( + ) ( + ) ( + ) ( - ) ( - )

The dependent variable, the Capex Ratio, is the firm’s capital expenditures in year t

divided by the book value of net plant, property, and equipment in year t. A dummy variable

for family ownership reveals the relation between the investment ratio and family firms. The

regressions include interaction terms to show the differences between the investment ratio for

high family control firms and low family control firms, with respect to growth opportunities,

and with respect to financing constraints. 8 The regressions also include control variables.

For high family control firms, the proxy for growth opportunities is expected to have

a positive relation with the investment ratio (Fazzari, Hubbard, and Petersen, 1988 and 2000;

Kaplan and Zingales, 1997 and 2000; Cleary, 1999 and 2005). I expect to see no relation

between growth opportunities and investment ratio for low family ownership firms. With

respect to the financing constraint variable, previous research by Kaplan and Zingales (1997,

2000) and Cleary (1999, 2005) show that the investment sensitivities are highest for firms

that are unconstrained. Thus, the expected relation between financing constraints and the

investment ratio is negative for high family ownership firms but I expect no relation for low

family ownership firms. Cash flow is expected to have a positive relation to investment

8 Cleary (1999) and (2005) estimates a regression equation similar to Equation (1) but without the interaction terms. He estimates regressions for three subsamples: financially constrained firms (FC); partially financially constrained (PFC); and not financially constrained (NFC).

14

policy, since the availability of cash will increase capital investment. The wedge is expected

to have a negative relation the investment ratio, showing that as the wedge value falls

(indicating rising information asymmetries), the investment ratio rises.

The model I estimate includes control variables for profitability, size, and leverage,

plus dummy variables for industry and year. Profitability is expected to have a positive

relation to investment policy, as more profitable firms have more cash available to invest.

Firm size is expected to be positively related to investment policy, since larger firms would

be more likely to have higher investment needs, if only to maintain their existing bases of

assets. Lastly, leverage is expected to have a negative relation with the investment ratio.

Firms with higher amounts of leverage have less financial slack, and less access to additional

debt capital. These firms may also have bank loans or bond issues that carry restrictive

covenants and limit capital expenditures.

3.4 Description of Variables

Table 1 shows the variables used in the investment policy analyses. The dependent

variable is the Capex Ratio, defined as the capital expenditures in year t, divided by the book

value of net plant, property, and equipment, measured at the beginning of year t.

The market to book ratio (MKT_TO_BOOK) is the proxy for growth opportunities.

This variable is defined as the ratio of the market value of equity divided by the book value of

common equity. Both the market value of equity and the book value of equity are measured

at the end of the previous year (the beginning of year t). The beginning of the period values

reflect the growth opportunities present at the beginning of the year, which drive a firm’s

investment spending during the year. D_FAMILY_25 and D_FAMILY_10 are dummy

variables that equals one if the firm is a family firm and zero otherwise. KZ_SCORE is a

measure of the lack of financing constraint, or a measure of financial slack. The construction

15

of the KZ_SCORE is discussed in detail in Appendix 2. CF2_NET_PPE is the cash flow in

year t, divided by book value of net plant, property, and equipment at the beginning of year t.

Cash flow is defined as net income before extraordinary items (or earnings before interest but

after tax) plus depreciation and amortization.

The control variable for profitability is NOI_TA, measured as earnings before interest

and taxes in year t divided by total assets at the end of year t. SIZE_TA is the variable that

captures firm size, calculated as the natural logarithm of total assets at the end of fiscal year t.

TD_TA is a measure of leverage, measured as the book value of total interest-bearing debt

(including short-term financing) at the end of year t divided by total assets at the end of year

t. Dummy variables for each of the nine years in the sample (2002 – 2010) are included in

the regression analyses. I also include 21 industry dummy variables.9

3.5 Description of Sample and Data

The sample is drawn from non-financial public companies in Thailand, from 2001 –

2010. Firms must have a complete set of financial and ownership data available for each

fiscal year, 2001 through 2010.

The dataset contains 2,091 firm-year observations across the ten-year sample period.

Some observations are winsorized to eliminate extreme values. The values of the Capex

Ratio and market to book (MARKET_TO_BOOK) are winsorized at the 99th percentile. The

values of the cash flow measure, CF2_NET_PPE, are winsorized at the 99th and 1st

percentiles, as is the profitability measure, NOI_TA.

Table 2 contains the descriptive statistics for the variables used. The Capex Ratio

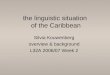

shows a significant amount of variation, even after winsorizing. Figure 1 is a histogram of

9 I use 2001 as the reference year for the year dummy variables, while “Other” is the reference industry.

16

the Capex Ratio values, illustrating the fact that the Capex Ratio is bounded at zero.10 Table 3

contains the Pearson correlation coefficients for the variables used in the regression analyses.

The low values for the correlation coefficients imply there are no issues with

multicollinearity.

4. Results

In Table 4, the dependent variable is the Capex Ratio. Model 1 regresses the high

family ownership dummy, the market-to-book ratio, and an interaction term on Capex Ratio,

while Model 2 regresses the high family ownership dummy, the financing constraint measure

KZ_SCORE, and an interaction term on Capex Ratio. Model 3 is a full model as shown in

Equation 2. Model 4 is a Tobit model.

