Embed Size (px)

Citation preview

© 2019 IHS Markit. All Rights Reserved.

Automotive Industry

Outlook:Managing Volatility and Leveraging Opportunities

in a Dynamic Market Environment

Mike Wall

Executive Director, Automotive Analysis

+1 248 728 8400 Direct

+1 616 446 6885 Mobile

February 2019

© 2019 IHS Markit. All Rights Reserved.

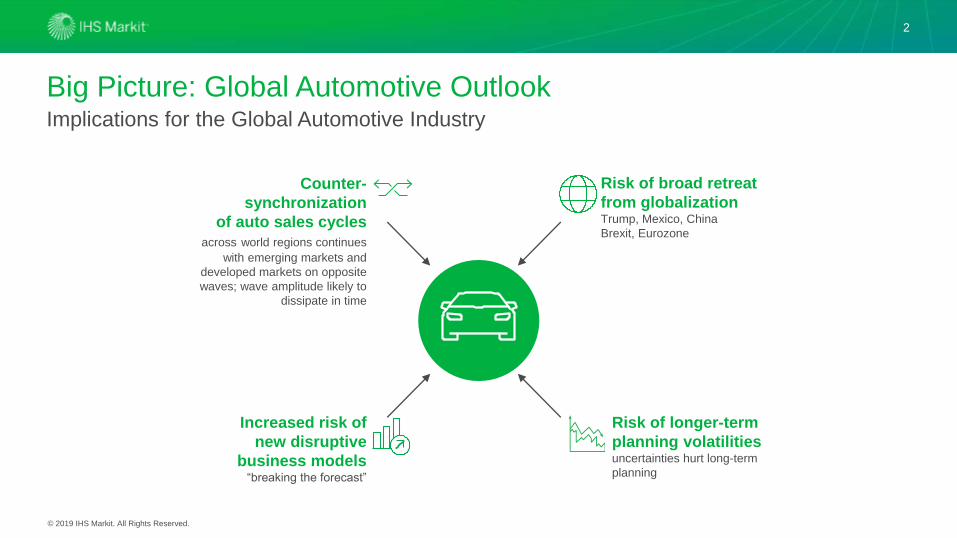

Big Picture: Global Automotive Outlook

2

Implications for the Global Automotive Industry

Counter-

synchronization

of auto sales cycles

across world regions continues

with emerging markets and

developed markets on opposite

waves; wave amplitude likely to

dissipate in time

Risk of broad retreat

from globalizationTrump, Mexico, China

Brexit, Eurozone

Increased risk of

new disruptive

business models “breaking the forecast”

Risk of longer-term

planning volatilitiesuncertainties hurt long-term

planning

© 2019 IHS Markit. All Rights Reserved.

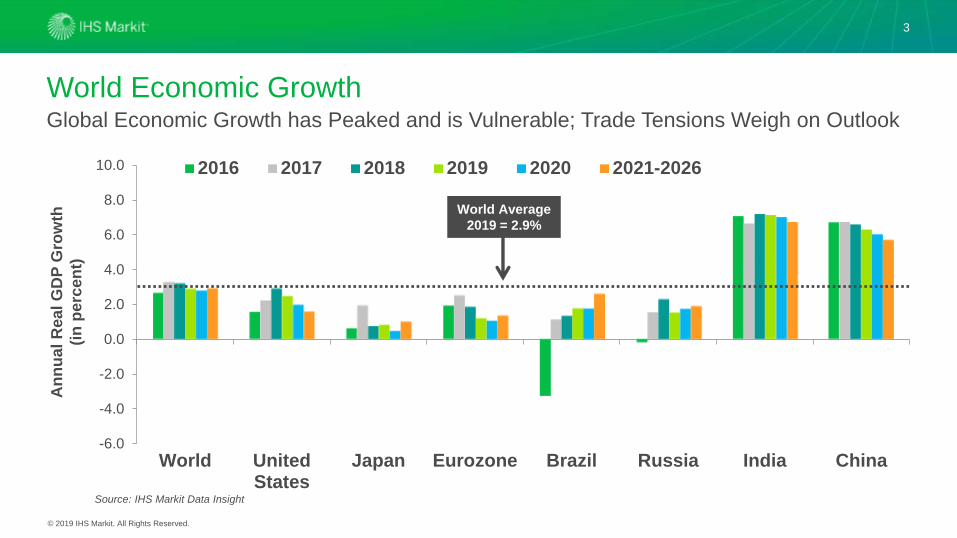

World Economic Growth

3

Global Economic Growth has Peaked and is Vulnerable; Trade Tensions Weigh on Outlook

Source: IHS Markit Data Insight

An

nu

al

Real

GD

P G

row

th

(in

perc

en

t)

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

World UnitedStates

Japan Eurozone Brazil Russia India China

2016 2017 2018 2019 2020 2021-2026

World Average

2019 = 2.9%

© 2019 IHS Markit. All Rights Reserved.

