Embed Size (px)

Citation preview

12

CHAPTER 2

THEORITICAL FOUNDATION

2.1 Auditing

2.1.1. Nature of audit

Audit definition based on Arens, et al (2006):

“Auditing is the accumulation and evaluation of evidence about information to

determine and report on the degree of correspondence between the information

and establish criteria. Auditing should be done by a competent, independent

person.”

Audit definition based on Konrath (2002):

“Auditing defined as a systematic process of objectively obtaining and

evaluating evidence regarding assertions about economics actions and events to

ascertain the degree of correspondence between those assertions and established

criteria and communicating the results to interested users.”

Based on above statements, we can conclude that audit form of systematic process

implemented by competent and independent person, to gather and evaluate the evidence

objectively in order to determine the level of concordance between the information with

predetermined criteria, and report the results to the management.

13

2.1.2. Purpose of Audit

Purpose of audit listed on SAS 1 (AU 110) cited by Arens, et al (2006):

“The objective of the ordinary audit of financial statement by the independent

auditor is the expression of an opinion on the fairness with which they present

fairly, in all material aspects, financial position, results of operations, and its

cash flows in conformity with generally accepted accounting principles.”

On statement above, purpose of audit can be defined as an assessment in a form of audit

report. Purpose of audit used as standardized plan for auditor in gathering evidence to

state an adequate operation in Clients Company, then based on these evidence, auditor

can perform an audit report.

Purpose of audit set by an auditor expected to correspond with management assertions,

the management's statement regarding the type of transaction and associated estimation

in the financial statements. Auditing purposes become a basic framework for collecting

material of competent evidence.

According to Arens, et al (2006), there is some purpose of audit which have to be

completed before auditor conclude that several transaction or operation that have been

recorded correctly, this purpose called Transaction Related Audit Objectives (TRAO),

while purpose of audit which have to be completed for each account balance called

Balance Related Audit Objective (BRAO).

14

2.1.3. Types of Audit

Types of audit according to Arens,et al (2006)

1. Operational Auditing

Operational audit also known as management audit. Examination conducted to

evaluate the efficiency and effectiveness of procedures and methods of operation of

an organization. Operational audits more like management consulting. At the end of

the audit, the auditor will make recommendations to management to improve

operations.

2. Compliance Audit

Compliance audit is an examination conducted to determine whether the client has

followed the procedures and rules set by the authorities. Compliance audit results are

usually reported to a particular party in the company, to assess the extent to which

compliance has been made.

3. Financial Statement Audit

Financial statement audit is an examination of the financial statements of an

enterprise, to determine whether the financial statements have been prepared in

accordance with the criteria established. Criteria normally used are the Generally

Accepted Accounting Principles (GAAP), while in Indonesia the criteria used is the

Standar Akutansi keuangan (SAK).

15

Audit of financial statements includes the examination of the balance sheet, income

statement, statement of cash flows, and notes to financial statements. The results of

this examination are audit report, which contains the auditor's opinion regarding the

fairness of the financial statements.

2.1.4. Audit Evidence

According to arens, et al (2008) there is seven types of audit evidence:

1. Physical Examination

Physical examination is the inspection or count by the auditor of a tangible asset.

Count a sample of inventory and compare quantity and description to client’s counts.

2. Confirmation

Confirmation describes the receipt of a written or oral response from an independent

third party verifying the accuracy of information that was requested by the auditor.

3. Documentation

Documentation is the auditor’s inspection of the client’s documents and records to

substiante the information that is, or should be, included in the financial statements.

Compare quantity on client’s perpetual records to quantity on client’s counts.

4. Analytical procedures

Analytical procedures use comparisons and relationship to asses whether account

balances or other data appear reasonable compared to the auditor’s expectations.

16

5. Inquiries of the client

Inquiry is the obtaining of written or oral information from the client in response to

questions from the auditor.

6. Recalculation

Recalculation involves rechecking a sample of calculations made by the client.

Rechecking client calculations consists of testing the client’s arithmetical accuracy

and procedures.

7. Reperformance

Is the auditor’s independent tests of client accounting procedures or controls that

were originally done as part of the entity’s accounting and internal control system.

Whereas recalculation involves rechecking a computation, reperformance involves

checking other procedures.

8. Observation

Observation is the use of the senses to assess client activities. Throughout the

engagement with a client, auditors have many opportunities to use their senses.