The family dummy variable, D_FAMILY_25, is not significant in Models 1 and 2. In

Model 1, the coefficient for MKT_TO_BOOK is positive and significant. This result is

logical and as expected, indicating higher investment at firms with growth opportunities. The

coefficient for the interaction term is not significant. This implies no significant difference in

the sensitivity to growth opportunities at high family ownership firms versus low family

ownership firms. In Model 2, the coefficient for the financing constraint measure is positive

and significant. Firms with higher KZ_SCORE values (meaning a lower level of financing

constraint or more financial slack) have higher levels of investment. This result is also

expected, because firms with less financing constraints (meaning a higher KZ_SCORE value)

have more financial slack, and be able to invest more. The insignificant coefficient for the

10 According to the Worldscope data item used to construct the Capex Ratio, capital expenditures is defined as additions to fixed assets. Any divestitures are accounted for as part of another datatype. See the definitions of the Capex Ratio in Table 1.

17

interaction term indicates no difference in the sensitivity of the Capex Ratio to financing

constraints, whether a firm is a high family ownership or a low family ownership firm.

Model 3 is the full ordinary least squares (OLS) model, including control variables,

plus industry and year dummy variables. The coefficient of the dummy variable for high

family ownership is positive and significant in this model. This result shows high family

ownership firms have higher investment ratios than low family ownership firms. The

coefficient for growth opportunities (MKT_TO_BOOK) is positive and significant, and so is

the coefficient for KZ_SCORE. These two results are the same as in Models 1 and 2.

Neither of the coefficients for the two interaction terms is significant. The coefficient for

cash flow (CF2_NET_PPE) is positive and significant, indicating firms with higher cash flow

have higher Capex Ratio values.

Of the control variables, only the measure of size, SIZE_TA, is positive and

significant, indicating larger firms have a higher Capex Ratio. This result is as expected, as

larger firms would need to invest more, at the very least to maintain their larger asset bases.

The coefficients for profitability (NOI_TA) and leverage (TD_TA) are not significant in any

model. These results are different than the hypothesized relations. Firms with higher

profitability were expected to have more cash available for investment and thus higher Capex

Ratio values. Firms with higher leverage were expected to have lower Capex Ratio values

because these firms may face difficulties securing additional capital to fund investments. For

example, firms with greater leverage may carry restrictive loan covenants which limit capital

expenditures. The effects of theses the profitability and leverage variables may have been

subsumed by other variables in the multiple regression model.

Model 4 uses a different econometric specification: a Tobit model. I include this

model because the distribution of the Capex Ratio is bounded at zero (see Figure 1). The

18

results from Model 4 confirm the results of Model 3, the full model. However, one

interaction term, high family ownership interacted with the growth opportunities proxy

variable, is negative and significant. When the coefficient of the interaction term is combined

with the coefficient for the high family ownership dummy, the net effect is that high family

ownership firms have higher Capex Ratio values than low family firms, but the difference is

smaller among firms with high growth opportunities.

The conclusions from Table 4 are as follows:

• High family ownership firms have on average a greater Capex Ratio than low

family ownership firms.

• Firms with growth opportunities have on average a greater Capex Ratio than

firms without. As growth opportunities become higher, the gap in the Capex

Ratio between high and low ownership firms narrows.

• Firms with lower levels of financing constraints have greater Capex Ratio

values. There is no difference in the relation whether a firm is a low or high

family ownership firm.

• Higher investment ratios are observed at larger firms, and at firms with higher

cash flow. There is no difference in the relation whether a firm is a low or

high family ownership firm.

• There is no relation between profitability or leverage and the Capex Ratio.

Table 5 repeats the regression analyses in Table 4, but I use a lower ownership cutoff

value to classify firms as high or low family ownership. The results in Table 5 reflect the use

of a 10 percent cutoff value, rather than the 25 percent cutoff value used in Table 4.

19

Using the lower (10 percent) cutoff value, there are far fewer firms with low family

ownership. At the 25 percent cutoff, about 29 percent (605 out of 2,091 firm-year

observations) of the sample was low family ownership firms. At the 10 percent cutoff, only

6.4 percent (117 out of 1,935 firm-year observations) are considered low family ownership

firms.11

The regression results in Table 5 are notably different from the results shown in Table

4. The family dummy variable, D_FAMILY_10, is not significant in any regression. The

proxy for growth opportunities, MKT_TO_BOOK, is significant in two OLS models (Models

1 and 3) as well as the Tobit model (Model 4). The coefficient of the interaction term is not

significant in Model 1 or Model 3, but it is significant at the 10 percent level in Model 4. The

coefficient of cash flow (CF2_NET_PPE) is positive and significant in Models 3 and 4. The

coefficients for KZ_SCORE are not significant in any model and the coefficients of the

interaction terms are not significant either. Of the control variables, only the coefficient for

size is positive and significant (Models 3 and 4).

A comparison of the results in Tables 4 and 5 leads to the conclusion that the results

are influenced by firms where family ownership is between 10 percent and 25 percent. This

group of firms is included in the low family ownership group in Table 4, but in the high

family ownership group in Table 5. Firms with higher levels of family ownership, and firms

with lower levels of financing constraints (higher KZ_SCORE values), have higher Capex

Ratio values. These results are driven by firms with higher (25 percent or above) family

ownership. The positive relations between family ownership and investment, and between

11 The lower cutoff value causes the sample to become slightly smaller, as I eliminate 156 firm-year observations (7.5 percent of the original 2,091 firm-year observations) from the sample. At the higher 25 percent cutoff, 156 firm-year observations are classified as low family ownership firms, since a family or other organization or institution does not own more than 25 percent of the outstanding shares. However, at the lower 10 percent cutoff value, these firms now have the state, a foreign corporation, a widely-held domestic financial institution, or another type of institution (such as a charitable foundation) as the ultimate controller.

