Embed Size (px)

Citation preview

Analysis and Recording

of Transactions

Module 3

SAP 2007 / SAP University Alliances Introductory Accounting

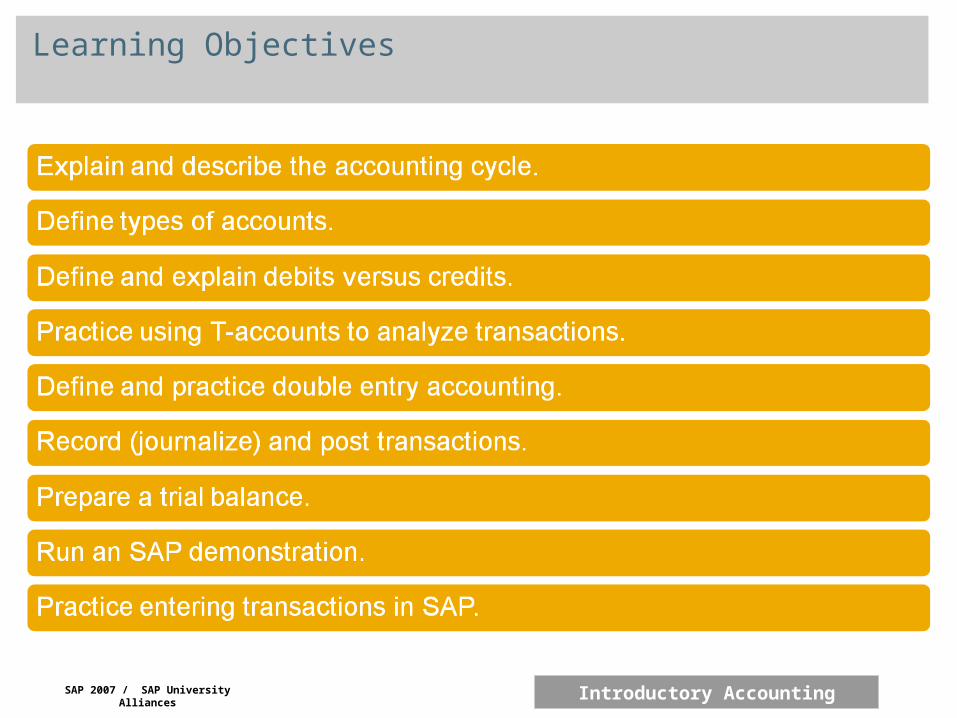

Learning Objectives

SAP 2007 / SAP University Alliances Introductory Accounting

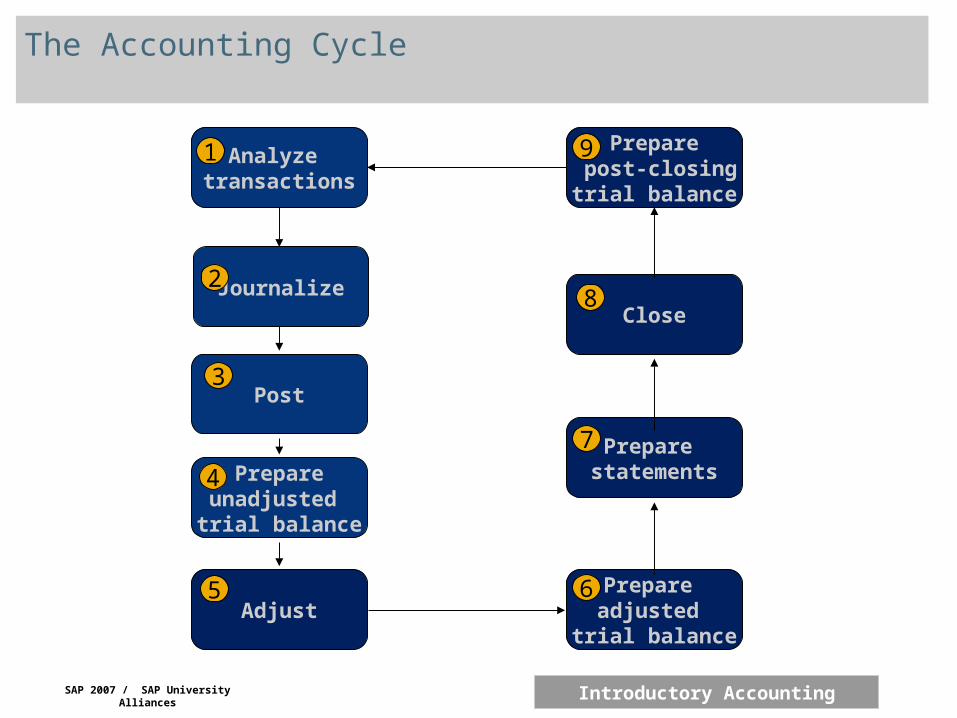

The Accounting Cycle

Analyze transactions

Journalize

Post

Prepare statements

Close

Prepare post-closingtrial balance

Adjust

Prepareunadjusted trial balance

Prepare adjusted

trial balance

22

3

4

5 6

7

8

91

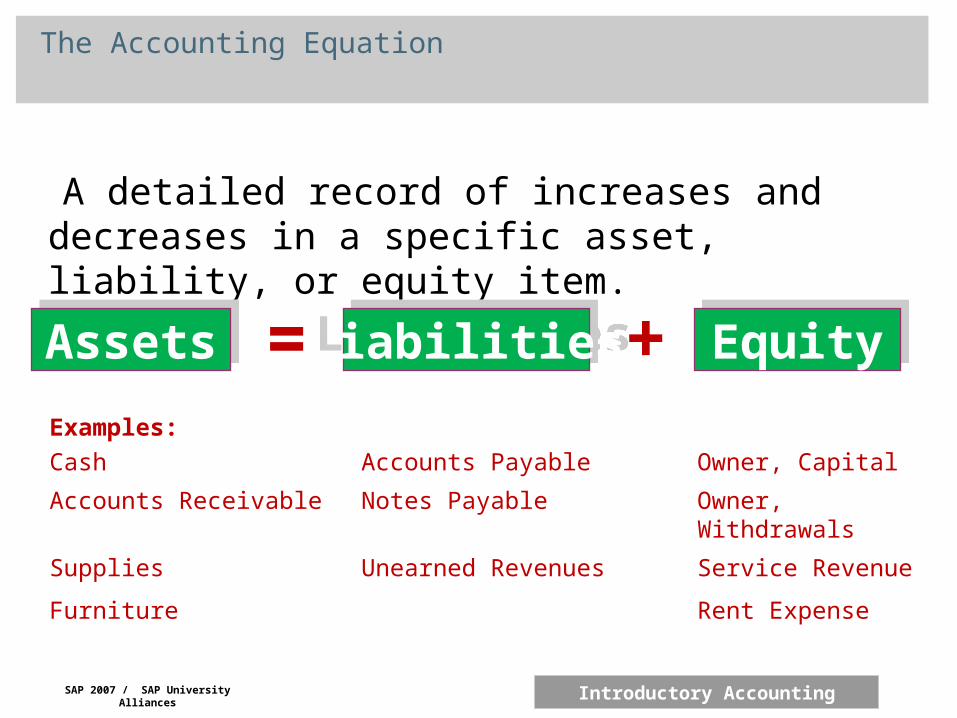

The Accounting Equation

A detailed record of increases and decreases in a specific asset, liability, or equity item.

Examples:

