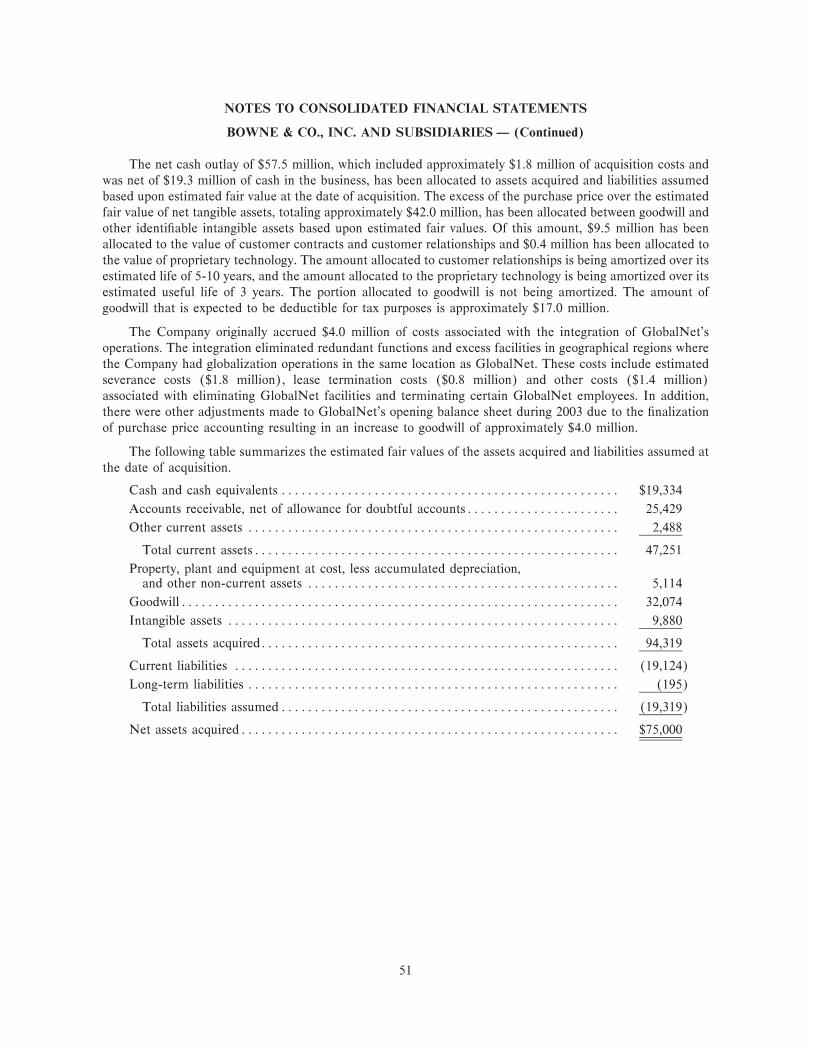

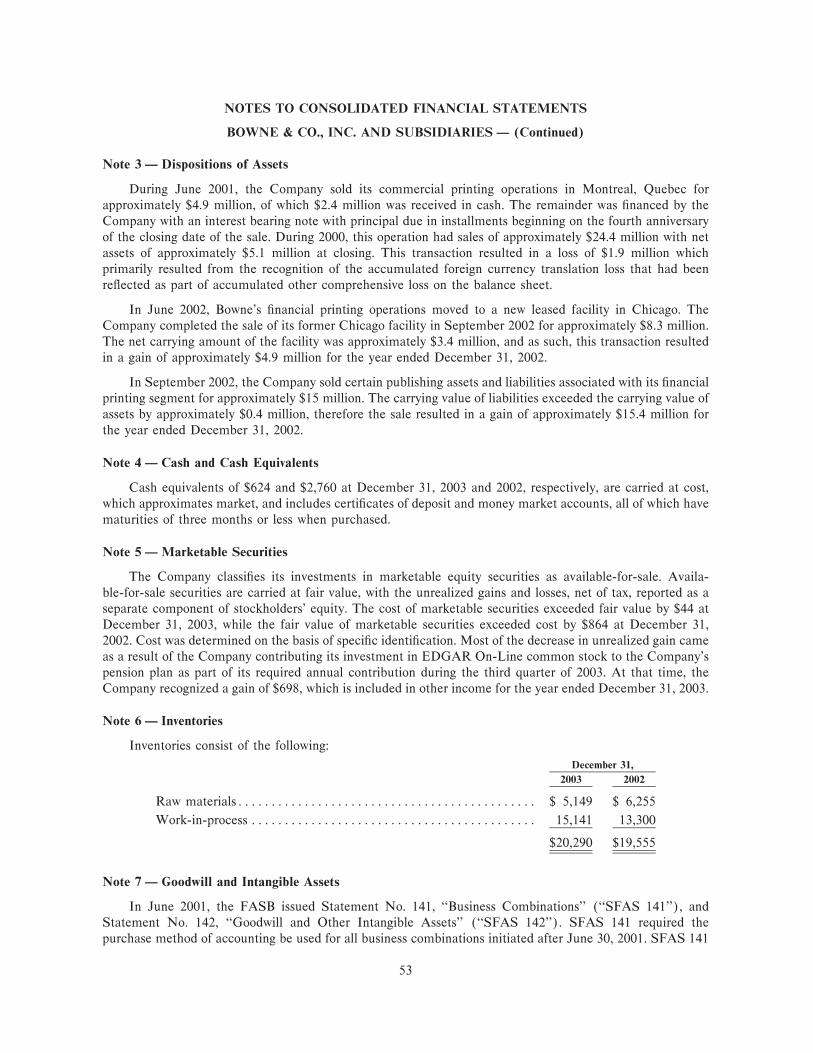

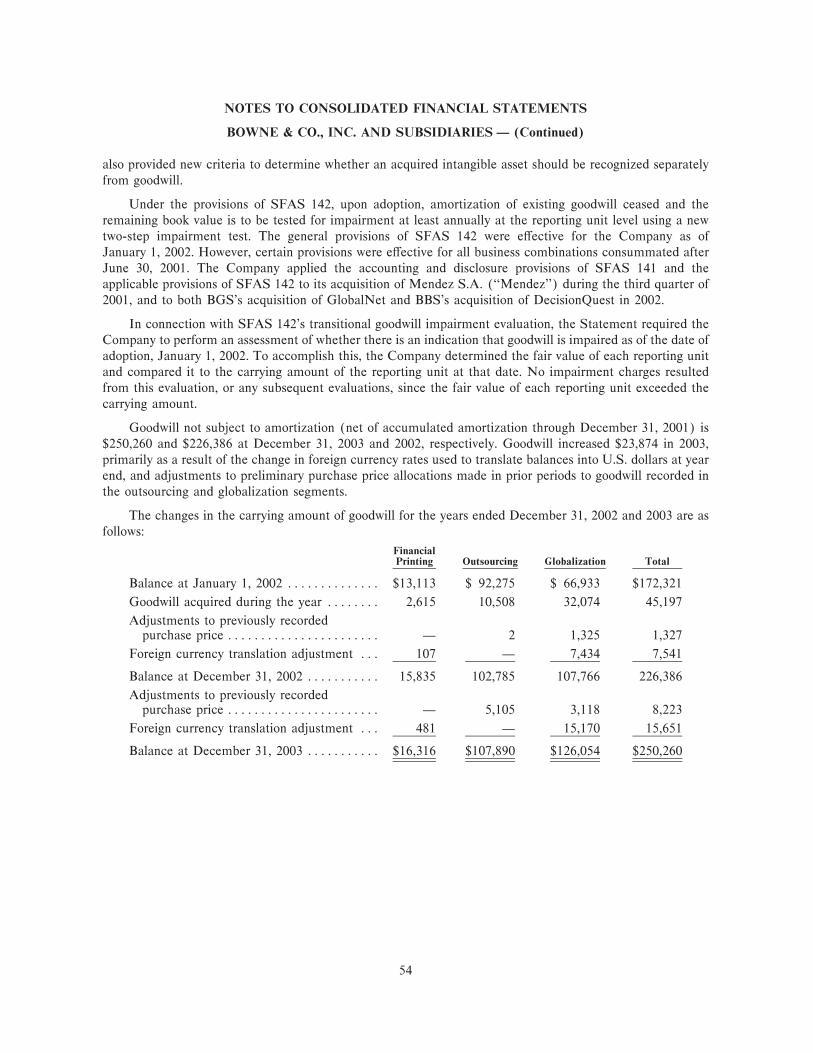

Embed Size (px)

Citation preview

009407_Bowne cover cmyk 4/6/04 2:21 PM Page 1

Opportunity

Table of ContentsFinancial Highlights p1Letter from the Chairman p2Greater Efficiencies p4Smarter Approaches p9Future Opportunities p11Letter from the CFO p14Leadership p15Corporate Governance p16Form 10-K

DisciplinFrom adversity comes strengthFrom strength comes discipline And from discipline comes opportunity

A BLUEPRINT FOR SUCCESS:It has been a rough ride in the global economy and capital markets these past few years.

Companies could easily be forgiven for just tightening their belts and awaiting the rebound. At Bowne,

we took action. We made some tough decisions, but we strengthened our company and our market

leadership position in all our business segments. Our efforts have produced greater efficiencies,

smarter approaches and enhanced capabilities. The discipline to do what is needed, in good times and

bad, has served us well throughout our history. And it continues to give us a competitive advantage

in capturing greater opportunities for growth as the economy gains strength.

Design by Addison www.addison.comBowne & Co., Inc. is an equal opportunity employer.Bowne,® Empowering Your Information,SM BowneFAX,TM

BowneFile16,® BowneLink,® DecisionQuest,® Elcano,TM

Litigation Lifecycle,TM RapidView,TM SecuritiesConnect,TM

and XMarkTM are trademarks or service marks of the Bowne companies.©2004 Bowne & Co., Inc.

Read more about Bowne’s business segments and their blueprints for future success and opportunity by visiting our Website at www.bowne.com.

About Bowne & Co., Inc.—Bowne & Co., Inc. (NYSE: BNE), founded in 1775, is a global leader

in providing high-value solutions that empower our clients’ communications.

Bowne Financial Print —The world’s largest financial printer and leading EDGAR filer, specializing

in the creation, management, translation and distribution of regulatory and compliance documents.

Within this segment, Bowne Enterprise Solutions provides digital printing and electronic delivery

of personalized communications that enable companies to strengthen relationships and increase

market leadership.

Bowne Business Solutions —A full array of business process outsourcing and litigation support

services that seamlessly integrate technology and operational support.

Bowne Global Solutions —A broad range of language and cultural solutions that use translation,

localization, technical writing and interpretation services to help companies adapt their

communications or products for use in other cultures and countries around the world.

Bowne combines all of these capabilities with superior customer service, new technologies,

confidentiality and integrity to manage, repurpose and distribute a client’s information to any

audience, through any medium, in any language, anywhere in the world.

009407_Bowne cover cmyk 4/6/04 2:21 PM Page 2

(1) Includes 906 employeesfrom Berlitz GlobalNet andDecisionQuest acquisitionsin 2002