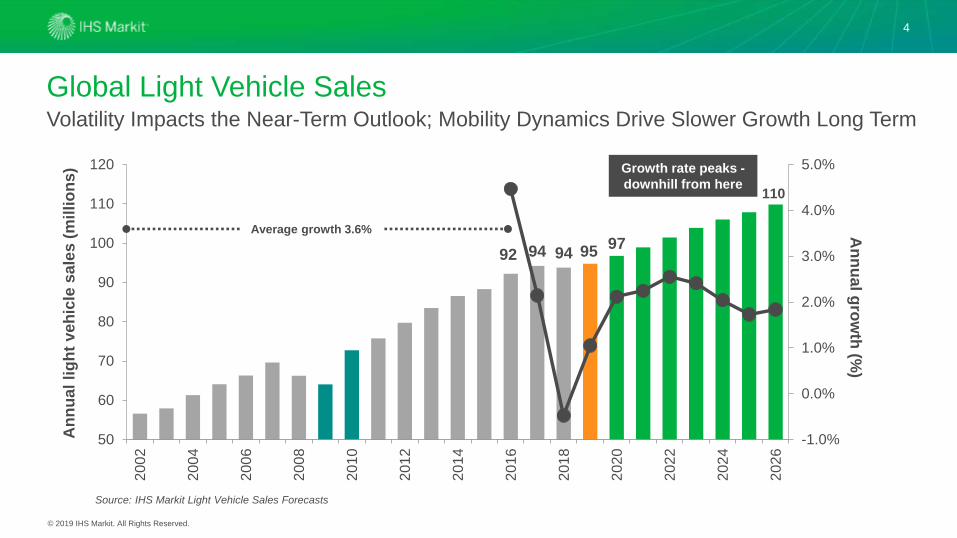

Global Light Vehicle Sales

4

Volatility Impacts the Near-Term Outlook; Mobility Dynamics Drive Slower Growth Long Term

92 94 94

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

50

60

70

80

90

100

110

120

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

20

18

20

20

20

22

20

24

20

26

Source: IHS Markit Light Vehicle Sales Forecasts

An

nu

al

lig

ht

veh

icle

sale

s (

mil

lio

ns)

An

nu

al g

row

th (%

)

Average growth 3.6%

Growth rate peaks -

downhill from here110

9597

© 2019 IHS Markit. All Rights Reserved.

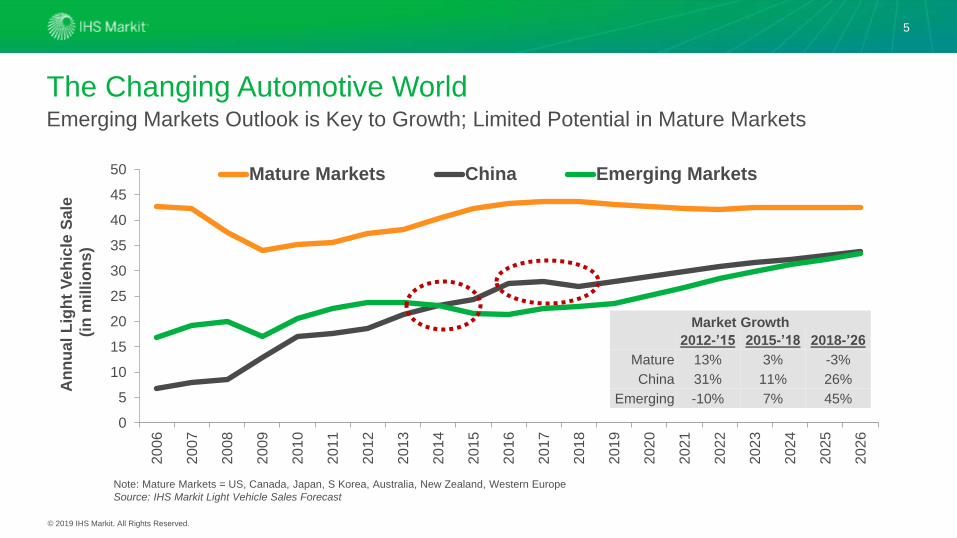

The Changing Automotive World

5

Emerging Markets Outlook is Key to Growth; Limited Potential in Mature Markets

0

5

10

15

20

25

30

35

40

45

502

00

6

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

Mature Markets China Emerging Markets

An

nu

al

Lig

ht

Veh

icle

Sale

(in

mil

lio

ns)

Note: Mature Markets = US, Canada, Japan, S Korea, Australia, New Zealand, Western Europe

Source: IHS Markit Light Vehicle Sales Forecast

Market Growth

2012-’15 2015-’18 2018-’26

Mature 13% 3% -3%

China 31% 11% 26%

Emerging -10% 7% 45%

© 2019 IHS Markit. All Rights Reserved.

