Embed Size (px)

Citation preview

Chapter 4Accounting for

Deposits Department

Ibrahim Sammour

DepositsThe bank dose not work in it is capital only, but even with the amounts from others (Deposits), the bank is paying interest on these deposits.

DepositsDeposit is Money given in advance to show intention to complete the purchase of a property.OR Money transferred into a customer's account at a financial institution.

Kinds of deposits:

1- A Current account .2- Notice deposits .3- Time deposits .4- Savings deposits .5- Certificate of deposit.

1 -A Current account is a deposit account held at a bank or

other financial institution, for the purpose of securely and quickly providing frequent access to funds on demand, through a variety of different channels. Because money is available on demand these accounts are also referred to as o cm a no accounts or demand deposit accounts.

1 -A Current account Current accounts in the bank opening of

current accounts to customers for the purpose of depositing their money in cash, cheques, or transfer, and against the Bank is developing systems that enable these clients to withdraw from these amounts usually do not pay interest. Also, they may restrict or impose additional fees for excessive activity.

1 -A Current account

It is usually the agreement between the bank and the customer to open a current account by signing a request to open the account (account opening form) and update the documents and papers necessary to do so.

1 -A Current account To regulate this process opening

bank account records reflect serial number that gives a figure of the current account of the customer, restrict the left side of the amounts deposited in the account, and limit on the right side of withdrawals by the customer on the account. The difference between them is a balance of the account.

1 -A Current account

The process of opening accounts as a contract between the client and the bank, and the relationship between them is the relationship of (creditor and debtor).

2 -Notice deposits:

This kind of deposits means that the customer can withdraw only by giving advanced notice (such like a week) and the bank will pay interest on this kind of deposits.

3 -Time deposits:

Time deposit is money deposit at a banking institution that cannot be withdrawn for a certain "term" or period of time. When the term is over it can be withdrawn or it can be held for another term

4 -Savings deposits:

Accounts that pay interest and can be withdrawn upon demand are offered by banks, credit unions, and Savings and Loans.

5 -Certificate of deposit

Receipt issued by a depository institution (such as a bank, credit union, or a finance or insurance company) to a depositor who opens a certificate account or time deposit account.

5 -Certificate of deposit

Issued in a negotiable or non-negotiable form, it states the:

(1) amount deposited, (2) rate of interest, (3) minimum period for which the

deposit should be maintained without incurring early withdrawal penalties.

Financial transactions for the deposits department:

1- Deposits:

Treasury *** Time /Savings/Note ***

Financial transactions for the deposits department:

2- Drawings:

Time/Savings/Note *** Treasury ***

Financial transactions for the deposits department:

3- A- Transferring to deposits from current account:

Current Account *** Time /Savings/Note ***

Financial transactions for the deposits department:

B-Transferring from deposits to current account:

Time /Savings/Note *** Current Account ***

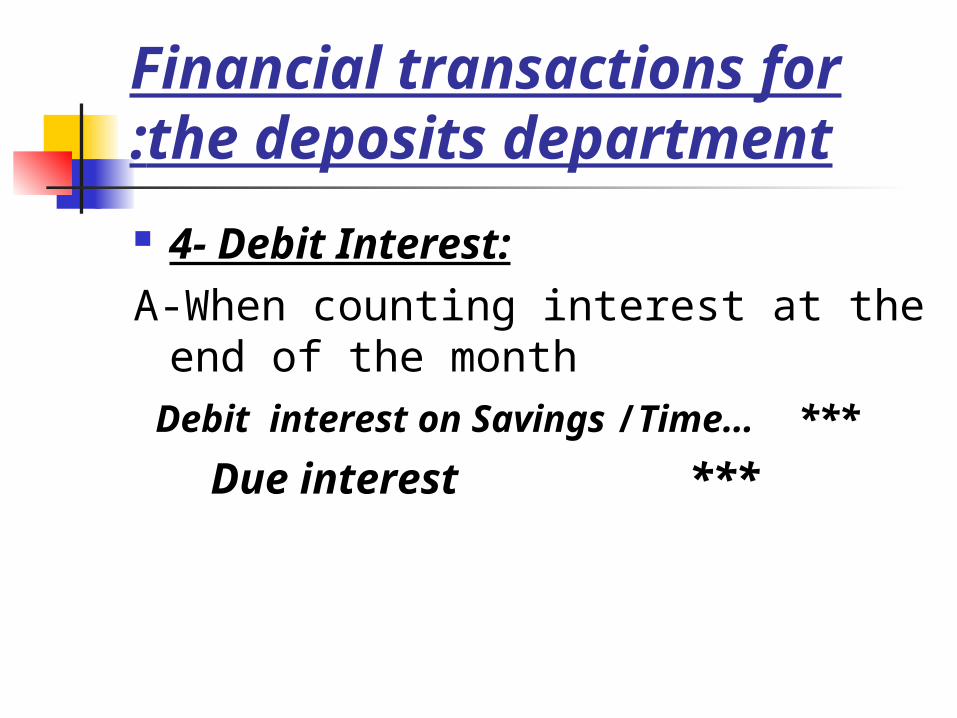

Financial transactions for the deposits department:

4- Debit Interest:A-When counting interest at the end

of the month Debit interest on Savings /Time…

***

Due interest ***

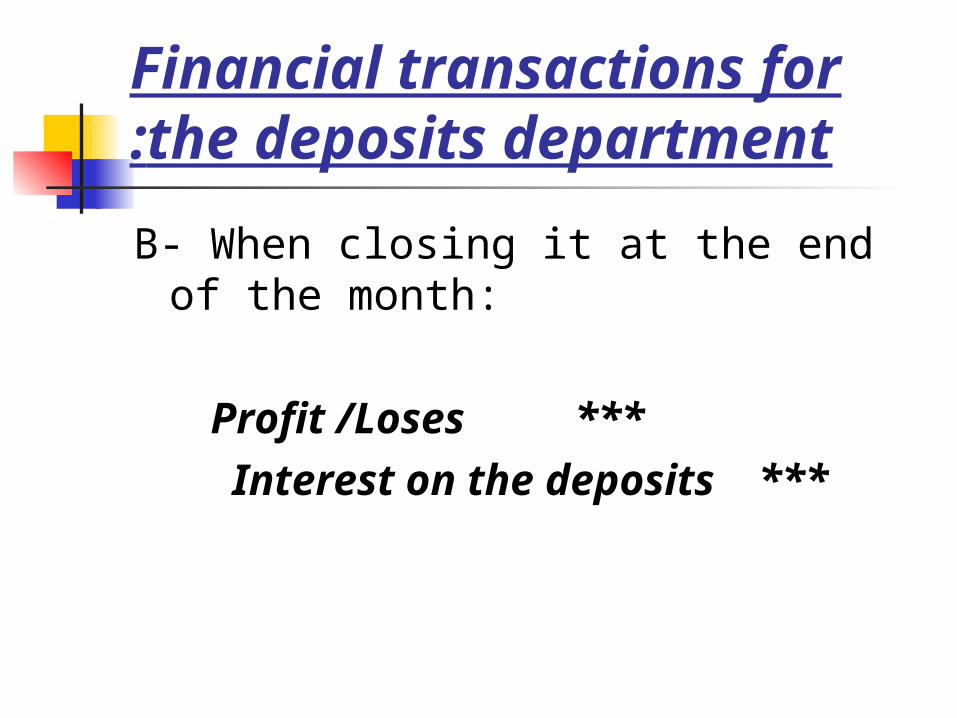

Financial transactions for the deposits department:

B- When closing it at the end of the month:

Profit /Loses *** Interest on the deposits

***

Financial transactions for the deposits department:

C- At the end of each month, the interest due amount must be closed, and then the interests will be added to deposits, or be transferred to current account, or be paid in cash.