(2) Current assets divided bycurrent liabilities

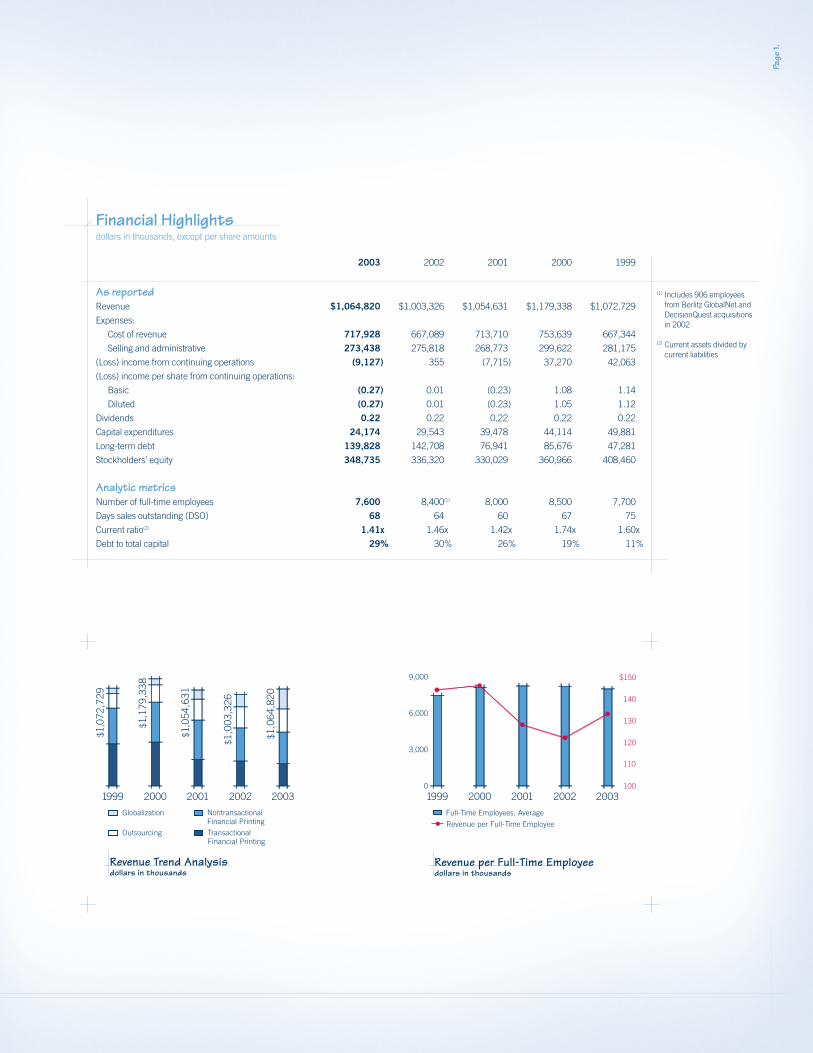

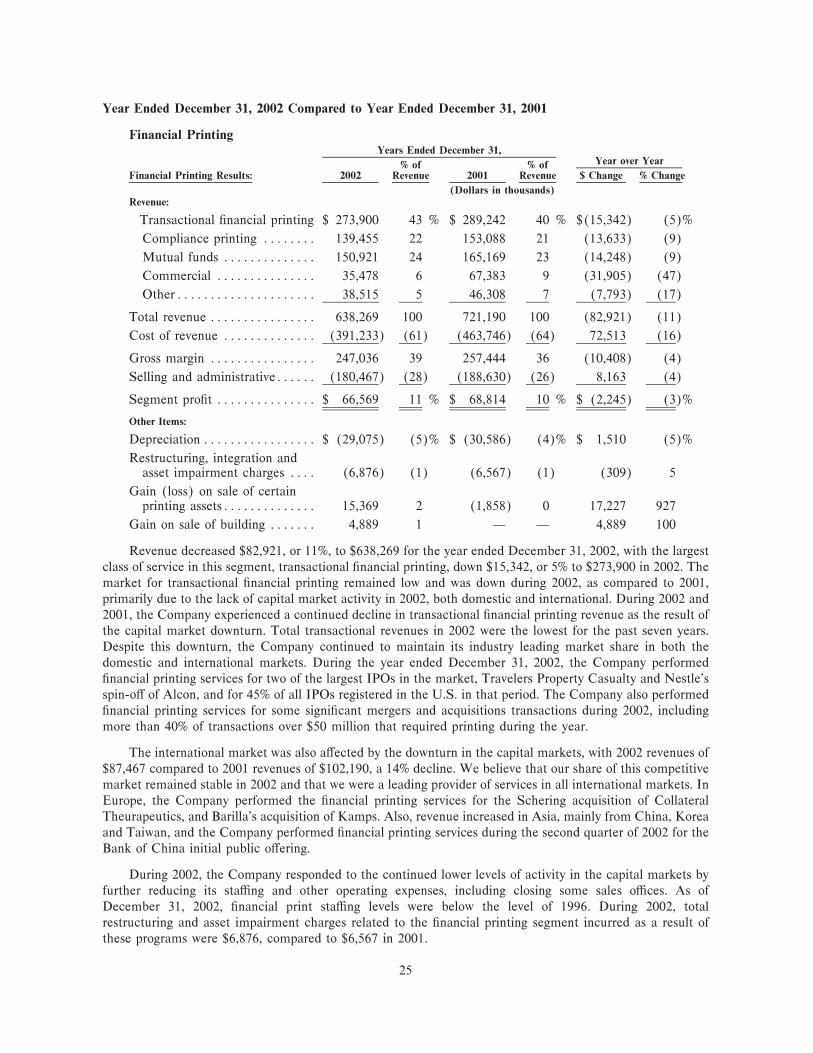

Financial Highlightsdollars in thousands, except per share amounts

2003 2002 2001 2000 1999

As reportedRevenue $1,064,820 $1,003,326 $1,054,631 $1,179,338 $1,072,729

Expenses:

Cost of revenue 717,928 667,089 713,710 753,639 667,344

Selling and administrative 273,438 275,818 268,773 299,622 281,175

(Loss) income from continuing operations (9,127) 355 (7,715) 37,270 42,063

(Loss) income per share from continuing operations:

Basic (0.27) 0.01 (0.23) 1.08 1.14

Diluted (0.27) 0.01 (0.23) 1.05 1.12

Dividends 0.22 0.22 0.22 0.22 0.22

Capital expenditures 24,174 29,543 39,478 44,114 49,881

Long-term debt 139,828 142,708 76,941 85,676 47,281

Stockholders’ equity 348,735 336,320 330,029 360,966 408,460

Analytic metricsNumber of full-time employees 7,600 8,400(1) 8,000 8,500 7,700

Days sales outstanding (DSO) 68 64 60 67 75

Current ratio(2) 1.41x 1.46x 1.42x 1.74x 1.60x

Debt to total capital 29% 30% 26% 19% 11%

Full-Time Employees, Average

Revenue per Full-Time Employee

Revenue per Full-Time Employeedollars in thousands

9,000

6,000

3,000

0

$150

140

120

130

110

100

$1,0

64,8

20

$1,0

03,3

26

$1,0

54,6

31

$1,1

79,3

38

$1,0

72,7

29

20001999 2001 2002 2003 20001999 2001 2002 2003

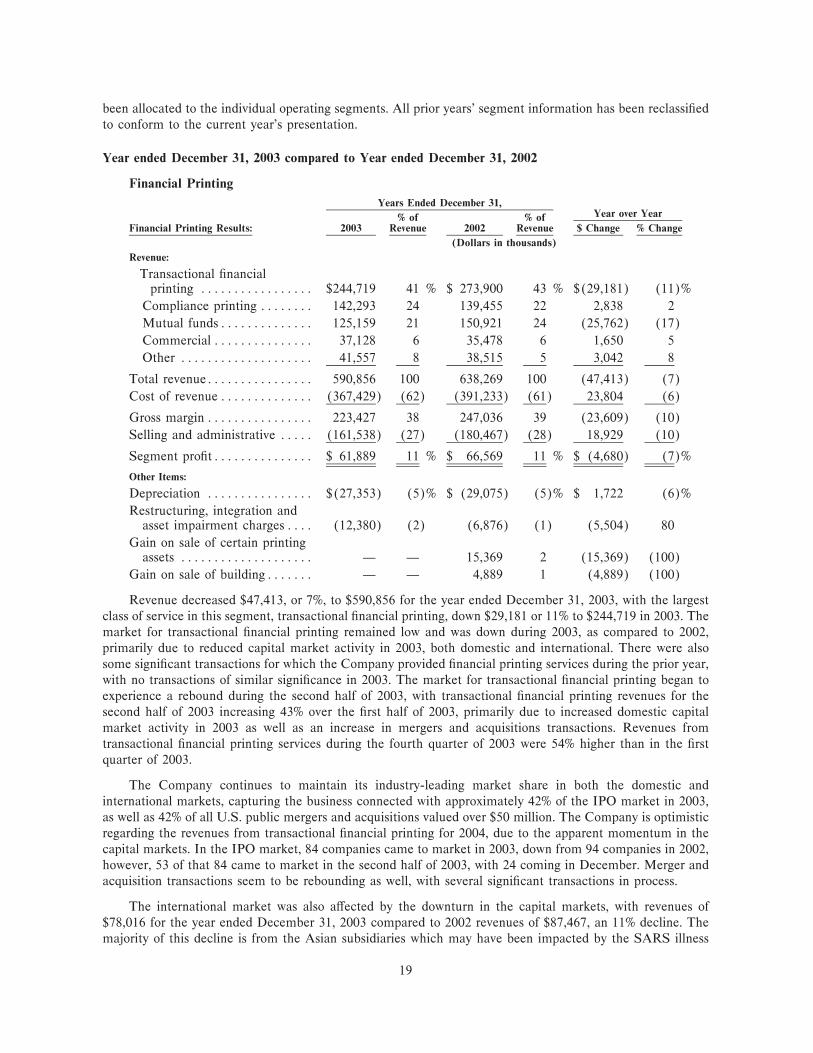

Globalization NontransactionalFinancial Printing

Outsourcing TransactionalFinancial Printing

Revenue Trend Analysisdollars in thousands

Page

1.

009407_Bowne cmyk 4/6/04 4:23 PM Page 1

We began 2003 with a high degree of

uncertainty for each of our businesses.

In Bowne Financial Print, we were

coming off the weakest six months of

capital market activity in the past

decade. With the impending war in

Iraq, there was little to suggest

improvement.

Our digital print group within Financial

Print, Bowne Enterprise Solutions,

was coping with continuing

contraction in its largest customer

segment—the mutual fund

industry—and the challenges of

introducing new customized

communications solutions to an

uncertain financial services market.

In Bowne Global Solutions, we had

just completed the acquisition

of Berlitz GlobalNet, and were in

the midst of integrating the two

organizations while also addressing

integration-related customer relations

and retention issues.

Finally, in Bowne Business Solutions,

we had just acquired DecisionQuest®,

further strengthening the suite of liti-

gation support services provided by our

outsourcing business. However, this

business was also faced with the

dissolution of two large legal clients and

a weak capital market that depressed

its investment banking business.

We entered the year with the need to

strengthen our capital structure and

maximize our performance during

unpredictable times. Discussions

began in March to renegotiate the

covenants with our banks and private

note holders. The resulting amendment

enabled the Company to maintain its

long-term strategy through 2003 and

comfortably meet the terms of its

credit facilities, even with the market

uncertainties. We also concluded we

were carrying too much senior debt

and that, after the acquisition of

To OurStockholders

Bown

e20

03

Ann

ual R

epor

tLe

tter

Fro

m T

he C

hairm

anPa

ge 2

.

Because we extended our discipline

to improve our communications

with investors, we were able to instill

confidence and generate a year-over-

year share price increase of more

than 13%. Since the end of 2003,

our share price has continued its rise,

hitting not only a 52-week high of

$17.90, but also its highest level

since we joined the NYSE in July

1999. This tells me investors

understand and value our deliberate

approach in managing costs, cash,

capital structure and growth potential.

.

.

.

.From Discipline Comes Opportunity —the theme of thisannual report — conveys the link between our behavior inmanaging your company through a difficult 2003 andhow our approach to improving the operation of each ofour businesses positions us for the future.

Robert M. JohnsonChairman of the Board,Chief Executive Officerand President

009407_Bowne cmyk 4/6/04 4:24 PM Page 2

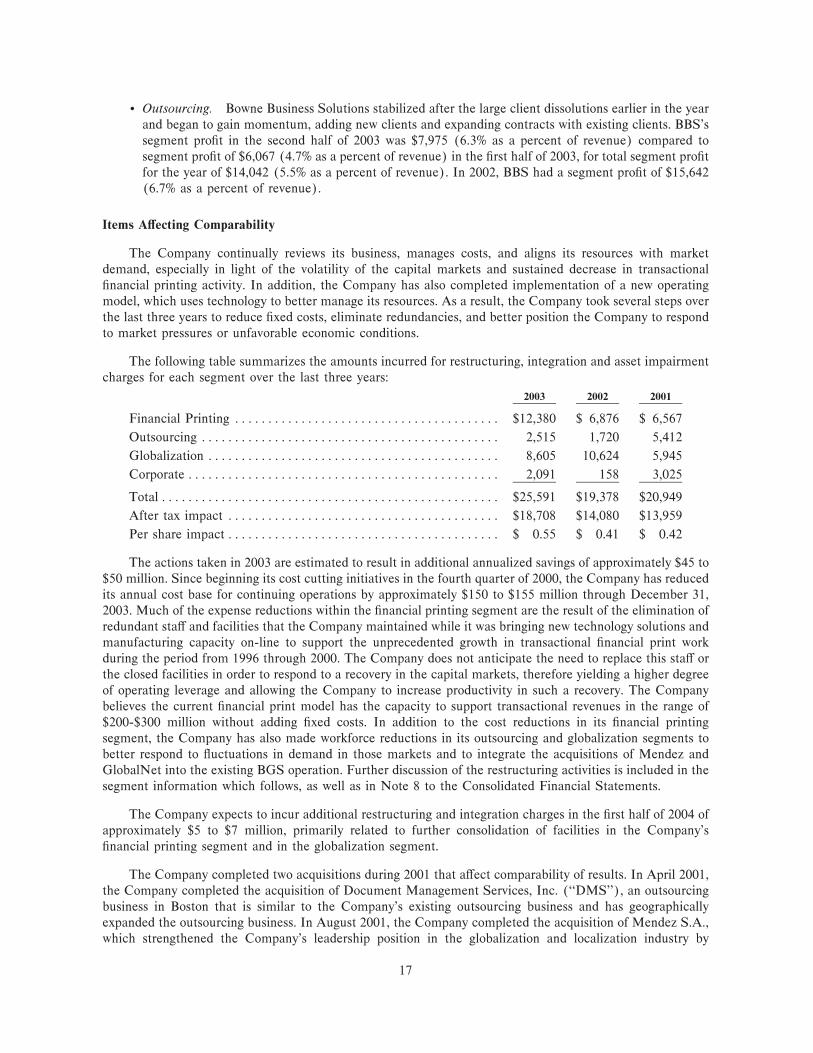

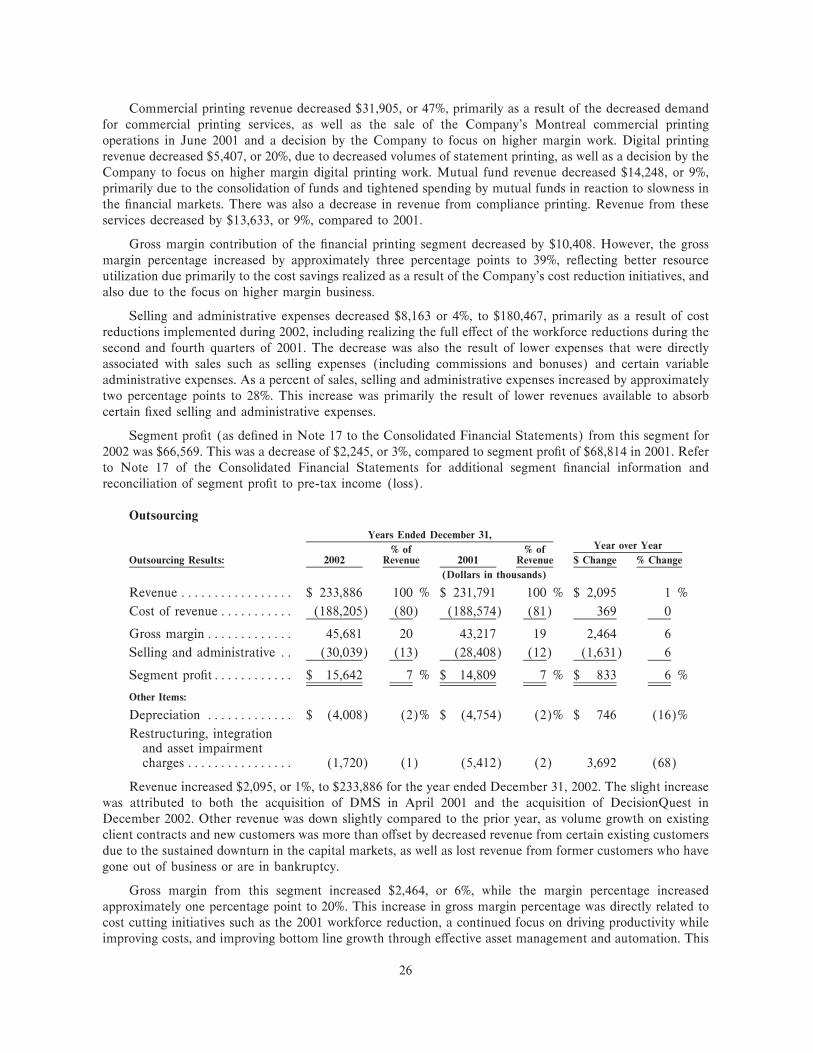

What were the results of our disciplined actions in 2003? In large part, due to the restructuring

of Financial Print, segment profits

in the fourth quarter rose $9.9 million,

or 225%, versus the 2002 fourth

quarter. Comparing the stronger second

half of the year with the same period

in 2002, revenues increased $12.3

million, or 4.8%, with segment profits

increasing $15.6 million, or 121%.

