Embed Size (px)

Citation preview

E&P Business TrendCSFB Oil & Gas Conference

London, June 8th, 2005

A. BelottiSenior Vice PresidentE&P Business Planning

2

Disclaimer

This presentation contains forward-looking statements regarding future events and the future results of Eni that are based on current expectations, estimates, forecasts, and projections about the industries in which Eni operates and the beliefs and assumptions of the management of Eni. In particular, among other statements, certain statements with regard to management objectives, trends in results of operations, margins, costs, return on equity, risk management and competition are forward-looking in nature. Words such as ‘expects’, ‘anticipates’, ‘targets’, ‘goals’, ‘projects’, ‘intends’, ‘plans’, ‘believes’, ‘seeks’, ‘estimates’, variations of such words, and similar expressions are intended to identify such forward-looking statements. These forward-looking statements are only predictions and are subject to risks, uncertainties, and assumptions that are difficult to predict because they relate to events and depend on circumstances that will occur in the future. Therefore, Eni’s actual results may differ materially and adversely from those expressed or implied in any forward-looking statements. Factors that might cause or contribute to such differences include, but are not limited to, economic conditions globally, the impact of competition, political and economic developments in the countries in which Eni operates, regulatory developments in Italy and internationally and changes in oil prices and in the margins for Eni products. Any forward-looking statements made by or on behalf of Eni speak only as of the date they are made. Eni does not undertake to update forward-looking statements to reflect any changes in Eni’s expectations with regard thereto or any changes in events, conditions or circumstances on which any such statement is based. The reader should, however, consult any further disclosures Eni may make in documents it files with the US Securities and Exchange Commission.

Production Trend

Capital Investment

Projects

New Opportunities

Highlights

3

4

High Quality Portfolio to Fuel Future Growth

� Strong organic production growth

� Solid reserve replacement ratio

� World scale projects

� Selective Exploration

Solid upstream Portfolio

Efficiency and strong cash generation

� Focus on efficiency

� Strong cash flow per boe

� New initiatives in producing regions

� Access to high potential areas

� New themes

New opportunities

SustainableMedium/Long term growth

5

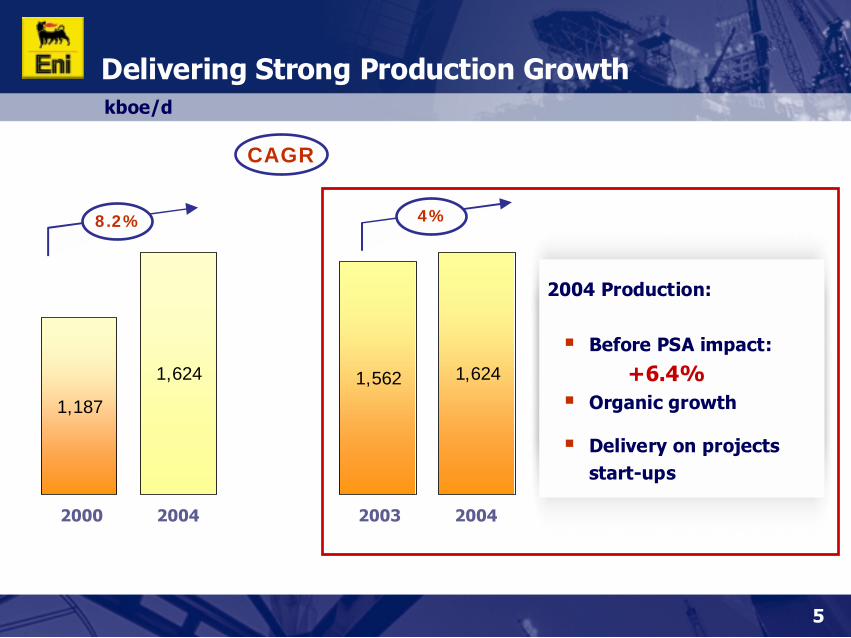

Delivering Strong Production Growthkboe/d

1,6241,5621,624

1,187

0

200

400

600

800

1000

1200

1400

1600

1800

2000 2004 2003 2004

4%

2004 Production:

� Before PSA impact:

+6.4%� Organic growth

� Delivery on projects start-ups

CAGR

8.2%

6

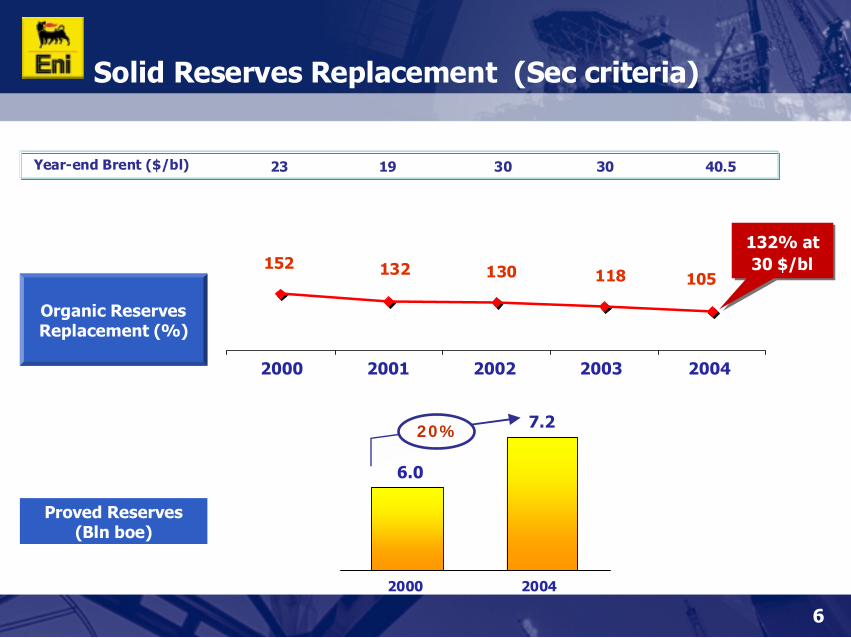

Solid Reserves Replacement (Sec criteria)

105130152 132 118

2000 2001 2002 2003 2004

Organic Reserves Replacement (%)

23 19 30 30 40.5Year-end Brent ($/bl)