Global Light Vehicle Production

6

Marginal Growth Driven by Asia and South America; Material Risks Remain

65

70

75

80

85

90

95

100

2017 2018 GreaterChina

SouthAsia

SouthAmerica

Japan/Korea

Europe NorthAmerica

ME/Africa

2019

95.1

million94.1

million

94.5

million

422,000 281,000 216,000 15,000 -168,000 -176,000 -205,000

Pro

du

cti

on

(m

illi

on

s)

Source: IHS Markit Light Vehicle Production Forecast

+0.4%

© 2019 IHS Markit. All Rights Reserved.

59

95

110

50

60

70

80

90

100

110

120

2007 2009 2011 2013 2015 2017 2019 2021 2023 2025

Mil

lio

ns

15 million

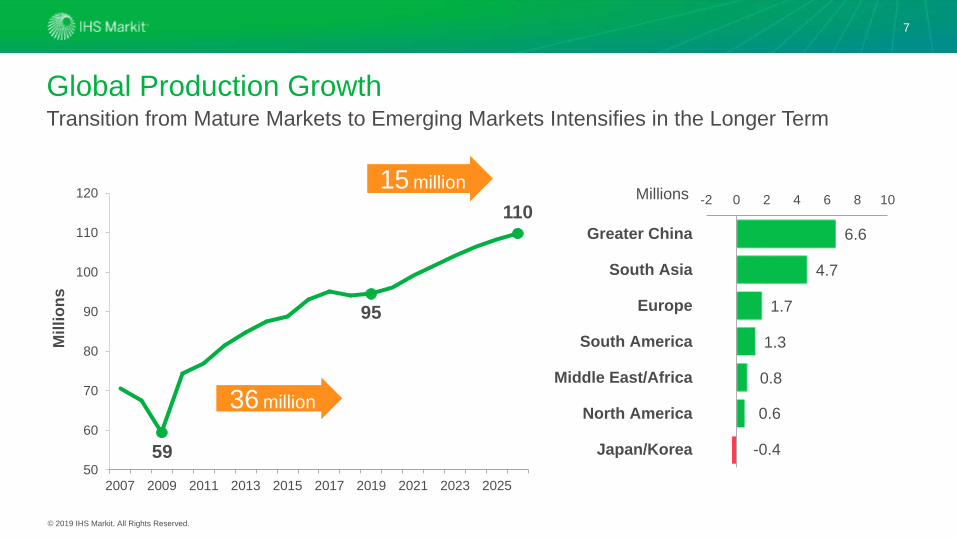

Global Production Growth

7

Transition from Mature Markets to Emerging Markets Intensifies in the Longer Term

6.6

4.7

1.7

1.3

0.8

0.6

-0.4

-2 0 2 4 6 8 10

Greater China

South Asia

Europe

South America

Middle East/Africa

North America

Japan/Korea

Millions

36 million

© 2019 IHS Markit. All Rights Reserved.

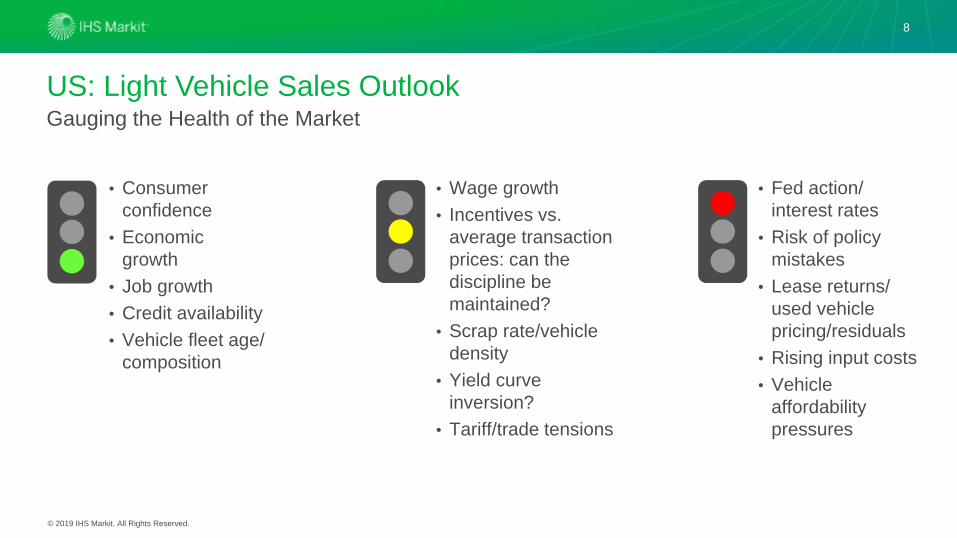

• Consumer

confidence

• Economic

growth

• Job growth

• Credit availability

• Vehicle fleet age/

composition

US: Light Vehicle Sales Outlook

8

Gauging the Health of the Market

• Fed action/

interest rates

• Risk of policy

mistakes

• Lease returns/

used vehicle

pricing/residuals

• Rising input costs

• Vehicle

affordability

pressures

• Wage growth

• Incentives vs.

average transaction

prices: can the

discipline be

maintained?

