Embed Size (px)

Citation preview

1643 Merrimac Trail, Williamsburg, VA 23185

WWW.BORRELLASSOCIATES.COM

©2020 Borrell Associates Inc. All Rights Reserved

2020AUTOMOTIVEADVERTISING OUTLOOK

FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING

PRICE: $1,195

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 02

Executive Summary ............................................................................................... 03

Chapter 1: “New” Yields to “Almost New,” Altering the Landscape ................ 04Figure 1.1 U.S. New-Vehicle Sales Vs. Licensed Drivers, 2001-2025 ................................04Figure 1.2 New and “Nearly New” Vehicle Sales, 2012-2020 ..............................................06Figure 1.3 U.S. Average Ad Spending Per Vehicle Sold, 2014-2020..................................06Figure 1.4 Forecast U.S. New-Vehicle Annual Sales: Current Forecast vs. Alternatives ...............................................................................................07

Chapter 2: 2020 Automotive Ad-Spending Forecasts ......................................... 08Figure 2.1: 2020 U.S. Automotive Advertising, By Who Spends It .....................................08Figure 2.2: Projected 2020 U.S. Ad Spending to Support New-Vehicle Sales ................ 09Figure 2.3: 2018-2020 Change in Average Per-Vehicle Ad Spending for New Cars...... 09Figure 2.4: 2020 Projected U.S. Auto Dealer Ad Spending .................................................10Figure 2.5: Number of U.S. Independent Dealerships, 2010-2024 ...................................11

Chapter 3: Digital Advertising Forecasts ............................................................. 15Figure 3.1: 2020 Digital Auto Ad Spending for Dealers, Manufacturers & Private Party ...................................................................................................15Figure 3.2: 2020 Projected U.S. Auto Digital Ad Spending ..................................................15Figure 3.3: Franchised Auto Dealer Digital Ad Spending, 2018-2025...............................16Figure 3.4: Independent Auto Dealer Digital Ad Spending, 2018-2025 ...........................17Figure 3.5: Dealer Association Digital Ad Spending, 2018-2025 ........................................18Figure 3.6: Auto Manufacturer Digital Ad Spending, 2018-2025 .......................................19

Conclusions ............................................................................................................. 20

Appendix A: Other Scenarios ................................................................................ 21

Appendix B: Automotive LA$R ............................................................................. 23

About Borrell Associates ....................................................................................... 32

PRINCIPAL AUTHOR OF THIS REPORT

KIP CASSINOAuthor and Research Analyst

BORRELL ASSOCIATES LEADERSHIP TEAM:

COLBY ATWOOD Executive Director and Senior Advisor

GORDON BORRELL CEO

JIM BROWN Executive Vice President of Sales and Marketing

COREY ELLIOTT Executive Vice President of Local

Market Intelligence

WWW.BORRELLASSOCIATES.COM

CONTENTS

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 03

EXECUTIVE SUMMARY

The gears continue to turn in one of the largest and most important advertising verticals, automotive. But the gears are turning slowly, shifting from mass messaging and toward targeted messages. The biggest driver isn’t so much the appeal of targeting offered by digital channels as it is a change in consumer buying patterns. Car buyers have become far more interested in “almost new” vehicles. The problem is, more than three-fourths of automotive advertising is driven by the marketing of “new” vehicles.

This report details the massive U.S. Automotive Advertising category, which we’re forecasting to be $33.3 billion this year. New-vehicle advertising, at $26 billion, is declining at an average annual rate of 3.1%.

The new-car advertising decline is due in part to price compression, as the industry shifts to lower-priced targeted advertising, but also to depressed new-vehicle sales. For 2020, we’re forecasting new-car sales at 16.48 million – more than half a million less than 2019’s 17.04 million. The trend is more vivid framed in a 20-year perspective: There’s been a 21.3% increase in the number of licensed drivers in the past two decades, but a 3.7% decline in the number of new vehicles sold annually. It’s why so much advertising has shifted from top-of-the-funnel branding to lower-level “information” based advertising keyed more to availability, pricing, and financing.

Targeting has hit broadcasters particularly hard. Local dealerships now favor digital media and direct mail – both very targeted forms of marketing – to the point at which broadcast TV now gets less than 4% of dealer ad budgets. Meanwhile, direct mail now gets four times the share of TV, and digital media 15 times the share.

Paid search once took the lion’s share of automotive dollars. Control has shifted to targeted banner advertising and, more recently, streaming video. The video portion is now being driven by OTT sales, which has become a cheaper and more targeted alternative to broadcast TV. Combined, targeted display and streaming video account for 64% of digital expenditures and 40% of all advertising expenditures by dealers, manufacturers, and third-party advertisers. We foresee that dominance increasing over the next five years for franchised auto dealers.

In this report, we detail the underlying factors driving the gears of U.S. automotive advertising and examine each of the five buying segments: manufacturers, franchise dealers, dealer associations, independent dealers, and private-party advertising. Forecasts for 2020 and 2025 for each are included. We also lay out several scenarios of how forecasts might change due to potential shifts in economic and regulatory matters.

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 04

C H A P T E R 1 : “NEW” YIELDS TO “ALMOST NEW,” ALTERING THE LANDSCAPE

Automotive advertising is driven heavily by what’s new and exciting, whether it’s automated parking, a multi-position tailgate, or a back-up camera that can make your trailer invisible. But more and more, “new” cars aren’t driving sales. At least, not like they used to. Despite 40 million more licensed drivers on the road today than in 2001, there will be more than 600,000 fewer new vehicles sold. To put it differently, there’s been a 21.3% increase in licensed drivers in the past two decades, but a 3.7% decline in the number of new vehicles sold annually. It’s one of the reasons so much advertising has shifted from top-of-the-funnel branding to lower-level “information” based advertising keyed more to availability, pricing, and financing.

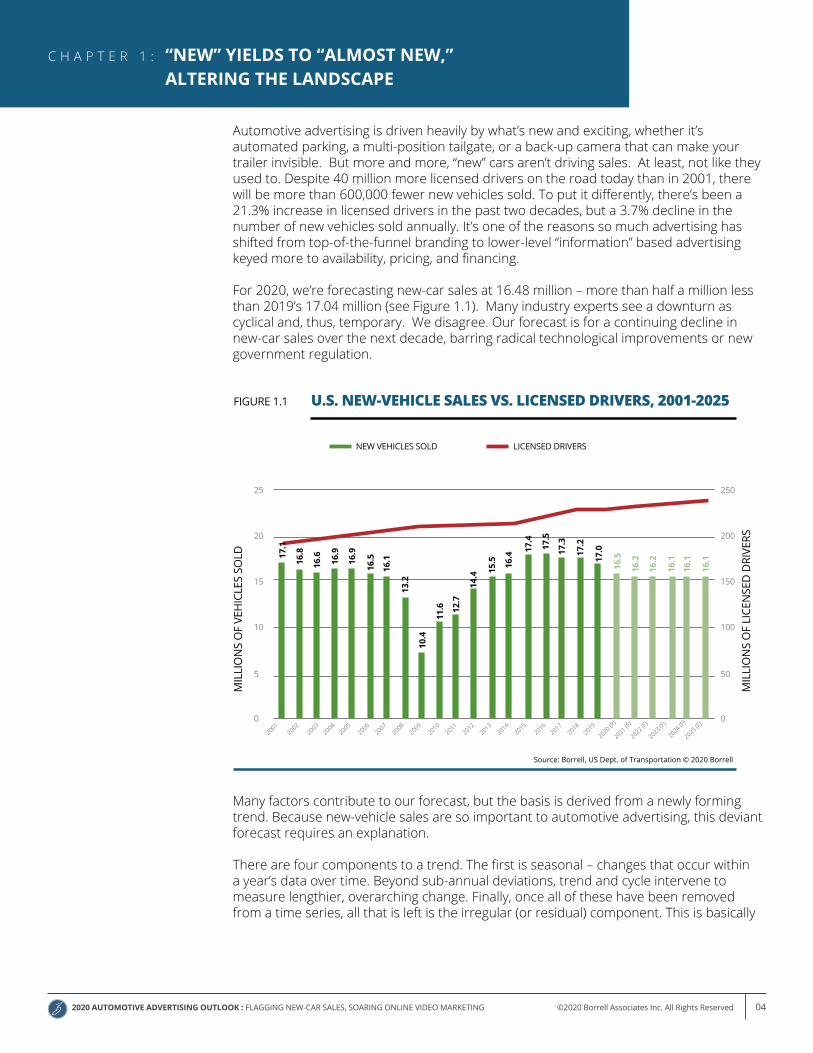

For 2020, we’re forecasting new-car sales at 16.48 million – more than half a million less than 2019’s 17.04 million (see Figure 1.1). Many industry experts see a downturn as cyclical and, thus, temporary. We disagree. Our forecast is for a continuing decline in new-car sales over the next decade, barring radical technological improvements or new government regulation.

Many factors contribute to our forecast, but the basis is derived from a newly forming trend. Because new-vehicle sales are so important to automotive advertising, this deviant forecast requires an explanation.

There are four components to a trend. The first is seasonal – changes that occur within a year’s data over time. Beyond sub-annual deviations, trend and cycle intervene to measure lengthier, overarching change. Finally, once all of these have been removed from a time series, all that is left is the irregular (or residual) component. This is basically

Source: Borrell, US Dept. of Transportation © 2020 Borrell

U.S. NEW-VEHICLE SALES VS. LICENSED DRIVERS, 2001-2025FIGURE 1.1

MIL

LIO

NS

OF

VEH

ICLE

S SO

LD

MIL

LIO

NS

OF

LICE

NSE

D D

RIVE

RS

25

20

15

10

5

02001

20062011

20162002

20072012

2017

2021 (F)

20032008

20132018

2022 (F)

20042009

20142019

2023 (F)

20052010

2015

2020 (P)

2024 (F)

2025 (F)

250

200

150

100

50

0

16.5

16.1

11.6

13.2

12.7

14.4 15

.5

10.4

16.4

17.4

17.5

17.3

17.2

17.0

16.5

16.2

16.2

16.1

16.1

16.117

.1

16.8

16.9

16.9

16.6

NEW VEHICLES SOLD LICENSED DRIVERS

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 05

“noise” – the random leftovers once all explainable trend components have been removed. Typically of small value, irregulars are generally ignored when trend analysis is performed.

Irregulars can serve an important purpose. When their values climb from small to more noticeable, they signal failure of the computed trend to accurately explain what has happened to the measured event over time – and invalidate the established relationships as clear forecasters of future activity. Irregulars now become a “tripwire” that can warn analysts of changes which have ended the utility of the time series they have come to depend upon.

U.S. new car sales trends crossed this tripwire in 2007, when the first warnings of the Great Recession were sounded. Indicators are calling new-car sales forecasts into question once again. The solid trend-cycle relationship which asserted itself as the nation climbed out of recession is no longer valid. A new trend is beginning.Four factors have contributed heavily to this realignment:

1. The rise in the price of used cars, which now stands at almost 65% of new-carprices. As auto auction house Manheim has observed, once the pricing of usedcars approaches this level, the clear distinction between the value of new and usedvehicles for buyers erodes. Buyers become as likely to purchase used vehicles withthe features they desire as they are to purchase new vehicles with fewer of thosefeatures.

2. The decline of advertising effectiveness in driving vehicle buyers to new carshowrooms. Twenty years ago, newspapers and broadcast TV were the primeadvertising channels used to bring buyers to their new cars and trucks. Newspaperreadership and broadcast viewing has aged and declined. Digital advertising hasbecome the solution of choice, but ad blocking and the enormous variation in usagepatterns has limited its impact. At the same time, individual dealers have been unableto effectively utilize digital ad platforms, which operate 24/7 and demand immediateresponse.

3. The attenuation of the car purchase cycle – which has shortened from a six-month purchase funnel of the ‘90’s to the six-week “shot-glass” extant today. Youngerbuyers check with friends and peers for the validity of a purchase choice almostinstantly via social media and arrive at a dealership with more knowledge of featuresand prices than many of the salespeople they deal with.

4. The decreasing requirement for car ownership. Younger consumers, besetwith enormous college debt, have found alternatives to new car ownership. Besidessimply purchasing used, many find Uber, carsharing or similar services sufficient fortheir social transportation needs.

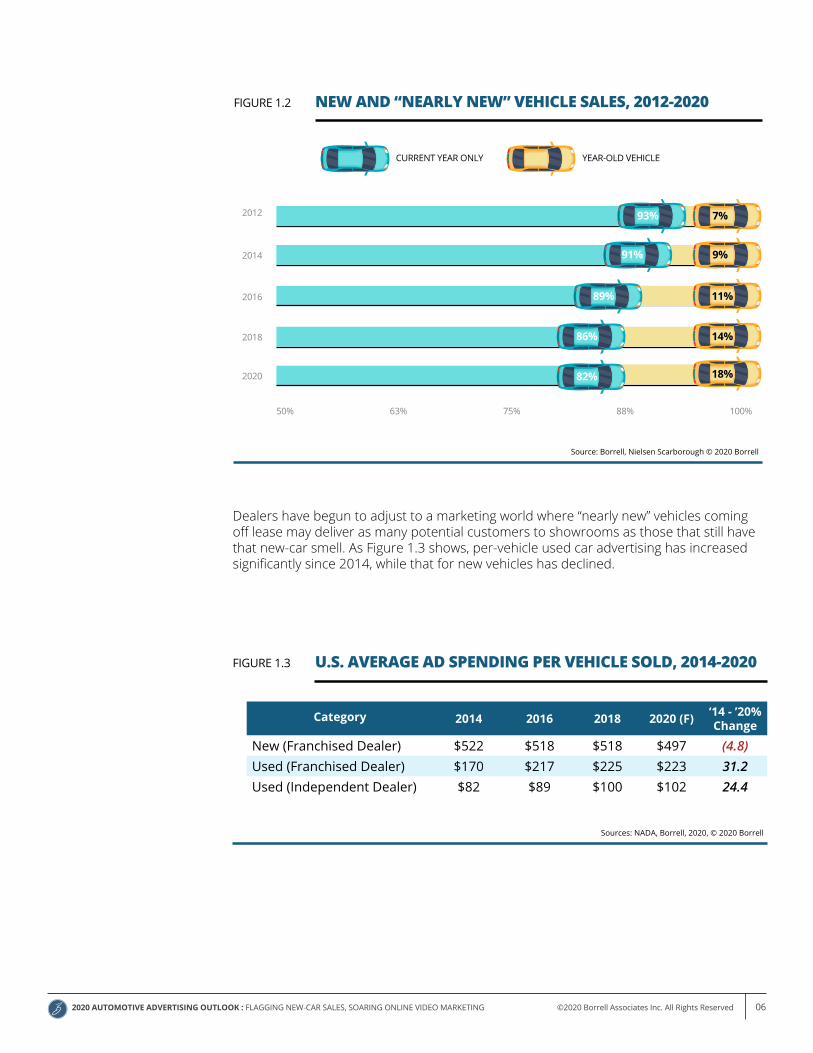

Part of the problem in accurately identifying true new-car demand is one of basic recognition. In the past, when respondents to national surveys indicated their intention of buying a new car in the coming year, the supposition was made that “new” meant an unused car produced during the current (or immediately previous) model year. In recent years, this definition has become less clear. “New” simply may mean new to the buyer, rather than never used. As shown in Figure 1.2, the impact of this incongruity is growing as new car costs increase.

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 06

Dealers have begun to adjust to a marketing world where “nearly new” vehicles coming off lease may deliver as many potential customers to showrooms as those that still have that new-car smell. As Figure 1.3 shows, per-vehicle used car advertising has increased significantly since 2014, while that for new vehicles has declined.

Category 2014 2016 2018 2020 (F) ‘14 - ’20%Change

New (Franchised Dealer) $522 $518 $518 $497 (4.8)Used (Franchised Dealer) $170 $217 $225 $223 31.2Used (Independent Dealer) $82 $89 $100 $102 24.4

U.S. AVERAGE AD SPENDING PER VEHICLE SOLD, 2014-2020FIGURE 1.3

Sources: NADA, Borrell, 2020, © 2020 Borrell

NEW AND “NEARLY NEW” VEHICLE SALES, 2012-2020FIGURE 1.2

CURRENT YEAR ONLY YEAR-OLD VEHICLE

2012

2014

2016

2018

2020

50% 63% 75% 88% 100%

93%

91%

86%

7%

9%

14%

82% 18%

89% 11%

Source: Borrell, Nielsen Scarborough © 2020 Borrell

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 07

We believe our U.S. sales forecast in Figure 1.1 is the most likely scenario based on current data. Here are events that could dramatically alter our forecast:

Alternative A: Fracking Banned. The elimination of hydraulic fracturing as a petroleum extraction process has become a presidential campaign issue. Substantial reduction or a total fracking ban will quickly return the nation from its current position as a major oil exporter to that of a net importer. If the price of oil increases due to these restrictions, less-efficient vehicles would become less valuable and more readily traded. Vehicles with more fuel efficiency will receive greater buyer demand, sparking an uptick in sales for new vehicles with higher fuel efficiency.

Alternative B: College loans forgiven. The overwhelming amounts of these loans have forced millions of consumers to forgo major purchases, such as homes and new cars. The partial or complete abolition of this debt would fuel increased demand for new vehicles.

Alternative C: Corporate MPG requirements increased. The federal government’s Corporate Average Fuel Economy (CAFE) requirements continue to climb, but at a slower rate. If National Highway Traffic Safety Administration (NHTSA) MPG minimums are stiffened again, automakers would raise new-vehicle pricing to absorb the cost of increasing fuel efficiency. This would reduce demand in the short term, but not in the longer term, as consumer demand to save money through fuel efficiency outweighs it.

