Embed Size (px)

Citation preview

85

Chapter IV

PROFILE OF DPs AND INVESTORS ATTITUDE ON DP

SERVICES

This chapter deals with profile of select DPs and investors attitude towards

demat charges, reasonability of charges, mode of trading, basis of investment

decision, brokerage charge, business activities of DPs, equity research of DPs

transfer of shares, add on services of DPs .

Profile of select Depository Participants

India Info Line IIFL

IIFL (India Infoline group), comprising the holding company, India Info

line Ltd (NSE: INDIAINFO, BSE: 532636) and its subsidiaries, is one of one of

India’s premier providers of financial services. IIFL offers advice and an

execution platform for the entire range of financial services covering products

ranging from loans, company wealth management, asset management, insurance,

fixed deposits, investment banking, equities and derivatives, commodities,

Government of India bonds and other small savings instruments. It owns and

manages the company site, www.indiainfoline.com, which is one of India’s

leading online destinations for personal finance, economy, corporate updates and

equity and commodity-related updates.The company services 2.1 million

customers with a team of 14,000 employees in 3,820 business locations present in

eight countries.

Credit and finance

The facility is offered by subsidiaries, India Infoline Finance Ltd and India

Infoline Housing Finance Ltd. The diversified lending portfolio includes home

loans, healthcare finance for medical equipments, SME and trader loans, secured

loans against gold jewellery, commercial vehicle financing, property loans, and

capital market finance secured against securities. In FY13, this segment posted an

82.10% year-on-year growth in revenues at Rs. 17.37bn. The high quality loan

86

book of `. 93.75bn as on March 31, 2013 is backed by strong capital adequacy of

over 20% companyll above the stipulated 15%.

Private wealth management

In an increasingly unpredictable world, there is greater investor need for a

comprehensive company wealth management solution as opposed to disparate

services. Under this segment, IIFL Private Company wealth offers advisory

services to high net worth individuals and corporate clients. It manages

over `. 400bn of assets under advice on a client base exceeding 7,000 families.

Financial products division

The Group distributes a range of financial products like insurance, mutual

funds, National Pension Scheme, bonds and debentures through its extensive

distribution network. The company is a leader among non-bank promoted entities

in the distribution of life insurance and mutual funds. For FY13, annual premium

mobilisation stood at `. 3.2bn.

Asset management

The business was launched in 2011 with a unique proposition. The maiden

scheme was, and still is, the lowers cost Nifty ETF in India. A total of six

schemes have been launched, including four close-ended debt schemes and two

open-ended equity schemes. Total Assets Under Management stands at `. 3.27bn

as on March 31, 2013.

Equity, commodities and currency

Though the contribution to revenues is less than 15%, IIFL Group

continues to remain a leading online and offline broking as company as advisory

services provider for cash and derivative segments directed at retail and

institutional clients. Over a decade, the company has created a brand marked by

informed research, systemic uptime, transaction speed, cutting-edge technology,

extensive footprint, high service standards and competitive brokerage. It

87

pioneered the concept of internet broking in India and rationalised brokerage rates

from 1-1.5% in the late 90s to as low as 0.05%. The extension into commodities

and currency trading reconciles with its vision to emerge as a one-stop-shop

financial intermediary.

Research

A forerunner in the field of equity research, IIFL’s research is

acknowledged by none other than Forbes as ‘Best of the Company’ and ‘…a must

read for investors in Asia’. IIFL research is available not just over the Internet but

also on international wire services like Bloomberg, Thomson, Dow Jones Factiva

and Internet Securities. It is amongst the most read incisive pieces from among

Indian brokerages.

Milestones of IIFL

On a consolidated basis, the company has posted a record all-time high

income and profit for FY13. Income and profit stood at `. 26.7bn and `. 2.79bn,

respectively. Some important milestones for the year gone by include loan book

at `. 93.75bn, total borrowing at `. 92.2bn, capital adequacy ratio of 21.6%, net

interest margin of 9.5%, net non-performing assets at 0.17% and cost to income

ratio of 58.16%.

The company supports employment of over 24,000 people directly and

thousands more indirectly. The company services its 2.1mn customers through its

network of 3,820 locations present in 900 cities, covering literally every nook and

corner of the country IIFL is physically present in key global markets includes

subsidiaries in Colombo, Dubai, New York, Mauritius, London, Singapore and

Hong Kong. It is a proud corporate citizen with cumulative contribution since

inception to the exchequer of over `. 5 bn. The company has set an example for

the peer group with its financial literacy campaign or Financial Literacy Agenda

For Mass Empowerment touching more than 30mn people.vIIFL’s short-term

debt is rated CRISIL A1+ and ICRA (A1+) by Crisil and ICRA, respectively. For

88

the long-term, it has been rated ICRA (AA-) and CRISIL AA-/Stable indicating a

high degree of safety for timely servicing of financial obligations.

KARVY STOCK BROKING LTD

Stock Broking Services

It is an undisputed fact that the stock market is unpredictable and yet enjoys a

high success rate as a Wealth management and Wealth accumulation option. The

difference between unpredictability and a safety anchor in the market is provided

by in-depth knowledge of market functioning and changing trends, planning with

foresight and choosing one's options with care. This is what company provides in

our Stock Broking services. Company offer services that are beyond just a

medium for buying and selling stocks and shares. Instead companies provide

services which are multi dimensional and multi-focused in their scope. There are

several advantages in utilizing our Stock Broking services, which are the reasons

why it is one of the best in the country.

Company offer trading on a vast platform; National Stock Exchange, Bombay

Stock Exchange and Hyderabad Stock Exchange. More importantly, company

make trading safe to the maximum possible extent, by accounting for several risk

factors and planning accordingly. Companies are assisted in this task by our in-

depth research, constant feedback and sound advisory facilities. Our highly skilled

research team, comprising of technical analysts as well as fundamental specialists,

secure result-oriented information on market trends, market analysis and market

predictions. This crucial information is given as a constant feedback to our

customers, through the following daily reports which are delivered to them thrice

a day;

• The Pre-session Report, where market scenario for the day is predicted

• The Mid-session Report, timed to arrive during lunch break , where the

market forecast for the rest of the day is given and

89

• The Post-session Report, the final report for the day, where the market and

the report itself is reviewed.

• To add to this repository of information, company publish a monthly

magazine called KARVY The Finapolis which analyzes the latest stock

market trends and takes a close look at the various investment options, and

products available in the market, while a weekly report, called KARVY

Bazaar Baatein, keeps you more informed on the immediate trends in the

stock market. In addition, our specific industry reports give

comprehensive information on various industries. Besides this, company

also offer special portfolio analysis packages that provide daily technical

advice on scrip’s for successful portfolio management and provide

customized advisory services to help you make the right financial moves

that are specifically suited to your portfolio.

Our Stock Broking services are widely networked across India, with the

number of our trading terminals providing retail stock broking facilities. Our

services have increasingly offered customer oriented convenience, which

company provide to a spectrum of investors, high-net worth or otherwise, with

equal dedication and competence. But true to our spirit, this success is not our

final destination, but just a platform to launch further enhanced quality services to

provide you the latest in convenient, customer-friendly stock management. Over

the years company have ensured that the trust of our customers is our biggest

returns. Factors such as our success in the Electronic custody business has helped

build on our tradition of trust even more. Consequentially our retail client base

expanded very fast. To empower the investor further company have made serious

efforts to ensure that our research calls are disseminated systematically to all our

stock broking clients through various delivery channels like email, chat, SMS,

phone calls etc.

Our foray into commodities broking has been path breaking and company are

in the process of converting existing traders in commodities into the more

organized mainstream of trading in commodity futures, both as a trading and risk

90

hedging mechanism. In the future, our focus will be on the emerging businesses

and to meet this objective, company have enhanced our manpower and revitalized

our knowledge base with enhances focus on Futures and Options as well as the

commodities business.

Depository Participant Services

The onset of the technology revolution in financial services Industry saw

the emergence of KARVY as an electronic custodian registered with National

Securities Depository Ltd (NSDL) and Central Securities Depository Ltd (CSDL)

in 1998. KARVY set standards enabling further comfort to the investor by

promoting paperless trading across the country and emerged as the top 3

Depository Participants in the country in terms of customer serviced.

Financial Products Distribution Services

The paradigm shift from pure selling to knowledge based selling drives

the business today. With our wide portfolio offerings, company occupies all

segments in the retail financial services industry. A team of highly qualified and

dedicated professionals drawn from the best of academic and professional

backgrounds are committed to maintaining high levels of client service delivery.

This has propelled us to a position among the top distributors for equity and debt

issues with an estimated market share of 15% in terms of applications mobilized,

besides being established as the leading procurer in all public issues. To further

tap the immense growth potential in the capital markets company enhanced the

scope of our retail brand, KARVY – the Finapolis, thereby providing planning

and advisory services to the mass affluent.

Advisory Services

Under our retail brand ‘KARVY – the Finapolis, company deliver

advisory services to a cross-section of customers. The service is backed by a team

of dedicated and expert professionals with varied experience and background in

handling investment portfolios. They are continually engaged in designing the

right investment portfolio for each customer according to individual needs and

91

budget considerations with a comprehensive support system that focuses on

trading customers' portfolios and providing valuable inputs, monitoring and

managing the portfolio through varied technological initiatives. This is made

possible by the expertise company have gained in the business over the years.

Another venture towards being investor-friendly is the circulation of a monthly

magazine called ‘KARVY - the Finapolis covering the latest of market news,

trends, investment schemes and research-based opinions from experts in various

financial fields.

Private Client Group Services

This specialized division was set up to cater to the high net worth

individuals and institutional clients keeping in mind that they require a different

kind of financial planning and management that will augment not just existing

finances but their life-style as well. Here company follows a hard-nosed business

approach with the soft touch of dedicated customer care and personalized

attention. For this purpose company offer a comprehensive and personalized

service that encompasses planning and protection of finances, planning of

business needs and retirement needs and a host of other services, all provided on a

one-to-one basis. Our research reports have been widely appreciated by this

segment. The delivery and support modules have been fine tuned by giving our

clients access to online portfolio information, constant updates on their portfolios

as well as value-added advice on portfolio churning, sector switches etc. The

investment recommendations given by our research team in the cash market have

enjoyed a high success rate. Offering a wide trading platform with a dual

membership at both NSDL and CDSL, companies are a powerful medium for

trading and settlement of dematerialized shares.

PCS SECURITIES LTD

PCS Securities Ltd. adds the dynamic growth factor to your savings and

investments by guiding you through the land of opportunities and maximizing

your returns. PCS is a fourth generation stock broking powerhouse - one among

the top 100 national brokerage firms in India and has served thousands of

92

investors over the past six decades. PCS is now present at over 340 locations

across the Nation and one of the top CDSL Participants in South India.

PCS Securities Ltd Powered by Generation Inpired by Trust

Today's world of advanced technology and blink-of-an-eye

communication has opened a magic box full of opportunities and wealth

fulfillment formulae. PCS is here to offer you some such opportunities which help

you stretch your investment horizon and unleash the true potential of your wealth.

PCS Securities Ltd. adds the dynamic growth factor to your savings and

investments by guiding you through the land of opportunities and maximizing

your returns. PCS is a fourth generation stock broking power house - one among

the top 100 national brokerage firms in India and has served thousands of

investors over the past six decades. PCS is now present at over 340 locations

across the Nation and one of the top CDSL Participants in South India.

PCS was born out of the aspirations of Late Mr. K. C. Shrimal - founder

member of Hyderabad Stock Exchange - and nurtured through generations by

Late Mr. S. C. Shrimal and his son Mr. P. C. Shrimal, Promoter and Chairman of

PCS Securities Ltd., twice President of HSE, who has also served as the Chairman

of the FISE - Federation of Indian Stock Exchanges. He is currently assisted by

his son, Mr. Prashant Shrimal. The Board consists not only of the highly

experienced generational hierarchy, but also industry stalwarts with a

companyalth of expertise including Whole-time Director Mr. Paresh Shah and

Director Mr. Jagdish Ahuja (Ex-President, Bangalore Stock Exchange).

NETWORTH STOCK BROKINGM LTD

Net worth has always endeavored to make a difference in the financial

services space. It constantly focuses on scaling and upgrading the technology

infrastructure so as to provide the best services to the investors.The Company

have presence of around 350 centers across India.

93

The Company Strengths

• Managed by a talented team of around 800 professionals.

• Serving nearly 100,000 clients across the country.

• ISO 9001:2000 Certified Software Division.

• Winner of CNBC-TV18’s Financial Advisor Awards 2008 for Best

Regional Level Financial Advisor.

• Proclaimed amongst the most read research analyst (Team Networth) by

Thomson Reuters consistently over a period of time.

• A Charter member of Financial Planning Standards Board of India

[FPSB].

• Alliance partners with PNB for online trading.

• Corporate Agents for MetLife India Insurance Co Ltd.

NET WORTH GROUP COMPANIES

Net worth Stock Broking Ltd. [NSBL]

NSBL is a member of the National Stock Exchange of India Ltd (NSE)

and the Bombay Stock Exchange Ltd (BSE) in the Capital Market and Derivatives

(Futures & Options) segment. NSBL has also acquired membership of the

currency derivatives segment with NSE, BSE, USE & MCX-SX. It is Depository

participants with Central Depository Services India (CDSL) and National

Securities Depository (India) Limited (NSDL). With a client base of around

100,000 loyal customers, NSBL is spread across the country though its around

350 branches. NSBL is listed on the BSE since 1994.

Net worth Wealth Solutions Ltd. [NWSL]

NWSL is into the business of delivery of Financial Planning & Advice.

It’s vision is to ‘Advice & Execute money related solutions to/for our customers

in the most Convenient & Consolidated manner, while making sure that their

experience with us is always pleasant & memorable resulting in positive

advocacy’. The product & Services include Financial Planning, Life Insurance,

94

On-line Trading Account, Mutual Funds, Debentures/Bonds, General Insurance,

Loans and Depository Services.

Net worth Commodities & Investments Limited [NCIL]

NCIL is the commodities arm of NSBL. It is a member at the Multi

Commodity Exchange of India (MCX), National Commodity & Derivatives

Exchange (NCDEX) and ICEX & is backed by solid research & analytics in

Commodities.

Net worth Soft Tech Ltd. [NSL]

NSL is an ISO 9001:2000 Certified Company. It is into Application

Development & maintenance. Building & Implementation of packaged software

across various functions within the Financial Services Industry is at its core. It

also provides data center services which include hosting of websites, applications

& related services. It combines a unique delivery model infused by a distinct

culture of customer satisfaction.

Ravisha Financial Services Pvt. Ltd. [RFSL]

RFSL is a RBI registered NBFC engaged in financing, primarily it

provides loan against securities.

Demat Account Charges

The charges for opening demat account definitely influence the

membership of the depository participants. If they provide demat account for free

then membership also increases as large number of small investors are attracted.

If depository participant’s charges for opening demat account then their

membership decreases as high net worth investors are attracted only. For instance

in the table 4.1, when ever depository participants are providing demat account

for free then 18.7 % of total investors or 56 investors of urban area responded

only where as semi urban and rural investors are not responded due to lack of

95

awareness . Whenever depository participants are charging less than 500 rupees

for opening demat account then 34.7 % of total investors or 104 urban investors,

33.3 % of total investors or semi-urban investors and 13.3 % total investors or 40

rural investors have opened demat account only.

Table 4.1 Charges for Demat Account by Area Wise

Charges for Demat Account Residential Status

Total Urban Semi

Urban

Rural

Free Count

Expected Count

%within Charges

for Demat Account

%within residential

Status

% of Total

56

29.9

100.0%

35.0%

18.7%

0

18.7

.0%

.0%

.0%

0

7.5

.0%

.0%

.0%

56

56.0

100.0%

18.7%

18.7%

< 500 Rupees Count

Expected Count

%within Charges

for Demat Account

%within residential

Status

% of Total

104

130.1

42.6%

65.0%

34.7%

100

81.3

41.0%

100.0%

33.3%

40

32.5

16.4%

100.0%

13.3%

244

244.0

100.0%

81.3%

81.3%

Total Count

Expected Count

%within Charges

for Demat Account

%within residential

Status

% of Total

160

160.0

53.3%

100.0%

53.3%

100

100.0

33.3%

100.0%

33.3%

40

40.0

13.3%

100.0%

13.3%

300

300.0

100.0%

100.0%

100.0% Source: Primary data and SPSS

It is observed that 18.7 % of total investors or 56 urban investors are

availed only for opening demat account with the select depository participants

when they provide demat account for free , semi-urban and rural investors are not

availed the facility of opening demat account for free due to lack of awareness

and also investors may not demand quality of services from the depository

participants. Whenever depository participants are charging less than 500 rupees /

nominal amount for opening demat account large number of investors availed as

96

investors can demand quality of services from the concerned depository

participants.

