Embed Size (px)

Citation preview

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 1/28

SECTOR ANALYSIS OF

BANKING SECTOR

Project Report Submitted to (SIBAR)

In Partial Fulfillment of Requirement for the Award of

PGDM (Marketing)

BY

KRATIKA MATHUR

UNDER THE GUIDENCE OF

PROF. SHITAL BHUSARE

Sinhgad Institute Of Business Administration And Research,

Kondhwa (Bk), Pune.

2010-2012

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 2/28

CONTENTS:

1. INTRODUCTION

2. OVERVIEW OF THE SECTOR

3. GLOBAL SCENARIO

4. NATIONAL SCENARIO/ LOCAL; KEY PLAYERS IN THE

SECTOR

5. FUTURE GROWTH OPPORTUNITIES

6. OBSERVATIONS FROM PERSONAL INTERACTION

WITH COMPANY PROFESSIONALS

7. CONCLUSIONS

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 3/28

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 4/28

INTRODUCTION

Modem banking developed around 500 years ago in other countries and 200 years ago

in India. The Indianfinancial system comprises a vast network of different banks. The

banking sector is the core segment indecidingthe progress of the entire economy of

the country. Activities of a modem economy are significantly influenced by the

functions and services of banks and became an indispensable part of socio-economic

life of the people.Banks not only accept the deposits from the public and deploy large

amounts of uncollateralised public fundsin a fiduciary capacity, but also leverage such

funds through the process of credit creation. In India, the bankingsector was restricted

mainly to the urban areas and neglected in the rural and semi-urban areas. After

thenationalization of 14 major banks in 1969 and six more in 1980, the scenario

changed. Since then the bankingsector in India has played a pivotal role in the Indian

economy. The Indian commercial system comprises two groups i.e. Scheduled Banks

and the other Non-Scheduled Banks. Scheduled Banks are those banks included inthe

second schedule of the banking regulation Act, 1965 and satisfying the conditions laid

down by the schedule.Non-Scheduled Banks refer to those that are not included in the

second schedule of the Banking regulation Actof 1965 and do not satisfy the

conditions laid down by that schedule. The primary objective of this study is

toanalyse the performance of Scheduled Commercial Banks since 2000 and after. The

indicators selected to studyare aggregate deposits, total credits, investments made by

the banks and priority sector lending etc. The paper isorganized as follows:. At

present, Indian public sector banksare performing well and they are at par with the

best banks in the world.

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 5/28

OVERVIEW OF THE SECTOR

Indian Banking Sector: A Retrospect

The Indian financial system consists of different types of financial institutions which

are responsible for thedevelopment of the country's economy. Financial institutions

can broadly be classified into banking andnon-banking institutions. Banking

institutions are of three types: Commercial Banks, Industrial or InvestmentBanks and

Rural Banks. The most active sector of the Indian money market is the commercial

banking sector.Commercial banks in India can be classified into three groups; PublicSector, Private Sector and Foreign Banks.The majority of commercial banking in

India is in the public sector with the State Bank of India and itsassociated banks. After

liberalization, several private sector banks and foreign banks were allowed to open

theirbusiness in the Indian financial system.Modem banking in India was developed

during the British Era. In the first half of the 19th century, the BritishEast India

Company established three banks-the Bank of Bengal in 1809, the Bank of Bombay in

1840 and theBank of Madras in 1843 and then these three banks were amalgamated

into a new bank called Imperial Bank.Later it was taken over by the State Bank of

India hi 1955. For the purpose of assessment of performance ofbanks in India, the

Reserve Bank of India which was established in 1935, categories them as a Public

SectorBanks, Old Private Sector Banks, New Private Sector Banks and Foreign

Banks.

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 6/28

Commercial Banks and its Structure

Commercial banks are the oldest of all types of banks. They form the base on which

other types of banksdeveloped. Commercial banks constitute the larger part of the

total banking system and these banks play a vitalrole in the country's economy and for

the general public. The commercial banking activities have a verypowerful and strong

influence on the Indian financial system. In India, commercial banks are established

as jointstock companies with the profit motive. These banks provide short-term

financial services to trade, smallindustry, agriculture, service sector and the general

public. They accept chequable deposits called demand deposits and facilitate an easy

payment mechanism. Commercial banks pool small savings and canalize the sameto

all the productive investments. The commercial banking structure in India consists of

Scheduled CommercialBanks and Non- Scheduled Commercial Batiks. Scheduled

Commercial Banks constitute those banks whichhave been included in the second

schedule of the Reserve Bank of India (RBI) Act, 1934. To become ascheduled bank,

the bank has to satisfy a few conditions. Scheduled Commercial Banks enjoy several

advantagesfrom the Reserve Bank of India and can get loans in times of need.

Banking Sector Reforms in India

The banking sector in India has undergone remarkable changes. In 1969, 14 major

banks were nationalized andin 1980, 6 major private sector banks were taken over by

the government. The government did not nationalizethe banks whose deposits were

less than Rs.5O crore. Nationalization of commercial banks in 1968 and 1980 wasa

mixed blessing to the Indian banking sector.

Evolution of commercial banking in India is unique in the sense that during a span of

around30 years following nationalization it has emerged as the single most important

financialintermediary of the country engulfing all sections of people. Before that

Indian BankingSystem experienced a phase of regulated growth for the first time

during 1949 to 1968.Enactment of Banking Companies Act in 1949, formation of

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 7/28

term lending institutions tofinance industrial sector and the appointment of the

National Credit Council in 1967 for thenecessary flow of bank credit to the preferred

sectors of the economy etc. were importantdevelopments to be noted. It should be

mentioned that till the late 60s agricultural sector wasnot supported by the banking

system in any form. Total bank branches numbering 4288 as atDecember 1947 were

concentrated in urban areas primarily having deposits of Rs.1164 croreas against the

advance of Rs. 531 crore.

