Embed Size (px)

Citation preview

NAFTA Automotive Outlook: Focus Mexico

UDEM

April 2013

Copyright © 2013 IHS Inc. All Rights Reserved.

Agenda

• Macroeconomic outlook

• Global sales and production outlook

• Europe outlook

• Americas outlook

• Mexico Production

• Summary

Copyright © 2013 IHS Inc. All Rights Reserved.

-8

-6

-4

-2

0

2

4

6

8

10

World UnitedStates

Japan Eurozone Brazil Russia India China

2011 2012 2013 2014 2015-20

World economic growth Modest gains expected; significant threats remain

Annu

al re

al G

DP

gro

wth

in %

Debt crisis

continues

Source: IHS DataInsight

World average

2013

Political stalemate may

cause US recession Hard landing

averted?

Copyright © 2013 IHS Inc. All Rights Reserved.

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

Jan'0

7

Ja

n'0

8

Jan'0

9

Jan'1

0

Jan'1

1

Jan'1

2

Jan'1

3

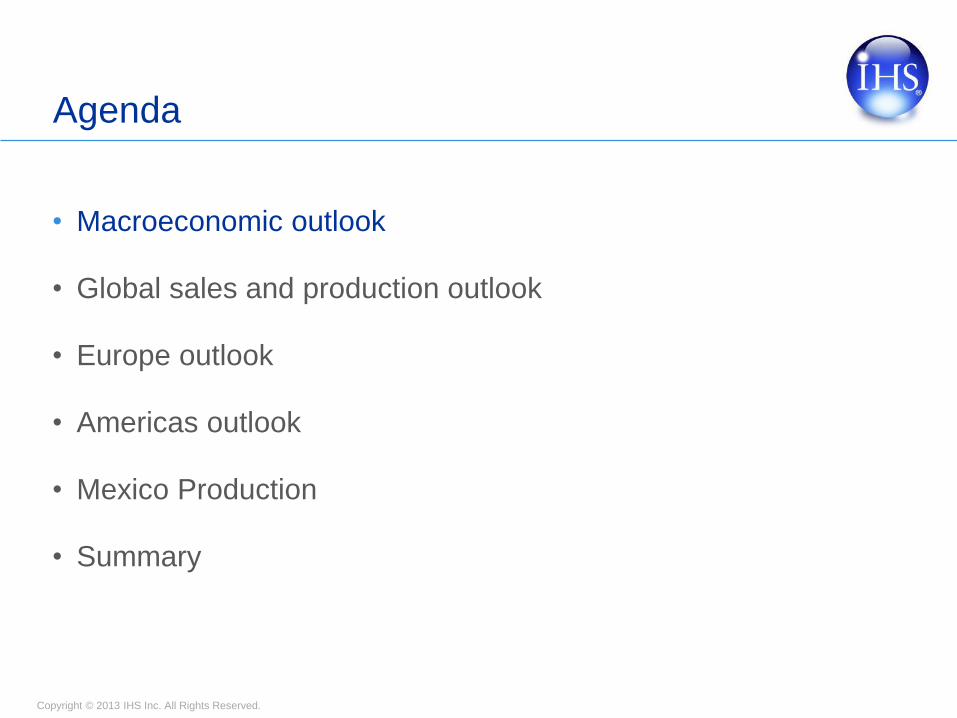

ASEAN C Europe E Europe

Gr China India Japan Korea

N America S America W Europe

Light vehicle selling rates Western and Central Europe still lag rest of world

Seasonally

adju

ste

d s

elli

ng r

ate

s

Indexed 2

007=

1

GC

IN

AS

NA

2007

sales level

Source: IHS Automotive analysis

CE

SA

JK

WE

Lehman Bros.

collapse

EE

Copyright © 2013 IHS Inc. All Rights Reserved.

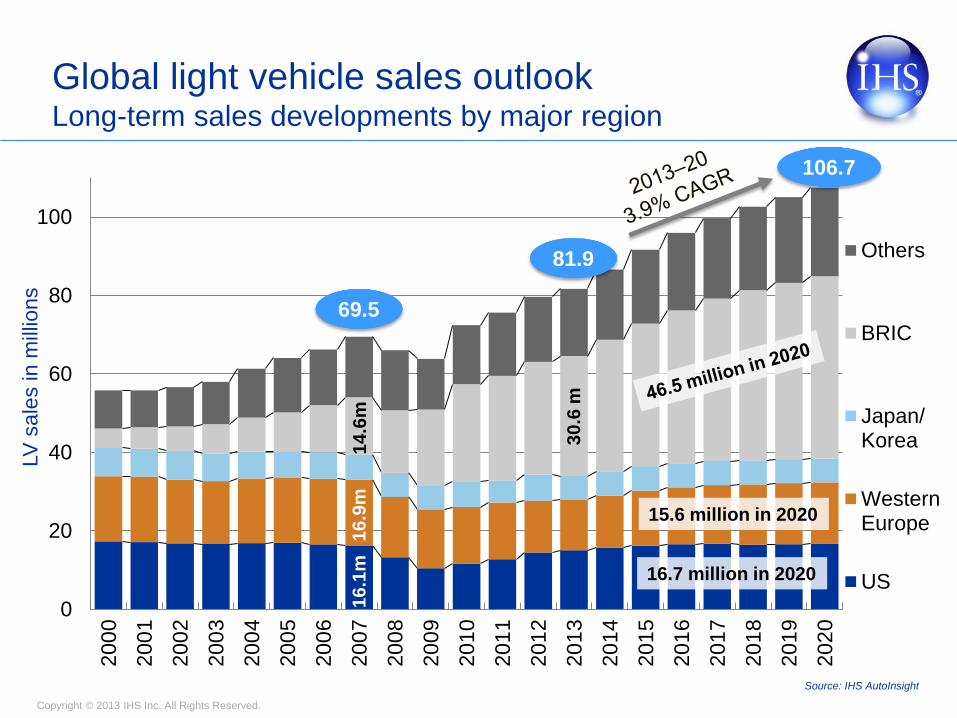

0

20

40

60

80

100

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

Others

BRIC

Japan/Korea

WesternEurope

US

81.9

LV

sale

s in m

illio

ns

69.5

106.7

Global light vehicle sales outlook Long-term sales developments by major region

30

.6 m

16.7 million in 2020

15.6 million in 2020

16

.9m

1

6.1

m

14

.6m

Source: IHS AutoInsight

Copyright © 2013 IHS Inc. All Rights Reserved.

Contingency risk: sales regions Fast-growing regions have largest downside potential

-18%

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

So

uth

Am

erica

Gre

ate

rC

hin

a

Ind

ian

Su

bco

ntin

en

t

AS

EA

N

Mid

dle

Ea

st/

Afr

ica

Ea

st

Eu

rop

e

No

rth

Am

erica

Ce

ntr

al

Eu

rop

e

Oce

an

ia

We

st

Eu

rop

e

Ja

pa

n/

Ko

rea

Pe

ssim

istic c

on

tin

gen

cy

Ch

an

ge

in

sa

les fro

m b

ase

fo

reca

st

World

average

Pessimistic total volume change in 2013-20

Copyright © 2013 IHS Inc. All Rights Reserved.

Agenda

• Macroeconomic outlook

• Global sales and production outlook

• Europe outlook

• Americas outlook

• Mexico

• Summary

Copyright © 2013 IHS Inc. All Rights Reserved.

Global light vehicle sales outlook 2011–13 sales volume

58

63

68

73

78

83

2011 2012 GreaterChina

NorthAmerica

Japan/Korea

SouthAsia

SouthAmerica

Central/East

Europe

MiddleEast/Africa

WestEurope

2013

75.7

million

79.5

million

1.9

million

827,000 26,000 351,000 138,000

-445,000

82.0

million

-478,000

Sa

les in

mill

ion

s

3.1%

135,000

Copyright © 2013 IHS Inc. All Rights Reserved.

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

10

20

30

40

50

60

70

80

90

100

2010 2011 2012 Feb 2013

YTD 2013 2014 2015

Global sales Change

Global sales

Sa

les in

mill

ion

s

Ye

ar-o

n-y

ea

r ch

an

ge

s

• In February 2013, global demand slipped 2.9% year-over-year (y/y), but most of the decline relates to

comparative seasonality issues relating to the lunar new year in China.

• From January to February 2013, global light vehicle sales grew an estimated 3.2% y/y. Gains in North

America, South Asia, China, and Eastern Europe have helped to fend off the negativity elsewhere in the

world.

• The light vehicle demand picture continues to be mixed, although bright spots remain, and for 2013, we

have penciled in 81.97 million units, a gain of 3.1%.

Copyright © 2013 IHS Inc. All Rights Reserved.

40

50

60

70

80

90

4

6

8

10

12

14

16

18

20

22

24

26

Jan2010

Apr2010

Jul2010

Oct2010

Jan2011

Apr2011

Jul2011

Oct2011

Jan2012

Apr2012

Jul2012

Oct2012

Jan2013

Apr2013

Jul2013

Oct2013

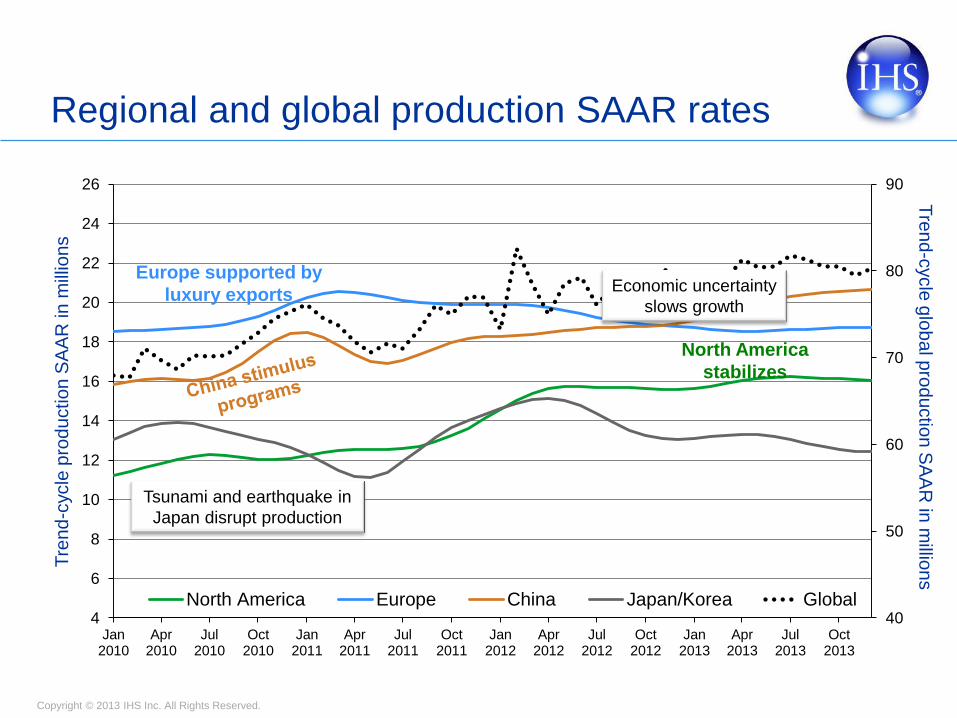

North America Europe China Japan/Korea Global

Regional and global production SAAR rates

Europe supported by

luxury exports

North America

stabilizes

Tre

nd-c

ycle

glo

ba

l pro

du

ctio

n S

AA

R in

millio

ns

T

ren

d-c

ycle

pro

du

ction

SA

AR

in

mill

ion

s

Tsunami and earthquake in

Japan disrupt production

Economic uncertainty

slows growth

Copyright © 2013 IHS Inc. All Rights Reserved.