• Scrap rate/vehicle

density

• Yield curve

inversion?

• Tariff/trade tensions

© 2019 IHS Markit. All Rights Reserved.

4.8m

12.1m

4

6

8

10

12

14

16

18

20

196

7

196

9

197

1

197

3

197

5

197

7

197

9

198

1

198

3

198

5

198

7

198

9

199

1

199

3

199

5

199

7

199

9

200

1

200

3

200

5

200

7

200

9

201

1

201

3

201

5

201

7

201

9

202

1

202

3

202

5

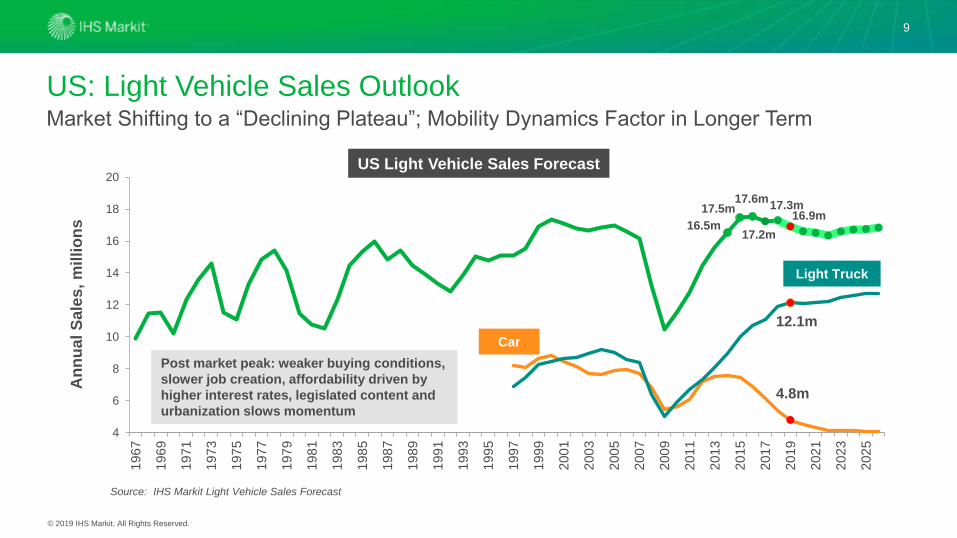

17.3m

US: Light Vehicle Sales Outlook

9

Market Shifting to a “Declining Plateau”; Mobility Dynamics Factor in Longer Term

US Light Vehicle Sales Forecast

Source: IHS Markit Light Vehicle Sales Forecast

Car

Light Truck

Post market peak: weaker buying conditions,

slower job creation, affordability driven by

higher interest rates, legislated content and

urbanization slows momentum

16.5m

17.5m17.6m

An

nu

al

Sale

s,

mil

lio

ns

17.2m

16.9m

© 2019 IHS Markit. All Rights Reserved.

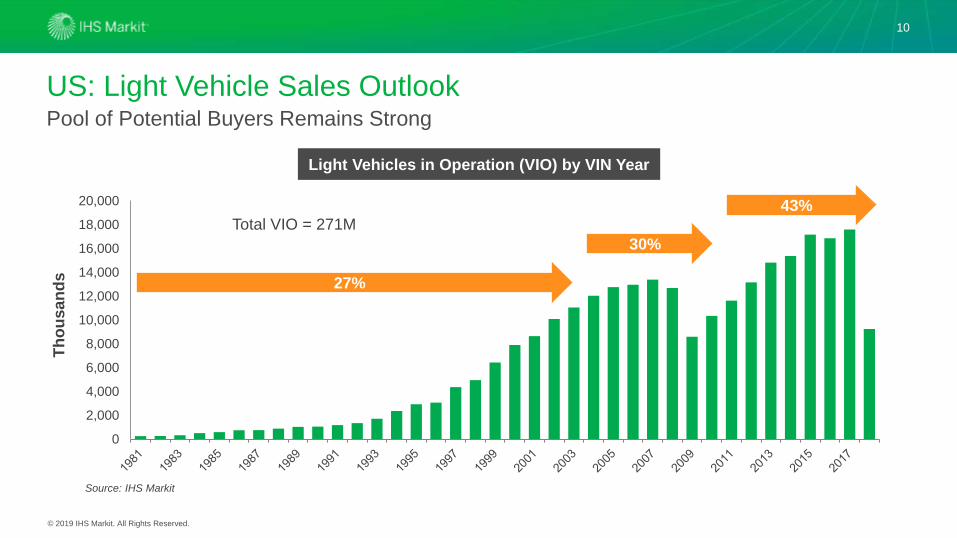

US: Light Vehicle Sales Outlook

10

Pool of Potential Buyers Remains Strong

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

Th

ou

san

ds

Light Vehicles in Operation (VIO) by VIN Year

Source: IHS Markit

Total VIO = 271M

27%

30%

43%

© 2019 IHS Markit. All Rights Reserved.