Indian banking system underwent sea changes after nationalisation in all spheres of

itsactivities. Geographical expansion was the most important among other

developments. Forinstance, during 1969 and March 1999, as many as 56,857 new

branches were opened. On theeve of bank nationalisation, the total number of branches existing throughout the country wasonly 8,261. The population served per

branch was as high as 65,000. The number of branchesoperating at the end of March

1999 rose to 65,118 and increased further to 66,255 inSeptember 2001. Out of the

56,857 new branches opened during the last 30 years, 31,024branches were opened in

rural areas, of which 30,347 branches were opened during June1969 to March 1989.

The branches in rural areas now account for 50.46% of the total numberof branches as

compared to 22.17% as at June-end 1969. The population per office has comedown

abruptly to 13,000. Aggregate deposits of the banking system crossed the 10

millionmark at June end 2001 and reached Rs.1011461 crore on September 2001 from

a meagre amount of Rs.4665 crore at June 1969. At the time of independence, it was

only Rs.1164crore. The credit disbursement pattern of the banks also recorded

remarkable changes both inits functional and geographical coverage during the last

three decades. Total bank advanceshave increased from Rs.3, 609 crore at the end of

June 1969 to Rs.3, 89,460 crore at the endof March 1999 and further to Rs.567707

crore in September 2001. C-D ratio has improvedsignificantly from a mere 45.62% to

77.36% from 1947 to 1969 indicating a massive creditoff take following

nationalisation.

Along with the massive credit expansion, therehas been appreciable change in the

directionof credit flow. The share of rural credit increased from Rs.54 crores as at

June 1969 to Rs.41,193crores as at March-end 1999, and an annual average growth of

24.99%. The share ofcredit in rural areas increased from 1.5% to 14.6% as at March-

end 1989 and declined to10.58% as at March end 1999. Thus, the phenomenal hike in

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 8/28

rural credit has contributedimmensely to the growth of Indian agriculture. It should be

mentioned here that one-third ofthe total advances of the scheduled commercial banks

has gone to rural and semi-urban areas.Mergers and takeovers are leading to

transnational conglomerates, which offer traditional,commercial banking services as

well as investment banking and insurance services.

After nationalization, there was a shift of emphasis from industryto agriculture. The

country witnessed rapid expansion in bank branches, even in rural areas.

Bankingdevelopment in India after nationalization was wonderful and received global

compliments. The commercial banking system gained substantial strength to improve

nation building programs. However, the nationalization process created its own

problems, like excessive bureaucratization, red-tapism and disruptive tactics of tradeunions by bank employees. Reforms in the commercial banking sector have two

distinct phases. The first phaseof reforms introduced subsequent to the release of the

Report of the Committee on Financial System(Chairman-M. Narasimham), 1992

focused mainly on enabling and strengthening measures. The second phase ofreforms,

introduced subsequent to the recommendations of the Committee on Banking Sector

Reforms(Chairman- M. Narasimham)in 1998 placed greater emphasis on structural

measures and an improvement instandards of disclosure and levels of transparency, in

order to align the Indian standards with the bestinternational practices. Reforms have

brought about considerable improvements, as reflected in variousparameters relating

to capital adequacy, asset quality, profitability and operational efficiency.

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 9/28

BANKING SECTOR HIGHLIGHTS

In India, there are 84 commercial banks, which account for about 81 per cent

(total assets) of the financial sector at end-March 2006; over 3000 cooperative

banks, which account for 11 per cent; and 133 Regional Rural Banks, which

account for 3 per cent.

The capital adequacy ratio has increased to 12.4 per cent for scheduled

commercial banks as at end March 2006, which is much above the

international norm.

Commercial banks‟ net profits remained at 0.9 per cent of total assets during

2004-05 and 2005-06, up from 0.16 per cent in 1995-96.

The ratio of NPLs to total loans of scheduled commercial banks, which was as

high as 15.7 per cent at end-March 1997, declined steadily to 3.3 per cent by

end-March 2006.

The net non-performing assets declined to 1.2 per cent of net advances during

2005-06 from 2.0 per cent in 2004-05. According to the preliminary financial

results available for most of the banks for the year 2006-07, the financial

soundness has improved further.