More importantly, the leverage of

having a more efficient operating model

gave shareholders confidence that

profitability could improve rapidly as

capital markets continued to rebound.

Enterprise Solutions continued to add

new clients and finished 2003 with

a more than 50% increase in monthly

on-demand volumes in its critical new

product offerings.

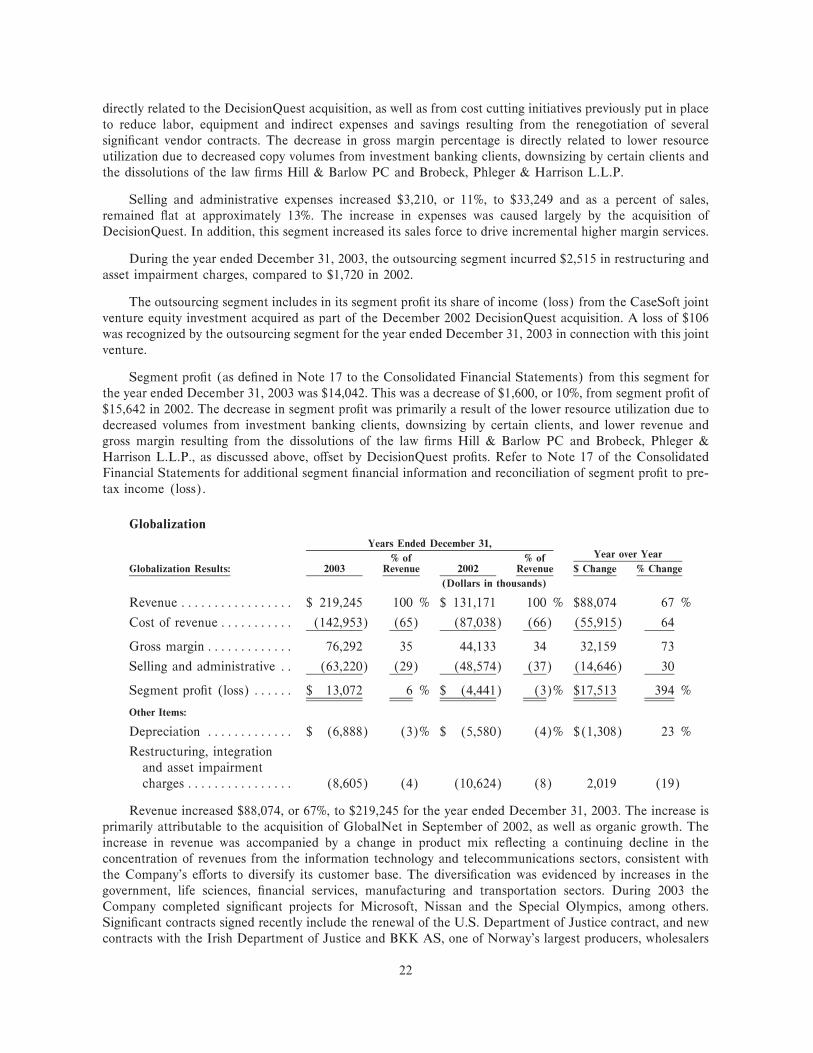

Global Solutions successfully

completed the GlobalNet integration

without losing a customer, while

margins and profitability improved

each quarter, creating a positive trend

as we moved into 2004. BGS’s

segment profit in the second half of

2003 was $6.8 million (6.4% as

a percent of revenue) compared to a

segment loss of $1.7 million in the

second half of 2002. Total segment

profit for 2003 was $13.1 million

(6.0% as a percent of revenue).

In 2002, BGS had a segment loss

of $4.4 million.

Business Solutions stabilized after

the large client dissolutions earlier

in the year and began to gain

momentum, adding new clients and

expanding contracts with existing

clients. BBS’s segment profit in the

second half of 2003 was $8 million

(6.3% as a percent of revenue)

compared to segment profit of

$6.1 million (4.7% as a percent of

revenue) in the first half of 2003

and segment profit of $7.3 million in

the second half of 2002.

Each of our businesses employed

great discipline in weathering the

challenges of 2003. Each finished

the year stronger and better prepared

for the opportunities we believe will

be available in 2004 and beyond.

I consider 2003 a testament to my

colleagues who met the challenges

head-on and ensured we would

emerge a better company. Thanks to

their efforts, and your continuing sup-

port, we expect 2004 will be a year in

which we reap even greater rewards

from our continuing discipline.

Robert M. JohnsonChairman of the Board, Chief Executive Officer and President

DecisionQuest and GlobalNet, there

was a mismatch between the term of

our bank facility and our capital

needs. In response, we executed a

$75 million convertible debt offering

that effectively reduced our senior

credit facility to working capital cov-

erage. The resulting capital structure

enhances stability and lowers our expo-

sure to increases in borrowing rates.

We were pleased the offering had no

adverse impact on our share price—a

rarity in the 2003 convertible market.

Within operations, we continued to

aggressively pursue process improve-

ments throughout the Company. We

sought to increase efficiencies while

controlling capital expenditures.

Considering the anemic condition of

the capital markets in the first half of

the year, we further reduced staffing

and closed small offices and ineffi-

cient plants that supported Financial

Print. Our goal was to maintain

acceptable levels of profitability and

superior service at an annual run rate

of $200 million in transactional

Financial Print revenue, the approxi-

mate run rate for the twelve months

ending June 30, 2003. Our actions

resulted in 2003 restructuring

charges of $12.4 million and brought

total reductions in annual fixed costs

within Financial Print to more than

$120 million. Our continued integra-

tion and reductions within Global

Solutions resulted in restructuring

charges of $8.6 million in 2003.

Nontransactional

Revenue

Transactional

Revenue

Segment Profit %

2002 2003

Second Half Segment Performancedollars in millions

$300

225

150

75

0

Financial Print

Revenue

Segment Profit %

2002 2003

Outsourcing

Revenue

Segment Profit %

2002 2003

12%

9

6

0

3

-3

Globalization

MD&A

Form 10-K

.

.

.

.

MD&A: Read more detail about Bowne’s financial condition and results of operationsin the Management’sDiscussion and Analysis section within the enclosed Form 10-K.

Page

3.

009407_Bowne cmyk 4/6/04 4:24 PM Page 3

Livin

g Th

e Di

scip

line/

Gre

ater

Effi

cien

cies

Page

4.

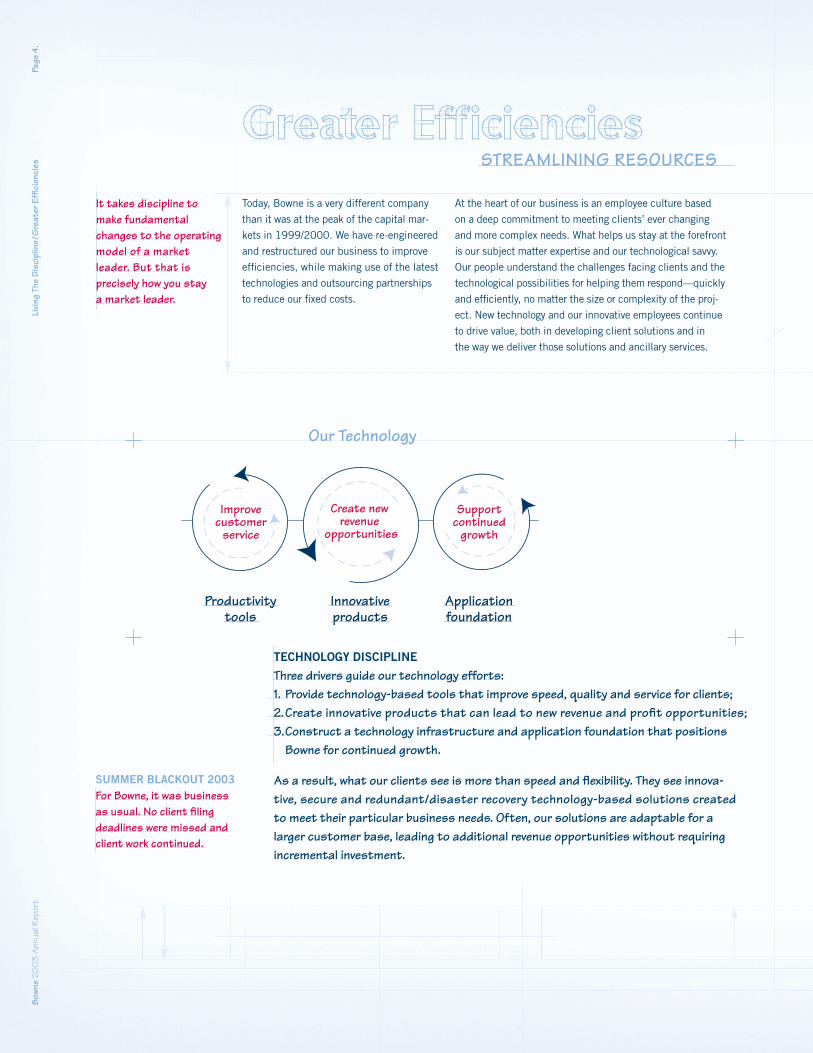

At the heart of our business is an employee culture based

on a deep commitment to meeting clients’ ever changing

and more complex needs. What helps us stay at the forefront

is our subject matter expertise and our technological savvy.

Our people understand the challenges facing clients and the

technological possibilities for helping them respond—quickly

and efficiently, no matter the size or complexity of the proj-

ect. New technology and our innovative employees continue

to drive value, both in developing client solutions and in

the way we deliver those solutions and ancillary services.

Today, Bowne is a very different company

than it was at the peak of the capital mar-

kets in 1999/2000. We have re-engineered

and restructured our business to improve

efficiencies, while making use of the latest

technologies and outsourcing partnerships

to reduce our fixed costs.

Improvecustomer

service

Create new revenue

opportunities

Supportcontinued

growth

Productivitytools

Innovativeproducts

Applicationfoundation

TECHNOLOGY DISCIPLINE

Three drivers guide our technology efforts: 1. Provide technology-based tools that improve speed, quality and service for clients;2.Create innovative products that can lead to new revenue and profit opportunities;3.Construct a technology infrastructure and application foundation that positions

Bowne for continued growth.

As a result, what our clients see is more than speed and flexibility. They see innova-tive, secure and redundant/disaster recovery technology-based solutions created to meet their particular business needs. Often, our solutions are adaptable for a larger customer base, leading to additional revenue opportunities without requiringincremental investment.

Greater EfficienciesSTREAMLINING RESOURCES

Our Technology

It takes discipline tomake fundamentalchanges to the operatingmodel of a market leader. But that is precisely how you stay a market leader.

SUMMER BLACKOUT 2003For Bowne, it was businessas usual. No client filingdeadlines were missed andclient work continued.