Proved Reserves (Bln boe)

132% at30 $/bl

132% at30 $/bl

6.0

7.2

2000 2004

20%

7

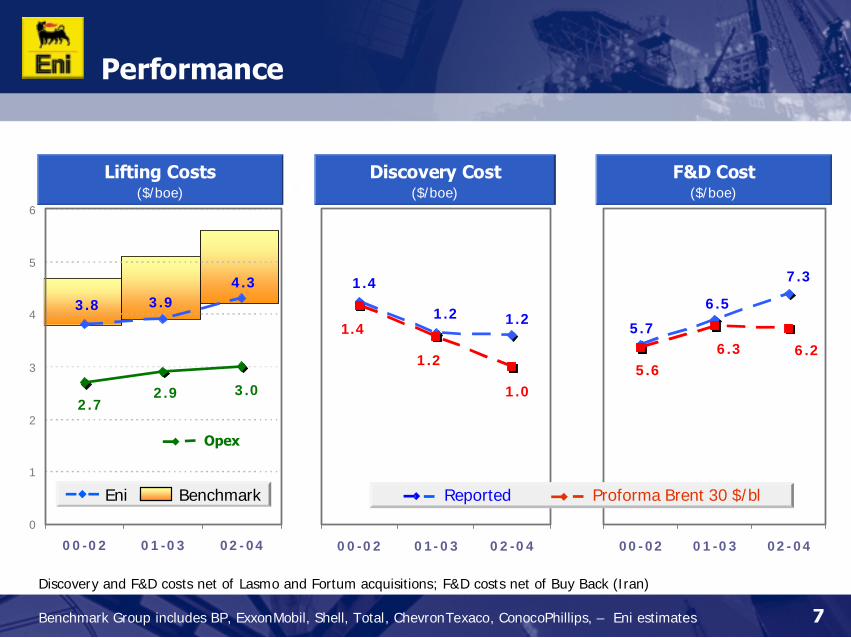

Performance

Discovery and F&D costs net of Lasmo and Fortum acquisitions; F&D costs net of Buy Back (Iran)

Benchmark Group includes BP, ExxonMobil, Shell, Total, ChevronTexaco, ConocoPhillips, – Eni estimates

1.21.2

1.4

1.4

1.2

1.0

0,0

0,5

1,0

1,5

2,0

00-02 01-03 02-04

5.7

6.5

7.3

6.26.35.6

0,0

2,0

4,0

6,0

8,0

10,0

00-02 01-03 02-04

F&D Cost($/boe)

Discovery Cost($/boe)

Proforma Brent 30 $/blReported

0

1

2

3

4

5

6

00-02 '01-03 '02-04

Opex

Lifting Costs($/boe)

4.33.93.8

2.92.7

3.0

0

1

2

3

4

5

6

00-02 01-03 02-04

BenchmarkEni

8

Cash Flow and Free Cash Flow

Cash Flow = Net Income + Exploration expenses + DD&A

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

00-02 '01-03 '02-04

13.4

11.711.8

12.6

10.910.9

3

6

9

12

15

18

00-02 01-03 02-04

International

Domestic & International

Cash Flow($/boe)

Free Cash Flow = Cash Flow - F&D Costs

-5-4-3-2-10123456789

101112131415

00-02 '01-03 '02-04

Free Cash Flow($/boe)

5,85,2

6,1

-5

0

5

10

15

00-02 01-03 02-04

BenchmarkEni

Highlights

Capital Investment

Projects

New Opportunities

Production Trend

9

10

Maintaining a Strong Production Growthkboe/d

1,624

1,187

>1,700

2000 2004 2005 2008

2,000

CAGR

8.2%

>5%

Reference conditions: Brent 30 $/bl 2005, 28 $/bl 2006, 26 $/bl 2007, 25 $/bl 2008

05/08 Growth� Driven by projects

build up and new start-ups

� Portfolio management

05/08 Replac. Ratio� Target >100%

11

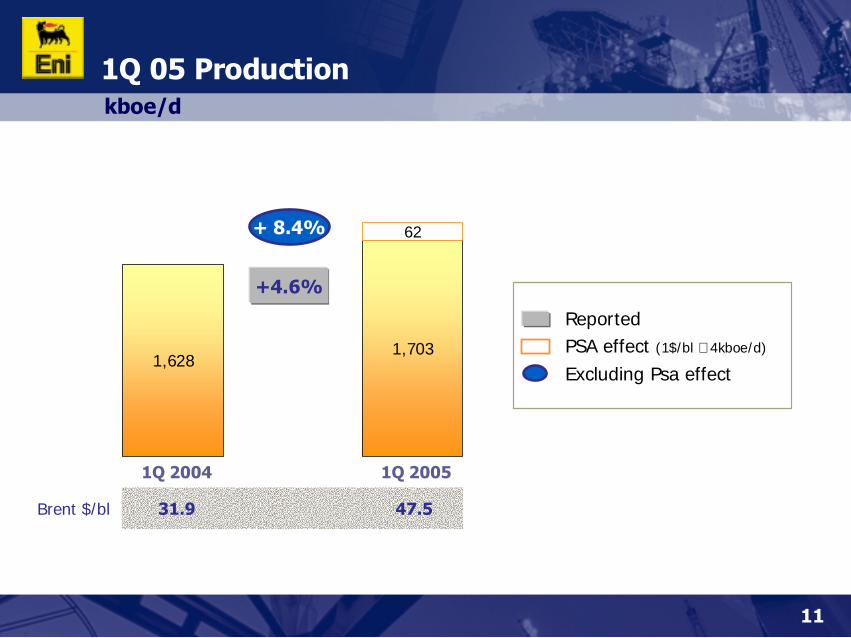

kboe/d

1Q 05 Production

1,7031,628

62

1000

1100

1200

1300

1400

1500

1600

1700

1800

1Q 2004 1Q 2005

+ 8.4%

+4.6%

31.9 47.5Brent $/bl

Reported PSA effect (1$/bl ∼ 4kboe/d)

