Embed Size (px)

Citation preview

DOI: 10.1111/j.1475-679X.2010.00397.xJournal of Accounting Research

Vol. 00 No. 0 xxxx 2011Printed in U.S.A.

Earnings Quality Basedon Corporate Investment Decisions

F E N G L I ∗

Received 25 July 2007; accepted 20 September 2010

ABSTRACT

In this paper, I examine a new approach for measuring earnings quality, de-fined as the closeness of reported earnings to “permanent earnings,” based onfirm decisions with regard to capital and labor investments. Specifically, I mea-sure earnings quality as the contemporaneous association between changesin the levels of capital and labor investment and the change in reportedearnings. This approach follows the reasoning that (1) firms make invest-ment decisions based on the net present value (NPV) of investment projectsand (2) reported earnings with higher quality should more closely associatewith real investment decisions. I find that measures of earnings quality basedon managerial labor and capital decisions correlate positively with earningspersistence and have incremental explanatory power relative to earnings-quality measures used in the accounting literature. Furthermore, investment-based earnings-quality measures are less informative when managers tend tooverinvest.

1. Introduction

Prior research on earnings quality generally relies on one of two ap-proaches: studying the properties of accounting numbers or extracting

∗Stephen M. Ross School of Business, University of Michigan. I thank Ray Ball, Phil Berger,Ilia Dichev, Kenneth Merkley, workshop participants at the University of Chicago, and espe-cially an anonymous reviewer and Richard Leftwich (the journal editor) for their comments.

1

Copyright C©, University of Chicago on behalf of the Accounting Research Center, 2011

2 F. LI

information from stock prices.1 This paper explores a new measure of earn-ings quality by examining firm investment decisions.2 Managerial invest-ment decisions likely contain information about earnings quality becausemanagers make many decisions based on future profitability, and arguablyhave more precise and complete information about their firm’s profitabilitythan do other stakeholders. Therefore, to the extent that information asym-metry exists between managers and outsiders, the earnings quality inferredfrom managerial decisions can provide incremental information to existingempirical measures based on the information set of outside investors or onthe properties of the accounting numbers.3

In this study, I examine whether corporate investment decisions containinformation about earnings quality. In a simplified setting, managers in-vest more in projects with a higher net present value (NPV). All else be-ing equal, if a firm’s expected future earnings or permanent earnings in-crease, then it makes additional investment, because permanent earningsare equivalent to annuitized NPV (Black [1980], Beaver [1998], Ohlsonand Zhang [1998]). Hence, if a firm experiences an increase in reportedearnings and management views this earnings innovation to be permanent(i.e., the reported earnings have high “quality”), then that firm usually in-creases its investment level. However, if the innovation in reported earningsis purely transitory, then there should not be a corresponding change in theinvestment level. This reasoning suggests that earnings surprises that aremore associated with changes in corporate investment decisions are morelikely to be permanent and of higher quality than are earnings surprisesthat are less associated with such changes.

Inferring earnings quality from corporate investment decisions has lim-itations. Because of agency problems, managers have incentives to over-invest for empire building and other reasons (Stein [2003]). As a result,project profitability does not solely determine observed investment deci-sions and this reduces these decisions’ informativeness for assessing earn-ings quality. Ultimately, whether one can derive useful and reliable mea-sures of earnings quality from management investment decisions is anempirical question.

In this paper, I provide empirical evidence to answer this question byfirst examining whether corporate investment-based earnings-quality mea-sures are informative about future earnings. I measure earnings quality byexamining decisions regarding capital and labor investments, two of the

1 See, for instance, Sloan [1996], Dechow and Dichev [2002], Francis LaFond and Olsson[2005], Basu [1997], Collins Maydew and Weiss [1999], Francis and Schipper [1999], andEcker Francis and Kim [2006].

2 I define earnings quality as the closeness of reported earnings to the “permanent earn-ings” following Dechow and Schrand [2004] and use earnings persistence to operationalizethis concept.

3 Consistent with this argument, prior papers find that managerial decisions, which includedividend policy (Skinner and Soltes [2009]) and disclosure quality (Li [2008]), contain infor-mation about earnings quality.

EARNINGS QUALITY AND CORPORATE INVESTMENT 3

most important investment decisions managers make. I construct earnings-quality measures by regressing changes in the number of employees andthe amounts of capital and R&D expenditures on the change in reportedearnings, using rolling data from the last 10 years for every firm year. Theslopes from these regressions capture the sensitivity of investment to theinnovation in reported earnings and measure the information content ofthose earnings for expected future profitability as reflected in corporate in-vestment decisions. Because this regression approach requires a long timeseries of data, I also construct two other earnings-quality measures calcu-lated as the current changes in capital investment and labor investment (asproxied by the number of employees) divided by the change in reportedearnings for every firm year.

The empirical findings can be summarized as follows. First, the earnings-quality measures based on corporate investment decisions do not correlatehighly with other commonly used measures of earnings quality. This findingsuggests that the information contained in corporate investment decisionsdiffers somewhat from that reflected by stock prices and the properties ofhistorical accounting numbers. I then show that earnings-quality measuresbased on corporate investment decisions positively associate with earningspersistence. Furthermore, the predictive power of investment-based earn-ings quality for earnings persistence still holds and is economically mean-ingful even after controlling for typical measures of earnings quality suchas the absolute amount of accruals (Sloan [1996]), estimation errors inaccruals (Dechow and Dichev [2002]), the earnings–returns association,and the volatility of earnings and accruals. I also find that the investment-based earnings quality contains significant information about future earn-ings only for firms with a relatively low tendency to overinvest, measured us-ing the amount of free cash flows, the sensitivity of investment to cash flows,and the amount of excess investment based on Richardson [2006]. Finally, Ifind that the investment decisions are more informative about future earn-ings for capital-intensive firms, firms from highly unionized industries, andfirms with a high frequency of earnings increases. These additional testsfurther validate the utility of corporate investment decisions for assessingearnings quality.

Overall, the evidence indicates that there is substantial information incorporate investment decisions about earnings quality and it is incrementalto other commonly used earnings-quality measures. However, researchersor investors need to consider the severity of possible overinvestment dueto agency problems when using the investment-based earnings-quality mea-sures.

The remainder of this paper is organized as follows. Section 2 discussesthe literature on earnings quality and defines earnings-quality measuresbased on corporate investment decisions. Section 3 presents the data, sum-mary statistics of the measures, and their relation with firm characteristicsand other earnings-quality measures used in the literature. Section 4 pro-vides a discussion of the empirical results, and section 5 concludes.

4 F. LI

2. Literature and Hypotheses Development

2.1 LITERATURE ON EARNINGS QUALITY

There is an extensive literature on the earnings quality (see Dechowand Schrand [2004] for a comprehensive review). However, because of itscontext-dependent nature, there is no consensus on the underlying con-ceptual construct that “earnings quality” represents. In this paper, I followDechow and Schrand [2004] and define earnings quality as the closenessof reported earnings to the “permanent earnings” (Black [1980], Beaver[1998], and Ohlson and Zhang [1998]). I use earnings persistence to oper-ationalize this concept.

Earnings quality varies with many factors, including a firm’s businessmodel and economic situation, estimation errors (Dechow and Dichev[2002]), and earnings management (Healy and Wahlen [1999]). To cap-ture earnings quality, prior studies generally follow one of two approaches.The first approach measures earnings quality by using properties of the ob-served accounting numbers. The measures based on this approach includethe level of accruals (Sloan [1996]), the estimation error in accruals (De-chow and Dichev [2002]), and the volatility of earnings (Dichev and Tang[2009]). Because of the historical nature of the current accounting system,the information contained in accounting numbers is unlikely to be com-plete concerning future profitability. The second approach focuses on theassociation between earnings and stock returns (e.g., Basu [1997], CollinsMaydew and Weiss [1999], Francis and Schipper [1999], and Ecker Fran-cis and Kim [2006]). This approach assumes market efficiency and extractsinformation about future earnings from stock prices.

I take a different approach by emphasizing the management perspective.Managers arguably have more complete information about earnings qual-ity than do outsiders. Therefore, earnings-quality measures based on theinformation set of managers can provide better proxies for earnings qual-ity than measures that are based on historical accounting numbers or onthe information set of outside equity investors.

2.2 EARNINGS QUALITY BASED ON FIRM INVESTMENT DECISIONS

In a simplified setting, making corporate investment decisions is straight-forward: a firm invests more if the marginal NPV of the investment projectis positive. In accounting terms, the NPV of future investment is a mono-tonic function of the expected “permanent earnings,” which is essentiallythe annuitized NPV (Black [1980], Beaver [1998], and Ohlson and Zhang[1998]). Therefore, a firm invests (disinvests) if its permanent earningsincrease (decrease). Ignoring potential agency problems, the associationbetween firms’ observed investment decisions and reported earnings cap-tures the closeness of the reported earnings to the permanent earnings.Hence, the investment-earnings association provides information on thequality of the reported earnings. To the extent that managers have privateinformation that investors do not have, corporate investment decisions can

EARNINGS QUALITY AND CORPORATE INVESTMENT 5

provide informative signals about earnings quality relative to the market-based earnings-quality measures.

One point worth discussing is the parallel between a firm’s investmentdecision and the valuation of its equity by outside investors. In both cases,the involved parties (managers or investors) want to make their decisions bydoing valuations based on the expected profitability of the firm. Measuringearnings quality by using stock price information requires a maintained as-sumption of stock market efficiency, but assessing earnings quality throughmanagerial investment decisions relies on the assumption that managersmake optimal investment decisions.

I seek to contribute to the literature that explores the implications ofmanagerial decisions for earnings quality. Skinner and Soltes [2009] studythe information content of dividend decisions by firms for earnings qual-ity. Investment and dividend policies are both important managerial deci-sions and are likely to contain information about future earnings. Com-pared with dividend policy, firm labor and capital-investment decisions aresimpler in the sense that they are less likely to be influenced by signalingconsiderations. A subtle difference between this paper and Skinner andSoltes [2009] is that their emphasis is on testing the dividend informa-tion content hypothesis, which has been examined in the dividend liter-ature and has not received much support. The purpose of this paper is totest whether corporate investment decisions, despite potential agency prob-lems, can provide information about earnings quality that is incremental toother typical earnings-quality constructs. Consequently, it is important tocontrol for other measures of earnings quality.

Empirically, I examine two types of investment decisions and their asso-ciations with reported earnings: labor and capital investment. Labor andcapital are the two major factors that determine the output of a firm andthey are also the main managerial decision parameters in microeconomics.The labor- and capital-investment decisions can be affected by different eco-nomic factors. Therefore, examining both decisions can complement eachother.

