Embed Size (px)

Citation preview

Please refer to the important disclosures and analyst certification on inside back cover of this document, or on our website www.macquarie.com.au/disclosures.

INDIA

Inside Solid but slow 3

Demanding valuation: stock selection is key 11

Long-term fundamentals strong 14

What’s ailing rural income growth? 17

Passenger Vehicles: MSIL to lead growth 20

Two-wheelers: cyclical slowdown in demand25

2–wheelers: Changing dynamics 31

CV – too early to play demand recovery 38

Tractors sales – cyclical slowdown in growth44

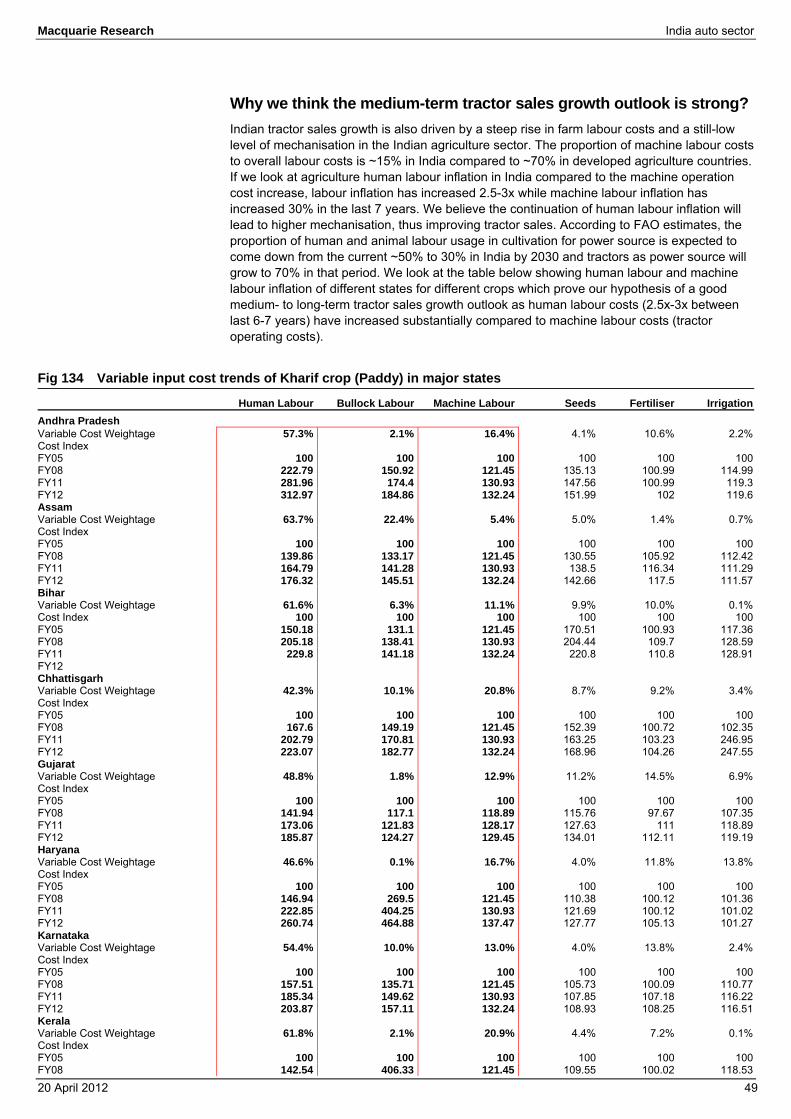

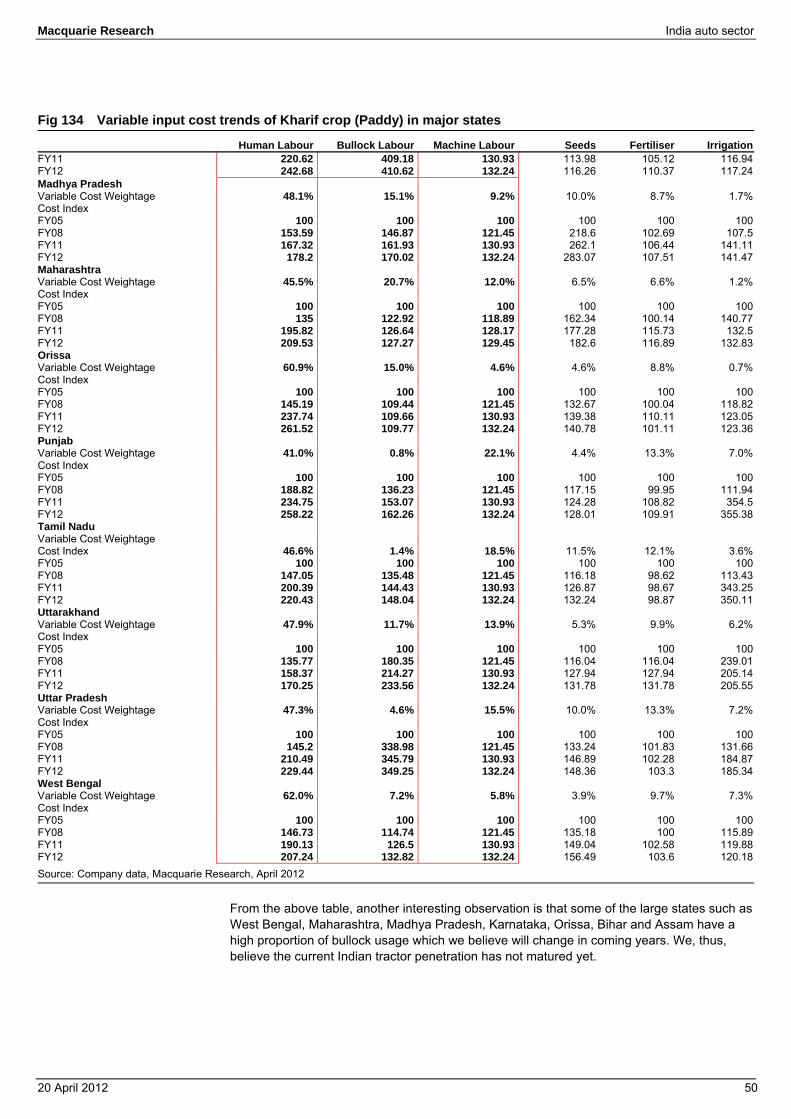

Growth driver of tractor industry intact 48

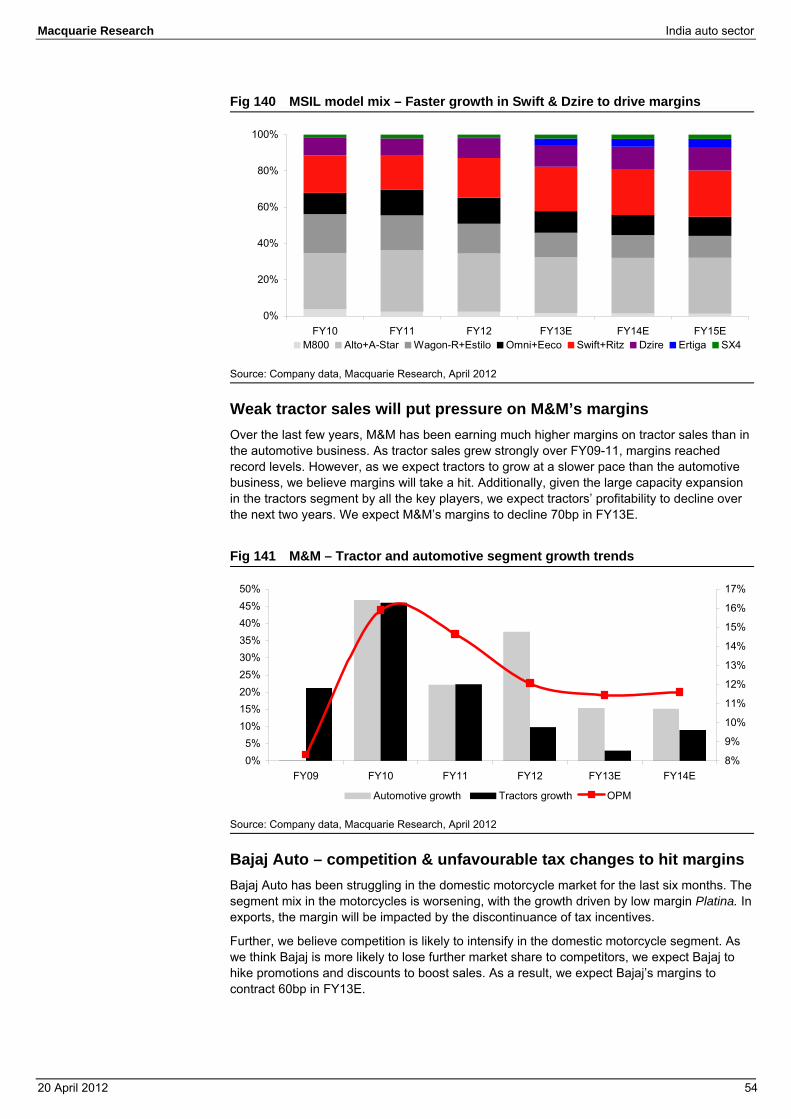

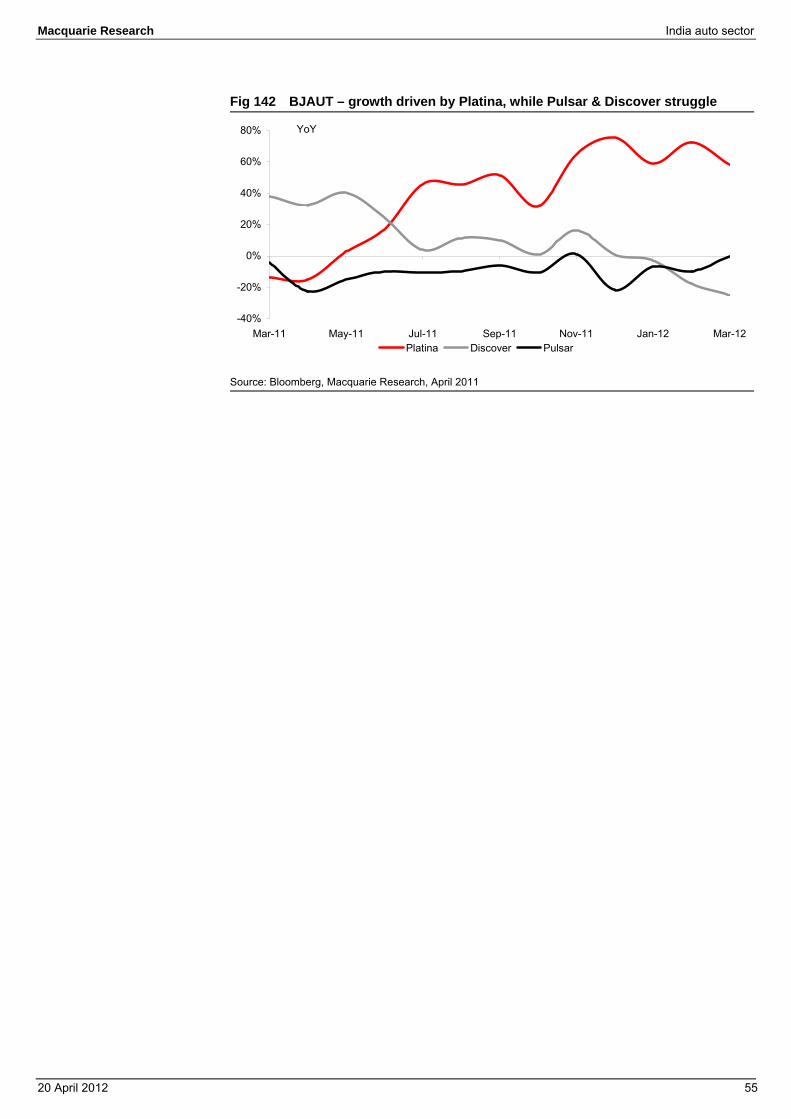

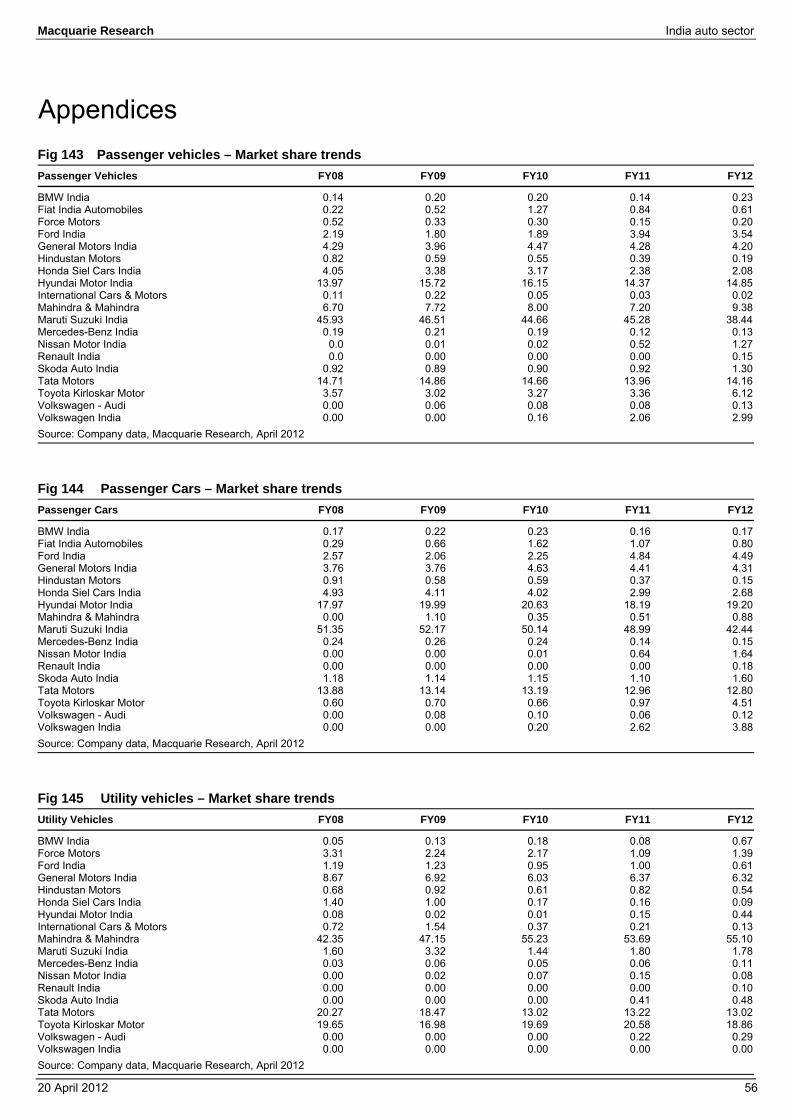

Margin outlook – mix & competition to drive 53

Appendices 56

Maruti Suzuki India 60

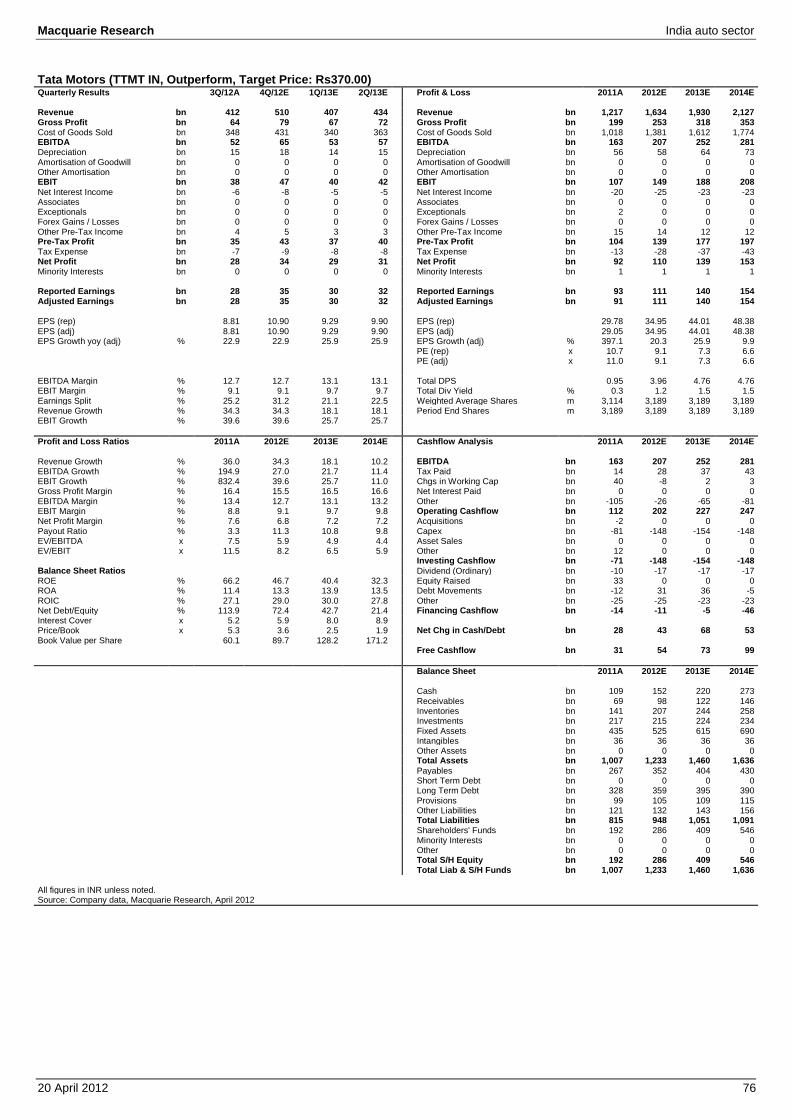

Tata Motors 72

Mahindra & Mahindra 77

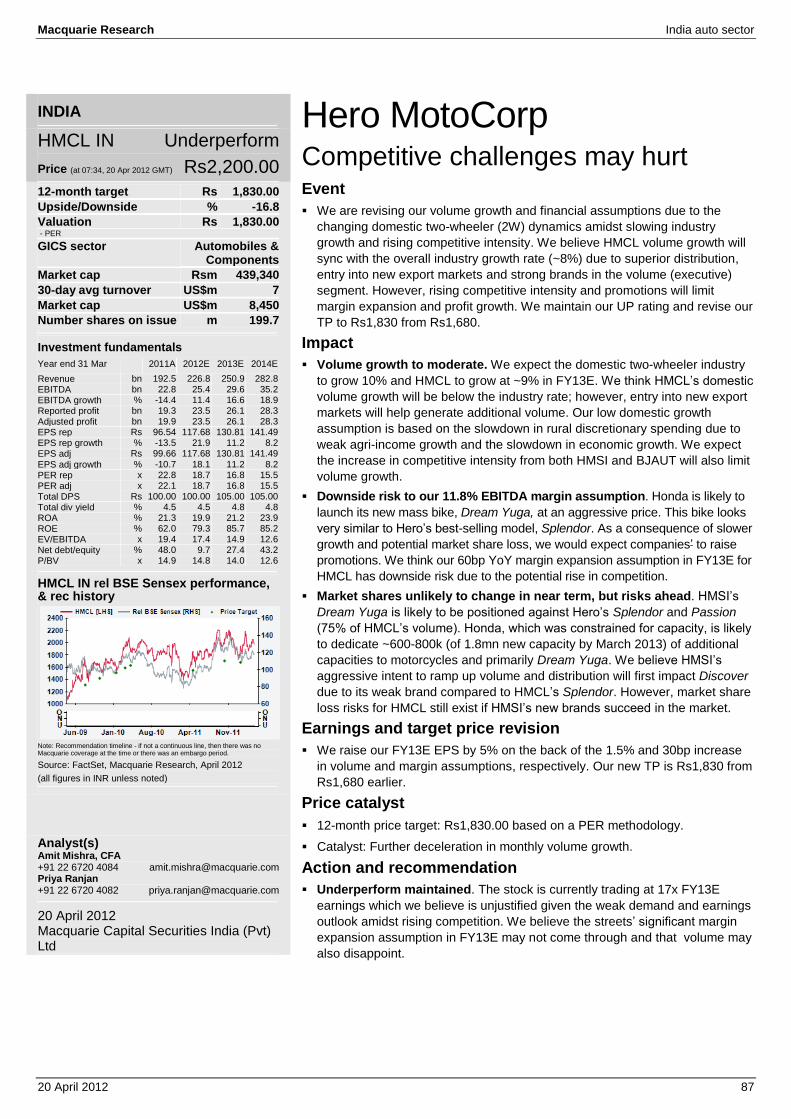

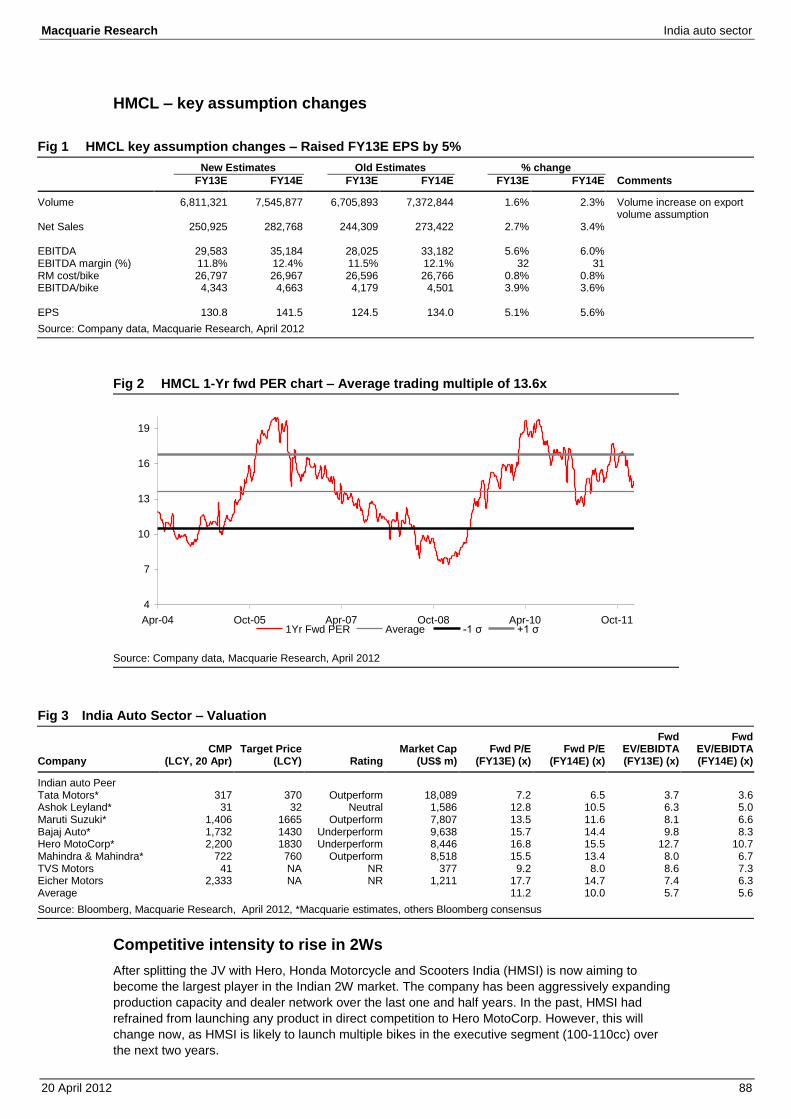

Hero MotoCorp 87

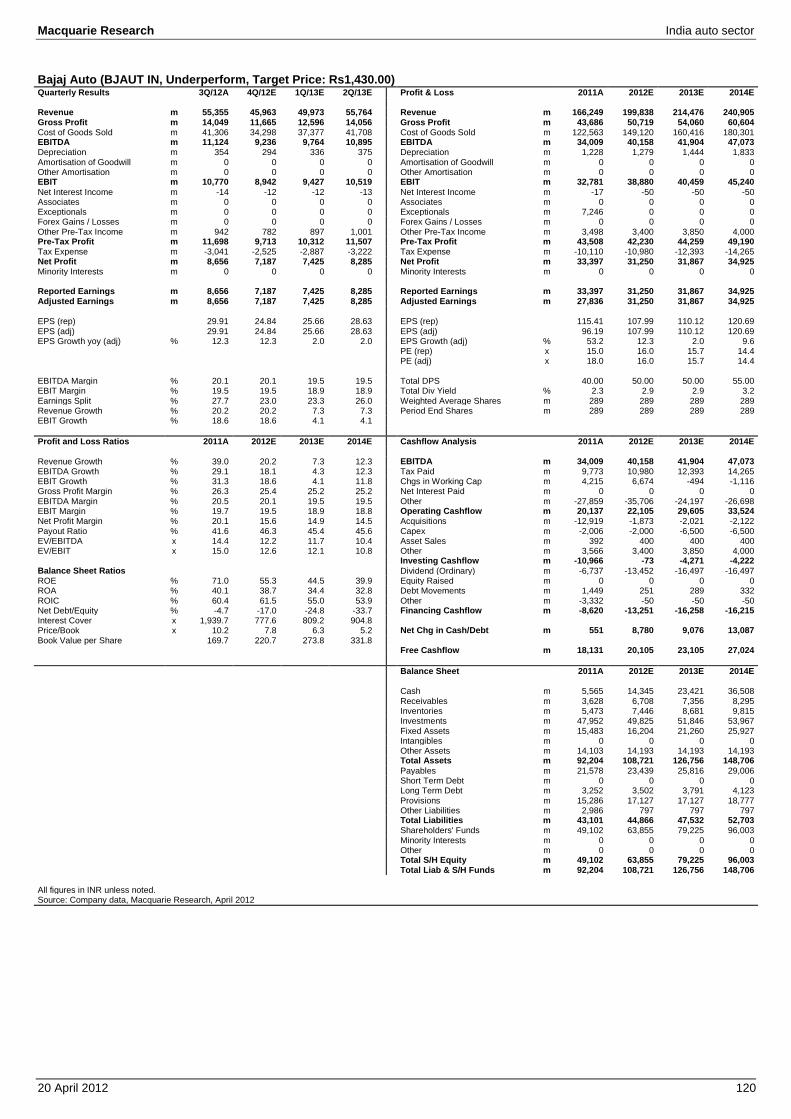

Bajaj Auto 104

Ashok Leyland 121 Analyst(s) Amit Mishra, CFA +91 22 6720 4084 [email protected] Priya Ranjan +91 22 6720 4082 [email protected]

20 April 2012 Macquarie Capital Securities India (Pvt) Ltd

India auto sector Solid but slow Time to recalibrate – Maruti top buy, Bajaj top sell idea While we remain positive on the long-term fundamentals of the Indian auto market, we believe there are significant headwinds to growth and profitability in the near-term. We expect sales growth to slow further in FY13E due to rise in ownership cost, weak sentiment and slower income growth. As stock valuations are not reflecting the near-term challenges; risk-return seems unfavourable. We recommend OP on MSIL and TTMT and a contrarian UP on BJAUT and HMCL.

Long-term fundamentals strong – prefer PV over 2Ws Rising income, improving affordability and low penetration provides large growth opportunity for the automobile companies in India. We expect passenger vehicle (cars and UV) sales to double in next four years as we expect growth higher than 16% CAGR achieved in the last 10 years. Further, the margin profile for PVs is likely to be stable as strong finance presence (70% vs 10% in China) limits the scope of sharp price cuts (like China). We expect 2W sales growth to be slower (10% CAGR) over FY12-16E as 2W penetration in urban India has reached high levels similar to other mature markets and incremental growth will be expensive

The year ahead – where is the growth? After two years of 26% growth, auto volume growth slowed to 12% in FY12. We expect a further decline in growth to 10% in FY13E due to slower rural income growth, weak consumer sentiment and high ownership cost (2-7% tax hike, high fuel price). Our analysis of farm income across key states indicates that rural consumption will likely remain subdued in the near-term. We think 5-10% hike in fuel prices is inevitable, which will further delay the pick-up in growth. We don’t expect large interest rate cuts in CY12 that would be enough to boost sentiment.

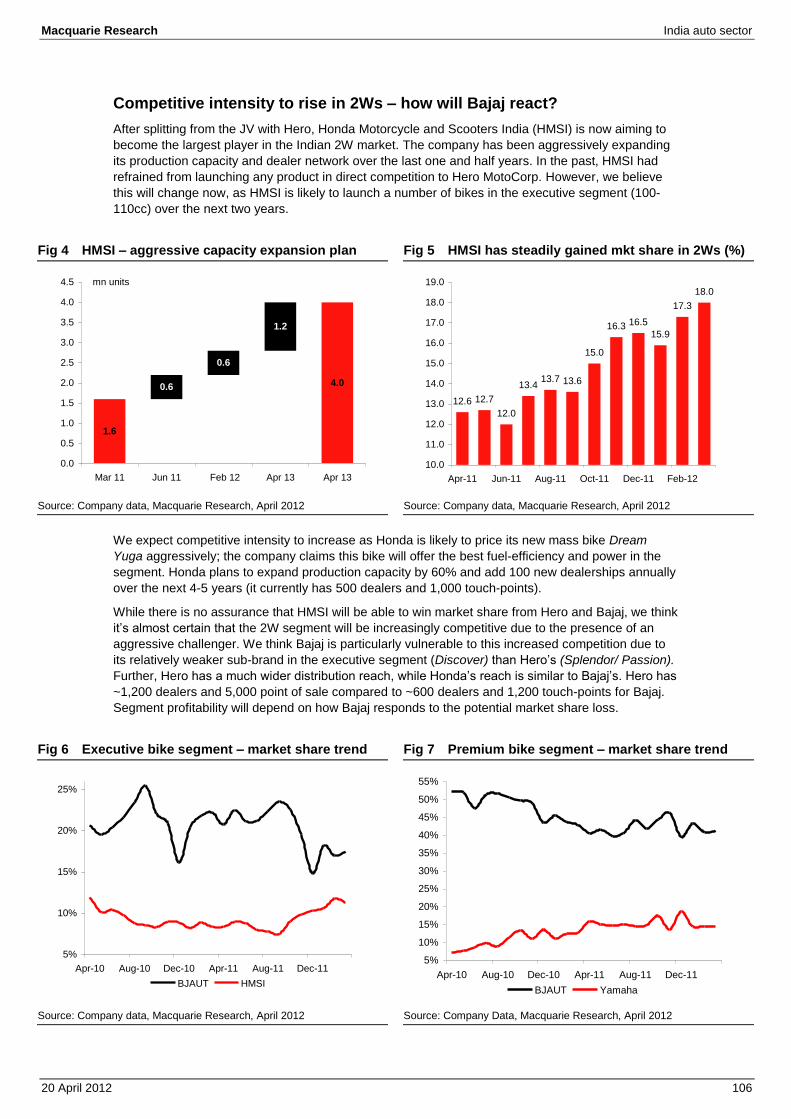

Competitive intensity to rise in 2Ws – how will Bajaj react? Given the attractive growth opportunity, we are not surprised by the number of new players that are entering the Indian auto market. In the medium-term, we expect competitive intensity to rise most in 2Ws as Honda (3rd largest player) plans to raise production capacity by 60% in the next 12 months and expand sales reach to non-urban markets. Honda will aggressively price its new bike, Dream Yuga, which they claim, offers best fuel-efficiency and power in the segment. Bajaj is vulnerable to competition due to what we believe is a weaker sub-brand in the executive segment (Discover) vs Hero’s (Splendor/ Passion). Further, Hero has a wider distribution reach, while Honda’s reach is similar to Bajaj’s. Segment profitability will depend on how Bajaj responds to the potential market share loss.

Premium valuations not factoring in cyclical slowdown Auto stocks are trading near all-time high multiples and valuation premium to the broader-market. As in the previous cycles, we believe valuation multiples should reflect the volume and margin outlook. We expect multiple de-rating for Bajaj & Hero as volume growth slows, competition intensifies and margin contracts.

MSIL is our top-pick in the sector. We expect earning upgrades to continue as new models (and upgrades) drive growth and favourable mix boost margins. We like TTMT for JLR business, where strong volume momentum is likely to sustain. (Please refer Figure 2 for changes to EPS, TP and recommendations).

