Embed Size (px)

Citation preview

BIBLIOGRAPHY Bisnis Indonesia, [Online], http://web.bisnis.com, [2008]

Bahana Research products, 2007, Bahana securities

Bahana Research products, 2008, Bahana securities

Policy, Pearson educational Inc, New Jersey

PT Wijaya Karya, [Online], http://www.wika.co.id, [2008, Dec]

Wheeler, Thomas and Hunger, David, 2006, Strategic Management and Business

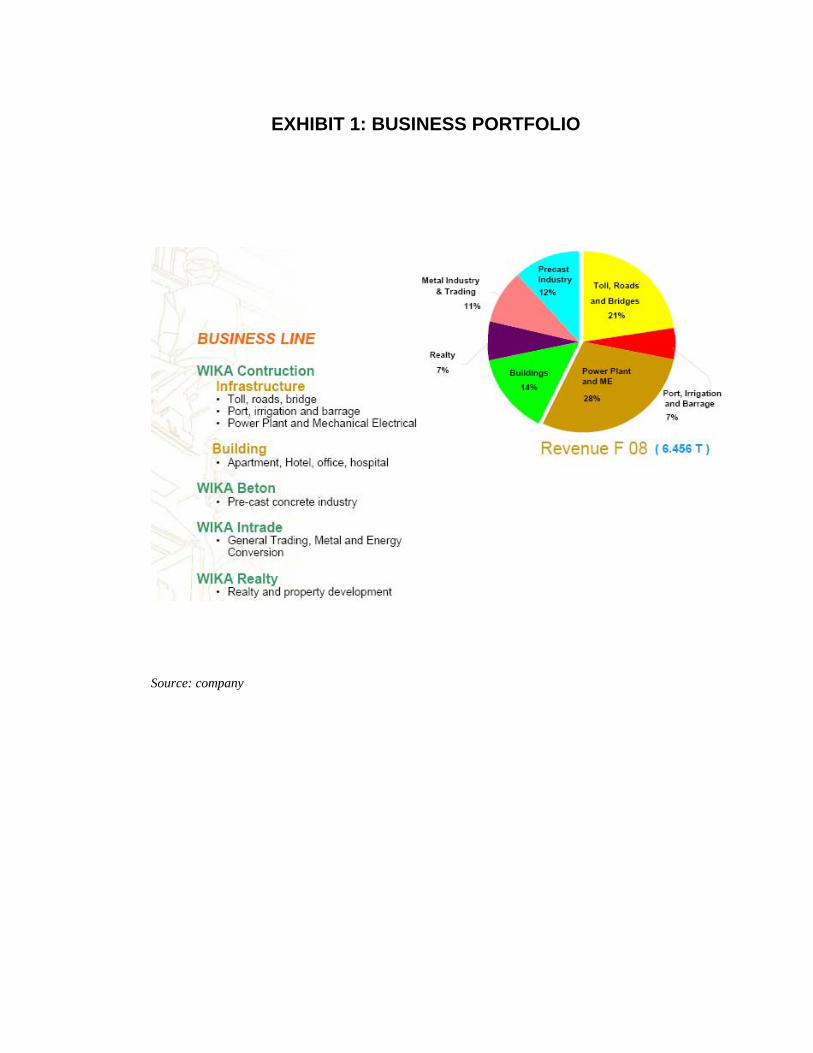

EXHIBIT 1: BUSINESS PORTFOLIO

Source: company

EXHIBIT 2: MANAGEMENT & ORGANIZATION STRUCTURE

Management

Commissioner President Commissioner : Ir. Junius Saringar Ulibasa Hutabarat Commissioner : DR. Budi Suradji Commissioner : Pontas Tambunan, SH., MM Commissioner : Roslan Zaris, SE., MSc

Director President Director : Ir. Aloysius Sutjipto, MM., MT Director of Finance : Ir. Slamet Maryono Director of Operation I : Ir. Sutedjo Wirokusumo, MM Director of Operation II : Ir. Djokomulyono, MM Direktur of Human Capital : Ir. Tonny Warsono Hardjo, MM