17

2.1.5. Audit Phase

According to Arens, et al (2006), there are four phase in audit process:

1. Plan and design audit approach

Information obtained during client acceptance and initial planning; understand the

business and clients industry, client’s business risk assessments and early

implementation of analytical procedures to determine the inherent risk and

acceptable audit risk. Assessment of materiality, acceptable audit risk, inherent risk,

and control risk is used to develop a plan and audit program as a whole.

2. Perform test of control and substantive test of transaction

Purpose of this phase are (1) to obtain material evidence supporting the procedures

and control policies that contribute to the risk controls that have been set by the

auditor (with a test of control) and (2) to obtain material evidence supporting the

truth of the monetary and the number of transactions (by performing substantive

tests of transactions).

3. Perform analytical procedures and test of detail of balances.

The purpose of this phase is to get additional evidence, analytical procedure is a

procedure used to qualify overall operation of transaction and account balance. Test

of detail balances is specific procedure which used to qualify account balance in

financial statement.

18

4. Complete the audit and issue an audit report.

Next step after finishing all the procedure of each purpose of audit and each account

in financial statement, auditor needs to combine information that used for prepare

audit report 1) reviewing contingent liabilities 2) over viewing subsequent event 3)

gathering evidence 4) publish audit report 5) communicate the result with audit

committee and management.

2.1.6. Audit Risk

Auditor gives reasonable assurance, which means there are risks that related to audited

subjects.

Definition of audit risk according to Arens, et al (2006):

“The risk that auditor will conclude that the financial statements are fairly stated

and on unqualified opinion can be issued when, in fact, they are materially

misstated.”

2.1.7. Audit Program

The audit program is bridge between preliminary survey and the field work. In the

preliminary survey internal auditor identify operating objectives, risks, operating

conditions, and controls. In the field work, auditor should gather evidence according to

effectiveness of control system, the efficiency of operations, the accomplishment of

objectives, and the effects of risks on the enterprise.

19

According to sawyer (1996) criteria of audit programs are identified as follows:

• The objectives of the operation under review should be stated carefully and

agreed to by the auditee.

• Programs should be tailor made to the audit assignment unless compelling

reasons dictate otherwise.

• Each programmed work step should show the reason behind it, i.e., the objective

of the operation and the controls to be tested.

• Work steps should include positive instructions.

• Whenever practicable, the audit program should indicate the relative priority of

the work steps.

• Audit programs should be flexible and permit the use of initiative and sound

judgment in deviating from prescribed procedures or extending the work done.

• Programs should not be cluttered with material from sources readily available to

the staff.

• Unnecessary information should be avoided.

• Audit programs should bear evidence of supervisory approval before they are

carried out.

• When the auditee management asks the auditor to perform certain tests, these

should be included in the audit program if the audit budgets permits.

20

This data will be gathered in the form of Standard Audit Programme Guides

(SAPG). SAPG provide detailed guidance and direction during projects and field

visits. SAPG define the key and essential knowledge about a given subject used in

audit documentation.

According to chambers (1997), SAPG divided to three distinctions:

• A title page

• The risk/ control issues

• System interfaces

To calculate the effectiveness of the activity, the auditor use standard formula from

Badan Pengawasan Keuangan dan Pembangunan (BPKP) (2001)

2.2. Internal Auditing

2.2.1. The nature of internal auditing

Modern internal auditing evolved from essentially accounting oriented craft to a

management oriented profession. Before, internal auditing assessing more on financial

matters, but today auditing provides series that include examination and appraisal of

both control and performance issue of private or public organization. Internal auditor’s

across the world practicing different auditing work differently, based on audit scope they

21

are try to reach or what they rely in to. Is it true that different names have been given to

the function of internal auditing, for example; operational auditing, performance

auditing, program auditing, results auditing, comprehensive auditing, and management

oriented auditing.

Yet, when all is said and done, the forms of audits practiced today fall into three

fundamental approaches. Based on Lawrence B. Sawyer (1996) internal auditing

practices, they are:

• Financial. The analysis of the economic activity of an entity as measured and

reported by accounting methods

• Compliance. The review of both financial and operating controls and

transactions to see how well they conform with established laws, standards,

regulations, and procedures.

• Operational. The comprehensive review of the varied functions within the

enterprise to appraise the efficiency and economy of operations and the

effectiveness with which those functions achieve their objectives.