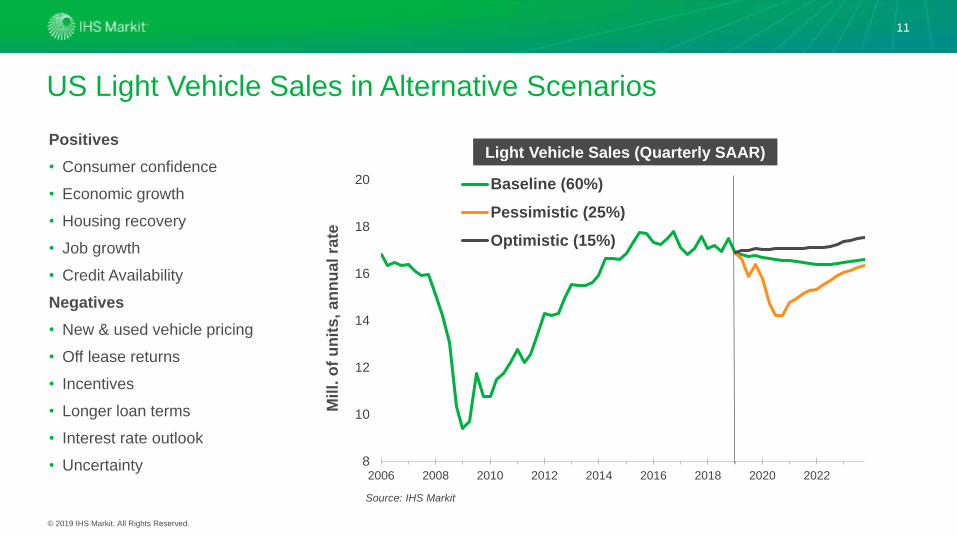

US Light Vehicle Sales in Alternative Scenarios

Positives

• Consumer confidence

• Economic growth

• Housing recovery

• Job growth

• Credit Availability

Negatives

• New & used vehicle pricing

• Off lease returns

• Incentives

• Longer loan terms

• Interest rate outlook

• Uncertainty

11

8

10

12

14

16

18

20

2006 2008 2010 2012 2014 2016 2018 2020 2022

Mil

l. o

f u

nit

s, an

nu

al

rate

Baseline (60%)

Pessimistic (25%)

Optimistic (15%)

Light Vehicle Sales (Quarterly SAAR)

Source: IHS Markit

© 2019 IHS Markit. All Rights Reserved.

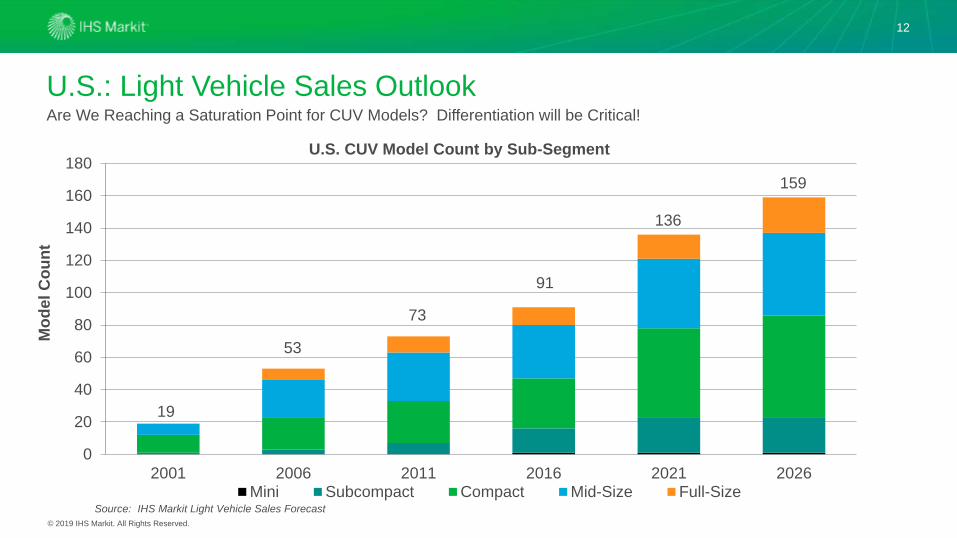

12

U.S.: Light Vehicle Sales OutlookAre We Reaching a Saturation Point for CUV Models? Differentiation will be Critical!

0

20

40

60

80

100

120

140

160

180

2001 2006 2011 2016 2021 2026Mini Subcompact Compact Mid-Size Full-Size

U.S. CUV Model Count by Sub-Segment

Mo

del

Co

un

t

Source: IHS Markit Light Vehicle Sales Forecast

19

159

73

53

91

136

© 2019 IHS Markit. All Rights Reserved.

