Embed Size (px)

Citation preview

Grange St. Paul’s Hotel, London

18 October 2012

2012 Insurance Market Briefing -Europe

Welcome

2012 Insurance Market Briefing - Europe 18 October 2012 2

Dr Roger Sellek,Chief Executive Officer,A.M. Best EMEA & Asia-Pacific

10:35 European Outlook

11:20 Reinsurance Panel

12:05 Emerging Markets

12:45 Open Q&A

13:00

Agenda

2012 Insurance Market Briefing - Europe 18 October 2012 3

08:30 Registration

09:00 Welcome

09:10 EMEA Market Overview

09:30 Key Note Speaker

10:15

EMEA Market Overview

2012 Insurance Market Briefing - Europe 18 October 2012 4

Stefan HolzbergerManaging Director, AnalyticsA.M. Best Europe – Rating Services Ltd

2% 2%8%

14%

36%

25%

9%3% 1%

AA+ AA AA‐ A+ A A‐ BBB+ BBB BBB‐

Rating distribution as of 1 October, 2012

Western Europe

2012 Insurance Market Briefing - Europe 18 October 2012 5

• Key Market Characteristics– Economic uncertainty and

volatility– Heightened investment risk

– Sound underwriting and reserving fundamentals

– ERM advancements

Western Europe

2012 Insurance Market Briefing - Europe 18 October 2012 6

• Review– Strong technical profits– Baseline capital strength improved– Stressed capital strength currently

supports ratings• Preview

– Turbulent market conditions– Regulatory uncertainty– ERM focus

75%

15%

10%AffirmDowngradeUpgrade

14%86% Positive

NegativeStable

Rating Actions

Outlook Summary

Emerging Markets: Non-MENA

2012 Insurance Market Briefing - Europe 18 October 2012 7

• CEE Key Characteristics– Hard hit by financial crisis– Exceptions: Poland, Czech

Republic and Slovakia– Influence of Western insurers

• CIS Key Characteristics– Severe market contraction– Banking sector crisis– Consolidation– Tax optimisation schemes

0%

12%8%

19%

35%

15%8%

3% 0%

A A‐ BBB+ BBB BBB‐ BB+ BB BB‐ B+Rating distribution as of 1 October, 2012

63%

23%

14%

AffirmDowngradeUpgrade

4%

12%

84%

PositiveNegativeStable

Emerging Markets: Non-MENA

2012 Insurance Market Briefing - Europe 18 October 2012 8

• Review– Good technical profitability– Increased retention– Increased regulatory capital

requirements– Clampdown on tax avoidance

• Preview– Competition increasing– Feeling strain from financial crisis– Premium volumes recovering– Increase in foreign direct

investment

CEE

CIS

CEE

CIS

Rating Actions

Outlook Summary

Middle East & North Africa

2012 Insurance Market Briefing - Europe 18 October 2012 9

• Key Market Characteristics– Insurance market dominated

by Motor and Medical lines– Greatest threat: political

instability

– Competition heating up– ERM and regulatory

environment considered weak

0%

9%

26% 26%22%

17%

0%

A+ A A‐ BBB+ BBB BBB‐ BB+

Rating distribution as of 1 October, 2012

96%

4%

AffirmDowngradeUpgrade

Middle East & North Africa

2012 Insurance Market Briefing - Europe 18 October 2012 10

• Review– Country Risk issues– Low retention– High investment risk– Strong technical performance

• Preview– Profits squeezed– New entrants– Sound balance sheets– Takaful market growing

3%

17%

80%

PositiveNegativeStable

Rating Actions

Outlook Summary

Innovation in Insurance –Can Europe Compete?

2012 Insurance Market Briefing - Europe 18 October 2012 11

David LawGlobal Insurance LeaderPricewaterhouseCoopers LLP

Innovation in insurance –Can Europe compete?

www.pwc.co.uk/insurance

David Law, PwC Global Insurance leader

October 2012

PwC

Transformation of Mature Industries: Kodak

13

1880 1885

Kodak is founded by George Eastman

Invents roll film, the backbone of the motion picture business and portable cameras

Introduces the first model of

the lightweight and effective

Kodak handheld

camera

The company sells 90% of the photographic film and 85% of the cameras in the US market

1976 2010

Kodak resorts to patent litigation and

patent licensing to generate revenue

1888

Kodak’s Brownie low cost camera triggers the creation of a new mass market for amateur photography

1900

Kodak’s introduces Kodachrome, the first 35 mm color film

1935

Kodak invents the digital camera

1975

Kodak ranks No. 7 in US

digital camera sales

2009

Start of erosion of Kodak’s US photography film market share due

to effective foreign competitors in the market

1984

Kodak initiates

strategy of moving towards

digital technology

1990

Kodak ranks No. 1 in US

digital camera s sales

2005

Cellphones and tablets displace digital cameras as the preferred means of digital photography

Kodak’s attempts to increase its global footprint are thwarted as penetrating the world's second largest film market proves to be nearly impossible

1997 2001

Film sales worldwide significantly drop with the increasing penetration of digital photography devices

Ma

rket

Per

form

an

ceIn

nov

ati

ons

Kodak files Chapter 11 -Bankruptcy Protection

2012

Source: PwC analysis

PwC

‘The future isn’t what it used to be’

October 2012Innovation in insurance – Can Europe compete?Slide 14

The environment in which executives have spent most, if not all, of their careers is changing

PwC

Telematics: Best practice – Progressive, State Farm and Allstate

October 2012Innovation in insurance – Can Europe compete?Slide 15

PwC

Carriers are layering unstructured and sensor data over Geographic Information System data to analyze and better manage concentration risk

Basic GIS has been used for• Accurate underwriting and rating at the point of sale• Risk concentration assessment of their catastrophic

risk management activities

GIS data can be layered with• Wildfire hazard assessment, terrain slope, road

network etc.• Community investment in fire protection, location of

fire hydrants• Smart sensor data on temperature, moisture at various

locations

Build sophisticated predictive analytics• Non-catastrophic portion of expected losses at the

policy level by peril• New variables that are better indicators

of losses• Scenario modelling of concentration risks

October 2012Innovation in insurance – Can Europe compete?Slide 16

Concentration risk analyzer

PwC

Focus on underwriting

October 2012Innovation in insurance – Can Europe compete?Slide 17

Underwriting resource requirement

High

Low

Risk complexity

HighLow

Avoid using underwriting talent inefficiently

Find opportunities to automate and standardise to free up underwriting talent

If the risk complexity is high, assign underwriting resource to it

Align underwriting resources to risk complexity

PwC

SMEs are evolving their service models, and needing to interact and transact through a variety of channels…

October 2012Innovation in insurance – Can Europe compete?Slide 18

Survey of small and medium enterprises on Preferred channels for purchasing insurance

Source: Defaqto Insight, ‘The Future is Online’, April 2010Source: ‘Businesses embrace iPads, but don’t know why,’ CNET News, May 2011

There is an increasing use of tablets by businesses for core operations, information gathering and transacting …

… 49% of SMEs now using the Internet to supplement or replace agents and brokers in their search for commercial insurance

We have no plans to deploy tablets

20%We have already deployed tablets

22%

Sometime thisyear (2011)

22%Sometime

next year (2012)24%

In two years(2013)10%

More thantwo yearsfrom now

2%

Would only consider using their Agent/Broker

51% Would use the internet for research and quotes

16%

Would consider using the Internet to buy direct instead of

through an agent…

PwC

The resulting operating model is expected to support unprecedented connectivity, speed and customization

Insurers are reworking their operations to provide complete service and solutions to meet specialized customer and distributor expectations of customized solutions, speedy service and seamless information integration across all channels

October 2012Innovation in insurance – Can Europe compete?Slide 19

13

26

29

19

14

%

Likelihood of scenarios over next 10 years

1. Businesses use online channels to research insurance products, but use traditional channels for purchasing

2. Businesses use online channels for research; some small businesses use online channels for purchasing; however, mid to large companies use traditional channels for purchasing

3. Small and mid-large businesses use multiple channels to interact with insurers expecting speedy service and seamless information integration across all channels

4. Small business customers expect price transparency and customized bundled packages, speedy issuance, service and claims payment; Mid-to-large business customers seek even greater customization

5. A large proportion of commercial products get ‘standardized’ and all business groups (small, mid-market, large) can customize their coverage using agents/brokers and online tools

Source: PwC international Insurer Survey ‘Project Blue’ , 2011-12

PwC

PwC’s recent global CEO survey shows that Insurance is just behind technology, communications, and entertainment sectors in business model innovationInsurance CEOs are ‘significantly increasing’ the emphasis of business model innovation in their company’s overall innovation portfolio

October 2012Innovation in insurance – Can Europe compete?Slide 20

PwC

Businesses are evaluating new ways of thinking about geographies, products, customer segments and channels

October 2012Innovation in insurance – Can Europe compete?Slide 21

Wh

y

Social

Technology

Economy

Environment

Political

Where

What

How

Information advantage

through ‘big data’

Distribution disruption

and customer

revolutionEvolving business models‘big and

fast’

‘Two-speed’ global

growth

1

4

2 3

PwC

Strategic questions to guide your future

October 2012Innovation in insurance – Can Europe compete?Slide 22

What risks and opportunities do these trends and potential disruptors present you (or others)?