Macquarie Research India auto sector

20 April 2012 2

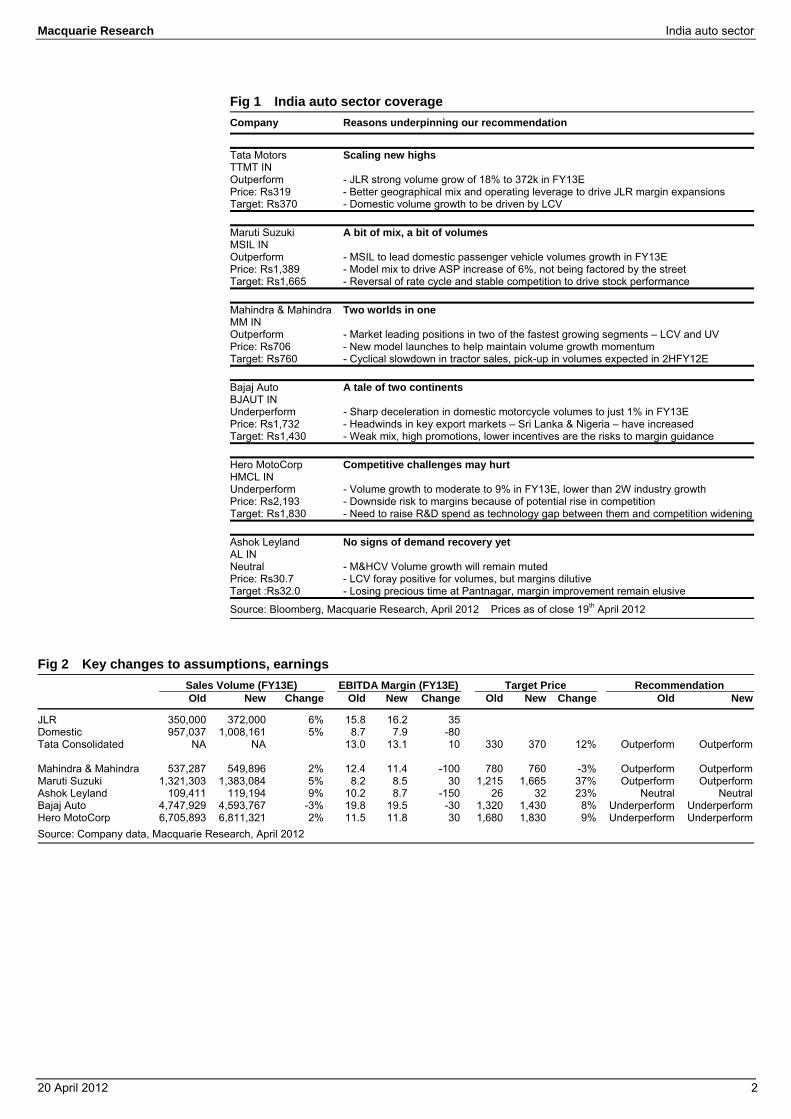

Fig 1 India auto sector coverage Company Reasons underpinning our recommendation Tata Motors Scaling new highs TTMT IN Outperform - JLR strong volume grow of 18% to 372k in FY13E Price: Rs319 - Better geographical mix and operating leverage to drive JLR margin expansions Target: Rs370 - Domestic volume growth to be driven by LCV Maruti Suzuki A bit of mix, a bit of volumes MSIL IN Outperform - MSIL to lead domestic passenger vehicle volumes growth in FY13E Price: Rs1,389 - Model mix to drive ASP increase of 6%, not being factored by the street Target: Rs1,665 - Reversal of rate cycle and stable competition to drive stock performance Mahindra & Mahindra Two worlds in one MM IN Outperform - Market leading positions in two of the fastest growing segments – LCV and UV Price: Rs706 - New model launches to help maintain volume growth momentum Target: Rs760 - Cyclical slowdown in tractor sales, pick-up in volumes expected in 2HFY12E Bajaj Auto A tale of two continents BJAUT IN Underperform - Sharp deceleration in domestic motorcycle volumes to just 1% in FY13E Price: Rs1,732 - Headwinds in key export markets – Sri Lanka & Nigeria – have increased Target: Rs1,430 - Weak mix, high promotions, lower incentives are the risks to margin guidance Hero MotoCorp Competitive challenges may hurt HMCL IN Underperform - Volume growth to moderate to 9% in FY13E, lower than 2W industry growth Price: Rs2,193 - Downside risk to margins because of potential rise in competition Target: Rs1,830 - Need to raise R&D spend as technology gap between them and competition widening Ashok Leyland No signs of demand recovery yet AL IN Neutral - M&HCV Volume growth will remain muted Price: Rs30.7 - LCV foray positive for volumes, but margins dilutive Target :Rs32.0 - Losing precious time at Pantnagar, margin improvement remain elusive

Source: Bloomberg, Macquarie Research, April 2012 Prices as of close 19th April 2012

Fig 2 Key changes to assumptions, earnings Sales Volume (FY13E) EBITDA Margin (FY13E) Target Price Recommendation

Old New Change Old New Change Old New Change Old New

JLR 350,000 372,000 6% 15.8 16.2 35 Domestic 957,037 1,008,161 5% 8.7 7.9 -80 Tata Consolidated NA NA 13.0 13.1 10 330 370 12% Outperform Outperform Mahindra & Mahindra 537,287 549,896 2% 12.4 11.4 -100 780 760 -3% Outperform OutperformMaruti Suzuki 1,321,303 1,383,084 5% 8.2 8.5 30 1,215 1,665 37% Outperform OutperformAshok Leyland 109,411 119,194 9% 10.2 8.7 -150 26 32 23% Neutral NeutralBajaj Auto 4,747,929 4,593,767 -3% 19.8 19.5 -30 1,320 1,430 8% Underperform UnderperformHero MotoCorp 6,705,893 6,811,321 2% 11.5 11.8 30 1,680 1,830 9% Underperform UnderperformSource: Company data, Macquarie Research, April 2012

Macquarie Research India auto sector

20 April 2012 3

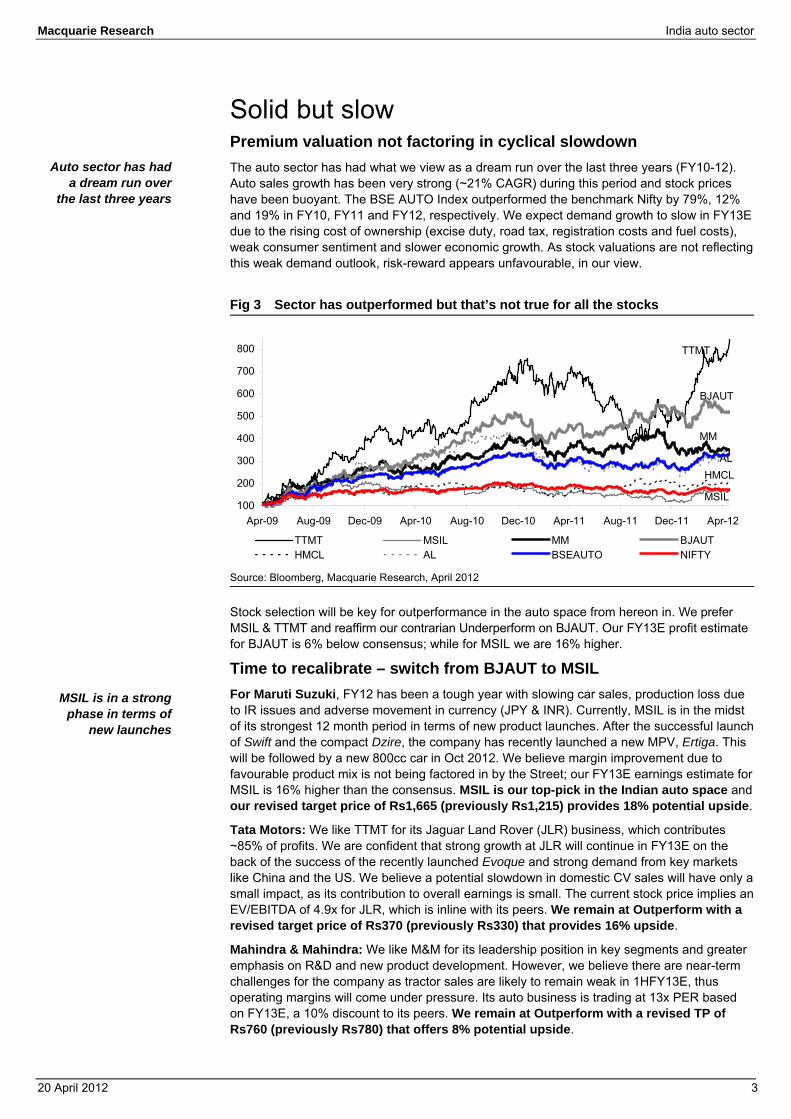

Solid but slow Premium valuation not factoring in cyclical slowdown The auto sector has had what we view as a dream run over the last three years (FY10-12). Auto sales growth has been very strong (~21% CAGR) during this period and stock prices have been buoyant. The BSE AUTO Index outperformed the benchmark Nifty by 79%, 12% and 19% in FY10, FY11 and FY12, respectively. We expect demand growth to slow in FY13E due to the rising cost of ownership (excise duty, road tax, registration costs and fuel costs), weak consumer sentiment and slower economic growth. As stock valuations are not reflecting this weak demand outlook, risk-reward appears unfavourable, in our view.

Fig 3 Sector has outperformed but that’s not true for all the stocks

Source: Bloomberg, Macquarie Research, April 2012

Stock selection will be key for outperformance in the auto space from hereon in. We prefer MSIL & TTMT and reaffirm our contrarian Underperform on BJAUT. Our FY13E profit estimate for BJAUT is 6% below consensus; while for MSIL we are 16% higher.

Time to recalibrate – switch from BJAUT to MSIL For Maruti Suzuki, FY12 has been a tough year with slowing car sales, production loss due to IR issues and adverse movement in currency (JPY & INR). Currently, MSIL is in the midst of its strongest 12 month period in terms of new product launches. After the successful launch of Swift and the compact Dzire, the company has recently launched a new MPV, Ertiga. This will be followed by a new 800cc car in Oct 2012. We believe margin improvement due to favourable product mix is not being factored in by the Street; our FY13E earnings estimate for MSIL is 16% higher than the consensus. MSIL is our top-pick in the Indian auto space and our revised target price of Rs1,665 (previously Rs1,215) provides 18% potential upside.

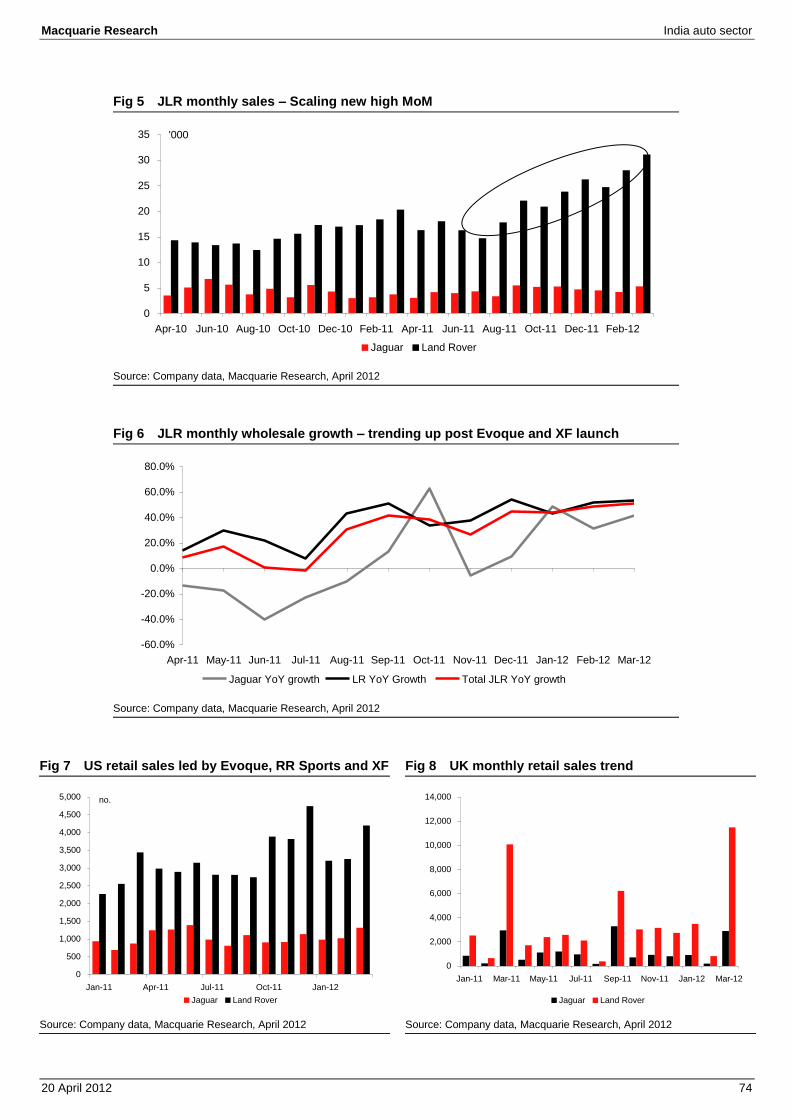

Tata Motors: We like TTMT for its Jaguar Land Rover (JLR) business, which contributes ~85% of profits. We are confident that strong growth at JLR will continue in FY13E on the back of the success of the recently launched Evoque and strong demand from key markets like China and the US. We believe a potential slowdown in domestic CV sales will have only a small impact, as its contribution to overall earnings is small. The current stock price implies an EV/EBITDA of 4.9x for JLR, which is inline with its peers. We remain at Outperform with a revised target price of Rs370 (previously Rs330) that provides 16% upside.

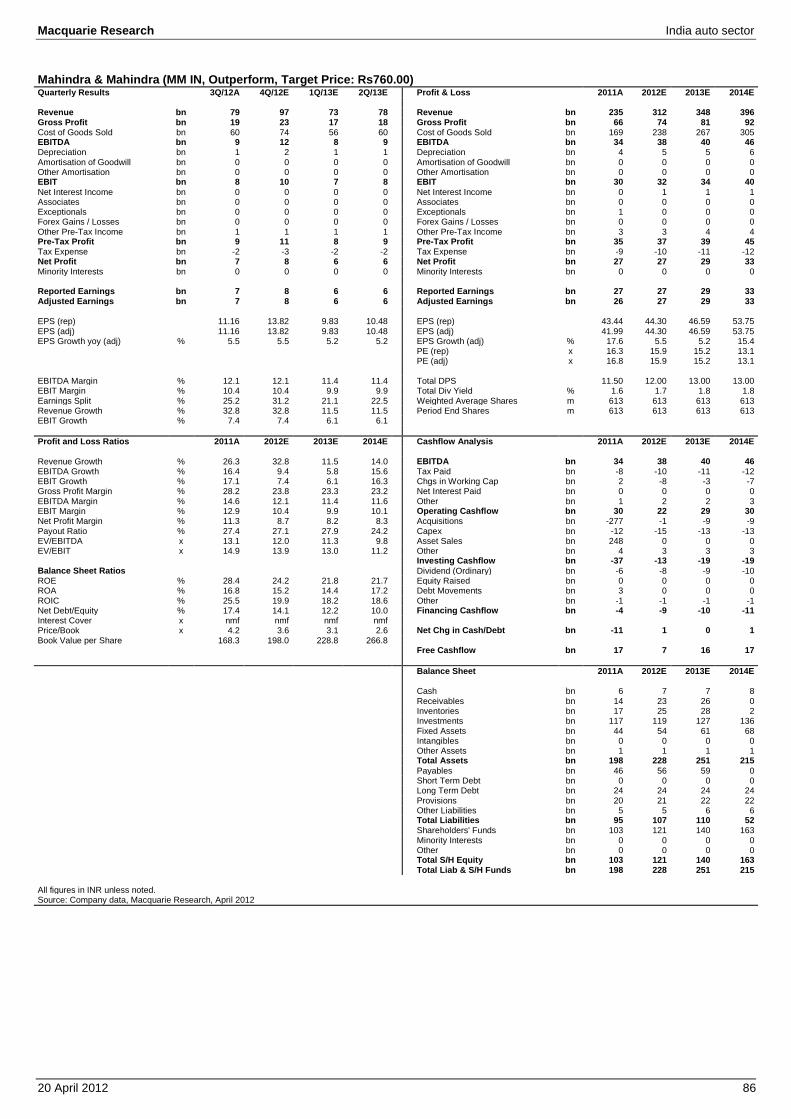

Mahindra & Mahindra: We like M&M for its leadership position in key segments and greater emphasis on R&D and new product development. However, we believe there are near-term challenges for the company as tractor sales are likely to remain weak in 1HFY13E, thus operating margins will come under pressure. Its auto business is trading at 13x PER based on FY13E, a 10% discount to its peers. We remain at Outperform with a revised TP of Rs760 (previously Rs780) that offers 8% potential upside.

100

200

300

400

500

600

700

800

Apr-09 Aug-09 Dec-09 Apr-10 Aug-10 Dec-10 Apr-11 Aug-11 Dec-11 Apr-12

TTMT MSIL MM BJAUTHMCL AL BSEAUTO NIFTY

TTMT

BJAUT

MM

ALHMCL

MSIL

Auto sector has had a dream run over

the last three years

MSIL is in a strong phase in terms of

new launches

Macquarie Research India auto sector

20 April 2012 4

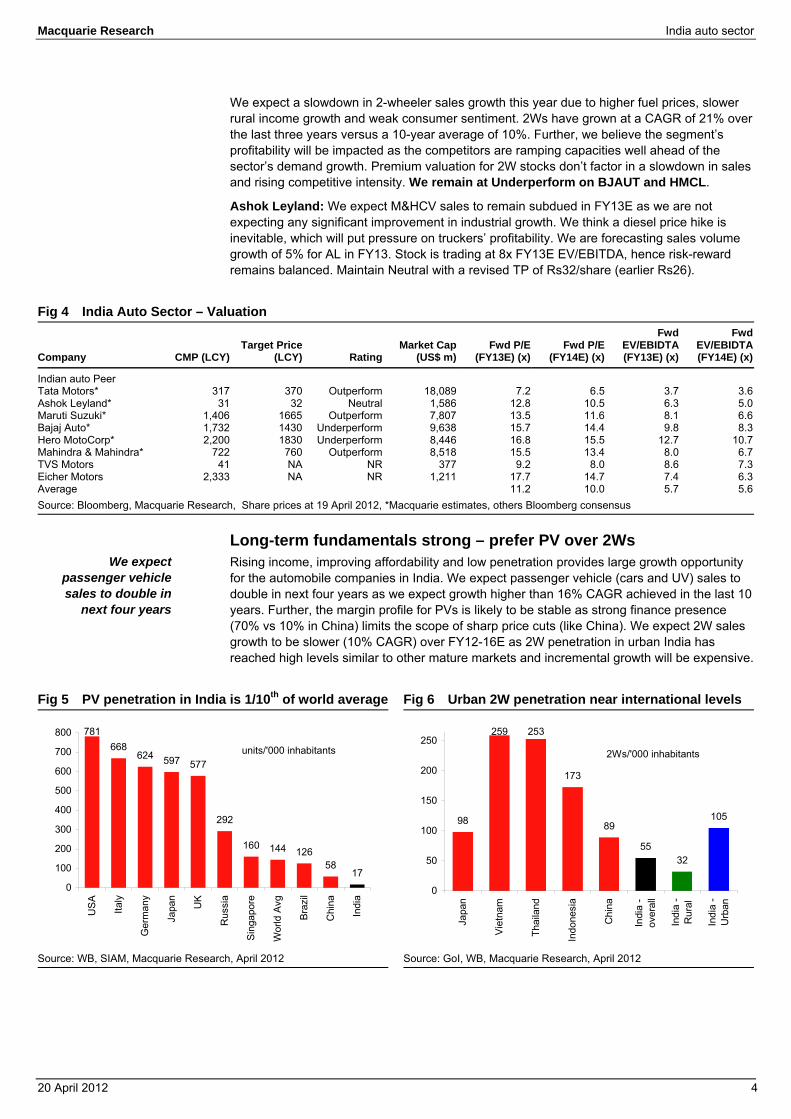

We expect a slowdown in 2-wheeler sales growth this year due to higher fuel prices, slower rural income growth and weak consumer sentiment. 2Ws have grown at a CAGR of 21% over the last three years versus a 10-year average of 10%. Further, we believe the segment’s profitability will be impacted as the competitors are ramping capacities well ahead of the sector’s demand growth. Premium valuation for 2W stocks don’t factor in a slowdown in sales and rising competitive intensity. We remain at Underperform on BJAUT and HMCL.

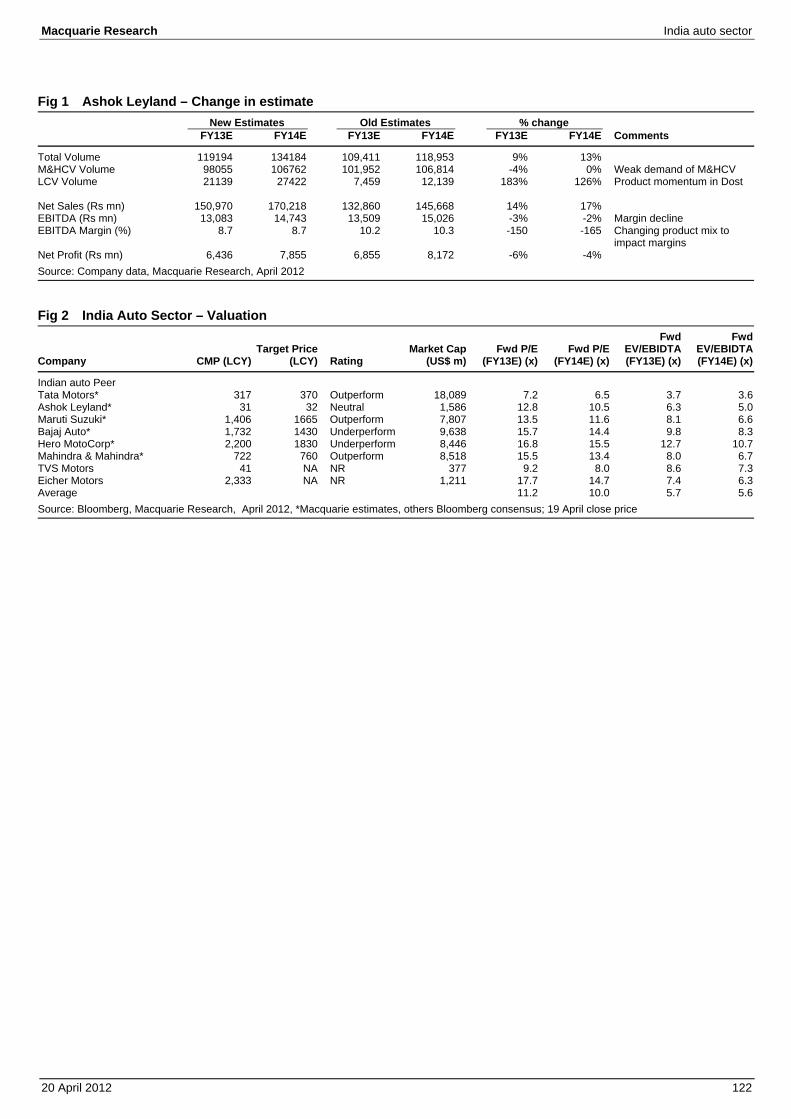

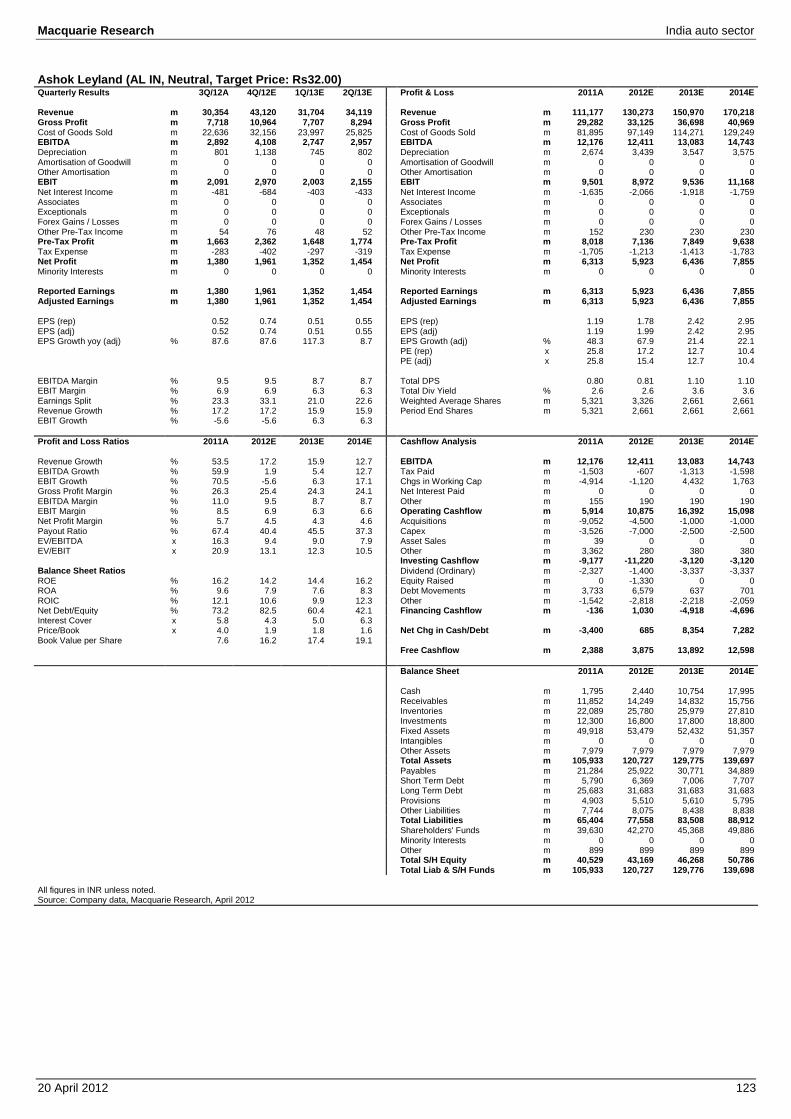

Ashok Leyland: We expect M&HCV sales to remain subdued in FY13E as we are not expecting any significant improvement in industrial growth. We think a diesel price hike is inevitable, which will put pressure on truckers’ profitability. We are forecasting sales volume growth of 5% for AL in FY13. Stock is trading at 8x FY13E EV/EBITDA, hence risk-reward remains balanced. Maintain Neutral with a revised TP of Rs32/share (earlier Rs26).

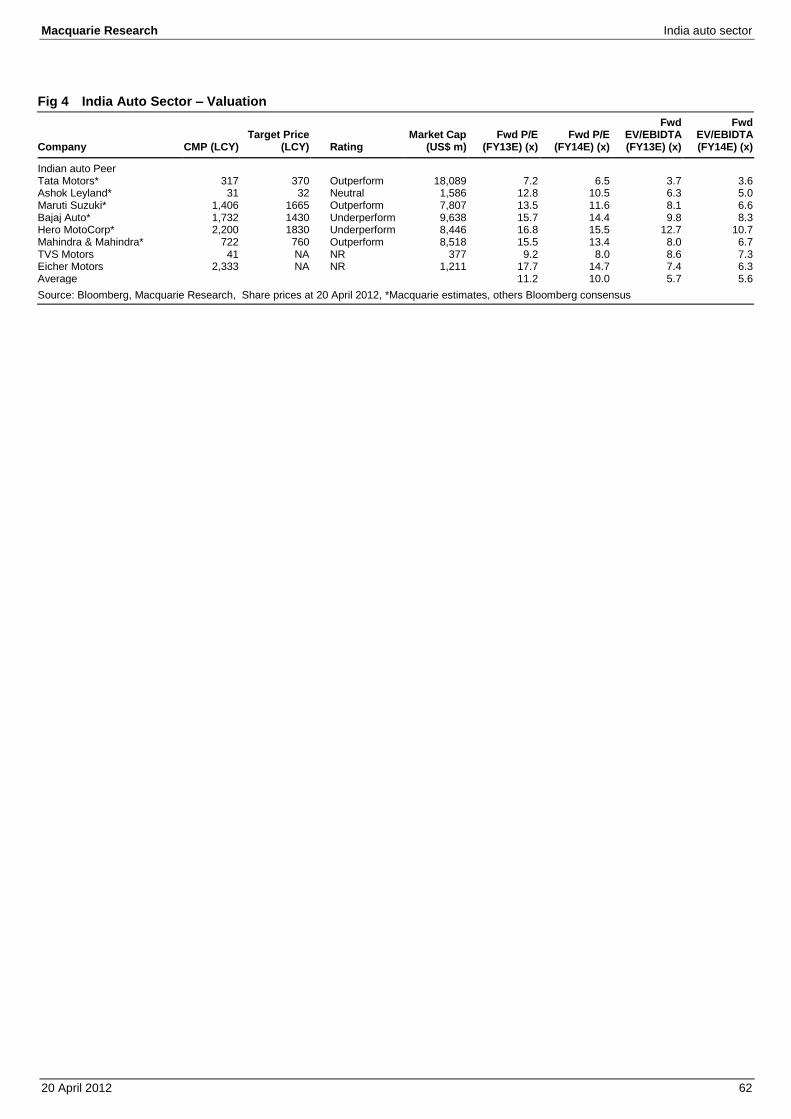

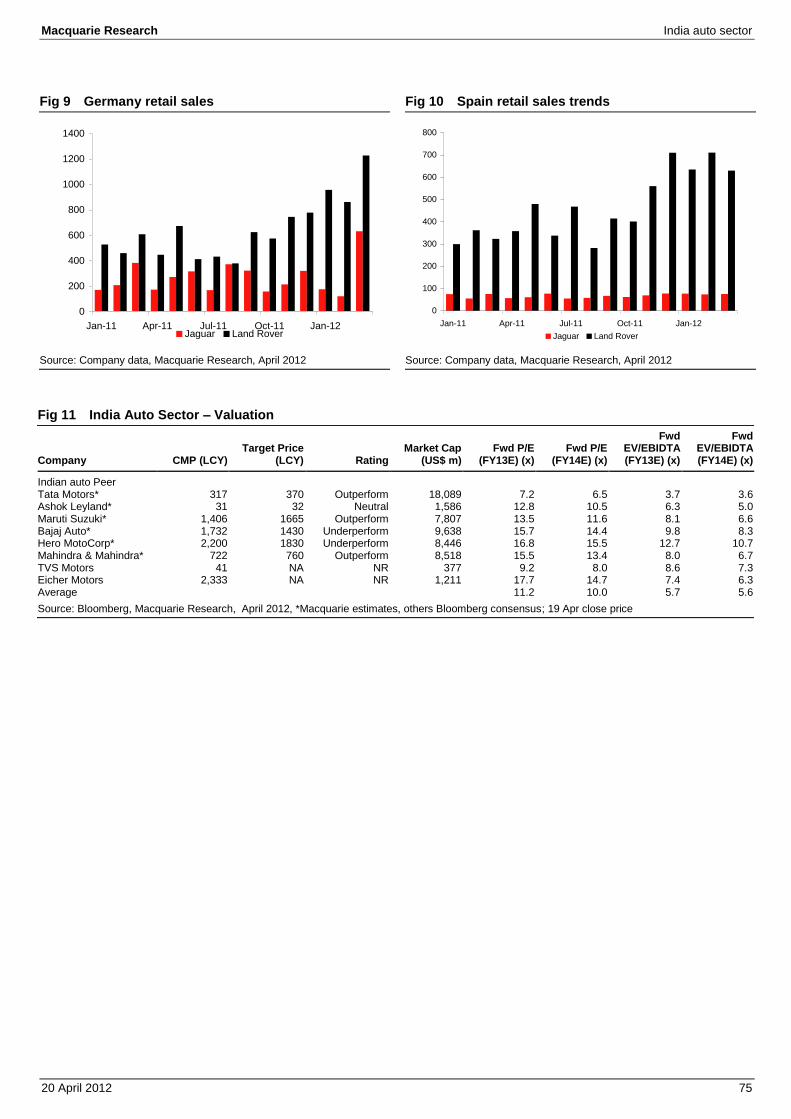

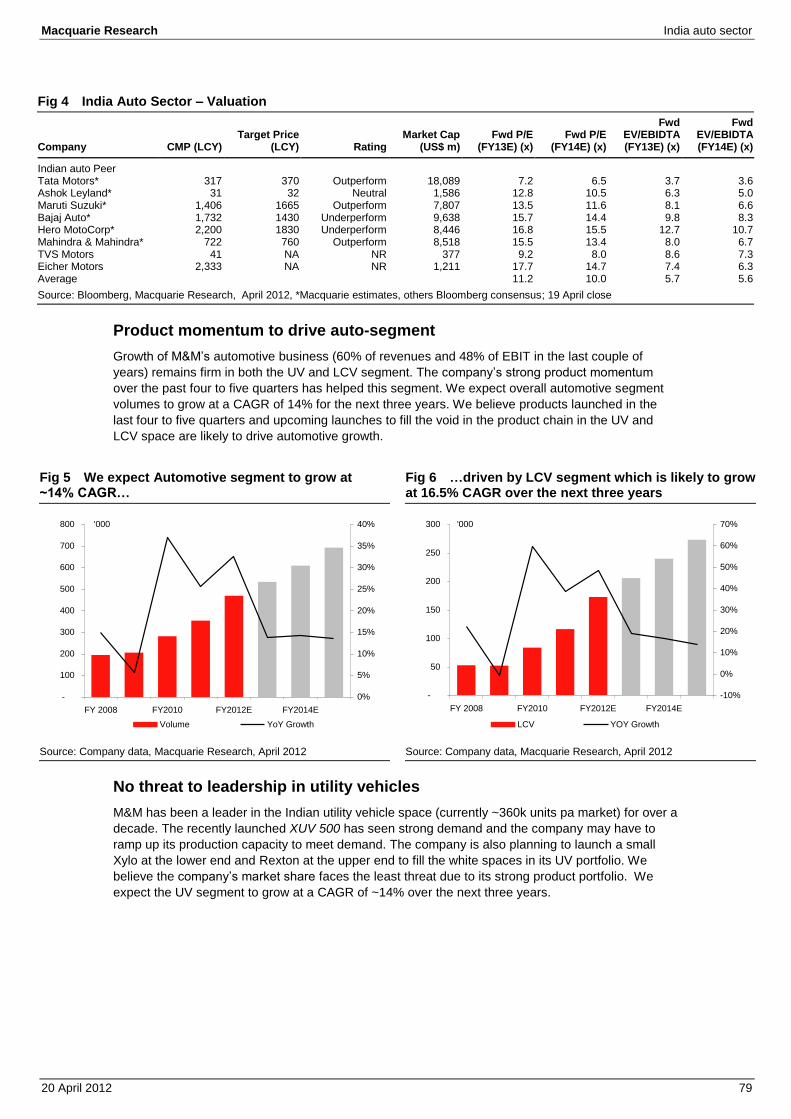

Fig 4 India Auto Sector – Valuation

Company CMP (LCY) Target Price

(LCY) RatingMarket Cap

(US$ m)Fwd P/E

(FY13E) (x)Fwd P/E

(FY14E) (x)

FwdEV/EBIDTA(FY13E) (x)

FwdEV/EBIDTA(FY14E) (x)

Indian auto Peer Tata Motors* 317 370 Outperform 18,089 7.2 6.5 3.7 3.6Ashok Leyland* 31 32 Neutral 1,586 12.8 10.5 6.3 5.0Maruti Suzuki* 1,406 1665 Outperform 7,807 13.5 11.6 8.1 6.6Bajaj Auto* 1,732 1430 Underperform 9,638 15.7 14.4 9.8 8.3Hero MotoCorp* 2,200 1830 Underperform 8,446 16.8 15.5 12.7 10.7Mahindra & Mahindra* 722 760 Outperform 8,518 15.5 13.4 8.0 6.7TVS Motors 41 NA NR 377 9.2 8.0 8.6 7.3Eicher Motors 2,333 NA NR 1,211 17.7 14.7 7.4 6.3Average 11.2 10.0 5.7 5.6Source: Bloomberg, Macquarie Research, Share prices at 19 April 2012, *Macquarie estimates, others Bloomberg consensus

Long-term fundamentals strong – prefer PV over 2Ws Rising income, improving affordability and low penetration provides large growth opportunity for the automobile companies in India. We expect passenger vehicle (cars and UV) sales to double in next four years as we expect growth higher than 16% CAGR achieved in the last 10 years. Further, the margin profile for PVs is likely to be stable as strong finance presence (70% vs 10% in China) limits the scope of sharp price cuts (like China). We expect 2W sales growth to be slower (10% CAGR) over FY12-16E as 2W penetration in urban India has reached high levels similar to other mature markets and incremental growth will be expensive.