Bown

e20

03

Ann

ual R

epor

t

009407_Bowne cmyk 4/6/04 4:24 PM Page 4

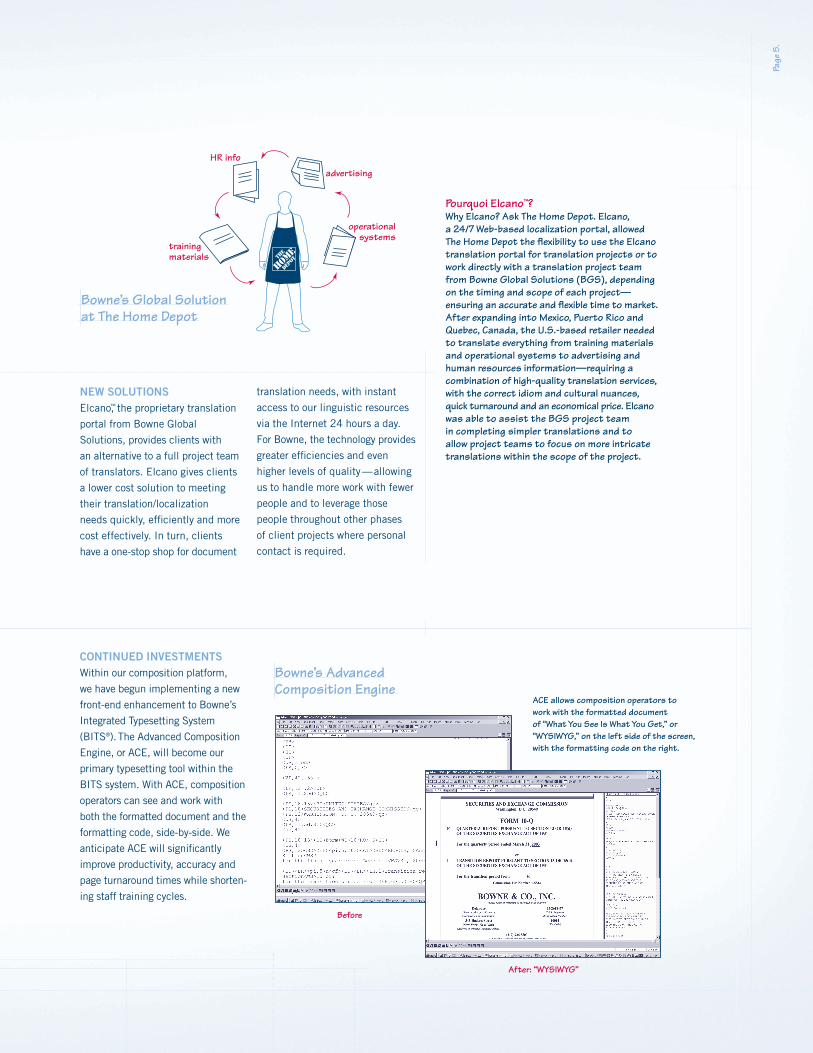

trainingmaterials

operational systems

advertisingHR info

Bowne’s Global Solution at The Home Depot

Pourquoi Elcano™?Why Elcano? Ask The Home Depot. Elcano, a 24/7 Web-based localization portal, allowedThe Home Depot the flexibility to use the Elcanotranslation portal for translation projects or towork directly with a translation project teamfrom Bowne Global Solutions (BGS), dependingon the timing and scope of each project—ensuring an accurate and flexible time to market.After expanding into Mexico, Puerto Rico andQuebec, Canada, the U.S.-based retailer neededto translate everything from training materialsand operational systems to advertising andhuman resources information—requiring a combination of high-quality translation services,with the correct idiom and cultural nuances,quick turnaround and an economical price. Elcanowas able to assist the BGS project team in completing simpler translations and toallow project teams to focus on more intricatetranslations within the scope of the project.

NEW SOLUTIONSElcano™, the proprietary translation

portal from Bowne Global

Solutions, provides clients with

an alternative to a full project team

of translators. Elcano gives clients

a lower cost solution to meeting

their translation/localization

needs quickly, efficiently and more

cost effectively. In turn, clients

have a one-stop shop for document

translation needs, with instant

access to our linguistic resources

via the Internet 24 hours a day.

For Bowne, the technology provides

greater efficiencies and even

higher levels of quality—allowing

us to handle more work with fewer

people and to leverage those

people throughout other phases

of client projects where personal

contact is required.

CONTINUED INVESTMENTSWithin our composition platform,

we have begun implementing a new

front-end enhancement to Bowne’s

Integrated Typesetting System

(BITS®).The Advanced Composition

Engine, or ACE, will become our

primary typesetting tool within the

BITS system. With ACE, composition

operators can see and work with

both the formatted document and the

formatting code, side-by-side. We

anticipate ACE will significantly

improve productivity, accuracy and

page turnaround times while shorten-

ing staff training cycles.

ACE allows composition operators to work with the formatted document of “What You See Is What You Get,” or“WYSIWYG,” on the left side of the screen,with the formatting code on the right.

Bowne’s AdvancedComposition Engine

Before

After: “WYSIWYG”

Page

5.

009407_Bowne cmyk 4/6/04 4:24 PM Page 5

Page

6.

XMark™ reduces data conversion time by 50-90%

=Standardconversionturnaround

XMark advantage

Fasterturnaround for clients

Stan CookSenior Technology Advisor for Bowne’sTechnology Platform, is the “Father ofXMark™” and the 2002 recipient ofBowne’s Franz von Ziegesar InnovationAward. He developed XMark to automatethe high-speed conversion of customer-supplied electronic files into variousformats, resulting in greater efficienciesand a shortened production cycle byreducing data conversion time.

Michael VorelDirector of Emerging Technologies with Bowne Business Solutions,is the 2003 recipient of the Franz von Ziegesar Innovation Award.His innovative contributions include the integration of a new imagingsoftware package with a client’s proprietary electronic documentrepository, and as part of a BBS proposal team to develop aunique dual platform solution for a client to meet its specificdocument management needs.

Dick JohnsonDirector of Pre-Press Technology forBowne’s Technology Platform, is the2002 recipient of Bowne’s Edmund A.Stanley, Jr. Award for excellence in performance and client service. He spenttwo years teaming with industry-leadingvendors to create BowneFAX,TM a way to provide composing operators with a higher-quality image of customer-editedpages than is possible with a conven-tional fax, shortening cycle time andreducing copy clarification calls betweenthe client and customer service centers.

Bown

e20

03

Ann

ual R

epor

tLi

ving

The

Disc

iplin

e/G

reat

er E

ffici

enci

esPa

ge 6

.

XMARK™ is a revolutionary file conversion technology that works

with a variety of document formats producing near-perfect data con-

versions the first time, by standardizing the document and outputting

the information in the desired format. XMark reduces the standard

time for data conversion and composition production in the range of

50 to 90 percent, thus speeding client turnaround time. This cost-

effective proprietary technology gives Bowne a competitive advantage

by automatically creating output files in a variety of formats that

clients can use for EDGAR II filings, conversion from RTF (Rich

Text Format) to other formats, conversion from text to HTML (Hypertext

Markup Language) and PDF files for the Web, and integration with

BITS for fast, efficient and accurate filing needs.

009407_Bowne cmyk 4/6/04 4:25 PM Page 6

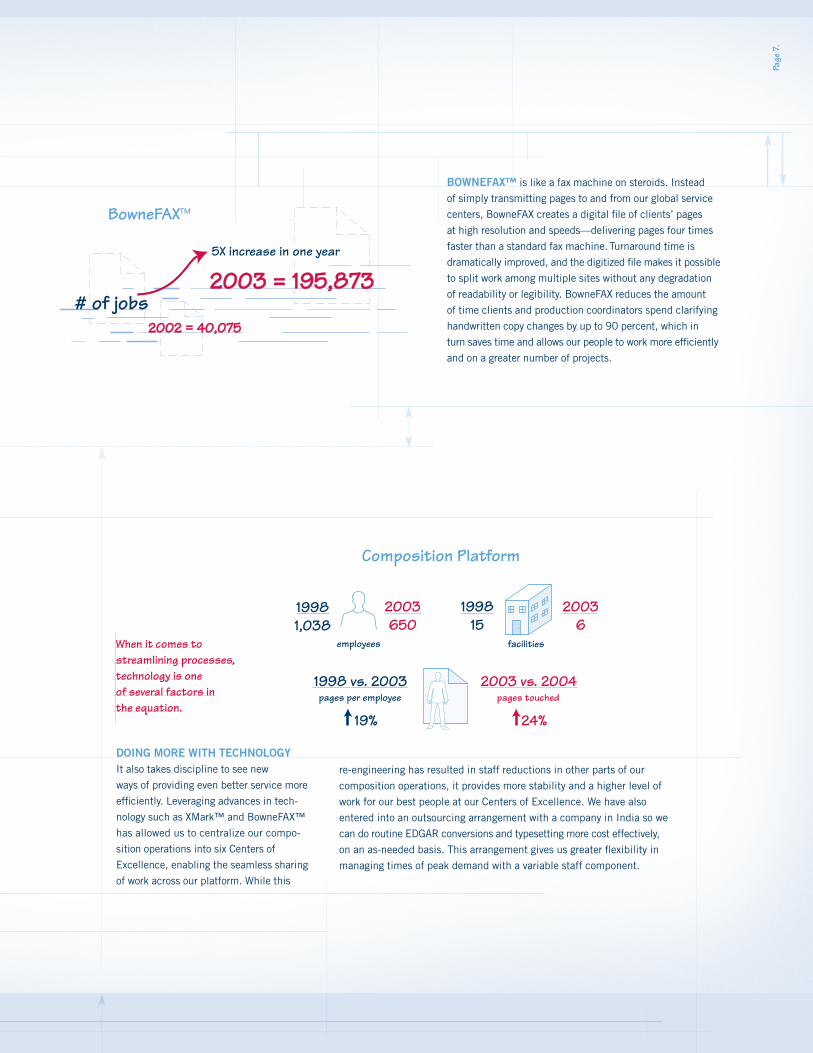

DOING MORE WITH TECHNOLOGYIt also takes discipline to see new

ways of providing even better service more

efficiently. Leveraging advances in tech-

nology such as XMark™ and BowneFAX™

has allowed us to centralize our compo-

sition operations into six Centers of

Excellence, enabling the seamless sharing

of work across our platform. While this

5X increase in one year

2003 2003 == 195,873 195,873

2002 2002 == 40,075 40,075

# of jobs

BOWNEFAX™ is like a fax machine on steroids. Instead

of simply transmitting pages to and from our global service

centers, BowneFAX creates a digital file of clients’ pages

at high resolution and speeds—delivering pages four times

faster than a standard fax machine.Turnaround time is

dramatically improved, and the digitized file makes it possible

to split work among multiple sites without any degradation

of readability or legibility. BowneFAX reduces the amount

of time clients and production coordinators spend clarifying

handwritten copy changes by up to 90 percent, which in

turn saves time and allows our people to work more efficiently

and on a greater number of projects.

re-engineering has resulted in staff reductions in other parts of our

composition operations, it provides more stability and a higher level of

work for our best people at our Centers of Excellence. We have also

entered into an outsourcing arrangement with a company in India so we

can do routine EDGAR conversions and typesetting more cost effectively,

on an as-needed basis. This arrangement gives us greater flexibility in

managing times of peak demand with a variable staff component.

19981,038

2003650

199815

20036

employees facilities

pages per employee1998 vs. 2003

19%

pages touched2003 vs. 2004

24%

BowneFAXTM

Composition Platform

When it comes tostreamlining processes,technology is one of several factors in the equation.

Page

7.

009407_Bowne cmyk 4/6/04 4:25 PM Page 7

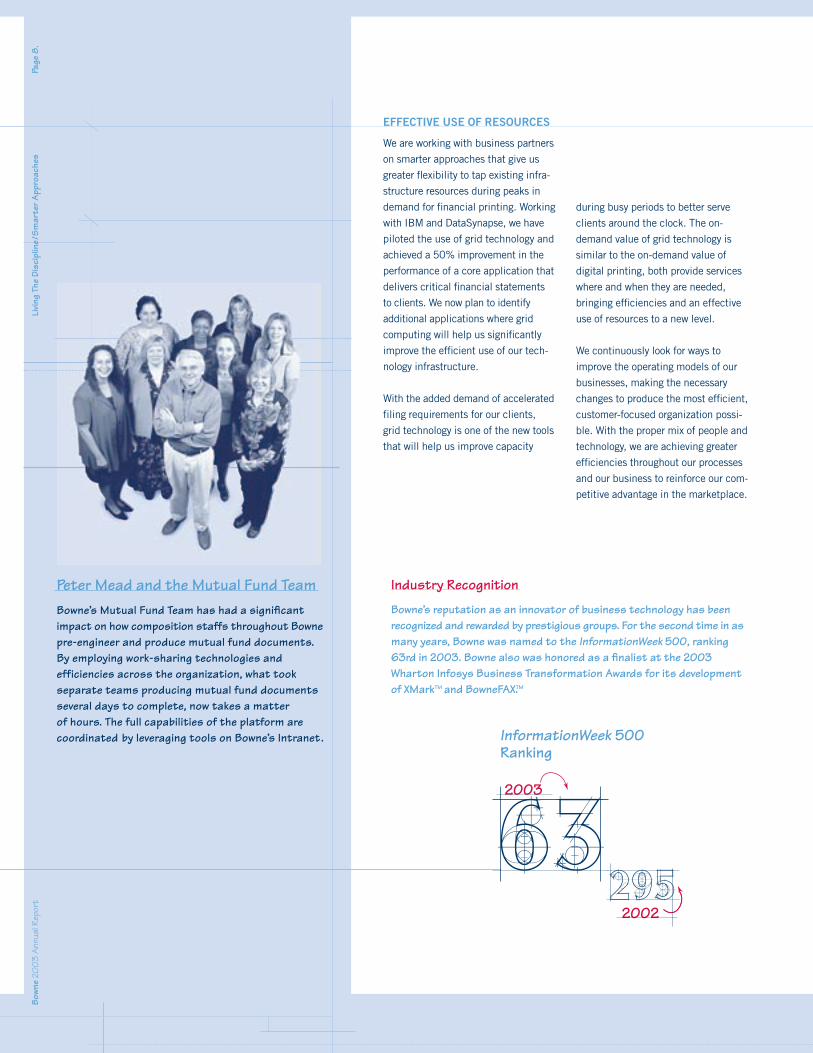

Peter Mead and the Mutual Fund TeamBowne’s Mutual Fund Team has had a significantimpact on how composition staffs throughout Bownepre-engineer and produce mutual fund documents.By employing work-sharing technologies and efficiencies across the organization, what took separate teams producing mutual fund documentsseveral days to complete, now takes a matter of hours. The full capabilities of the platform arecoordinated by leveraging tools on Bowne’s Intranet. InformationWeek 500

Ranking

2003

632002295

We are working with business partners

on smarter approaches that give us

greater flexibility to tap existing infra-

structure resources during peaks in

demand for financial printing. Working

with IBM and DataSynapse, we have

piloted the use of grid technology and

achieved a 50% improvement in the

performance of a core application that

delivers critical financial statements

to clients. We now plan to identify

additional applications where grid

computing will help us significantly

improve the efficient use of our tech-

nology infrastructure.

With the added demand of accelerated

filing requirements for our clients,

grid technology is one of the new tools

that will help us improve capacity

EFFECTIVE USE OF RESOURCES

during busy periods to better serve

clients around the clock. The on-

demand value of grid technology is

similar to the on-demand value of

digital printing, both provide services

where and when they are needed,

bringing efficiencies and an effective

use of resources to a new level.