New-car sales forecasts for each alternative are shown in Figure 1.4. Note that all forecasts increase demand over currently forecast levels. That’s because each affects the value and utility of currently used vehicles or consumer purchase capabilities.FORECAST U.S. NEW-VEHICLE ANNUAL SALES:

CURRENT FORECAST VS. ALTERNATIVESFIGURE 1.4

Sources: Borrell, 2020 © 2020 Borrell

MIL

LIO

NS

OF

VEH

ICLE

S SO

LD

16.0

16.8

CURRENT POINT FORECAST

ALTERNATIVE “B” (STUDENT LOANS FORGIVEN)

ALTERNATIVE “A” (NO FRACKING)

ALTERNATIVE “C” (CAFE AVERAGE STIFFENED)

Appendix A examines the most likely alternatives – an exercisein scenariobuilding. Byexamining thebase premisesthat supporteach of thesescenarios, itis possibleto monitorongoing eventsto determinewhich ofthe futuresdescribedare becomingmore possible,and which arereceding invalidity.

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 08

C H A P T E R 2 : 2020 AUTOMOTIVE AD-SPENDING FORECASTS

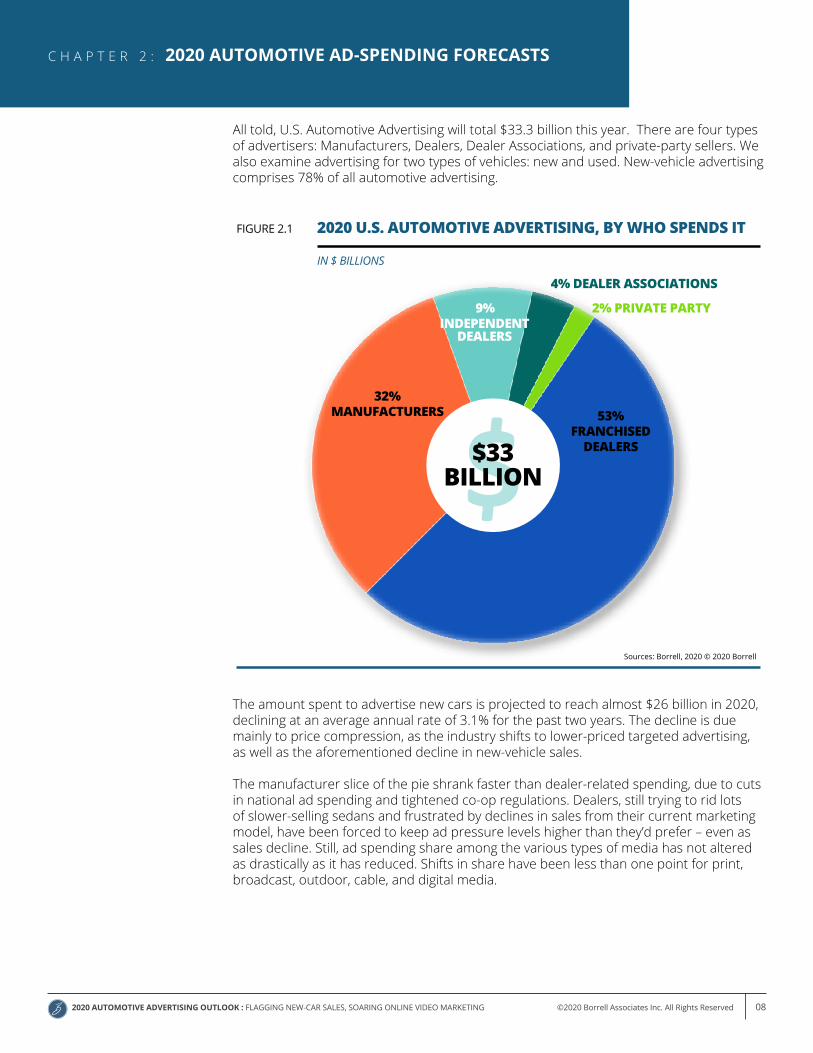

All told, U.S. Automotive Advertising will total $33.3 billion this year. There are four types of advertisers: Manufacturers, Dealers, Dealer Associations, and private-party sellers. We also examine advertising for two types of vehicles: new and used. New-vehicle advertising comprises 78% of all automotive advertising.

The amount spent to advertise new cars is projected to reach almost $26 billion in 2020, declining at an average annual rate of 3.1% for the past two years. The decline is due mainly to price compression, as the industry shifts to lower-priced targeted advertising, as well as the aforementioned decline in new-vehicle sales.

The manufacturer slice of the pie shrank faster than dealer-related spending, due to cuts in national ad spending and tightened co-op regulations. Dealers, still trying to rid lots of slower-selling sedans and frustrated by declines in sales from their current marketing model, have been forced to keep ad pressure levels higher than they’d prefer – even as sales decline. Still, ad spending share among the various types of media has not altered as drastically as it has reduced. Shifts in share have been less than one point for print, broadcast, outdoor, cable, and digital media.

2020 U.S. AUTOMOTIVE ADVERTISING, BY WHO SPENDS ITFIGURE 2.1

Sources: Borrell, 2020 © 2020 Borrell

IN $ BILLIONS

53%FRANCHISED

DEALERS

32%MANUFACTURERS

4% DEALER ASSOCIATIONS

9% INDEPENDENT

DEALERS

2% PRIVATE PARTY

$33 BILLION

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 09

The amount of money spent to advertise a new vehicle continues to fall. In the past two years it dropped 2.9% and now stands at $503, on average. At its peak in 2009, the total was $664. It’s interesting to see how these changes occur among dealerships of different sizes (see Figure 2.3). The smallest dealers get the worst advertising rates, and their advertising expenses have increased the most. The largest dealers are willing to spend more to move their new vehicles, since inventory, payroll, and other expenses are higher. Those above and below the poles simply spend less as demand declines.

PROJECTED 2020 U.S. AD SPENDING TO SUPPORT NEW-VEHICLE SALES

FIGURE 2.2

IN $ MILLIONS

Media Choice Dealers Co-op* Dealers+-Co-op

Dealer Assoc.**

AutoManuf.

New Car Ad $$ Totals

Share%

Change from 2018

‘18 - ‘20 Share Point Shift

Broadcast TV $422.60 $332.72 $755.32 $209.60 $932.95 $1,897.87 7.3% (7.9) (0.1)Cable $271.09 $200.29 $471.38 $189.35 $1,483.65 $2,144.37 8.3% 1.9 0.7Cinema $194.92 $130.90 $325.82 $131.10 $254.42 $711.35 2.7% 5.7 0.3Direct Mail $647.83 $153.99 $801.82 $39.54 $223.61 $1,064.97 4.1% 1.7 0.3Directories $26.70 $187.56 $214.25 $27.94 $242.19 0.9% (12.4) (0.1)Newspapers $419.33 $389.99 $809.32 $160.14 $486.08 $1,455.54 5.6% (11.3) (0.3)Online/Digital $5,370.74 $4,061.75 $9,432.48 $236.31 $6,569.24 $16,238.03 62.6% (7.3) (0.7)Other Print $170.35 $127.11 $297.46 $132.27 $224.87 $654.61 2.5% (7.5) (0.0)Outdoor $64.54 $34.24 $98.78 $30.93 $247.22 $376.93 1.5% (9.8) (0.1)Radio $484.08 $106.35 $590.37 $176.29 $68.99 $835.65 3.2% (4.9) 0.0Telemarketing $217.85 $217.85 $80.59 $298.44 1.2% (6.7) (0.1)Projected ‘20 Market Totals $8,289.97 $5,724.90 $14,014.87 $1,305.53 $10,599.56 $25,919.96 100% (6.2)

% Change from ‘18 (1.9) (5.1) (3.2) 1.1 (10.7) (6.2)

Sources: Borrell, 2020 © 2020 Borrell

2018-2020 CHANGE IN AVERAGE PER-VEHICLE AD SPENDING FOR NEW CARS

FIGURE 2.3

Sources: Borrell, 2020 © 2020 Borrell

# of Dealership Employees

2018 2020 % Change

Less Than 5 $702 $818 16.5

5 to 9 $636 $771 21.2

10 to 24 $602 $570 (5.3)

25 to 49 $560 $528 (5.7)

50 to 99 $519 $505 (2.7)

100 to 249 $463 $454 (1.9)

250 to 499 $383 $438 14.4

500 or More $332 $420 26.5

Average $518 $503 (2.9)

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 10

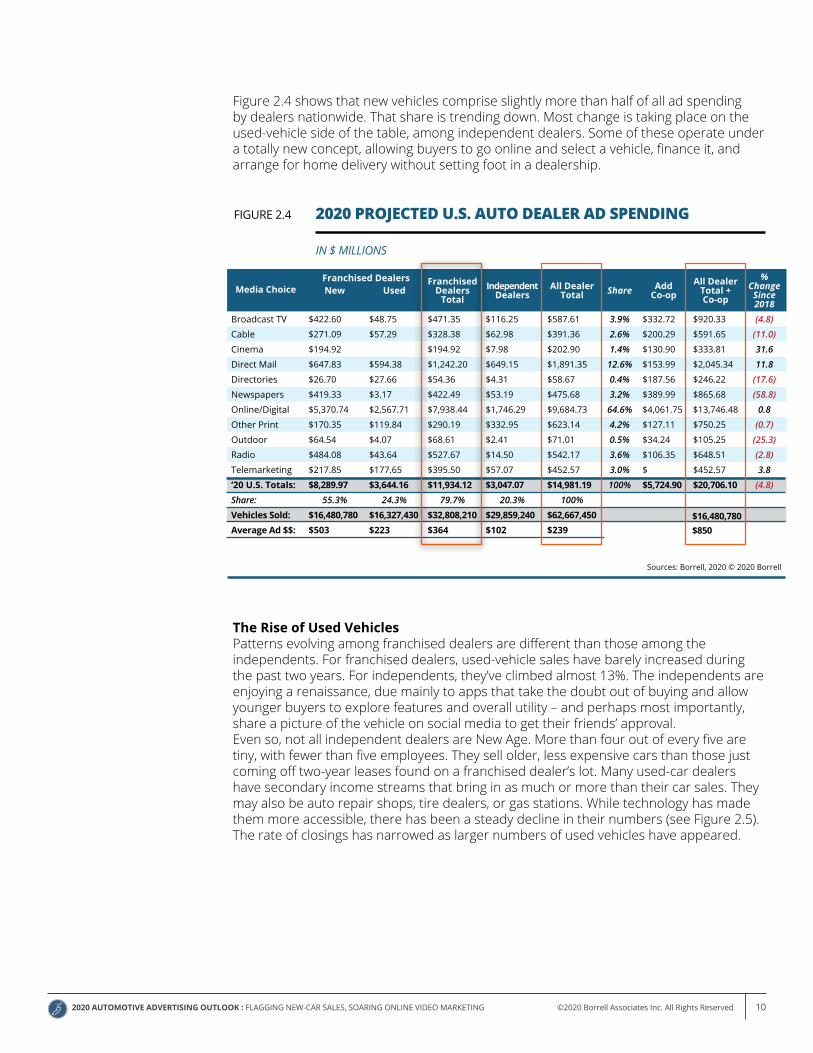

Figure 2.4 shows that new vehicles comprise slightly more than half of all ad spending by dealers nationwide. That share is trending down. Most change is taking place on the used-vehicle side of the table, among independent dealers. Some of these operate under a totally new concept, allowing buyers to go online and select a vehicle, finance it, and arrange for home delivery without setting foot in a dealership.

The Rise of Used VehiclesPatterns evolving among franchised dealers are different than those among the independents. For franchised dealers, used-vehicle sales have barely increased during the past two years. For independents, they’ve climbed almost 13%. The independents are enjoying a renaissance, due mainly to apps that take the doubt out of buying and allow younger buyers to explore features and overall utility – and perhaps most importantly, share a picture of the vehicle on social media to get their friends’ approval.Even so, not all independent dealers are New Age. More than four out of every five are tiny, with fewer than five employees. They sell older, less expensive cars than those just coming off two-year leases found on a franchised dealer’s lot. Many used-car dealers have secondary income streams that bring in as much or more than their car sales. They may also be auto repair shops, tire dealers, or gas stations. While technology has made them more accessible, there has been a steady decline in their numbers (see Figure 2.5). The rate of closings has narrowed as larger numbers of used vehicles have appeared.

Media Choice New UsedFranchised

Dealers Total

Independent Dealers

All Dealer Total Share Add

Co-opAll Dealer

Total + Co-op

% Change

Since 2018

Broadcast TV $422.60 $48.75 $471.35 $116.25 $587.61 3.9% $332.72 $920.33 (4.8)Cable $271.09 $57.29 $328.38 $62.98 $391.36 2.6% $200.29 $591.65 (11.0)Cinema $194.92 $194.92 $7.98 $202.90 1.4% $130.90 $333.81 31.6Direct Mail $647.83 $594.38 $1,242.20 $649.15 $1,891.35 12.6% $153.99 $2,045.34 11.8Directories $26.70 $27.66 $54.36 $4.31 $58.67 0.4% $187.56 $246.22 (17.6)Newspapers $419.33 $3.17 $422.49 $53.19 $475.68 3.2% $389.99 $865.68 (58.8)Online/Digital $5,370.74 $2,567.71 $7,938.44 $1,746.29 $9,684.73 64.6% $4,061.75 $13,746.48 0.8Other Print $170.35 $119.84 $290.19 $332.95 $623.14 4.2% $127.11 $750.25 (0.7)Outdoor $64.54 $4.07 $68.61 $2.41 $71.01 0.5% $34.24 $105.25 (25.3)Radio $484.08 $43.64 $527.67 $14.50 $542.17 3.6% $106.35 $648.51 (2.8)Telemarketing $217.85 $177.65 $395.50 $57.07 $452.57 3.0% $ $452.57 3.8‘20 U.S. Totals: $8,289.97 $3,644.16 $11,934.12 $3,047.07 $14,981.19 100% $5,724.90 $20,706.10 (4.8)Share: 55.3% 24.3% 79.7% 20.3% 100%Vehicles Sold: $16,480,780 $16,327,430 $32,808,210 $29,859,240 $62,667,450Average Ad $$: $503 $223 $364 $102 $239

2020 PROJECTED U.S. AUTO DEALER AD SPENDINGFIGURE 2.4

IN $ MILLIONS

Sources: Borrell, 2020 © 2020 Borrell

Franchised Dealers

$16,480,780$850

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 11

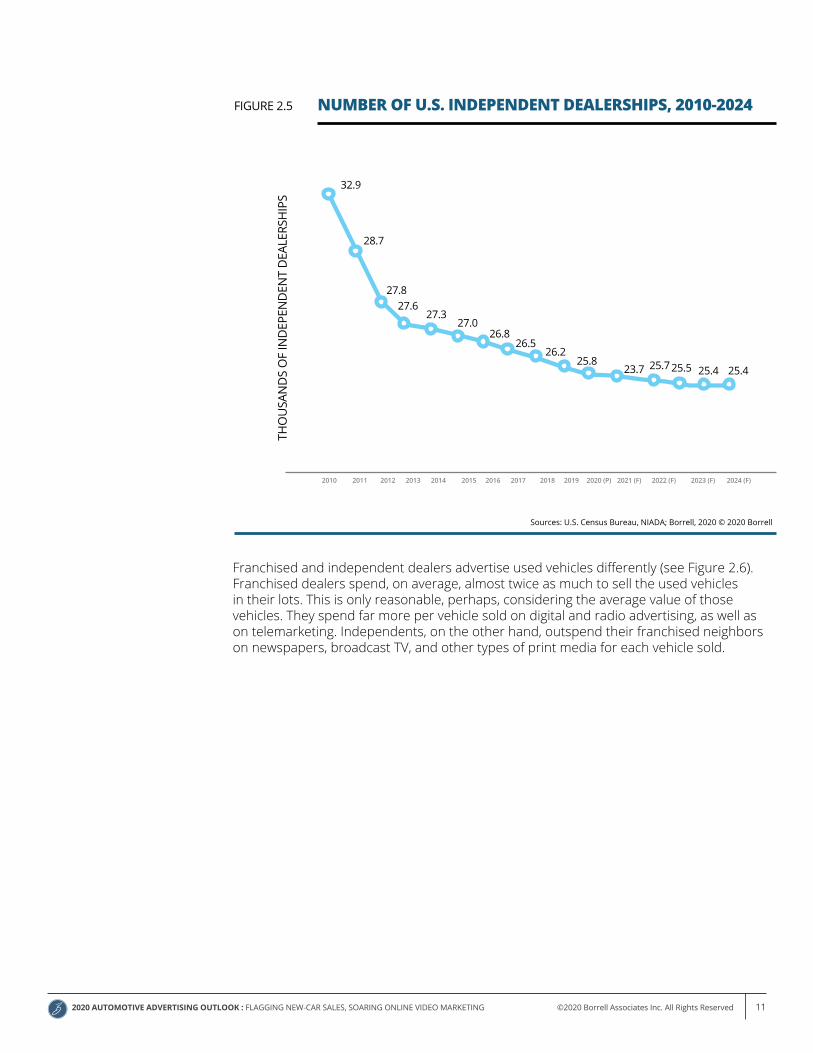

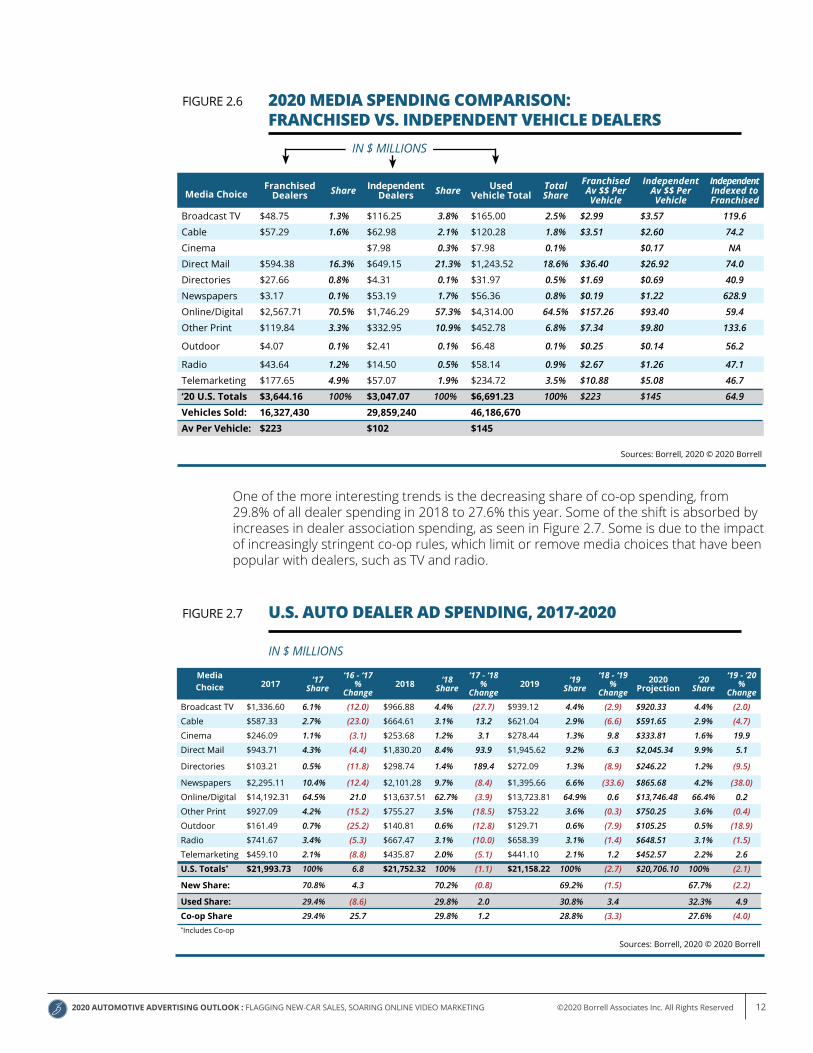

Franchised and independent dealers advertise used vehicles differently (see Figure 2.6). Franchised dealers spend, on average, almost twice as much to sell the used vehicles in their lots. This is only reasonable, perhaps, considering the average value of those vehicles. They spend far more per vehicle sold on digital and radio advertising, as well as on telemarketing. Independents, on the other hand, outspend their franchised neighbors on newspapers, broadcast TV, and other types of print media for each vehicle sold.