2.3 OVERINVESTMENT AND INVESTMENT-BASED EARNINGS QUALITY

In this subsection, I explore the implications of firms’ nonoptimal invest-ment decision making for the investment-based earnings quality. My moti-vation is the existence of agency problems, a central theme in the corporatefinance literature with a lineage going back to Berle and Means [1932] andJensen and Meckling [1976]. Agency problems can lead to overinvestmentby managers (Stein [2003] provides a comprehensive review of the litera-ture). One consequence of the agency problem is that managers have anexcessive taste for running large firms, as opposed to simply profitable ones.This “empire building” tendency is emphasized by Williamson [1964], Don-aldson [1984], and Jensen [1986], among many other studies. Agencyproblems can also give rise to overinvestment through channels otherthan “empire building.” Bertrand and Mullainathan [2003] argue that amanagerial preference for the “quiet life”—effectively, a resistance to

6 F. LI

change—can lead to excessive continuation of negative-NPV projects. Ina somewhat similar vein, Baker [2000] builds a model in which reputa-tional concerns deter managers from discontinuing negative-NPV projects,because this would be an admission of failure.

Many empirical studies provide evidence on corporate overinvestment,including evidence from specific industries (e.g., the oil industry overin-vestment documented by Jensen [1986]) and evidence of poor acquisitions(Blanchard de Silanes and Shleifer [1994]). More recently, Richardson[2006] finds that investment decisions by firms are excessively sensitive tocurrent cash flows, which is a symptom of overinvestment.

Ceteris paribus, if a firm is more likely to overinvest, its labor- and capital-investment decisions are less likely to be a useful signal of earnings qualitybecause the investment decisions can be affected by other considerations(e.g., empire building motivations) and are not solely determined by theprofitability of the project. I therefore examine whether the informationcontent of the investment-based earnings-quality measures varies with theoverinvestment tendency cross-sectionally.

I use three empirical constructs to measure the overinvestment ten-dency. First, Richardson [2006] shows that firms with a large amount offree cash flows tend to overinvest. This finding implies that investment-based earnings-quality measures are less informative for firms with morefree cash flows. Second, a high sensitivity of investment to the free cashflows available for investment can indicate potential agency problems(Stein [2003]).4 Richardson [2006] also finds that firms that tend tooverinvest have higher investment–cash flow sensitivity. Hence, I use theinvestment–cash flow sensitivity as the second measure of the overinvest-ment tendency. Third, I rely directly on the overinvestment measure con-structed by Richardson [2006] for the cross-sectional tests. Because thismeasure directly relates to capital expenditure, I focus on the capitalinvestment-based earnings-quality measures.

To summarize, I expect that for firms that are likely to overinvest (i.e.,firms that have more free cash flows, higher sensitivity of investment tocash flows, and more excess investment), the investment-based measuresof earnings quality less strongly associate with earnings persistence and areless useful in predicting future earnings.

3. Estimation of Earnings Quality Based on Investment Decisions

3.1 EMPIRICAL ESTIMATION OF EARNINGS QUALITY

I obtain my sample from the Compustat annual industrial and researchfiles between 1952 and 2004. For every firm i in year T , I estimate the

4 The corporate finance literature also argues that firms with higher investment–cash flowsensitivity tend to have more severe financing constraints, in addition to overinvestment prob-lems. Nevertheless, the financial constraint interpretation of the investment–cash flow sensi-tivity also leads to a prediction of suboptimal investment for firms with higher investment–cashflow sensitivity.

EARNINGS QUALITY AND CORPORATE INVESTMENT 7

following two regressions using the data from year T − 9 to T :

(NEMPi,t − NEMPi,t−1)/TAi,t−1 = αL,iT + βL,iT (Ei,t − Ei,t−1)/TAi,t−1 + εL,i t

(1)and

(CAPX i,t + RNDi,t − CAPX i,t−1 − RNDi,t−1)/TAi,t−1

= αC,iT + βC,iT (Ei,t − Ei,t−1)/TAi,t−1 + εC,i t , (2)where T − 9 ≤ t ≤ T , NEMP is the number of employees at the end of a fis-cal year (#29 of the Compustat annual files), CAPX is the amount of capitalexpenditure for the year (#128), RND is the amount of R&D expenditurefor the year (#46), E is the operating earnings (#178) with some possibleadjustment (details in the next paragraph), and TA is the book value ofassets at the end of the fiscal year (#6).

Similar to prior studies (e.g., Richardson [2006]), I include R&D expen-diture in the capital investment together with capital expenditure. My mo-tivation is the fact that, even though R&D is fully expensed under currentU.S. generally accepted accounting principles (U.S. GAAP), prior studiesshow that the market views it more like an investment (Lev and Sougiannis[1996]). There is also a potential endogeneity problem in the estimationprocedure—an increase in capital and R&D expenditures in a given yearreduces the reported earnings because of additional expensing. This reduc-tion leads to a mechanical negative relation between investment and earn-ings. To mitigate this problem, I adjust the reported earnings by addingback the current R&D expense and the depreciation expense due to thenew capital expenditure. Specifically, for firm i in year t , Eit is calculated as

Eit = #178 + RNDit + CAPX it/(PPEit/DEPit ), (3)

where PPE is the average of the beginning and end values of the grossamount of property, plant, and equipment (#7) and DEP is the depreci-ation expense (#14). This adjustment assumes that the new assets, due tocurrent capital expenditure, are depreciated using the same rate as existingassets-in-place with a straight-line depreciation method.

Item #29 of Compustat represents the number of company workers (in-cluding all employees of consolidated domestic and foreign subsidiaries, allpart-time and seasonal employees, full-time equivalent employees, and offi-cers, and excluding consultants, contract workers, directors, and employeesof unconsolidated subsidiaries) as reported to shareholders.5 The amountof salary expense is a better variable to capture the amount of investment inlabor than the number of employees, especially when the scaling variableis the book value of assets. However, only about 20% of firm years in Com-pustat report a nonmissing labor expense (#42), but about 95% of the firm

5 This figure is reported by some firms as an average number of employees and by othersas the number of employees at year end. If both are given, the year-end figure is used. Thereis no reason to believe that this difference introduces a systematic bias to our estimates.

8 F. LI

years have the number of employees (#29). Using the number of employ-ees therefore can increase the number of observations dramatically. Thenumber of employees scaled by the book value of assets captures the laborintensity (i.e., the number of employees per dollar of assets). To the ex-tent that the salary per employee remains relatively stable over time for thesame firm, scaling the number of employees by total assets is not a problem.In unreported analysis, I also redo all the tests by replacing the dependentvariable in equation (1) with log(NEMPt/NEMPt−1) and the results are sim-ilar.

I use a firm-level regression because managerial decisions most natu-rally apply at the firm level. I expect that a firm-level specification is bet-ter than cross-sectional specifications because the regression coefficientsare likely to differ across firms because managers have firm-specific infor-mation about future profitability. The βL and βC are the “response coef-ficients” of corporate investment level to current reported earnings. For afirm to have βL and βC estimated in year t, it needs to have nonmissing datain the 10 years from t − 9 to t to estimate equations (1) and (2).

Because this regression approach uses 10 years of rolling data and there-fore shrinks the sample size greatly, I also construct two other measuresof earnings quality based on investment decisions for firm i in year T asfollows:

γL,iT = (NEMPiT − NEMPi,T−1)/(EiT − Ei,T−1) (4)

and

γC,iT = (CAPX iT + RNDiT − CAPX i,T−1 − RNDi,T−1)/(EiT − Ei,T−1), (5)

where all the definitions of the variables are the same as in equations (1)and (2). Thus, γ L and γ C capture the response of investment to the changein earnings in a given year. Compared with βL and βC , the advantage ofthese measures is that they require only two years of data, but the cost is thatthey might not measure the association between earnings and investmentprecisely and that it is more difficult to interpret the measures when thechange in earnings is negative.6

Also, I construct two measures that combine the information content ofboth the capital and labor investment decisions. To smooth out any possiblenonlinear effect of the variables, I average the measures based on capitaland labor decisions using their decile ranks

EQ 1 = (Decile(βL) + (Decile(βC ))/2 (6)

and

EQ 2 = (Decile(γL) + (Decile(γC ))/2, (7)

where Decile(·) is the decile rank of a variable in a year.

6 This is especially true during recession years.

EARNINGS QUALITY AND CORPORATE INVESTMENT 9

T A B L E 1Summary Statistics

Standard 25th 50th 75thVariable N Mean Deviation Pctl Pctl Pctl p-ValueβC 34,594 0.187 0.561 −0.080 0.142 0.426 0.00RSQC 34,594 0.166 0.185 0.022 0.096 0.252 –βL 34,594 0.035 0.067 0.000 0.013 0.048 0.00RSQL 34,594 0.223 0.223 0.035 0.147 0.355 –γ C 83,848 0.209 1.584 −0.442 0.162 0.982 0.00γ L 83,848 0.050 0.533 −0.009 0.009 0.078 0.00DD 34,594 0.024 0.016 0.012 0.020 0.031 –ABSACC 83,848 0.060 0.060 0.020 0.043 0.080 –VOL CFO 34,594 0.060 0.032 0.036 0.053 0.077 –VOL ACC 34,594 0.052 0.030 0.029 0.045 0.067 –VOL EARN 34,594 0.044 0.029 0.023 0.038 0.058 –βR 28,948 3.234 5.815 0.328 1.678 4.391 0.00SALGRW 34,594 0.088 0.064 0.048 0.085 0.125 –MTB 74,348 1.506 1.422 0.960 1.183 1.640 –OPCYC 77,100 0.051 0.549 0.014 0.020 0.036 –DIV 83,628 0.702 0.458 0 1 1 –

This table presents the summary statistics of the investment-based earnings-quality measures and othervariables. The p-value is for the test that examines whether the variable is significantly different from zero.

The βC is estimated for every firm year as the slope coefficient from the regression of change in capitaland R&D expenditures (scaled by lagged book value of assets) on the change in reported earnings (adjustedfor the impact of current capital and R&D expenditures and scaled by lagged book value of assets) usingdata from the last 10 years. The RSQ C is the adjusted R -squared from the regression. The βL is estimatedfor every firm year as the slope coefficient from the regression of change in the number of employees(scaled by lagged book value of assets) on the change in reported earnings (scaled by lagged book valueof assets) using data from the last 10 years. The RSQL is the adjusted R -squared from the regression. Fora firm year to have βC and βL , it must have nonmissing data for the last 10 years. The γ C is the changein capital and R&D expenditures divided by the change in reported earnings. The γ L is the change in thenumber of employees divided by the change in reported earnings. The DD is estimated for every firm yearas the standard deviation of the Dechow and Dichev [2002] residuals from the regression of accruals onlagged CFO (operating cash flows), current CFO, and next year’s CFO using the last 10 years of data. TheABSACC is the absolute amount of accruals scaled by lagged book value of assets. The VOL CFO, VOL ACC ,and VOL EARN are the volatility of operating cash flows, accruals, and earnings (all scaled by lagged bookvalue of assets) calculated using data from the last 10 years. The βR is estimated for every firm year as theslope coefficients from the regression of stock returns on the change in reported earnings (scaled by laggedbook value of assets) using data from the last 10 years. The SALGRW is the average sales growth in the last10 years. The MTB is the market value of a firm’s asset divided by the book value of the assets. The OPCYC isthe operating cycle of a firm, calculated as 360/(Sales Average AR) +360/((Cost of Goods Sold)/(AverageInventory)). The DIV is a dummy variable that equals 1 if a firm pays dividend and 0 otherwise.