Fig 5 PV penetration in India is 1/10th of world average Fig 6 Urban 2W penetration near international levels

Source: WB, SIAM, Macquarie Research, April 2012 Source: GoI, WB, Macquarie Research, April 2012

781668

624 597 577

292

160 144 12658

170

100

200

300

400

500

600

700

800

US

A

Italy

Ger

man

y

Japa

n

UK

Rus

sia

Sin

gapo

re

Wor

ld A

vg

Bra

zil

Chi

na

Indi

a

units/'000 inhabitants

98

259 253

173

89

5532

105

0

50

100

150

200

250

Japa

n

Vie

tnam

Thai

land

Indo

nesi

a

Chi

na

Indi

a -

over

all

Indi

a -

Rur

al

Indi

a -

Urb

an

2Ws/'000 inhabitants

We expect passenger vehicle sales to double in

next four years

Macquarie Research India auto sector

20 April 2012 5

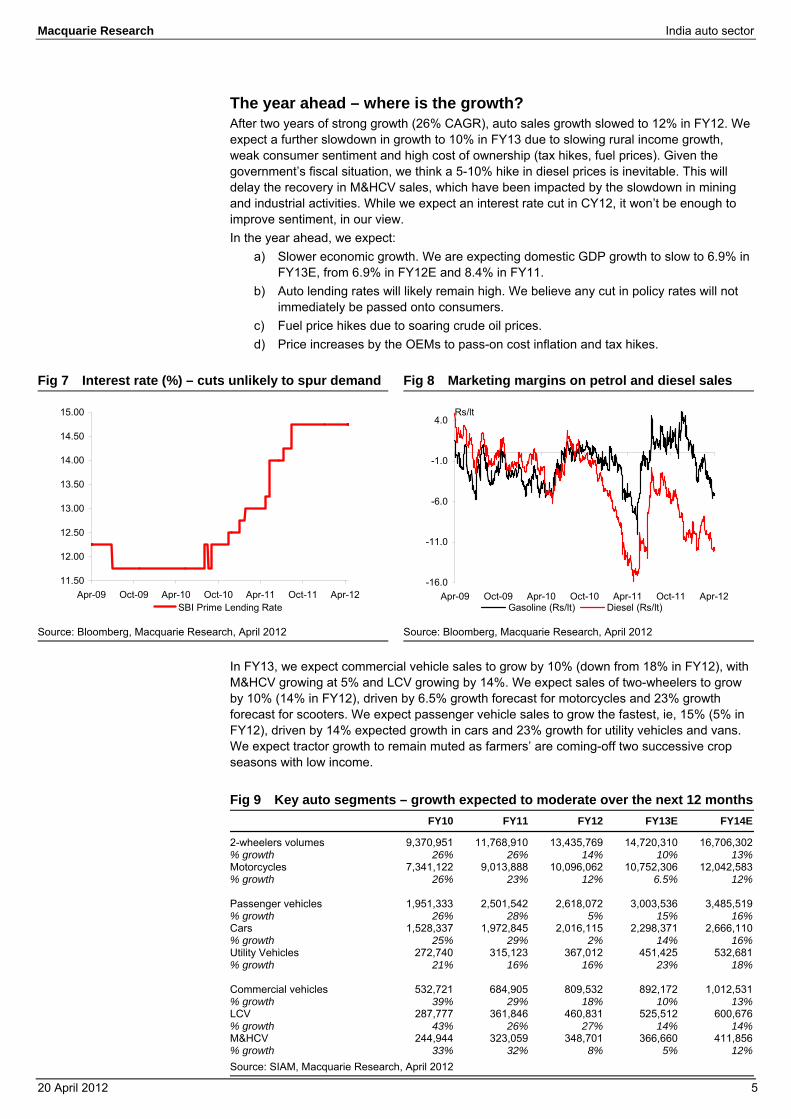

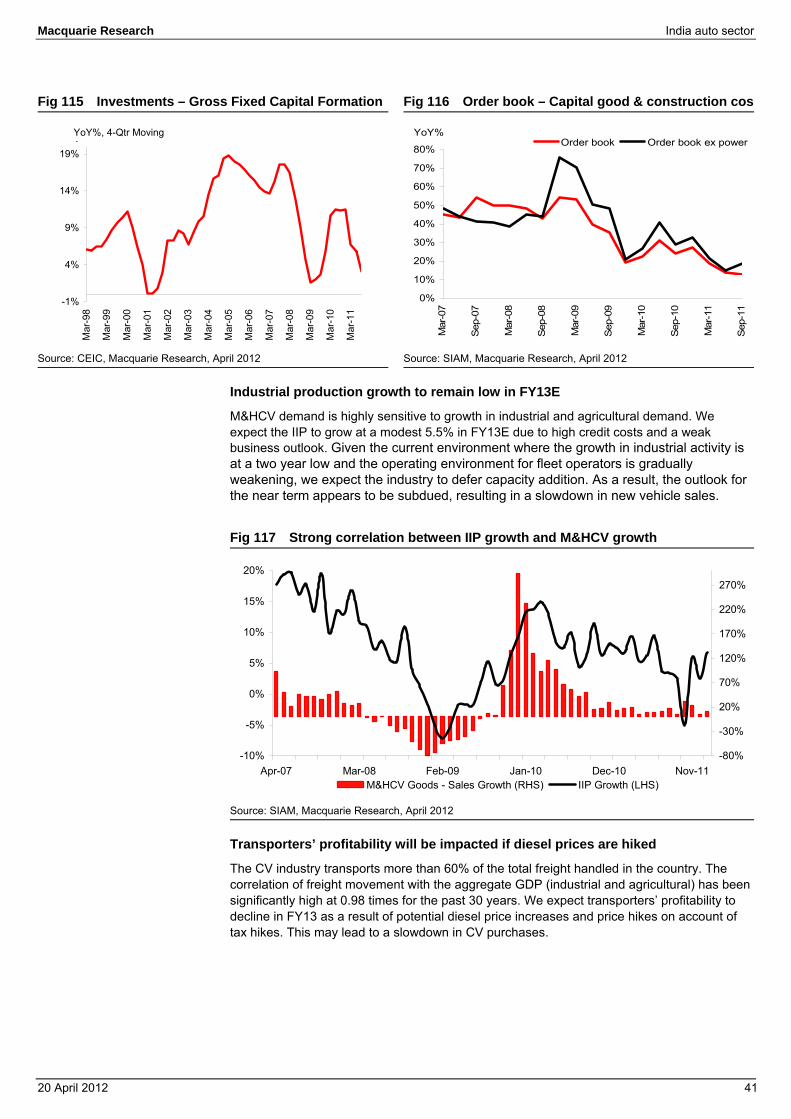

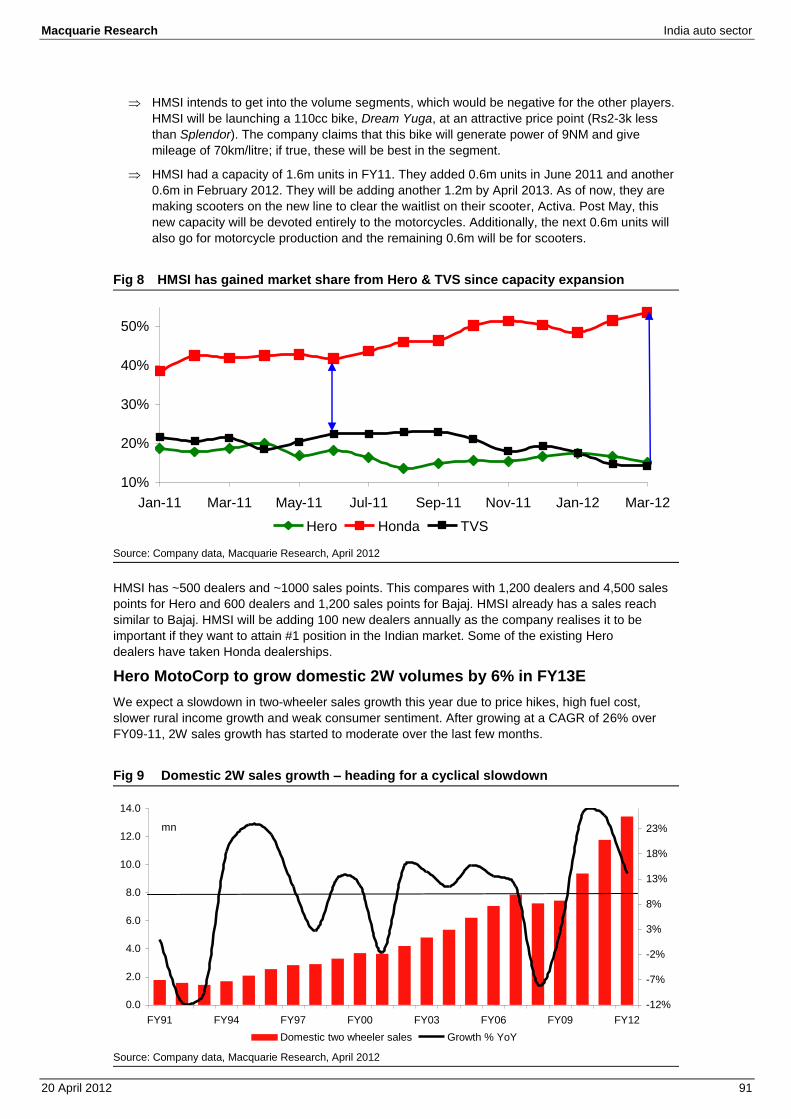

The year ahead – where is the growth? After two years of strong growth (26% CAGR), auto sales growth slowed to 12% in FY12. We expect a further slowdown in growth to 10% in FY13 due to slowing rural income growth, weak consumer sentiment and high cost of ownership (tax hikes, fuel prices). Given the government’s fiscal situation, we think a 5-10% hike in diesel prices is inevitable. This will delay the recovery in M&HCV sales, which have been impacted by the slowdown in mining and industrial activities. While we expect an interest rate cut in CY12, it won’t be enough to improve sentiment, in our view. In the year ahead, we expect:

a) Slower economic growth. We are expecting domestic GDP growth to slow to 6.9% in FY13E, from 6.9% in FY12E and 8.4% in FY11.

b) Auto lending rates will likely remain high. We believe any cut in policy rates will not immediately be passed onto consumers.

c) Fuel price hikes due to soaring crude oil prices. d) Price increases by the OEMs to pass-on cost inflation and tax hikes.

Fig 7 Interest rate (%) – cuts unlikely to spur demand Fig 8 Marketing margins on petrol and diesel sales

Source: Bloomberg, Macquarie Research, April 2012 Source: Bloomberg, Macquarie Research, April 2012

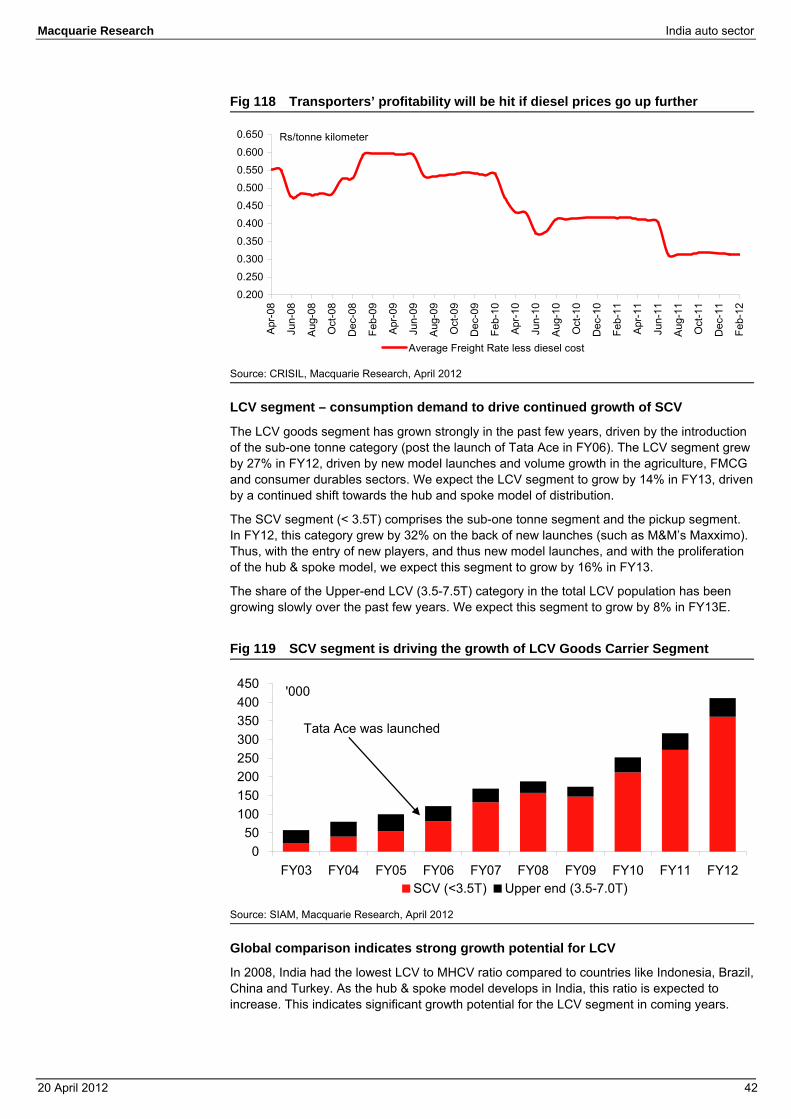

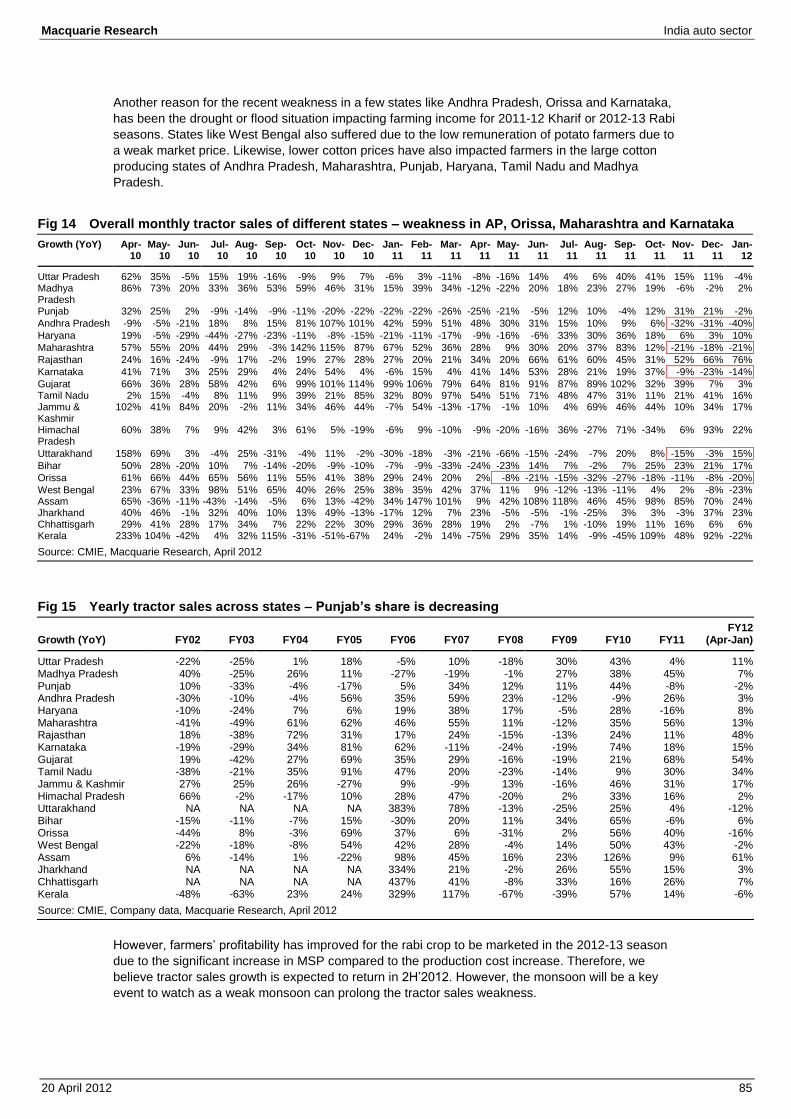

In FY13, we expect commercial vehicle sales to grow by 10% (down from 18% in FY12), with M&HCV growing at 5% and LCV growing by 14%. We expect sales of two-wheelers to grow by 10% (14% in FY12), driven by 6.5% growth forecast for motorcycles and 23% growth forecast for scooters. We expect passenger vehicle sales to grow the fastest, ie, 15% (5% in FY12), driven by 14% expected growth in cars and 23% growth for utility vehicles and vans. We expect tractor growth to remain muted as farmers’ are coming-off two successive crop seasons with low income.

Fig 9 Key auto segments – growth expected to moderate over the next 12 months FY10 FY11 FY12 FY13E FY14E

2-wheelers volumes 9,370,951 11,768,910 13,435,769 14,720,310 16,706,302% growth 26% 26% 14% 10% 13%Motorcycles 7,341,122 9,013,888 10,096,062 10,752,306 12,042,583% growth 26% 23% 12% 6.5% 12% Passenger vehicles 1,951,333 2,501,542 2,618,072 3,003,536 3,485,519% growth 26% 28% 5% 15% 16%Cars 1,528,337 1,972,845 2,016,115 2,298,371 2,666,110% growth 25% 29% 2% 14% 16%Utility Vehicles 272,740 315,123 367,012 451,425 532,681% growth 21% 16% 16% 23% 18% Commercial vehicles 532,721 684,905 809,532 892,172 1,012,531% growth 39% 29% 18% 10% 13%LCV 287,777 361,846 460,831 525,512 600,676% growth 43% 26% 27% 14% 14%M&HCV 244,944 323,059 348,701 366,660 411,856% growth 33% 32% 8% 5% 12%Source: SIAM, Macquarie Research, April 2012

11.50

12.00

12.50

13.00

13.50

14.00

14.50

15.00

Apr-09 Oct-09 Apr-10 Oct-10 Apr-11 Oct-11 Apr-12SBI Prime Lending Rate

-16.0

-11.0

-6.0

-1.0

4.0

Apr-09 Oct-09 Apr-10 Oct-10 Apr-11 Oct-11 Apr-12

Rs/lt

Gasoline (Rs/lt) Diesel (Rs/lt)

Macquarie Research India auto sector

20 April 2012 6

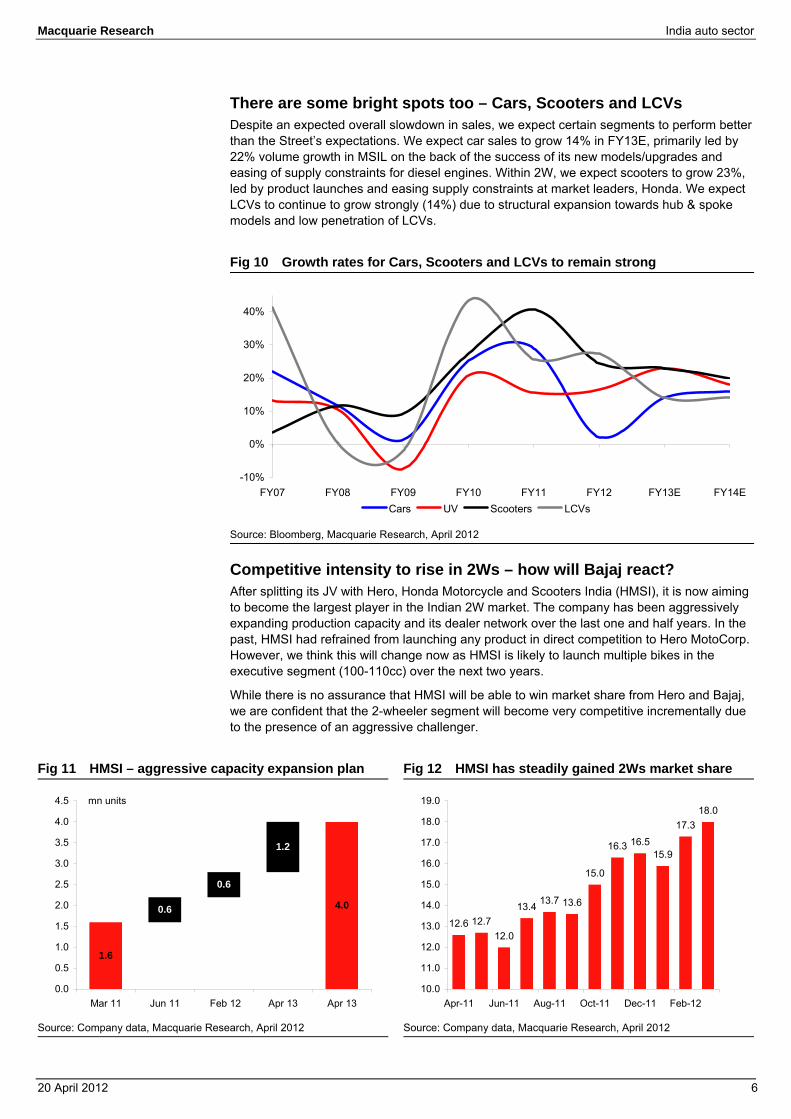

There are some bright spots too – Cars, Scooters and LCVs Despite an expected overall slowdown in sales, we expect certain segments to perform better than the Street’s expectations. We expect car sales to grow 14% in FY13E, primarily led by 22% volume growth in MSIL on the back of the success of its new models/upgrades and easing of supply constraints for diesel engines. Within 2W, we expect scooters to grow 23%, led by product launches and easing supply constraints at market leaders, Honda. We expect LCVs to continue to grow strongly (14%) due to structural expansion towards hub & spoke models and low penetration of LCVs.

Fig 10 Growth rates for Cars, Scooters and LCVs to remain strong

Source: Bloomberg, Macquarie Research, April 2012

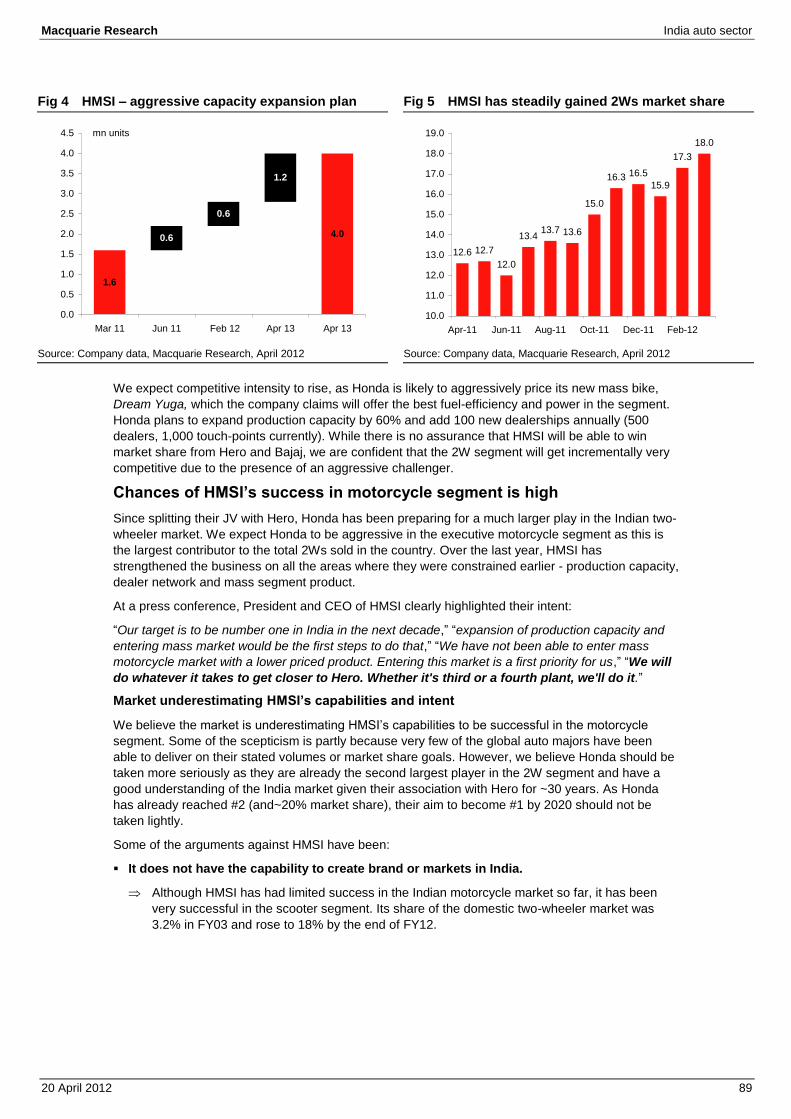

Competitive intensity to rise in 2Ws – how will Bajaj react? After splitting its JV with Hero, Honda Motorcycle and Scooters India (HMSI), it is now aiming to become the largest player in the Indian 2W market. The company has been aggressively expanding production capacity and its dealer network over the last one and half years. In the past, HMSI had refrained from launching any product in direct competition to Hero MotoCorp. However, we think this will change now as HMSI is likely to launch multiple bikes in the executive segment (100-110cc) over the next two years.

While there is no assurance that HMSI will be able to win market share from Hero and Bajaj, we are confident that the 2-wheeler segment will become very competitive incrementally due to the presence of an aggressive challenger.

Fig 11 HMSI – aggressive capacity expansion plan Fig 12 HMSI has steadily gained 2Ws market share

Source: Company data, Macquarie Research, April 2012 Source: Company data, Macquarie Research, April 2012

-10%

0%

10%

20%

30%

40%

FY07 FY08 FY09 FY10 FY11 FY12 FY13E FY14ECars UV Scooters LCVs

1.6

4.00.6

0.6

1.2

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Mar 11 Jun 11 Feb 12 Apr 13 Apr 13

mn units

12.6 12.712.0

13.4 13.7 13.6

15.0

16.3 16.515.9

17.318.0

10.0

11.0

12.0

13.0

14.0

15.0

16.0

17.0

18.0

19.0

Apr-11 Jun-11 Aug-11 Oct-11 Dec-11 Feb-12

Macquarie Research India auto sector

20 April 2012 7

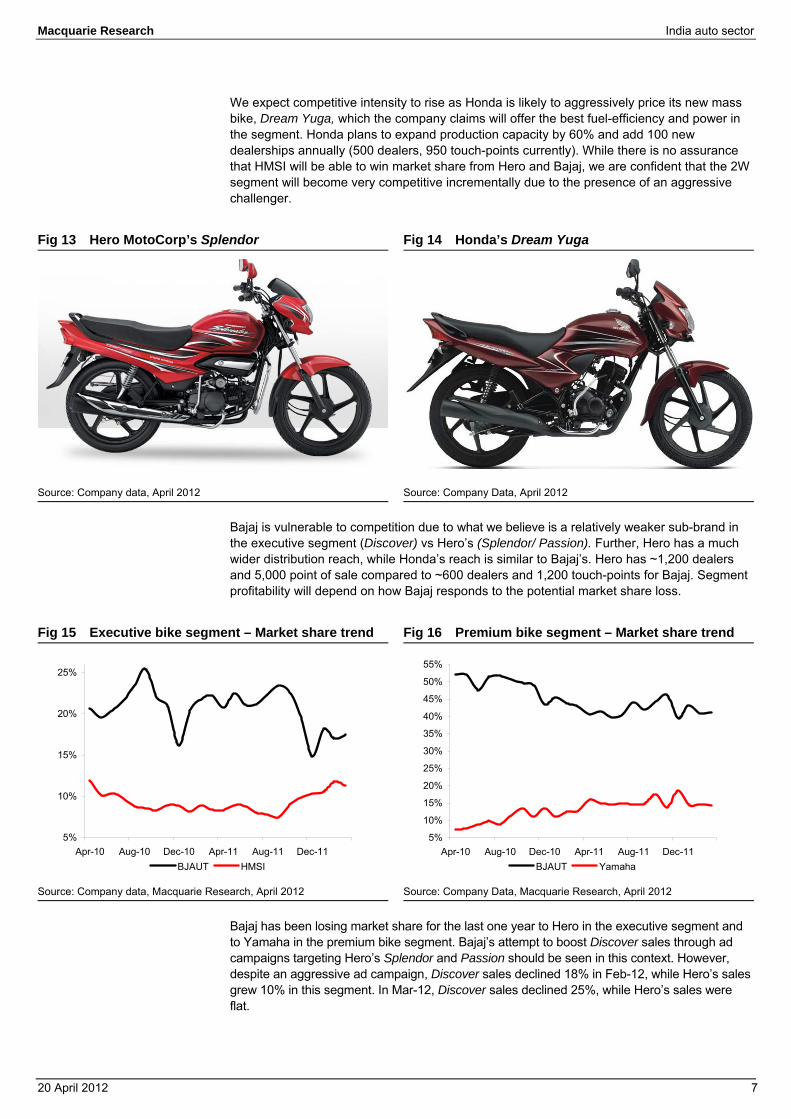

We expect competitive intensity to rise as Honda is likely to aggressively price its new mass bike, Dream Yuga, which the company claims will offer the best fuel-efficiency and power in the segment. Honda plans to expand production capacity by 60% and add 100 new dealerships annually (500 dealers, 950 touch-points currently). While there is no assurance that HMSI will be able to win market share from Hero and Bajaj, we are confident that the 2W segment will become very competitive incrementally due to the presence of an aggressive challenger.

Fig 13 Hero MotoCorp’s Splendor Fig 14 Honda’s Dream Yuga

Source: Company data, April 2012 Source: Company Data, April 2012

Bajaj is vulnerable to competition due to what we believe is a relatively weaker sub-brand in the executive segment (Discover) vs Hero’s (Splendor/ Passion). Further, Hero has a much wider distribution reach, while Honda’s reach is similar to Bajaj’s. Hero has ~1,200 dealers and 5,000 point of sale compared to ~600 dealers and 1,200 touch-points for Bajaj. Segment profitability will depend on how Bajaj responds to the potential market share loss.

Fig 15 Executive bike segment – Market share trend Fig 16 Premium bike segment – Market share trend

Source: Company data, Macquarie Research, April 2012 Source: Company Data, Macquarie Research, April 2012

Bajaj has been losing market share for the last one year to Hero in the executive segment and to Yamaha in the premium bike segment. Bajaj’s attempt to boost Discover sales through ad campaigns targeting Hero’s Splendor and Passion should be seen in this context. However, despite an aggressive ad campaign, Discover sales declined 18% in Feb-12, while Hero’s sales grew 10% in this segment. In Mar-12, Discover sales declined 25%, while Hero’s sales were flat.

5%

10%

15%

20%

25%

Apr-10 Aug-10 Dec-10 Apr-11 Aug-11 Dec-11BJAUT HMSI

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

Apr-10 Aug-10 Dec-10 Apr-11 Aug-11 Dec-11BJAUT Yamaha

Macquarie Research India auto sector

20 April 2012 8

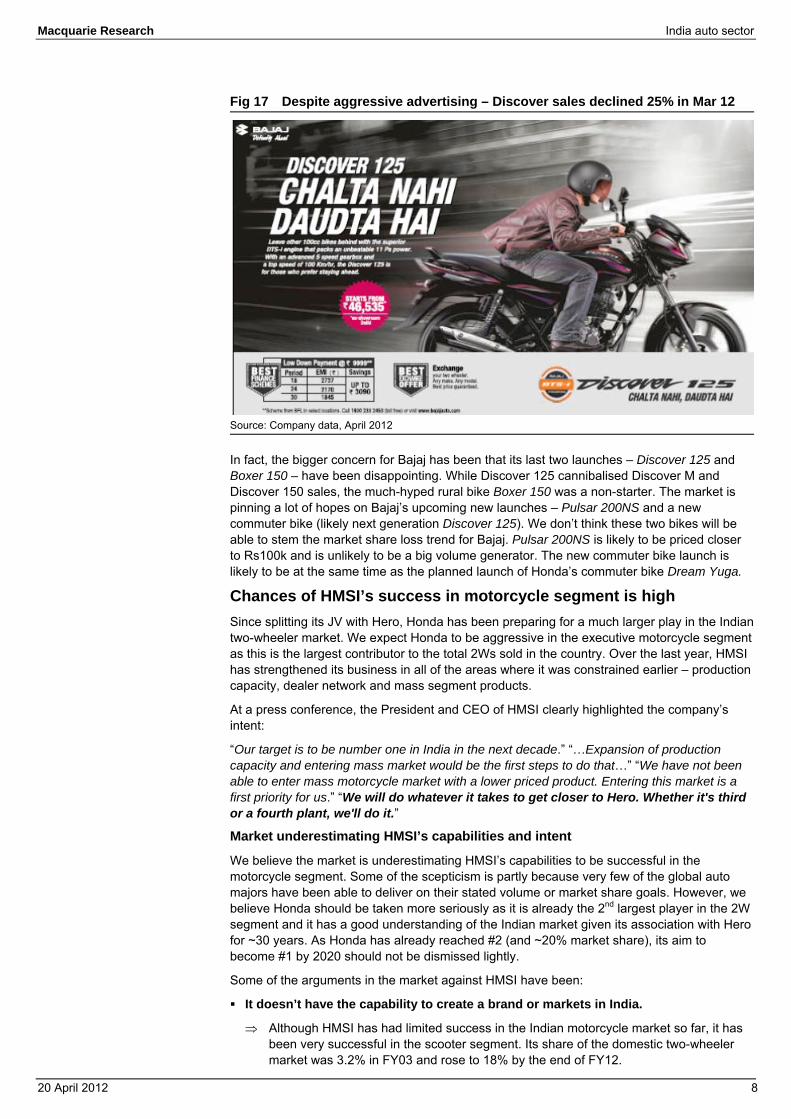

Fig 17 Despite aggressive advertising – Discover sales declined 25% in Mar 12

Source: Company data, April 2012

In fact, the bigger concern for Bajaj has been that its last two launches – Discover 125 and Boxer 150 – have been disappointing. While Discover 125 cannibalised Discover M and Discover 150 sales, the much-hyped rural bike Boxer 150 was a non-starter. The market is pinning a lot of hopes on Bajaj’s upcoming new launches – Pulsar 200NS and a new commuter bike (likely next generation Discover 125). We don’t think these two bikes will be able to stem the market share loss trend for Bajaj. Pulsar 200NS is likely to be priced closer to Rs100k and is unlikely to be a big volume generator. The new commuter bike launch is likely to be at the same time as the planned launch of Honda’s commuter bike Dream Yuga.

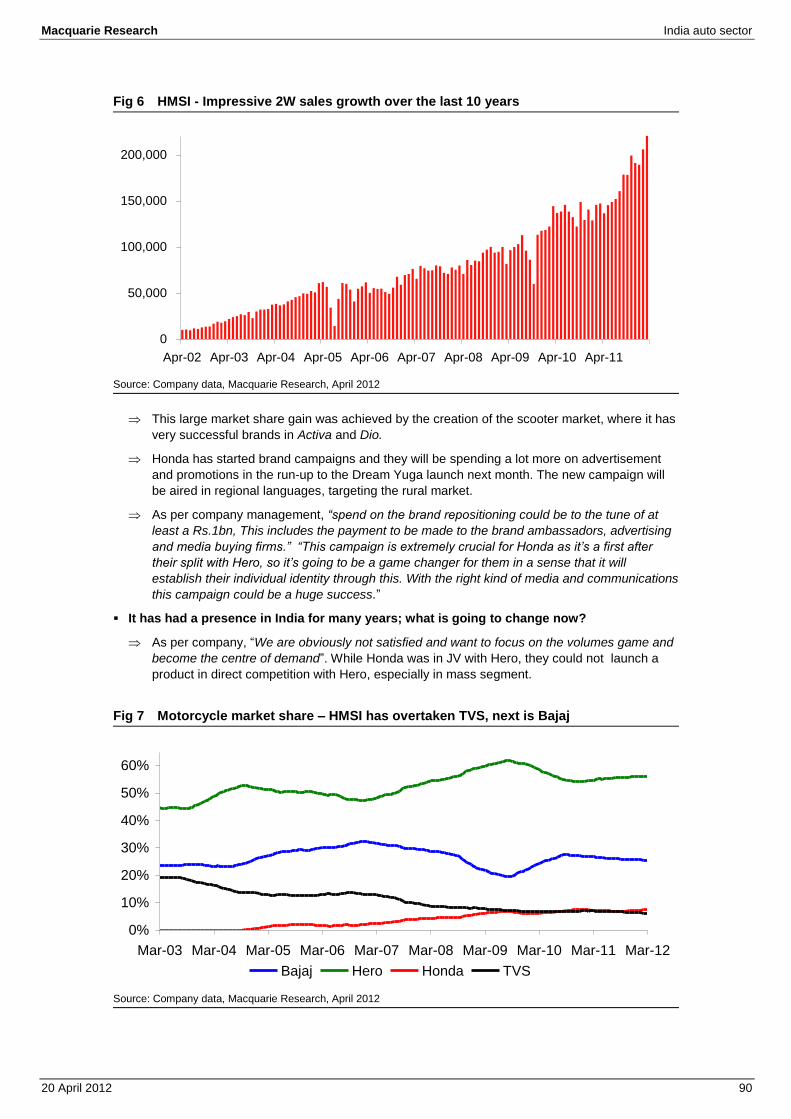

Chances of HMSI’s success in motorcycle segment is high Since splitting its JV with Hero, Honda has been preparing for a much larger play in the Indian two-wheeler market. We expect Honda to be aggressive in the executive motorcycle segment as this is the largest contributor to the total 2Ws sold in the country. Over the last year, HMSI has strengthened its business in all of the areas where it was constrained earlier – production capacity, dealer network and mass segment products.