NUMBER OF U.S. INDEPENDENT DEALERSHIPS, 2010-2024FIGURE 2.5

Sources: U.S. Census Bureau, NIADA; Borrell, 2020 © 2020 Borrell

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 (P) 2021 (F) 2022 (F) 2023 (F) 2024 (F)

THO

USA

ND

S O

F IN

DEP

END

ENT

DEA

LERS

HIP

S

32.9

28.7

27.827.6

27.327.0

26.826.5

26.225.8

23.7 25.725.5 25.4 25.4

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 12

One of the more interesting trends is the decreasing share of co-op spending, from 29.8% of all dealer spending in 2018 to 27.6% this year. Some of the shift is absorbed by increases in dealer association spending, as seen in Figure 2.7. Some is due to the impact of increasingly stringent co-op rules, which limit or remove media choices that have been popular with dealers, such as TV and radio.

Media Choice 2017 ‘17

Share‘16 - ‘17

%Change

2018 ‘18 Share

‘17 - ‘18%

Change2019 ‘19

Share‘18 - ‘19

%Change

2020 Projection

‘20 Share

‘19 - ‘20%

ChangeBroadcast TV $1,336.60 6.1% (12.0) $966.88 4.4% (27.7) $939.12 4.4% (2.9) $920.33 4.4% (2.0)

Cable $587.33 2.7% (23.0) $664.61 3.1% 13.2 $621.04 2.9% (6.6) $591.65 2.9% (4.7)

Cinema $246.09 1.1% (3.1) $253.68 1.2% 3.1 $278.44 1.3% 9.8 $333.81 1.6% 19.9

Direct Mail $943.71 4.3% (4.4) $1,830.20 8.4% 93.9 $1,945.62 9.2% 6.3 $2,045.34 9.9% 5.1

Directories $103.21 0.5% (11.8) $298.74 1.4% 189.4 $272.09 1.3% (8.9) $246.22 1.2% (9.5)

Newspapers $2,295.11 10.4% (12.4) $2,101.28 9.7% (8.4) $1,395.66 6.6% (33.6) $865.68 4.2% (38.0)

Online/Digital $14,192.31 64.5% 21.0 $13,637.51 62.7% (3.9) $13,723.81 64.9% 0.6 $13,746.48 66.4% 0.2

Other Print $927.09 4.2% (15.2) $755.27 3.5% (18.5) $753.22 3.6% (0.3) $750.25 3.6% (0.4)

Outdoor $161.49 0.7% (25.2) $140.81 0.6% (12.8) $129.71 0.6% (7.9) $105.25 0.5% (18.9)

Radio $741.67 3.4% (5.3) $667.47 3.1% (10.0) $658.39 3.1% (1.4) $648.51 3.1% (1.5)

Telemarketing $459.10 2.1% (8.8) $435.87 2.0% (5.1) $441.10 2.1% 1.2 $452.57 2.2% 2.6

U.S. Totals* $21,993.73 100% 6.8 $21,752.32 100% (1.1) $21,158.22 100% (2.7) $20,706.10 100% (2.1)

New Share: 70.8% 4.3 70.2% (0.8) 69.2% (1.5) 67.7% (2.2)

Used Share: 29.4% (8.6) 29.8% 2.0 30.8% 3.4 32.3% 4.9

Co-op Share 29.4% 25.7 29.8% 1.2 28.8% (3.3) 27.6% (4.0)*Includes Co-op

U.S. AUTO DEALER AD SPENDING, 2017-2020FIGURE 2.7

IN $ MILLIONS

Sources: Borrell, 2020 © 2020 Borrell

Sources: Borrell, 2020 © 2020 Borrell

2020 MEDIA SPENDING COMPARISON: FRANCHISED VS. INDEPENDENT VEHICLE DEALERS

FIGURE 2.6

Media ChoiceFranchised

Dealers Share IndependentDealers Share Used

Vehicle TotalTotal Share

Franchised Av $$ Per Vehicle

Independent Av $$ Per Vehicle

Independent Indexed to Franchised

Broadcast TV $48.75 1.3% $116.25 3.8% $165.00 2.5% $2.99 $3.57 119.6

Cable $57.29 1.6% $62.98 2.1% $120.28 1.8% $3.51 $2.60 74.2

Cinema $7.98 0.3% $7.98 0.1% $0.17 NA

Direct Mail $594.38 16.3% $649.15 21.3% $1,243.52 18.6% $36.40 $26.92 74.0

Directories $27.66 0.8% $4.31 0.1% $31.97 0.5% $1.69 $0.69 40.9

Newspapers $3.17 0.1% $53.19 1.7% $56.36 0.8% $0.19 $1.22 628.9

Online/Digital $2,567.71 70.5% $1,746.29 57.3% $4,314.00 64.5% $157.26 $93.40 59.4

Other Print $119.84 3.3% $332.95 10.9% $452.78 6.8% $7.34 $9.80 133.6

Outdoor $4.07 0.1% $2.41 0.1% $6.48 0.1% $0.25 $0.14 56.2

Radio $43.64 1.2% $14.50 0.5% $58.14 0.9% $2.67 $1.26 47.1

Telemarketing $177.65 4.9% $57.07 1.9% $234.72 3.5% $10.88 $5.08 46.7

‘20 U.S. Totals $3,644.16 100% $3,047.07 100% $6,691.23 100% $223 $145 64.9Vehicles Sold: 16,327,430 29,859,240 46,186,670Av Per Vehicle: $223 $102 $145

IN $ MILLIONS

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 13

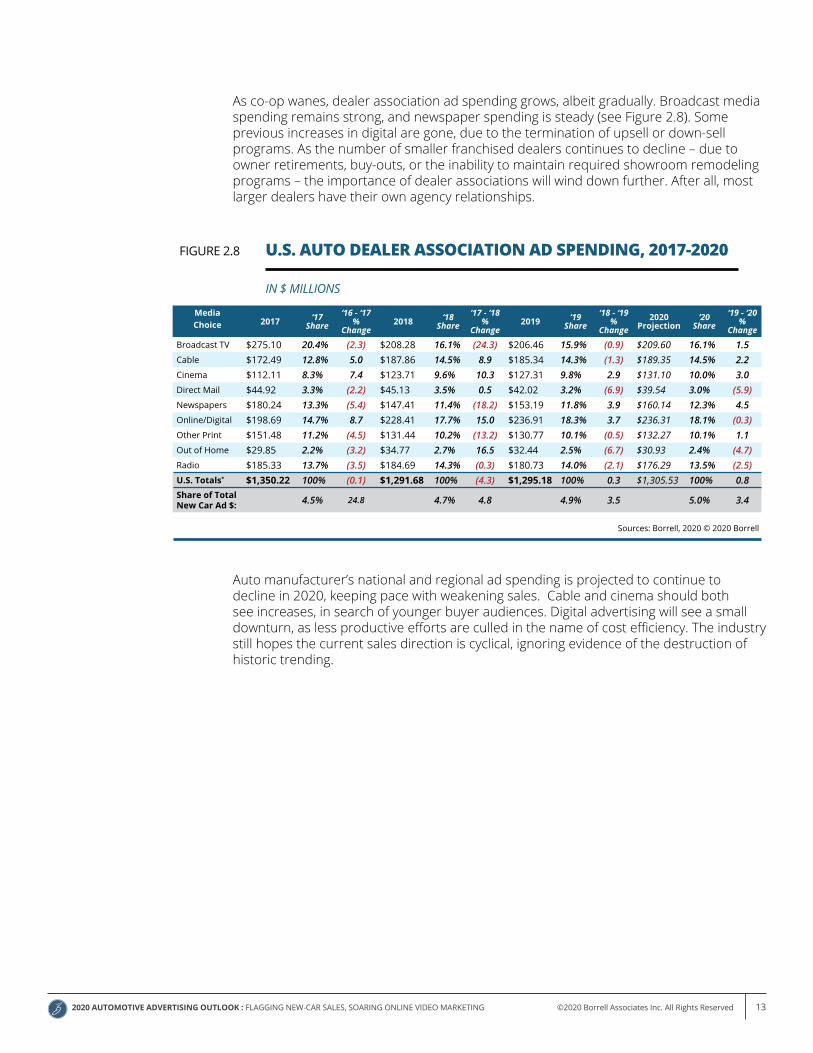

As co-op wanes, dealer association ad spending grows, albeit gradually. Broadcast media spending remains strong, and newspaper spending is steady (see Figure 2.8). Some previous increases in digital are gone, due to the termination of upsell or down-sell programs. As the number of smaller franchised dealers continues to decline – due to owner retirements, buy-outs, or the inability to maintain required showroom remodeling programs – the importance of dealer associations will wind down further. After all, most larger dealers have their own agency relationships.

U.S. AUTO DEALER ASSOCIATION AD SPENDING, 2017-2020FIGURE 2.8

IN $ MILLIONS

Media Choice 2017 ‘17

Share‘16 - ‘17

%Change

2018 ‘18 Share

‘17 - ‘18%

Change2019 ‘19

Share‘18 - ‘19

%Change

2020Projection

‘20 Share

‘19 - ‘20%

Change

Broadcast TV $275.10 20.4% (2.3) $208.28 16.1% (24.3) $206.46 15.9% (0.9) $209.60 16.1% 1.5 Cable $172.49 12.8% 5.0 $187.86 14.5% 8.9 $185.34 14.3% (1.3) $189.35 14.5% 2.2 Cinema $112.11 8.3% 7.4 $123.71 9.6% 10.3 $127.31 9.8% 2.9 $131.10 10.0% 3.0 Direct Mail $44.92 3.3% (2.2) $45.13 3.5% 0.5 $42.02 3.2% (6.9) $39.54 3.0% (5.9)Newspapers $180.24 13.3% (5.4) $147.41 11.4% (18.2) $153.19 11.8% 3.9 $160.14 12.3% 4.5 Online/Digital $198.69 14.7% 8.7 $228.41 17.7% 15.0 $236.91 18.3% 3.7 $236.31 18.1% (0.3)Other Print $151.48 11.2% (4.5) $131.44 10.2% (13.2) $130.77 10.1% (0.5) $132.27 10.1% 1.1 Out of Home $29.85 2.2% (3.2) $34.77 2.7% 16.5 $32.44 2.5% (6.7) $30.93 2.4% (4.7)Radio $185.33 13.7% (3.5) $184.69 14.3% (0.3) $180.73 14.0% (2.1) $176.29 13.5% (2.5)U.S. Totals* $1,350.22 100% (0.1) $1,291.68 100% (4.3) $1,295.18 100% 0.3 $1,305.53 100% 0.8 Share of Total New Car Ad $: 4.5% 24.8 4.7% 4.8 4.9% 3.5 5.0% 3.4

Sources: Borrell, 2020 © 2020 Borrell

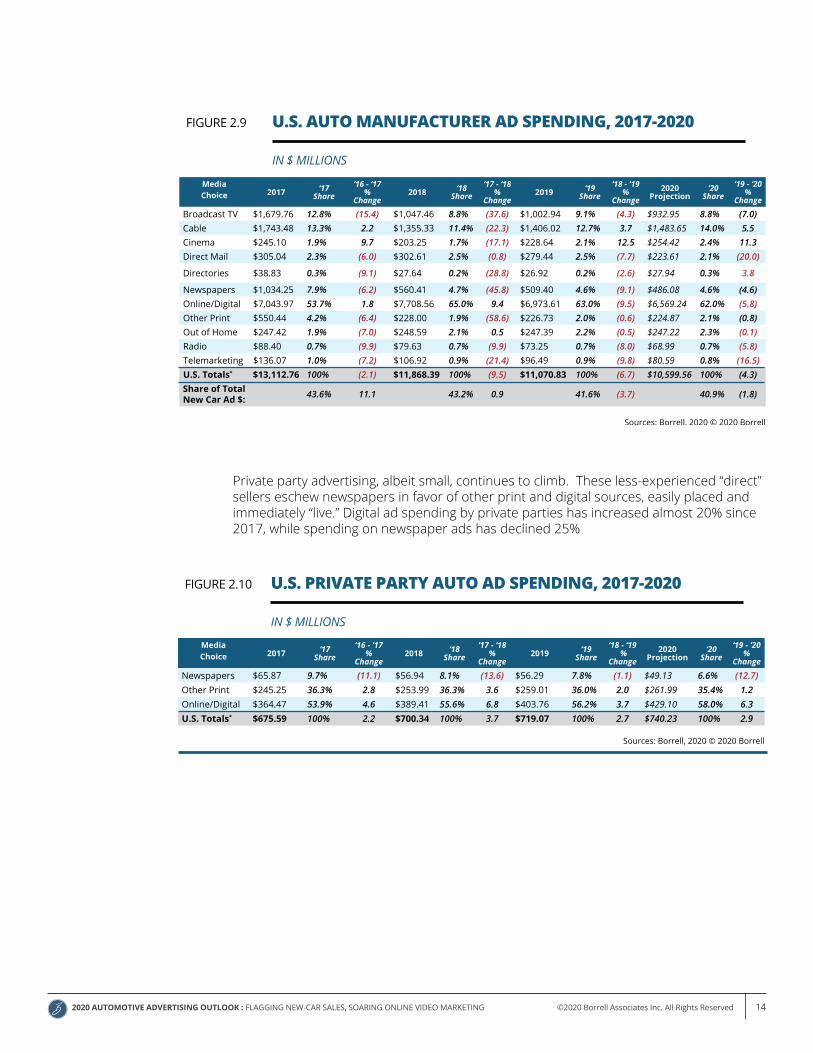

Auto manufacturer’s national and regional ad spending is projected to continue to decline in 2020, keeping pace with weakening sales. Cable and cinema should both see increases, in search of younger buyer audiences. Digital advertising will see a small downturn, as less productive efforts are culled in the name of cost efficiency. The industry still hopes the current sales direction is cyclical, ignoring evidence of the destruction of historic trending.