13

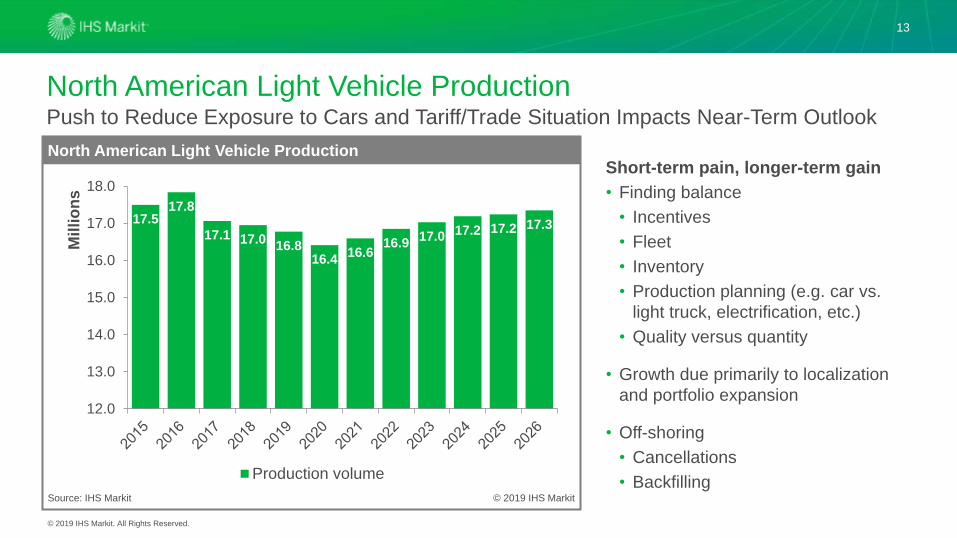

North American Light Vehicle Production

Short-term pain, longer-term gain

• Finding balance

• Incentives

• Fleet

• Inventory

• Production planning (e.g. car vs.

light truck, electrification, etc.)

• Quality versus quantity

• Growth due primarily to localization

and portfolio expansion

• Off-shoring

• Cancellations

• BackfillingSource: IHS Markit

North American Light Vehicle Production

© 2019 IHS Markit

17.517.8

17.1 17.016.8

16.416.6

16.917.0 17.2 17.2 17.3

12.0

13.0

14.0

15.0

16.0

17.0

18.0

Mil

lio

ns

Production volume

Push to Reduce Exposure to Cars and Tariff/Trade Situation Impacts Near-Term Outlook

© 2019 IHS Markit. All Rights Reserved.

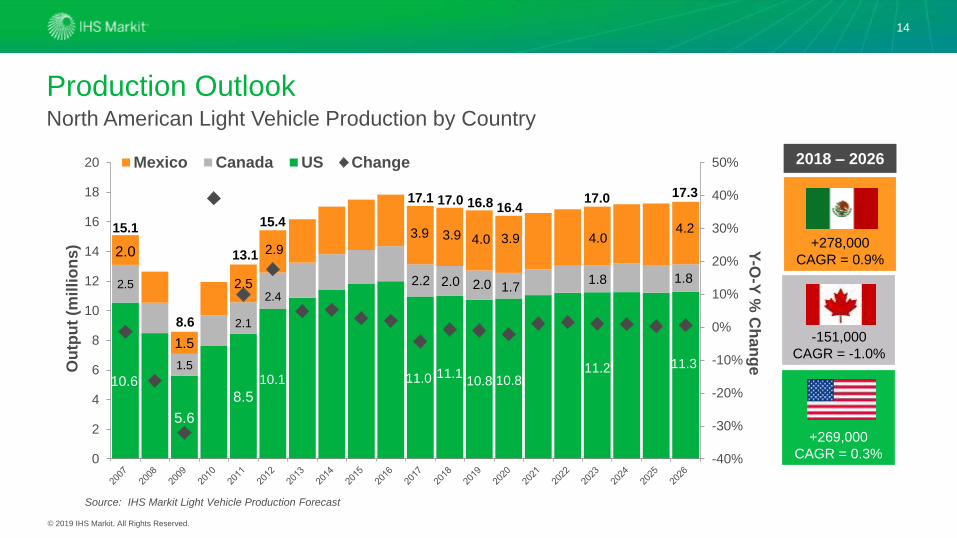

Production Outlook

14

North American Light Vehicle Production by Country

10.6

5.6

8.5

2.5

1.5

2.1

2.0

1.5

2.5

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

0

2

4

6

8

10

12

14

16

18

20

Y-O

-Y %

Ch

an

geO

utp

ut

(mil

lio

ns)

Mexico Canada US Change 2018 – 2026

-151,000

CAGR = -1.0%

+278,000

CAGR = 0.9%

15.4

16.8 17.0

15.1

8.6

13.1

10.1

2.4

2.9

17.3

11.3

1.8

4.2

Source: IHS Markit Light Vehicle Production Forecast

11.2

4.0

1.8

17.1

11.0

3.9

2.2

+269,000

CAGR = 0.3%

17.0

11.1

3.9

2.0

10.8

4.0

2.0

16.4

10.8

3.9

1.7

© 2019 IHS Markit. All Rights Reserved.