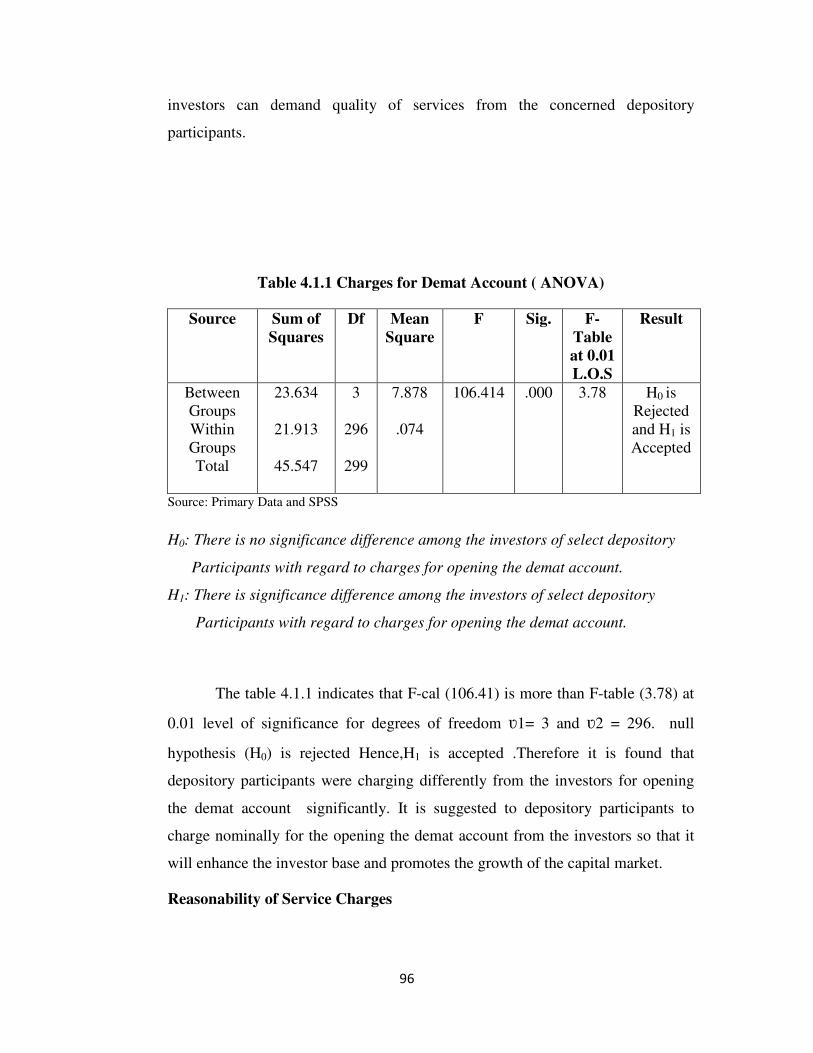

Table 4.1.1 Charges for Demat Account ( ANOVA)

Source Sum of

Squares

Df Mean

Square

F Sig. F-

Table

at 0.01

L.O.S

Result

Between

Groups

Within

Groups

Total

23.634

21.913

45.547

3

296

299

7.878

.074

106.414 .000 3.78 H0 is

Rejected

and H1 is

Accepted

Source: Primary Data and SPSS

H0: There is no significance difference among the investors of select depository

Participants with regard to charges for opening the demat account.

H1: There is significance difference among the investors of select depository

Participants with regard to charges for opening the demat account.

The table 4.1.1 indicates that F-cal (106.41) is more than F-table (3.78) at

0.01 level of significance for degrees of freedom ʋ1= 3 and ʋ2 = 296. null

hypothesis (H0) is rejected Hence,H1 is accepted .Therefore it is found that

depository participants were charging differently from the investors for opening

the demat account significantly. It is suggested to depository participants to

charge nominally for the opening the demat account from the investors so that it

will enhance the investor base and promotes the growth of the capital market.

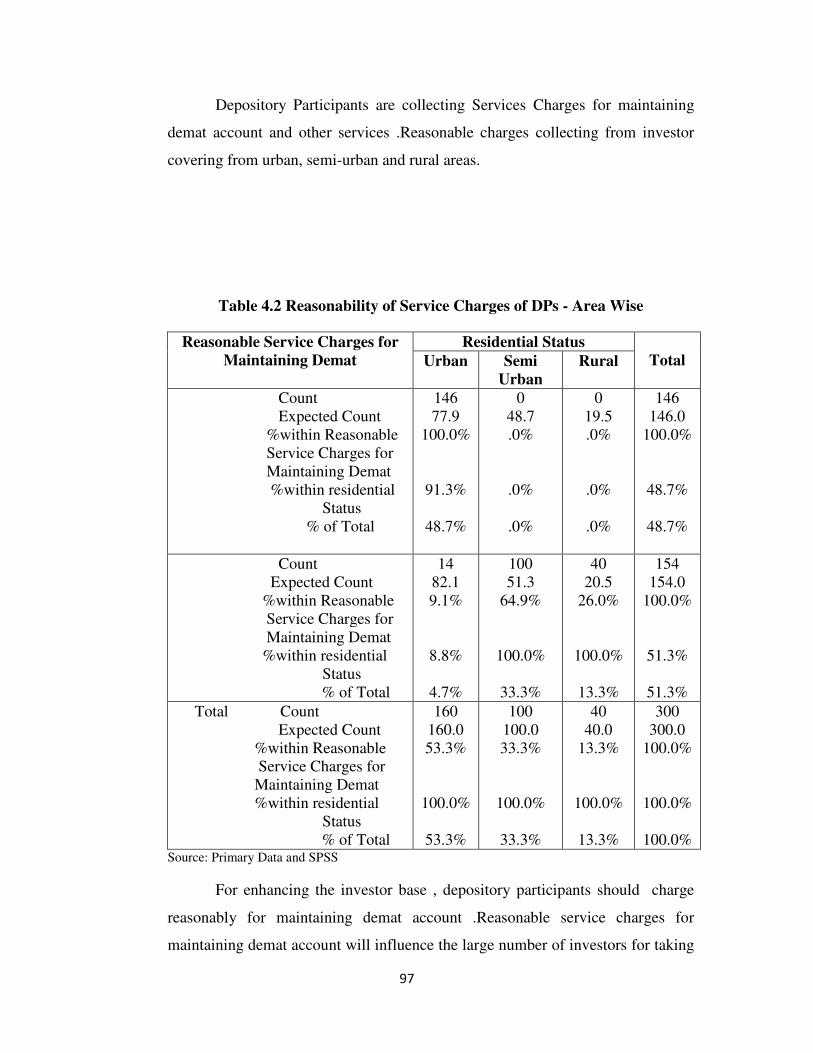

Reasonability of Service Charges

97

Depository Participants are collecting Services Charges for maintaining

demat account and other services .Reasonable charges collecting from investor

covering from urban, semi-urban and rural areas.

Table 4.2 Reasonability of Service Charges of DPs - Area Wise

Reasonable Service Charges for

Maintaining Demat

Residential Status

Total Urban Semi

Urban

Rural

Count

Expected Count

%within Reasonable

Service Charges for

Maintaining Demat

%within residential

Status

% of Total

146

77.9

100.0%

91.3%

48.7%

0

48.7

.0%

.0%

.0%

0

19.5

.0%

.0%

.0%

146

146.0

100.0%

48.7%

48.7%

Count

Expected Count

%within Reasonable

Service Charges for

Maintaining Demat

%within residential

Status

% of Total

14

82.1

9.1%

8.8%

4.7%

100

51.3

64.9%

100.0%

33.3%

40

20.5

26.0%

100.0%

13.3%

154

154.0

100.0%

51.3%

51.3%

Total Count

Expected Count

%within Reasonable

Service Charges for

Maintaining Demat

%within residential

Status

% of Total

160

160.0

53.3%

100.0%

53.3%

100

100.0

33.3%

100.0%

33.3%

40

40.0

13.3%

100.0%

13.3%

300

300.0

100.0%

100.0%

100.0% Source: Primary Data and SPSS

For enhancing the investor base , depository participants should charge

reasonably for maintaining demat account .Reasonable service charges for

maintaining demat account will influence the large number of investors for taking

98

membership in depository participants. The table 4.2 reveals that 48.7 % of total

investors or 146 urban investors are opinioned that depository participants are

charging reasonably for maintaining the demat account where as 51.3 % of total

investors or 154 investors which includes 14 urban, 100 semi-urban and 40 rural

investors have opinioned that service charges for maintaining demat account are

not reasonable.

It is found that majority number of investors (51.3 % of investors)

opinioned that depository participants are not collecting the reasonable service

charges for maintaining demat account. Moreover, all the semi-urban and rural

investors opinioned that depository participants are not charging reasonably for

maintaining the demat account and majority of the urban investors opinioned that

DP’s are charging reasonably for maintaining demat account. Therefore, it is

suggested to the depository participants to collect reasonable service charges for

maintaining the demat account so that to motivate large number of investors from

sem-urban and rural areas and retaining the existing investors for maximizing

their investment turnover and profits.

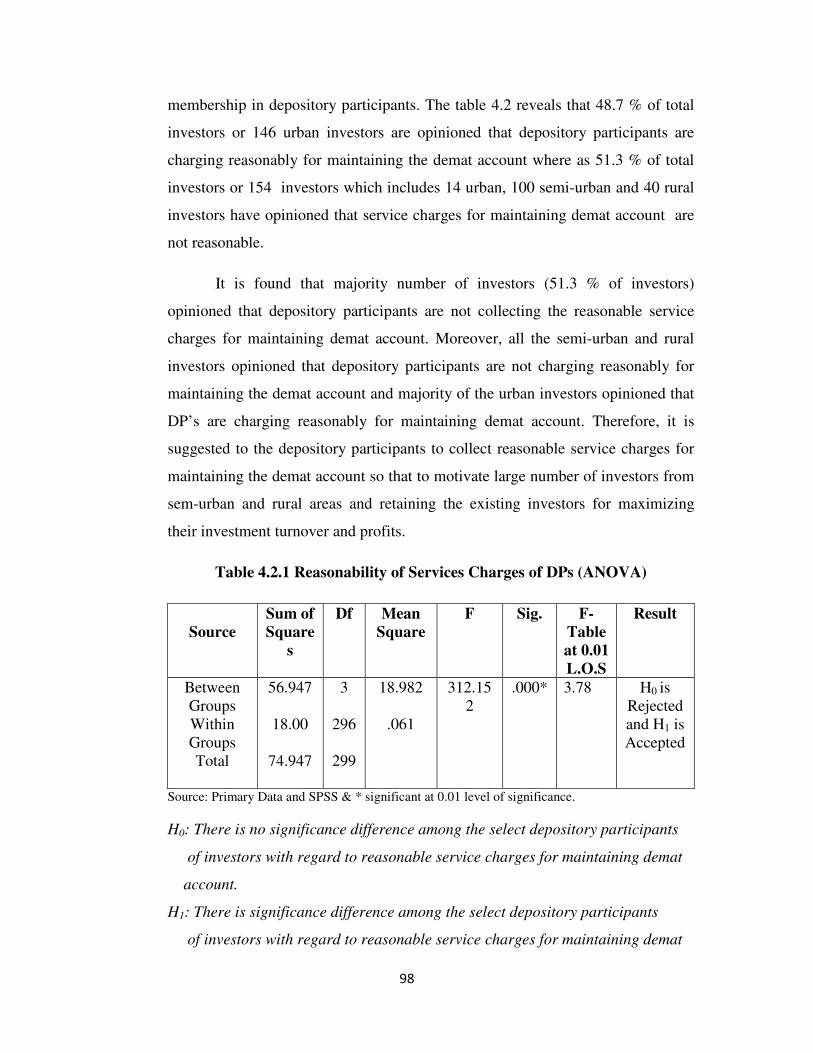

Table 4.2.1 Reasonability of Services Charges of DPs (ANOVA)

Source

Sum of

Square

s

Df Mean

Square

F Sig. F-

Table

at 0.01

L.O.S

Result

Between

Groups

Within

Groups

Total

56.947

18.00

74.947

3

296

299

18.982

.061

312.15

2

.000* 3.78 H0 is

Rejected

and H1 is

Accepted

Source: Primary Data and SPSS & * significant at 0.01 level of significance.

H0: There is no significance difference among the select depository participants

of investors with regard to reasonable service charges for maintaining demat

account.

H1: There is significance difference among the select depository participants

of investors with regard to reasonable service charges for maintaining demat

99

account.

The table 4.2.1 indicates that F-cal (312.15) is more than F-table (3.78) at

0.01 level of significance for degrees of freedom ʋ1= 3 and ʋ2 = 296. The null

hypothesis (H0) is rejected and hence, H1 is accepted. It is concluded that there is

significance difference among the select depository participants of investors with

regard to reasonable service charges for maintaining demat account. (or)Therefore

it is found that investor’s opinion towards the reasonable service charges for

maintaining demat account among the select depository participants differed

significantly. It is suggested to the investors to know the average service charges

for maintaining demat account per year before opening account with the

depository participant. It is also suggested to the depository participants that they

should charge nominal /reasonable service charges for maintaining the investors

demat account.

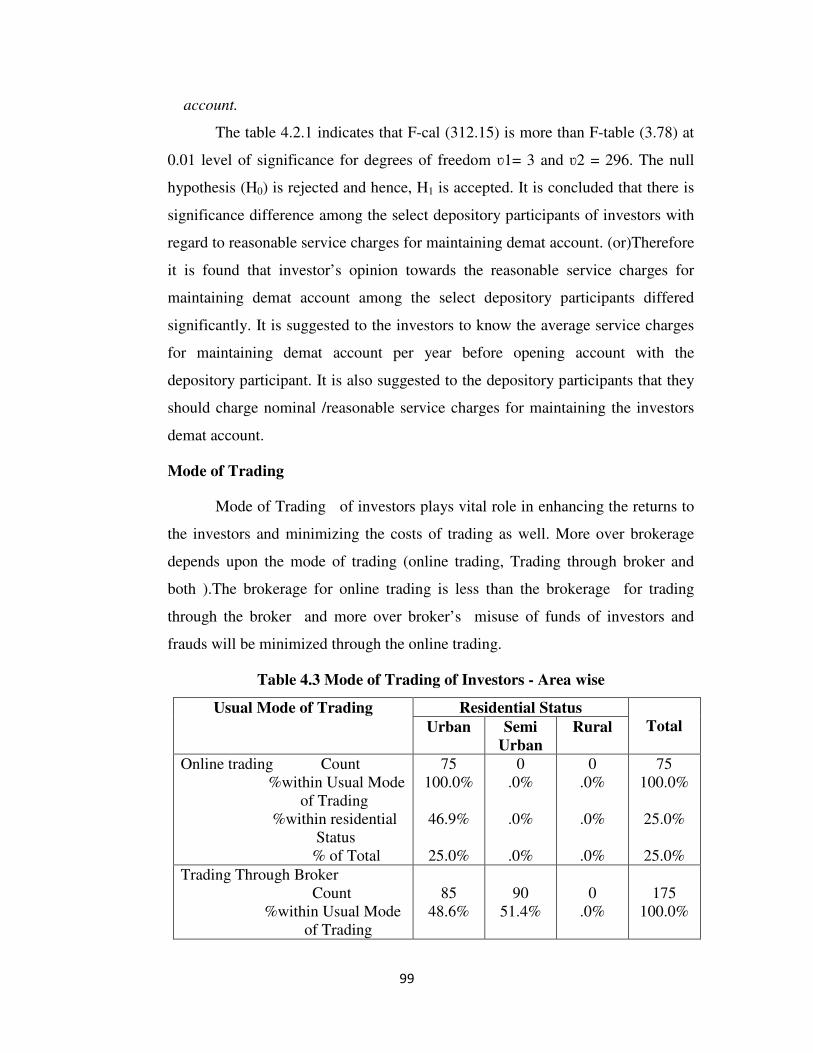

Mode of Trading

Mode of Trading of investors plays vital role in enhancing the returns to

the investors and minimizing the costs of trading as well. More over brokerage

depends upon the mode of trading (online trading, Trading through broker and

both ).The brokerage for online trading is less than the brokerage for trading

through the broker and more over broker’s misuse of funds of investors and

frauds will be minimized through the online trading.