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 10/28

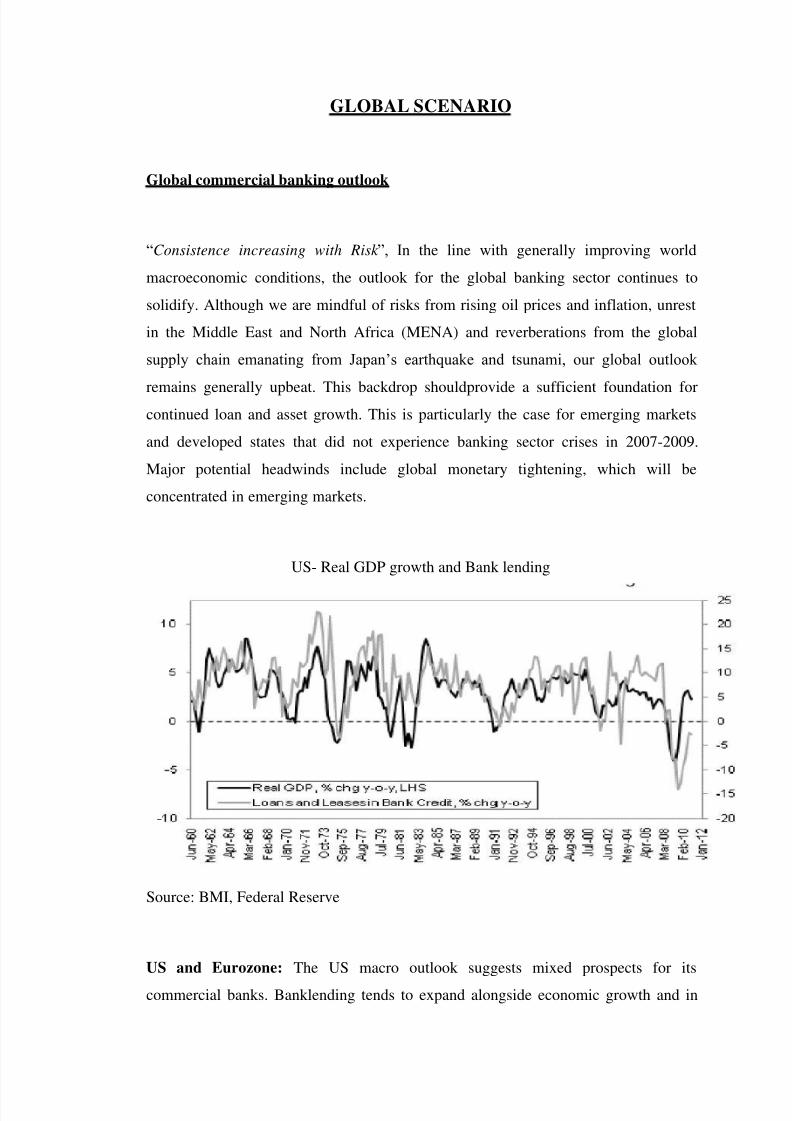

GLOBAL SCENARIO

Global commercial banking outlook

“Consistence increasing with Risk ”, In the line with generally improving world

macroeconomic conditions, the outlook for the global banking sector continues to

solidify. Although we are mindful of risks from rising oil prices and inflation, unrest

in the Middle East and North Africa (MENA) and reverberations from the global

supply chain emanating from Japan‟s earthquake and tsunami, our global outlook

remains generally upbeat. This backdrop shouldprovide a sufficient foundation forcontinued loan and asset growth. This is particularly the case for emerging markets

and developed states that did not experience banking sector crises in 2007-2009.

Major potential headwinds include global monetary tightening, which will be

concentrated in emerging markets.

US- Real GDP growth and Bank lending

Source: BMI, Federal Reserve

US and Eurozone: The US macro outlook suggests mixed prospects for its

commercial banks. Banklending tends to expand alongside economic growth and in

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 11/28

this respect, with decent but not particularlystrong economic expansion forecast for

the foreseeable future, banking sector loan growth will be slowfor some time.

Importantly, we continue to believe that in the current climate of household

deleveraging,there will be subdued demand for credit. 2011 and 2012 are set to be

slow growth years for theEuro zone‟s banking sector as the effects of fiscal austerity

are felt across the currency bloc and banksremain hesitant to significantly ramp up

lending towards the levels experienced prior to the globalfinancial crisis, particularly

amid tighter capital constraints. That said, despite monetary tightening,confidence in

the Eurozone banking sector has continued to hold up well. This supports our view

that therisks from monetary tightening to consumer demand and banking sector

stability in the Eurozone havebeen overplayed.

Emerging Asia: The Emerging Asia banking outlook is generally positive, though we

have someconcerns about some of the highest flying sectors. In particular, we are

concerned that loan lossprovisions in the Chinese banking system are hugely

underestimated and that the stability of the industryrests on non-performing loans

remaining well behaved, which has historically not been the case followingpolicy-

driven lending sprees. Despite the potential for economic damage following theMarch 2011earthquake and tsunami to have a negative impact on Japanese banks‟

assets in the short term, ii isbullish about Japanese banking sector equities. However,

we note that this is due to our expectation ofmultiple expansion rather than

improvements to banks‟ balance sheets, which we expect to be negativelyaffected by

rising bond yields.

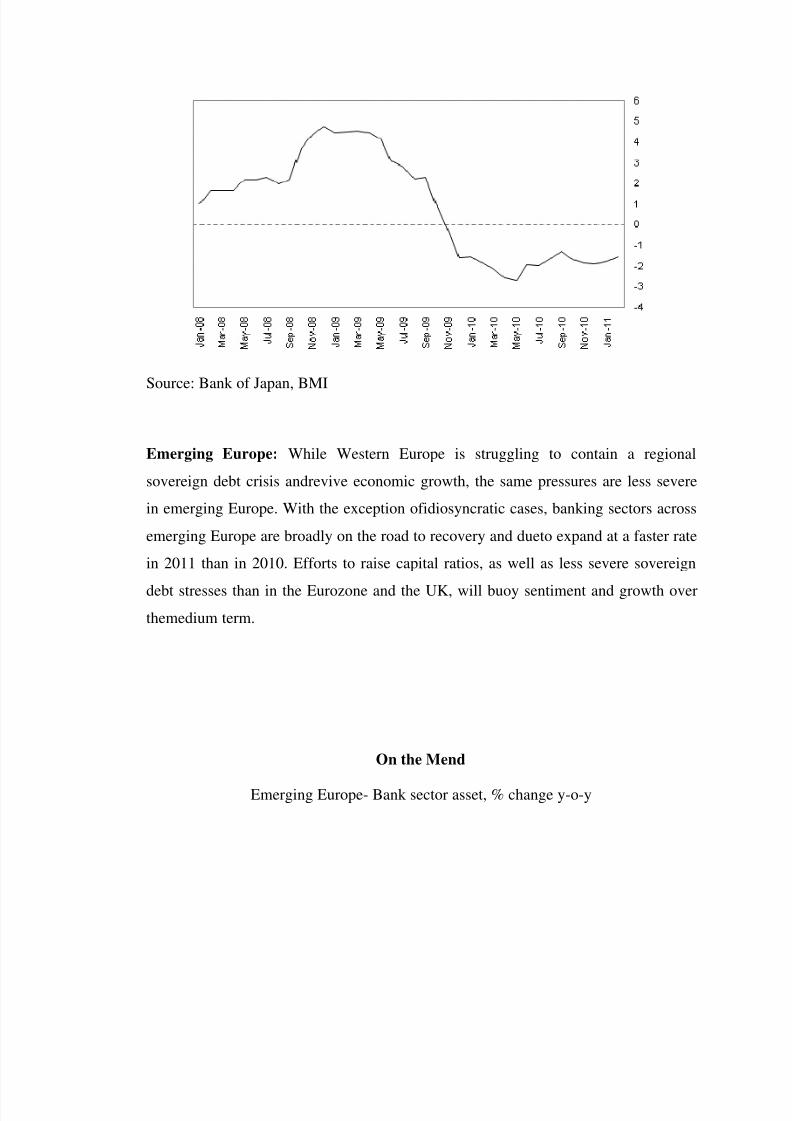

End to Deflation in Sight

Japan- Client loans, % change in Y-O-Y

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 12/28

Source: Bank of Japan, BMI

Emerging Europe: While Western Europe is struggling to contain a regional

sovereign debt crisis andrevive economic growth, the same pressures are less severe