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

0

10

20

30

40

50

60

70

80

90

100

2010 2011 2012 Feb2013

YTD 2013 2014 2015

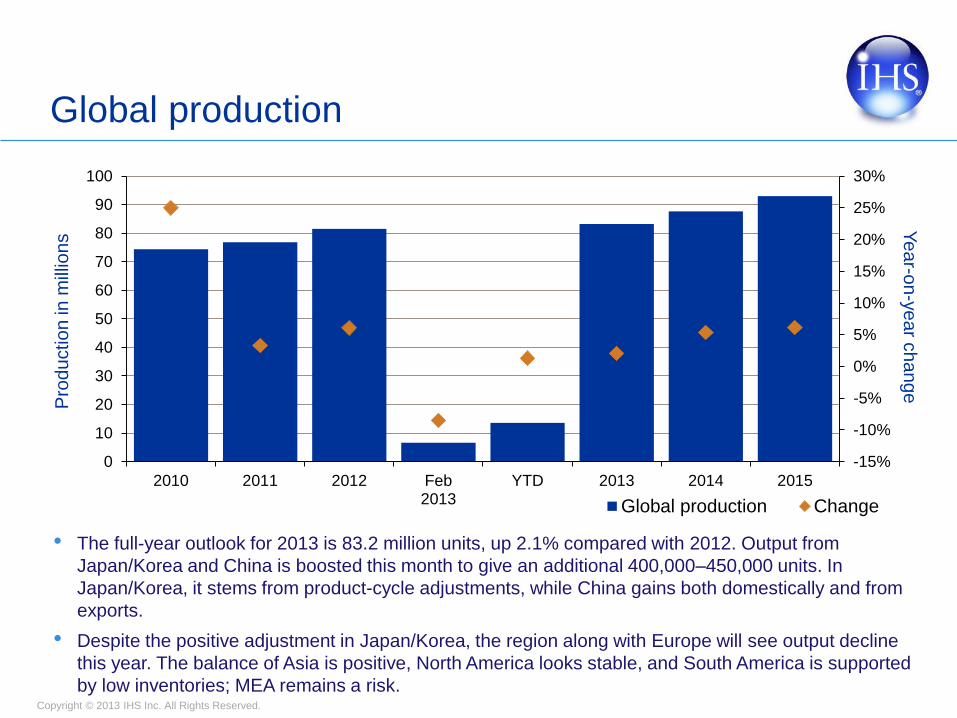

Global production Change

Global production

Pro

du

ctio

n in

mill

ion

s Y

ea

r-on-y

ea

r ch

an

ge

• The full-year outlook for 2013 is 83.2 million units, up 2.1% compared with 2012. Output from

Japan/Korea and China is boosted this month to give an additional 400,000–450,000 units. In

Japan/Korea, it stems from product-cycle adjustments, while China gains both domestically and from

exports.

• Despite the positive adjustment in Japan/Korea, the region along with Europe will see output decline

this year. The balance of Asia is positive, North America looks stable, and South America is supported

by low inventories; MEA remains a risk.

Copyright © 2013 IHS Inc. All Rights Reserved. 12

0

20

40

60

80

100

120

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

20

11

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

Millio

ns

Other ASEAN S AM India C/E EU China Japan/Kor W EU N AM

2013-20 Global Growth Rates Global Markets 3.8%

Developing Markets 5.8%

Developed Markets 1.5%

58

% D

eve

lop

ing

Re

gio

ns

Source: IHS Automotive Light Vehicle Production Forecast

Global Light Vehicle Production Near-Term Volatility, Long-Term Growth Trajectory

Copyright © 2013 IHS Inc. All Rights Reserved.

Agenda

• Macroeconomic outlook

• Global sales and production outlook

• Europe outlook

• Americas outlook

• The rest of the world

• Questions and answers

Copyright © 2013 IHS Inc. All Rights Reserved.

Euro crisis: Long-term bond yields ECB action easing fears; Cyprus may be trouble

Lo

ng

-term

bond y

ield

s

(in p

erc

ent)

Source: IHS DataInsight

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0F

eb'0

8

May'0

8

Aug'0

8

Nov'0

8

Fe

b'0

9

May'0

9

Aug'0

9

Nov'0

9

Fe

b'1

0

May'1

0

Aug'1

0

Nov'1

0

Fe

b'1

1

May'1

1

Aug'1

1

Nov'1

1

Fe

b'1

2

May'1

2

Aug'1

2

Nov'1

2

Fe

b'1

3

ItalyFranceUnited StatesGermanySpain

The cause of the

current euro crisis Breaking point threshold

Copyright © 2013 IHS Inc. All Rights Reserved.

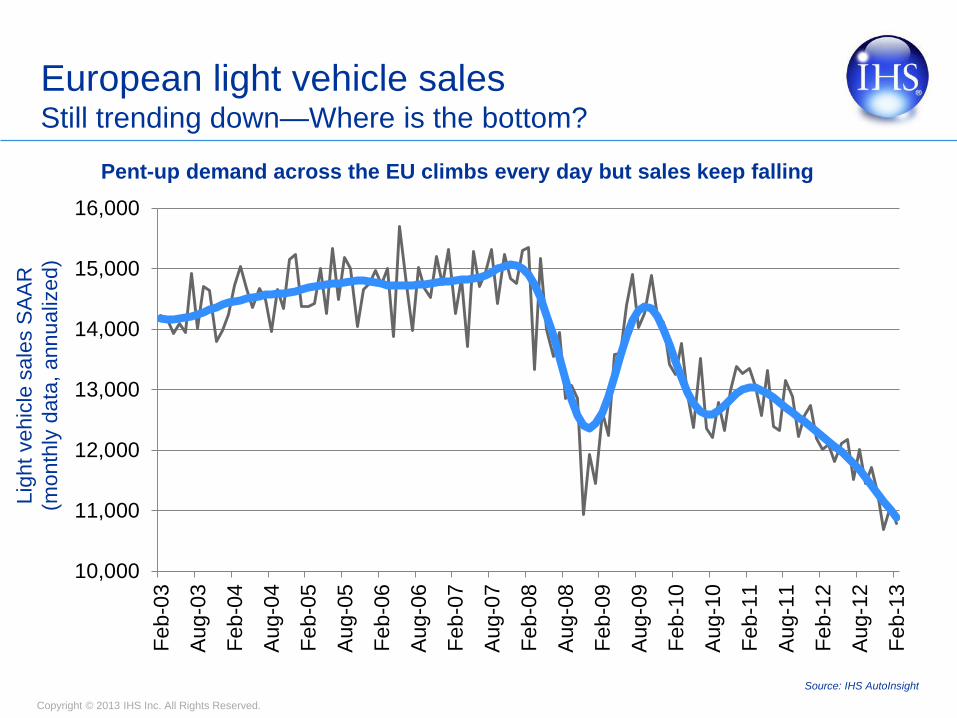

European light vehicle sales Still trending down—Where is the bottom?

Pent-up demand across the EU climbs every day but sales keep falling

10,000

11,000

12,000

13,000

14,000

15,000

16,000

Fe

b-0

3

Aug-0

3

Fe

b-0

4

Aug-0

4

Fe

b-0

5

Aug-0

5

Fe

b-0

6

Aug-0

6

Fe

b-0

7

Aug-0

7

Fe

b-0

8

Au

g-0

8

Fe

b-0

9

Aug-0

9

Fe

b-1

0

Aug-1

0

Fe

b-1

1

Aug-1

1

Fe

b-1

2

Aug-1

2

Fe

b-1

3

Lig

ht

vehic

le s

ale

s S

AA

R

(month

ly d

ata

, annualiz

ed)

Source: IHS AutoInsight

Copyright © 2013 IHS Inc. All Rights Reserved.

-8%

-6%

-4%

-2%

0%

2%

4%

6%

0

5

10

15

20

25

2010 2011 2012 Feb

2013

YTD 2013 2014 2015

Central Europe East Europe West Europe Change

Europe sales outlook S

ale

s in

mill

ion

s

Ye

ar-o

n-y

ea

r ch

an

ge

s

• In February 2013, European sales reached 1.22 million units, down 6.7% versus February 2012. This

result remains in line with the trend that was valid for most of 2012. Once again, Western Europe suffered

heavy declines (down 10.7%), whereas Central and Eastern Europe fared much better (up 4.6%).

Nevertheless, even this side of the continent has been experiencing a clear deceleration lately related to

the cooling off in the Russian market.

• For the near future, we expect the situation to remain bleak: following the 2012 decline, full-year 2013

should keep pointing down, not reaching the 18.0-million-units threshold.

Copyright © 2013 IHS Inc. All Rights Reserved.