20

investment and lower levels of financing constraint, do not hold at firms where family

ownership is between 10 percent and 25 percent. However, the positive relation between

growth opportunities and Capex Ratio, and the positive relation between cash flow and Capex

Ratio, are both robust to the choice of the cutoff value delineating high versus low family

ownership.

One possible explanation behind the inconsistent relation between family ownership

and investment rests on the classification of the firms themselves. At the higher threshold

designating family ownership, family firms have higher investment ratios (Table 5). The

information asymmetries may seem to be higher at firms with higher family ownership. This

is true when considering the differences in information between large (family) shareholders

and the minority shareholders. However, effect of the asymmetries are counterbalanced by

the desire of the family members to pursue a rational investment policy in order to protect

their wealth. As family members have a great deal of their wealth tied up in their firm, they

would be more likely to pursue a rational investment policy. They would be less inclined to

overinvest or underinvest.

At a lower threshold for family ownership, some firms previously designated as low

family ownership are now shifted into the high ownership group. Family members at these

firms hold a medium-sized stake in their firm. They own in total between 10 percent and 25

percent of the shares. Once these firms are added to the group of high family ownership

firms, the effect of family ownership on investment policy vanishes (Table 6, Panel B). The

effect of financing constraints also vanishes. Clearly these firms exert an influence on the

results. The information asymmetries at firms in the 10 percent to 25 percent ownership

group would also be quite high. Family members in this type of firm may have a reduced

21

incentive to pursue a rational investment policy. They may be inclined to underinvest and

enjoy private benefits of control, given their influential ownership stake.

Managers at low family ownership firms may have very little of their wealth tied up

in the firm. These managers may be tempted to ensure that they keep their jobs, with the

consequences being underinvestment, perhaps due to monitoring by a wider base of

shareholders or even creditors. For family firms with pyramidal ownership structures, the

results are different. The results show evidence of overinvestment, which could be evidence

of expropriation of minority shareholders.

The final set of results, shown in Table 6, include an additional explanatory variable.

I add the “wedge”, a measure of the deviation between cash flow rights and control or voting

rights, as an additional explanatory variable. My sample size shrinks slightly due to data

availability for the wedge. I have a total of 1,837 firm-year observations in Table 6. The

largest portion of the sample (1,495 firm-year observations or about 81 percent of the sample)

shows no evidence of pyramidal shareholding and the wedge value is one. The balance of the

sample (342 observations or about 19 percent of the sample; all are family firms) shows

evidence of a control-enhancing pyramidal shareholding structure.

Table 6 contains regression results using two cutoff values for high family ownership,

and two different econometric specifications. Models 1 and 2, an OLS model and a Tobit

model respectively, use 25 percent as the cutoff value for high family ownership. Models 3

and 4, an OLS model and a Tobit model, repeat the analyses but use 10 percent as the cutoff

value.

The results show that high family ownership firms have higher values of the Capex

Ratio, on average. The coefficients of the high family ownership dummy variable are

significant in Models 1 and 2, but not significant in Model 3, and significant at the 10 percent

22

level in Model 4. The coefficients for the wedge are negative and significant in Models 1, 3

and 4, but at the 10 percent level in Models 1 and 4. These results indicate that family firms

with pyramidal ownership have higher values of the Capex Ratio. The greater the deviation

between cash flow rights and voting rights, shown by lower values for the wedge, the higher

the Capex Ratio. These results are consistent with overinvestment, as expected.

The coefficients of the growth proxy (MKT_TO_BOOK) are positive and significant

across all four models. This result is robust to the use of different cutoff values to determine

high family ownership. The coefficients of the interaction terms are negative and significant

in the two Tobit models (Model 2 and Model 4), and negative and significant at the 10

percent level in Model 1. These results indicate family firms have lower Capex Ratio values,

irrespective of the cutoff value. The coefficients for the cash flow measure are positive and

significant in every model. The coefficient of the KZ_SCORE is significant at the 10 percent

level only in Model 3, while none of the coefficients for the interaction terms is significant.

The coefficients for profitability are significant only in the two Tobit models, Models 2 and

4, with Model 2 showing significance at the ten percent level. The coefficients for size are

positive and significant in all models.

As mentioned earlier, the coefficient for cash flow (CF2_NET_PPE) is positive and

significant in nearly every model in Tables, 4, 5, and 6. These results show firms with higher

cash flow have higher Capex Ratio values. My finding for the cash flow term is similar to

earlier work by Cleary (1999, 2005). In Cleary’s two papers (1999 and 2005), he shows the

coefficient of the cash flow ratio (the sensitivity of investment to changes in cash flow) is

positive, that the investment ratio has a positive relation to growth opportunities. My results

support these previous findings. Cleary (2005) finds firms with financial slack (that is, the

lack of financing constraint) have higher investment ratios. However, I find mixed evidence

23

in support of this result. My findings show a positive relation between financial slack and the

investment ratio, but only when using the 25 percent share ownership cutoff to designate with

high family ownership.

My results differ in a second aspect. Cleary (2005, p. 149) notes “…firm investment

decisions are sensitive to investment opportunities as proxied by market-to-book, but are

even more sensitive to cash flow.” In contrast, my results show that investment ratios are

more sensitive to growth opportunities than cash flow. My finding show the growth

opportunities themselves induce the firms to act and invest, irrespective of the level of family

ownership. One reason for the difference in sensitivities could be due to the difference in the

level of market development. Cleary’s 2005 study used developed nations, while my study is

only for firms in one developing market. One explanation for my results is that managers at

public companies, in a developing market, are more attuned to grabbing available growth

opportunities. The availability of the cash needed for investment seems to be a secondary

concern. This could imply that firms in a developing market can more easily find the capital

needed for their investment opportunities.