in emerging Europe. With the exception ofidiosyncratic cases, banking sectors across

emerging Europe are broadly on the road to recovery and dueto expand at a faster rate

in 2011 than in 2010. Efforts to raise capital ratios, as well as less severe sovereign

debt stresses than in the Eurozone and the UK, will buoy sentiment and growth over

themedium term.

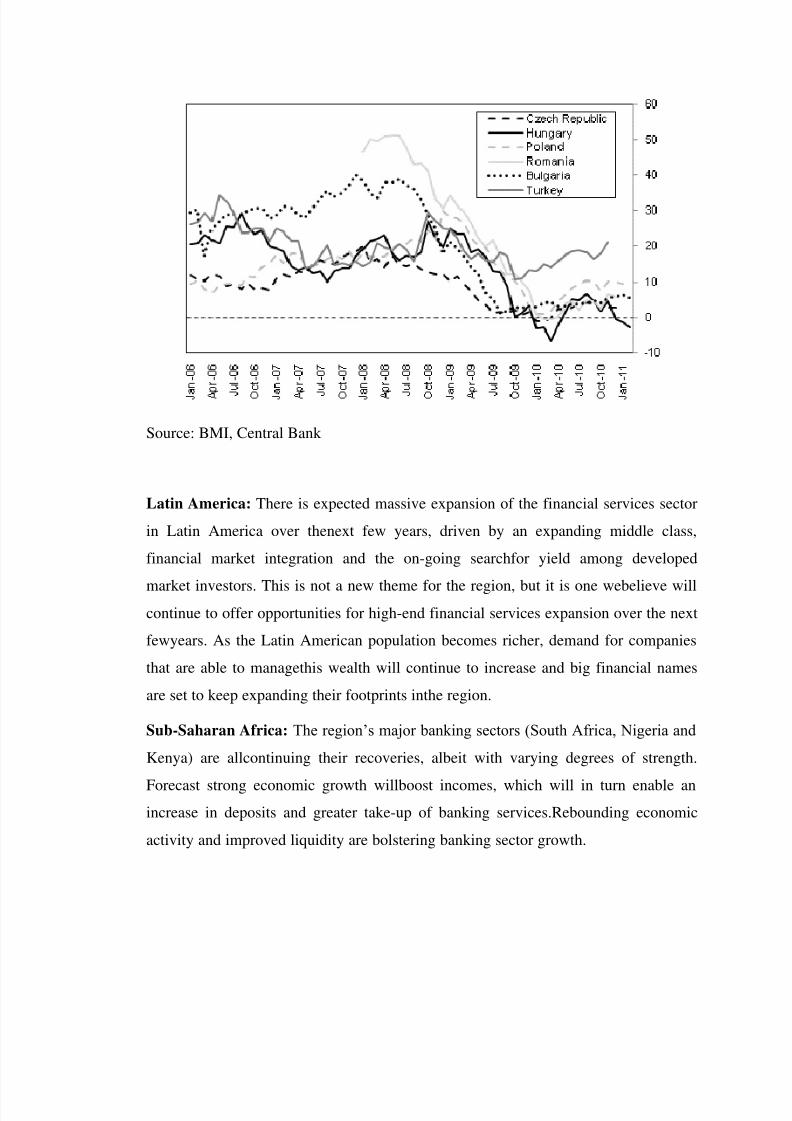

On the Mend

Emerging Europe- Bank sector asset, % change y-o-y

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 13/28

Source: BMI, Central Bank

Latin America: There is expected massive expansion of the financial services sector

in Latin America over thenext few years, driven by an expanding middle class,

financial market integration and the on-going searchfor yield among developed

market investors. This is not a new theme for the region, but it is one webelieve willcontinue to offer opportunities for high-end financial services expansion over the next

fewyears. As the Latin American population becomes richer, demand for companies

that are able to managethis wealth will continue to increase and big financial names

are set to keep expanding their footprints inthe region.

Sub-Saharan Africa: The region‟s major banking sectors (South Africa, Nigeria and

Kenya) are allcontinuing their recoveries, albeit with varying degrees of strength.

Forecast strong economic growth willboost incomes, which will in turn enable an

increase in deposits and greater take-up of banking services.Rebounding economic

activity and improved liquidity are bolstering banking sector growth.

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 14/28

WHERE DOES INDIAN BANKING SECTOR STAND

COMPARED TOINTERNATIONAL LEVEL?

NATIONAL SCENARIO

The banking sector all over the world is passing through a process of change and our

countryis no exception to it. It was after the beginning of the Uruguay Round of

multilateral tradenegotiations under the aegis of General Agreement on Tariffs and

Trade (GATT), crossborder trade in services came under the purview of multilateral

norms. It is important to notethat the industrialised countries dominate the cross

border trade in services. It may be pointedout that as compared to the 1980s and early

1990s, the share of foreign banks operating inIndia in the scheduled commercial

banking increased significantly since mid-1990s in termsof almost all the indicators

including income, deposits, investment, loans and advances andassets. Therefore,

during the period following the establishment of the GATS, there has

beenconsiderable increase in market access of the foreign banking service providers

in India'sdomestic market.