Source: company

Organization Structure

Source: company

EXHIBIT 3: OUTLOOK

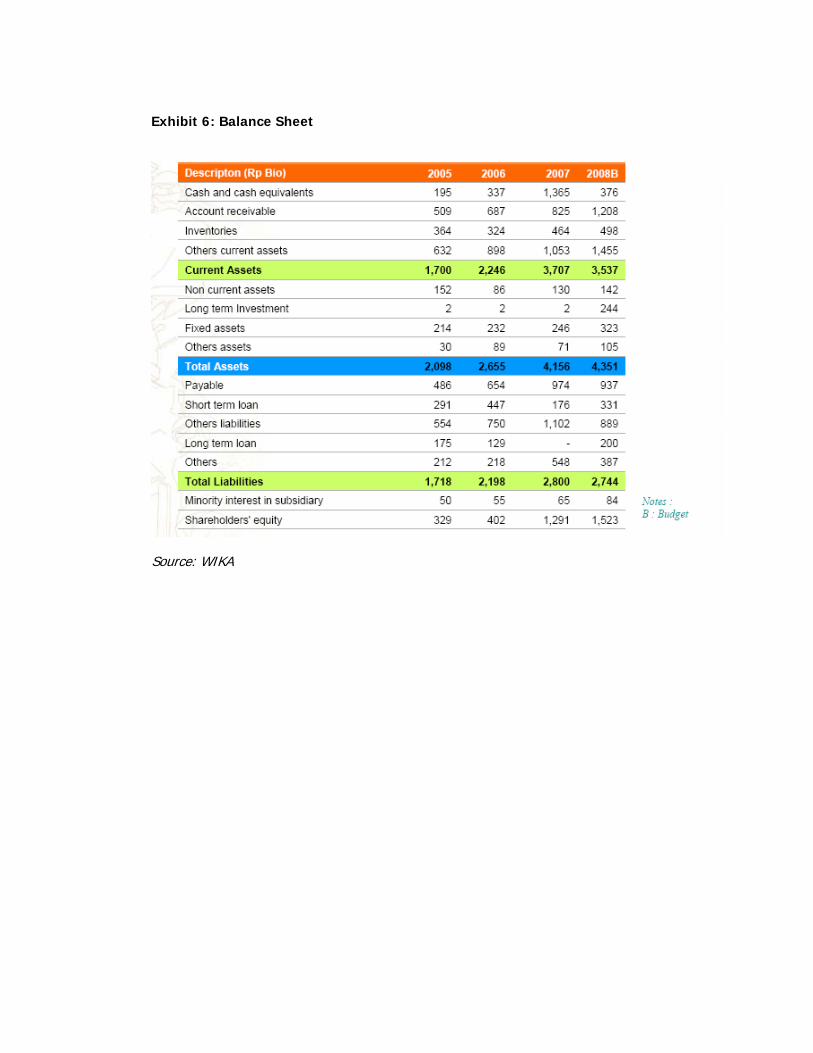

EXHIBIT 4: BALANCE SHEET

Source: company

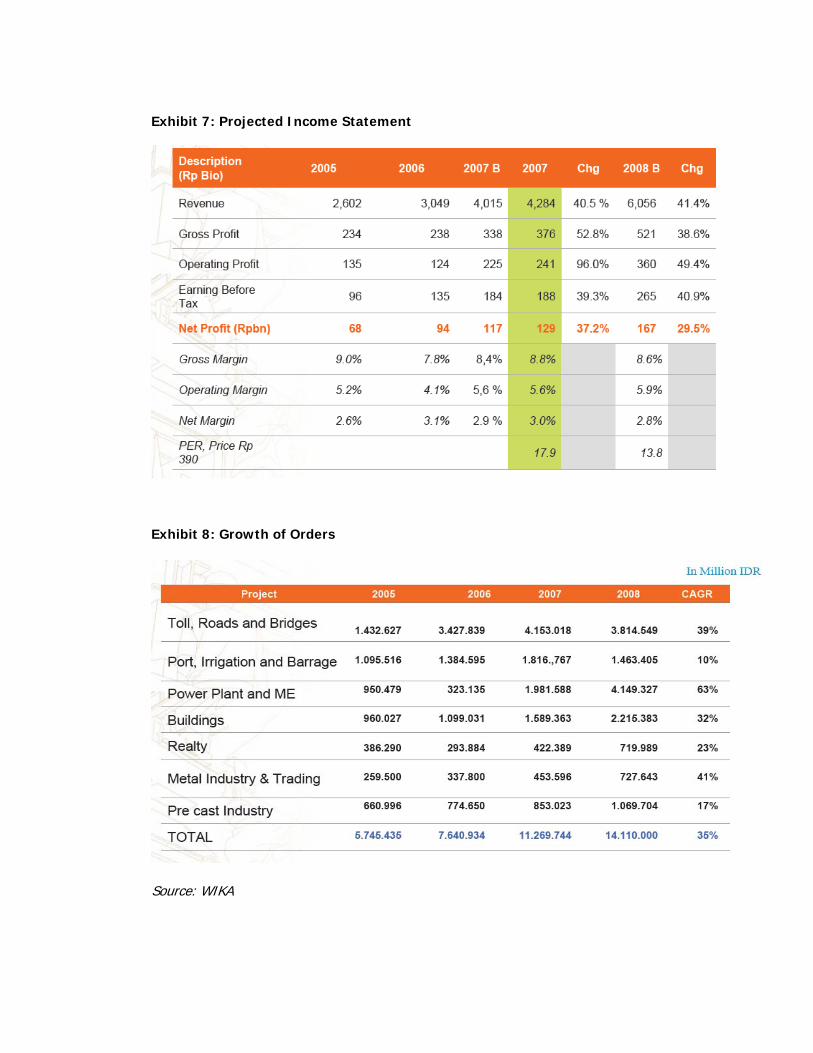

EXHIBIT 5: PROJECTED INCOME STATEMENT

EXHIBIT 6: GROWTH OF ORDERS

Source: company

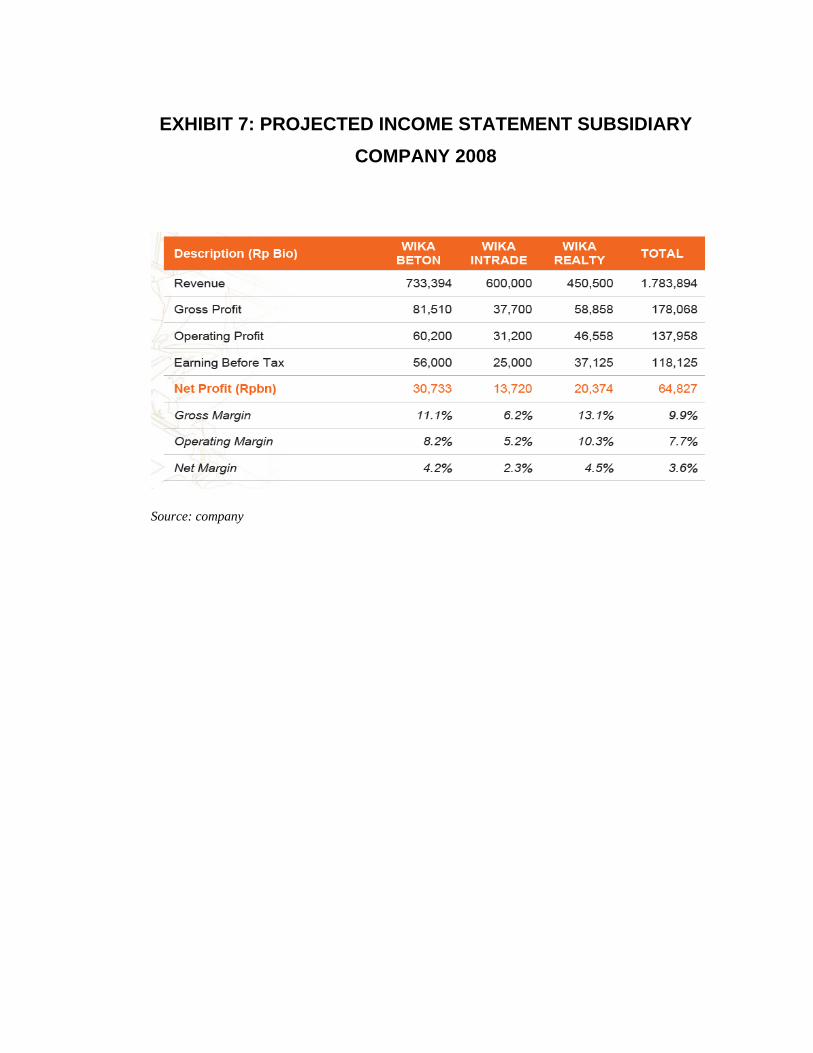

EXHIBIT 7: PROJECTED INCOME STATEMENT SUBSIDIARY COMPANY 2008

Source: company

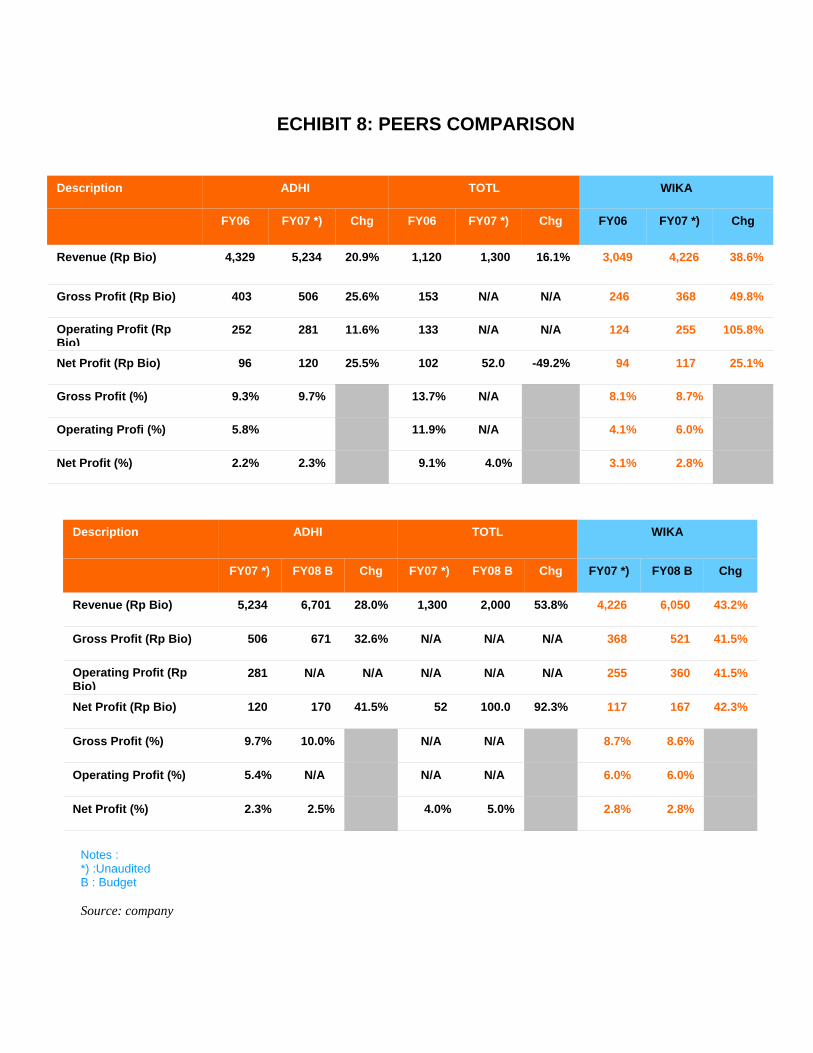

ECHIBIT 8: PEERS COMPARISON

Notes : *) :Unaudited B : Budget Source: company

Description ADHI TOTL WIKA

FY07 *) FY08 B Chg FY07 *) FY08 B Chg FY07 *) FY08 B Chg

Revenue (Rp Bio) 5,234 6,701 28.0% 1,300 2,000 53.8% 4,226 6,050 43.2%

Gross Profit (Rp Bio) 506 671 32.6% N/A N/A N/A 368 521 41.5%

Operating Profit (Rp Bio)

281 N/A N/A N/A N/A N/A 255 360 41.5%

Net Profit (Rp Bio) 120 170 41.5% 52 100.0 92.3% 117 167 42.3%

Gross Profit (%) 9.7% 10.0% N/A N/A 8.7% 8.6%

Operating Profit (%) 5.4% N/A N/A N/A 6.0% 6.0%

Net Profit (%) 2.3% 2.5% 4.0% 5.0% 2.8% 2.8%

Description ADHI TOTL WIKA

FY06 FY07 *) Chg FY06 FY07 *) Chg FY06 FY07 *) Chg

Revenue (Rp Bio) 4,329 5,234 20.9% 1,120 1,300 16.1% 3,049 4,226 38.6%

Gross Profit (Rp Bio) 403 506 25.6% 153 N/A N/A 246 368 49.8%

Operating Profit (Rp Bio)

252 281 11.6% 133 N/A N/A 124 255 105.8%

Net Profit (Rp Bio) 96 120 25.5% 102 52.0 -49.2% 94 117 25.1%

Gross Profit (%) 9.3% 9.7% 13.7% N/A 8.1% 8.7%

Operating Profi (%) 5.8% 11.9% N/A 4.1% 6.0%

Net Profit (%) 2.2% 2.3% 9.1% 4.0% 3.1% 2.8%

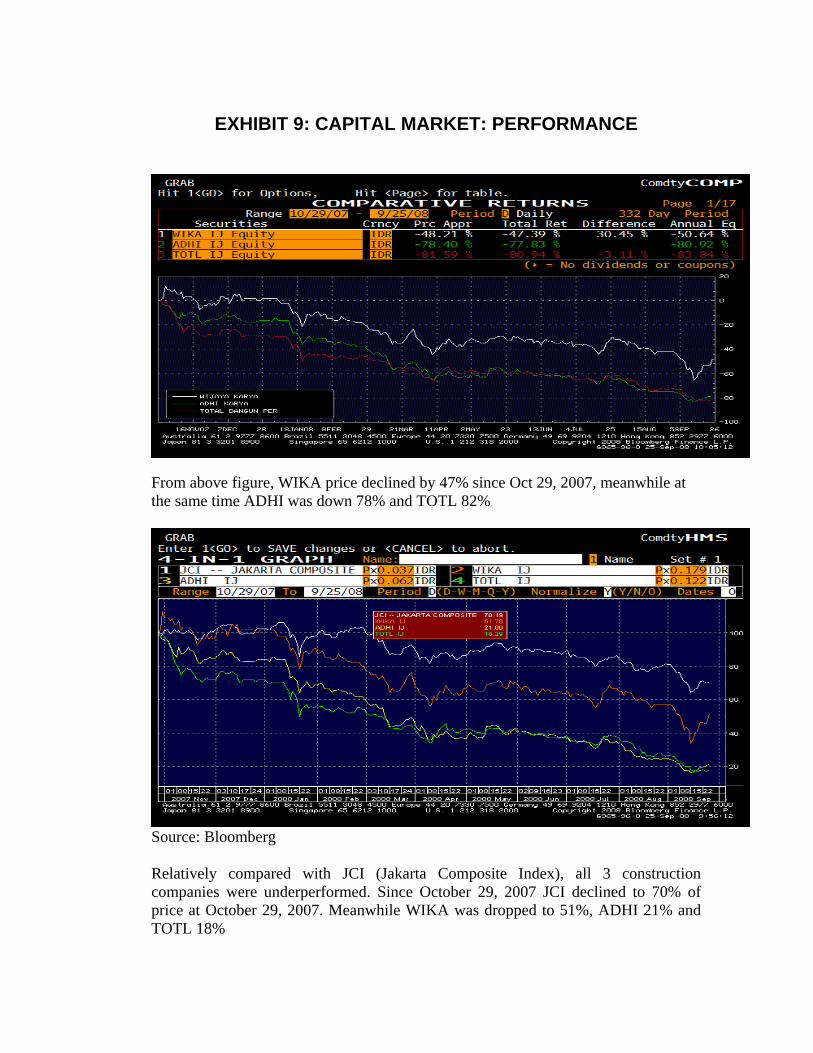

EXHIBIT 9: CAPITAL MARKET: PERFORMANCE

From above figure, WIKA price declined by 47% since Oct 29, 2007, meanwhile at the same time ADHI was down 78% and TOTL 82%

Source: Bloomberg

Relatively compared with JCI (Jakarta Composite Index), all 3 construction companies were underperformed. Since October 29, 2007 JCI declined to 70% of price at October 29, 2007. Meanwhile WIKA was dropped to 51%, ADHI 21% and TOTL 18%

ECHIBIT 10: PROJECTS

EXHIBIT 11: NEWS

EXHIBIT 12 : CASE STUDY : PT WIJAYA KARYA : DIVERSIFICATION STRATEGY

BENNY B. SOEBAGJO FIRDAUS ALAMSJAH

WIJAYA KARYA (WIKA): Diversification Strategy

About competition ” I think if we stay competing like this, it would be tough. Competition in construction-projects is getting tightened”

About new businesses “We find that WIKA’s core business is construction-services. But it doesn’t mean other businesses will be deleted. The existing businesses will be maintained to grow”

A. Sutjipto, President Director of PT Wijaya Karya. (1990 – 2008)

When the economic-crisis hit Indonesia in 1998, WIKA realized that the company must change its strategy. Target for 1998 – 2000 only for survival but for 2000 – 2004 was better performance. Sutjipto as a President Director at that time had to decide what kind of strategies would be implemented. “We start from the business first. We question if we will stay with our businesses or change to new businesses or even leave the existing businesses we have” said Sutjipto. Actually WIKA had been diversified its businesses several years ago, but this time, at the crisis situation, some questions revealed about continuing the diversification or even left the existing businesses meant back significantly to only focus at certain business-line. It had to be answered soon. WIKA started the business from electrical and pipe-installation for houses and buildings. WIKA’s management realized that WIKA would not become a big-corporate if only relied on electrical-business. Now, WIKA’s projects were various from high-rise building, fly-over, toll-road, railway until solar water heater (SWH) and LPG tank producer. Also WIKA became a producer of automotive-component. WIKA actually made its diversification without leaving its core-business as construction-services but trying hard to synergy with its core i.e. for power plant projects; WIKA could use its expertise in construction, got the material from WIKA Beton and install the equipment by PT Catur Insan Pertiwi which has just been acquired this year, from Steel Fabrication Division. WIKA became LPG tank producer where WIKA implemented the expertise they have in WIKA Beton in WIKA Intrade subsidiary. WIKA had decided to diversify through related-diversification. Many things must be prepared along with diversification-decision, what was the cost that must be paid for this diversification – policy? Sutjipto said that resistance for some policies was a usual problem that could be solved by logical reason and reasonable prediction in the future. Human- resources were also the cost for diversification because company had to be able to prepare people for several divisions with different skills, which included how to manage and retained the talented sources. The cost must be paid also for penetrating new market i.e. how to survive in solar energy conversion industry where WIKA had a famous product WIKA Solar Water Heater. Acquisition was a quick strategy to speed up successful diversification-projects.