Due interest *** Deposits ***OR Current account ***OR Treasury ***

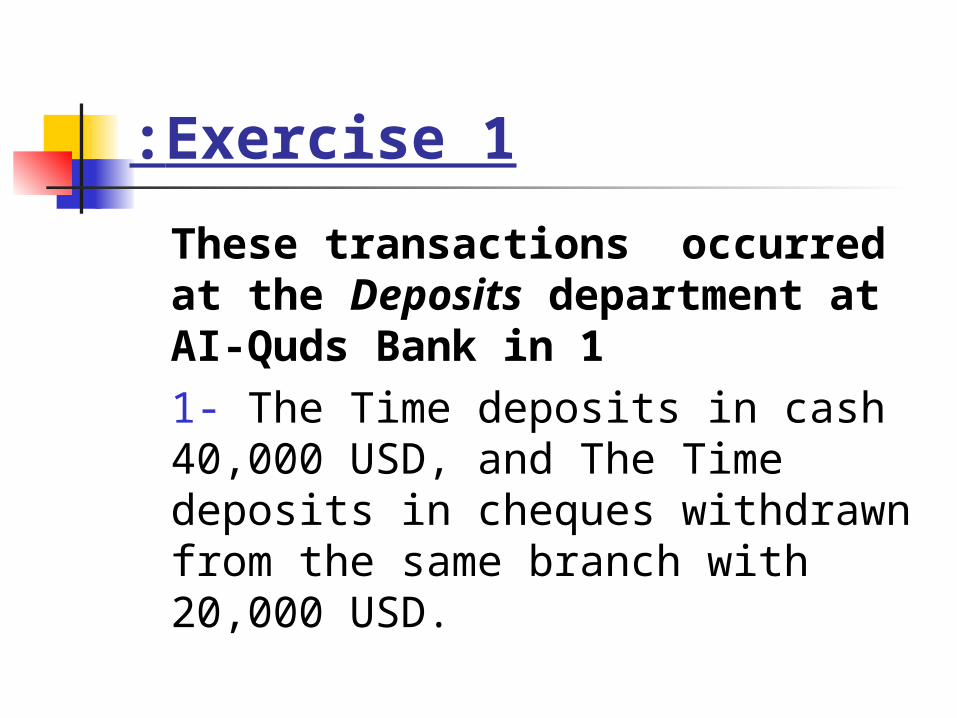

Exercise 1:

These transactions occurred at the Deposits department at AI-Quds Bank in 11- The Time deposits in cash 40,000 USD, and The Time deposits in cheques withdrawn from the same branch with 20,000 USD.

Exercise 1:

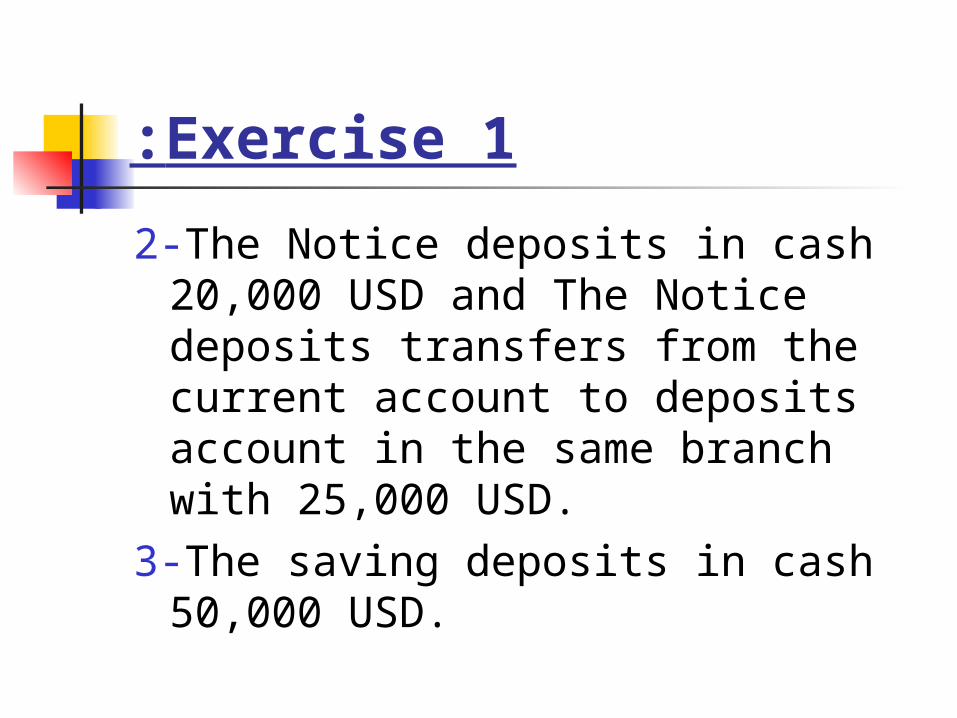

2-The Notice deposits in cash 20,000 USD and The Notice deposits transfers from the current account to deposits account in the same branch with 25,000 USD.