At a press conference, the President and CEO of HMSI clearly highlighted the company’s intent:

“Our target is to be number one in India in the next decade.” “…Expansion of production capacity and entering mass market would be the first steps to do that…” “We have not been able to enter mass motorcycle market with a lower priced product. Entering this market is a first priority for us.” “We will do whatever it takes to get closer to Hero. Whether it's third or a fourth plant, we'll do it.”

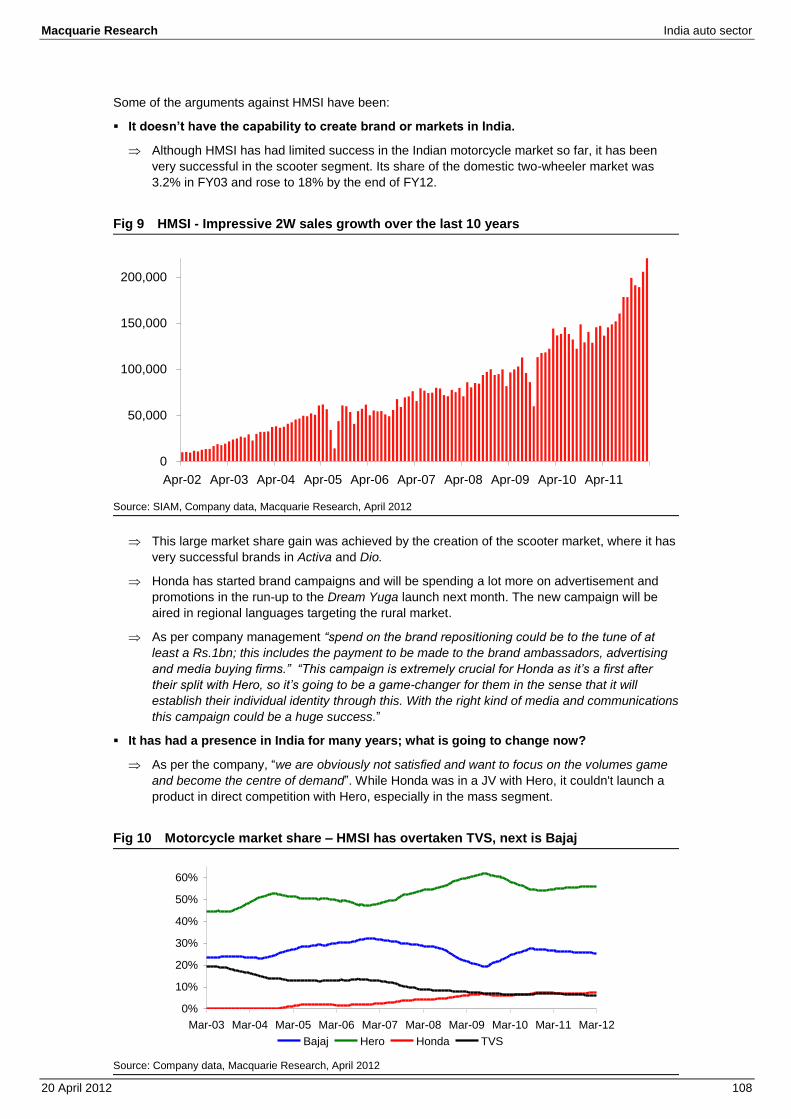

Market underestimating HMSI’s capabilities and intent

We believe the market is underestimating HMSI’s capabilities to be successful in the motorcycle segment. Some of the scepticism is partly because very few of the global auto majors have been able to deliver on their stated volume or market share goals. However, we believe Honda should be taken more seriously as it is already the 2nd largest player in the 2W segment and it has a good understanding of the Indian market given its association with Hero for ~30 years. As Honda has already reached #2 (and ~20% market share), its aim to become #1 by 2020 should not be dismissed lightly.

Some of the arguments in the market against HMSI have been:

It doesn’t have the capability to create a brand or markets in India.

⇒ Although HMSI has had limited success in the Indian motorcycle market so far, it has been very successful in the scooter segment. Its share of the domestic two-wheeler market was 3.2% in FY03 and rose to 18% by the end of FY12.

Macquarie Research India auto sector

20 April 2012 9

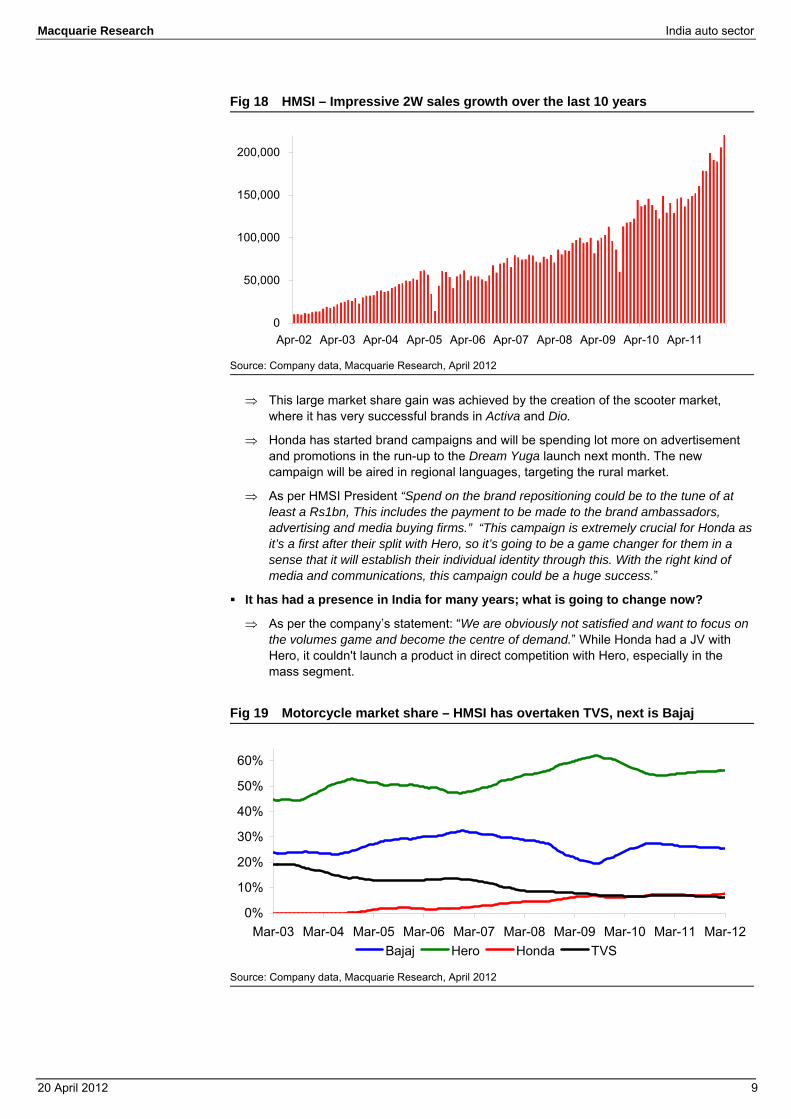

Fig 18 HMSI – Impressive 2W sales growth over the last 10 years

Source: Company data, Macquarie Research, April 2012

⇒ This large market share gain was achieved by the creation of the scooter market, where it has very successful brands in Activa and Dio.

⇒ Honda has started brand campaigns and will be spending lot more on advertisement and promotions in the run-up to the Dream Yuga launch next month. The new campaign will be aired in regional languages, targeting the rural market.

⇒ As per HMSI President “Spend on the brand repositioning could be to the tune of at least a Rs1bn, This includes the payment to be made to the brand ambassadors, advertising and media buying firms.” “This campaign is extremely crucial for Honda as it’s a first after their split with Hero, so it’s going to be a game changer for them in a sense that it will establish their individual identity through this. With the right kind of media and communications, this campaign could be a huge success.”

It has had a presence in India for many years; what is going to change now?

⇒ As per the company’s statement: “We are obviously not satisfied and want to focus on the volumes game and become the centre of demand.” While Honda had a JV with Hero, it couldn't launch a product in direct competition with Hero, especially in the mass segment.

Fig 19 Motorcycle market share – HMSI has overtaken TVS, next is Bajaj

Source: Company data, Macquarie Research, April 2012

0

50,000

100,000

150,000

200,000

Apr-02 Apr-03 Apr-04 Apr-05 Apr-06 Apr-07 Apr-08 Apr-09 Apr-10 Apr-11

0%

10%

20%

30%

40%

50%

60%

Mar-03 Mar-04 Mar-05 Mar-06 Mar-07 Mar-08 Mar-09 Mar-10 Mar-11 Mar-12Bajaj Hero Honda TVS

Macquarie Research India auto sector

20 April 2012 10

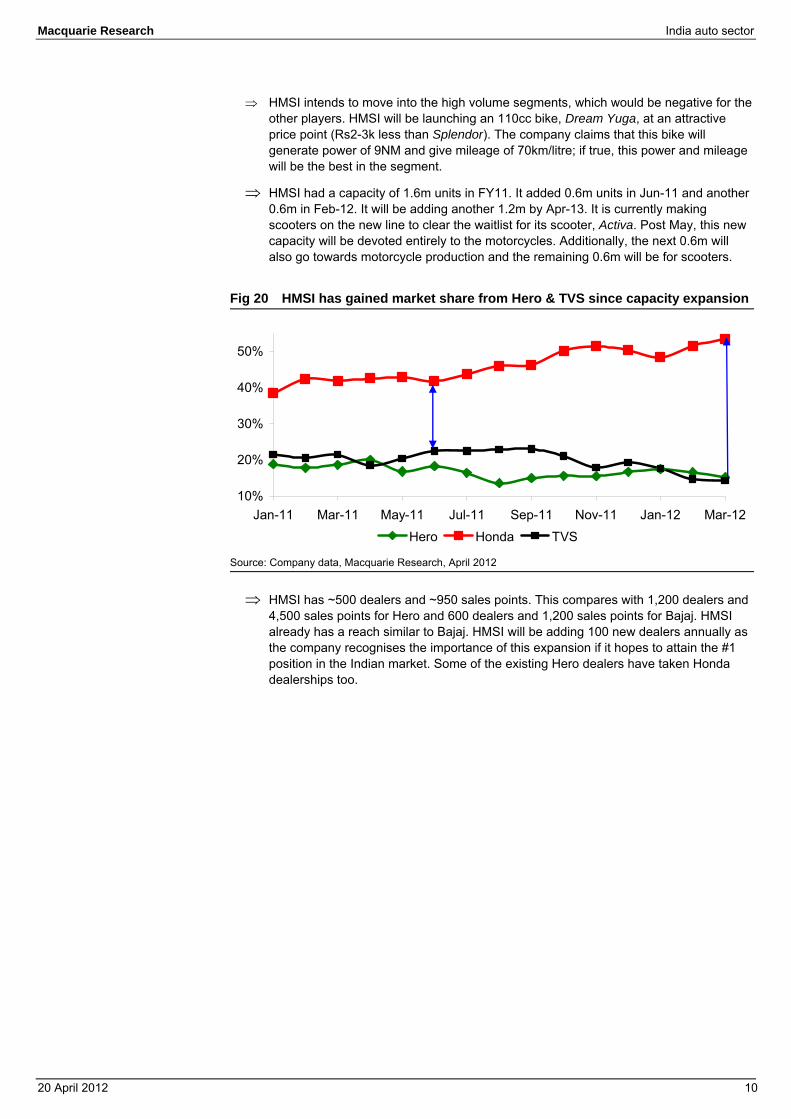

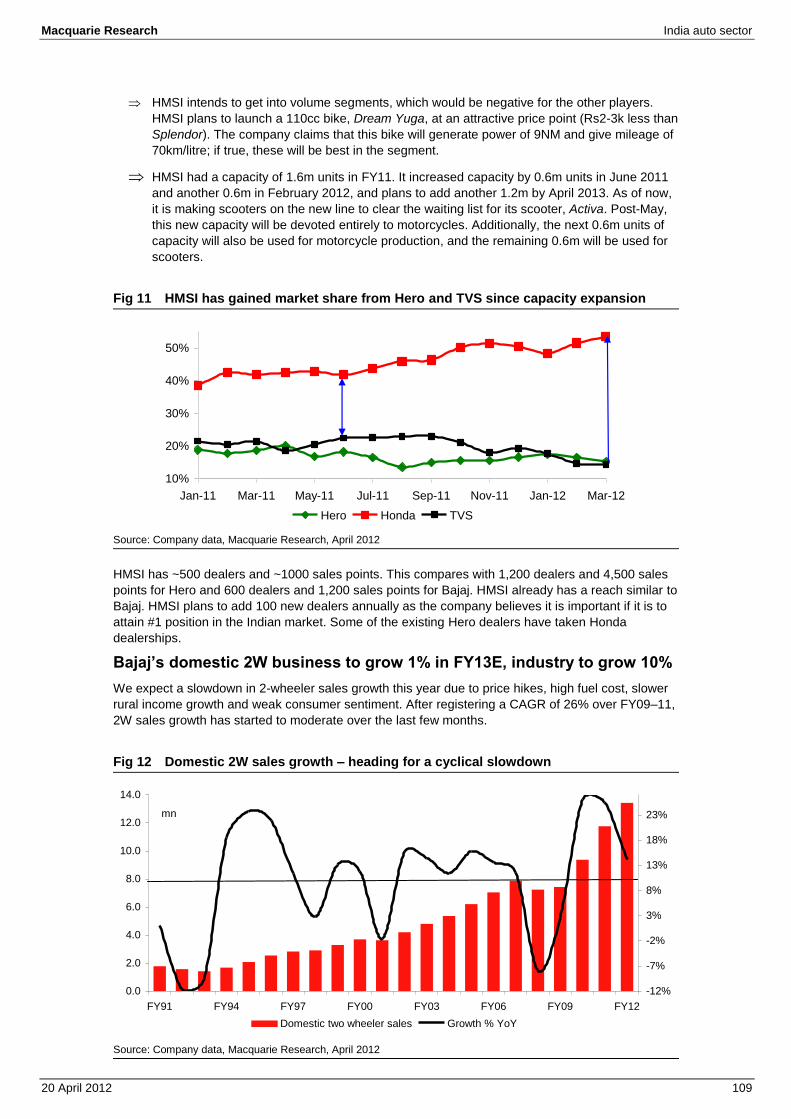

⇒ HMSI intends to move into the high volume segments, which would be negative for the other players. HMSI will be launching an 110cc bike, Dream Yuga, at an attractive price point (Rs2-3k less than Splendor). The company claims that this bike will generate power of 9NM and give mileage of 70km/litre; if true, this power and mileage will be the best in the segment.

⇒ HMSI had a capacity of 1.6m units in FY11. It added 0.6m units in Jun-11 and another 0.6m in Feb-12. It will be adding another 1.2m by Apr-13. It is currently making scooters on the new line to clear the waitlist for its scooter, Activa. Post May, this new capacity will be devoted entirely to the motorcycles. Additionally, the next 0.6m will also go towards motorcycle production and the remaining 0.6m will be for scooters.

Fig 20 HMSI has gained market share from Hero & TVS since capacity expansion

Source: Company data, Macquarie Research, April 2012

⇒ HMSI has ~500 dealers and ~950 sales points. This compares with 1,200 dealers and 4,500 sales points for Hero and 600 dealers and 1,200 sales points for Bajaj. HMSI already has a reach similar to Bajaj. HMSI will be adding 100 new dealers annually as the company recognises the importance of this expansion if it hopes to attain the #1 position in the Indian market. Some of the existing Hero dealers have taken Honda dealerships too.

10%

20%

30%

40%

50%

Jan-11 Mar-11 May-11 Jul-11 Sep-11 Nov-11 Jan-12 Mar-12

Hero Honda TVS

Macquarie Research India auto sector

20 April 2012 11

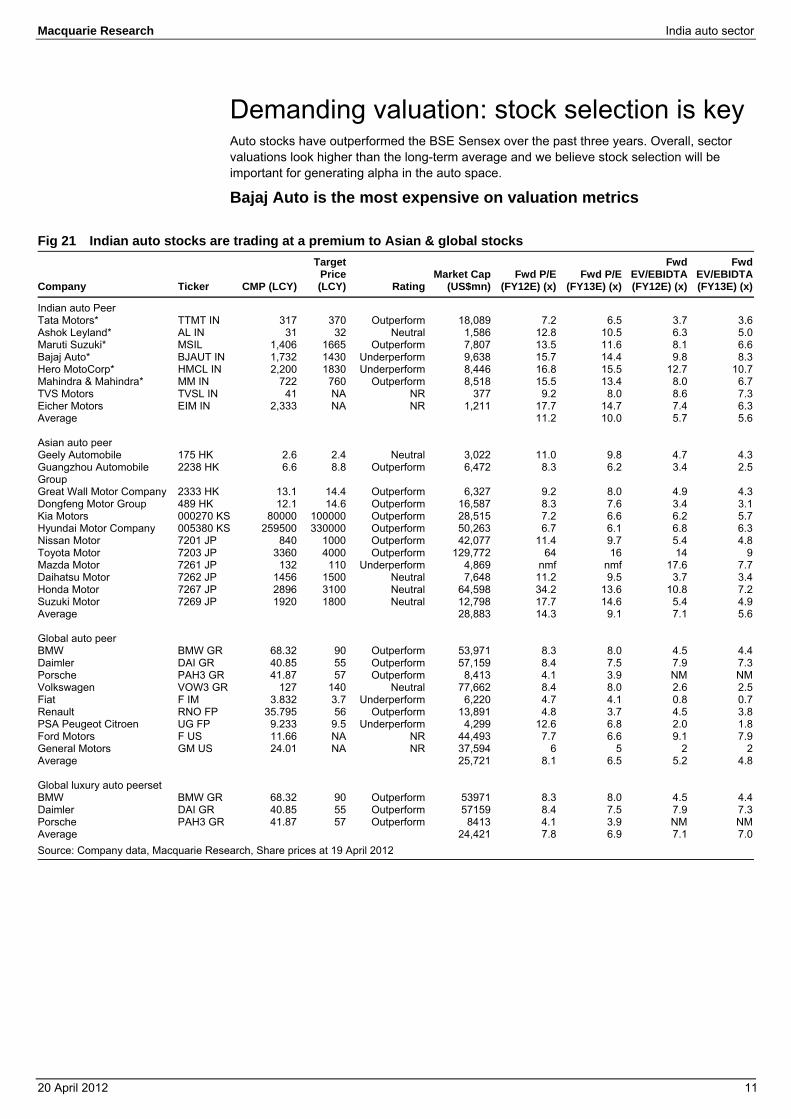

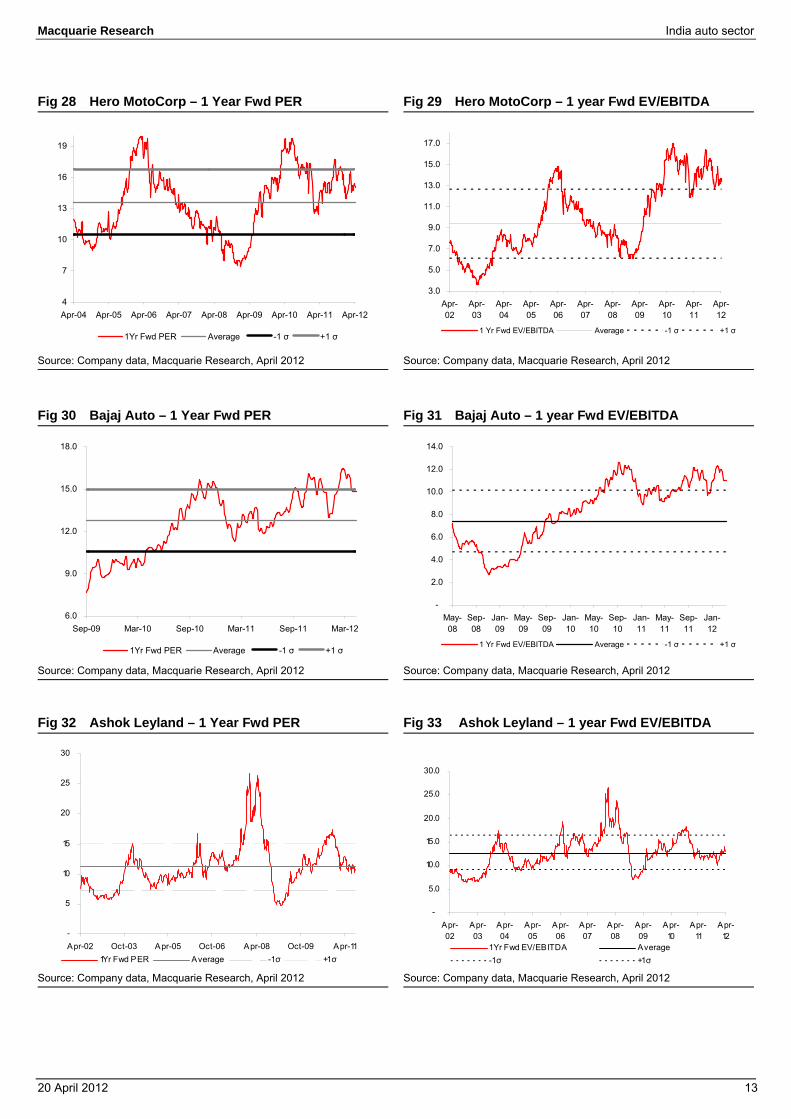

Demanding valuation: stock selection is key Auto stocks have outperformed the BSE Sensex over the past three years. Overall, sector valuations look higher than the long-term average and we believe stock selection will be important for generating alpha in the auto space.

Bajaj Auto is the most expensive on valuation metrics

Fig 21 Indian auto stocks are trading at a premium to Asian & global stocks

Company Ticker CMP (LCY)

Target Price (LCY) Rating

Market Cap (US$mn)

Fwd P/E (FY12E) (x)

Fwd P/E (FY13E) (x)

Fwd EV/EBIDTA (FY12E) (x)

Fwd EV/EBIDTA (FY13E) (x)

Indian auto Peer Tata Motors* TTMT IN 317 370 Outperform 18,089 7.2 6.5 3.7 3.6Ashok Leyland* AL IN 31 32 Neutral 1,586 12.8 10.5 6.3 5.0Maruti Suzuki* MSIL 1,406 1665 Outperform 7,807 13.5 11.6 8.1 6.6Bajaj Auto* BJAUT IN 1,732 1430 Underperform 9,638 15.7 14.4 9.8 8.3Hero MotoCorp* HMCL IN 2,200 1830 Underperform 8,446 16.8 15.5 12.7 10.7Mahindra & Mahindra* MM IN 722 760 Outperform 8,518 15.5 13.4 8.0 6.7TVS Motors TVSL IN 41 NA NR 377 9.2 8.0 8.6 7.3Eicher Motors EIM IN 2,333 NA NR 1,211 17.7 14.7 7.4 6.3Average 11.2 10.0 5.7 5.6 Asian auto peer Geely Automobile 175 HK 2.6 2.4 Neutral 3,022 11.0 9.8 4.7 4.3Guangzhou Automobile Group

2238 HK 6.6 8.8 Outperform 6,472 8.3 6.2 3.4 2.5

Great Wall Motor Company 2333 HK 13.1 14.4 Outperform 6,327 9.2 8.0 4.9 4.3Dongfeng Motor Group 489 HK 12.1 14.6 Outperform 16,587 8.3 7.6 3.4 3.1Kia Motors 000270 KS 80000 100000 Outperform 28,515 7.2 6.6 6.2 5.7Hyundai Motor Company 005380 KS 259500 330000 Outperform 50,263 6.7 6.1 6.8 6.3Nissan Motor 7201 JP 840 1000 Outperform 42,077 11.4 9.7 5.4 4.8Toyota Motor 7203 JP 3360 4000 Outperform 129,772 64 16 14 9Mazda Motor 7261 JP 132 110 Underperform 4,869 nmf nmf 17.6 7.7Daihatsu Motor 7262 JP 1456 1500 Neutral 7,648 11.2 9.5 3.7 3.4Honda Motor 7267 JP 2896 3100 Neutral 64,598 34.2 13.6 10.8 7.2Suzuki Motor 7269 JP 1920 1800 Neutral 12,798 17.7 14.6 5.4 4.9Average 28,883 14.3 9.1 7.1 5.6 Global auto peer BMW BMW GR 68.32 90 Outperform 53,971 8.3 8.0 4.5 4.4Daimler DAI GR 40.85 55 Outperform 57,159 8.4 7.5 7.9 7.3Porsche PAH3 GR 41.87 57 Outperform 8,413 4.1 3.9 NM NMVolkswagen VOW3 GR 127 140 Neutral 77,662 8.4 8.0 2.6 2.5Fiat F IM 3.832 3.7 Underperform 6,220 4.7 4.1 0.8 0.7Renault RNO FP 35.795 56 Outperform 13,891 4.8 3.7 4.5 3.8PSA Peugeot Citroen UG FP 9.233 9.5 Underperform 4,299 12.6 6.8 2.0 1.8Ford Motors F US 11.66 NA NR 44,493 7.7 6.6 9.1 7.9General Motors GM US 24.01 NA NR 37,594 6 5 2 2Average 25,721 8.1 6.5 5.2 4.8 Global luxury auto peerset BMW BMW GR 68.32 90 Outperform 53971 8.3 8.0 4.5 4.4Daimler DAI GR 40.85 55 Outperform 57159 8.4 7.5 7.9 7.3Porsche PAH3 GR 41.87 57 Outperform 8413 4.1 3.9 NM NMAverage 24,421 7.8 6.9 7.1 7.0Source: Company data, Macquarie Research, Share prices at 19 April 2012

Macquarie Research India auto sector

20 April 2012 12

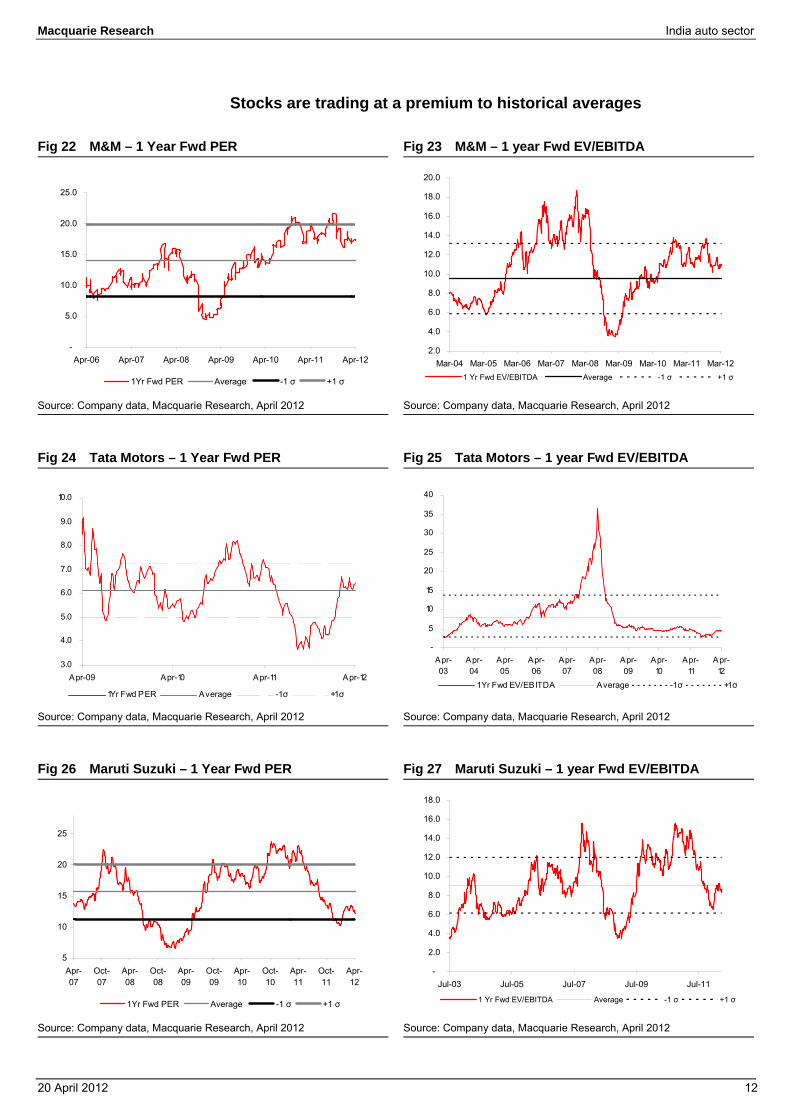

Stocks are trading at a premium to historical averages

Fig 22 M&M – 1 Year Fwd PER Fig 23 M&M – 1 year Fwd EV/EBITDA

Source: Company data, Macquarie Research, April 2012 Source: Company data, Macquarie Research, April 2012

Fig 24 Tata Motors – 1 Year Fwd PER Fig 25 Tata Motors – 1 year Fwd EV/EBITDA

Source: Company data, Macquarie Research, April 2012 Source: Company data, Macquarie Research, April 2012

Fig 26 Maruti Suzuki – 1 Year Fwd PER Fig 27 Maruti Suzuki – 1 year Fwd EV/EBITDA

Source: Company data, Macquarie Research, April 2012 Source: Company data, Macquarie Research, April 2012

-

5.0

10.0

15.0

20.0

25.0

Apr-06 Apr-07 Apr-08 Apr-09 Apr-10 Apr-11 Apr-12

1Yr Fwd PER Average -1 σ +1 σ

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Mar-04 Mar-05 Mar-06 Mar-07 Mar-08 Mar-09 Mar-10 Mar-11 Mar-121 Yr Fwd EV/EBITDA Average -1 σ +1 σ

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Apr-09 Apr-10 Apr-11 Apr-12

1Yr Fwd PER Average -1 σ +1 σ

-

5

10

15

20

25

30

35

40

Apr-03

Apr-04

Apr-05

Apr-06

Apr-07

Apr-08

Apr-09

Apr-10

Apr-11

Apr-12

1 Yr Fwd EV/EBITDA Average -1 σ +1 σ

5

10

15

20

25

Apr-07

Oct-07

Apr-08

Oct-08

Apr-09

Oct-09

Apr-10

Oct-10

Apr-11

Oct-11

Apr-12

1Yr Fwd PER Average -1 σ +1 σ

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

Jul-03 Jul-05 Jul-07 Jul-09 Jul-11

1 Yr Fwd EV/EBITDA Average -1 σ +1 σ

Macquarie Research India auto sector

20 April 2012 13

Fig 28 Hero MotoCorp – 1 Year Fwd PER Fig 29 Hero MotoCorp – 1 year Fwd EV/EBITDA

Source: Company data, Macquarie Research, April 2012 Source: Company data, Macquarie Research, April 2012

Fig 30 Bajaj Auto – 1 Year Fwd PER Fig 31 Bajaj Auto – 1 year Fwd EV/EBITDA

Source: Company data, Macquarie Research, April 2012 Source: Company data, Macquarie Research, April 2012

Fig 32 Ashok Leyland – 1 Year Fwd PER Fig 33 Ashok Leyland – 1 year Fwd EV/EBITDA

Source: Company data, Macquarie Research, April 2012 Source: Company data, Macquarie Research, April 2012

4

7

10

13

16

19

Apr-04 Apr-05 Apr-06 Apr-07 Apr-08 Apr-09 Apr-10 Apr-11 Apr-12

1Yr Fwd PER Average -1 σ +1 σ

3.0

5.0

7.0

9.0

11.0

13.0

15.0

17.0

Apr-02

Apr-03

Apr-04

Apr-05

Apr-06

Apr-07

Apr-08

Apr-09

Apr-10

Apr-11

Apr-12

1 Yr Fwd EV/EBITDA Average -1 σ +1 σ

6.0

9.0

12.0

15.0

18.0

Sep-09 Mar-10 Sep-10 Mar-11 Sep-11 Mar-12

1Yr Fwd PER Average -1 σ +1 σ

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

May-08

Sep-08

Jan-09

May-09

Sep-09

Jan-10

May-10

Sep-10

Jan-11

May-11

Sep-11

Jan-12

1 Yr Fwd EV/EBITDA Average -1 σ +1 σ

-

5

10

15

20

25

30

Apr-02 Oct-03 Apr-05 Oct-06 Apr-08 Oct-09 Apr-111Yr Fwd PER Average -1 σ +1 σ

-

5.0

10.0

15.0

20.0

25.0

30.0

Apr-02

Apr-03

Apr-04

Apr-05

Apr-06

Apr-07

Apr-08

Apr-09

Apr-10

Apr-11

Apr-12

1 Yr Fwd EV/EBITDA Average-1 σ +1 σ

Macquarie Research India auto sector

20 April 2012 14

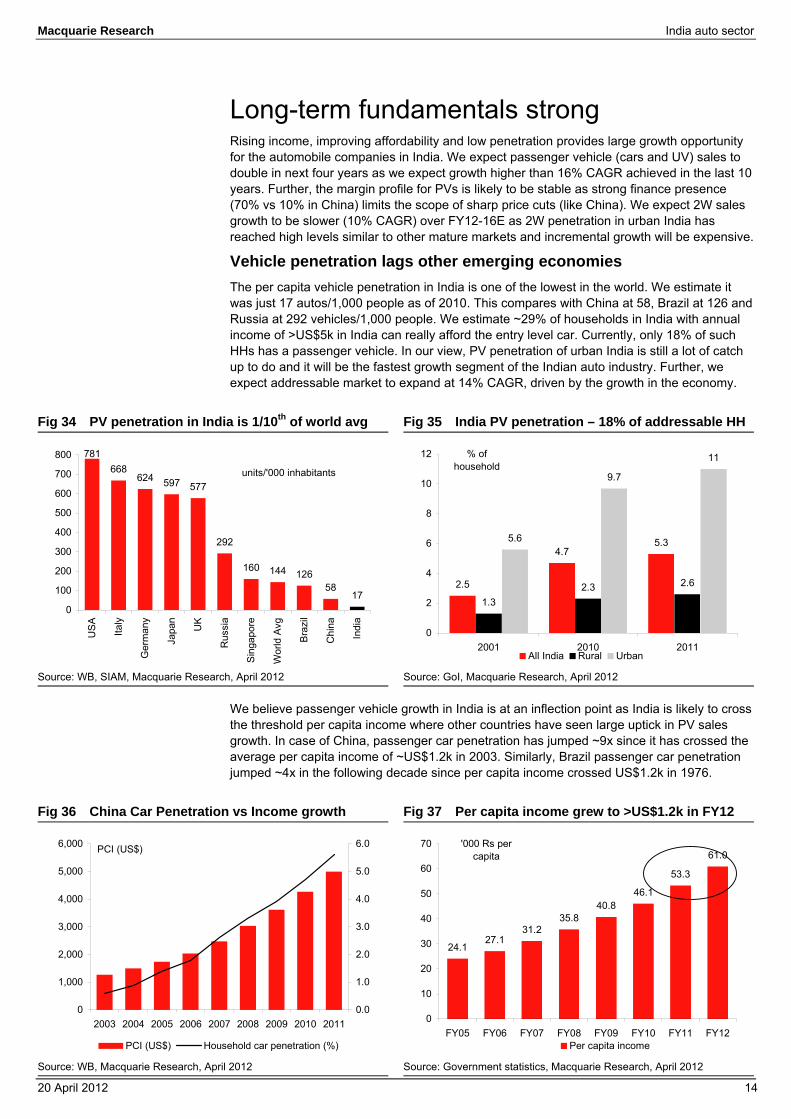

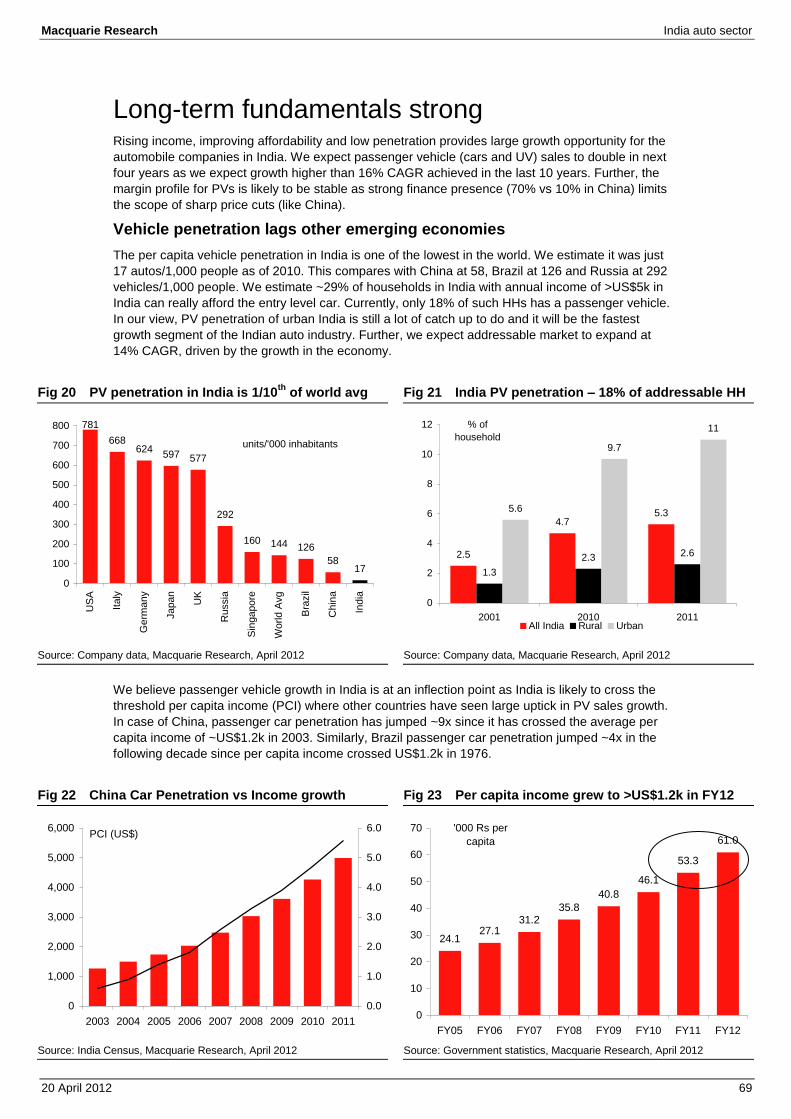

Long-term fundamentals strong Rising income, improving affordability and low penetration provides large growth opportunity for the automobile companies in India. We expect passenger vehicle (cars and UV) sales to double in next four years as we expect growth higher than 16% CAGR achieved in the last 10 years. Further, the margin profile for PVs is likely to be stable as strong finance presence (70% vs 10% in China) limits the scope of sharp price cuts (like China). We expect 2W sales growth to be slower (10% CAGR) over FY12-16E as 2W penetration in urban India has reached high levels similar to other mature markets and incremental growth will be expensive.