We continuously look for ways to

improve the operating models of our

businesses, making the necessary

changes to produce the most efficient,

customer-focused organization possi-

ble. With the proper mix of people and

technology, we are achieving greater

efficiencies throughout our processes

and our business to reinforce our com-

petitive advantage in the marketplace.

as

he

Industry Recognition

Bowne’s reputation as an innovator of business technology has beenrecognized and rewarded by prestigious groups. For the second time in asmany years, Bowne was named to the InformationWeek 500, ranking63rd in 2003. Bowne also was honored as a finalist at the 2003Wharton Infosys Business Transformation Awards for its developmentof XMarkTM and BowneFAX.TM

Bown

e20

03

Ann

ual R

epor

tPa

ge 8

.Li

ving

The

Disc

iplin

e/Sm

arte

r App

roac

hes

009407_Bowne cmyk 4/6/04 4:25 PM Page 8

Page

9.

Through our discipline in staying abreastof the latest market requirements andtechnological capabilities, we are able todevelop strategic approaches for thedelivery of high-value solutions to clients.

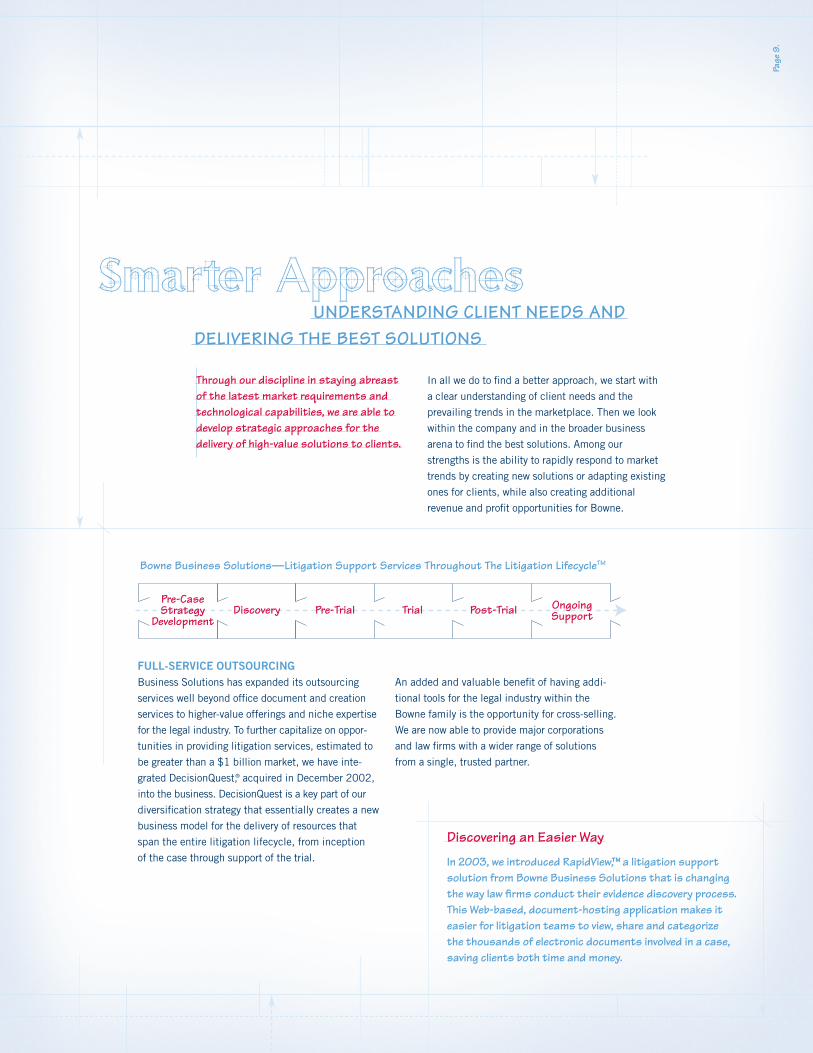

Pre-Case Strategy

DevelopmentDiscovery Pre-Trial Trial Post-Trial Ongoing

Support

Bowne Business Solutions—Litigation Support Services Throughout The Litigation LifecycleTM

In all we do to find a better approach, we start with

a clear understanding of client needs and the

prevailing trends in the marketplace. Then we look

within the company and in the broader business

arena to find the best solutions. Among our

strengths is the ability to rapidly respond to market

trends by creating new solutions or adapting existing

ones for clients, while also creating additional

revenue and profit opportunities for Bowne.

FULL-SERVICE OUTSOURCINGBusiness Solutions has expanded its outsourcing

services well beyond office document and creation

services to higher-value offerings and niche expertise

for the legal industry. To further capitalize on oppor-

tunities in providing litigation services, estimated to

be greater than a $1 billion market, we have inte-

grated DecisionQuest,® acquired in December 2002,

into the business. DecisionQuest is a key part of our

diversification strategy that essentially creates a new

business model for the delivery of resources that

span the entire litigation lifecycle, from inception

of the case through support of the trial.

An added and valuable benefit of having addi-

tional tools for the legal industry within the

Bowne family is the opportunity for cross-selling.

We are now able to provide major corporations

and law firms with a wider range of solutions

from a single, trusted partner.

Smarter ApproachesUNDERSTANDING CLIENT NEEDS AND

DELIVERING THE BEST SOLUTIONS

Discovering an Easier Way

In 2003, we introduced RapidView,™ a litigation support solution from Bowne Business Solutions that is changing the way law firms conduct their evidence discovery process.This Web-based, document-hosting application makes it easier for litigation teams to view, share and categorize the thousands of electronic documents involved in a case,saving clients both time and money.

009407_Bowne cmyk 4/6/04 4:25 PM Page 9

Beyond the customization benefits of on-demand technologies, clients also gain:Efficiencies in both time and money.

Web-based ordering and database capabilities.

Lower document lifecycle costs, as on-demand

production eliminates the need for warehousing

documents and manual pick-and-pack fulfillment.

The ability to order and print only those documents

they need when they need them, so there is no

waste from storing outdated documents.

Whether our clients are looking to differentiate their services in

an ever-crowded marketplace or trying to make sense of new

compliance requirements for public companies, they continue to

find Bowne a trusted, reliable resource with smart approaches

and the best solutions for delivering what they need.

EFFECTIVE, TARGETED COMMUNICATIONSEnterprise Solutions, the part of Financial Print that specializes in digital, on-demand

technologies, has developed a smart approach that brings the benefits of just-in-time

content creation and production to its financial services and insurance clients. By incor-

porating digital capabilities with customer databases, our clients gain the ability to

create and produce enrollment kits for retirement plans and other communications for

asset management investment funds, tailored to specific audience segments. Our

approach gives clients the ultimate in document flexibility, with the ability to mix both

standard and customized content.

...

.

WelcomeKit

Personally yoursThe personalization approach is beginning to resonate in the marketplace as companies look todifferentiate themselves from their competitors, better manage costs, and gain a larger share oftheir customers’ investment income.

With Merrill Lynch, Bowne:Leveraged our capabilities in on-demand tech-nologies with an overall strategic review of the company’s current communication practices.Created a more effective method for Merrill Lynchto welcome its new investors within 24 to 48hours, reinforcing the post-purchase experience.Provided a platform for cross-selling additionalproducts and services to existing investors.

For Merrill Lynch, the Bowne solution has translated into: Better customer experience.Improved document compliance.Faster updating process for disclosure information.Streamlined processes and lowered costs.

For more information on how Bowne can help clients with their personalized communications, visit our Website at: www.bowne.com/bes.

.

..

.

...

.

ALLISON BRATHWAITE Leading Bowne’s efforts with Merrill Lynch is Allison Brathwaite,strategic account manager for BowneEnterprise Solutions and recipient of the 2003 Edmund A. Stanley, Jr.Award for excellence in performanceand client service. Merrill Lynch invitedher to participate in its Six Sigmatraining program—the first time an outside person has been invited ontothe team. This program is gearedtowards identifying and implementingbusiness process improvements.

Bown

e20

03

Ann

ual R

epor

tLi

ving

The

Disc

iplin

e/Sm

arte

r App

roac

hes

Page

10.

009407_Bowne cmyk 4/6/04 4:25 PM Page 10

Page

11.

Today, we have the most modern facilities and technologies

in all our respective businesses. And we have the expertise

and the most knowledgeable people in the industry who

can leverage these assets to deliver high-value solutions for

our clients’ communications. With our major capital expen-

ditures behind us, we have tremendous flexibility to grow

the business as markets improve, without adding overhead

costs. We have the know-how, technology and solutions

to help our clients meet today’s needs. . . and the discipline

to stay ahead of ever-changing requirements.

.

.

.

.

As always, Bowne continues to makesense of complex regulations—historicallyour area of expertise.The regulatory landscape has changed dramatically in the last few years, with along and daunting list of compliance regulations for public companies. The mostsignificant of these is the Sarbanes-Oxley Act of 2002, enacted to improveaccountability, transparency and restoreinvestor confidence after accountingfraud was uncovered at several big-namecorporations.

Just as important, our businesses are well prepared to take advantage of strategic opportunities for growth. Financial Print has made fundamental changes to its business model and made

appropriate investments so that a significant portion of incremental revenues will

impact the bottom line.

Enterprise Solutions allows clients to customize and personalize their communications

for mass or individual mailings—reinforcing our diversification strategy by reducing

reliance on cyclical transactional financial print.

Global Solutions now has the scale to manage large global projects and sees significant

growth opportunities ahead, in a market where 60% of localization projects are

managed in-house at large corporations serving global markets.

Business Solutions has expanded into new vertical markets—consulting firms,

pharmaceuticals and corporate legal departments—while increasing penetration of

existing customers by offering broader and higher-value services.

The disciplined actions we have taken to make Bowne a better company alsoprepare us for a better future.

Future OpportunitiesENHANCING CAPABILITIES

AND BEING PREPARED FOR WHAT COMES NEXT

009407_Bowne cmyk 4/6/04 4:25 PM Page 11

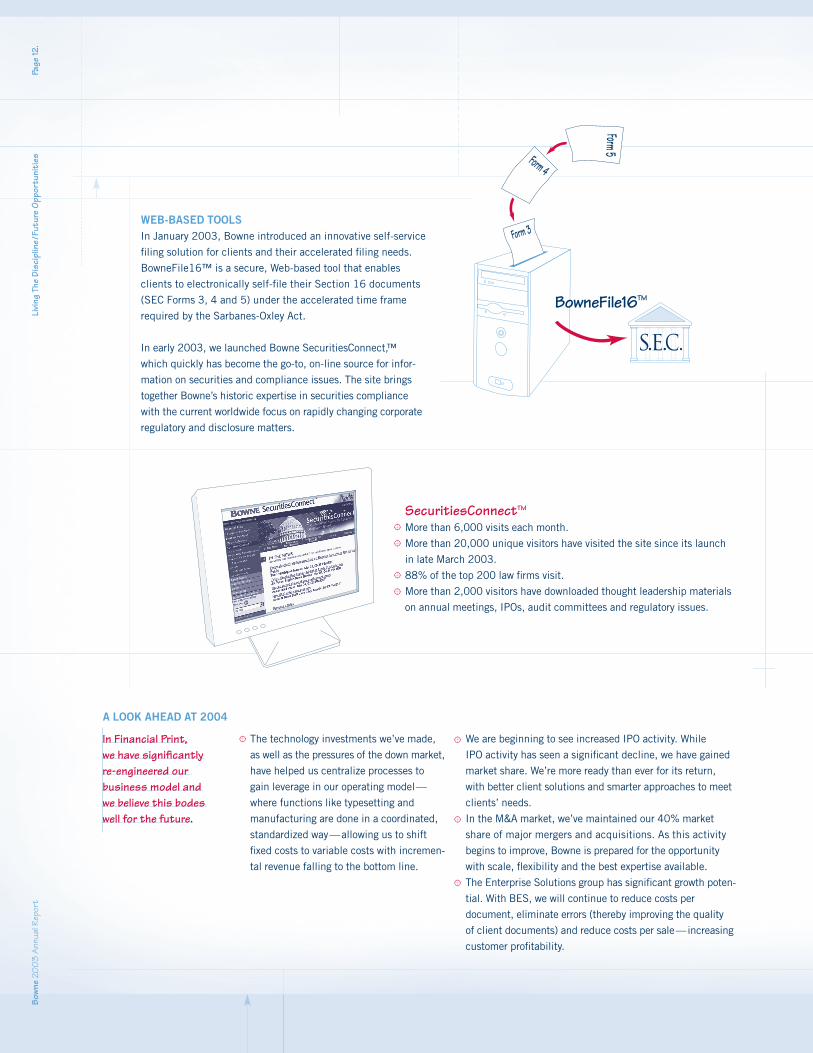

SecuritiesConnectTM

More than 6,000 visits each month.

More than 20,000 unique visitors have visited the site since its launch

in late March 2003.

88% of the top 200 law firms visit.

More than 2,000 visitors have downloaded thought leadership materials

on annual meetings, IPOs, audit committees and regulatory issues.

We are beginning to see increased IPO activity. While

IPO activity has seen a significant decline, we have gained

market share. We’re more ready than ever for its return,

with better client solutions and smarter approaches to meet

clients’ needs.

In the M&A market, we’ve maintained our 40% market

share of major mergers and acquisitions. As this activity

begins to improve, Bowne is prepared for the opportunity

with scale, flexibility and the best expertise available.

The Enterprise Solutions group has significant growth poten-

tial. With BES, we will continue to reduce costs per

document, eliminate errors (thereby improving the quality

of client documents) and reduce costs per sale—increasing

customer profitability.

The technology investments we’ve made,

as well as the pressures of the down market,

have helped us centralize processes to

gain leverage in our operating model—

where functions like typesetting and

manufacturing are done in a coordinated,

standardized way—allowing us to shift

fixed costs to variable costs with incremen-

tal revenue falling to the bottom line.

A LOOK AHEAD AT 2004

. .

..

..

.

.

WEB-BASED TOOLSIn January 2003, Bowne introduced an innovative self-service

filing solution for clients and their accelerated filing needs.