To summarize, βL, βC , and E Q 1 (i.e., the decile rank average of βL

and βC ) capture the earnings quality inferred from labor- and capital-investment decisions by using a regression approach; γ L, γ C , and E Q 2 (i.e.,the decile rank average of γ L and γ C ) represent the response of corporateinvestments to earnings innovation in the current year.

3.2 SUMMARY STATISTICS

Table 1 presents the summary statistics of the investment-based earnings-quality measures and other variables needed in later analysis. Every year,if a firm has nonmissing data for the past 10 years, its βL is the estimationof the slope coefficient in the regression of the change in employment onthe change in earnings following equation (1), and βC is the estimation of

10 F. LI

the slope coefficient in the regression of the change in capital investmenton the change in earnings using equation (2). Because of the 10-year datarequirement, the sample size is relatively small (34,594 firm years or about800 firms per year).7

As predicted, current changes in reported earnings positively relate tothe contemporaneous changes in the level of labor and capital. As indi-cated in table 1, the mean coefficient on earnings change in the labor re-gression (βL) is 0.035 and the median is 0.013. The mean and median ofβC are 0.187 and 0.142, respectively. The RSQL and RSQC are the adjustedR -squared from the regressions that have a mean of 0.223 and 0.166, re-spectively, and indicate that earnings changes can explain 17–22% of thevariations in the changes of labor and capital investment. Based on thecross-sectional distribution of the coefficients, βL and βC are both statisti-cally significant with p-values of 0.00. The variations in the two measures aresubstantial: the standard deviations of βL and βC are 0.067 and 0.561 andtheir inter-quartile ranges are 0.048 and 0.506, respectively.

Table 1 also presents the summary statistics of γ L and γ C , the estimatesof earnings quality defined in equations (4) and (5). Because the estimatesonly require two years of data, the sample size is much bigger—83,848 firmyears (or about 2,000 firms per year). The γ L and γ C have a mean of 0.050and 0.209, respectively and both have substantial variations with standarddeviations of 0.533 and 1.584.

The table also presents the summary statistics of other commonly usedmeasures of earnings quality. The DD is the standard deviation of accrualsthat cannot be explained by cash flows as defined in Dechow and Dichev[2002], and is calculated using data from the last 10 years. The βR is theearnings–returns association calculated as the slope coefficient in the re-gression of stock returns on the change in reported earnings using datafrom the last 10 years. The ABSACC is the absolute amount of accrualsscaled by lagged book value of assets. The V OL CF O, V OL ACC , andV OL E ARN are the volatilities of cash flows, accruals, and earnings (allscaled by lagged book value of assets) calculated using data from the last 10years.

3.3 INVESTMENT-BASED EARNINGS QUALITY AND OTHER MEASURESOF EARNINGS QUALITY

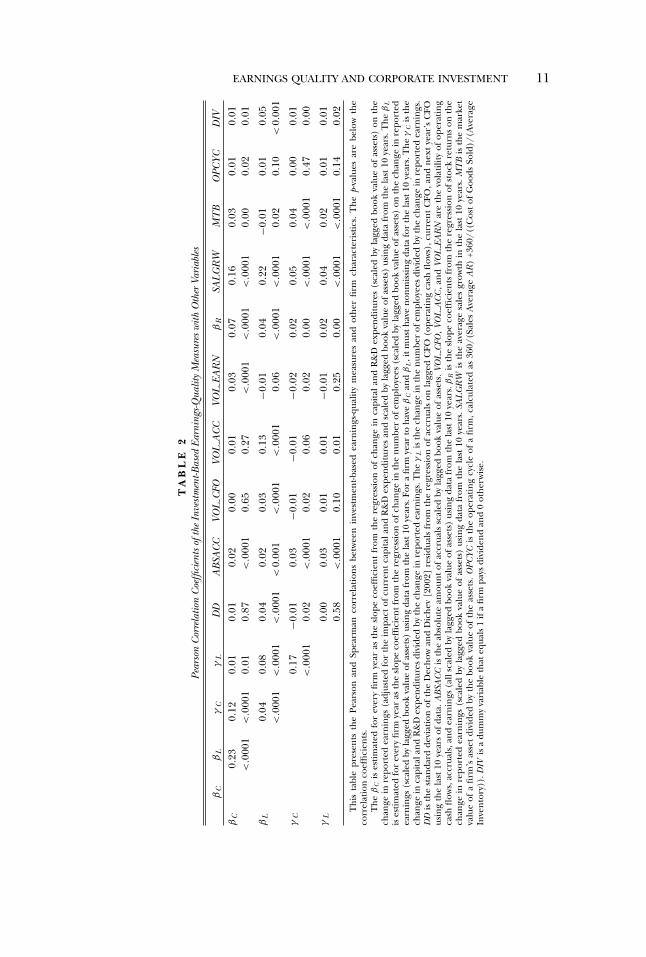

In this subsection, I examine the associations between the earnings-quality measures developed in this paper (i.e., βL, βC , γ L, and γ C ) and firmcharacteristics and other earnings-quality measures, such as the Dechowand Dichev [2002] measure, absolute value of accruals, volatility of earn-ings, earnings–returns association, growth, market-to-book ratio, and firmoperating cycle. Table 2 presents the Pearson correlation coefficients be-tween the investment-based earnings-quality measures and these variables.

7 To remove the influence of extreme observations, all variables are winsorized at the 1%and 99% levels.

EARNINGS QUALITY AND CORPORATE INVESTMENT 11

TA

BL

E2

Pear

son

Cor

rela

tion

Coe

ffici

ents

ofth

eIn

vest

men

t-Bas

edEa

rnin

gs-Q

ualit

yM

easu

res

with

Oth

erVa

riab

les

βC

βL

γC

γL

DD

AB

SAC

CVO

LC

FOVO

LA

CC

VOL

EAR

Nβ

RSA

LG

RW

MT

BO

PCYC

DIV

βC

0.23

0.12

0.01

0.01

0.02

0.00

0.01

0.03

0.07

0.16

0.03

0.01

0.01

<.0

001

<.0

001

0.01

0.87

<.0

001

0.65

0.27

<.0

001

<.0

001

<.0

001

0.00

0.02

0.01

βL

0.04

0.08

0.04

0.02

0.03

0.13

−0.0

10.

040.

22−0

.01

0.01

0.05

<.0

001

<.0

001

<.0

001

<0.

001

<.0

001

<.0

001

0.06

<.0

001

<.0

001

0.02

0.10

<0.

001

γC

0.17

−0.0

10.

03−0

.01

−0.0

1−0

.02

0.02

0.05

0.04

0.00

0.01

<.0

001

0.02

<.0

001

0.02

0.06

0.02

0.00

<.0

001

<.0

001

0.47

0.00

γL

0.00

0.03

0.01

0.01

−0.0

10.

020.

040.

020.

010.

010.

58<

.000

10.

100.

010.

250.

00<

.000

1<

.000

10.

140.

02T

his

tabl

epr

esen

tsth

ePe

arso

nan

dSp

earm

anco

rrel

atio

nsbe

twee

nin

vest

men

t-bas

edea

rnin

gs-q

ualit

ym

easu

res

and

othe

rfir

mch

arac

teri

stic

s.T

hep-

valu

esar

ebe

low

the

corr

elat

ion

coef

ficie

nts.

The

βC

ises

timat

edfo

rev

ery

firm

year

asth

esl

ope

coef

ficie

ntfr

omth

ere

gres

sion

ofch

ange

inca

pita

land

R&

Dex

pend

iture

s(s

cale

dby

lagg

edbo

okva

lue

ofas

sets

)on

the

chan

gein

repo

rted

earn

ings

(adj

uste

dfo

rth

eim

pact

ofcu

rren

tcap

itala

ndR

&D

expe

nditu

res

and

scal

edby

lagg

edbo

okva

lue

ofas

sets

)us

ing

data

from

the

last

10ye

ars.

The

βL

ises

timat

edfo

rev

ery

firm

year

asth

esl

ope

coef

ficie

ntfr

omth

ere

gres

sion

ofch

ange

inth

enu

mbe

rof

empl

oyee

s(s

cale

dby

lagg

edbo

okva

lue

ofas

sets

)on

the

chan

gein

repo

rted

earn

ings

(sca

led

byla

gged

book

valu

eof

asse

ts)

usin

gda

tafr

omth

ela

st10

year

s.Fo

ra

firm

year

toha

veβ

Can

dβ

L,i

tmus

thav

eno

nmis

sing

data

for

the

last

10ye

ars.

The

γC

isth

ech

ange

inca

pita

land

R&

Dex

pend

iture

sdi

vide

dby

the

chan

gein

repo

rted

earn

ings

.The

γL

isth

ech

ange

inth

enu

mbe

rof

empl

oyee

sdi

vide

dby

the

chan

gein

repo

rted

earn

ings

.D

Dis

the

stan

dard

devi

atio

nof

the

Dec

how

and

Dic

hev

[200

2]re

sidu

als

from

the

regr

essi

onof

accr

uals

onla

gged

CFO

(ope

ratin

gca

shfl

ows)

,cur

rent

CFO

,and

next

year

’sC

FOus

ing

the

last

10ye

ars

ofda

ta.A

BSA

CC

isth

eab

solu

team

ount

ofac

crua

lssc

aled

byla

gged

book

valu

eof

asse

ts.V

OL

CFO

,VO

LA

CC

,and

VOL

EAR

Nar

eth

evo

latil

ityof

oper

atin

gca

shfl

ows,

accr

uals

,and

earn

ings

(all

scal

edby

lagg

edbo

okva

lue

ofas

sets

)us

ing

data

from

the

last

10ye

ars.

βR

isth

esl

ope

coef

ficie

nts

from

the

regr

essi

onof

stoc

kre

turn

son

the

chan

gein

repo

rted

earn

ings

(sca

led

byla

gged

book

valu

eof

asse

ts)

usin

gda

tafr

omth

ela

st10

year

s.SA

LG

RW

isth

eav

erag

esa

les

grow

thin

the

last

10ye

ars.