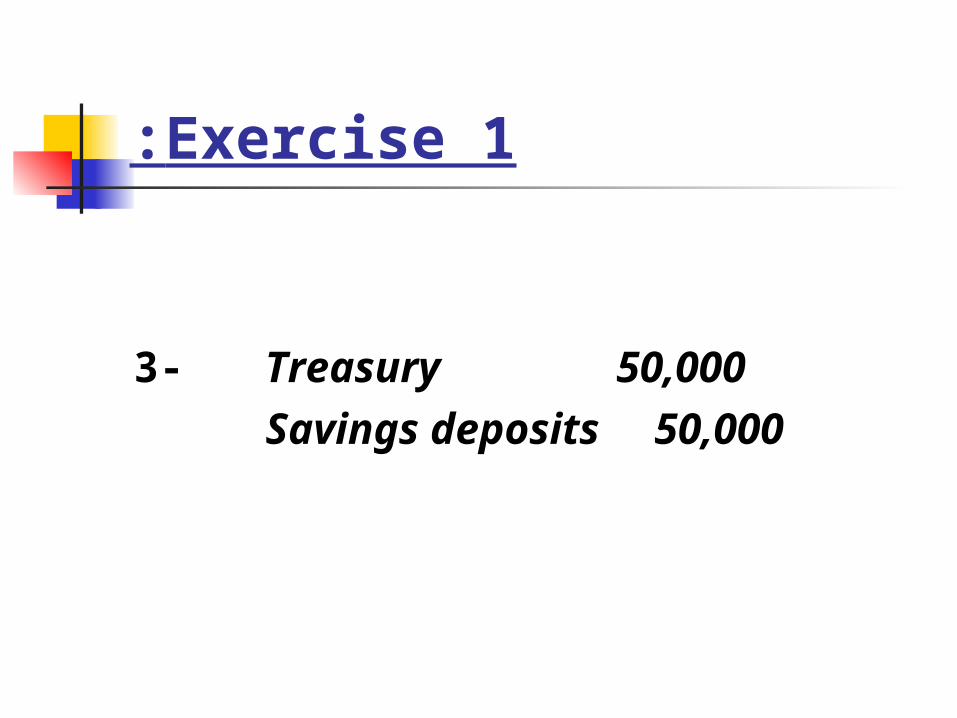

3-The saving deposits in cash 50,000 USD.

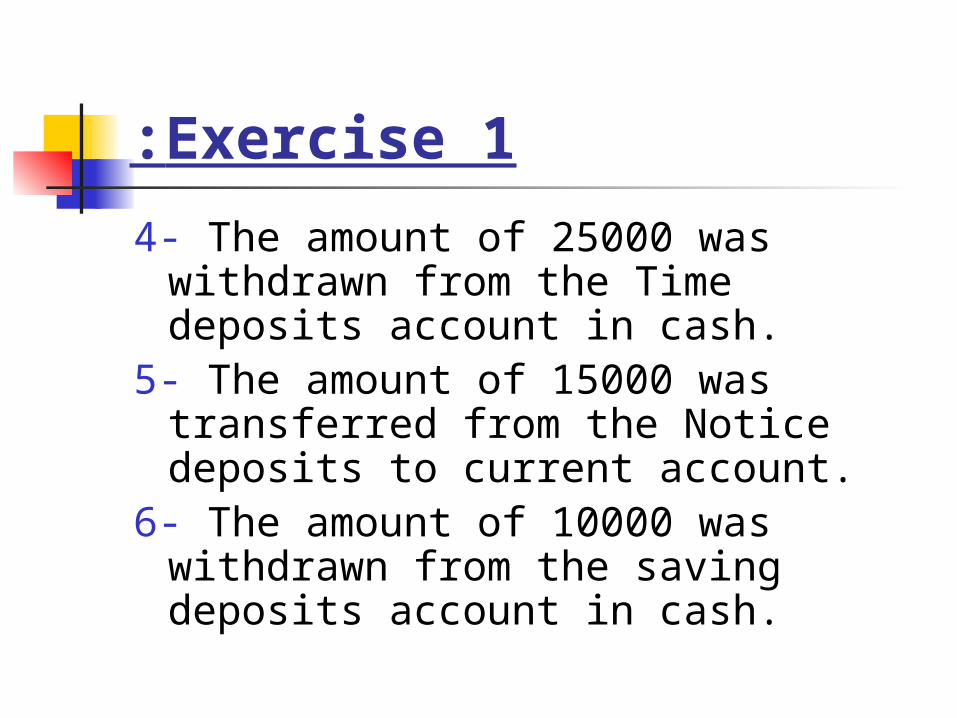

Exercise 1:

4- The amount of 25000 was withdrawn from the Time deposits account in cash.

5- The amount of 15000 was transferred from the Notice deposits to current account.

6- The amount of 10000 was withdrawn from the saving deposits account in cash.

Exercise 1:

Required:Recording the central journal

entries.

Exercise 1:

1- Treasury 40,000 Current accounts 20,000 Time deposits

60,000

Exercise 1:

2- Treasury 20,000 Current accounts 25,000 Notice deposits

45,000

Exercise 1:

3- Treasury 50,000 Savings deposits

50,000

Exercise 1:

4- Time deposits 25,000 Treasury 25,000

Exercise 1:

5- Notice deposits 15,000 Current accounts

15,000

Exercise 1:

6- Savings deposits 10,000 Treasury

10,000

Exercise 2:

In 1-5-2007, 10000 $ deposit was locked in AI-Quds Bank , for sex month with interest 5%, and this deposit relocked every sex month.

Required:Recording the central journal

entries.

Exercise 2:

Treasury 10,000 Time deposits 10,000

Exercise 2:

Debit interest on Time deposits 250

Time deposits 250

5x6x10000 100x12

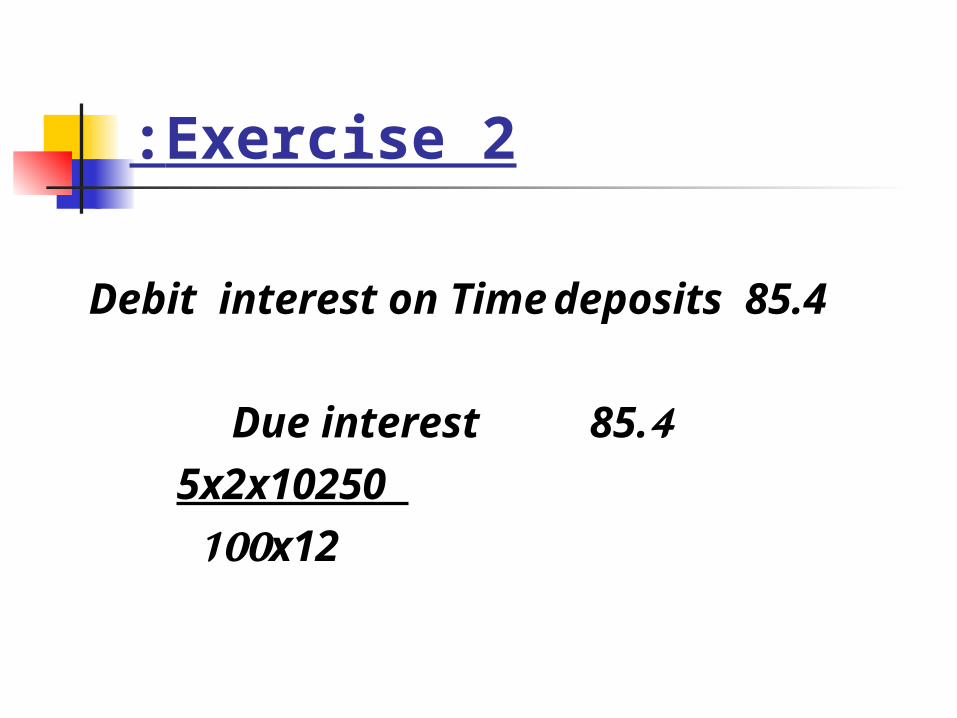

Exercise 2:

Debit interest on Time deposits 85.4

Due interest 85.4 5x2x10250 100x12

Exercise 2:

Debit interest 170.8

Due interest 85.4 Time deposits

256.2 5x4x10250 100x12 =170.8