Excluding Psa effect

12

Selectivity and Operatorship

25

98

7

9 7

59

2000 2004 2008

5%

37%

58%

6%

16%

78%

2004 1,62 mln boe/d 2008 2,00 mln boe/d

≥10030 ÷ 100<30kboe/d

7%

49%

44%

2000 1,19 mln boe/d

N° of producing countries

1560

2200

3100

830

1300

1040

2000 2004 2008

Gross Equity

Operated production(kboe/d)

13

Human Resources for growth

KnowledgeManagement

Processre- engineering

From 1 to 2 Mboe/d relying on

Human Resources

New Model of International ResourceManagement

Resources concerned

Main processes and instruments:

� Identification of strategic resources, definitionof management and development plans

� Change management activities

� Newly graduated hired from 2002: 300

� New types of contracts and innovative compensation schemes

� Eni International Resources Limited: Center for recruitment, development, retention of international resources to be assigned to the Operating Companies

home nationalsexpatriatesinternational staff

14

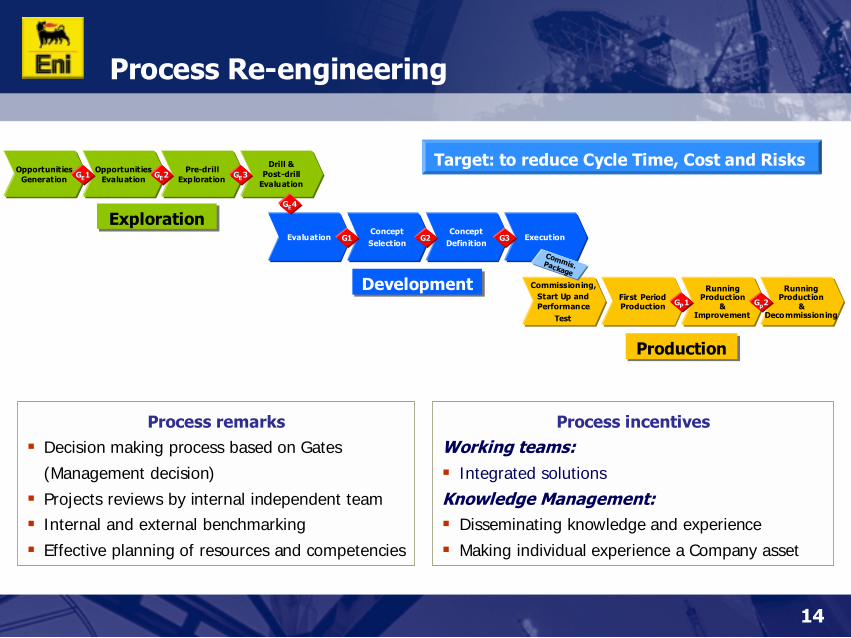

Process Re-engineering

Opportunities Generation

Opportunities Evaluation

Pre-drillExploration

Drill & Post-drill

EvaluationGGEE11 GGEE22 GGEE33

EvaluationConcept Selection

Concept Definition

ExecutionG1G1 G2G2 G3G3

ExplorationExploration

DevelopmentDevelopment Commissioning, Start Up and Performance

Test

First Period Production

Running Production

&Improvement

Running Production

& Decommissioning

GGPP11 GGpp22

ProductionProduction

GGEE44

Commis. Package

Process remarks� Decision making process based on Gates

(Management decision)

� Projects reviews by internal independent team� Internal and external benchmarking