Table 4.3 Mode of Trading of Investors - Area wise

Usual Mode of Trading Residential Status

Total Urban Semi

Urban

Rural

Online trading Count

%within Usual Mode

of Trading

%within residential

Status

% of Total

75

100.0%

46.9%

25.0%

0

.0%

.0%

.0%

0

.0%

.0%

.0%

75

100.0%

25.0%

25.0%

Trading Through Broker

Count

%within Usual Mode

of Trading

85

48.6%

90

51.4%

0

.0%

175

100.0%

100

%within residential

Status

% of Total

53.1%

28.3%

90.0%

30.0%

.0%

.0%

58.3%

58.3%

Both Count

%within Usual Mode

of Trading

%within residential

Status

% of Total

0

.0%

.0%

.0%

10

20.0%

10.0%

3.3%

40

80.0%

100.0%

13.3%

50

100.0%

16.7%

16.7%

Total Count

%within Usual Mode

of Trading

%within residential

Status

% of Total

160

53.3%

100.0%

53.3%

100

33.3%

100.0%

33.3%

40

13.3%

100.0%

13.3%

300

100.0%

100.0%

100.0% Source: Primary Data and SPSS

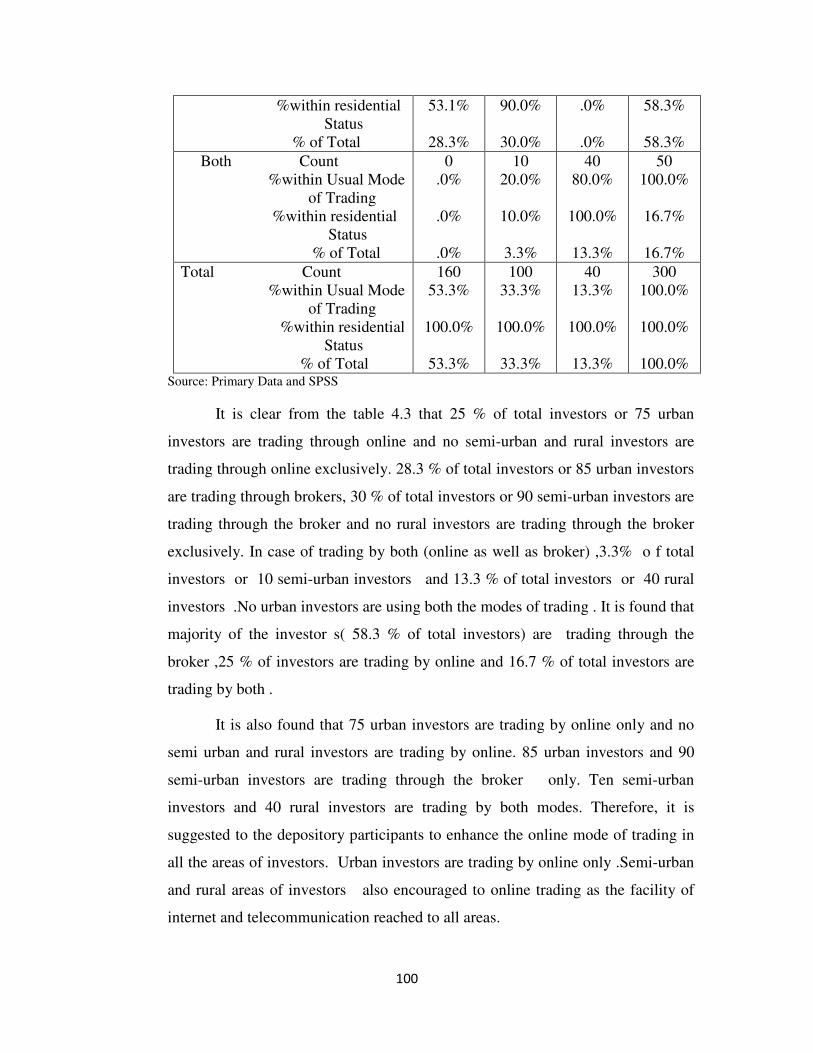

It is clear from the table 4.3 that 25 % of total investors or 75 urban

investors are trading through online and no semi-urban and rural investors are

trading through online exclusively. 28.3 % of total investors or 85 urban investors

are trading through brokers, 30 % of total investors or 90 semi-urban investors are

trading through the broker and no rural investors are trading through the broker

exclusively. In case of trading by both (online as well as broker) ,3.3% o f total

investors or 10 semi-urban investors and 13.3 % of total investors or 40 rural

investors .No urban investors are using both the modes of trading . It is found that

majority of the investor s( 58.3 % of total investors) are trading through the

broker ,25 % of investors are trading by online and 16.7 % of total investors are

trading by both .

It is also found that 75 urban investors are trading by online only and no

semi urban and rural investors are trading by online. 85 urban investors and 90

semi-urban investors are trading through the broker only. Ten semi-urban

investors and 40 rural investors are trading by both modes. Therefore, it is

suggested to the depository participants to enhance the online mode of trading in

all the areas of investors. Urban investors are trading by online only .Semi-urban

and rural areas of investors also encouraged to online trading as the facility of

internet and telecommunication reached to all areas.

101

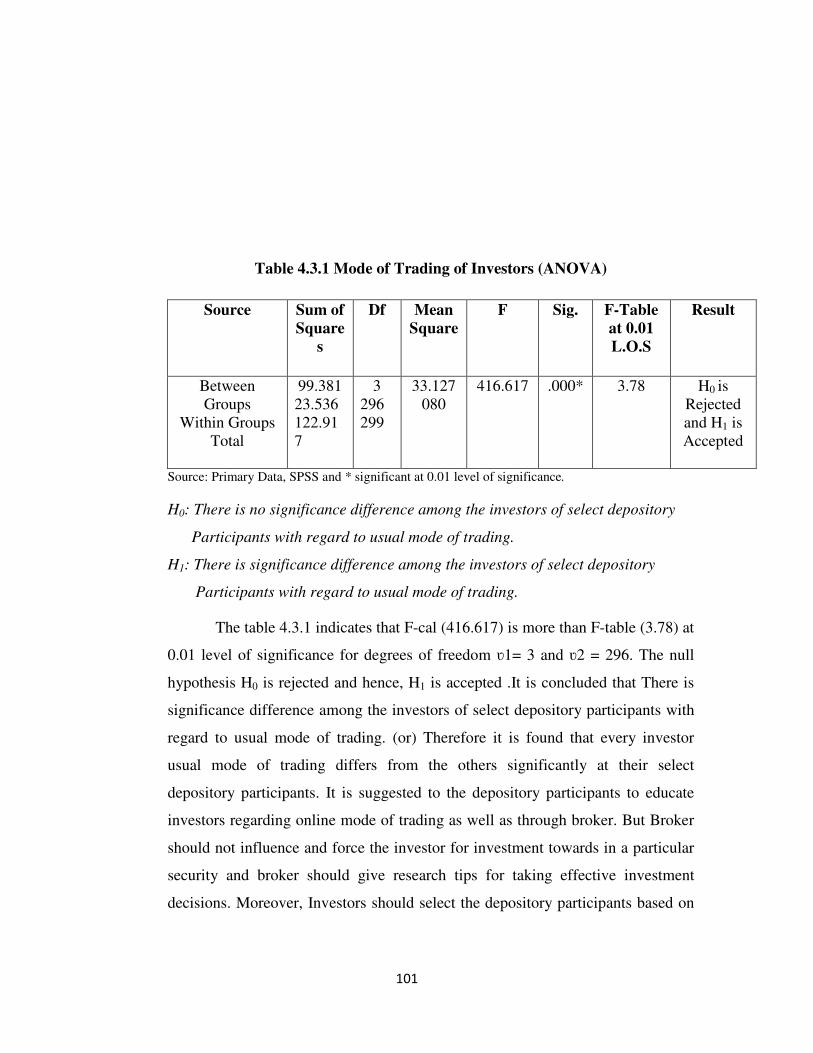

Table 4.3.1 Mode of Trading of Investors (ANOVA)

Source Sum of

Square

s

Df Mean

Square

F Sig. F-Table

at 0.01

L.O.S

Result

Between

Groups

Within Groups

Total

99.381

23.536

122.91

7

3

296

299

33.127

080

416.617 .000* 3.78 H0 is

Rejected

and H1 is

Accepted

Source: Primary Data, SPSS and * significant at 0.01 level of significance.

H0: There is no significance difference among the investors of select depository

Participants with regard to usual mode of trading.

H1: There is significance difference among the investors of select depository

Participants with regard to usual mode of trading.

The table 4.3.1 indicates that F-cal (416.617) is more than F-table (3.78) at

0.01 level of significance for degrees of freedom ʋ1= 3 and ʋ2 = 296. The null

hypothesis H0 is rejected and hence, H1 is accepted .It is concluded that There is

significance difference among the investors of select depository participants with

regard to usual mode of trading. (or) Therefore it is found that every investor

usual mode of trading differs from the others significantly at their select

depository participants. It is suggested to the depository participants to educate

investors regarding online mode of trading as well as through broker. But Broker

should not influence and force the investor for investment towards in a particular

security and broker should give research tips for taking effective investment

decisions. Moreover, Investors should select the depository participants based on

102

quality of investment advisory services which optimize risk and returns with

regard to different modes of trading.

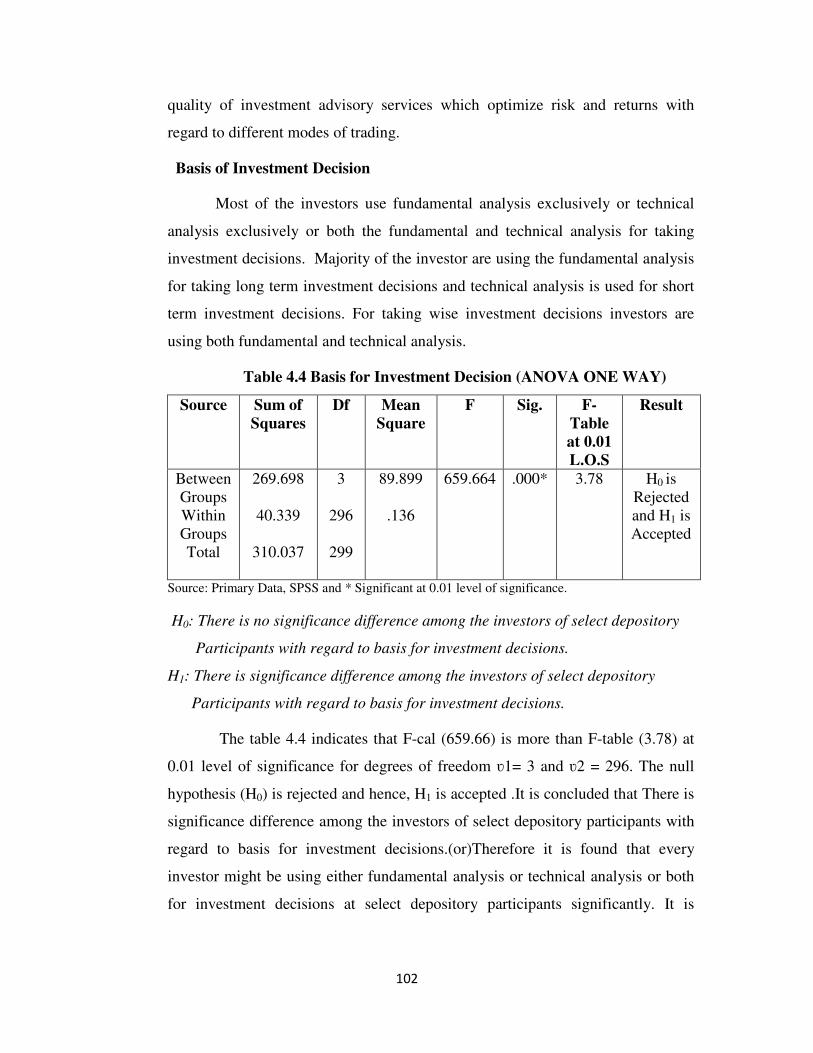

Basis of Investment Decision

Most of the investors use fundamental analysis exclusively or technical

analysis exclusively or both the fundamental and technical analysis for taking

investment decisions. Majority of the investor are using the fundamental analysis

for taking long term investment decisions and technical analysis is used for short

term investment decisions. For taking wise investment decisions investors are

using both fundamental and technical analysis.

Table 4.4 Basis for Investment Decision (ANOVA ONE WAY)

Source Sum of

Squares

Df Mean

Square

F Sig. F-

Table

at 0.01

L.O.S

Result

Between

Groups

Within

Groups

Total

269.698

40.339

310.037

3

296

299

89.899

.136

659.664 .000* 3.78 H0 is

Rejected

and H1 is

Accepted

Source: Primary Data, SPSS and * Significant at 0.01 level of significance.

H0: There is no significance difference among the investors of select depository

Participants with regard to basis for investment decisions.

H1: There is significance difference among the investors of select depository

Participants with regard to basis for investment decisions.

The table 4.4 indicates that F-cal (659.66) is more than F-table (3.78) at

0.01 level of significance for degrees of freedom ʋ1= 3 and ʋ2 = 296. The null

hypothesis (H0) is rejected and hence, H1 is accepted .It is concluded that There is

significance difference among the investors of select depository participants with

regard to basis for investment decisions.(or)Therefore it is found that every

investor might be using either fundamental analysis or technical analysis or both

for investment decisions at select depository participants significantly. It is

103

suggested that Investors should use both fundamental and technical analysis for

rational investment decisions.

Brokerage for Intraday Trading

Brokerage for intraday is important factor which decides the investment

turnover of the capital market and depository participants as most of the investors

are intraday traders.

Table 4.5 Brokerage for Intraday Trading

Brokerage for Intraday Trading Residential Status Total

Urban Semi Urban Rural

Count

Expected Count

%within Brokerage for

Intraday Trading

%within residential

Status

% of Total

160

157.9

54.1%

100.0%

53.3%

100

98.7

33.8%

100.0%

33.3%

36

39.5

12.2%

90.0%

12.0%

296

296.0%

100.0%

98.7%

98.7%

Count

Expected Count

%within Brokerage for

Intraday Trading

%within residential

Status

% of Total

0

2.1

.0%

.0%

.0%

0

1.3

.0%

.0%

.0%

4

.5

100.0%

10.0%

1.3%

4

4.0

100.0%

1.3%

1.3%

Total Count

Expected Count

%within Brokerage for

Intraday Trading

%within residential

Status

% of Total

160

160.0

53.3%

100.0%

53.3%

100

100.0

33.3%

100.0%

33.3%

40

40.0

13.3%

100.0%

100.0%

300

300.0

100.0%

100.0%

100.0% Source: Primary data and SPSS.

The table 4.5 indicates that 98.7 percent of total investors opinioned that

depository participants are charging brokerage of 0.03 % for intraday trades

irrespective of their area where as 1.3 percent of total investors opinioned that

depository participants charging other than 0.03 % .It is found that majority of the

investors (98.7 %) opinioned that depository participants are charging brokerage

104

of 0.03 % for intraday trades irrespective of area. It is also observed that 53.3 %

of total investors (160 urban investors) ,33.3 % of total investors (100 semi-

urban investors) and 12 % of investors (36 rural investors) opinioned that

depository participants are charging brokerage for intraday trading to the extent of

0.0 3%. Therefore, it is suggested to the depository participants that they should

levy brokerage uniformly / nominally for intraday trades depending upon the type

of investor , investment amount and residential area , neworth ,etc., so that it

enhances the investment turnover of the depository participants and capital

market.

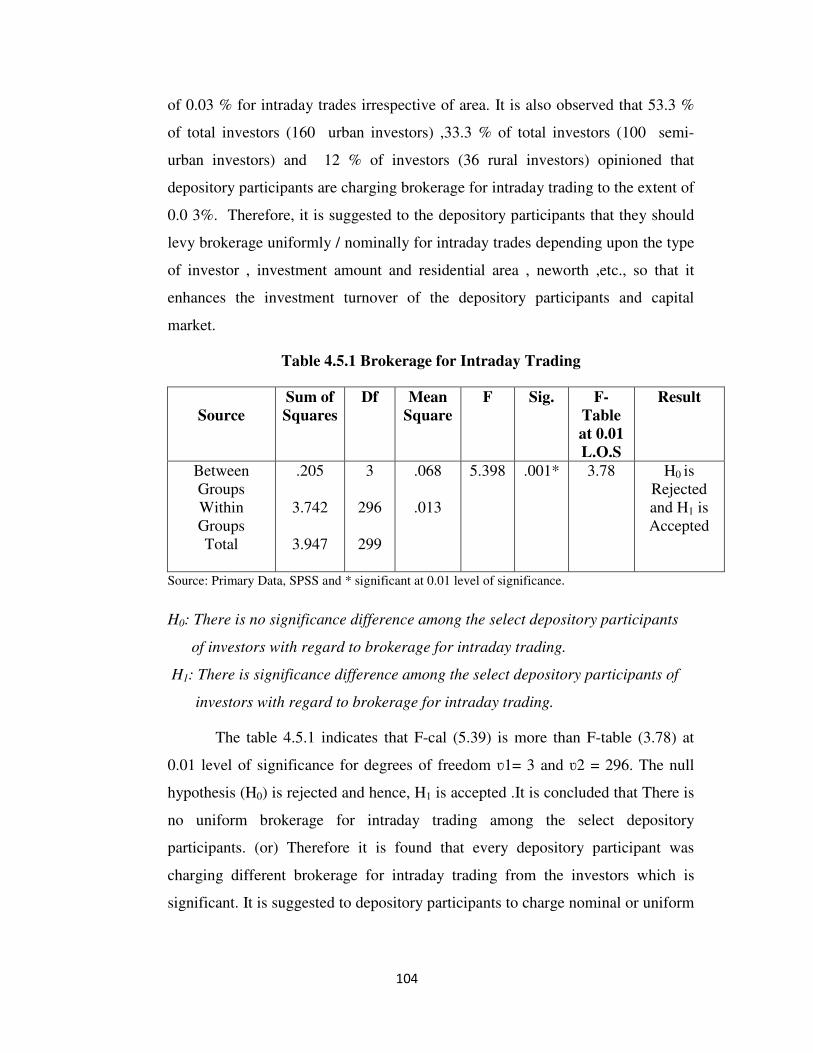

Table 4.5.1 Brokerage for Intraday Trading

Source

Sum of

Squares

Df Mean

Square

F Sig. F-

Table

at 0.01

L.O.S

Result

Between

Groups

Within

Groups

Total

.205

3.742

3.947

3

296

299

.068

.013

5.398 .001* 3.78 H0 is

Rejected

and H1 is

Accepted

Source: Primary Data, SPSS and * significant at 0.01 level of significance.