2.2.2. Internal auditor and External auditor

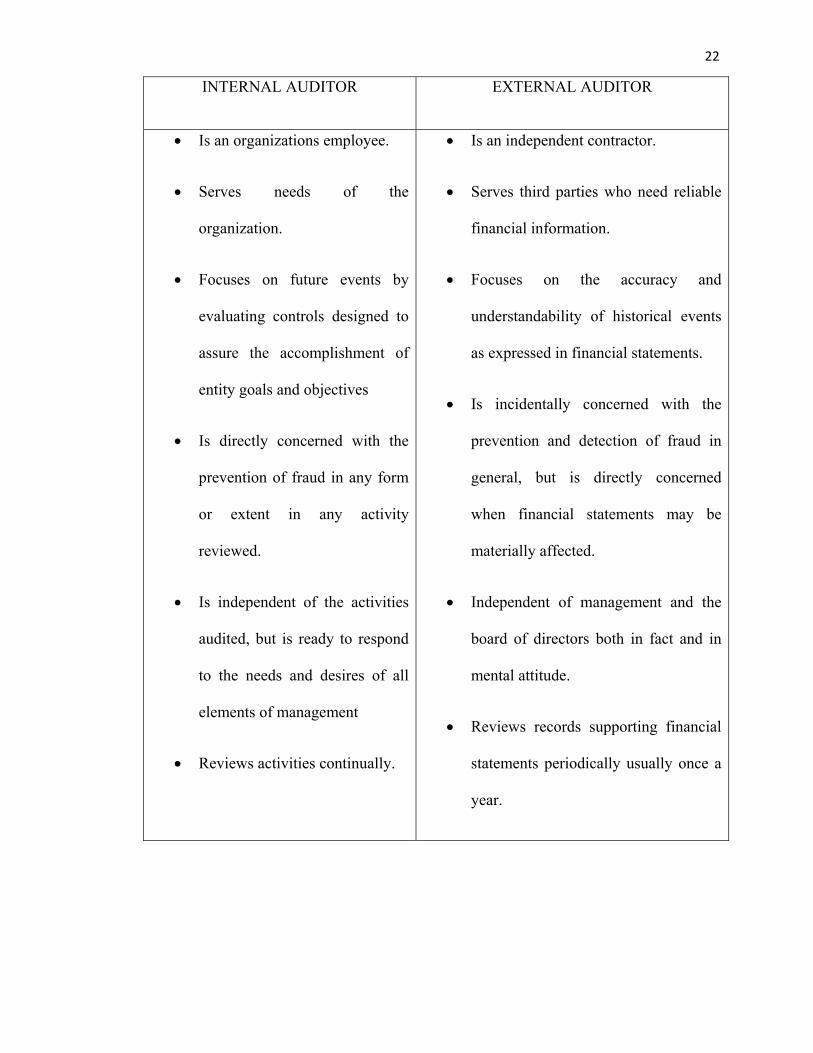

• Internal auditor and external auditor represent two distinct professions.

According to Sawyer (1996) internal auditing practices, the difference between

internal and external auditor are:

22

INTERNAL AUDITOR EXTERNAL AUDITOR

• Is an organizations employee.

• Serves needs of the

organization.

• Focuses on future events by

evaluating controls designed to

assure the accomplishment of

entity goals and objectives

• Is directly concerned with the

prevention of fraud in any form

or extent in any activity

reviewed.

• Is independent of the activities

audited, but is ready to respond

to the needs and desires of all

elements of management

• Reviews activities continually.

• Is an independent contractor.

• Serves third parties who need reliable

financial information.

• Focuses on the accuracy and

understandability of historical events

as expressed in financial statements.

• Is incidentally concerned with the

prevention and detection of fraud in

general, but is directly concerned

when financial statements may be

materially affected.

• Independent of management and the

board of directors both in fact and in

mental attitude.

• Reviews records supporting financial

statements periodically usually once a

year.

23

2.2.3. Fraud risk assessment by internal auditing

According to Schneider (2010) noted by the Treadway Commission (1987), internal

auditor can easily detect fraud with process and procedure of internal auditing, these

enable them to access organizational fraud effectively. This claim has been supported by

several KPMG surveys which indicate that internal auditors are more likely to uncover

fraud than external auditors (KPMG, 2003). Whereas 65% of frauds were discovered in

2003 by internal auditors, only 12% were discovered by external auditors (KPMG,

2003). This is because internal auditors may give greater exposure to the operation

inside the company or internal auditing work typically over external audit work.

