Embed Size (px)

Citation preview

© WorldpanelTM division of TNS 2008

Edward GarnerCommunications Director Worldpanel – UK

Ethical Consumption – Market TrendsBirmingham – April 2008

© WorldpanelTM division of TNS 2008

Agenda

Background

Organic Overview

Organic Markets

Fairtrade Overview

Fairtrade Markets

Free Range

Retail Aspects

Markets & Lifestyles

© WorldpanelTM division of TNS 2008

Agenda

Background

Organic Overview

Organic Markets

Fairtrade Overview

Fairtrade Markets

Free Range

Retail Aspects

Markets & Lifestyles

© WorldpanelTM division of TNS 2008

Real Household Disposable Income Per Head

0

50

100

150

200

250

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

*

Constant Prices - Indexed on 1970Source: ONS Series IHXZ * to June

© WorldpanelTM division of TNS 2008

Food and Drink as a Proportion of UK Household Expenditure %

0

5

10

15

20

25

19

63

19

64

19

65

19

66

19

67

19

68

19

69

19

70

19

71

19

72

19

73

19

74

19

75

19

76

19

77

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

*

Source: ONS Series ABQI / ABZV * MAT to June

© WorldpanelTM division of TNS 2008

Premium Private Label Sales Trends

0

10

20

30

40

50

60

70

80

90

2000

2001

2002

2003

2004

2005

2006

2007

2008

Sa

les

(E

xp

en

dit

ure

£m

)

Tesco Finest Sainsbury Taste the Difference Asda Extra Special Safeway/MorrisonsThe Best

© WorldpanelTM division of TNS 2008

Tesco PL Lifestyle Indices

Tesco Finest

Tesco Value

“I regard myself as a connoisseur of food and wine”

158 75

“Price is the most important factor when buying a product”

76 133

Share indexed on Total Trade – 52 w/e Apr 22 2007

“We are seeing a shift away from value-for-money to

what we call

[Prof. Tim Lang, City University Jan 2007]

‘values-for-money’….”

© WorldpanelTM division of TNS 2008

Hard Discounters Share of Till Roll Grocers

0

1

2

3

4

5

6

7

Ap

r 24

200

5

May

22

2005

Jun

19

2005

Jul 1

7 20

05

Au

g 1

4 20

05

Sep

11

2005

Oct

09

2005

No

v 06

200

5

Dec

04

2005

Jan

01

2006

Jan

29

2006

Feb

26

2006

Mar

26

2006

Ap

r 23

200

6

May

21

2006

Jun

18

2006

Jul 1

6 20

06

Au

g 1

3 20

06

Sep

10

2006

Oct

08

2006

No

v 05

200

6

Dec

03

2006

Dec

31

2006

Jan

28

2007

Feb

25

2007

Mar

25

2007

Ap

r 22

200

7

May

20

2007

Jun

17

2007

Jul 1

5 20

07

Au

g 1

2 20

07

Sep

09

2007

Oct

07

2007

No

v 04

200

7

Dec

02

2007

Dec

30

2007

Jan

27

2008

Feb

24

2008

Mar

23

2008

Weekly 3 Point Centred Moving Average

Sh

are

(E

xp

en

dit

ure

)

Aldi / Lidl / Netto Aldi / Lidl / Netto Baseline

© WorldpanelTM division of TNS 2008

Long-Term Share of Till Roll Grocers

0

1

2

3

4

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

Sh

are

(E

xp

en

dit

ure

)

Aldi Lidl Netto

© WorldpanelTM division of TNS 2008

Kwik Save Share of Till Roll Grocers

0

0.5

1

1.5

2

Ap

r 24

200

5

May

22

2005

Jun

19

2005

Jul 1

7 20

05

Au

g 1

4 20

05

Sep

11

2005

Oct

09

2005

No

v 06

200

5

Dec

04

2005

Jan

01

2006

Jan

29

2006

Feb

26

2006

Mar

26

2006

Ap

r 23

200

6

May

21

2006

Jun

18

2006

Jul 1

6 20

06

Au

g 1

3 20

06

Sep

10

2006

Oct

08

2006

No

v 05

200

6

Dec

03

2006

Dec

31

2006

Jan

28

2007

Feb

25

2007

Mar

25

2007

Ap

r 22

200

7

May

20

2007

Jun

17

2007

Jul 1

5 20

07

Au

g 1

2 20

07

Sep

09

2007

Oct

07

2007

No

v 04

200

7

Dec

02

2007

Dec

30

2007

Jan

27

2008

Feb

24

2008

Mar

23

2008

Weekly 3 Point Centred Moving Average

Sh

are

(E

xp

en

dit

ure

)

Kwik Save Kwik Save Baseline

© WorldpanelTM division of TNS 2008

Kwik Save + Discounters

0

1

2

3

4

5

6

7

8

12-S

ep-0

4

10-O

ct-0

4

07-N

ov-0

4

05-D

ec-0

4

02-J

an-0

5

30-J

an-0

5

27-F

eb-0

5

27-M

ar-0

5

24-A

pr-0

5

22-M

ay-0

5

19-J

un-0

5

17-J

ul-0

5

14-A

ug-0

5

11-S

ep-0

5

09-O

ct-0

5

06-N

ov-0

5

04-D

ec-0

5

01-J

an-0

6

29-J

an-0

6

26-F

eb-0

6

26-M

ar-0

6

23-A

pr-0

6

21-M

ay-0

6

18-J

un-0

6

16-J

ul-0

6

13-A

ug-0

6

10-S

ep-0

6

08-O

ct-0

6

05-N

ov-0

6

03-D

ec-0

6

31-D

ec-0

6

28-J

an-0

7

25-F

eb-0

7

25-M

ar-0

7

22-A

pr-0

7

20-M

ay-0

7

17-J

un-0

7

15-J

ul-0

7

12-A

ug-0

7

09-S

ep-0

7

07-O

ct-0

7

04-N

ov-0

7

02-D

ec-0

7

30-D

ec-0

7

27-J

an-0

8

24-F

eb-0

8

23-M

ar-0

8

Kwik Save + Discounters

© WorldpanelTM division of TNS 2008

12

6

39

1

2

11

10

5

4

7

8

12

6

39

1

2

11

10

5

4

7

8

12

6

39

1

2

11

10

5

4

7

8

12

6

39

1

2

11

10

5

4

7

8

34%

11%

55%

40%

23%

37%

Usage occasionsby stated reasons

1995 2007Source: TNS Worldpanel Usage, Foods ConsumptionYear to August 2007

© WorldpanelTM division of TNS 2008

Agenda

Background

Organic Overview

Organic Markets

Fairtrade Overview

Fairtrade Markets

Free Range

Retail Aspects

Markets & Lifestyles

© WorldpanelTM division of TNS 2008

0

10

20

30

40

50

60

70

80

90

1001998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

£m’s

Total Organic Products

Annualised Value = £1,300m

7.50.121.721.60Price per Vol

-8.9-0.161.61.8Trip Vol

-2.1-0.062.762.81Trip Spend

-2.1-0.6329.830.4AWP (Vol per Buyer)

