Embed Size (px)

Citation preview

Corporate Finance 2-1© Professor Ho-Mou Wu

Capital Investment DecisionsCapital Investment Decisions

2.1 Net Present Value

2.2 Project Valuation in a Riskless World

Fisher’s Principle

2.3 Present Value and Compounding

2.4 Present Value with Special Cash Flows

(RWJ Ch 3, 4)

Corporate Finance 2-2© Professor Ho-Mou Wu

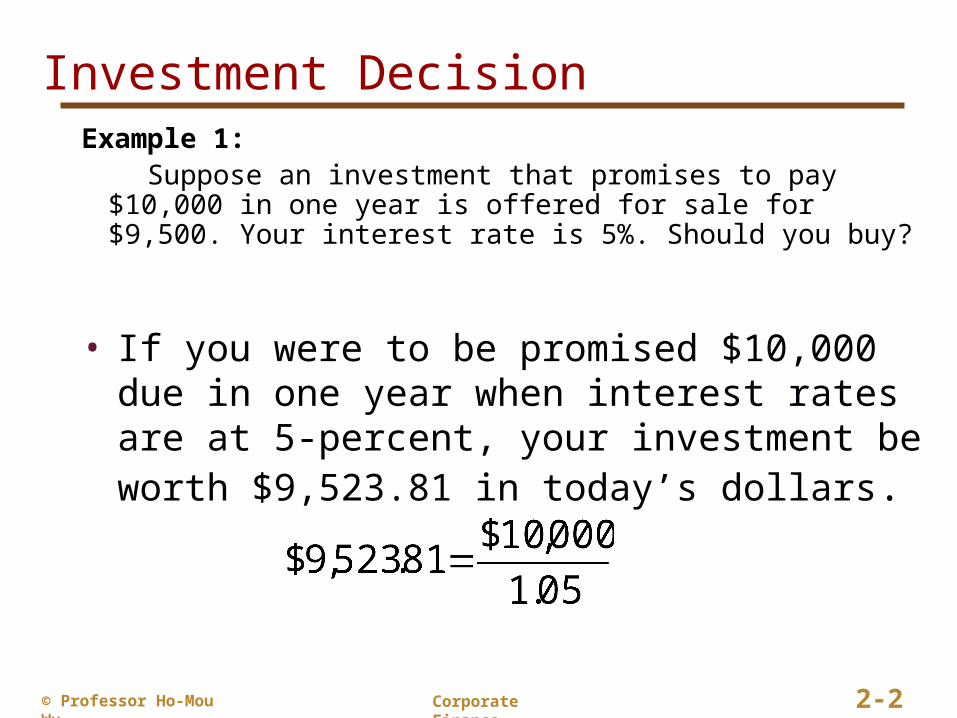

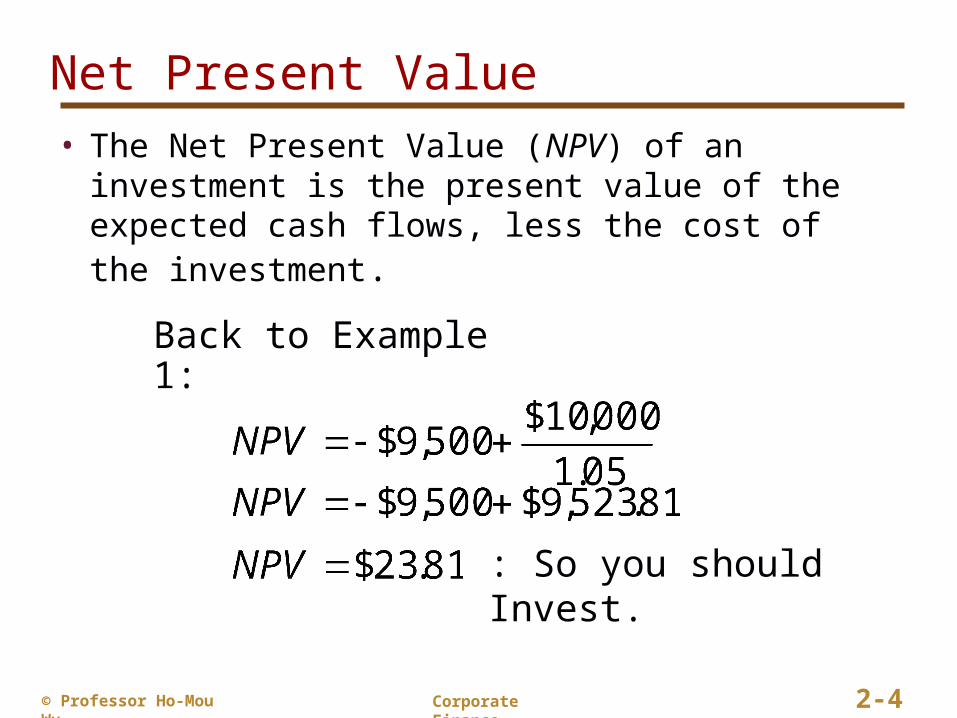

Investment DecisionExample 1: Suppose an investment that promises to pay $10,000 in one

year is offered for sale for $9,500. Your interest rate is 5%. Should you buy?

• If you were to be promised $10,000 due in one year when interest rates are at 5-percent, your investment be worth $9,523.81 in today’s dollars.

Corporate Finance 2-3© Professor Ho-Mou Wu

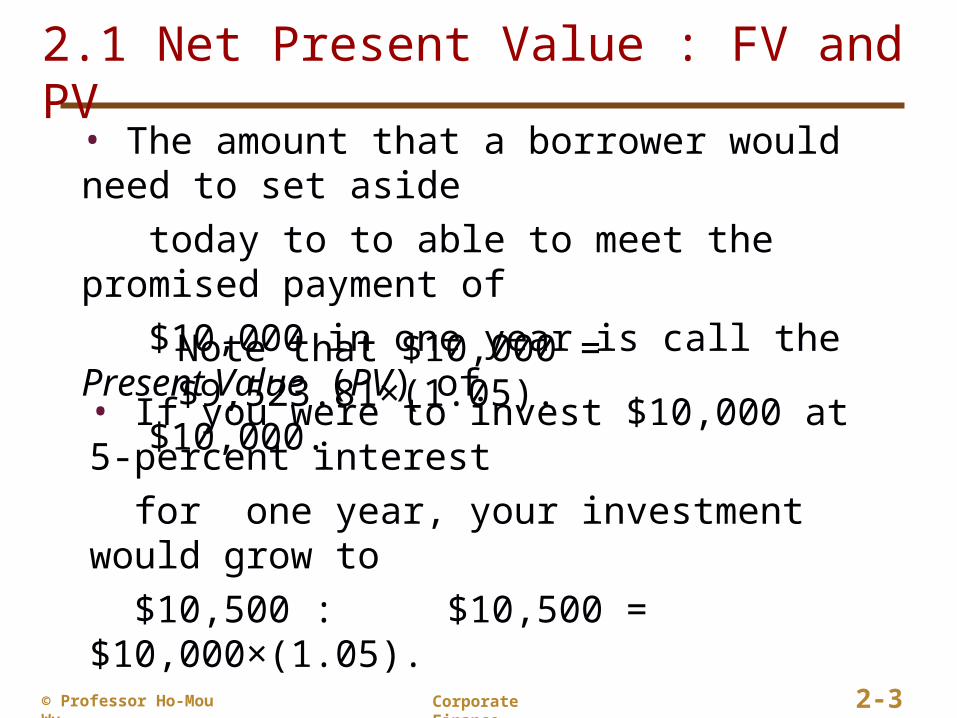

2.1 Net Present Value : FV and PV• The amount that a borrower would need to set aside

today to to able to meet the promised payment of

$10,000 in one year is call the Present Value (PV) of

$10,000.Note that $10,000 = $9,523.81×(1.05).

