Embed Size (px)

Citation preview

Oil Market Dynamics,

Paradigms and Performance

__________________________________________________________________________________________________________________________________________________________

___________________________________________________________________________________________________________________________

II Congreso Día de la Energía 2013 // 3 July 2013

Ramón Espinasa, Lead Specialist (Oil & Gas)

Dynamics of Petroleum Markets

Oil Sector Performance and Institutional Frameworks

1

3

A New World Energy Paradigm

2

The Peruvian Case

4

1

Dynamics of Petroleum Markets

Commodity Prices

Supply

A

Demand B

C

0

20

40

60

80

100

120

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

Avg. 1984─2001 US$ 19.9

(nominal prices)

Avg. 2002─2013 US$ 63.4

(nominal prices)

US$

/ b

arre

l, n

om

inal

A

Commodity Prices

Source: BP Statistical Review of World Energy 2012

0

20

40

60

80

100

120

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

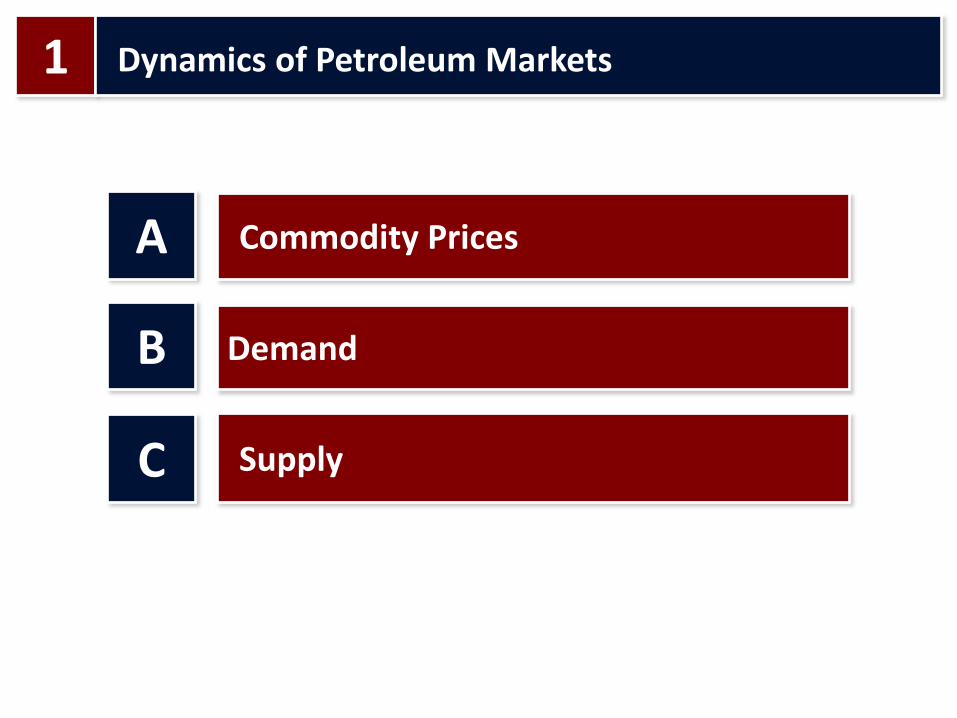

Avg. 1984─2001 US$ 33.0

(2011 US$ prices)

Avg. 2002─2013 US$ 68.6

(2011 US$ prices)