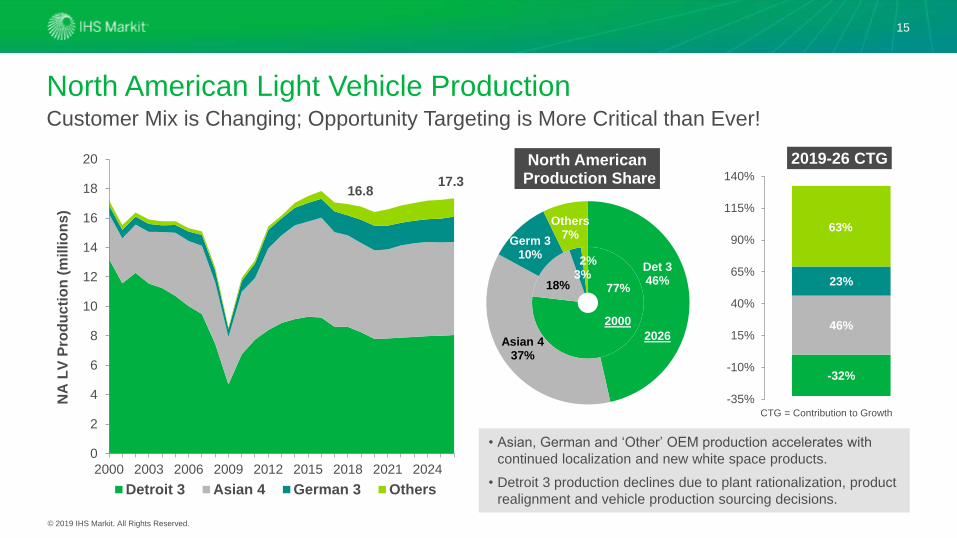

North American Light Vehicle Production

15

Customer Mix is Changing; Opportunity Targeting is More Critical than Ever!

77%18%3%2%

Det 346%

Asian 437%

Germ 310%

Others7%

North AmericanProduction Share

0

2

4

6

8

10

12

14

16

18

20

2000 2003 2006 2009 2012 2015 2018 2021 2024

NA

LV

Pro

du

cti

on

(m

illio

ns)

Detroit 3 Asian 4 German 3 Others

2000

2026

• Asian, German and ‘Other’ OEM production accelerates with

continued localization and new white space products.

• Detroit 3 production declines due to plant rationalization, product

realignment and vehicle production sourcing decisions.

-32%

46%

23%

63%

-35%

-10%

15%

40%

65%

90%

115%

140%

2019-26 CTG

CTG = Contribution to Growth

17.316.8

© 2019 IHS Markit. All Rights Reserved.

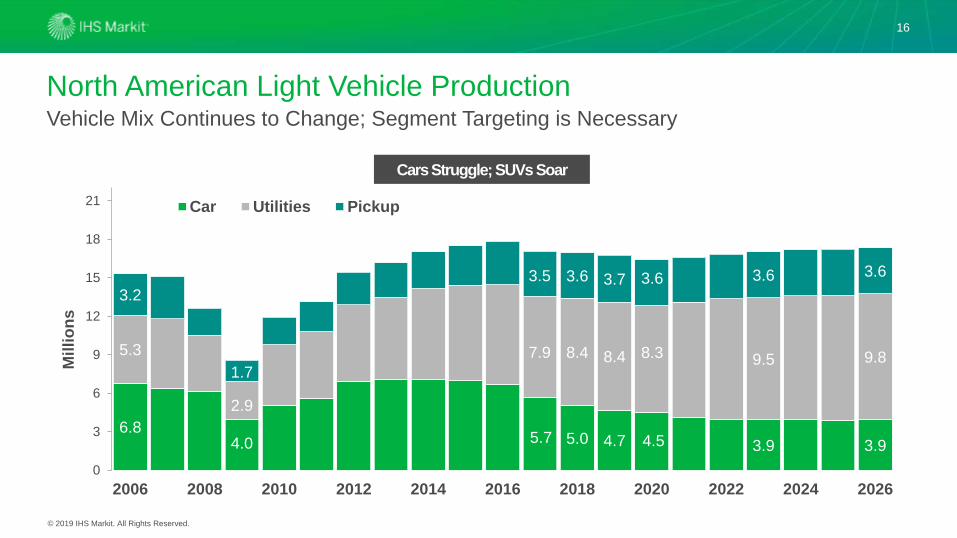

North American Light Vehicle Production

16

Vehicle Mix Continues to Change; Segment Targeting is Necessary

Cars Struggle; SUVs Soar

6.85.0 4.7 3.9 3.9

5.3 8.4 8.4 9.5 9.8

3.2

3.6 3.7 3.6 3.6

0

3

6

9

12

15

18

21

2006 2008 2010 2012 2014 2016 2018 2020 2022 2024 2026

Mil

lio

ns

Car Utilities Pickup

1.7

2.9

4.0

3.5

7.9

5.7

3.6

8.3

4.5

© 2019 IHS Markit. All Rights Reserved.

