Embed Size (px)

Citation preview

CANADA’S INTERMEDIATE GOLD PRODUCER

2018 PDAC Convention and Investors Exchange March 4-7, 2018 – Toronto, ON

2

This presentation contains certain forward-looking information and forward-looking statements, as defined in applicable securities laws (collectively referred to herein as “forward-

looking statements”). Forward-looking statements relate to future events or future performance and reflect current expectations or beliefs regarding future events and include, but

are not limited to, statements with respect to: (i) the amount of mineral resources and mineral reserves and exploration targets; (ii) the amount of future production over any period;

(iii) net present value and internal rates of return of mining operations; (iv) assumptions relating to recovered grade, average ore recovery, internal dilution, mining dilution and other

mining parameters set out in the technical reports, studies and disclosure of the Company; (v) assumptions relating to revenues, operating cash flow and other revenue metrics set

out in the Company’s disclosure materials; (vi) mine expansion potential and expected mine life; (vii) expected time frames for completion of permitting and regulatory approvals;

(viii) future capital and operating expenditures; (ix) future exploration plans; (x) future gold prices; and (xi) sources of and anticipated financing requirements. All statements other

than statements of historical fact are forward-looking statements. Often, but not always, forward-looking statements can be identified by the use of words such as “plans”, “expects”,

“is expected”, “budget”, “scheduled”, “estimates”, “continues”, “forecasts”, “projects”, “predicts”, “intends”, “anticipates”, “targets”, or “believes”, or variations of, or the negatives of,

such words and phrases or state that certain actions, events or results “may”, “could”, “would”, “should”, “might” or “will” be taken, occur or be achieved. Forward-looking statements

involve known and unknown risks, uncertainties and other factors, which may cause actual results to differ materially from those anticipated in such forward-looking statements. The

forward-looking statements in this presentation speak only as of the date of this presentation or as of the date or dates specified in such statements.

Forward-looking statements involve known and unknown risks, uncertainties and other factors which are beyond Detour Gold's ability to predict or control and may cause Detour

Gold's actual results, performance or achievements to be materially different from any of its future results, performance or achievements expressed or implied by forward-looking

statements. These risks, uncertainties and other factors include, but are not limited to, gold price volatility, changes in debt and equity markets, the uncertainties involved in

interpreting geological data, risks relating to variations in recovered grades and mining dilution, variations in rates of recovery, changes or delays in mining development and

exploration plans, the success of mining, development and exploration plans, changes in project parameters, risks related to the receipt of regulatory approvals, increases in costs,

environmental compliance and changes in environmental legislation and regulation, interest rate and exchange rate fluctuations, general economic conditions and other risks

involved in the gold exploration and development industry, as well as those risk factors discussed in the section entitled "Description of Business - Risk Factors" in Detour Gold's

2016 AIF and in the continuous disclosure documents filed by Detour Gold on and available on SEDAR at www.sedar.com. Such forward-looking statements are also based on a

number of assumptions which may prove to be incorrect, including, but not limited to, assumptions about the following: the availability of financing for exploration and development

activities; operating and capital costs; the Company's ability to attract and retain skilled staff; the mine development and production schedule and related costs, dilution control;

sensitivity to metal prices and other sensitivities; the supply and demand for, and the level and volatility of the price of, gold; timing of the receipt of regulatory and governmental

approvals for development projects and other operations; the timing and results of consultations with the Company’s Aboriginal partners; the supply and availability of consumables

and services; the exchange rates of the Canadian dollar to the U.S. dollar; energy and fuel costs; required capital investments; estimates of net present value and internal rate of

returns; the accuracy of reserve and resource estimates, production estimates and capital and operating cost estimates and the assumptions on which such estimates are based;

market competition; ongoing relations with employees and impacted communities and general business and economic conditions. Accordingly, readers should not place undue

reliance on forward-looking statements.

The forward-looking statements contained herein are made as of the date hereof, or such other date or dates specified in such statements.

Detour Gold undertakes no obligation to update publicly or otherwise revise any forward-looking statements contained herein whether as a result of new information or future events

or otherwise, except as may be required by law. If the Company does update one or more forward-looking statements, no inference should be drawn that it will make additional

updates with respect to those or other forward-looking statements.

Forward Looking Information

All monetary amounts are in U.S. dollars unless otherwise stated.

3

Notes to Investors Non-IFRS Financial Performance Measures The Company has included non-IFRS measures in this presentation: total cash costs and all-in sustaining costs. The Company believes that these measures, in addition to

conventional measures prepared in accordance with IFRS, provide investors an improved ability to evaluate the underlying performance of the Company. The non-IFRS

measures are intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with

IFRS. These measures do not have any standardized meaning prescribed under IFRS, and therefore may not be comparable to other issuers. Other companies may calculate

these measure differently.

Detour Gold reports total cash costs on a sales basis. Total cash costs include production costs such as mining, processing, refining and site administration, agreements with

Aboriginal communities, less non-cash share-based compensation and net of silver sales divided by gold ounces sold to arrive at total cash costs per gold ounce sold. The

measure also includes other mine related costs incurred such as mine standby costs and current inventory write downs. Production costs are exclusive of depreciation and

depletion. Production costs include the costs associated with providing the royalty in kind ounces.

The Company believes the measure all-in sustaining costs more fully defines the total costs associated with producing gold. The Company calculates all-in sustaining costs as

the sum of total cash costs (as described above), share-based compensation, corporate general and administrative expense, exploration and evaluation expenses that are

sustaining in nature, reclamation cost accretion, sustaining capital including deferred stripping, and realized gains and losses on hedges due to operating and capital costs, all

divided by the gold ounces sold to arrive at a per ounce figure.

