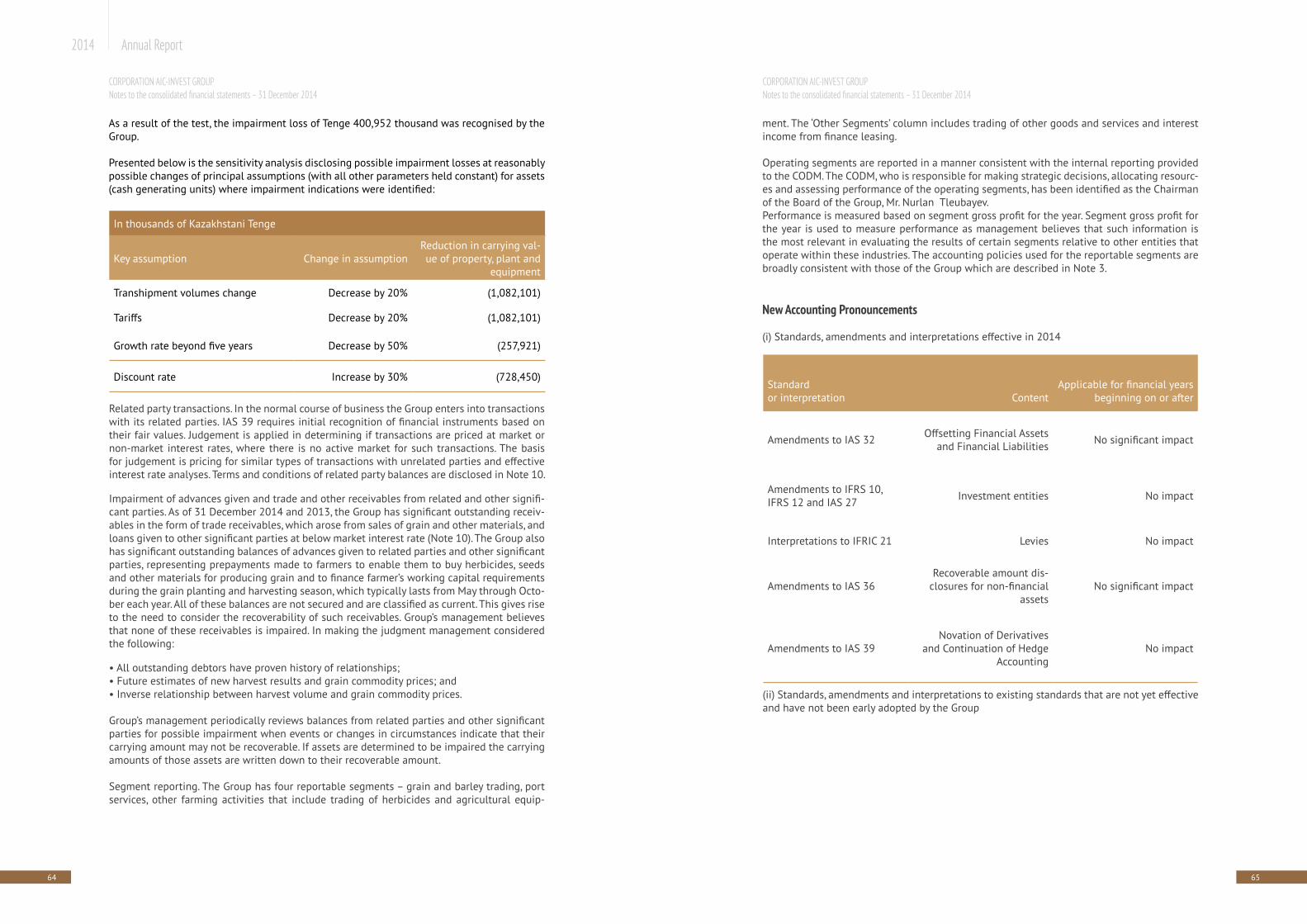

Embed Size (px)

Citation preview

2014 Annual Report

APK-Invest Corporation

ABOUT APK-INVEST CORPORATION 4

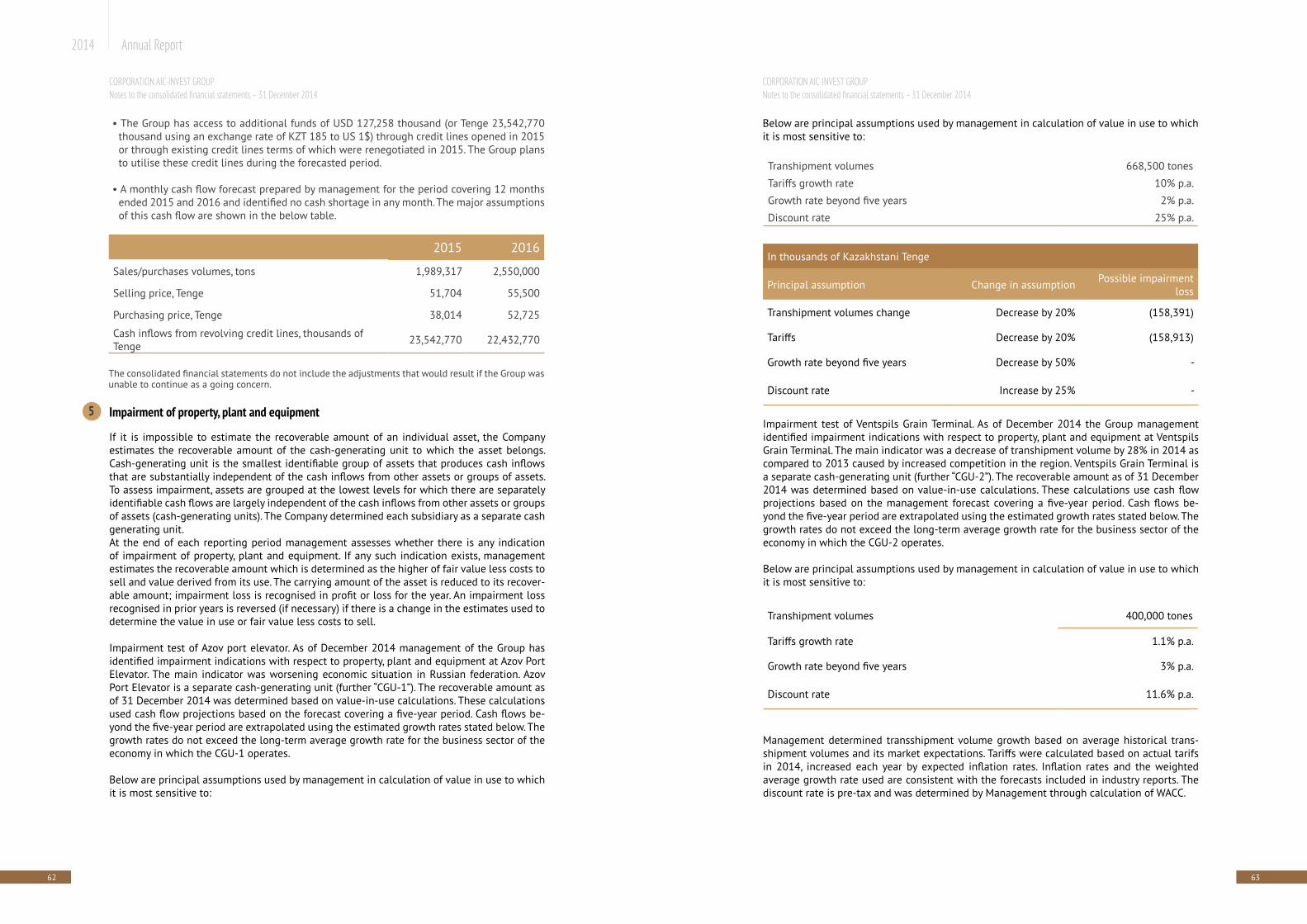

Company overview 4Areas of business 4Mission 5Operational highlights 6Brief history 8Corporate structure 9Business model 10Geography of operations 12

ADDRESS BY THE MANAGEMENT 13

DEVELOPMENT STRATEGY 16

PERFORMANCE OVERVIEW 17

Key market trends 17International grain market 19Production of grains in Kazakhstan 22Results 26Financial highlights 27Financial condition analysis 29Credit ratings 32

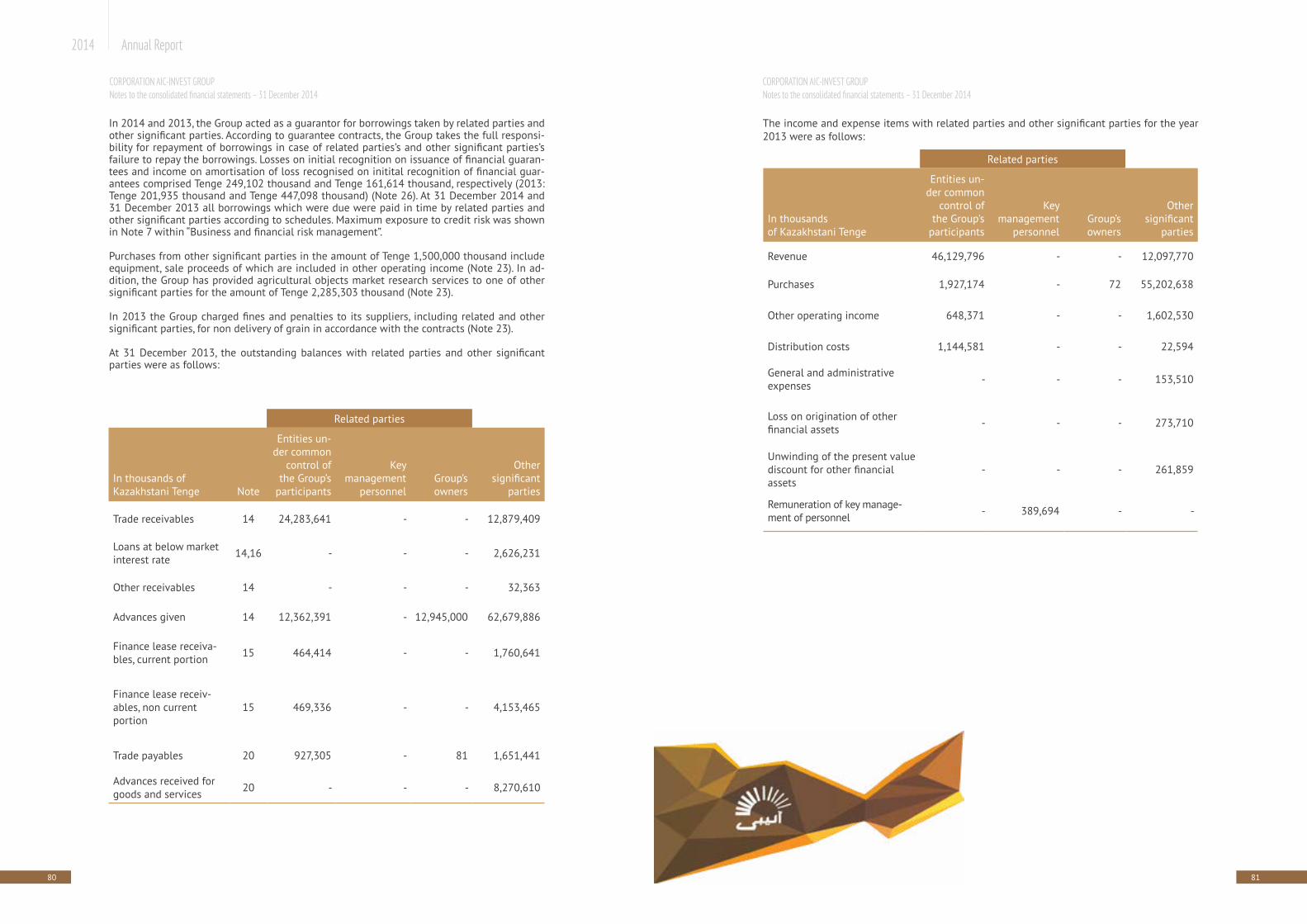

RISK MANAGEMENT 35

CORPORATE GOVERNANCE 37

Ownership structure 38Organizational structure 38Corporate governance principles 40Internal control and audit 41Liability section 42

ANNEX. Financial statements 43

GLOSSARY 111

CONTACT INFORMATION 113

Table of Contents

4 5

2014 Annual Report

Company overview

APK-Invest Corporation LLP (hereinafter – APK-Invest) is one of the leaders of Kazakhstan’s grain market. The company focuses on both grain imports and exports. APK-Invest accounts for about 25 percent of all Kazakhstan’s grain exports. The company has been on the market for more than 15 years. In 2014, APK-Invest was ranked 26th among Kazakhstan’s largest com-panies by RAEX rating agency (Expert RA Kazakhstan) and as the largest agricultural company.The Corporation has all the necessary resources for successful sustainable development, in-cluding professional employees, reliable suppliers and advanced transport infrastructure.

Areas of business

The Corporation focuses on buying and selling agricultural products domestically, as well as supplying products to other markets through both existing distribution channels and new routes that are being developed for the future.

80%

12%

7% 1%

■ Wheat sales■ Equipment sales■ Sales of plant pest control agents■ Barley sales

Revenue structure of APK-Invest Corporation in 2014

The Corporation’s main area of business is selling wheat as well as barley. In 2014, wheat sales made up more than 80 percent of the total sales revenue.Most grain is exported. We handle more than 1.5 million tons per year with a capacity of 2 million tons. APK-Invest operates in all major grain-producing regions of Kazakhstan, thus minimizing weather risks. In addition to grain sales, the Corporation sells agricultural equipment and leases it to farm-ers, as well as supplies them with fertilizers and crop protection products, earning some extra revenue and building stronger relationships with farmers.

Mission

APK-Invest strives to develop the domestic grain market and make local agricultural business-es more export-oriented by promoting local production of grains, as well as improving grain export channels from Kazakhstan to the world market.