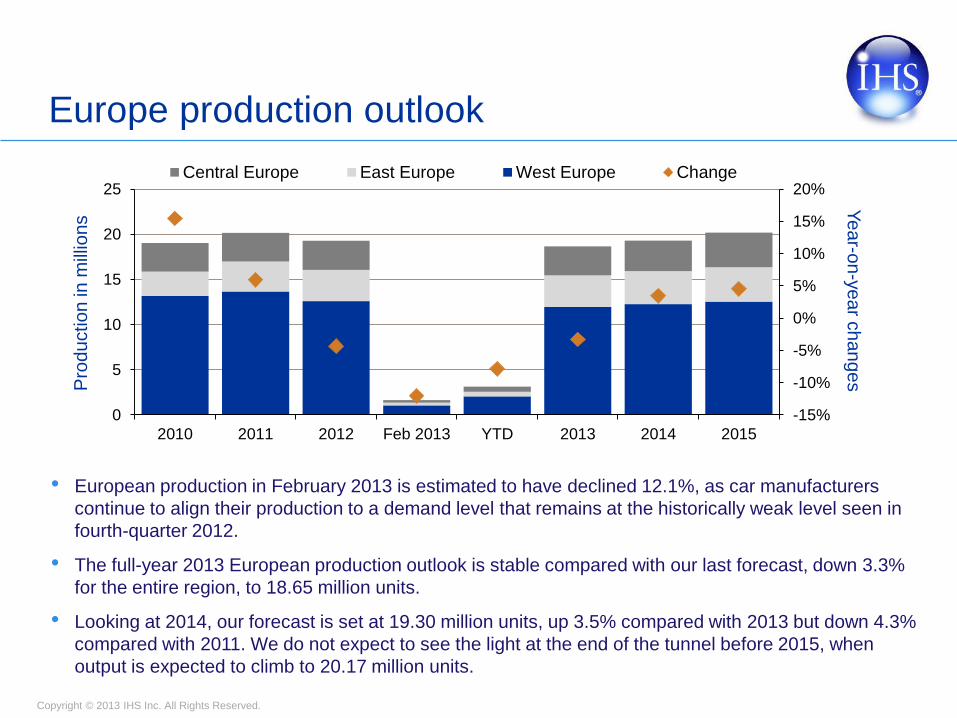

Europe production outlook P

rod

uctio

n in

mill

ion

s Y

ea

r-on-y

ea

r ch

an

ge

s

-15%

-10%

-5%

0%

5%

10%

15%

20%

0

5

10

15

20

25

2010 2011 2012 Feb 2013 YTD 2013 2014 2015

Central Europe East Europe West Europe Change

• European production in February 2013 is estimated to have declined 12.1%, as car manufacturers

continue to align their production to a demand level that remains at the historically weak level seen in

fourth-quarter 2012.

• The full-year 2013 European production outlook is stable compared with our last forecast, down 3.3%

for the entire region, to 18.65 million units.

• Looking at 2014, our forecast is set at 19.30 million units, up 3.5% compared with 2013 but down 4.3%

compared with 2011. We do not expect to see the light at the end of the tunnel before 2015, when

output is expected to climb to 20.17 million units.

Copyright © 2013 IHS Inc. All Rights Reserved.

Agenda

• Macroeconomic outlook

• Global sales and production outlook

• Europe outlook

• Americas outlook

• Mexico

• Summary

Copyright © 2013 IHS Inc. All Rights Reserved. 19

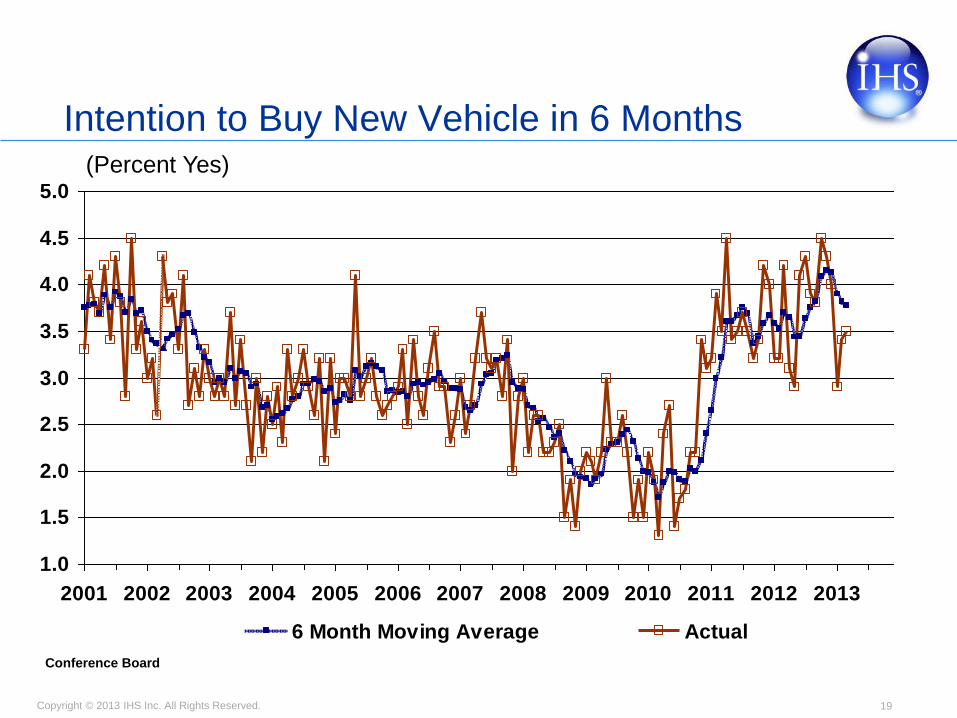

Intention to Buy New Vehicle in 6 Months

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

6 Month Moving Average Actual

(Percent Yes)

Conference Board

Copyright © 2013 IHS Inc. All Rights Reserved. 20

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

1975 1978 1981 1984 1987 1990 1993 1996 1999 2002 2005 2008 2011

Direct (Bank) Loans Indirect (Dealer) Loans

(% - Accounts past due 30 days or more)

Months

Source: American Bankers Association

New Auto Loans — Delinquency Rates

Copyright © 2013 IHS Inc. All Rights Reserved. 21

New Vehicle Buyers Average Credit Score

640

650

660

670

680

690

700

710

720

730

740

750

760

770

780

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13

6%7%8%9%10%11%12%13%14%15%16%17%18%19%20%21%22%

FICO SCORE % UNDER 670

Avg. Score

Source: CNW Marketing

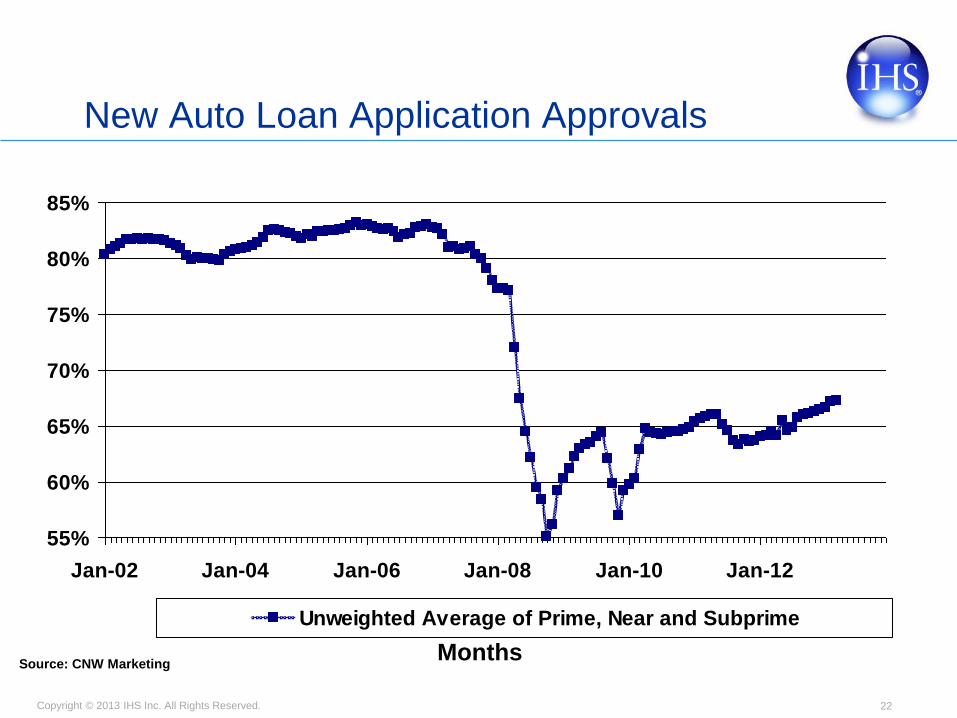

Copyright © 2013 IHS Inc. All Rights Reserved. 22

55%

60%

65%

70%

75%

80%

85%

Jan-02 Jan-04 Jan-06 Jan-08 Jan-10 Jan-12

Unweighted Average of Prime, Near and Subprime

Months

New Auto Loan Application Approvals

Source: CNW Marketing

Copyright © 2013 IHS Inc. All Rights Reserved. 23

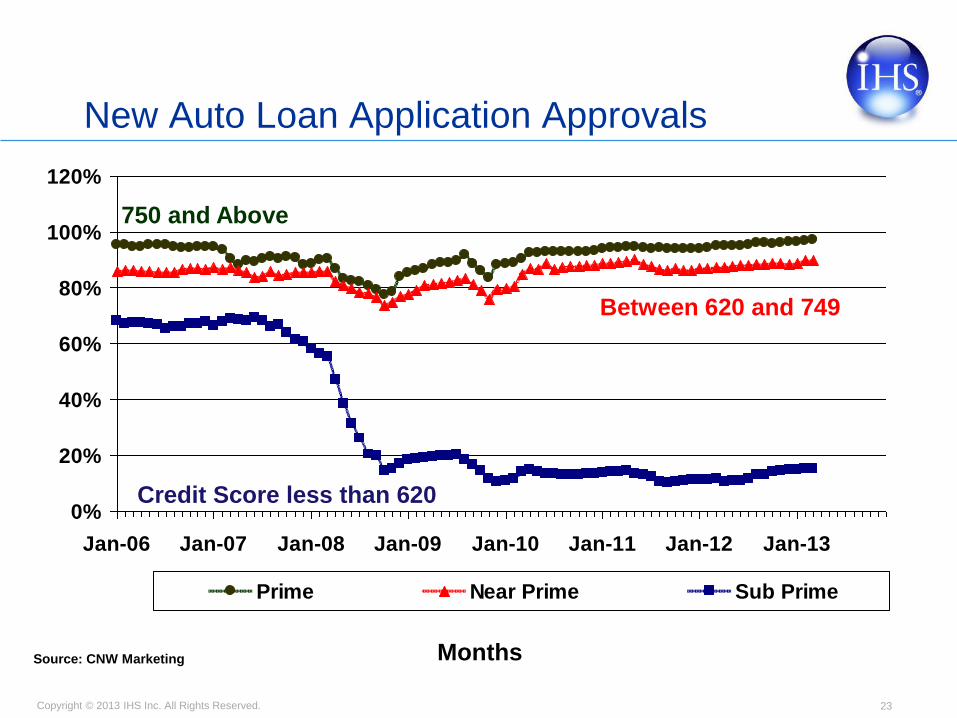

0%

20%

40%

60%

80%

100%

120%

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13

Prime Near Prime Sub Prime

Months

New Auto Loan Application Approvals

750 and Above

Between 620 and 749

Credit Score less than 620

Source: CNW Marketing

Copyright © 2013 IHS Inc. All Rights Reserved. 24

37

39

41

43

45

47

49

51

53

1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Months

(Years)

Median Age – New Vehicle Buyer

CNW Marketing

Copyright © 2013 IHS Inc. All Rights Reserved. 25

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

1998 2000 2002 2004 2006 2008 2010 2012

Quarters

(Percent)

Federal Reserve Board

New Auto Loan Rates – Commercial Banks

Copyright © 2013 IHS Inc. All Rights Reserved.