Costs excluded from all-in sustaining costs are non-sustaining capital expenditures and exploration costs that are expected to materially increase production, financing costs

and tax expense. Consequently, this measure is not representative of all of the Company’s cash expenditures. In addition, the calculation of all-in sustaining costs does not

include depreciation and depletion expense as it does not reflect the impact of expenditures incurred in prior periods.

Detour Gold reports total site costs and total site costs per ounce on a sales basis. Total site costs include production and operating costs such as mining, processing, site

general and administration, bullion shipment, refining, agreements with Aboriginal communities, capital costs (including closure costs) and net of silver sales. The Company

calculates total site costs per ounce as the sum of total site costs (as described above) divided by the total gold ounces sold. Gold ounces produced is noted before delivering

the royalty in kind ounces.

IFRS Measures The Company has included IFRS measure in this presentation: Free cash flow before financing activities, which is calculated as cash flow from operations less cash flow from

investing activities. It provides useful information to management and investors as an indicator of the cash generated from the Company’s operations before consideration of

how those activities are financed.

Qualified Persons

The scientific and technical content of this presentation was reviewed, verified and approved by Drew Anwyll, P.Eng., Senior Vice President Technical Services, a Qualified

Person as defined by Canadian Securities Administrators National Instrument 43-101 “Standards of Disclosure for Mineral Projects”.

All monetary amounts are in U.S. dollars unless otherwise stated.

4

DGC Investment Thesis

Unmatched combination of long

life and large production profile

Competitive cost profile

relative to industry peers

Production growth

Top-ranked jurisdiction

Strong exploration potential

4

5

OPERATIONS GROWTH BALANCE SHEET

Mine and mill optimization

Organic growth Continue debt reduction

Realize on economies of scale

Add value with Zone 58N Early-stage project acquisition/JV

Maintain capital discipline Shareholder returns

Gold Production (K oz)

DGC Strategic Focus

232

457 506 538 571

600- 650

2013 2014 2015 2016 2017 2018E

6

2017 Highlights¹

PRODUCTION

571 K OZ gold

COSTS FINANCIALS

$716

$1,065

TCC²

/oz sold

AISC²

/oz sold

$134 million

$166

CASH BALANCE

million

ACHIEVED ANNUAL GUIDANCE

GENERATED STRONG FREE CASH FLOW2 OF $ 115 M

100.1 MT mined

21.4 MT milled

1. All 2017 numbers are preliminary figures, unaudited and subject to final adjustment.

2. Refer to the section on IFRS Performance Measures on slide 3.

3. Includes Letters of Credit.

NET DEBT³

6

7

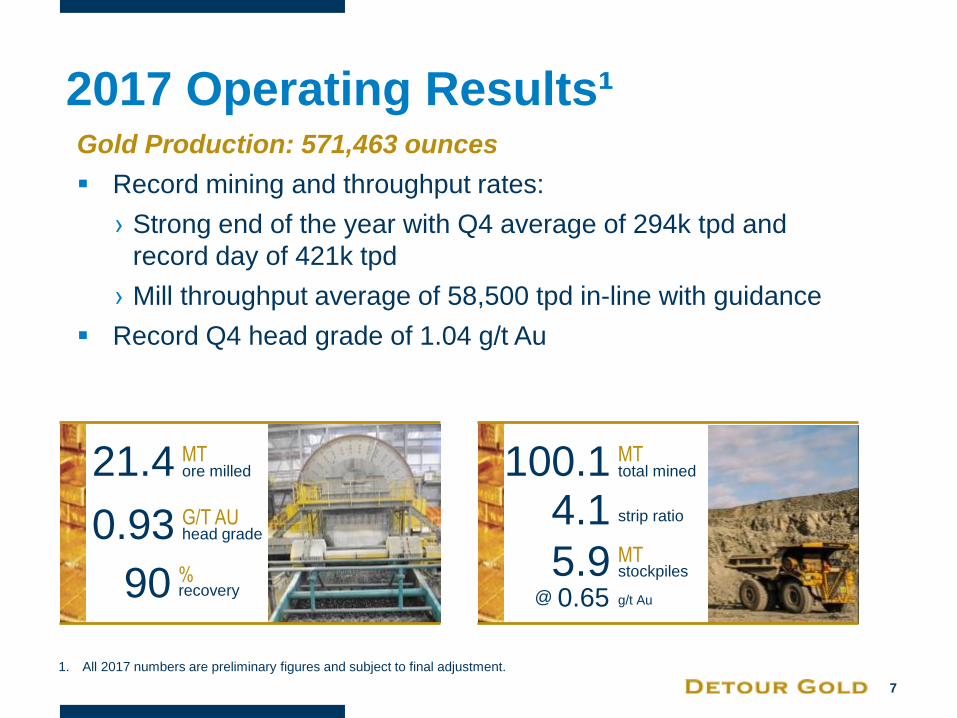

2017 Operating Results¹

total mined 100.1 MT

4.1 strip ratio

MT ore milled

0.93 G/T AU head grade

% recovery

21.4

90

Gold Production: 571,463 ounces

Record mining and throughput rates:

› Strong end of the year with Q4 average of 294k tpd and

record day of 421k tpd

› Mill throughput average of 58,500 tpd in-line with guidance

Record Q4 head grade of 1.04 g/t Au

5.9 stockpiles MT

g/t Au @ 0.65

1. All 2017 numbers are preliminary figures and subject to final adjustment.

8

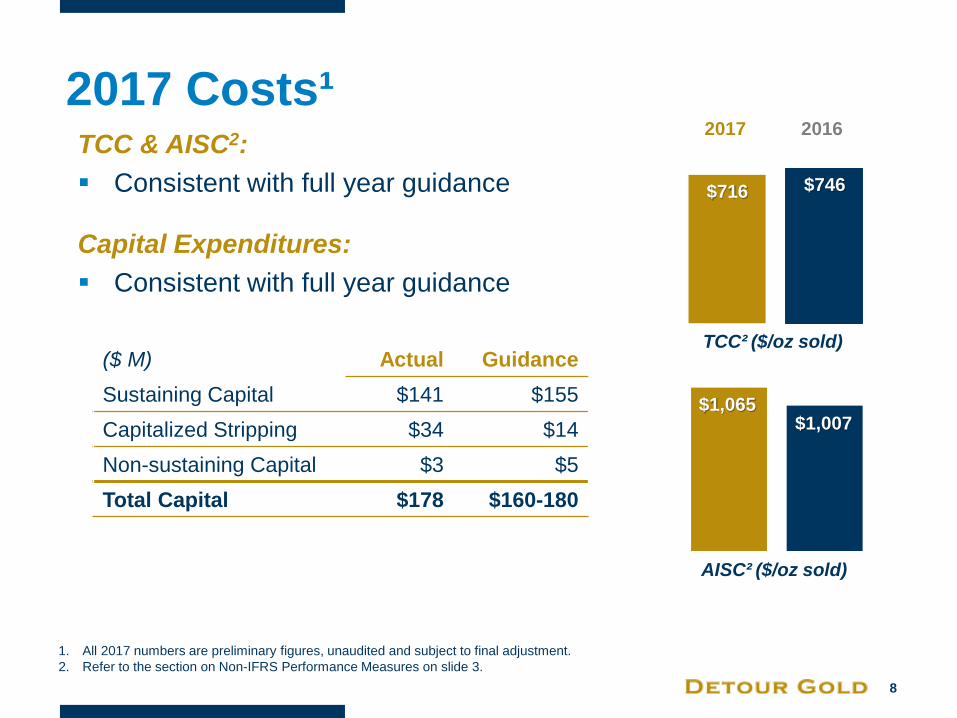

2017 Costs¹ TCC & AISC2:

Consistent with full year guidance

Capital Expenditures:

Consistent with full year guidance

TCC² ($/oz sold)

2016 2017

AISC² ($/oz sold)

$1,065 $1,007

$716 $746

($ M) Actual Guidance

Sustaining Capital $141 $155

Capitalized Stripping $34 $14

Non-sustaining Capital $3 $5

Total Capital $178 $160-180

1. All 2017 numbers are preliminary figures, unaudited and subject to final adjustment.

2. Refer to the section on Non-IFRS Performance Measures on slide 3.

9

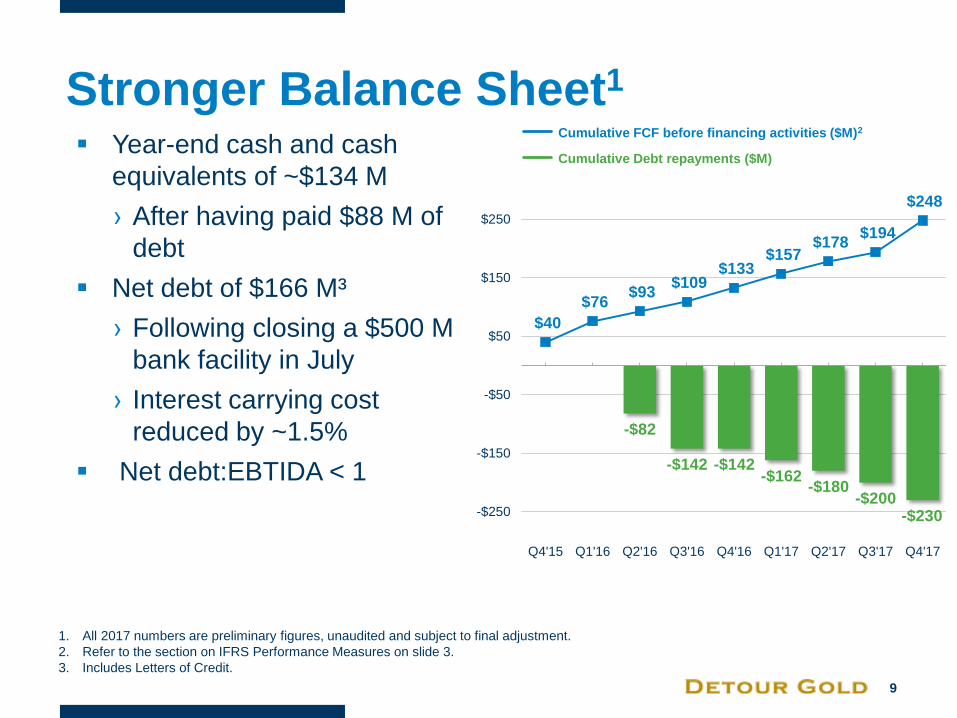

Stronger Balance Sheet1

-$82

-$142 -$142 -$162

-$180 -$200

-$230

$40

$76 $93

$109 $133

$157 $178

$194

$248

Q4'15 Q1'16 Q2'16 Q3'16 Q4'16 Q1'17 Q2'17 Q3'17 Q4'17

-$250

-$150

-$50

$50

$150

$250

Cumulative FCF before financing activities ($M)2

Cumulative Debt repayments ($M) Year-end cash and cash

equivalents of ~$134 M

› After having paid $88 M of

debt

Net debt of $166 M³

› Following closing a $500 M

bank facility in July

› Interest carrying cost

reduced by ~1.5%

Net debt:EBTIDA < 1

1. All 2017 numbers are preliminary figures, unaudited and subject to final adjustment.

2. Refer to the section on IFRS Performance Measures on slide 3.

3. Includes Letters of Credit.

10

Phase 2 (pre-stripping)