Cash Accounts Payable Owner, Capital

Accounts Receivable Notes Payable Owner, Withdrawals

Supplies Unearned Revenues Service Revenue

Furniture Rent Expense

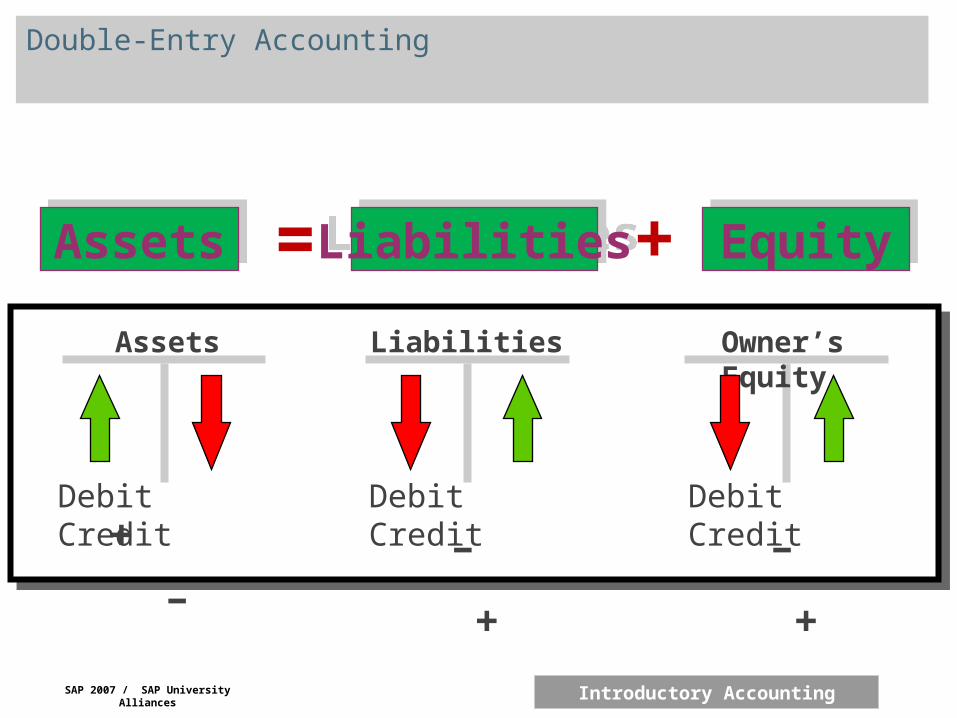

LiabilitiesLiabilities EquityEquityAssetsAssets = +

SAP 2007 / SAP University Alliances Introductory Accounting

SAP 2007 / SAP University Alliances Introductory Accounting

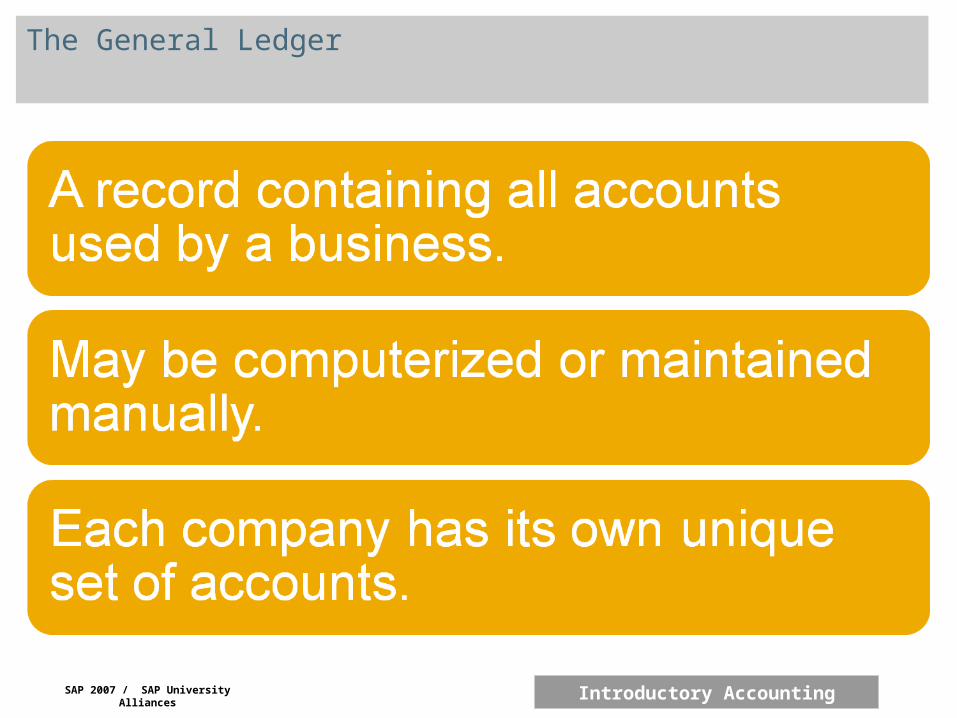

The General Ledger

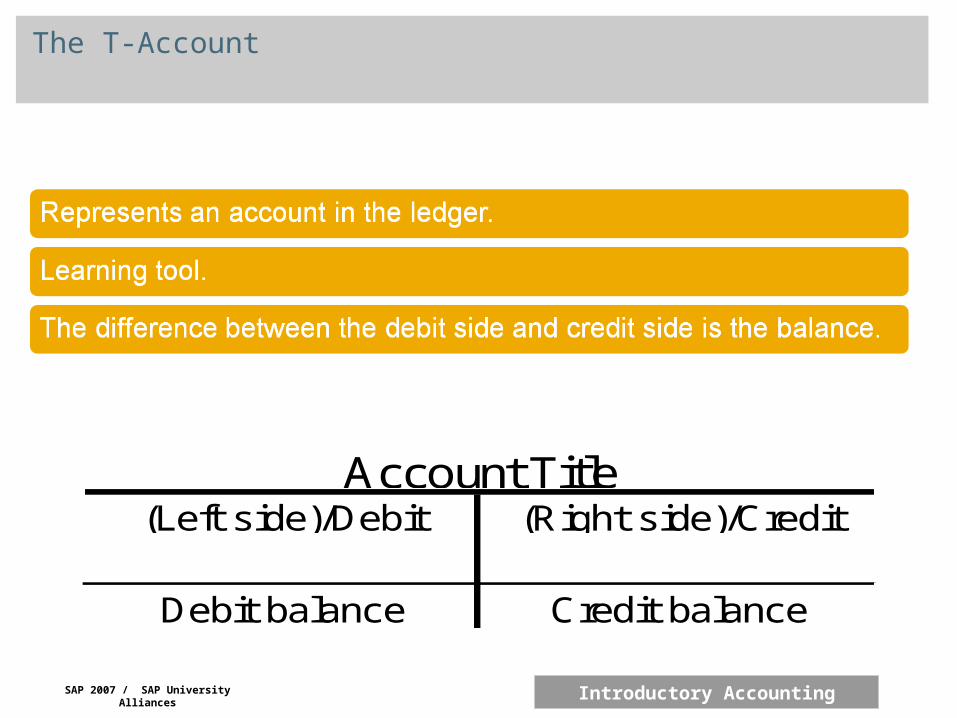

The T-Account

Debit balance Credit balance

Account Title(Left side)/Debit (Right side)/Credit

SAP 2007 / SAP University Alliances Introductory Accounting

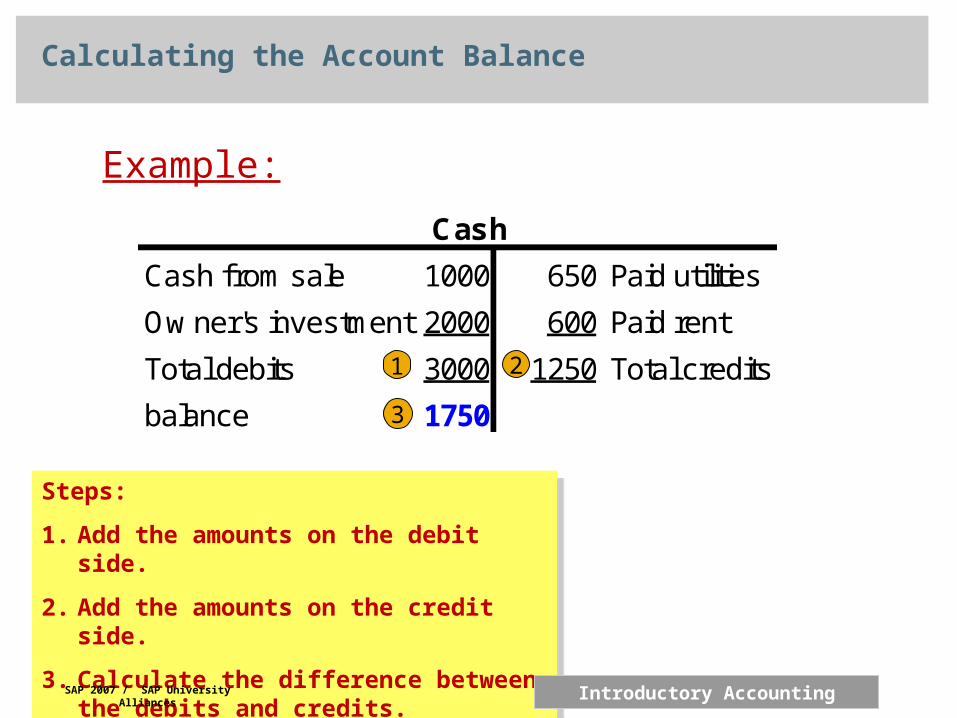

Cash from sale 1000 650 Paid utilities

Ow ner's investment 2000 600 Paid rent

Total debits 3000 1250 Total credits

balance 1750

Cash

Steps:

1. Add the amounts on the debit side.

2. Add the amounts on the credit side.

3. Calculate the difference between the debits and credits.

Steps:

1. Add the amounts on the debit side.

2. Add the amounts on the credit side.

3. Calculate the difference between the debits and credits.

Example:

1 2

3

Calculating the Account Balance

SAP 2007 / SAP University Alliances Introductory Accounting

SAP 2007 / SAP University Alliances Introductory Accounting

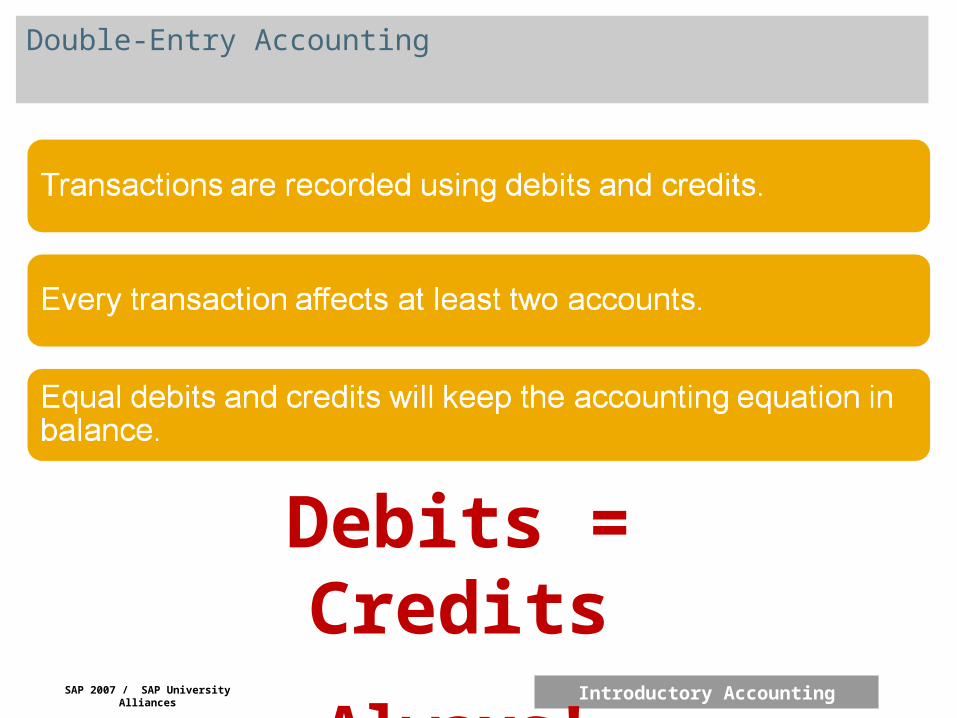

Double-Entry Accounting

Debits = Credits

Always!