ABOUT APK-INVEST CORPORATION

6 7

2014 Annual Report

Income, million Tenge Net income, million Tenge

EBITDA, million Tenge

Assets, million Tenge Grain sold, thousand tons

ROE, %

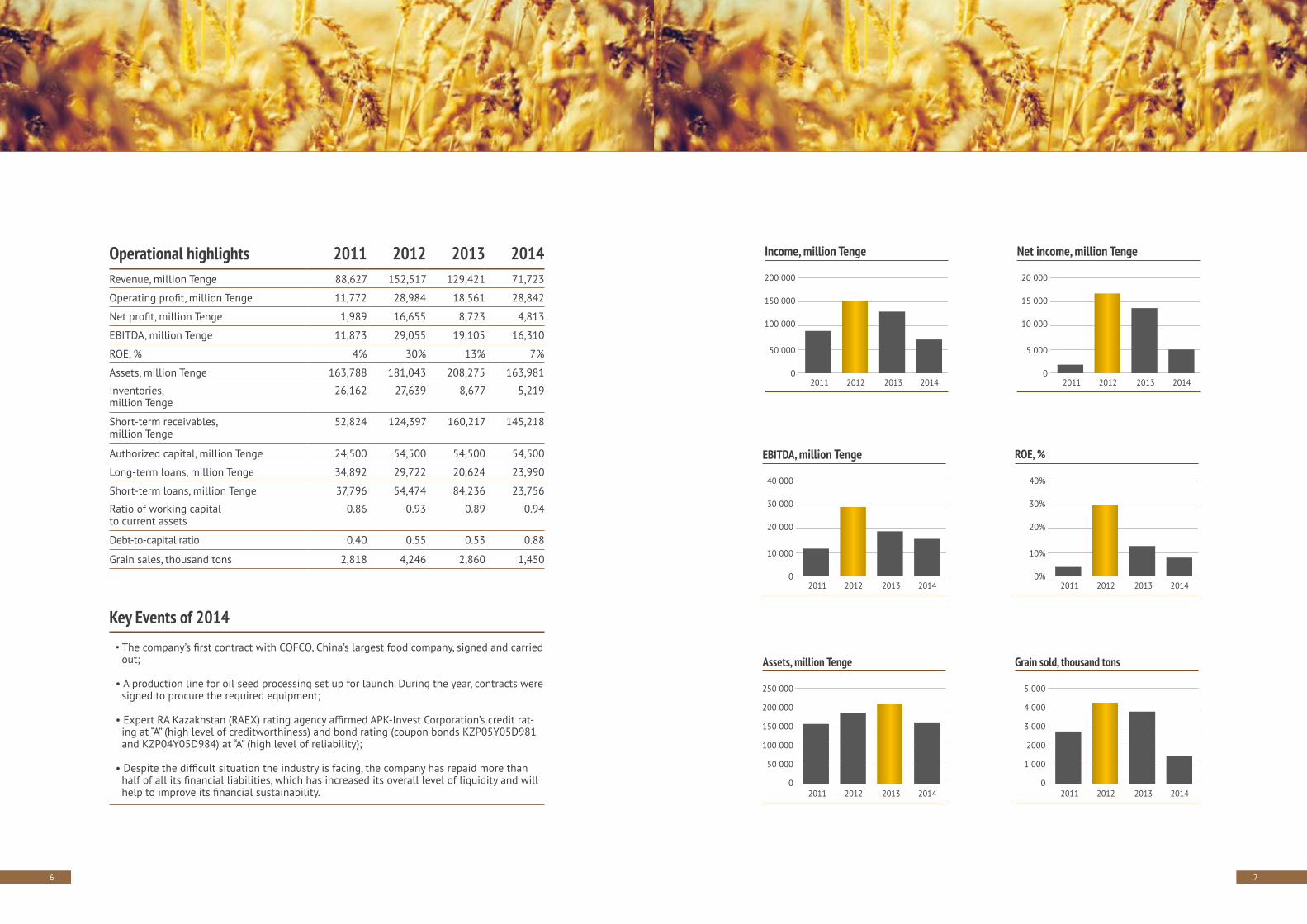

Operational highlights 2011 2012 2013 2014Revenue, million Tenge 88,627 152,517 129,421 71,723

Operating profit, million Tenge 11,772 28,984 18,561 28,842

Net profit, million Tenge 1,989 16,655 8,723 4,813

EBITDA, million Tenge 11,873 29,055 19,105 16,310

ROE, % 4% 30% 13% 7%

Assets, million Tenge 163,788 181,043 208,275 163,981

Inventories, million Tenge

26,162 27,639 8,677 5,219

Short-term receivables, million Tenge

52,824 124,397 160,217 145,218

Authorized capital, million Tenge 24,500 54,500 54,500 54,500

Long-term loans, million Tenge 34,892 29,722 20,624 23,990

Short-term loans, million Tenge 37,796 54,474 84,236 23,756

Ratio of working capital to current assets

0.86 0.93 0.89 0.94

Debt-to-capital ratio 0.40 0.55 0.53 0.88

Grain sales, thousand tons 2,818 4,246 2,860 1,450

Key Events of 2014• The company’s first contract with COFCO, China’s largest food company, signed and carried

out;

• A production line for oil seed processing set up for launch. During the year, contracts were signed to procure the required equipment;

• Expert RA Kazakhstan (RAEX) rating agency affirmed APK-Invest Corporation’s credit rat-ing at “A” (high level of creditworthiness) and bond rating (coupon bonds KZP05Y05D981 and KZP04Y05D984) at “A” (high level of reliability);

• Despite the difficult situation the industry is facing, the company has repaid more than half of all its financial liabilities, which has increased its overall level of liquidity and will help to improve its financial sustainability.

200 000

150 000

100 000

50 000

0

20 000

15 000

10 000

5 000

0

40 000

30 000

20 000

10 000

0

250 000

200 000

150 000

100 000

50 000

0

5 000

4 000

3 000

2000

1 000

0

40%

30%

20%

10%

0%

2011 2012 2013 2014 2011 2012 2013 2014

2011 2012 2013 2014

2011 2012 2013 2014 2011 2012 2013 2014

2011 2012 2013 2014

8 9

2014 Annual Report

Brief history 1998 – Agrofirma Alibi LLP was established, laying the foundation for Corporation. The found-ers included Mr. Tleubayev’s Alibi OJSC, an active grain business at the time.

2001 – From the very beginning Agrofirma Alibi focused on both domestic and international trade, shipping its first one million tons of grain to other markets by the end of the year.

2002 – Agrofirma Alibi is joined by other large players on the market, such as Alibi-Senim LLP, NurAl LLP and Agrofirma Zher-Ana LLP.

2003 – Agrofirma-Alibi LLP changes its name and re-registers as APK-Invest Corporation LLP. First acquisitions of agricultural equipment from such manufacturers as Case Corporation, Deere and Company, Degelman, Balzer, etc. The Corporation becomes a shareholder of Grain Insurance Company JSC after buying a 25 percent stake in the agricultural insurance company.

2005 – APK-Invest Corporation raises first loans from European banks.

2007 – Corporation acquires a 100 percent stake in Azov Port Elevator LLC.

2008 – Building partnership with farmers with a total land area of one million hectares. The Corporation receives Gold Key Customer award from John Deere. This manufacturer’s sales exceed one hundred million US dollars.

2009 – Corporation starts building a grain terminal at Beyneu station in Mangistau Region (western Kazakhstan). Beyneu Port Elevator LLP has a planned storage capacity of 100,000 tons with annual transhipments of at least one million tons. With its production capacity, the mill can produce up to 400 tons of flour daily.

2010 – Corporation receives Structured Finance Deal of the Year award from Islamic Finance News for attracting 40 million dollars of investments through Murabaha, an Islamic financing structure. One hundred percent of Beyneu Grain Terminal LLP was sold to Grain Leasing Com-pany LLP.

2011 – Corporation becomes the owner of Ventspils grain terminal, one of the most advanced grain terminals in the Baltic States.

2012 – Corporation sells record four million tons of wheat, including 1.5 million tons exported.

2013 – Corporation ships 3,000 tons to China, making this its first shipment to this country.

2014 – Preparation for launching a processing line for oilseed crops. During this year, the company signed contracts for supplying processing equipment for oilseed crops.

2015 – Opening of a new subsidiary MEZ-SKO LLP.

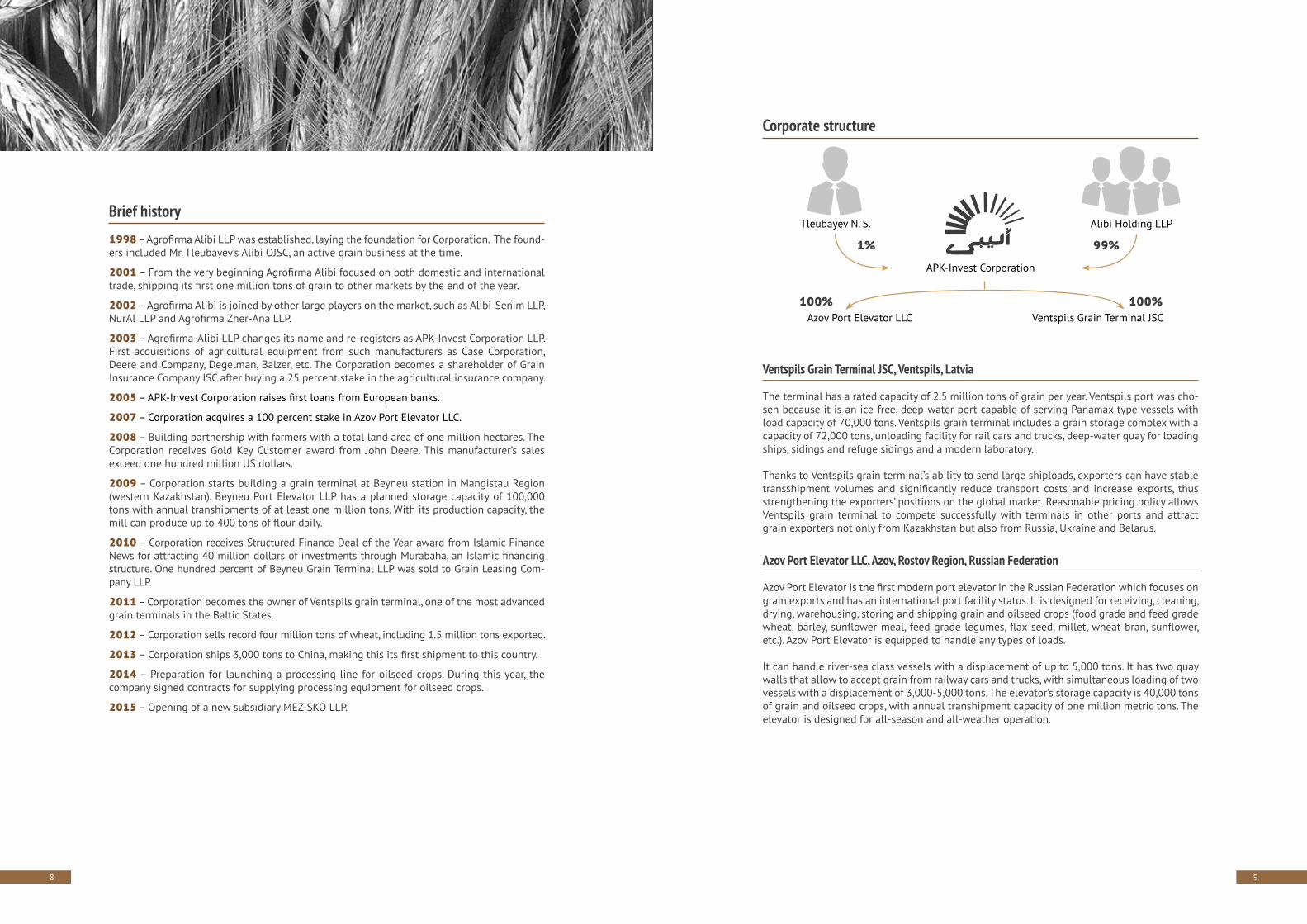

Corporate structure

Ventspils Grain Terminal JSC, Ventspils, Latvia

The terminal has a rated capacity of 2.5 million tons of grain per year. Ventspils port was cho-sen because it is an ice-free, deep-water port capable of serving Panamax type vessels with load capacity of 70,000 tons. Ventspils grain terminal includes a grain storage complex with a capacity of 72,000 tons, unloading facility for rail cars and trucks, deep-water quay for loading ships, sidings and refuge sidings and a modern laboratory.

Thanks to Ventspils grain terminal’s ability to send large shiploads, exporters can have stable transshipment volumes and significantly reduce transport costs and increase exports, thus strengthening the exporters’ positions on the global market. Reasonable pricing policy allows Ventspils grain terminal to compete successfully with terminals in other ports and attract grain exporters not only from Kazakhstan but also from Russia, Ukraine and Belarus.

Azov Port Elevator LLC, Azov, Rostov Region, Russian Federation

Azov Port Elevator is the first modern port elevator in the Russian Federation which focuses on grain exports and has an international port facility status. It is designed for receiving, cleaning, drying, warehousing, storing and shipping grain and oilseed crops (food grade and feed grade wheat, barley, sunflower meal, feed grade legumes, flax seed, millet, wheat bran, sunflower, etc.). Azov Port Elevator is equipped to handle any types of loads.

It can handle river-sea class vessels with a displacement of up to 5,000 tons. It has two quay walls that allow to accept grain from railway cars and trucks, with simultaneous loading of two vessels with a displacement of 3,000-5,000 tons. The elevator’s storage capacity is 40,000 tons of grain and oilseed crops, with annual transhipment capacity of one million metric tons. The elevator is designed for all-season and all-weather operation.

APK-Invest Corporation

Alibi Holding LLPTleubayev N. S.

Azov Port Elevator LLC Ventspils Grain Terminal JSC

1%

100% 100%

99%

10 11

2014 Annual Report

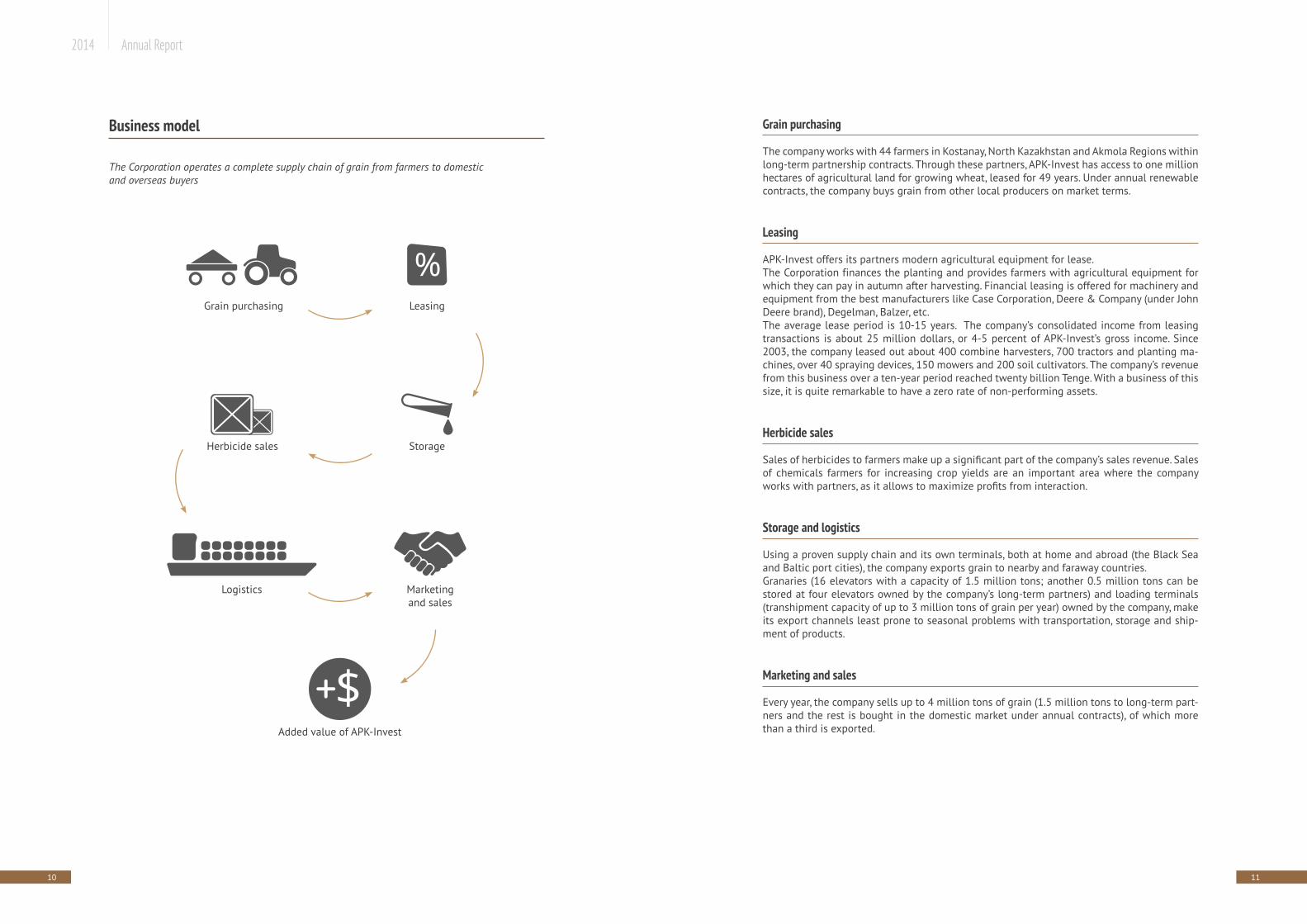

Grain purchasing

The company works with 44 farmers in Kostanay, North Kazakhstan and Akmola Regions within long-term partnership contracts. Through these partners, APK-Invest has access to one million hectares of agricultural land for growing wheat, leased for 49 years. Under annual renewable contracts, the company buys grain from other local producers on market terms.

Leasing

APK-Invest offers its partners modern agricultural equipment for lease.The Corporation finances the planting and provides farmers with agricultural equipment for which they can pay in autumn after harvesting. Financial leasing is offered for machinery and equipment from the best manufacturers like Case Corporation, Deere & Company (under John Deere brand), Degelman, Balzer, etc. The average lease period is 10-15 years. The company’s consolidated income from leasing transactions is about 25 million dollars, or 4-5 percent of APK-Invest’s gross income. Since 2003, the company leased out about 400 combine harvesters, 700 tractors and planting ma-chines, over 40 spraying devices, 150 mowers and 200 soil cultivators. The company’s revenue from this business over a ten-year period reached twenty billion Tenge. With a business of this size, it is quite remarkable to have a zero rate of non-performing assets.