October 13, 2017

Detour Lake Open Pit

10

2018 Mine Equipment

2 x CAT 7495 shovels

5 x CAT 6060 shovels

34 x CAT 795 trucks Phase 1: Campbell

Pit Area

Phase 1: West

(calcite zone)

Phase 2

11

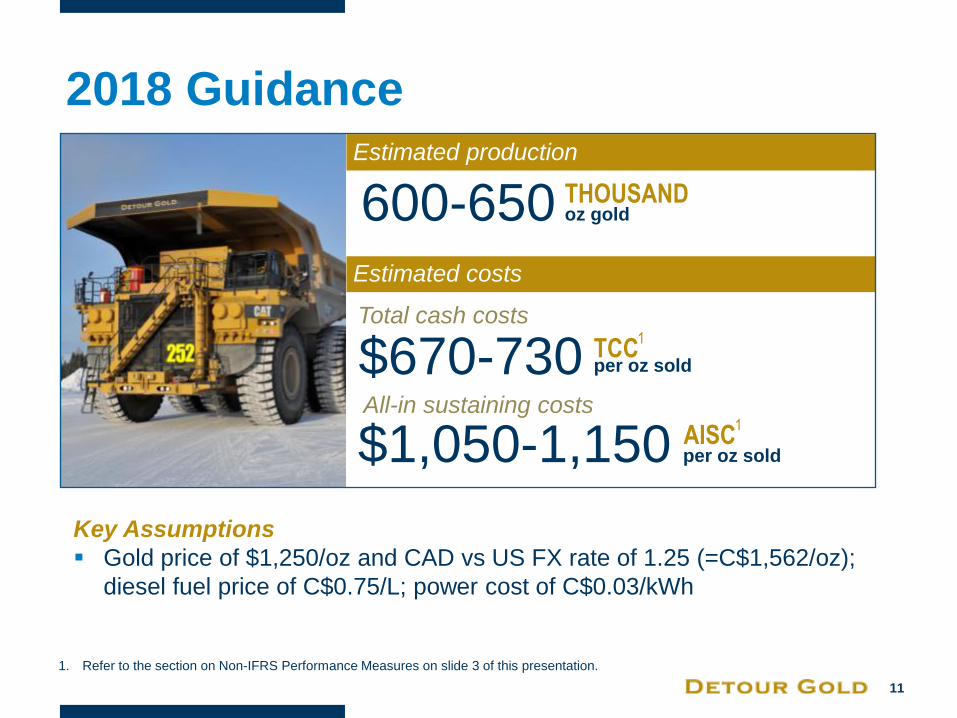

2018 Guidance

600-650 THOUSAND oz gold

$670-730 TCC per oz sold

1

$1,050-1,150 All-in sustaining costs

AISC per oz sold

1

Estimated costs

Total cash costs

Key Assumptions

Gold price of $1,250/oz and CAD vs US FX rate of 1.25 (=C$1,562/oz);

diesel fuel price of C$0.75/L; power cost of C$0.03/kWh

1. Refer to the section on Non-IFRS Performance Measures on slide 3 of this presentation.

Change photo;

same as last

year

Estimated production

12

2018 Operating Plan Mine: 112 Mt

Fleet to increase to 7 shovels

and 34 trucks supported by a

ROM fleet

~1.7 Mt of ore expected to be

mined and stockpiled

Strip ratio at 3.7:1

Mill: 22 Mt

Head grade expected to

average 0.99 g/t Au

Mill recoveries expected to

range between 90% and

91.5%

Gold Production: 600,000-650,000 oz

13

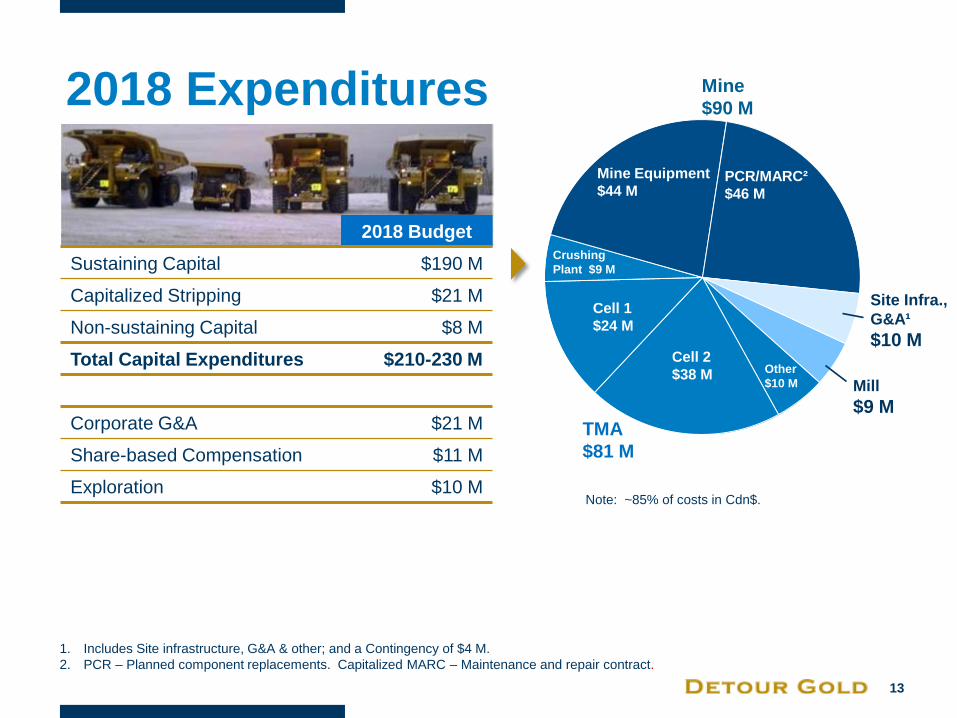

2018 Expenditures Mine

$90 M

TMA

$81 M

Site Infra.,

G&A¹

$10 M

Mill

$9 M

2018 Budget

Sustaining Capital $190 M

Capitalized Stripping $21 M

Non-sustaining Capital $8 M

Total Capital Expenditures $210-230 M

Corporate G&A $21 M

Share-based Compensation $11 M

Exploration $10 M Note: ~85% of costs in Cdn$.