1How does what you have today position you for any potential changes?

2

Where might you need to be on a different path?

4Where might you need to stay on the same path but increase investment and speed?

3

PwC

Speaker

October 2012Innovation in insurance – Can Europe compete?Slide 23

David LawGlobal Insurance leaderPartner PwC +44 (0)7710 173 [email protected]

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers does not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2012 PricewaterhouseCoopers LLP. All rights reserved. In this document, "PwC" refers to the UK member firm, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.

121012-104530-RP-OS

Grange St. Paul’s Hotel, London

18 October 2012

2012 Insurance Market Briefing -Europe

United Kingdom Non-Life and London Market

2012 Insurance Market Briefing - Europe 18 October 2012 26

Catherine ThomasDirector, AnalyticsA.M. Best Europe – Rating Services Ltd

UK Non-Life:Current State of the Market

2012 Insurance Market Briefing - Europe 18 October 2012 27

• Profit margins under pressure, in spite of modest rate increases for most lines of business

• Flood losses in June, July and September• Reserve releases expected to make a positive, albeit lower,

contribution to earnings• Low investment returns• Weak economic conditions persist• Partially insulated from financial instability in the Eurozone

Performance of the Top 100 Companies

2012 Insurance Market Briefing - Europe 18 October 2012 28

• Underwriting performance helped by rate increases and benign weather experience in the UK

• Investment earnings down due to financial market volatility and low interest rates

2011 2010

Underwriting result* 1,132 183

Pre-tax profit* 3,144 3,847

Capital and surplus 55,024 52,050

Data: GBP millions

Source: A.M. Best Co. based on FSA returns

Underwriting Result is before transfers to/from Equalisation Provision and includes allocated investment return

Capital and Surplus includes equalisation provisions

*Underwriting result and pre-tax profit do not include data for Aviva Insurance Ltd as comparable 2011 and 2010 data are not available.

UK Motor:Results Improved Last Year

2012 Insurance Market Briefing - Europe 18 October 2012 29

• Substantial rate increases led to better accident-year earnings• Prior-year development stabilised• Upward rate momentum beginning to slow• Claims environment remains unfavourable

UK Motor – Combined Ratios 2007 2008 2009 2010 2011Accident-Year Combined Ratio 113% 115% 122% 114% 105%

Effect of Prior Years Reserve Movements -12% -9% -2% 5% 0%Calendar-Year Combined Ratio 101% 106% 120% 119% 105%

Data based on FSA returns for all firms reporting on a one-year underwriting basis.

Source: Best's Statement File – United Kingdom

40%

45%

50%

55%

60%

65%

70%

75%

80%

2007 2008 2009 2010 2011

20072008200920102011

UK Property:Performance Driven by Weather

2012 Insurance Market Briefing - Europe 18 October 2012 30

• 14 percentage point drop in the gross ultimate loss ratio• Reserve strengthening required for 2010 freeze claims

Gross Ultimate Accident-Year Loss Ratio Development (2007-2011)Source: A.M. Best Co. based on FSA returns

UK Liability:Rate Increases Subdued

2012 Insurance Market Briefing - Europe 18 October 2012 31

• Reserve strengthening required for business written in 2009 and 2010

30%

40%

50%

60%

70%

80%

90%

100%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

2002200320042005200620072008200920102011

Gross Ultimate Accident-Year Loss Ratio Development (2002-2011)Source: A.M. Best Co. based on FSA returns

Employers’ Liability:Accident-Year Loss Ratios

2012 Insurance Market Briefing - Europe 18 October 2012 32

• Increase in trip and slip claims

40%

50%

60%

70%

80%

90%

100%

2009 2010 2011

200920102011

Gross Ultimate Accident-Year Loss Ratio Development (2009-2011)Source: A.M. Best Co. based on FSA returns

Professional Indemnity:Accident-Year Loss Ratios

2012 Insurance Market Briefing - Europe 18 October 2012 33

• Financial crisis related claims experience

40%

50%

60%

70%

80%

90%

100%

2009 2010 2011

200920102011

Gross Ultimate Accident-Year Loss Ratio Development (2009-2011)Source: A.M. Best Co. based on FSA returns

London Market:Catastrophe Losses

2012 Insurance Market Briefing - Europe 18 October 2012 34

London Market Company* Results

Company Currency(millions)

Pre-tax profit 2011

Year end 2011 SHF

Year end 2010 SHF

Net catastrophe losses

2011 cats as a % of 2010 SHF

Aspen Insurance Holdings Ltd USD -143 3,172 3,242 534 16%

Beazley plc USD 63 1,071 1,083 215 20%

Catlin Group Ltd USD 71 3,298 3,448 678 20%

Hiscox Ltd GBP 17 1,256 1,266 270 21%

Amlin plc GBP -194 1,420 1,728 501 29%

Hardy GBP -42 108 153 73 48%

Novae Group plc GBP -6 266 294 70 24%

Omega Insurance Holdings Ltd USD -95 333 422 86 20%

*Listed companies which write a significant portion of their business in the London marketSource: 2011 company report and accounts

Post Event Analysis

2012 Insurance Market Briefing - Europe 18 October 2012 35

• Loss estimate vs risk appetite

• Peer group comparison

• Extent of capital erosion

• Catastrophe risk and aggregate management

• Financial flexibility

London Market 2012

2012 Insurance Market Briefing - Europe 18 October 2012 36

• Material rate increases being achieved for loss affected business• Market conditions for non-catastrophe exposed classes remain

competitive • Capacity has not contracted substantially, in spite of 2011 loss

experience• Stagnant economic growth is curbing demand• Continued favourable reserve development

Lloyd’s Casualty Business

2012 Insurance Market Briefing - Europe 18 October 2012 37

2011 2010 2009 2008 2007 2006

Accident-year combined ratio 98.4% 101.1% 99.1% 103.9% 101.8% 96.3%

Prior year reserve movement -1.8% -4.5% -8.3% -8.8% -9.1% -7.3%

Calendar-year combined ratio 96.6% 96.6% 90.8% 95.1% 92.7% 89.0%

Source: Lloyd's annual reports

M&A Involving Lloyd’s Vehicles(2011-2012)

2012 Insurance Market Briefing - Europe 18 October 2012 38

Acquired Acquirer Deal Value

Hardy Underwriting Bermuda Ltd CNA Financial Corp GBP 143.0 million

Omega Insurance Holdings Ltd Canopius Group Ltd GBP 163.6 million

Flagstone Reinsurance Holdings ANV Holdings BV GBP 31.0 million

Whittington Insurance Markets Ltd Tawa plc, Icat Managers/Paraline Group, Skuld Group Not Disclosed

TSM Agencies Ltd ProSight Specialty Insurance Not Disclosed

Jubilee Group Holdings Ltd Ryan Specialty Group, LLC GBP 35.0 million

Chaucer Holdings plc 440 Tessera Ltd/The Hanover Insurance Group Inc GBP 313.0 million

Brit Insurance Holdings NV Achilles Netherlands Holdings BV GBP 888.0 million

European Non-Life Market Outlook

2012 Insurance Market Briefing - Europe 18 October 2012 39

Sam DobbynAssociate Director, AnalyticsA.M. Best Europe – Rating Services Ltd

Eurozone Financial Crisis

2012 Insurance Market Briefing - Europe 18 October 2012 40

Economy in Recession

2012 Insurance Market Briefing - Europe 18 October 2012 41

6

7

8

9

10

11

12

-6

-4

-2

0

2

4

6

2007 2008 2009 2010 2011 2012

GD

P G

row

th R

ate

(%)

Eurozone GDP Growth and Unemployment Rate

Une

mpl

oym

ent R

ate

(%)