MT

Bis

the

mar

ket

valu

eof

afir

m’s

asse

tdi

vide

dby

the

book

valu

eof

the

asse

ts.O

PCYC

isth

eop

erat

ing

cycl

eof

afir

m,c

alcu

late

das

360/

(Sal

esA

vera

geA

R)

+360

/((C

ost

ofG

oods

Sold

)/(A

vera

geIn

vent

ory)

).D

IVis

adu

mm

yva

riab

leth

ateq

uals

1if

afir

mpa

ysdi

vide

ndan

d0

othe

rwis

e.

12 F. LI

Table 2 shows a correlation between βL and βC with a Pearson correlationcoefficient of 0.23 (p-value < 0.001); similarly, the Pearson correlation co-efficient between γ L and γ C is 0.17 (p-value< 0.001). This finding suggeststhat labor- and capital-investment decisions capture common informationin earnings.

The evidence in table 2 also shows that the earnings-quality measuresdeveloped from corporate investment decisions do not have a strong cor-relation with other common measures of earnings quality. For instance, DD(the standard deviation of accruals that cannot be explained by CF Ot−1,CF Ot , and CF Ot+1 based on Dechow and Dichev [2002]) has a Pearsoncorrelation of 0.01 (p-value = 0.87) with βC , 0.04 (p-value < 0.001) with βL,−0.01 (p-value = 0.02) with γ C , and 0.00 (p-value = 0.58) with γ L. Theseresults show that DD captures a different set of information from that ofthe investment-based earnings-quality measures. Sales growth is the variablewith the largest correlation with the investment-based earnings-quality mea-sures: firms with a high sales growth rate tend to have stronger associationsbetween earnings and investment. For instance, βL has a Pearson correla-tion of 0.22 (p< 0.001) with the 10-year sales growth rate (SALGRW ).

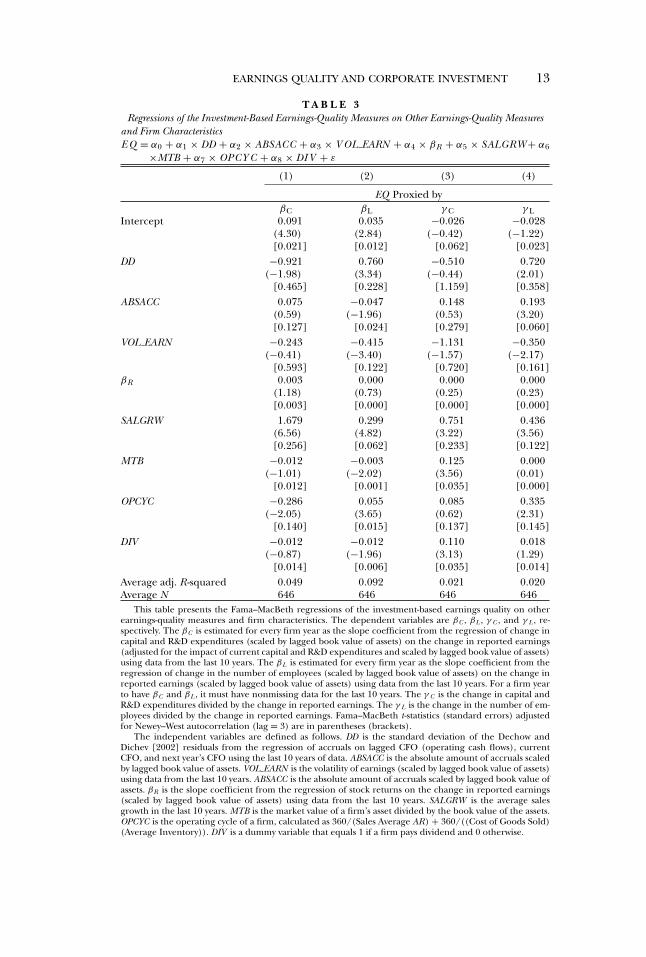

In table 3, I examine the relation between βC , βL, γ C , and γ L and otherearnings-quality measures and firm characteristics using a Fama–MacBethregression approach. Every year, I regress the investment-based earnings-quality measures on other variables, and the table reports the means andt-statistics based on the time-series distribution of the coefficients. Sincethe data that estimates βC and βL is the rolling data from the last 10 years,there are serial correlations in the error terms when they are the dependentvariables. To mitigate this concern, I adjust the Fama–MacBeth t-statisticsfor serial correlations using the Newey–West procedure with a lag of three.8

Consistent with the univariate correlations reported in table 2, thereseems to be no robust relation between the investment-based earnings-quality measures and many of the commonly used earnings-quality vari-ables. For instance, DD, the standard deviation of the accruals residualsbased on Dechow and Dichev [2002], is negatively associated with βC (co-efficient on DD = −0.921 and t = −1.98), but is positively related to βL (co-efficient 0.760 and t = 3.34). As another example, although the volatility ofearnings is consistently negatively associated with the earnings-quality mea-sures based on corporate investment, it is statistically significant only forβL and γ L. The only robust and significant factor that explains βC , βL, γ C ,and γ L is SALGRW , the 10-year sales growth rate, which is positively andsignificantly associated with all four variables.

Overall, the correlations between the investment-based earnings-qualitymeasures and other typical measures of earnings quality are modest, whichsuggests that corporate investment decisions capture information about

8 Newey and West [1994] suggest that the optimal length for the Newey–West adjustment isT 1/4, where T is the time-series length of the data.

EARNINGS QUALITY AND CORPORATE INVESTMENT 13

T A B L E 3Regressions of the Investment-Based Earnings-Quality Measures on Other Earnings-Quality Measures

and Firm CharacteristicsE Q = α0 + α1 × DD + α2 × ABSACC + α3 × V OL EARN + α4 × βR + α5 × SALGRW + α6

×MTB + α7 × OPCY C + α8 × DI V + ε

(1) (2) (3) (4)

EQ Proxied byβC βL γ C γ L

Intercept 0.091 0.035 −0.026 −0.028(4.30) (2.84) (−0.42) (−1.22)[0.021] [0.012] [0.062] [0.023]

DD −0.921 0.760 −0.510 0.720(−1.98) (3.34) (−0.44) (2.01)

[0.465] [0.228] [1.159] [0.358]ABSACC 0.075 −0.047 0.148 0.193

(0.59) (−1.96) (0.53) (3.20)[0.127] [0.024] [0.279] [0.060]

VOL EARN −0.243 −0.415 −1.131 −0.350(−0.41) (−3.40) (−1.57) (−2.17)

[0.593] [0.122] [0.720] [0.161]βR 0.003 0.000 0.000 0.000

(1.18) (0.73) (0.25) (0.23)[0.003] [0.000] [0.000] [0.000]

SALGRW 1.679 0.299 0.751 0.436(6.56) (4.82) (3.22) (3.56)[0.256] [0.062] [0.233] [0.122]

MTB −0.012 −0.003 0.125 0.000(−1.01) (−2.02) (3.56) (0.01)

[0.012] [0.001] [0.035] [0.000]OPCYC −0.286 0.055 0.085 0.335

(−2.05) (3.65) (0.62) (2.31)[0.140] [0.015] [0.137] [0.145]

DIV −0.012 −0.012 0.110 0.018(−0.87) (−1.96) (3.13) (1.29)

[0.014] [0.006] [0.035] [0.014]Average adj. R -squared 0.049 0.092 0.021 0.020Average N 646 646 646 646

This table presents the Fama–MacBeth regressions of the investment-based earnings quality on otherearnings-quality measures and firm characteristics. The dependent variables are βC , βL , γ C , and γ L , re-spectively. The βC is estimated for every firm year as the slope coefficient from the regression of change incapital and R&D expenditures (scaled by lagged book value of assets) on the change in reported earnings(adjusted for the impact of current capital and R&D expenditures and scaled by lagged book value of assets)using data from the last 10 years. The βL is estimated for every firm year as the slope coefficient from theregression of change in the number of employees (scaled by lagged book value of assets) on the change inreported earnings (scaled by lagged book value of assets) using data from the last 10 years. For a firm yearto have βC and βL , it must have nonmissing data for the last 10 years. The γ C is the change in capital andR&D expenditures divided by the change in reported earnings. The γ L is the change in the number of em-ployees divided by the change in reported earnings. Fama–MacBeth t-statistics (standard errors) adjustedfor Newey–West autocorrelation (lag = 3) are in parentheses (brackets).

The independent variables are defined as follows. DD is the standard deviation of the Dechow andDichev [2002] residuals from the regression of accruals on lagged CFO (operating cash flows), currentCFO, and next year’s CFO using the last 10 years of data. ABSACC is the absolute amount of accruals scaledby lagged book value of assets. VOL EARN is the volatility of earnings (scaled by lagged book value of assets)using data from the last 10 years. ABSACC is the absolute amount of accruals scaled by lagged book value ofassets. βR is the slope coefficient from the regression of stock returns on the change in reported earnings(scaled by lagged book value of assets) using data from the last 10 years. SALGRW is the average salesgrowth in the last 10 years. MTB is the market value of a firm’s asset divided by the book value of the assets.OPCYC is the operating cycle of a firm, calculated as 360/(Sales Average AR) + 360/((Cost of Goods Sold)(Average Inventory)). DIV is a dummy variable that equals 1 if a firm pays dividend and 0 otherwise.

14 F. LI

future earnings that is somewhat different from that reflected in the othervariables.

4. Empirical Results

4.1 INVESTMENT-BASED EARNINGS QUALITY AND EARNINGS PERSISTENCE

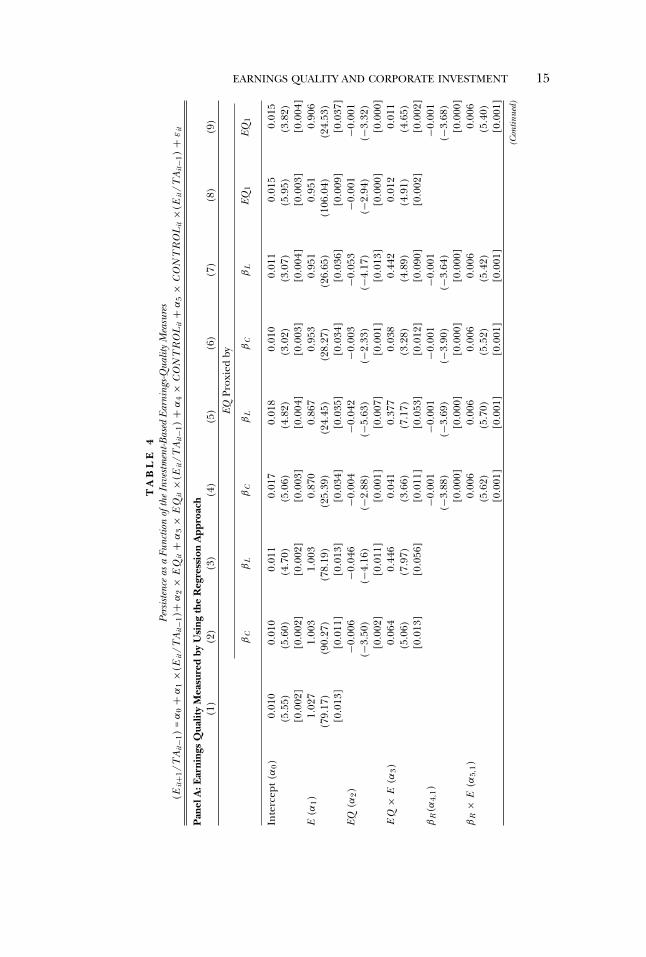

In this subsection, I present evidence that the earnings-quality measuresbased on firm labor and capital changes are informative about earningspersistence. To test this prediction, I estimate the following regression:

(Ei,t+1/TAi,t−1) = α0 + α1(Eit/TAi,t−1) + α2EQ it + α3EQ it(Eit/TAi,t−1)

+α4CONTROLit + α5CONTROLit(Eit/TAi,t−1) + εit ,

(8)

where Eit is earnings for firm i in year t , TAit is total assets for firm i inyear t, and E Qit is the earnings-quality measure of firm i in year t. If βL, βC ,or E Q 1 (the decile rank average of βL and βC ) proxies for E Qit , then theearnings-quality estimation requires data for firm i from year t − 9 to t; ifγ L, γ C , or E Q 2 (the decile rank average of γ L and γ C ) proxies for it, thenthe calculation uses data from year t and t − 1. In this regression, α2 mea-sures the persistence of earnings. Under the hypothesis that investment de-cisions are informative about the quality of reported earnings, I expect thecoefficient on current earnings to be larger for firms with a higher associa-tion between investment and earnings, which indicates that their earningsare more persistent (α3 > 0).

To assess the incremental information content of the investment-basedearnings-quality measures, the regression includes typical measures of earn-ings quality and their interactions with Eit . In the reported results, I use thefollowing control variables: earnings–returns association (βR), the absoluteamount of accruals in current earnings (ABSACC), the Dechow and Dichev[2002] measure of accruals quality (DD), and a dummy variable for currentdividend (DIV ) that equals one if a firm issues dividend and zero otherwise.In untabulated results, I further control for the volatility of earnings, thevolatility of cash flows, the market-to-book ratio, and the e-loadings mea-sure proposed by Ecker, Francis, and Kim [2006], because these variablesare also used as measures of earnings quality in the literature. These untab-ulated results remain qualitatively similar to the reported results.9 All of theregressions use the Fama and MacBeth [1973] approach with Newey–Westadjustment to standard errors.

Panel A of table 4 reports the results of estimating equation (8) with EQproxied by βL, βC , and their decile rank average (E Q 1). For my sample, the

9 I do not report the results with all the control variables because many of the variables arehighly correlated with each other. For instance, accruals volatility is highly correlated with theDechow and Dichev [2002] measure; including both variables in the regression makes it hardto interpret the coefficients.

EARNINGS QUALITY AND CORPORATE INVESTMENT 15

TA

BL

E4

Pers

iste

nce

asa

Func

tion

ofth

eIn

vest

men

t-Bas

edEa

rnin

gs-Q

ualit

yM

easu

res

(Eit+1

/TA

it−1

)=

α0

+α

1×(

Eit

/TA

it−1

)+α

2×

EQ

it+

α3

×E

Qit

×(E

it/T

Ait−1

)+

α4

×C

ON

TR

OL

it+

α5

×C

ON

TR

OL

it×(

Eit

/TA

it−1

)+

εit

Pan

elA

:Ear

ning

sQ

ualit

yM

easu

red

byU

sing

the

Reg

ress

ion

App

roac

h(1

)(2

)(3

)(4

)(5

)(6

)(7

)(8

)(9

)EQ

Prox

ied

by

βC

βL

βC

βL

βC

βL

EQ1

EQ1

Inte

rcep

t(α

0)0.

010

0.01

00.

011

0.01

70.

018

0.01

00.

011

0.01

50.

015

(5.5

5)(5

.60)

(4.7

0)(5

.06)

(4.8

2)(3

.02)

(3.0

7)(5

.95)

(3.8

2)[0

.002

][0

.002

][0

.002

][0

.003

][0

.004

][0

.003

][0

.004

][0

.003

][0

.004

]E

(α1)

1.02

71.

003

1.00

30.

870

0.86

70.

953

0.95

10.

951

0.90

6(7

9.17

)(9

0.27

)(7

8.19

)(2

5.39

)(2

4.45

)(2

8.27

)(2

6.65

)(1

06.0

4)(2

4.53

)[0

.013

][0

.011

][0

.013

][0

.034

][0

.035

][0

.034

][0

.036

][0

.009

][0

.037

]EQ

(α2)

−0.0

06−0

.046

−0.0

04−0

.042

−0.0

03−0

.053

−0.0

01−0

.001

(−3.

50)

(−4.

16)

(−2.

88)

(−5.

63)

(−2.

33)

(−4.

17)

(−2.

94)

(−3.

32)

[0.0

02]

[0.0

11]

[0.0

01]

[0.0

07]

[0.0

01]

[0.0

13]

[0.0

00]

[0.0

00]

EQ

×E

(α3)

0.06

40.

446

0.04

10.

377

0.03

80.

442

0.01

20.

011

(5.0

6)(7

.97)

(3.6

6)(7

.17)

(3.2

8)(4

.89)

(4.9

1)(4

.65)

[0.0

13]

[0.0

56]

[0.0

11]

[0.0

53]

[0.0

12]

[0.0

90]

[0.0

02]

[0.0

02]

βR

(α4,

1)−0

.001

−0.0

01−0

.001

−0.0

01−0

.001

(−3.

88)

(−3.

69)

(−3.

90)

(−3.

64)

(−3.

68)

[0.0

00]

[0.0

00]

[0.0

00]

[0.0

00]

[0.0

00]

βR

×E

(α5,

1)0.

006

0.00

60.

006

0.00

60.

006

(5.6

2)(5

.70)

(5.5

2)(5

.42)

(5.4

0)[0

.001

][0

.001

][0

.001

][0

.001

][0

.001

](C

ontin

ued)

16 F. LI

TA

BL

E4

—C

ontin

ued

Pan

elA

:Ear

ning

sQ

ualit

yM

easu

red

byU

sing

the

Reg

ress

ion

App

roac

h(1

)(2

)(3

)(4

)(5

)(6

)(7

)(8

)(9

)EQ

Prox

ied

by

βC

βL

βC

βL

βC

βL

EQ1

EQ1

AB

SAC

C(α

4,2)

0.07

40.

074

(3.0

2)(3

.02)

[0.0

25]

[0.0

25]

AB

SAC

C×

E(α

5,2)

−0.0

86−0

.099

(−0.

55)

(−0.

63)

[0.1

56]

[0.1

57]

DD

(α4,

3)

0.32

60.

340

0.33

8(4

.48)

(4.3

4)(4

.30)

[0.0

73]

[0.0

78]

[0.0

79]

DD

×E

(α5,

3)

−2.2

71−2

.361

−2.4

28(−

3.64

)(−

3.68

)(−

3.73

)[0

.624

][0

.642

][0

.651

]D

IV(α

4,4)

−0.0

10−0

.010

−0.0

08−0

.008

−0.0

08(−

4.38

)(−

4.24

)(−

3.42

)(−

3.23

)(−

3.32

)[0

.002

][0

.002

][0

.002

][0

.002

][0

.002

]D

IV×

E(α

5,4)

0.13

50.

133

0.10

60.

103

0.10

5(3

.91)

(3.8

8)(3

.35)

(3.2

1)(3

.26)

[0.0

35]

[0.0

34]

[0.0

32]

[0.0

32]

[0.0

32]

Ave

rage

adj.

R-sq

uare

d0.

695

0.74

00.

740

0.75

60.

756

0.75

70.

758

0.74

10.

758

Ave

rage

N1,

610

820

820

679

679

679

679

820

679

No.

ofye

ars

5242

4242

4242

4242

42(C

ontin

ued)

EARNINGS QUALITY AND CORPORATE INVESTMENT 17

TA

BL

E4

—C

ontin

ued

Pan

elB

:Ear

ning

sQ

ualit

yM

easu

red

byU

sing

the

Non

regr

essi

onA

ppro

ach

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

EQPr

oxie

dby

γC

γL

γC

γL

γC

γL

EQ2

EQ2

Inte

rcep

t(α

0)0.

010

0.01

00.

010

0.01

00.

009

0.00

90.

019

0.01

2(5

.16)

(5.7

6)(3

.71)

(3.7

5)(2

.84)

(2.8

2)(7

.72)

(3.6

8)[0

.002

][0

.002

][0

.003

][0

.003

][0

.003

][0

.003

][0

.002

][0

.003

]E

(α1)

1.02

31.

022

1.03

51.

037

0.96

30.

961

0.88

80.

890

(79.

25)

(80.

18)

(31.

42)

(32.

82)

(29.

35)

(28.

77)

(51.

39)

(25.

37)

[0.0

13]

[0.0

13]

[0.0

33]

[0.0

32]

[0.0

33]

[0.0

33]

[0.0

17]

[0.0

35]

EQ(α

2)−0

.000

−0.0

05−0

.000

−0.0

040.

001

−0.0

03−0

.001

−0.0

01(−

1.16

)(−

4.35

)(−

0.99

)(−

3.95

)(0

.19)

(−1.

61)

(−5.

67)

(−1.

32)

[0.0

00]

[0.0

01]

[0.0

00]

[0.0

01]

[0.0

05]

[0.0

02]

[0.0

00]

[0.0

01]

EQ

×E

(α3)

0.01

10.

060

0.01

00.

054

0.00

40.

030

0.02

30.

012

(3.1

2)(5

.67)

(2.9

4)(5

.02)

(1.0

5)(2

.39)

(11.

72)

(5.0

0)[0

.004

][0

.011

][0

.003

][0

.011

][0

.004

][0

.013

][0

.002

][0

.002

]β

R(α

4,1)

−0.0

01−0

.001

−0.0

01(−

3.74

)(−

3.60

)(−

3.58

)[0

.000

][0

.000

][0

.000

]β

R×

E(α

5,1)

0.00

60.

006

0.00

6(5

.61)

(5.4

2)(5

.60)

[0.0

01]

[0.0

01]

[0.0

01]

AB

SAC

C(α

4,2)

0.07

80.

078

(5.3

3)(5

.28)

[0.0

15]

[0.0

15]

AB

SAC

C×

E(α

5,2)

−0.2

34−0

.238

(−2.

45)

(−2.

44)

[0.0

96]

[0.0

98]

(Con

tinue

d)

18 F. LI

TA

BL

E4

—C

ontin

ued

Pan

elB

:Ear

ning

sQ

ualit

yM

easu

red

byU

sing

the

Non

regr

essi

onA

ppro

ach

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

EQPr

oxie

dby

γC

γL

γC

γL

γC

γL

EQ2

EQ2

DD

(α4,

3)

0.33

10.