H0: There is no significance difference among the select depository participants

of investors with regard to brokerage for intraday trading.

H1: There is significance difference among the select depository participants of

investors with regard to brokerage for intraday trading.

The table 4.5.1 indicates that F-cal (5.39) is more than F-table (3.78) at

0.01 level of significance for degrees of freedom ʋ1= 3 and ʋ2 = 296. The null

hypothesis (H0) is rejected and hence, H1 is accepted .It is concluded that There is

no uniform brokerage for intraday trading among the select depository

participants. (or) Therefore it is found that every depository participant was

charging different brokerage for intraday trading from the investors which is

significant. It is suggested to depository participants to charge nominal or uniform

105

brokerage for the intraday trading so that investors will be encouraged for

intraday trading in addition to other types of trading.

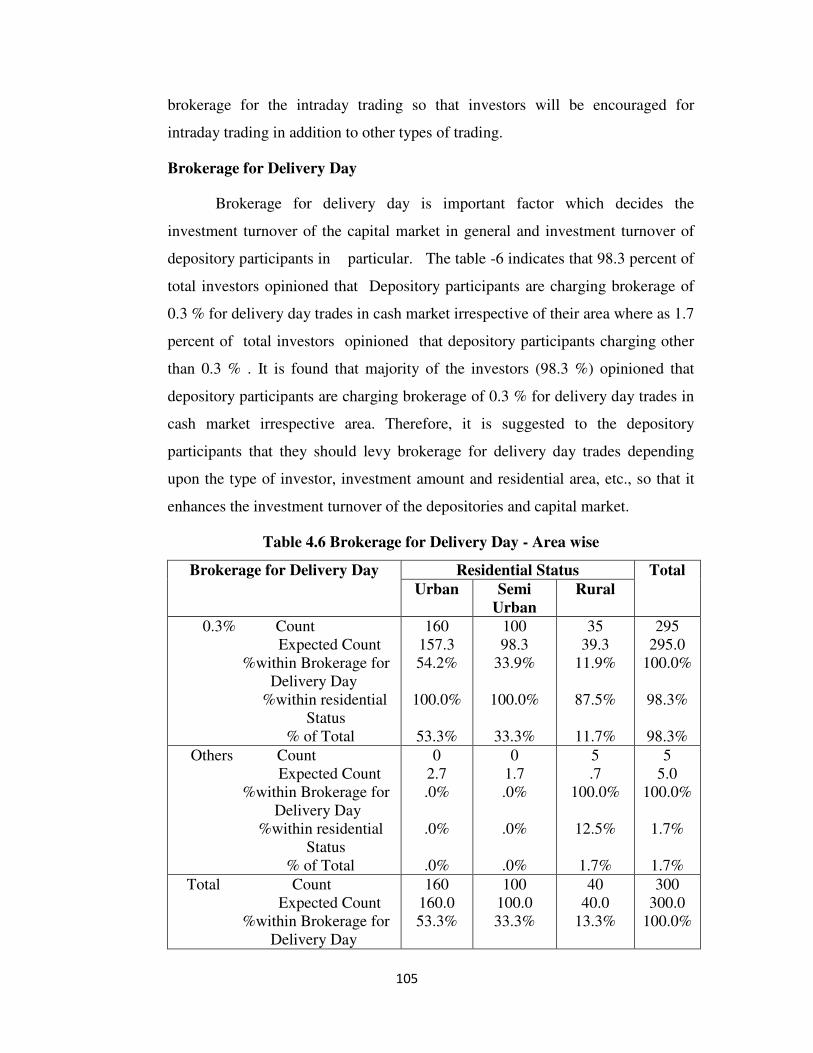

Brokerage for Delivery Day

Brokerage for delivery day is important factor which decides the

investment turnover of the capital market in general and investment turnover of

depository participants in particular. The table -6 indicates that 98.3 percent of

total investors opinioned that Depository participants are charging brokerage of

0.3 % for delivery day trades in cash market irrespective of their area where as 1.7

percent of total investors opinioned that depository participants charging other

than 0.3 % . It is found that majority of the investors (98.3 %) opinioned that

depository participants are charging brokerage of 0.3 % for delivery day trades in

cash market irrespective area. Therefore, it is suggested to the depository

participants that they should levy brokerage for delivery day trades depending

upon the type of investor, investment amount and residential area, etc., so that it

enhances the investment turnover of the depositories and capital market.

Table 4.6 Brokerage for Delivery Day - Area wise

Brokerage for Delivery Day Residential Status Total

Urban Semi

Urban

Rural

0.3% Count

Expected Count

%within Brokerage for

Delivery Day

%within residential

Status

% of Total

160

157.3

54.2%

100.0%

53.3%

100

98.3

33.9%

100.0%

33.3%

35

39.3

11.9%

87.5%

11.7%

295

295.0

100.0%

98.3%

98.3%

Others Count

Expected Count

%within Brokerage for

Delivery Day

%within residential

Status

% of Total

0

2.7

.0%

.0%

.0%

0

1.7

.0%

.0%

.0%

5

.7

100.0%

12.5%

1.7%

5

5.0

100.0%

1.7%

1.7%

Total Count

Expected Count

%within Brokerage for

Delivery Day

160

160.0

53.3%

100

100.0

33.3%

40

40.0

13.3%

300

300.0

100.0%

106

%within residential

Status

% of Total

100.0%

53.3%

100.0%

33.3%

100.0%

13.3%

100.0%

100.0% Source: Primary data and SPSS.

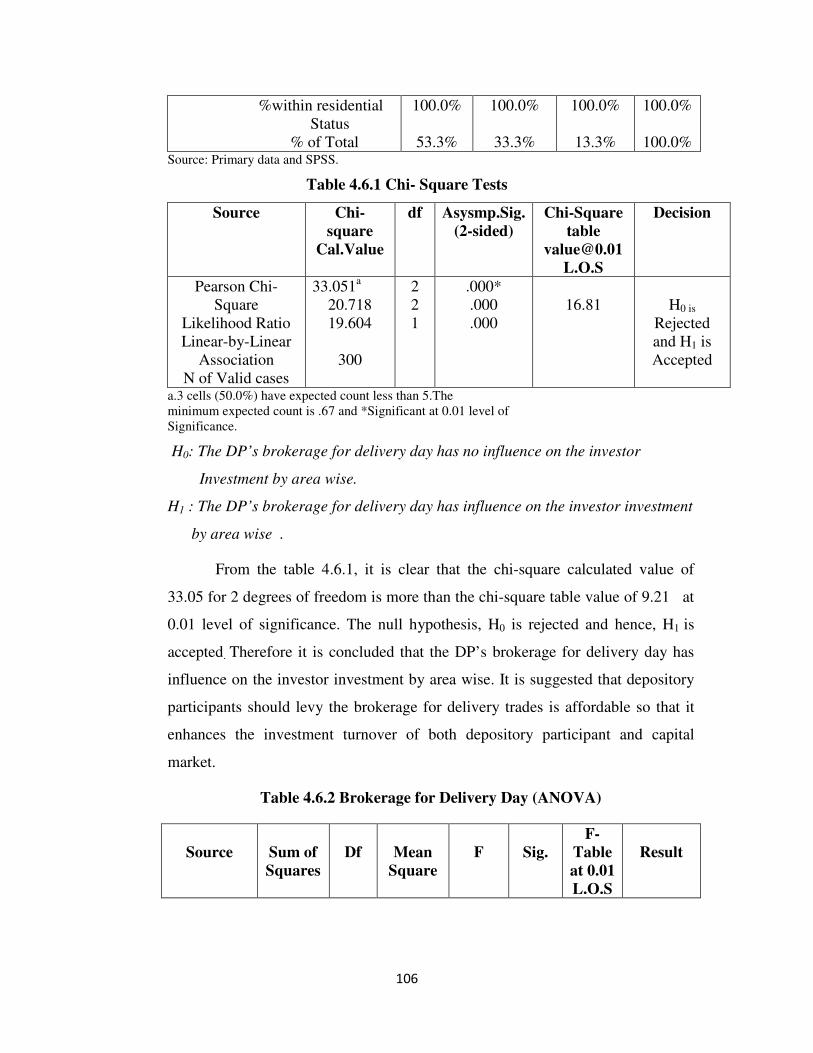

Table 4.6.1 Chi- Square Tests

Source Chi-

square

Cal.Value

df Asysmp.Sig.

(2-sided)

Chi-Square

table

L.O.S

Decision

Pearson Chi-

Square

Likelihood Ratio

Linear-by-Linear

Association

N of Valid cases

33.051a

20.718

19.604

300

2

2

1

.000*

.000

.000

16.81

H0 is

Rejected

and H1 is

Accepted

a.3 cells (50.0%) have expected count less than 5.The

minimum expected count is .67 and *Significant at 0.01 level of

Significance.

H0: The DP’s brokerage for delivery day has no influence on the investor

Investment by area wise.

H1 : The DP’s brokerage for delivery day has influence on the investor investment

by area wise .

From the table 4.6.1, it is clear that the chi-square calculated value of

33.05 for 2 degrees of freedom is more than the chi-square table value of 9.21 at

0.01 level of significance. The null hypothesis, H0 is rejected and hence, H1 is

accepted. Therefore it is concluded that the DP’s brokerage for delivery day has

influence on the investor investment by area wise. It is suggested that depository

participants should levy the brokerage for delivery trades is affordable so that it

enhances the investment turnover of both depository participant and capital

market.

Table 4.6.2 Brokerage for Delivery Day (ANOVA)

Source

Sum of

Squares

Df

Mean

Square

F

Sig.

F-

Table

at 0.01

L.O.S

Result

107

Between

Groups

Within

Groups

Total

.320

4.597

4.917

3

296

299

.107

.016

6.866 .000* 3.78

H0 is

Rejected

and H1 is

Accepted

Source: Primary Data & SPSS and * Significant at 0.01 level of significance.

H0: There is no significance difference among the select depository

Participants with regard to brokerage for delivery day trading.

H1: There is significance difference among the select depository Participants

with regard to brokerage for delivery day trading.

The table 4.6.2 indicates that F-cal (5.39) is more than F-table (3.78) at 0.01

level of significance for degrees of freedom ʋ1= 3 and ʋ2 = 296.The null

hypothesis (H0) is rejected and hence, H1 is accepted .It is concluded that There is

no uniform brokerage for delivery day trading among the select depository

participants (or) Therefore it is found that every depository participant was

charging different brokerage for delivery day trading from the investors which is

significant. It is suggested to depository participants to charge uniform brokerage

from the investors for the delivery day trading that enhance the investor’s base

and loyalty if quality services are provided to them.

Major Business Activities of DPs

The depository participants mainly deals in five segments of business

respectively, demat account opening, dematerialization, rematerialization, trading

and settlement and pledge and hypothecation. Many steps have been taken in

recent years to reform the secondary market so that it may function efficiently and

effectively. Steps are also being taken to broaden the market and make it function

with greater degree of transparency and in the best interest of investors. Some of

the developments in this direction are regulation of intermediaries, change in the

management structure, insistence of quality securities, prohibition of insider

trading, transparency of account practices, and protection of investor’s interest.

Table 4.7 Major Business Activity (ANOVA ONE WAY)

108

Source Sum of

Squares

Df Mean

Square

F Sig. F table

@ 0.01

L.O.S

Decision

Between

Groups

Within

Groups

Total

7.680

2.400

10.080

3

46

49

2.560

.052

49.067 .000* 4.13 H0 is

Reject

and H1 is

Accepted

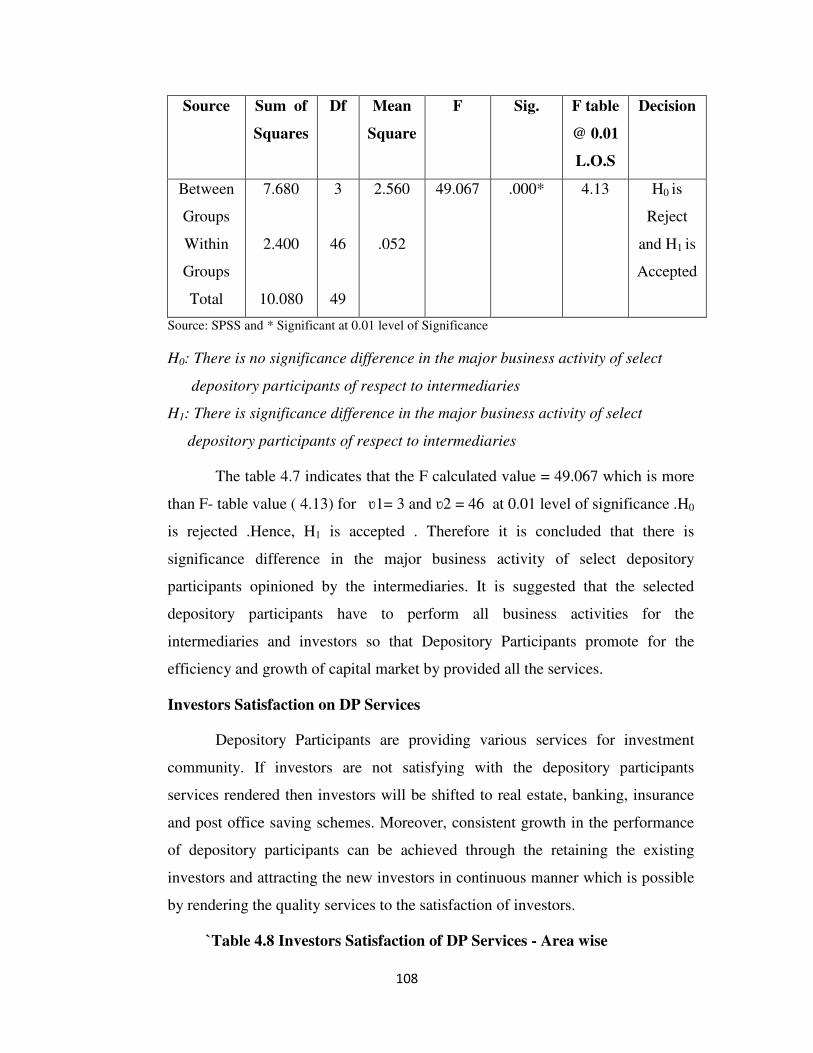

Source: SPSS and * Significant at 0.01 level of Significance

H0: There is no significance difference in the major business activity of select

depository participants of respect to intermediaries

H1: There is significance difference in the major business activity of select

depository participants of respect to intermediaries

The table 4.7 indicates that the F calculated value = 49.067 which is more

than F- table value ( 4.13) for ʋ1= 3 and ʋ2 = 46 at 0.01 level of significance .H0

is rejected .Hence, H1 is accepted . Therefore it is concluded that there is

significance difference in the major business activity of select depository

participants opinioned by the intermediaries. It is suggested that the selected

depository participants have to perform all business activities for the

intermediaries and investors so that Depository Participants promote for the

efficiency and growth of capital market by provided all the services.

Investors Satisfaction on DP Services

Depository Participants are providing various services for investment

community. If investors are not satisfying with the depository participants

services rendered then investors will be shifted to real estate, banking, insurance

and post office saving schemes. Moreover, consistent growth in the performance

of depository participants can be achieved through the retaining the existing

investors and attracting the new investors in continuous manner which is possible

by rendering the quality services to the satisfaction of investors.