Vehicle penetration lags other emerging economies The per capita vehicle penetration in India is one of the lowest in the world. We estimate it was just 17 autos/1,000 people as of 2010. This compares with China at 58, Brazil at 126 and Russia at 292 vehicles/1,000 people. We estimate ~29% of households in India with annual income of >US$5k in India can really afford the entry level car. Currently, only 18% of such HHs has a passenger vehicle. In our view, PV penetration of urban India is still a lot of catch up to do and it will be the fastest growth segment of the Indian auto industry. Further, we expect addressable market to expand at 14% CAGR, driven by the growth in the economy.

Fig 34 PV penetration in India is 1/10th of world avg Fig 35 India PV penetration – 18% of addressable HH

Source: WB, SIAM, Macquarie Research, April 2012 Source: GoI, Macquarie Research, April 2012

We believe passenger vehicle growth in India is at an inflection point as India is likely to cross the threshold per capita income where other countries have seen large uptick in PV sales growth. In case of China, passenger car penetration has jumped ~9x since it has crossed the average per capita income of ~US$1.2k in 2003. Similarly, Brazil passenger car penetration jumped ~4x in the following decade since per capita income crossed US$1.2k in 1976.

Fig 36 China Car Penetration vs Income growth Fig 37 Per capita income grew to >US$1.2k in FY12

Source: WB, Macquarie Research, April 2012 Source: Government statistics, Macquarie Research, April 2012

781668

624 597 577

292

160 144 12658

170

100

200

300

400

500

600

700

800

US

A

Italy

Ger

man

y

Japa

n

UK

Rus

sia

Sin

gapo

re

Wor

ld A

vg

Bra

zil

Chi

na

Indi

a

units/'000 inhabitants

2.5

4.75.3

1.32.3 2.6

5.6

9.7

11

0

2

4

6

8

10

12

2001 2010 2011

% of household

All India Rural Urban

0

1,000

2,000

3,000

4,000

5,000

6,000

2003 2004 2005 2006 2007 2008 2009 2010 2011

PCI (US$)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

PCI (US$) Household car penetration (%)

24.127.1

31.235.8

40.846.1

53.3

61.0

0

10

20

30

40

50

60

70

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12

'000 Rs per capita

Per capita income

Macquarie Research India auto sector

20 April 2012 15

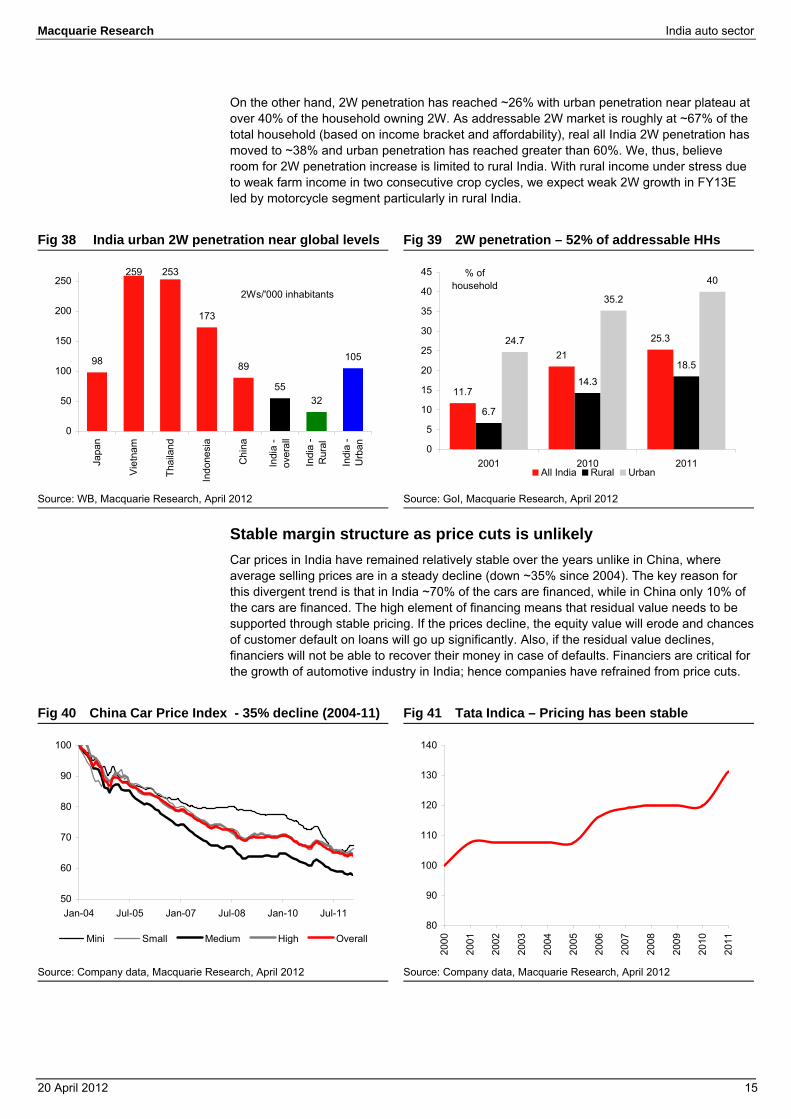

On the other hand, 2W penetration has reached ~26% with urban penetration near plateau at over 40% of the household owning 2W. As addressable 2W market is roughly at ~67% of the total household (based on income bracket and affordability), real all India 2W penetration has moved to ~38% and urban penetration has reached greater than 60%. We, thus, believe room for 2W penetration increase is limited to rural India. With rural income under stress due to weak farm income in two consecutive crop cycles, we expect weak 2W growth in FY13E led by motorcycle segment particularly in rural India.

Fig 38 India urban 2W penetration near global levels Fig 39 2W penetration – 52% of addressable HHs

Source: WB, Macquarie Research, April 2012 Source: GoI, Macquarie Research, April 2012

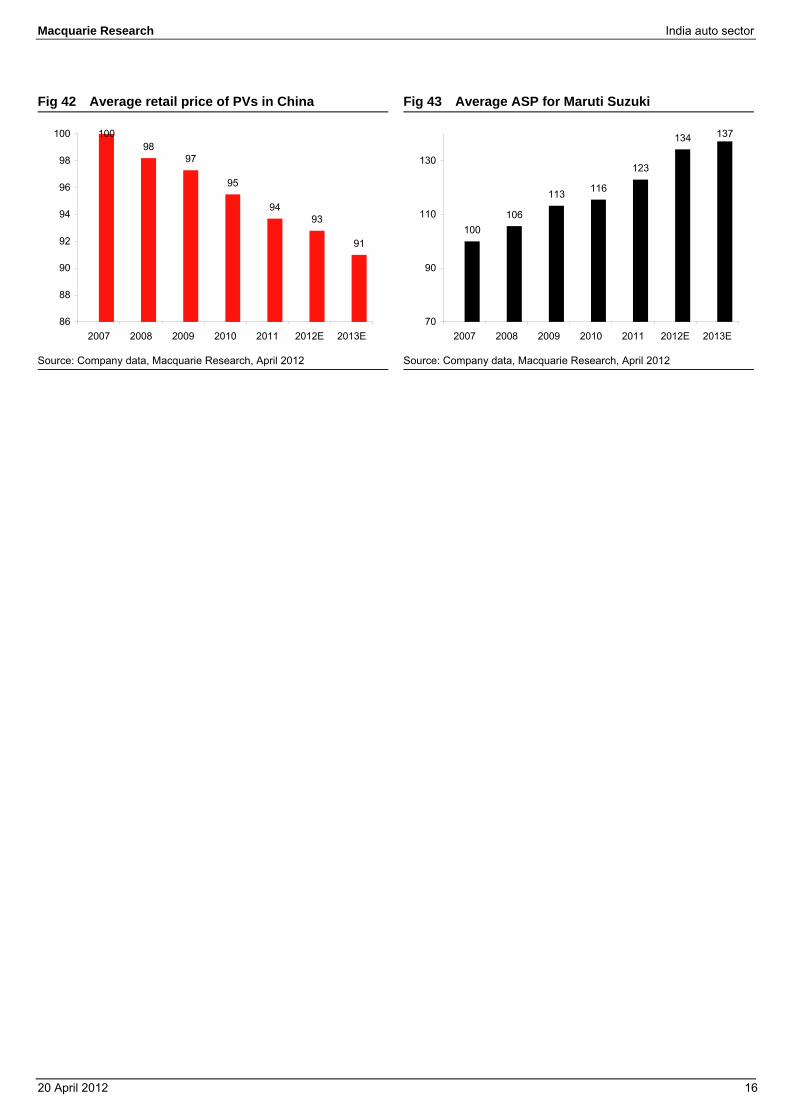

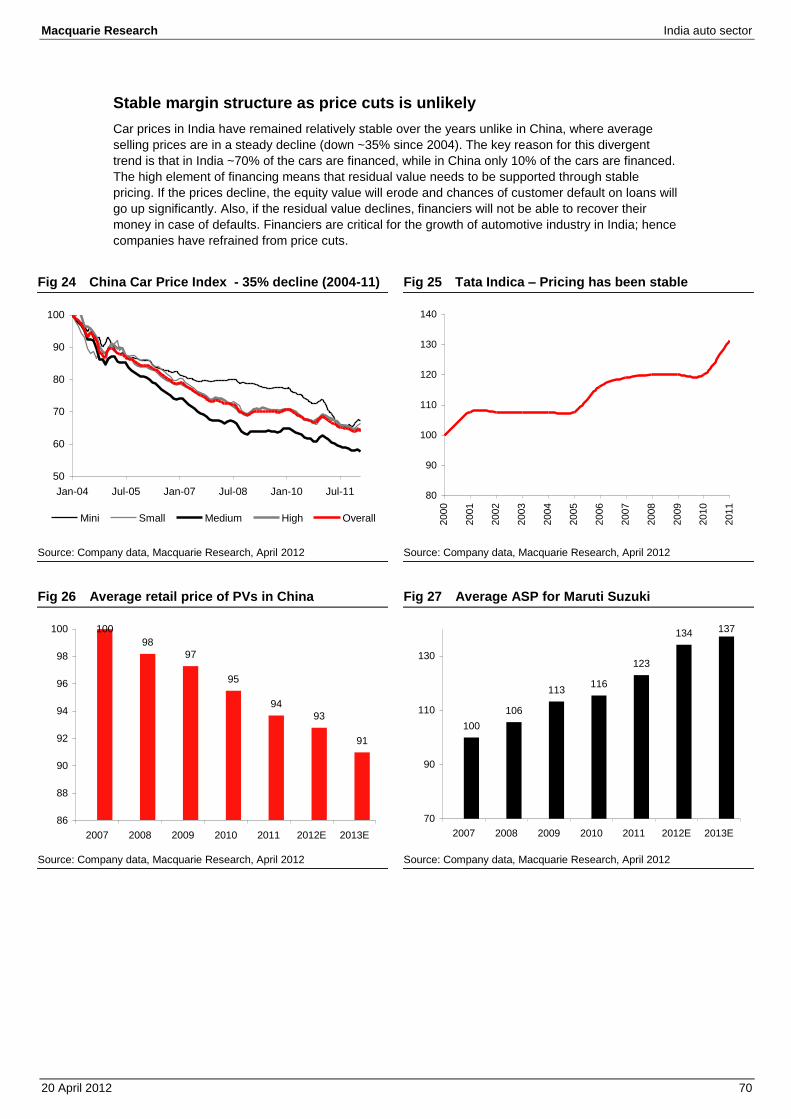

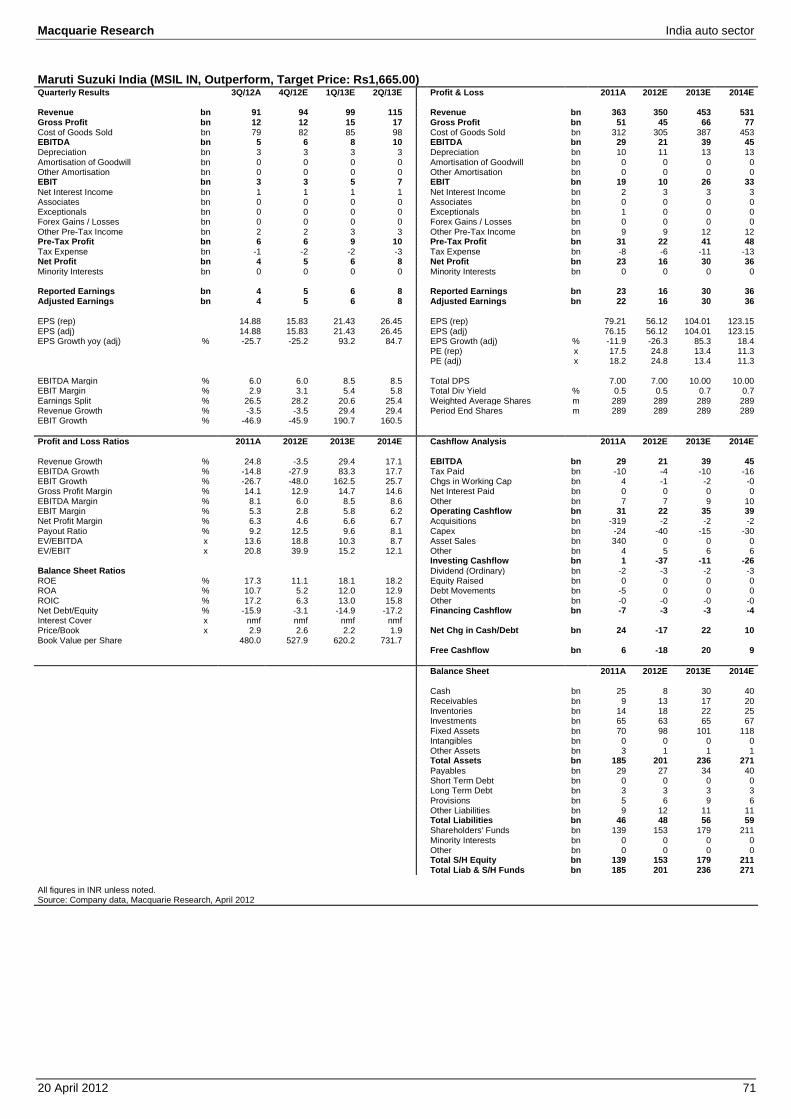

Stable margin structure as price cuts is unlikely Car prices in India have remained relatively stable over the years unlike in China, where average selling prices are in a steady decline (down ~35% since 2004). The key reason for this divergent trend is that in India ~70% of the cars are financed, while in China only 10% of the cars are financed. The high element of financing means that residual value needs to be supported through stable pricing. If the prices decline, the equity value will erode and chances of customer default on loans will go up significantly. Also, if the residual value declines, financiers will not be able to recover their money in case of defaults. Financiers are critical for the growth of automotive industry in India; hence companies have refrained from price cuts.

Fig 40 China Car Price Index - 35% decline (2004-11) Fig 41 Tata Indica – Pricing has been stable

Source: Company data, Macquarie Research, April 2012 Source: Company data, Macquarie Research, April 2012

98

259 253

173

89

5532

105

0

50

100

150

200

250

Japa

n

Vie

tnam

Thai

land

Indo

nesi

a

Chi

na

Indi

a -

over

all

Indi

a -

Rur

al

Indi

a -

Urb

an

2Ws/'000 inhabitants

11.7

21

25.3

6.7

14.3

18.5

24.7

35.2

40

0

5

10

15

20

25

30

35

40

45

2001 2010 2011

% of household

All India Rural Urban

50

60

70

80

90

100

Jan-04 Jul-05 Jan-07 Jul-08 Jan-10 Jul-11

Mini Small Medium High Overall80

90

100

110

120

130

140

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Macquarie Research India auto sector

20 April 2012 16

Fig 42 Average retail price of PVs in China Fig 43 Average ASP for Maruti Suzuki

Source: Company data, Macquarie Research, April 2012 Source: Company data, Macquarie Research, April 2012

10098

97

95

9493

91

86

88

90

92

94

96

98

100

2007 2008 2009 2010 2011 2012E 2013E

100106

113 116

123

134 137

70

90

110

130

2007 2008 2009 2010 2011 2012E 2013E

Macquarie Research India auto sector

20 April 2012 17

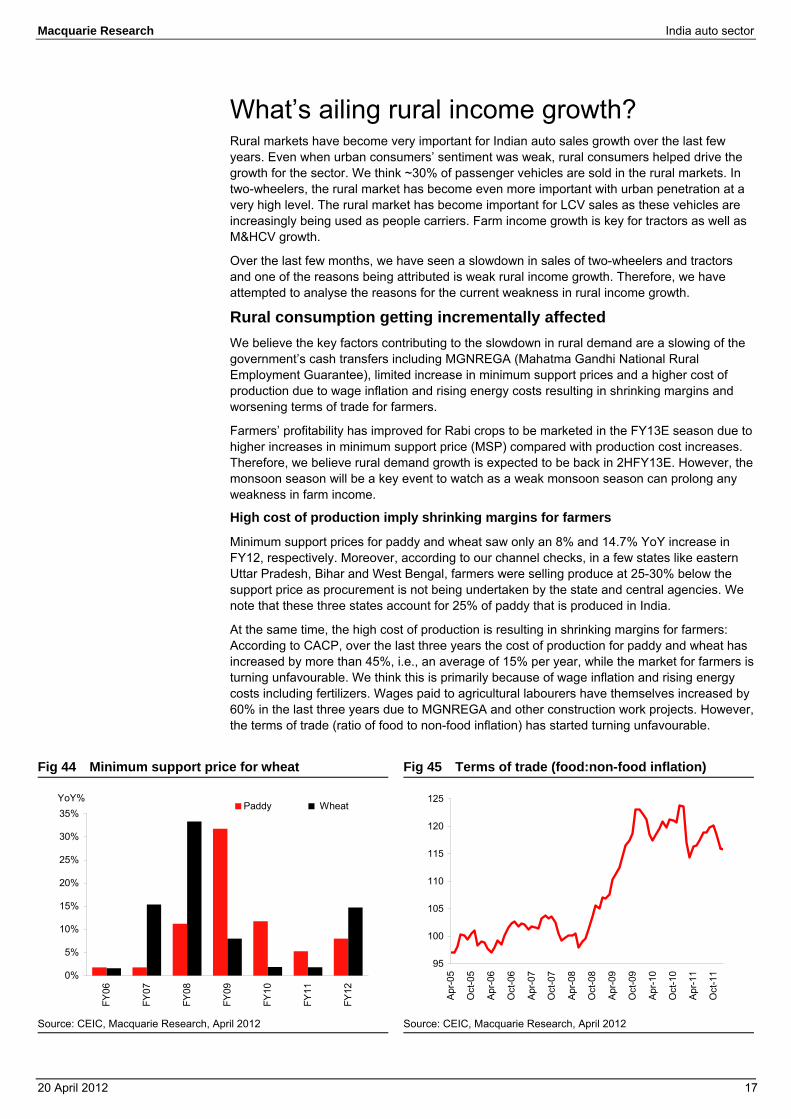

What’s ailing rural income growth? Rural markets have become very important for Indian auto sales growth over the last few years. Even when urban consumers’ sentiment was weak, rural consumers helped drive the growth for the sector. We think ~30% of passenger vehicles are sold in the rural markets. In two-wheelers, the rural market has become even more important with urban penetration at a very high level. The rural market has become important for LCV sales as these vehicles are increasingly being used as people carriers. Farm income growth is key for tractors as well as M&HCV growth.

Over the last few months, we have seen a slowdown in sales of two-wheelers and tractors and one of the reasons being attributed is weak rural income growth. Therefore, we have attempted to analyse the reasons for the current weakness in rural income growth.

Rural consumption getting incrementally affected We believe the key factors contributing to the slowdown in rural demand are a slowing of the government’s cash transfers including MGNREGA (Mahatma Gandhi National Rural Employment Guarantee), limited increase in minimum support prices and a higher cost of production due to wage inflation and rising energy costs resulting in shrinking margins and worsening terms of trade for farmers.

Farmers’ profitability has improved for Rabi crops to be marketed in the FY13E season due to higher increases in minimum support price (MSP) compared with production cost increases. Therefore, we believe rural demand growth is expected to be back in 2HFY13E. However, the monsoon season will be a key event to watch as a weak monsoon season can prolong any weakness in farm income.

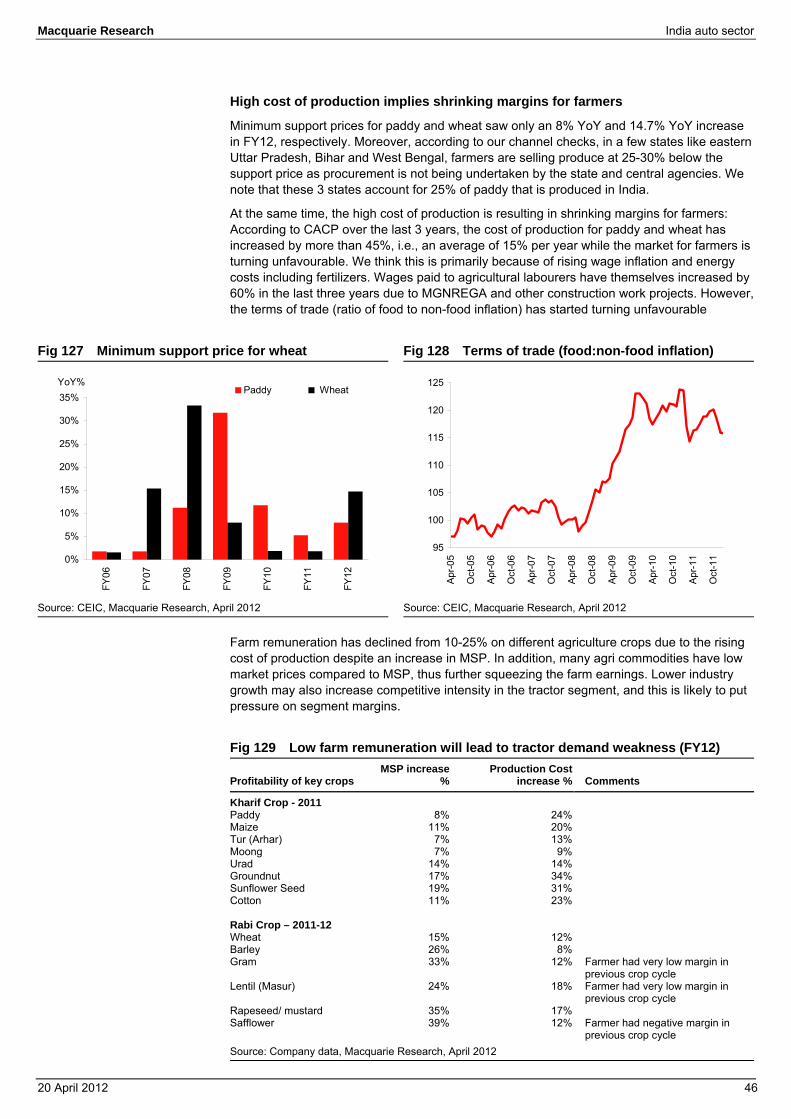

High cost of production imply shrinking margins for farmers

Minimum support prices for paddy and wheat saw only an 8% and 14.7% YoY increase in FY12, respectively. Moreover, according to our channel checks, in a few states like eastern Uttar Pradesh, Bihar and West Bengal, farmers were selling produce at 25-30% below the support price as procurement is not being undertaken by the state and central agencies. We note that these three states account for 25% of paddy that is produced in India.

At the same time, the high cost of production is resulting in shrinking margins for farmers: According to CACP, over the last three years the cost of production for paddy and wheat has increased by more than 45%, i.e., an average of 15% per year, while the market for farmers is turning unfavourable. We think this is primarily because of wage inflation and rising energy costs including fertilizers. Wages paid to agricultural labourers have themselves increased by 60% in the last three years due to MGNREGA and other construction work projects. However, the terms of trade (ratio of food to non-food inflation) has started turning unfavourable.

Fig 44 Minimum support price for wheat Fig 45 Terms of trade (food:non-food inflation)

Source: CEIC, Macquarie Research, April 2012 Source: CEIC, Macquarie Research, April 2012

0%

5%

10%

15%

20%

25%

30%

35%

FY06

FY07

FY08

FY09

FY10

FY11

FY12

Paddy WheatYoY%

95

100

105

110

115

120

125

Apr

-05

Oct

-05

Apr

-06

Oct

-06

Apr

-07

Oct

-07

Apr

-08

Oct

-08

Apr

-09

Oct

-09

Apr

-10

Oct

-10

Apr

-11

Oct

-11

Macquarie Research India auto sector

20 April 2012 18

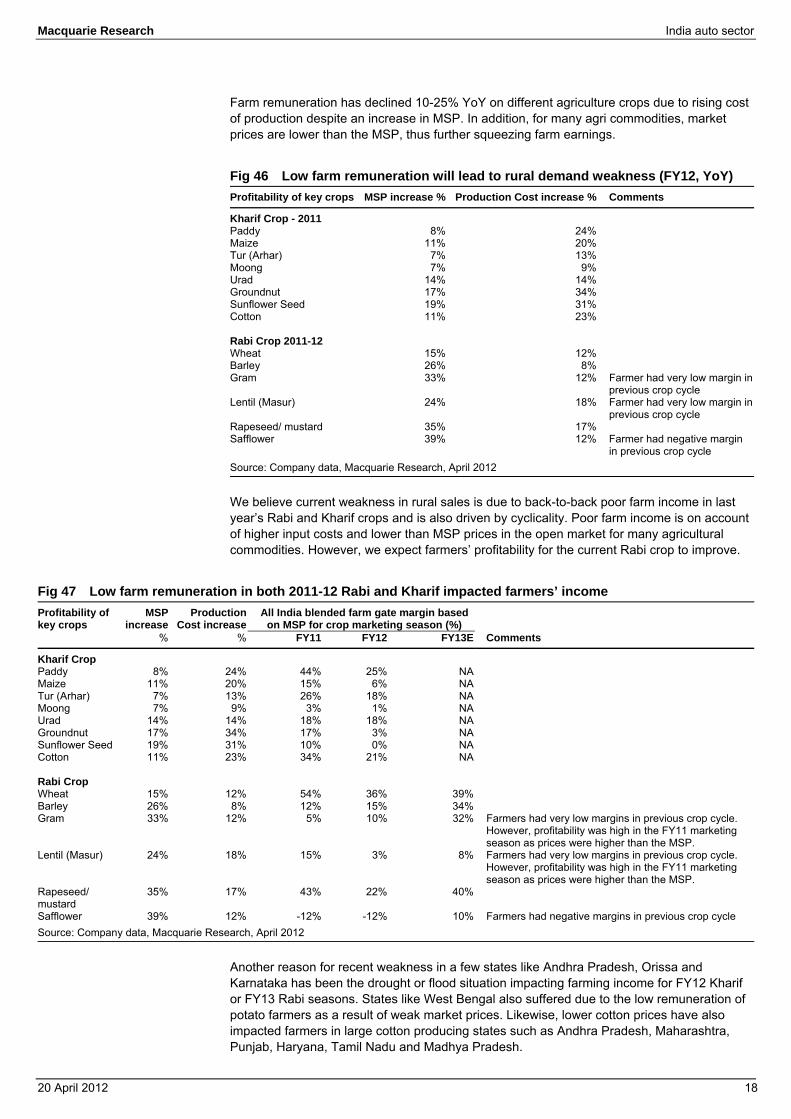

Farm remuneration has declined 10-25% YoY on different agriculture crops due to rising cost of production despite an increase in MSP. In addition, for many agri commodities, market prices are lower than the MSP, thus further squeezing farm earnings.

Fig 46 Low farm remuneration will lead to rural demand weakness (FY12, YoY) Profitability of key crops MSP increase % Production Cost increase % Comments

Kharif Crop - 2011 Paddy 8% 24% Maize 11% 20% Tur (Arhar) 7% 13% Moong 7% 9% Urad 14% 14% Groundnut 17% 34% Sunflower Seed 19% 31% Cotton 11% 23% Rabi Crop 2011-12 Wheat 15% 12% Barley 26% 8% Gram 33% 12% Farmer had very low margin in

previous crop cycle Lentil (Masur) 24% 18% Farmer had very low margin in

previous crop cycle Rapeseed/ mustard 35% 17% Safflower 39% 12% Farmer had negative margin

in previous crop cycle Source: Company data, Macquarie Research, April 2012

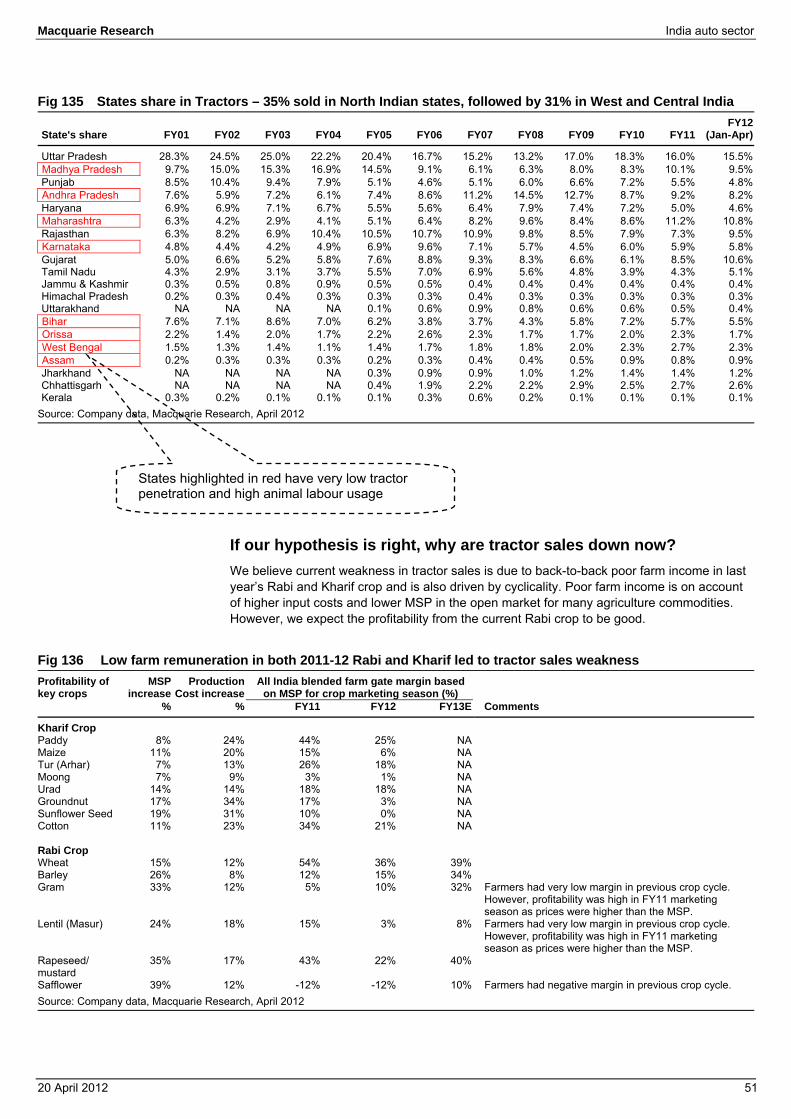

We believe current weakness in rural sales is due to back-to-back poor farm income in last year’s Rabi and Kharif crops and is also driven by cyclicality. Poor farm income is on account of higher input costs and lower than MSP prices in the open market for many agricultural commodities. However, we expect farmers’ profitability for the current Rabi crop to improve.

Fig 47 Low farm remuneration in both 2011-12 Rabi and Kharif impacted farmers’ income Profitability of key crops

MSP increase

Production Cost increase

All India blended farm gate margin based on MSP for crop marketing season (%)

% % FY11 FY12 FY13E Comments

Kharif Crop Paddy 8% 24% 44% 25% NA Maize 11% 20% 15% 6% NA Tur (Arhar) 7% 13% 26% 18% NA Moong 7% 9% 3% 1% NA Urad 14% 14% 18% 18% NA Groundnut 17% 34% 17% 3% NA Sunflower Seed 19% 31% 10% 0% NA Cotton 11% 23% 34% 21% NA Rabi Crop Wheat 15% 12% 54% 36% 39% Barley 26% 8% 12% 15% 34% Gram 33% 12% 5% 10% 32% Farmers had very low margins in previous crop cycle.