� Effective planning of resources and competencies

Process incentivesWorking teams:� Integrated solutions

Knowledge Management:� Disseminating knowledge and experience

� Making individual experience a Company asset

Target: to reduce Cycle Time, Cost and Risks

Highlights

Production Trend

Projects

New Opportunities

Capital Investment

15

16

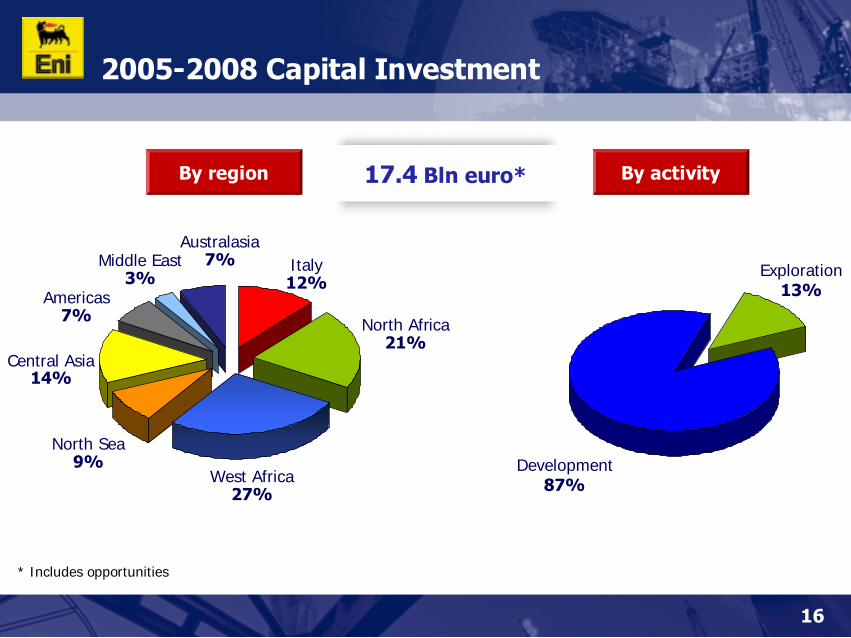

2005-2008 Capital Investment

By region By activity

Exploration13%

Development87%

Italy12%

North Africa 21%

West Africa 27%

North Sea9%

Central Asia14%

Americas7%

Middle East3%

Australasia7%

* Includes opportunities

17.4 Bln euro*

17

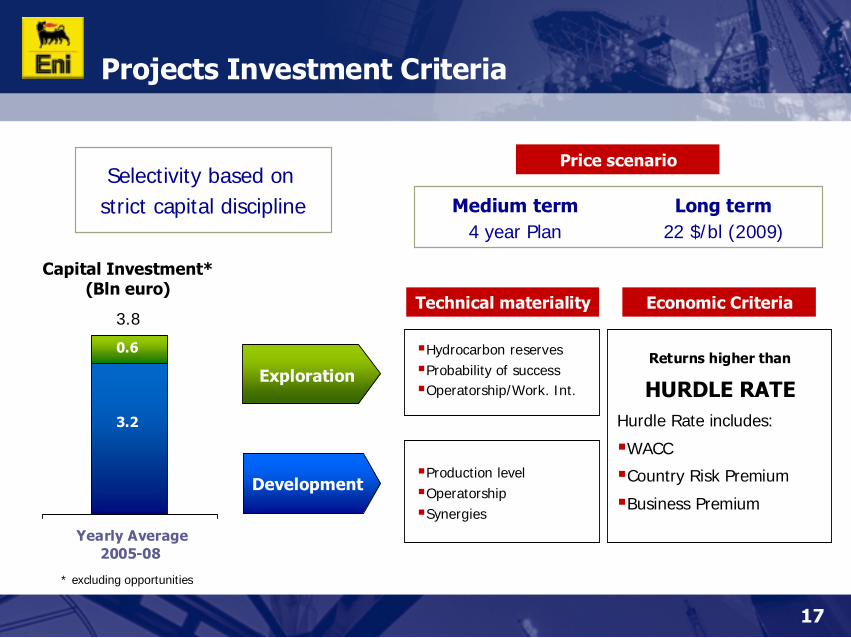

Projects Investment Criteria

Development

Exploration

Yearly Average 2005-08

3.8

Capital Investment*(Bln euro)

0.6

3.2

Technical materiality

�Hydrocarbon reserves�Probability of success �Operatorship/Work. Int.

�Production level�Operatorship�Synergies

Economic Criteria

Returns higher than

HURDLE RATEHurdle Rate includes:

�WACC

�Country Risk Premium

�Business Premium

Selectivity based on strict capital discipline

Price scenario

Medium term Long term4 year Plan 22 $/bl (2009)

* excluding opportunities

18

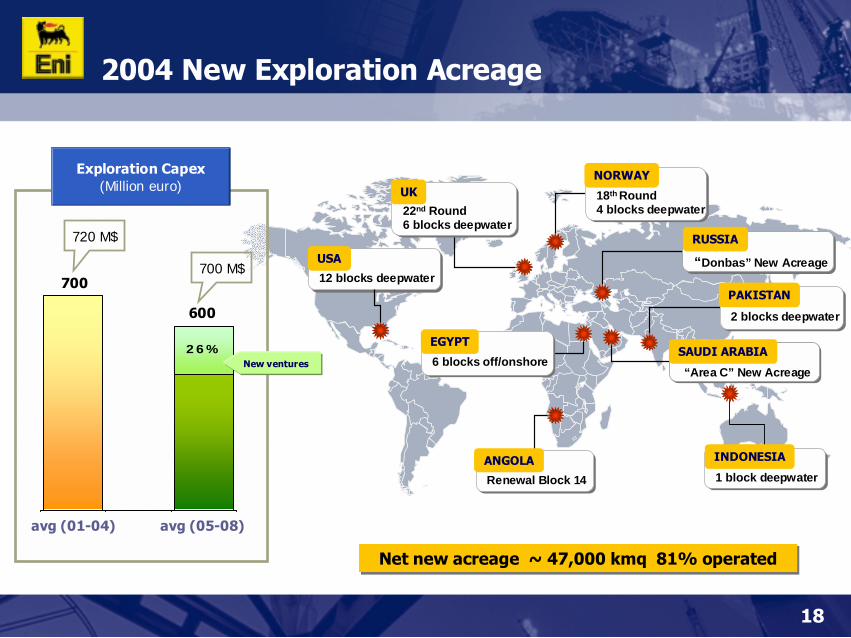

2004 New Exploration Acreage

Net new acreage ~ 47,000 kmq 81% operatedNet new acreage ~ 47,000 kmq 81% operated

6 blocks off/onshore6 blocks off/onshoreEGYPT

12 blocks deepwater12 blocks deepwaterUSA

18th Round4 blocks deepwater18th Round4 blocks deepwater

NORWAY

22nd Round 6 blocks deepwater22nd Round 6 blocks deepwater

UK

2 blocks deepwater2 blocks deepwater

PAKISTAN

Renewal Block 14Renewal Block 14ANGOLA

1 block deepwater1 block deepwaterINDONESIA

“Donbas” New Acreage“Donbas” New Acreage

RUSSIA

“Area C” New Acreage“Area C” New AcreageSAUDI ARABIA26%

0

0

0

0

0

0

0

0

0

0

New ventures

avg (05-08)avg (01-04)

600

720 M$

700 M$

Exploration Capex(Million euro)

700

19

New Acreage in Saudi Arabia – Area C

� “Area C” covers 52,000 square kilometres, located in prolific Rub Al Khali basin

� Eni (50%), Repsol-YPF (30%) and SaudiAramco (20%)

� First exploration period: 5 years

� Concession agreement

� Commercial discoveries of gas developed for domestic market with floor price and take or pay

Aram

co E

aste

rnPr

ovin

ce

Opera

ted

Area

Joint Venture (Shell Op. 40%,

TFE 30% SA 30%)

Gawar oil and gas Field

Rub-Al’Khali

Basin

Shaybah oil Field

20

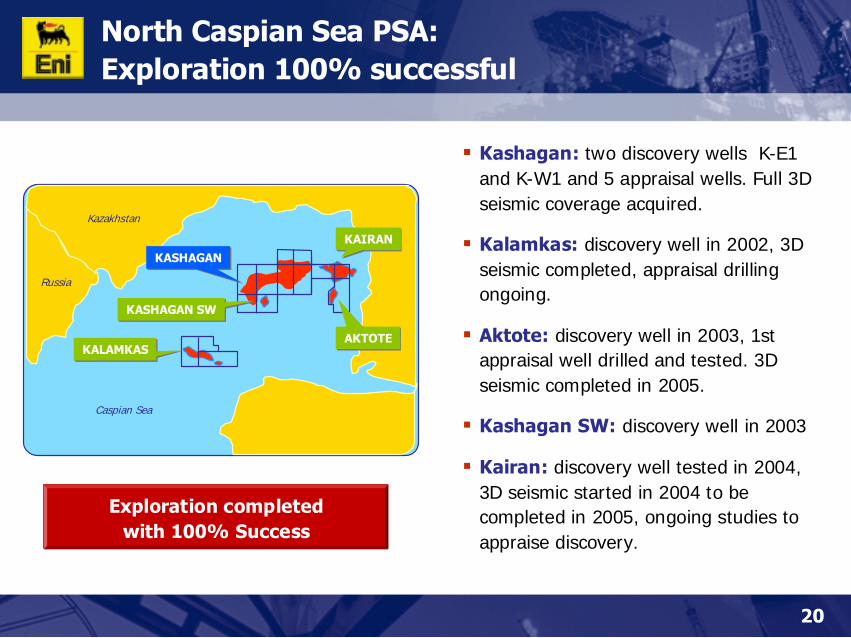

North Caspian Sea PSA: Exploration 100% successful

� Kashagan: two discovery wells K-E1 and K-W1 and 5 appraisal wells. Full 3D seismic coverage acquired.