1. Includes Site infrastructure, G&A & other; and a Contingency of $4 M.

2. PCR – Planned component replacements. Capitalized MARC – Maintenance and repair contract.

Mine Equipment

$44 M PCR/MARC²

$46 M

Crushing

Plant $9 M

Cell 1

$24 M

Cell 2

$38 M Other

$10 M

14

543

2018E 2019-20E¹ 2021-22E¹

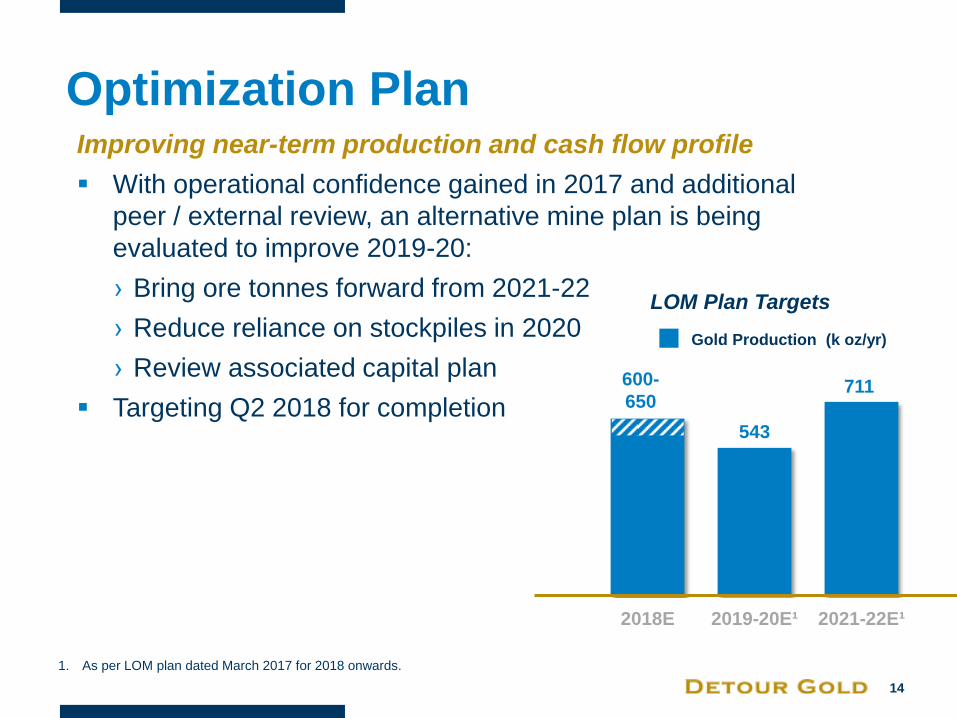

Optimization Plan Improving near-term production and cash flow profile

With operational confidence gained in 2017 and additional

peer / external review, an alternative mine plan is being

evaluated to improve 2019-20:

› Bring ore tonnes forward from 2021-22

› Reduce reliance on stockpiles in 2020

› Review associated capital plan

Targeting Q2 2018 for completion

600-

650

LOM Plan Targets

711

Gold Production (k oz/yr)