5.22.5551.1748.62AWP (Spend per Buyer)

7.51.2918.617.3Purchase Frequency

7.05.7888.883.0Penetration %

5.534185655777621592Volume (000s Units)

13.41328451126755993911Expenditure (£000s)

% Change

Actual Change

52 w/e 23 Mar 08

52 w/e 25 Mar 07

7.50.121.721.60Price per Vol

-8.9-0.161.61.8Trip Vol

-2.1-0.062.762.81Trip Spend

-2.1-0.6329.830.4AWP (Vol per Buyer)

5.22.5551.1748.62AWP (Spend per Buyer)

7.51.2918.617.3Purchase Frequency

7.05.7888.883.0Penetration %

5.534185655777621592Volume (000s Units)

13.41328451126755993911Expenditure (£000s)

% Change

Actual Change

52 w/e 23 Mar 08

52 w/e 25 Mar 07

-2E+05

-1E+05

-50000 0 50000 100000

150000

200000

250000

Penetration % Purchase Frequency

Trip Vol Price per Vol

Key Performance Indicators for Organic Grocery –Value up 13.4% worth £132.8m

Expenditure (£000s)

Volume (000s Units)

Penetration % *

Purchase FrequencyTrip Vol

AWP (Vol per Buyer)

Price per Vol

£1126.8m +13.4%

Increase of £132.8m

655.8m vol +5.5%

Contribution = £59.7m

88.8% +7%

Contribution = £75.7m

18.6 trips +7.5%

Contribution = £73.3m

1.6 vol -8.9%

Contribution = -£89.3m

29.8 vol -2.1%

Contribution = -£16m

£1.72 +7.5%

Contribution = £73.1m

* Pen Contribution includes Population

growth of 0.7%

© WorldpanelTM division of TNS 2008

Total Organics-£ Spend by Frequency Group

12

37

6

20

9

17

19

14

66

1

% Homes Buying % Spend

27+

13-26 Occasions

7-12 Occasions

2-6 Occasions

1 Occasion

12% of Organic buyers purchase once during the year & account for only 1% of spend14% of Organic buyers represent 66% of money spent on Organics