Source: OECD

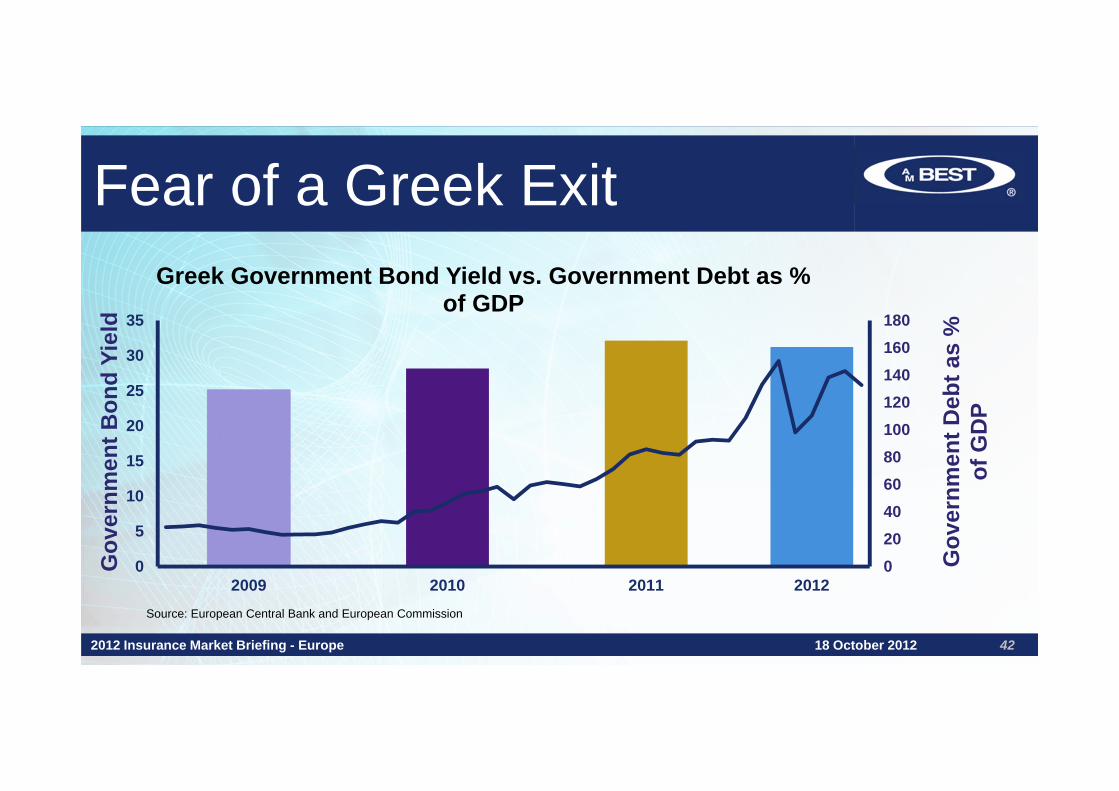

Fear of a Greek Exit

2012 Insurance Market Briefing - Europe 18 October 2012 42

020406080100120140160180

0

5

10

15

20

25

30

35

2009 2010 2011 2012

Greek Government Bond Yield vs. Government Debt as % of GDP

Source: European Central Bank and European Commission

Gov

ernm

ent B

ond

Yiel

d

Gov

ernm

ent D

ebt a

s %

of

GD

P

Italy and Spain: Yields

2012 Insurance Market Briefing - Europe 18 October 2012 43

3

4

5

6

7

8

2008 2009 2010 2011 2012

%

Government Bond Yields

Spain

Source: European Central Bank

Italy

ECB’s Policy Response

2012 Insurance Market Briefing - Europe 18 October 2012 44

ECB Target Policy Rate

Source: European Central Bank

Timeline Recap:Now What?

2012 Insurance Market Briefing - Europe 18 October 2012 45

Portugal receives a

€78bn bailout

25 EU members sign new fiscal

pact

20142013

Greece & Ireland receive EU-IMF loans (€110bn and

€85bn)

Oct. 26: EU

officials unveil plan

Nov.2010

Feb. 2011

Oct. 2011

Dec. 2011

ECB gives banks

3 years of unlimited funds

June 2011

Greece gets 3rd loan

Greece passes austerity

measures in return for

bailout and write- down

debt

Jan.2012

March2012

June2012

Spanish banks receive bailout

EU Summit concluded with

several agreements

Greek Yields: 11.7%

Italian Yields: 4.7%

Spanish Yields: 5.4%

Greek Yields: 21.1%

Italian Yields: 6.8%

Spanish Yields: 5.5%

Greek Yields: 25.8%

Italian Yields: 6.0%

Spanish Yields: 6.8%

What is the future of the Euro?

‘Draghi Plan’ ECB OMT

Sep2012

Will any members leave the

Eurozone?

Economic Pressures

2012 Insurance Market Briefing - Europe 18 October 2012 46

• Recessionary effects

– Less economic activity = lower claims

– This has maintained market profitability despite increase in recession related claims

– Lower demand remains a problem

• Investment effects

– Emphasis on technical profitability

– Search for yield in ‘safe-haven’ countries

Pressure on Ratings

2012 Insurance Market Briefing - Europe 18 October 2012 47

Economic Concerns

– EU Policy hurdles

– Recessionary conditions

– High unemployment

– Backlash to austerity

– Banks recapitalising

– Pressure on top line / performance

Investment risk

– Sovereign debt

– Pressure on FI

– Financial flexibility

– Cost of capital

– Guarantees

– Contagion

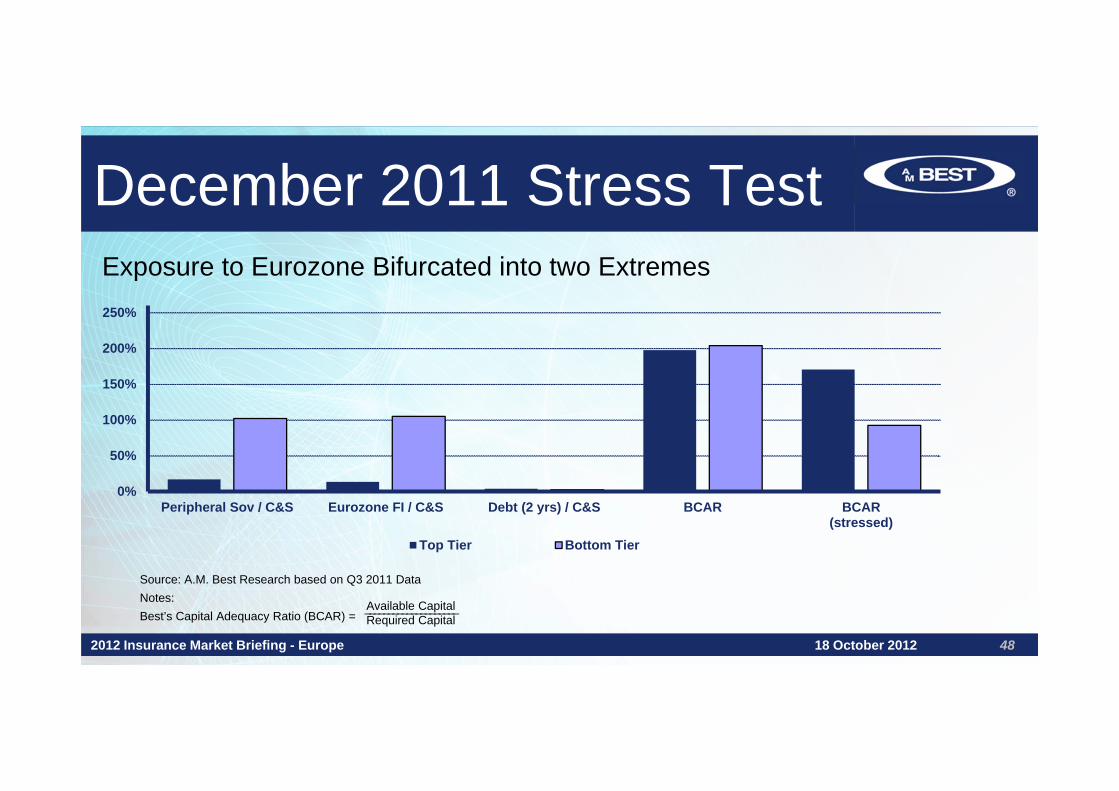

0%

50%

100%

150%

200%

250%

Peripheral Sov / C&S Eurozone FI / C&S Debt (2 yrs) / C&S BCAR BCAR(stressed)

Top Tier Bottom Tier

December 2011 Stress Test

2012 Insurance Market Briefing - Europe 18 October 2012 48

Exposure to Eurozone Bifurcated into two Extremes

Source: A.M. Best Research based on Q3 2011 DataNotes:Best’s Capital Adequacy Ratio (BCAR) =