1. As per LOM plan dated March 2017 for 2018 onwards.

15

Organic Growth

WEST DETOUR

DEVELOPMENT

ZONE 58N

LOWER DETOUR

Provincial ESR

approval by year-end

In LOM plan West

Detour production

in 2025

Reserves: 1.8 M oz

Finalize options for

mining widths and cut-off

grade for different UG

mining scenarios

Potential for high-

grade UG mine

BURNTBUSH

CLAIM BLOCK

Claim block 70 km

south of Detour

Lake

Drilling program in

summer 2018

16 15

16

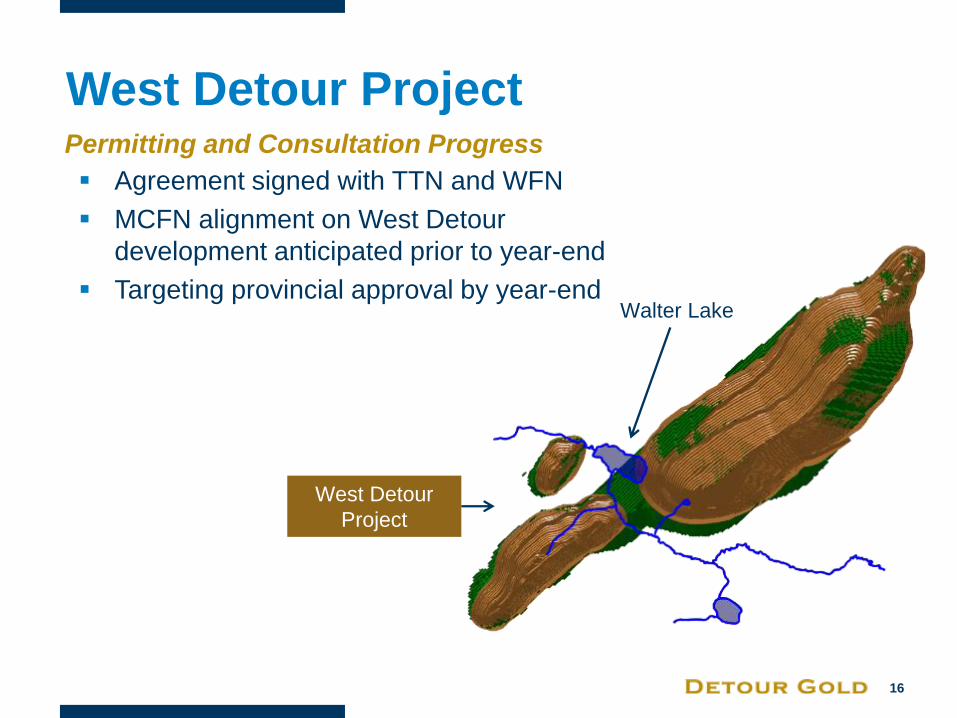

West Detour Project Permitting and Consultation Progress

Walter Lake

West Detour

Project

Agreement signed with TTN and WFN

MCFN alignment on West Detour

development anticipated prior to year-end

Targeting provincial approval by year-end

17

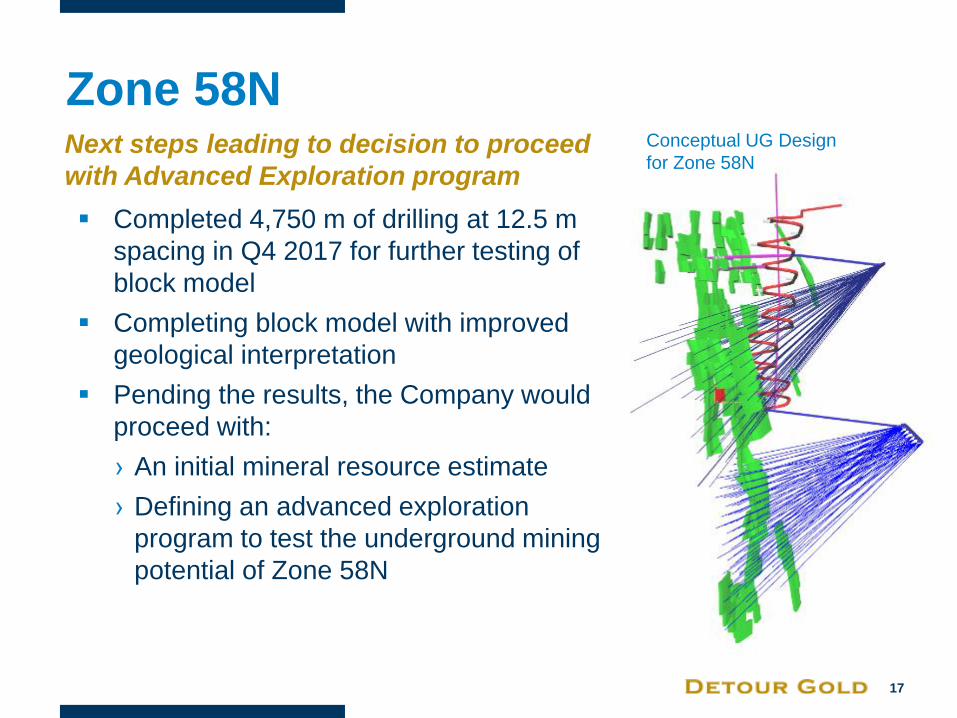

Zone 58N Next steps leading to decision to proceed

with Advanced Exploration program

Conceptual UG Design

for Zone 58N

Completed 4,750 m of drilling at 12.5 m

spacing in Q4 2017 for further testing of

block model

Completing block model with improved

geological interpretation

Pending the results, the Company would

proceed with:

› An initial mineral resource estimate

› Defining an advanced exploration

program to test the underground mining

potential of Zone 58N

18 18

Closing Comments 2018 to be another solid Year for

Detour Gold:

Production growth

Continued free cash flow growth

Financial strength and flexibility

Leverage to gold price

ATTRACTIVE VALUATION OPPORTUNITY

19 19

Additional Information Safety Performance

Shareholder Information

Operational Statistics

Detour Lake Property

Burntbush Property

Summary LOM Plan

Year-end 2016 Reserves & Resources

Analyst Coverage

Management & Directors

Contact Information

20

Safety Performance Total Recordable Injury

Frequency Rate (TRIFR)1

(12 Month Rolling Average)

1. TRIFR: Total recordable injuries x 200,000 hours

divided by total man hours worked.

2017:

TRIFR of 1.78 for the year

Safety performance

improvement in Q4

Completed hiring to bolster the

Safety team

Establish Safety Journey Plan

for 2018 including a

commitment to undertake

behavioral safety training

across workforce

0.0

1.0

2.0

DGC Target Contractor

Q2’17 Q1’17 Q3’17 Q4’17

1.67 1.60

1.87

21

Shareholder Information

>80% INSTITUTIONS TOTAL

4.7 M Share options & Units

179.6 M FULLY DILUTED

174.9 M Issued & outstanding

Share Structure (03/31/2014)