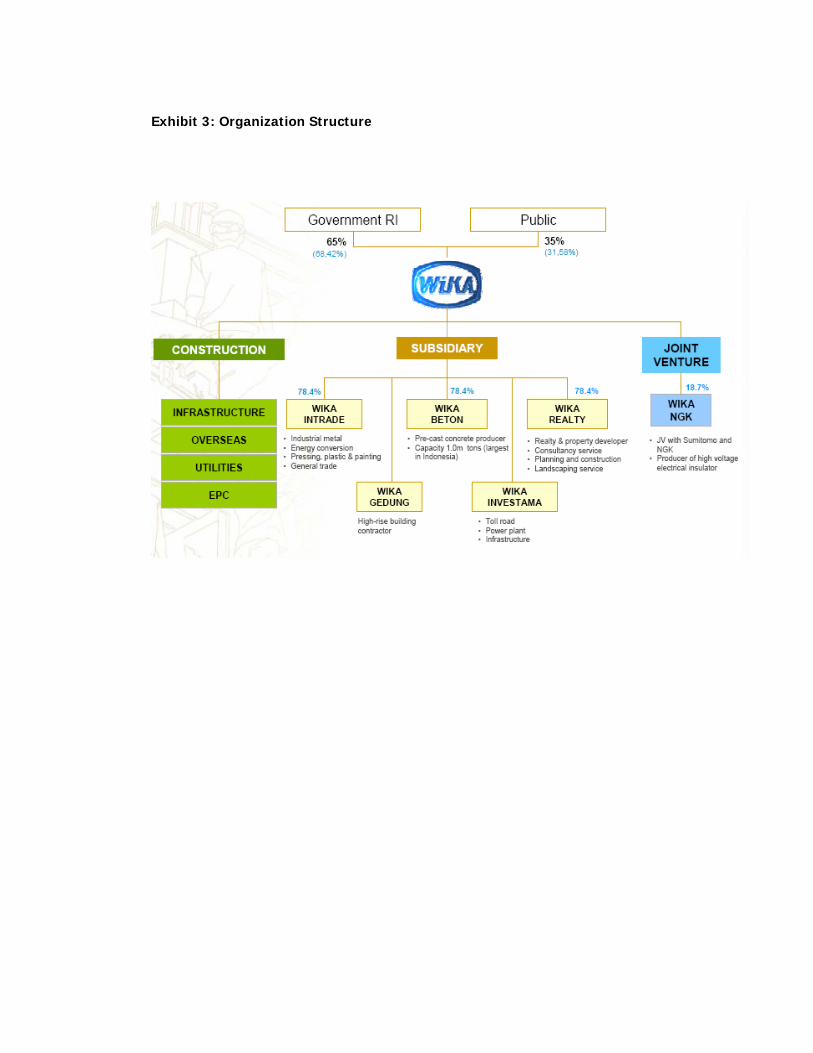

The company planned to acquire toll-road operators as well as engineering consultancy company. WIKA claims it has built approximately 30.0% of government-owned 10,000-MW power plant projects. The company plans to acquire a 70.0% stake of PT Catur Insan Pertiwi (CIP), a mechanical engineering and engineering consultancy company specializing in power plants. Going forward, WIKA also planned to acquire toll-road operators and mining contractors, apart from its plan to enter international market. Engineering Procurement and Construction (EPC) projects would become a future business but Tonny Warsono, Director of Human Capital said “EPC is not future target, but the process to get better added-value. Energy and environment sector will be an interesting market to be explored in the future” It looks very busy of diversification. Sutjipto considered what strategies will be implemented to reach the goals? What opportunities and challenges will be experienced by WIKA after diversifying its business? How best could WIKA execute its diversification strategy? Brief History of Wijaya Karya Established on March 11, 1960, PT Wijaya Karya (Limited), or commonly named WIKA, one of the state owned enterprises, is a product of nationalization of Dutch company, Naamloze Vennootschap Technische Handel Maatscappij en Bouwberijf Vies en Co abbreviated to NV Vis en Co.It began with electrical installation work, WIKA, along with rapidly economic growth, raised into a strong corporation with its four main business pillars that include construction, manufacturing, trade and realty. In the construction field, WIKA has coped with various scale of work through sophisticated technology, ranging from public facilities, architecture, mechanical, electrical, to landscape. In the manufacturing field, WIKA has developed an array of competitive products in the market. WIKA's leading products cover diverse concrete products, energy conversion, alloy component casting, furniture, and steel construction. In the field of trade, WIKA has, since 1987, exported a range of commodities that either of its manufacturing products or other's. Products such as furniture, concrete poles, solar water heater, connectors and accessories, not to mention other alloy component casting that are famous in the Malaysian, American, Dutch, French, and other European market. In the realty field, WIKA has developed a residential area using the brand "Tamansari" that are spread throughout Indonesia. It offers a collection of housing types with a sound and comfortably situated landscape. WIKA intended to make each of its business unit independent and has a great potential to grow more rapidly. This was achieved with establishment of PT WIKA Beton in the year of 1997, and followed with other business units; PT WIKA Intrade for manufacturing and trade and PT WIKA Realty for realty and property in early 2000. The company became a public company by listing 35.0% of its stock in the Indonesian Stock Exchange (BEI) in October 2007. WIKA’s construction business lines could be divided into 4 divisions: general civil construction, building construction, mechanical & electrical, and engineering, procurement and construction (EPC). WIKA also has 3 subsidiaries and a joint venture company (WIKA-NGK Insulator) to support the business. The subsidiaries are WIKA Beton, WIKA Intrade, and WIKA Realty. Government-related projects still has the biggest chunk (60.0%) in WIKA’s order book compared with projects from private companies (40.0%).

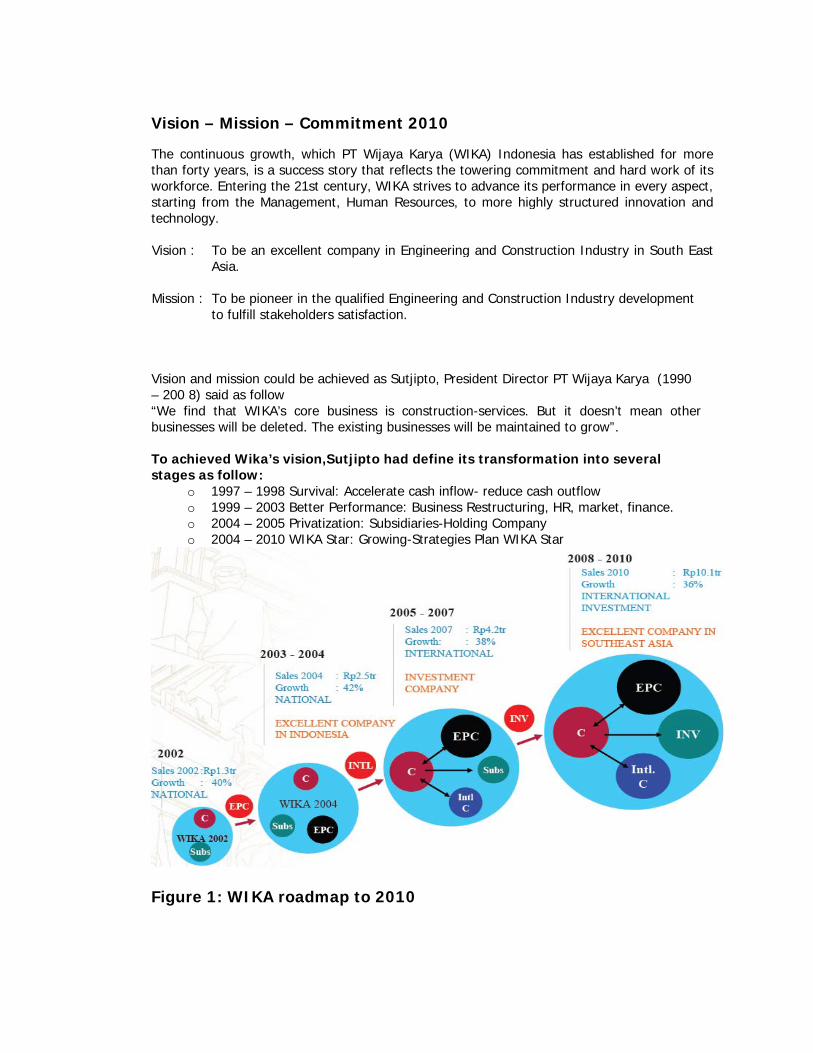

Vision – Mission – Commitment 2010

The continuous growth, which PT Wijaya Karya (WIKA) Indonesia has established for morethan forty years, is a success story that reflects the towering commitment and hard work of itsworkforce. Entering the 21st century, WIKA strives to advance its performance in every aspect,starting from the Management, Human Resources, to more highly structured innovation andtechnology. Vision : To be an excellent company in Engineering and Construction Industry in South East

Asia.

Mission : To be pioneer in the qualified Engineering and Construction Industry development to fulfill stakeholders satisfaction.

Vision and mission could be achieved as Sutjipto, President Director PT Wijaya Karya (1990 – 200 8) said as follow “We find that WIKA’s core business is construction-services. But it doesn’t mean other businesses will be deleted. The existing businesses will be maintained to grow”. To achieved Wika’s vision,Sutjipto had define its transformation into several stages as follow:

o 1997 – 1998 Survival: Accelerate cash inflow- reduce cash outflow o 1999 – 2003 Better Performance: Business Restructuring, HR, market, finance. o 2004 – 2005 Privatization: Subsidiaries-Holding Company o 2004 – 2010 WIKA Star: Growing-Strategies Plan WIKA Star

Figure 1: WIKA roadmap to 2010

Subsidiaries

Company Established Line of Business PT Wijaya Karya Beton 1997 Concrete Industry:

Pre–stressed concrete poles for power distribution lines and PC piles, concrete open channels, concrete railways sleepers, bridge girders, sheet piles, pipes, platform slabs and building components.