Herbicide sales

Sales of herbicides to farmers make up a significant part of the company’s sales revenue. Sales of chemicals farmers for increasing crop yields are an important area where the company works with partners, as it allows to maximize profits from interaction.

Storage and logistics

Using a proven supply chain and its own terminals, both at home and abroad (the Black Sea and Baltic port cities), the company exports grain to nearby and faraway countries. Granaries (16 elevators with a capacity of 1.5 million tons; another 0.5 million tons can be stored at four elevators owned by the company’s long-term partners) and loading terminals (transhipment capacity of up to 3 million tons of grain per year) owned by the company, make its export channels least prone to seasonal problems with transportation, storage and ship-ment of products.

Marketing and sales

Every year, the company sells up to 4 million tons of grain (1.5 million tons to long-term part-ners and the rest is bought in the domestic market under annual contracts), of which more than a third is exported.

Business model

The Corporation operates a complete supply chain of grain from farmers to domestic and overseas buyers

Grain purchasing

StorageHerbicide sales

Logistics Marketing and sales

Added value of APK-Invest

Leasing

12 13

2014 Annual Report

Geography of operationsThe Group owns the Azov Port Elevator at the Azov sea coast and the Ventspils Grain Terminal on the Baltic Sea.

The Azov facility gives Kazakhstan’s grain access to the Back Sea and Mediterranean markets. Ventspils terminal allows exporting to Egypt and other countries around the globe.On average, during the past 5 years APK-Invest has been responsible for about 20-25 percent of grain exports from Kazakhstan, i.e. one out of every four tons. A larger part of the company’s exports goes to Azerbaijan, Georgia, Tajikistan, Turkmenistan, Uzbekistan, Kyrgyzstan, Russian Siberia and Belarus, as well as to Turkey, U.A.E., Switzerland and Egypt.

The Corporation plans to increase shipments to China, which is becoming an important export destination. In 2010-2011 marketing year, APK-Invest shipped 10,600 tons to China, and as much as 213,960 tons in 2013/2014 marketing year. The company is also working to increase exports to other major wheat-importing countries.

ADDRESS BY THE MANAGEMENT

Lines: grain sales, all in one color

14 15

2014 Annual Report

ADDRESS BY THE MANAGEMENT

Dear friends and colleagues,

2014 was a tough year for our company and the industry as a whole. However, we have man-aged to achieve positive results and we have been quite successful in our endeavors.

Looking at the current situation in agriculture, it should be noted that Agrobusiness 2020, the government program for promoting agriculture in the Republic of Kazakhstan during 2013-2020, arrived at a very opportune moment, which undoubtedly will help the industry to grow and change dramatically.

The main challenges during the reporting year were crop failures and, of course, the systemic financial crisis. We managed to mitigate the impact of crop failure to some extent thanks to effective trading decisions and emerging opportunities. Because crop failure forced us to scale back our operations, the financial crisis has not been a big problem for us; on the contrary, it allowed the company to establish itself as a stable and reliable trader and helped us find new strategic partners.

As expected, prolonged grain crop failure affected earnings in the reporting year, yet, thanks to adequate measures and strategic planning, we managed to show a profit at the end of the period. It is important to note that, despite the difficult situation in the industry, we managed to repay more than half of all our debt, thus increasing the overall level of liquidity and im-proving financial sustainability. APK-Invest has vividly demonstrated its high credit worthiness and ability to honor its financial obligations without help, even in such harsh economic envi-ronment.

One of the successes of this year was signing a contract with COFCO Group, China’s largest food Corporation. COFCO is a diversified state-owned monopoly on the Chinese food market, buyer and trader of corn, rice and wheat; it also conducts enhanced grain processing.

The key event of 2015 was the opening of our subsidiary, MEZ-SKO LLP. The subsidiary will manufacture refined oils and fats, which in our opinion is a promising business.

As for production plans, in 2015 we intend to work in the same mode as in 2014, because the financial crisis is still a bitter reality. We plan to expand our sales geography, especially to China, as this country stands to become an important export customer. In financial terms, we intend to maintain the current level of debt and will carefully monitor the company’s effective-ness, maintaining its financial stability.

I am sure that this year, we will be able to achieve new successes and overcome the existing industry challenges. By focusing on strategic areas in the medium term, we will ensure suc-cessful development of the company and remain as one of the industry leaders.

Asylbek Tleubayev General Director

16 17

2014 Annual Report

Our main goal is to become one of the leading exporters of agricultural products in Central Asia. We are focused on regions with low productivity of agriculture and with potential to in-crease the number of transactions.

Key strategic medium-term goals:

• Modernization of logistics network The company expects the increase of export potential in all areas, which is facilitated by

practical implementation of key objectives of the State Transport Infrastructure Develop-ment Program. Therefore, the company intends to continue to expand and upgrade its logis-tics infrastructure.

• Increasing business liquidity The company intends to improve its financial performance through debt burden reduction

and cost optimization.

• Remaining Kazakhstan’s leading grain exporter We focus on traditional export destinations, like Azerbaijan, Georgia, Tajikistan, Kyrgyzstan,

the Middle East and we will use opportunities offered by new markets. Our goal is to keep export and domestic sales at the level of 4 million tons, achieved in 2012.

DEVELOPMENT STRATEGY PERFORMANCE OVERVIEW

Key market trends

Between 2010/11 and 2014/15 marketing years, the average world grain production totaled 1.9 billion tons. Seven largest producers account for 73 percent of grain production in the 2014/2015 season, including the United States, China, the EU-28 (EU countries), India, Russia, Canada and Ukraine.

Wheat makes up 36 percent of world grain production and 50 percent of grain exports.

Kazakhstan is one of the key producers of high-quality wheat and it is the world’s seventh largest exporter by volume, shipping 8.8 million tons of wheat for exports in 2013/2014.

The main drivers for growth of grain exports:- Population growth: the world’s population is expected to reach 9.1 billion people by 2050;- Changes in the global consumption structure: rising purchasing power of the developing countries;- Less agricultural land: driven by population growth, urbanization and desertification.

18 19

2014 Annual Report

International grain market

According to the International Grains Council (IGC), the global supply of grains, rice and oilseeds during 2013/2014 has surged, with the production of wheat, corn, soy beans and rice reaching new record highs. As experts note, there has been a faster than usual growth in consumption; however, carry-over stocks have also improved. According to the IGC report, the global trade in grains, pri-marily wheat and corn, has reached its historical maximum. However, sellers were affected by the decline in export prices. During the 2013/2014 fiscal year, on the average, Grains and Oilseeds In-dex (GOI) was 13 percent lower than in the previous period. The increased demand was not enough to provide sufficient support to declining prices.

Total worldwide production of grains (wheat and coarse grains) in 2013/2014 increased by 11 per-cent, reaching 1,994 million tons. The growth was driven by increased wheat, corn and barley crops. Large crops were harvested almost everywhere, as a result, production in the eight major exporting countries increased by approximately 20 percent, for the first time exceeding one billion tons.

World wheat production in 2013/2014 increased by 9 percent and reached its historic maximum of 713 million tons. Record crops of wheat were harvested in Canada, China, Egypt and Morocco, with production in the CIS recovering after the previous season’s drought. Increased crop harvesting also took place in Argentina, Australia and the EU. India’s crop was a bit smaller than a year earlier, but still it was the second largest in the country’s history.

The world’s total land area for growing barley slightly declined compared to the last year; however, the record average yield resulted in boosting production to a four-year high of 145 million tons (12 percent more than in the previous year). High barley yields occurred in the EU, Russia, Ukraine, Canada, Turkey, Morocco and Australia. However, in Australia, reduction of cultivated lands and bad weather conditions caused a decline in production.

After the first decline in 14 years, which happened in the previous season, the total world consump-tion of grain in 2013/2014 grew by 6 percent to 1,926 million tons, which is a new high, according to the IGC. Significant growth in grain production caused a drop in prices, resulting in an 8 percent rise of the global feed use to 839 million tons. Yet, the growing use of coarse grains has limited the interest in wheat fodder. According to the International Grains Council, cheaper prices for raw materials caused a 6 percent increase in demand in the industrial sector, reaching 314 million tons. Global food grains consumption totaled 649 million tons, which is 2 percent more than the year before.

The world consumption of wheat in 2013/2014 increased by 3 percent reaching 695 million tons. Total barley consumption rose by 8 million tons reaching 141 million tons, including an increase of 7 million tons in feed barley consumption totaling 94 million tons. Industrial use of barley in-creased by 2 percent reaching 30 million tons. IGC experts say that the growth is mostly driven by stronger demand from the beer industry in certain countries, particularly in China and Brazil.

According to the International Grains Council, the world carry-over grain stocks at the end of 2013/2014 (total volume for the relevant local marketing years) increased for the first time in four seasons by 68 million tons, reaching 403 million tons. After record harvests, most of the growth occurred in wheat and corn production with an increase of 18 million tons and 44 million tons respectively. The ratio of world reserves and grain use increased by two percentage points to a four-year high of 21 percent.

The world grain trade in 2013/2014 (July/June) increased by 38 million tons compared with last

World’s largest grain exporters

World’s largest arable lands for wheat growing, million ha

IndiaKazakhstanArgentina

RussiaAustralia

Canada Ukraine

EU-27USA

Argentina

Ukraine

Canada

Kazakhstan

Australia

USA

Russia

China

EU-28

India

2013/2014, % of world exports

3%

3,7

3%

4,2

7%

6,6

8%

6,3

9%

10,4

10%

9,5

11%

13

14%

11,9

28%

13,513,8

18,8

23,623,7

24,124,1

25,726,7

29,7

■ 13/14 ■ 14/15

31,5

18,3

0% 5% 10% 15% 20% 25% 30%

World’s largest wheat exporters

IndiaKazakhstanArgentina

RussiaAustralia

Canada Ukraine

EU-27USA

2013/2014, % of world exports

1%

4%

5%6%

9%

9%14%19%19%

0% 5% 10% 15% 20%

20 21

2014 Annual Report

year to a record of 307 million tons. Wheat trade increased by 14 million tons to 155 million tons. There was an increase in demand for milling wheat in China, the United States, Egypt and Saudi Arabia. China’s imports doubled due to poor grain quality of local crops, reaching a nine-year high of nearly 7 million tons. The EU showed a particularly strong export appetite, with shipments reaching a record high of 31 million tons. And this is despite strong competition from the CIS, with soaring sales from Kazakhstan, Russia and Ukraine. According to the IGC, supply chain problems impeded shipments in North America, yet, exports from the United States and Canada still exceed-ed last year’s figures.

World barley trade in 2013/2014 increased by 18 percent to 22.9 million tons. Saudi imports reached 9 million tons, which is 10 percent more than last year. Growth in demand was due to competitive prices. China’s imports (especially barley for malting) increased by 95 percent to 4.1 million tons, which is also due to poor local crops and substandard grain quality. Australia’s exports in July/June surged by 45 percent to 6.4 million tons thanks to a large crop, while shipments from the EU increased by 14 percent to 5.7 million tons, which is a record high since 2000/2001.

As expected, record grain yields and growing supply caused a decline in export prices for grains and oilseeds during 12 months leading to June 2014, with the biggest drop being in corn prices. In early August, the IGC’s GOI dropped to its absolute low in 20 months, mostly because of the decline in the cultivated crops sector. Although prices recovered slightly, especially in February and early March, they were increasingly affected by an unfavorable supply and demand forecast. At the end of June 2014, GOI was 9 percent lower than a year earlier, due to a 27 percent decline in corn. Sub-in-dexes for both soybeans and rice dropped 7 percent compared to the last year, as the subindex for wheat fell by 2 percent.

Initially, export prices for wheat dropped due to abundant global supply and in view of the adverse impact from the reduction in corn prices, the trend towards weakening persisted on the markets until the end of January. Early in 2014, prices partly recovered due to uncertainty created by the conflict in Ukraine, excessively dry weather for the next crop in the United States and Canada’s supply chain problems. However, given the increasingly optimistic crop prospects for 2014/2015 in other regions, prices dropped again in May and June.

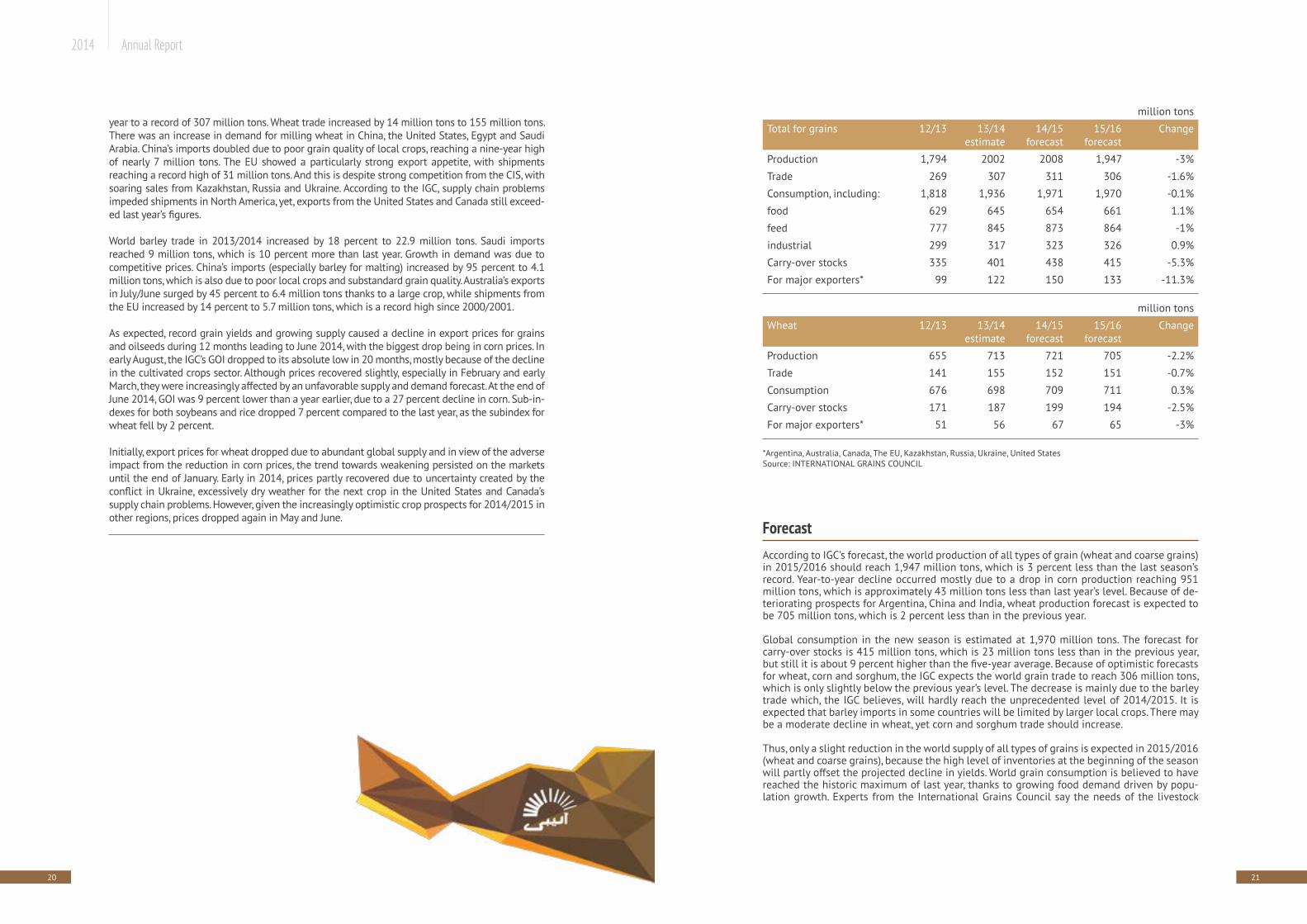

million tons

Total for grains 12/13 13/14 estimate

14/15 forecast

15/16 forecast

Change

Production 1,794 2002 2008 1,947 -3%

Trade 269 307 311 306 -1.6%

Consumption, including: 1,818 1,936 1,971 1,970 -0.1%

food 629 645 654 661 1.1%

feed 777 845 873 864 -1%

industrial 299 317 323 326 0.9%

Carry-over stocks 335 401 438 415 -5.3%

For major exporters* 99 122 150 133 -11.3%

million tons

Wheat 12/13 13/14 estimate

14/15 forecast

15/16 forecast

Change

Production 655 713 721 705 -2.2%

Trade 141 155 152 151 -0.7%

Consumption 676 698 709 711 0.3%

Carry-over stocks 171 187 199 194 -2.5%

For major exporters* 51 56 67 65 -3%

*Argentina, Australia, Canada, The EU, Kazakhstan, Russia, Ukraine, United StatesSource: INTERNATIONAL GRAINS COUNCIL

ForecastAccording to IGC’s forecast, the world production of all types of grain (wheat and coarse grains) in 2015/2016 should reach 1,947 million tons, which is 3 percent less than the last season’s record. Year-to-year decline occurred mostly due to a drop in corn production reaching 951 million tons, which is approximately 43 million tons less than last year’s level. Because of de-teriorating prospects for Argentina, China and India, wheat production forecast is expected to be 705 million tons, which is 2 percent less than in the previous year.