Available Capital––––––––––––––––––––Required Capital

June 2012 Stress Test

2012 Insurance Market Briefing - Europe 18 October 2012 49

0%

50%

100%

150%

200%

250%

Peripheral Sov / C&S Eurozone FI / C&S Debt (2 yrs) / C&S BCAR BCAR(stressed)

Top Tier Bottom Tier

Companies are Managing Down Eurozone Exposure

Source: A.M. Best Research based on Q3 2011 DataNotes:Best’s Capital Adequacy Ratio (BCAR) =

Available Capital––––––––––––––––––––Required Capital

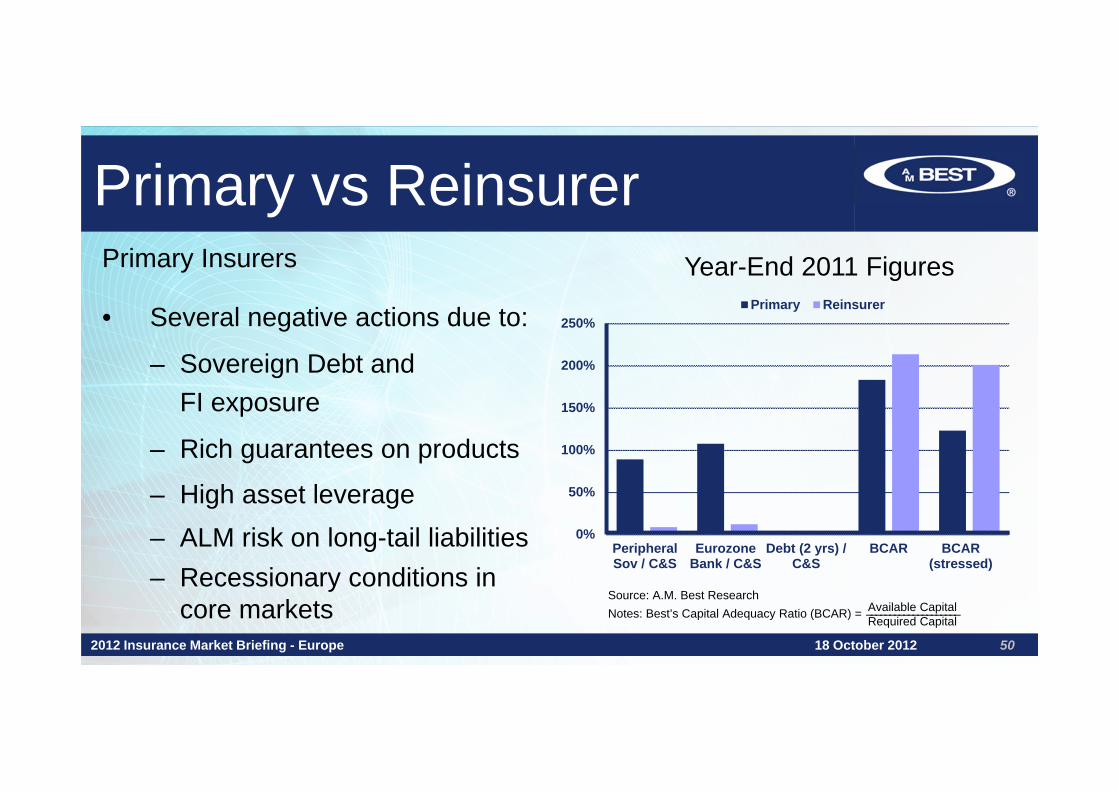

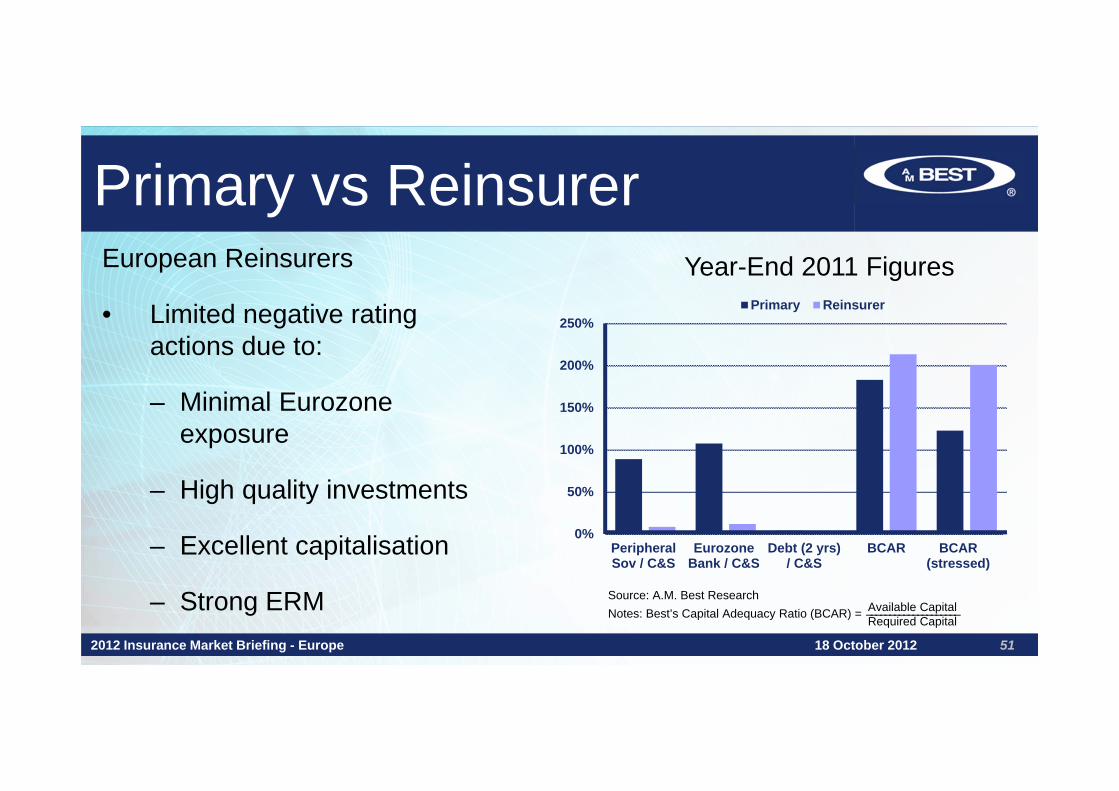

Primary vs Reinsurer

2012 Insurance Market Briefing - Europe 18 October 2012 50

Primary Insurers

• Several negative actions due to:

– Sovereign Debt and FI exposure

– Rich guarantees on products

– High asset leverage– ALM risk on long-tail liabilities– Recessionary conditions in

core markets

Year-End 2011 Figures

0%

50%

100%

150%

200%

250%

PeripheralSov / C&S

EurozoneBank / C&S

Debt (2 yrs) /C&S

BCAR BCAR(stressed)

Primary Reinsurer

Source: A.M. Best ResearchNotes: Best’s Capital Adequacy Ratio (BCAR) = Available Capital––––––––––––––––––––Required Capital

Primary vs Reinsurer

2012 Insurance Market Briefing - Europe 18 October 2012 51

European Reinsurers

• Limited negative rating actions due to:

– Minimal Eurozone exposure

– High quality investments

– Excellent capitalisation

– Strong ERM

Year-End 2011 Figures

0%

50%

100%

150%

200%

250%

PeripheralSov / C&S

EurozoneBank / C&S

Debt (2 yrs)/ C&S

BCAR BCAR(stressed)

Primary Reinsurer

Source: A.M. Best ResearchNotes: Best’s Capital Adequacy Ratio (BCAR) = Available Capital––––––––––––––––––––Required Capital

Company Actions

2012 Insurance Market Briefing - Europe 18 October 2012 52

• Hedging Activity

• Adverse scenario planning

• De-risking investment portfolio

• Maintaining strong cash position

• Focusing on price adequacy / risk selection

Outlook

2012 Insurance Market Briefing - Europe 18 October 2012 53

• Increase in negative rating actions over the past twelve months

• Increase in assignment of negative rating outlooks

• On-going discussions with management

• Consideration for ERM, earnings strength and competitive market position

• Monitor investment portfolios

• Legislative developments critical to solving crisis

European Life Insurance Market Outlook

2012 Insurance Market Briefing - Europe 18 October 2012 54

Carlos Wong-FupuySenior Director, AnalyticsA.M. Best Europe – Rating Services Ltd