PT Wijaya Karya Realty 2000 Realty & Property: Realty & property development, consultancy services, planning, constructions and landscaping services

PT Wijaya Karya Intrade 2000 Industry and Trade: General Trading, metal and Energy conversion

Infrastructure Industry Construction & Global Crisis The construction industry's average growth rate was 7.6% during the past five years, higher than average real GDP growth rate of 5.5% for the same period. The contribution of the construction industry to GDP had also gradually increased to 7.5% and 7.7% in 2006 and 2007 respectively, closer to the pre-crisis level of 8%. Hence, continued development of both public and private infrastructure is required in order to boost the nation's economic growth. As for this year, the government had predicted national construction activities to reach Rp170tn, of which Rp76.5tn (or 45%) are government related projects. The government had committed in stimulating infrastructure projects since the past 2 years, which include 10,000-MW power plant projects, 1,000-km toll road projects, and 1,000 towers of subsidized apartments. It would substantially affect the construction industry directly and indirectly (e.g. projects from private companies), as infrastructure projects may create multiplier effects in the long-run, in our view. Yet in reality, a Coordinating Ministry of Economy official stated that only 70% of the projects will be completed and meet the targeted time schedule, an estimation that was still aggressive in our view.

The Indonesian government still played a dominant role in infrastructure projects, although they had started taking some action towards public-private partnership in carrying out the projects. Yet, high oil prices placed great pressure on the government, which eventually would limit its capital expansion. The projects Private investment in GOI sponsored or supported infrastructure projects have been ongoing for a number of years in sectors such as oil, gas and mining exploration and development. In 2005, the GOI held the first Infrastructure Summit at which it formally offered more than 90 projects (valued at more than US $22 billion) to private investors in all infrastructure sectors,

including telecommunications, power and electricity generation and distribution, transportation (toll roads, airports, railway and sea ports) and water supply and waste management. Given the lack of progress on these PPP projects since the 2005 conference (only six winning bidders were announced and only one project has begun construction) the GOI has scaled back its list of critical infrastructure projects to 10 'model' projects (see Model Infrastructure Projects). These projects are considered by the GOI to be realistic and financially feasible, with planning (including feasibility studies) already at an advanced stage. It is hoped that these projects will serve as successful models for future infrastructure projects. In addition, the GOI has put more than 90 other infrastructure projects on the table, worth approximately US$15 billion (see Current Infrastructure Projects). In total, the GOI has stated that it needs US$22 billion each year for infrastructure spending.

Table 1: Current Infrastructure Projects1

Projects Number Project models

Potential projects

(US$ million)

Total Investment

Turn pikes 20 2 18 5,340.34

Drinking water 13 3 10 502.46

Power plants 36 2 34 4,527.00

Gas pipelines 12 - 12 2,855.00

Transportation 29 2 27 1,998.82

Telecommunications 1 1 - 1,517.00

Total 111 10 101 16,740.62 Source: National Development Planning Agency (Bappenas) EPC EPC (Engineering, Procurement and Construction): means the company is contracted to provide engineering, procurement and construction services by the owner. Think Design & Construct style contracts, where the project is largely Contractor managed and the cost risk and control are weighted towards the Contractor and away from the Owner. The EPC contractor has direct contracts with the construction contractors.2 Would EPC become the business’s leader of WIKA?

1 www.aar.com.au/pubs/asia/foindonov06.htm 2 www.prodigyengr.com/front/showcontent.aspx?fileid=73

Interest Level Highest on Energy Projects3 Interest among potential investors remains highest in energy sector projects, particularly in the electric power generation sub-sector. The GOI offered two model projects in this sub-sector:

o Central Java Coal-Fired Power Plant: A 1,200 MW coal-fired thermal plant developed on a build-own-operate basis at an estimated cost of USD 1.2 billion

o Pasuruan Combined Cycle Power Plant, East Java: A 500 MW double chambered coal-fired plant developed on a build-own-operate basis at an estimated cost of USD 275 million.

Minister of Energy and Mineral Resources Purnomo Yusgiantoro said the GOI would strictly follow the KKPPI (Komite Kebijakan Percepatan Penyediaan Infrastuktur) process for the two model electricity projects. The GOI has completed site studies and bidding documents for both projects, but potential investors must complete feasibility, environmental, and energy sourcing studies, according to Purnomo. Although Purnomo set a goal of getting the projects into KKPPI process by 2007, he was unable to give an exact timeline, noting much of the institutional structure of the KKPPI process is not yet fully functional. Investors also focused their interest and questions on projects announced earlier in the year under the so-called 10,000 MW "crash program." The program aims to add 10,000 MW to the national grid by 2009. To date, the GOI has identified 40 fast-track projects totaling more than 8,750 MW. The largest project will be on the island of Java with planned operational dates of 2010. Purnomo said these projects must be transparent. He also said GOI funding for these projects should not take precedence over those following the full KKPPI process. The two model electricity projects are former "crash" projects previously offered through direct bid. Table 2: Contribution of the construction industry to GDP tend to increase (Rpbn) 2003 2004 2005 2006 2007Nominal GDP construction 125,337.1 151,247.6 195,110.6 251,132.3 305,215.Total nominal GDP 2,013,674.6 2,295,826.2 2,774,281.1 3,339,479.6 3,957,40% construction to total 6.2% 6.6% 7.0% 7.5% 7.7% Real construction growth 6.1% 7.5% 7.5% 8.3% 8.6%Real GDP growth 4.8% 5.0% 5.7% 5.5% 6.3%

Source: CEIC Key Players PT Adhi Karya (Persero) Tbk (ADHI)

Background Adhi Karya (ADHI) was a 47-year old state-owned construction company. ADHI derived most of its cash flow by performing public civil engineering, building construction, mechanical and

3 www.usembassy.gov/infra-summit05/infrastructure-summit06.html

electrical, as well as trading of building material procurement and construction equipments. Adhi Karya went public and became listed in the JSX and SSX after its IPO in March 2004. Expecting lower cost of contracts in 2009 However, the trending down in commodity prices (including fuel) might led to improvement in its cost structure next year. Judging from it, the outlook for ADHI should consequently improve, driving up FY09 earnings growth expectations of 10 % Table 3: Key forecast and valuation (ADHI)

Year to 31 Dec 2007 2008F 2009F 2010FRevenue (IDRb) 4.974 6.008 6.554 7.363EBITDA (IDRb) 304 304 333 358Net Profit (IDRb) 112 98 108 127EPS (IDR) 62 55 60 71Growth (%)37.5 16.8 (11.9) 10.4 17.4P/E (x) 7.7 8.8 8.0 6.8BVPS (IDR) 29.5 331 375 427P/BV (x)221 1.6 1.5 1.3 1.1EV/EBITDA (x) 3.8 4.8 4.5 4.3ROA (%) 2.6 2.4 2.4 2.5ROE (%) 21.0 16.5 16.1 16.5Dividend (IDR) 11.7 18.6 16.4 18.1Dividend Yield (%) 2.4 3.9 3.4 3.8

Source: Adhi, Bahana estimates PT Total Bangun Persada Tbk. (TOTL) Background Established in 1971, Total Bangun Persada (TOTL) was a construction and trading company, focusing on the construction of premium buildings, housing, industry and resort. The company went public and became listed in the JSX, and SSX after its IPO in July 2006 Concerns going into 2008

• Going forward, in an effort to mitigate increasing raw materials prices and recover margins, the company has engaged in a re-sharing scheme between the developers and the contractors. This is expected to provide risk sharing should costs of raw materials continue to increase.

• Additionally, the management is continuing to attempt to place some sort of escalation clauses in particular for the shorter-term contracts (i.e: 1-year of less) in an attempt to boost margins.

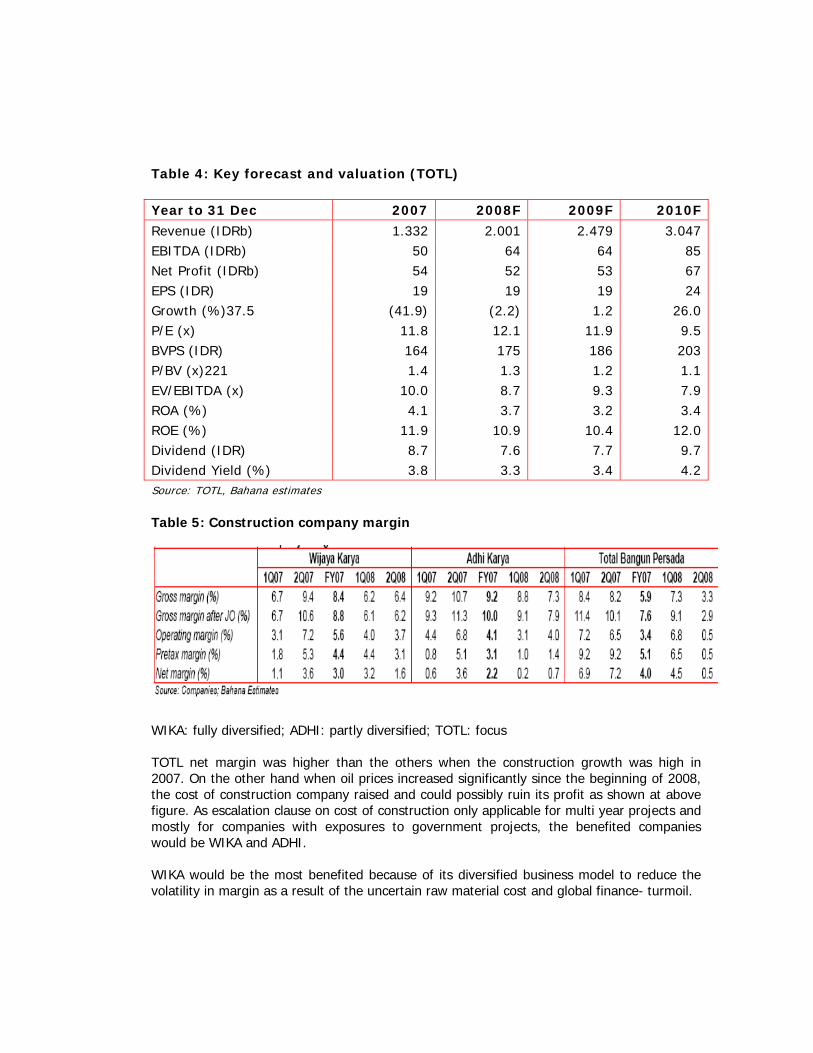

Table 4: Key forecast and valuation (TOTL) Year to 31 Dec 2007 2008F 2009F 2010FRevenue (IDRb) 1.332 2.001 2.479 3.047EBITDA (IDRb) 50 64 64 85Net Profit (IDRb) 54 52 53 67EPS (IDR) 19 19 19 24Growth (%)37.5 (41.9) (2.2) 1.2 26.0P/E (x) 11.8 12.1 11.9 9.5BVPS (IDR) 164 175 186 203P/BV (x)221 1.4 1.3 1.2 1.1EV/EBITDA (x) 10.0 8.7 9.3 7.9ROA (%) 4.1 3.7 3.2 3.4ROE (%) 11.9 10.9 10.4 12.0Dividend (IDR) 8.7 7.6 7.7 9.7Dividend Yield (%) 3.8 3.3 3.4 4.2Source: TOTL, Bahana estimates Table 5: Construction company margin

WIKA: fully diversified; ADHI: partly diversified; TOTL: focus TOTL net margin was higher than the others when the construction growth was high in 2007. On the other hand when oil prices increased significantly since the beginning of 2008, the cost of construction company raised and could possibly ruin its profit as shown at above figure. As escalation clause on cost of construction only applicable for multi year projects and mostly for companies with exposures to government projects, the benefited companies would be WIKA and ADHI. WIKA would be the most benefited because of its diversified business model to reduce the volatility in margin as a result of the uncertain raw material cost and global finance- turmoil.