(Church, McMillan, & Schneider, 1998). SAS No. 99, Consideration of Fraud in a

Financial Statement Audit, acknowledges the important role of internal auditors by

requiring external auditors to: ‘‘inquire of appropriate internal audit personnel about

their views about the risks of fraud, whether they have performed any procedures to

identify or detect fraud during the year, whether management has satisfactorily

responded to any findings resulting from these procedures, and whether the internal

auditors have knowledge of any fraud or suspected fraud (AICPA, 2002, AU § 316.23).”

This SAS No. 99 requirement

24

2.3. Operational Audit

2.3.1. Definitions of operational audit

Term “operational auditing” may reflect to several pictures for internal auditing. Audit

of operating units such as factories, subsidiary companies, overseas operations. Which

make it limited for some accounting or financial controls or it may give bigger picture.

Institute of internal auditors’ publication defines operational auditing as:

“A systematic process of evaluating an organization’s effectiveness, effeciency, and

economy of operations under management’s control and reporting to appropriate

persons the results of the evaluation along with recommendations for improvement”

(Gill and Cosserat 1996, P.809)

Audit of accounting and financial perspective in the functional areas of the business, it is

different from audit in financial and accounting area, these functional area might be

marketing, sales, distribution, production, and etc, which based on the business nature

itself. Operational audit stressed on the internal audit that reviews all the operating area

in the business.

Bussiness audit such as operating, functional, department of accounting, treasury, etc.

The objective of the activity is to review the effectiveness and efficiency also the

economical way to achieve the management objectives. The operational auditing may go

over the internal control issues.

25

The categorization of operational audit in the business sector may fall to these areas:

1. Management and administration

2. Financial and accounting

3. Personnel

4. Procurement

5. Stock and materials handlings

6. Production and manufacturing

7. Marketing and sales

8. After sales support

9. Research and development

10. Information technology

26

2.3.2. Objectives of operational audit

Pany and whittington (1997, p.770) states several objectives of operational audit:

1. To assess the unit’s performance in relation to management’s objectives or other

appropriate criteria.

2. To assure that its plan (as described in statements of objectives, programs,

budgets, and defectiveness) are comprehensive, reliable, and understandable at

the operating levels.

3. To provide information on weaknesses in operating controls, principally as to

possible sources of waste.

4. To reassure that all operating reports can be relied on as basis for action.

2.3.3. Differences between operational auditing and financial auditing

According to D. C. Lane (1983), the main differences between financial audit and

internal audit, the operational audit has a much wider time horizon. Financial audit

focused on historical data, operational audit looks at the present and medium term-

future. Operational audit provide reliable forecasts and judgments about changes and

developments in industrial and technological environments. The operational auditors

verify the validity of forecasting and planning.

27

Arens et al. (2003, p738) states three main differences between operational and financial

audit.

1. Purpose of audit

Financial audit underlines the fair presentation of financial statement, whereas

operational audit underlines on effectiveness and efficiency. In addition, financial

audit concern with historical financial information, whereas operational audit

concern with operating performance for the future.

2. Distribution of the report

Financial audit report is normally intended for public use, such as shareholders,

investors, creditors, bank, governments, etc. Operational audit report, on the other

hand, is primarily intended for internal user, which is management.

3. Inclusion of non-financial areas

Operational audit covers any aspect of efficiency and effectiveness in an

organization. Hence, operational audit can involve a wide variety of activities. On

the contrary, financial audit are limited to materials that directly affect the fairness of

financial statement presentations.