The process of integrating with the globalisation in a bid to develop a sound and

efficientbanking system in India at, par with international banking standards and

practices has comeinto increased focus in recent years. However, it is interesting that

the share of foreign banksin the total profitability of the scheduled commercial

banking sector in India has fallenconsiderably since mid-1990s. The increased

competitiveness in the Indian banking sector inthe post-reforms period, especially the

entry of new private sector banks and increasedefficiency of the public sector bankscould be major reasons for the fall in the profit share ofthe foreign banks.

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 15/28

WHY INTERNATIONAL PERSPECTIVE NOW?

Competition in most, if not all economic activities is no longer confined to nations to

and isgetting to be more and more global. There are several reasons behind it. First,

presence offoreign banks, either as branches or even subsidiaries will grow, at least in

accordance withour own commitments to the World Trade Organization (WTO).

Second, recent experiencehas shown that foreign-owned non-banking financial

companies in India do compete both fordeposited mobilization and asset-creation,

mainly through investments. Third, even in regard tocross border payments,

organization such as Western Union and other Money Changers whoare licensed by

RBI, are spreading their reach. Forth, as multinational expand theiroperationin India;

they could justifiably continue their banking ties of the home country, even if

therange and quality of service of Indian banks are equally good. Fifth many Indian

companiesare tending to become multi-nationals and they legitimately expect banking

services to be onper with best international standards. Sixth, as disinvestments

progresses, the link betweenlarge business units and public sector banks could get

diluted unless their services are ascompetitive. In fact, even in regard to services to

governments, both central and stategovernments, a beginning has been made by theGovernments allowing private owned banksalso to undertake the business of banker

to government as agents of RBI instead of confining to Public Sector Banks. Seventh,

in respect of business in activities related to financial markets, the expanding the

presence if foreign banks and their subsidiaries; particularly ingovernment securities

market, is all too evident. Eighth, the business overseas branches ofIndian banks in

the recent years is perhaps not growing a rapidly as their counterparts andpossible

threat to their continued profitability, and hence their presence should not beignored.

Finally, the relatively strong and growing presence of foreign banks, especially

intransactions of non-public sector organizations is too obvious to be missed. The

businessremittances of non-resident Indians (NRIs) were largely with public sector

banks as long asthe transactions emanated from West Asia. With emergence of the

more enlightenedmetropolitan or urban centred NRIs, particularly those in the USA

and hailing businessopportunitiesassociated with them are tending to drift towards

foreign banks.

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 16/28

Key player of Indian Banking Sector

The roots of the State Bank of India rest in the first decade of 19th century, when the

Bank of Calcutta, later renamed the Bank of Bengal, was established on 2 June 1806.

The Bank of Bengal was one of three Presidency banks, the other two being the Bank

of Bombay (incorporated on 15 April 1840) and the Bank of Madras (incorporated on

1 July 1843). All three Presidency banks were incorporated as joint stock companies

and were the result of the royal charters. These three banks received the exclusive

right to issue paper currency in 1861 with the Paper Currency Act, a right they

retained until the formation of the Reserve Bank of India. The Presidency banks

amalgamated on 27 January 1921, and the reorganized banking entity took as its

name: Imperial Bank of India. The Imperial Bank of India remained a joint stock

company

Pursuant to the provisions of the State Bank of India Act (1955), the Reserve Bank of

India, which is India's central bank, acquired a controlling interest in the Imperial

Bank of India. On 30 April 1955, the Imperial Bank of India became the State Bank

of India. The government of India recently acquired the Reserve Bank of India's stake

in SBI so as to remove any conflict of interest because the RBI is the country's

banking regulatory authority.

In 1959, the government passed the State Bank of India (Subsidiary Banks) Act,

enabling the State Bank of India to take over eight former state-associated banks as its

subsidiaries. On 13 September 2008, the State Bank of Saurashtra, one of its associate

banks, merged with the State Bank of India.

SBI has acquired local banks in rescues. For instance, in 1985, it acquired the Bank of Cochin in Kerala, which had 120 branches. SBI was the acquirer as its affiliate, the

State Bank of Travancore, already had an extensive network in Kerala.

State Bank of India (SBI) is the leading commercial bank in India, offering services

such as retailbanking, commercial banking, international banking and treasury

operations. The bank is an integralpart of State Bank Group, which includes seven

other banks and offers additional services such asmutual funds and insurance. The

bank primarily operates in India. It is headquartered in Mumbai,India and employsabout 222,933 people.

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 17/28

The company recorded revenues of INR 1478439.2 million ($32,229.9 million) in the

financial yearended March 2011 (FY2011), an increase of 10.5% over FY2010.

Operating profit was INR199197.6million ($4,342.5 million) in FY2011, an increase

of 6.6% over FY2010. Its net profit was INR1,11,799.4 million ($2,437.2 million) in

FY2011, a decline of 6.9% over FY2010.

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 18/28

FUTURE GROWTH OPPORTUNITIES

With the Indian economy growing at a brisk clip of nine-plus percent per annum,

there is growing global and domestic interest inthe nation‟s banking industry.

Attracted by the idea of servicing afast growing economy and the promiseof a

liberalized scenario in 2009, a hostof foreign banks have either applied to orare in

talks with India‟s banking regulator,the Reserve Bank of India (RBI), for licenses. The

Royal Bank of Scotland,Royal Bank of Canada, Credit Suisse and

Switzerland‟s UBS AG are among themany banks reported to have evincedinterest in

being part of the Indianbanking sector.The entry of new banks is unlikelyto result in

overcrowding as the Indian banking sector has tremendous potentialfor growth.

According to the PwCreport, total domestic credit in India wasaround $400 billion

compared to China‟s$ 2.8 trillion.But the new banks will have to competewith

existing banks including nationalized ones, private sector banks,foreign banks,

smaller institutions includingco-operative banks and in someareas with non-banking

finance companiestoo.