Wijaya Karya’s Strategic Repositioning: Was Company ready to diversify? Diversification provides natural hedge against segment-specific fluctuations A genuine infrastructure player As an expert in the infrastructure business, WIKA provided the widest exposure across construction sub-sectors, including infrastructure (roads, bridges, irrigation facilities, harbors, airports, power plants), building construction (hotels, offices, schools, hospitals, commercials, manufacturing and industrial buildings), mechanical and electrical works, as well as engineering procurement construction services (EPC). This gave WIKA a natural hedge against segment-specific fluctuations in performance. In addition, WIKA also had expertise in the industrial manufacturing and trading of building materials, as well as realty services and construction equipment rentals. Hence the company was well-positioned to capture opportunities in the robust construction market. Sustainable market position with solid reputation WIKA’s more that 47 years experience in delivering high quality construction services and products had served the company well in securing sizeable order books from new and repeat customers. This enabled WIKA to maintain its position as Indonesia’s second largest construction company by revenue in 2006. The company had recorded 39.0% and 23.1% CAGR in revenue and net profit growth during the past five years, respectively. Large portion of repeat customers Strong customer base The rising portion of repeat customers; i.e. 5%, 15%, and 20% in 2004, 2005, and 2006, respectively indicate customer satisfaction. Apart from government related entities such as the Ministry of Public Works, Ministry of Transportation, Jasa Marga (state-owned toll road company), PLN (state-owned electricity company), Bank Indonesia (the central bank), and Pertamina (state-owned oil and gas company), a number of non-government related entities in the private sector have also given WIKA repeat orders, including Agung Podomoro, Gapura Inti Graha, Exelcomindo Pratama, Mitsubishi Heavy Equipment, Cheng Da Corporation, Truba Jurong, as well as the International Red Cross society. For the past three years, on average government-affiliated customers contributed for 46.3% of WIKA’s revenue, while the remaining 53.7% was from purely private customers. Synergy between WIKA and its subsidiaries Synergy promoted by a vertically integrated business Currently WIKA’s operations was supported by four business pillars namely construction, industrial, trading and realty services. In carrying out daily activities, WIKA acts as an operating holding company overseeing the main construction business. The remaining three business were each handled by subsidiaries WIKA Beton, WIKA Intrade, and WIKA Realty, as well as a joint venture company (WIKA-NGK Insulators). All of them are vertically integrated

to support one another, in particular WIKA’s main construction business. This differentiated WIKA from its competitors and also benefited WIKA in supply and demand of construction materials produced by each subsidiary, including priority in delivery and supply guarantee. As a quality builder, WIKA complied with international standards for performance Experienced management with international standard performance WIKA was the first Indonesian construction company to receive the ISO 9001; 2000 certification for quality management system in 2001. WIKA also received the OHSAS (Occupational, Health and Safety Assessment Series) accreditation in 2003. WIKA’s CEO, A. Sutjipto had been granted the “CEO of the Year 2006” from Business Review Magazine. Moreover, WIKA also received the “Best Operation 2006” and the “Best Human Resources 2006” form SOE & CEO Award along with the “Best Human Resources Development 2006” form Business Review magazine. We believed this was crucial as WIKA’s success in executing its strategy was very much dependent on the management’s commitment to its circle of competence. Earnings growth was estimated at 23.7% CAGR over 2006 – 2011 periods Strong financials on solid growth profile Going forward, WIKA will undertake more overseas projects in the Middle East countries through joint operations schemes with foreign contractors. WIKA would also expand its EPC segment (engineering, procurement and construction) which not only conducts plain construction but also provided design, planning and procurement services. At the same time, WIKA would also invest in infrastructure projects such as the RaiLink project (Jakarta downtown – airport railway). Accordingly, these strategic plans would show WIKA’s revenue and net profit growing 22.2% and 23.7% CAGR over 2006 – 2011 period, respectively. The increasing number of players would further boost competition in the industry going forward Competition intensify In general, low barriers to entry had attracted a large number of domestic players, including small-scale and newly established companies, to the competition. The domestic construction industry was once dominated by state-owned “Karya” companies including Wijaya Karya, Adhi Karya, Waskita Karya, Hutama Karya, Istaka Karya, Pembangunan Perumahan, Nindya Karya and Brantas Abipraya. Competition is tightening with the existence of private construction companies such as Total Bangun Persada, Murinda, Tata Mulia, Pulau Intan, and Jaya Construction, as well as foreign construction companies such as those form Japan, Singapore, and Korea. Going forward, we believed companies offering unique areas of expertise will be better equipped for the competition. Performance susceptible to inflation of raw material prices As a construction company, WIKA required raw materials such as cement, steel, sand, and ready mix. The surge in raw material prices had resulted in submitted cost estimates for construction projects becoming frequently outdated. Hence most construction companies had faced difficulties in maintaining their margins. Accordingly, WIKA was securing future

contracts for raw material delivery throughout the entire construction period for new projects. Should the material price surge persist in the long term, there would be risk of lower demand form construction projects. Materials account for 40.8% of cost of sales (COGS) in 2006 The interest rate fluctuations falling interest rates will result in cheaper financing, hence stimulating constructions activities. On the other hand, construction activities may be negatively affected should interest rates reverse its trend,. Human Resources Integration of Organization Strategy and Management Strategy of Human Resources to maintain growth. Knowledge Management would become a tool to compete strongly in the industry. In the future WIKA might face challenges, depend on the strategies that company had been chosen. Knowledge management would be the way to create human capital who realized that sharing and learning working-experiences among employees would be very important to compete in this industry. Looking Ahead

It was believed that the limited capital expansion on government budget , uncertainty on new tax regulations, and high inflationary pressure which may squeeze margins, would bring negative sentiment to the industry, although chances of Wijaya Karya (WIKA) overcoming this unfavorable condition was still intact.

Higher raw material prices and other operating expenses. The prices of raw materials (such as steel and cement), which had the biggest chunk of total construction costs (around 45.0%) had jumped significantly. Average steel price had increased by approximately 45.0% Year on Year, whereas domestic cement price had increased by 22.5% Year on Year. After global economic crisis hit all countries in the world, the prices gradually moved down on concerning global-demand would decrease, but IDR currencies got weakened around 15% to approximately Rp.11.000 per US$.

Prefer company with exposure to government projects Company’s target should choose the contracts with exposure towards government projects, which mostly involves public infrastructure such as public roads, toll roads, power plants, dams, irrigations, airports and harbors. It might be better equipped in facing raw material cost fluctuations as the majority of government projects have cost escalation clauses in their contracts.

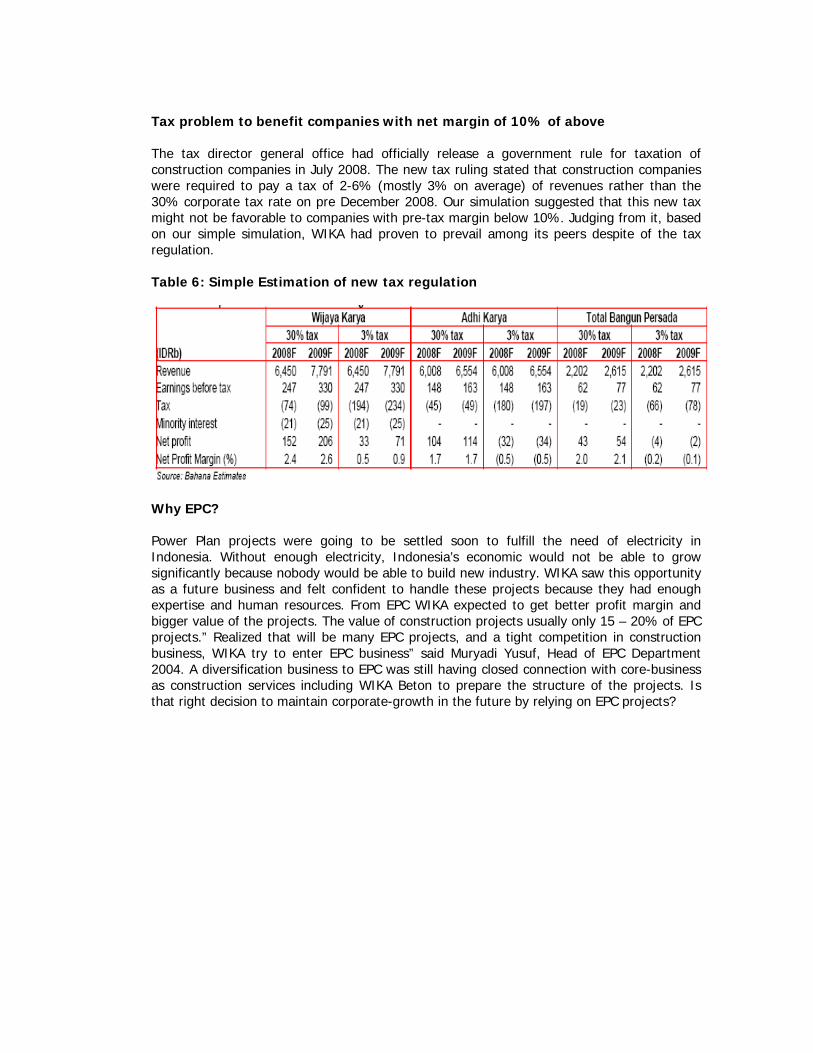

Tax problem to benefit companies with net margin of 10% of above The tax director general office had officially release a government rule for taxation of construction companies in July 2008. The new tax ruling stated that construction companies were required to pay a tax of 2-6% (mostly 3% on average) of revenues rather than the 30% corporate tax rate on pre December 2008. Our simulation suggested that this new tax might not be favorable to companies with pre-tax margin below 10%. Judging from it, based on our simple simulation, WIKA had proven to prevail among its peers despite of the tax regulation. Table 6: Simple Estimation of new tax regulation

Why EPC? Power Plan projects were going to be settled soon to fulfill the need of electricity in Indonesia. Without enough electricity, Indonesia’s economic would not be able to grow significantly because nobody would be able to build new industry. WIKA saw this opportunity as a future business and felt confident to handle these projects because they had enough expertise and human resources. From EPC WIKA expected to get better profit margin and bigger value of the projects. The value of construction projects usually only 15 – 20% of EPC projects.” Realized that will be many EPC projects, and a tight competition in construction business, WIKA try to enter EPC business” said Muryadi Yusuf, Head of EPC Department 2004. A diversification business to EPC was still having closed connection with core-business as construction services including WIKA Beton to prepare the structure of the projects. Is that right decision to maintain corporate-growth in the future by relying on EPC projects?