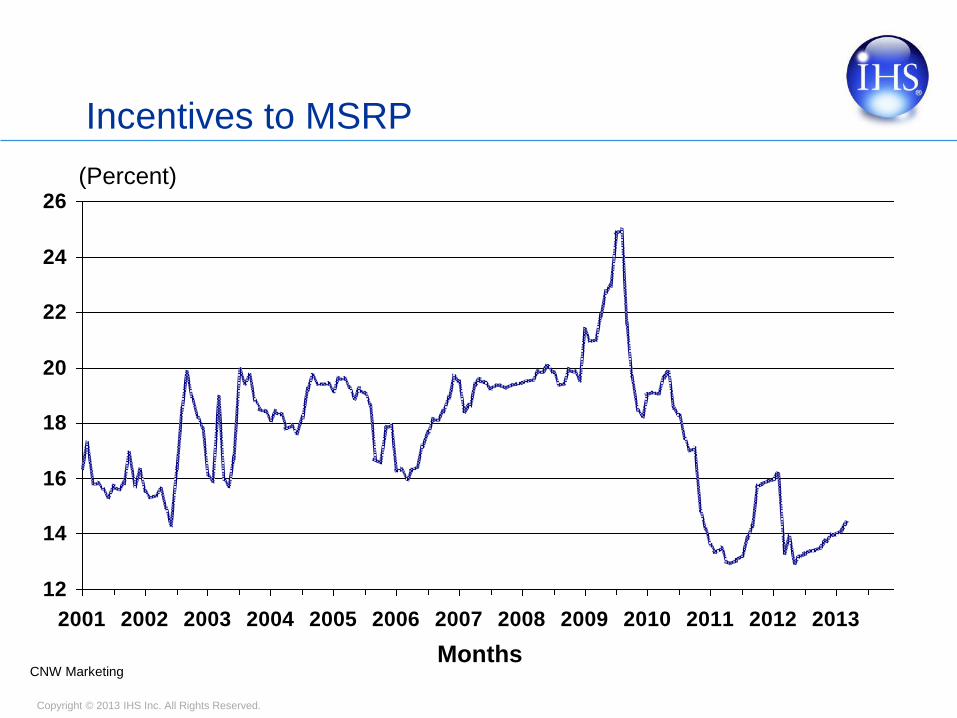

12

14

16

18

20

22

24

26

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

(Percent)

CNW Marketing Months

Incentives to MSRP

Copyright © 2013 IHS Inc. All Rights Reserved. 27

30%

40%

50%

60%

70%

80%

90%

100%

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13

GM Ford Chrysler IndustryToyota Honda Nissan

Source: CNW Marketing Months

Residual Value Index

(Index = Lease contract residual value versus CNW estimate of residual at end of lease term)

Copyright © 2013 IHS Inc. All Rights Reserved. 28

20%

21%

22%

23%

24%

25%

26%

27%

28%

29%

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13

Leases by Month

(Share)

U.S. Light Vehicle Sales — Lease Penetration

Source: CNW Marketing

Copyright © 2013 IHS Inc. All Rights Reserved. 29

U.S. Light Vehicle Inventory — Units

Months — Seasonally Adjusted

(Units in thousands)

1,500

2,000

2,500

3,000

3,500

4,000

4,500

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Copyright © 2013 IHS Inc. All Rights Reserved. 30

U.S. Light Vehicle Inventory — Days Supply

30

40

50

60

70

80

90

100

110

120

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

(Days Supply)

Months — Seasonally Adjusted

Light Trucks

Cars

Copyright © 2013 IHS Inc. All Rights Reserved.

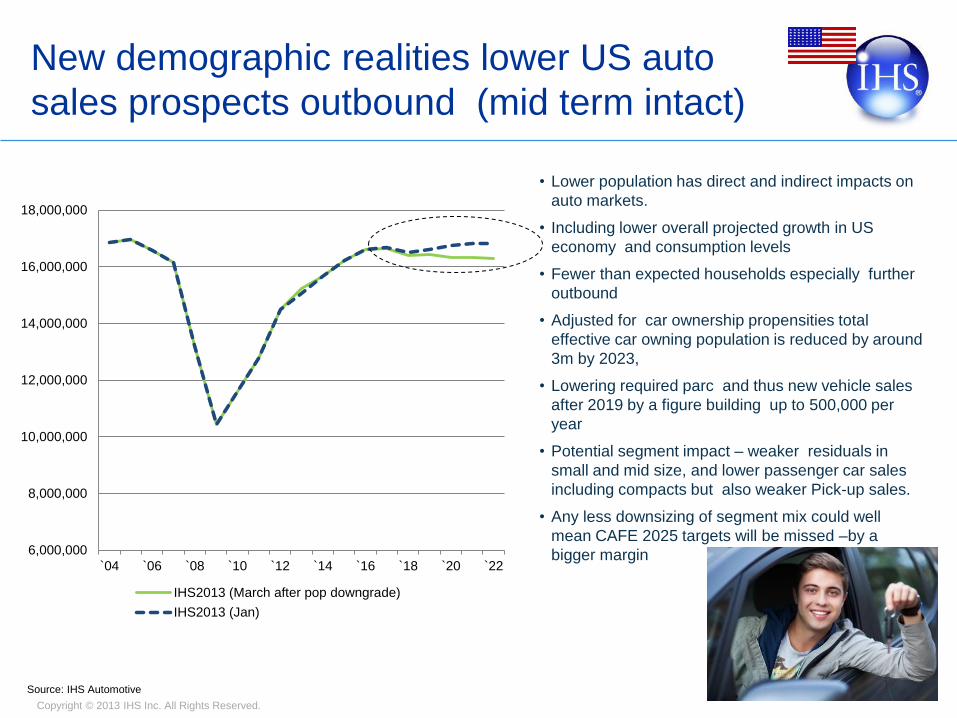

• Lower population has direct and indirect impacts on

auto markets.

• Including lower overall projected growth in US

economy and consumption levels

• Fewer than expected households especially further

outbound

• Adjusted for car ownership propensities total

effective car owning population is reduced by around

3m by 2023,

• Lowering required parc and thus new vehicle sales

after 2019 by a figure building up to 500,000 per

year

• Potential segment impact – weaker residuals in

small and mid size, and lower passenger car sales

including compacts but also weaker Pick-up sales.

• Any less downsizing of segment mix could well

mean CAFE 2025 targets will be missed –by a

bigger margin

Source: IHS Automotive

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

18,000,000

`04 `06 `08 `10 `12 `14 `16 `18 `20 `22

IHS2013 (March after pop downgrade)

IHS2013 (Jan)

New demographic realities lower US auto

sales prospects outbound (mid term intact)

Copyright © 2013 IHS Inc. All Rights Reserved. 32

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13

SUVL

(Units in millions)

United States — Light Vehicle Sales, SAAR

Copyright © 2013 IHS Inc. All Rights Reserved. 33

4

5

6

7

8

9

10

11

12

13

Jan-00 Jan-02 Jan-04 Jan-06 Jan-08 Jan-10 Jan-12

CARS LT. TRUCKS

(Units in millions)

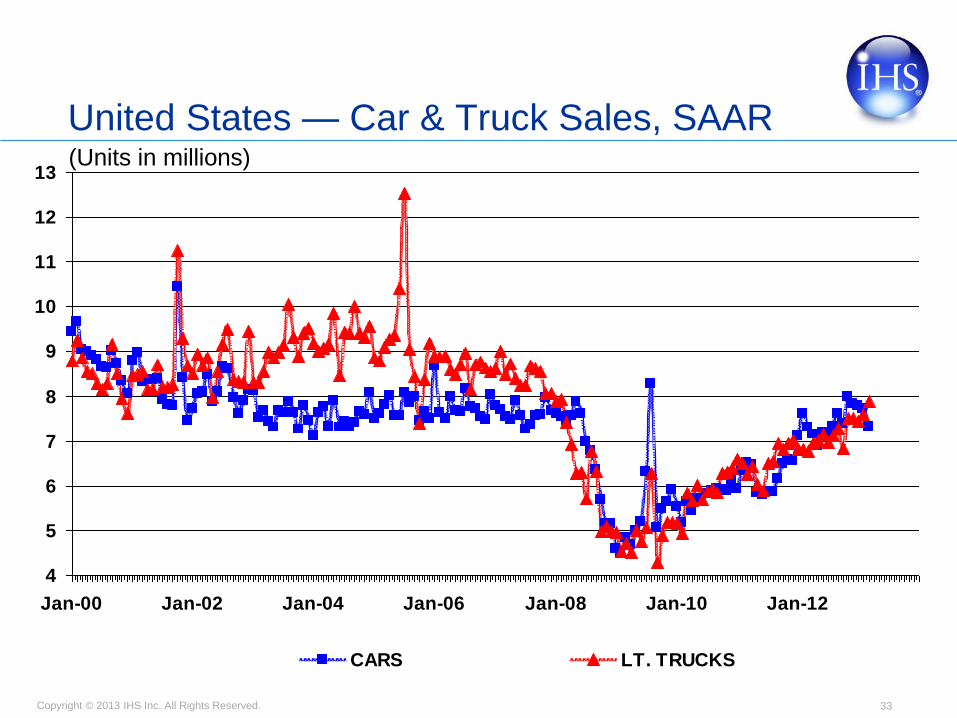

United States — Car & Truck Sales, SAAR

Copyright © 2013 IHS Inc. All Rights Reserved. 34

4

5

6

7

8

9

10

11

12

13

Jan-00 Jan-02 Jan-04 Jan-06 Jan-08 Jan-10 Jan-12

Months

(Units in millions)