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 14

U.S. AUTO MANUFACTURER AD SPENDING, 2017-2020FIGURE 2.9

IN $ MILLIONS

Media Choice 2017 ‘17

Share‘16 - ‘17

% Change

2018 ‘18 Share

‘17 - ‘18 %

Change2019 ‘19

Share‘18 - ‘19

% Change

2020Projection

‘20 Share

‘19 - ‘20%

Change

Broadcast TV $1,679.76 12.8% (15.4) $1,047.46 8.8% (37.6) $1,002.94 9.1% (4.3) $932.95 8.8% (7.0)Cable $1,743.48 13.3% 2.2 $1,355.33 11.4% (22.3) $1,406.02 12.7% 3.7 $1,483.65 14.0% 5.5 Cinema $245.10 1.9% 9.7 $203.25 1.7% (17.1) $228.64 2.1% 12.5 $254.42 2.4% 11.3 Direct Mail $305.04 2.3% (6.0) $302.61 2.5% (0.8) $279.44 2.5% (7.7) $223.61 2.1% (20.0)

Directories $38.83 0.3% (9.1) $27.64 0.2% (28.8) $26.92 0.2% (2.6) $27.94 0.3% 3.8

Newspapers $1,034.25 7.9% (6.2) $560.41 4.7% (45.8) $509.40 4.6% (9.1) $486.08 4.6% (4.6)Online/Digital $7,043.97 53.7% 1.8 $7,708.56 65.0% 9.4 $6,973.61 63.0% (9.5) $6,569.24 62.0% (5.8)Other Print $550.44 4.2% (6.4) $228.00 1.9% (58.6) $226.73 2.0% (0.6) $224.87 2.1% (0.8)Out of Home $247.42 1.9% (7.0) $248.59 2.1% 0.5 $247.39 2.2% (0.5) $247.22 2.3% (0.1)Radio $88.40 0.7% (9.9) $79.63 0.7% (9.9) $73.25 0.7% (8.0) $68.99 0.7% (5.8)Telemarketing $136.07 1.0% (7.2) $106.92 0.9% (21.4) $96.49 0.9% (9.8) $80.59 0.8% (16.5)U.S. Totals* $13,112.76 100% (2.1) $11,868.39 100% (9.5) $11,070.83 100% (6.7) $10,599.56 100% (4.3)Share of Total New Car Ad $: 43.6% 11.1 43.2% 0.9 41.6% (3.7) 40.9% (1.8)

Sources: Borrell, 2020 © 2020 Borrell

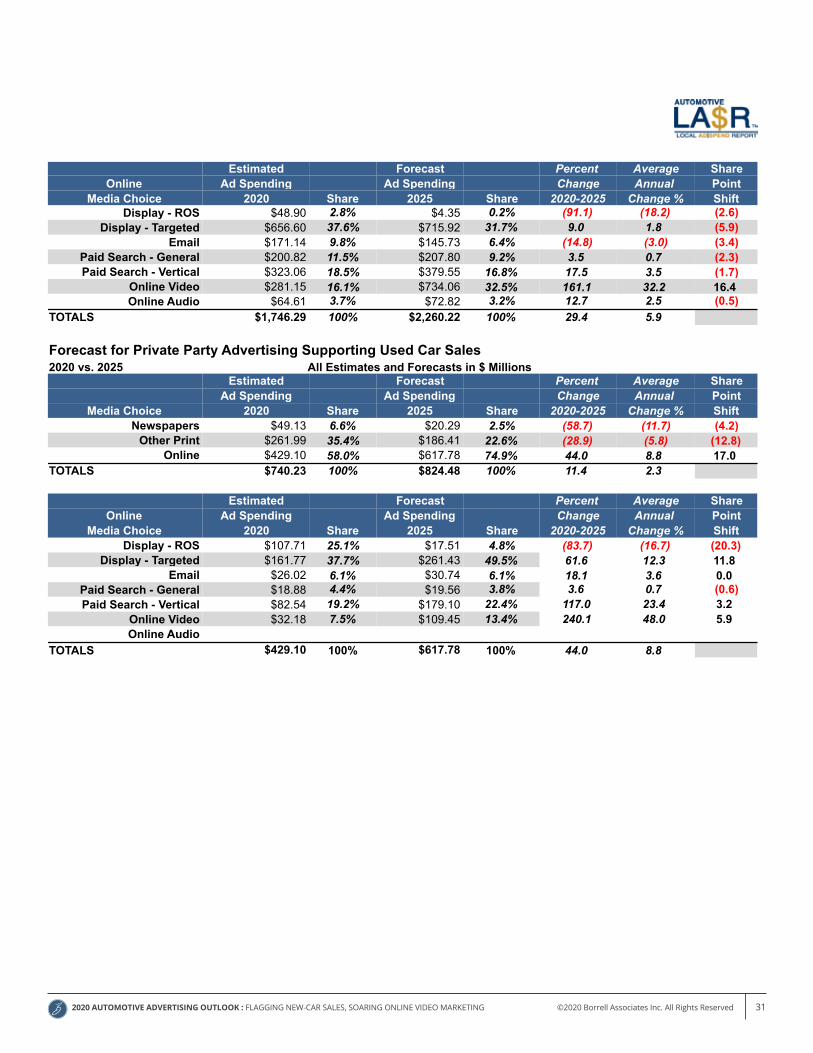

U.S. PRIVATE PARTY AUTO AD SPENDING, 2017-2020FIGURE 2.10

IN $ MILLIONS

Media Choice 2017 ‘17

Share‘16 - ‘17

% Change

2018 ‘18Share

‘17 - ‘18 %

Change2019 ‘19

Share‘18 - ‘19

% Change

2020 Projection

‘20 Share

‘19 - ‘20 %

Change

Newspapers $65.87 9.7% (11.1) $56.94 8.1% (13.6) $56.29 7.8% (1.1) $49.13 6.6% (12.7)Other Print $245.25 36.3% 2.8 $253.99 36.3% 3.6 $259.01 36.0% 2.0 $261.99 35.4% 1.2 Online/Digital $364.47 53.9% 4.6 $389.41 55.6% 6.8 $403.76 56.2% 3.7 $429.10 58.0% 6.3 U.S. Totals* $675.59 100% 2.2 $700.34 100% 3.7 $719.07 100% 2.7 $740.23 100% 2.9

Sources: Borrell, 2020 © 2020 Borrell

Private party advertising, albeit small, continues to climb. These less-experienced “direct” sellers eschew newspapers in favor of other print and digital sources, easily placed and immediately “live.” Digital ad spending by private parties has increased almost 20% since 2017, while spending on newspaper ads has declined 25%

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 15

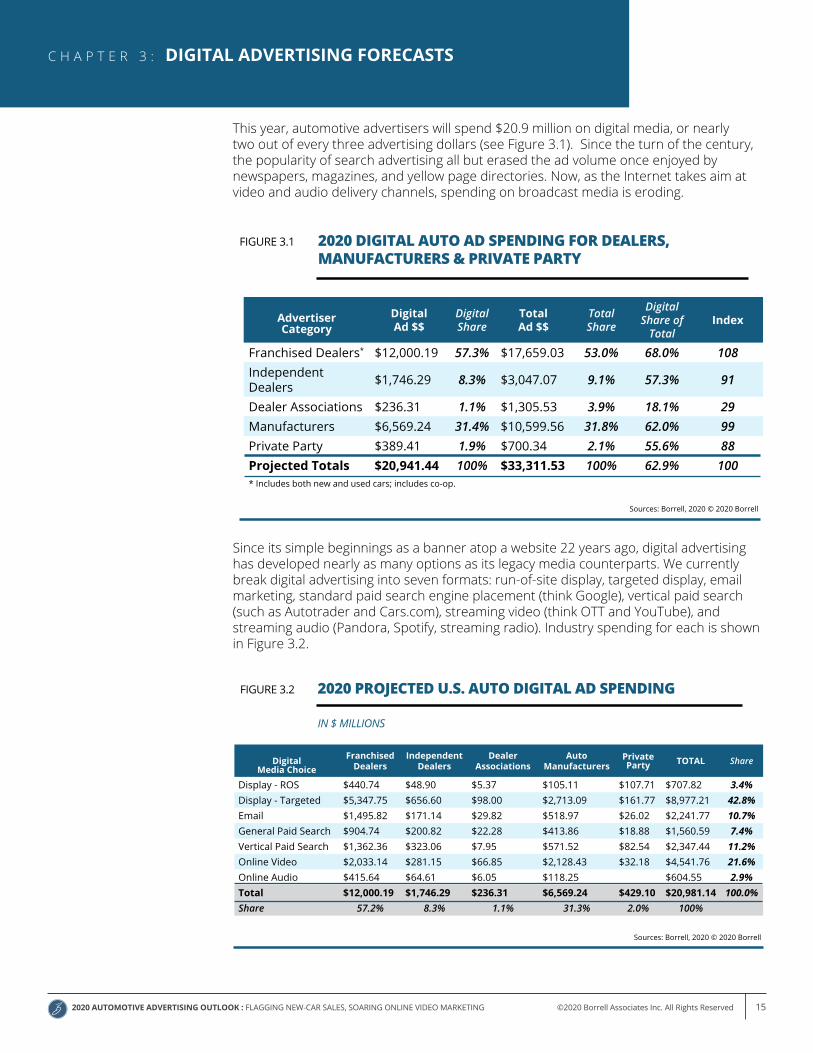

This year, automotive advertisers will spend $20.9 million on digital media, or nearly two out of every three advertising dollars (see Figure 3.1). Since the turn of the century, the popularity of search advertising all but erased the ad volume once enjoyed by newspapers, magazines, and yellow page directories. Now, as the Internet takes aim at video and audio delivery channels, spending on broadcast media is eroding.

C H A P T E R 3 : DIGITAL ADVERTISING FORECASTS

Since its simple beginnings as a banner atop a website 22 years ago, digital advertising has developed nearly as many options as its legacy media counterparts. We currently break digital advertising into seven formats: run-of-site display, targeted display, email marketing, standard paid search engine placement (think Google), vertical paid search (such as Autotrader and Cars.com), streaming video (think OTT and YouTube), and streaming audio (Pandora, Spotify, streaming radio). Industry spending for each is shown in Figure 3.2.

2020 DIGITAL AUTO AD SPENDING FOR DEALERS, MANUFACTURERS & PRIVATE PARTY

FIGURE 3.1

Sources: Borrell, 2020 © 2020 Borrell

Advertiser Category

Digital Ad $$

Digital Share

Total Ad $$

Total Share

Digital Share of

TotalIndex

Franchised Dealers* $12,000.19 57.3% $17,659.03 53.0% 68.0% 108Independent Dealers $1,746.29 8.3% $3,047.07 9.1% 57.3% 91

Dealer Associations $236.31 1.1% $1,305.53 3.9% 18.1% 29Manufacturers $6,569.24 31.4% $10,599.56 31.8% 62.0% 99Private Party $389.41 1.9% $700.34 2.1% 55.6% 88Projected Totals $20,941.44 100% $33,311.53 100% 62.9% 100* Includes both new and used cars; includes co-op.

Digital Media Choice

Franchised Dealers

IndependentDealers

Dealer Associations

AutoManufacturers

Private Party TOTAL Share

Display - ROS $440.74 $48.90 $5.37 $105.11 $107.71 $707.82 3.4%Display - Targeted $5,347.75 $656.60 $98.00 $2,713.09 $161.77 $8,977.21 42.8%Email $1,495.82 $171.14 $29.82 $518.97 $26.02 $2,241.77 10.7%General Paid Search $904.74 $200.82 $22.28 $413.86 $18.88 $1,560.59 7.4%Vertical Paid Search $1,362.36 $323.06 $7.95 $571.52 $82.54 $2,347.44 11.2%Online Video $2,033.14 $281.15 $66.85 $2,128.43 $32.18 $4,541.76 21.6%Online Audio $415.64 $64.61 $6.05 $118.25 $604.55 2.9%Total $12,000.19 $1,746.29 $236.31 $6,569.24 $429.10 $20,981.14 100.0%Share 57.2% 8.3% 1.1% 31.3% 2.0% 100%

2020 PROJECTED U.S. AUTO DIGITAL AD SPENDINGFIGURE 3.2

Sources: Borrell, 2020 © 2020 Borrell

IN $ MILLIONS

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 16

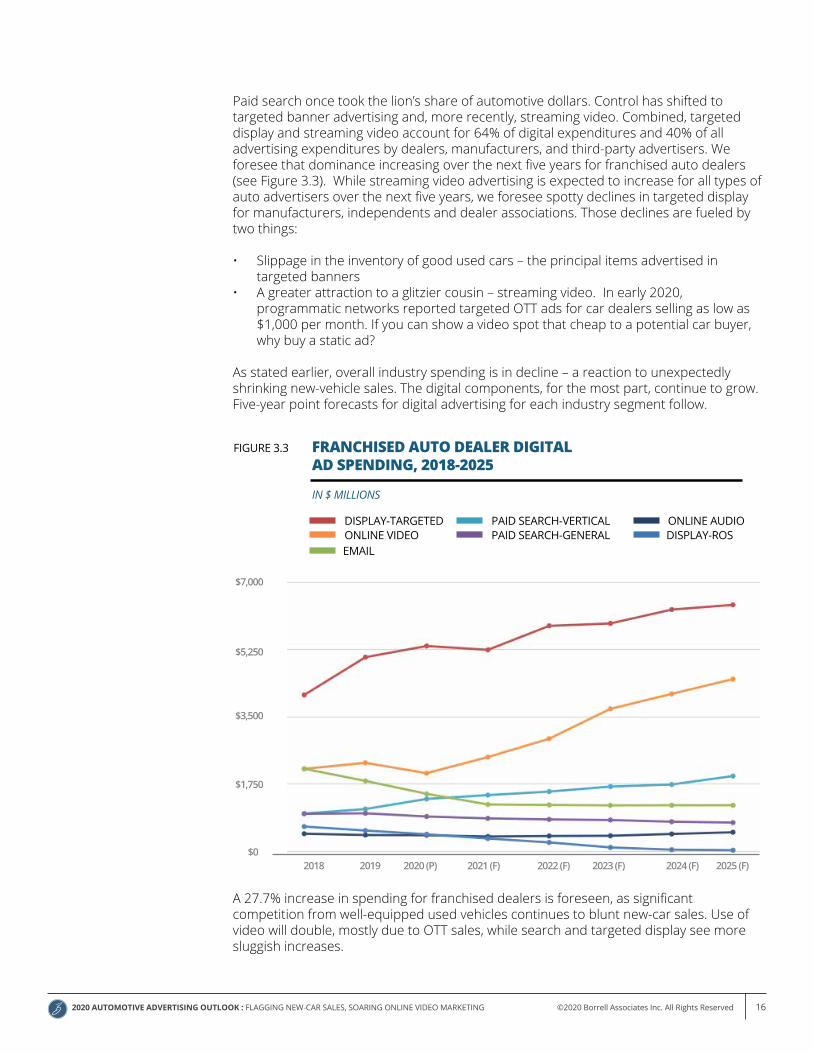

Paid search once took the lion’s share of automotive dollars. Control has shifted to targeted banner advertising and, more recently, streaming video. Combined, targeted display and streaming video account for 64% of digital expenditures and 40% of all advertising expenditures by dealers, manufacturers, and third-party advertisers. We foresee that dominance increasing over the next five years for franchised auto dealers (see Figure 3.3). While streaming video advertising is expected to increase for all types of auto advertisers over the next five years, we foresee spotty declines in targeted display for manufacturers, independents and dealer associations. Those declines are fueled by two things:

• Slippage in the inventory of good used cars – the principal items advertised in targeted banners

• A greater attraction to a glitzier cousin – streaming video. In early 2020, programmatic networks reported targeted OTT ads for car dealers selling as low as $1,000 per month. If you can show a video spot that cheap to a potential car buyer, why buy a static ad?

As stated earlier, overall industry spending is in decline – a reaction to unexpectedly shrinking new-vehicle sales. The digital components, for the most part, continue to grow. Five-year point forecasts for digital advertising for each industry segment follow.

FRANCHISED AUTO DEALER DIGITAL AD SPENDING, 2018-2025

FIGURE 3.3

Sources: Borrell, 2020 © 2020 Borrell

IN $ MILLIONS

2018 2019 2020 (P) 2021 (F) 2022 (F) 2023 (F) 2024 (F) 2025 (F)

$7,000

$5,250

$3,500

$1,750

$0

DISPLAY-TARGETED PAID SEARCH-VERTICALPAID SEARCH-GENERALONLINE VIDEO

ONLINE AUDIO

EMAILDISPLAY-ROS

A 27.7% increase in spending for franchised dealers is foreseen, as significant competition from well-equipped used vehicles continues to blunt new-car sales. Use of video will double, mostly due to OTT sales, while search and targeted display see more sluggish increases.

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 17

INDEPENDENT AUTO DEALER DIGITAL AD SPENDING, 2018-2025

FIGURE 3.4

2018 2019 2020 (P) 2021 (F) 2022 (F) 2023 (F) 2024 (F) 2025 (F)

$1,000

$750

$500

$250

$0

Sources: Borrell, 2020 © 2020 Borrell

IN $ MILLIONS

DISPLAY-TARGETED PAID SEARCH-VERTICALPAID SEARCH-GENERALONLINE VIDEO

ONLINE AUDIO

EMAILDISPLAY-ROS

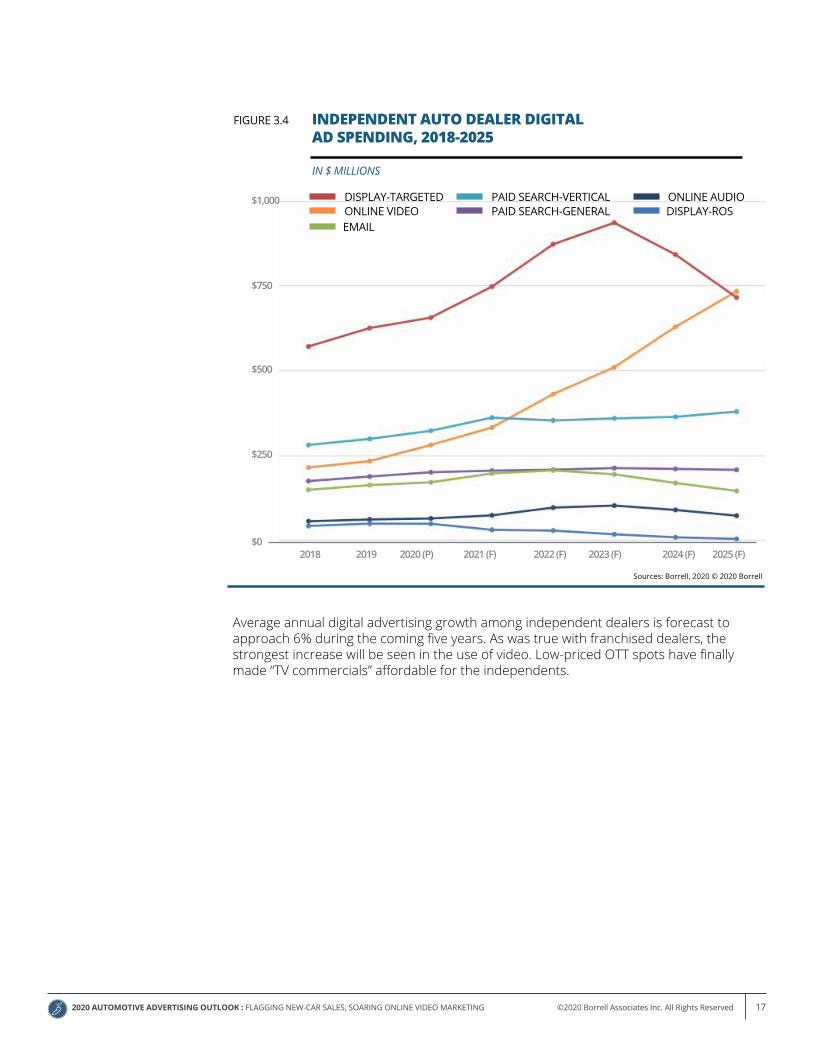

Average annual digital advertising growth among independent dealers is forecast to approach 6% during the coming five years. As was true with franchised dealers, the strongest increase will be seen in the use of video. Low-priced OTT spots have finally made “TV commercials” affordable for the independents.