• If you were to invest $10,000 at 5-percent interest

for one year, your investment would grow to

$10,500 : $10,500 = $10,000×(1.05).

The total amount due at the end of the investment is call the Future Value (FV).

Corporate Finance 2-4© Professor Ho-Mou Wu

Net Present Value

• The Net Present Value (NPV) of an investment is the present value of the expected cash flows, less the cost of the investment.

: So you should Invest.

Back to Example 1:

Corporate Finance 2-5© Professor Ho-Mou Wu

Net Present Value as the Investment Criterion

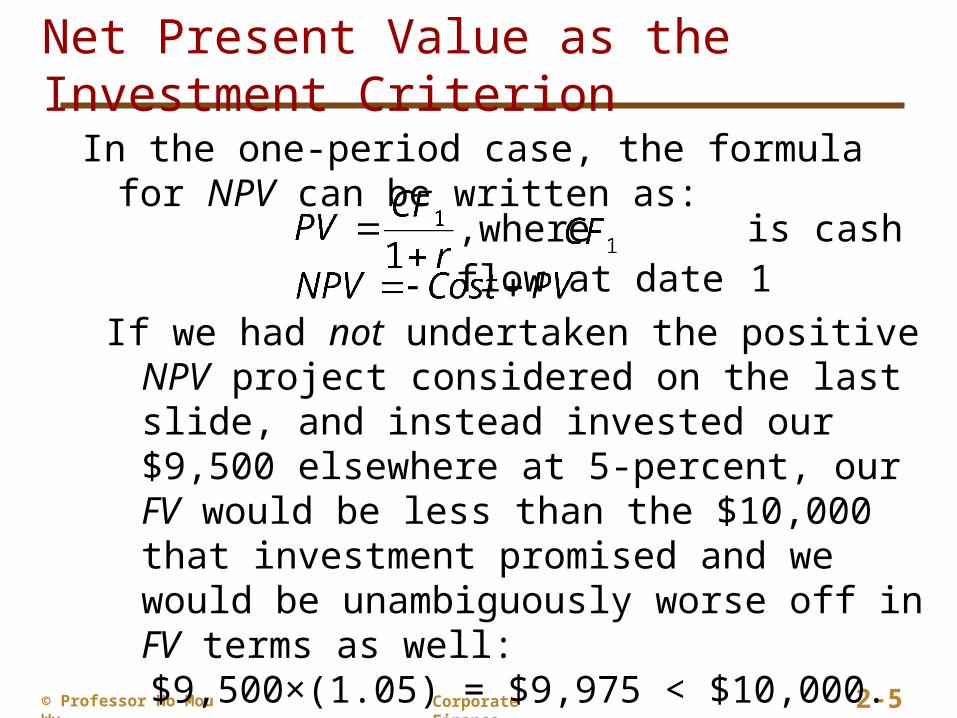

In the one-period case, the formula for NPV can be written as:

If we had not undertaken the positive NPV project considered on the last slide, and instead invested our $9,500 elsewhere at 5-percent, our FV would be less than the $10,000 that investment promised and we would be unambiguously worse off in FV terms as well:

$9,500×(1.05) = $9,975 < $10,000.

,where is cash flow at date 1

Corporate Finance 2-6© Professor Ho-Mou Wu

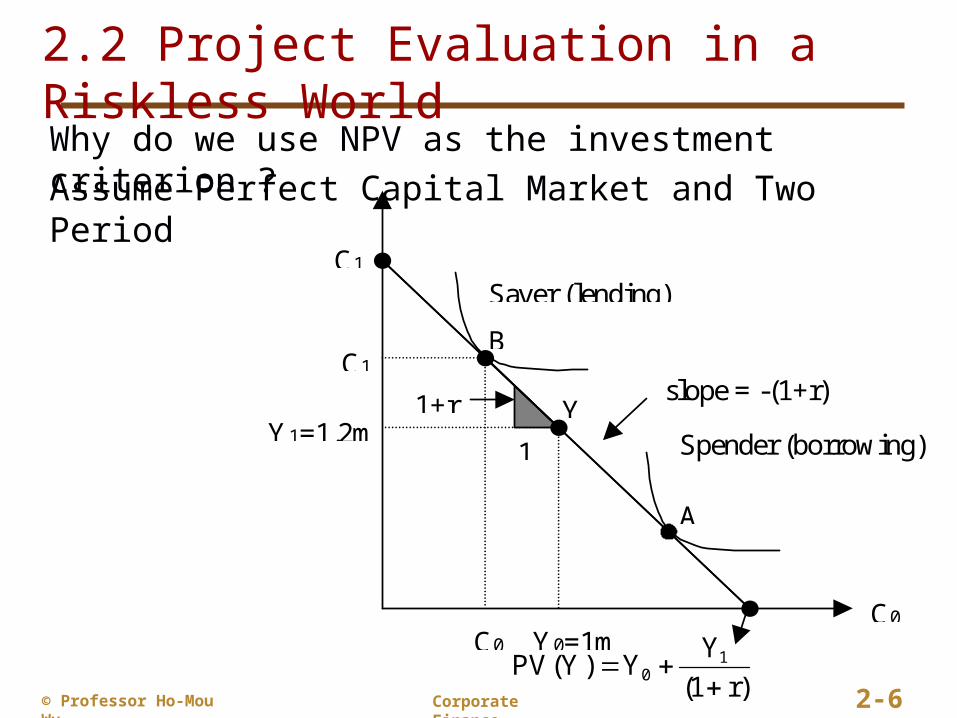

2.2 Project Evaluation in a Riskless World

C0

C0

C1

C1

Y1=1.2m

Y0=1m

Saver (lending)

B

Spender (borrowing)

A

Y

)r1(

YY)Y(PV 1

0

1

1+r slope = -(1+r)

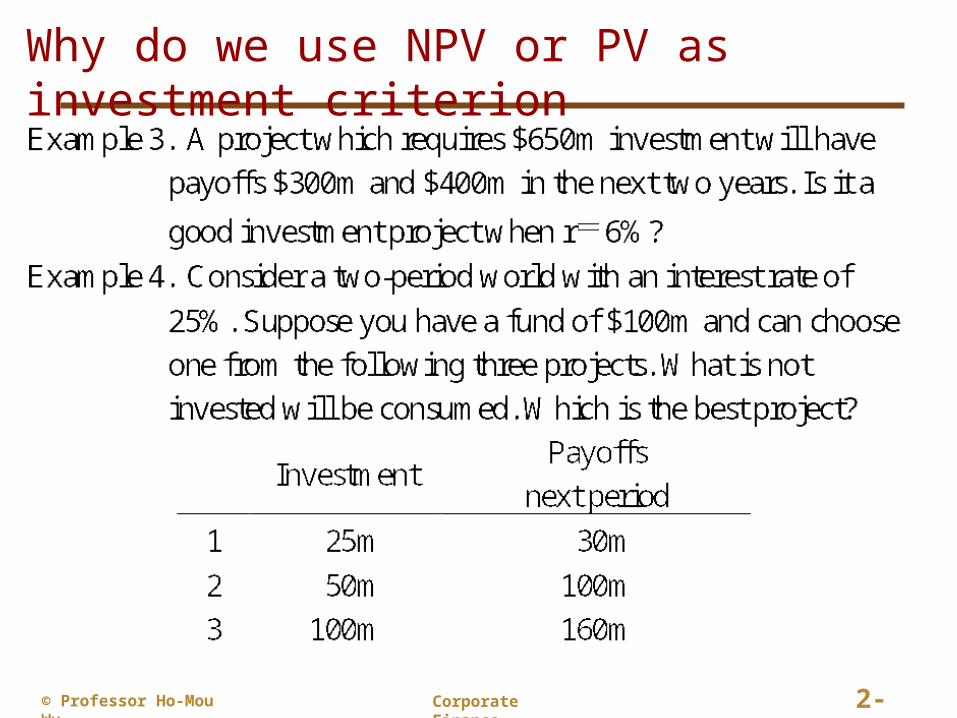

Why do we use NPV as the investment criterion ?