5. Conclusion

The results discussed in the preceding section show that firms with high family

ownership have investment ratios which are higher, on average, than the investing ratios of

low family ownership firms. I see these results for firms where a family owns 25 percent or

more of the outstanding shares. However, the results depend on the threshold used to

determine high family ownership. At a lower family ownership threshold of 10 percent share

ownership, high family and low family ownership firms have investment policies that are not

significantly different.

24

The same pattern holds when I include the wedge, a measure of the likelihood of

expropriation, as an additional explanatory variable. I find a negative relation between the

investment ratio and the wedge. The wedge, defined as the deviation of the cash flow rights

and ownership rights, measures an increased potential for expropriation of minority

shareholders. I find evidence of overinvestment at firms with pyramidal ownership

structures. With the wedge included in the regression analyses, I again find high family

ownership firms (using the 25 percent cutoff) have higher investment ratios. But when the

cutoff value is lowered to 10 percent, the investment ratios of high family and low family

ownership are not different.

The results show growth opportunities are associated with higher investment ratios.

This result is robust, irrespective of the ownership cutoff level used, and no matter whether a

firm has high or low family ownership. Lastly, I find mixed evidence that the lack of

financing constraints is associated with higher values of the Capex Ratio. The positive

association is not robust to the use of lower threshold for family ownership, and the effect

vanishes when the wedge is included as an additional explanatory variable.

References

Anderson, R.C., A. Duru, and D.M. Reeb. 2012. Investment policy in family controlled firms.

Journal of Banking & Finance 36: 1744-1758.

Andres, C. 2008. Family ownership, financing constraints and investment decisions.

Available at SSRN: http://ssrn.com/abstract=1101453.

Berle, M., and G. Means. 1932. The modern corporation and private property. New York:

Macmillan.

Brooker Group Public Company Ltd. 2003. Thai business groups: A unique guide to who

owns what. Brooker Group: Bangkok.

Claessens, S., S. Djankov, J. Fan, and L. Lang. 2002. Disentangling the incentive and

entrenchment effects of large shareholdings. Journal of Finance 57, 2741-2771.

Claessens, S., S. Djankov, and L. Lang. 2000. The separation of ownership and control in

East Asian corporations. Journal of Financial Economics 58, 81-112.

Cleary, S. 1999. The relationship between firm investment and financial status. Journal of

Finance 54, 673-692.

Cleary, S. 2005. Corporate investment and financial slack: International evidence.

International Journal of Managerial Finance 1, 140-163.

Connelly, J.T., N. Nagarajan, and P. Limpaphayom. 2012. Form versus substance: The

effect of ownership structure and corporate governance on firm value in Thailand.

Journal of Banking and Finance 25, 599-638.

Fazzari, S., R. G. Hubbard, and B. Petersen. 1988. Financing constraints and corporate

investment. Brookings Papers on Economic Activity, 141-206.

Fazzari, S., R. G. Hubbard, and B. Petersen. 2000. Investment-cash flow sensitivities are

useful: a comment on Kaplan and Zingales. Quarterly Journal of Economics 115:695-

705.

Goergen, M., and L. Renneboog, 2001. Investment policy, internal financing and ownership

concentration in the UK. Journal of Corporate Finance 7, 257-284.

Kaplan, S. N. and L. Zingales. 1997. Do financing constraints explain why investment is

correlated with cash flow? Quarterly Journal of Economics 112:169-215.

Kaplan, S.N. and L. Zingales. 2000. Investment-cash flow sensitivities are not valid

measures of financing constraints. Quarterly Journal of Economics 115: 707-12.

La Porta, R., F. Lopez-de-Silanes, and A. Shleifer. 1999. Corporate ownership around the

world. Journal of Finance 54:471-517.

Myers, S. and N. Majluf. 1984. Corporate financing and investment decisions when firms

have information investors do not have. Journal of Financial Economics 13: 187-221.

Prasetyantoko, A. 2007. Financing constraint and firm-level investment following a

financial crisis in Indonesia. Available at SSRN: http://ssrn.com/abstract=1014326.

Pallathitta, R., R. Kabir, and J. Qian. 2011. Investment - cash flow and financing constraints:

New evidence from Indian business group firms, Journal of Multinational Financial

Management, 21: 69-88.

Wei, K.C.J., and Y. Zhang. 2008. Ownership structure, cash flow, and capital investment:

Evidence from East Asian economies before the financial crisis, Journal of Corporate

Finance, 14: 118-132.

Villalonga, B., and R. Amit. 2006. How do family ownership, control and management affect

firm value?. Journal of Financial Economics 80: 385–417.

Wiwattanakantang, Y. 2001. The ownership structure of Thai firms. Center for Economic

Institutions, Institute of Economic Research, Hitotsubashi University, Working Paper

8, Tokyo: Hitosubashi University.

Figure 1: Histogram of Capex Ratio

0.0%5.0%

10.0%15.0%20.0%25.0%30.0%35.0%40.0%45.0%50.0%

0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4 1.6 1.8

Percent of SampleCapex Ratio

Table 1: Variables Used in the Analyses

Variable of Interest

Variable Name Definition

Measures of Investment Investment in Fixed Assets

Capex Ratio Capital expenditures in year t, divided by the book value of net plant, property, and equipment, measured at the beginning of year t. Capital expenditures is defined as Worldscope code WC04601 from the cash flow statement: Capital Expenditures (Additions to Fixed Assets)

Proxy for Growth Opportunities Market to book ratio

MKT_TO_BOOK Ratio of market value (common shares outstanding times price per share divided by the book value of common equity). The measurement is made using the market equity and book equity values from the end of the previous year (the beginning of year t).