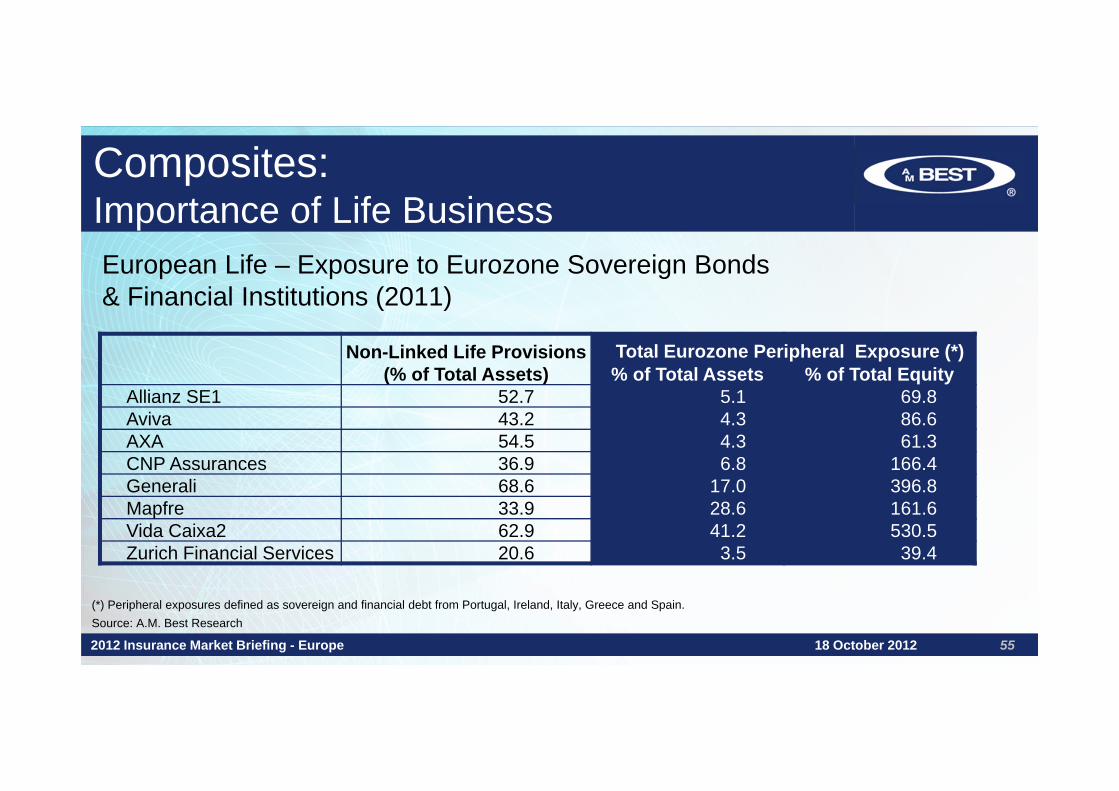

Non-Linked Life Provisions (% of Total Assets) % of Total Assets % of Total Equity

Allianz SE1 52.7 5.1 69.8Aviva 43.2 4.3 86.6AXA 54.5 4.3 61.3CNP Assurances 36.9 6.8 166.4Generali 68.6 17.0 396.8Mapfre 33.9 28.6 161.6Vida Caixa2 62.9 41.2 530.5Zurich Financial Services 20.6 3.5 39.4

Composites:Importance of Life Business

2012 Insurance Market Briefing - Europe 18 October 2012 55

European Life – Exposure to Eurozone Sovereign Bonds & Financial Institutions (2011)

Total Eurozone Peripheral Exposure (*)

(*) Peripheral exposures defined as sovereign and financial debt from Portugal, Ireland, Italy, Greece and Spain.Source: A.M. Best Research

Composites:Importance of Life Business

2012 Insurance Market Briefing - Europe 18 October 2012 56

Savings participatory Business – Historically Two Models

asset ‐ equity driven

asset ‐ fixed income driven

policy values

0 t

€/£

Composites:Importance of Life Business

2012 Insurance Market Briefing - Europe 18 October 2012 57

• Equity Driven Model – Stock market crisis late 1990s

- Deliberate asset liability mis-matching pursuing higher expected returns. Sizeable surpluses

- Asset shares < Policy values

- Options and guarantees reduced

- Investment portfolios de-risked

- Model virtually abandoned and closed to new business

Composites:Importance of Life Business

2012 Insurance Market Briefing - Europe 18 October 2012 58

• Fixed Income Driven Model – much less affected

– Tighter ALM. Less room for surpluses

– OK for as long as moderate yields could be achieved

– Sovereign credit risk has not been an issue

Composites:Importance of Life Business

2012 Insurance Market Briefing - Europe 18 October 2012 59

German Life – Guaranteed Rates & Net Investment Returns (2006-2012)

0%

1%

2%

3%

4%

5%

6%

2006 2007 2008 2009 2010 2011 2012

Minimum guaranteed rates

Current return onpolicyholder's creditbalance

Average guaranteedreturn across all lifecontracts

Net return on investments

Source: GDV and Deutsche Bundesbank eurosystem

Composites:Significance of Life Business

2012 Insurance Market Briefing - Europe 18 October 2012 60

French Life – Return on Investment (2011) (Gross of tax)

-20 -15 -10 -5 0 5 10

Traditional Life Insurance

Unit-Linked Life Insurance

Livret A (savings account)

PEL (home savings plan)

Equities

Real Estate

Source: FFSA

Composites:Significance of Life Business

2012 Insurance Market Briefing - Europe 18 October 2012 61

• Today’s challenges:

– Low interest rate environments

– Consumer appetite for “old style” with-profits

– Domestic investments “match” consumers’ investment profile

– Life insurers’ role as institutional investors

– Regulatory approach to sovereign credit risk

Composites:Importance of Life Business

2012 Insurance Market Briefing - Europe 18 October 2012 62

Available options:• Reduce guarantees? Close to new business? • Move to unit-linked?• Accept “some” level of credit risk?

– Even if assuming a zero default risk:• Need to manage cash flow generation very carefully• In particular given the increase in surrenders and lapses• And declines in new business

Composites:Importance of Life Business

2012 Insurance Market Briefing - Europe 18 October 2012 63

Italy: Life market compositionJuly2012

July2011

Amount(EUR millions) %

Amount(EUR millions) % Variance

Traditional Products 22,598 76.2% 28,205 81.3% -19.9%

Linked Products 7,017 23.7% 6,456 18.6% 8.7%

Others 48 0.2% 48 0.1% -0.6%

Total 29,663 34,709 -14.5%Source: ANIA fact-pack mercato vita, September 2012

Composites:Importance of Life Business

2012 Insurance Market Briefing - Europe 18 October 2012 64

France: Performance of life sector

2011 2010 2009 2008 2007

Life premiums 124 147.8 140.7 138.4 152

Claims paid 117 94 87.1 106.8 82.6 Increase/decrease in math reserves -13.5 53.4 65.3 -28.4 77.6

Technical result 1.5 4.2 4 2.5 5

Overall result 2.8 4.2 3.9 4.1 5.1

EUR billionsSource: FFSA

Composites:Importance of Life Business

2012 Insurance Market Briefing - Europe 18 October 2012 65

Conclusions:• Any change in new business strategy is likely to take time• Assets risks to remain in the balance sheet for a while• Eurozone stress BCAR recognises:

- Any surpluses in savings participatory funds- The ability of PH liabilities partially to absorb investment losses

• But this ability is not unlimited, due to contractual and business reasons

Reinsurance Panel

2012 Insurance Market Briefing - Europe 18 October 2012 66

Chair:Nick Charteris-Black, Managing Director, Market Development - EMEAA.M. Best EuropeDavid Flandro, Managing Director, Head of Global Business, Guy Carpenter & Co LtdJohn Andre, Group Vice President, A.M. Best CompanySam Dobbyn, Associate Director, Analytics, A.M. Best Europe