Assume Perfect Capital Market and Two Period

Corporate Finance 2-7© Professor Ho-Mou Wu

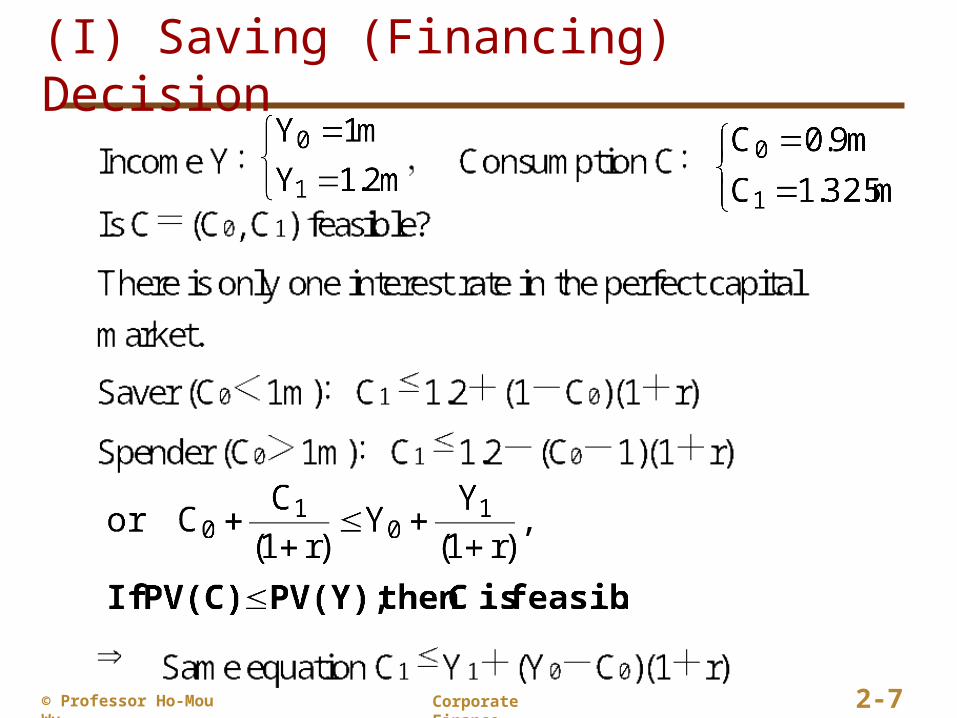

(I) Saving (Financing) Decision

Corporate Finance 2-8© Professor Ho-Mou Wu

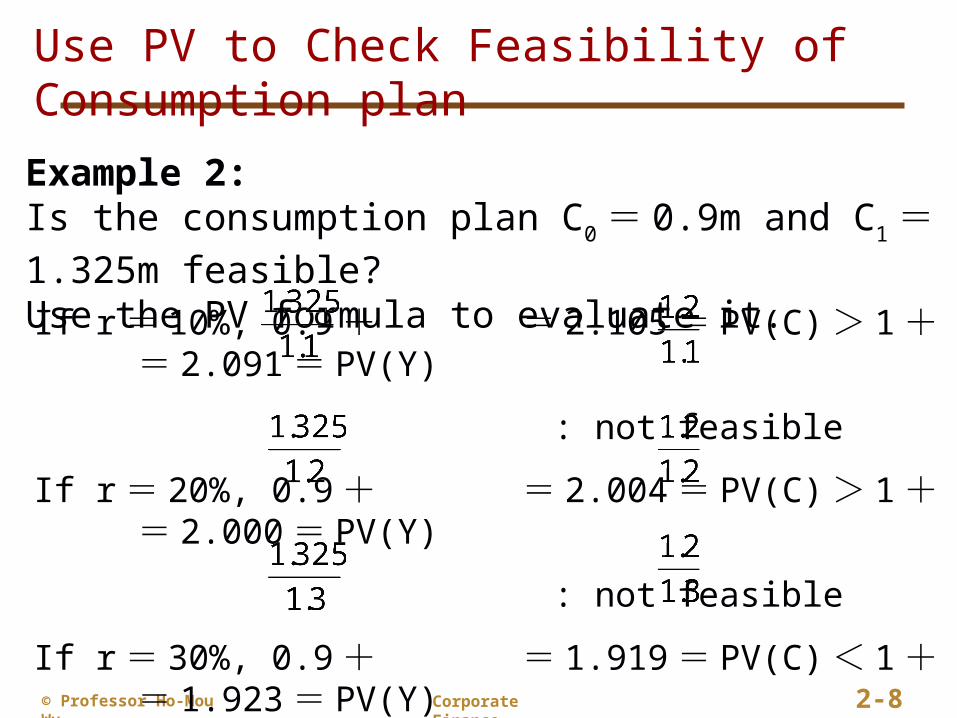

Use PV to Check Feasibility of Consumption plan

Example 2: Is the consumption plan C0 = 0.9m and C1 = 1.325m

feasible?Use the PV formula to evaluate it.If r = 10%, 0.9 + = 2.105 = PV(C) > 1 + = 2.091= PV(Y)

: not feasible

If r = 20%, 0.9 + = 2.004 = PV(C) > 1 + = 2.000= PV(Y)

: not feasible

If r = 30%, 0.9 + = 1.919 = PV(C) < 1 + = 1.923= PV(Y)

: feasible!