The Indian banking system hascome a long way since 1786 when thefirst bank was

set up in India. In the pre-Independence days, initially banks wereset up as private

institutions with mostlyEuropean shareholders. Post-independence,most of the banks

were nationalized in 1969.In the 1990s, following economicreforms, the banking

sector was alsoliberalized. The entry of private banks and increasing competition

resultedin nationalised banks becoming more efficient and turning aggressive in

themarket place. The introduction of automatedteller machines (ATMs),

phonebanking and internet banking by mostbanks has bid adieu to the

serpentinequeues seen earlier. A younger populationand rapid economic growth

hasboosted consumer banking.

The traditional banking businessthat caters to the needs of corporate isalso growing at

a fast pace. Today IndiaInc‟s global aspirations are being fuelledby foreign bankers,

who help them raisefunds (either equity or debt) or financetheir acquisition plans. For

instance, Citibankhas reportedly helped in financingup to $15 billion of acquisitions

by Indiancorporate overseas. The small andmedium enterprises (SMEs) segment toois

seeing resurgence as they go global in technology, markets and funds.

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 19/28

A fast developing country like Indiaalso needs good infrastructure to sustaineconomic

growth, leading to opportunitiesin the areas of infrastructure / projectfinance.

Incidentally, the governmenttoo is keen to ensure that credit growthmoves into the

productive side, that is,industry and the rural economy.

Thanks to the RBI, the Indian bankingsector remains on track. When

inflationthreatened to derail the growth story, itenforced strict norms that helped to

reinin inflation. The level of nonperformingassets (NPA) in Indian banks too is

inkeeping with internationally acceptablelevels and is lower than in some SouthEast

Asian countries.

In anticipation of the growth in thecoming years, existing players in India aredrawing

up major expansion plans. TheTatas are said to have lined up a massiveinvestment of

over a billion dollarsover the next three to four years througha new company, Tata

Capital. AnilAmbani wants Reliance Capital, one of the fastest growing financial

sector companies,to be among the top three financialservices companies, including

banks,in the country. It plans to increase itsemployee strength from current 11,000to

50,000 over the next two years.

The resilience of the Indian bankingsystem was first visible when the countrycame

out unscathed from the EastAsian crisis. The gradual pace of reformsin the country

have only resulted in makingthe banking sector one of the mostsound and robust in

the world. Barringsocial or political volatility, most industryofficials are confident

that the sector willcontinue to do well.

The banking industry has been apartner in the nation‟s progress. India‟stryst with

growth is likely to continuein the future as a robust banking sectorprovides the critical

support necessaryfor stable and sustained growth.

Experts have also projected that Indiawould emerge as the third largest banking hub

in the world by 2040.The banking sector will grow significantlyfaster than GDP in the

„E7‟emerging economies of China, India,Brazil, Russia, Indonesia, Mexico

andTurkey, ccording to new projectionsby PricewaterhouseCoopers. Totalprofits from

domestic banking in theE7 could be around half those in theG7 (US, Japan, Germany,

UK, France,Italy and Canada) by 2025 and largerthan in the G7 much before

2050.The new projections for the bankingmarket, using projected marketexchange

rates, suggest that total domesticcredit in China could overtakethe UK and Germanyby 2010, Japanby 2025 and the US before 2050. Indiacould also rise from relatively

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 20/28

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 21/28

OBSERVATIONS FROM PERSONAL INTERACTION WITH

COMPANY PROFESSIONAL

GLOBAL

As of 31 December 2009, the bank had 157 overseas offices spread over 32 countries.

In Nepal, SBI owns 55% of Nepal SBI Bank, which has branches throughout the

country. In Moscow, SBI owns 60% of Commercial Bank of India, with Canara Bank

owning the rest. In Indonesia, it owns 76% of PT Bank Indo Monex. In Kenya, State

Bank of India owns 76% of Giro Commercial Bank, which it acquired for US$8

million.

NATIONAL

State Bank of India (SBI) is the largest banking and financial services company in

India by revenue and total assets. As of March 2011, it had assets of US$ 370 billion

with over 13,000 outlets including 150 overseas branches and agents globally.

The achievements in the recent years are:-

SBI has turned into the third-largest employer in India among listed

companies after Coal India Limited and Tata Consultancy Services.

Best Online Banking Award, Best Customer Initiative Award & Best Risk

Management Award (Runner Up) by IBA Banking Technology Awards 2010

Best Bank 2009 by Business India

Best Bank – Large and Most Socially Responsible Bank by the Business Bank

Awards 2009

The Most Trusted Brand 2009 by the Economic Times

B.L Mathur

Administrative Officer

SBBJ ( Associated Bank - SBI)