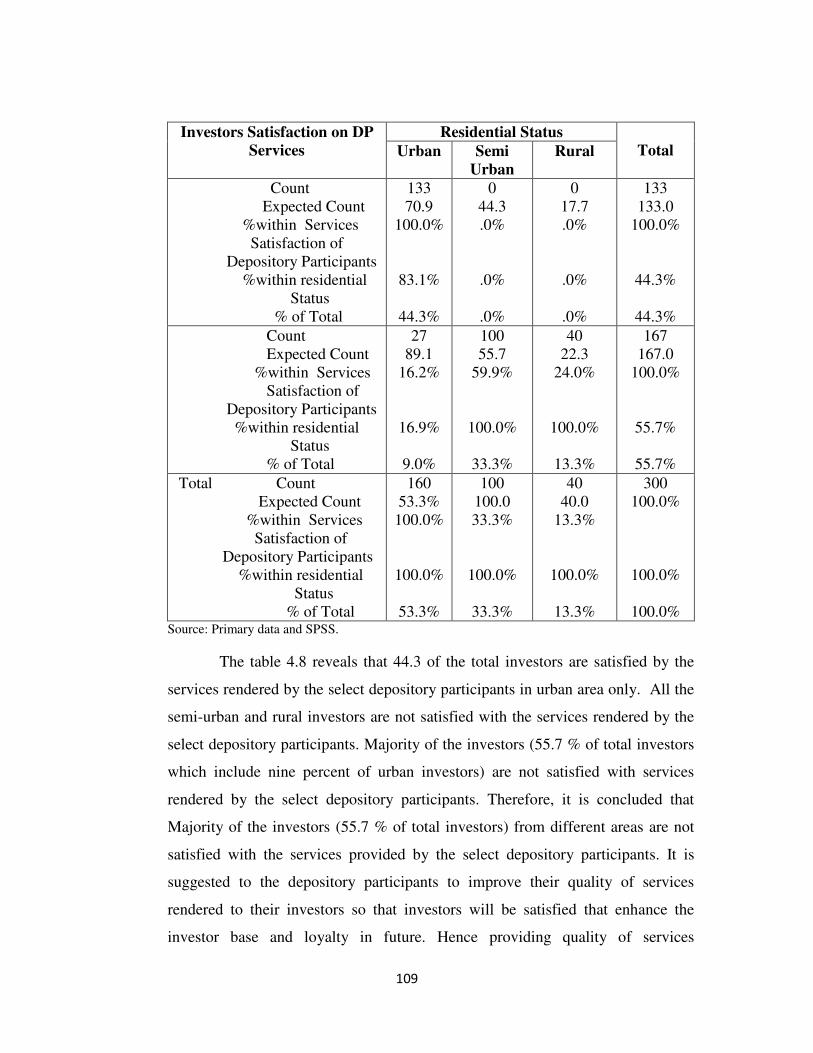

`Table 4.8 Investors Satisfaction of DP Services - Area wise

109

Investors Satisfaction on DP

Services

Residential Status

Total Urban Semi

Urban

Rural

Count

Expected Count

%within Services

Satisfaction of

Depository Participants

%within residential

Status

% of Total

133

70.9

100.0%

83.1%

44.3%

0

44.3

.0%

.0%

.0%

0

17.7

.0%

.0%

.0%

133

133.0

100.0%

44.3%

44.3%

Count

Expected Count

%within Services

Satisfaction of

Depository Participants

%within residential

Status

% of Total

27

89.1

16.2%

16.9%

9.0%

100

55.7

59.9%

100.0%

33.3%

40

22.3

24.0%

100.0%

13.3%

167

167.0

100.0%

55.7%

55.7%

Total Count

Expected Count

%within Services

Satisfaction of

Depository Participants

%within residential

Status

% of Total

160

53.3%

100.0%

100.0%

53.3%

100

100.0

33.3%

100.0%

33.3%

40

40.0

13.3%

100.0%

13.3%

300

100.0%

100.0%

100.0% Source: Primary data and SPSS.

The table 4.8 reveals that 44.3 of the total investors are satisfied by the

services rendered by the select depository participants in urban area only. All the

semi-urban and rural investors are not satisfied with the services rendered by the

select depository participants. Majority of the investors (55.7 % of total investors

which include nine percent of urban investors) are not satisfied with services

rendered by the select depository participants. Therefore, it is concluded that

Majority of the investors (55.7 % of total investors) from different areas are not

satisfied with the services provided by the select depository participants. It is

suggested to the depository participants to improve their quality of services

rendered to their investors so that investors will be satisfied that enhance the

investor base and loyalty in future. Hence providing quality of services

110

consistently is the key for improving the satisfaction of investors and enhancing

the performance of depository participants.

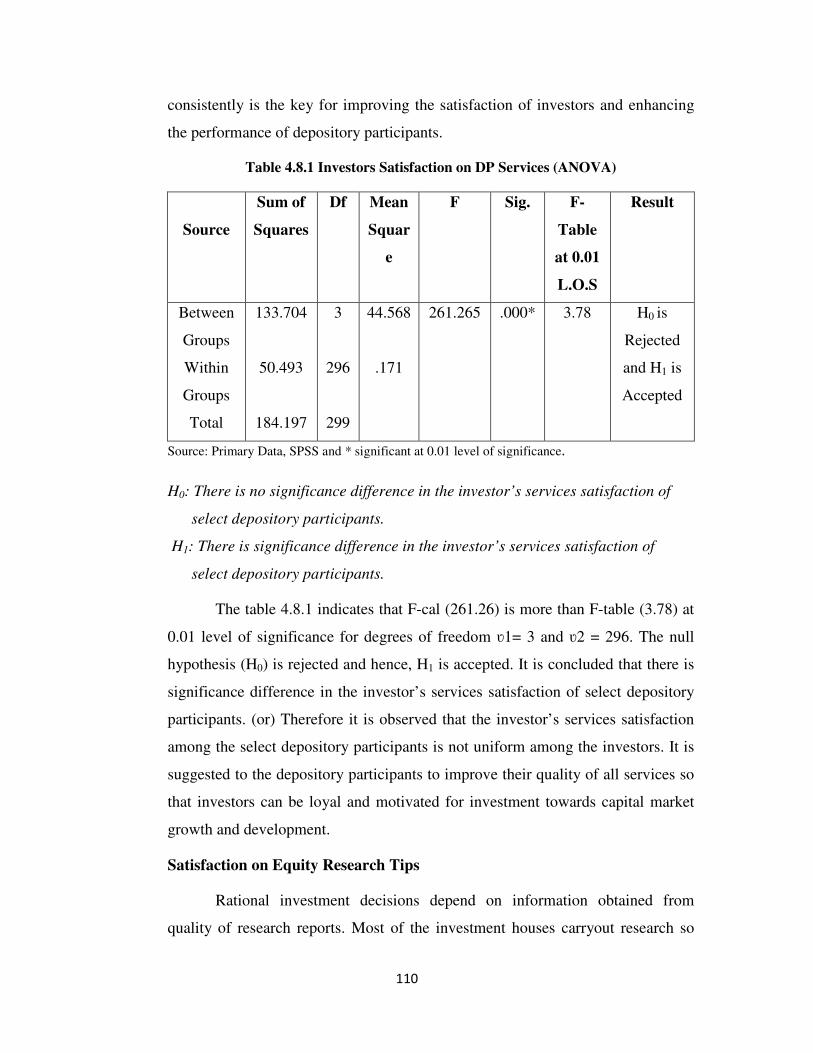

Table 4.8.1 Investors Satisfaction on DP Services (ANOVA)

Source

Sum of

Squares

Df Mean

Squar

e

F Sig. F-

Table

at 0.01

L.O.S

Result

Between

Groups

Within

Groups

Total

133.704

50.493

184.197

3

296

299

44.568

.171

261.265 .000* 3.78 H0 is

Rejected

and H1 is

Accepted

Source: Primary Data, SPSS and * significant at 0.01 level of significance.

H0: There is no significance difference in the investor’s services satisfaction of

select depository participants.

H1: There is significance difference in the investor’s services satisfaction of

select depository participants.

The table 4.8.1 indicates that F-cal (261.26) is more than F-table (3.78) at

0.01 level of significance for degrees of freedom ʋ1= 3 and ʋ2 = 296. The null

hypothesis (H0) is rejected and hence, H1 is accepted. It is concluded that there is

significance difference in the investor’s services satisfaction of select depository

participants. (or) Therefore it is observed that the investor’s services satisfaction

among the select depository participants is not uniform among the investors. It is

suggested to the depository participants to improve their quality of all services so

that investors can be loyal and motivated for investment towards capital market

growth and development.

Satisfaction on Equity Research Tips

Rational investment decisions depend on information obtained from

quality of research reports. Most of the investment houses carryout research so

111

that to provide research tips or information to their investors for taking rational

investment decisions that enhances the returns and minimizes the risk involved in

the investment decisions. It is a challenging task for the investment houses to

provide quality research tips to their investor’s .More over investors satisfaction

largely depends on research tips / information related to investment decisions.

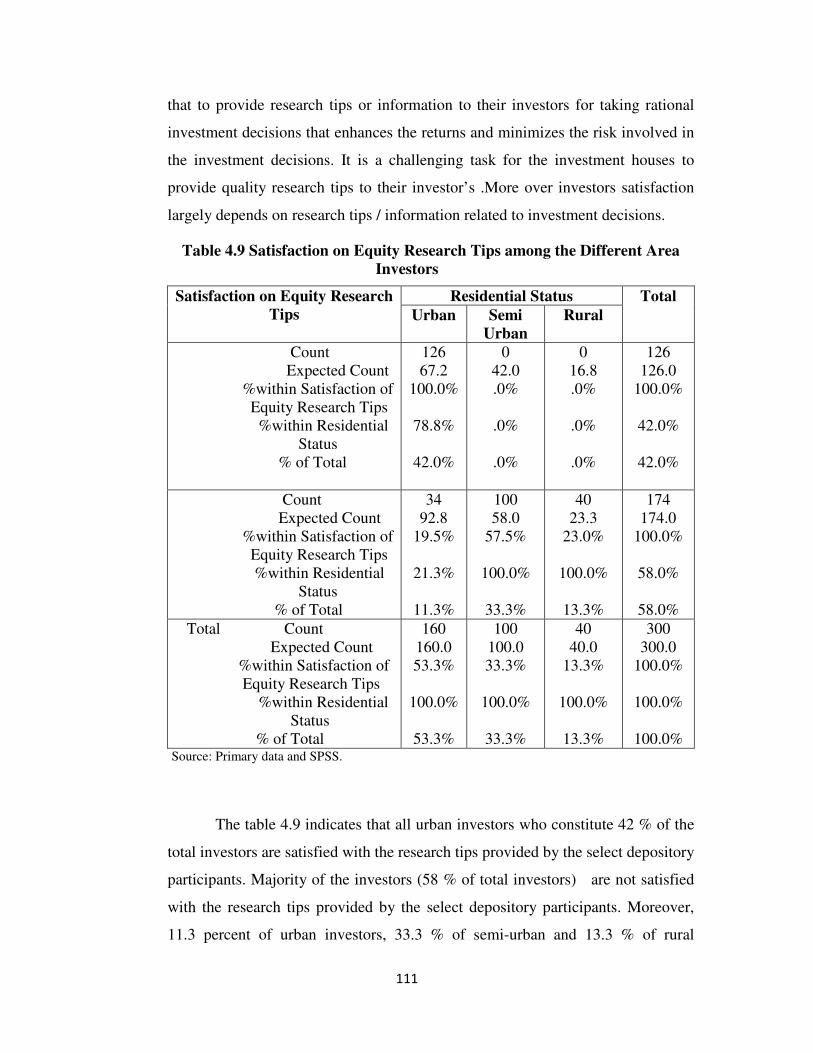

Table 4.9 Satisfaction on Equity Research Tips among the Different Area

Investors

Satisfaction on Equity Research

Tips

Residential Status Total

Urban Semi

Urban

Rural

Count

Expected Count

%within Satisfaction of

Equity Research Tips

%within Residential

Status

% of Total

126

67.2

100.0%

78.8%

42.0%

0

42.0

.0%

.0%

.0%

0

16.8

.0%

.0%

.0%

126

126.0

100.0%

42.0%

42.0%

Count

Expected Count

%within Satisfaction of

Equity Research Tips

%within Residential

Status

% of Total

34

92.8

19.5%

21.3%

11.3%

100

58.0

57.5%

100.0%

33.3%

40

23.3

23.0%

100.0%

13.3%

174

174.0

100.0%

58.0%

58.0%

Total Count

Expected Count

%within Satisfaction of

Equity Research Tips

%within Residential

Status

% of Total

160

160.0

53.3%

100.0%

53.3%

100

100.0

33.3%

100.0%

33.3%

40

40.0

13.3%

100.0%

13.3%

300

300.0

100.0%

100.0%

100.0% Source: Primary data and SPSS.

The table 4.9 indicates that all urban investors who constitute 42 % of the

total investors are satisfied with the research tips provided by the select depository

participants. Majority of the investors (58 % of total investors) are not satisfied

with the research tips provided by the select depository participants. Moreover,

11.3 percent of urban investors, 33.3 % of semi-urban and 13.3 % of rural

112

investors are not satisfied with the research tips provided by the select depository

participants. Therefore, it is observed that majority (58 % of total investors) of

investors which include 11.3 % of total investors from urban area; all semi-urban

and rural investors are not satisfied with the research tips provided by the select

depository participants. In this regard, it is suggested to the depository

participants to improve the quality of research tips so that it provides quality of

investment information to their investors for taking wise investment decisions that

optimize the returns and risk to the investors and also satisfies the investor

community.

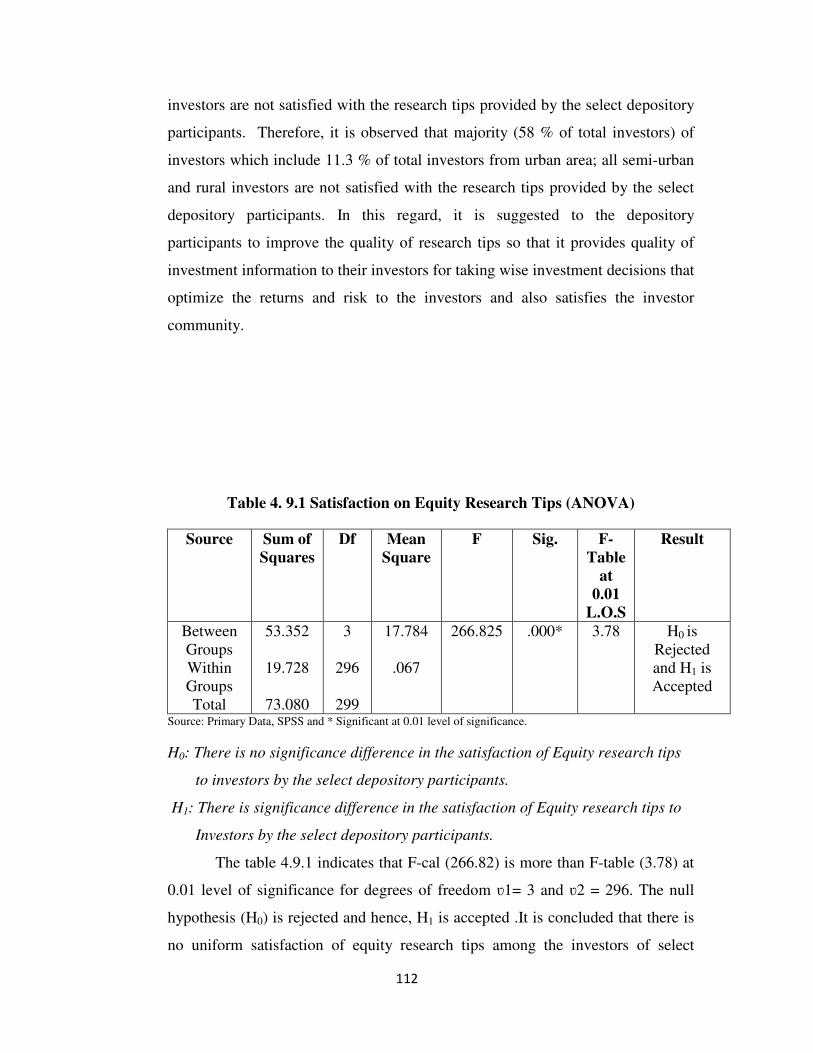

Table 4. 9.1 Satisfaction on Equity Research Tips (ANOVA)

Source Sum of

Squares

Df Mean

Square

F Sig. F-

Table

at

0.01

L.O.S

Result

Between

Groups

Within

Groups

Total

53.352

19.728

73.080

3

296

299

17.784

.067

266.825 .000* 3.78 H0 is

Rejected

and H1 is

Accepted

Source: Primary Data, SPSS and * Significant at 0.01 level of significance.

H0: There is no significance difference in the satisfaction of Equity research tips

to investors by the select depository participants.

H1: There is significance difference in the satisfaction of Equity research tips to

Investors by the select depository participants.

The table 4.9.1 indicates that F-cal (266.82) is more than F-table (3.78) at

0.01 level of significance for degrees of freedom ʋ1= 3 and ʋ2 = 296. The null

hypothesis (H0) is rejected and hence, H1 is accepted .It is concluded that there is

no uniform satisfaction of equity research tips among the investors of select

113

depository participants. It is suggested to depository participants that to provide

quality of equity research tips to the investors for improving their satisfaction and

enhancing the investors’ confidence.