Corporate Finance 2-9© Professor Ho-Mou Wu

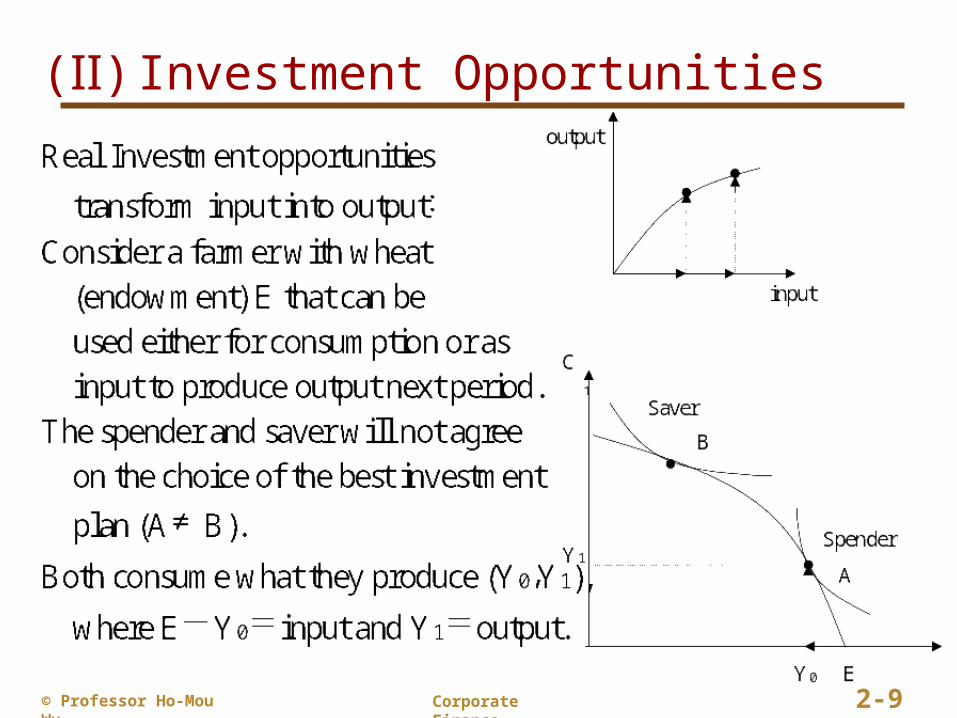

( )Ⅱ Investment Opportunities

Corporate Finance 2-10© Professor Ho-Mou Wu

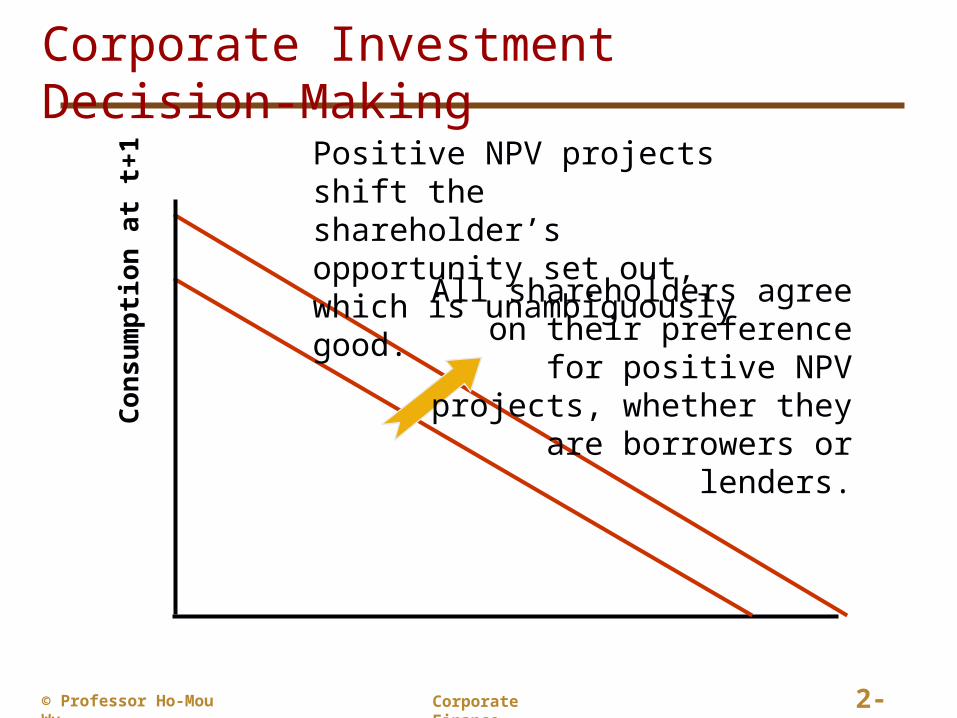

Corporate Investment Decision‑MakingC

onsu

mp

tion

at

t+1

Positive NPV projects shift the shareholder’s opportunity set out, which is unambiguously good.

All shareholders agree on their preference for positive NPV

projects, whether they are borrowers or lenders.

Corporate Finance 2-11© Professor Ho-Mou Wu

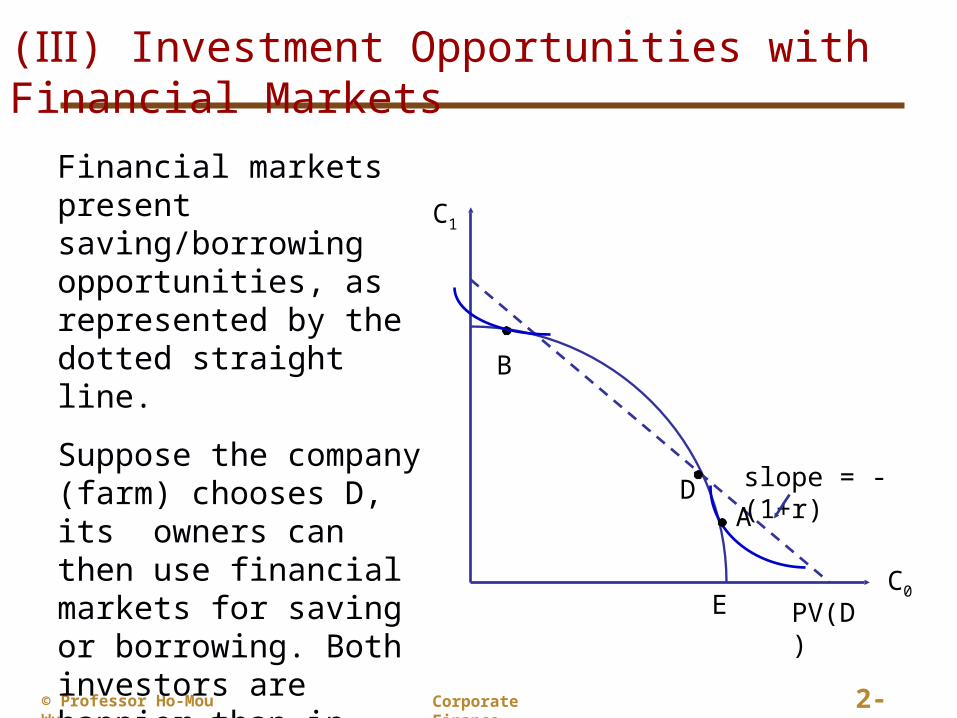

( ) Ⅲ Investment Opportunities with Financial Markets

Financial markets present saving/borrowing opportunities, as represented by the dotted straight line.

Suppose the company (farm) chooses D, its owners can then use financial markets for saving or borrowing. Both investors are happier than in ( ), but D is not the Ⅱoptimal investment plan yet. C0

B

AD

E

C1

slope = -(1+r)

PV(D)

Corporate Finance 2-12© Professor Ho-Mou Wu

Project Valuation in a Riskless World

C0

A’D

E

slope = -(1+r)

PV(Y)

C1

B’