BowneFile16™ is a secure, Web-based tool that enables

clients to electronically self-file their Section 16 documents

(SEC Forms 3, 4 and 5) under the accelerated time frame

required by the Sarbanes-Oxley Act.

In early 2003, we launched Bowne SecuritiesConnect,™

which quickly has become the go-to, on-line source for infor-

mation on securities and compliance issues. The site brings

together Bowne’s historic expertise in securities compliance

with the current worldwide focus on rapidly changing corporate

regulatory and disclosure matters.

Form 3

Form 4

Form 5

S.E.C.

BowneFile16TM

In Financial Print, we have significantly re-engineered our business model and we believe this bodes well for the future.

Bown

e20

03

Ann

ual R

epor

tLi

ving

The

Disc

iplin

e/Fu

ture

Opp

ortu

niti

esPa

ge 12

.

009407_Bowne cmyk 4/6/04 4:25 PM Page 12

Page

13.

THE DISCIPLINE TO FIND OPPORTUNITYTime and again, we have helped our clients

respond to developing market trends and

complex regulations as quickly and efficiently

as possible. Today, we are a global leader

with a history that goes back 229 years.

We have tremendous potential to leverage

earnings growth, having reduced fixed

costs $150 million in the last three years.

Our diversification strategy reduces our

reliance on cyclical businesses and allows us

to focus on higher-margin business in high-

growth markets. Our clients are among the

leaders in their industries, giving us a

world-class customer base. Through our disci-

plined approach, we continue to find greater

efficiencies, smarter approaches and enhanced

capabilities that improve value—for Bowne,

our clients and our stockholders.

. .

..

. .

.

.

Our unique value proposition is chang-

ing the way clients approach their

localization needs. Clients are turning

to Bowne for the scale, resources and

technological capabilities to manage

large, global projects.

Significant market opportunities exist

for interpretation services in govern-

ment, healthcare, and commercial

sectors, both in the US and abroad.

We see growing demand in 2004 in

the IT and telecommunications

industries, fueling renewed demand

within our top accounts.

Further expansion in the pharmaceu-

tical, medical device and automotive

markets provides additional opportu-

nities for growth.

The outsourcing segment is also well positioned for growth in the year ahead. Our discipline in monitoring and improving margins has better prepared us for the opportunity in front of us. Currently, we provide outsourcing and transactional litigation services to 8 of thetop 10 investment banks and a majority of the 200 largest law firms (50 percent receiving on-site support) — with a 95 percent customerretention rate overall.

We continue to see a resurgence

tied to capital market growth, as well

as an improvement in the higher

margin litigation support services for

key accounts.

Market share within the legal and

investment banking markets

further supports our ability to expand

value-added services provided to

existing clients.

Outsourcing continues to be a growth

industry as we look to provide oppor-

tunities for deeper client penetration

and expanded service offerings.

Expansion of outsourcing services

into new verticals bodes well for

the future. Continued expansion into

the pharmaceutical industry and

corporate legal departments looks

promising for expanding outsourcing’s

revenue base while improving segment

profit margins.

Bowne has long beenknown as a premierbrand in the businessservices industry.

90%90% 80%80% 95%95%

200 LargestLaw Firms

Top 10Investment Banks

CustomerRetention Rate

A Premier Brand

Within the globalization segment, a renewed demand among our topaccounts is showing positive signs of opportunity in the year ahead.

009407_Bowne cmyk 4/6/04 4:25 PM Page 13

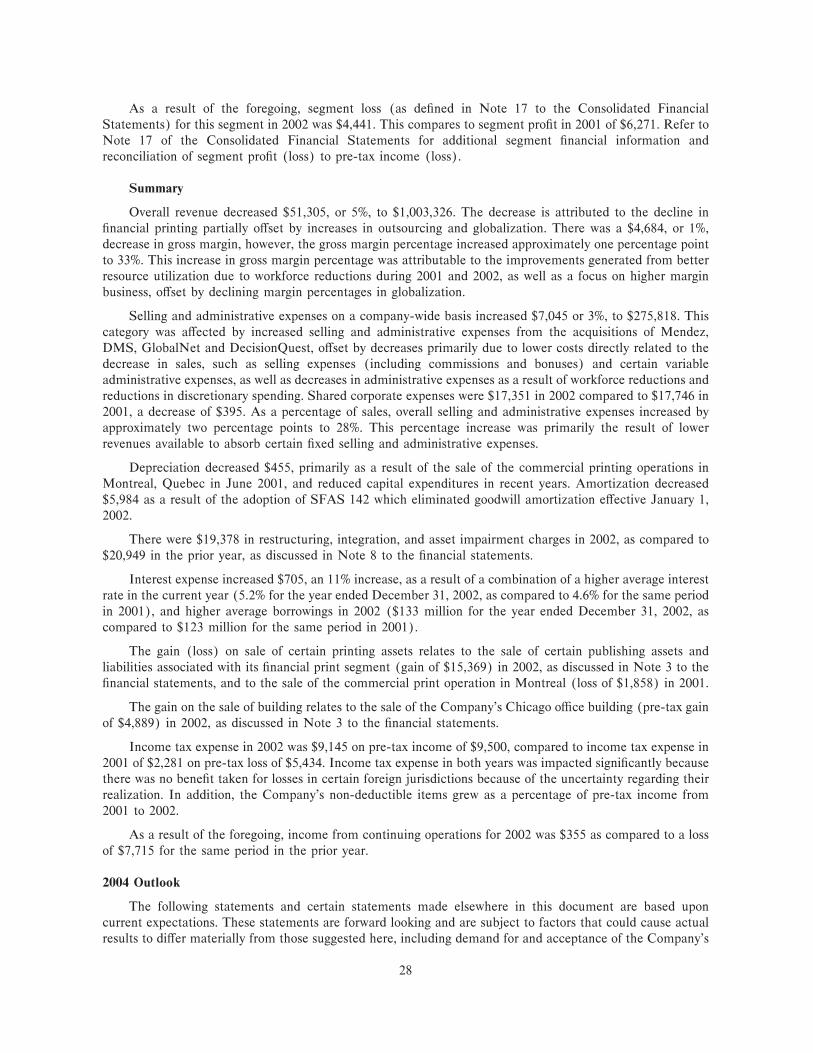

While total revenues in Financial

Print were down 7% for the full year,

second half revenues increased 5%

over the same period in 2002 while

segment profits rose $15.6 million,

or 121%, further underscoring the

leverage and cost savings in our more

efficient business model.

In Global Solutions, fourth quarter

revenues rose 5% over the same

period of 2002 and, importantly,

segment profit increased $3.9

million despite currency volatility.

Our strategy to extend services to a

more diversified client base to

capture broader market opportunities

served us well in 2003, with gains

in the medical devices, government,

education, automotive, aerospace,

pharmaceutical and transportation

industries.

In Business Solutions, the first half

of 2003 saw declining volumes

within our investment banking

clients, downsizing of key clients and

the dissolution of several law firm

clients. Yet in the fourth quarter,

this segment added $22 million in

total new annual contract revenue

with seven new outsourcing contracts;

five within the legal sector, one in

investment banking, and one in the

consulting industry.

In September 2003, we completed a

$75 million convertible subordinated

debt offering as a way of achieving

a more efficient capital structure. The

proceeds were used to pay down

short-term debt, with the net effect

being that we gained more flexibility

even as our overall debt level

remained the same. The offering

allowed us to match our long-term

business plan with similarly termed

financing at a reasonable cost.

We entered 2004 with cautious

optimism after seeing positive signs

of increased activity in the capital

markets. With the restructuring actions

we’ve taken the past few years, we

believe we are well positioned to

benefit when demand levels return.

Even then we will hold to our disci-

pline, making course corrections

when necessary, in order to provide

the maximum value to our clients

and shareholders.

C. Cody ColquittSenior Vice President and Chief Financial Officer

To Our Stockholders

20011st half 2nd half

Revenue

Segment Profit %

20021st half 2nd half

20031st half 2nd half

Outsourcing dollars in millions

$150

100

50

0

9%9%

77

55

33

11

20011st half 2nd half

Revenue

Segment Profit %

20021st half 2nd half

20031st half 2nd half

Globalization dollars in millions

$120

60

90

30

0

8%8%

44

00

--44

--88

20011st half 2nd half

Nontransactional Revenue

Segment Profit %

20021st half 2nd half

20031st half 2nd half

TransactionalRevenue

Financial Print dollars in millions

$450

300

150

0

15%15%

1212

99

33

66

00

Today Bowne is reaping the benefits of our discipline in strengthening the business. A difficult business environment has tested everyone thesepast few years, clients and competitors alike. We certainly have felt theimpact of the downturn in capital markets and a slower global economy.Our response was to focus on creating more efficient and effective operat-ing models in our business segments, with diversification, restructuringand technology investments as key factors in our efforts.

We began to see a rebound in the second half of 2003.

.

.

.

Bown

e20

03

Ann

ual R

epor

tLe

tter

Fro

m T

he C

FOPa

ge 14

.

009407_Bowne cmyk 4/6/04 4:25 PM Page 14

Page

15.

Lead

ersh

ip

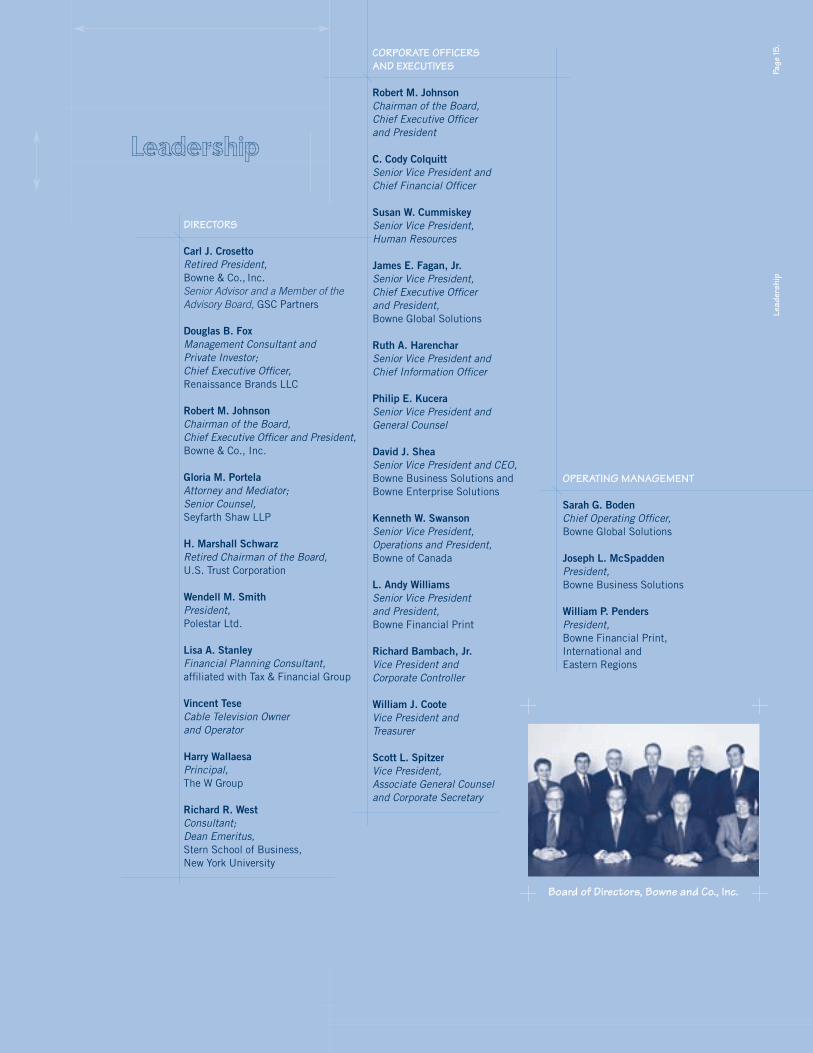

DIRECTORS

Carl J. CrosettoRetired President,Bowne & Co., Inc.Senior Advisor and a Member of theAdvisory Board, GSC Partners

Douglas B. FoxManagement Consultant andPrivate Investor;Chief Executive Officer,Renaissance Brands LLC

Robert M. JohnsonChairman of the Board,Chief Executive Officer and President,Bowne & Co., Inc.

Gloria M. PortelaAttorney and Mediator;Senior Counsel,Seyfarth Shaw LLP

H. Marshall SchwarzRetired Chairman of the Board,U.S. Trust Corporation

Wendell M. SmithPresident, Polestar Ltd.

Lisa A. StanleyFinancial Planning Consultant, affiliated with Tax & Financial Group

Vincent TeseCable Television Owner and Operator

Harry WallaesaPrincipal, The W Group

Richard R. WestConsultant; Dean Emeritus,Stern School of Business,New York University

CORPORATE OFFICERS AND EXECUTIVES

Robert M. JohnsonChairman of the Board, Chief Executive Officer and President

C. Cody ColquittSenior Vice President andChief Financial Officer

Susan W. CummiskeySenior Vice President,Human Resources

James E. Fagan, Jr.Senior Vice President,Chief Executive Officerand President,Bowne Global Solutions

Ruth A. HarencharSenior Vice President andChief Information Officer

Philip E. KuceraSenior Vice President andGeneral Counsel

David J. SheaSenior Vice President and CEO,Bowne Business Solutions andBowne Enterprise Solutions

Kenneth W. SwansonSenior Vice President,Operations and President, Bowne of Canada

L. Andy WilliamsSenior Vice President and President,Bowne Financial Print

Richard Bambach, Jr.Vice President and Corporate Controller

William J. CooteVice President and Treasurer

Scott L. SpitzerVice President,Associate General Counseland Corporate Secretary

OPERATING MANAGEMENT

Sarah G. BodenChief Operating Officer,Bowne Global Solutions

Joseph L. McSpaddenPresident,Bowne Business Solutions

William P. PendersPresident,Bowne Financial Print,International andEastern Regions

Leadership

Board of Directors, Bowne and Co., Inc.