� Kalamkas: discovery well in 2002, 3D seismic completed, appraisal drillingongoing.

� Aktote: discovery well in 2003, 1st appraisal well drilled and tested. 3D seismic completed in 2005.

� Kashagan SW: discovery well in 2003

� Kairan: discovery well tested in 2004, 3D seismic started in 2004 to becompleted in 2005, ongoing studies toappraise discovery.

Russia

Kazakhstan

Caspian Sea

KASHAGAN SWKASHAGAN SW

KALAMKASKALAMKAS

KAIRANKAIRAN

AKTOTEAKTOTE

KASHAGANKASHAGAN

Exploration completedwith 100% Success

Highlights

Production Trend

Capital Investment

New Opportunities

Projects

21

22

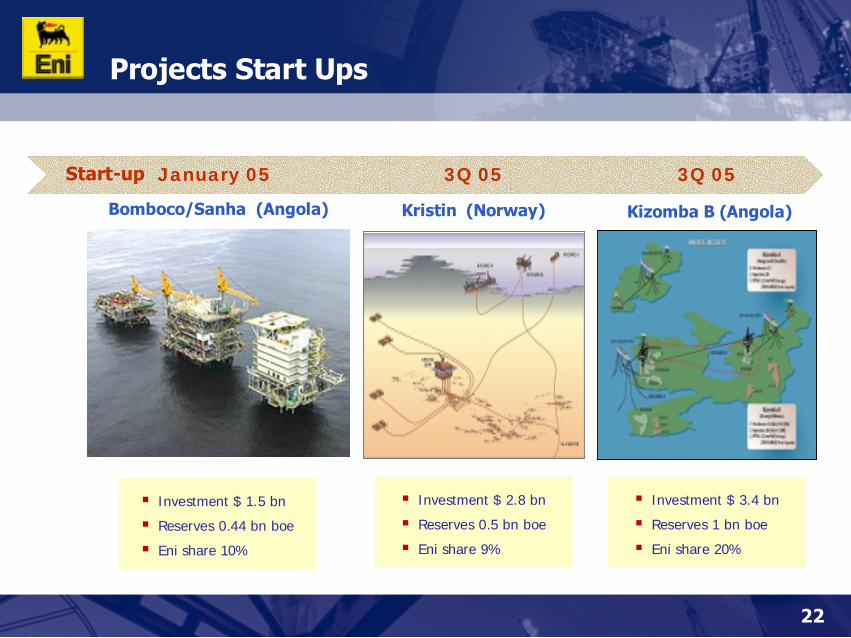

Projects Start Ups

Start-up

Bomboco/Sanha (Angola)

� Investment $ 1.5 bn

� Reserves 0.44 bn boe

� Eni share 10%

January 05

� Investment $ 2.8 bn

� Reserves 0.5 bn boe

� Eni share 9%

Kristin (Norway)

3Q 05

Kizomba B (Angola)

� Investment $ 3.4 bn

� Reserves 1 bn boe

� Eni share 20%

3Q 05

23

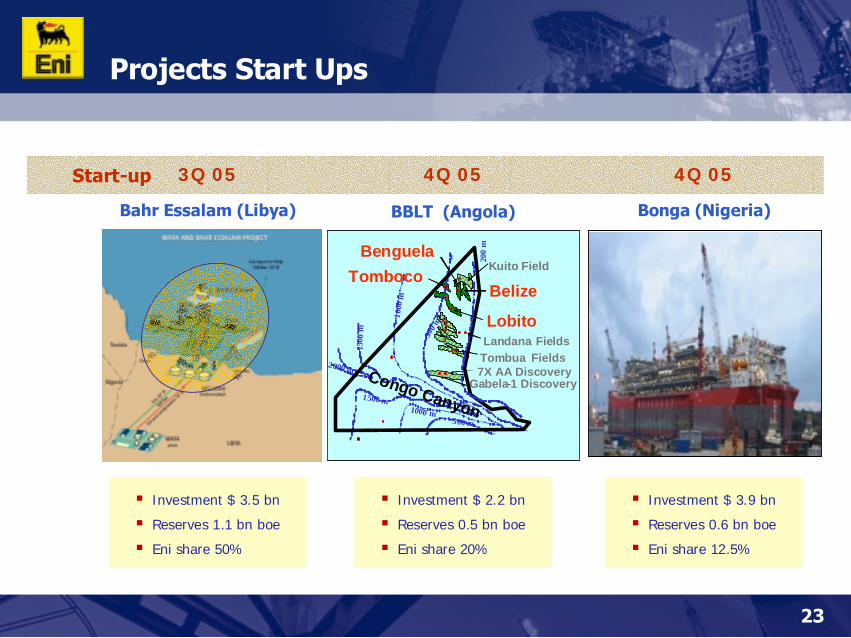

Projects Start Ups

� Investment $ 3.9 bn

� Reserves 0.6 bn boe

� Eni share 12.5%

Bonga (Nigeria)

� Investment $ 3.5 bn

� Reserves 1.1 bn boe

� Eni share 50%

Bahr Essalam (Libya)

3Q 05 4Q 05Start-up

Bahr Essalam

BBLT (Angola)