Proxy for Amount of Funds Available to Invest Cash flow CF2_NET_PPE Cash flow in year t, divided by book value of net plant,

property, and equipment at the beginning of year t. Cash flow is defined as net income before extraordinary items (or earnings before interest after tax) plus depreciation and amortization.

Control variables

High family ownership firm dummy variable

D_FAMILY_25

Equals one if the firm is a high family ownership firm (25 percent or greater family ownership of the outstanding shares, owned directly or through a chain of control), and zero otherwise.

KZ Score KZ_SCORE Calculated by discriminant analysis Net operating income ratio NOI_TA Earnings before interest and taxes in year t divided by total

assets at the end of year t Total assets SIZE_TA Natural logarithm of total assets at the end of the fiscal year

Total debt / total assets TD_TA

Book value of total interest-bearing debt (including short-term financing) at the end of year t divided by total assets at the end of year t

Table 2: Descriptive Statistics Table 2 presents summary statistics of variables used in the study. The sample consists of non-financial firms listed on the Stock Exchange of Thailand from 2001 – 2010. Financial services companies (banks, finance and securities companies, and insurance firms) are not included in the sample. Panel A shows the full sample, while Panel B divides the sample depending on whether the firm has a high level or low level of family ownership. High family ownership means 25 percent or greater family ownership of the outstanding shares, owned directly or through a chain of control), while low family ownership means family holdings are less than 25 percent. Capex Ratio is capital expenditures in year t, divided by the book value of net plant, property, and equipment, measured at the beginning of year t. MKT_TO_BOOK is the ratio of market value of equity (common shares outstanding times price per share) divided by the book value of common equity, measured at the end of the previous year (the beginning of year t). CF2_NET_PPE is the cash flow in year t, divided by book value of net plant, property, and equipment at the beginning of year t, where cash flow is defined as net income before extraordinary items (or earnings before interest after tax) plus depreciation and amortization. KZ_SCORE is a measure of financing constraint. NOI_TA is earnings before interest and taxes divided by total assets. SIZE_TA is the natural logarithm of total assets at the end of the fiscal year. TD_TA is the book value of total interest-bearing debt (including short-term financing) divided by total assets. Some variables in the sample have been winsorized to eliminate extreme values: 99th percentile for Capex Ratio and MKT_TO_BOOK; 99th and 1st percentiles for CF2_NET_PPE and NOI_TA. There are a total of 2,091 firm-year observations. Panel A: Full Sample

Variable Mean Median Std Dev Maximum Minimum Skewness Kurtosis

Capex Ratio MKT_TO_BOOK CF2_NET_PPE KZ_SCORE NOI_TA SIZE_TA TD_TA

0.189 1.416 0.587 2.126 0.052

14.767 0.254

0.1150.9490.2611.7590.051

14.5890.230

0.2421.4121.6342.3170.0971.3040.213

1.600 9.300

11.900 13.000 0.330

19.081 0.857

0.000 0.094

-1.900 -8.053 -0.300 11.220 0.000

3.196 2.947 5.297 0.809

-0.356 0.438 0.427

13.029 11.236 31.350 3.569 2.179

-0.074 -0.865

Panel B: Divided by Level of Family Ownership

N Variable Mean Median Std Dev Max Min Skewness Kurtosis

Low Family

Ownership 605

Capex Ratio MKT_TO_BOOK CF2_NET_PPE KZ_SCORE NOI_TA SIZE_TA TD_TA

0.1851.3540.5471.6130.029

14.8030.277

0.0920.8570.2121.6060.040

14.5850.273

0.2761.4991.8582.2530.1001.2960.206

1.6009.300

11.90011.9620.330

19.0810.857

0.0000.151

-1.900-8.053-0.30011.2260.000

3.354 3.238 4.825 0.260

-0.822 0.442 0.328

12.974 12.519 26.032 4.070 1.819

-0.158 -0.842

High Family

Ownership 1,486

Capex Ratio MKT_TO_BOOK CF2_NET_PPE KZ_SCORE NOI_TA SIZE_TA TD_TA

0.1911.4420.6032.3350.061

14.7530.245

0.1230.9880.2811.8230.054

14.5910.216

0.2271.3751.5342.3110.0941.3070.215

1.6009.300

11.90013.0000.330

18.6520.844

0.0000.094

-1.900-7.403-0.30011.2200.000

3.025 2.802 5.550 1.040

-0.116 0.437 0.477

12.199 10.542 34.175 3.311 2.165

-0.037 -0.852

Table 3: Pearson Correlation Coefficients Table 3 presents the Pearson correlation coefficients for the variables used in the study. The sample consists of non-financial firms listed on the Stock Exchange of Thailand from 2001 – 2010. Financial services companies (banks, finance and securities companies, and insurance firms) are not included in the sample. Capex Ratio is defined as capital expenditures in year t, divided by the book value of net plant, property, and equipment, measured at the beginning of year t. MKT_TO_BOOK is the ratio of market value of equity (common shares outstanding times price per share) divided by the book value of common equity, measured at the end of the previous year (the beginning of year t). CF2_NET_PPE is the cash flow in year t, divided by book value of net plant, property, and equipment at the beginning of year t, where cash flow is defined as net income before extraordinary items (or earnings before interest after tax) plus depreciation and amortization. KZ_SCORE is a measure of financing constraint. NOI_TA is earnings before interest and taxes divided by total assets. SIZE_TA is the natural logarithm of total assets at the end of the fiscal year. TD_TA is the book value of total interest-bearing debt (including short-term financing) divided by total assets. Some variables in the sample have been winsorized to eliminate extreme values: 99th percentile for Capex Ratio and MARKET_TO_BOOK; 99th and 1st percentiles for CF2_NET_PPE and NOI_TA. Correlations that are statistically significant at the 10 percent level or better are shown in bold.