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 18

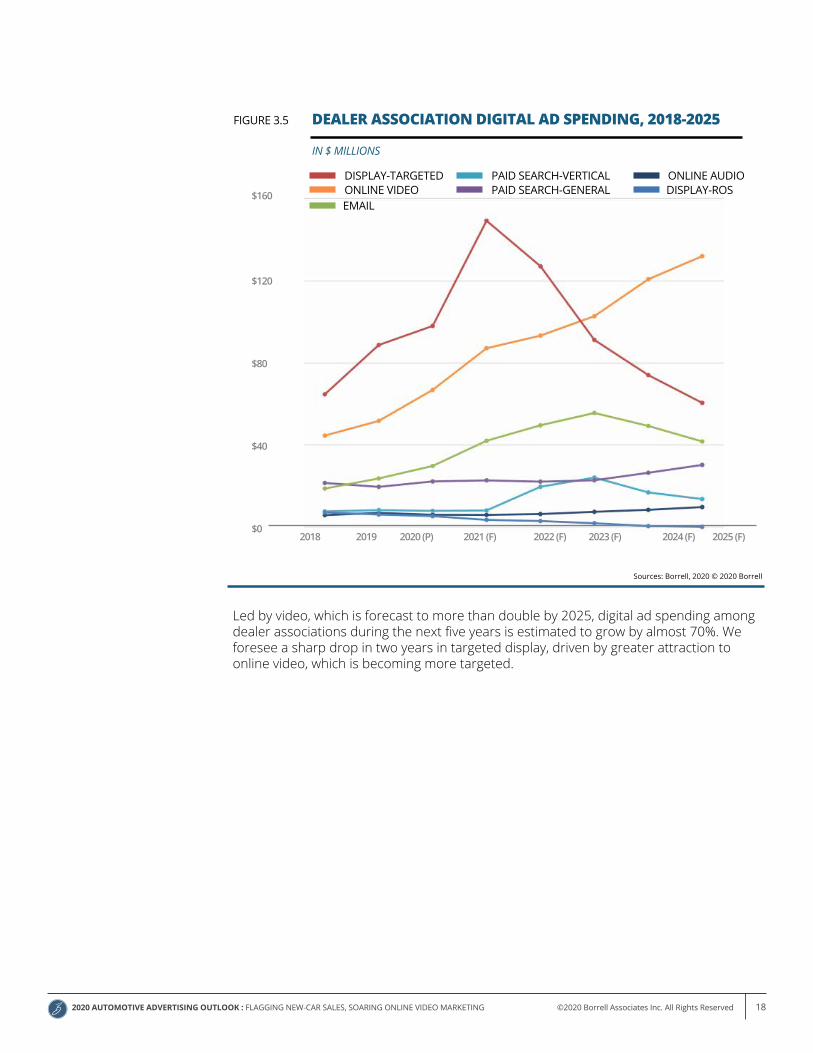

Led by video, which is forecast to more than double by 2025, digital ad spending among dealer associations during the next five years is estimated to grow by almost 70%. We foresee a sharp drop in two years in targeted display, driven by greater attraction to online video, which is becoming more targeted.

DEALER ASSOCIATION DIGITAL AD SPENDING, 2018-2025FIGURE 3.5

IN $ MILLIONS

2018 2019 2020 (P) 2021 (F) 2022 (F) 2023 (F) 2024 (F) 2025 (F)

$160

$120

$80

$40

$0

Sources: Borrell, 2020 © 2020 Borrell

DISPLAY-TARGETED PAID SEARCH-VERTICALPAID SEARCH-GENERALONLINE VIDEO

ONLINE AUDIO

EMAILDISPLAY-ROS

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 19

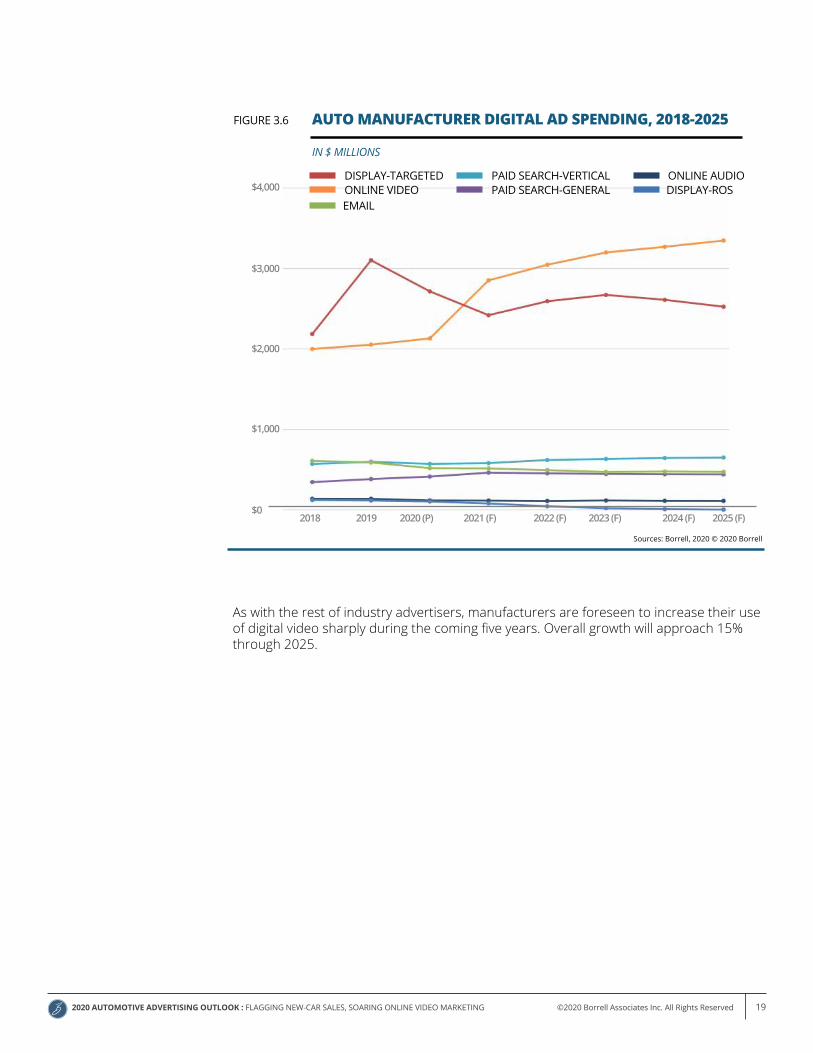

As with the rest of industry advertisers, manufacturers are foreseen to increase their use of digital video sharply during the coming five years. Overall growth will approach 15% through 2025.

AUTO MANUFACTURER DIGITAL AD SPENDING, 2018-2025FIGURE 3.6

IN $ MILLIONS

Sources: Borrell, 2020 © 2020 Borrell

2018 2019 2020 (P) 2021 (F) 2022 (F) 2023 (F) 2024 (F) 2025 (F)

$4,000

$3,000

$2,000

$1,000

$0

DISPLAY-TARGETED PAID SEARCH-VERTICALPAID SEARCH-GENERALONLINE VIDEO

ONLINE AUDIO

EMAILDISPLAY-ROS

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 20

This analysis has shown readers a massive set of data and forecasts, all presented to provide the best look possible on what is likely to happen during the coming five years. Stripped of the tables, charts, and graphs, these are the most important take-aways:

• The auto industry is undergoing a slow evolution. Old trends and forecasts no longerapply. We expect two to three years of uncertainty on the lynchpin of an uncertaineconomy and government regulation that could go either way.

• If currently predicted outcomes persist, the auto industry will experience severalmore years – perhaps a decade – of slow decline in new car demand, principally dueto competition from “slightly used” vehicles and student loan debt delaying entryfrom younger buyers.

• Despite hopes fueled by stories of car dealers coming back to print and broadcastmedia, there’s no evidence and thus, no chance. However, there is strong evidencethat local auto marketers don’t handle the digital space well and still favor seeing theirfaces on broadcast TV spots. Longstanding business practices hold them back frombeing able to respond to leads 24/7, thus losing to pureplay Internet competitors.CarGurus, TrueCar, Carvana and others thrive by shunning something that traditionaldealerships continue to take pride in: Personal contact and high touch.

• Traditional media companies that have their own online audiences might do besttaking a page from the likes of Google, Amazon, Facebook, and others who make ascience of understanding their users’ behavior. Knowledge of a media company’suser base (including and especially its digital component) will be important to gain orretain Tier 2 and Tier 3 advertisers. Combining this user data with dealerships’ owncustomer data and with location data is growing into a marketing holy grail.

• Many auto dealerships still operate as though a substantial number of those comingto their showrooms are merely browsers. As “auto intender” studies have shown,that is no longer true. Many prospects – especially younger people – have alreadystudied the brand and model they’re interested in. They are highly likely to purchasethe moment they walk onto the lot. This has broadly increased the attractiveness ofgeofencing, or the practice of serving a dealership ad or offer to someone’s cellphoneas they walk onto a competitor’s lot.

Appendix A contains scenarios built from alternative futures that could affect the point forecasts portrayed in this report. Appendix B shows a national compilation of our Auto LA$R report.

CONCLUSIONS

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 21

To quote Yogi Berra, the future ain’t what it used to be. That is, forecasts change as more information is gleaned, making the future a dynamic vision. Unforeseen events may occur that change the picture. Even when events are expected, they may have unforeseen consequences.

One way to attempt to take future events and their impact into account is scenario building. Part art, part science, this process considers events that might happen and weaves them into narratives. Included here are descriptions of three very different alternative futures, each fueled by events that could take place.

Alternative 1: Status Quo Current Probability: 65%The new U.S. president took the oath of office just three months ago. Both houses of Congress have opposing majorities, but do not control enough votes to overcome the veto pen the President has already vowed to use. Little groundbreaking legislation is expected out of Washington any time soon.

The nation’s economic growth continues to glide along between 2% and 3% annually. The price of oil has remained relatively steady, and the continued use of hydraulic fracturing as an extraction technique ensures that no change is on the horizon. The price of a gallon of gas remains steady at around $2.30.

Unemployment remains low, at just over 3%. However, 40% of college graduates find themselves working in jobs that do not require advanced education. The average college loan debt among new graduates is $45,000.

About 50 new car dealers shut down every year – mostly smaller stores. New-car demand continues to erode. Current estimates are for 16.2 million sales or leases this year.

General Motors has spun off its Buick Division to Chinese buyers. Ford has ended the Lincoln brand – its place to be taken by a newly redesigned Thunderbird. Chrysler’s best-selling car this year is a Peugeot SUV. India’s TATA has shown models for the U.S. market at the last Detroit Auto Show, but franchise interest is low. Tesla sales remain steady, but the brand does not gain U.S. share.

Alternative 2: Unintended Consequences Current Probability: 22%Progressives sweep the 2024 election. The new president immediately signs three executive orders. The first bans fracking as an oil or gas extraction technique on federal land. The second directs the NHTSA to elevate the CAFE (corporate average fuel economy) levels to 30 mpg next year, rising to 40 mpg in five years. The third directs the new Secretary of State to start immediate negotiations for the nation to join the Paris Accord.

Within three months, legislation cancelling all collegiate student debt is on the president’s desk. He (or she) signs immediately, unleashing pent-up demand among millions of younger consumers. Marriage rates climb, as does home buying. Many buy their first new cars as well.

The impact of the new CAFE regulations staggers domestic auto manufacturers, forcing them to reevaluate their production designs. Within a year, the first truly high-mileage

A P P E N D I X A : OTHER SCENARIOS

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 22

models begin to appear in showrooms, along with electric and hybrid alternatives. In the meantime, the price of gasoline at U.S. pumps climbs to an average of $4.10 a gallon. India’s TATA and some Chinese micro compacts find franchisees to bring their brands to the U.S. market.

New car demand climbs to more than 17 million units as car owners who can hurry to trade their inefficient gas guzzlers in for transportation they can afford to use. However, U.S. brands are late to market with their answers to current market conditions. For nearly a year, only imports can meet their needs.

Alternative 3: The New Battery Current Probability: 13%Elon Musk announces the availability of a new battery, now in production at his enormous Las Vegas facility. The battery is three times as efficient as current auto batteries. It will allow electric cars to have ranges of more than 1,000 miles. His newest designs, soon to be available, will have double that range.

Other manufacturers hurry to adapt the new battery to their own products. Within three years, electric vehicles outsell those powered by gasoline, and the price of gas at the pumps begins to tumble. New-car demand soars, reaching more than 19 million units by 2029.

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 23

A P P E N D I X B : AUTOMOTIVE LA$R REPORT

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 24

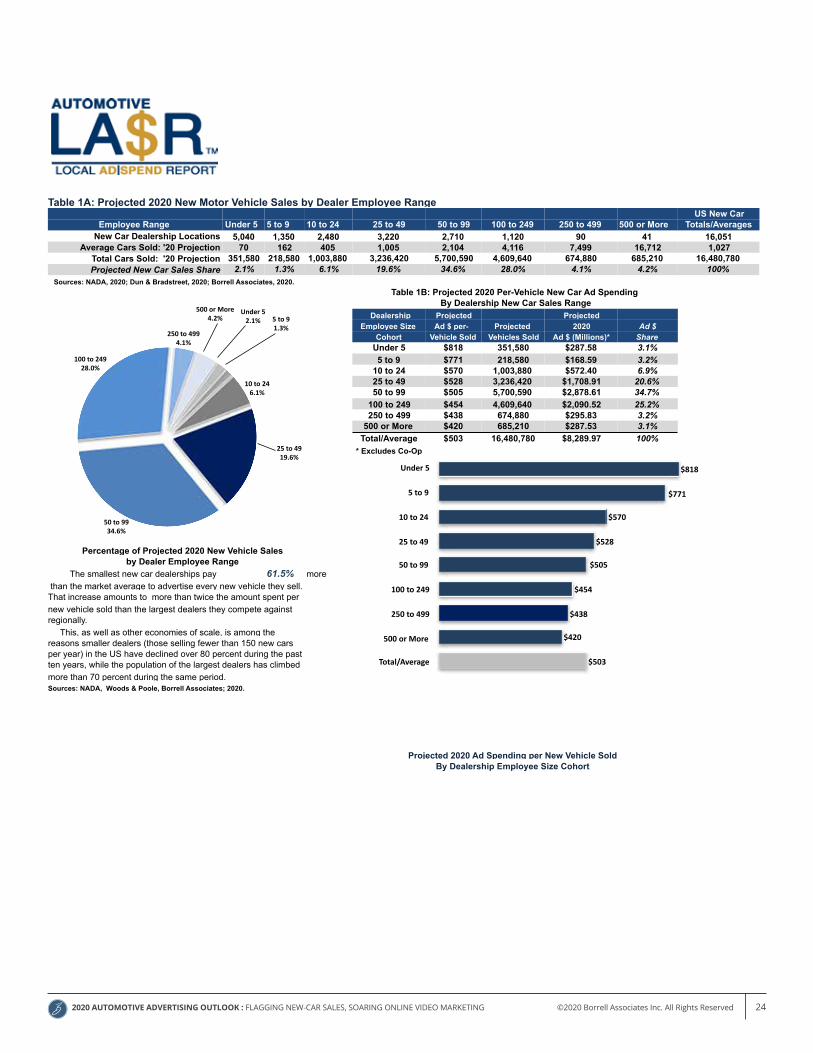

Table 1A: Projected 2020 New Motor Vehicle Sales by Dealer Employee RangeUS New Car

Employee Range Under 5 5 to 9 10 to 24 25 to 49 50 to 99 100 to 249 250 to 499 500 or More Totals/AveragesNew Car Dealership Locations 5,040 1,350 2,480 3,220 2,710 1,120 90 41 16,051

Average Cars Sold: '20 Projection 70 162 405 1,005 2,104 4,116 7,499 16,712 1,027Total Cars Sold: '20 Projection 351,580 218,580 1,003,880 3,236,420 5,700,590 4,609,640 674,880 685,210 16,480,780Projected New Car Sales Share 2.1% 1.3% 6.1% 19.6% 34.6% 28.0% 4.1% 4.2% 100%

Sources: NADA, 2020; Dun & Bradstreet, 2020; Borrell Associates, 2020.Table 1B: Projected 2020 Per-Vehicle New Car Ad Spending

By Dealership New Car Sales Range Dealership Projected Projected

Employee Size Ad $ per- Projected 2020 Ad $Cohort Vehicle Sold Vehicles Sold Ad $ (Millions)* Share

Under 5 $818 351,580 $287.58 3.1%5 to 9 $771 218,580 $168.59 3.2%

10 to 24 $570 1,003,880 $572.40 6.9%25 to 49 $528 3,236,420 $1,708.91 20.6%50 to 99 $505 5,700,590 $2,878.61 34.7%

100 to 249 $454 4,609,640 $2,090.52 25.2%250 to 499 $438 674,880 $295.83 3.2%

500 or More $420 685,210 $287.53 3.1%Total/Average $503 16,480,780 $8,289.97 100%

* Excludes Co-Op

Percentage of Projected 2020 New Vehicle Sales by Dealer Employee Range

The smallest new car dealerships pay 61.5% more than the market average to advertise every new vehicle they sell.That increase amounts to more than twice the amount spent per new vehicle sold than the largest dealers they compete againstregionally. 0.614914425427873 This, as well as other economies of scale, is among thereasons smaller dealers (those selling fewer than 150 new carsper year) in the US have declined over 80 percent during the pastten years, while the population of the largest dealers has climbedmore than 70 percent during the same period.Sources: NADA, Woods & Poole, Borrell Associates; 2020.