52 w/e Mar 23 2008

© WorldpanelTM division of TNS 2008

© WorldpanelTM division of TNS 2008

Agenda

Background

Organic Overview

Organic Markets

Fairtrade Overview

Fairtrade Markets

Free Range

Retail Aspects

Markets & Lifestyles

© WorldpanelTM division of TNS 2008

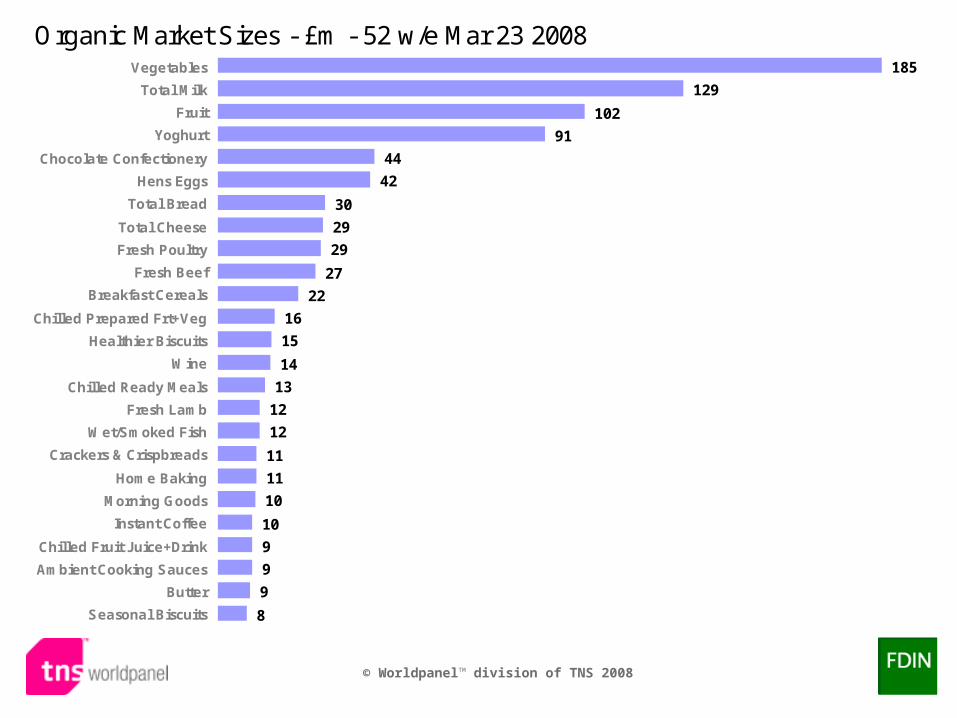

Organic Market Sizes - £m - 52 w/e Mar 23 2008185

129

102

91

44

42

30

29

29

27

22

16

15

14

13

12

12

11

11

10

10

9

9

9

8

Vegetables

Total Milk

Fruit

Yoghurt

Chocolate Confectionery

Hens Eggs

Total Bread

Total Cheese

Fresh Poultry

Fresh Beef

Breakfast Cereals

Chilled Prepared Frt+Veg

Healthier Biscuits

Wine

Chilled Ready Meals

Fresh Lamb

Wet/Smoked Fish

Crackers & Crispbreads

Home Baking

Morning Goods

Instant Coffee

Chilled Fruit Juice+Drink

Ambient Cooking Sauces

Butter

Seasonal Biscuits

© WorldpanelTM division of TNS 2008

Organic Proportion - £% - 52 w/e Mar 23 200824.4

16.9

12.2

9.2

9.1

8.9

8.3

8.1

7.4

6.8

6.7

6.6

6.5

6.3

5.9

4.8

4.7

4.7

4.5

4.4

4.3

4.2

4.0

3.9

3.8

Chilled Gravy+Stock

Canned Lemonade

Herbal Tea

Dry Pulses+Cereal

Ambient Flavoured Milk

Yoghurt

Vinegar

Ambient Vgtrn Products

Peanut Butter

Chilled Vegetarian

Hens Eggs

Honey

Flour

Syrup & Treacle

Chilled Salad Accomps

Cous Cous

Seasonal Biscuits

Liquid+Grnd Coffee+Beans

Crackers & Crispbreads

Total Milk

Vegetable

Dry Pasta

Healthier Biscuits

Tomato Products

Fresh Soup

© WorldpanelTM division of TNS 2008

Organic Growth - £m - 52 w/e Mar 23 2008 v. year ago17.6

14.1

14.0

9.4

7.7

7.0

5.3

3.7

3.7

3.0

2.9

2.8

2.6

2.4

2.4

2.2

2.1

2.0

2.0

1.9

1.8

1.7

1.5

1.3

1.3

Vegetables

Chocolate Confectionery

Total Milk

Yoghurt

Seasonal Biscuits

Fruit

Hens Eggs

Fresh Beef

Crackers & Crispbreads

Chilled Prepared Frt+Veg

Wine

Fresh Poultry

Shellfish

Chilled Ready Meals

Total Cheese

Nuts

Chilled Desserts

Beer+Lager

Fresh Sausages

Total Bread

Cooked Meats

Fresh Bacon Rashers

Dry Pasta

Tomato Products

Home Baking

© WorldpanelTM division of TNS 2008

Agenda

Background

Organic Overview

Organic Markets

Fairtrade Overview

Fairtrade Markets

Free Range

Retail Aspects

Markets & Lifestyles

-22.2-0.541.882.41Price per Vol

-7.9-0.060.70.8Trip Vol

-28.4-0.531.351.88Trip Spend

53.02.938.45.5AWP (Vol per Buyer)

19.02.5315.8513.32AWP (Spend per Buyer)

66.14.6811.77.1Purchase Frequency

23.612.8167.154.3Penetration %

90.46681714072973912Volume (000s Units)

48.185718264002178284Expenditure (£000s)

% Change

Actual Change

52 w/e 23 Mar 08

52 w/e 25 Mar 07

-22.2-0.541.882.41Price per Vol

-7.9-0.060.70.8Trip Vol

-28.4-0.531.351.88Trip Spend

53.02.938.45.5AWP (Vol per Buyer)

19.02.5315.8513.32AWP (Spend per Buyer)

66.14.6811.77.1Purchase Frequency

23.612.8167.154.3Penetration %

90.46681714072973912Volume (000s Units)

48.185718264002178284Expenditure (£000s)

% Change

Actual Change

52 w/e 23 Mar 08

52 w/e 25 Mar 07

-100000 -50000 0 50000 100000 150000 200000

Penetration % Purchase Frequency

Trip Vol Price per Vol

Key Performance Indicators for Fairtrade Grocery –Value up 48.1% worth £85.7m

Expenditure (£000s)

Volume (000s Units)

Penetration % *

Purchase FrequencyTrip Vol

AWP (Vol per Buyer)

Price per Vol

£264m +48.1%

Increase of £85.7m

140.7m vol +90.4%

Contribution = £129.4m

67.1% +23.6%

Contribution = £39.1m

11.7 trips +66.1%

Contribution = £105.8m

0.7 vol -7.9%

Contribution = -£15.5m

8.4 vol +53%

Contribution = £90.3m

£1.88 -22.2%

Contribution = -£43.7m

* Pen Contribution includes Population

growth of 0.7%

© WorldpanelTM division of TNS 2008

Total Fairtrade-£ Spend by Frequency Group

27

41

19

14

17

12

28

6

32

4

% Homes Buying % Spend

27+

13-26 Occasions

7-12 Occasions

2-6 Occasions

1 Occasion

27% of Fairtrade buyers purchase once during the year & account for only 4% of spend6% of Fairtrade buyers represent 32% of money spent on Fairtrade