28

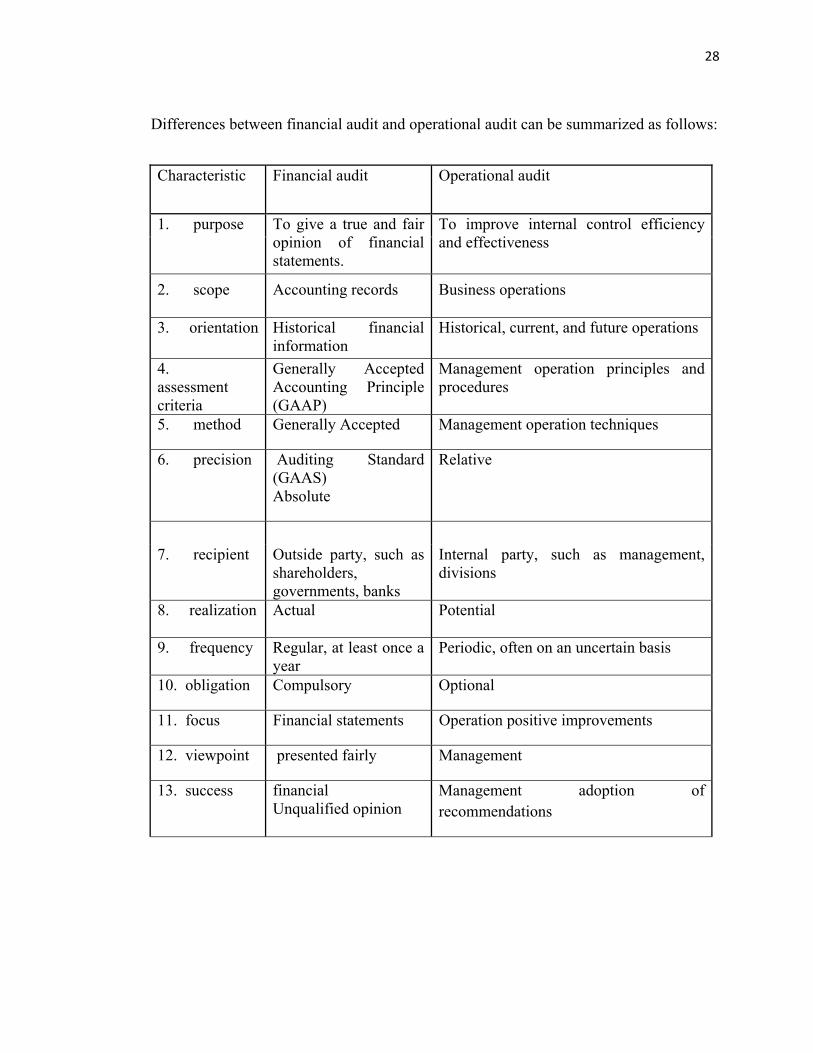

Differences between financial audit and operational audit can be summarized as follows:

Characteristic Financial audit Operational audit

1. purpose To give a true and fair opinion of financial statements.

To improve internal control efficiency and effectiveness

2. scope Accounting records Business operations

3. orientation Historical financial information

Historical, current, and future operations

4. assessment criteria

Generally Accepted Accounting Principle (GAAP)

Management operation principles and procedures

5. method Generally Accepted Management operation techniques

6. precision Auditing Standard (GAAS) Absolute

Relative

7. recipient Outside party, such as

shareholders, governments, banks

Internal party, such as management, divisions

8. realization Actual Potential

9. frequency Regular, at least once a year

Periodic, often on an uncertain basis

10. obligation Compulsory Optional

11. focus Financial statements Operation positive improvements

12. viewpoint presented fairly Management

13. success financial Unqualified opinion

Management adoption of recommendations

29

2.3.4. Scope of operational auditing

The breakdown of the organization into set of separate audit reviews could be said to

form the audit universe of potential audit projects. The activities require coordination

between number of department or function. For example, the development of new

product may involve the marketing, accounting and research function. Each organization

may differ in audit function. According to chambers (1997) operational auditing

handbook scope of operational auditing divide as follows:

Management and administration:

• the control environment

• organization (i.e. structure)

• management information

• planning

• risk management

• legal department

• quality management

• estates management and facilities

• environmental issues

• insurance

• security

30

• capital projects

• industry regulation and compliance

• media, public and external relations

• company secretarial department

Financial and accounting:

• treasury

• payroll

• accounts payable

• accounts receivable

• general ledger/ management accounts

• fixed asset (and capital charges)

• budgeting and monitoring

• bank accounts and banking arrangements

• sales tax (i.e. VAT) accounting

• taxation

• inventories

• product/project accounting

• petty cash and expenses

• financial information and reporting

• investment

31

Personnel:

• human resources department (including policies)

• recruitment

• manpower and succession planning

• staff training and development

• welfare

• pension scheme (and other benefits)

• health insurance

• staff appraisal and disciplinary matters

• health and safety

• labor relations

• company vehicles

Procurement:

• purchasing

• contracting

Stock and materials handling:

• stock control

• warehousing and storage

• distribution, transport and logistics

32

Production/manufacturing:

• planning and production control

• facilities, plant, and equipment

• personnel

• materials and energy

• quality control

• safety

• environmental issues

• law and regulatory compliance

• maintenance

Marketing and sales:

• product development

• market research

• promotion and advertising

• pricing and discount policies

• sales management

• sales performance and monitoring

• distribution

• relationship with parent company (for overseas of subsidiary operations)

• agents

• order processing

33

After sales support:

• warranty arrangements

• maintenance and servicing

• spare parts and supply

Research and Development:

• product development

• project appraisal and monitoring

• plant and equipment

• development project management

• legal and regulatory issues

Information Technology:

• IT strategic planning

• IT organization

• IT sites

• Processing operations

• Back-up and media

• Systems/operating software

• System access control

• Personal computers

• Software maintenance

• Local area networks

• Databases

34

• Data protection

• Facilities management

• System development

• Software selection

• Contingency planning

• Electronic data interchange

• Viruses

• Electronic office

• User support

• Spreadsheet design

• Expert system

• IT accounting

2.3.5. Operational audit variables (6 E’s)

In operational auditing according to Andrew Chambers and Graham Rand (1997), auditor must consider 3 primary variables and 3 further audit interest. These are:

• Effectiveness: “doing the right things” which is achieving entity objectives.

• Efficiency: “doing them well” choosing the appropriate system to avoid waste of input and rework.

• Economy: “doing them cheap” for instance, unit costs for labor, materials, etc. Being under control.

35

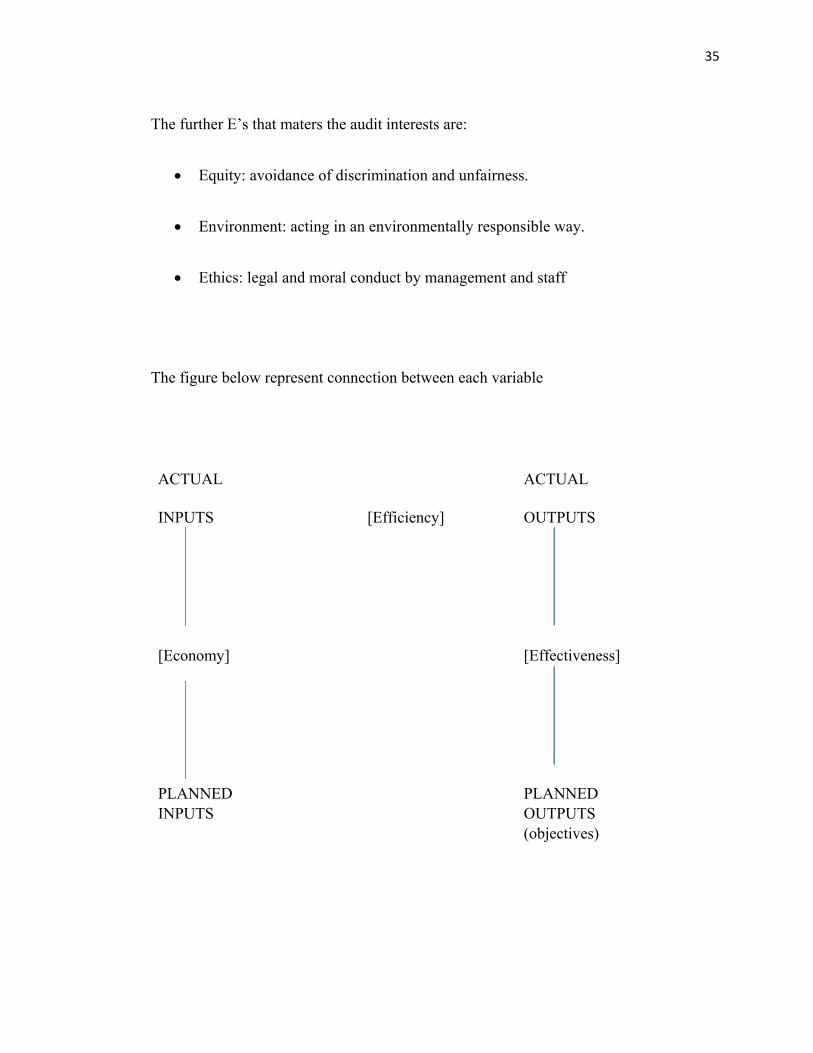

The further E’s that maters the audit interests are:

• Equity: avoidance of discrimination and unfairness.

• Environment: acting in an environmentally responsible way.