Exhibit 1: Business Portfolio

Source: WIKA

Exhibit 2: Management

Commissioner President Commissioner : Ir. Junius Saringar Ulibasa Hutabarat Commissioner : DR. Budi Suradji Commissioner : Pontas Tambunan, SH., MM Commissioner : Roslan Zaris, SE., MSc

Director President Director : Ir. Aloysius Sutjipto, MM., MT Director of Finance : Ir. Slamet Maryono Director of Operation I : Ir. Sutedjo Wirokusumo, MM Director of Operation II : Ir. Djokomulyono, MM Direktur of Human Capital : Ir. Tonny Warsono Hardjo, MM

Exhibit 3: Organization Structure

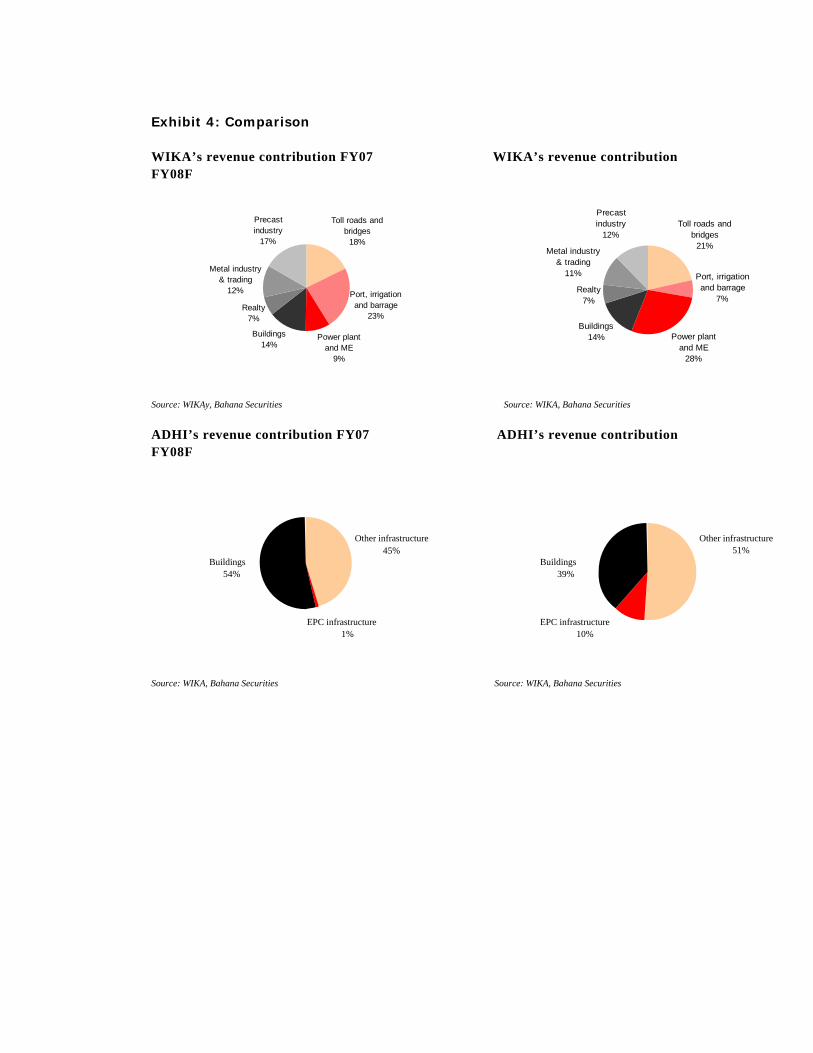

Exhibit 4: Comparison WIKA’s revenue contribution FY07 WIKA’s revenue contribution FY08F

Toll roads and bridges

18%

Port, irrigation and barrage

23%

Power plant and ME

9%

Buildings14%

Realty7%

Metal industry & trading

12%

Precast industry

17%

Toll roads and bridges

21%

Port, irrigation and barrage

7%

Power plant and ME

28%

Buildings14%

Realty7%

Metal industry & trading

11%

Precast industry

12%

Source: WIKAy, Bahana Securities Source: WIKA, Bahana Securities ADHI’s revenue contribution FY07 ADHI’s revenue contribution FY08F

Source: WIKA, Bahana Securities Source: WIKA, Bahana Securities

EPC infrastructure1%

Buildings54%

Other infrastructure45%

EPC infrastructure10%

Buildings39%

Other infrastructure51%

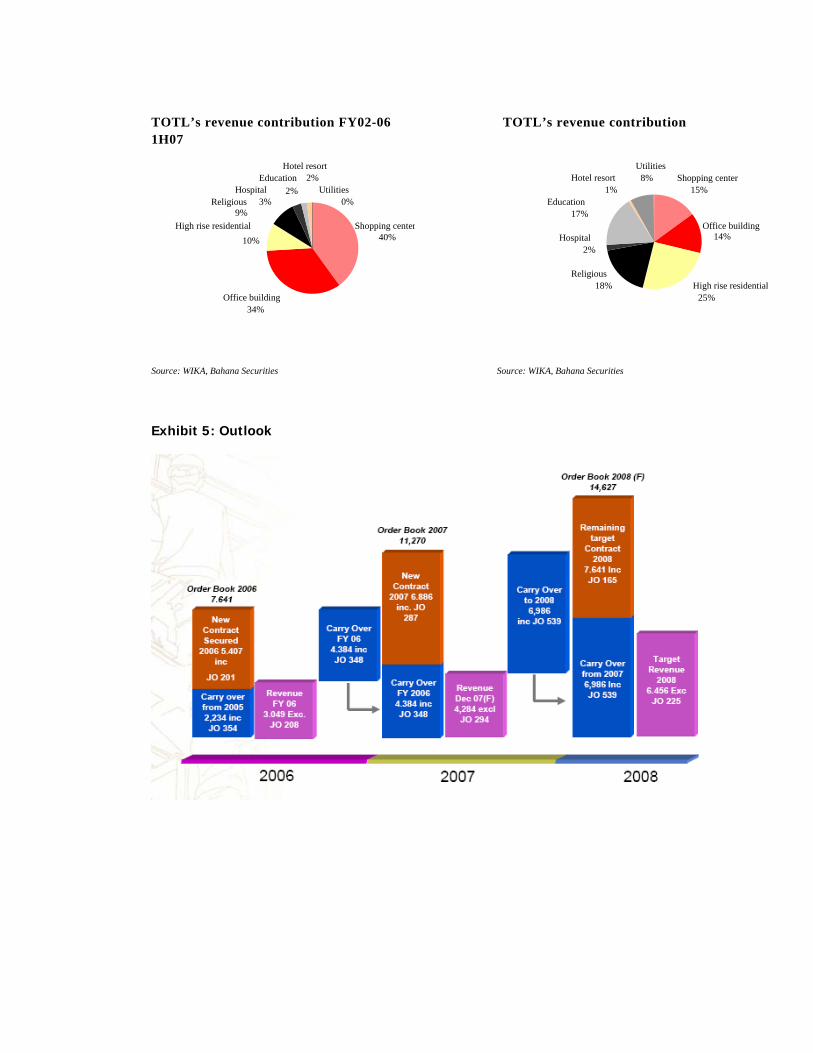

TOTL’s revenue contribution FY02-06 TOTL’s revenue contribution 1H07

Source: WIKA, Bahana Securities Source: WIKA, Bahana Securities Exhibit 5: Outlook