Projected 2020 Ad Spending per New Vehicle SoldBy Dealership Employee Size Cohort

© 2020, Borrell Associates Inc. All rights reserved.

Under5

5to9

10to24

25to49

50to99

100to249

250to499

500orMore

Total/Average $503

$420

$438

$454

$505

$528

$570

$771

$818

Page of 1 1

Market-level Auto Ad Spending Estimates

Market: Total US

Drawn From 2020 Data

Thisreportconsistsof6tables:

NewVehicles-Table1:Projected2020marketsalesbydealeremployeerange.Table2:Projected2020adspendingbymediachoice.

UsedVehicles-Table1:Projected2020marketsalesbydealeremployeerange.Table2:Projected2020adspendingbymediachoice.

2020-2025Forecastofnewvehiclespendingbymediachoice.

2020-2025Forecastofusedvehiclespendingbymediachoice.

Borrell'stableareportusesdatafromNADA,Scarborough,Woods&Poole,NIADA,MannheimAuctions,Dun&Bradstreet,andtheU.S.BureauofTransportationStatisticstocreateanassessmentofnewandusedvehiclepurchasingandassociatedadspendingatthemarketlevel.Forbestresults,printthisreportusingacolorprinter.Forfurtherinformationabouttheestimates,projections,andforecastsinthisreport,contactBorrellAssociatesat757/221-6641,[email protected].

1

100 to 24928.0%

250 to 4994.1%

500 or More4.2%

Under 52.1% 5 to 9

1.3%

10 to 246.1%

25 to 4919.6%

50 to 9934.6%

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 25

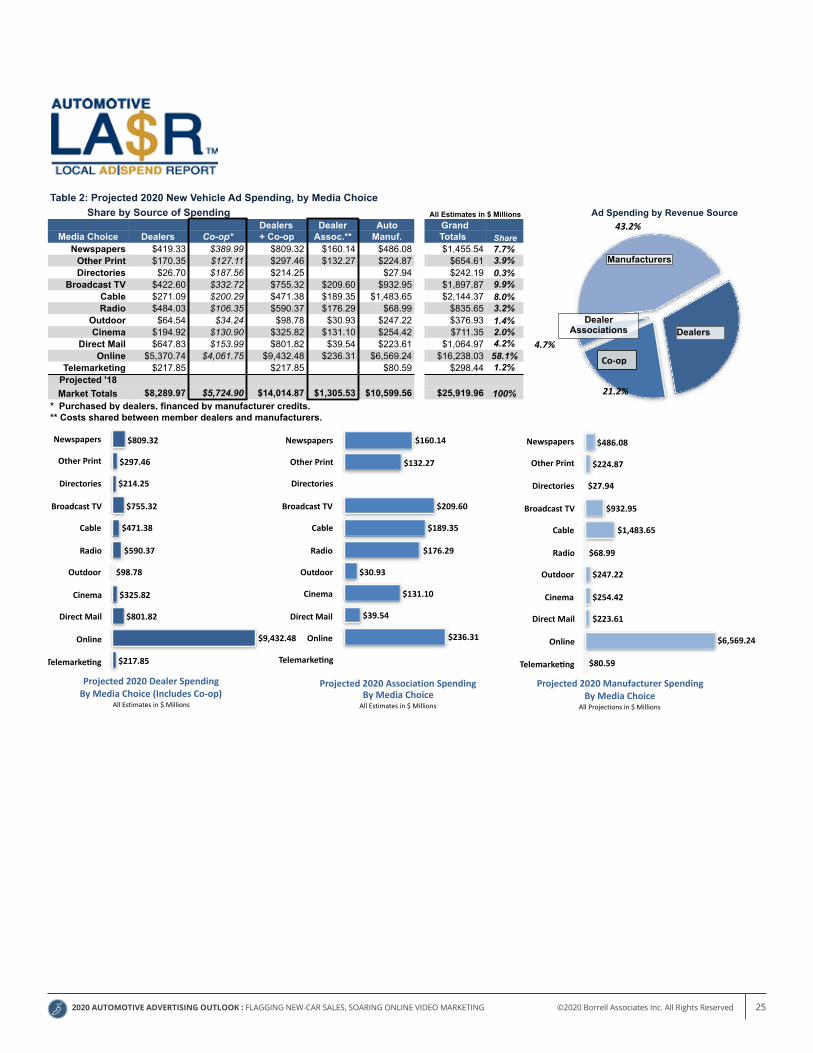

Table 2: Projected 2020 New Vehicle Ad Spending, by Media Choice Share by Source of Spending All Estimates in $ Millions Ad Spending by Revenue Source

Dealers Dealer Auto Grand $8,454.78Media Choice Dealers Co-op* + Co-op Assoc.** Manuf. Totals Share $5,829.40

Newspapers $419.33 $389.99 $809.32 $160.14 $486.08 $1,455.54 7.7% $1,291.68Other Print $170.35 $127.11 $297.46 $132.27 $224.87 $654.61 3.9% $11,868.39Directories $26.70 $187.56 $214.25 $27.94 $242.19 0.3%

Broadcast TV $422.60 $332.72 $755.32 $209.60 $932.95 $1,897.87 9.9%Cable $271.09 $200.29 $471.38 $189.35 $1,483.65 $2,144.37 8.0%Radio $484.03 $106.35 $590.37 $176.29 $68.99 $835.65 3.2%

Outdoor $64.54 $34.24 $98.78 $30.93 $247.22 $376.93 1.4%Cinema $194.92 $130.90 $325.82 $131.10 $254.42 $711.35 2.0%

Direct Mail $647.83 $153.99 $801.82 $39.54 $223.61 $1,064.97 4.2%Online $5,370.74 $4,061.75 $9,432.48 $236.31 $6,569.24 $16,238.03 58.1%

Telemarketing $217.85 $217.85 $80.59 $298.44 1.2%Projected '18Market Totals $8,289.97 $5,724.90 $14,014.87 $1,305.53 $10,599.56 $25,919.96 100%

* Purchased by dealers, financed by manufacturer credits.** Costs shared between member dealers and manufacturers.

© 2020, Borrell Associates Inc. All rights reserved.

43.2%

4.7%

21.2%30.8%

Dealer Associations

Manufacturers

Dealers

Newspapers

OtherPrint

Directories

BroadcastTV

Cable

Radio

Outdoor

Cinema

DirectMail

Online

Telemarke>ng $217.85

$9,432.48

$801.82

$325.82

$98.78

$590.37

$471.38

$755.32

$214.25

$297.46

$809.32 Newspapers

OtherPrint

Directories

BroadcastTV

Cable

Radio

Outdoor

Cinema

DirectMail

Online

Telemarke>ng

$236.31

$39.54

$131.10

$30.93

$176.29

$189.35

$209.60

$132.27

$160.14 Newspapers

OtherPrint

Directories

BroadcastTV

Cable

Radio

Outdoor

Cinema

DirectMail

Online

Telemarke>ng $80.59

$6,569.24

$223.61

$254.42

$247.22

$68.99

$1,483.65

$932.95

$27.94

$224.87

$486.08

Projected2020DealerSpendingByMediaChoice(IncludesCo-op)

AllEstimatesin$Millions

Projected2020AssociationSpendingByMediaChoiceAllEstimatesin$Millions

Projected2020ManufacturerSpendingByMediaChoice

AllProjectionsin$Millions

Co-op

Page of 1 1

Market-level Auto Ad Spending Estimates

Market: Total US

Drawn From 2020 Data

Thisreportconsistsof6tables:

NewVehicles-Table1:Projected2020marketsalesbydealeremployeerange.Table2:Projected2020adspendingbymediachoice.

UsedVehicles-Table1:Projected2020marketsalesbydealeremployeerange.Table2:Projected2020adspendingbymediachoice.

2020-2025Forecastofnewvehiclespendingbymediachoice.

2020-2025Forecastofusedvehiclespendingbymediachoice.

Borrell'stableareportusesdatafromNADA,Scarborough,Woods&Poole,NIADA,MannheimAuctions,Dun&Bradstreet,andtheU.S.BureauofTransportationStatisticstocreateanassessmentofnewandusedvehiclepurchasingandassociatedadspendingatthemarketlevel.Forbestresults,printthisreportusingacolorprinter.Forfurtherinformationabouttheestimates,projections,andforecastsinthisreport,contactBorrellAssociatesat757/221-6641,[email protected].

1

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 26

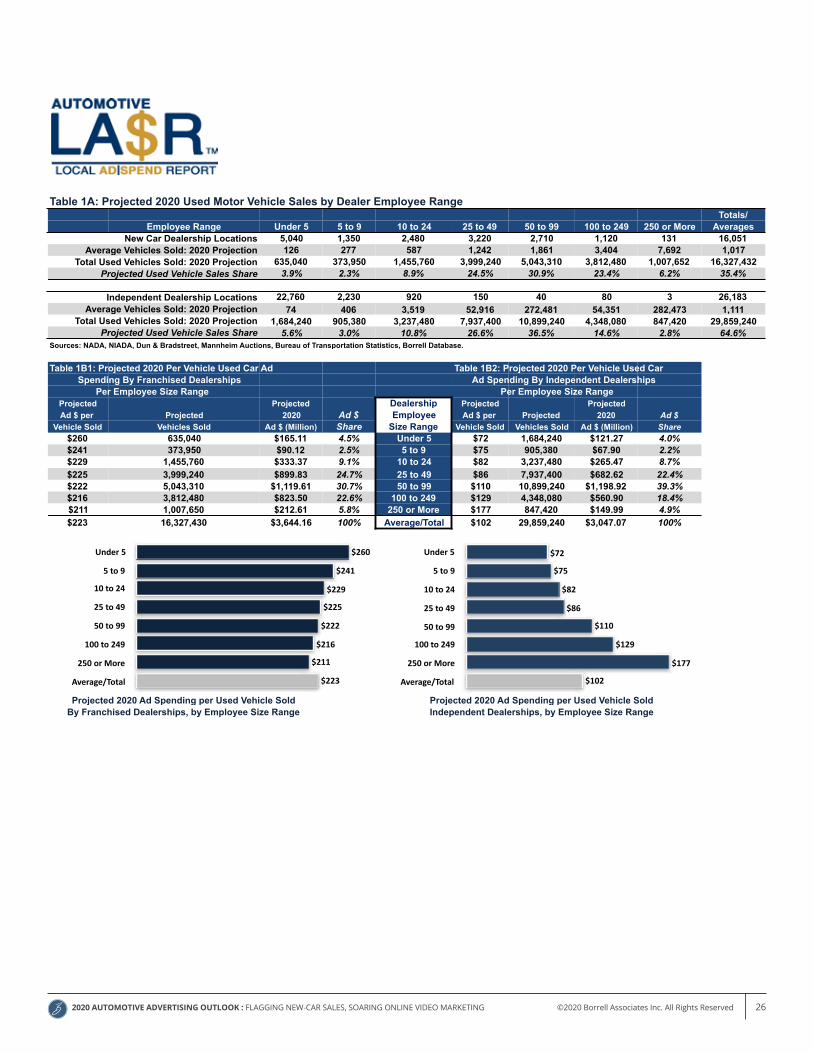

Table 1A: Projected 2020 Used Motor Vehicle Sales by Dealer Employee RangeTotals/

Employee Range Under 5 5 to 9 10 to 24 25 to 49 50 to 99 100 to 249 250 or More AveragesNew Car Dealership Locations 5,040 1,350 2,480 3,220 2,710 1,120 131 16,051

Average Vehicles Sold: 2020 Projection 126 277 587 1,242 1,861 3,404 7,692 1,017Total Used Vehicles Sold: 2020 Projection 635,040 373,950 1,455,760 3,999,240 5,043,310 3,812,480 1,007,652 16,327,432

Projected Used Vehicle Sales Share 3.9% 2.3% 8.9% 24.5% 30.9% 23.4% 6.2% 35.4%

Independent Dealership Locations 22,760 2,230 920 150 40 80 3 26,183Average Vehicles Sold: 2020 Projection 74 406 3,519 52,916 272,481 54,351 282,473 1,111

Total Used Vehicles Sold: 2020 Projection 1,684,240 905,380 3,237,480 7,937,400 10,899,240 4,348,080 847,420 29,859,240Projected Used Vehicle Sales Share 5.6% 3.0% 10.8% 26.6% 36.5% 14.6% 2.8% 64.6%

Sources: NADA, NIADA, Dun & Bradstreet, Mannheim Auctions, Bureau of Transportation Statistics, Borrell Database.

Table 1B1: Projected 2020 Per Vehicle Used Car Ad Table 1B2: Projected 2020 Per Vehicle Used Car Spending By Franchised Dealerships Ad Spending By Independent Dealerships

Per Employee Size Range Per Employee Size RangeProjected Projected Dealership Projected ProjectedAd $ per Projected 2020 Ad $ Employee Ad $ per Projected 2020 Ad $

Vehicle Sold Vehicles Sold Ad $ (Million) Share Size Range Vehicle Sold Vehicles Sold Ad $ (Million) Share$260 635,040 $165.11 4.5% Under 5 $72 1,684,240 $121.27 4.0%$241 373,950 $90.12 2.5% 5 to 9 $75 905,380 $67.90 2.2%$229 1,455,760 $333.37 9.1% 10 to 24 $82 3,237,480 $265.47 8.7%$225 3,999,240 $899.83 24.7% 25 to 49 $86 7,937,400 $682.62 22.4%$222 5,043,310 $1,119.61 30.7% 50 to 99 $110 10,899,240 $1,198.92 39.3%$216 3,812,480 $823.50 22.6% 100 to 249 $129 4,348,080 $560.90 18.4%$211 1,007,650 $212.61 5.8% 250 or More $177 847,420 $149.99 4.9%$223 16,327,430 $3,644.16 100% Average/Total $102 29,859,240 $3,047.07 100%

Projected 2020 Ad Spending per Used Vehicle Sold Projected 2020 Ad Spending per Used Vehicle SoldBy Franchised Dealerships, by Employee Size Range Independent Dealerships, by Employee Size Range

© 2020, Borrell Associates Inc. All rights reserved.

Under5

5to9

10to24

25to49

50to99

100to249

250orMore

Average/Total $102

$177

$129

$110

$86

$82

$75

$72Under5

5to9

10to24

25to49

50to99

100to249

250orMore

Average/Total $223

$211

$216

$222

$225

$229

$241

$260

Page of 1 1

Market-level Auto Ad Spending Estimates

Market: Total US

Drawn From 2020 Data

Thisreportconsistsof6tables:

NewVehicles-Table1:Projected2020marketsalesbydealeremployeerange.Table2:Projected2020adspendingbymediachoice.

UsedVehicles-Table1:Projected2020marketsalesbydealeremployeerange.Table2:Projected2020adspendingbymediachoice.

2020-2025Forecastofnewvehiclespendingbymediachoice.

2020-2025Forecastofusedvehiclespendingbymediachoice.

Borrell'stableareportusesdatafromNADA,Scarborough,Woods&Poole,NIADA,MannheimAuctions,Dun&Bradstreet,andtheU.S.BureauofTransportationStatisticstocreateanassessmentofnewandusedvehiclepurchasingandassociatedadspendingatthemarketlevel.Forbestresults,printthisreportusingacolorprinter.Forfurtherinformationabouttheestimates,projections,andforecastsinthisreport,contactBorrellAssociatesat757/221-6641,[email protected].