� Investment $ 2.2 bn

� Reserves 0.5 bn boe

� Eni share 20%

4Q 05

2000 m15

0 0 m

1500 m10

00 m

1000 m50

0 m500 m

200

m

Congo Canyon

Lobito

Belize

Tombua Fields7X AA Discovery

BenguelaKuito Field

Tomboco

Landana Fields

Gabela-1 Discovery

2000 m15

0 0 m

1500 m10

00 m

1000 m50

0 m500 m

200

m

Congo Canyon

Lobito

Belize

Tombua Fields7X AA Discovery

BenguelaKuito Field

Tomboco

Landana Fields

Gabela-1 Discovery

24

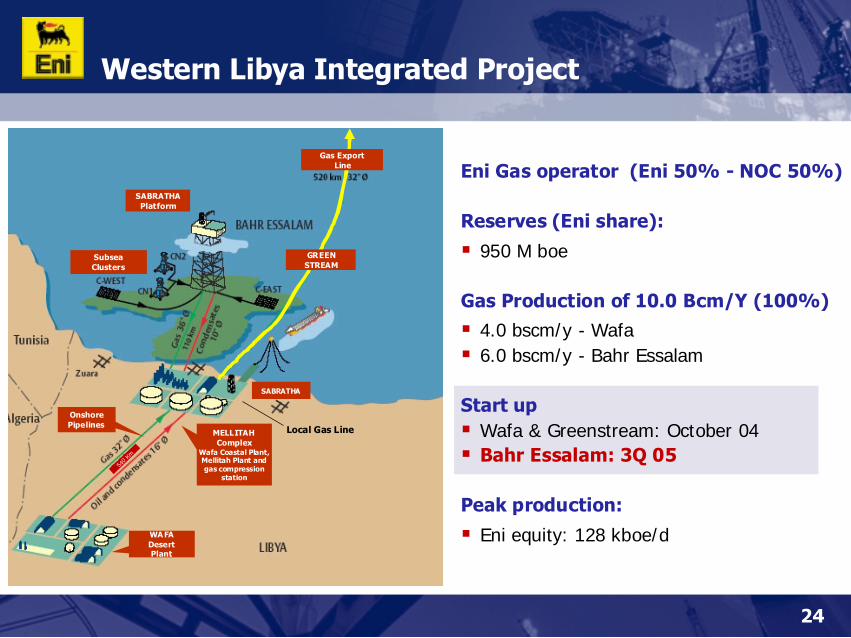

Western Libya Integrated Project

Eni Gas operator (Eni 50% - NOC 50%)

Reserves (Eni share):

� 950 M boe

Gas Production of 10.0 Bcm/Y (100%)� 4.0 bscm/y - Wafa� 6.0 bscm/y - Bahr Essalam

Start up� Wafa & Greenstream: October 04� Bahr Essalam: 3Q 05

Peak production:

� Eni equity: 128 kboe/d

Local Gas Line

540 K

m

Onshore Pipelines

WA FADesert Plant

MELLITAHComplex

Wafa Coastal Plant, Mellitah Plant and gas compression

station

SABRATHA

SABRATHAPlatform

SubseaClusters

Gas Export Line

GREEN STREAM

25

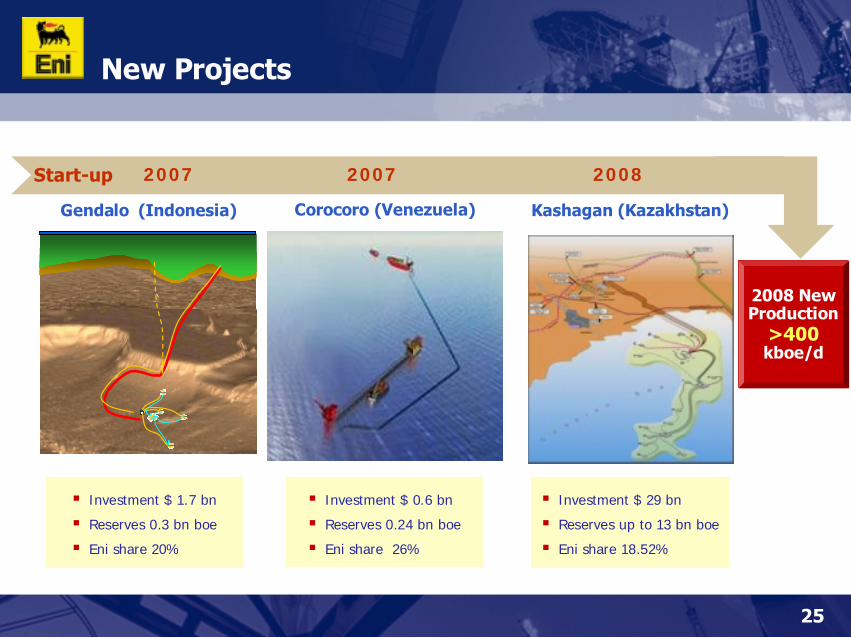

New Projects

2007 2008Start-up

� Investment $ 29 bn

� Reserves up to 13 bn boe

� Eni share 18.52%

Kashagan (Kazakhstan)

� Investment $ 0.6 bn

� Reserves 0.24 bn boe

� Eni share 26%

Corocoro (Venezuela)

2008 New Production

>400kboe/d

� Investment $ 1.7 bn

� Reserves 0.3 bn boe

� Eni share 20%

Gendalo (Indonesia)