Shopping center40%

Office building 34%

High rise residential 10%

Education2%

Hotel resort2%

Utilities 0%

Hospital 3%Religious

9%

Shopping center15%

Office building14%

High rise residential25%

Education 17%

Hotel resort 1%

Utilities8%

Hospital 2%

Religious 18%

Exhibit 6: Balance Sheet

Source: WIKA

Exhibit 7: Projected Income Statement

Exhibit 8: Growth of Orders

Source: WIKA

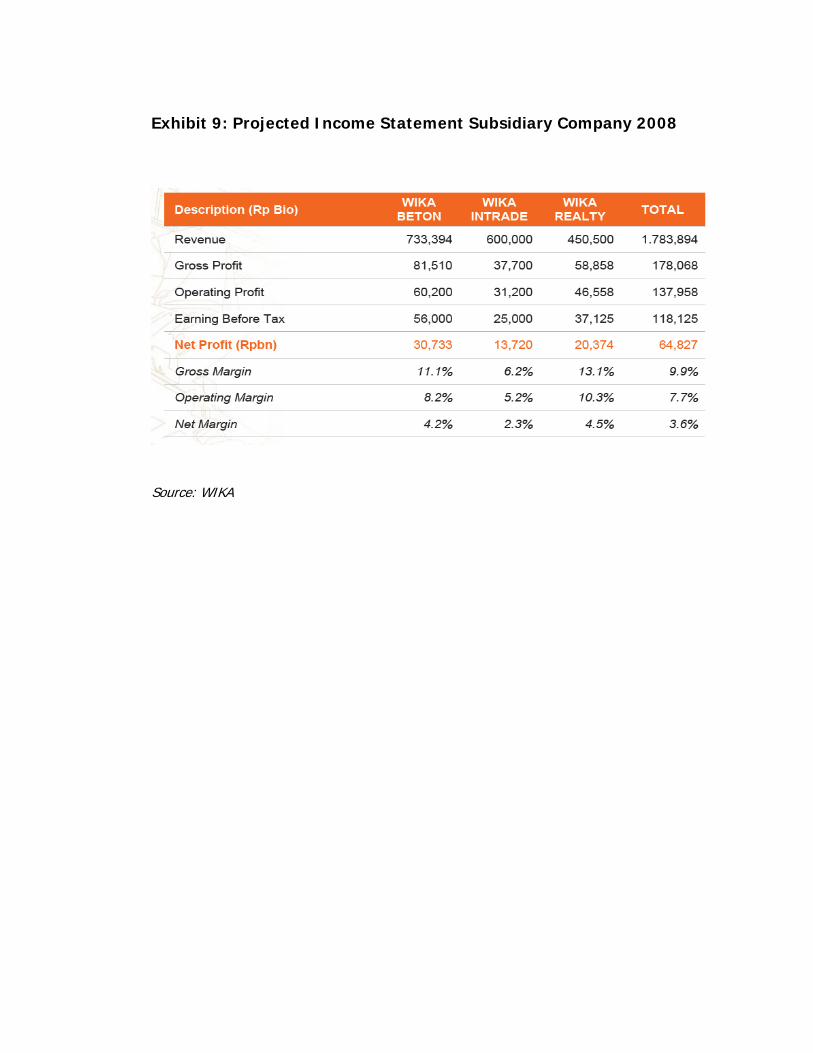

Exhibit 9: Projected Income Statement Subsidiary Company 2008

Source: WIKA

Exhibit 10: Peer comparison

Source: WIKA

Description ADHI TOTL WIKA

FY06 FY07 *) Chg FY06 FY07 *) Chg FY06 FY07 *) Chg

Revenue (Rp Bio) 4,329 5,234 20.9%

1,120 1,300 16.1% 3,049 4,226 38.6%

Gross Profit (Rp Bio) 403 506 25.6 153 N/A N/A 246 368 49.8%

Operating Profit (Rp 252 281 11.6 133 N/A N/A 124 255 105.8

Net Profit (Rp Bio) 96 120 25.5 102 52.0 - 94 117 25.1%

Gross Profit (%) 9.3% 9.7% 13.7% N/A 8.1% 8.7%

Operating Profit (%) 5.8% 5.4% 11.9% N/A 4.1% 6.0%

Net Profit (%) 2.2% 2.3% 9.1% 4.0% 3.1% 2.8%

Description ADHI TOTL WIKA

FY07 *) FY08 B Chg FY07 *) FY08 B Chg FY07 *) FY08 B Chg

Revenue (Rp Bio) 5,234 6,701 28.0% 1,300 2,000 53.8% 4,226 6,050 43.2%

Gross Profit (Rp Bio) 506 671 32.6% N/A N/A N/A 368 521 41.5%

Operating Profit (Rp Bio) 281 N/A N/A N/A N/A N/A 255 360 41.5%

Net Profit (Rp Bio) 120 170 41.5% 52 100.0 92.3% 117 167 42.3%

Gross Profit (%) 9.7% 10.0% N/A N/A 8.7% 8.6%

Operating Profit (%) 5.4% N/A N/A N/A 6.0% 6.0%

Net Profit (%) 2.3% 2.5% 4.0% 5.0% 2.8% 2.8%

Notes : *) :Unaudited B : Budget

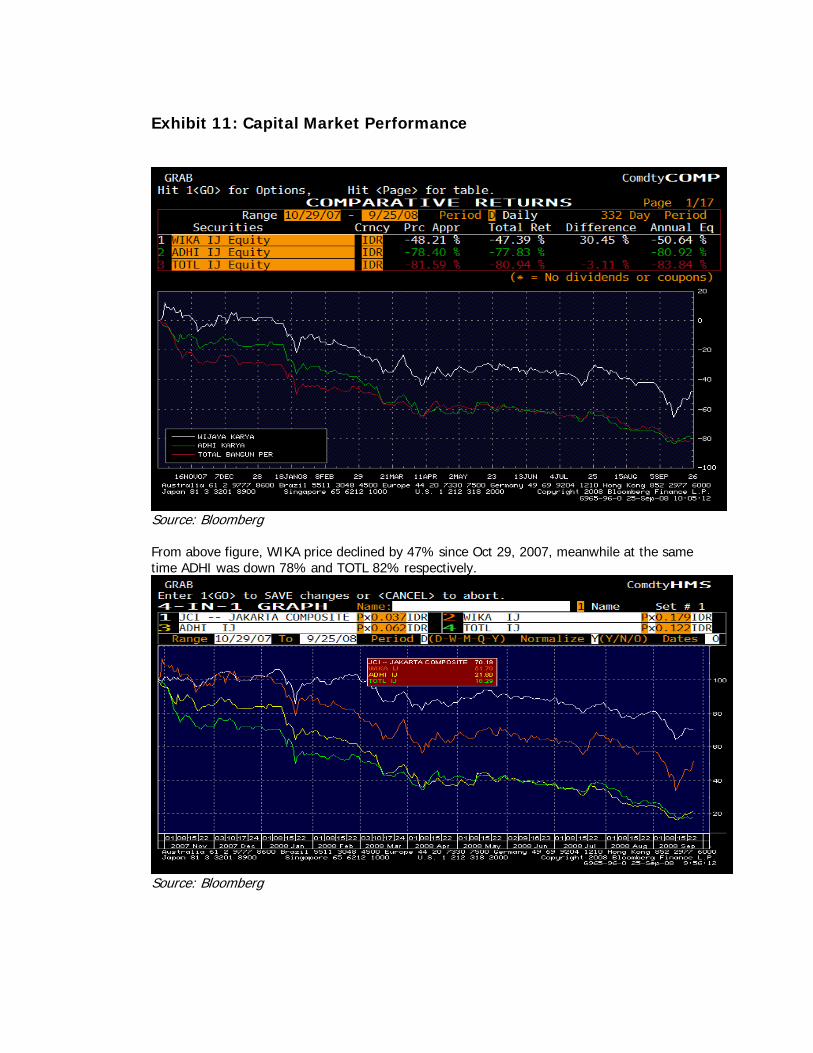

Exhibit 11: Capital Market Performance

Source: Bloomberg From above figure, WIKA price declined by 47% since Oct 29, 2007, meanwhile at the same time ADHI was down 78% and TOTL 82% respectively.

Source: Bloomberg

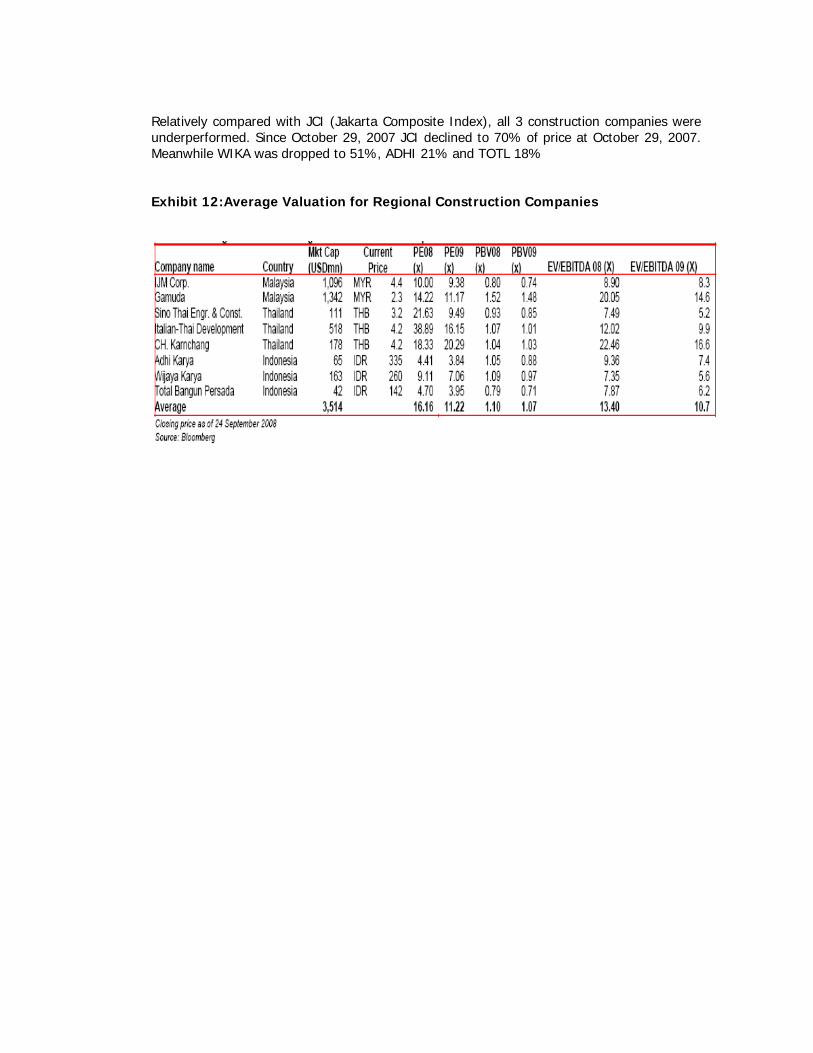

Relatively compared with JCI (Jakarta Composite Index), all 3 construction companies were underperformed. Since October 29, 2007 JCI declined to 70% of price at October 29, 2007. Meanwhile WIKA was dropped to 51%, ADHI 21% and TOTL 18% Exhibit 12:Average Valuation for Regional Construction Companies

Exhibit 13: Model Infrastructure Projects

Telecommunications sector:

1 The 'Palapa Ring' fiber optics network US$ 1.5 billion

Power plants:

2 2x600 megawatt (MW) coal-fired power plant in Central Java

US$ 1.2 billion

3 500MW coal-and-oil-fired power plant in Pasuruan, East Java

US$ 275 million

Toll roads:

4 165-km Solo-Kertosono toll road in Central Java US$ 928 million

5 60-km Medan-Kuala Namu-Tebing Tinggi toll road in North Sumatra

US$ 142 million

Sea ports:

6 Surabaya's Tanjung Perak port expansion US$ 280 million

7 Margagiri-Ketapang ferry terminal US$ 97 million

Water projects:

8 Dumai, Riau US$ 44 million

9 Tangerang, Banten US$ 37 million

10 Bandung US$ 26 million

Total US$ 4.5 billion Source: National Development Planning Board (Bappenas)

Exhibit 14: FY07 performance of large construction companies in Indonesia Income statement Adhi Karya Wijaya Karya Total Bangun PersadaTotal sales 4,973.9 4,284.6 1,331.7Gross profit 456.9 359.0 79.0Gross profit aft. joint oper. 495.5 376.3 101.6Operating profit 291.1 240.6 45.2Pre-tax profit 153.8 187.9 68.2Net profit 111.6 129.1 53.6 Gross margin 9.2 8.4 5.9Gross margin aft. joint 10.0 8.8 7.6Operating margin 5.9 5.6 3.4Pre-tax margin 3.1 4.4 5.1Net margin 2.2 3.0 4.0ROA 2.6 3.1 4.1ROE 21.0 10.0 11.9 Balance sheet (Rpbn) Current assets 3,952.7 3,687.3 1,087.0Total assets 4,333.2 4,133.1 1,305.9Current liabilities 3,268.5 2,232.0 786.7Total liabilities 3,801.9 2,841.9 854.3Total equity 531.2 1,291.2 451.7Total liabilities and equity 4,333.2 4,133.1 1,305.9

Source: WIKA, Bahana Securities

Dec-2001 Dec-2003 Dec-2005 Dec-2007

18

17

16

15

14

13

12

11

10

9

8

7

10

9

8

7

6

5

4

3

2

ID% pa, % change

1M SBI rate (LHS) Construction (RHS)

138,289

192,134

294,520

361,219

457,161

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

2003 2004 2005 2006 2007

(Rpbn)

Source: CEIC Source: Bank Indonesia

+34.8% CAGR

Exhibit 16: Rising credit to signifies the growth of the industry

Exhibit 15: Construction sector activities correlate negatively with the interest-

rate

Exhibit 17: Awards

Exhibit 18: News

WIKA Beton jacked up capacity by 15%

By M. Syahran W. Lubis Bisnis Indonesia, 26/ 11 / 2008 JAKARTA: PT Wika Beton made efforts to confirm its leadership in preprinted concrete market by increasing its production capacity by 15% from 1 million ton to become 1.14 ton next year. “One of the strategic actions which we will complete to improve the production capacity is by adding the facility to produce the preprinted concrete to meet the national need,” said Adji Firmantoro, Director of Wika Beton this week. According to him, with this addition, Wika Beton shall be able to maintain the company’s strong performance. Adji said that this subsidiary of PT Wijaya Karya Tbk (Wika) – a State Owned Company involved in construction services – currently controls the biggest market share of preprinted concrete in Indonesia. Wika Beton booked sales of IDR 704 billion during the first 9 months this year. This is caused by a strong sales performance of the company and a sharp increase of demand in quality preprinted concrete. The increase is equivalent to 18.8% compared to the same period in the previous year at IDR 592.82 billion.