Current Position

2012 Insurance Market Briefing - Europe 18 October 2012 67

• Capitalisation strong on both an absolute and risk-adjusted basis• Both base line and stressed capital ratios trending favourably• Capital stress tested for catastrophe losses and negative economic

scenarios– Catastrophe stress test includes two PMLs– Multiple economic stress tests contemplating write down of assets– Diminished level of reserve adequacy consequence

of soft casualty market• Companies performed well through live stress tests• Financial flexibility constrained by current stock valuations, however

capital markets remained accessible

Current Position

2012 Insurance Market Briefing - Europe 18 October 2012 68

• Rating actions reflect the financial resilience of the market• Mostly affirmations, average rating for the sector is ICR “a+” FSR ”A”• Multiple loss events in 2011 detracted from earnings but within loss

tolerances• Impact from underwriting losses were tempered by investment income

and capital gains on investments• Companies took advantage of the low interest rate environment to

refinance existing debt and extend duration • Favourable trends have continued through six months 2012 with global

capital up about 7%

Global Reinsurance Rating Outlook

2012 Insurance Market Briefing - Europe 18 October 2012 69

• Outlook remains stable

• Loss events, though large, equated to earnings events

• Capital cushion only slightly eroded, balance sheets remain sound

• Asset risk conservatively managed

• Market remains disciplined from an underwriting perspective

• Pricing momentum has turned positive (for now)

• Enterprise risk management tested and functioning well

Global Reinsurance Rating Outlook

2012 Insurance Market Briefing - Europe 18 October 2012 70

• Concerns:

– Possibility for short-lived pricing improvements– Investment situation puts more emphasis on underwriting

margins– Regulatory uncertainty– Financial flexibility

Developments in Central and Eastern Europe

2012 Insurance Market Briefing - Europe 18 October 2012 71

Carlos Wong-FupuySenior Director, AnalyticsA.M. Best Europe – Rating Services Ltd

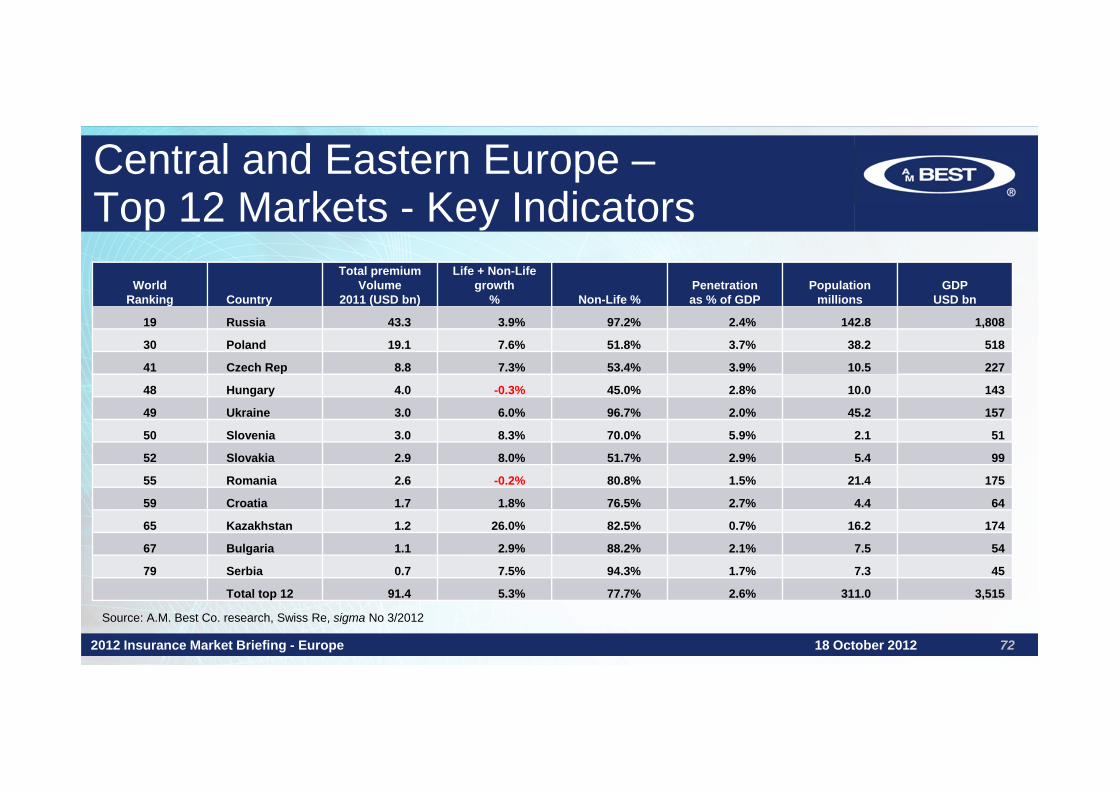

Central and Eastern Europe –Top 12 Markets - Key Indicators

2012 Insurance Market Briefing - Europe 18 October 2012 72

WorldRanking Country

Total premium Volume

2011 (USD bn)