009407_Bowne cmyk 4/6/04 4:25 PM Page 15

Bown

e20

03

Ann

ual R

epor

tCo

rpor

ate

Gov

erna

nce

Page

16.

World Headquarters345 Hudson StreetNew York, NY 10014Telephone: 212-924-5500e-mail: [email protected]

Stock ListingNew York Stock Exchange: BNE

Websitewww.bowne.com

Our Website contains complete elec-tronic copies of Bowne stockholderdocuments, news releases, U.S.Securities and Exchange Commissionfilings, descriptions of Bowne’s prod-ucts and services, and other informa-tion about the Company.

Investor Relations ContactWilliam J. CooteVice President and [email protected]

Stockholder ContactScott L. SpitzerVice President, Associate GeneralCounsel and Corporate [email protected]

AuditorsKPMG LLP345 Park AvenueNew York, NY 10154

Transfer Agent and RegistrarThe Bank of New York101 Barclay StreetNew York, NY 10286

Bowne’s Form 10-K Annual Reportto the U.S. Securities andExchange Commission is incorpo-rated in this report to stockholders.A printed copy of Form 10-K maybe obtained without charge bycontacting William J. Coote.These documents are also availableon the Company’s Website.

BOARD OF DIRECTORSThe Board of Directors, which is elected by the stockhold-

ers, is the ultimate decision-making body of the company,

except with respect to those matters reserved to the stock-

holders. The Board of Directors has adopted corporate gov-

ernance guidelines to support the Board’s role in carrying

out its duties. The Board selects the CEO and the other

executive officers who are responsible and accountable for

the company’s daily business operations.

COMMITTEES OF THE BOARDThe Board has an Audit Committee, Compensation and

Management Development Committee, Finance Committee

and a Nominating and Corporate Governance Committee.

Committee members are appointed by the Board upon rec-

ommendation of the Nominating and Corporate Governance

Committee. All members of these committees meet the cri-

teria for independence contained in the rules of the New

York Stock Exchange and also satisfy the New York Stock

Exchange’s more rigorous independence requirements for

members of the Audit Committee. In addition, all members

of the Audit Committee have sufficient financial experience

and ability to enable them to discharge their responsibilities,

and at least two members shall be an “Audit Committee

financial expert” as defined in the Sarbanes-Oxley Act of

2002. The Board also has an Executive Committee which is

comprised of four independent Board members and the

Chief Executive Officer.

The Board has adopted charters for the Audit Committee,

Compensation and Management Development Committee and

the Nominating and Corporate Governance Committee setting

forth the purposes and responsibilities of the committees.

For additional information on Bowne’s Board of Directors,

Committees of the Board or other Corporate Governance

information, please refer to the company’s 2003 Proxy

Statement for the annual meeting of stockholders scheduled

for May 27, 2004. Information concerning Bowne’s corpo-

rate governance matters, including Corporate Governance

Guidelines, Committee Charters, Stock Ownership

Guidelines, Stock Trading Policy, Stock Transactions, Code

of Ethics, Complaint Notification Policy, Certificate of

Incorporation and By-Laws may also be viewed at the

Company’s Website (www.bowne.com) in the Corporate

Governance section. A copy of any of these policies may be

obtained without charge by writing to Scott L. Spitzer, Vice

President, Associate General Counsel and Corporate

Secretary, Bowne & Co., Inc., 345 Hudson Street, New York,

NY 10014, or by e-mail to [email protected].

Stockholders of record should contact The Bank of New York at its Website,

www.stockbny.com, regarding stock accounts, transfers, address changes,

dividend payments and like matters. A first-time user may gain access to confi-

dential account information by following the on-screen instructions to establish

a Personal Identification Number (PIN). The same information is available

by telephone (toll-free) at 800-524-4458, or for speech- and hearing-impaired

stockholders at 800-936-4237. The Bank’s e-mail address for such matters is:

[email protected]. Stockholders may also write to Shareholder

Relations Department, Post Office Box 11258, Church Street Station, New

York, NY 10286. Please ask the Bank for further instructions before sending

stock certificates for any purpose.

Corporate Governance at Bowne

The Board of Directors and its committees meet periodically throughout the

year to direct and oversee management of the company. Bowne’s Board cur-

rently has 10 members, eight of whom meet the criteria for independence

contained in the rules of the New York Stock Exchange.

Corporate Information

009407_Bowne cmyk 4/6/04 4:25 PM Page 16

UNITED STATESSECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D. C. 20549

Form 10-K¥ Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

for the Ñscal year ended December 31, 2003, orn Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

for the transition period from to

Commission File No. 1-5842

Bowne & Co., Inc.(Exact name of Registrant as speciÑed in its charter)

Delaware 13-2618477(State or other jurisdiction of incorporation (I.R.S. Employer IdentiÑcation Number)

or organization)

345 Hudson Street 10014(Zip code)New York, New York

(Address of principal executive oÇces)

(212) 924-5500(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Name of each exchange onTitle of each class which registered

Common Stock, Par Value $.01 New York Stock Exchange

Securities registered pursuant to Section 12(g) of the Act:

None(Title of class)

Indicate by check mark whether the Registrant (1) has Ñled all reports required to be Ñled by Section 13 or 15(d) ofthe Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant wasrequired to Ñle such reports), and (2) has been subject to such Ñling requirements for the past 90 days: Yes ¥ No n

Indicate by check mark if disclosure of delinquent Ñlers pursuant to Item 405 of Regulation S-K is not containedherein, and will not be contained, to the best of Registrant's knowledge, in deÑnitive proxy or information statementsincorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. n

Indicate by check mark whether the registrant is an accelerated Ñler (as deÑned in Exchange Act Rule 12b-2).Yes ¥ No n

The aggregate market value of the Common Stock issued and outstanding and held by nonaÇliates of the Registrantas of February 27, 2004, based upon the closing price for the Common Stock on the New York Stock Exchange onJune 30, 2003, was $426,607,243. For purposes of the foregoing calculation, the Registrant's Employees' Stock PurchasePlan and its Global Employees Stock Purchase Plan are deemed to be aÇliates of the Registrant.

The Registrant had 34,449,830 shares of Common Stock outstanding as of February 27, 2004.

Documents Incorporated by Reference

Certain portions of the documents of the Registrant listed below have been incorporated by reference into theindicated parts of this Annual Report on Form 10-K:

Notice of Annual Meeting of Stockholders and Proxy Statement anticipated to be datedApril 12, 2004 ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ Part III, Items 10-12

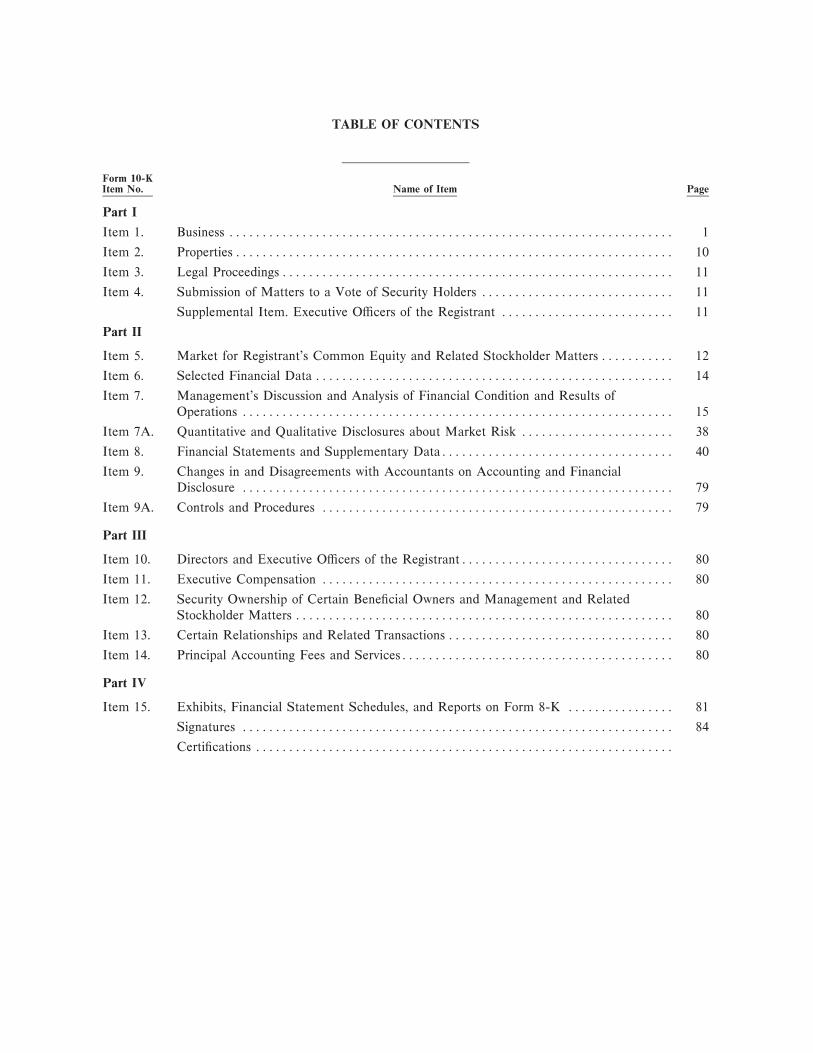

TABLE OF CONTENTS

Form 10-KItem No. Name of Item Page

Part I

Item 1. Business ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 1

Item 2. Properties ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 10

Item 3. Legal Proceedings ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 11

Item 4. Submission of Matters to a Vote of Security Holders ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 11

Supplemental Item. Executive OÇcers of the Registrant ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 11

Part II

Item 5. Market for Registrant's Common Equity and Related Stockholder Matters ÏÏÏÏÏÏÏÏÏÏÏ 12

Item 6. Selected Financial Data ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 14

Item 7. Management's Discussion and Analysis of Financial Condition and Results ofOperations ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 15

Item 7A. Quantitative and Qualitative Disclosures about Market Risk ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 38

Item 8. Financial Statements and Supplementary DataÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 40

Item 9. Changes in and Disagreements with Accountants on Accounting and FinancialDisclosure ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 79

Item 9A. Controls and Procedures ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 79

Part III

Item 10. Directors and Executive OÇcers of the RegistrantÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 80

Item 11. Executive Compensation ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 80

Item 12. Security Ownership of Certain BeneÑcial Owners and Management and RelatedStockholder Matters ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 80

Item 13. Certain Relationships and Related Transactions ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 80

Item 14. Principal Accounting Fees and ServicesÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 80

Part IV

Item 15. Exhibits, Financial Statement Schedules, and Reports on Form 8-K ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 81

Signatures ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 84

CertiÑcations ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ

PART I

Item 1. Business

Bowne & Co., Inc. (Bowne and its subsidiaries are hereinafter collectively referred to as ""Bowne'', the""Company'', ""We'' or ""Our'' unless otherwise noted), established in 1775, is a global provider of high-valuedocument management services. The Company has grown from a Ñnancial printing company to an integrateddocument and information management company. The Company is the world's largest Ñnancial printer, amarket leader in outsourcing document management services for law Ñrms and investment banks and a marketleader in providing globalization, localization and translation services. The Company built its diversiÑedbusiness in the following three segments:

Financial Print Ì Historically Bowne's principal segment, it encompasses:

‚ Bowne Financial Print, the Company's traditional Ñnancial printing services and the world's largestÑnancial printer, oÅers a comprehensive array of transactional and compliance-related services tocreate, manage, translate and distribute documents. Bowne provides these services to its clients inconnection with capital market and corporate transactions, such as equity and debt issuances andmergers and acquisitions, which the Company calls ""transactional Ñnancial printing''. Bowne alsoprovides these services to public corporations and mutual fund clients in connection with the fulÑllmentof their compliance obligations to produce and deliver periodic and other reports under applicable lawsand regulations, as well as in connection with general commercial and other printing needs.

‚ Bowne Enterprise Solutions (""BES''), the Company's newest Ñnancial printing business, provides acommunications solution that gives its clients an eÇcient and cost-eÅective system for producing anddelivering personalized and customized communications to their customers. From desktop editing todigital on-demand printing, Bowne oÅers the capability for ""just-in-time'' delivery of communicationsthat can be both individually personalized by the client and professionally produced and distributed.

Overall, the Ñnancial print segment generated revenue of $590.9 million in 2003 and $638.3 millionin 2002, representing approximately 55% and 64% of total revenue, respectively. The Company's Ñnancialprint segment generated segment proÑt of $61.9 million and $66.6 million in 2003 and 2002, respectively.The Company's segment proÑt is measured as gross margin (revenue less cost of revenue) less selling andadministrative expenses. The largest class of service in this segment, transactional Ñnancial printing,accounted for $244.7 million, or 23% of total 2003 Company revenue.

Outsourcing Ì This segment consists of Bowne Business Solutions (""BBS''), which provides on-sitedocument management services for law Ñrms, Ñnancial institutions and large companies that choose tooutsource these functions. The outsourced services that BBS oÅers cover the spectrum from basicdocument reproduction and distribution services, to medium skilled services such as word processing anddesktop publishing, to highly technical and specialized services such as litigation consulting. Theoutsourcing segment generated revenue of $254.7 million in 2003 and $233.9 million in 2002, represent-ing approximately 24% and 23% of total revenue, respectively. Outsourcing generated segment proÑt of$14.0 million and $15.6 million in 2003 and 2002, respectively.

Globalization Ì This segment consists of Bowne Global Solutions (""BGS''), which providesglobalization, interpretation, translation, localization and technical writing services to adapt the Com-pany's clients' products and communications for use in targeted countries in a manner that is bothtranslated to the speciÑc dialect for the target region and culturally appropriate. The globalizationsegment generated revenue of $219.2 million in 2003 and $131.2 million in 2002, representingapproximately 21% and 13% of total revenue, respectively. Globalization generated a segment proÑt of$13.1 million for 2003 and a segment loss of $4.4 million in 2002.