1

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 27

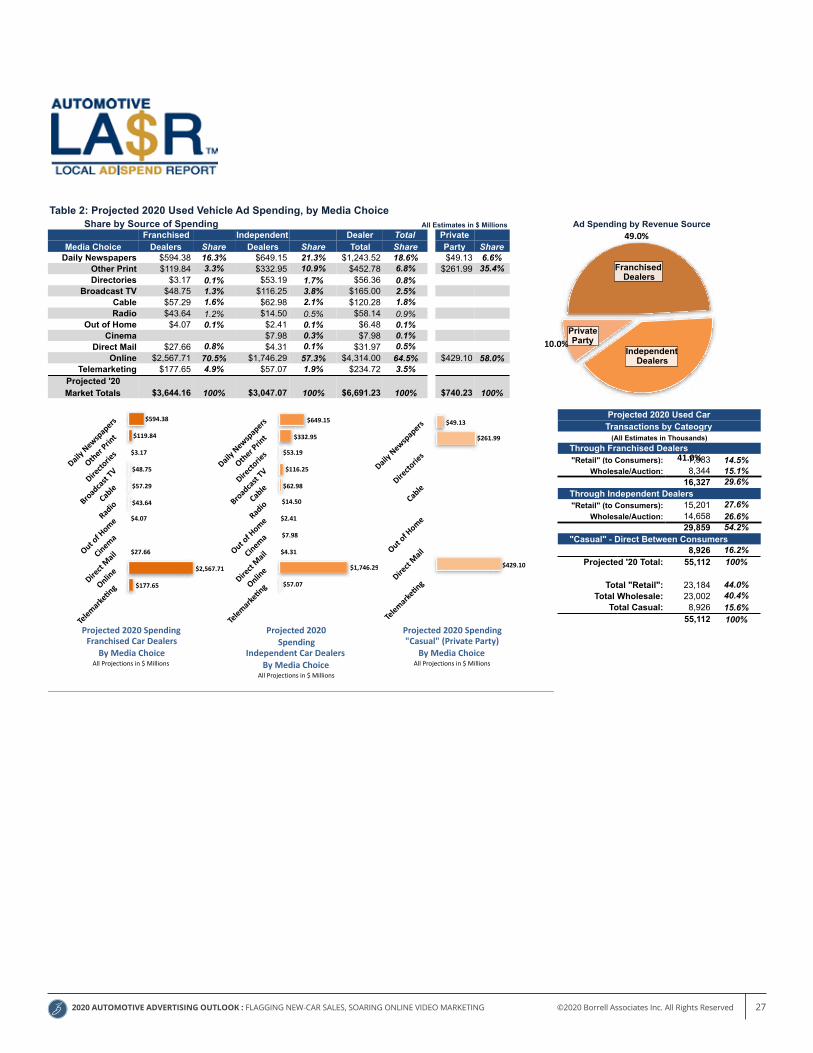

Table 2: Projected 2020 Used Vehicle Ad Spending, by Media Choice Share by Source of Spending All Estimates in $ Millions Ad Spending by Revenue Source

Franchised Independent Dealer Total Private$3,644.16

Media Choice Dealers Share Dealers Share Total Share Party Share$3,047.07

Daily Newspapers $594.38 16.3% $649.15 21.3% $1,243.52 18.6% $49.13 6.6%$740.23

Other Print $119.84 3.3% $332.95 10.9% $452.78 6.8% $261.99 35.4%Directories $3.17 0.1% $53.19 1.7% $56.36 0.8%

Broadcast TV $48.75 1.3% $116.25 3.8% $165.00 2.5%Cable $57.29 1.6% $62.98 2.1% $120.28 1.8%Radio $43.64 1.2% $14.50 0.5% $58.14 0.9%

Out of Home $4.07 0.1% $2.41 0.1% $6.48 0.1%Cinema $7.98 0.3% $7.98 0.1%

Direct Mail $27.66 0.8% $4.31 0.1% $31.97 0.5%Online $2,567.71 70.5% $1,746.29 57.3% $4,314.00 64.5% $429.10 58.0%

Telemarketing $177.65 4.9% $57.07 1.9% $234.72 3.5%Projected '20Market Totals $3,644.16 100% $3,047.07 100% $6,691.23 100% $740.23 100%

Projected 2020 Used CarTransactions by Cateogry

(All Estimates in Thousands) Through Franchised Dealers

"Retail" (to Consumers): 7,983 14.5%Wholesale/Auction: 8,344 15.1%

16,327 29.6% Through Independent Dealers

"Retail" (to Consumers): 15,201 27.6%Wholesale/Auction: 14,658 26.6%

29,859 54.2% "Casual" - Direct Between Consumers

8,926 16.2%Projected '20 Total: 55,112 100%

Total "Retail": 23,184 44.0%Total Wholesale: 23,002 40.4%

Total Casual: 8,926 15.6%55,112 100%

© 2020, Borrell Associates Inc. All rights reserved.

10.0%

41.0%

49.0%

Franchised Dealers

Private Party

DailyNe

wspa

pers

Othe

rPrin

t

Director

ies

Broa

dcast

TV

Cable

Radio

Outo

fHom

e

Cinem

a

DirectM

ail

Onlin

e

Telem

arkeA

ng$177.65

$2,567.71

$27.66

$4.07

$43.64

$57.29

$48.75

$3.17

$119.84

$594.38

DailyNe

wspa

pers

Othe

rPrin

t

Director

ies

Broa

dcast

TV

Cable

Radio

Outo

fHom

e

Cinem

a

DirectM

ail

Onlin

e

Telem

arkeA

ng$57.07

$1,746.29

$4.31

$7.98

$2.41

$14.50

$62.98

$116.25

$53.19

$332.95

$649.15

Independent Dealers

DailyNe

wspa

pers

Director

ies

Cable

Outo

fHom

e

DirectM

ail

Telem

arkeA

ng

$429.10

$261.99

$49.13

Projected2020SpendingFranchisedCarDealers

ByMediaChoiceAllProjectionsin$Millions

Projected2020Spending"Casual"(PrivateParty)

ByMediaChoiceAllProjectionsin$Millions

Projected2020Spending

IndependentCarDealersByMediaChoice

AllProjectionsin$Millions

Page of 1 1

Market-level Auto Ad Spending Estimates

Market: Total US

Drawn From 2020 Data

Thisreportconsistsof6tables:

NewVehicles-Table1:Projected2020marketsalesbydealeremployeerange.Table2:Projected2020adspendingbymediachoice.

UsedVehicles-Table1:Projected2020marketsalesbydealeremployeerange.Table2:Projected2020adspendingbymediachoice.

2020-2025Forecastofnewvehiclespendingbymediachoice.

2020-2025Forecastofusedvehiclespendingbymediachoice.

Borrell'stableareportusesdatafromNADA,Scarborough,Woods&Poole,NIADA,MannheimAuctions,Dun&Bradstreet,andtheU.S.BureauofTransportationStatisticstocreateanassessmentofnewandusedvehiclepurchasingandassociatedadspendingatthemarketlevel.Forbestresults,printthisreportusingacolorprinter.Forfurtherinformationabouttheestimates,projections,andforecastsinthisreport,contactBorrellAssociatesat757/221-6641,[email protected].

1

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 28

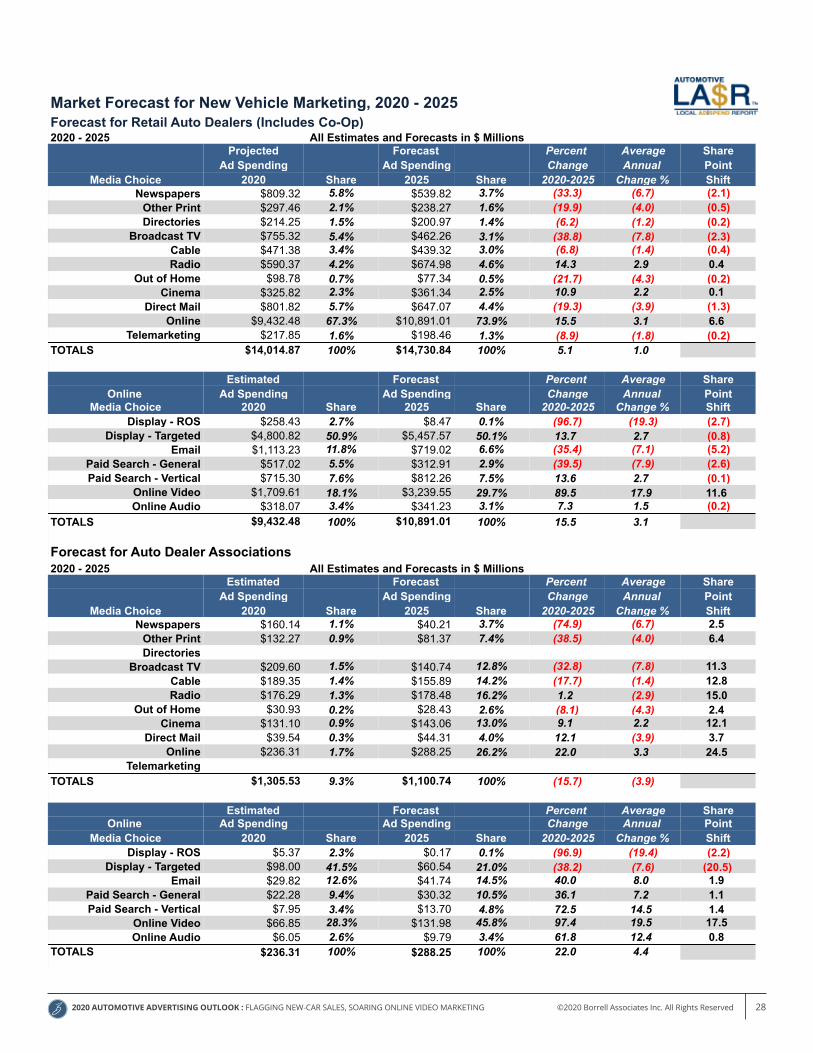

Market Forecast for New Vehicle Marketing, 2020 - 2025Forecast for Retail Auto Dealers (Includes Co-Op)2020 - 2025 All Estimates and Forecasts in $ Millions

Projected Forecast Percent Average ShareAd Spending Ad Spending Change Annual Point

Media Choice 2020 Share 2025 Share 2020-2025 Change % ShiftNewspapers $809.32 5.8% $539.82 3.7% (33.3) (6.7) (2.1)

Other Print $297.46 2.1% $238.27 1.6% (19.9) (4.0) (0.5)Directories $214.25 1.5% $200.97 1.4% (6.2) (1.2) (0.2)

Broadcast TV $755.32 5.4% $462.26 3.1% (38.8) (7.8) (2.3)Cable $471.38 3.4% $439.32 3.0% (6.8) (1.4) (0.4)Radio $590.37 4.2% $674.98 4.6% 14.3 2.9 0.4

Out of Home $98.78 0.7% $77.34 0.5% (21.7) (4.3) (0.2)Cinema $325.82 2.3% $361.34 2.5% 10.9 2.2 0.1

Direct Mail $801.82 5.7% $647.07 4.4% (19.3) (3.9) (1.3)Online $9,432.48 67.3% $10,891.01 73.9% 15.5 3.1 6.6

Telemarketing $217.85 1.6% $198.46 1.3% (8.9) (1.8) (0.2)TOTALS $14,014.87 100% $14,730.84 100% 5.1 1.0

Estimated Forecast Percent Average ShareOnline Ad Spending Ad Spending Change Annual Point

Media Choice 2020 Share 2025 Share 2020-2025 Change % ShiftDisplay - ROS $258.43 2.7% $8.47 0.1% (96.7) (19.3) (2.7)

Display - Targeted $4,800.82 50.9% $5,457.57 50.1% 13.7 2.7 (0.8)Email $1,113.23 11.8% $719.02 6.6% (35.4) (7.1) (5.2)

Paid Search - General $517.02 5.5% $312.91 2.9% (39.5) (7.9) (2.6)Paid Search - Vertical $715.30 7.6% $812.26 7.5% 13.6 2.7 (0.1)

Online Video $1,709.61 18.1% $3,239.55 29.7% 89.5 17.9 11.6 Online Audio $318.07 3.4% $341.23 3.1% 7.3 1.5 (0.2)

TOTALS $9,432.48 100% $10,891.01 100% 15.5 3.1

Forecast for Auto Dealer Associations2020 - 2025 All Estimates and Forecasts in $ Millions

Estimated Forecast Percent Average ShareAd Spending Ad Spending Change Annual Point

Media Choice 2020 Share 2025 Share 2020-2025 Change % ShiftNewspapers $160.14 1.1% $40.21 3.7% (74.9) (6.7) 2.5

Other Print $132.27 0.9% $81.37 7.4% (38.5) (4.0) 6.4 Directories

Broadcast TV $209.60 1.5% $140.74 12.8% (32.8) (7.8) 11.3 Cable $189.35 1.4% $155.89 14.2% (17.7) (1.4) 12.8 Radio $176.29 1.3% $178.48 16.2% 1.2 (2.9) 15.0

Out of Home $30.93 0.2% $28.43 2.6% (8.1) (4.3) 2.4 Cinema $131.10 0.9% $143.06 13.0% 9.1 2.2 12.1

Direct Mail $39.54 0.3% $44.31 4.0% 12.1 (3.9) 3.7 Online $236.31 1.7% $288.25 26.2% 22.0 3.3 24.5

TelemarketingTOTALS $1,305.53 9.3% $1,100.74 100% (15.7) (3.9)

Estimated Forecast Percent Average ShareOnline Ad Spending Ad Spending Change Annual Point

Media Choice 2020 Share 2025 Share 2020-2025 Change % ShiftDisplay - ROS $5.37 2.3% $0.17 0.1% (96.9) (19.4) (2.2)

Display - Targeted $98.00 41.5% $60.54 21.0% (38.2) (7.6) (20.5)Email $29.82 12.6% $41.74 14.5% 40.0 8.0 1.9

Paid Search - General $22.28 9.4% $30.32 10.5% 36.1 7.2 1.1 Paid Search - Vertical $7.95 3.4% $13.70 4.8% 72.5 14.5 1.4

Online Video $66.85 28.3% $131.98 45.8% 97.4 19.5 17.5 Online Audio $6.05 2.6% $9.79 3.4% 61.8 12.4 0.8

TOTALS $236.31 100% $288.25 100% 22.0 4.4

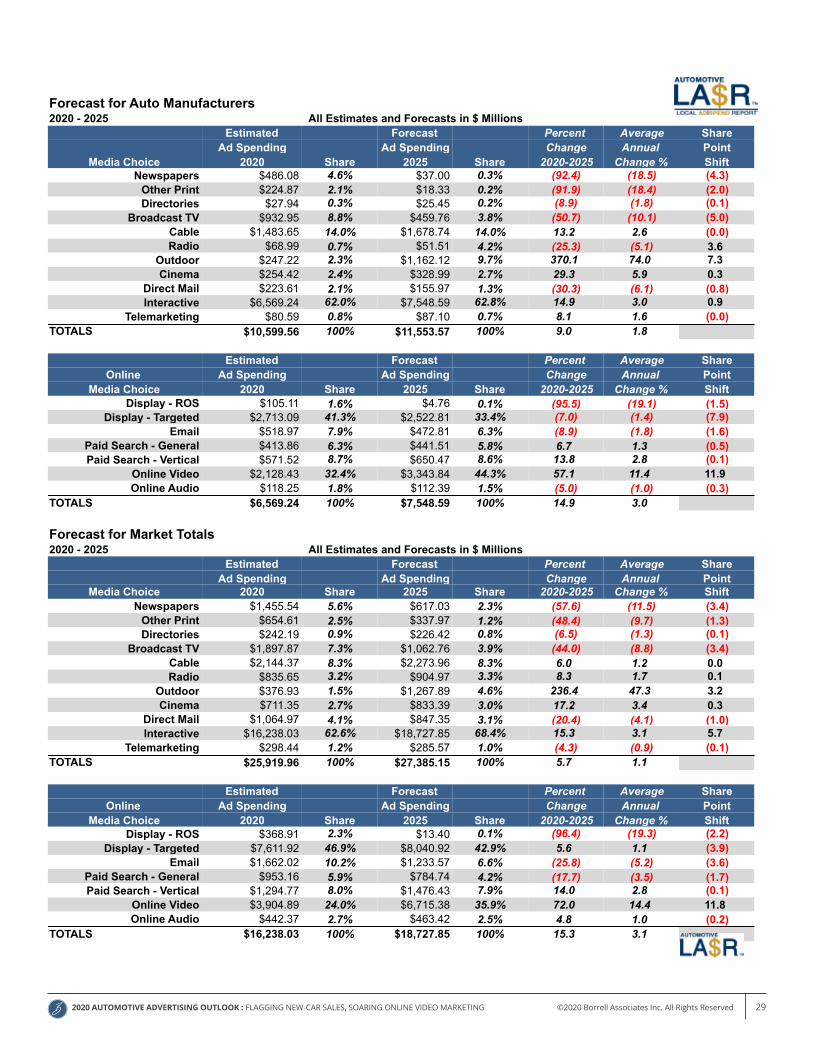

Forecast for Auto Manufacturers2020 - 2025 All Estimates and Forecasts in $ Millions

Estimated Forecast Percent Average ShareAd Spending Ad Spending Change Annual Point

Media Choice 2020 Share 2025 Share 2020-2025 Change % ShiftNewspapers $486.08 4.6% $37.00 0.3% (92.4) (18.5) (4.3)

Other Print $224.87 2.1% $18.33 0.2% (91.9) (18.4) (2.0)

Page of 1 4

Market-level Auto Ad Spending Estimates

Market: Total US

Drawn From 2020 Data

Thisreportconsistsof6tables:

NewVehicles-Table1:Projected2020marketsalesbydealeremployeerange.Table2:Projected2020adspendingbymediachoice.

UsedVehicles-Table1:Projected2020marketsalesbydealeremployeerange.Table2:Projected2020adspendingbymediachoice.

2020-2025Forecastofnewvehiclespendingbymediachoice.

2020-2025Forecastofusedvehiclespendingbymediachoice.

Borrell'stableareportusesdatafromNADA,Scarborough,Woods&Poole,NIADA,MannheimAuctions,Dun&Bradstreet,andtheU.S.BureauofTransportationStatisticstocreateanassessmentofnewandusedvehiclepurchasingandassociatedadspendingatthemarketlevel.Forbestresults,printthisreportusingacolorprinter.Forfurtherinformationabouttheestimates,projections,andforecastsinthisreport,contactBorrellAssociatesat757/221-6641,[email protected].