However, profitability was high in the FY11 marketing season as prices were higher than the MSP.

Lentil (Masur) 24% 18% 15% 3% 8% Farmers had very low margins in previous crop cycle. However, profitability was high in the FY11 marketing season as prices were higher than the MSP.

Rapeseed/ mustard

35% 17% 43% 22% 40%

Safflower 39% 12% -12% -12% 10% Farmers had negative margins in previous crop cycle Source: Company data, Macquarie Research, April 2012

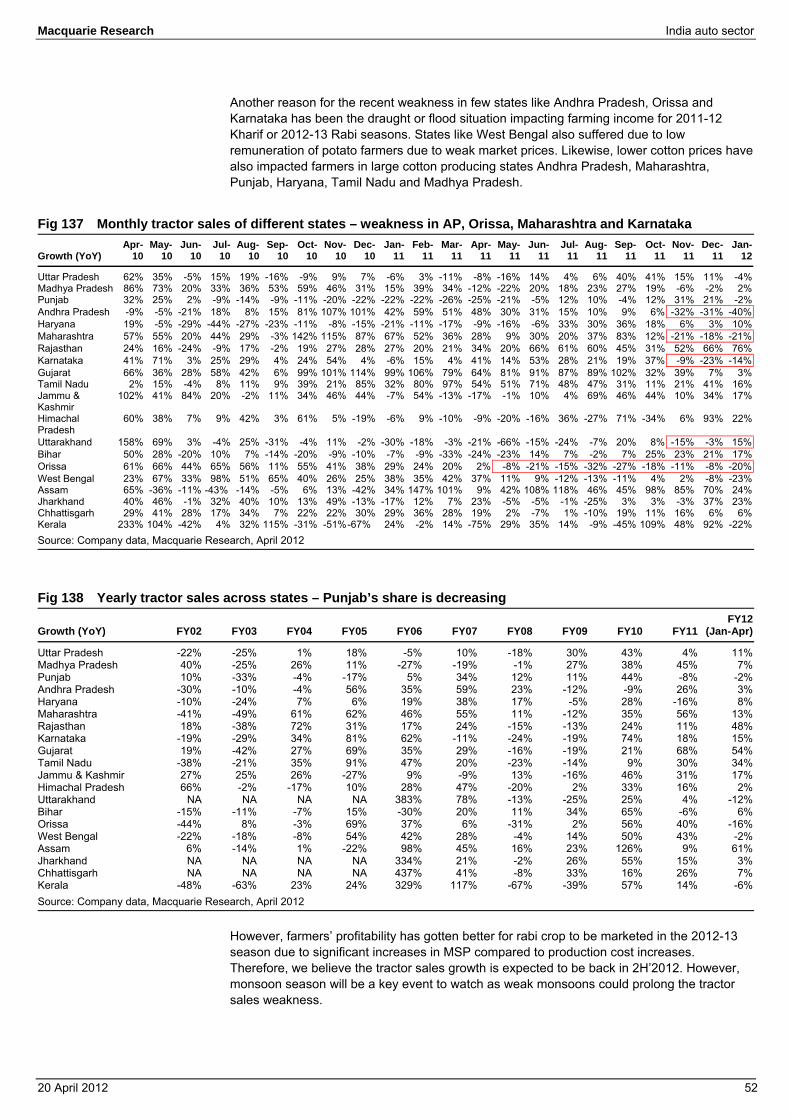

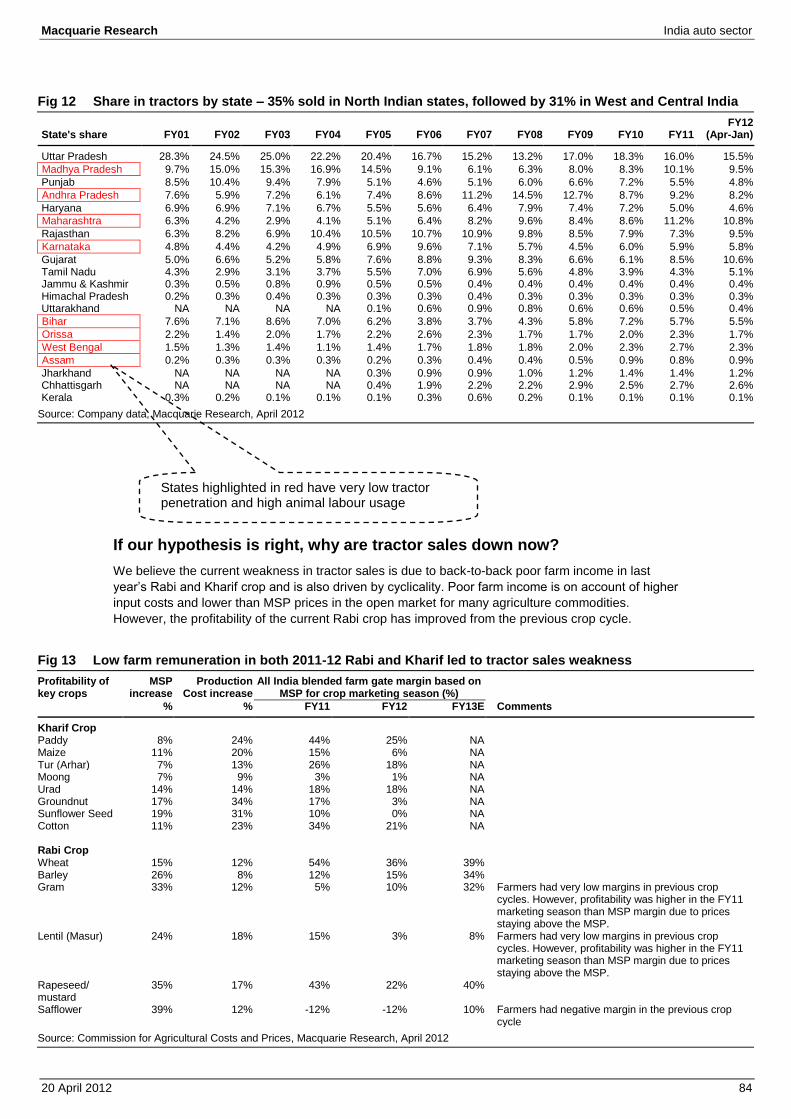

Another reason for recent weakness in a few states like Andhra Pradesh, Orissa and Karnataka has been the drought or flood situation impacting farming income for FY12 Kharif or FY13 Rabi seasons. States like West Bengal also suffered due to the low remuneration of potato farmers as a result of weak market prices. Likewise, lower cotton prices have also impacted farmers in large cotton producing states such as Andhra Pradesh, Maharashtra, Punjab, Haryana, Tamil Nadu and Madhya Pradesh.

Macquarie Research India auto sector

20 April 2012 19

Rural income growth has been buoyant for the last 4 years

Rural wages have increased manifold over the last few years: Following higher wages to farmers under the government’s socialist programmes like MGNREGA, the average daily wage rate for various agricultural occupations including ploughing, sowing, harvesting, picking, etc. has increased by an average of 15% YoY in the last four years (FY08-FY11) compared to an average increase of 4.3% YoY in the previous five years (FY04-FY07). The farming-related activities wage inflation in real terms (adjusted using CPI-agricultural labourers) increased to 10.3% YoY in FY11 from 3.7% YoY in FY10, thus boosting rural income levels.

Fig 48 Average daily wage rate for agricultural occupations

Fig 49 CPI – agricultural labourers vs nominal and real farming related wage inflation

Source: Labour bureau, Macquarie Research, April 2012 Source: Labour bureau, Macquarie Research, April 2012

However, rural spending by the government has started slowing

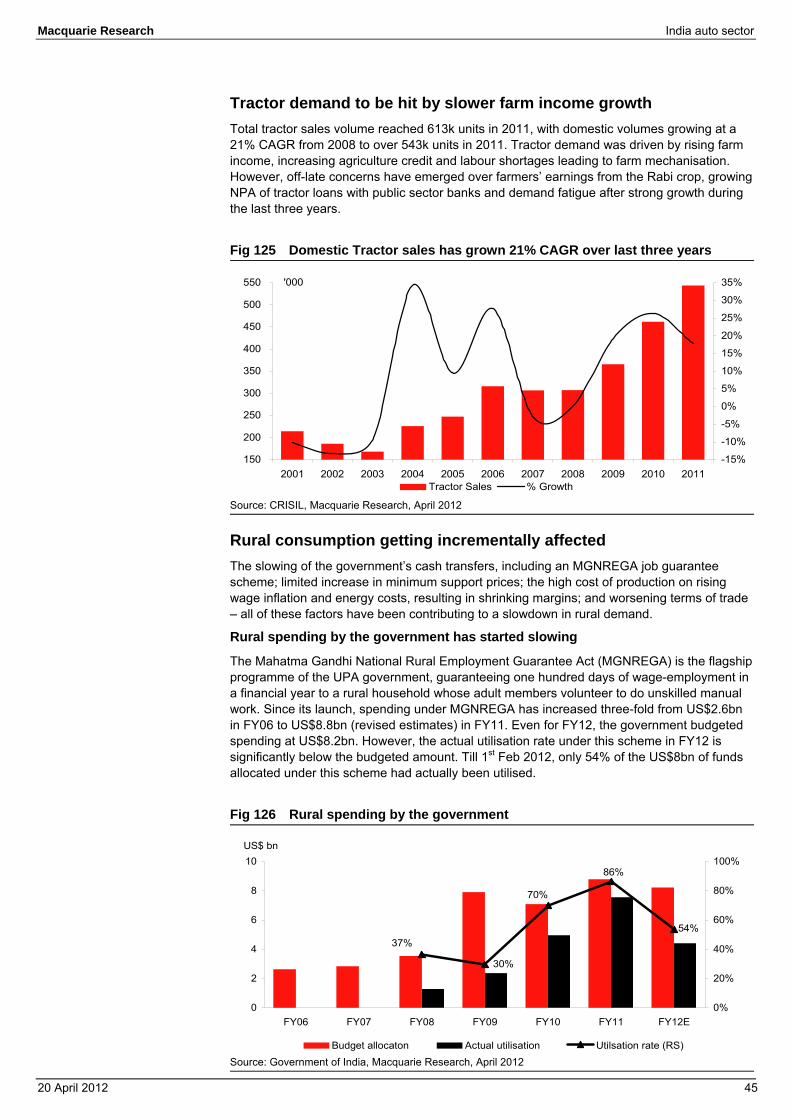

The Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA) is the flagship programme of the UPA government, guaranteeing 100 days of wage-employment in a financial year to a rural household whose adult members volunteer to do unskilled manual work. Since its launch, spending under NREGA has increased threefold from US$2.6bn in FY06 to US$8.8bn (revised estimates) in FY11. Even for FY12, the government budgeted spending at US$8.2bn.

However, according to our economist, Tanvee Gupta Jain, the actual utilisation rate under this scheme in FY12 is significantly below the budgeted amount. As of 1st Feb 2012, only 54% of the US$8bn of funds allocated under this scheme had actually been utilised. The slowdown in social sector spending will result in a slowdown in income levels for the rural segment.

Fig 50 Rural spending by the government

Source: Government of India, Macquarie Research, April 2012

20.5%

17.6%

13.7%

8.7%

6.9%2.2%

2.4%

6.2%

1.8%

0

20

40

60

80

100

120

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

-3%

2%

7%

12%

17%

22%Rs YoY%

0%

5%

10%

15%

20%

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

-4%-2%0%2%4%6%8%10%12%

CPI agricultural laborers, LSFarming related activites wage inflation (Nominal terms, LS)Farming related activites wage inflation (Real terms, RS)

YoY% YoY%

30%

54%

86%

70%

37%

0

2

4

6

8

10

FY06 FY07 FY08 FY09 FY10 FY11 FY12E0%

20%

40%

60%

80%

100%

Budget allocaton Actual utilisation Utilsation rate (RS)

US$ bn

Macquarie Research India auto sector

20 April 2012 20

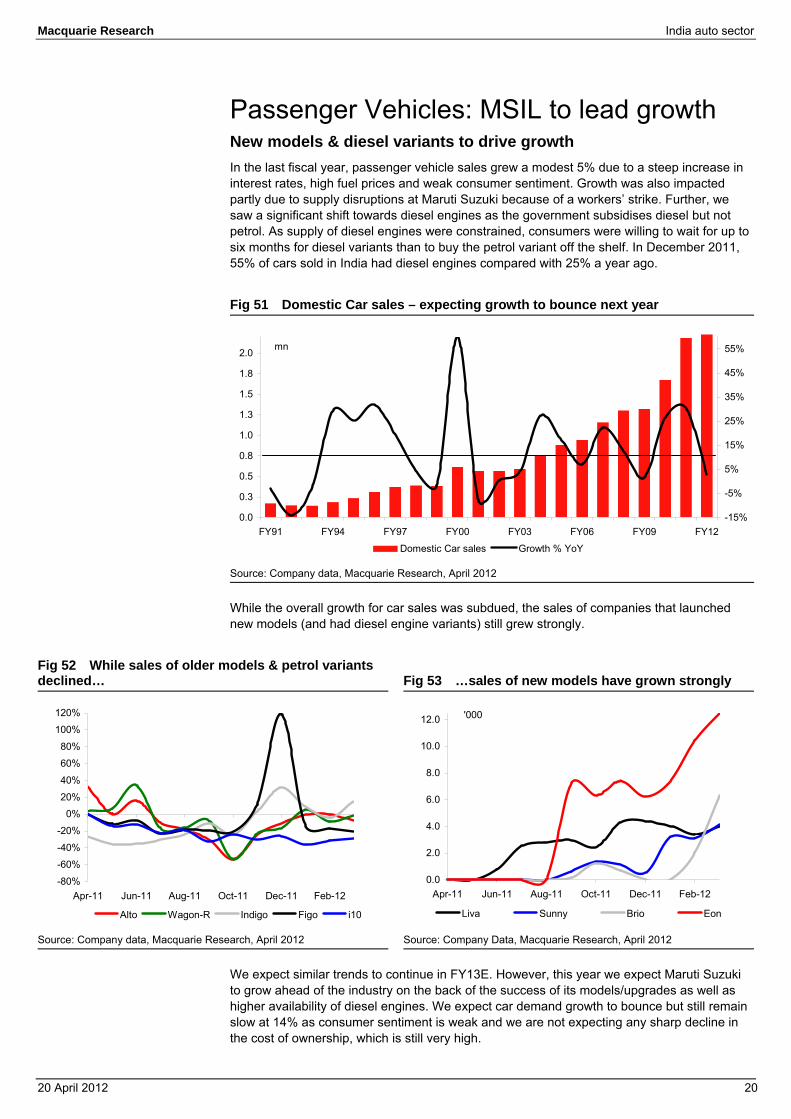

Passenger Vehicles: MSIL to lead growth New models & diesel variants to drive growth In the last fiscal year, passenger vehicle sales grew a modest 5% due to a steep increase in interest rates, high fuel prices and weak consumer sentiment. Growth was also impacted partly due to supply disruptions at Maruti Suzuki because of a workers’ strike. Further, we saw a significant shift towards diesel engines as the government subsidises diesel but not petrol. As supply of diesel engines were constrained, consumers were willing to wait for up to six months for diesel variants than to buy the petrol variant off the shelf. In December 2011, 55% of cars sold in India had diesel engines compared with 25% a year ago.

Fig 51 Domestic Car sales – expecting growth to bounce next year

Source: Company data, Macquarie Research, April 2012

While the overall growth for car sales was subdued, the sales of companies that launched new models (and had diesel engine variants) still grew strongly.

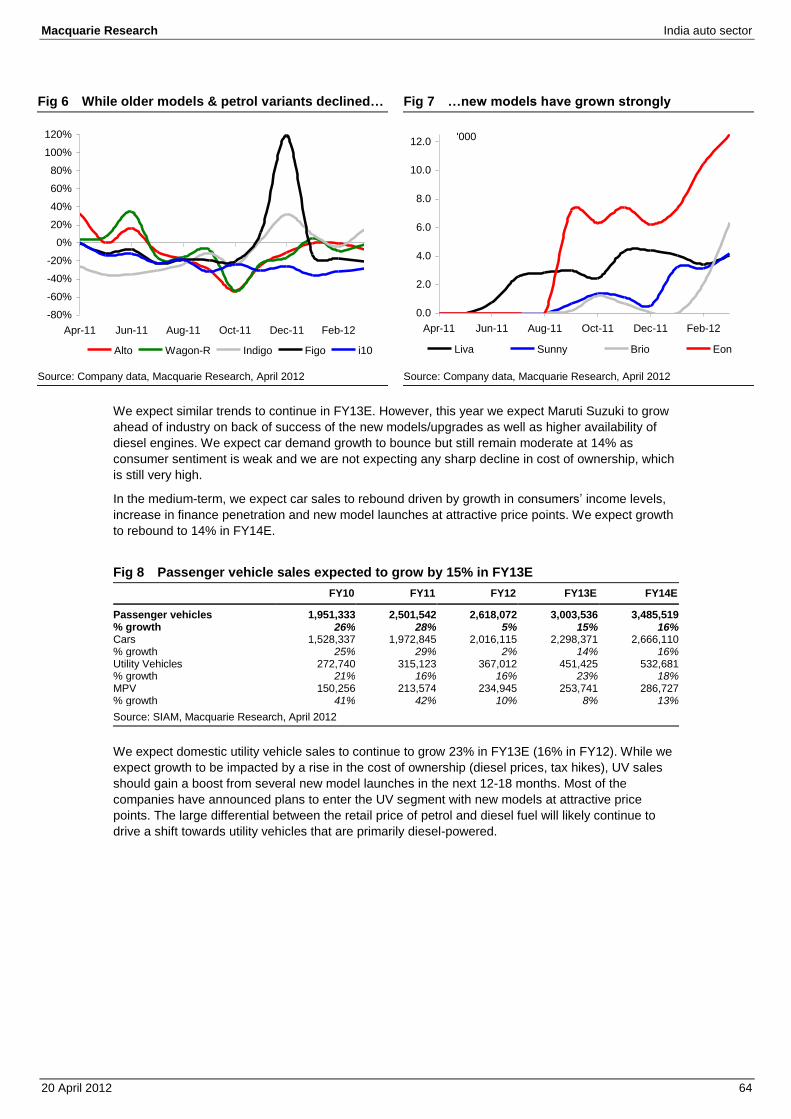

Fig 52 While sales of older models & petrol variants declined…

Fig 53 …sales of new models have grown strongly

Source: Company data, Macquarie Research, April 2012 Source: Company Data, Macquarie Research, April 2012

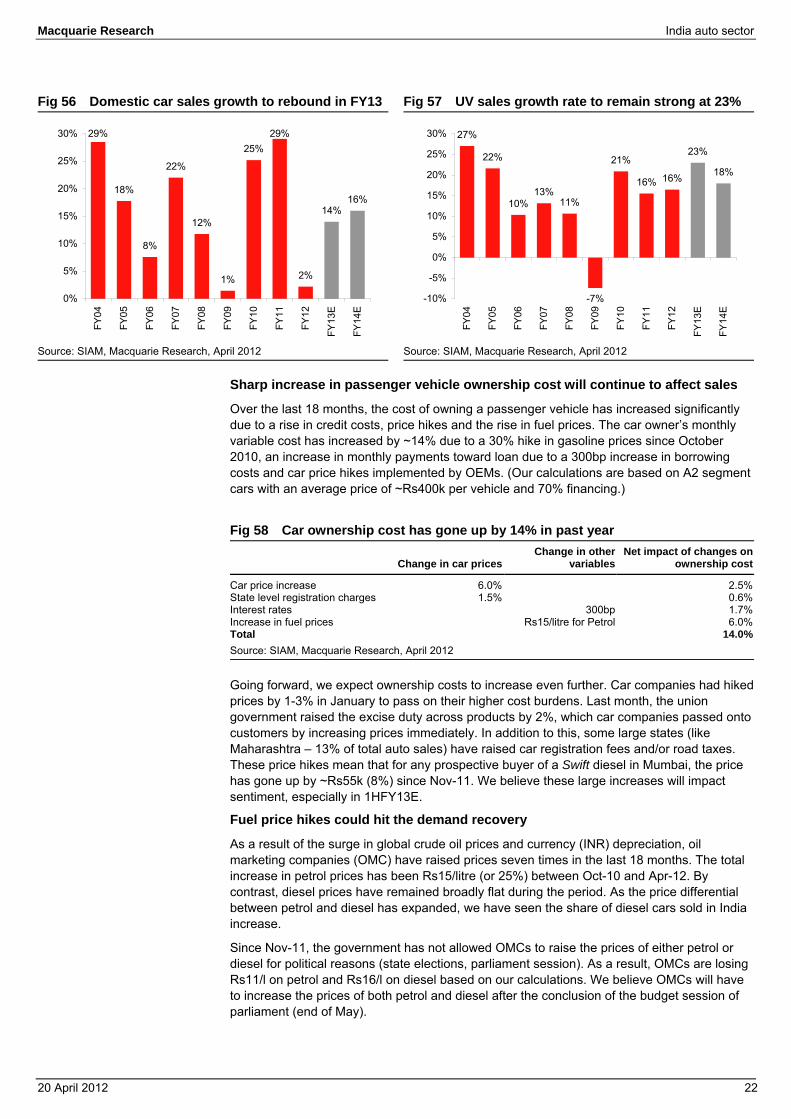

We expect similar trends to continue in FY13E. However, this year we expect Maruti Suzuki to grow ahead of the industry on the back of the success of its models/upgrades as well as higher availability of diesel engines. We expect car demand growth to bounce but still remain slow at 14% as consumer sentiment is weak and we are not expecting any sharp decline in the cost of ownership, which is still very high.

0.0

0.3

0.5

0.8

1.0

1.3

1.5

1.8

2.0

FY91 FY94 FY97 FY00 FY03 FY06 FY09 FY12-15%

-5%

5%

15%

25%

35%

45%

55%

Domestic Car sales Growth % YoY

mn

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

Apr-11 Jun-11 Aug-11 Oct-11 Dec-11 Feb-12

Alto Wagon-R Indigo Figo i10

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Apr-11 Jun-11 Aug-11 Oct-11 Dec-11 Feb-12

Liva Sunny Brio Eon

'000

Macquarie Research India auto sector

20 April 2012 21

In the medium term, we expect car sales to rebound driven by growth in consumers’ income levels, an increase in finance penetration and new model launches at attractive price points. We expect growth to rebound to 16% in FY14E.

Fig 54 Passenger vehicle sales expected to grow by 13% in FY13E FY10 FY11 FY12 FY13E FY14E

Passenger vehicles 1,951,333 2,501,542 2,618,072 3,003,536 3,485,519% growth 26% 28% 5% 15% 16%Cars 1,528,337 1,972,845 2,016,115 2,298,371 2,666,110% growth 25% 29% 2% 14% 16%Utility Vehicles 272,740 315,123 367,012 451,425 532,681% growth 21% 16% 16% 23% 18%MPV 150,256 213,574 234,945 253,741 286,727% growth 41% 42% 10% 8% 13%Source: SIAM, Macquarie Research, April 2012

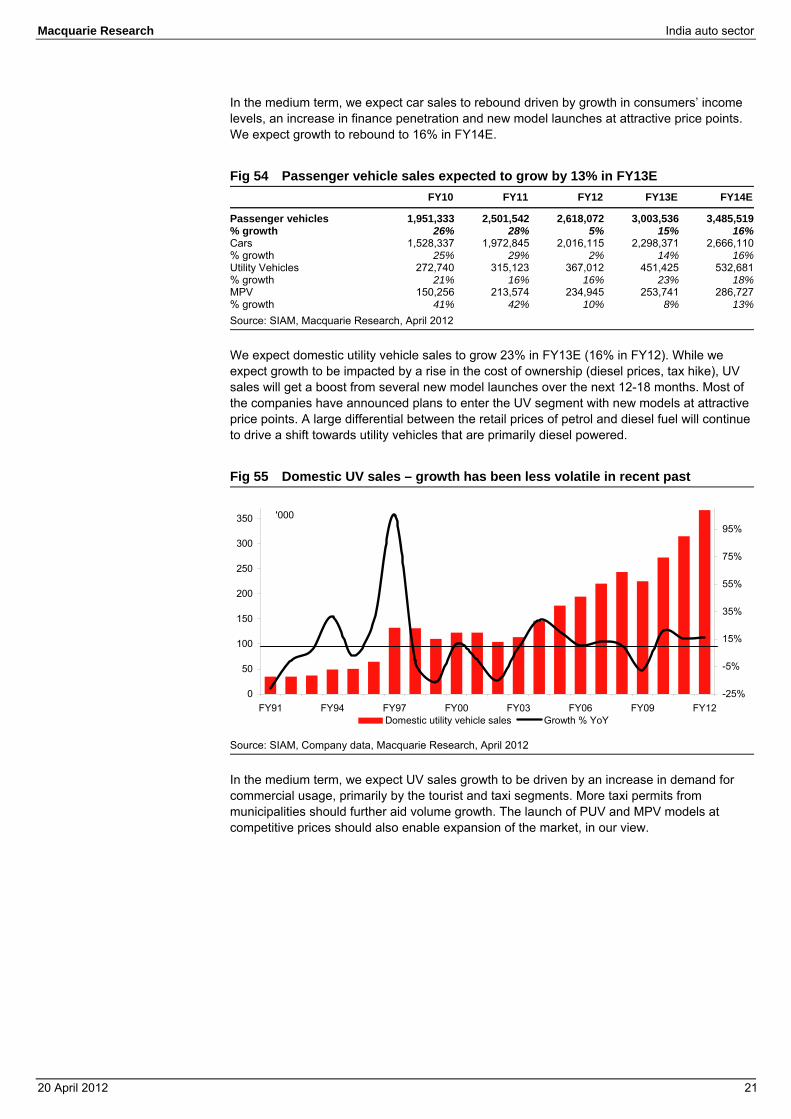

We expect domestic utility vehicle sales to grow 23% in FY13E (16% in FY12). While we expect growth to be impacted by a rise in the cost of ownership (diesel prices, tax hike), UV sales will get a boost from several new model launches over the next 12-18 months. Most of the companies have announced plans to enter the UV segment with new models at attractive price points. A large differential between the retail prices of petrol and diesel fuel will continue to drive a shift towards utility vehicles that are primarily diesel powered.

Fig 55 Domestic UV sales – growth has been less volatile in recent past

Source: SIAM, Company data, Macquarie Research, April 2012

In the medium term, we expect UV sales growth to be driven by an increase in demand for commercial usage, primarily by the tourist and taxi segments. More taxi permits from municipalities should further aid volume growth. The launch of PUV and MPV models at competitive prices should also enable expansion of the market, in our view.

0

50

100

150

200

250

300

350

FY91 FY94 FY97 FY00 FY03 FY06 FY09 FY12-25%

-5%

15%

35%

55%

75%

95%

Domestic utility vehicle sales Growth % YoY

'000

Macquarie Research India auto sector

20 April 2012 22

Fig 56 Domestic car sales growth to rebound in FY13 Fig 57 UV sales growth rate to remain strong at 23%

Source: SIAM, Macquarie Research, April 2012 Source: SIAM, Macquarie Research, April 2012

Sharp increase in passenger vehicle ownership cost will continue to affect sales

Over the last 18 months, the cost of owning a passenger vehicle has increased significantly due to a rise in credit costs, price hikes and the rise in fuel prices. The car owner’s monthly variable cost has increased by ~14% due to a 30% hike in gasoline prices since October 2010, an increase in monthly payments toward loan due to a 300bp increase in borrowing costs and car price hikes implemented by OEMs. (Our calculations are based on A2 segment cars with an average price of ~Rs400k per vehicle and 70% financing.)

Fig 58 Car ownership cost has gone up by 14% in past year

Change in car pricesChange in other

variables Net impact of changes on

ownership cost

Car price increase 6.0% 2.5%State level registration charges 1.5% 0.6%Interest rates 300bp 1.7%Increase in fuel prices Rs15/litre for Petrol 6.0%Total 14.0%Source: SIAM, Macquarie Research, April 2012

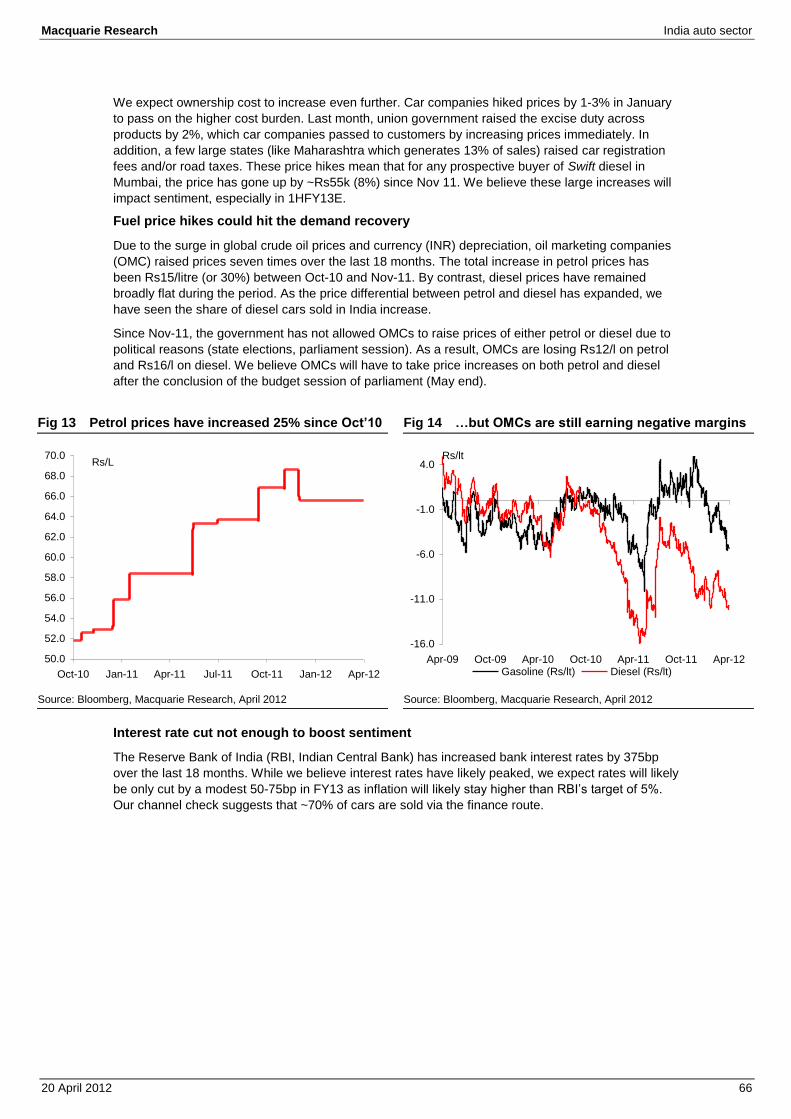

Going forward, we expect ownership costs to increase even further. Car companies had hiked prices by 1-3% in January to pass on their higher cost burdens. Last month, the union government raised the excise duty across products by 2%, which car companies passed onto customers by increasing prices immediately. In addition to this, some large states (like Maharashtra – 13% of total auto sales) have raised car registration fees and/or road taxes. These price hikes mean that for any prospective buyer of a Swift diesel in Mumbai, the price has gone up by ~Rs55k (8%) since Nov-11. We believe these large increases will impact sentiment, especially in 1HFY13E.

Fuel price hikes could hit the demand recovery

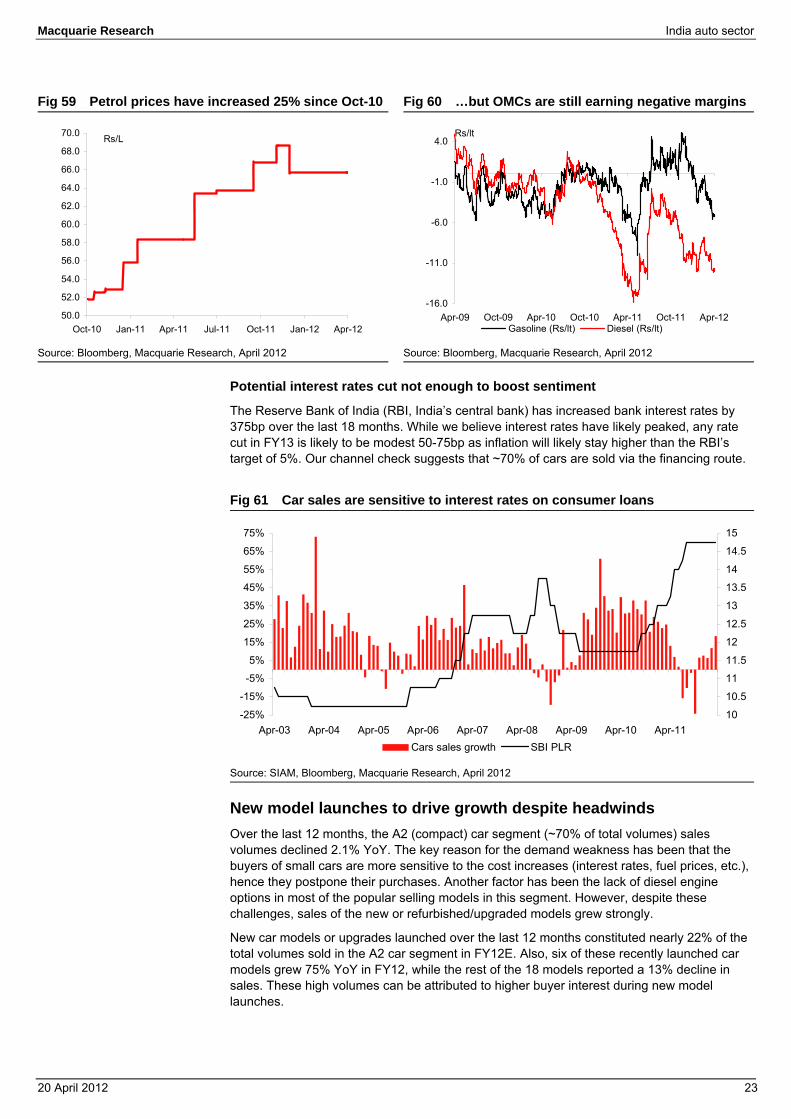

As a result of the surge in global crude oil prices and currency (INR) depreciation, oil marketing companies (OMC) have raised prices seven times in the last 18 months. The total increase in petrol prices has been Rs15/litre (or 25%) between Oct-10 and Apr-12. By contrast, diesel prices have remained broadly flat during the period. As the price differential between petrol and diesel has expanded, we have seen the share of diesel cars sold in India increase.

Since Nov-11, the government has not allowed OMCs to raise the prices of either petrol or diesel for political reasons (state elections, parliament session). As a result, OMCs are losing Rs11/l on petrol and Rs16/l on diesel based on our calculations. We believe OMCs will have to increase the prices of both petrol and diesel after the conclusion of the budget session of parliament (end of May).

29%

18%

8%

22%

12%

1%

25%29%

2%

14%16%

0%

5%

10%

15%

20%

25%

30%

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

E

FY14

E

27%

22%

10%13%

11%

-7%

21%

16% 16%

23%

18%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

E

FY14

E

Macquarie Research India auto sector

20 April 2012 23

Fig 59 Petrol prices have increased 25% since Oct-10 Fig 60 …but OMCs are still earning negative margins

Source: Bloomberg, Macquarie Research, April 2012 Source: Bloomberg, Macquarie Research, April 2012

Potential interest rates cut not enough to boost sentiment

The Reserve Bank of India (RBI, India’s central bank) has increased bank interest rates by 375bp over the last 18 months. While we believe interest rates have likely peaked, any rate cut in FY13 is likely to be modest 50-75bp as inflation will likely stay higher than the RBI’s target of 5%. Our channel check suggests that ~70% of cars are sold via the financing route.