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 22/28

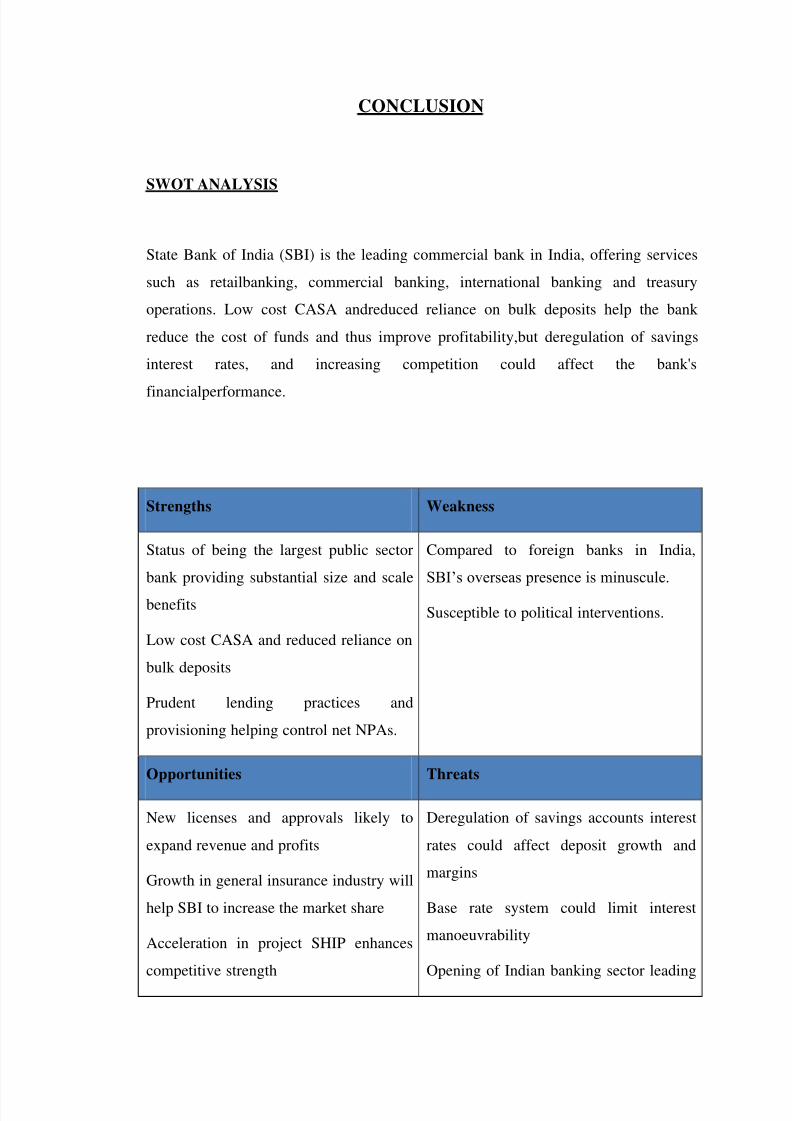

CONCLUSION

SWOT ANALYSIS

State Bank of India (SBI) is the leading commercial bank in India, offering services

such as retailbanking, commercial banking, international banking and treasury

operations. Low cost CASA andreduced reliance on bulk deposits help the bank

reduce the cost of funds and thus improve profitability,but deregulation of savings

interest rates, and increasing competition could affect the bank's

financialperformance.

Strengths Weakness

Status of being the largest public sector

bank providing substantial size and scale

benefits

Low cost CASA and reduced reliance on

bulk deposits

Prudent lending practices and

provisioning helping control net NPAs.

Compared to foreign banks in India,

SBI‟s overseas presence is minuscule.

Susceptible to political interventions.

Opportunities Threats

New licenses and approvals likely to

expand revenue and profits

Growth in general insurance industry will

help SBI to increase the market share

Acceleration in project SHIP enhances

competitive strength

Deregulation of savings accounts interest

rates could affect deposit growth and

margins

Base rate system could limit interest

manoeuvrability

Opening of Indian banking sector leading

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 23/28

Expansion of home loan market in

Bangladesh would increase profits

to intnse competition.

Strengths

Status of being the largest public sector bank providing substantial size andscale benefits

SBI is the largest commercial bank in India. The bank ranks amongst the top

25 banks in the Asianregion and is the only Indian bank to appear in the list of

the world's top 100 banks. Magnitude ofthe bank's size is evident from the

total business done (deposits and advances in 2010-11(INR14,78,439.2

million or $32229.97million), branch network (21500 branches ,including

branchesthat belong to its associate banks), ATM network (25,000 belong to

SBI). This is one of the largestcore banking networks in the world and

growing as well. During 2008-10, the bank increased itsscale by acquiring

State Bank of Saurashtra, and State Bank of Indore. Leveraging its strong

presencein the Indian banking industry, the bank has been able to effectively

position itself on the world mapand gain global recognition.

Low cost CASA and reduced reliance on bulk deposits

Low cost current account and savings account (CASA) deposits has been SBI

a key strength of thebank. During 2010-11, SBI saw excellent growth in all

businesses/market segments in which itoperated. SBI's average CASA growth

during 2010-11 was around 22.52%. Growth in low costCASA deposit base

has helped the bank to reduce reliance on bulk deposits, unlike its private

sectorcompetitors or foreign banks with significant presence in India. Low

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 24/28

cost CASA and reduced relianceon bulk deposits help the bank reduce the cost

of funds and thus improve profitability.

Prudent lending practices and provisioning helping control net NPAs

SBI is known for prudent lending practices. The bank's net non performing

assets NPAs) declined by INR28,470 million. The net NPA as at the end of

March 2011 was 1.63%. Account TrackingCentres have also been set up at all

Local Head Offices for centralised follow up of borrowers in theNPA

category. The bank's healthy NPA ratio not only meets the requirements of the

regulatorsworldwide but is also comparable to the best banks globally. Prudent

lending practices andprovisioning helped the bank register higher return on

average assets compared to its peers.

Weaknesses

Compared to foreign banks in India, SBI's overseas presence is minuscule.

SBI is one of the top 100 banks in the world. It is also one of the top 10 banks

in Asia. The numberof foreign offices increased from 142 as on 31st March

2010 to 156 as on 31st March 2011 spreadacross 32 countries.Yet, the bank's

dependence on the domestic market (India) is too high at 95.13%in 20010-11.

Compared to its peers (top 10 largest banks in Asia), SBI's international

operationscontribution to revenue and profits are miniscule. The

management's aim to transform the bank intoa global bank can't be realized

without expanding the contribution from international operations.Moreover,

the lack of significant contribution from international operations increases the

businessrisk for the bank.

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 25/28

Susceptible to political interventions

Government of India is the largest shareholder in SBI. In June 2008, Reserve

Bank of India (RBI)transferred its stake (59.73%) in SBI to the Government of

India (GOI). It is widely believed thatruling political party could misuse GOI's

stake in SBI to direct lending to priority sectors/preferredsectors to achieve

certain political objectives. As a result, SBI may not be able to deploy its

assetsoptimally. Over a period, if GOI doesn't reduce its stake in SBI then that

could have an impact onthe SBI management's strategies as well. Moreover,

SBI which used to enjoy above sovereign ratings on its debt issues could

increasingly find it difficult to get above sovereign ratings. This inturn would

lead to rise in cost of capital.