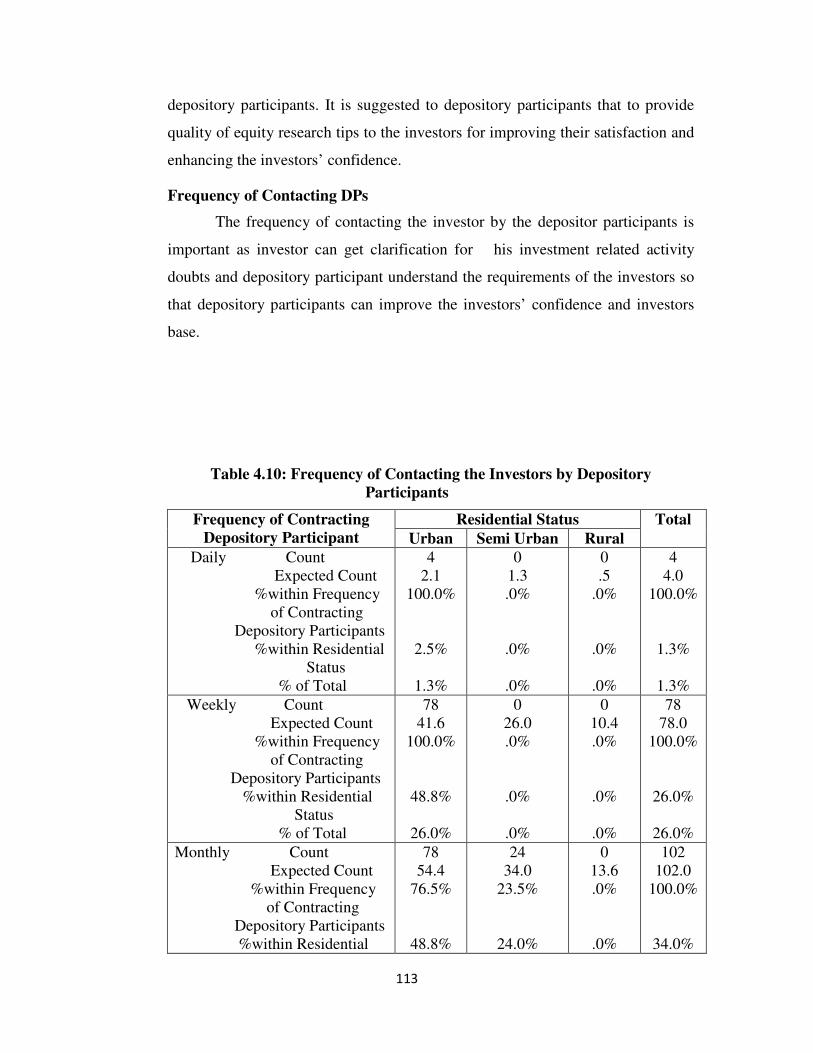

Frequency of Contacting DPs

The frequency of contacting the investor by the depositor participants is

important as investor can get clarification for his investment related activity

doubts and depository participant understand the requirements of the investors so

that depository participants can improve the investors’ confidence and investors

base.

Table 4.10: Frequency of Contacting the Investors by Depository

Participants

Frequency of Contracting

Depository Participant

Residential Status Total

Urban Semi Urban Rural

Daily Count

Expected Count

%within Frequency

of Contracting

Depository Participants

%within Residential

Status

% of Total

4

2.1

100.0%

2.5%

1.3%

0

1.3

.0%

.0%

.0%

0

.5

.0%

.0%

.0%

4

4.0

100.0%

1.3%

1.3%

Weekly Count

Expected Count

%within Frequency

of Contracting

Depository Participants

%within Residential

Status

% of Total

78

41.6

100.0%

48.8%

26.0%

0

26.0

.0%

.0%

.0%

0

10.4

.0%

.0%

.0%

78

78.0

100.0%

26.0%

26.0%

Monthly Count

Expected Count

%within Frequency

of Contracting

Depository Participants

%within Residential

78

54.4

76.5%

48.8%

24

34.0

23.5%

24.0%

0

13.6

.0%

.0%

102

102.0

100.0%

34.0%

114

Status

% of Total

26.0%

8.0%

.0%

34.0%

Rarely Count

Expected Count

%within Frequency

of Contracting

Depository Participants

%within Residential

Status

% of Total

0

61.9

.0%

.0%

.0%

76

38.7

65.5%

76.0%

25.3%

40

15.5

34.5%

100.0%

13.3%

116

116.0

100.0%

38.7%

38.7%

Total Count

Expected Count

%within Frequency

of Contracting

Depository Participants

%within Residential

Status

% of Total

160

160.0

53.3%

100.0%

53.3%

100

100.0

33.3%

100.0%

33.3%

40

40.0

13.3%

100.0%

13.3%

300

300.0

100.0%

100.0%

100.0% Source: Primary Data and SPSS

The table 4.10 reveals that four urban investors or 1.3 % of total

investors are informed that DP’s are contacting them by daily , 78 urban

investors who constitute 26 % of total investors are informed that DP’s are

contacting them by weekly, 78 urban investors who constitute 26 % of total

investors and 24 semi-urban investors who constitute eight percent of total

investors are informed that DP’s are contacting them by monthly, 76 semi- urban

investors who constitute 25.3 % of total investors and 40 rural investors who

constitute 13.3 % of total investors are informed that DP’s are contacting them

by rarely. It is observed that Majority of the investors (38.7 % of total investors)

are informed that DP’s are contacting them by rarely, 34 % of total investors are

informed that DP’s are contacting them by monthly, 26 % of total investors are

informed that DP’s are contacting them by weekly and remaining 1.3 % of total

investors are informed that DP’s are contacting them by daily. Therefore, it is

suggested that depository participants should improve the frequency of contacting

the investors at least to weekly so that investors can get clarification for their

investment activity related doubts and thus it helps to improve investor-

depository relationship and also enhance the investor base and investor loyalty.

115

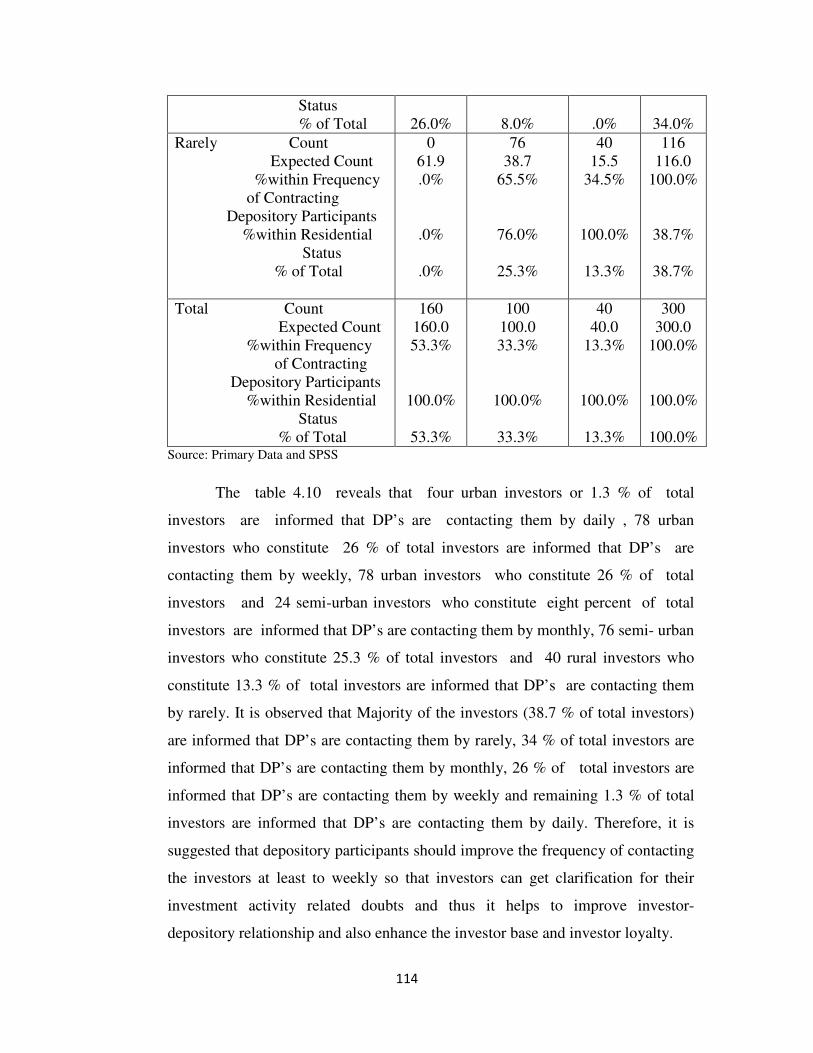

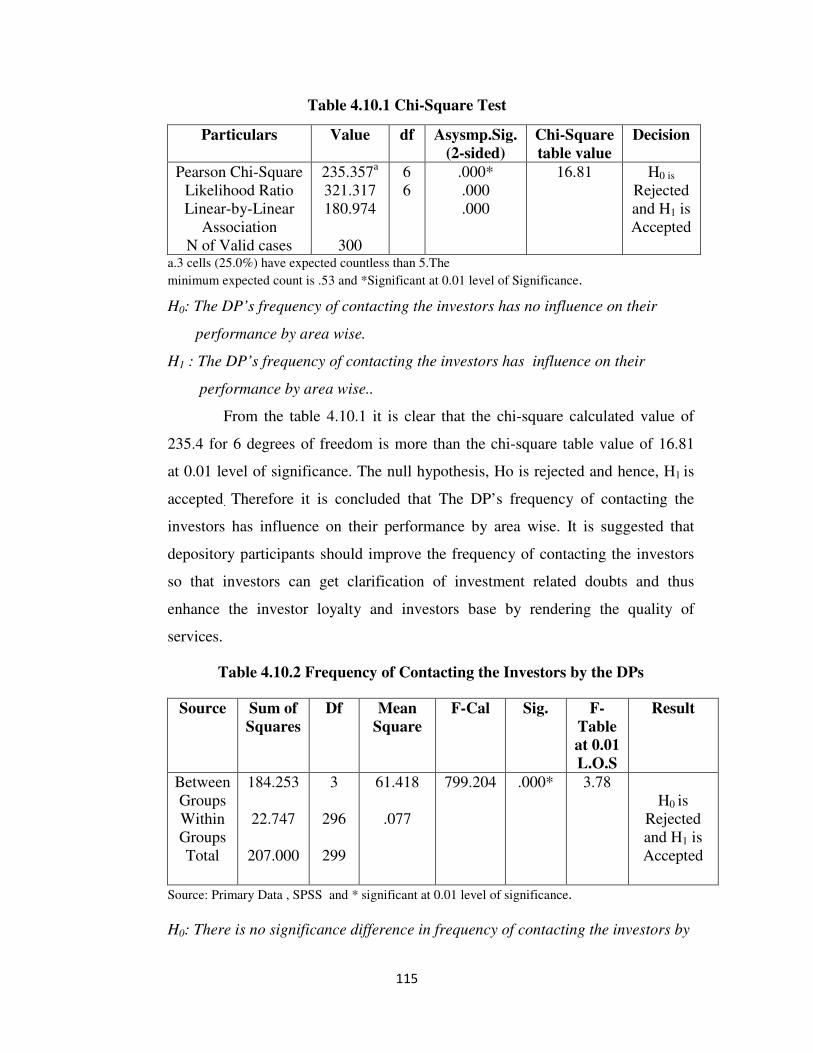

Table 4.10.1 Chi-Square Test

Particulars Value df Asysmp.Sig.

(2-sided)

Chi-Square

table value

Decision

Pearson Chi-Square

Likelihood Ratio

Linear-by-Linear

Association

N of Valid cases

235.357a

321.317

180.974

300

6

6

.000*

.000

.000

16.81 H0 is

Rejected

and H1 is

Accepted

a.3 cells (25.0%) have expected countless than 5.The

minimum expected count is .53 and *Significant at 0.01 level of Significance.

H0: The DP’s frequency of contacting the investors has no influence on their

performance by area wise.

H1 : The DP’s frequency of contacting the investors has influence on their

performance by area wise..

From the table 4.10.1 it is clear that the chi-square calculated value of

235.4 for 6 degrees of freedom is more than the chi-square table value of 16.81

at 0.01 level of significance. The null hypothesis, Ho is rejected and hence, H1 is

accepted. Therefore it is concluded that The DP’s frequency of contacting the

investors has influence on their performance by area wise. It is suggested that

depository participants should improve the frequency of contacting the investors

so that investors can get clarification of investment related doubts and thus

enhance the investor loyalty and investors base by rendering the quality of

services.

Table 4.10.2 Frequency of Contacting the Investors by the DPs

Source Sum of

Squares

Df Mean

Square

F-Cal Sig. F-

Table

at 0.01

L.O.S

Result

Between

Groups

Within

Groups

Total

184.253

22.747

207.000

3

296

299

61.418

.077

799.204 .000* 3.78

H0 is

Rejected

and H1 is

Accepted

Source: Primary Data , SPSS and * significant at 0.01 level of significance.

H0: There is no significance difference in frequency of contacting the investors by

116

the select depository participants.

H1: There is significance difference in frequency of contacting the investors by

the select depository participants.

The table 4.10.2 indicates that F-cal (799.20) is more than F-table (3.78) at

0.01 level of significance for degrees of freedom ʋ1= 3 and ʋ2 = 296. The null

hypothesis (H0) is rejected and hence, H1 is accepted .It is concluded that there is

no uniformity in the frequency of contacting the investors by the select depository

participants which is significant. It is suggested to depository participants to

improve their frequency of contacting the investors for clarifying their investment

related problems and to render quality of investment advisory services.

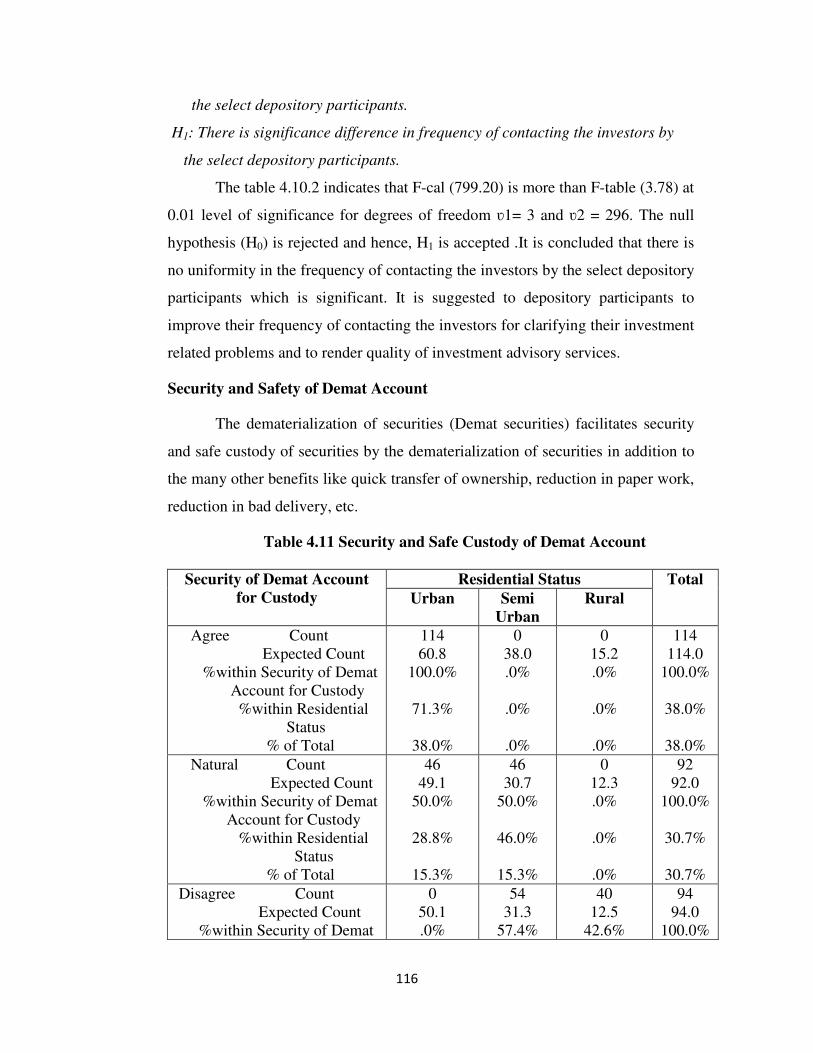

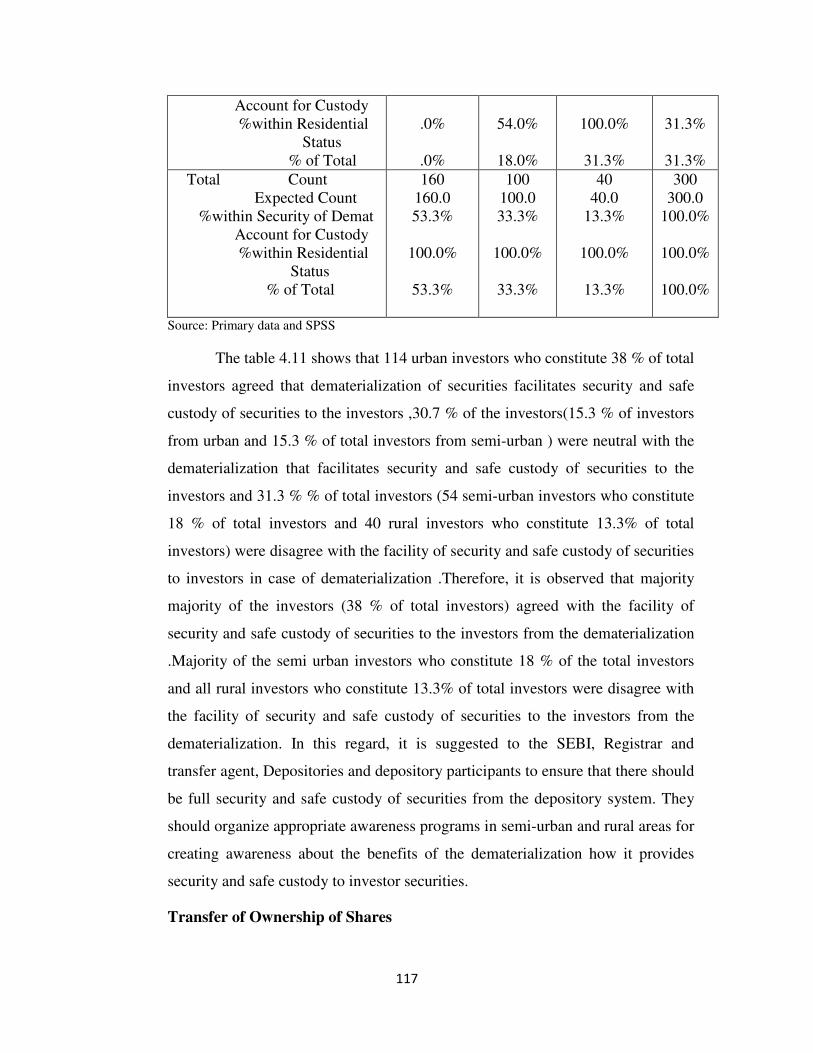

Security and Safety of Demat Account

The dematerialization of securities (Demat securities) facilitates security

and safe custody of securities by the dematerialization of securities in addition to

the many other benefits like quick transfer of ownership, reduction in paper work,

reduction in bad delivery, etc.