During the Ñrst quarter of 2003, the Company changed the way it reports and evaluates segmentinformation. The Company now reports certain administrative, legal, Ñnance, and other support services whichare not directly attributable to the segments in the category ""Corporate/Other''. These costs had previouslybeen allocated to the individual operating segments. The Company's previous years' segment information has

1

been restated to conform to the current year's presentation. Further information regarding segment revenues,operating results, identiÑable assets and capital spending attributable to the Company's operations for thecalendar years 2003, 2002 and 2001, as well as a reconciliation of segment proÑt to pre-tax income (loss), areshown in Note 17 of the Notes to Consolidated Financial Statements.

Industry Overview

Through Bowne's diversiÑed business units, the Company competes in a number of related industries,namely Ñnancial printing, personalized communications, document management outsourcing and globaliza-tion services.

The printing industry is highly fragmented, with hundreds of independent printers that provide a fullrange of traditional printing services. However, speciÑc to transactional and compliance Ñnancial printing,there are three primary companies, including Bowne, and a few regional Ñnancial printers that participate inthe market. Transactional Ñnancial printing volume tends to be cyclical with the markets for new debt andequity issuances and public mergers and acquisitions activity. Compliance Ñnancial printing volume is lesssensitive to market changes and represents a recurring periodic activity, with some seasonality linked tosigniÑcant Ñling deadlines imposed by law on public reporting companies and mutual funds.

The complete and integrated communications solution Bowne provides to its clients to help them deliverpersonalized and customized communications to their customers is a subset of an emerging customerrelationship management industry. This industry is populated by a number of active participants with diÅerentfocus and core capabilities that range from creative branding and message design services, to technicalsoftware design, to printing. The Company competes in this industry through its BES unit, which it operates aspart of its Ñnancial print segment. The Company's BES unit is focused on providing integrated documentcreation, production, distribution and management solutions that address the growing personalized communi-cations needs of the Ñnancial services industry, in particular the retirement services, asset management anddistributor segments. Financial services Ñrms are increasingly looking to digital, variable-data-driven solutionsthat will provide them with a broad range of competitive and operational beneÑts. For example, a Ñnancialservices Ñrm's ability to create relevant, engaging, and targeted communications to both customers andprospective customers can help increase customer retention and sales, as well as protect brand integrity. Thetechnologies Bowne leverages to provide clients with automated, web-based creation, printing and distributioncapabilities also create eÇciencies that will help Bowne's clients lower document-related costs.

The document management outsourcing industry has numerous competitors in the United States thatcompete for clients among medium-sized to large corporations, law Ñrms, investment banks, consulting Ñrmsand similar enterprises that have signiÑcant document management needs. Bowne is currently a leader inproviding outsourcing services to the legal industry and the investment banking industry. Furthermore, theCompany is targeting pharmaceutical companies, consulting and professional services Ñrms as well as generalcounsel oÇces of Fortune 500 companies, all of whom have high volume complex document needs. Theservices that are outsourced generally fall into the three following categories:

‚ traditional reproduction and transmission services, such as reprographics, faxing, messenger services,and similar services, which tend to be high volume, on-site work;

‚ value-added systems management and content creation services such as information technology, wordprocessing, desktop publishing, litigation support, imaging & coding, and similar skilled services, whichtend to be medium-volume work that can be performed either on-site or at the provider's location andcommand higher margins than traditional reproduction services; and

‚ outsourcing opportunities for niche expertise, such as electronic document discovery and data rooms,multi-media services, trial consulting, and other highly-specialized technical capabilities.

The globalization services industry traditionally has been managed by in-house departments of multina-tional companies that use a large cottage industry of small translation and localization contractors located indiÅerent countries around the world, which oÅer their services to adapt foreign materials for use in thatcountry. While the in-house operations and independent single-language translators traditionally have worked

2

together, over the past few years two trends have begun to change the globalization industry. First, althoughthousands of independent freelance translators remain, the highly fragmented industry has started toconsolidate, with three major participants today, including BGS. An advantage to employing a consolidatedprovider of globalization services is that the scale of the larger players allows them to manage largeglobalization projects across multiple countries and oÅer integrated services. Second, multinational companiesare increasingly outsourcing their globalization needs, although the Company estimates that a majority of allglobalization management is still performed in-house. The advantage to increased outsourcing is the ability ofclients to reduce their Ñxed costs in these non-core activities.

The Company

Financial Print

Bowne Financial Print has long ranked as the world's largest Ñnancial printer in a Ñeld populated by threeprimary companies, including Bowne, and a few regional Ñnancial printers. The Company's transactionalÑnancial printing includes registration statements, prospectuses, bankruptcy solicitation materials, specialproxy statements, oÅering circulars, tender oÅer materials and other documents related to corporateÑnancings, acquisitions and mergers. The Company's compliance Ñnancial printing includes annual andinterim reports, regular proxy materials and other periodic reports that public companies are required to Ñlewith the SEC or other regulatory bodies around the world. Bowne Financial Print is also the leading Ñlingagent for EDGAR, the SEC's electronic Ñling system. The Company provides both full-service and self-service Ñling, the latter through a new Internet-based Ñling product, BowneFile16TM, launched in early 2003. Acomponent of compliance printing includes mutual fund printing. Mutual fund printing includes regulatoryand shareholder communications such as annual or interim reports, prospectuses, information statements andmarketing-related documents. Bowne Financial Print also provides some commercial printing, which consistsof annual reports, sales and marketing literature, point of purchase materials, research reports, newsletters andother custom-printed matter. The Company also provides language translation services for highly conÑdentiallegal and Ñnancial documents in connection with its Ñnancial print operations. Over the past few years, Bownehas expanded its Ñnancial print capabilities within all phases of the document life-cycle, including electronicreceipt of client documents, composition, content management, conversion, translation, assembly, packaging,output, delivery, and archiving.

The Company's international Ñnancial printing business provides similar services as those delivered by itsdomestic operations. International print capabilities are delivered primarily by the Company or in some areas,through a number of strategic relationships.

Historically, transactional Ñnancial print has been the largest contributor to the Company's total revenue.However, because this line of business is cyclical with the Ñnancial markets, over the past three years Bownehas experienced a marked downturn in this line of business, with its total 2003 transactional Ñnancial printrevenue 49% lower than when the Ñnancial markets peaked in 2000. In response, the Company beganimplementing a new operating model that seeks to reduce Ñxed costs and increases the Öexibility of itsÑnancial print segment in response to market Öuctuations. The Company has reorganized its regionaloperations and closed or consolidated nine of its U.S. oÇces and facilities. While the Company still maintainsits own printing capabilities, having retooled its facilities in 1999 and 2000, Bowne also outsources someprinting needs to independent printers, especially during times of peak demand. This outsourcing allows theCompany to preserve Öexibility while reducing its staÇng, maintenance and operating expense of underutil-ized facilities, and is in line with industry practice. In addition, since November 2000, Bowne has reduced itsÑnancial print workforce by approximately 32%. The Company also has successfully established an arrange-ment with a company in India that allows it to outsource some of its EDGAR conversions and relatedfunctions on very cost-eÅective terms, especially at times of peak demand. Between the fourth quarter of 2000and December 31, 2003, the Company implemented or initiated approximately $150 to $155 million inannualized reductions to its cost base, a majority of which have been reductions made in Bowne's Ñnancialprint segment. Importantly, in the preceding years the Company had invested signiÑcantly in new technologiesthat it now leverages to perform the same volume of high-quality service for its clients despite the reductionsin its workforce. This has allowed the Company to permanently reduce its Ñxed and direct labor costs. As a

3

result of the Öexibility Bowne has achieved in the last few years, the Company expects that its cost savings willbe long term and that it will not need to fully replace personnel or otherwise incur such costs. Accordingly, theCompany believes that when the transactional Ñnancial print business returns to greater volumes it will be ableto serve much of the increased demand with only minimal increases in Ñxed and direct labor costs.

The Company believes that its technology investments have produced one of the most Öexible andeÇcient typesetting, printing and distribution systems in the industry, for example:

‚ Recent advances in technology have permitted Bowne to centralize its typesetting operations into six""Centers of Excellence'', to reduce its typesetting workforce and to outsource oÅshore the more routineand less critical typesetting work at a lower cost than performing it in-house.

‚ The Company expects to begin implementing its newest proprietary typesetting system, ACE(Advanced Composition Engine), in 2004. It believes that ACE will signiÑcantly improve productivity,accuracy and page turnaround, and substantially shorten training cycles, giving the Company evengreater Öexibility and responsiveness to its clients.

‚ The digital, print-on-demand services the Company oÅers through BES use advanced databasetechnology, coupled with high-speed digital printing, to assist clients, primarily in the Ñnancial servicesindustry, to reach their customers with more targeted levels of customized and personalizedcommunications.

‚ The Company also developed BowneFaxTM to replace its standard fax machines. While a standard faxmachine simply transmits a page from one location to another, BowneFaxTM creates a digital Ñle at highresolution and speeds and facilitates work-sharing. In terms of speed, BowneFaxTM shortens turnaroundtime because pages are read and processed Ñve to ten times faster than standard faxes. In terms ofservice, BowneFaxTM reduces the time the Company and its clients need to clarify unclear copy changesand signiÑcantly enhances accuracy through reduction of editing errors and page tracking.

‚ XMarkTM, another one of the Company's proprietary technologies, takes input from clients in a varietyof formats and allows conversion personnel to produce near-perfect conversions in a single cycle,standardizes the document format, and then produces output in a variety of formats. In terms of speed,XMarkTM reduces data conversion and composition production time in the range of 50 to 90 percent.

‚ Bowne was one of four U.S. Ñnalists for the Wharton Infosys Business Transformation Award in 2003.This award is given to a Global 2000 company that has transformed its business and industry throughthe creative application of technology. Also, in this past year, Bowne moved from 295th to 63rd placein 2003 in the top 500 ranking of the most innovative users of technology by Information Weekmagazine.

The Company has continued to diversify its business mix within the Ñnancial print business segment withthe introduction of Bowne Enterprise Solutions. Using a model that involves extensive consultation withclients with respect to their customer communications challenges, BES partners with clients to deliver qualityapplications based upon the eÅective integration of document creation, content management and distributionmethods. These methods include oÅset and digital printing and electronic delivery. BES helps its clientscreate, manage and distribute critical information, such as introductory enrollment kits and brokeragestatements, in order to produce better returns on their marketing dollars. Using advanced database technology,coupled with high-speed digital printing, BES oÅers clients the opportunity to personalize and customizecommunications to their customers. BES's digital, print-on-demand services also eliminate the need toconventionally print generic information and hold it in inventory until it is used or becomes obsolete. BESmaintains an electronic library of the client's documents that can be edited in real-time by the client's sales,marketing, legal and other authorized users. This allows customized and individual fulÑllment with the mostcurrent copies available, while reducing waste. Because of the extensive integration of systems between BESand its clients, contracts for these services tend to involve longer-term relationships. The clients for theseservices include mutual funds, stock brokerage Ñrms, deÑned contribution providers, investment banks,insurance companies and commercial banks.

4

Outsourcing

The Company's document management outsourcing business has greatly expanded since 1998 throughacquisitions, and Bowne Business Solutions has grown to become the industry leader in providing outsourcingservices primarily to the legal and Ñnancial services communities. BBS has sought to expand its business toexisting and new clients by broadening the range of services that it provides. BBS is also growing its existingcustomer base through increased penetration of the legal and investment banking industries. Furthermore,BBS seeks to expand its business through its eÅorts to reach potential clients in new industries, such as theconsulting and pharmaceutical industries.

The Company's outsourcing services include:

‚ on-site management of document creation, reproduction and distribution operations at its clients'facilities, and oÅ-site backup of those same services;

‚ specialized applications of graphics and presentation technologies, such as pitch books, charting, Öowcharts, conceptual diagrams and maps and multimedia applications such as animation, video andsound;

‚ information technology management, desktop support services, data center support, technical trainingand telephone system support; and

‚ litigation support services, including litigation resource management, which involves ongoing case andproject management; electronic data discovery processing; litigation software application support andtraining; document imaging, optical character recognition, coding and high-speed, high-volumeprinting; custom database management; creation and implementation of litigation support proceduresbest practices; creation and conversion of PDF Ñles; and creation of CD-ROMs.

BBS's acquisition of DecisionQuest in December 2002 allowed the Company to deliver litigation supportservices spanning the entire ""litigation lifecycle''TM, from inception of the case through trial. These additionalservices include trial consulting and jury research, advanced strategic communications and marketing,courtroom graphics and presentation technologies, litigation support and case evaluation software, and customcase strategy Web sites.

Outsourcing allows BBS clients to focus on their core businesses, gain access to the latest in technologicalinnovations without making direct investments, and reduce the operating costs of investing in and managingnon-core business activities. Initially, the Company must earn the conÑdence and trust of its clients bydemonstrating its competency, eÇciency and quality of service in the more basic functions. Once BBS hasproven its reliability, the Company believes that many of its clients become more comfortable withoutsourcing other more skilled and complex functions to them.

A joint venture agreement with Williams Lea, one of the United Kingdom's leading providers ofdocument management solutions, has helped BBS to extend its services to Europe and Asia. Together, BBSand Williams Lea provide global outsourcing services to multinational corporations, international law Ñrms,commercial and investment banks, and Ñnancial institutions around the globe.

Globalization

Bowne Global Solutions enables customers to succeed in global markets by providing innovative linguisticand cultural solutions. As a company's domestic market becomes saturated or faces an economic downturn,the drive to ""go global'' is accelerated. Whether this means establishing international sales channels,developing manufacturing plants in low cost regions, or simply putting up an e-commerce Web site, the resultis that companies today, large and small, are doing more and more business across borders and languages. Yet,while forecasts and market potential often look promising on paper, successfully executing in these marketsagainst entrenched local competition is very challenging. As a result, these companies seek a Öexible partnerwith the scope and breadth to support their globalization eÅorts. With its scale and skill, backed by provenproject management methods, BGS is able to rapidly respond to its clients' changing needs while maintainingthe highest standards of production quality.

5