Variable ( 1 ) ( 2 ) ( 3 ) ( 4 ) ( 5 ) ( 6 ) ( 7 ) ( 1 ) Capex Ratio 1.00 ( 2 ) MKT_TO_BOOK 0.23 1.00 ( 3 ) CF2_NET_PPE 0.26 0.13 1.00 ( 4 ) KZ_SCORE 0.11 0.07 0.13 1.00 ( 5 ) NOI_TA 0.10 0.18 0.31 0.40 1.00 ( 6) SIZE_TA 0.08 0.11 0.14 -0.09 0.15 1.00 ( 7 ) TD_TA -0.03 0.05 -0.02 -0.56 -0.22 0.35 1.00

Table 4: Regression Results Table 4 presents regression results with the Capex Ratio as the dependent variable, using 25 percent ownership as the cutoff value to determine whether or not a firm is a high family ownership firm. A total of four regression models are shown: three ordinary least squares (OLS) models and a Tobit model. The sample consists of non-financial firms listed on the Stock Exchange of Thailand from 2001 – 2010. Financial services companies (banks, finance and securities companies, and insurance firms) are not included in the sample. The Capex Ratio is defined as capital expenditures in year t, divided by the book value of net plant, property, and equipment, measured at the beginning of year t. D_FAMILY_25 is a dummy variable that equals one if the firm is a firm with high family ownership (25 percent or greater family ownership of the outstanding shares, owned directly or through a chain of control), and zero otherwise. MKT_TO_BOOK, a proxy for growth opportunities, is the ratio of market value of equity (common shares outstanding times price per share) divided by the book value of common equity, measured at the end of the previous year (the beginning of year t). CF2_NET_PPE is the cash flow in year t, divided by book value of net plant, property, and equipment at the beginning of year t, where cash flow is defined as net income before extraordinary items (or earnings before interest after tax) plus depreciation and amortization. KZ_SCORE is a measure of financing constraint. NOI_TA is earnings before interest and taxes divided by total assets. SIZE_TA is the natural logarithm of total assets at the end of the fiscal year. TD_TA is the book value of total interest-bearing debt (including short-term financing) divided by total assets. MKT_TO_BOOK * Family and KZ_SCORE * Family are interaction terms, multiplying MKT_TO_BOOK and KZ_SCORE, respectively, with the D_FAMILY_25 dummy variable. Some variables in the sample have been winsorized to eliminate extreme values: 99th percentile for Capex Ratio and MARKET_TO_BOOK; 99th and 1st percentiles for CF2_NET_PPE and NOI_TA. The standard errors of the coefficients have been adjusted for heteroskedasticity. t-statistics are shown in parentheses. *, **, and *** denote statistically significant differences at the 10, 5, and 1 percent level (two-tailed) respectively.

OLS OLS OLS Tobit

Expected

Sign ( 1 ) ( 2 ) ( 3 ) ( 4 )

D_FAMILY_25 ( + ) 0.006 0.011 0.046*** 0.045*** (0.33) (0.70) (2.62) (2.63)

MKT_TO_BOOK ( + ) 0.040*** 0.038*** 0.038*** (3.59) (3.64) (6.22)

Mkt to Book * Family Dummy ( + ) -0.002 -0.018 -0.017** (-0.18) (-1.41) (-2.33)

CF2_NET_PPE ( + ) 0.030*** 0.030*** (4.78) (9.15)

KZ_SCORE ( + ) 0.016*** 0.015*** 0.015*** (3.50) (3.19) (3.44)

KZ_SCORE * Family Dummy ( + ) -0.007 -0.007 -0.007 (-1.30) (-1.40) (-1.47)

NOI_TA ( + ) -0.089 -0.091 (-1.12) (-1.46)

SIZE_TA ( + ) 0.016*** 0.016*** (3.23) (3.29)

TD_TA ( - ) -0.023 -0.022 (-0.70) (-0.70)

Intercept 0.130*** 0.158*** -0.118* -0.118* (8.49) 12.64 (-1.75) (-1.64)

Time (Year) Dummies No No Yes Yes Industry Dummies No No Yes Yes

Adj. R-squared 0.050 0.011 0.172 F-Statistic 37.74*** 8.994*** 12.11*** Log Likelihood 206.47 No. of Observations 2,091 2,091 2,091 2,091