Life + Non-Lifegrowth

% Non-Life %Penetrationas % of GDP

Populationmillions

GDPUSD bn

19 Russia 43.3 3.9% 97.2% 2.4% 142.8 1,808

30 Poland 19.1 7.6% 51.8% 3.7% 38.2 518

41 Czech Rep 8.8 7.3% 53.4% 3.9% 10.5 227

48 Hungary 4.0 -0.3% 45.0% 2.8% 10.0 143

49 Ukraine 3.0 6.0% 96.7% 2.0% 45.2 157

50 Slovenia 3.0 8.3% 70.0% 5.9% 2.1 51

52 Slovakia 2.9 8.0% 51.7% 2.9% 5.4 99

55 Romania 2.6 -0.2% 80.8% 1.5% 21.4 175

59 Croatia 1.7 1.8% 76.5% 2.7% 4.4 64

65 Kazakhstan 1.2 26.0% 82.5% 0.7% 16.2 174

67 Bulgaria 1.1 2.9% 88.2% 2.1% 7.5 54

79 Serbia 0.7 7.5% 94.3% 1.7% 7.3 45

Total top 12 91.4 5.3% 77.7% 2.6% 311.0 3,515

Source: A.M. Best Co. research, Swiss Re, sigma No 3/2012

Central and Eastern Europe –Top 12 Markets - Key Indicators

2012 Insurance Market Briefing - Europe 18 October 2012 73

Total CEE – Top 12 Comparable to

Population > 300 million United States

GDP > USD 3,500 billion Germany /Brazil + Mexico combined

Total premiums > USD 90 billion Australia

Penetration (% of GDP) 2.6% Latin AmericaMoroccoBahrain

EU Countries + Croatia and Serbia

2012 Insurance Market Briefing - Europe 18 October 2012 74

Impact from Financial Crisis

Country € Comments ImpactPoland N Importance of domestic market Moderate

Czech Republic N EU exports / Germany, Italy Moderate

Hungary N High foreign debt / devaluation / low FDI Severe

Slovenia Y High indebtedness / banking crisis Severe

Slovakia Y EU exports / Germany Moderate

Romania N Slight recovery / Weak fundamentals Severe

Croatia N Early stages of privatisation and FDI Severe

Bulgaria Peg High FDI / Weak institutions Severe

Serbia N Dependent on EU exports / Weak institutions Severe

0% 10% 20% 30% 40% 50% 60% 70% 80%

Poland

Czech Republic

Hungary

Slovenia

Slovakia

Romania

Croatia

Bulgaria

Serbia

EU Average

EU Countries + Croatia and Serbia

2012 Insurance Market Briefing - Europe 18 October 2012 75

Motor business as a % of non-life premiums

EU Countries + Croatia and Serbia

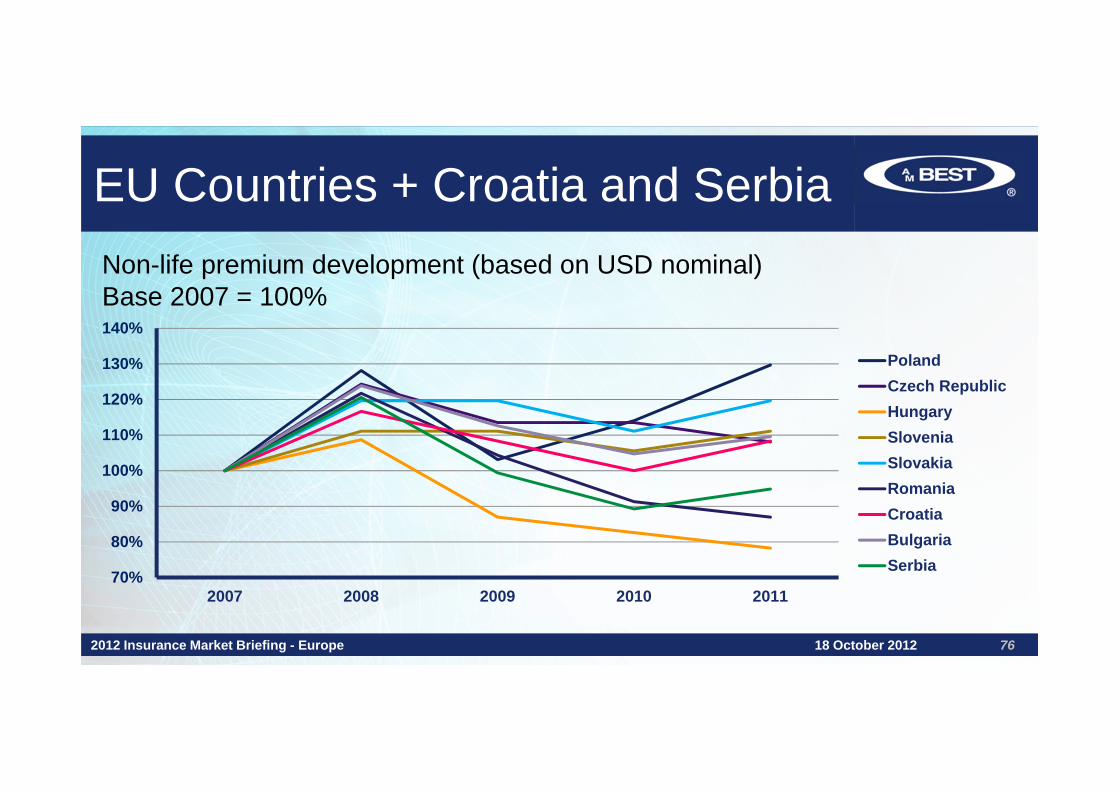

2012 Insurance Market Briefing - Europe 18 October 2012 76

Non-life premium development (based on USD nominal)Base 2007 = 100%

70%

80%

90%

100%

110%

120%

130%

140%

2007 2008 2009 2010 2011

PolandCzech RepublicHungarySloveniaSlovakiaRomaniaCroatiaBulgariaSerbia

EU Countries + Croatia and Serbia

2012 Insurance Market Briefing - Europe 18 October 2012 77

• Severe losses due to floods in the region in 2010• Hardening pricing environment since then• In general, profitable technical accounts despite strong competition in

particular in MTPL• Romania loss making after EU accession and market liberalisation• Croatia – profits driven by MTPL / pre-liberalisation / still rigid market

dominated by national insurer / shrinking market• Most markets slightly contracting in real terms

EU Countries + Croatia and Serbia

2012 Insurance Market Briefing - Europe 18 October 2012 78

Foreign Participants• Main foreign players –

– VIG, Allianz, Generali, Ergo, Uniqa– Also KBC, Groupama– Recently Talanx/HDI: Poland’s Warta

• Retentions increased • International programmes – from proportional to XL

EU Countries + Croatia and Serbia

2012 Insurance Market Briefing - Europe 18 October 2012 79

State Participation• Poland: PZU• Slovenia: Triglav and Sava Re• Croatia: Croatia Osiguranje• Romania and Serbia: Disaster pools• Credit Insurance• Regional expansion plans

Central and Eastern Europe –Russia, Ukraine and Kazakhstan

2012 Insurance Market Briefing - Europe 18 October 2012 80

• Commodity driven economies• Relatively low level of foreign participation• Ukraine and Kazakhstan – source of reinsurance business

into Russia• Market trends towards consolidation• Tax avoidance schemes remain an issue• Extremely low loss ratios – debatable insurance content?• Poor quality of asset portfolios• Low capitalisation in an overcrowded market

Central and Eastern Europe –Russia, Ukraine and Kazakhstan

2012 Insurance Market Briefing - Europe 18 October 2012 81

Non-life premium development (based on USD nominal)Base 2007 = 100%

60%

70%

80%

90%

100%

110%

120%

130%

140%

2007 2008 2009 2010 2011

RussiaUkraineKazakhstan

Central and Eastern Europe –Russia

2012 Insurance Market Briefing - Europe 18 October 2012 82

Foreign Participation• 25% foreign shareholding cap – to 50% following WTO accession• Generali (Ingosstrakh), Allianz (Rosno), AXA (Reso Garantia)• Interest from International Development Banks

Central and Eastern Europe –Russia, Ukraine and Kazakhstan

2012 Insurance Market Briefing - Europe 18 October 2012 83

• Mainly local ownership• Strong links with industrial groups• Banking ownership – KZ• No direct state participation except for credit insurance

and State Annuity company in Kazakhstan

Central and Eastern Europe –Russia, Ukraine and Kazakhstan

2012 Insurance Market Briefing - Europe 18 October 2012 84

Market trends towards consolidationCountry GWP

USD bnNumber of companies

Average GWPUSD mn

Top 5 companies

Russia 43.3 600 72.0 40%

Ukraine 3.0 450 6.7 30%

Kazakhstan 1.2 38 31.6 45%

Conclusions

2012 Insurance Market Briefing - Europe 18 October 2012 85

CEE – EU countries, Croatia and Serbia

• Almost all countries, except for Poland, Czech Republic and Slovakia severely impacted by the financial crisis

• Foreign investor presence important

• Retentions relatively high • Market motor driven• State control still material in some economies• Consolidation opportunities

Conclusions

2012 Insurance Market Briefing - Europe 18 October 2012 86

CEE – Russia, Ukraine, Kazakhstan

• Some recovery after severe crisis in 2008-09

• Poor quality of investment portfolios

• Low capitalisation: Russia and Ukraine

• Dominated by local companies

• Strong links to industrials and banks

• “Financial schemes” remain an issue

• Consolidation opportunities

Middle East, North Africa and Takaful

2012 Insurance Market Briefing - Europe 18 October 2012 87

Mahesh MistryAssociate Director, AnalyticsA.M. Best Europe – Rating Services Ltd

Middle East & North Africa Overview

2012 Insurance Market Briefing - Europe 18 October 2012 88

• Despite challenging market conditions, the Middle East & North Africa insurance markets continue to grow

• The slowdown is attributed to depressed financial markets, regional political instability and delay in the implementation of compulsory lines

Gross Premiums Written for Middle East & North Africa

0%

10%

20%

30%

40%

0

5

10

15

20

25

2005 2006 2007 2008 2009 2010 2011 2012e

Gro

wth

(% C

hang

e)

(USD

bill

ions

)

Source: A.M. Best research (excludes Israel and Iran)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

UAE SaudiArabia

Morocco Egypt Lebanon Algeria Qatar Tunisia Kuwait Oman Jordan Bahrain

USD

(bill

ions

) Non-Life Life

Source: A.M. Best research – Life and Non‐Life Premium Volumes (2011)

Middle East & North Africa Overview

2012 Insurance Market Briefing - Europe 18 October 2012 89

• Dominated by the UAE and the Saudi Arabia, with non-life being the key component in the region

Middle East & North Africa Overview

2012 Insurance Market Briefing - Europe 18 October 2012 90

• Young markets with significant potential

+ Small market size, with low penetration rates

+ Oil prices above budgets will foster growth in the region

+ Expansion of compulsory lines

+ Changing demographics in the region- Political instability creates

challenging environment

• Competition

+ Top players consolidating their position

+ Slowdown in new entrants- Fragmented markets- Companies chasing top line growth

+/- Regional expansion by top players+/- Consolidation / M&A

Middle East & North Africa:Political Instability

2012 Insurance Market Briefing - Europe 18 October 2012 91

• Slowdown in growth in affected markets

• Rated companies have shown resilience, despite difficult trading conditions

• Tightening of policy wordings

• Review of risk management and business continuity plans

• The longer the disruption, the greater the impact on their country risk and company ratings

• Operating environment is more challenging

Country Country Risk Tier

Political Risk Assessment

Algeria CRT-5 Low

Bahrain CRT-3 Moderate

Egypt CRT-5 High

Jordan CRT-4 Low

Libya CRT-5 High

Morocco CRT-4 Low

Syria CRT-5 High

Tunisia CRT-5 High

Source: AM Best, September 2012

CRT-1 (low risk) to CRT-5 (high risk)

Middle East & North Africa:Technical Performance

2012 Insurance Market Briefing - Europe 18 October 2012 92

• Strong, albeit declining technical profitability

• New entrants and fierce competition adds pressure on performance

• Low retention on commercial lines highlights dependence on inward reinsurance commission

• Top companies maintain strong underwriting performance

• Smaller players’ profitability under strain

A.M. Best Rated Primary Insurers Technical Performance (2006-2011)