LiabilitiesLiabilities EquityEquityAssetsAssets = + Owner’s EquityAssets Liabilities

Debit Credit Debit Credit Debit Credit

+ - - + - +

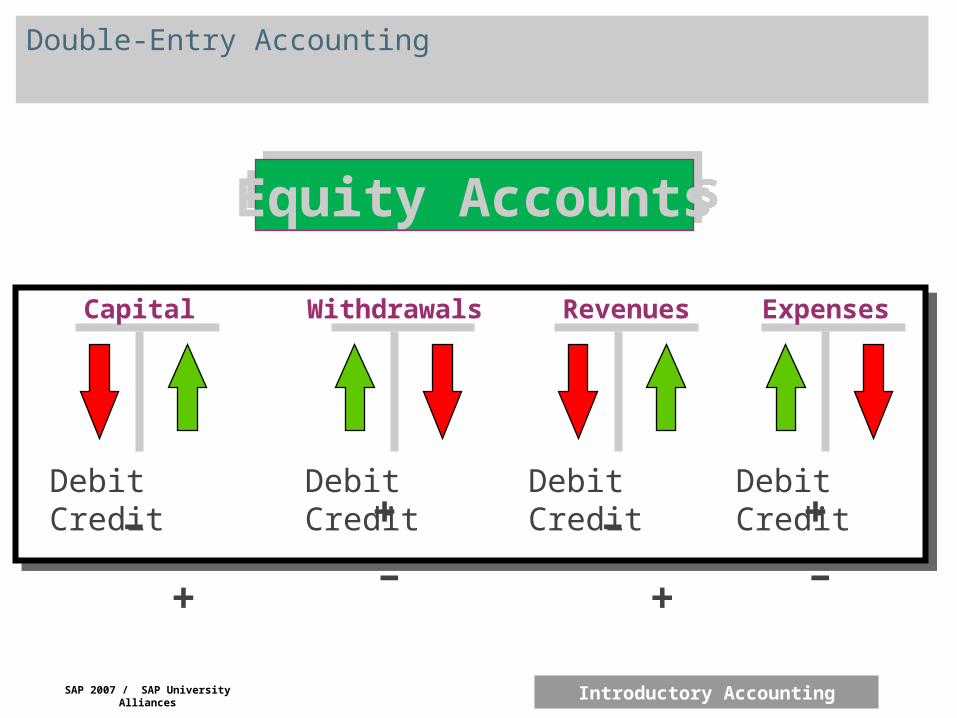

Double-Entry Accounting

SAP 2007 / SAP University Alliances Introductory Accounting

Debit Credit

Capital

- +

Equity AccountsEquity Accounts

Debit Credit

Withdrawals

+ -Debit Credit

Expenses

+ -Debit Credit

Revenues

- +

Double-Entry Accounting

SAP 2007 / SAP University Alliances Introductory Accounting

LiabilitiesLiabilities EquityEquityAssetsAssets

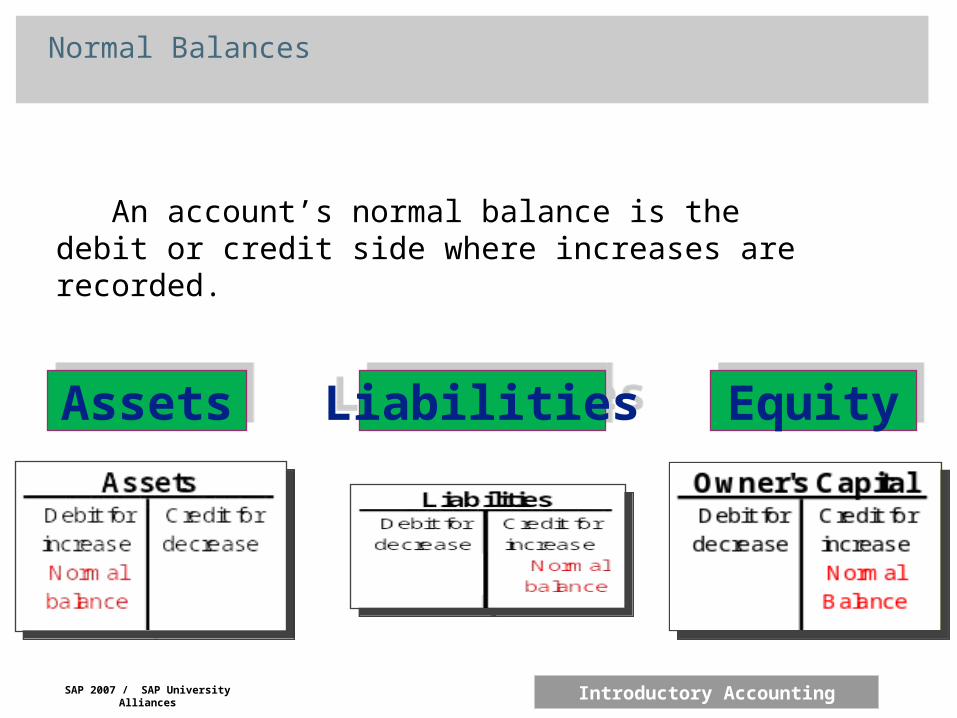

Normal Balances

An account’s normal balance is the debit or credit side where increases are recorded.