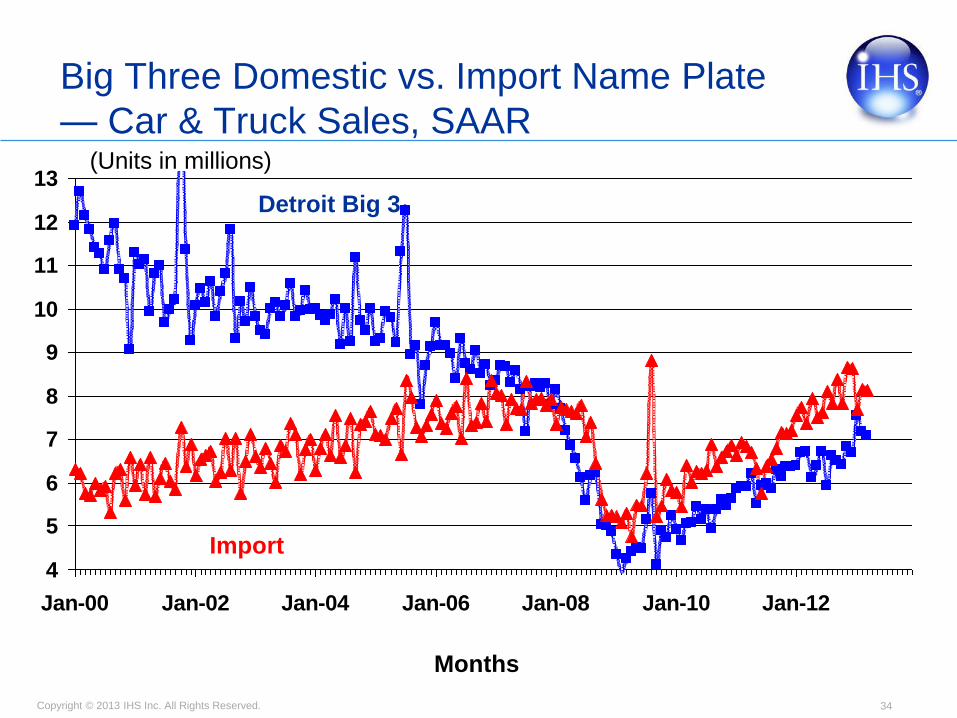

Big Three Domestic vs. Import Name Plate

— Car & Truck Sales, SAAR

Import

Detroit Big 3

Copyright © 2013 IHS Inc. All Rights Reserved.

0.5

1.0

1.5

2.0

2.5

3.0

Jan-95 Jan-97 Jan-99 Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13

TOYOTA HONDA NISSAN

Months

(Units in millions)

United States — Car & Truck Sales, SAAR

- Asian Manufacturers

X12A Seasonal Adjustment

Copyright © 2013 IHS Inc. All Rights Reserved.

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

Jan-95 Jan-97 Jan-99 Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13

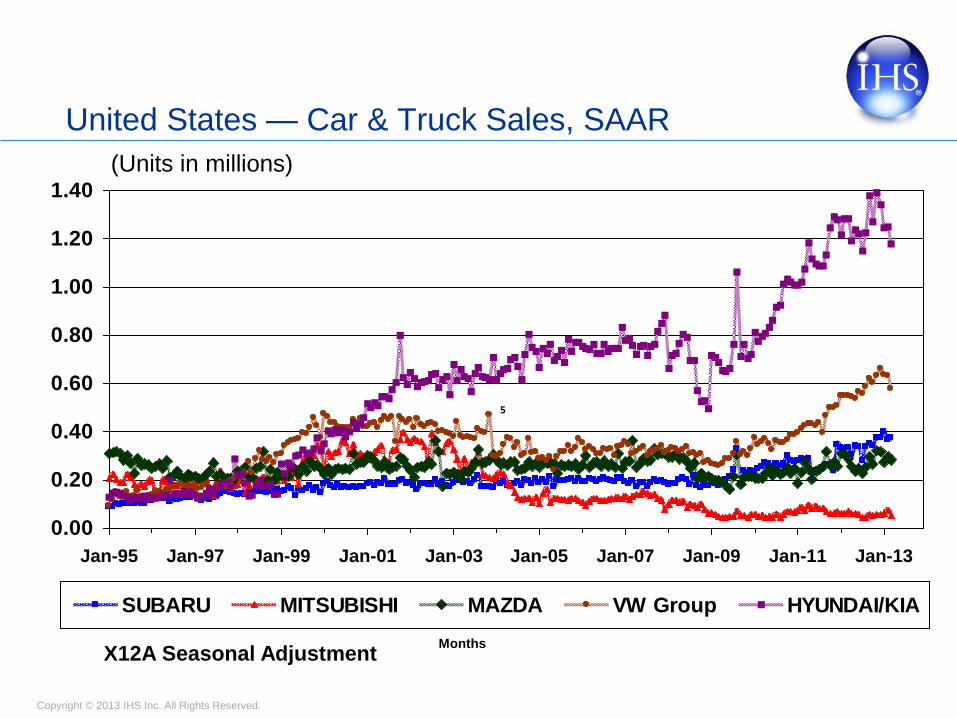

SUBARU MITSUBISHI MAZDA VW Group HYUNDAI/KIA

5

Months

(Units in millions)

United States — Car & Truck Sales, SAAR

X12A Seasonal Adjustment

Copyright © 2013 IHS Inc. All Rights Reserved.

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

2

4

6

8

10

12

14

16

18

2010 2011 2012 Feb2013

YTD 2013 2014 2015

United States Change

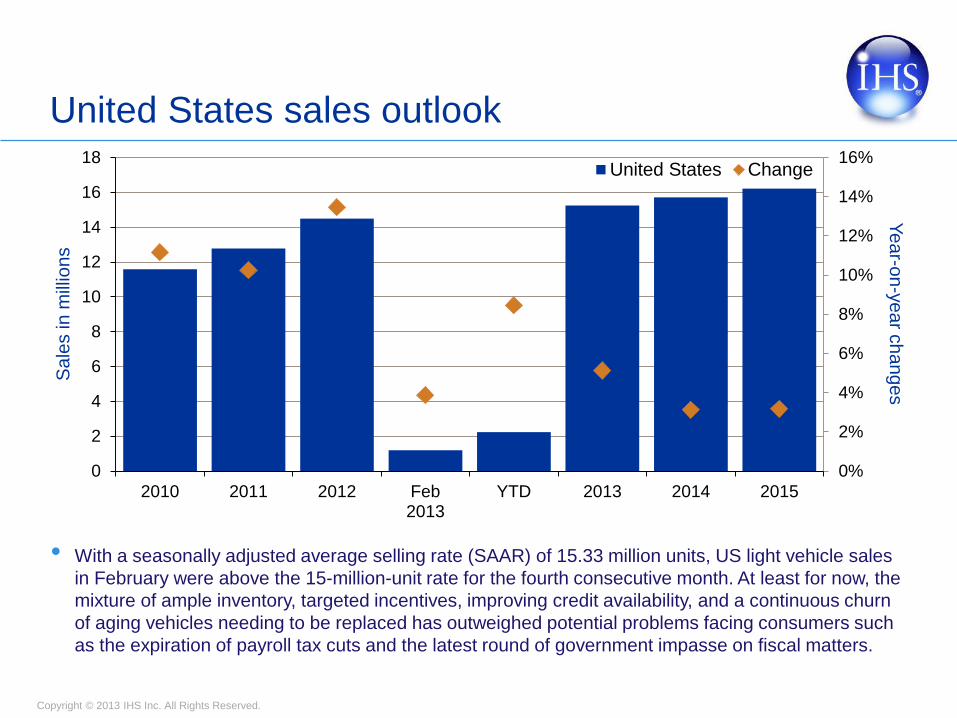

United States sales outlook

Sa

les in

mill

ion

s

Ye

ar-o

n-y

ea

r ch

an

ge

s

• With a seasonally adjusted average selling rate (SAAR) of 15.33 million units, US light vehicle sales

in February were above the 15-million-unit rate for the fourth consecutive month. At least for now, the

mixture of ample inventory, targeted incentives, improving credit availability, and a continuous churn

of aging vehicles needing to be replaced has outweighed potential problems facing consumers such

as the expiration of payroll tax cuts and the latest round of government impasse on fiscal matters.

Copyright © 2013 IHS Inc. All Rights Reserved.

-5%

0%

5%

10%

15%

20%

0

1

2

3

4

5

6

7

2010 2011 2012 Feb2013

YTD 2013 2014 2015

South America Change

-6%-4%-2%0%

2%4%6%8%10%

12%14%

0

1

2

3

4

5

6

2010 2011 2012 Feb2013

YTD 2013 2014 2015

South America Change

South America sales and production outlook

Sa

les in m

illio

ns

Ye

ar-o

n-y

ea

r ch

an

ge

s

Pro

du

ctio

n in m

illio

ns Y

ea

r-on

-ye

ar c

ha

nge

s

• Year to date, the region is

experiencing pent-up demand with a

5% uptick relative to 2012, reporting

906,000 units sold.

• IPI hike was delayed until the end of

the year.

• Venezuela is facing political

uncertainty.

• Credit limits Brazil, Argentina and

Colombia

• Full-year 2013 sales will essentially be

flat.

• South American production reached

292,660 units in February 2013, up

1.4% versus February 2012. Brazilian

output decreased 19.1% compared

with January 2013, reaching 212,945

units due to lower production days

and holidays.

• South American production volumes

of 4.45 million units in 2013 and 5.23

million units in 2015.

Copyright © 2013 IHS Inc. All Rights Reserved.

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0

2

4

6

8

10

12

14

16

18

2010 2011 2012 Feb2013

YTD 2013 2014 2015

North America Change

North America production P

rod

uctio

n in

mill

ion

s Y

ea

r-on-y

ea

r ch

an

ge

s

• North American output in February 2013 was flat, up just 5,800 units from year-ago levels to 1,329,648

units produced. Inventory levels at the end of February 2013 (US inventory stands at 3.23 million units)

have been largely replenished since supply-chain shocks in 2011 and 2012, resulting in more limited

incremental production gains in 2013.