327

0.32

4(4

.64)

(4.5

4)(4

.50)

[0.0

71]

[0.0

72]

[0.0

72]

DD

×E

(α5,

3)

−2.2

33−2

.287

−2.2

61(−

3.86

)(−

3.78

)(−

3.79

)[0

.578

][0

.605

][0

.597

]D

IV(α

4,4)

−0.0

08−0

.007

−0.0

08−0

.008

−0.0

08(−

4.59

)(−

4.38

)(−

3.38

)(−

3.37

)(−

3.47

)[0

.002

][0

.002

][0

.002

][0

.002

][0

.002

]D

IV×

E(α

5,4)

0.02

00.

017

0.10

50.

107

0.10

5(0

.65)

(0.5

6)(3

.35)

(3.3

6)(3

.42)

[0.0

31]

[0.0

30]

[0.0

31]

[0.0

32]

[0.0

31]

Ave

rage

adj.

R-sq

uare

d0.

697

0.69

60.

704

0.70

30.

757

0.75

80.

699

0.75

9A

vera

geN

1,59

31,

610

1,58

91,

610

678

679

1,61

067

9N

o.of

year

s52

5252

5242

4252

42T

his

tabl

epr

esen

tsth

eFa

ma–

Mac

Bet

hre

gres

sion

sth

ates

timat

eea

rnin

gspe

rsis

tenc

eas

afu

nctio

nof

the

inve

stm

ent-b

ased

earn

ings

qual

ity.

The

depe

nden

tva

riab

leis

Eit+1

/TA

it−1

,ne

xtye

ar’s

earn

ings

scal

edby

the

lagg

edbo

okva

lue

ofas

sets

.Fa

ma–

Mac

Bet

ht-s

tatis

tics

(sta

ndar

der

rors

)ad

just

edfo

rN

ewey

–Wes

tau

toco

rrel

atio

n(l

ag=

3)ar

ein

pare

nthe

ses

(bra

cket

s).

The

inde

pend

entv

aria

bles

are

defin

edas

follo

ws.

Eis

,Eit

/TA

it−1

,cur

rent

earn

ings

scal

edby

the

lagg

edbo

okva

lue

ofas

sets

.The

βC

ises

timat

edfo

rev

ery

firm

year

asth

esl

ope

coef

ficie

ntfr

omth

ere

gres

sion

ofch

ange

inca

pita

land

R&

Dex

pend

iture

s(s

cale

dby

lagg

edbo

okva

lue

ofas

sets

)on

the

chan

gein

repo

rted

earn

ings

(adj

uste

dfo

rth

eim

pact

ofcu

rren

tca

pita

land

R&

Dex

pend

iture

san

dsc

aled

byla

gged

book

valu

eof

asse

ts)

usin

gda

tafr

omth

ela

st10

year

s.T

heβ

Lis

estim

ated

for

ever

yfir

mye

aras

the

slop

eco

effic

ient

from

the

regr

essi

onof

chan

gein

the

num

ber

ofem

ploy

ees

(sca

led

byla

gged

book

valu

eof

asse

ts)

onth

ech

ange

inre

port

edea

rnin

gs(s

cale

dby

lagg

edbo

okva

lue

ofas

sets

)us

ing

data

from

the

last

10ye

ars.

For

afir

mye

arto

have

βC

and

βL

,itm

usth

ave

nonm

issi

ngda

tafo

rth

ela

st10

year

s.EQ

1is

the

aver

age

ofth

ede

cile

rank

sof

βC

and

βL

.The

γC

isth

ech

ange

inca

pita

lexp

endi

ture

divi

ded

byth

ech

ange

inre

port

edea

rnin

gs.T

heγ

Lis

the

chan

gein

the

num

ber

ofem

ploy

ees

divi

ded

byth

ech

ange

inre

port

edea

rnin

gs.E

Q2

isth

eav

erag

eof

the

deci

lera

nks

ofγ

Can

dγ

L.D

Dis

the

stan

dard

devi

atio

nof

the

Dec

how

and

Dic

hev

[200

2]re

sidu

als

from

the

regr

essi

onof

accr

uals

onla

gged

CFO

(ope

ratin

gca

shfl

ows)

,cur

rent

CFO

,and

next

year

’sC

FOus

ing

the

last

10ye

ars

ofda

ta.A

BSA

CC

isth

eab

solu

team

ount

ofac

crua

ls,s

cale

dby

the

lagg

edbo

okva

lue

ofas

sets

.βR

isth

esl

ope

coef

ficie

ntfr

omth

ere

gres

sion

ofst

ock

retu

rns

onth

ech

ange

inre

port

edea

rnin

gs(s

cale

dby

lagg

edbo

okva

lue

ofas

sets

)us

ing

data

from

the

last

10ye

ars.

DIV

isa

dum

my

vari

able

that

equa

ls1

ifa

firm

pays

divi

dend

and

0ot

herw

ise.

EARNINGS QUALITY AND CORPORATE INVESTMENT 19

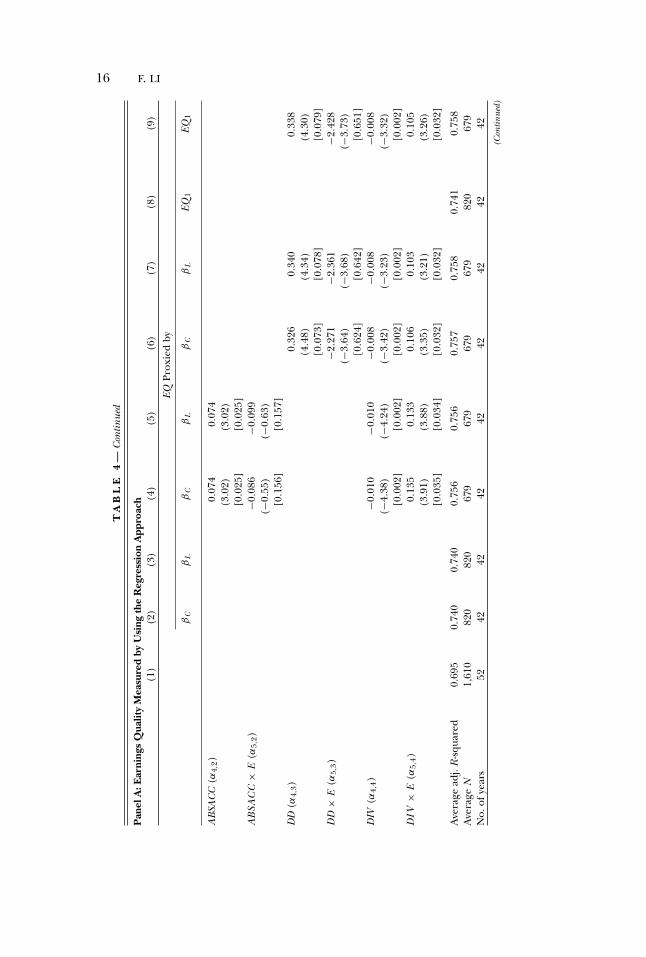

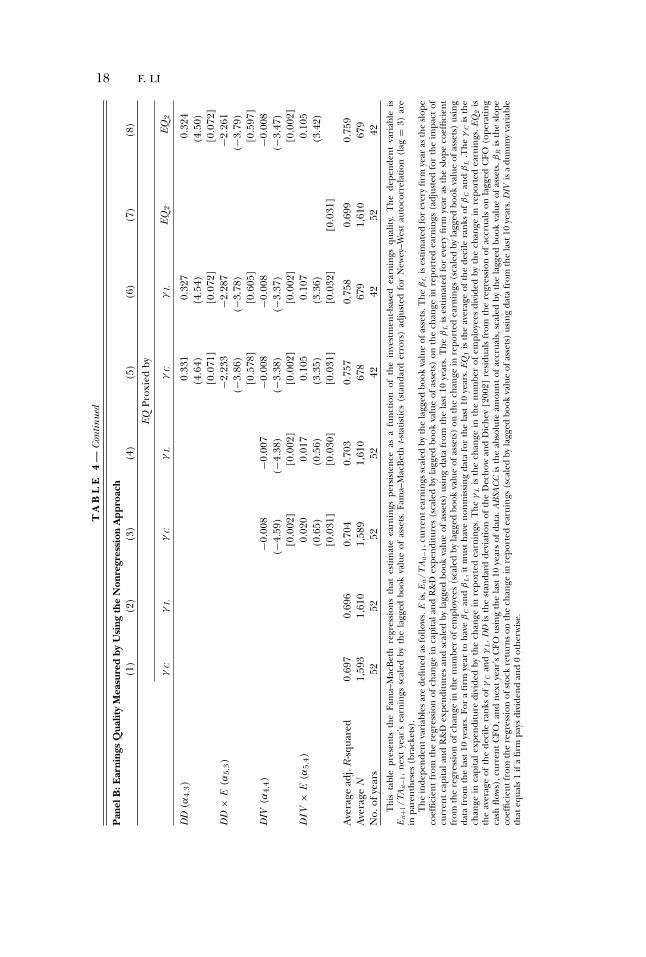

coefficient on earnings, when used alone to explain next year’s earnings,is 1.027 (column (1)). Consistent with the prediction, the coefficient onthe interaction of EQ and Eit is reliably positive, implying that earnings aremore persistent for firms with a higher association between investment andreported earnings. For instance, in column (2), the α3 is 0.064 (t = 5.06).The R -squared in column (2) is 0.74 and the R -squared in column (1) is0.70, which suggests that adding βC incrementally explains 4% more of thevariation in next year’s earnings.

When I control for the earnings–returns association, the absoluteamount of accruals, the Dechow–Dichev measure, and the dividenddummy, then the size of the α3 coefficient is smaller, but it remains eco-nomically and statistically significant. For example, in column (6), the co-efficient on the interaction of βC and Eit is 0.038 (t = 3.28). This effect isalso robust to using the rank specification of the earnings-quality measures.In column (9), when E Q 1 represents investment-based earnings quality,then the α3 is estimated at 0.011 (t = 4.65). This result implies a sub-stantial economic magnitude—increasing E Q 1 from decile 1 to decile 10means that earnings persistence increases by about 0.10. As a benchmark,the results in table 4 show that, after controlling for other variables, mov-ing DD from the bottom decile (i.e., 5th percentile = 0.006) to the topdecile (i.e., 95th percentile = 0.055) reduces the earnings persistence by0.11 (=(0.055−0.006)×(−2.3)).