= +

SAP 2007 / SAP University Alliances Introductory Accounting

SAP 2007 / SAP University Alliances Introductory Accounting

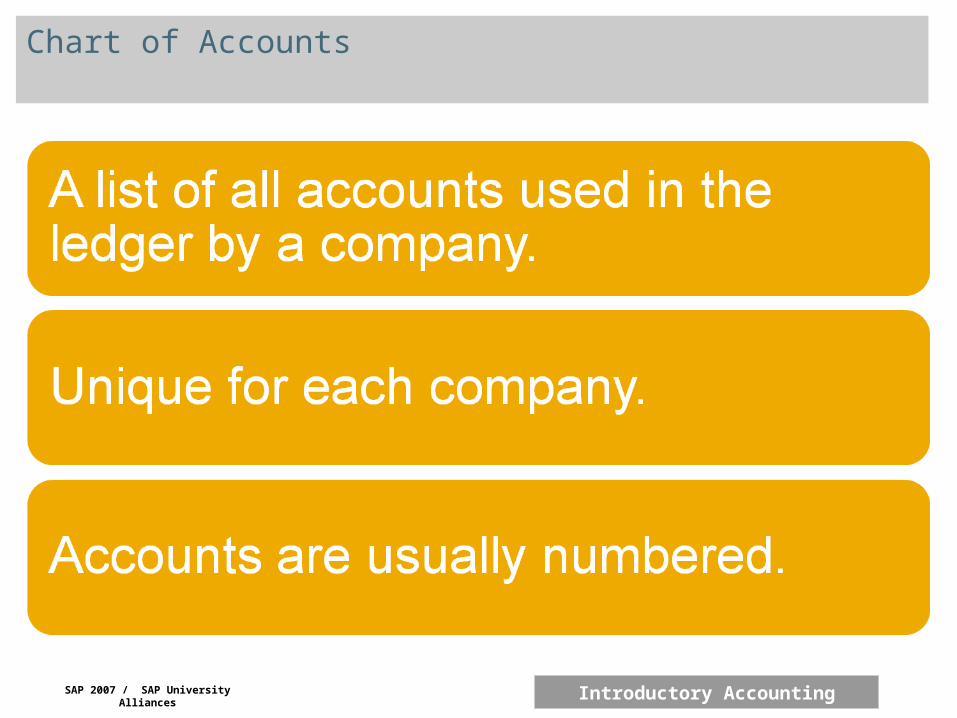

Chart of Accounts

SAP 2007 / SAP University Alliances Introductory Accounting

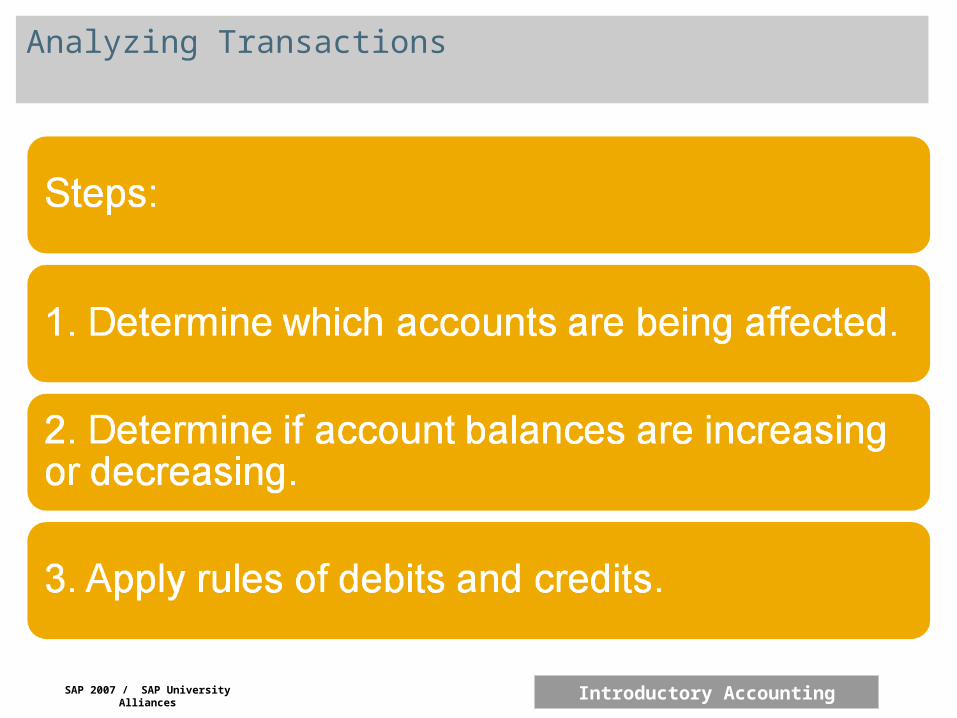

Analyzing Transactions

SAP 2007 / SAP University Alliances Introductory Accounting

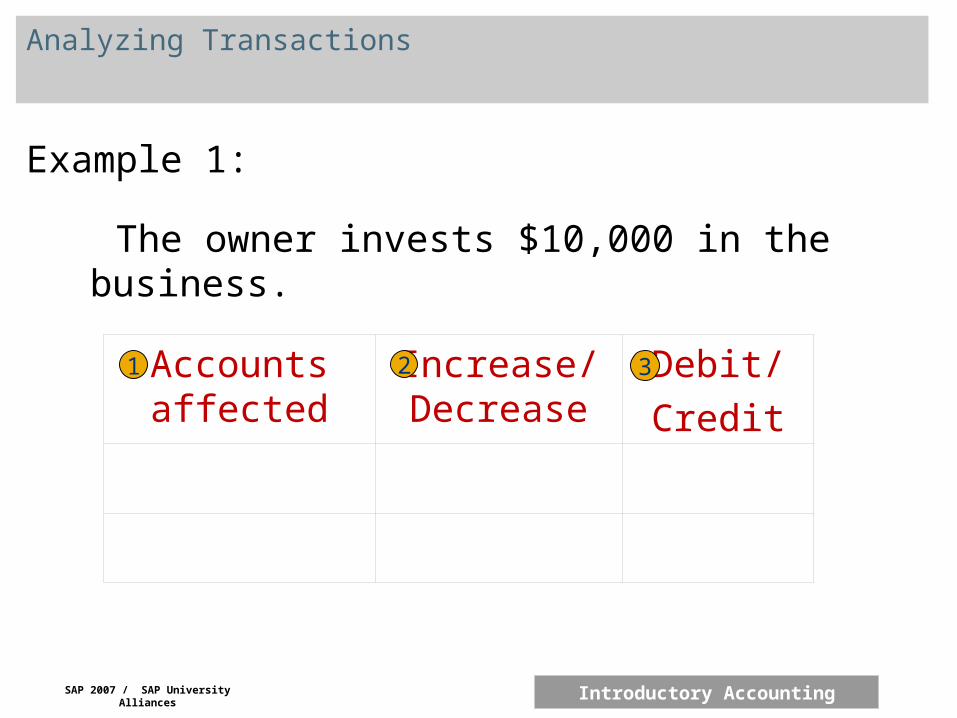

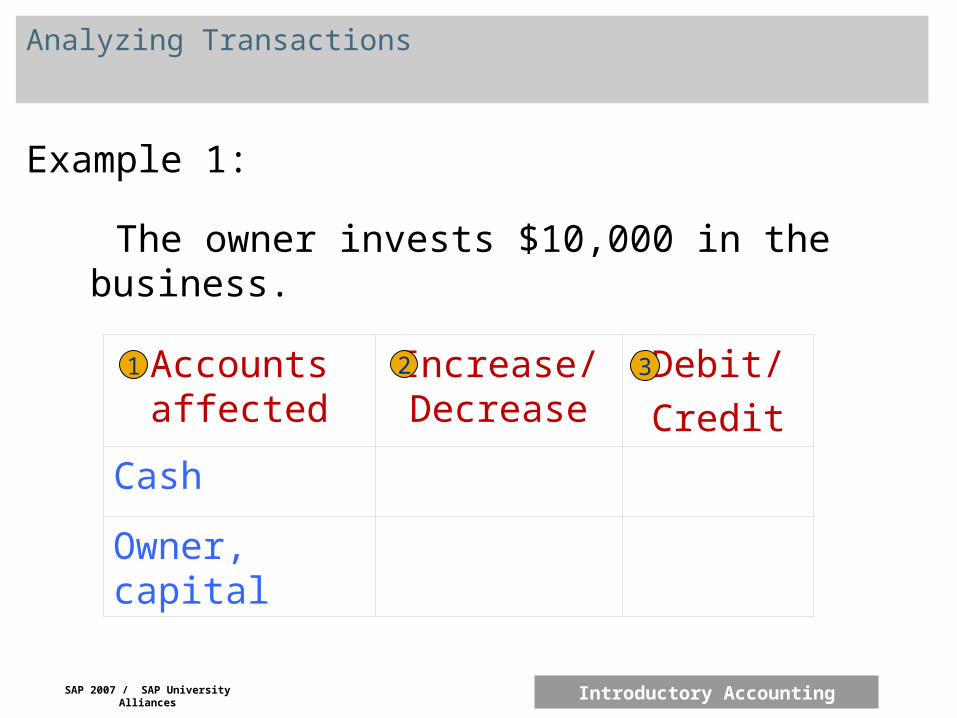

Analyzing Transactions

Example 1:

The owner invests $10,000 in the business.

Accounts affected

Increase/ Decrease

Debit/

Credit

1 32

SAP 2007 / SAP University Alliances Introductory Accounting

Analyzing Transactions

Example 1:

The owner invests $10,000 in the business.

Accounts affected

Increase/ Decrease

Debit/

Credit

Cash

Owner, capital

1 32

SAP 2007 / SAP University Alliances Introductory Accounting

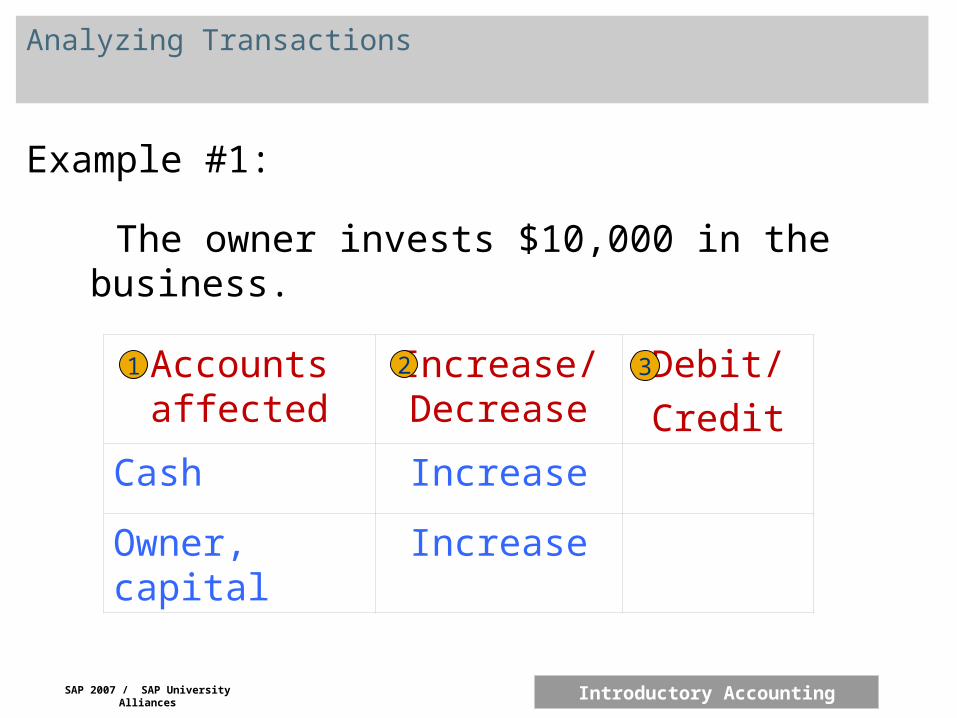

Analyzing Transactions

Example #1:

The owner invests $10,000 in the business.

Accounts affected

Increase/ Decrease

Debit/

Credit

Cash Increase

Owner, capital Increase

1 32

SAP 2007 / SAP University Alliances Introductory Accounting

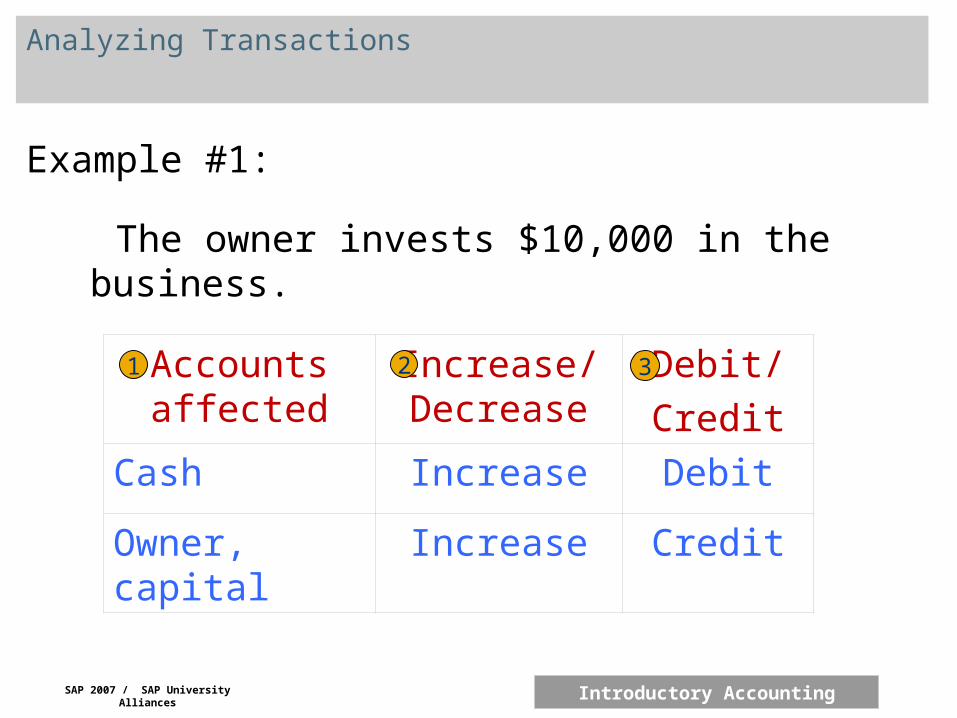

Analyzing Transactions

Example #1:

The owner invests $10,000 in the business.