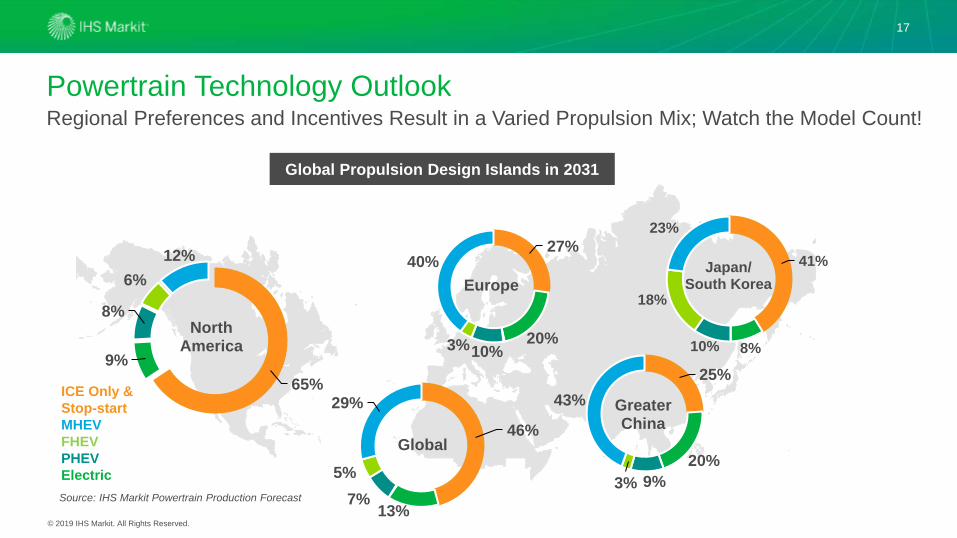

Powertrain Technology Outlook

17

Regional Preferences and Incentives Result in a Varied Propulsion Mix; Watch the Model Count!

ICE Only &

Stop-start

MHEV

FHEV

PHEV

Electric

Source: IHS Markit Powertrain Production Forecast

27%

20%10%3%

40%

Europe

41%

8%10%

18%

23%

Japan/South Korea

Global Propulsion Design Islands in 2031

65%

9%

8%

6%

12%

NorthAmerica

25%

20%

9%3%

43% GreaterChina46%

13%7%

5%

29%

Global

© 2019 IHS Markit. All Rights Reserved.

Thank You!

Mike Wall

Executive Director, Automotive Analysis

+1 248 728 8400 Direct

+1 616 446 6885 Mobile

18

IHS Markit Customer Care

Americas: +1 800 IHS CARE (+1 800 447 2273)

Europe, Middle East, and Africa: +44 (0) 1344 328 300

Asia and the Pacific Rim: +604 291 3600

Disclaimer

The information contained in this presentation is confidential. Any unauthorized use, disclosure, reproduction, or dissemination, in full or in part, in any media or by any means, without the prior written permission

of IHS Markit Ltd. or any of its affiliates ("IHS Markit") is strictly prohibited. IHS Markit owns all IHS Markit logos and trade names contained in this presentation that are subject to license. Opinions, statements,

estimates, and projections in this presentation (including other media) are solely those of the individual author(s) at the time of writing and do not necessarily reflect the opinions of IHS Markit. Neither IHS Markit

nor the author(s) has any obligation to update this presentation in the event that any content, opinion, statement, estimate, or projection (collectively, "information") changes or subsequently becomes inaccurate.

IHS Markit makes no warranty, expressed or implied, as to the accuracy, completeness, or timeliness of any information in this presentation, and shall not in any way be liable to any recipient for any

inaccuracies or omissions. Without limiting the foregoing, IHS Markit shall have no liability whatsoever to any recipient, whether in contract, in tort (including negligence), under warranty, under statute or

otherwise, in respect of any loss or damage suffered by any recipient as a result of or in connection with any information provided, or any course of action determined, by it or any third party, whether or not based

on any information provided. The inclusion of a link to an external website by IHS Markit should not be understood to be an endorsement of that website or the site's owners (or their products/services). IHS

Markit is not responsible for either the content or output of external websites. Copyright © 2018, IHS MarkitTM. All rights reserved and all intellectual property rights are retained by IHS Markit.