Y*

Y1

Y0

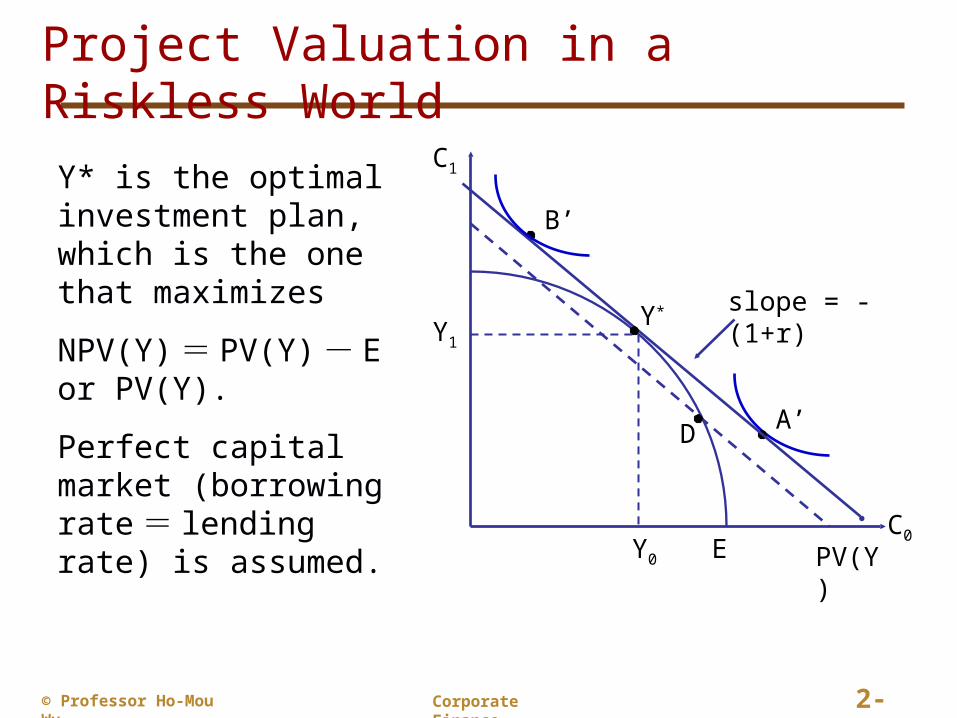

Y* is the optimal investment plan, which is the one that maximizes

NPV(Y) = PV(Y) - E or PV(Y).

Perfect capital market (borrowing rate = lending rate) is assumed.

Corporate Finance 2-13© Professor Ho-Mou Wu

Corporate Investment Decision‑Making

• In reality, shareholders do not vote on every investment decision faced by a firm and the managers of firms need decision rules to operate by.

• All shareholders of a firm will be made better off if managers follow the NPV rule—undertake positive NPV projects and reject negative NPV projects.

Corporate Finance 2-14© Professor Ho-Mou Wu

Optimal Investment Plan

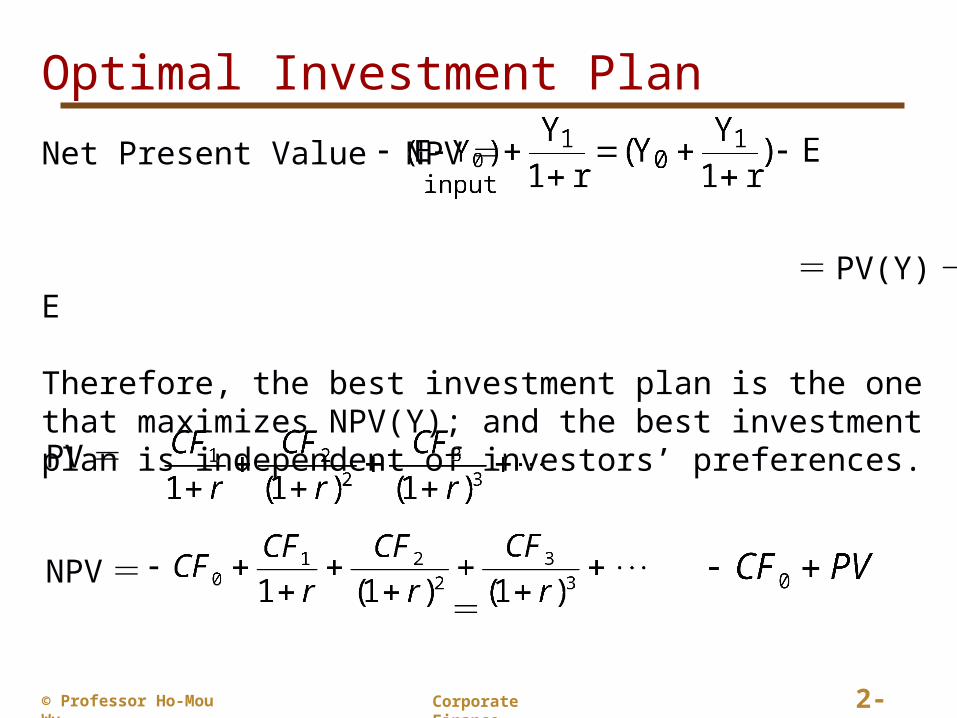

Net Present Value NPV =

= PV(Y) - E

Therefore, the best investment plan is the one that maximizes NPV(Y); and the best investment plan is independent of investors’ preferences.

PV =

NPV = =

Corporate Finance 2-15© Professor Ho-Mou Wu

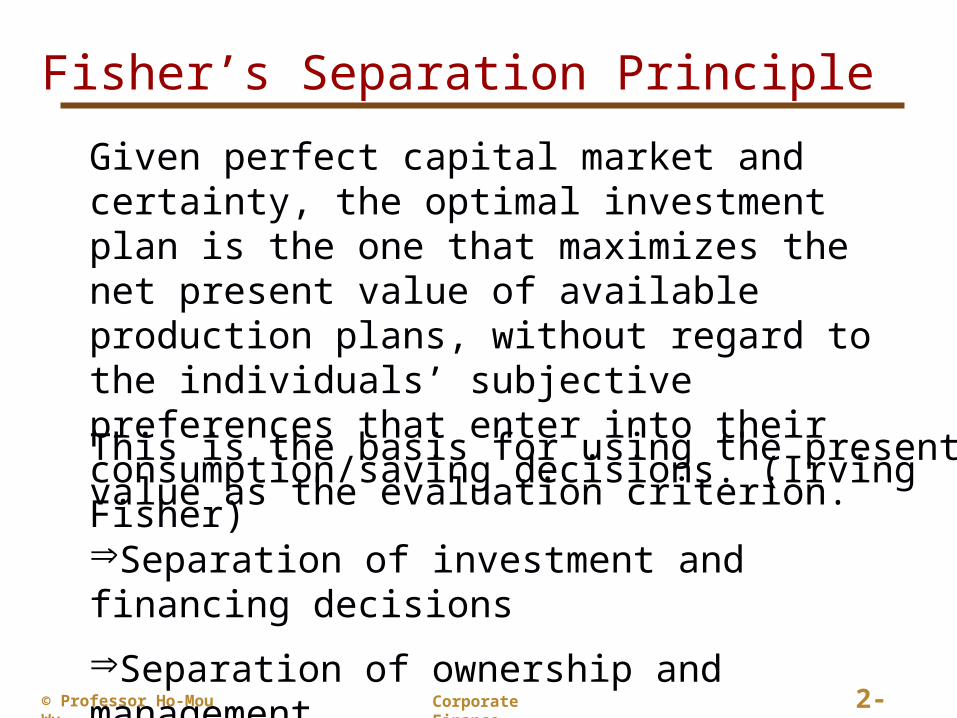

Fisher’s Separation Principle

Given perfect capital market and certainty, the optimal investment plan is the one that maximizes the net present value of available production plans, without regard to the individuals’ subjective preferences that enter into their consumption/saving decisions. (Irving Fisher)

This is the basis for using the present value as the evaluation criterion.

Separation of investment and financing decisions

Separation of ownership and management.