Accounts affected

Increase/ Decrease

Debit/

Credit

Cash Increase Debit

Owner, capital Increase Credit

1 32

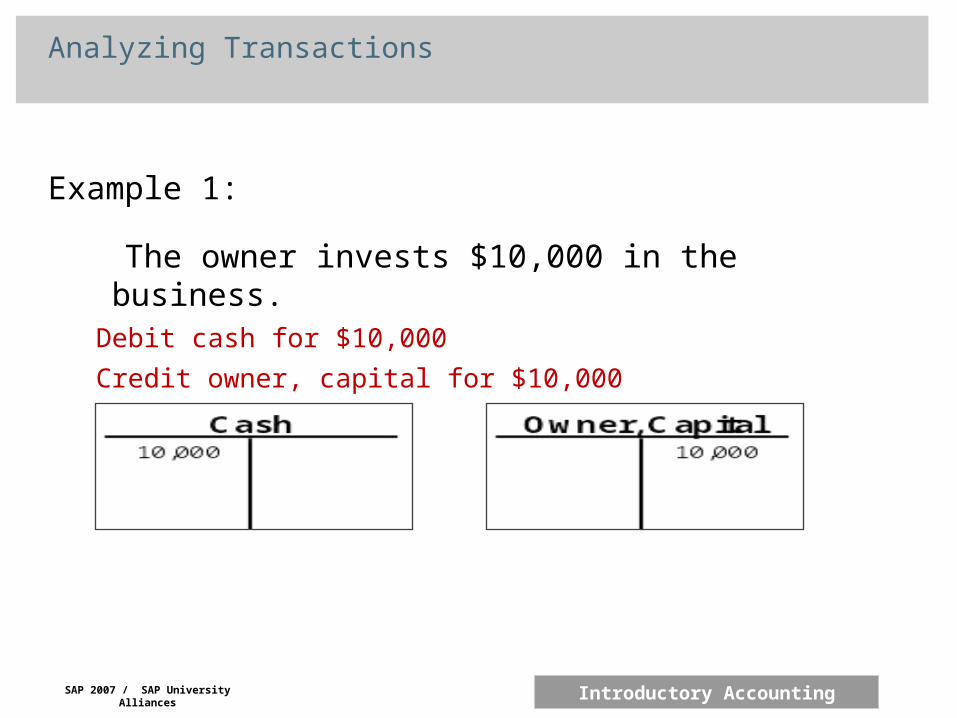

Analyzing Transactions

Example 1:

The owner invests $10,000 in the business.Debit cash for $10,000

Credit owner, capital for $10,000

SAP 2007 / SAP University Alliances Introductory Accounting

SAP 2007 / SAP University Alliances Introductory Accounting

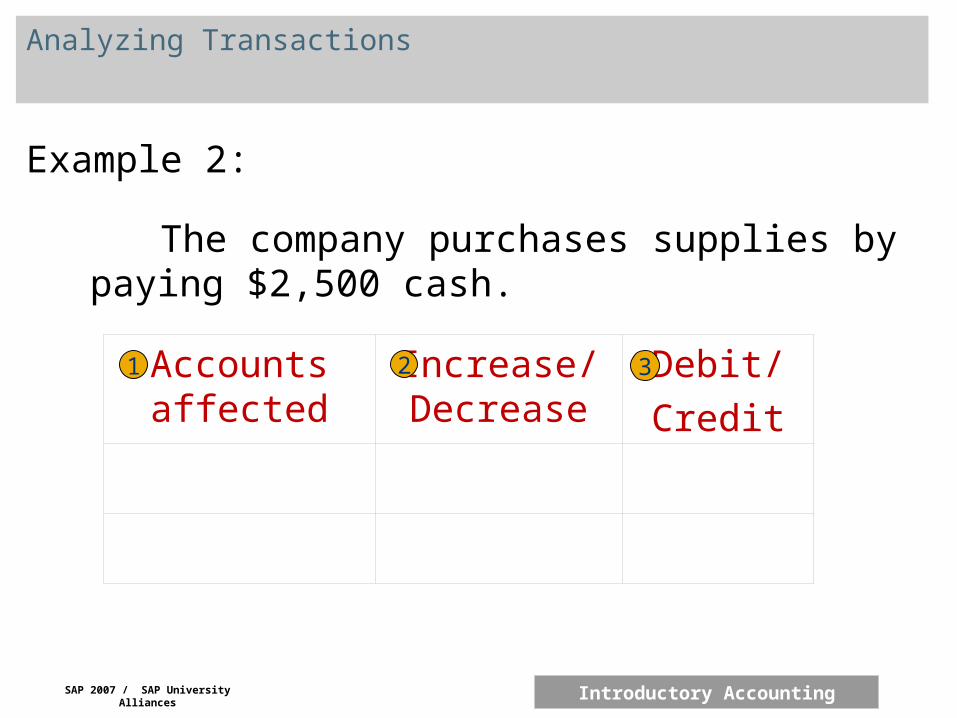

Analyzing Transactions

Example 2:

The company purchases supplies by paying $2,500 cash.

Accounts affected

Increase/ Decrease

Debit/

Credit

1 32

SAP 2007 / SAP University Alliances Introductory Accounting

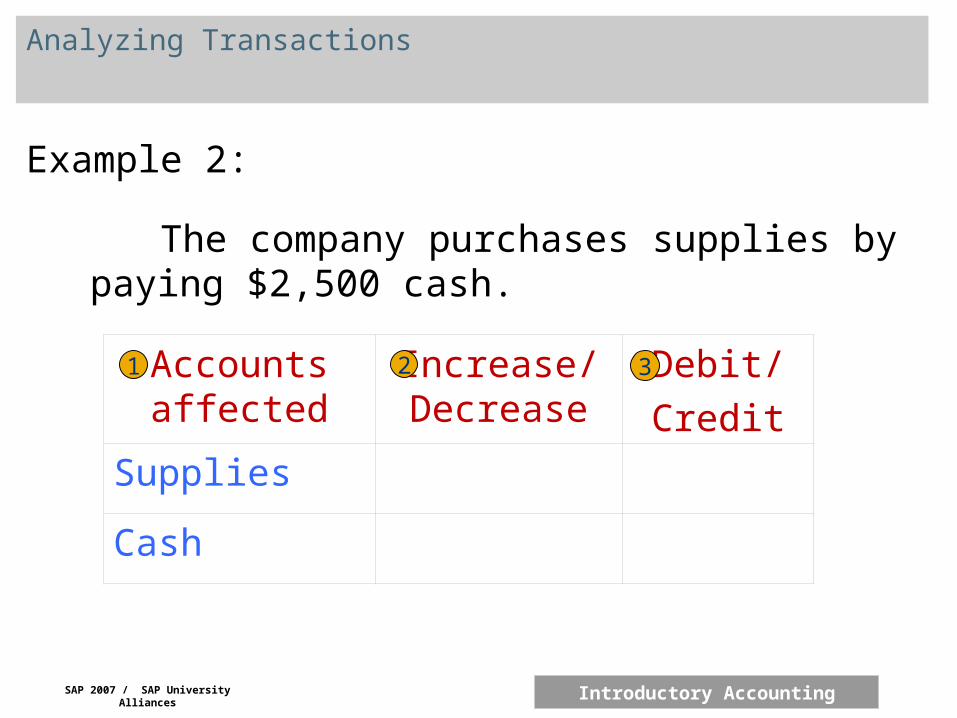

Analyzing Transactions

Example 2:

The company purchases supplies by paying $2,500 cash.

Accounts affected

Increase/ Decrease

Debit/

Credit

Supplies

Cash

1 32

SAP 2007 / SAP University Alliances Introductory Accounting

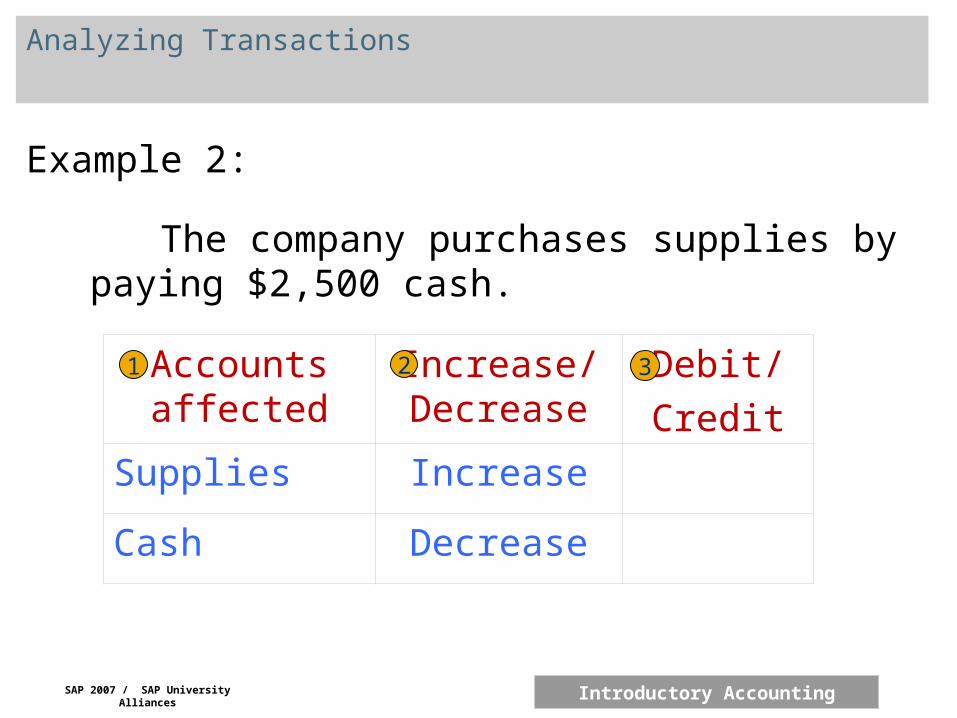

Analyzing Transactions

Example 2:

The company purchases supplies by paying $2,500 cash.