• In February 2013, US production rose 1.4% to 890,005 units, up 12,354 units from year-ago levels. In

2013, US production of 10.73 million units will reflect a 6% gain in production levels to support stronger

sales.

• Forecast settings will reach 15.9 million units in 2013, rising to 16.3 million units in 2014 before breaking

the 17.0-million-unit mark in 2015.

Copyright © 2013 IHS Inc. All Rights Reserved. 40

North American Light Vehicle Production 2013 vs. 2012

OEM 2013F

(000s)

2012

(000s) % ∆

∆ Units

(000s)

GM 3,237 3,233 0.1% 4

Ford 3,003 2,842 5.7% 161

Chry/Fiat 2,457 2,371 3.6% 86

Detroit 3 8,697 8,446 3.0% 251

Toyota 1,782 1,776 0.3% 6

Honda 1,721 1,676 2.7% 45

Ren/Nissan 1,454 1,316 10.5% 138

Hyundai 722 714 1.1% 8

Asian 4 5,679 5,482 3.6% 197

VW 765 766 -0.1% -1

BMW 289 302 -4.3% -13

Daimler 176 191 -7.9% -15

German 3 1,230 1,259 -2.3% -29

Others 249 227 9.7% 22

Total 15.9M 15.4M 2.9% ~450

• Production growth rate

moderates, yet recovery

progresses

• GM – Significant launch

activity, including new

K2XX Pickups

• Chrysler – Fiat-based

product ramps-up

• Nissan – Migration of

CUV production; Mexico

expansion

• Transitional year prior to

new program/plant

launches in 2014/2015

Source: IHS Automotive Light Vehicle Production Forecast

Copyright © 2013 IHS Inc. All Rights Reserved.

North American Light Vehicle Production Compelling Growth Prospects

41

4.94.2

1.93.1 3.4 3.43.2

4.4

2.9

1.9

2.73.1 3.22.8

2.9

2.5

0.9

2.0

2.4 2.42.4

2.4

4.6

3.2

4.1

6.46.7

5.5

0.50.8

0.5

1.0

1.41.6

1.3

0

3

6

9

12

15

18

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Millio

ns

• Production outlook follows demand recovery with import substitution and export activity

providing additional support

• Most manufacturers are poised to post gains; favors OEMs with further capacity

expansion plans: BMW, Hyundai, VW, Nissan, Toyota & Honda

• Global product/platform strategies enable competitive sourcing shifts

15.6 15.1 German 3

Asian 4

Chrysler/

Fiat

Ford

General

Motors

Others

8.6

13.1

17.0 17.7

15.4

17.2

5.6

4.7

2.9

2.9

0.6

Source: IHS Automotive Light Vehicle Production Forecast

Copyright © 2013 IHS Inc. All Rights Reserved.

6

8

10

12

14

16

18

20

22

Mill

ions

NA Sales NA Production

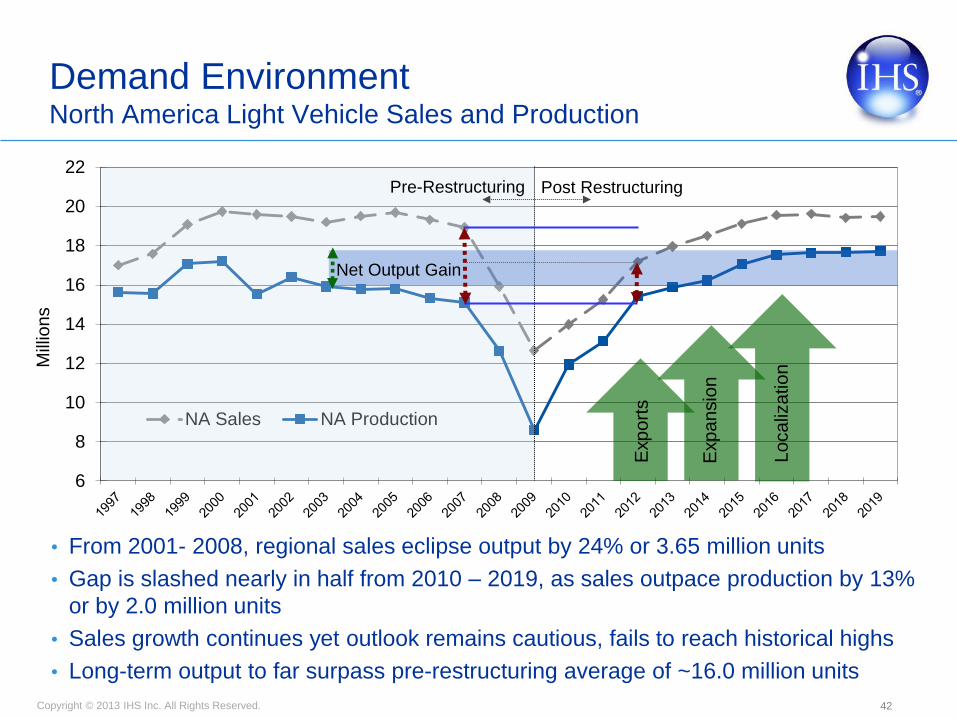

Demand Environment North America Light Vehicle Sales and Production

42

• From 2001- 2008, regional sales eclipse output by 24% or 3.65 million units

• Gap is slashed nearly in half from 2010 – 2019, as sales outpace production by 13%

or by 2.0 million units

• Sales growth continues yet outlook remains cautious, fails to reach historical highs

• Long-term output to far surpass pre-restructuring average of ~16.0 million units

Post Restructuring Pre-Restructuring

Net Output Gain

Lo

ca

liza

tio

n

Exp

an

sio

n

Exp

ort

s

Copyright © 2013 IHS Inc. All Rights Reserved. 43

Production Outlook North American Produced Vehicle Exports Bolster Prospects

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Europe

South America

Middle East/Africa

Greater China

Other

No

rth

Am

erica

n V

eh

icle

Exp

ort

s (

Mill

ion

s)

North American Vehicle Exports by Region

0.67

0.89

0.71

0.87 0.78

1.05

1.28 1.28

1.37

1.62

• Greater use of global

platforms allows for more

“export ready” product

• 40+ Free trade agreements

drive Mexican output

• Expansion of luxury

segment capability across

the region into Mexico

• EU sovereign debt crisis

tempers EU exports, yet

BRIC demand grows

• Sourcing patterns favor NA

expansion as a safe haven;

with currency hedge &

export prospects

1.78

Source: IHS Automotive Light Vehicle Forecast

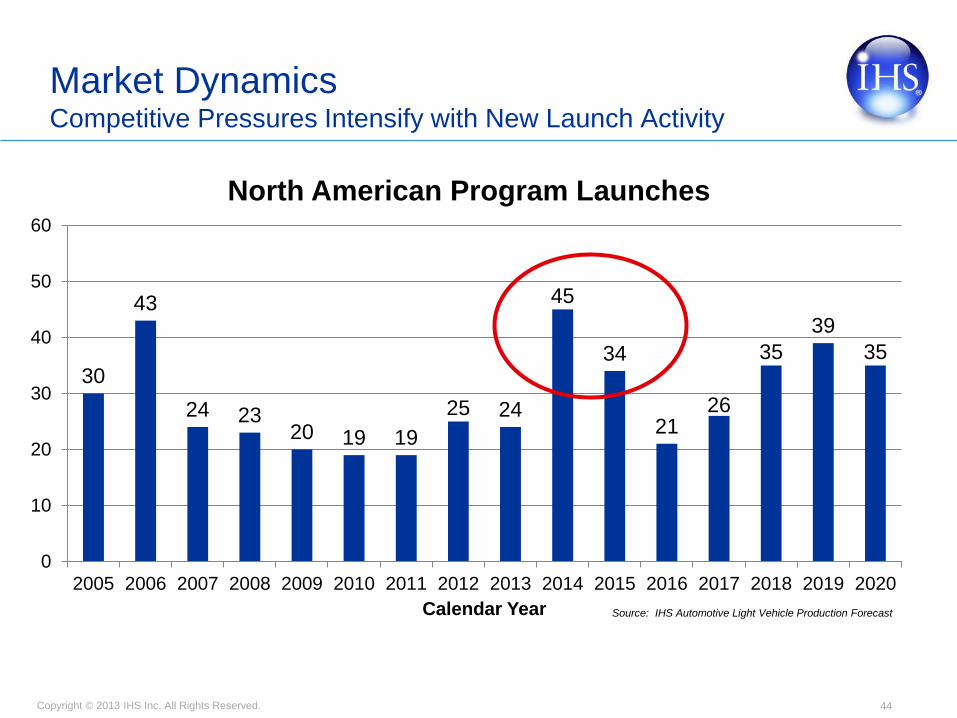

Copyright © 2013 IHS Inc. All Rights Reserved. 44

30

43

24 23 20 19 19

25 24

45

34

21 26

35

39

35

0

10

20

30

40

50

60

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Calendar Year

North American Program Launches

Market Dynamics Competitive Pressures Intensify with New Launch Activity

Source: IHS Automotive Light Vehicle Production Forecast

Copyright © 2013 IHS Inc. All Rights Reserved.

Production Outlook Global Output of D-/E-Segment CUVs By Region

• North America is the

leading producer of

high-margin CUVs

• Positioned evolved

from strength in SUV

category, comes full

circle via global

platform deployment

• Powertrain advances

help drive role as

global exporter: BRIC

markets, ME/Africa, S.

America, China, etc.