Global consumption in the new season is estimated at 1,970 million tons. The forecast for carry-over stocks is 415 million tons, which is 23 million tons less than in the previous year, but still it is about 9 percent higher than the five-year average. Because of optimistic forecasts for wheat, corn and sorghum, the IGC expects the world grain trade to reach 306 million tons, which is only slightly below the previous year’s level. The decrease is mainly due to the barley trade which, the IGC believes, will hardly reach the unprecedented level of 2014/2015. It is expected that barley imports in some countries will be limited by larger local crops. There may be a moderate decline in wheat, yet corn and sorghum trade should increase.

Thus, only a slight reduction in the world supply of all types of grains is expected in 2015/2016 (wheat and coarse grains), because the high level of inventories at the beginning of the season will partly offset the projected decline in yields. World grain consumption is believed to have reached the historic maximum of last year, thanks to growing food demand driven by popu-lation growth. Experts from the International Grains Council say the needs of the livestock

22 23

2014 Annual Report

sector will remain strong; however, the use of coarse grains will still face competition from alternative feeds, especially oilseed meals with an abundant supply of them being available. Industrial use is expected to grow, mainly in starch production and beer brewing, while de-mand in the ethanol industry as a whole will remain at last year’s level.

Production of grains in Kazakhstan

КKazakhstan has about 21.5 million hectares of arable lands, of which approximately 60 per-cent is used for wheat growing. Kazakhstan is the second largest country in Europe and the CIS in terms of cultivated land area, with 11.9 million hectares of land used for wheat growing in 2014/2015 marketing year.

In 2012, the Ministry of Agriculture, regional authorities, KazAgro National Managing Holding and Kazagroinnovacia signed memorandums of cooperation to ensure crop diversification. As a result, in the ensuing five years the wheat crop area declined by 2.4 million hectares. Accord-ing to the Ministry of Agriculture, the measures taken have made it possible to balance supply and demand for wheat, eliminated the causes of dumping prices, helped to introduce crop ro-tation and expanded the crop areas of coarse grains, oilseeds, feed and cucurbits/melon crops.About 95 percent of the wheat produced in Kazakhstan is spring wheat grown in the steppe and forest-steppe areas. According to the International Grains Council, the average annual wheat production in Kazakhstan is 14 million tons. Kazakhstan’s climate is perfect for the pro-duction of high-quality wheat. Up to 90 percent of cultivated wheat with a minimum gluten content of 23 percent is suitable for making flour.

Kazakhstan’s wheat is known for its high quality and has traditionally been used for flour blending. This product is exported to 40 countries, with the main customers being in the CIS, and the largest partners in the EU, Turkey, Egypt, etc. Further growth in wheat and grain ex-ports from Kazakhstan will be driven by rising demand in Asia, where wheat consumption and imports are expected to increase in the medium term.

Kazakhstan has a record harvest of grains, 26.5 million tons, in 2011/2012, which was 2.2 times more than in the 2010/2011 season. As a result, exports reached 12.6 million tons. Ka-zakhstan became one of the world’s 10 largest wheat exporters, shipping 11.3 million tons, or 7 percent of world exports of wheat (IGC data). In the 2013/2014 season, about 17.8 million tons of wheat were harvested, of which 8.8 million tons were exported.

According to the Ministry of Agriculture, today, Kazakhstan’s total grain storage capacity is 25.1 million. tons. As of January 1 of this year, Kazakhstan had 13.2 million tons of grain. Granaries were filled at 52.6 percent of their capacity.

Production and export of Kazakh wheat, million tons

25

20

15

10

5

0

2007-2008

ExportProduction

2008-2009 2009-2010 2010-2011 2011-2012 2012-2013 2013-2014

Kazakh wheat export structure by destination, 2013/2014 marketing year, %

Russia Iran Uzbekistan Аzerbaijan

Tadzhikistan Kyrgyzstan China Turkey

Georgia Other

17%

22%

15%12%

12%

7%

5%

3%3%

5%

24 25

2014 Annual Report

Industry prospects

Kazakhstan’s 2013-2020 agriculture development program is aimed at improving sustainabil-ity of grain production and stabilizing the grain market in Kazakhstan, as well as improving productivity in agriculture.

The targets of this master plan include:

• Crop diversification with decreasing wheat crop areas to 11.5 million ha by 2020 and in-creasing feed grains, legumes and cereal grains crop areas to 4.3 million ha, oilseeds – to 2.1 million ha, cucurbits/melon crops and potatoes – to 430,000 ha, feed grains – to 4.3 million ha;

• Adoption of scientifically proven crop rotations throughout the acreage;• Introduction of water and resource-saving technologies on 12.8 million ha, including 4.8

million ha of no-tillage areas;

• Increasing grain yields to 13.2 hundred kg/ha by 2020, and grain production to 21.1 million tons;

• Increasing exports of grain and flour in grain equivalent to 9.1 million tons by 2020;• Increasing the share of insured acreage to 100 percent by 2020;

• Introduction of additional storage facilities with a capacity of 3.5 million tons by 2020, in-cluding 350,000 tons for major export destinations.

Share of APK-Invest in Kazakhstan’s grain exports, %35%

30%

25%

20%

15%

10%

5%

0%

2008 2009 2010 2011 2012 2013 2014

APK-Invest remains the leading exporter of Kazakh grains. The company also is a major player in the domestic market.

Originators of the master plan highlighted the following key problems impeding the growth of grain production and grain market in Kazakhstan:

• Wheat monoculture (in Kazakhstan, wheat takes up 66 percent of crop areas instead of the scientifically recommended 45-50 percent). According to the program, this results in overproduction of grain in bumper-crop years, which, given the shortage of silo capacities and hopper cars, requires significant budget spending to regulate the market (moving grain from silos in northern areas to silos in other areas, subsidizing transportation costs of grain exporters, buying grain surplus to prevent market disturbance), and it also causes price dumping;

• Insufficient grain storage capacity. Available capacities are sufficient to ensure grain stor-age in years with moderate yields, but are not enough in bumper-crop years. In addition, most grain processing businesses suffer from worn-down infrastructure that has to be restored. Storage facilities are mostly located in the main grain-producing regions, so the infrastructure is not diversified and not focused on export destinations;

• Slow pace of introduction of advanced sustainable agriculture technologies, in particular, no-tillage soils (in 2012, no-tillage technology was used on 2.5 million hectares, or 15.4 percent of crop lands);

• Inadequate seed breeding for grain crops (durum wheat, malted barley, legumes);

• Poorly equipped grain production industry. The average age of over 78 percent of combine harvesters and tractors is 13-14 years, with a rated service life of 8-10 years. 65.2 percent of combine harvesters, 90 percent of tractors and 94 percent of seeders are operating beyond their useful service life. On the whole, the wear and tear of the current fleet of agricultural machinery is up to 84 percent;

• Insufficient use of chemicals (the amount of mineral fertilizers used for grain crops only covers 12 percent of the needs, herbicide purchased through subsidies is not enough to ensure effective weed control in addition to the use of water and resource-saving tech-nologies, particularly no-tillage methods);

• Insufficient government support for the industry.

26 27

2014 Annual Report

ResultsAPK-Invest Corporation operates in the following areas of business:

• Wheat and barley trade;• Port services;• Other agricultural activities, which includes selling herbicides, agricultural equipment

and fuel;• Other areas, including selling diversified goods and services, plus interest income from

lease finance.

Sales in 2014 declined by 50 percent, or by 1.5 million tons. The main reason is decline in sales on the domestic market, where shipments decreased by almost 1 million tons.

Revenue by segment, million Tenge

2010 2011 2012 2013 2014 Change compared with 2014, %

Wheat and barley trade

86,620 83,146 14,2821 122,270 62,959 -49%

Port services 668 1,447 2,711 1,896 1,974 4%

Other agricultural activities

4,328 3,797 4,862 3,420 5,545 62%

Other segments 3,832 4,008 2,825 1,704 1,244 -27%

Total 95,448 92,398 153,219 129,421 71,723 -45%

Grain sold by APK-Invest 2008 2009 2010 2011 2012 2013 2014

Exports, million tons 0.56 0.77 1.79 0.59 1.81 1.1 0.64

Domestic market, million tons

0.58 0.72 1.77 2.28 2.2 1.8 0.81

The bulk of grain, 60 percent, is sold on the domestic market with 40 percent shipped for export. Azerbaijan is the largest export destination, accounting for 22 percent of the company’s revenues in 2014. Other major markets are Iran (8 percent) and Russia (5 percent). High geographic diver-sification and continuous development of new sales channels provide the company with good opportunities for effective growth in the medium term.

Financial highlights

Key indicators of the income statementmillion Tenge

Item 2010 2011 2012 2013 2014

Revenue 92,857 88,627 152,517 129,421 71,723

Cost of production 69,370 65,765 110,100 100,545 49,780

Gross profit 23,487 22,861 42,416 28,876 21,943

Other income 6,505 3,514 3,969 5,303 18,963

Other expenses 21,790 23,119 25,003 23,556 34,885

Pre-tax profits 8,202 3,257 21,383 10,623 6,021

Corporate income tax costs 914 1,268 4,728 1,900 1,209

Net profit 7,288 1,989 16,655 8,723 4,813

Exchange rate difference -56 -320 411 -200 -1,885

Aggregate income 7,232 1,669 17,066 8,523 2,928

Revenue structure by country, 2014

Kazakhstan Аzerbaijan

Latvia Turkey

Iran Russia

Other

Georgia Tadzhikistan

59%22%

8%

5%

2%1%

1% 0%2%

28 29

2014 Annual Report

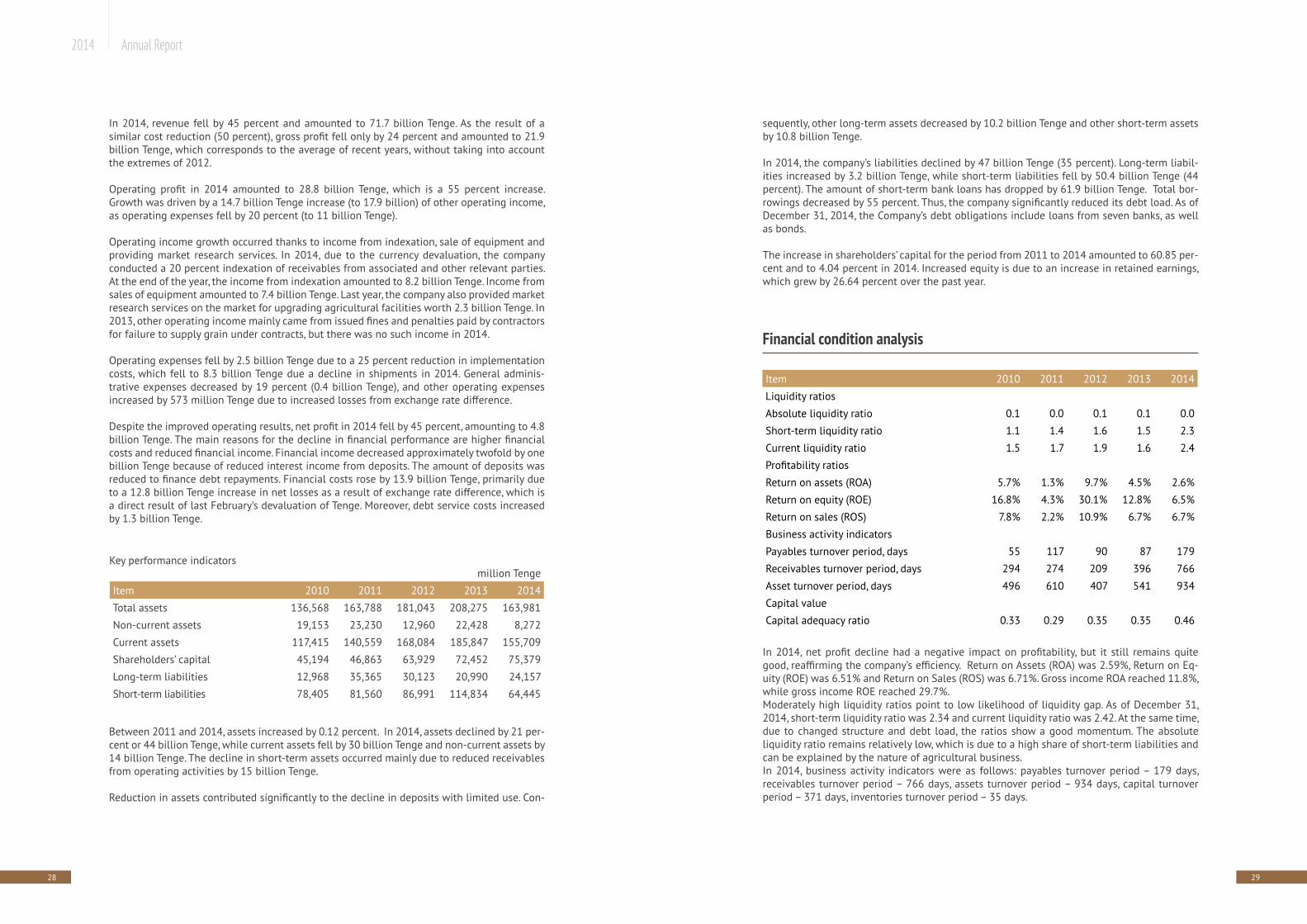

In 2014, revenue fell by 45 percent and amounted to 71.7 billion Tenge. As the result of a similar cost reduction (50 percent), gross profit fell only by 24 percent and amounted to 21.9 billion Tenge, which corresponds to the average of recent years, without taking into account the extremes of 2012.

Operating profit in 2014 amounted to 28.8 billion Tenge, which is a 55 percent increase. Growth was driven by a 14.7 billion Tenge increase (to 17.9 billion) of other operating income, as operating expenses fell by 20 percent (to 11 billion Tenge).

Operating income growth occurred thanks to income from indexation, sale of equipment and providing market research services. In 2014, due to the currency devaluation, the company conducted a 20 percent indexation of receivables from associated and other relevant parties. At the end of the year, the income from indexation amounted to 8.2 billion Tenge. Income from sales of equipment amounted to 7.4 billion Tenge. Last year, the company also provided market research services on the market for upgrading agricultural facilities worth 2.3 billion Tenge. In 2013, other operating income mainly came from issued fines and penalties paid by contractors for failure to supply grain under contracts, but there was no such income in 2014.

Operating expenses fell by 2.5 billion Tenge due to a 25 percent reduction in implementation costs, which fell to 8.3 billion Tenge due a decline in shipments in 2014. General adminis-trative expenses decreased by 19 percent (0.4 billion Tenge), and other operating expenses increased by 573 million Tenge due to increased losses from exchange rate difference.

Despite the improved operating results, net profit in 2014 fell by 45 percent, amounting to 4.8 billion Tenge. The main reasons for the decline in financial performance are higher financial costs and reduced financial income. Financial income decreased approximately twofold by one billion Tenge because of reduced interest income from deposits. The amount of deposits was reduced to finance debt repayments. Financial costs rose by 13.9 billion Tenge, primarily due to a 12.8 billion Tenge increase in net losses as a result of exchange rate difference, which is a direct result of last February’s devaluation of Tenge. Moreover, debt service costs increased by 1.3 billion Tenge.