Accounts affected

Increase/ Decrease

Debit/

Credit

Supplies Increase

Cash Decrease

1 32

SAP 2007 / SAP University Alliances Introductory Accounting

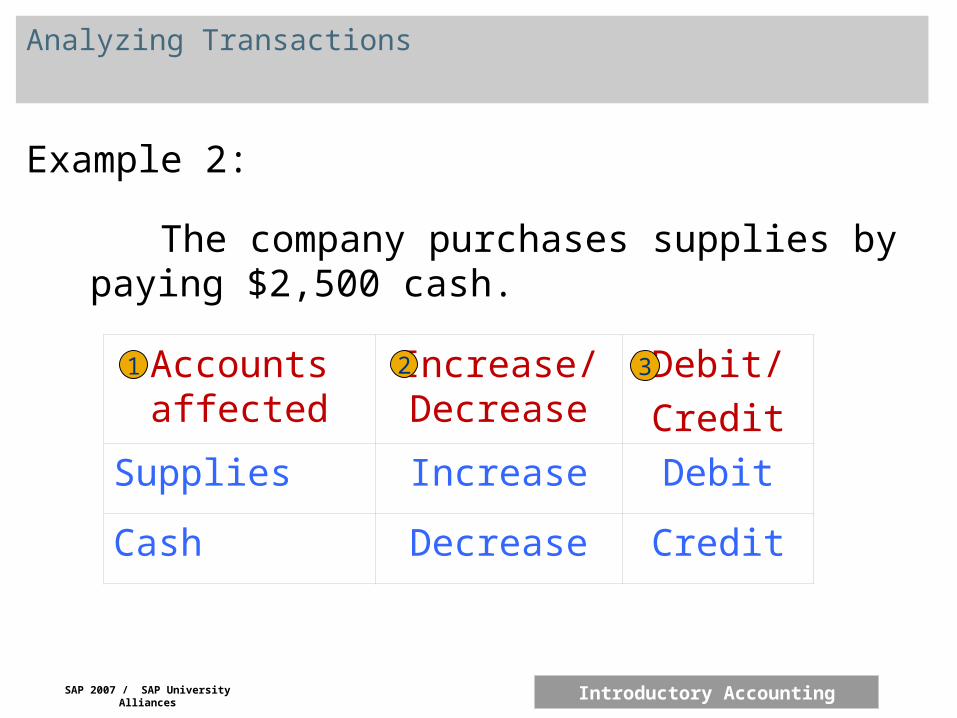

Analyzing Transactions

Example 2:

The company purchases supplies by paying $2,500 cash.

Accounts affected

Increase/ Decrease

Debit/

Credit

Supplies Increase Debit

Cash Decrease Credit

1 32

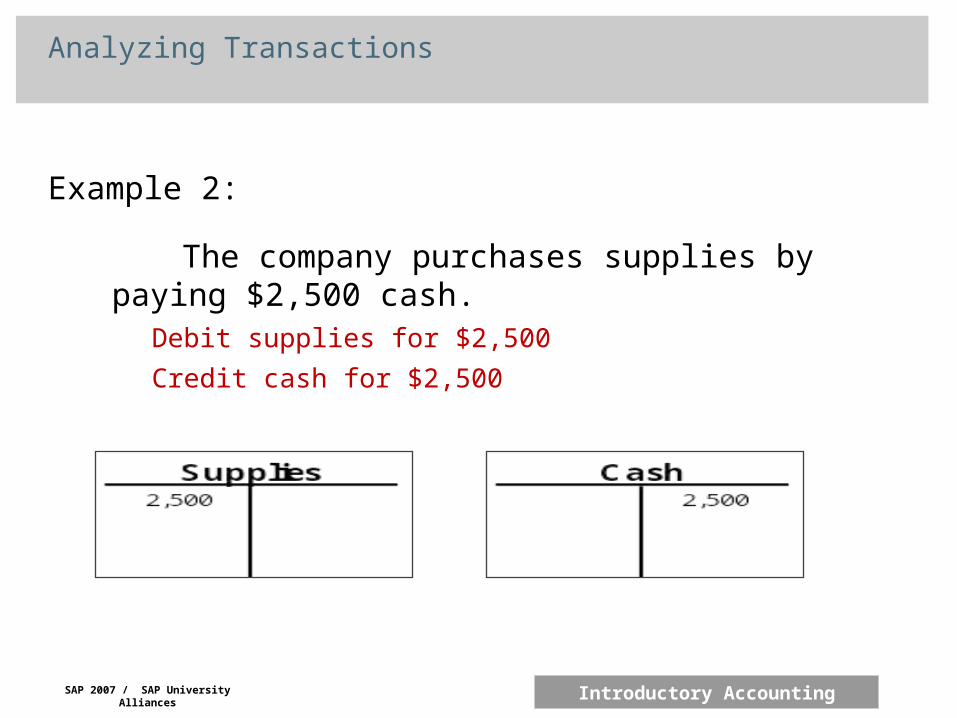

Analyzing Transactions

Example 2:

The company purchases supplies by paying $2,500 cash.

Debit supplies for $2,500

Credit cash for $2,500

SAP 2007 / SAP University Alliances Introductory Accounting

SAP 2007 / SAP University Alliances Introductory Accounting

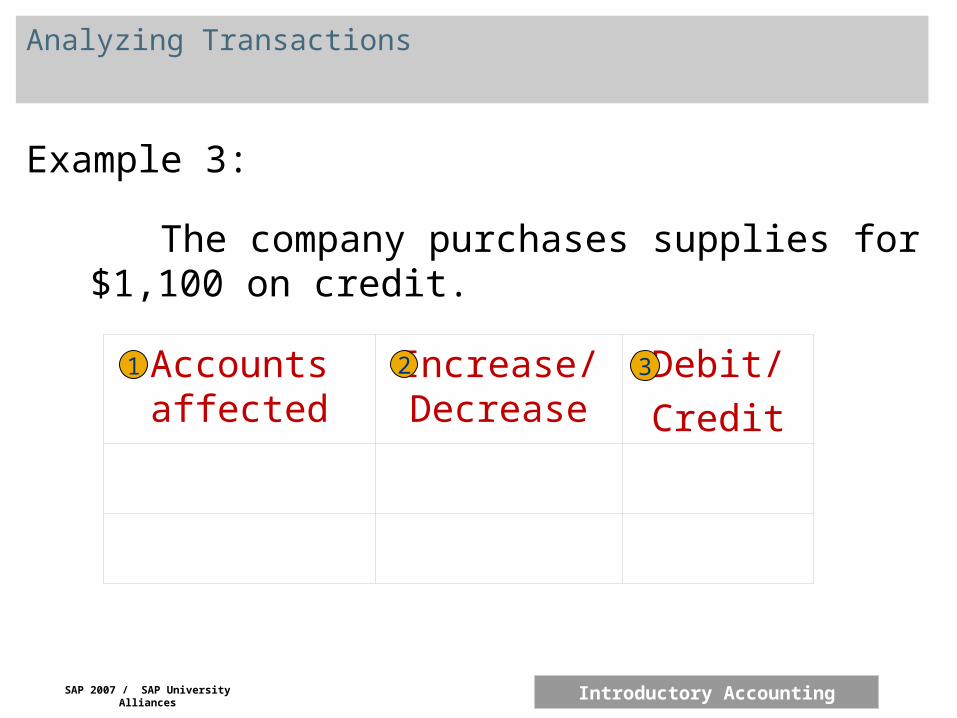

Analyzing Transactions

Example 3:

The company purchases supplies for $1,100 on credit.

Accounts affected

Increase/ Decrease

Debit/

Credit

1 32

SAP 2007 / SAP University Alliances Introductory Accounting

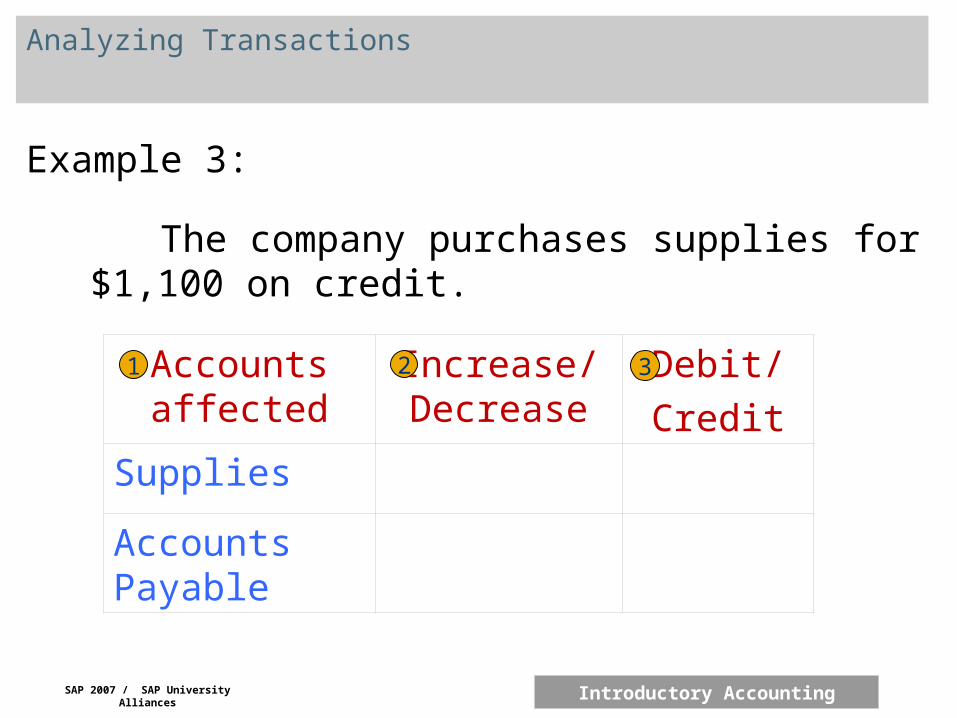

Analyzing Transactions

Example 3:

The company purchases supplies for $1,100 on credit.