11%

$134 MILLION cash and cash equivalents at December 31, 2017¹

Share Structure (December 31, 2017) Top Shareholders

Van Eck Associates

8% BlackRock

1. All 2017 numbers are preliminary figures, unaudited and subject to final adjustment.

22

2017 Operational Statistics¹

Q1’17 Q2’17 Q3’17 Q4’17 2017

Ore mined (Mt) 4.8 4.9 5.4 4.7 19.7

Waste mined (Mt) 17.0 20.4 20.6 22.4 80.4

Total mined (Mt) 21.8 25.2 26.1 27.0 100.1

Strip ratio (waste:ore) 3.6 4.2 3.8 4.8 4.1

Mining rate (tpd) 242,000 277,000 283,000 294,000 274,000

Ore milled (Mt) 5.2 5.5 5.7 5.0 21.4

Mill grade (g/t Au) 0.88 0.95 0.86 1.04 0.93

Recovery (%) 89 90 90 90 90

Mill throughput (tpd) 58,114 60,259 61,548 54,144 58,508

Ounces produced (oz) 131,418 150,138 139,861 150,046 571,463

Ounces sold (oz) 134,213 142,970 128,498 156,293 561,974

1. All 2017 numbers are preliminary figures and subject to final adjustment.

23

Detour Lake Property

24

Burntbush Property

Basement Gneiss

Intermediate to Mafic Volcanics

Mafic Intrusives

Sediments

Felsic to Intermediate Intrusives

Felsic to Intermediate Volcanics

Detour Lake

Burntbush

25

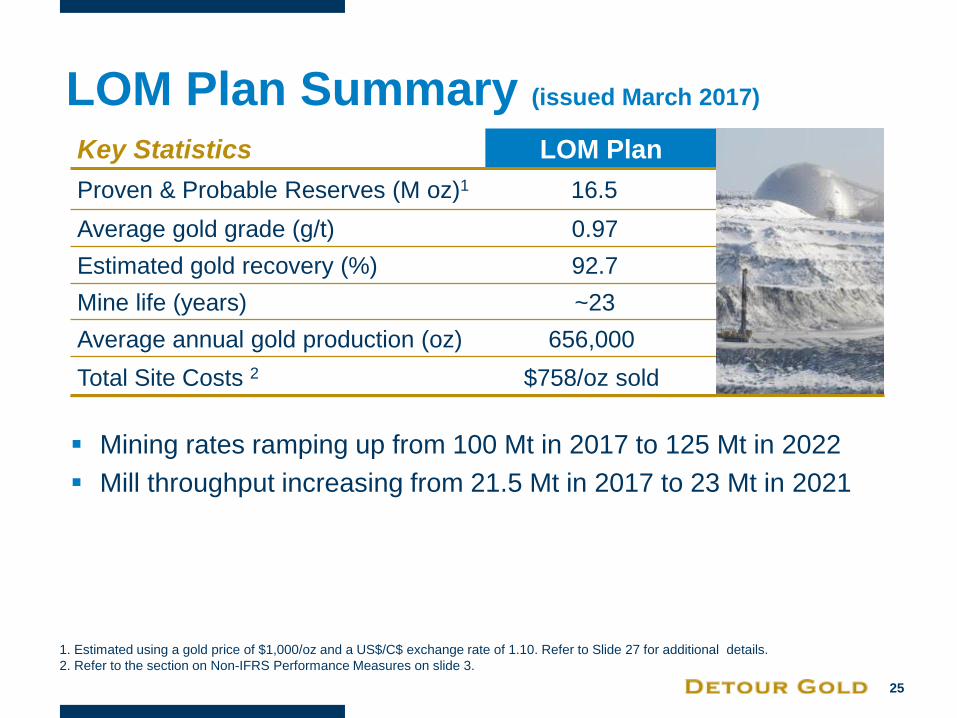

LOM Plan Summary (issued March 2017)

Key Statistics LOM Plan

Proven & Probable Reserves (M oz)1 16.5

Average gold grade (g/t) 0.97

Estimated gold recovery (%) 92.7

Mine life (years) ~23

Average annual gold production (oz) 656,000

Total Site Costs 2 $758/oz sold

1. Estimated using a gold price of $1,000/oz and a US$/C$ exchange rate of 1.10. Refer to Slide 27 for additional details.

2. Refer to the section on Non-IFRS Performance Measures on slide 3.

Mining rates ramping up from 100 Mt in 2017 to 125 Mt in 2022

Mill throughput increasing from 21.5 Mt in 2017 to 23 Mt in 2021

26

LOM Production Plan

Yearly Average per Period Total

2017-

18

2019-

20

2021-

22

2023-

25

2026-

28

2029-

31

2032-

34

2035-

37

2038-

401 LOM LOM

Ore milled (Mt) 21.8 22.5 23.0 23.0 23.0 23.0 23.0 23.0 22.5 22.8 530

Head grade (g/t Au) 0.97 0.82 1.04 0.90 0.90 0.95 0.96 1.10 1.04 0.97 0.97

Gold recovery (%) 90.6 92.1 92.9 92.8 92.8 92.9 92.9 93.2 93.3 92.7 92.7

Gold production (k oz) 617 543 711 616 619 652 662 760 702 656 15,250

Total mined (Mt) 107.0 127.2 129.0 125.8 117.3 90.7 80.1 50.7 24.5 93.6 2,175

Strip ratio (waste:ore) 3.93 6.10 3.70 4.63 4.18 3.07 2.53 1.38 0.60 3.33 3.33

1. Average for the last years at 2.25 years.

27

LOM Plan Financial Summary

1. Ounces sold = Production x 97.95% (= 100% - 2% NSR - 0.05% Refiners take).

2. Includes all site costs including bullion delivery, refining and costs related to agreements with Aboriginal communities.