Corporate Finance 2-16© Professor Ho-Mou Wu

Why do we use NPV or PV as investment criterion

Corporate Finance 2-17© Professor Ho-Mou Wu

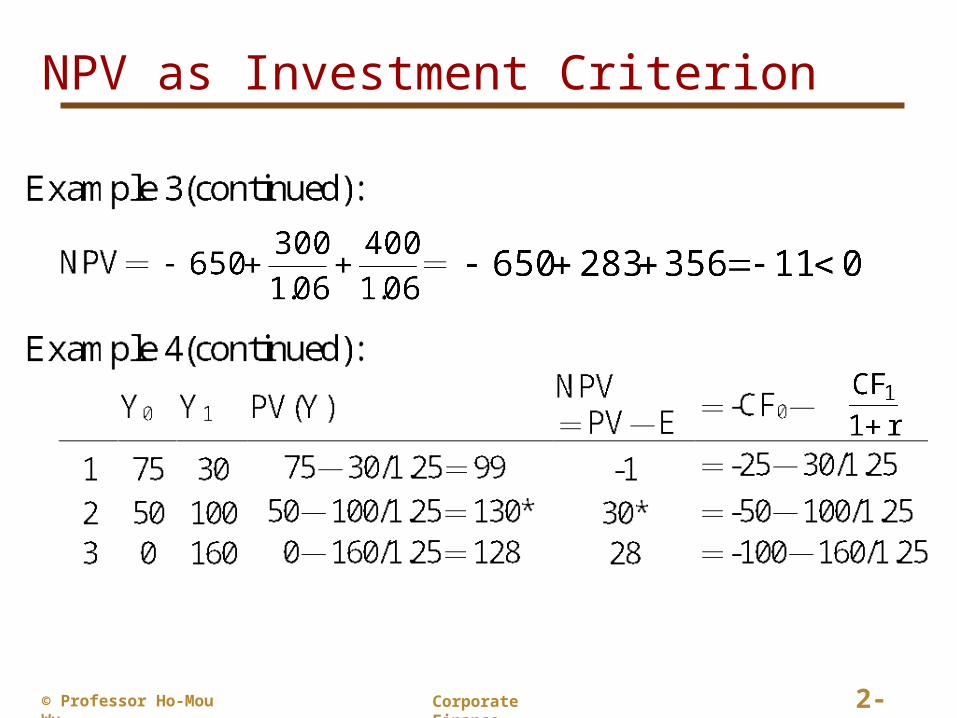

NPV as Investment Criterion

Corporate Finance 2-18© Professor Ho-Mou Wu

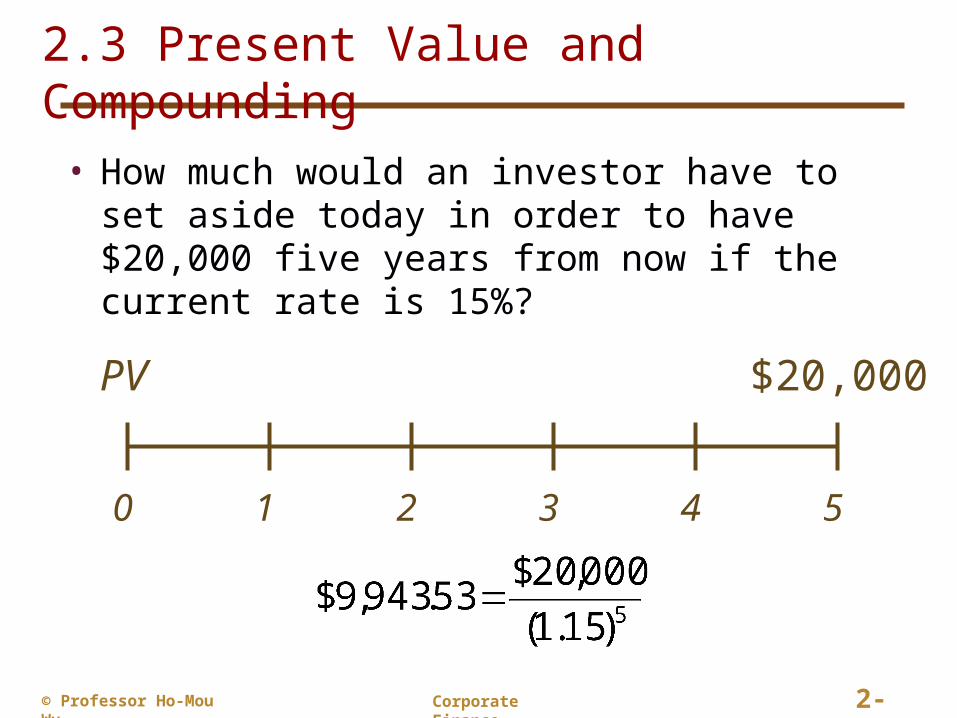

2.3 Present Value and Compounding

• How much would an investor have to set aside today in order to have $20,000 five years from now if the current rate is 15%?

0 1 2 3 4 5

$20,000PV

Corporate Finance 2-19© Professor Ho-Mou Wu

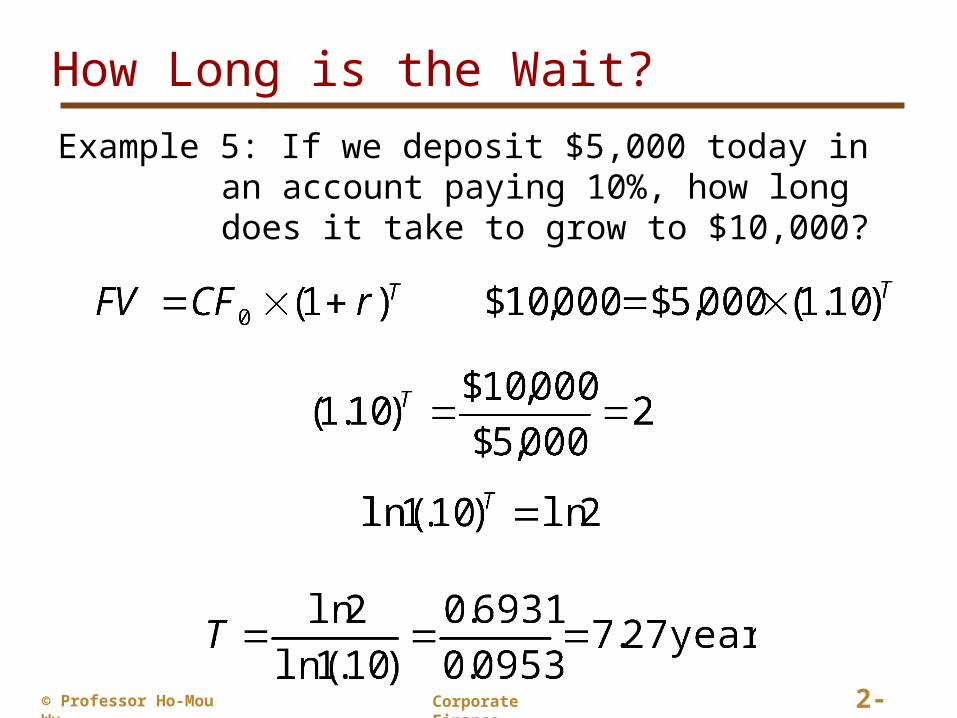

How Long is the Wait?

Example 5: If we deposit $5,000 today in an account paying 10%, how long does it take to grow to $10,000?