Profit before tax of Wika Beton per third quarter of 2008 increased to become IDR 48.85 billion compared to the same period in the previous year of IDR 35.29 billion. In the previous year the profit before tax was booked at IDR 51.44 billion or contributed 27.37% to the overall profit of PT Wika. “We are very pleased with the achievement of the sales performance of Wika Beton. This is a strong indication that Wika Beton shall be able to exceed the sales target of 2008,” said A. Boediono, President Director of Wika Beton. Wika Beton has supplied preprinted concrete to various mega projects and construction developments in Indonesia for almost 30 years. A modern production capacity process has been applied at seven locations of Wika Beton factories to fulfill the increase in demand and an increase of efficiency. The factories of Wika Beton are spread in Binjau (North Sumatera), Bogor and Majalengka (West Java), Boyolali (Central Java), Pasuruan (East Java), Makassar (South Sulawesi) and Lampung.

Source: Bisnis Indonesia, 26 Nov 2008

WIKA obtained 2 new contracts of IDR 299.5 billion

By M. Syahran W. Lubis Bisnis Indonesia , 19 / 08 / 2008 JAKARTA: PT Wijaya Karya (Persero) Tbk obtained two new contracts for a total value of IDR 299.5 billion. One of the new contracts is the rehabilitation and flexibility operation (RFO) PF II project from PT Petrokimia Gresik at the value of IDR 129.5 billion. The other new project is the procurement of power plant gas turbine (PLTG) with a capacity of 40 WM in North Sumatera from PT Perusahaan Listrik Negara (PLN) at the value of IDR 170 billion. Imam Sudiyono, Corporate Secretary of Wika, explained the success to obtain the RFO PF II Petrokimia Gresik project confirmed Wika as an engineering procurement construction (EPC) company. Several EPC projects which have been successfully done by Wika are Tuban Aromatic and palm oil factories. Now Wika is also working on two power plant projects in its capacity as EPC, i.e. PLTU North Sulawesi (2x25 MW) and PLTU South Kalimantan (2x65 WM). Each project has the value of IDR 647 billion and IDR 600 billion. The work done by Wika at Petrokimia Gresik is to modify the phosphate SP36 fertilizer producing factory, so that in addition to produce this type of fertilizer, the factory can also produce NPK a complex fertilizer.

The production capacity of the RFO PF II factory expected to be achieved is 500,000 ton per annum of SP36 fertilizer of 480,000 ton per annum of NPK fertilizer. The scope of work of Wika is the design, procurement, installation, inspection and testing in mechanical, civil, electrical and instrument sectors. In connection with the supply of PLTU gas turbine in North Sumatera, Imam stated that via the project Wika again contributed to the national energy sector. The State-Owned Company in construction services now controls 30% of the power plant projects included in the government 10,000 WM cash program. Several power plant projects being constructed by Wika, other than PLTU North Sumatera and PLTU South Kalimantan, are also PLTU Banten 2 Labuan (2x300 WM), PLTU Indramayu (2x330 WM), PLTGU Tanjung Priok (2x350 WM) and PLTU Pelabuhan Ratu (3x300 WM). Wika is also participating in a PLN tender to become an independent power producer for two power plants i.e. PLTGU Tampomas in West Java and PLTU in Bali. Up to the end of semester I/2008, the income of Wika is recorded at 2.7 trillion or around 44.62% of the 2008 target of IDR 6.05 trillion. Order book being done by the State-Owned Company up to the end of semester I/2008 reached IDR 11.1 trillion or 78.7% of the 2008 order book target of IDR 14.1 trillion.

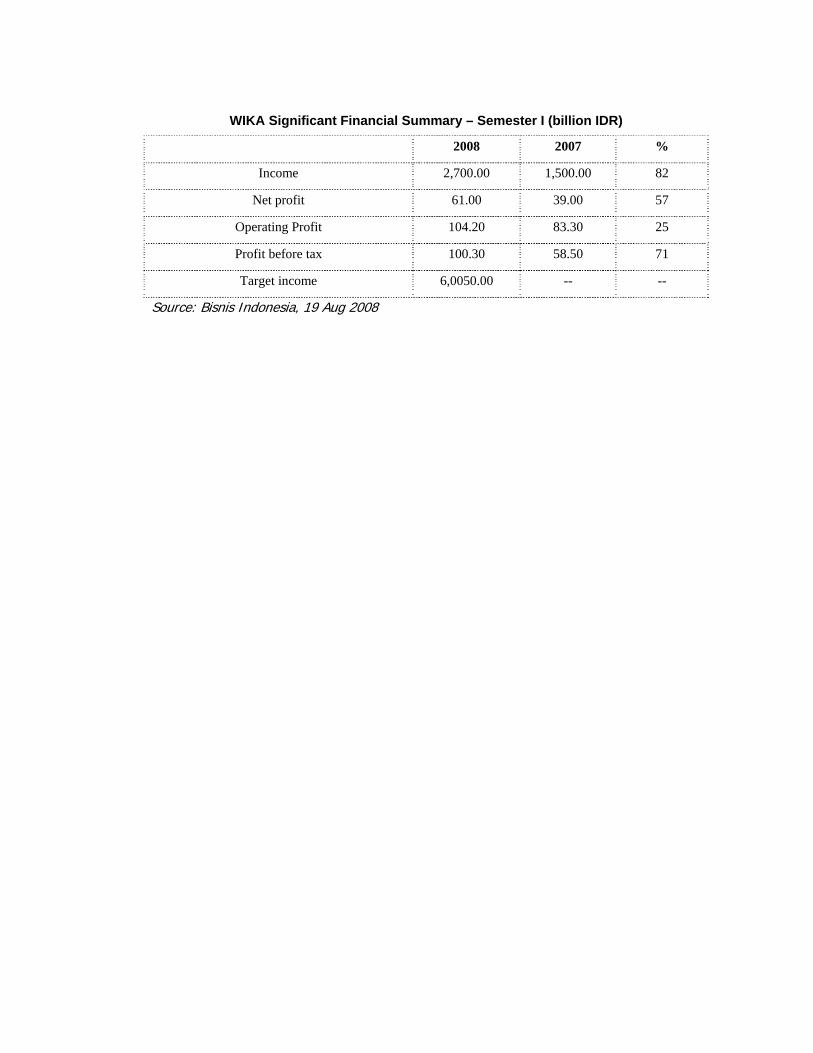

WIKA Significant Financial Summary – Semester I (billion IDR)

2008 2007 %

Income 2,700.00 1,500.00 82

Net profit 61.00 39.00 57

Operating Profit 104.20 83.30 25

Profit before tax 100.30 58.50 71

Target income 6,0050.00 -- --

Source: Bisnis Indonesia, 19 Aug 2008

Construction Business to recover mid 2009

JAKARTA: The national construction companies are expected to recover from the impact of the global crisis at the latest in semester II next year, due to a government commitment to push the infrastructure sector via increasing budget. Pribadi Agung, Director Asia Finance network (AFN), an investment consultant company, stated that the growth in construction and infrastructure sectors shall still be good in 2009, although the growth of the national and global economic slowed down. The growth in infrastructure sector next year is expected to be 30% higher than the national growth predicted at 5%-7%. “The government’s plan to speed up the infrastructure development projects shall benefit the companies struggling in this sector. The competitiveness of the contractors shall continue to strengthen in the midst of the slow down in other sectors,” he said when disclosing the prospect of the infrastructure sector in 20090 yesterday. Agung explained that the budget for the infrastructure projects in the technical departments in 2009 State Budget increased between 6% to 8%. The budget increase will be very useful to the contractors to be able to obtain projects and to maintain their performance. He added that the government action to spend funds for manpower intensive projects and infrastructure is correct, in the midst of the global crisis condition and the many employment terminations.

The spending for infrastructure is also being done by the Governments of the United States, China and India to maintain the economic growth. Agung also suggested the operator or the construction project companies such as developers or toll road operators to expand selectively and limitedly during the crisis. Easy to recover Jhon Paulus Pantouw, a member of the National Construction Service Development Institution said that the infrastructure sector is the easiest to recover after the crisis compared to other companies if the government is serious to support this sector. “We see various regulations to support the infrastructure projects being taken care of, such as the tender execution, the cooperation scheme between government and private, land procurement. Just wait for the realization,” he said to Bisnis yesterday. Deputy Minister of Economic Coordination of Infrastructure & Area Development Coordination Sector, Bambang Susantono said the next the government has committed to focus on real sector. “The directive from the president is already clear, the real sector has to be increased. This shall be followed by the issuance of new policies,” he said end of last week at the discussion regarding the toll road projects.

Source: Bisnis Indonesia, 16 Dec 2008

Exhibit 19: Projects

CURRICULUM VITAE

Name : Benny Bambang Soebagjo

Place/ Date of Birth : Malang, 10 April 1960

Sex: Male

Religion : Catholic

Address : Jl. Kartika Alam III/ 35, Jakarta

Telephone : +62-811 136 220

EDUCATION:

Binus Business School, Jakarta ....................................... 2006 – 2008

Universitas Katholik Parahyangan, Bandung

SMA St. Albertus, Malang

SMP St. Maria II, Malang

SD St. Maria II, Malang

WORKING EXPERIENCE :

PT. BAHANA SECURITIES

Director, Head of Equity Sales & Trading ................................ 2007 – Now

Head Equity Sales & Trading ....................................... 2003 – 2007

Vice President/ associate Director Equity Sales ...................... 1999 – 2003

![WIKA Instruments Limited - Company presentation A · PDF fileA strong group. For your success. WIKA Instruments Limited - Company presentation 1 [16.01.2018] WIKA Instruments Company](https://img.pdfslide.us/doc/110x75/5a9e4a607f8b9a6a218d40e6/wika-instruments-limited-company-presentation-a-a-strong-group-for-your.jpg)