• Region holds global

sourcing position for

luxury & volume brands

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

NorthAmerica

Japan/Korea Europe GreaterChina

South Asia

Mil

lio

ns

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

Copyright © 2013 IHS Inc. All Rights Reserved. 46

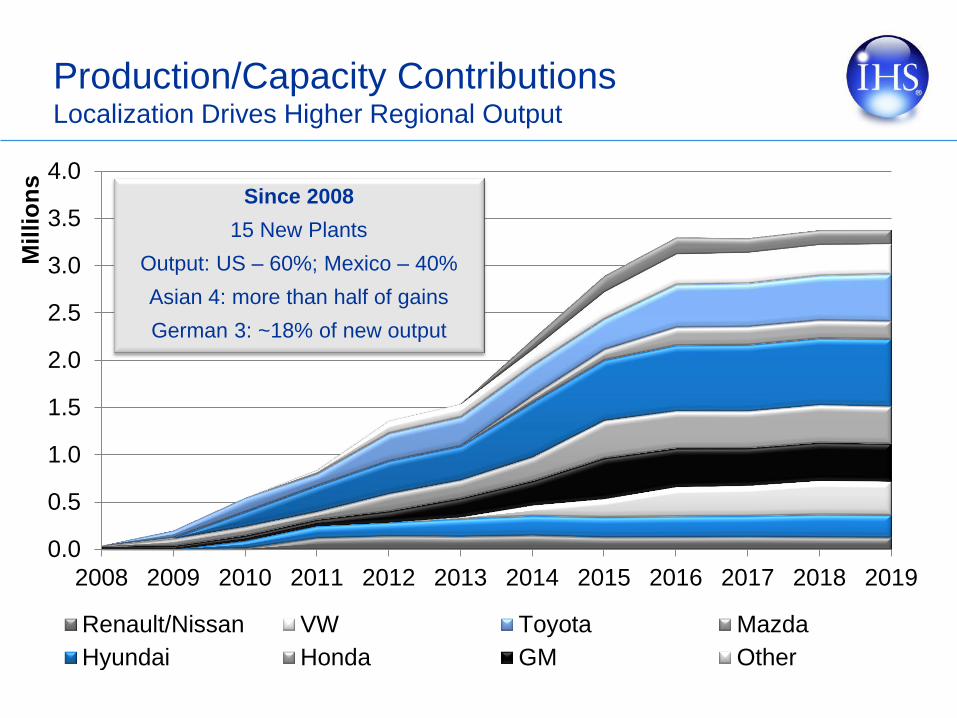

Production/Capacity Contributions Localization Drives Higher Regional Output

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Mil

lio

ns

Renault/Nissan VW Toyota Mazda

Hyundai Honda GM Other

Since 2008

15 New Plants

Output: US – 60%; Mexico – 40%

Asian 4: more than half of gains

German 3: ~18% of new output

Copyright © 2013 IHS Inc. All Rights Reserved.

Agenda

• Macroeconomic outlook

• Global sales and production outlook

• Europe outlook

• Americas outlook

• Mexico

• Summary

Copyright © 2013 IHS Inc. All Rights Reserved. 50

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1/1/1997 1/1/1999 1/1/2001 1/1/2003 1/1/2005 1/1/2007 1/1/2009 1/1/2011 1/1/2013

(Units in Millions)

Mexico Light Vehicle Sales —

Seasonally Adjusted Annual Selling Rate - SAAR

Monthly

Annual Average

Copyright © 2013 IHS Inc. All Rights Reserved. 51

70

80

90

100

110

120

700

800

900

1000

1100

1200

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

LV Sales (left scale) Consumer Confidence

Monthly Sales — Moving Average vs.

Consumer Confidence

Thousand Units Index

Copyright © 2013 IHS Inc. All Rights Reserved. 52

-30%

-20%

-10%

0%

10%

20%

30%

600,000

700,000

800,000

900,000

1,000,000

1,100,000

1,200,000

1,300,000

1,400,000

1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020Light Veh -L Annual Change -R

Mexico - Light Vehicle Sales

Units

Used car imports and credit availability limit growth

Copyright © 2013 IHS Inc. All Rights Reserved.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2007 2009 2011 2013 2015 2017 2019

Others Mitsubishi Daimler Suzuki BMW

Mazda Honda Toyota Ford Fiat

Volkswagen General Motors Renault/Nissan

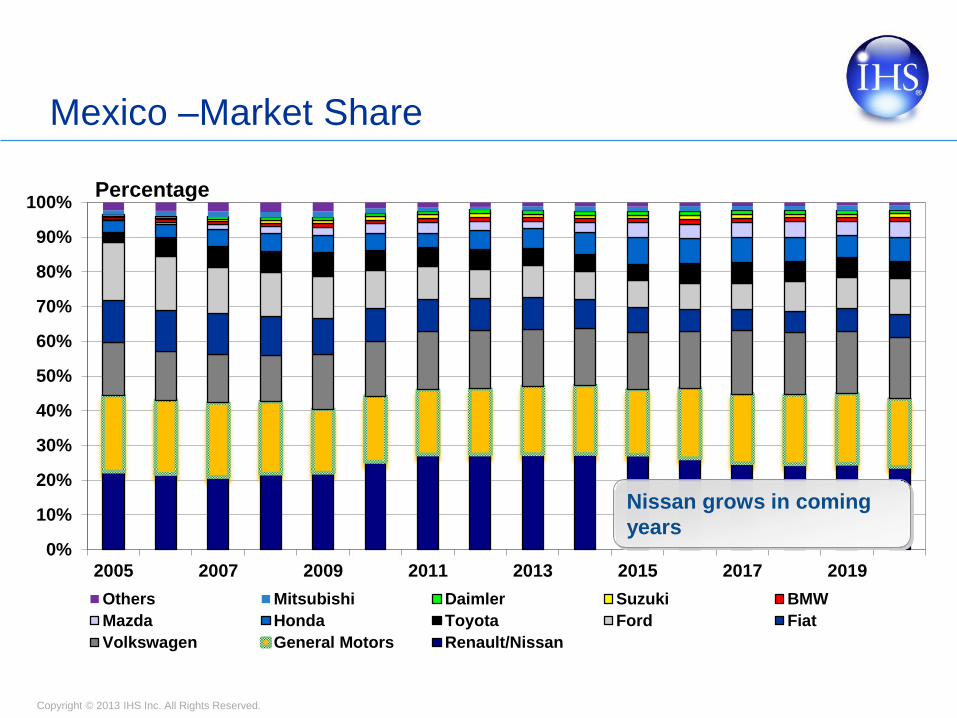

Percentage

Mexico –Market Share

Nissan grows in coming

years

Copyright © 2013 IHS Inc. All Rights Reserved. 54

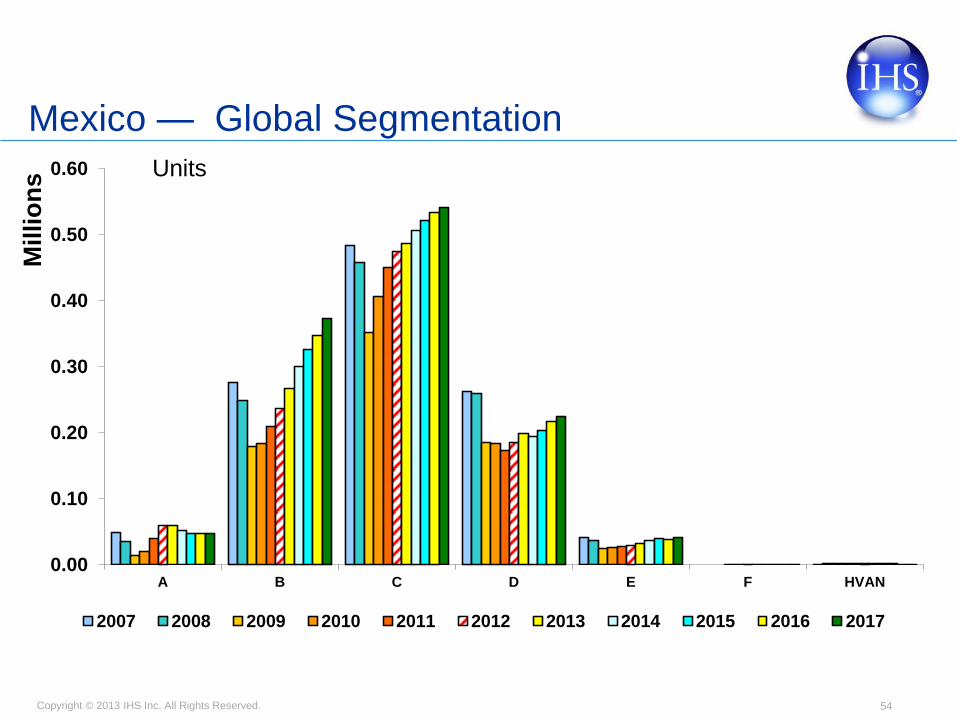

Mexico — Global Segmentation

0.00

0.10

0.20

0.30

0.40

0.50

0.60

A B C D E F HVAN

Mil

lio

ns

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Units

Copyright © 2013 IHS Inc. All Rights Reserved. 55

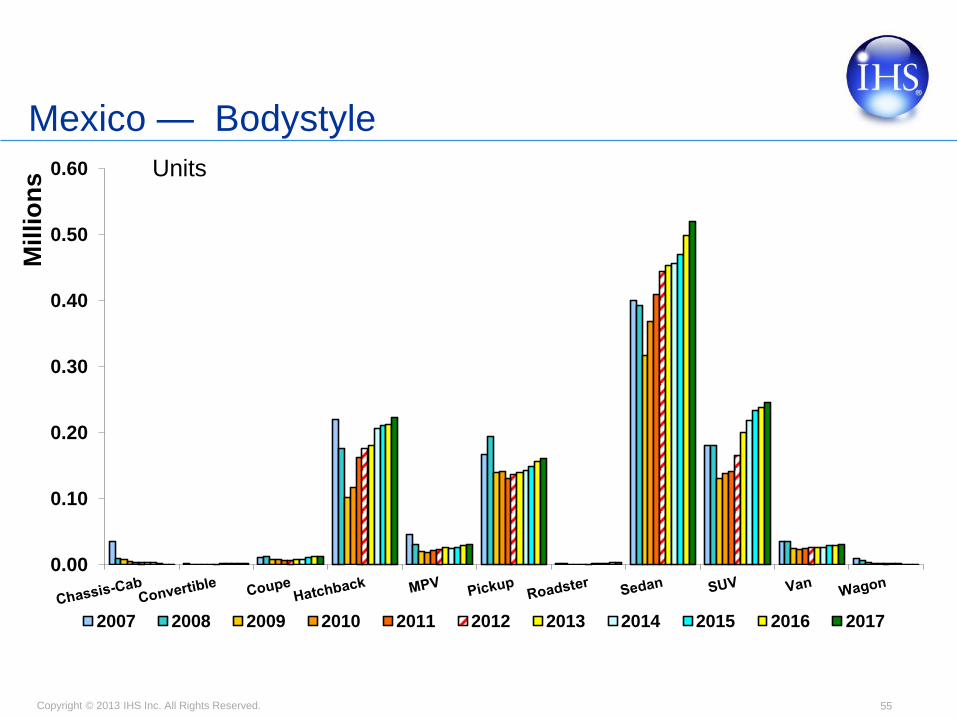

Mexico — Bodystyle

0.00

0.10

0.20

0.30

0.40

0.50

0.60

Millio

ns

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Units

Copyright © 2013 IHS Inc. All Rights Reserved. 56

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

PROD

Producing for Export

Mexico Light Vehicle Production (millions of units)

Forecast at risk due to Brazil

Copyright © 2013 IHS Inc. All Rights Reserved.