Table 4.11 Security and Safe Custody of Demat Account

Security of Demat Account

for Custody

Residential Status Total

Urban Semi

Urban

Rural

Agree Count

Expected Count

%within Security of Demat

Account for Custody

%within Residential

Status

% of Total

114

60.8

100.0%

71.3%

38.0%

0

38.0

.0%

.0%

.0%

0

15.2

.0%

.0%

.0%

114

114.0

100.0%

38.0%

38.0%

Natural Count

Expected Count

%within Security of Demat

Account for Custody

%within Residential

Status

% of Total

46

49.1

50.0%

28.8%

15.3%

46

30.7

50.0%

46.0%

15.3%

0

12.3

.0%

.0%

.0%

92

92.0

100.0%

30.7%

30.7%

Disagree Count

Expected Count

%within Security of Demat

0

50.1

.0%

54

31.3

57.4%

40

12.5

42.6%

94

94.0

100.0%

117

Account for Custody

%within Residential

Status

% of Total

.0%

.0%

54.0%

18.0%

100.0%

31.3%

31.3%

31.3%

Total Count

Expected Count

%within Security of Demat

Account for Custody

%within Residential

Status

% of Total

160

160.0

53.3%

100.0%

53.3%

100

100.0

33.3%

100.0%

33.3%

40

40.0

13.3%

100.0%

13.3%

300

300.0

100.0%

100.0%

100.0%

Source: Primary data and SPSS

The table 4.11 shows that 114 urban investors who constitute 38 % of total

investors agreed that dematerialization of securities facilitates security and safe

custody of securities to the investors ,30.7 % of the investors(15.3 % of investors

from urban and 15.3 % of total investors from semi-urban ) were neutral with the

dematerialization that facilitates security and safe custody of securities to the

investors and 31.3 % % of total investors (54 semi-urban investors who constitute

18 % of total investors and 40 rural investors who constitute 13.3% of total

investors) were disagree with the facility of security and safe custody of securities

to investors in case of dematerialization .Therefore, it is observed that majority

majority of the investors (38 % of total investors) agreed with the facility of

security and safe custody of securities to the investors from the dematerialization

.Majority of the semi urban investors who constitute 18 % of the total investors

and all rural investors who constitute 13.3% of total investors were disagree with

the facility of security and safe custody of securities to the investors from the

dematerialization. In this regard, it is suggested to the SEBI, Registrar and

transfer agent, Depositories and depository participants to ensure that there should

be full security and safe custody of securities from the depository system. They

should organize appropriate awareness programs in semi-urban and rural areas for

creating awareness about the benefits of the dematerialization how it provides

security and safe custody to investor securities.

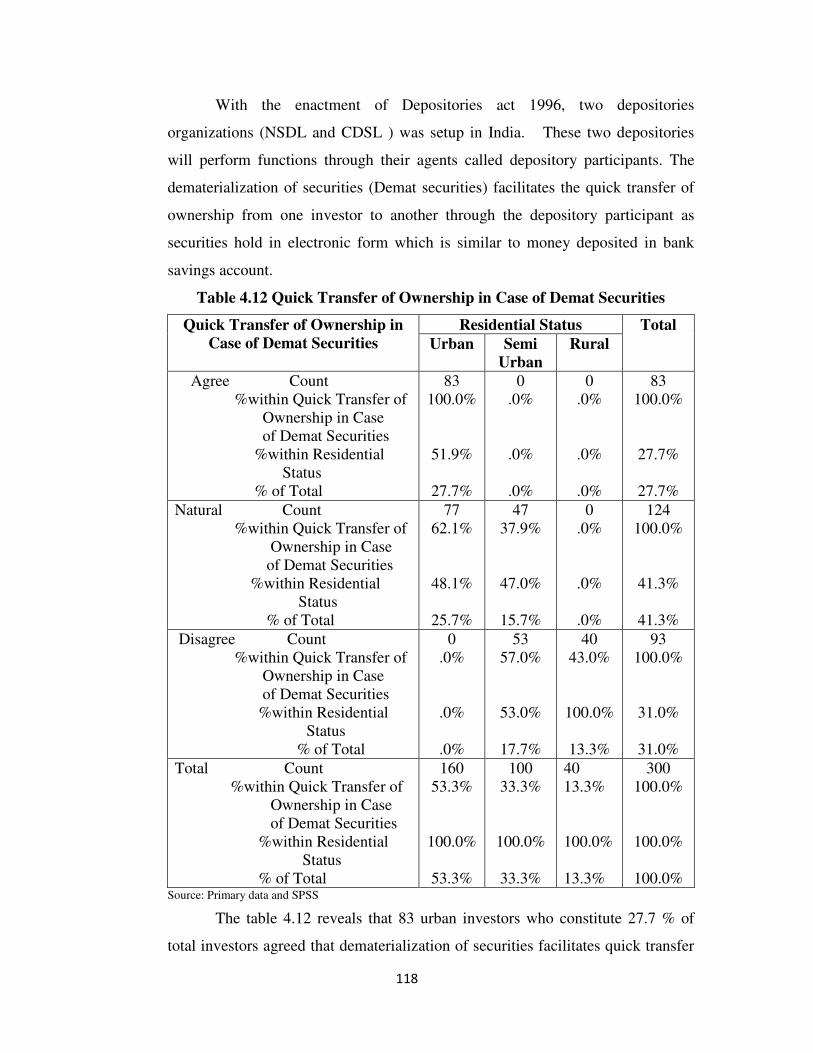

Transfer of Ownership of Shares

118

With the enactment of Depositories act 1996, two depositories

organizations (NSDL and CDSL ) was setup in India. These two depositories

will perform functions through their agents called depository participants. The

dematerialization of securities (Demat securities) facilitates the quick transfer of

ownership from one investor to another through the depository participant as

securities hold in electronic form which is similar to money deposited in bank

savings account.

Table 4.12 Quick Transfer of Ownership in Case of Demat Securities

Quick Transfer of Ownership in

Case of Demat Securities

Residential Status Total

Urban Semi

Urban

Rural

Agree Count

%within Quick Transfer of

Ownership in Case

of Demat Securities

%within Residential

Status

% of Total

83

100.0%

51.9%

27.7%

0

.0%

.0%

.0%

0

.0%

.0%

.0%

83

100.0%

27.7%

27.7%

Natural Count

%within Quick Transfer of

Ownership in Case

of Demat Securities

%within Residential

Status

% of Total

77

62.1%

48.1%

25.7%

47

37.9%

47.0%

15.7%

0

.0%

.0%

.0%

124

100.0%

41.3%

41.3%

Disagree Count

%within Quick Transfer of

Ownership in Case

of Demat Securities

%within Residential

Status

% of Total

0

.0%

.0%

.0%

53

57.0%

53.0%

17.7%

40

43.0%

100.0%

13.3%

93

100.0%

31.0%

31.0%

Total Count

%within Quick Transfer of

Ownership in Case

of Demat Securities

%within Residential

Status

% of Total

160

53.3%

100.0%

53.3%

100

33.3%

100.0%

33.3%

40

13.3%

100.0%

13.3%

300

100.0%

100.0%

100.0% Source: Primary data and SPSS

The table 4.12 reveals that 83 urban investors who constitute 27.7 % of

total investors agreed that dematerialization of securities facilitates quick transfer

119

of ownership , 41.3 % of total investors (77 urban investors who constitute 25.7 %

of total investors and 47 semi-urban investors constitute 15.7 % of total

investors) were neutral with regard to quick transfer of ownership by the

dematerialization and 31 % of total investors (53 semi-urban investors who

constitute 17.7 % of total investors and 40 rural investors who constitute 13.3%

of total investors) were disagree with the facility of quick transfer of ownership in

case of dematerialization of securities. Therefore, it is observed that majority of

the (27.7 % of total investors) urban investors agreed with facility of quick

transfer of ownership in case of dematerialization of securities only.

Majority of the investors (41.3% of total investors) neither agree nor

disagree with the facility of quick transfer of ownership in case of

dematerialization of securities. Majority of the semi-urban investors (17.7 % of

total investors) and half of the rural investors ( 13.3 % of total investors ) were

disagree with the quick transfer of ownership from the dematerialization of

securities. In this regard, it is suggested to the SEBI, Registrar and transfer agent,

Depositories and depository participants to minimize the time taken to transfer the

ownership of securities in the dematerialization process and it helps the quick

transfer of ownership of securities from the dematerialization. The benefits of

dematerialization must reach to the investors so that they will be comfortable and

confident; it in turn promotes growth of the capital market.

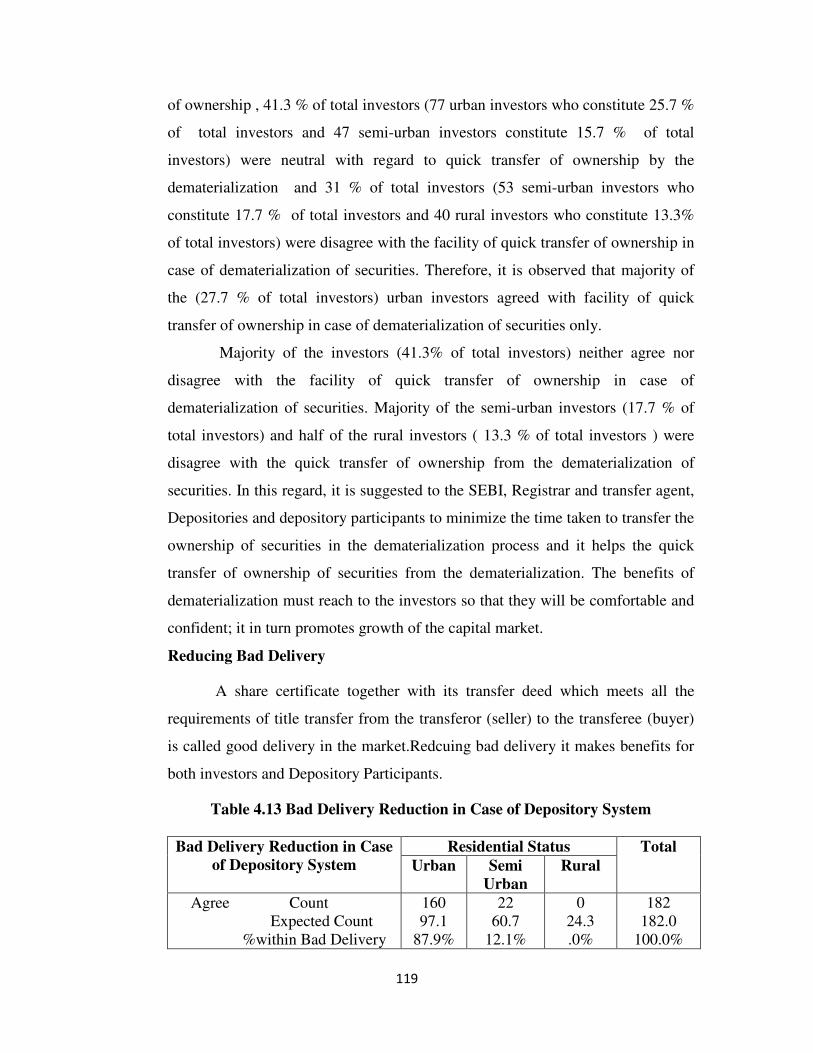

Reducing Bad Delivery

A share certificate together with its transfer deed which meets all the

requirements of title transfer from the transferor (seller) to the transferee (buyer)

is called good delivery in the market.Redcuing bad delivery it makes benefits for

both investors and Depository Participants.

Table 4.13 Bad Delivery Reduction in Case of Depository System

Bad Delivery Reduction in Case

of Depository System

Residential Status Total

Urban Semi

Urban

Rural

Agree Count

Expected Count

%within Bad Delivery

160

97.1

87.9%

22

60.7

12.1%

0

24.3

.0%

182

182.0

100.0%

120

Reduction in Case of

Depository System

%within Residential

Status

% of Total

100.0%

53.3%

22.0%

7.3%

.0%

.0%

60.7%

60.7%

Natural Count

Expected Count

%within Bad Delivery

Reduction in Case of

Depository System

%within Residential

Status

% of Total

0

40.0

.0%

.0%

.0%

75

25.0

100.0%

75.0%

25.0%

0

10.0

.0%

.0%

.0%

75

75.0

100.0%

25.0%

25.0%

Disagree Count

Expected Count

%within Bad Delivery

Reduction in Case of

Depository System

%within Residential

Status

% of Total

0

22.9

.0%

.0%

.0%

3

14.3

7.0%

3.0%

1.0%

40

5.7

93.0%

100.0%

13.3%

43

43.0

100.0%

14.3%

14.3%

Total Count

Expected Count

%within Bad Delivery

Reduction in Case of

Depository System

%within Residential

Status

% of Total

160

160.0

53.3%

100.0%

53.3%

100

100.0

33.3%

100.0%

33.3%

40

40.0

13.3%

100.0%

13.3%

300

300.0

100.0%

100.0%

100.0% Source: Primary data and SPSS

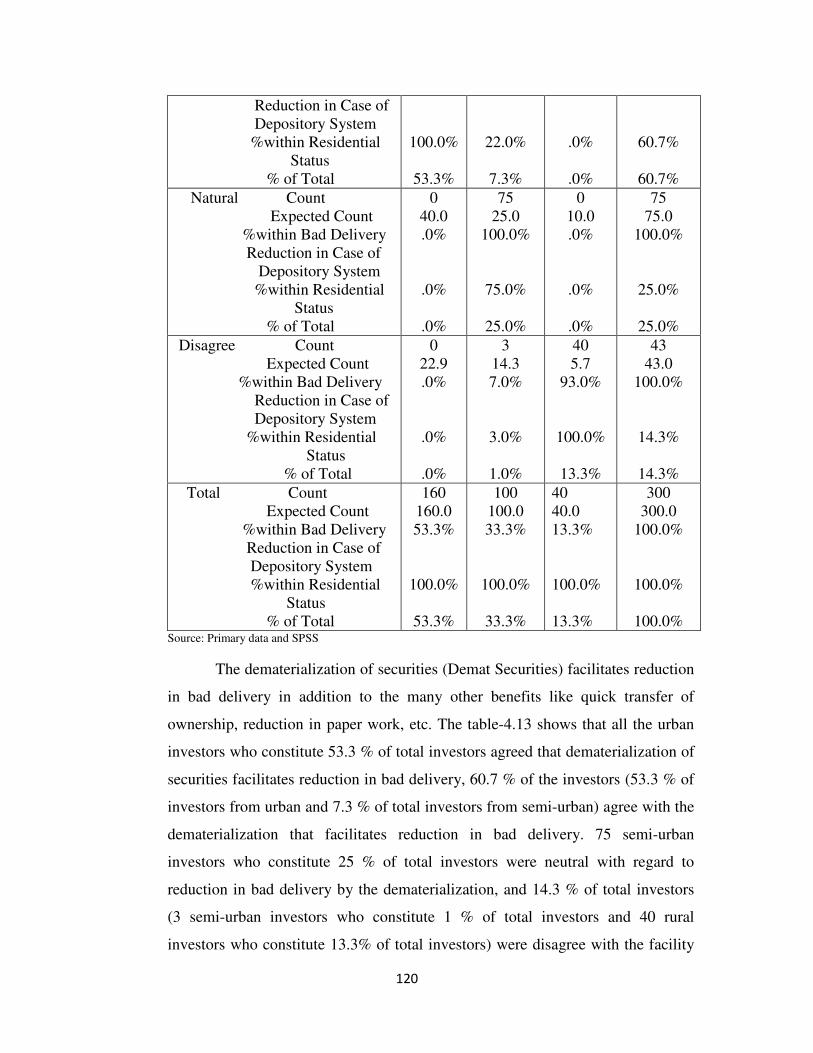

The dematerialization of securities (Demat Securities) facilitates reduction

in bad delivery in addition to the many other benefits like quick transfer of

ownership, reduction in paper work, etc. The table-4.13 shows that all the urban

investors who constitute 53.3 % of total investors agreed that dematerialization of

securities facilitates reduction in bad delivery, 60.7 % of the investors (53.3 % of

investors from urban and 7.3 % of total investors from semi-urban) agree with the

dematerialization that facilitates reduction in bad delivery. 75 semi-urban

investors who constitute 25 % of total investors were neutral with regard to

reduction in bad delivery by the dematerialization, and 14.3 % of total investors

(3 semi-urban investors who constitute 1 % of total investors and 40 rural

investors who constitute 13.3% of total investors) were disagree with the facility

121

of reduction in bad delivery in case of dematerialization of securities. Therefore, it

is observed that majority of the (53.3 % of total investors) urban investors agreed

with facility of reduction in paper work in case of dematerialization of securities

only. Majority of the investors (60.7 % of total investors) agreed with the facility

of reduction in bad delivery in case of dematerialization of securities. Majority of

the semi-urban investors (75 semi-urban investors who constitute 25 % of total

investors) were neutral with regard to reduction in bad delivery by the

dematerialization. All the rural investors who constitute 13.3% of total investors)

disagreed with the facility of reduction in bad delivery in case of

dematerialization of securities. In this regard, it is suggested to the SEBI,

Registrar and transfer agent, Depositories and depository participants to ensure

that there should be no bad delivery of securities by the dematerialization. They

should organize appropriate awareness programs in semi-urban and rural areas for

creating awareness about the benefits of the dematerialization particularly how

dematerialization process eliminates /reduces the bad delivery. The benefits of

dematerialization must reach to the all the stakeholders of the capital market in

general and particularly to the investors so that they will be comfortable and

confident; it in turn promotes the efficiency and growth of the capital market.