3. Includes closure costs.

4. Refer to the section on Non-IFRS Performance Measures on slide 3.

5. US$/C$ exchange rate of 1.30 in 2017, 1.27 in 2018, and 1.25 in 2019+.

2-Year Average 2017LOM

Units 2017-18 2019-20 2021-22 Average Total

Gold Production k oz 617 543 711 656 15,250

Gold Sales1 k oz 604 531 696 643 14,937

Site Costs

Operating Costs2 C$ M 519 482 500 471 10,960

Sustaining Capital3 C$ M 209 173 96 107 2,488

Deferred Stripping C$ M 34 134 30 38 884

Total Capital Costs C$ M 243 307 127 145 3,372

Total Site Costs C$ M 762 789 627 616 14,332

US$/oz sold4 980 1,187 718 758 -

Cash Flow

Site Cash Flow5

(after Tax) C$ M 186 52 448 301 7,038

NPV5% (after tax) = C$3.7 B

28

Year-end 2017 Reserves & Resources Notes:

1. The Company’s mineral resources and

reserves conform with generally accepted

definitions and guidelines given in the

Canadian Institute of Mining, Metallurgy

and Petroleum (CIM) Standards on

Mineral Resources and Mineral Reserves

as required by NI 43-101.

2. Mineral reserves were estimated using a

gold price of US$1,000/oz and mineral

resources were estimated using a gold

price of US$1,200/oz at a US$/C$

exchange rate of 1.10.

3. Mineral reserves and resources were

based on a cut-off grade of 0.50 g/t Au.

4. LG Fines (sourced from material grading

0.40-0.50 g/t Au) classified as Measured

and Indicated were reported as Probable

mineral reserves and included in the mine

plan.

5. Further information, including key

assumptions, parameters, and methods

used to estimate mineral resources and

mineral reserves are described in the

Technical Report on the Detour Lake

operation, dated March 22, 2017.

6. Mineral resources are reported exclusive

of mineral reserves. Mineral resources that

are not mineral reserves do not have

demonstrated economic viability. Mineral

resources are constrained within an

economic pit shell.

7. Totals may not add due to rounding.

At Dec. 31, 2017

Reserves Tonnes

(millions)

Grade

(g/t Au)

Contained

Gold Ounces

(000’s oz)

Detour Lake Pit Proven 87.9 1.24 3,504

Probable 338.4 0.93 10,064

Total P&P 426.3 0.99 13,568

West Detour Pit Proven 1.9 0.96 60

Probable 53.0 0.94 1,596

North Pit Probable 6.0 0.98 187

Total P&P 60.9 0.94 1,843

LG Fines Probable 20.9 0.60 403

Total P&P 508.0 0.97 15,814

Resources

Detour Lake Pit Measured 17.3 1.32 735

Indicated 71.2 0.98 2,255

M+I 88.5 1.05 2,991

West Detour Pit Measured 0.3 0.93 9

Indicated 28.5 0.88 806

North Pit Indicated 2.1 0.93 64

M+I 31.0 0.88 878

Total M+I 119.5 1.01 3,869

Detour Lake Mine Inferred 35.7 0.79 906

West Detour Pit Inferred 9.2 0.95 280

North Pit Inferred 0.1 0.85 2

Total Inferred 44.9 0.82 1,188

29

Analyst Coverage (20)

Firm Analyst Target Price at

February 6, 2018

Bank of America Merrill Lynch Michael Jalonen $19.50

Beacon Securities Michael Curran $17.75

BMO Brian Quast $26.00

Canaccord Rahul Paul $23.50

CIBC World Markets Cosmos Chiu $20.00

Cormark Securities Richard Gray $20.00

Credit Suisse Anita Soni $16.00

Desjardins Josh Wolfson $15.50

Eight Capital Research Craig Stanley $18.00

Global Mining Research David Radclyffe/David Cotterell $18.00

GMP Securities Ian Parkinson $19.00

Haywood Kerry Smith $26.00

Laurentian Bank Barry Allan $20.00

Macquarie Mike Siperco $22.00

National Bank Mike Parkin $21.50

Paradigm Don Blyth/Don MacLean $25.50

Raymond James Farooq Hamed $21.00

RBC Dan Rollins $20.00

Scotiabank Trevor Turnbull $19.00

TD Dan Earle $23.00

Average target $20.56

30

Management & Directors

Paul Martin President and CEO

Frazer Bourchier COO

James Mavor CFO

Julie Galloway General Counsel &

Corporate Secretary

Drew Anwyll Sr VP Technical Services

Derek Teevan Sr VP Corporate &

Aboriginal Affairs

Charles Hennessey Mine General Manager

Laurie Gaborit VP Investor Relations

Ruben Wallin VP Environment & Sustainability

Alberto Heredia Controller

Jacques McMullen Corporate Technical Advisor

Lisa Colnett

Edward C. Dowling

Robert E. Doyle

Paul Martin

Alex G. Morrison

Jonathan Rubenstein

André Falzon

Ingrid Hibbard

Michael Kenyon

MANAGEMENT

DIRECTORS

31 31

Contact Information

Laurie Gaborit VP Investor Relations

Email: [email protected]

Phone: 416.304.0581

www.detourgold.com

Paul Martin President and Chief Executive Officer

Email: [email protected]

Phone: 416.304.0800

![Feeding Part Two [Recovered] [Recovered]](https://img.pdfslide.us/doc/110x75/55cf9b65550346d033a5ea4b/feeding-part-two-recovered-recovered.jpg)

![Govt Acctg Recovered] Recovered]](https://img.pdfslide.us/doc/110x75/577d26c61a28ab4e1ea2266a/govt-acctg-recovered-recovered.jpg)

![Evaluation media presentation1 [recovered] [recovered]](https://img.pdfslide.us/doc/110x75/54953ac6b47959a84e8b457e/evaluation-media-presentation1-recovered-recovered-5584a8d0c6efc.jpg)