Between 2011 and 2014, assets increased by 0.12 percent. In 2014, assets declined by 21 per-cent or 44 billion Tenge, while current assets fell by 30 billion Tenge and non-current assets by 14 billion Tenge. The decline in short-term assets occurred mainly due to reduced receivables from operating activities by 15 billion Tenge.

Reduction in assets contributed significantly to the decline in deposits with limited use. Con-

Key performance indicators million Tenge

Item 2010 2011 2012 2013 2014

Total assets 136,568 163,788 181,043 208,275 163,981

Non-current assets 19,153 23,230 12,960 22,428 8,272

Current assets 117,415 140,559 168,084 185,847 155,709

Shareholders’ capital 45,194 46,863 63,929 72,452 75,379

Long-term liabilities 12,968 35,365 30,123 20,990 24,157

Short-term liabilities 78,405 81,560 86,991 114,834 64,445

sequently, other long-term assets decreased by 10.2 billion Tenge and other short-term assets by 10.8 billion Tenge.

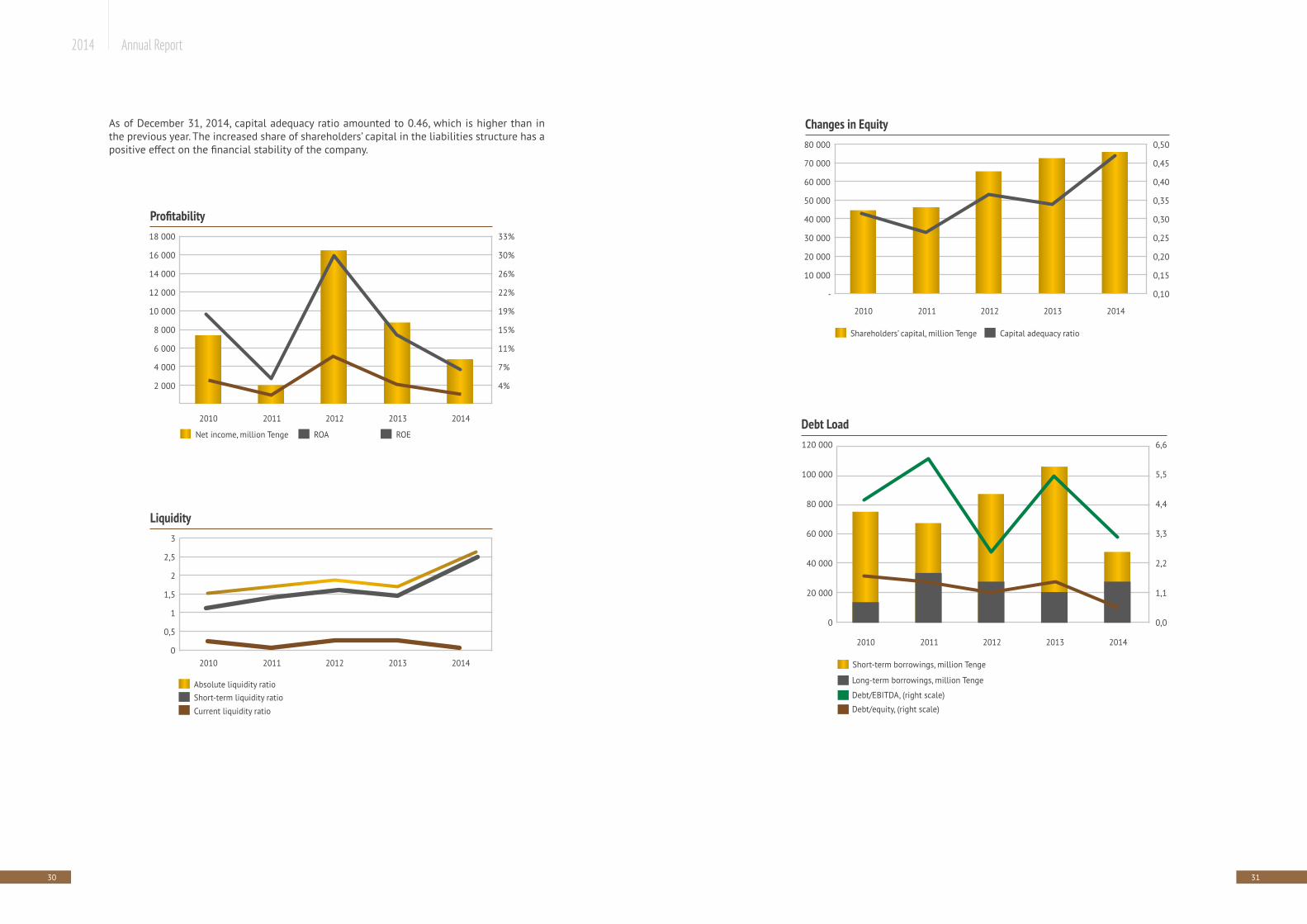

In 2014, the company’s liabilities declined by 47 billion Tenge (35 percent). Long-term liabil-ities increased by 3.2 billion Tenge, while short-term liabilities fell by 50.4 billion Tenge (44 percent). The amount of short-term bank loans has dropped by 61.9 billion Tenge. Total bor-rowings decreased by 55 percent. Thus, the company significantly reduced its debt load. As of December 31, 2014, the Company’s debt obligations include loans from seven banks, as well as bonds.

The increase in shareholders’ capital for the period from 2011 to 2014 amounted to 60.85 per-cent and to 4.04 percent in 2014. Increased equity is due to an increase in retained earnings, which grew by 26.64 percent over the past year.

Financial condition analysis

In 2014, net profit decline had a negative impact on profitability, but it still remains quite good, reaffirming the company’s efficiency. Return on Assets (ROA) was 2.59%, Return on Eq-uity (ROE) was 6.51% and Return on Sales (ROS) was 6.71%. Gross income ROA reached 11.8%, while gross income ROE reached 29.7%. Moderately high liquidity ratios point to low likelihood of liquidity gap. As of December 31, 2014, short-term liquidity ratio was 2.34 and current liquidity ratio was 2.42. At the same time, due to changed structure and debt load, the ratios show a good momentum. The absolute liquidity ratio remains relatively low, which is due to a high share of short-term liabilities and can be explained by the nature of agricultural business. In 2014, business activity indicators were as follows: payables turnover period – 179 days, receivables turnover period – 766 days, assets turnover period – 934 days, capital turnover period – 371 days, inventories turnover period – 35 days.

Item 2010 2011 2012 2013 2014

Liquidity ratios

Absolute liquidity ratio 0.1 0.0 0.1 0.1 0.0

Short-term liquidity ratio 1.1 1.4 1.6 1.5 2.3

Current liquidity ratio 1.5 1.7 1.9 1.6 2.4

Profitability ratios

Return on assets (ROA) 5.7% 1.3% 9.7% 4.5% 2.6%

Return on equity (ROE) 16.8% 4.3% 30.1% 12.8% 6.5%

Return on sales (ROS) 7.8% 2.2% 10.9% 6.7% 6.7%

Business activity indicators

Payables turnover period, days 55 117 90 87 179

Receivables turnover period, days 294 274 209 396 766

Asset turnover period, days 496 610 407 541 934

Capital value

Capital adequacy ratio 0.33 0.29 0.35 0.35 0.46

30 31

2014 Annual Report

As of December 31, 2014, capital adequacy ratio amounted to 0.46, which is higher than in the previous year. The increased share of shareholders’ capital in the liabilities structure has a positive effect on the financial stability of the company.

Profitability

Liquidity

18 000

16 000

14 000

12 000

10 000

8 000

6 000

4 000

2 000

3

2,5

2

1,5

1

0,5

0

33%

30%

26%

22%

19%

15%

11%

7%

4%

2010

2010

Net income, million Tenge

Absolute liquidity ratioShort-term liquidity ratioCurrent liquidity ratio

ROA ROE

2011

2011

2012

2012

2013

2013

2014

2014

Changes in Equity80 000

70 000

60 000

50 000

40 000

30 000

20 000

10 000

-

0,50

0,45

0,40

0,35

0,30

0,25

0,20

0,15

0,10

2010

Shareholders’ capital, million Tenge Capital adequacy ratio

2011 2012 2013 2014

Debt Load120 000

100 000

80 000

60 000

40 000

20 000

0

6,6

5,5

4,4

3,3

2,2

1,1

0,0

2010

Short-term borrowings, million Tenge

Long-term borrowings, million Tenge

Debt/EBITDA, (right scale)

Debt/equity, (right scale)

2011 2012 2013 2014

32 33

2014 Annual Report

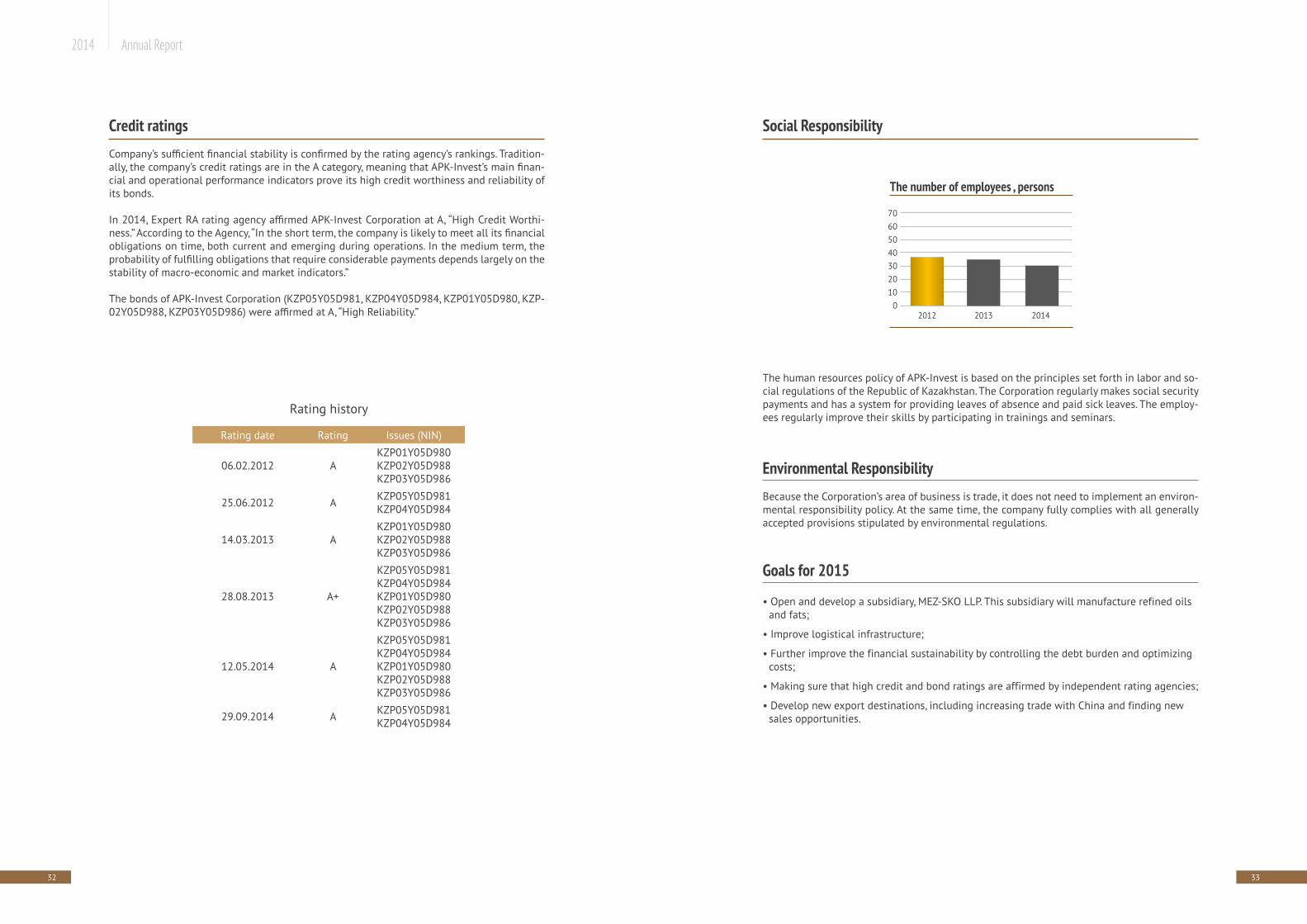

Credit ratingsCompany’s sufficient financial stability is confirmed by the rating agency’s rankings. Tradition-ally, the company’s credit ratings are in the A category, meaning that APK-Invest’s main finan-cial and operational performance indicators prove its high credit worthiness and reliability of its bonds.

In 2014, Expert RA rating agency affirmed APK-Invest Corporation at A, “High Credit Worthi-ness.” According to the Agency, “In the short term, the company is likely to meet all its financial obligations on time, both current and emerging during operations. In the medium term, the probability of fulfilling obligations that require considerable payments depends largely on the stability of macro-economic and market indicators.”

The bonds of APK-Invest Corporation (KZP05Y05D981, KZP04Y05D984, KZP01Y05D980, KZP-02Y05D988, KZP03Y05D986) were affirmed at A, “High Reliability.”

Social Responsibility

The human resources policy of APK-Invest is based on the principles set forth in labor and so-cial regulations of the Republic of Kazakhstan. The Corporation regularly makes social security payments and has a system for providing leaves of absence and paid sick leaves. The employ-ees regularly improve their skills by participating in trainings and seminars.

Environmental Responsibility Because the Corporation’s area of business is trade, it does not need to implement an environ-mental responsibility policy. At the same time, the company fully complies with all generally accepted provisions stipulated by environmental regulations.

Goals for 2015

• Open and develop a subsidiary, MEZ-SKO LLP. This subsidiary will manufacture refined oils and fats;

• Improve logistical infrastructure;

• Further improve the financial sustainability by controlling the debt burden and optimizing costs;

• Making sure that high credit and bond ratings are affirmed by independent rating agencies;

• Develop new export destinations, including increasing trade with China and finding new sales opportunities.

2012

Rating history

Rating date Rating Issues (NIN)

06.02.2012 АKZP01Y05D980KZP02Y05D988KZP03Y05D986

25.06.2012 А KZP05Y05D981KZP04Y05D984

14.03.2013 АKZP01Y05D980KZP02Y05D988KZP03Y05D986

28.08.2013 А+

KZP05Y05D981KZP04Y05D984 KZP01Y05D980KZP02Y05D988KZP03Y05D986

12.05.2014 А

KZP05Y05D981KZP04Y05D984 KZP01Y05D980KZP02Y05D988KZP03Y05D986

29.09.2014 А KZP05Y05D981KZP04Y05D984

The number of employees , persons

70605040302010

02013 2014

34 35

2014 Annual Report

Risk factors:

Business risks.

The company mostly operates in the agricultural sector, which is exposed to a number of risks. In this regard, the key business risks depend on external factors, such as weather, which affect the yield and quality of wheat and other products. This may cause sharp fluctuations in the crops harvested.

Key industry risks:• Weather and other natural hazards (droughts, floods, locust)• Overproduction of similar products in the world• High volatility in grain prices• Policies of neighboring countries• Reduced demand as a result of reduced consumption• Sharp increase in production costs (prices for fuel, herbicides and seeds) • Loss and seizure of lands by the state• Inadequate logistics of delivering grain to the end consumer (lack of hopper cars)

The occurrence of one or more of the above risks may cause a decline in income and deterio-ration of business conditions.

In exchange for wheat and other products for trading after harvesting, the company provides farms with financing, which is shown in the balance sheet as Advances Paid. These advances are a financial risk for the company. The management strictly monitors the balance of ad-vanced paid to minimize credit losses.

Financial risk factors.

Financial risk management in the company covers risks associated with prices for goods, finan-cial risks, operational risks and legal risks.

RISK MANAGEMENT

As mentioned before, the company’s main business is selling wheat, which exposes it to risks of product price changes. Local and global market conditions could cause changes, including significant changes in prices for agricultural products.

Operational and legal risk management was established to ensure the proper functioning of the internal policies and procedures and minimize operational and legal risks.

Financial risks include market risks (currency risk, interest rate risk and other price risks), credit risk and liquidity risk. The main goal of financial risk management is to determine risk limits and further ensure compliance with established limits.