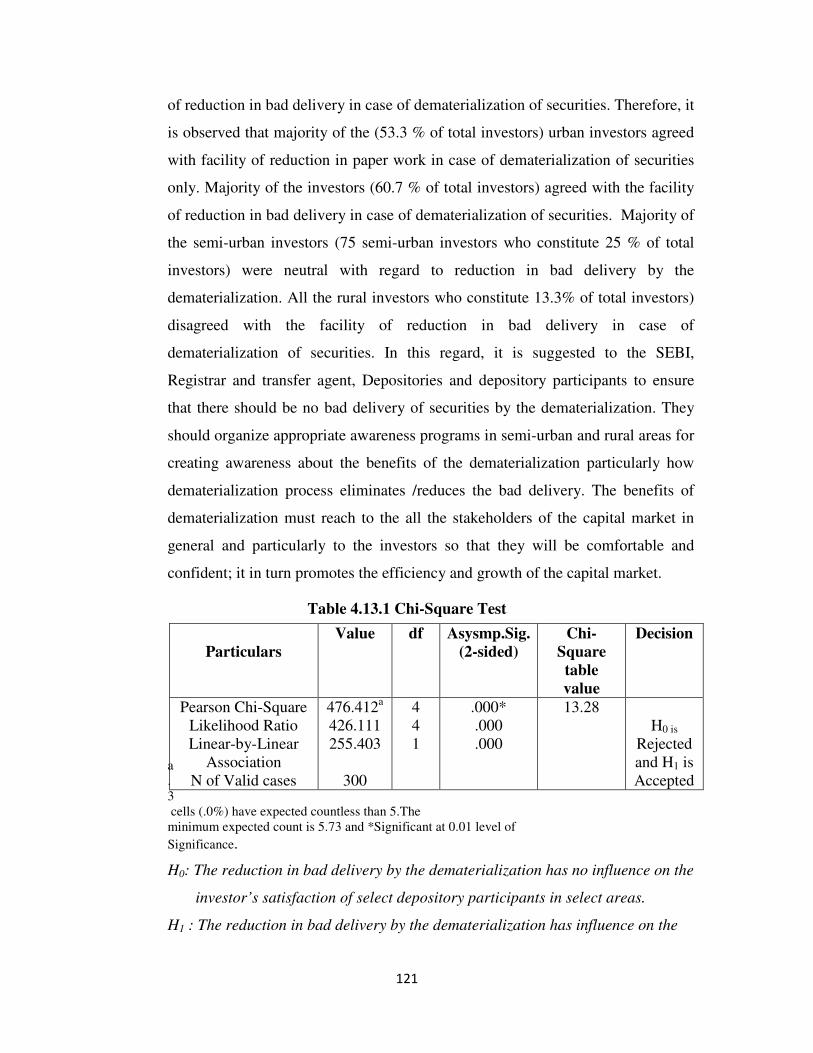

Table 4.13.1 Chi-Square Test

a

.

3

cells (.0%) have expected countless than 5.The

minimum expected count is 5.73 and *Significant at 0.01 level of

Significance.

H0: The reduction in bad delivery by the dematerialization has no influence on the

investor’s satisfaction of select depository participants in select areas.

H1 : The reduction in bad delivery by the dematerialization has influence on the

Particulars

Value df Asysmp.Sig.

(2-sided)

Chi-

Square

table

value

Decision

Pearson Chi-Square

Likelihood Ratio

Linear-by-Linear

Association

N of Valid cases

476.412a

426.111

255.403

300

4

4

1

.000*

.000

.000

13.28

H0 is

Rejected

and H1 is

Accepted

122

Investor’s satisfaction of select depository participants in select areas

From the table 4.13.1, it is clear that the chi-square calculated value of

476.4 for 4 degrees of freedom is more than the chi-square table value of 13.28

at 0.01 level of significance. The null hypothesis, Ho is rejected and hence, H1 is

accepted. Therefore it is concluded that the reduction in bad delivery of securities

by the dematerialization has influence on the investor’s satisfaction of select

depository participants in select areas. It is suggested to the SEBI, Registrar and

transfer agent, Depositories and depository participants to ensure that there should

be no bad delivery of securities by the dematerialization as reduction in bad

delivery enhances the investor’s satisfaction and confidence in the depository

system that promotes the efficiency and growth of the capital market.

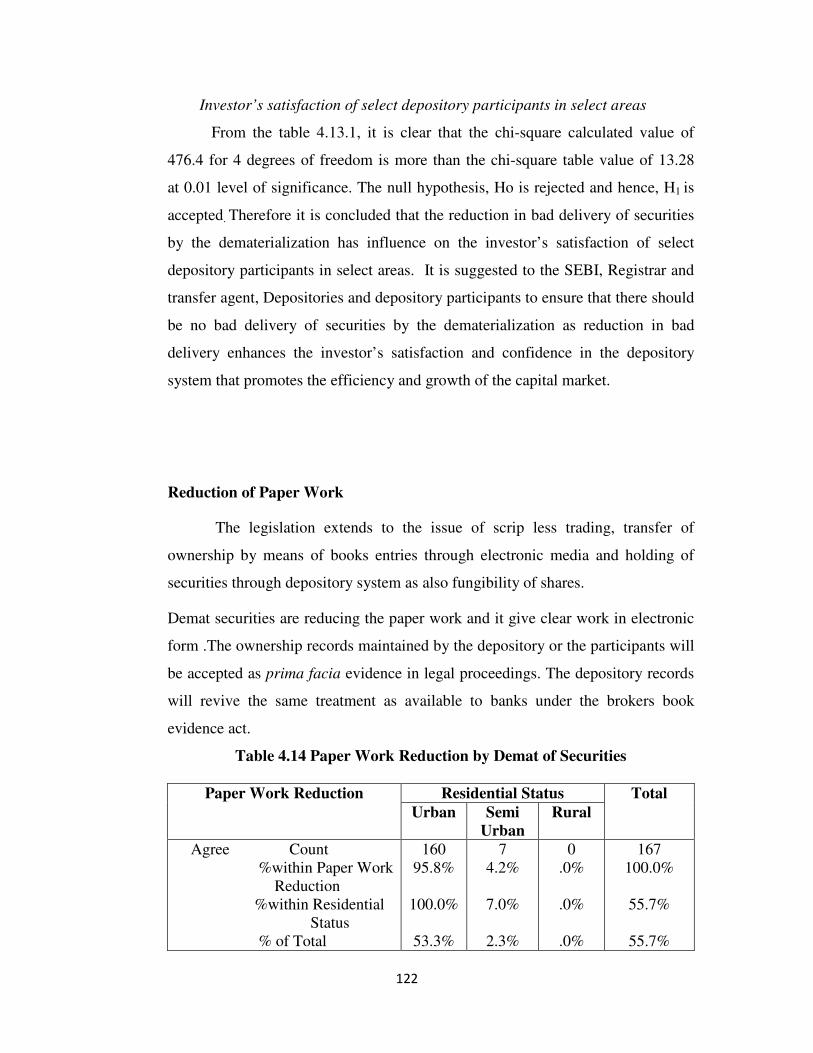

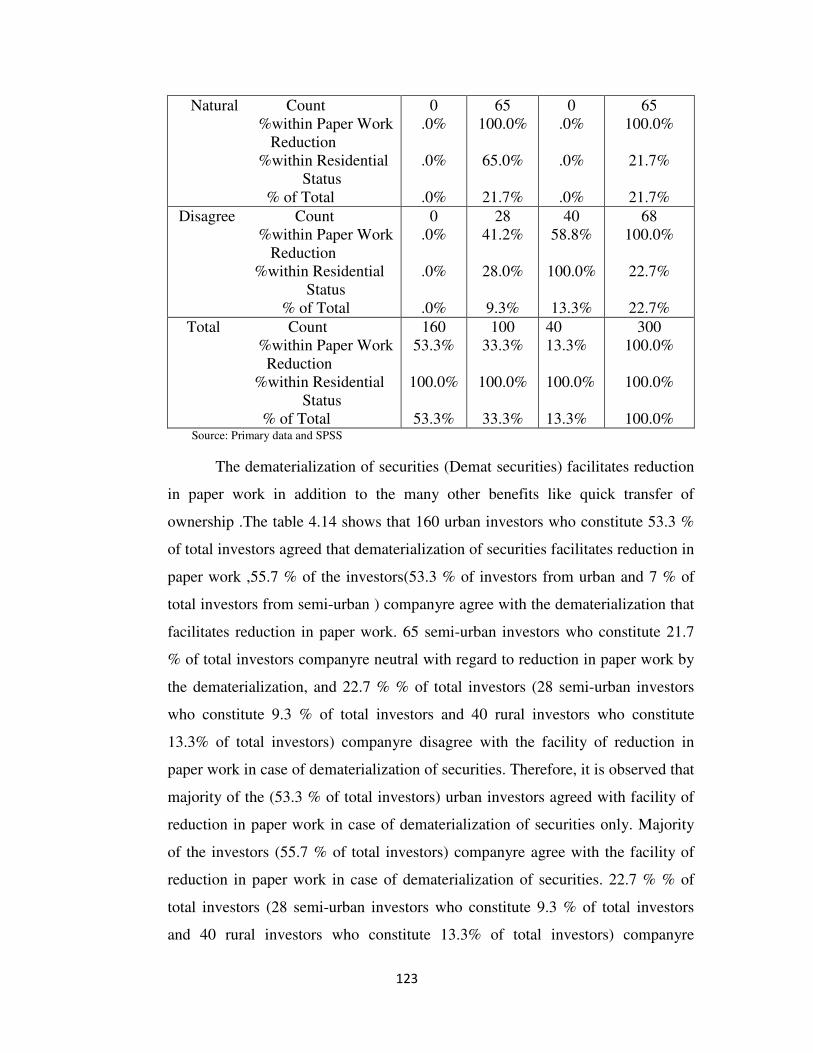

Reduction of Paper Work

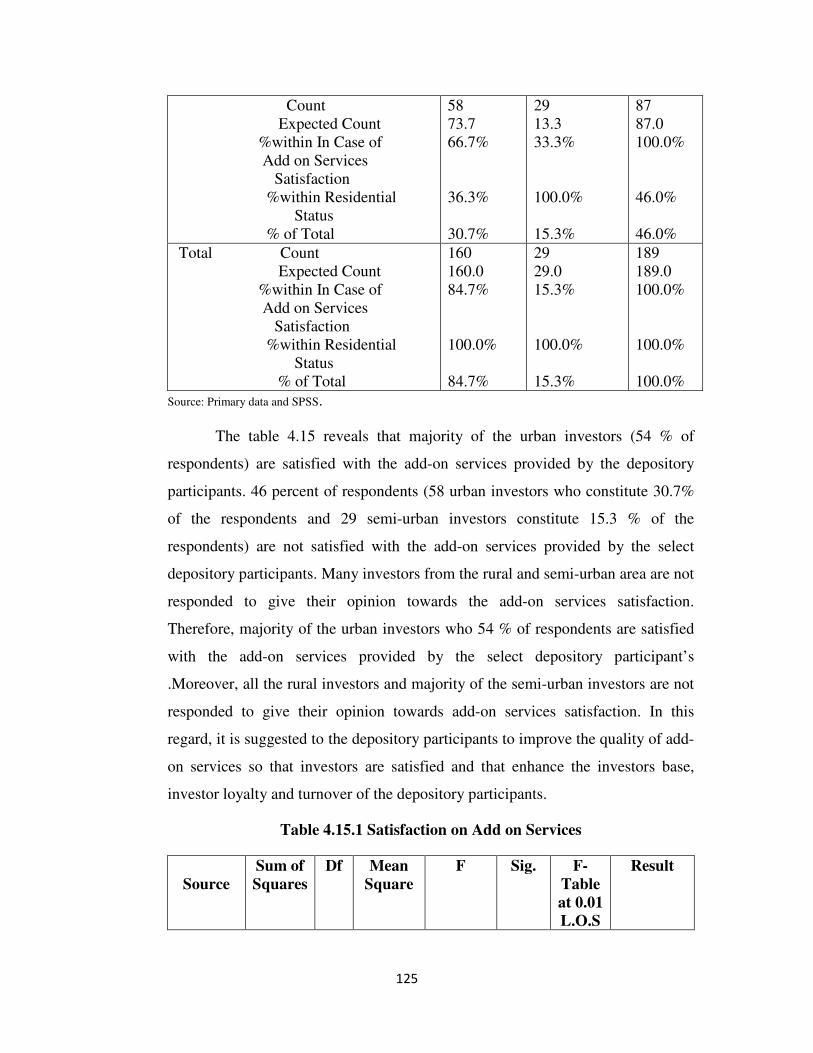

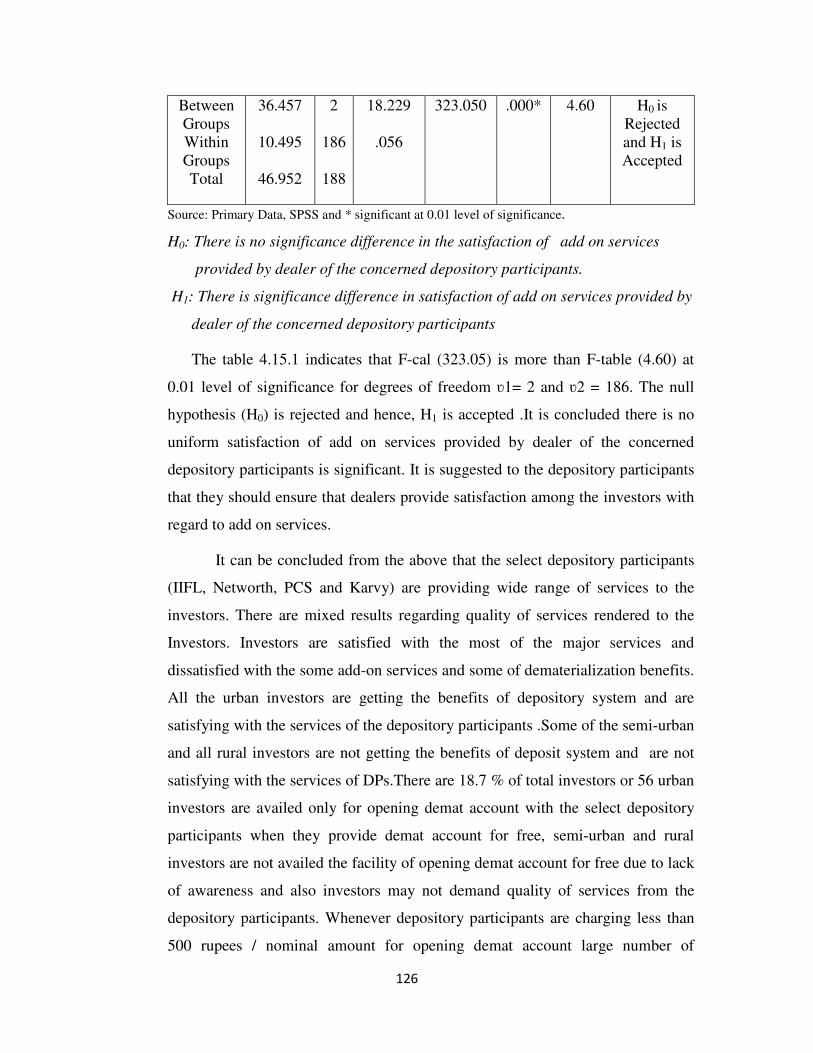

The legislation extends to the issue of scrip less trading, transfer of