52 w/e Mar 23 2008

© WorldpanelTM division of TNS 2008

Agenda

Background

Organic Overview

Organic Markets

Fairtrade Overview

Fairtrade Markets

Free Range

Retail Aspects

Markets & Lifestyles

© WorldpanelTM division of TNS 2008

Fairtrade Market Sizes - £m - 52 w/e Mar 23 2008140.4

27.0

21.2

20.3

15.0

13.6

4.4

2.8

2.0

1.6

1.5

1.4

1.4

1.4

1.4

1.3

1.1

1.1

0.9

0.7

0.7

0.4

0.4

0.3

0.2

Fruit

Instant Coffee

Liquid+Grnd Coffee+Beans

Tea

Chocolate Confectionery

Wine

Food Drinks

Sugar

Ambnt Fruit/Yght Juc+Drnk

Chocolate Biscuit Bars

Ambient Cakes+Pastries

Vegetables

Preserves

Nuts

Beer+Lager

Total Ice Cream

Honey

Healthier Biscuits

Powd Desserts&Custard

Home Baking

Herbs+Spices

Crackers & Crispbreads

Chilled Fruit Juice+Drink

Chilled Prepared Frt+Veg

Breakfast Cereals

© WorldpanelTM division of TNS 2008

Fairtrade Proportion - £% - 52 w/e Mar 23 200814.7

4.5

4.43.8

2.9

1.51.4

1.1

1.00.9

0.8

0.60.50.50.4

0.40.40.4

0.30.20.2

0.20.20.1

0.1

Liquid+Grnd Coffee+Beans

Tea

Instant Coffee

Fruit

Food Drinks

Honey

Powd Desserts&Custard

Sugar

Ambient Sponge Puddings

Preserves

Chocolate Confectionery

Herbs+Spices

Nuts

Chocolate Biscuit Bars

Ambnt Fruit/Yght Juc+Drnk

Wine

Chocolate Spread

Chilled Flavoured Milk

Healthier Biscuits

Total Ice Cream

Home Baking

Crackers & Crispbreads

Special Treats

Chilled One Shot Drinks

Ambient Cakes+Pastries

© WorldpanelTM division of TNS 2008

Fairtrade Growth - £m - 52 w/e Mar 23 2008 v. year ago72.9

2.9

2.4

1.1

1.0

1.0

0.9

0.9

0.9

0.9

0.7

0.7

0.6

0.5

0.4

0.4

0.2

0.1

0.1

0.1

0.1

0.1

0.1

0.0

0.0

Fruit

Wine

Chocolate Confectionery

Sugar

Beer+Lager

Preserves

Instant Coffee

Powd Desserts&Custard

Liquid+Grnd Coffee+Beans

Chocolate Biscuit Bars

Total Ice Cream

Healthier Biscuits

Nuts

Herbs+Spices

Home Baking

Crackers & Crispbreads

Chilled Prepared Frt+Veg

Chilled Flavoured Milk

Ambient Sponge Puddings

Chilled Fruit Juice+Drink

Honey

Vegetable

Cleaning Accessories

Ambient One Shot Drinks

Breakfast Cereals

© WorldpanelTM division of TNS 2008

Agenda

Background

Organic Overview

Organic Markets

Fairtrade Overview

Fairtrade Markets

Free Range

Retail Aspects

Markets & Lifestyles

© WorldpanelTM division of TNS 2008

Hens Eggs - Pricing Trends

4p

6p

8p

10p

12p

14p

16p

18p

20p

22p

24p

26p

28p

30p

32p

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

Free Range Non-Free Range Organic

Ave. Price per Egg

© WorldpanelTM division of TNS 2008

Hens Eggs - Organic Share Trends

0

1

2

3

4

5

6

7

8

9

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

Organic

Share - £%

© WorldpanelTM division of TNS 2008

Hens Eggs - 'Free Range' Share Trends

28

30

32

34

36

38

40

42

44

46

48

50

52

54

56

58

60

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

Free Range

Share - £%

© WorldpanelTM division of TNS 2008

Free Range Eggs - Performance Analysis

39.4 40.6

46.148.1

52.054.3

147140

133 132 134 138

20

25

30

35

40

45

50

55

60

52 w/e Jul 21 2002

52 w/e Jul 20 2003

52 w/e Jul 17 2005

52 w/e Mar26 2006

52 w/e Mar25 2007

52 w/e Mar23 2008

Sh

are

£%

100

150

200

250

Pri

ce p

er V

olu

me

Ind

ex

Share of Eggs Price per Volume Index

© WorldpanelTM division of TNS 2008

Free Range Chickens - Performance Analysis

7.48.0

9.0

129137 138

0

5

10

52 w/e Mar 26 2006 52 w/e Mar 25 2007 52 w/e Mar 23 2008

Sh

are

£%

100

150

200

250

Pri

ce p

er V

olu

me

Ind

ex

Share of Chickens Price per Volume Index

© WorldpanelTM division of TNS 2008

Free-range Market Share

0

2

4

6

8

10

12

14

Ap

r 2

4 2

00

5

Ma

y 2

2 2

00

5

Jun

19

20

05

Jul 1

7 2

00

5

Au

g 1

4 2

00

5

Se

p 1

1 2

00

5

Oct

09

20

05

No

v 0

6 2

00

5

De

c 0

4 2

00

5

Jan

01

20

06

Jan

29

20

06

Fe

b 2

6 2

00

6

Ma

r 2

6 2

00

6

Ap

r 2

3 2

00

6

Ma

y 2

1 2

00

6

Jun

18

20

06

Jul 1

6 2

00

6

Au

g 1

3 2

00

6

Se

p 1

0 2

00

6

Oct

08

20

06

No

v 0

5 2

00

6

De

c 0

3 2

00

6

De

c 3

1 2

00

6

Jan

28

20

07

Fe

b 2

5 2

00

7

Ma

r 2

5 2

00

7

Ap

r 2

2 2

00

7

Ma

y 2

0 2

00

7

Jun

17

20

07

Jul 1

5 2

00

7

Au

g 1

2 2

00

7

Se

p 0

9 2

00

7

Oct

07

20

07

No

v 0

4 2

00

7

De

c 0

2 2

00

7

De

c 3

0 2

00

7

Jan

27

20

08

Fe

b 2

4 2

00

8

Ma

r 2

3 2

00

8

Chickens

© WorldpanelTM division of TNS 2008

Free-range Market Share

0

10

20

30

40

50

60

70

Ap

r 2

4 2

00

5

Ma

y 2

2 2

00

5

Jun

19

20

05

Jul 1

7 2

00

5

Au

g 1

4 2

00

5

Se

p 1

1 2

00

5

Oct

09

20

05

No

v 0

6 2

00

5

De

c 0

4 2

00

5

Jan

01

20

06

Jan

29

20

06

Fe

b 2

6 2

00

6

Ma

r 2

6 2

00

6

Ap

r 2

3 2

00

6

Ma

y 2

1 2

00

6

Jun

18

20

06

Jul 1

6 2

00

6

Au

g 1

3 2

00

6

Se

p 1

0 2

00

6

Oct

08

20

06

No

v 0

5 2

00

6

De

c 0

3 2

00

6

De

c 3

1 2

00

6

Jan

28

20

07

Fe

b 2

5 2

00

7

Ma

r 2

5 2

00

7

Ap

r 2

2 2

00

7

Ma

y 2

0 2

00

7

Jun

17

20

07

Jul 1

5 2

00

7

Au

g 1

2 2

00

7

Se

p 0

9 2

00

7

Oct

07

20

07

No

v 0

4 2

00

7

De

c 0

2 2

00

7

De

c 3

0 2

00

7

Jan

27

20

08

Fe

b 2

4 2

00

8

Ma

r 2

3 2

00

8

Chickens

Hens eggs

© WorldpanelTM division of TNS 2008

Agenda

Background

Organic Overview

Organic Markets

Fairtrade Overview

Fairtrade Markets

Free Range

Retail Aspects

Markets & Lifestyles

© WorldpanelTM division of TNS 2008

I Regard Myself As A Connoisseur Of Food And Wine 215I Am Prepared To Pay More For Organic Food 202Country Of Origin Is Important To Me When Choosing Groceries 169The BBC Is An Institution That I Can Rely On 163I Look For Supermarkets That Are Less Crowded And Less Stressful To Shop In 160I Think It Is Worth Paying More To Shop Where I Can Get In And Out Of Quickly 159I Try To Support Regional Food Producers 159I Am Prepared To Pay More For Quality Ingredients 155I Try To Buy Local Produce Whenever I Can 145I Feel Good About Buying Fair Trade Products 145I Buy Free Range Products Whenever I Can 145I Always Pay My Credit Card Bills In Full 143I Eat Out Regularly 143I Believe In A Holistic Approach To Medical Treatment 140I Try To Buy Environmentally Friendly Products 139I Don't Tend To Compromise On Quality If I Can't Find What I Want 138I Don't Mind Paying For Quality 136I Think Of Myself As A Brand Loyal Consumer 136I Think We Should All Try To Buy More Fair Trade Products 135I/My Partner Enjoy Cooking To Entertain Friends And Family 134