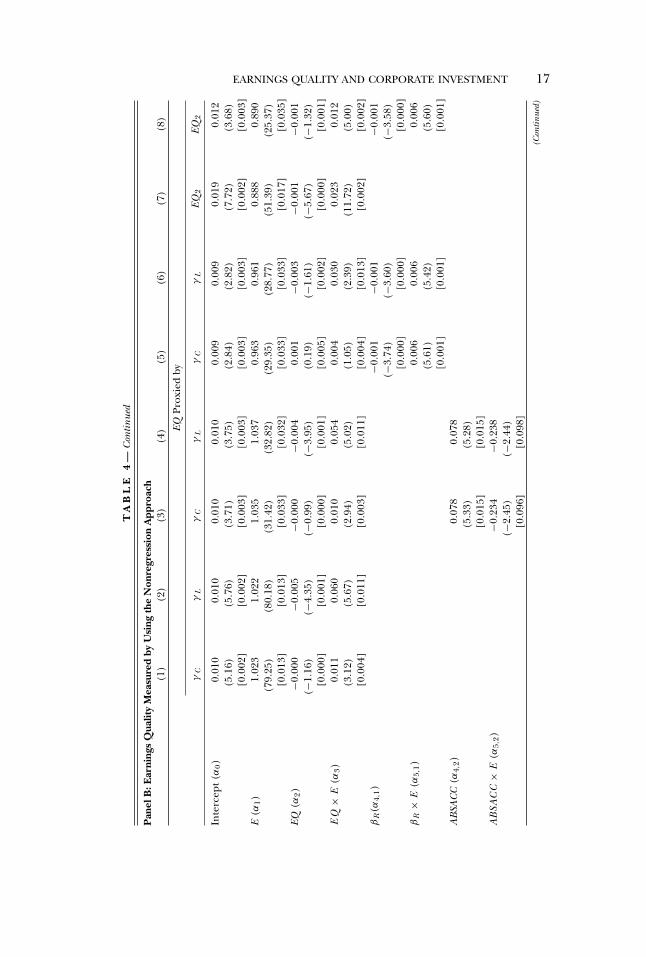

Panel B of table 4 presents the evidence based on γ L and γ C . The resultspaint the same picture as those from panel A. Throughout different spec-ifications, the interaction terms of the investment-based earnings-qualitymeasure and current earnings appear positive and statistically significant,with only the exception of column (5), where α3 is 0.004 and insignificant(t = 1.05). The economic magnitude is comparable to that of panel A. Theresults in column (9) of panel B indicate that moving from decile 1 to decile10 of E Q 2, the decile rank average of γ L and γ C , increases earnings persis-tence by about 0.10, even after controlling for the effects of other earnings-quality measures.

A very interesting finding is that the main effects of the investment-basedearnings-quality measures on future earnings (i.e., the coefficients on E Q ,α2) are generally negative.10 One possible explanation for this finding isthat the mechanical impact of investment on reported earnings throughexpensing leads to a negative bias that cannot be completely accountedfor by adding back an estimate of the expensing in equation (3). However,

10 In a multivariate regression with interaction terms, the coefficient on the main term (EQ)is not its marginal effect. The marginal effect of EQ on next year’s earnings is determined byboth the main effect and the interaction effect (conditional on the level of current earnings).For instance, in column (9) of panel A of table 4, the interactive effect (E Q × E ) coefficientis 0.011 and the main effect of EQ is −0.001; unreported results show that the mean value ofcurrent earnings (EARN ) is 0.12. Therefore, for an average firm, the marginal effect of EQ onfuture earnings is positive (i.e., −0.001 + 0.011 × 0.12 > 0).

20 F. LI

other reasons likely exist for this result because similar relations can beobserved for βR , the earnings–returns association. In all of the tests, βR

× E is positively associated with earnings persistence, yet the main effectof βR on future earnings is always negative and significant. To make surethat it is not the main effect that drives the interaction effect, I repeat allthe empirical tests without including the main effect in the regression, andthe unreported results show that the coefficients on the interaction termE Q × E remain positive and significant.

4.2 OVERINVESTMENT AND THE INVESTMENT-BASED EARNINGS QUALITY

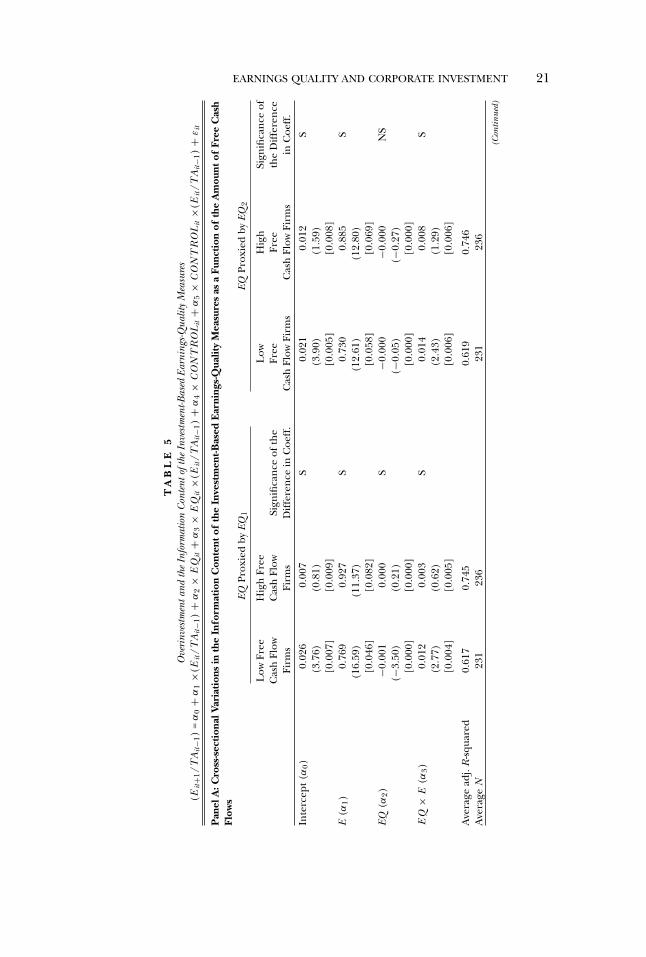

This subsection explores the implications of the nonoptimal investmentdecision making for the investment-based earnings-quality measures devel-oped in this paper. The motivation comes from prior studies that demon-strate rather pervasive evidence of overinvestment for a large sample offirms over an extended period of time (Richardson [2006]).

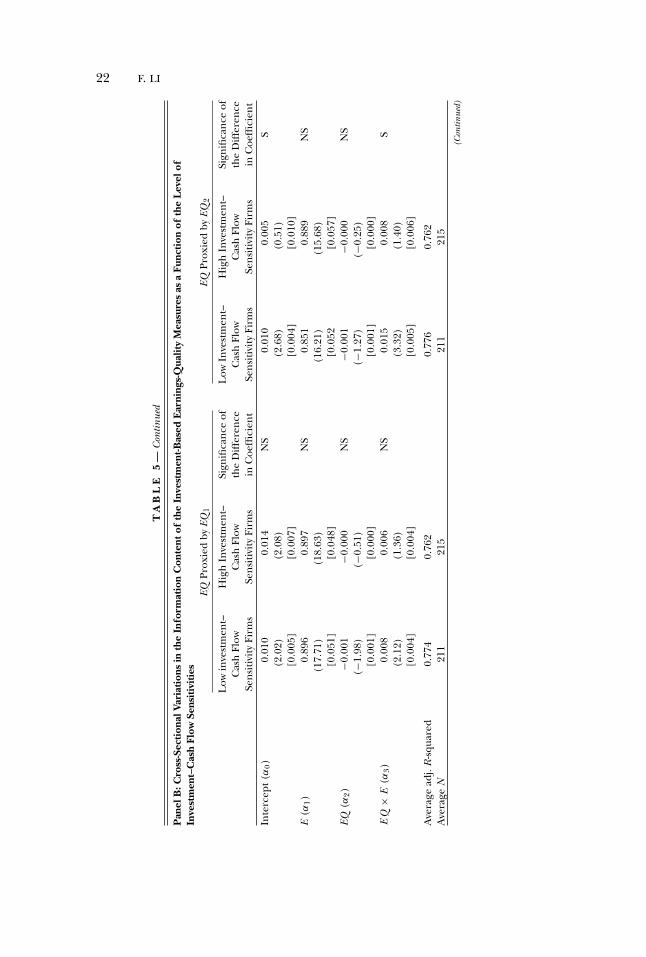

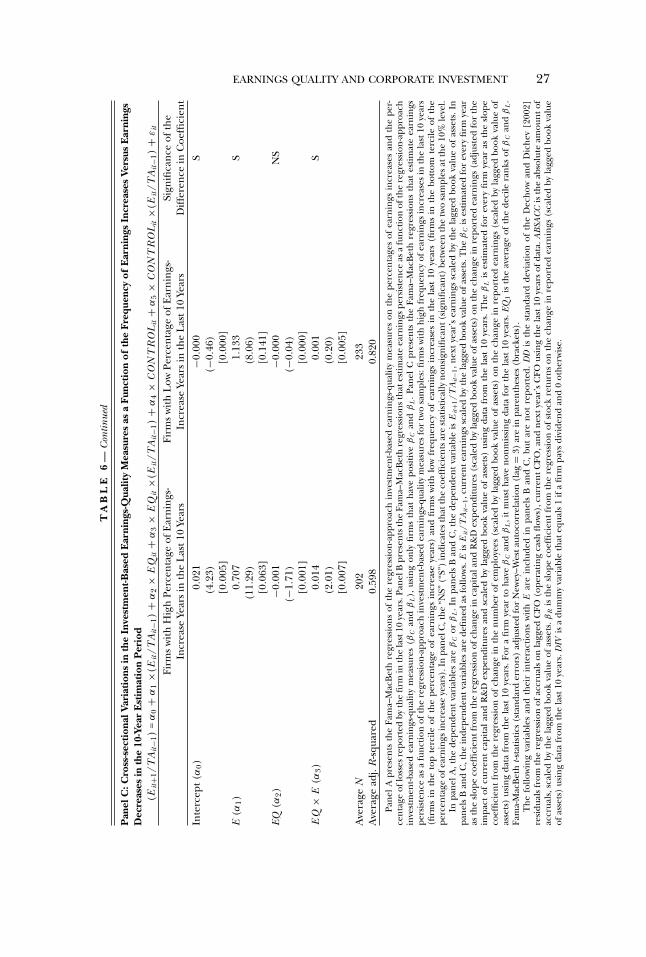

Panel A of table 5 presents the association of E Q 1 and E Q 2 with earn-ings persistence for firms with low and high free cash flows, respectively.I follow Richardson [2006] and calculate free cash flow as cash flow gen-erated from assets in place minus expected new investment; I then definefirms in the top tercile of free cash flows as high overinvestment tendencyfirms. The evidence in panel A of table 5 is consistent with the ex ante pre-diction that overinvesting firms tend to have less informative investment-based earnings-quality measures. For instance, the coefficient on E Q 1 ×E is 0.012 (t = 2.77) for firms in the bottom tercile of free cash flows and0.003 (t = 0.62) for those in the top tercile; the difference is also statisticallysignificant at the 10% level.