Risk management program is based on the implied unpredictability of financial markets and focuses on minimizing the adverse impacts on the company’s financial condition. Daily oper-ations are overseen by the supreme body of operational management, responsible for oper-ating decision making and legal risk management under the control of the company’s legal department.

Credit risk. The company is exposed to credit risk, meaning that one party to a financial instru-ment could bring financial loss to the other party, being unable to perform its contractual ob-ligations. Exposure to credit risk arises from selling the company products on credit, as well as from other transactions with counterparties, where financial assets are created. The company has policies to ensure it sells its products and services to customers with an appropriate credit history. The company has no internal ranking procedures or limits imposed on counterparties. The management analyses the unpaid receivables by maturity and keeps track of overdue receivables.

Concentration of credit risk. The company is exposed to concentration of credit risk. As of December 31, 2014, the company had four counterparties, of which two are significant other parties (2013: four counterparties, of which two were related parties and the other two were other significant parties). Receivables outstanding from these counterparties made up over 10 percent of the total receivables from the core business and other receivables. The receivables totaled 12.2 billion Tenge (2013: 19.7 billion, or 50 percent of the total receivables from the core business and other receivables, 2013: 40 percent).

36 37

2014 Annual Report

Market risk. The company is exposed to market risks. Market risks are associated with open po-sitions on a) foreign currencies and b) assets, generating interest income and interest obliga-tions that are exposed to general and specific market movements. The management sets risk limits and monitors compliance with them on a regular basis. However, this approach cannot prevent losses in excess of these limits in the event of more significant market movements.

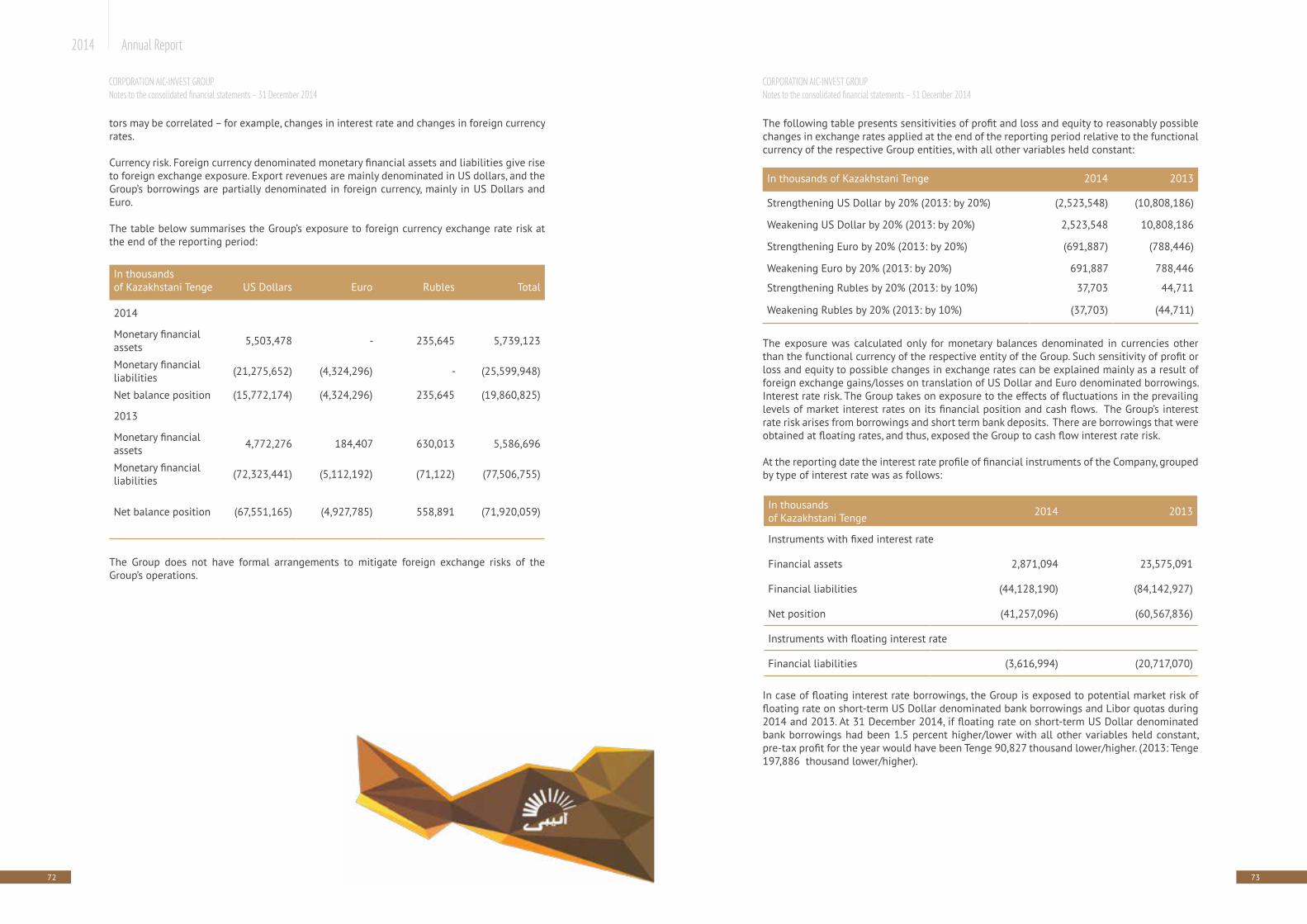

Currency risk. Revenue from export sales is mainly in United States dollars, while loans are partially in foreign currency, mainly in United States dollars and euros.

Risk of interest rate changes affecting cash flow. The company is exposed to the risk of interest rate fluctuations affecting its financial condition and cash flow. In particular, we are talking about the risk of interest rate changes associated with loans and short-term bank deposits. The company has floating-rate loans.

Liquidity risk. Liquidity risk affects the company’s ability to meet its financial obligations. The company’s approach to liquidity management is to ensure continuous and sufficient liquidity to repay obligations as they mature (in both normal and unusual situations), avoiding unac-ceptable losses or reputational risks.

By virtue of the dynamic nature of the business, the company tries to maintain a stable funding base, consisting mostly of shareholders’ capital, loans, payables from core activities and other payables.

The management controls cash flow projections. The company ensures the availability of funds at short notice in an amount sufficient to cover the expected operating costs. At the same time, the potential impact of exceptional circumstances – which could not be reasonably foreseen, like for instance, natural disasters – is not taken into account.

Capital risk management. The goal of risk management with regard to capital management is to ensure continuity of the company’s operations in order to preserve ROE for the members and provide benefits for other stakeholders.

Like other companies in the industry, APK-Invest has substantial borrowing needs. Financing management is carried out on a daily basis by the supreme operational management body, re-sponsible for operational decision making, and by other senior managers. The company active-ly manages its debt obligations to reduce financing costs. There are certain borrowings, where a certain debt-to-capital ratio has to be met. When discussing new credit lines, the company needs to get approval from such borrowers, who have to agree with the new debt-to-capital ratio.

As of December 31, 2014 and 2013, the company considered the ratio of its total debt to its to-tal capital to be adequate and consistent with industry standards. The share of debt declined from 59 percent in 2013 to 39 percent in 2014.

CORPORATE GOVERNANCE

38 39

2014 Annual Report

CORPORATE GOVERNANCE

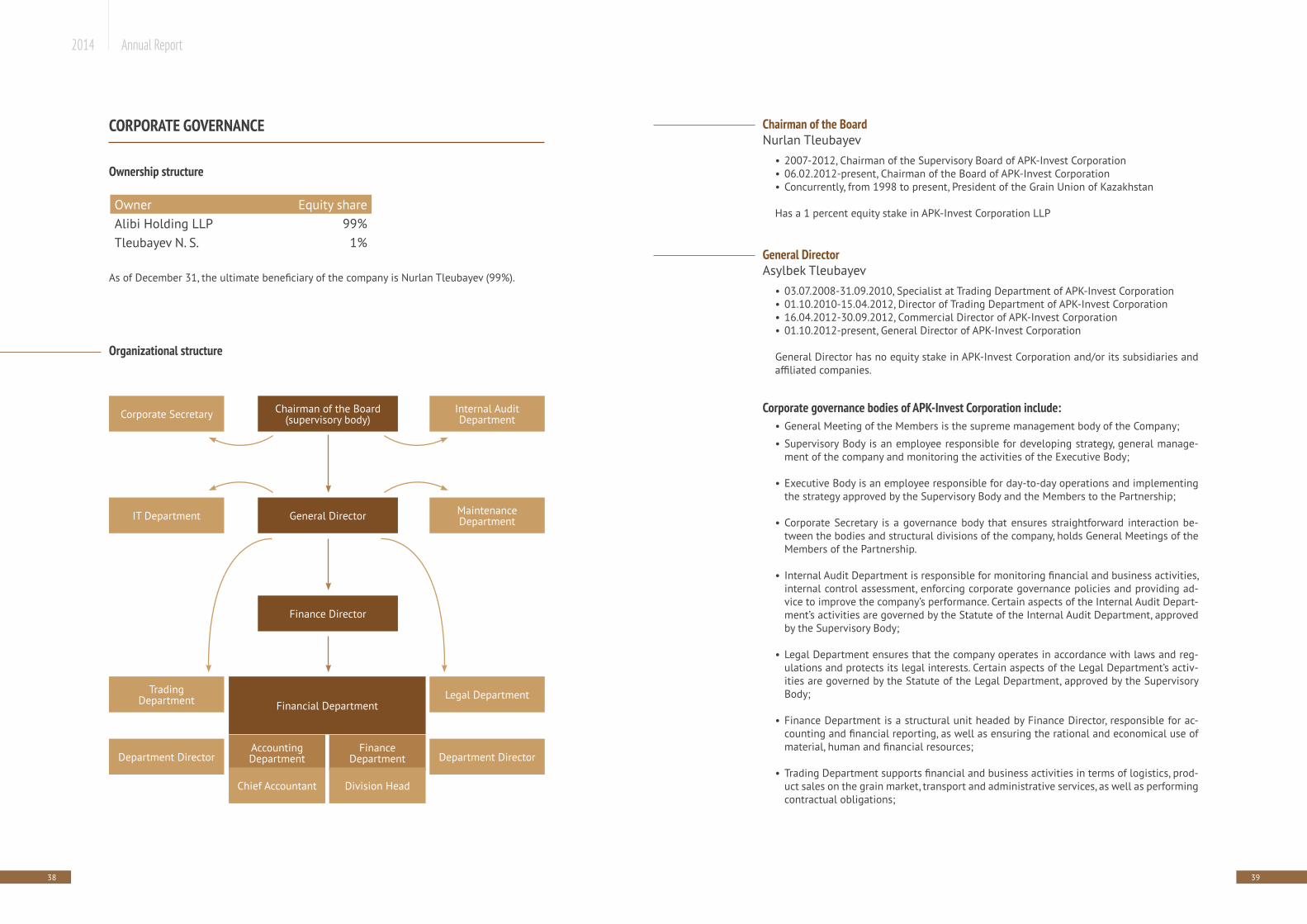

Ownership structure

As of December 31, the ultimate beneficiary of the company is Nurlan Tleubayev (99%).

Owner Equity shareAlibi Holding LLP 99%Tleubayev N. S. 1%

Organizational structure

Corporate Secretary

IT Department

Trading Department Financial Department

Accounting Department

Chief Accountant

Finance Department

Division Head

Legal Department

Department DirectorDepartment Director

Chairman of the Board(supervisory body)

General Director

Finance Director

Internal Audit Department

MaintenanceDepartment

Chairman of the Board Nurlan Tleubayev

• 2007-2012, Chairman of the Supervisory Board of APK-Invest Corporation• 06.02.2012-present, Chairman of the Board of APK-Invest Corporation• Concurrently, from 1998 to present, President of the Grain Union of Kazakhstan

Has a 1 percent equity stake in APK-Invest Corporation LLP

General DirectorAsylbek Tleubayev

• 03.07.2008-31.09.2010, Specialist at Trading Department of APK-Invest Corporation• 01.10.2010-15.04.2012, Director of Trading Department of APK-Invest Corporation• 16.04.2012-30.09.2012, Commercial Director of APK-Invest Corporation• 01.10.2012-present, General Director of APK-Invest Corporation

General Director has no equity stake in APK-Invest Corporation and/or its subsidiaries and affiliated companies.

Corporate governance bodies of APK-Invest Corporation include:• General Meeting of the Members is the supreme management body of the Company;

• Supervisory Body is an employee responsible for developing strategy, general manage-ment of the company and monitoring the activities of the Executive Body;

• Executive Body is an employee responsible for day-to-day operations and implementing the strategy approved by the Supervisory Body and the Members to the Partnership;

• Corporate Secretary is a governance body that ensures straightforward interaction be-tween the bodies and structural divisions of the company, holds General Meetings of the Members of the Partnership.

• Internal Audit Department is responsible for monitoring financial and business activities, internal control assessment, enforcing corporate governance policies and providing ad-vice to improve the company’s performance. Certain aspects of the Internal Audit Depart-ment’s activities are governed by the Statute of the Internal Audit Department, approved by the Supervisory Body;

• Legal Department ensures that the company operates in accordance with laws and reg-ulations and protects its legal interests. Certain aspects of the Legal Department’s activ-ities are governed by the Statute of the Legal Department, approved by the Supervisory Body;

• Finance Department is a structural unit headed by Finance Director, responsible for ac-counting and financial reporting, as well as ensuring the rational and economical use of material, human and financial resources;

• Trading Department supports financial and business activities in terms of logistics, prod-uct sales on the grain market, transport and administrative services, as well as performing contractual obligations;

40 41

2014 Annual Report

• IT Department is responsible for organization, management, coordination, monitoring and implementation of activities to ensure the smooth functioning and development of the company’s software and hardware systems;

• Maintenance Department is responsible for keeping the car fleet up and running, its safe operation and timely provision of vehicles to other staff to perform their responsibilities.

Corporate governance principles

Corporate governance of APK-Invest Corporation is based on the principles of justice, honesty, responsibility, transparency, professionalism and competence. Effective corporate governance means respect for the rights and interests of all stakeholders, helping the company to be suc-cessful, including increasing its value, fostering its financial stability and profitability.

The fundamental principles of corporate governance include:

• Protection of the rights and interests of the Members;Corporate governance in the Partnership is based on the principle of protection of and respect for the rights and legitimate interests of its Members, facilitating efficient opera-tion of the Partnership, including increasing its assets and fostering its financial stability and profitability.

• Independence of the Partnership;The Partnership operates with a view to respect the interests of its Members to the max-imum extent possible. The Partnership operates independently. Transactions and the re-lationship between the Members of the Partnership are based on the usual commercial principles in accordance with the current laws and regulations.

• Transparency and objectivity of disclosure of information about the activities of the Part-nership;

For informed decision making, the Partnership ensures timely disclosure of accurate in-formation about the Partnership to its Members and other interested parties, including its financial condition and performance, business results, ownership and management structure.

• Legality and ethics;The Partnership is guided by the law, generally accepted principles of business and cor-porate ethics, its Charter, the Corporate Governance Code and its contractual obligations. The relationship between the Members, the Supervisory Body, the Executive Body and other structural units of the Partnership are based on mutual trust, respect, accountability and control.

• Effective human resources policy.Corporate governance in the Partnership is based on the principle of protecting the rights of its employees in accordance with laws and regulations, and seeks to promote co-oper-ation between the Partnership and its employees in resolving social issues and regulating working conditions. One of the key principles of the human resources policy is to preserve jobs to the extent possible, depending on the performance of the Partnership, improve working conditions and provide employees with the necessary social protection.

Internal control and audit

To ensure internal control and internal audit, APK-Invest Corporation has the Internal Audit Department reporting to the Chairman of the Board. The Internal Audit Department is respon-sible for monitoring financial and business activities of the company.

To enforce the principles of objectivity and impartiality, the Supervisory Body approved the Statute of the Internal Audit Department.

Internal control and internal audit allow to quickly identify, prevent and limit financial and operational risks, as well as possible employee misconduct. Thus, internal control and inter-nal audit help the company to reduce its costs and facilitate the effective management of its resources.