Worldpanel Lifestyles - Waitrose Share Index

Till Roll Share indexed on All Shoppers – 52 w/e Feb 24 2008

© WorldpanelTM division of TNS 2008

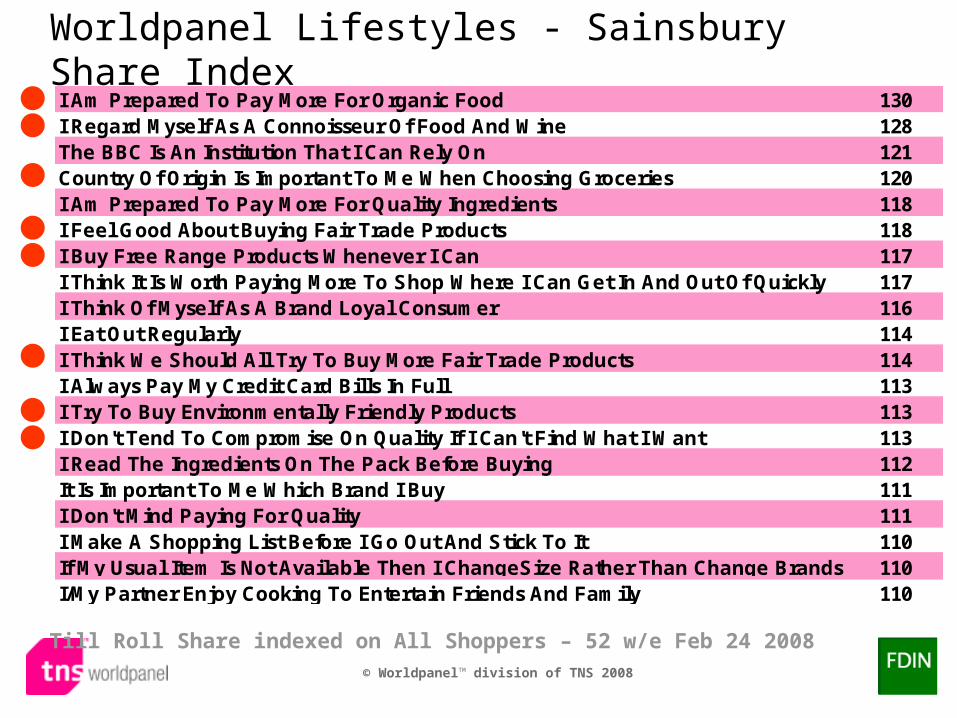

I Am Prepared To Pay More For Organic Food 130I Regard Myself As A Connoisseur Of Food And Wine 128The BBC Is An Institution That I Can Rely On 121Country Of Origin Is Important To Me When Choosing Groceries 120I Am Prepared To Pay More For Quality Ingredients 118I Feel Good About Buying Fair Trade Products 118I Buy Free Range Products Whenever I Can 117I Think It Is Worth Paying More To Shop Where I Can Get In And Out Of Quickly 117I Think Of Myself As A Brand Loyal Consumer 116I Eat Out Regularly 114I Think We Should All Try To Buy More Fair Trade Products 114I Always Pay My Credit Card Bills In Full 113I Try To Buy Environmentally Friendly Products 113I Don't Tend To Compromise On Quality If I Can't Find What I Want 113I Read The Ingredients On The Pack Before Buying 112It Is Important To Me Which Brand I Buy 111I Don't Mind Paying For Quality 111I Make A Shopping List Before I Go Out And Stick To It 110If My Usual Item Is Not Available Then I ChangeSize Rather Than Change Brands 110I/My Partner Enjoy Cooking To Entertain Friends And Family 110

Till Roll Share indexed on All Shoppers – 52 w/e Feb 24 2008

Worldpanel Lifestyles - Sainsbury Share Index

© WorldpanelTM division of TNS 2008

I Visit Different Shops For The Best Prices

151

139

130

130

126

117

106

103

101

100

95

89

87

83

Netto

Lidl

Aldi

Iceland

Farm Foods

Somerfield

Morrisons

Tot Indepts

Total Co-op

Asda

Tesco

Sainsbury

M & S

Waitrose

Outlet Share Index52 w/e Feb 24 2008

© WorldpanelTM division of TNS 2008

Organic Index v Social Class

Farm FoodsNetto Aldi

LidlIndepts

Co-op

Iceland

Morrisons

Waitrose

Somerfield

Asda

Tesco

Sainsbury

Tot Grocers

0

50

100

150

200

250

300

350

400

450

20 25 30 35 40 45 50 55 60 65 70

ABC1

Org

an

ic In

de

x

52 w/e Jan 27 2008

© WorldpanelTM division of TNS 2008

The Olive Index

© WorldpanelTM division of TNS 2008

The Olive Index

M & S

Farm Foods

Netto

Aldi

LidlTot Indepts

Total Co-op

Iceland

Morrisons

Waitrose

Kwik Save

SomerfieldAsda

Tesco

Sainsbury

0

5

10

15

20

25

30

35

40

0 50 100 150 200 250 300 350 400

Olive Trading Index

% C

las

s A

B

52 w/e Mar 23 2008

© WorldpanelTM division of TNS 2008

Organic Indices

445

151

140

103

100

61

55

49

37

33

22

21

10

1

0

Waitrose

Sainsbury

M & S

Tesco

Total Grocers

Asda

Co-op

Morrisons

Tot Indepts

Somerfield

Lidl

Aldi

Netto

Farm Foods

Iceland

Share of Organic Indexed onTotal Grocery Share - 52 w/e Mar 23 2008

© WorldpanelTM division of TNS 2008

Fairtrade Indices

379

331

226

200

100

54

52

42

37

15

12

10

1

0

0

Co-op

Waitrose

Sainsbury

M & S

Total Grocers

Morrisons

Asda

Tesco

Somerfield

Lidl

Tot Indepts

Netto

Aldi

Farm Foods

Iceland

Share of Fairtrade Indexed onTotal Grocery Share - 52 w/e Mar 23 2008

© WorldpanelTM division of TNS 2008

Asda Demographic SignaturesTill RollOutlet Share within Demographic Group - MAT to March

0

5

10

15

20

25

Class AB Class C1 Class C2 Class D Class E

2006 2007 2008

Social Class

0

5

10

15

20

25

Age under28

Age 28-34 Age 35-44 Age 45-64 Age 65+

2006 2007 2008

Housewife Age

0

5

10

15

20

25

1 in HH 2 in HH 3 in HH 4 in HH 5+ in HH

2006 2007 2008

Household Size

0

5

10

15

20

25

No Children 1 Child HH 2 Child HH 3+ Child HH

2006 2007 2008

No. of Children

13.5 C2DE Large households

Younger With children

© WorldpanelTM division of TNS 2008

Share of Total Grocers - Organic

32.6

25.8

18.2

9.1

6.4

3.6

2.4

1.4

0.7

0.2

0.2

0.1

0.0

0.0

0.0

0.0

33.2

25.2

17.6

10.1

6.2

4.6

2.4

1.3

0.7

0.5

0.5

0.1

0.0

0.0

0.0

0.0

Tesco

Sainsbury

Waitrose

Asda

Morrisons

M & S

Total Co-op

Somerfield

Tot Indepts

Lidl

Aldi

Netto

Safeway

Kwik Save

Iceland

Farm Foods

52 w/e Feb 24 200852 w/e Feb 25 2007

© WorldpanelTM division of TNS 2008

Year-on-Year Expenditure TrendsOrganic

23

13

11

8

7

7

Asda

Tesco

Tot Grocers

Sainsbury

Waitrose

Morrisons

52 w/e Feb 24 2008% Change

Strong performance in Organic

© WorldpanelTM division of TNS 2008

£% Change y/y 52 w/e Mar 23 2008

TPR Multibuy TPR Multibuy

All Outlets 15 -24 28 10Tesco 21 -23 55 25Asda 7 -22 51 -19 Sainsbury 28 -22 47 -10 Morrisons 24 -17 60 1Somerfield -2 -28 21 -27 Iceland -13 -18 -18 -99 Total Co-op -6 -55 -13 -42 Boots #N/A #N/A 18 8Superdrug #N/A #N/A 14 38