Corporate Finance 2-20© Professor Ho-Mou Wu

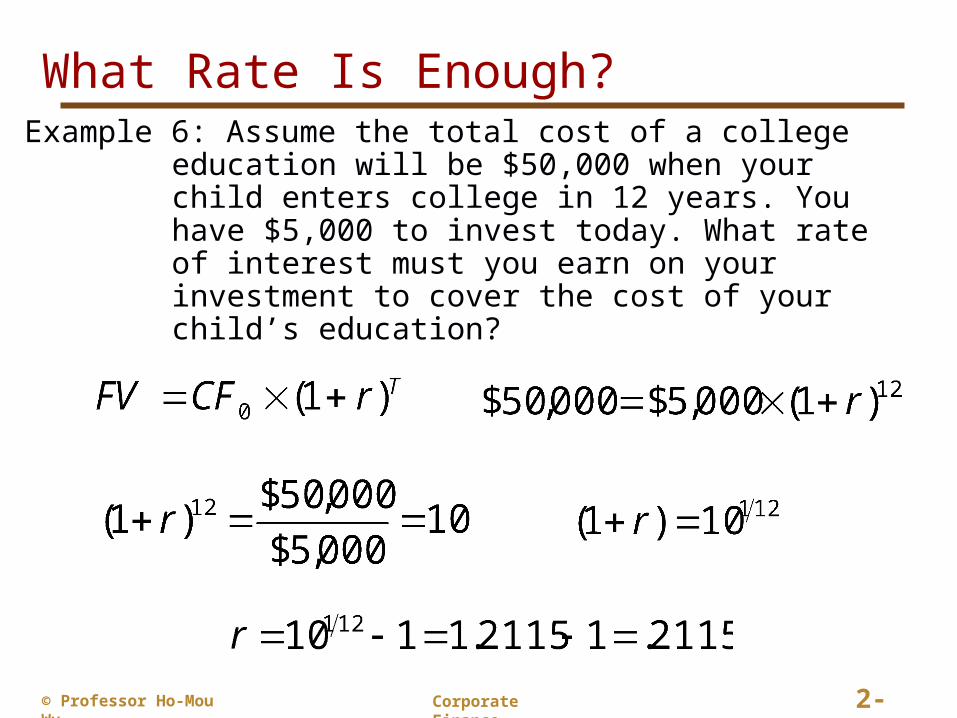

Example 6: Assume the total cost of a college education will be $50,000 when your child enters college in 12 years. You have $5,000 to invest today. What rate of interest must you earn on your investment to cover the cost of your child’s education?

What Rate Is Enough?

Corporate Finance 2-21© Professor Ho-Mou Wu

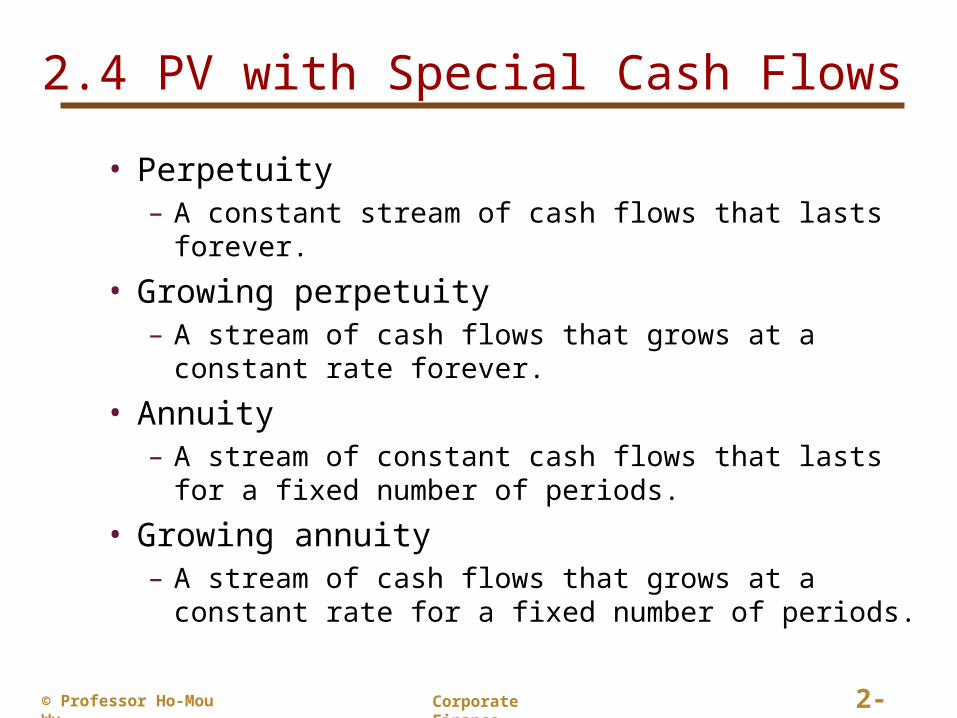

2.4 PV with Special Cash Flows

• Perpetuity– A constant stream of cash flows that lasts forever.

• Growing perpetuity– A stream of cash flows that grows at a constant rate

forever.

• Annuity– A stream of constant cash flows that lasts for a fixed

number of periods.

• Growing annuity– A stream of cash flows that grows at a constant rate for a

fixed number of periods.

Corporate Finance 2-22© Professor Ho-Mou Wu

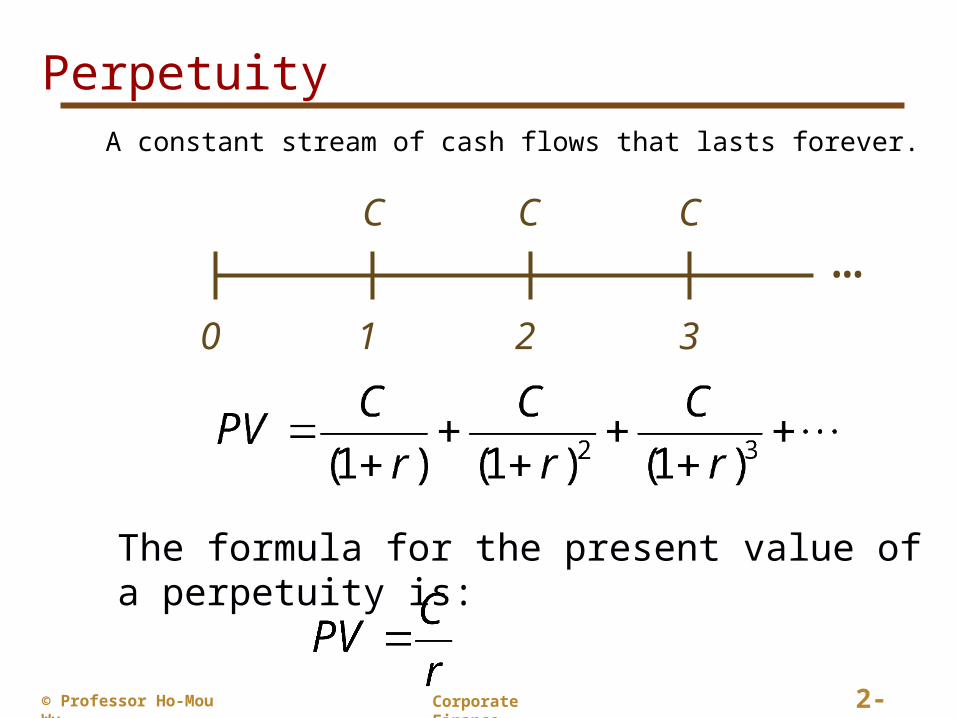

Perpetuity

A constant stream of cash flows that lasts forever.