1

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 29

Market Forecast for New Vehicle Marketing, 2020 - 2025Forecast for Retail Auto Dealers (Includes Co-Op)2020 - 2025 All Estimates and Forecasts in $ Millions

Projected Forecast Percent Average ShareAd Spending Ad Spending Change Annual Point

Media Choice 2020 Share 2025 Share 2020-2025 Change % ShiftNewspapers $809.32 5.8% $539.82 3.7% (33.3) (6.7) (2.1)

Other Print $297.46 2.1% $238.27 1.6% (19.9) (4.0) (0.5)Directories $214.25 1.5% $200.97 1.4% (6.2) (1.2) (0.2)

Broadcast TV $755.32 5.4% $462.26 3.1% (38.8) (7.8) (2.3)Cable $471.38 3.4% $439.32 3.0% (6.8) (1.4) (0.4)Radio $590.37 4.2% $674.98 4.6% 14.3 2.9 0.4

Out of Home $98.78 0.7% $77.34 0.5% (21.7) (4.3) (0.2)Cinema $325.82 2.3% $361.34 2.5% 10.9 2.2 0.1

Direct Mail $801.82 5.7% $647.07 4.4% (19.3) (3.9) (1.3)Online $9,432.48 67.3% $10,891.01 73.9% 15.5 3.1 6.6

Telemarketing $217.85 1.6% $198.46 1.3% (8.9) (1.8) (0.2)TOTALS $14,014.87 100% $14,730.84 100% 5.1 1.0

Estimated Forecast Percent Average ShareOnline Ad Spending Ad Spending Change Annual Point

Media Choice 2020 Share 2025 Share 2020-2025 Change % ShiftDisplay - ROS $258.43 2.7% $8.47 0.1% (96.7) (19.3) (2.7)

Display - Targeted $4,800.82 50.9% $5,457.57 50.1% 13.7 2.7 (0.8)Email $1,113.23 11.8% $719.02 6.6% (35.4) (7.1) (5.2)

Paid Search - General $517.02 5.5% $312.91 2.9% (39.5) (7.9) (2.6)Paid Search - Vertical $715.30 7.6% $812.26 7.5% 13.6 2.7 (0.1)

Online Video $1,709.61 18.1% $3,239.55 29.7% 89.5 17.9 11.6 Online Audio $318.07 3.4% $341.23 3.1% 7.3 1.5 (0.2)

TOTALS $9,432.48 100% $10,891.01 100% 15.5 3.1

Forecast for Auto Dealer Associations2020 - 2025 All Estimates and Forecasts in $ Millions

Estimated Forecast Percent Average ShareAd Spending Ad Spending Change Annual Point

Media Choice 2020 Share 2025 Share 2020-2025 Change % ShiftNewspapers $160.14 1.1% $40.21 3.7% (74.9) (6.7) 2.5

Other Print $132.27 0.9% $81.37 7.4% (38.5) (4.0) 6.4 Directories

Broadcast TV $209.60 1.5% $140.74 12.8% (32.8) (7.8) 11.3 Cable $189.35 1.4% $155.89 14.2% (17.7) (1.4) 12.8 Radio $176.29 1.3% $178.48 16.2% 1.2 (2.9) 15.0

Out of Home $30.93 0.2% $28.43 2.6% (8.1) (4.3) 2.4 Cinema $131.10 0.9% $143.06 13.0% 9.1 2.2 12.1

Direct Mail $39.54 0.3% $44.31 4.0% 12.1 (3.9) 3.7 Online $236.31 1.7% $288.25 26.2% 22.0 3.3 24.5

TelemarketingTOTALS $1,305.53 9.3% $1,100.74 100% (15.7) (3.9)

Estimated Forecast Percent Average ShareOnline Ad Spending Ad Spending Change Annual Point

Media Choice 2020 Share 2025 Share 2020-2025 Change % ShiftDisplay - ROS $5.37 2.3% $0.17 0.1% (96.9) (19.4) (2.2)

Display - Targeted $98.00 41.5% $60.54 21.0% (38.2) (7.6) (20.5)Email $29.82 12.6% $41.74 14.5% 40.0 8.0 1.9

Paid Search - General $22.28 9.4% $30.32 10.5% 36.1 7.2 1.1 Paid Search - Vertical $7.95 3.4% $13.70 4.8% 72.5 14.5 1.4

Online Video $66.85 28.3% $131.98 45.8% 97.4 19.5 17.5 Online Audio $6.05 2.6% $9.79 3.4% 61.8 12.4 0.8

TOTALS $236.31 100% $288.25 100% 22.0 4.4

Forecast for Auto Manufacturers2020 - 2025 All Estimates and Forecasts in $ Millions

Estimated Forecast Percent Average ShareAd Spending Ad Spending Change Annual Point

Media Choice 2020 Share 2025 Share 2020-2025 Change % ShiftNewspapers $486.08 4.6% $37.00 0.3% (92.4) (18.5) (4.3)

Other Print $224.87 2.1% $18.33 0.2% (91.9) (18.4) (2.0)

Page of 1 4Directories $27.94 0.3% $25.45 0.2% (8.9) (1.8) (0.1)

Broadcast TV $932.95 8.8% $459.76 3.8% (50.7) (10.1) (5.0)Cable $1,483.65 14.0% $1,678.74 14.0% 13.2 2.6 (0.0)Radio $68.99 0.7% $51.51 4.2% (25.3) (5.1) 3.6

Outdoor $247.22 2.3% $1,162.12 9.7% 370.1 74.0 7.3 Cinema $254.42 2.4% $328.99 2.7% 29.3 5.9 0.3

Direct Mail $223.61 2.1% $155.97 1.3% (30.3) (6.1) (0.8)Interactive $6,569.24 62.0% $7,548.59 62.8% 14.9 3.0 0.9

Telemarketing $80.59 0.8% $87.10 0.7% 8.1 1.6 (0.0)TOTALS $10,599.56 100% $11,553.57 100% 9.0 1.8

Estimated Forecast Percent Average ShareOnline Ad Spending Ad Spending Change Annual Point

Media Choice 2020 Share 2025 Share 2020-2025 Change % ShiftDisplay - ROS $105.11 1.6% $4.76 0.1% (95.5) (19.1) (1.5)

Display - Targeted $2,713.09 41.3% $2,522.81 33.4% (7.0) (1.4) (7.9)Email $518.97 7.9% $472.81 6.3% (8.9) (1.8) (1.6)

Paid Search - General $413.86 6.3% $441.51 5.8% 6.7 1.3 (0.5)Paid Search - Vertical $571.52 8.7% $650.47 8.6% 13.8 2.8 (0.1)

Online Video $2,128.43 32.4% $3,343.84 44.3% 57.1 11.4 11.9 Online Audio $118.25 1.8% $112.39 1.5% (5.0) (1.0) (0.3)

TOTALS $6,569.24 100% $7,548.59 100% 14.9 3.0

Forecast for Market Totals2020 - 2025 All Estimates and Forecasts in $ Millions

Estimated Forecast Percent Average ShareAd Spending Ad Spending Change Annual Point

Media Choice 2020 Share 2025 Share 2020-2025 Change % ShiftNewspapers $1,455.54 5.6% $617.03 2.3% (57.6) (11.5) (3.4)

Other Print $654.61 2.5% $337.97 1.2% (48.4) (9.7) (1.3)Directories $242.19 0.9% $226.42 0.8% (6.5) (1.3) (0.1)

Broadcast TV $1,897.87 7.3% $1,062.76 3.9% (44.0) (8.8) (3.4)Cable $2,144.37 8.3% $2,273.96 8.3% 6.0 1.2 0.0 Radio $835.65 3.2% $904.97 3.3% 8.3 1.7 0.1

Outdoor $376.93 1.5% $1,267.89 4.6% 236.4 47.3 3.2 Cinema $711.35 2.7% $833.39 3.0% 17.2 3.4 0.3

Direct Mail $1,064.97 4.1% $847.35 3.1% (20.4) (4.1) (1.0)Interactive $16,238.03 62.6% $18,727.85 68.4% 15.3 3.1 5.7

Telemarketing $298.44 1.2% $285.57 1.0% (4.3) (0.9) (0.1)TOTALS $25,919.96 100% $27,385.15 100% 5.7 1.1

Estimated Forecast Percent Average ShareOnline Ad Spending Ad Spending Change Annual Point

Media Choice 2020 Share 2025 Share 2020-2025 Change % ShiftDisplay - ROS $368.91 2.3% $13.40 0.1% (96.4) (19.3) (2.2)

Display - Targeted $7,611.92 46.9% $8,040.92 42.9% 5.6 1.1 (3.9)Email $1,662.02 10.2% $1,233.57 6.6% (25.8) (5.2) (3.6)

Paid Search - General $953.16 5.9% $784.74 4.2% (17.7) (3.5) (1.7)Paid Search - Vertical $1,294.77 8.0% $1,476.43 7.9% 14.0 2.8 (0.1)

Online Video $3,904.89 24.0% $6,715.38 35.9% 72.0 14.4 11.8 Online Audio $442.37 2.7% $463.42 2.5% 4.8 1.0 (0.2)

TOTALS $16,238.03 100% $18,727.85 100% 15.3 3.1

© 2020, Borrell Associates Inc. All rights reserved.

Page of 2 4

Market-level Auto Ad Spending Estimates

Market: Total US

Drawn From 2020 Data

Thisreportconsistsof6tables:

NewVehicles-Table1:Projected2020marketsalesbydealeremployeerange.Table2:Projected2020adspendingbymediachoice.

UsedVehicles-Table1:Projected2020marketsalesbydealeremployeerange.Table2:Projected2020adspendingbymediachoice.

2020-2025Forecastofnewvehiclespendingbymediachoice.

2020-2025Forecastofusedvehiclespendingbymediachoice.

Borrell'stableareportusesdatafromNADA,Scarborough,Woods&Poole,NIADA,MannheimAuctions,Dun&Bradstreet,andtheU.S.BureauofTransportationStatisticstocreateanassessmentofnewandusedvehiclepurchasingandassociatedadspendingatthemarketlevel.Forbestresults,printthisreportusingacolorprinter.Forfurtherinformationabouttheestimates,projections,andforecastsinthisreport,contactBorrellAssociatesat757/221-6641,[email protected].

1

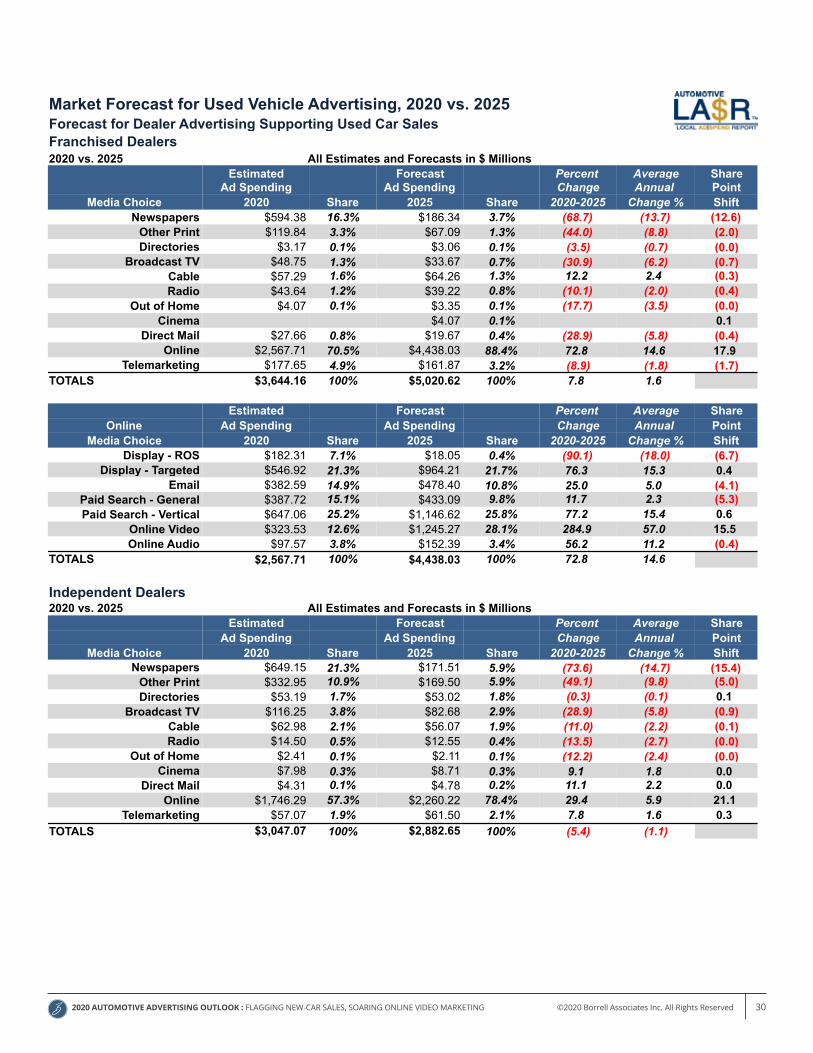

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 30

Market Forecast for Used Vehicle Advertising, 2020 vs. 2025Forecast for Dealer Advertising Supporting Used Car SalesFranchised Dealers2020 vs. 2025 All Estimates and Forecasts in $ Millions

Estimated Forecast Percent Average ShareAd Spending Ad Spending Change Annual Point

Media Choice 2020 Share 2025 Share 2020-2025 Change % ShiftNewspapers $594.38 16.3% $186.34 3.7% (68.7) (13.7) (12.6)

Other Print $119.84 3.3% $67.09 1.3% (44.0) (8.8) (2.0)Directories $3.17 0.1% $3.06 0.1% (3.5) (0.7) (0.0)

Broadcast TV $48.75 1.3% $33.67 0.7% (30.9) (6.2) (0.7)Cable $57.29 1.6% $64.26 1.3% 12.2 2.4 (0.3)Radio $43.64 1.2% $39.22 0.8% (10.1) (2.0) (0.4)

Out of Home $4.07 0.1% $3.35 0.1% (17.7) (3.5) (0.0)Cinema $4.07 0.1% 0.1

Direct Mail $27.66 0.8% $19.67 0.4% (28.9) (5.8) (0.4)Online $2,567.71 70.5% $4,438.03 88.4% 72.8 14.6 17.9

Telemarketing $177.65 4.9% $161.87 3.2% (8.9) (1.8) (1.7)TOTALS $3,644.16 100% $5,020.62 100% 7.8 1.6

Estimated Forecast Percent Average ShareOnline Ad Spending Ad Spending Change Annual Point

Media Choice 2020 Share 2025 Share 2020-2025 Change % ShiftDisplay - ROS $182.31 7.1% $18.05 0.4% (90.1) (18.0) (6.7)

Display - Targeted $546.92 21.3% $964.21 21.7% 76.3 15.3 0.4 Email $382.59 14.9% $478.40 10.8% 25.0 5.0 (4.1)

Paid Search - General $387.72 15.1% $433.09 9.8% 11.7 2.3 (5.3)Paid Search - Vertical $647.06 25.2% $1,146.62 25.8% 77.2 15.4 0.6

Online Video $323.53 12.6% $1,245.27 28.1% 284.9 57.0 15.5 Online Audio $97.57 3.8% $152.39 3.4% 56.2 11.2 (0.4)

TOTALS $2,567.71 100% $4,438.03 100% 72.8 14.6

Independent Dealers2020 vs. 2025 All Estimates and Forecasts in $ Millions

Estimated Forecast Percent Average ShareAd Spending Ad Spending Change Annual Point

Media Choice 2020 Share 2025 Share 2020-2025 Change % ShiftNewspapers $649.15 21.3% $171.51 5.9% (73.6) (14.7) (15.4)

Other Print $332.95 10.9% $169.50 5.9% (49.1) (9.8) (5.0)Directories $53.19 1.7% $53.02 1.8% (0.3) (0.1) 0.1

Broadcast TV $116.25 3.8% $82.68 2.9% (28.9) (5.8) (0.9)Cable $62.98 2.1% $56.07 1.9% (11.0) (2.2) (0.1)Radio $14.50 0.5% $12.55 0.4% (13.5) (2.7) (0.0)

Out of Home $2.41 0.1% $2.11 0.1% (12.2) (2.4) (0.0)Cinema $7.98 0.3% $8.71 0.3% 9.1 1.8 0.0

Direct Mail $4.31 0.1% $4.78 0.2% 11.1 2.2 0.0 Online $1,746.29 57.3% $2,260.22 78.4% 29.4 5.9 21.1

Telemarketing $57.07 1.9% $61.50 2.1% 7.8 1.6 0.3 TOTALS $3,047.07 100% $2,882.65 100% (5.4) (1.1)

Estimated Forecast Percent Average ShareOnline Ad Spending Ad Spending Change Annual Point

Media Choice 2020 Share 2025 Share 2020-2025 Change % ShiftDisplay - ROS $48.90 2.8% $4.35 0.2% (91.1) (18.2) (2.6)

Display - Targeted $656.60 37.6% $715.92 31.7% 9.0 1.8 (5.9)Email $171.14 9.8% $145.73 6.4% (14.8) (3.0) (3.4)

Paid Search - General $200.82 11.5% $207.80 9.2% 3.5 0.7 (2.3)Paid Search - Vertical $323.06 18.5% $379.55 16.8% 17.5 3.5 (1.7)

Online Video $281.15 16.1% $734.06 32.5% 161.1 32.2 16.4 Online Audio $64.61 3.7% $72.82 3.2% 12.7 2.5 (0.5)

TOTALS $1,746.29 100% $2,260.22 100% 29.4 5.9

Page of 1 4

Market-level Auto Ad Spending Estimates

Market: Total US

Drawn From 2020 Data

Thisreportconsistsof6tables:

NewVehicles-Table1:Projected2020marketsalesbydealeremployeerange.Table2:Projected2020adspendingbymediachoice.

UsedVehicles-Table1:Projected2020marketsalesbydealeremployeerange.Table2:Projected2020adspendingbymediachoice.

2020-2025Forecastofnewvehiclespendingbymediachoice.

2020-2025Forecastofusedvehiclespendingbymediachoice.

Borrell'stableareportusesdatafromNADA,Scarborough,Woods&Poole,NIADA,MannheimAuctions,Dun&Bradstreet,andtheU.S.BureauofTransportationStatisticstocreateanassessmentofnewandusedvehiclepurchasingandassociatedadspendingatthemarketlevel.Forbestresults,printthisreportusingacolorprinter.Forfurtherinformationabouttheestimates,projections,andforecastsinthisreport,contactBorrellAssociatesat757/221-6641,[email protected].

1

2020 AUTOMOTIVE ADVERTISING OUTLOOK : FLAGGING NEW-CAR SALES, SOARING ONLINE VIDEO MARKETING ©2020 Borrell Associates Inc. All Rights Reserved 31

Market Forecast for Used Vehicle Advertising, 2020 vs. 2025Forecast for Dealer Advertising Supporting Used Car SalesFranchised Dealers2020 vs. 2025 All Estimates and Forecasts in $ Millions