Total Grocery

Promotion Trends

© WorldpanelTM division of TNS 2008

Favourite Promotions amongst the Obese

107

106

104

104

100

99

Extra Free

Y for £X

2F1

MultiBuy

TPR

No Promotion

Share of Promotional PurchasingIndexed on All Households52 w/e Jan 27 2008

© WorldpanelTM division of TNS 2008

Fairtrade Bananas - Performance Analysis

20.0

21.5

27.7

129 130124

14

16

18

20

22

24

26

28

52 w/e Mar 26 2006 52 w/e Mar 25 2007 52 w/e Mar 23 2008

Sh

are

£%

100

150

200

250

Pri

ce p

er V

olu

me

Ind

ex

Share of Pre-packed Bananas Price per Volume Index

© WorldpanelTM division of TNS 2008

Fairtrade Prepacked Bananas Market Share

0

10

20

30

40

50

60

70

80

90

100

Apr

24

2005

May

22

2005

Jun

19 2

005

Jul 1

7 20

05

Aug

14

2005

Sep

11

2005

Oct

09

2005

Nov

06

2005

Dec

04

2005

Jan

01 2

006

Jan

29 2

006

Feb

26

2006

Mar

26

2006

Apr

23

2006

May

21

2006

Jun

18 2

006

Jul 1

6 20

06

Aug

13

2006

Sep

10

2006

Oct

08

2006

Nov

05

2006

Dec

03

2006

Dec

31

2006

Jan

28 2

007

Feb

25

2007

Mar

25

2007

Apr

22

2007

May

20

2007

Jun

17 2

007

Jul 1

5 20

07

Aug

12

2007

Sep

09

2007

Oct

07

2007

Nov

04

2007

Dec

02

2007

Dec

30

2007

Jan

27 2

008

Feb

24

2008

Mar

23

2008

Total Grocers

© WorldpanelTM division of TNS 2008

Fairtrade Prepacked Bananas Market Share

0

10

20

30

40

50

60

70

80

90

100

Apr

24

2005

May

22

2005

Jun

19 2

005

Jul 1

7 20

05

Aug

14

2005

Sep

11

2005

Oct

09

2005

Nov

06

2005

Dec

04

2005

Jan

01 2

006

Jan

29 2

006

Feb

26

2006

Mar

26

2006

Apr

23

2006

May

21

2006

Jun

18 2

006

Jul 1

6 20

06

Aug

13

2006

Sep

10

2006

Oct

08

2006

Nov

05

2006

Dec

03

2006

Dec

31

2006

Jan

28 2

007

Feb

25

2007

Mar

25

2007

Apr

22

2007

May

20

2007

Jun

17 2

007

Jul 1

5 20

07

Aug

12

2007

Sep

09

2007

Oct

07

2007

Nov

04

2007

Dec

02

2007

Dec

30

2007

Jan

27 2

008

Feb

24

2008

Mar

23

2008

Total Grocers

Sainsbury's

© WorldpanelTM division of TNS 2008

Free-range Eggs Market Share

30

40

50

60

70

80

90

100

Ap

r 2

4 2

00

5

Ma

y 2

2 2

00

5

Jun

19

20

05

Jul 1

7 2

00

5

Au

g 1

4 2

00

5

Se

p 1

1 2

00

5

Oct

09

20

05

No

v 0

6 2

00

5

De

c 0

4 2

00

5

Jan

01

20

06

Jan

29

20

06

Fe

b 2

6 2

00

6

Ma

r 2

6 2

00

6

Ap

r 2

3 2

00

6

Ma

y 2

1 2

00

6

Jun

18

20

06

Jul 1

6 2

00

6

Au

g 1

3 2

00

6

Se

p 1

0 2

00

6

Oct

08

20

06

No

v 0

5 2

00

6

De

c 0

3 2

00

6

De

c 3

1 2

00

6

Jan

28

20

07

Fe

b 2

5 2

00

7

Ma

r 2

5 2

00

7

Ap

r 2

2 2

00

7

Ma

y 2

0 2

00

7

Jun

17

20

07

Jul 1

5 2

00

7

Au

g 1

2 2

00

7

Se

p 0

9 2

00

7

Oct

07

20

07

No

v 0

4 2

00

7

De

c 0

2 2

00

7

De

c 3

0 2

00

7

Jan

27

20

08

Fe

b 2

4 2

00

8

Ma

r 2

3 2

00

8

Total Grocers

© WorldpanelTM division of TNS 2008

Free-range Eggs Market Share

30

40

50

60

70

80

90

100

Ap

r 2

4 2

00

5

Ma

y 2

2 2

00

5

Jun

19

20

05

Jul 1

7 2

00

5

Au

g 1

4 2

00

5

Se

p 1

1 2

00

5

Oct

09

20

05

No

v 0

6 2

00

5

De

c 0

4 2

00

5

Jan

01

20

06

Jan

29

20

06

Fe

b 2

6 2

00

6

Ma

r 2

6 2

00

6

Ap

r 2

3 2

00

6

Ma

y 2

1 2

00

6

Jun

18

20

06

Jul 1

6 2

00

6

Au

g 1

3 2

00

6

Se

p 1

0 2

00

6

Oct

08

20

06

No

v 0

5 2

00

6

De

c 0

3 2

00

6

De

c 3

1 2

00

6

Jan

28

20

07

Fe

b 2

5 2

00

7

Ma

r 2

5 2

00

7

Ap

r 2

2 2

00

7

Ma

y 2

0 2

00

7

Jun

17

20

07

Jul 1

5 2

00

7

Au

g 1

2 2

00

7

Se

p 0

9 2

00

7

Oct

07

20

07

No

v 0

4 2

00

7

De

c 0

2 2

00

7

De

c 3

0 2

00

7

Jan

27

20

08

Fe

b 2

4 2

00

8

Ma

r 2

3 2

00

8

Total Grocers

Sainsbury's