2007

26

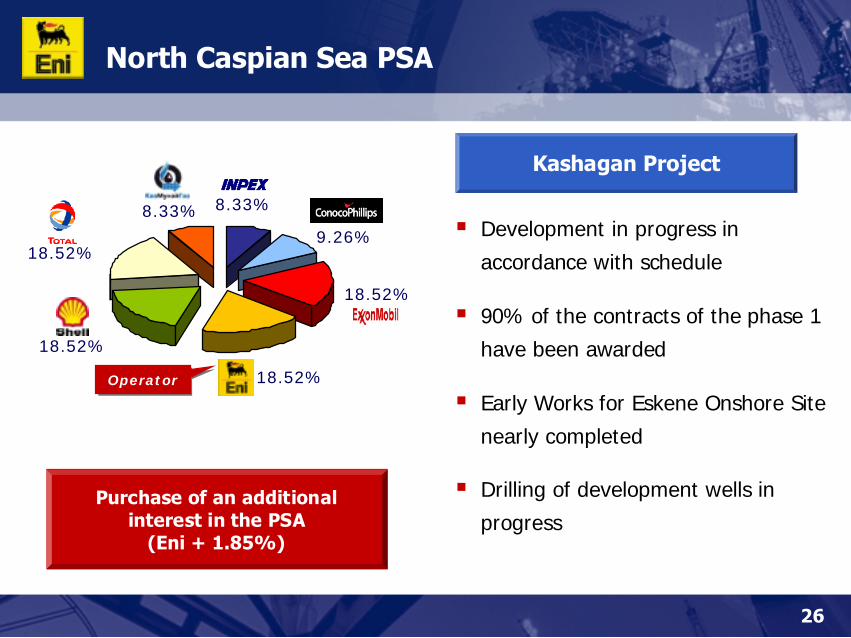

North Caspian Sea PSA

Purchase of an additional interest in the PSA

(Eni + 1.85%)

OperatorOperator 18.52%

18.52%

9.26%

8.33%

18.52%

18.52%

8.33%� Development in progress in

accordance with schedule

� 90% of the contracts of the phase 1

have been awarded

� Early Works for Eskene Onshore Site

nearly completed

� Drilling of development wells in

progress

Kashagan Project

27

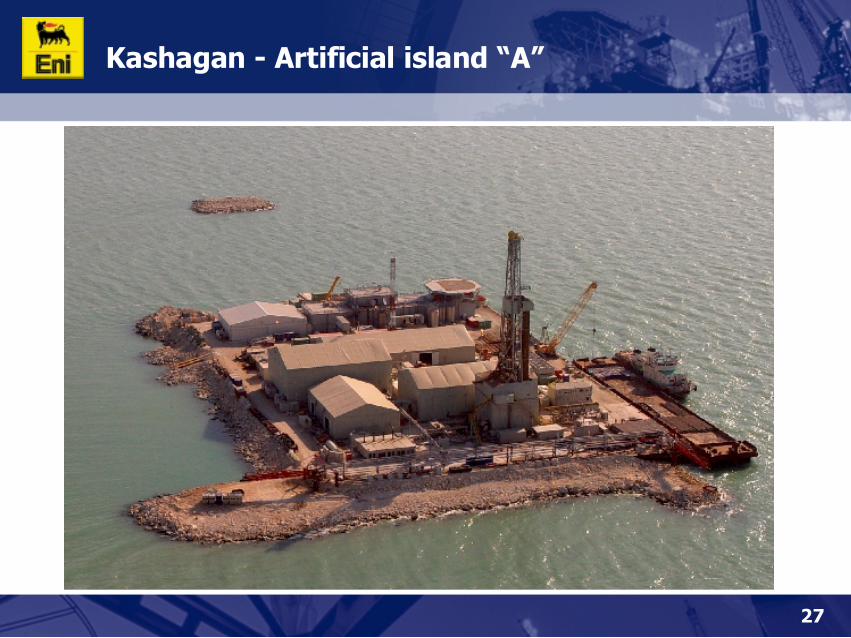

Kashagan - Artificial island “A”

28

Kashagan - Onshore Early Works Progress

29

Kashagan - Export Alternatives

Iraq

CaspianSea

KASHAGANKASHAGAN

Samara Samara

Turkey

Uzbekistan

Kazakhstan

Russia

Iran

Georgia

Ukraine

Moldavia

Poland

Turkmenistan

Azerbaijan

CeyhanCeyhan

BTC (1st lifting expected October 2005)BTC (1st lifting expected October 2005)

TbilisiTbilisi

BakuBaku

AtyrauAtyrau

NovorossiyskNovorossiysk

CPCCPC

To Novorossiysk (a Bosphorusbypass is required)

To Novorossiysk (a Bosphorusbypass is required) AktauAktau

To AktauTo Aktau

Trans-Caspian ShippingTrans-Caspian Shipping

To ChinaTo China

To Baltic SeaTo Baltic Sea

ExistingFuture alternatives

Selection by early 2006

MakhachkalaMakhachkala

Highlights

Production Trend

Capital Investment

Projects

New Opportunities

30

31

New opportunities

� Access to large oil reservesMiddle East

� Development of existing resourcesCentral Asia

� Non conventional oilleveraging on technological know-howCanada, Venezuela and others

� Gas integrated projectsFar East, Mediterranean, West Africa

32

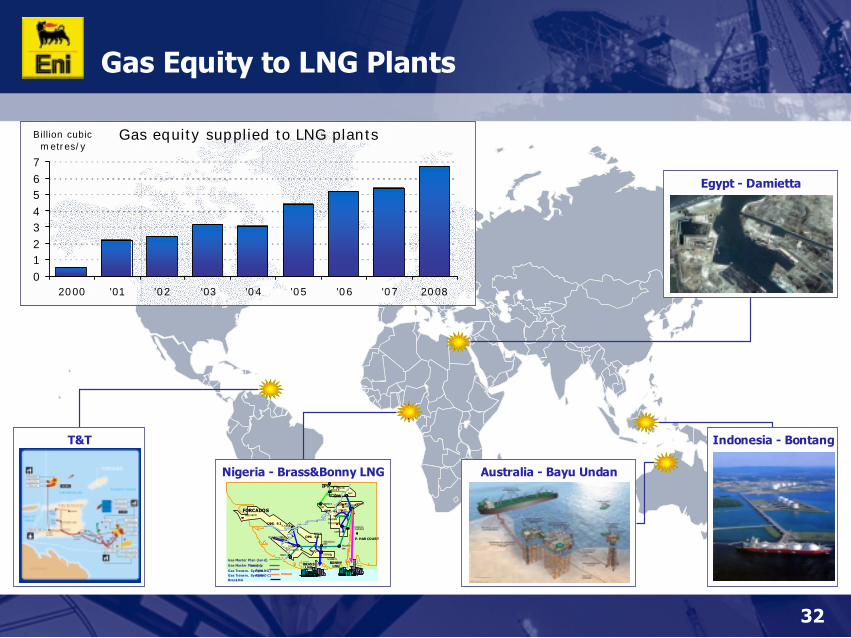

Gas Equity to LNG Plants

Gas equity supplied to LNG plants

01234567

2000 '01 '02 '03 '04 '05 '06 '07 2008

Billion cubic metres/y

Nigeria - Brass&Bonny LNG

TEBIDABA OBAMA

OKPAI

OML 61

MBEDE

EBEGORO

IDUSAMABRI

KWALE

CLOUGH CREEK

OML 6 2

OML 6 3

TUOMO W

ISOKO S. UMUORU

TAYLOR CR.