0%10%20%30%40%50%60%70%80%90%100%

201120102009200820072006

Combined ratio Loss ratioExpense ratio Acquisition cost ratio

Middle East & North Africa:Investment Profile

2012 Insurance Market Briefing - Europe 18 October 2012 93

• Weak investment profiles / aggressive strategies

• High asset concentration in equities and real estate

• High concentration in financial institutions, restricted to few assets

• Profitability impacted by volatile investment performance

• Gradual de-risking of investment profile

• Investment strategy largely dictated by board

A.M. Best Rated Primary Insurers Investment Split

12%10%11%9%9%10%

21%24%22%28%41%36%

16%15%15%12%

8%8%

12%12%11%10%

10%13%

38%39%41%40%32%33%

0%

25%

50%

75%

100%

201120102009200820072006Others Shares Real estate Bonds Cash

Middle East & North Africa:Strong Capital but Weak ERM

2012 Insurance Market Briefing - Europe 18 October 2012 94

• Balance Sheet Strength+ Strong risk-adjusted capitalisation+ Absorb aggressive investment policy+ No leverage+ Low CAT exposure– Surplus capital used for aggressive

investment policy– Limited capital modelling capabilities– High dividend payout ratios– High counter-party credit risk

• ERM+ Some companies have made

significant improvements+ Deployment of resources and skills

should improve controls and risk mitigation

– Generally low ERM awareness– Dependence on consultants– Models are in use, however, with

limited understanding

Middle East & North Africa: Takaful

2012 Insurance Market Briefing - Europe 18 October 2012 95

• Global Takaful contributions reached USD 8.3 billion in 2010, up 19% from 2009

• The five-year compound annual growth rate between 2005-2009 was 29%

207 285 375 453 610 694544 695 901 11091479

1951

174239

558842

991

1313

1065

1850

2289

2911

3896

4370

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

2005 2006 2007 2008 2009 2010e

SaudiCooperative

GCC (exclKSA)

S.E. Asia

Other

Source: Ernst & Young World Takaful Report 2012

Basic Takaful Model

2012 Insurance Market Briefing - Europe 18 October 2012 96

Takaful

2012 Insurance Market Briefing - Europe 18 October 2012 97

• Competition– Compete in the same space as

conventional insurers– Conventional companies expanding

offering through Takaful windows or subsidiaries

• Weak capital strength of policyholders’ fund– Difficulty in generating surpluses in the

policyholders’ fund• Poor underwriting results• High management charges and

fees

– Dependence on Qard’ Hasan– Gradual improvement in surplus

generation• Regulation

– Lack of transparency on regulation implies unclear protection to policyholders

– Conflict between regulators and Sharia board

– Stronger regulation expected as countries adopt specific Takaful regulation

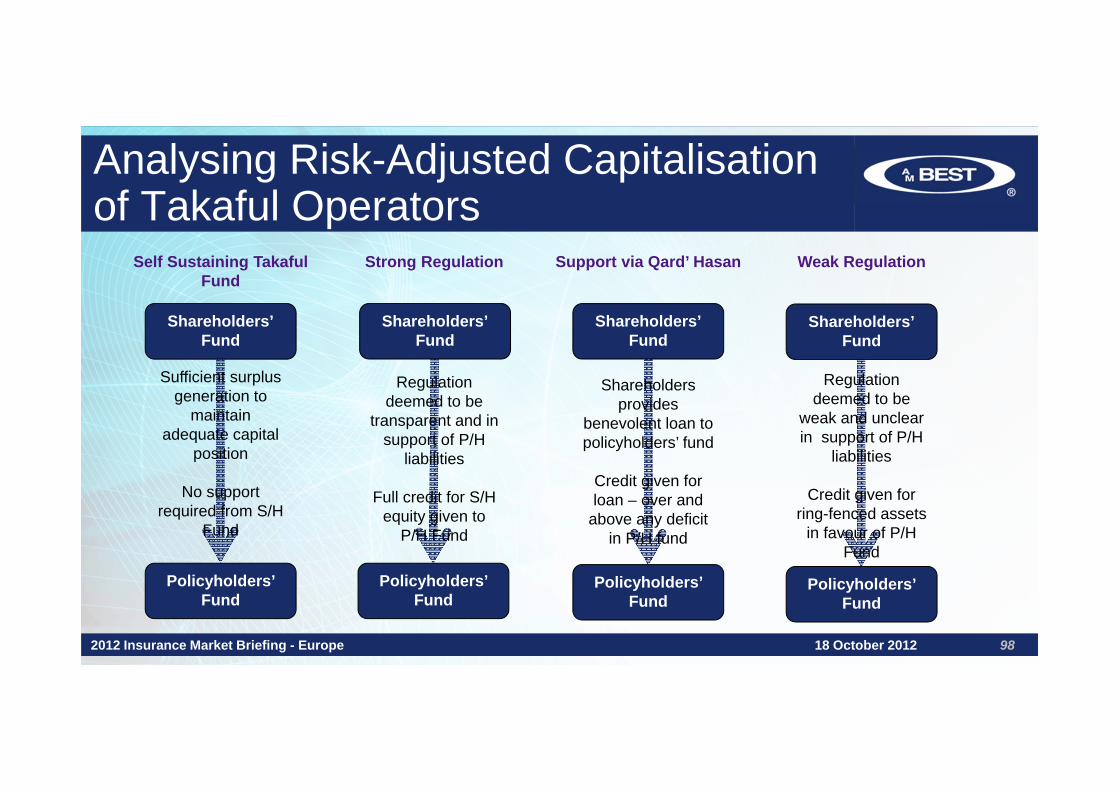

Analysing Risk-Adjusted Capitalisation of Takaful Operators

2012 Insurance Market Briefing - Europe 18 October 2012 98

Self Sustaining Takaful Fund

Shareholders’Fund

Policyholders’ Fund

Sufficient surplus generation to

maintain adequate capital

position

No support required from S/H

Fund

Shareholders’Fund

Policyholders’ Fund

Regulation deemed to be

transparent and in support of P/H

liabilities

Full credit for S/H equity given to

P/H Fund

Strong Regulation

Shareholders’Fund

Policyholders’ Fund

Support via Qard’ Hasan

Shareholders provides

benevolent loan to policyholders’ fund

Credit given for loan – over and

above any deficit in P/H fund

Shareholders’Fund

Policyholders’ Fund

Weak Regulation

Regulation deemed to be

weak and unclear in support of P/H

liabilities

Credit given for ring-fenced assets

in favour of P/H Fund

Middle East & North Africa:Conclusion

2012 Insurance Market Briefing - Europe 18 October 2012 99

• Market Potential– Growth by energy prices and expansion of compulsory medical – Changing dynamics of underlying population

• Political instability– Create volatility and reduce growth prospects– Longer disruptions may impact ratings

• Competition– Expected to be fierce with top companies strengthening their

positions, with consolidation expected in the medium term

Middle East & North Africa:Conclusion

2012 Insurance Market Briefing - Europe 18 October 2012 100

• ERM– Current climate highlights weaknesses (capital and investment

management, regional instability)– Rebalancing of portfolios; focus on underwriting over investments

activity• Regulation

– Must keep pace as companies and markets continue to develop– Start regulating and increasing insurance awareness

Q & A

2012 Insurance Market Briefing - Europe 18 October 2012 101

Nick Charteris-Black, Managing Director, Market Development - EMEAA.M. Best Europe

2012 Insurance Market Briefing - Europe 18 October 2012 102

© AM Best Company (AMB) and/or its licensors and affiliates. All rights reserved. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY COPYRIGHT LAW AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT AM Best Company PRIOR WRITTEN CONSENT. All information contained herein is obtained by AMB from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. Under no circumstances shall AM Best Company have any liability to any person or entity for (a) any loss or damage in whole or in part caused by, resulting from, or relating to, any error (negligent or otherwise) or other circumstance or contingency within or outside the control of AM Best or any of its directors, officers, employees or agents in connection with the procurement, collection, compilation, analysis, interpretation, communication, publication or delivery of any such information, or (b) any direct, indirect, special, consequential, compensatory or incidental damages whatsoever (including without limitation, lost profits), even if AM Best Company is advised in advance of the possibility of such damages, resulting from the use of or inability to use, any such information. The ratings, financial reporting analysis, projections, and other observations, if any, constituting part of the information contained herein are, and must be construed solely as, statements of opinion and not statements of fact or recommendations to purchase, sell or hold any securities. NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY AM BEST COMPANY IN ANY FORM OR MANNER WHATSOEVER. Each rating or other opinion must be weighed solely as one factor in any investment decision made by or on behalf of any user of the information contained herein, and each such user must accordingly make its own study and evaluation of each security and of each issuer and guarantor of, and each provider of credit support for, each security that it may consider purchasing, holding or selling.

Grange St. Paul’s Hotel, London

18 October 2012

2012 Insurance Market Briefing -Europe