© WorldpanelTM division of TNS 2008

Free-range Eggs Market Share

30

40

50

60

70

80

90

100

Ap

r 2

4 2

00

5

Ma

y 2

2 2

00

5

Jun

19

20

05

Jul 1

7 2

00

5

Au

g 1

4 2

00

5

Se

p 1

1 2

00

5

Oct

09

20

05

No

v 0

6 2

00

5

De

c 0

4 2

00

5

Jan

01

20

06

Jan

29

20

06

Fe

b 2

6 2

00

6

Ma

r 2

6 2

00

6

Ap

r 2

3 2

00

6

Ma

y 2

1 2

00

6

Jun

18

20

06

Jul 1

6 2

00

6

Au

g 1

3 2

00

6

Se

p 1

0 2

00

6

Oct

08

20

06

No

v 0

5 2

00

6

De

c 0

3 2

00

6

De

c 3

1 2

00

6

Jan

28

20

07

Fe

b 2

5 2

00

7

Ma

r 2

5 2

00

7

Ap

r 2

2 2

00

7

Ma

y 2

0 2

00

7

Jun

17

20

07

Jul 1

5 2

00

7

Au

g 1

2 2

00

7

Se

p 0

9 2

00

7

Oct

07

20

07

No

v 0

4 2

00

7

De

c 0

2 2

00

7

De

c 3

0 2

00

7

Jan

27

20

08

Fe

b 2

4 2

00

8

Ma

r 2

3 2

00

8

Total Grocers

Sainsbury's

Waitrose

© WorldpanelTM division of TNS 2008

Morrisons+Safeway Year-on-Year Trends - Till Roll £%

-20

-15

-10

-5

0

5

10

12-S

ep-0

4

10-O

ct-0

4

07-N

ov-

04

05-D

ec-0

4

02-J

an-0

5

30-J

an-0

5

27-F

eb-0

5

27-M

ar-0

5

24-A

pr-

05

22-M

ay-0

5

19-J

un

-05

17-J

ul-

05

14-A

ug

-05

11-S

ep-0

5

09-O

ct-0

5

06-N

ov-

05

04-D

ec-0

5

01-J

an-0

6

29-J

an-0

6

26-F

eb-0

6

26-M

ar-0

6

23-A

pr-

06

21-M

ay-0

6

18-J

un

-06

16-J

ul-

06

13-A

ug

-06

10-S

ep-0

6

08-O

ct-0

6

05-N

ov-

06

03-D

ec-0

6

31-D

ec-0

6

28-J

an-0

7

25-F

eb-0

7

25-M

ar-0

7

22-A

pr-

07

20-M

ay-0

7

17-J

un

-07

15-J

ul-

07

12-A

ug

-07

09-S

ep-0

7

07-O

ct-0

7

04-N

ov-

07

02-D

ec-0

7

30-D

ec-0

7

27-J

an-0

8

24-F

eb-0

8

23-M

ar-0

8

12 w/e Periods

Store sell-offs

Now stable

© WorldpanelTM division of TNS 2008

© WorldpanelTM division of TNS 2008

© WorldpanelTM division of TNS 2008

Morrisons Shoppers – London Lifestyles

Till Roll Share indexed on All Shoppers – 52 w/e Mar 25 2007

I Only Eat To Fill Up 142I Think Health Foods Are Only Bought By Fanatics 142It's A Struggle To Pay Bills At The End Of The Month 140I'm Not Really Worried About Eating Healthily 131I Work To A Strict Budget When I'm Buying Groceries 127I Visit Different Shops For The Best Prices 126People Regularly Smoke In My House 122I Shop Around To Take Advantage Of Special Offers 114I Buy Clothes For Comfort Not Style 112I'm Often On A Diet To Lose Weight 112I Consider That Price Is The Most Important Factor 111

111111110108

I Like Having My Evening Meal In Front Of The TV 108108

I Live For The Moment 108107107

© WorldpanelTM division of TNS 2008

In the opinion of Londoners………

=

© WorldpanelTM division of TNS 2008

© WorldpanelTM division of TNS 2008

© WorldpanelTM division of TNS 2008

Latest Quarter Till Roll Totals Expenditure Trends

12

11

11

8

8

7

6

6

5

4

2

Iceland

Morrisons

Total Hard Disc

Waitrose

Asda

Tot Grocers

Tesco

Tot Indepts

Sainsbury

Somerfield

Total Co-op

12 w/e Mar 23 2008y/y % Change

© WorldpanelTM division of TNS 2008

I Try To Support Regional Food Producers

70

75

80

85

90

95

100

105

110

115

12024

-Ap

r-05

22-M

ay-0

5

19-J

un

-05

17-J

ul-

05

14-A

ug

-05

11-S

ep-0

5

09-O

ct-0

5

06-N

ov-

05

04-D

ec-0

5

01-J

an-0

6

29-J

an-0

6

26-F

eb-0

6

26-M

ar-0

6

23-A

pr-

06

21-M

ay-0

6

18-J

un

-06

16-J

ul-

06

13-A

ug

-06

10-S

ep-0

6

08-O

ct-0

6

05-N

ov-

06

03-D

ec-0

6

31-D

ec-0

6

28-J

an-0

7

25-F

eb-0

7

25-M

ar-0

7

22-A

pr-

07

20-M

ay-0

7

17-J

un

-07

15-J

ul-

07

12-A

ug

-07

09-S

ep-0

7

07-O

ct-0

7

04-N

ov-

07

02-D

ec-0

7

30-D

ec-0

7

27-J

an-0

8

24-F

eb-0

8

23-M

ar-0

8

Sainsbury

Tesco

Asda

Morrisons

Till Roll Share Index - Share amongst respondents agreeing with statement indexed on All Respondents