Panel B of table 5 measures the overinvestment tendency by using thesensitivity of investment to the amount of free cash flows measured for eachfirm year using data from the last 10 years. Based on the findings in Richard-son [2006], firms that tend to overinvest have higher investment–cash flowsensitivity.11 Results in panel B of table 5 are largely consistent with thisreasoning. The coefficient on E Q 2 × E is 0.015 (t = 3.32) for the lowinvestment–cash flow sensitivity firms, much higher than that for firms withhigh investment–cash flow sensitivity (0.008 with t = 1.40). For E Q 1 × E ,this difference is also positive (0.008 vs. 0.006), although it is smaller andstatistically insignificant.

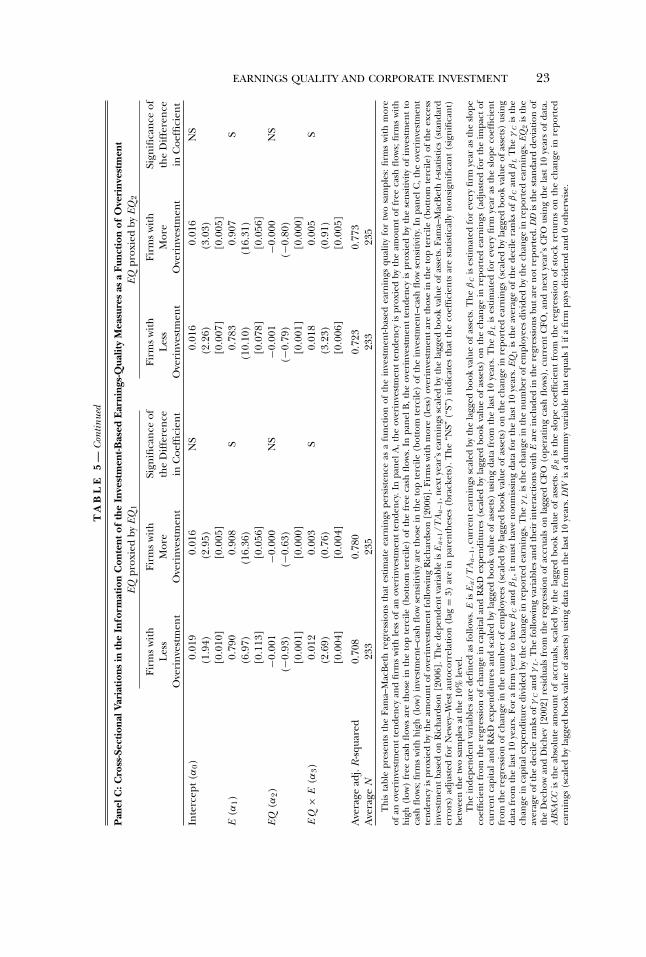

In Panel C of table 5, I rely directly on the overinvestment measureconstructed by Richardson [2006] for the cross-sectional tests. Becausethis measure directly relates to capital expenditure, I focus on the capitalinvestment-based earnings-quality measures. I calculate overinvestment asthe residual from a regression of new capital investment on growth oppor-tunities, leverage, cash, firm age, size, stock returns, lagged investment, year

11 The finance literature has argued that firms with higher investment–cash flow sensitivitytend to have more severe financing constraint. Nevertheless, this interpretation also leads toa prediction of suboptimal investment for firms with higher investment–cash flow sensitivity.

EARNINGS QUALITY AND CORPORATE INVESTMENT 21

TA

BL

E5

Ove

rinv

estm

enta

ndth

eIn

form

atio

nC

onte

ntof

the

Inve

stm

ent-B

ased

Earn

ings

-Qua

lity

Mea

sure

s(E

it+1

/TA

it−1

)=

α0

+α

1×(

Eit

/TA

it−1

)+

α2

×E

Qit

+α

3×

EQ

it×(

Eit

/TA

it−1

)+

α4

×C

ON

TR

OL

it+

α5

×C

ON

TR

OL

it×(

Eit

/TA

it−1

)+

εit

Pan

elA

:Cro

ss-s

ecti

onal

Vari

atio

nsin

the

Info

rmat

ion

Con

tent

ofth

eIn

vest

men

t-Bas

edE

arni

ngs-

Qua

lity

Mea

sure

sas

aFu

ncti

onof

the

Am

ount

ofFr

eeC

ash

Flow

sEQ

Prox

ied

byEQ

1EQ

Prox

ied

byEQ

2

Low

Free

Hig

hFr

eeL

owH

igh

Sign

ifica

nce

ofC

ash

Flow

Cas

hFl

owSi

gnifi

canc

eof

the

Free

Free

the

Diff

eren

ceFi

rms

Firm

sD

iffer

ence

inC

oeff

.C

ash

Flow

Firm

sC

ash

Flow

Firm

sin

Coe

ff.

Inte

rcep

t(α

0)0.

026

0.00

7S

0.02

10.

012

S(3

.76)

(0.8

1)(3

.90)

(1.5

9)[0

.007

][0

.009

][0

.005

][0

.008

]E

(α1)

0.76

90.

927

S0.

730

0.88

5S

(16.

59)

(11.

37)

(12.

61)

(12.

80)

[0.0

46]

[0.0

82]

[0.0

58]

[0.0

69]

EQ(α

2)−0

.001

0.00

0S

−0.0

00−0

.000

NS

(−3.

50)

(0.2

1)(−

0.05

)(−

0.27

)[0

.000

][0

.000

][0

.000

][0

.000

]E

Q×

E(α

3)0.

012

0.00

3S

0.01

40.

008

S(2

.77)

(0.6

2)(2

.43)

(1.2

9)[0

.004

][0

.005

][0

.006

][0

.006

]

Ave

rage

adj.

R-sq

uare

d0.

617

0.74

50.

619

0.74

6A

vera

geN

231

236

231

236

(Con

tinue

d)

22 F. LI

TA

BL

E5

—C

ontin

ued

Pan

elB

:Cro

ss-S

ecti

onal

Vari

atio

nsin

the

Info

rmat

ion

Con

tent

ofth

eIn

vest

men

t-Bas

edE

arni

ngs-

Qua

lity

Mea

sure

sas

aFu

ncti

onof

the

Lev

elof

Inve

stm

ent–

Cas

hFl

owSe

nsit

ivit

ies

EQPr

oxie

dby

EQ1

EQPr

oxie

dby

EQ2

Low

inve

stm

ent–

Hig

hIn

vest

men

t–Si

gnifi

canc

eof

Low

Inve

stm

ent–

Hig

hIn

vest

men

t–Si

gnifi

canc

eof

Cas

hFl

owC

ash

Flow

the

Diff

eren

ceC

ash

Flow

Cas

hFl

owth

eD

iffer

ence

Sens

itivi

tyFi

rms

Sens

itivi

tyFi

rms

inC

oeffi

cien

tSe

nsiti

vity

Firm

sSe

nsiti

vity

Firm

sin

Coe

ffici

ent

Inte

rcep

t(α

0)

0.01

00.

014

NS

0.01

00.

005

S(2

.02)

(2.0

8)(2

.68)

(0.5

1)[0

.005

][0

.007

][0

.004

][0

.010

]E

(α1)

0.89

60.

897

NS

0.85

10.

889

NS

(17.

71)

(18.

63)

(16.

21)

(15.

68)

[0.0

51]

[0.0

48]

[0.0

52[0

.057

]EQ

(α2)

−0.0

01−0

.000

NS

−0.0

01−0

.000

NS

(−1.

98)

(−0.

51)

(−1.

27)

(−0.

25)

[0.0

01]

[0.0

00]

[0.0

01]

[0.0

00]

EQ

×E

(α3)

0.00

80.

006

NS

0.01

50.

008

S(2

.12)

(1.3

6)(3

.32)

(1.4

0)[0

.004

][0

.004

][0

.005

][0

.006

]

Ave

rage

adj.

R-sq

uare

d0.

774

0.76

20.

776

0.76

2A

vera

geN

211

215

211

215

(Con

tinue

d)

EARNINGS QUALITY AND CORPORATE INVESTMENT 23T

AB

LE

5—

Con

tinue

d

Pan

elC

:Cro

ss-S

ecti

onal

Vari

atio

nsin

the

Info

rmat

ion

Con

tent

ofth

eIn

vest

men

t-Bas

edE

arni

ngs-

Qua

lity

Mea

sure

sas

aFu

ncti

onof

Ove

rinv

estm

ent

EQpr

oxie

dby

EQ1

EQpr

oxie

dby

EQ2

Firm

sw

ithFi

rms

with

Sign

ifica

nce

ofFi

rms

with

Firm

sw

ithSi

gnifi

canc

eof

Les

sM

ore

the

Diff

eren

ceL

ess

Mor

eth

eD

iffer

ence

Ove

rinv

estm

ent

Ove

rinv

estm

ent

inC

oeffi

cien

tO

veri

nves

tmen

tO

veri

nves

tmen

tin

Coe

ffici

ent

Inte

rcep

t(α

0)0.

019

0.01

6N

S0.

016

0.01

6N

S(1

.94)

(2.9

5)(2

.26)

(3.0

3)[0

.010

][0

.005

][0

.007

][0

.005

]E

(α1)

0.79

00.

908

S0.

783

0.90

7S

(6.9

7)(1

6.36

)(1

0.10

)(1

6.31

)[0

.113

][0

.056

][0

.078

][0

.056

]EQ

(α2)

−0.0

01−0

.000

NS

−0.0

01−0

.000

NS

(−0.

93)

(−0.

63)

(−0.

79)

(−0.

80)

[0.0

01]

[0.0

00]

[0.0

01]

[0.0

00]

EQ

×E

(α3)

0.01

20.

003

S0.

018

0.00

5S

(2.6

9)(0

.76)

(3.2

3)(0

.91)

[0.0

04]

[0.0

04]

[0.0

06]

[0.0

05]

Ave

rage

adj.

R-sq

uare

d0.

708

0.78

00.

723

0.77

3A

vera

geN

233

235

233

235

Thi

sta

ble

pres

ents

the

Fam

a–M

acB

eth

regr

essi

ons

that

estim

ate

earn

ings

pers

iste

nce

asa

func

tion

ofth

ein

vest

men

t-bas

edea

rnin

gsqu

ality

for

two

sam

ples

:firm

sw

ithm

ore

ofan

over

inve

stm

ent

tend

ency

and

firm

sw

ithle

ssof

anov

erin

vest

men

tte

nden

cy.I

npa

nelA

,the

over

inve

stm

ent

tend

ency

ispr

oxie

dby

the

amou

ntof

free

cash

flow

s;fir

ms

with

high

(low

)fr

eeca

shfl

ows

are

thos

ein

the

top

terc