Accounts affected

Increase/ Decrease

Debit/

Credit

Supplies

Accounts Payable

1 32

SAP 2007 / SAP University Alliances Introductory Accounting

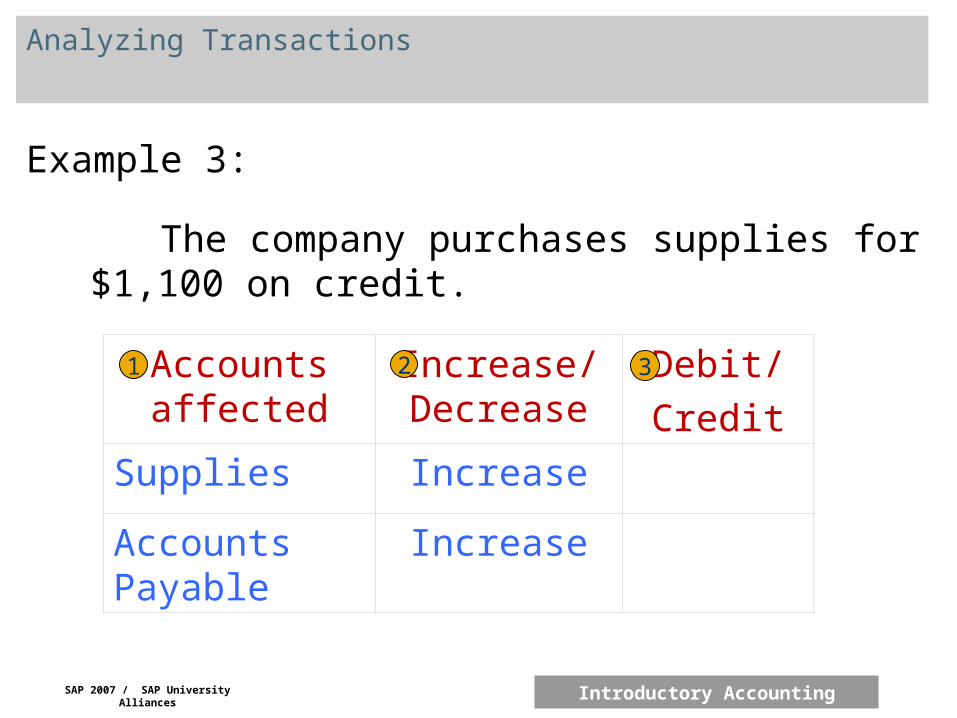

Analyzing Transactions

Example 3:

The company purchases supplies for $1,100 on credit.

Accounts affected

Increase/ Decrease

Debit/

Credit

Supplies Increase

Accounts Payable

Increase

1 32

SAP 2007 / SAP University Alliances Introductory Accounting

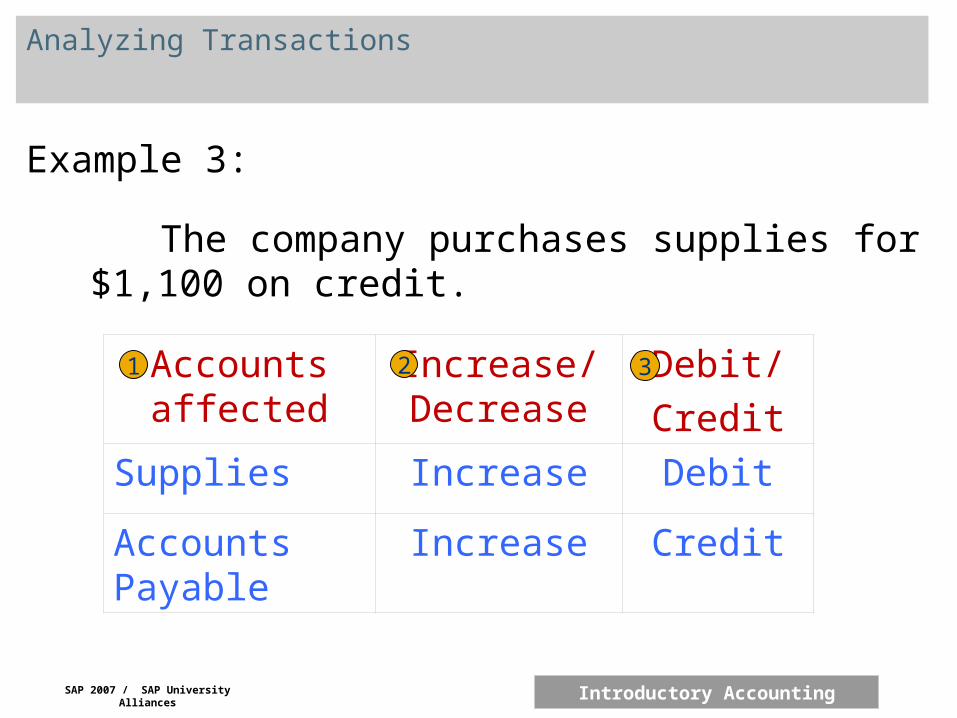

Analyzing Transactions

Example 3:

The company purchases supplies for $1,100 on credit.

Accounts affected

Increase/ Decrease

Debit/

Credit

Supplies Increase Debit

Accounts Payable

Increase Credit

1 32

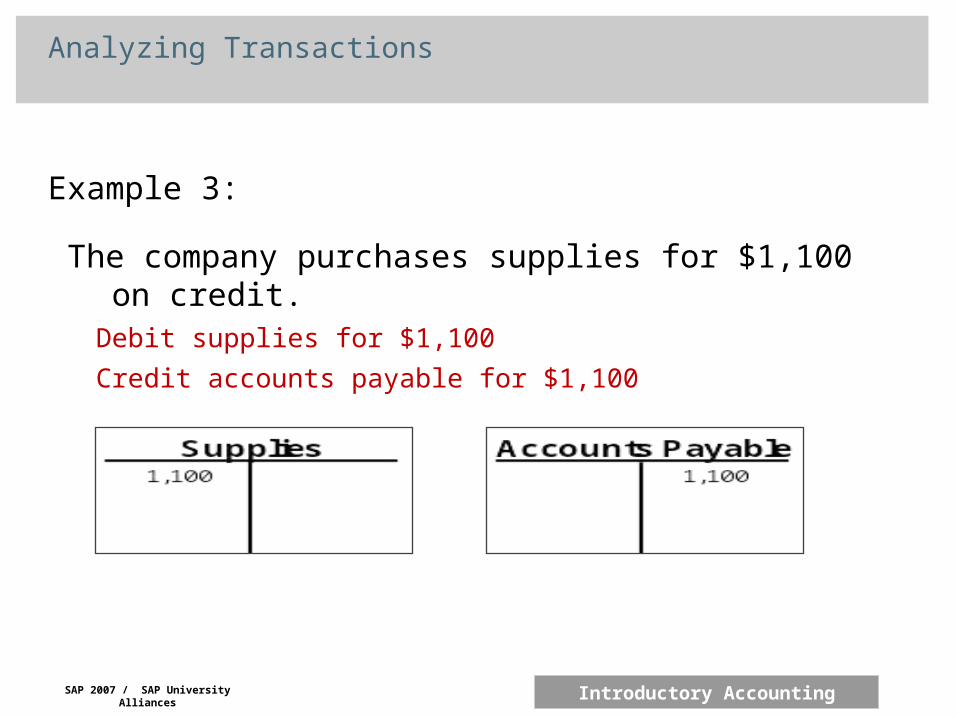

Analyzing Transactions

Example 3:

The company purchases supplies for $1,100 on credit.Debit supplies for $1,100

Credit accounts payable for $1,100

SAP 2007 / SAP University Alliances Introductory Accounting

SAP 2007 / SAP University Alliances Introductory Accounting

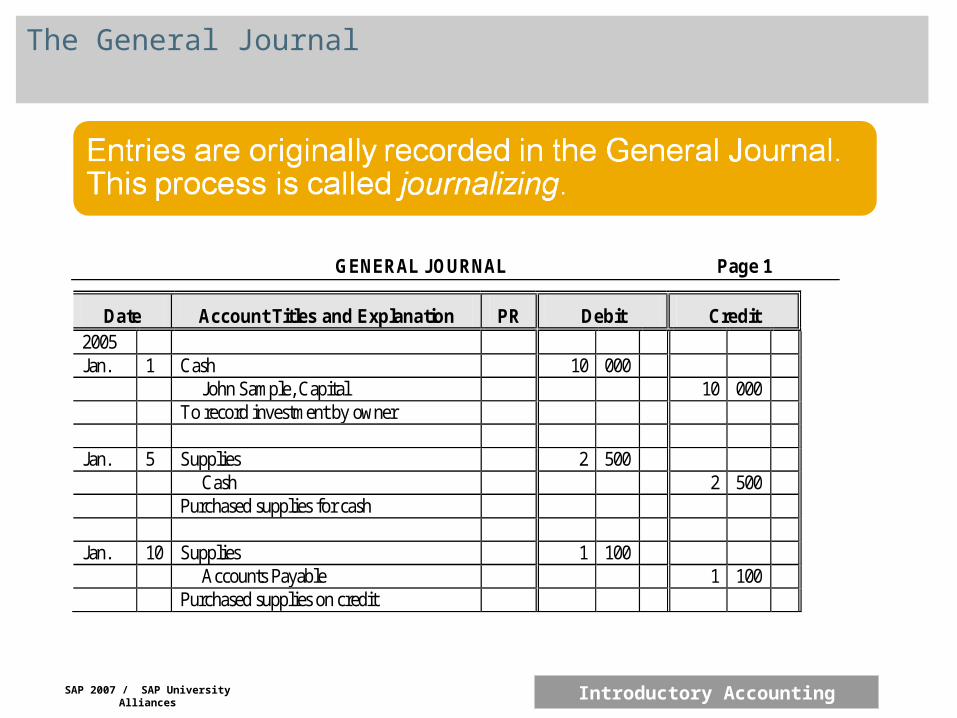

The General Journal

GENERAL JOURNAL Page 1

Date Account Titles and Explanation PR Debit Credit 2005 Jan. 1 Cash 10 000 John Sample, Capital 10 000 To record investment by owner Jan. 5 Supplies 2 500 Cash 2 500 Purchased supplies for cash Jan. 10 Supplies 1 100 Accounts Payable 1 100 Purchased supplies on credit

SAP 2007 / SAP University Alliances Introductory Accounting

Posting Journal Entries

SAP 2007 / SAP University Alliances Introductory Accounting

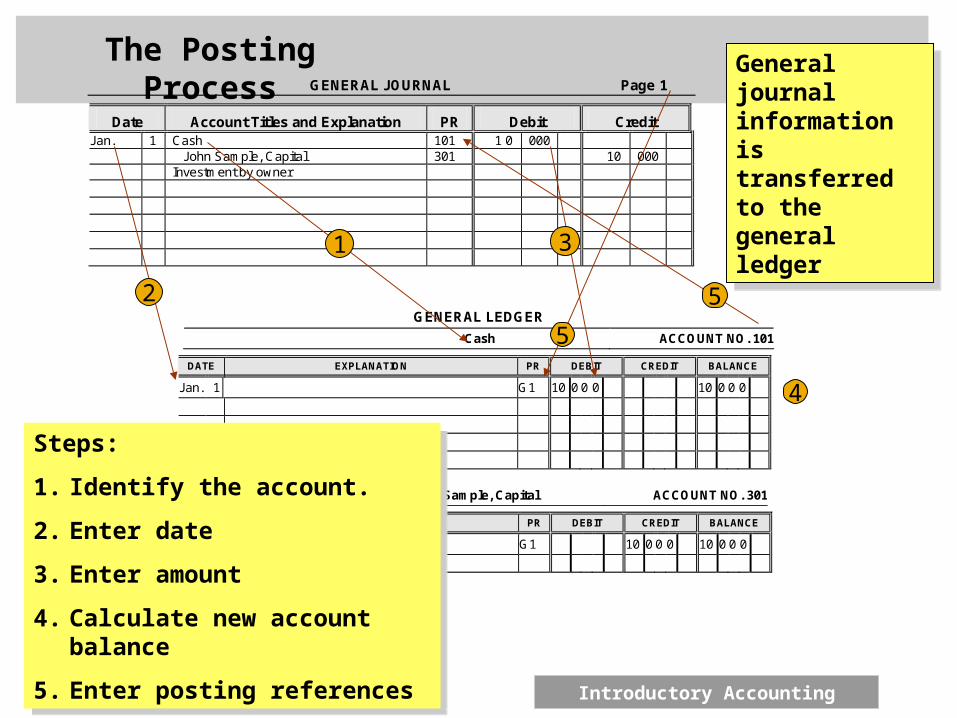

GENERAL JOURNAL Page 1

Date Account Titles and Explanation PR Debit Credit Jan. 1 Cash 101 1 0 000 John Sample, Capital 301 10 000 Investment by owner

GENERAL LEDGER

Cash ACCOUNT NO. 101

DATE EXPLANATION PR DEBIT CREDIT BALANCE

Jan. 1 G1 10 0 0 0 10 0 0 0

John Sample, Capital ACCOUNT NO. 301

DATE EXPLANATION PR DEBIT CREDIT BALANCE

Jan . 1 G1 10 0 0 0 10 0 0 0

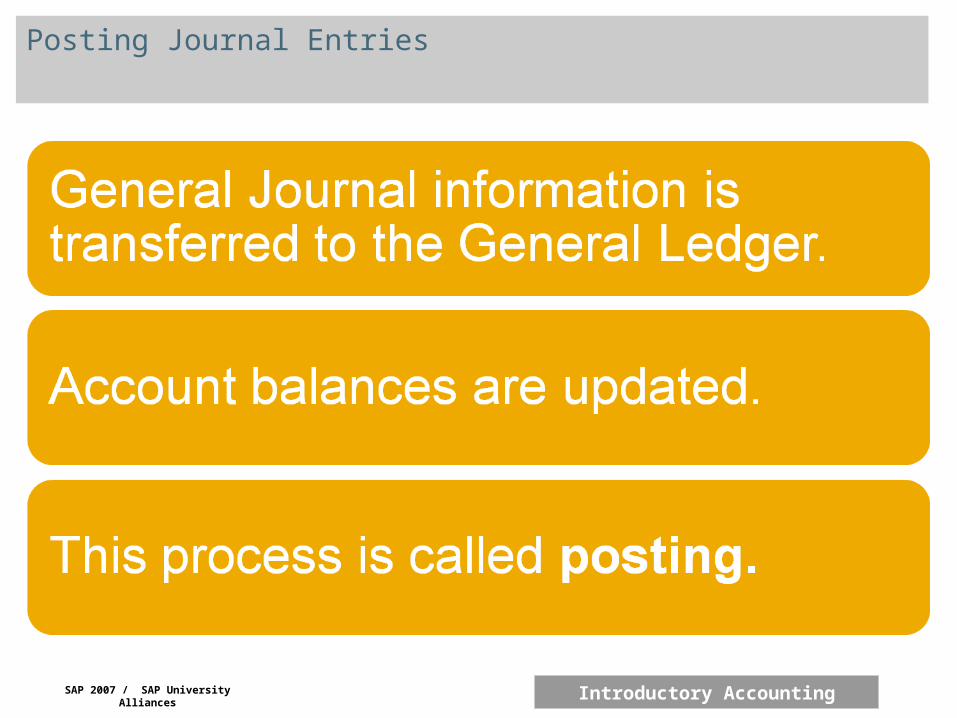

General journal information is transferred to the general ledger

General journal information is transferred to the general ledger

The Posting Process

Steps:

1. Identify the account.

2. Enter date

3. Enter amount

4. Calculate new account balance

5. Enter posting references

Steps:

1. Identify the account.

2. Enter date

3. Enter amount

4. Calculate new account balance

5. Enter posting references

2

1 3

4

5

5

SAP 2007 / SAP University Alliances Introductory Accounting

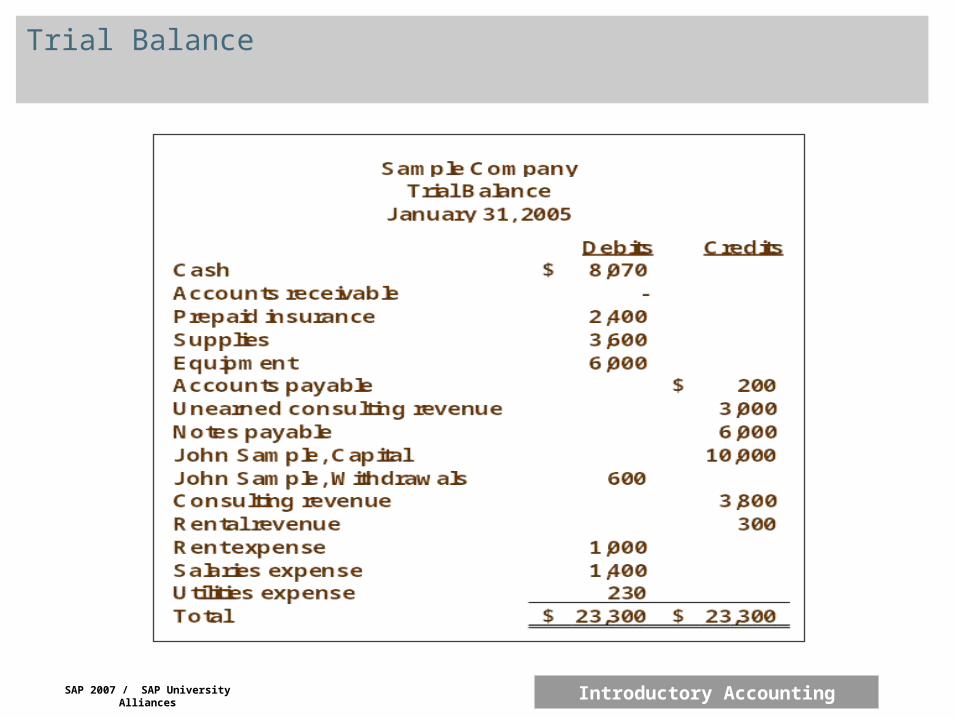

Trial Balance

SAP 2007 / SAP University Alliances Introductory Accounting

Trial Balance