© WorldpanelTM division of TNS 2008

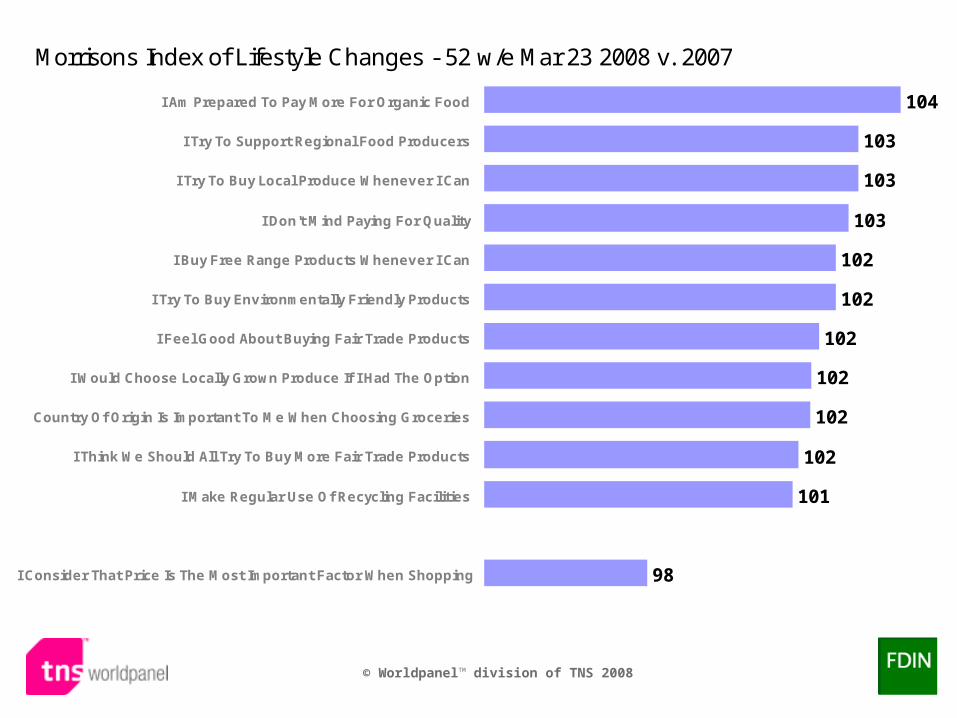

Morrisons Index of Lifestyle Changes - 52 w/e Mar 23 2008 v. 2007

104

103

103

103

102

102

102

102

102

102

101

98

I Am Prepared To Pay More For Organic Food

I Try To Support Regional Food Producers

I Try To Buy Local Produce Whenever I Can

I Don't Mind Paying For Quality

I Buy Free Range Products Whenever I Can

I Try To Buy Environmentally Friendly Products

I Feel Good About Buying Fair Trade Products

I Would Choose Locally Grown Produce If I Had The Option

Country Of Origin Is Important To Me When Choosing Groceries

I Think We Should All Try To Buy More Fair Trade Products

I Make Regular Use Of Recycling Facilities

I Consider That Price Is The Most Important Factor When Shopping

© WorldpanelTM division of TNS 2008

Agenda

Background

Organic Overview

Organic Markets

Fairtrade Overview

Fairtrade Markets

Free Range

Retail Aspects

Markets & Lifestyles

© WorldpanelTM division of TNS 2008

I Feel Good About Buying Fair Trade Products

146

134

131

127

127

127

124

122

120

119

119

118

117

116

116

115

115

114

113

Chilled Olives

Chilled Vegetarian

Herbal Tea

Dry Pulses+Cereal

Fresh Soup

Frozen Vegetarian Prods

Liquid+Grnd Coffee+Beans

Home Baking

Chilled Salad Accomps

Fresh Stuffing

Wet/Smoked Fish

Flour

Chilled Dips

Mincemeat (Sweet)

Fresh Pasta

Honey

Syrup & Treacle

Chilled Fruit Juice+Drink

Chilled One Shot Drinks

Market Share Index52 w/e Mar 23 2008

© WorldpanelTM division of TNS 2008

I Try To Buy Environmentally Friendly Products

139

131

130

130

124

123

121

121

120

120

120

119

119

118

117

115

115

113

113

Chilled Vegetarian

Frozen Vegetarian Prods

Dry Pulses+Cereal

Herbal Tea

Chilled Olives

Liquid+Grnd Coffee+Beans

Flour

Ambient Vgtrn Products

Fresh Soup

Honey

Syrup & Treacle

Home Baking

Wet/Smoked Fish

Mincemeat (Sweet)

Chilled Dips

Cous Cous

Soda Water

Peanut Butter

Fortified Wines

Market Share Index52 w/e Mar 23 2008

© WorldpanelTM division of TNS 2008

I Try To Buy Local Produce Whenever I Can 131

128

126

126

126

126

125

125

125

124

123

122

122

122

121

120

119

118

118

Fresh Other Meat & Offal

Mincemeat (Sweet)

Honey

Liquid+Grnd Coffee+Beans

Herbal Tea

Flour

Ginger Ale

Dry Pulses+Cereal

Suet

Fresh Stuffing

Wet/Smoked Fish

Fresh/Chilled Pastry

Home Baking

Tonic Water

Fortified Wines

Fresh Soup

Ready To Use Icing

Chilled Olives

Vinegar

Market Share Index52 w/e Mar 23 2008

© WorldpanelTM division of TNS 2008

I Am Prepared To Pay More For Organic Food

180

175

166

157

157

149

146

146

142

142

142

139

138

136

136

135

135

132

131

Chilled Vegetarian

Fresh Soup

Dry Pulses+Cereal

Chilled One Shot Drinks

Herbal Tea

Honey

Chilled Salad Accomps

Chilled Olives

Chilled Dips

Frozen Vegetarian Prods

Soda Water

Liquid+Grnd Coffee+Beans

Chilled Cooking Sauces

Chilled Fruit Juice+Drink

Fresh Pasta

Home Baking

Cous Cous

Flour

Ambient Vgtrn Products

Market Share Index52 w/e Mar 23 2008

© WorldpanelTM division of TNS 2008

I Buy Free Range Products Whenever I Can

142

136

133

132

131

128

126

125

124

119

119

118

118

117

117

117

116

116

115

Chilled Vegetarian

Chilled Olives

Herbal Tea

Frozen Vegetarian Prods

Fresh Soup

Dry Pulses+Cereal

Honey

Liquid+Grnd Coffee+Beans

Wet/Smoked Fish

Fresh Other Meat & Offal

Chilled Prepared Fish

Flour

Home Baking

Chilled Cooking Sauces

Fresh Pasta

Tonic Water

Chilled Dips

Vinegar

Chilled Salad Accomps

Market Share Index52 w/e Mar 23 2008

© WorldpanelTM division of TNS 2008

I Make Regular Use Of Recycling Facilities

109

108

108

108

108

108

107

107

107

107

107

107

106

106

106

106

106

106

105

Home Baking

Suet

Flour

Honey

Mincemeat (Sweet)

Chilled Olives

Herbal Tea

Fresh Other Meat & Offal

Liquid+Grnd Coffee+Beans

Syrup & Treacle

Frozen Stuffing

Wet/Smoked Fish

Tonic Water

Wine

Ginger Ale

Ready To Use Icing

Fresh Stuffing

Instant Milk

Dry Pulses+Cereal

Market Share Index52 w/e Mar 23 2008

© WorldpanelTM division of TNS 2008

27

30

% of French homes buying

‘organic’ 2005 2007

12

22

% of French homes buying

‘fair trade’

2005 2007

© WorldpanelTM division of TNS 2008

Will pay for quality

42676065

GB France Spain Germany

Like to keep myself in shape

617385

46

GB France Spain Germany

© WorldpanelTM division of TNS 2008

Reminders

© WorldpanelTM division of TNS 2008

Reminders

Background

© WorldpanelTM division of TNS 2008

Organic

Reminders

Background

© WorldpanelTM division of TNS 2008

Background

Fairtrade

Reminders

Organic

© WorldpanelTM division of TNS 2008

Free Range

Background

Reminders

Organic

Fairtrade

© WorldpanelTM division of TNS 2008

Background

Reminders

RetailAspects

Organic

Fairtrade

Free Range

© WorldpanelTM division of TNS 2008

Markets&

Lifestyles

Background

Reminders

Organic

Fairtrade

Free Range

RetailAspects