Table 5: Regression Results Using a Lower Cutoff Value to Determine High Family Ownership Firms Table 5 presents regression results with the Capex Ratio as the dependent variable, using a lower cutoff value (10 percent ownership) to determine whether or not a firm is a high family ownership firm. A total of four regression models are shown: three ordinary least squares (OLS) models and a Tobit model. The sample consists of non-financial firms listed on the Stock Exchange of Thailand from 2001 – 2010. Financial services companies (banks, finance and securities companies, and insurance firms) are not included in the sample. The Capex Ratio is defined as capital expenditures in year t, divided by the book value of net plant, property, and equipment, measured at the beginning of year t. D_FAMILY_10 is a dummy variable that equals one if the firm is a firm with high family ownership (10 percent or greater family ownership of the outstanding shares, owned directly or through a chain of control), and zero otherwise. MKT_TO_BOOK, a proxy for growth opportunities, is the ratio of market value of equity (common shares outstanding times price per share) divided by the book value of common equity, measured at the end of the previous year (the beginning of year t). CF2_NET_PPE is the cash flow in year t, divided by book value of net plant, property, and equipment at the beginning of year t, where cash flow is defined as net income before extraordinary items (or earnings before interest after tax) plus depreciation and amortization. KZ_SCORE is a measure of financing constraint. NOI_TA is earnings before interest and taxes divided by total assets. SIZE_TA is the natural logarithm of total assets at the end of the fiscal year. TD_TA is the book value of total interest-bearing debt (including short-term financing) divided by total assets. MKT_TO_BOOK * Family and KZ_SCORE * Family are interaction terms, multiplying MKT_TO_BOOK and KZ_SCORE, respectively, with the D_FAMILY_10 dummy variable. Some variables in the sample have been winsorized to eliminate extreme values: 99th percentile for Capex Ratio and MARKET_TO_BOOK; 99th and 1st percentiles for CF2_NET_PPE and NOI_TA. The standard errors of the regression coefficients have been adjusted for heteroskedasticity. t-statistics are shown in parentheses. *, **, and *** denote statistically significant differences at the 10, 5, and 1 percent level (two-tailed) respectively.

OLS OLS OLS Tobit

Expected

Sign ( 1 ) ( 2 ) ( 3 ) ( 4 )

D_FAMILY_10 ( + ) 0.041 -0.010 0.038 0.036 (1.22) (-0.34) (1.10) (1.20)

MKT_TO_BOOK ( + ) 0.045** 0.045** 0.045*** (2.01) (2.15) (4.69)

Mkt to Book * Family Dummy ( + ) -0.004 -0.020 -0.019* (-0.19) (-0.88) (-1.84)

CF2_NET_PPE ( + ) 0.026*** 0.025*** (3.99) (7.67)

KZ_SCORE ( + ) 0.005 0.012 0.012 (0.59) (1.55) (1.42)

KZ_SCORE * Family Dummy ( + ) 0.007 -0.001 -0.001 (0.81) (-0.17) (-0.14)

NOI_TA ( + ) -0.053 -0.056 (-0.67) (-0.89)

SIZE_TA ( + ) 0.016*** 0.016*** (3.35) (3.30)

TD_TA ( - ) -0.006 -0.004 (-0.17) (-0.14)

Intercept 0.089*** 0.172*** -0.122 -0.121 (2.72) (6.36) (-1.59) (-1.57)

Time (Year) Dummies No No Yes Yes Industry Dummies No No Yes Yes

Adj. R-squared 0.062 0.010 0.169 F-Statistic 43.23*** 7.56*** 11.09*** Log Likelihood 248.18 No. of Observations 1,935 1,935 1,935 1,935

Table 6: Analyses Including Ownership Wedge as an Additional Explanatory Variable Table 6 presents regression results with the Capex Ratio as the dependent variable, and incorporating the ownership wedge as an additional explanatory variable. The sample consists of non-financial firms listed on the Stock Exchange of Thailand from 2001 – 2010. Financial services companies (banks, finance and securities companies, and insurance firms) are not included in the sample. The Capex Ratio is defined as capital expenditures in year t, divided by the book value of net plant, property, and equipment, measured at the beginning of year t. WEDGE is the ratio of the cash flow (ownership) rights and the voting (control) rights. A WEDGE value of one indicates that a firm shows no evidence of pyramidal ownership, while a value less than one means pyramidal shareholding is present because the cash flow rights are less than the control rights. The values of WEDGE are for a single year (2005) but are assumed to be constant across the whole ten-year sample period. D_FAMILY_25 and D_FAMILY_10 are dummy variables that equals one if the firm is a high family ownership firm and zero otherwise. D_FAMILY_25 uses a cutoff value equal to 25 percent family ownership (25 percent or greater family ownership of the outstanding shares, owned directly or through a chain of control) to designate high family ownership firm, while D_FAMILY_10 uses 10 percent as the cutoff value. MKT_TO_BOOK, a proxy for growth opportunities, is the ratio of market value of equity (common shares outstanding times price per share) divided by the book value of common equity, measured at the end of the previous year (the beginning of year t). CF2_NET_PPE is the cash flow in year t, divided by book value of net plant, property, and equipment at the beginning of year t, where cash flow is defined as net income before extraordinary items (or earnings before interest after tax) plus depreciation and amortization. KZ_SCORE is a measure of financing constraint. NOI_TA is earnings before interest and taxes divided by total assets. SIZE_TA is the natural logarithm of total assets at the end of the fiscal year. TD_TA is the book value of total interest-bearing debt (including short-term financing) divided by total assets. MKT_TO_BOOK * Family and KZ_SCORE * Family are interaction terms, multiplying MKT_TO_BOOK and KZ_SCORE, respectively, with the family ownership dummy variable (D_FAMILY_25 or D_FAMILY_10). Some variables in the sample have been winsorized to eliminate extreme values: 99th percentile for Capex Ratio and MARKET_TO_BOOK; 99th and 1st percentiles for CF2_NET_PPE and NOI_TA. The standard errors of the regression coefficients have been adjusted for heteroskedasticity. t-statistics are shown in parentheses. *, **, and *** denote statistically significant differences at the 10, 5, and 1 percent level (two-tailed) respectively.