The goals of internal control and internal audit in APK-Invest Corporation include: • Achieving operational and financial effectiveness, which involves inspecting the efficiency

and cost-effectiveness of asset management and determining the probability of losses;• Reliability, completeness and timeliness of financial and management information; This in-

volves ensuring that financial statements are reliable and of high quality, which also applies to other financial instruments used by the company when making decisions.

The system of internal control and internal audit in APK-Invest Corporation consists of five main elements: the internal control environment, identification of risks and control objects, control procedures, information support and monitoring.

The existence of the internal control environment means APK-Invest Corporation should have an appropriate organizational structure, helping to minimize risks, increase employee aware-ness of risk management and internal control as a part of the company’s corporate culture.

42 43

2014 Annual Report

Liability section

The present annual report may contain certain forward-looking statements with respect to business activities, strategies and development plans of the Company, as well as the develop-ment of the industry.

Statements containing a forecast of future events are influenced by risk factors, uncertainties and other factors, because of which the actual results may not match the expected results.In this regard, the Company recommends against excessive reliance on the accuracy of fore-casting of future events provided in this Annual Report. The Company does not undertake any obligation to review these forward-looking statements publicly, except as otherwise required by applicable laws and regulations.

ANNEX

Financial statements

44 45

2014 Annual Report

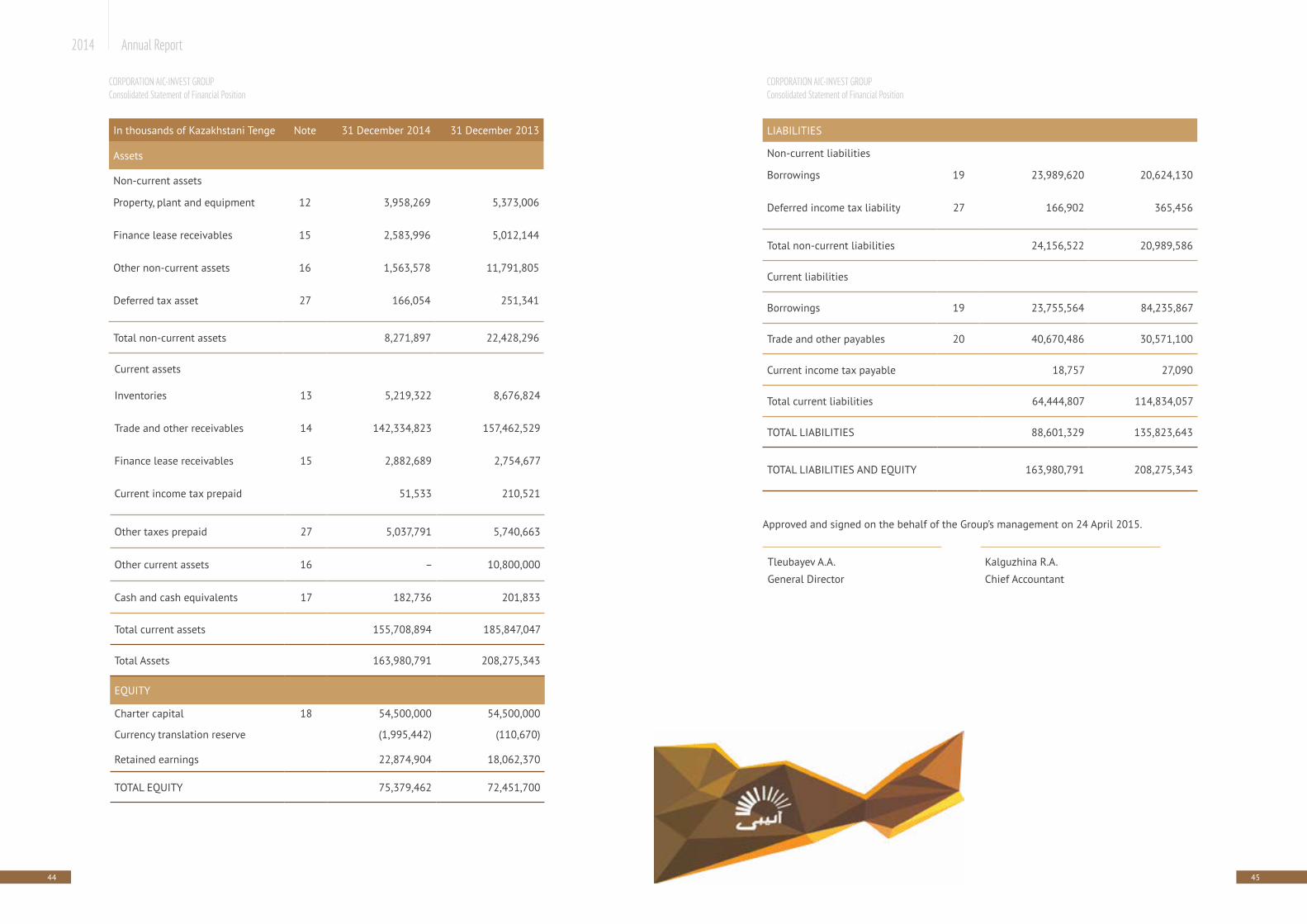

LIABILITIES

Non-current liabilities

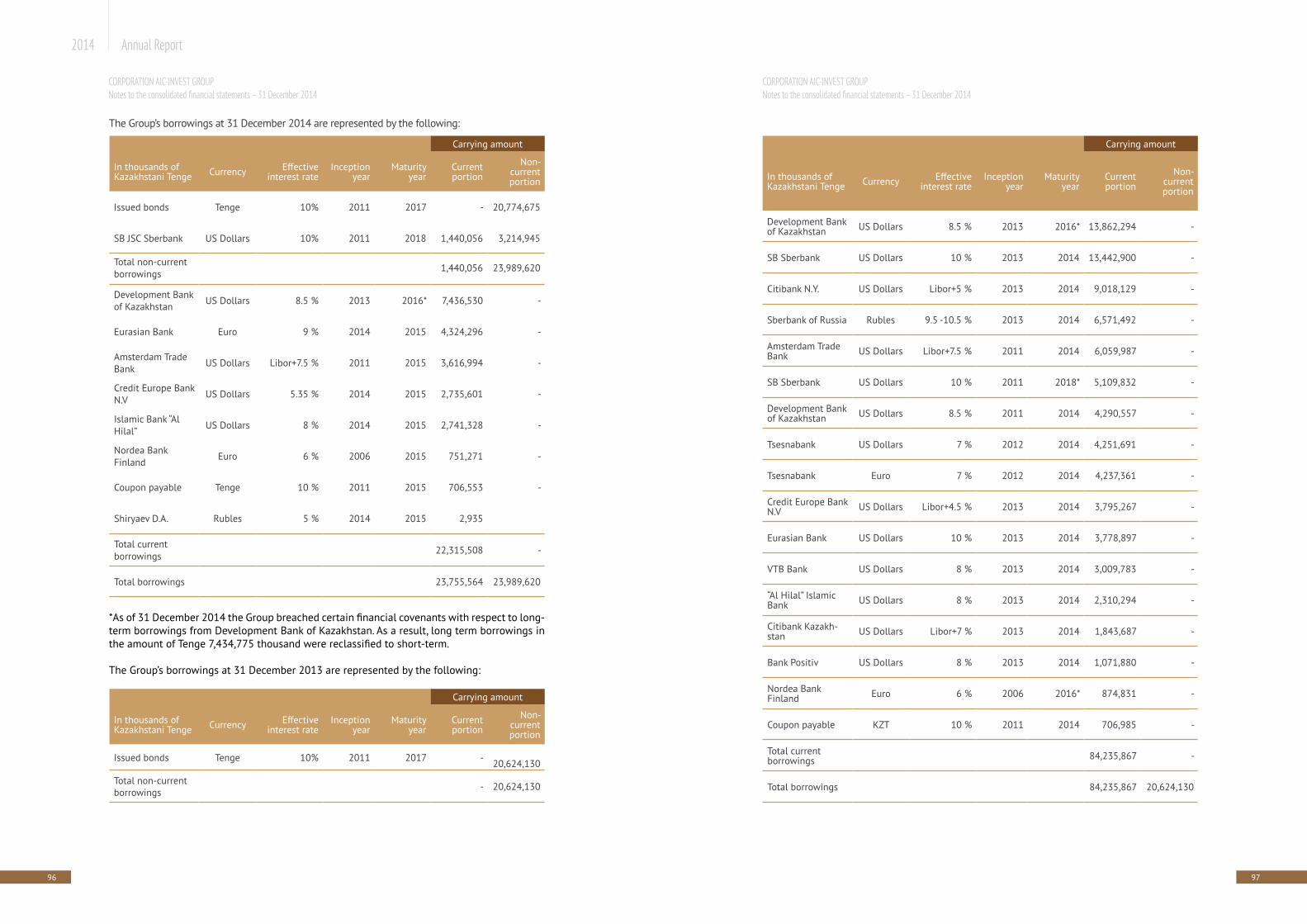

Borrowings 19 23,989,620 20,624,130

Deferred income tax liability 27 166,902 365,456

Total non-current liabilities 24,156,522 20,989,586

Current liabilities

Borrowings 19 23,755,564 84,235,867

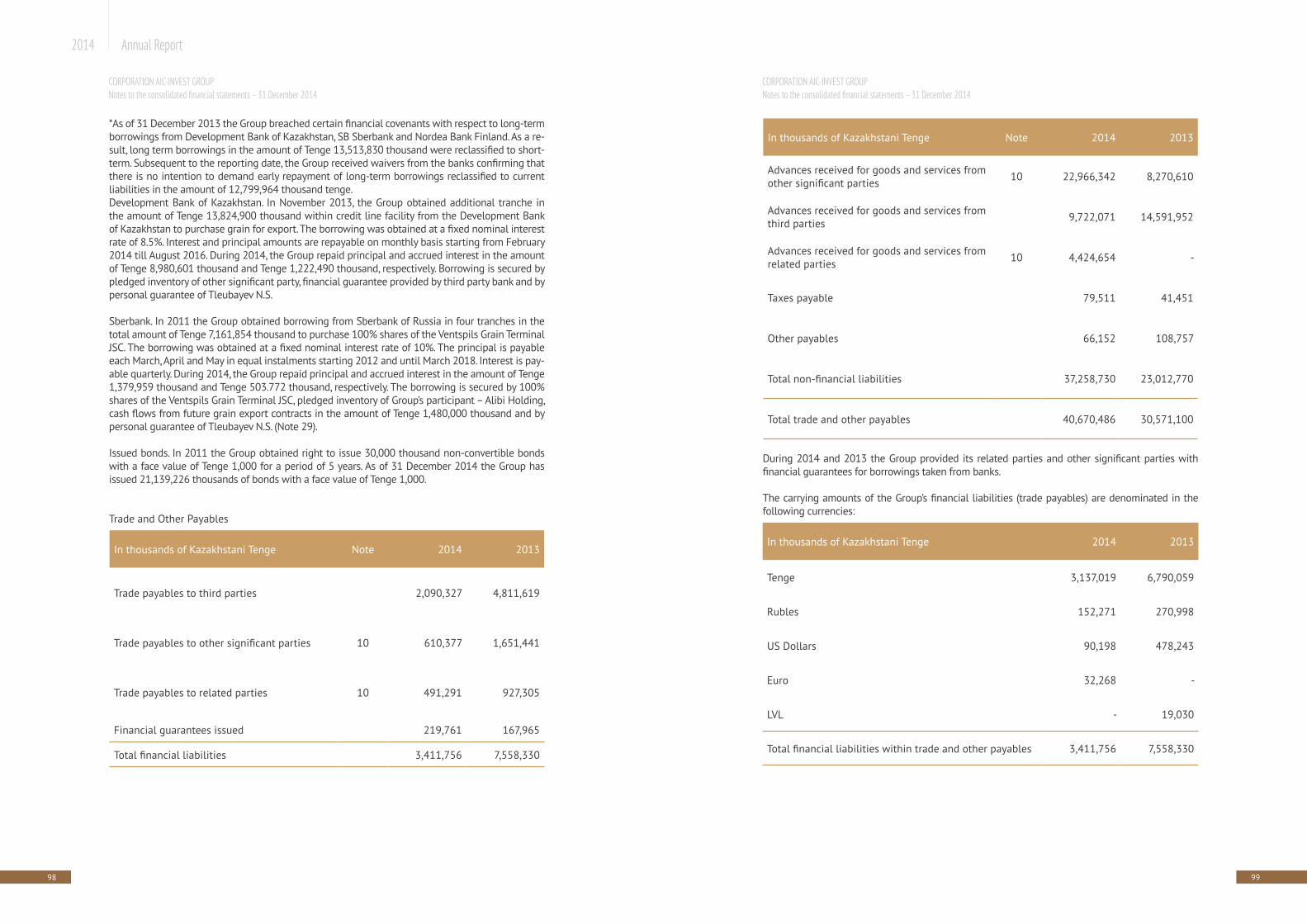

Trade and other payables 20 40,670,486 30,571,100

Current income tax payable 18,757 27,090

Total current liabilities 64,444,807 114,834,057

TOTAL LIABILITIES 88,601,329 135,823,643

TOTAL LIABILITIES AND EQUITY 163,980,791 208,275,343

Approved and signed on the behalf of the Group’s management on 24 April 2015.

Tleubayev A.A. Kalguzhina R.A.

General Director Chief Accountant

In thousands of Kazakhstani Tenge Note 31 December 2014 31 December 2013

Assets

Non-current assets

Property, plant and equipment 12 3,958,269 5,373,006

Finance lease receivables 15 2,583,996 5,012,144

Other non-current assets 16 1,563,578 11,791,805

Deferred tax asset 27 166,054 251,341

Total non-current assets 8,271,897 22,428,296

Current assets

Inventories 13 5,219,322 8,676,824

Trade and other receivables 14 142,334,823 157,462,529

Finance lease receivables 15 2,882,689 2,754,677

Current income tax prepaid 51,533 210,521

Other taxes prepaid 27 5,037,791 5,740,663

Other current assets 16 – 10,800,000

Cash and cash equivalents 17 182,736 201,833

Total current assets 155,708,894 185,847,047

Total Assets 163,980,791 208,275,343

EQUITY

Charter capital 18 54,500,000 54,500,000

Currency translation reserve (1,995,442) (110,670)