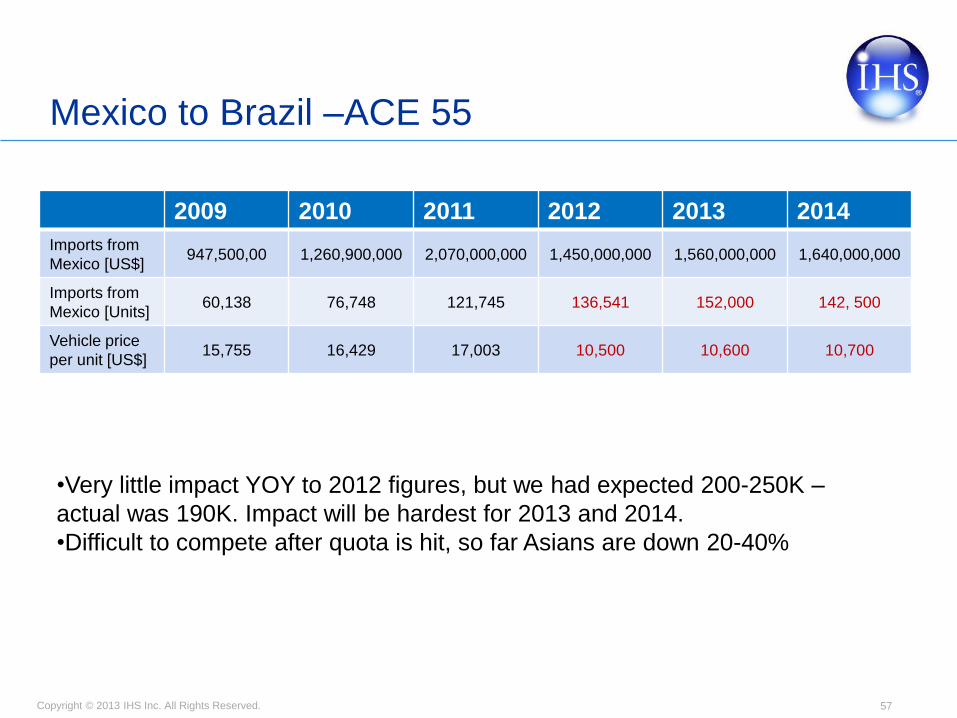

Mexico to Brazil –ACE 55

57

2009 2010 2011 2012 2013 2014

Imports from

Mexico [US$] 947,500,00 1,260,900,000 2,070,000,000 1,450,000,000 1,560,000,000 1,640,000,000

Imports from

Mexico [Units] 60,138 76,748 121,745 136,541 152,000 142, 500

Vehicle price

per unit [US$] 15,755 16,429 17,003 10,500 10,600 10,700

•Very little impact YOY to 2012 figures, but we had expected 200-250K –

actual was 190K. Impact will be hardest for 2013 and 2014.

•Difficult to compete after quota is hit, so far Asians are down 20-40%

Copyright © 2013 IHS Inc. All Rights Reserved.

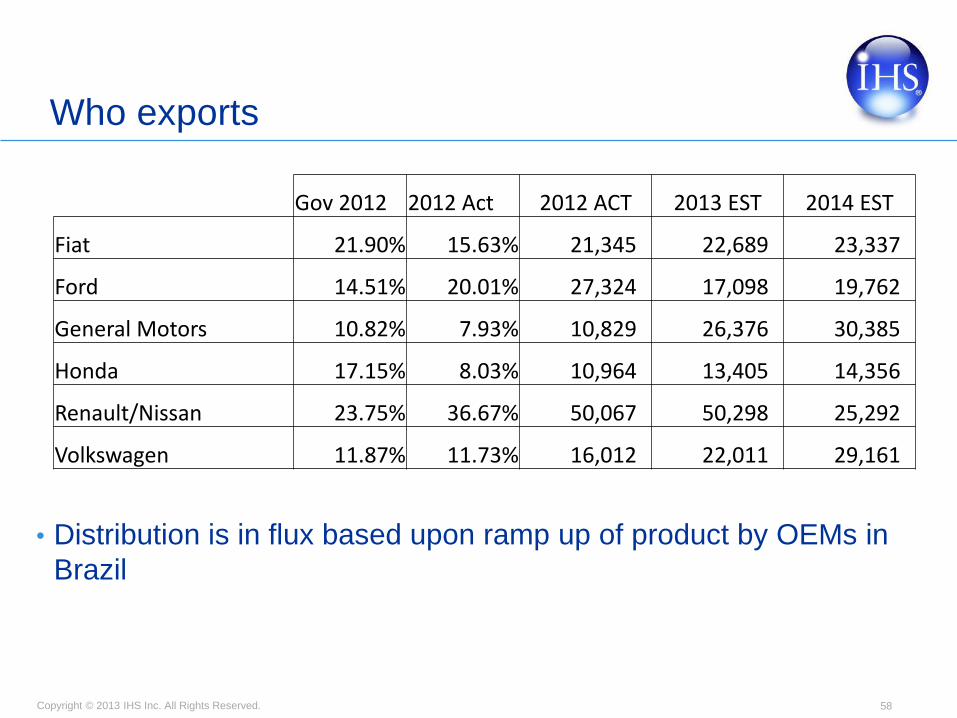

Who exports

• Distribution is in flux based upon ramp up of product by OEMs in

Brazil

58

Gov 2012 2012 Act 2012 ACT 2013 EST 2014 EST

Fiat 21.90% 15.63% 21,345 22,689 23,337

Ford 14.51% 20.01% 27,324 17,098 19,762

General Motors 10.82% 7.93% 10,829 26,376 30,385

Honda 17.15% 8.03% 10,964 13,405 14,356

Renault/Nissan 23.75% 36.67% 50,067 50,298 25,292

Volkswagen 11.87% 11.73% 16,012 22,011 29,161

Copyright © 2013 IHS Inc. All Rights Reserved. 59

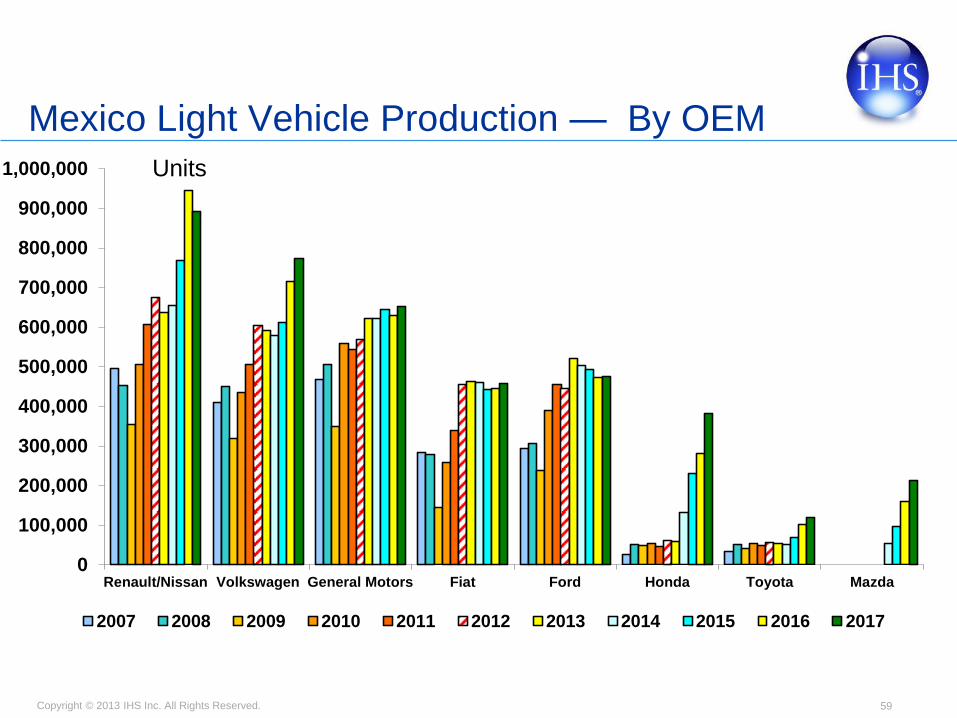

Mexico Light Vehicle Production — By OEM

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

Renault/Nissan Volkswagen General Motors Fiat Ford Honda Toyota Mazda

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Units

Copyright © 2013 IHS Inc. All Rights Reserved.

Agenda

• Macroeconomic outlook

• Global sales and production outlook

• Europe outlook

• Americas outlook

• Mexico

• Summary

Copyright © 2013 IHS Inc. All Rights Reserved.

Bottom Line

• With the exception of Western Europe, global demand will continue to gather momentum

• The US has turned the corner, promising outlook for sales and production

• Risks are still out there for US and EU

• Mexican demand has broken the million unit mark!

• Mexico has to explore new opportunities given this scenario, South America presents great potential

• Production is promising but big uncertainties lie in the future

Copyright © 2013 IHS Inc. All Rights Reserved.

Thank you for your participation! April 2013

Guido Vildozo Manager, Latin America Vehicle Sales Forecasts +1 781-301-9037 [email protected]

Copyright © 2013 IHS Inc. All Rights Reserved.

Copyright © 2013 IHS inc.

IHS inc. is the copyright holder for this document. No part(s) of this document may be copied,

downloaded, stored in a retrieval system, further transmitted or otherwise reproduced, stored,

disseminated, transferred or used in any form or by any means without prior written agreement from

IHS inc. Each reproduction of any part of this document must contain notice of the IHS inc. copyright as

follows: © 2013 IHS inc. Viewing and/or using the data contained in this copyrighted document shall

constitute a contract between the viewer and/or user and IHS that the viewer and/or user will not violate

the IHS inc. above stated copyright policy. By viewing and/or using the data contained in this

copyrighted document, the viewer and/or user warrants that he/she is authorized and has the full

authority to bind any corporate entity that may benefit from said viewing and/or use to the above

referenced copyright contract and a general subscription contract for the viewing and/or use of the

document, including payment of all subscription fees.

Disclaimer

All information included in this report has been cross-verified to the greatest extent possible. Although

every attempt has been made to ensure the accuracy of the information included in this report, IHS inc.

claims no responsibility for any loss or damage resulting from any publication, error or omission in this

report.