Regression Results

OLS Tobit OLS Tobit

Expected

Sign ( 1 ) ( 2 ) ( 3 ) ( 4 )

WEDGE ( - ) -0.031* -0.032 -0.036** -0.037* (-1.70) (-1.55) (-2.01) (-1.83)

D_FAMILY_25 (Family dummy) ( + ) 0.053*** 0.054*** (2.80) (2.75)

D_FAMILY_10 (Family dummy) 0.060 0.059* (1.41) (1.77)

MKT_TO_BOOK ( + ) 0.047*** 0.047*** 0.059** 0.059*** (3.10) (6.43) (2.11) (5.25)

Mkt to Book * Family Dummy ( + ) -0.027* -0.027*** -0.036 -0.036*** (-1.64) (-3.19) (-1.26) (-3.01)

CF2_NET_PPE ( + ) 0.032*** 0.032*** 0.032*** 0.032*** (4.28) (8.56) (4.26) (8.59)

KZ_SCORE ( + ) 0.010 0.010* 0.013 0.012 (1.60) (1.75) (1.12) (1.24)

KZ_SCORE * Family Dummy ( + ) -0.001 -0.001 -0.003 -0.003 (-0.18) (-0.22) (-0.28) (-0.28)

NOI_TA ( + ) -0.122 -0.124* -0.124 -0.125** (-1.51) (-1.95) (-1.54) (-1.98)

SIZE_TA ( + ) 0.024*** 0.024*** 0.025*** 0.025*** (4.95) (4.79) (5.04) (4.93)

TD_TA ( - ) -0.002 -0.001 -0.004 -0.003 (-0.06) (-0.01) (-0.11) (-0.08)

Intercept -0.210*** -0.209*** -0.229*** -0.228*** (-3.14) (-2.76) (-2.77) (-2.81)

Time (Year) Dummies Yes Yes Yes Yes Industry Dummies Yes Yes Yes Yes

Adj. R-squared 0.185 0.184 F-Statistic 11.44*** 11.36*** Log Likelihood 265.95 264.56 No. of Observations 1,837 1,837 1,837 1,837

Appendix 1: Ownership Characteristics of Non-Financial Public Companies in Thailand, 2001 – 2010

To keep the ownership statistics as comparable as possible with previous studies of

ownership, the classification categories I use match the classification scheme described by La

Porta, Lopez-de-Silanes, and Shleifer (1999). These authors identify six types of ultimate

controllers: widely held (the firm has no ultimate controller); family (members of the same

family with the same last name); state (government ownership); widely held financial

institutions (financial institutions that do not have a single controlling large shareholder);

widely held corporations (corporations that do not have a single controlling large shareholder;

and widely held groups (other widely held entities not fitting into the above categories;

examples would be a voting trust or a cooperative). 12

The thresholds for determining control (ownership) may be set by the researchers or

by law. For example, 50 percent ownership is the cutoff for absolute control; other

researchers have used 20 percent or even as low as 10 percent ownership of the voting rights

to determine the extent of the control that a firm’s owners have over the company. The lower

level(s) are also important because prior research has shown that it is possible to control a

firm by owning a significantly lower portion of the shares.13

Wiwattanakantang (2001) notes that 25 percent can be used to give practical control

of Thai firms. Thai law states that rather than having an absolute majority of shares (greater

than 50 percent), the ownership threshold for effective control is 25 percent. I set the

designation of control at 25 percent of the outstanding shares, since this is the threshold for

control by Thai law. I use 25 percent ownership to determine high versus low family

12 Essentially the same classification scheme is used by others in several subsequent studies. See for example Claessens, Djankov, and Lang, (2000) and Claessens, Djankov, Fan, and Lang, (2002). 13 See La Porta, Lopez-de-Silanes, and Shleifer (1999) who find that 80% of firms can be controlled by stockholders owning less than 20% of the shares.

ownership. I also use a lower cutoff value (10 percent) and re-determine the high versus low

family ownership classifications.

The main source for the ownership data is the SETSMART data service, published by

the Stock Exchange of Thailand. In addition to company shareholding records and annual

reports, it is often necessary to consult outside sources to trace the ownership chains.

Examples of these outside sources would be company filings at the Ministry of Commerce,

an online database of company records provided by Business Online Co., Ltd., and numerous

business directories (for example, Brooker Group, 2003).

For each sample firm, the owner(s) of the voting rights determines the ultimate

controller (ownership) classification. Though it is possible to have differences in voting

rights and cash flow rights, Thai law requires one share, one vote.

I classify each firm into one ownership category based on the shareholder record

available that is closest to the end of the fiscal year. I examine the list of the top ten

shareholders to see if any individual, family, or organization owns 25 percent or more of the

outstanding shares. If no ultimate controller is present, the firm is classified as ‘low family

ownership’. As needed, ownership of the shares is traced upwards through the network of

companies, both private and public. Individual family members and family-controlled firms

are all grouped together as “family”. Shareholders with the same last name are counted as

family, as are known familial relationships (relatives, spouses, children, and other relatives)

even if the last names are different. Corporations that are part of a family-controlled network

are classified as ‘family’. Firms classified as ‘corporate controlled’ are companies that have

another non-family company as the ultimate controller, whether public or private, domestic or

foreign. If an ultimate owner of the shares can be determined, the company is classified into

one of the five remaining categories depending on the type of ultimate controller.