• Ethics: legal and moral conduct by management and staff

The figure below represent connection between each variable

ACTUAL ACTUAL

INPUTS [Efficiency] OUTPUTS

[Economy] [Effectiveness]

PLANNED PLANNED INPUTS OUTPUTS

(objectives)

36

2.3.6. Audit performance measure

According to Andrew Chambers and Graham Rand (1997) operational auditing

handbook, Audit performance measure categorized as follows:

• Workload/demand performance measures:

This measurement indicates the output volume, the quality and quantity of the

service or product. Such as number of users, number of units produced, percentage,

etc.

• Economy performance measures:

These may highlight waste in the provision of resources indicating that the same

resources may be provided more cheaply. Such as; cleaning cost per hour worked,

maintenance cost, cost of finance function, etc.

• Efficiency performance measures:

These may highlight potential opportunities to convert given resources to end

product with less waste. Many performance measures will point to either

uneconomic or inefficient practices. Such as; breakdown per production day, ratio of

actual input and actual output, accidents at work per 1000 personnel, etc.

37

• Effectiveness performance measures:

These performance measure reviews about how to achieve entity’s objectives

regardless of economy, efficiency, or equity except if they are correlated.

Effectiveness performance measuring things such as; actual output in comparison to

planned output, ration of customer complain compare to the sales, etc.

• Equity performance measures:

These performance measures draw attention to unfairness or social irresponsibility in

terms of corporate policy and practice. Such as; departmental grant per member or

staff, proportion of female employees, etc.

2.3.7. Phases of operational audit

According to Arens et al (2003) pg. 743-745, phases of operational audit are as follow:

1. Planning

Operational audit planning phase is quite similar to financial audit planning. It

involves determining the scope of the engagement, assigning proper staff to the

engagement, obtain proper understanding of the client’s business industry, obtain

information of internal control and decide on proper evidence to accumulate.

38

2. Evidence accumulation and evaluation

Operational auditors must accumulate applicable and related evidence for a

reasonable basis result in making a conclusion about the objective being tested. The

following activities involved in evidence collections are:

o Reviewing operating policies and documentation

o Confirming procedures with management and operating personnel

o Observing operating functions and activities

o Examining financial and operating plans and reports

o Testing the accuracy of operating information

o Testing controls (romney and steinbart 2003, p.342).

3. Reporting and follow up

Operational audit report is prepared for internal management, which make a

standardized wording is less necessary. However, operational audit report needs

tailor-made report addressing the scope of audit, findings, and recommendation are

made to the management. This is to determine whether recommendation is

applicable or not.

39

2.3.8. Types of operational audit

1. Functional auditing

Functional audit deals with one or more functions in an organization, for example

effectivness and efficiency of payroll department for the company as a whole.

2. Organizational audit

An operational audit of an organization deals with an entire organizational unit, such

as department, branch or subsdiary. An organizational audit emphasizes on how

efficiently and effectively functions interact.

3. Special assignments

Special assignments in operational audit depend on the request of management for

kinds of audit, such as determining the ineffectiveness of the IT system, etc.

2.3.9. Relation of internal auditing and operational auditing

According to Mark Penno (1990) the scope of internal audit department typically

extends beyond financial reporting. The internal audit also performs operational (or

management) auditing. Operational auditing is not constrained by the limited

informational requirements of financial reporting and considers a much wider variety

of information than does a financial audit. The operational audit fills the gap

between the economic organizations informational requirements. Operational audit

40

or management audit fulfill the gap between financial requirements needed by

internal auditing. Operational auditing also eliminates data manipulation which

becomes important requirements in internal auditing.

2.3.10. Auditing operations and resource management.

Auditing operations and resource management is the operational auditing dimensions of

production and manufacturing as being representative of operations in general.

According to Andrew Chambers and Graham Rand (1997) operational auditing

handbook, they normally involve the following aspects:

• Identifying an underlying requirement and endeavoring to cost effectively exploit

it

• Ensuring that suitable and adequate resources (human and material) are brought

together at the right time and place to fulfill the identified requirements.

• Ensuring that the operation is conducted safely, economically, efficiently,

effectively, to the required standard, and in accordance with any prevailing

regulations and laws; and so on.

41

System/function components of a production/manufacturing environment:

• planning and production control

• facilities, plant, and equipment

• personnel

• materials and energy

• quality control

• safety

• environmental issues

• law and regulatory compliance

• maintenance

2.4 Internal Control

2.4.1. Definition of internal control

According to Arens et al (2003, p.274) , a system of internal control consist of policies

and procedures designed to provide management with reasonable assurance that the

company achieves its objectives and goals.