Opportunities

New licenses and approvals likely to expand revenue and profits

The financial year 2009-10 saw several positive developments for the bank. A

joint venture formed with Societe Generale Securities Services for undertaking

custodial services business commencesbusiness. Similarly, another joint

venture with Insurance Australia Group (IAG) commenced business.In the

years to come, the bank is likely to expand into seven niche areas viz. Mobile

Banking,Merchant Acquisition Business, SME Current account and Supply

Chain Finance, Savings Bank,Cash Management Product, NRI remittances

and Government business. The bank is likely toannounce aggressive business

plans, improving processes and matching organizational structuresin order to

grow in these areas.

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 26/28

Growth in general insurance industry will help SBI to increase the market

share

Insurance penetration in India is very low and the general insurance industry is

expected to grow at15 to 20 % annually over 10 years. There are 14 general

insurance companies in India, whichincludes the four government owned

players accounting for over 60% of the market at the end ofMarch 2009.

Following detariffing last year, the general insurance saw a steep reduction in

premiumrates resulting in a 12.5% growth in premium in 2008-09. The Indian

non-life insurance market grewby 12.6% in 2008 to reach a value of $7.1

billion, representing a compound annual growth rate(CAGR) of 14.7% for the

period spanning 2003-2008. In 2012, the Indian non-life insurance marketisforecast to have a value of $11.2 billion, an increase of 57.6% since 2008, at a

CAGR of 9.5% forthe five-year period 2008-2012. SBI's joint venture with

Insurance Australia Group (IAG) wills enableit to benefit from insurance

market expansion in India.

Acceleration in Project SHIP enhances competitive strength

SBI is in talks with the government of India to hasten the process of merging

some of its associatebanks with itself. In July 2010, State Bank of Indore

merged with SBI. Earlier in August 2008, State Bank of Saurasthra (SBS)

merged with SBI.These mergers are expected to accelerate Project SHIP(SHIP

is short form for four associates State Bank of Saurashtra, State Bank of

Hyderabad, StateBank of Indore and State Bank of Patiala.) signalling for the

merger of sequence of associate banksin the near future. All the above

mentioned four banks are wholly owned subsidiaries directly controlledby

SBI. So, there is no need for any annual general body meeting (AGM)

approval and the mergerdecision can be taken anytime after convening a

formal meeting of the boards of directors.Acceleration in Project SHIP

enhances SBI's competitive strength against its global peers operatingin India.

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 27/28

8/2/2019 Sector Analysis of Auto Saved)

http://slidepdf.com/reader/full/sector-analysis-of-auto-saved 28/28

Base rate system could limit interest rate manoeuvrability

The Indian banking transited from a benchmark prime lending rate (BPLR)

regime to a base rate system of lending, in July 2010. The base rate is the

minimum rate at which banks can lend after meeting all their costs. So the

base rate includes the cost of deposits, the cost of running the bank and a bit of

profit margin. Though, SBI being one of the banks with highest low cost

CASA deposits and thus can lend customers at a base rate lower than that of

its peers, the room to manage net interest margin is now difficult for the bank.

This could have negative consequences for credit off-take and thus limit

interest income of the bank. Another consequence that could be foreseen is the

increased demand for foreign deposits and borrowings in order to increase

interest ratemanoeuvrability. Increased dependence on bulk foreign deposits

and borrowings could lead to higher foreign exchange risks and asset liability

management risks.

Opening of Indian banking sector leading to intense competition

The Indian banking sector is progressively being opened to foreign banks.

Reserve Bank of India,India's central bank will allow foreign banks to invest

up to 74% in Indian banking sector and also set up branches in rural India. The

regulatory changes will be made to industry structure and sector consolidation

in areas such as freedom to deploy capital; regulatory coverage; corporate

governance; labour reforms and human capital development; and support for

creating industry utilities and service bureaus. At present in India, there are 28

public sector banks, 27 private sector banks and 29 foreign banks. These

numbers are set to increase in the months to come as RBI intends to increase

competition levels in Indian banking industry. New private-sector, foreign

banks and other large public-sector banks (PSBs) are quite competitive, posing

a serious challenge to SBI's franchise.

![OB Notes.pptx Auto Saved]](https://img.pdfslide.us/doc/110x75/577d1e601a28ab4e1e8e64ef/ob-notespptx-auto-saved.jpg)

![fINALsEMINAR.ppt Auto Saved]](https://img.pdfslide.us/doc/110x75/577d29e21a28ab4e1ea8234f/finalseminarppt-auto-saved.jpg)

![Apollo Tyres_1 Auto Saved]](https://img.pdfslide.us/doc/110x75/577d279e1a28ab4e1ea45eea/apollo-tyres1-auto-saved.jpg)

![Crypto Ppt Auto Saved]](https://img.pdfslide.us/doc/110x75/577d20f21a28ab4e1e941a72/crypto-ppt-auto-saved.jpg)

![Quality by Auto Saved]](https://img.pdfslide.us/doc/110x75/577d21781a28ab4e1e954ba7/quality-by-auto-saved.jpg)

![Controlling Auto Saved]](https://img.pdfslide.us/doc/110x75/577d35171a28ab3a6b8f9027/controlling-auto-saved.jpg)

![Distinction Ppt.pptx Auto Saved]](https://img.pdfslide.us/doc/110x75/577d1dc61a28ab4e1e8cedb5/distinction-pptpptx-auto-saved.jpg)

![FORTUNE....Pptx Auto Saved]](https://img.pdfslide.us/doc/110x75/577d20cd1a28ab4e1e93c8a4/fortunepptx-auto-saved.jpg)