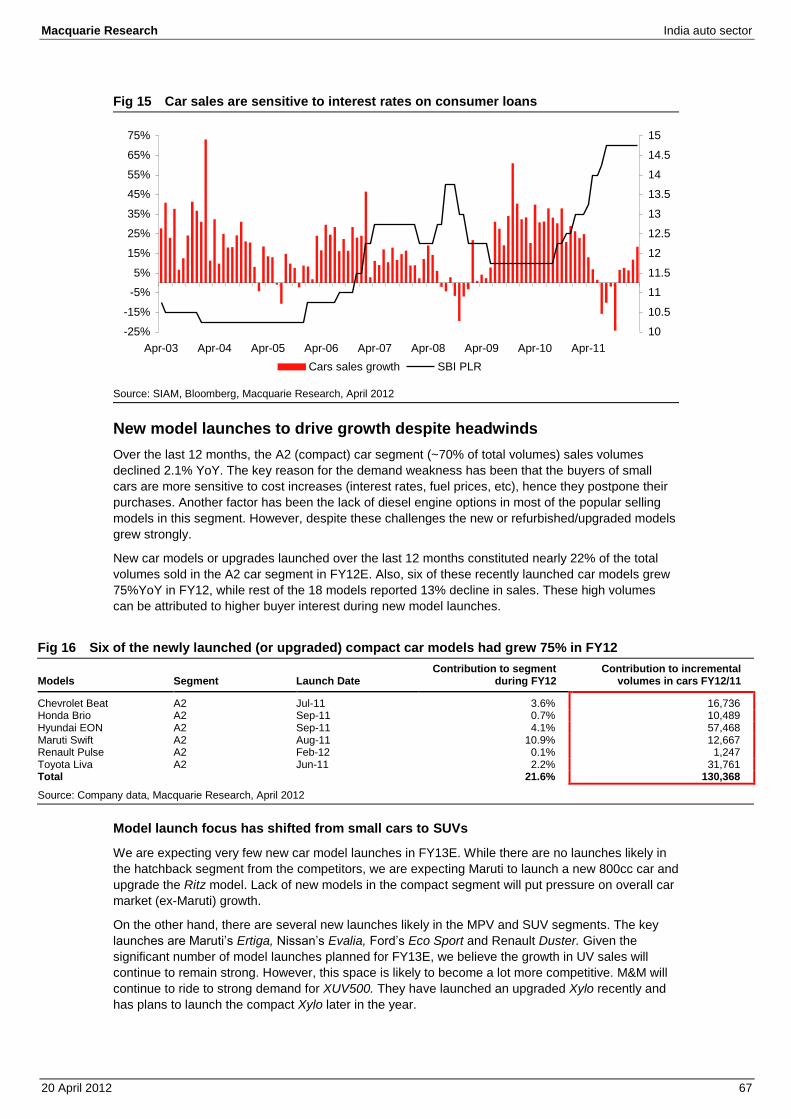

Fig 61 Car sales are sensitive to interest rates on consumer loans

Source: SIAM, Bloomberg, Macquarie Research, April 2012

New model launches to drive growth despite headwinds Over the last 12 months, the A2 (compact) car segment (~70% of total volumes) sales volumes declined 2.1% YoY. The key reason for the demand weakness has been that the buyers of small cars are more sensitive to the cost increases (interest rates, fuel prices, etc.), hence they postpone their purchases. Another factor has been the lack of diesel engine options in most of the popular selling models in this segment. However, despite these challenges, sales of the new or refurbished/upgraded models grew strongly.

New car models or upgrades launched over the last 12 months constituted nearly 22% of the total volumes sold in the A2 car segment in FY12E. Also, six of these recently launched car models grew 75% YoY in FY12, while the rest of the 18 models reported a 13% decline in sales. These high volumes can be attributed to higher buyer interest during new model launches.

50.0

52.0

54.0

56.0

58.0

60.0

62.0

64.0

66.0

68.0

70.0

Oct-10 Jan-11 Apr-11 Jul-11 Oct-11 Jan-12 Apr-12

Rs/L

-16.0

-11.0

-6.0

-1.0

4.0

Apr-09 Oct-09 Apr-10 Oct-10 Apr-11 Oct-11 Apr-12

Rs/lt

Gasoline (Rs/lt) Diesel (Rs/lt)

-25%

-15%

-5%

5%

15%

25%

35%

45%

55%

65%

75%

Apr-03 Apr-04 Apr-05 Apr-06 Apr-07 Apr-08 Apr-09 Apr-10 Apr-1110

10.5

11

11.5

12

12.5

13

13.5

14

14.5

15

Cars sales growth SBI PLR

Macquarie Research India auto sector

20 April 2012 24

Fig 62 Six of the newly launched (or upgraded) compact car models had grew 75% in FY12

Models Segment Launch DateContribution to segment

during FY12 Contribution to incremental

volumes in cars FY12/11

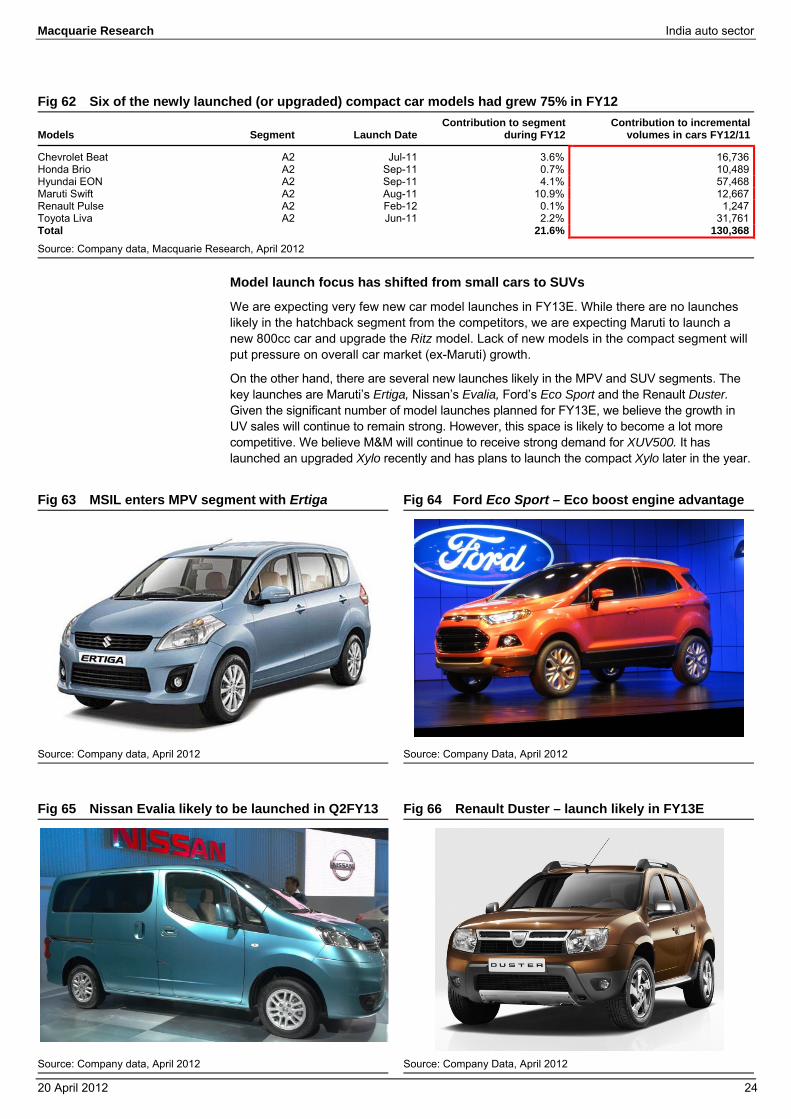

Chevrolet Beat A2 Jul-11 3.6% 16,736Honda Brio A2 Sep-11 0.7% 10,489Hyundai EON A2 Sep-11 4.1% 57,468Maruti Swift A2 Aug-11 10.9% 12,667Renault Pulse A2 Feb-12 0.1% 1,247Toyota Liva A2 Jun-11 2.2% 31,761Total 21.6% 130,368Source: Company data, Macquarie Research, April 2012

Model launch focus has shifted from small cars to SUVs

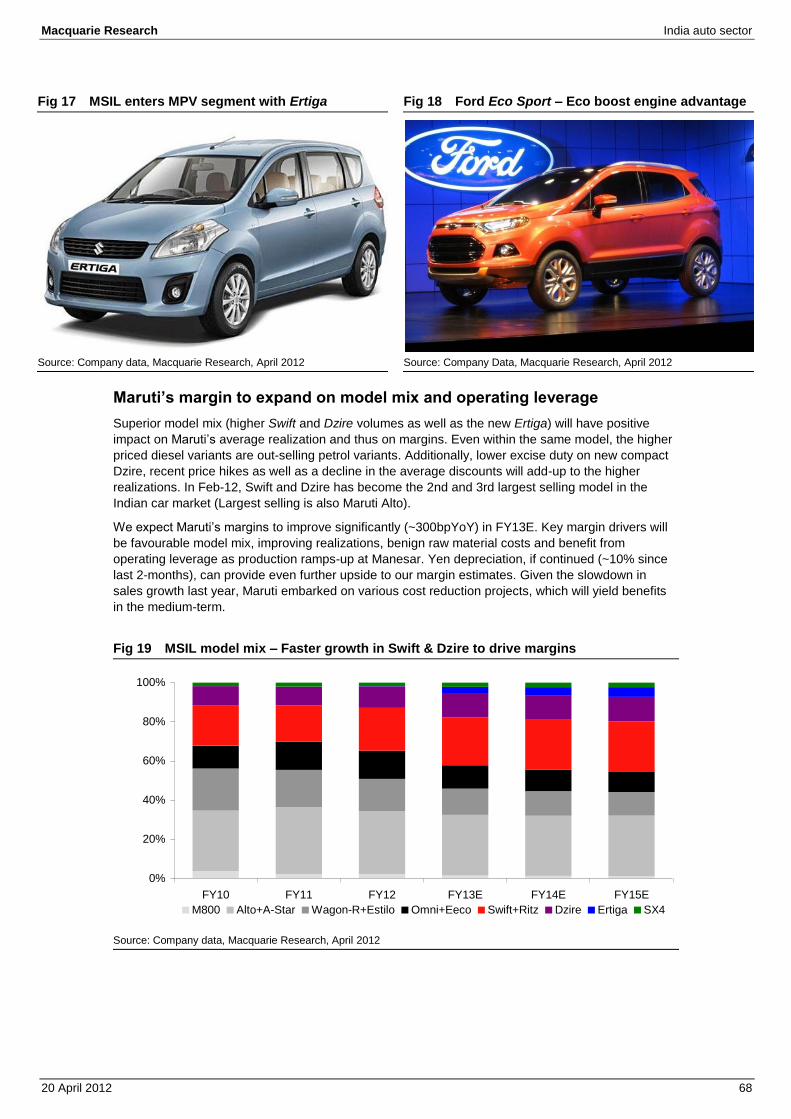

We are expecting very few new car model launches in FY13E. While there are no launches likely in the hatchback segment from the competitors, we are expecting Maruti to launch a new 800cc car and upgrade the Ritz model. Lack of new models in the compact segment will put pressure on overall car market (ex-Maruti) growth.

On the other hand, there are several new launches likely in the MPV and SUV segments. The key launches are Maruti’s Ertiga, Nissan’s Evalia, Ford’s Eco Sport and the Renault Duster. Given the significant number of model launches planned for FY13E, we believe the growth in UV sales will continue to remain strong. However, this space is likely to become a lot more competitive. We believe M&M will continue to receive strong demand for XUV500. It has launched an upgraded Xylo recently and has plans to launch the compact Xylo later in the year.

Fig 63 MSIL enters MPV segment with Ertiga Fig 64 Ford Eco Sport – Eco boost engine advantage

Source: Company data, April 2012 Source: Company Data, April 2012

Fig 65 Nissan Evalia likely to be launched in Q2FY13 Fig 66 Renault Duster – launch likely in FY13E

Source: Company data, April 2012 Source: Company Data, April 2012

Macquarie Research India auto sector

20 April 2012 25

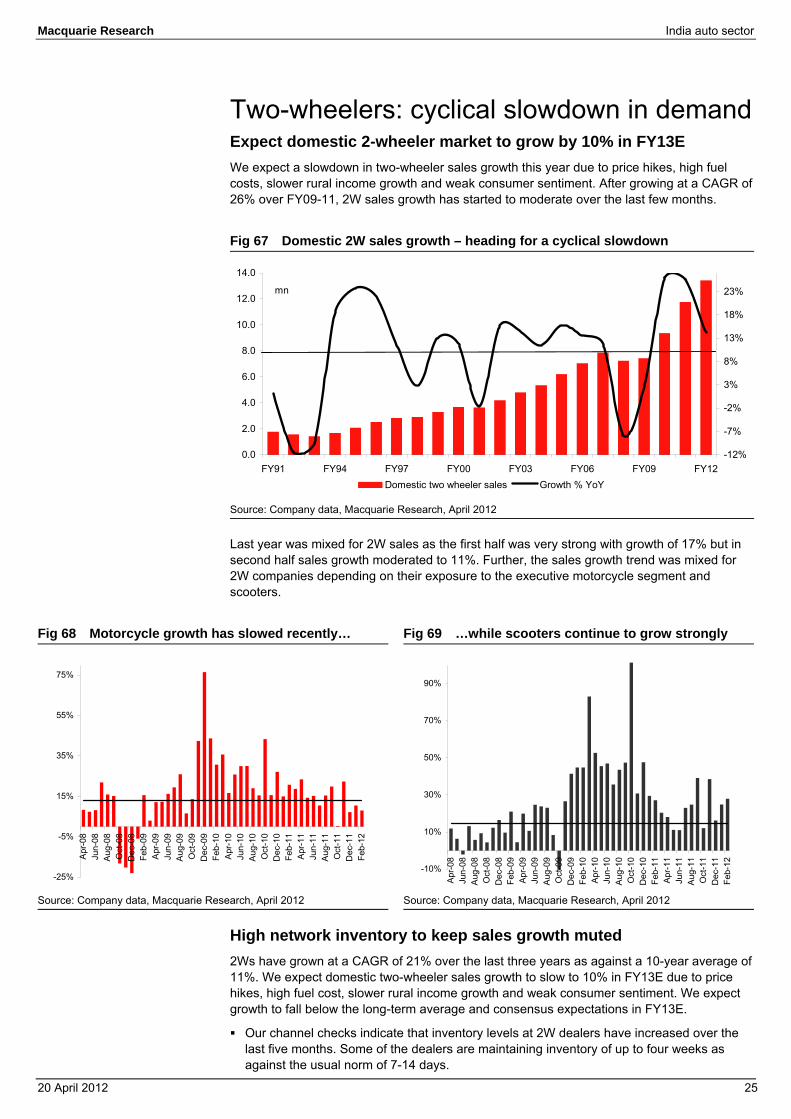

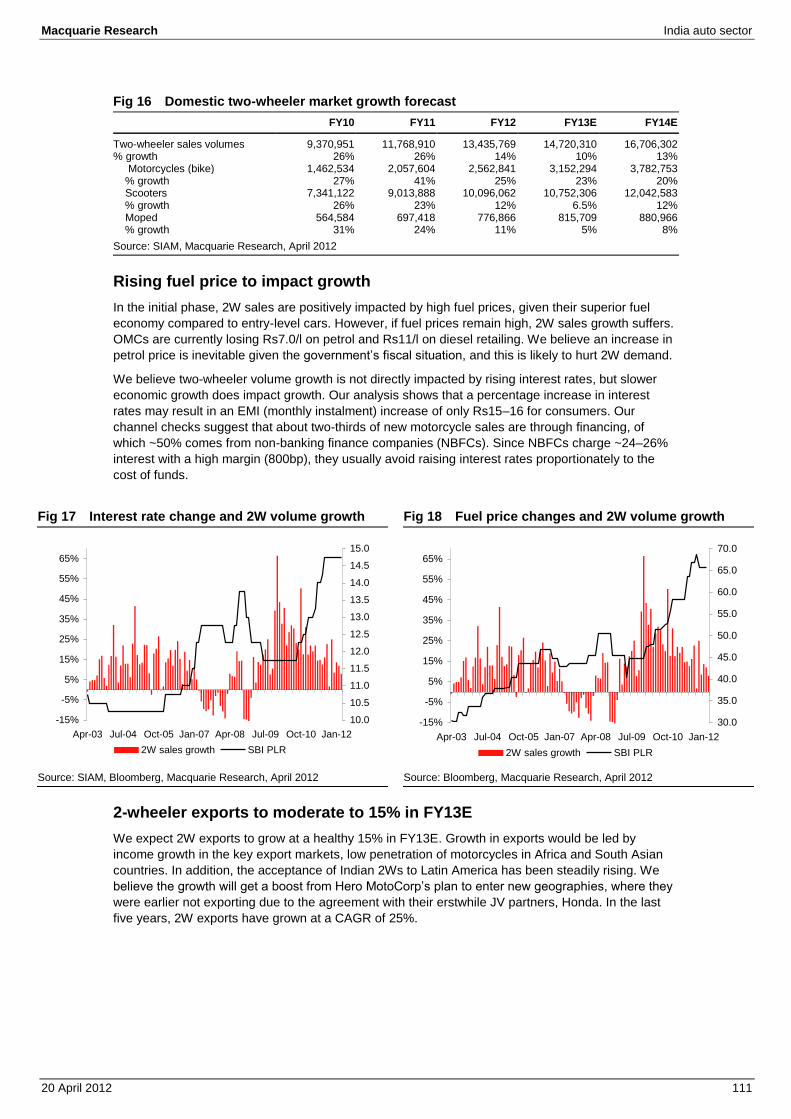

Two-wheelers: cyclical slowdown in demand Expect domestic 2-wheeler market to grow by 10% in FY13E We expect a slowdown in two-wheeler sales growth this year due to price hikes, high fuel costs, slower rural income growth and weak consumer sentiment. After growing at a CAGR of 26% over FY09-11, 2W sales growth has started to moderate over the last few months.

Fig 67 Domestic 2W sales growth – heading for a cyclical slowdown

Source: Company data, Macquarie Research, April 2012

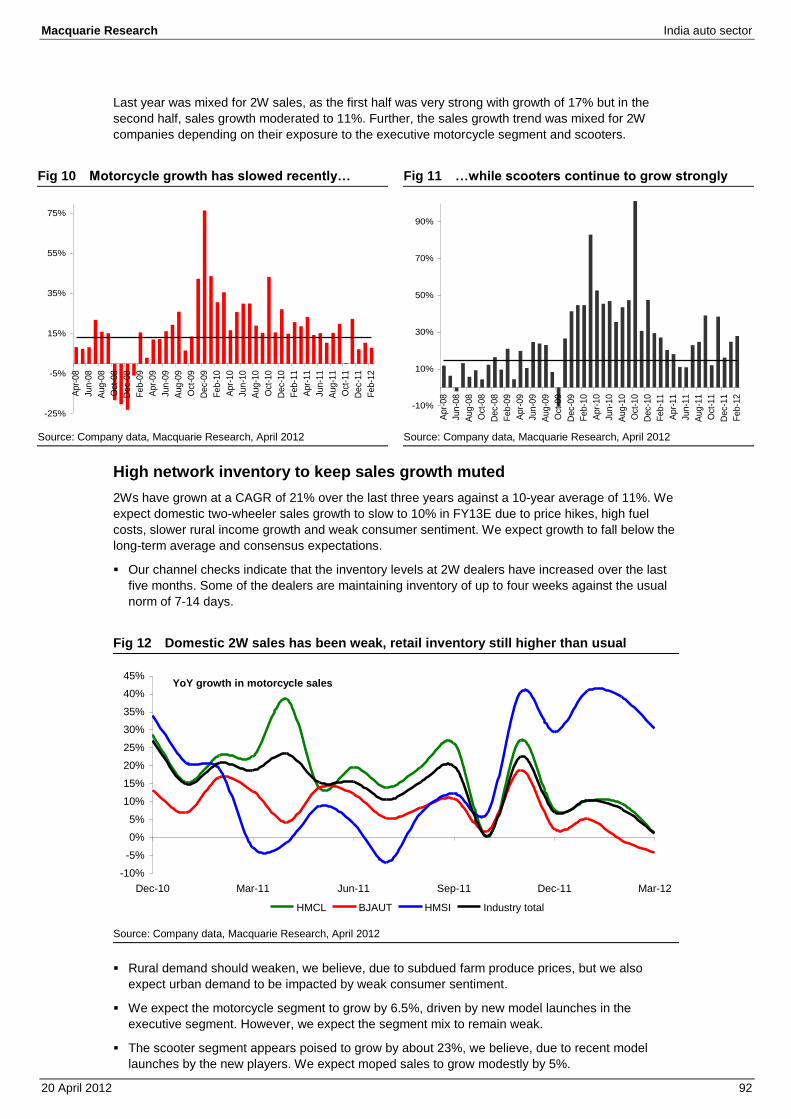

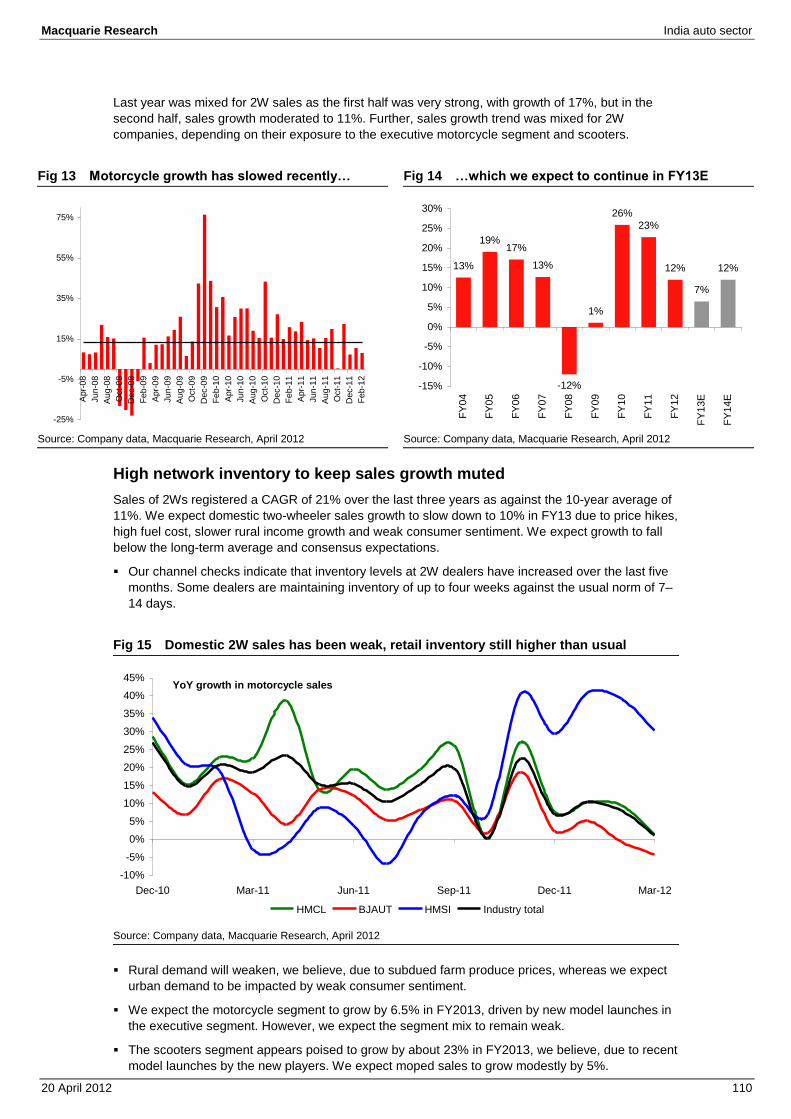

Last year was mixed for 2W sales as the first half was very strong with growth of 17% but in second half sales growth moderated to 11%. Further, the sales growth trend was mixed for 2W companies depending on their exposure to the executive motorcycle segment and scooters.

Fig 68 Motorcycle growth has slowed recently… Fig 69 …while scooters continue to grow strongly

Source: Company data, Macquarie Research, April 2012 Source: Company data, Macquarie Research, April 2012

High network inventory to keep sales growth muted 2Ws have grown at a CAGR of 21% over the last three years as against a 10-year average of 11%. We expect domestic two-wheeler sales growth to slow to 10% in FY13E due to price hikes, high fuel cost, slower rural income growth and weak consumer sentiment. We expect growth to fall below the long-term average and consensus expectations in FY13E.

Our channel checks indicate that inventory levels at 2W dealers have increased over the last five months. Some of the dealers are maintaining inventory of up to four weeks as against the usual norm of 7-14 days.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

FY91 FY94 FY97 FY00 FY03 FY06 FY09 FY12-12%

-7%

-2%

3%

8%

13%

18%

23%

Domestic two wheeler sales Growth % YoY

mn

-25%

-5%

15%

35%

55%

75%

Apr

-08

Jun-

08A

ug-0

8O

ct-0

8D

ec-0

8Fe

b-09

Apr

-09

Jun-

09A

ug-0

9O

ct-0

9D

ec-0

9Fe

b-10

Apr

-10

Jun-

10A

ug-1

0O

ct-1

0D

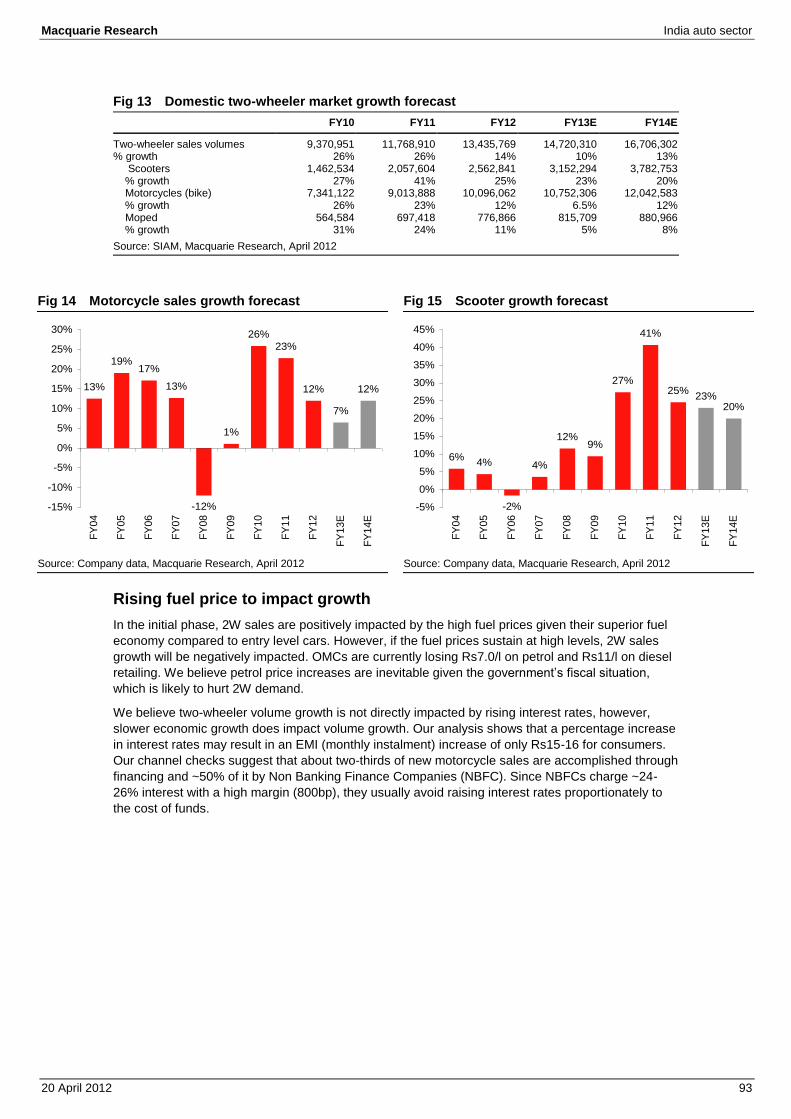

ec-1

0Fe

b-11

Apr

-11

Jun-

11A

ug-1

1O

ct-1

1D

ec-1

1Fe

b-12

-10%

10%

30%

50%

70%

90%

Apr-0

8Ju

n-08

Aug

-08

Oct

-08

Dec

-08

Feb-

09Ap

r-09

Jun-

09A

ug-0

9O

ct-0

9D

ec-0

9Fe

b-10

Apr-1

0Ju

n-10

Aug

-10

Oct

-10

Dec

-10

Feb-

11Ap

r-11

Jun-

11A

ug-1

1O

ct-1

1D

ec-1

1Fe

b-12

Macquarie Research India auto sector

20 April 2012 26

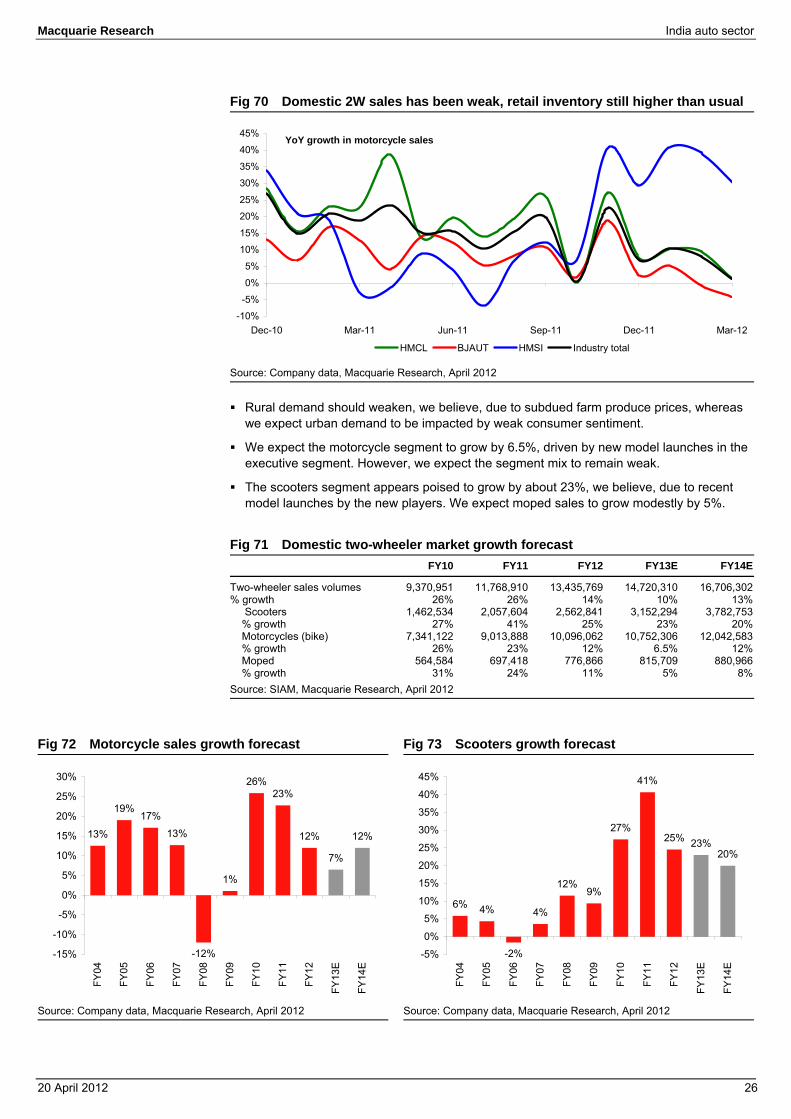

Fig 70 Domestic 2W sales has been weak, retail inventory still higher than usual

Source: Company data, Macquarie Research, April 2012

Rural demand should weaken, we believe, due to subdued farm produce prices, whereas we expect urban demand to be impacted by weak consumer sentiment.

We expect the motorcycle segment to grow by 6.5%, driven by new model launches in the executive segment. However, we expect the segment mix to remain weak.

The scooters segment appears poised to grow by about 23%, we believe, due to recent model launches by the new players. We expect moped sales to grow modestly by 5%.

Fig 71 Domestic two-wheeler market growth forecast FY10 FY11 FY12 FY13E FY14E

Two-wheeler sales volumes 9,370,951 11,768,910 13,435,769 14,720,310 16,706,302% growth 26% 26% 14% 10% 13% Scooters 1,462,534 2,057,604 2,562,841 3,152,294 3,782,753 % growth 27% 41% 25% 23% 20% Motorcycles (bike) 7,341,122 9,013,888 10,096,062 10,752,306 12,042,583 % growth 26% 23% 12% 6.5% 12% Moped 564,584 697,418 776,866 815,709 880,966 % growth 31% 24% 11% 5% 8%Source: SIAM, Macquarie Research, April 2012

Fig 72 Motorcycle sales growth forecast Fig 73 Scooters growth forecast

Source: Company data, Macquarie Research, April 2012 Source: Company data, Macquarie Research, April 2012

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Dec-10 Mar-11 Jun-11 Sep-11 Dec-11 Mar-12

HMCL BJAUT HMSI Industry total

YoY growth in motorcycle sales

13%

19%17%

13%

-12%

1%

26%23%

12%

7%

12%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

E

FY14

E

6% 4%

-2%

4%

12%9%

27%

41%

25% 23%20%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

E

FY14

E

Macquarie Research India auto sector

20 April 2012 27

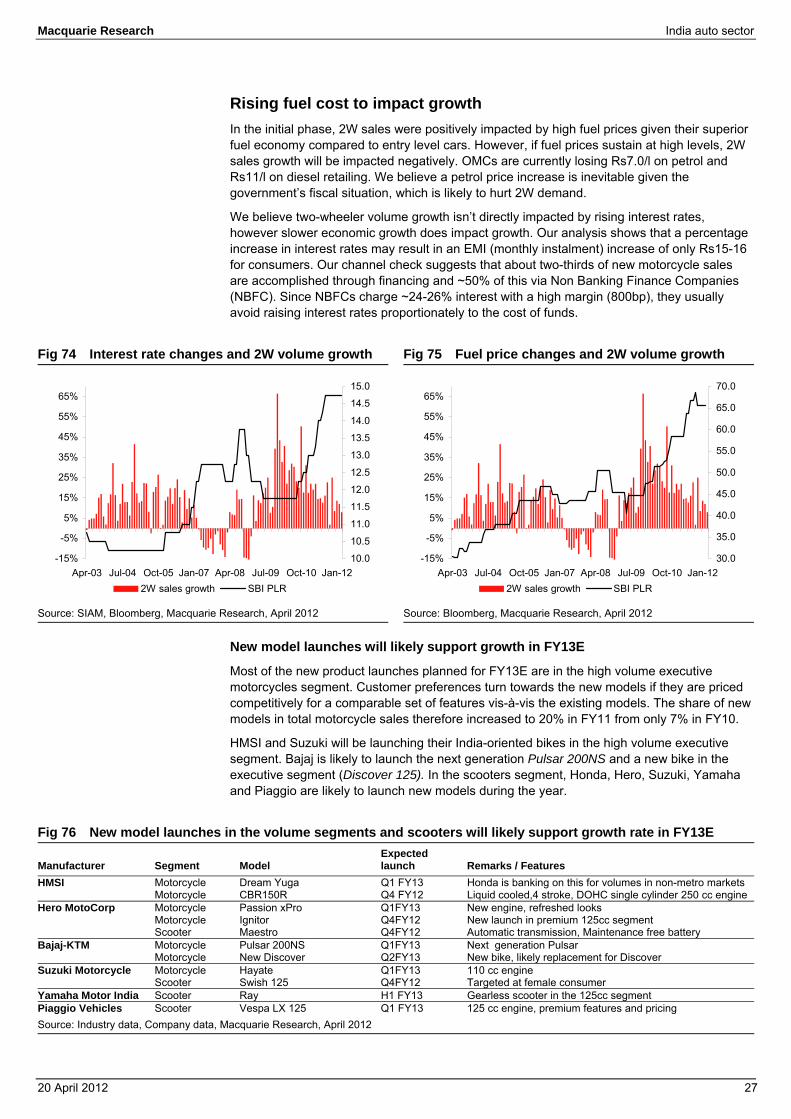

Rising fuel cost to impact growth In the initial phase, 2W sales were positively impacted by high fuel prices given their superior fuel economy compared to entry level cars. However, if fuel prices sustain at high levels, 2W sales growth will be impacted negatively. OMCs are currently losing Rs7.0/l on petrol and Rs11/l on diesel retailing. We believe a petrol price increase is inevitable given the government’s fiscal situation, which is likely to hurt 2W demand.