BENIKU

OGBOGENE

OMOKU W

TUOMO

PIRIGBENE

NIMBE S

AZUZUAMA

ASHAKA

OBIAFU

SAMABRI E.

EBOCHA

OML 6 0

OBRIKOMIRRI

OGBAINBIRI

BENIBOYE

OSHI

EMETTE

EKEDEI

ASEMOKE

AJAKETON

MANUSO

BRAS SBRAS SLNGLNG

FORCADOSFORCADOS

AKRI

OGODAmanifold

YENAGOAtie-in

ENWHEtie-in

BONNYBONNYLNGLNG

IPPIPP

Gas Master Plan (lan d)

Gas Master Plan (swamp)

Gas Transm. System 1 (N-LNG)Gas Transm. System 4 (NAO C)BrassLNG

P. HAR COURT

T&T Indonesia - Bontang

Australia - Bayu Undan

Egypt - Damietta

33

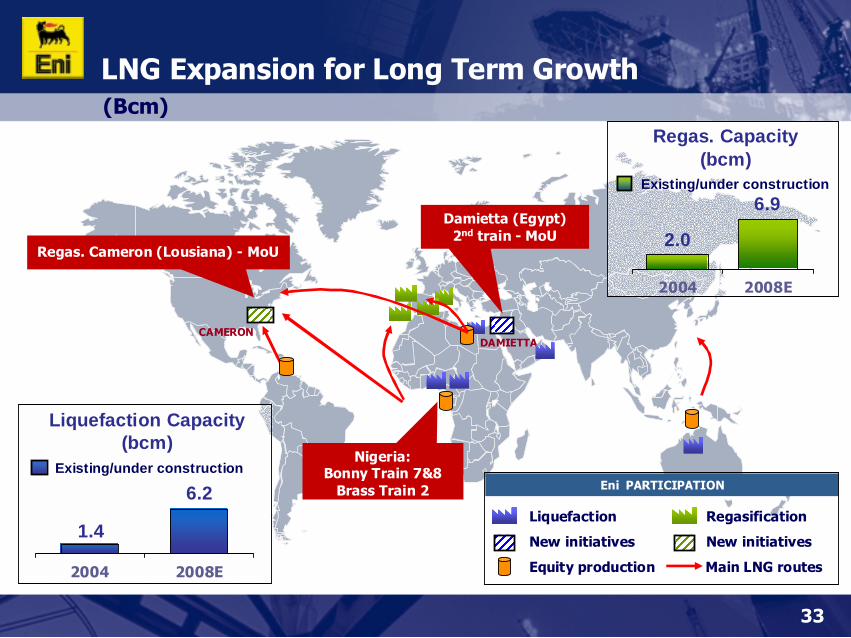

(Bcm)

LNG Expansion for Long Term Growth

DAMIETTA

Regas. Cameron (Lousiana) - MoU

CAMERON

2004 2008E

Liquefaction Capacity(bcm)

1.4

6.2Existing/under construction

Eni PARTICIPATION

Liquefaction Regasification

New initiatives New initiatives

Equity production Main LNG routes

Damietta (Egypt) 2nd train - MoU

Nigeria:Bonny Train 7&8

Brass Train 2

2.0

6.9

Regas. Capacity(bcm)

Existing/under construction

2004 2008E

34

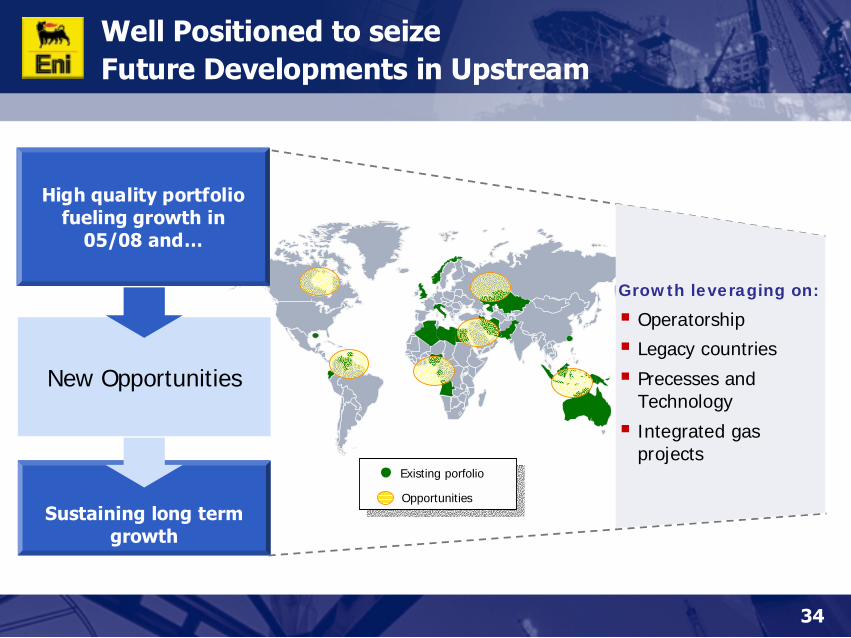

Well Positioned to seizeFuture Developments in Upstream

Sustaining long term growth

New Opportunities

Existing porfolio

Opportunities

High quality portfolio fueling growth in

05/08 and…

Growth leveraging on:

� Operatorship

� Legacy countries

� Precesses and Technology

� Integrated gas projects

E&P Business TrendCSFB Oil & Gas Conference

London, June 8th, 2005

A. BelottiSenior Vice PresidentE&P Business Planning

![CSFB OG Industry Primer[1]](https://img.pdfslide.us/doc/110x75/577ccf8d1a28ab9e789003f4/csfb-og-industry-primer1.jpg)