0

…1

C

2

C

3

C

The formula for the present value of a perpetuity is:

Corporate Finance 2-23© Professor Ho-Mou Wu

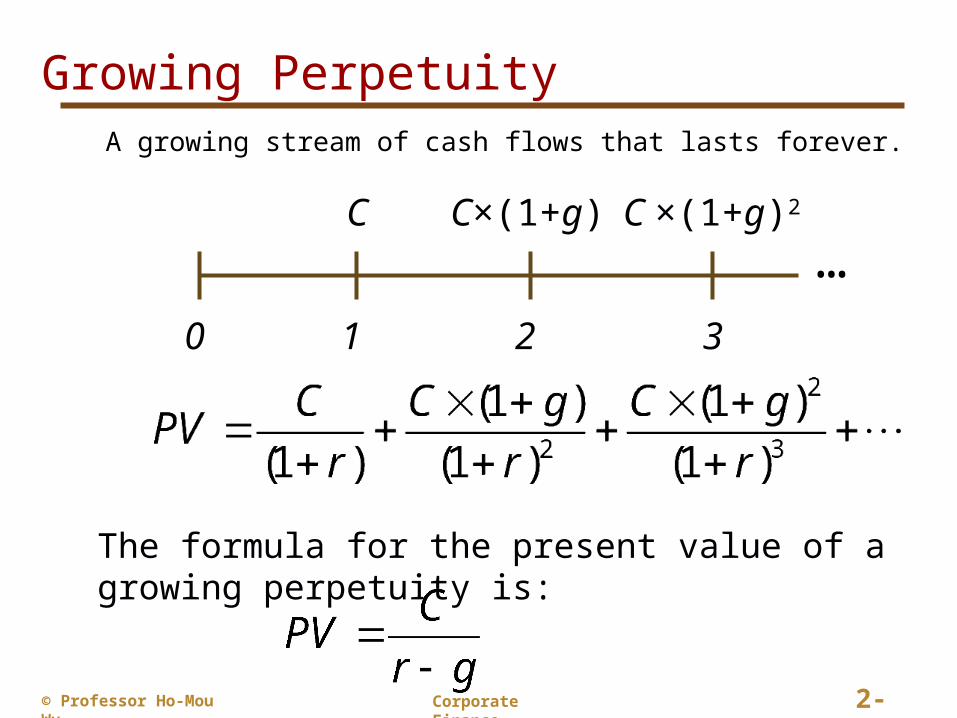

Growing Perpetuity

A growing stream of cash flows that lasts forever.

0

…1

C

2

C×(1+g)

3

C ×(1+g)2

The formula for the present value of a growing perpetuity is:

Corporate Finance 2-24© Professor Ho-Mou Wu

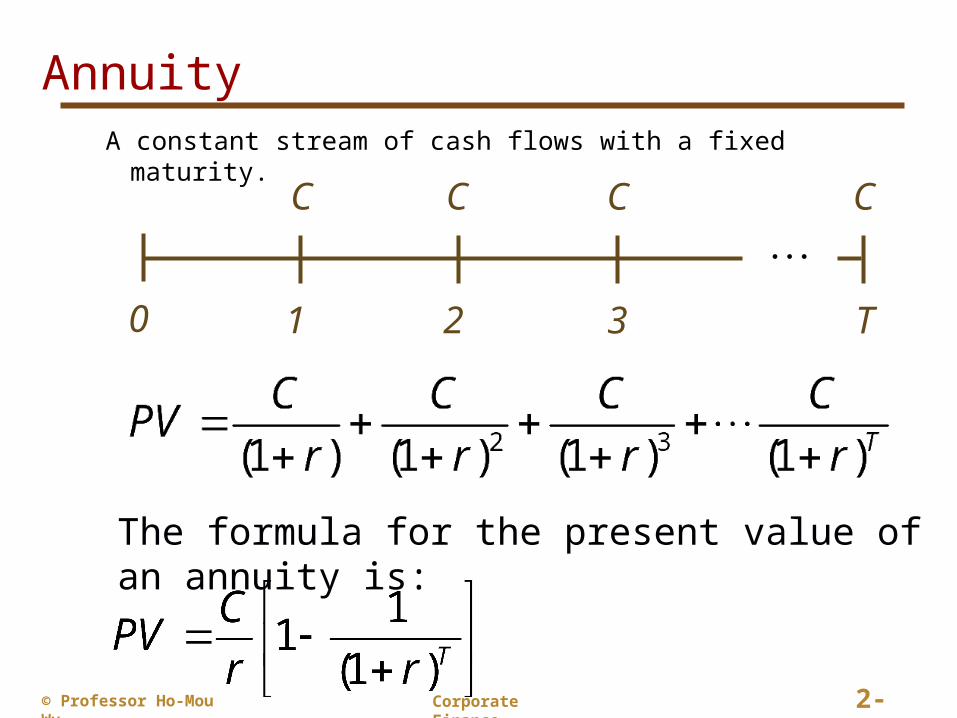

Annuity

A constant stream of cash flows with a fixed maturity.

0 1

C

2

C

3

C

The formula for the present value of an annuity is:

T

C

Corporate Finance 2-25© Professor Ho-Mou Wu

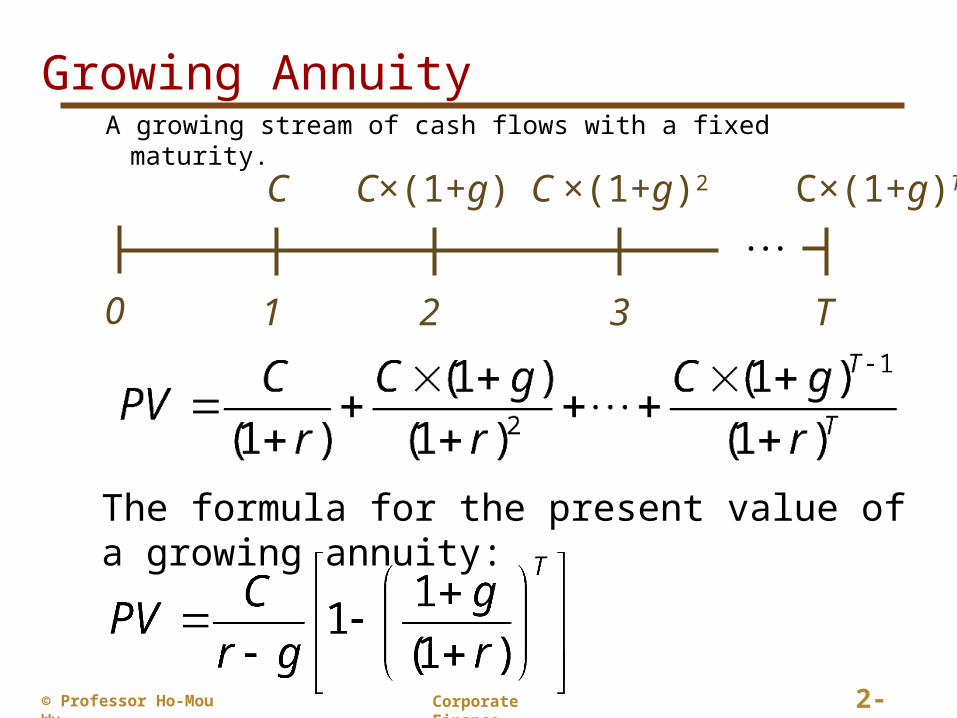

Growing AnnuityA growing stream of cash flows with a fixed maturity.

0 1

C

The formula for the present value of a growing annuity:

2

C×(1+g)

3

C ×(1+g)2

T

C×(1+g)T-1

Corporate Finance 2-26© Professor Ho-Mou Wu

What Is a Firm Worth?

• Conceptually, a firm should be worth the present value of the firm’s cash flows.

• The tricky part is determining the size, timing and “risk” of those cash flows : we will probe further in later class..