We believe two-wheeler volume growth isn’t directly impacted by rising interest rates, however slower economic growth does impact growth. Our analysis shows that a percentage increase in interest rates may result in an EMI (monthly instalment) increase of only Rs15-16 for consumers. Our channel check suggests that about two-thirds of new motorcycle sales are accomplished through financing and ~50% of this via Non Banking Finance Companies (NBFC). Since NBFCs charge ~24-26% interest with a high margin (800bp), they usually avoid raising interest rates proportionately to the cost of funds.

Fig 74 Interest rate changes and 2W volume growth Fig 75 Fuel price changes and 2W volume growth

Source: SIAM, Bloomberg, Macquarie Research, April 2012 Source: Bloomberg, Macquarie Research, April 2012

New model launches will likely support growth in FY13E

Most of the new product launches planned for FY13E are in the high volume executive motorcycles segment. Customer preferences turn towards the new models if they are priced competitively for a comparable set of features vis-à-vis the existing models. The share of new models in total motorcycle sales therefore increased to 20% in FY11 from only 7% in FY10.

HMSI and Suzuki will be launching their India-oriented bikes in the high volume executive segment. Bajaj is likely to launch the next generation Pulsar 200NS and a new bike in the executive segment (Discover 125). In the scooters segment, Honda, Hero, Suzuki, Yamaha and Piaggio are likely to launch new models during the year.

Fig 76 New model launches in the volume segments and scooters will likely support growth rate in FY13E Expected

launch

Manufacturer Segment Model Remarks / Features HMSI Motorcycle Dream Yuga Q1 FY13 Honda is banking on this for volumes in non-metro markets Motorcycle CBR150R Q4 FY12 Liquid cooled,4 stroke, DOHC single cylinder 250 cc engine Hero MotoCorp Motorcycle Passion xPro Q1FY13 New engine, refreshed looks Motorcycle Ignitor Q4FY12 New launch in premium 125cc segment Scooter Maestro Q4FY12 Automatic transmission, Maintenance free battery Bajaj-KTM Motorcycle Pulsar 200NS Q1FY13 Next generation Pulsar Motorcycle New Discover Q2FY13 New bike, likely replacement for Discover Suzuki Motorcycle Motorcycle Hayate Q1FY13 110 cc engine Scooter Swish 125 Q4FY12 1Targeted at female consumer Yamaha Motor India Scooter Ray H1 FY13 Gearless scooter in the 125cc segment Piaggio Vehicles Scooter Vespa LX 125 Q1 FY13 125 cc engine, premium features and pricing Source: Industry data, Company data, Macquarie Research, April 2012

-15%

-5%

5%

15%

25%

35%

45%

55%

65%

Apr-03 Jul-04 Oct-05 Jan-07 Apr-08 Jul-09 Oct-10 Jan-1210.0

10.5

11.0

11.5

12.0

12.5

13.0

13.5

14.0

14.5

15.0

2W sales growth SBI PLR

-15%

-5%

5%

15%

25%

35%

45%

55%

65%

Apr-03 Jul-04 Oct-05 Jan-07 Apr-08 Jul-09 Oct-10 Jan-1230.0

35.0

40.0

45.0

50.0

55.0

60.0

65.0

70.0

2W sales growth SBI PLR

Macquarie Research India auto sector

20 April 2012 28

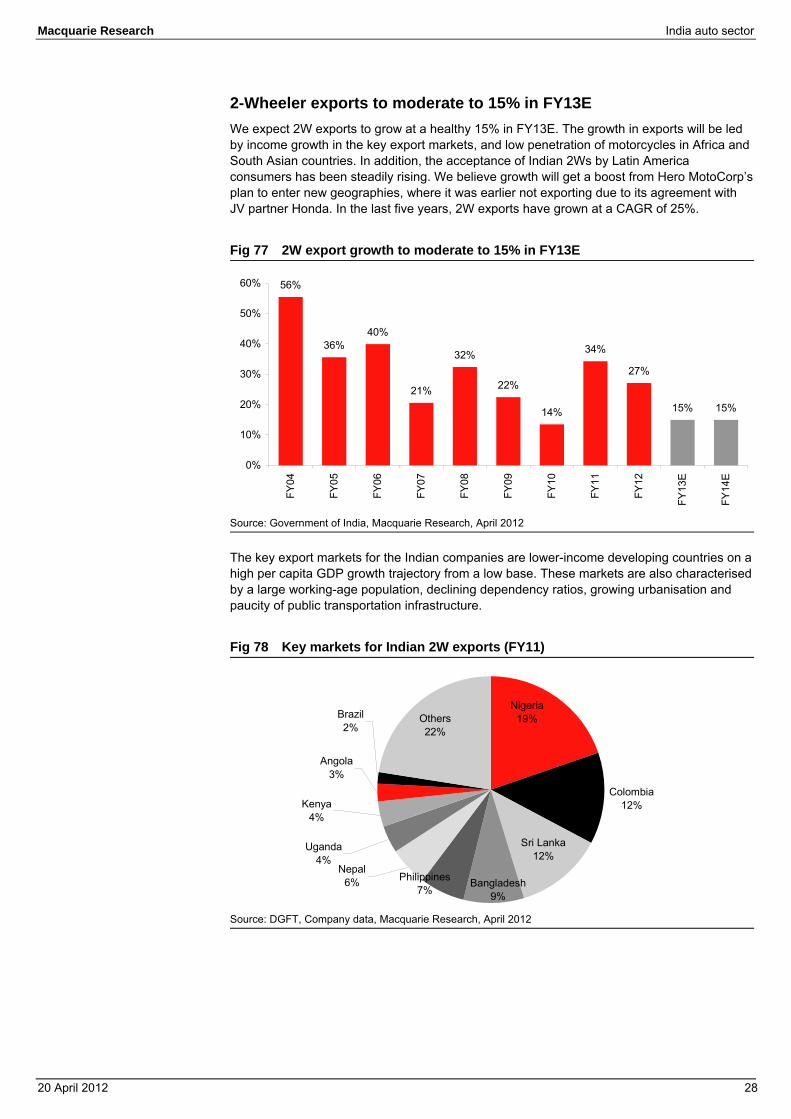

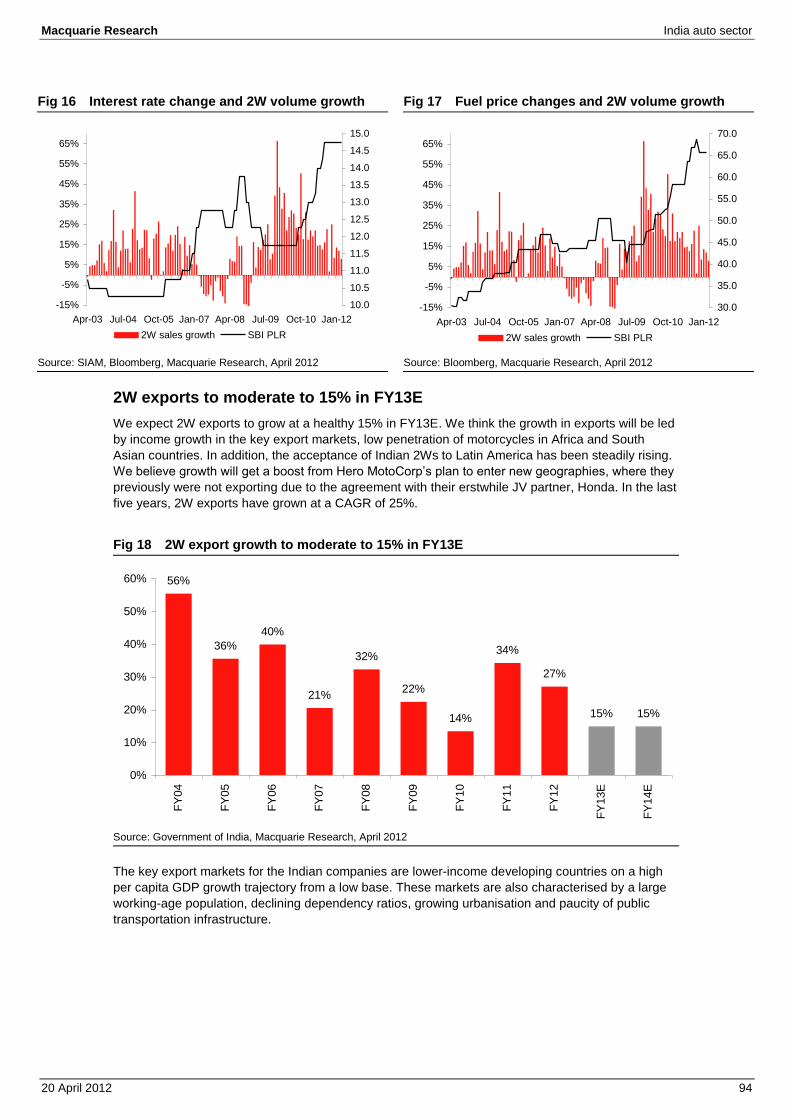

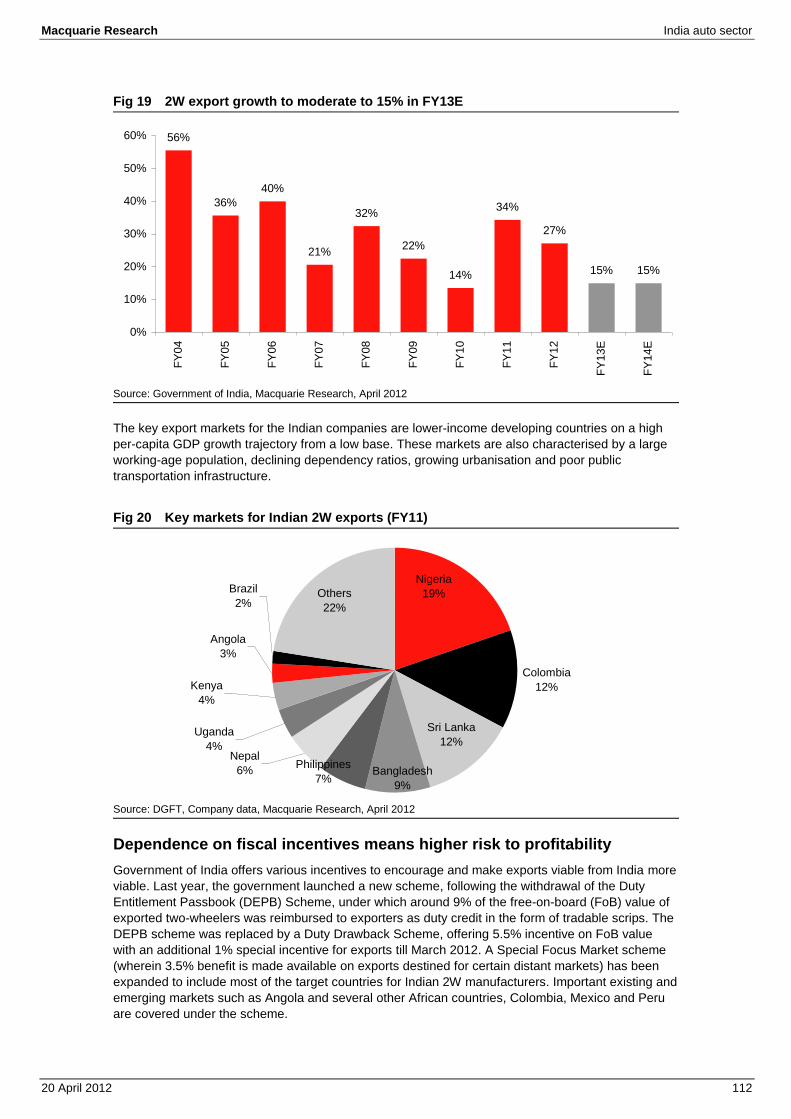

2-Wheeler exports to moderate to 15% in FY13E We expect 2W exports to grow at a healthy 15% in FY13E. The growth in exports will be led by income growth in the key export markets, and low penetration of motorcycles in Africa and South Asian countries. In addition, the acceptance of Indian 2Ws by Latin America consumers has been steadily rising. We believe growth will get a boost from Hero MotoCorp’s plan to enter new geographies, where it was earlier not exporting due to its agreement with JV partner Honda. In the last five years, 2W exports have grown at a CAGR of 25%.

Fig 77 2W export growth to moderate to 15% in FY13E

Source: Government of India, Macquarie Research, April 2012

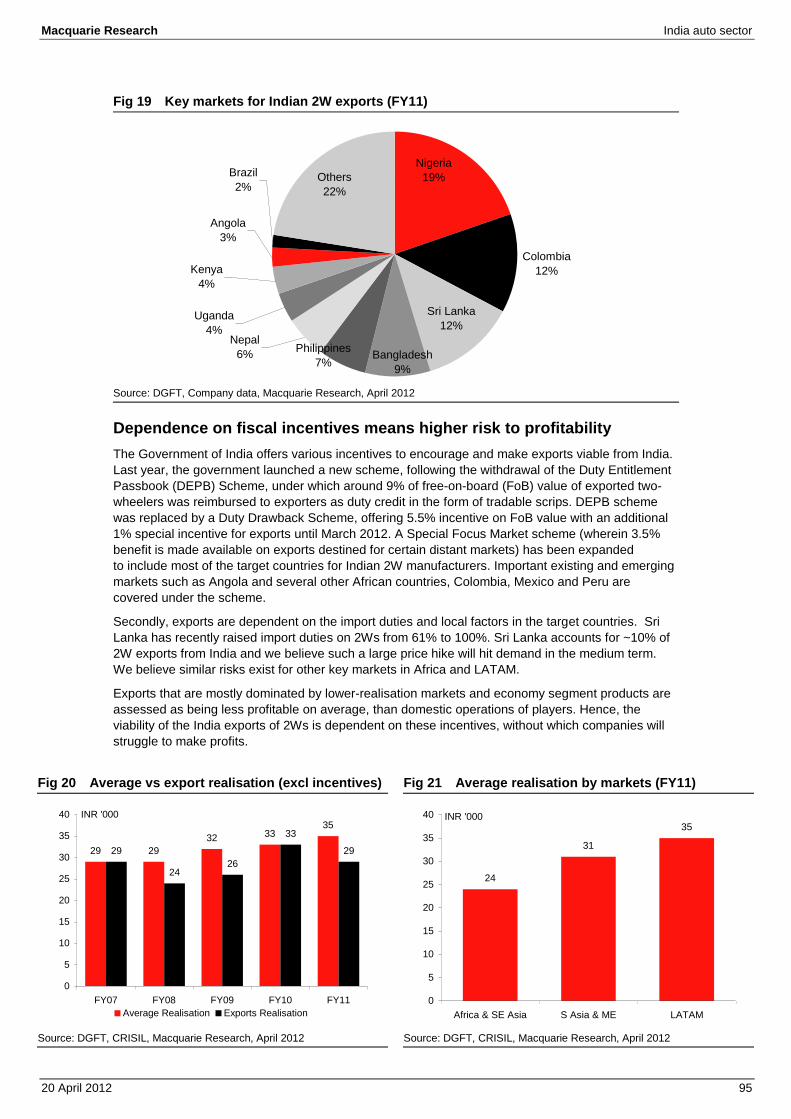

The key export markets for the Indian companies are lower-income developing countries on a high per capita GDP growth trajectory from a low base. These markets are also characterised by a large working-age population, declining dependency ratios, growing urbanisation and paucity of public transportation infrastructure.

Fig 78 Key markets for Indian 2W exports (FY11)

Source: DGFT, Company data, Macquarie Research, April 2012

56%

36%40%

21%

32%

22%

14%

34%

27%

15% 15%

0%

10%

20%

30%

40%

50%

60%FY

04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

E

FY14

E

Colombia12%

Bangladesh9%

Philippines7%

Nepal6%

Uganda4%

Kenya4%

Angola3%

Brazil2%

Sri Lanka12%

Others22%

Nigeria19%

Macquarie Research India auto sector

20 April 2012 29

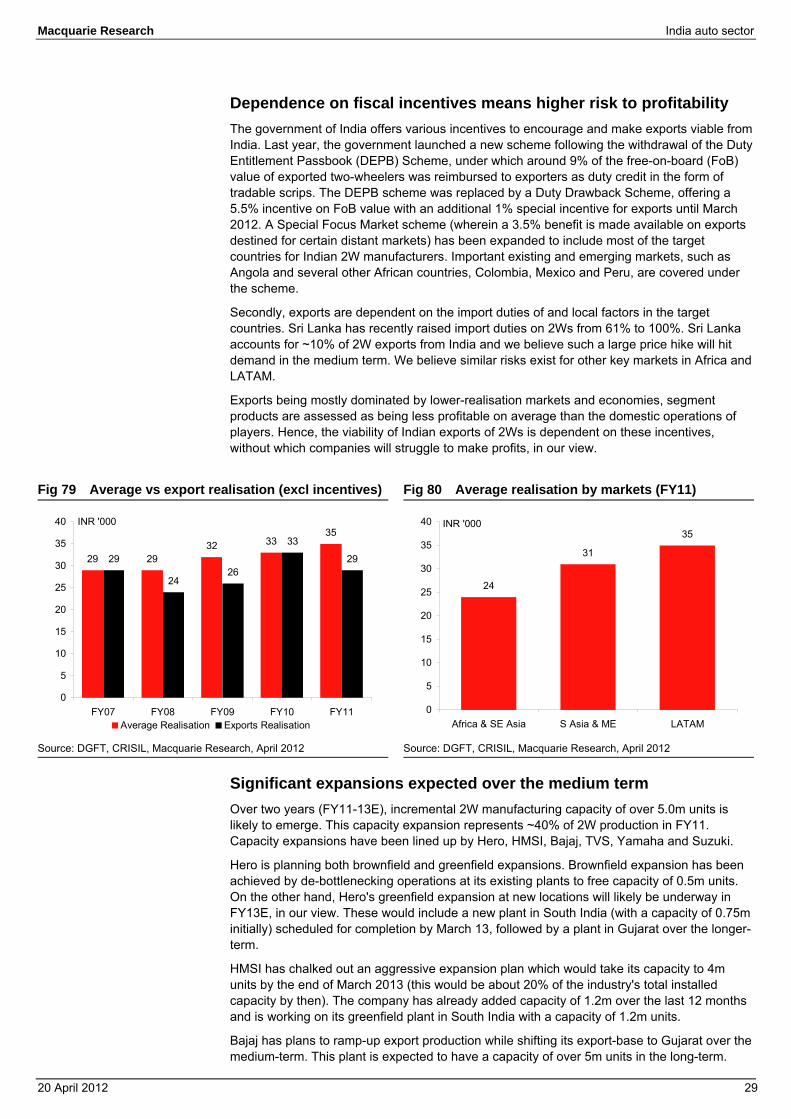

Dependence on fiscal incentives means higher risk to profitability The government of India offers various incentives to encourage and make exports viable from India. Last year, the government launched a new scheme following the withdrawal of the Duty Entitlement Passbook (DEPB) Scheme, under which around 9% of the free-on-board (FoB) value of exported two-wheelers was reimbursed to exporters as duty credit in the form of tradable scrips. The DEPB scheme was replaced by a Duty Drawback Scheme, offering a 5.5% incentive on FoB value with an additional 1% special incentive for exports until March 2012. A Special Focus Market scheme (wherein a 3.5% benefit is made available on exports destined for certain distant markets) has been expanded to include most of the target countries for Indian 2W manufacturers. Important existing and emerging markets, such as Angola and several other African countries, Colombia, Mexico and Peru, are covered under the scheme.

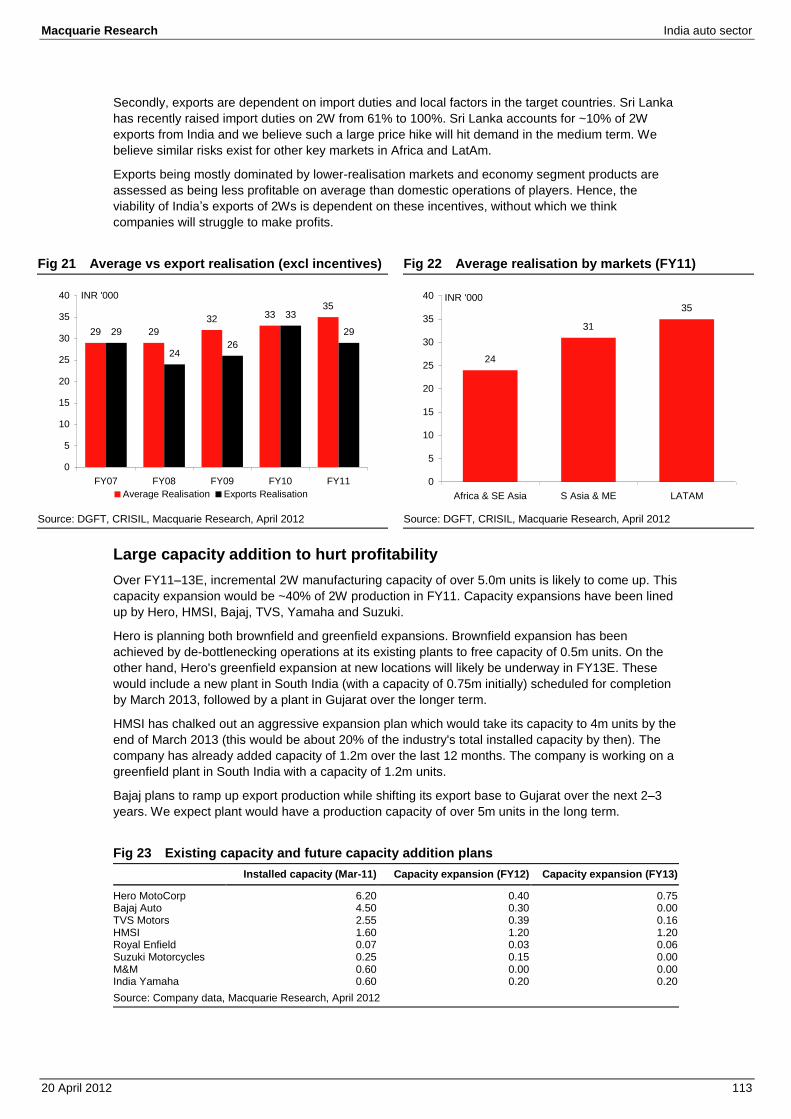

Secondly, exports are dependent on the import duties of and local factors in the target countries. Sri Lanka has recently raised import duties on 2Ws from 61% to 100%. Sri Lanka accounts for ~10% of 2W exports from India and we believe such a large price hike will hit demand in the medium term. We believe similar risks exist for other key markets in Africa and LATAM.

Exports being mostly dominated by lower-realisation markets and economies, segment products are assessed as being less profitable on average than the domestic operations of players. Hence, the viability of Indian exports of 2Ws is dependent on these incentives, without which companies will struggle to make profits, in our view.

Fig 79 Average vs export realisation (excl incentives) Fig 80 Average realisation by markets (FY11)

Source: DGFT, CRISIL, Macquarie Research, April 2012 Source: DGFT, CRISIL, Macquarie Research, April 2012

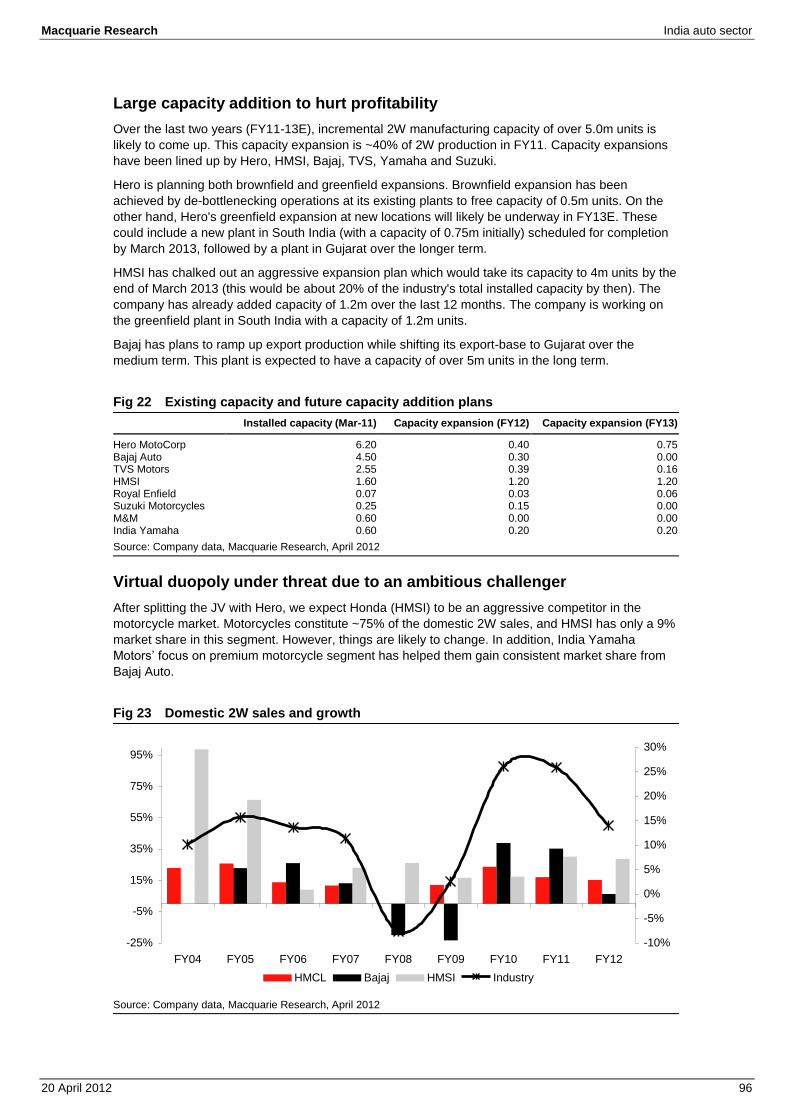

Significant expansions expected over the medium term Over two years (FY11-13E), incremental 2W manufacturing capacity of over 5.0m units is likely to emerge. This capacity expansion represents ~40% of 2W production in FY11. Capacity expansions have been lined up by Hero, HMSI, Bajaj, TVS, Yamaha and Suzuki.

Hero is planning both brownfield and greenfield expansions. Brownfield expansion has been achieved by de-bottlenecking operations at its existing plants to free capacity of 0.5m units. On the other hand, Hero's greenfield expansion at new locations will likely be underway in FY13E, in our view. These would include a new plant in South India (with a capacity of 0.75m initially) scheduled for completion by March 13, followed by a plant in Gujarat over the longer-term.

HMSI has chalked out an aggressive expansion plan which would take its capacity to 4m units by the end of March 2013 (this would be about 20% of the industry's total installed capacity by then). The company has already added capacity of 1.2m over the last 12 months and is working on its greenfield plant in South India with a capacity of 1.2m units.

Bajaj has plans to ramp-up export production while shifting its export-base to Gujarat over the medium-term. This plant is expected to have a capacity of over 5m units in the long-term.

29 2932 33

35

29

2426

33

29

0

5

10

15

20

25

30

35

40

FY07 FY08 FY09 FY10 FY11

INR '000

Average Realisation Exports Realisation

24

31

35

0

5

10

15

20

25

30

35

40

Africa & SE Asia S Asia & ME LATAM

INR '000

Macquarie Research India auto sector

20 April 2012 30

Fig 81 Existing capacity and future capacity addition plans Installed capacity (Mar-11) Capacity expansion (FY12) Capacity expansion (FY13)

Hero MotoCorp 6.20 0.40 0.75Bajaj Auto 4.50 0.30 0.00TVS Motors 2.55 0.39 0.16HMSI 1.60 1.20 1.20Royal Enfield 0.07 0.03 0.06Suzuki Motorcycles 0.25 0.15 0.00M&M 0.60 0.00 0.00India Yamaha 0.60 0.20 0.20Source: Company data, Macquarie Research, April 2012

Macquarie Research India auto sector

20 April 2012 31

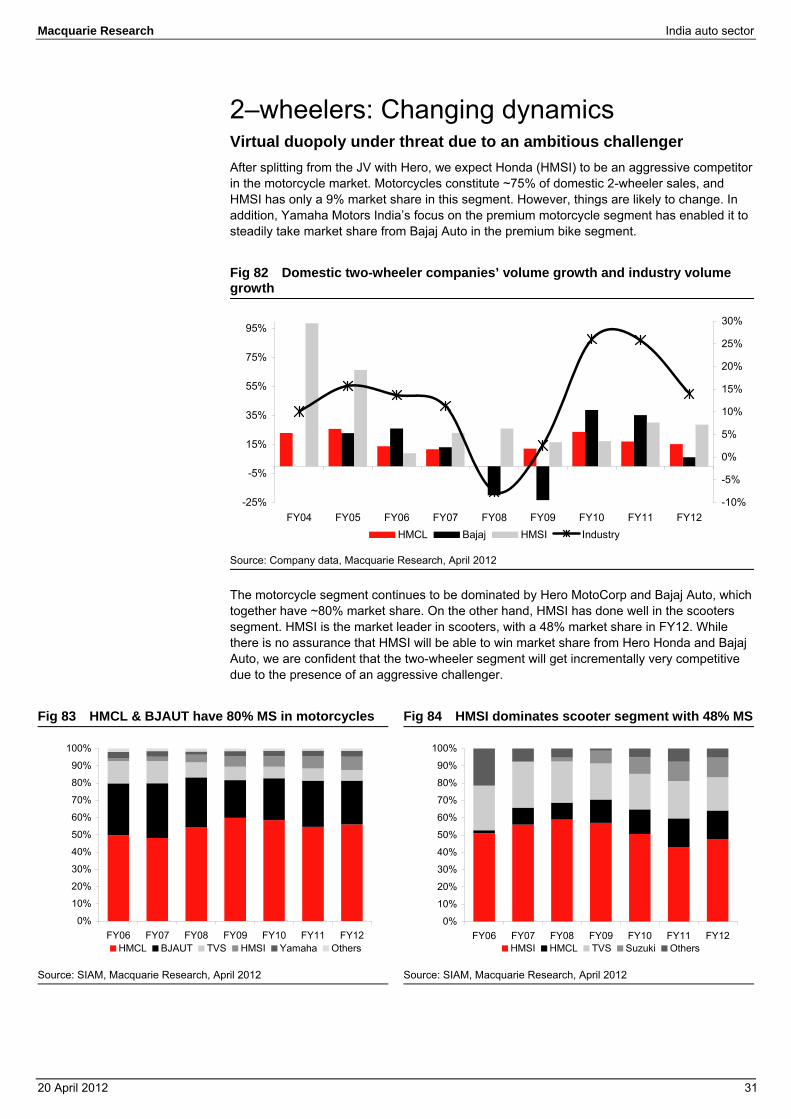

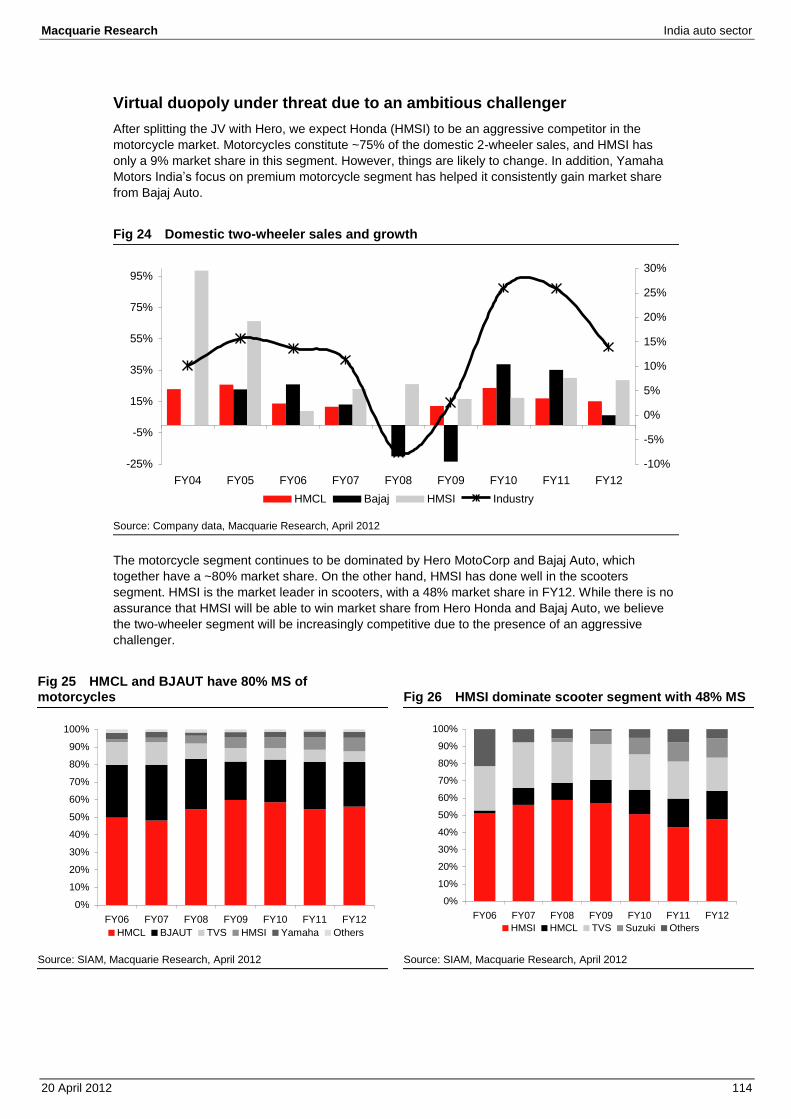

2–wheelers: Changing dynamics Virtual duopoly under threat due to an ambitious challenger After splitting from the JV with Hero, we expect Honda (HMSI) to be an aggressive competitor in the motorcycle market. Motorcycles constitute ~75% of domestic 2-wheeler sales, and HMSI has only a 9% market share in this segment. However, things are likely to change. In addition, Yamaha Motors India’s focus on the premium motorcycle segment has enabled it to steadily take market share from Bajaj Auto in the premium bike segment.

Fig 82 Domestic two-wheeler companies’ volume growth and industry volume growth

Source: Company data, Macquarie Research, April 2012