Retained earnings 22,874,904 18,062,370

TOTAL EQUITY 75,379,462 72,451,700

CORPORATION AIC-INVEST GROUPConsolidated Statement of Financial Position

CORPORATION AIC-INVEST GROUPConsolidated Statement of Financial Position

46 47

2014 Annual Report

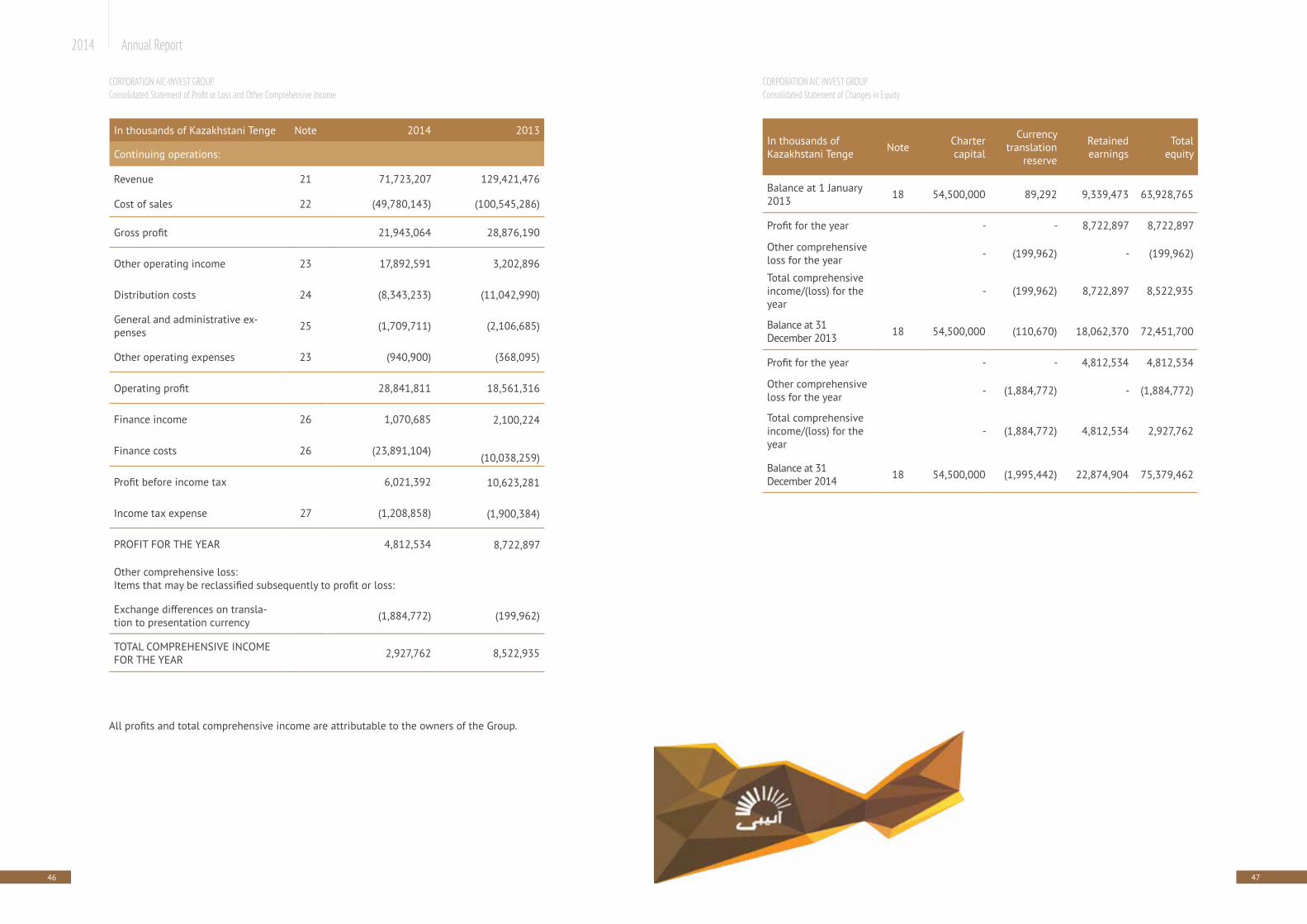

In thousands of Kazakhstani Tenge Note Charter

capital

Currencytranslation

reserve

Retainedearnings

Totalequity

Balance at 1 January 2013 18 54,500,000 89,292 9,339,473 63,928,765

Profit for the year - - 8,722,897 8,722,897

Other comprehensive loss for the year - (199,962) - (199,962)

Total comprehensive income/(loss) for the year

- (199,962) 8,722,897 8,522,935

Balance at 31 December 2013 18 54,500,000 (110,670) 18,062,370 72,451,700

Profit for the year - - 4,812,534 4,812,534

Other comprehensive loss for the year - (1,884,772) - (1,884,772)

Total comprehensive income/(loss) for the year

- (1,884,772) 4,812,534 2,927,762

Balance at 31 December 2014 18 54,500,000 (1,995,442) 22,874,904 75,379,462

In thousands of Kazakhstani Tenge Note 2014 2013

Continuing operations:

Revenue 21 71,723,207 129,421,476

Cost of sales 22 (49,780,143) (100,545,286)

Gross profit 21,943,064 28,876,190

Other operating income 23 17,892,591 3,202,896

Distribution costs 24 (8,343,233) (11,042,990)

General and administrative ex-penses 25 (1,709,711) (2,106,685)

Other operating expenses 23 (940,900) (368,095)

Operating profit 28,841,811 18,561,316

Finance income 26 1,070,685 2,100,224

Finance costs 26 (23,891,104) (10,038,259)

Profit before income tax 6,021,392 10,623,281

Income tax expense 27 (1,208,858) (1,900,384)

PROFIT FOR THE YEAR 4,812,534 8,722,897

Other comprehensive loss:Items that may be reclassified subsequently to profit or loss:

Exchange differences on transla-tion to presentation currency (1,884,772) (199,962)

TOTAL COMPREHENSIVE INCOME FOR THE YEAR 2,927,762 8,522,935

All profits and total comprehensive income are attributable to the owners of the Group.

CORPORATION AIC-INVEST GROUPConsolidated Statement of Profit or Loss and Other Comprehensive Income

CORPORATION AIC-INVEST GROUPConsolidated Statement of Changes in Equity

48 49

2014 Annual Report

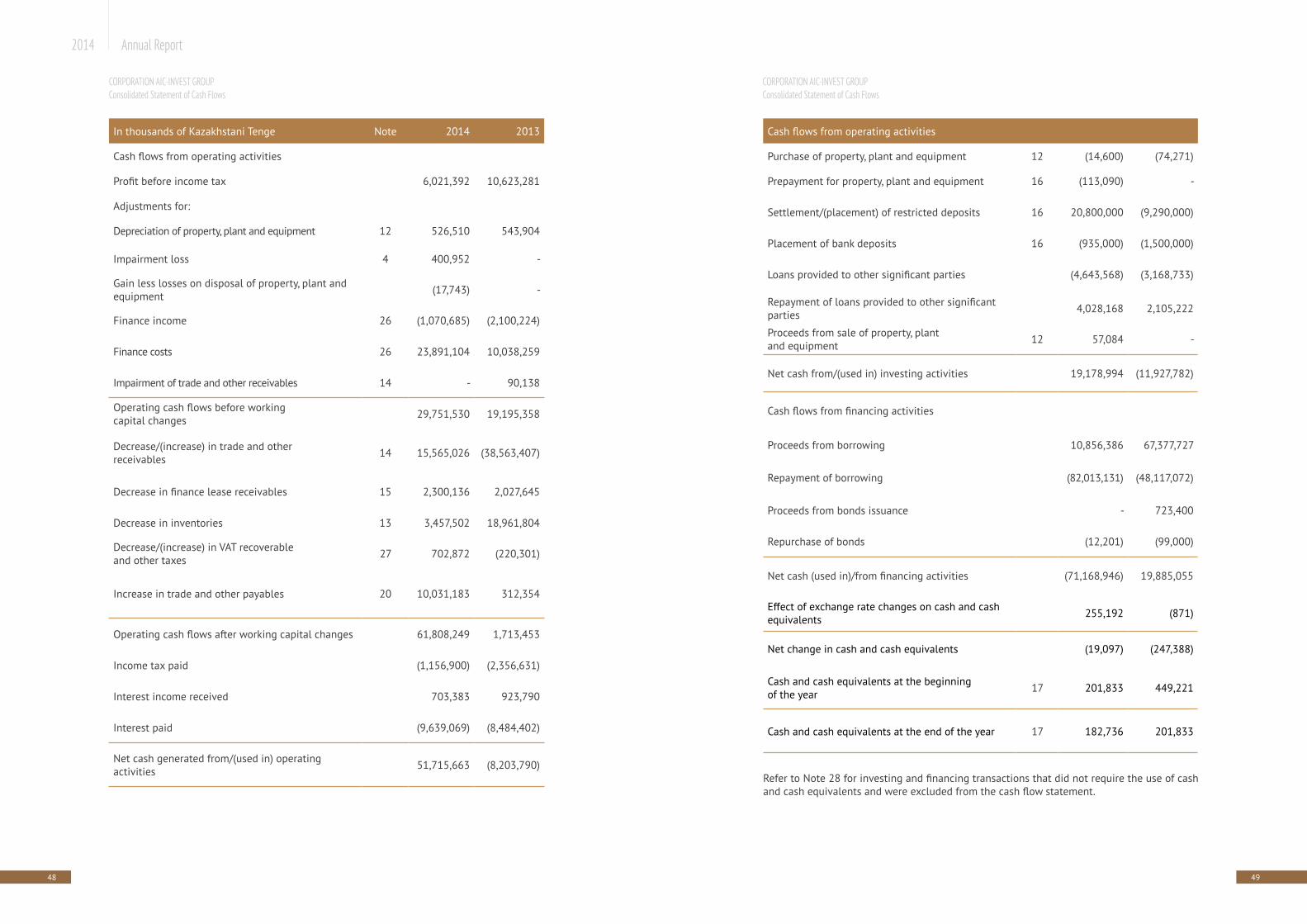

Cash flows from operating activities

Purchase of property, plant and equipment 12 (14,600) (74,271)

Prepayment for property, plant and equipment 16 (113,090) -

Settlement/(placement) of restricted deposits 16 20,800,000 (9,290,000)

Placement of bank deposits 16 (935,000) (1,500,000)

Loans provided to other significant parties (4,643,568) (3,168,733)

Repayment of loans provided to other significant parties 4,028,168 2,105,222

Proceeds from sale of property, plant and equipment 12 57,084 -

Net cash from/(used in) investing activities 19,178,994 (11,927,782)

Cash flows from financing activities

Proceeds from borrowing 10,856,386 67,377,727

Repayment of borrowing (82,013,131) (48,117,072)

Proceeds from bonds issuance - 723,400

Repurchase of bonds (12,201) (99,000)

Net cash (used in)/from financing activities (71,168,946) 19,885,055

Effect of exchange rate changes on cash and cash equivalents 255,192 (871)

Net change in cash and cash equivalents (19,097) (247,388)

Cash and cash equivalents at the beginningof the year 17 201,833 449,221

Cash and cash equivalents at the end of the year 17 182,736 201,833

Refer to Note 28 for investing and financing transactions that did not require the use of cash and cash equivalents and were excluded from the cash flow statement.

In thousands of Kazakhstani Tenge Note 2014 2013

Cash flows from operating activities

Profit before income tax 6,021,392 10,623,281

Adjustments for:

Depreciation of property, plant and equipment 12 526,510 543,904

Impairment loss 4 400,952 -

Gain less losses on disposal of property, plant and equipment (17,743) -

Finance income 26 (1,070,685) (2,100,224)

Finance costs 26 23,891,104 10,038,259

Impairment of trade and other receivables 14 - 90,138

Operating cash flows before working capital changes 29,751,530 19,195,358

Decrease/(increase) in trade and other receivables 14 15,565,026 (38,563,407)

Decrease in finance lease receivables 15 2,300,136 2,027,645

Decrease in inventories 13 3,457,502 18,961,804

Decrease/(increase) in VAT recoverable and other taxes 27 702,872 (220,301)

Increase in trade and other payables 20 10,031,183 312,354

Operating cash flows after working capital changes 61,808,249 1,713,453

Income tax paid (1,156,900) (2,356,631)

Interest income received 703,383 923,790

Interest paid (9,639,069) (8,484,402)

Net cash generated from/(used in) operating activities 51,715,663 (8,203,790)

CORPORATION AIC-INVEST GROUPConsolidated Statement of Cash Flows

CORPORATION AIC-INVEST GROUPConsolidated Statement of Cash Flows

50 51

2014 Annual Report

Azov Port Elevator LLP (the “Azov”) was incorporated in 2002 and is domiciled in the Russian Federation town of Azov, approximately 40 kilometres from the city of Rostov. The main ac-tivity of Azov is loading, drying, storage and dispatch of grain and oil-bearing crops. It was ac-quired by the Company to promote the sale of Kazakhstani grain and grain products to Turkey, Iran, and the Russian Federation.

Ventspils Grain Terminal JSC (the “VGT”) was incorporated in 2001 and is domiciled in the Latvian town of Ventspils. The main activity of VGT is the storage and dispatch of grain, barley and rape. It was acquired by the Company to facilitate export sales shipments at the Baltic Sea.Registered address and place of business

The Company’s registered address is 4/3, Otyrar Str., office 15, Astana, 010000, the Republic of Kazakhstan.

Operating Environment of the Group

The Republic of Kazakhstan displays certain characteristics of an emerging market. Tax, cur-rency and customs legislation is subject to varying interpretations and contributes to the chal-lenges faced by companies operating in the Republic of Kazakhstan (Note 30).The ongoing uncertainty and volatility of the financial markets, in particular in Europe, and other risks could have significant negative effects on the Kazakhstan financial and corporate sectors. The future economic and regulatory situation may differ from management’s current expectations. Management has assessed the potential impairment of non-current assets of the Group, taking into account the current economic situation and prospects (Note 4). Future economic situation and the regulatory environment may differ from current expectations of management.

The Group’s major risks arise from external factors. The main factor is the volume of harvest in Kazakhstan and neighbouring countries, which directly affects the price and the demand. The volume of harvest is highly dependent on the weather conditions, directly impacting the harvest particularly its yield and quality.

Significant Accounting Policies

Basis of preparation. These consolidated financial statements have been prepared in accord-ance with International Financial Reporting Standards (“IFRS”) under the historical cost con-vention as modified by the initial recognition of financial instruments based on fair value. The principal accounting policies applied in the preparation of these consolidated financial statements are set out below. These policies have been consistently applied to all the periods presented, unless otherwise stated (Note 5). Going concern. Management prepared these financial statements on a going concern basis. Refer to Note 4 for judgment applied by management.

Consolidated financial statements. Subsidiaries are those investees, that the Group controls because the Group (i) has power to direct relevant activities of the investees that significantly affect their returns, (ii) has exposure, or rights, to variable returns from its involvement with the investees, and (iii) has the ability to use its power over the investees to affect the amount of investor’s returns. The existence and effect of substantive rights, including substantive po-

The Group’s interest

Company Country ofincorporation

31 December 2014

31 December 2013

Azov Port Elevator” LLP Russian Federation 100% 100%

Ventspils Grain Terminal” JSC Republic of Latvia 100% 100%

CORPORATION AIC-INVEST GROUP Notes to the consolidated financial statements – 31 December 2014

CORPORATION AIC-INVEST GROUP Notes to the consolidated financial statements – 31 December 2014

2

1 The Group and its Operations

These consolidated financial statements have been prepared in accordance with International Financial Reporting Standards for the year ended 31 December 2014 for “Corporation “AIC-In-vest” Limited Liability Partnership (the “Company”) and its subsidiaries (together referred to as the “Group”). Corporate background The Company was incorporated in September 1998 and is domiciled in the Republic of Ka-zakhstan. On 15 February 2012 the Company’s charter documents were changed resulting in “Holding Alibi” LLP and Mr. Tleubayev Nurlan becoming the new participants of the Company, with respective interests of 99% and 1%. The Group’s ultimate controlling party (the “UCP”) is Mr. Nurlan Tleubayev. The aforementioned change in the Company’s charter document did not change the ultimate controlling party.Principal activityThe Group’s core businesses are the purchase, storage and sale of grain and other agricultural products. The Group purchases mainly from related parties and other significant parties (Note 10). All agricultural products are produced or purchased in the Republic of Kazakhstan and sold both on domestic markets and primarily exported to Central Asia. SubsidiariesPresented below is the list of the Company’s subsidiaries:

3

52 53

2014 Annual Report

ment of orders for the sale of products in a single transaction might affect the quoted price.Valuation techniques such as discounted cash flow models or models based on recent arm’s length transactions or consideration of financial data of the investees are used to fair value certain financial instruments for which external market pricing information is not available. Fair value measurements are analysed by level in the fair value hierarchy as follows: (i) level one are measurements at quoted prices (unadjusted) in active markets for identical assets or liabilities, (ii) level two measurements are valuations techniques with all material inputs ob-servable for the asset or liability, either directly (that is, as prices) or indirectly (that is, derived from prices), and (iii) level three measurements are valuations not based on solely observable market data (that is, the measurement requires significant unobservable inputs). There are no recurring fair value measurements.

Transaction costs are incremental costs that are directly attributable to the acquisition, issue or disposal of a financial instrument. An incremental cost is one that would not have been in-curred if the transaction had not taken place. Transaction costs include fees and commissions paid to agents (including employees acting as selling agents), advisors, brokers and dealers, levies by regulatory agencies and securities exchanges, and transfer taxes and duties. Transac-tion costs do not include debt premiums or discounts, financing costs or internal administra-tive or holding costs.

Amortised cost is the amount at which the financial instrument was recognised at initial rec-ognition less any principal repayments, plus accrued interest, and for financial assets less any write-down for incurred impairment losses. Accrued interest includes amortisation of transac-tion costs deferred at initial recognition and of any premium or discount to maturity amount using the effective interest method. Accrued interest income and accrued interest expense, including both accrued coupon and amortised discount or premium (including fees deferred at origination, if any), are not presented separately and are included in the carrying values of related items in the statement of financial position.