The Auditing Methods Committee of the American Institute of Certified Public

Accountants (AICPA) defined the internal control as being involve the organizational

plan, coordination methods, measures followed to protect the assts, checking, and

reviewing accounting data check their accuracy, dependability, increase productive

efficiency, and encourage employee's adoption of established management policies.

42

According to Al-Qudah(2011), The essential goals of internal control that can be

deduced from the earlier definitions include :

• First: authorities, powers and responsibilities of an organization, clearly state the

existence of organizational structure in the organization which important for

achieving internal control that supported by structured organizational

components.

• Second: provide protection of company’s assets from fraudulent manipulations.

• Third: accurate accounting information needed for overall company’s operations

and processes that become a subject of internal control.

• Fourth: Encouraging compliance with policies, regulations, and administrative

instructions in organization.

2.4.2. Internal control components

The COSO concept of internal control includes five components of internal control.

They are:

1. The control environment

The control environment consists of actions, policies, and procedures that expose the

overall position of top management concerning the extent of internal control importance.

Several factors that contribute to the control environment are:

o Integrity and ethical values

o Commitment to competence

43

o Board of directors or audit committee participation

o Management’s philosophy and operating style

o Organizational structure

o Assignment of authority and responsibility

o Human resources policies and practices

2. Risk assessment

Risk assessment is management’s identification and analysis of risks in relation to

the preparation of financial statements in conformity with GAAP. Factors that may

increase risk include failure to meet prior objectives, quality of personnel, company

operations, geographic scatter, significance and complexity of core business

processes, introduction of new system, and entrance of new competitors.

3. Control activities

Control activities are policies and procedures that are intended to ensure that actions

are taken to address risks in an attempt to achieve the entity’s objectives. Control

activities closely relate to policies and procedures that concern:

o Adequate segregation of duties

o Proper authorization of transactions and activities

o Adequate documents and records

44

o Physical control over assets and records

o Independent checks on performance

4. Information and communication

The rationale behind information and communication is to initiate, record, process, and

report the entity’s transactions as well as to preserve accountability for the related assets.

This is typically achieved and documented by narrative description of the system or by a

flowchart.

5. Monitoring

Monitoring activity cope with continuing or regular assessment of the quality of internal

control by management in an attempt to determine that controls are operating as

intended. Information for assessment and modification comes from a range of sources,

including internal auditor reports, evaluation of the current internal control, feedback

from operating personnel, reports by regulators and complaints from customers.

2.4.3. General characteristic of good internal control structure

Gay and Simnett (2000, p.305) present general characteristics of a good internal control

structure:

1. There should be proper segregation of duties. There should be no incompatible

functions, so that no person has a chance to commit or cover irregularities in the

normal course of duties.

45

2. The internal control structure should have a system of authorization, recording,

and custodianship procedures sufficient enough to provide accounting control of

assets, liabilities, revenues and expenses.

3. There should be reliable business practices in performance of duties and

functions by each department.

4. Internal control should ensure that persons have qualifications corresponding to

their responsibilities.

2.4.4. Relationship between internal control and operational auditing

Fadzil et al. (2005) as cited by Agbejule (2007) state that the primary concern of

organization internal control system are providing administrative management along

with reasonable assurances that financial information is accurate and reliable:

organization must concern about plans, procedures, policies, laws, regulation and

contract; assets are safeguarded against loss and theft; resources are used economically

and efficiently; and established objectives and goals for operations or programs can be

met. The following three internal control objectives can be found in the COSO

framework:

(1) Effectiveness and efficiency of activities;

(2) Reliability of financial information; and

(3) Compliance with applicable laws and regulations.

Obviously, the first of these three clients concerns directly relate to operational auditing,

but the other two also effect the efficiency and effectiveness.

46

Purpose of operational auditing of internal control is to evaluate efficiency and

effectiveness and to make recommendations to management. In contrast, internal control

evaluation for financial auditing has two primary purposes: to determine the extent of

substantive audit testing required and to report on the effectiveness of internal control

over financial reporting for public companies.

The scope of operational auditing concerns any control that related to efficiency

and effectiveness, while the scope of internal control evaluation for financial audit is

restricted to the effectiveness of internal control over financial reporting and its effect in

the fair presentation of financial statements.