20

11

US$

/ b

arre

l

A

Commodity Prices

Source: BP Statistical Review of World Energy 2012

-

50

100

150

200

250

ene

-96

jul-

96

ene

-97

jul-

97

ene

-98

jul-

98

ene

-99

jul-

99

ene

-00

jul-

00

ene

-01

jul-

01

ene

-02

jul-

02

ene

-03

jul-

03

ene

-04

jul-

04

ene

-05

jul-

05

ene

-06

jul-

06

ene

-07

jul-

07

ene

-08

jul-

08

ene

-09

jul-

09

ene

-10

jul-

10

ene

-11

jul-

11

ene

-12

jul-

12

ene

-13

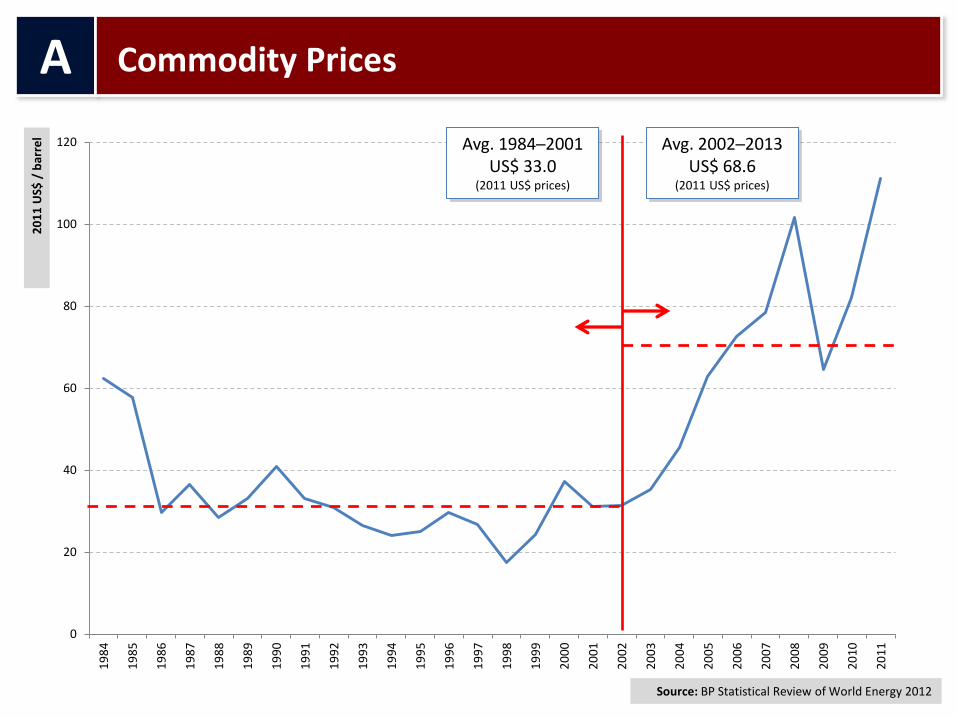

Energy

Pri

ce In

de

x, 2

00

5 =

10

0

A

Commodity Prices

Source: World Bank

-

50

100

150

200

250

ene

-96

jul-

96

ene

-97

jul-

97

ene

-98

jul-

98

ene

-99

jul-

99

ene

-00

jul-

00

ene

-01

jul-

01

ene

-02

jul-

02

ene

-03

jul-

03

ene

-04

jul-

04

ene

-05

jul-

05

ene

-06

jul-

06

ene

-07

jul-

07

ene

-08

jul-

08

ene

-09

jul-

09

ene

-10

jul-

10

ene

-11

jul-

11

ene

-12

jul-

12

ene

-13

Energy Food

Pri

ce In

de

x, 2

00

5 =

10

0

A

Commodity Prices

Source: World Bank

-

50

100

150

200

250

ene

-96

jul-

96

ene

-97

jul-

97

ene

-98

jul-

98

ene

-99

jul-

99

ene

-00

jul-

00

ene

-01

jul-

01

ene

-02

jul-

02

ene

-03

jul-

03

ene

-04

jul-

04

ene

-05

jul-

05

ene

-06

jul-

06

ene

-07

jul-

07

ene

-08

jul-

08

ene

-09

jul-

09

ene

-10

jul-

10

ene

-11

jul-

11

ene

-12

jul-

12

ene

-13

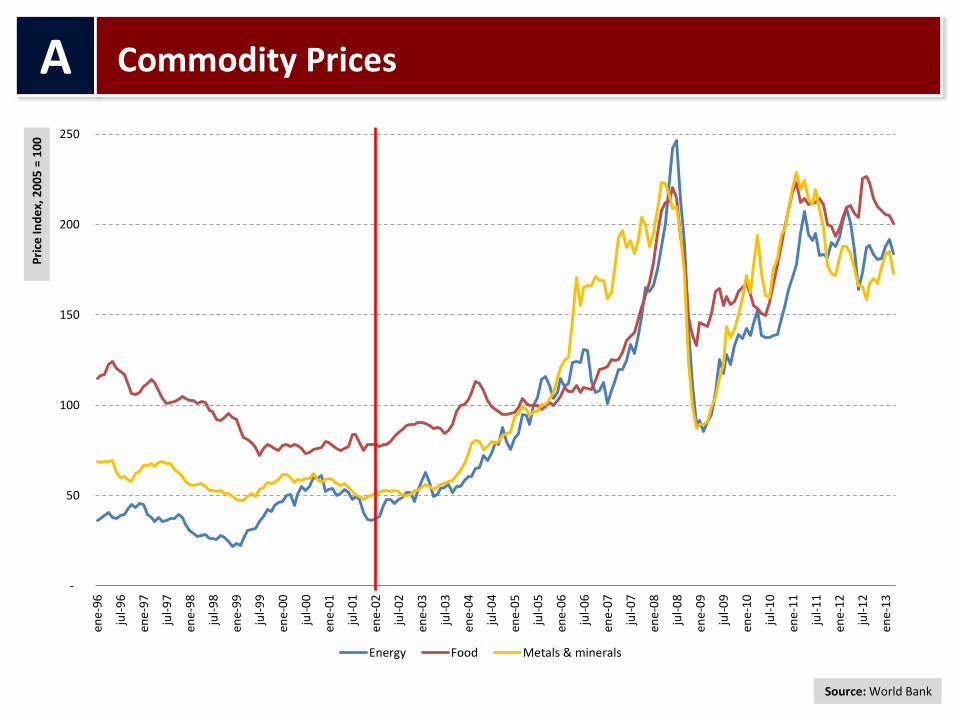

Energy Food Metals & minerals

Pri

ce In

de

x, 2

00

5 =

10

0

A

Commodity Prices

Source: World Bank

-

50

100

150

200

250

ene

-96

jul-

96

ene

-97

jul-

97

ene

-98

jul-

98

ene

-99

jul-

99

ene

-00

jul-

00

ene

-01

jul-

01

ene

-02

jul-

02

ene

-03

jul-

03

ene

-04

jul-

04

ene

-05

jul-

05

ene

-06

jul-

06

ene

-07

jul-

07

ene

-08

jul-

08

ene

-09

jul-

09

ene

-10

jul-

10

ene

-11

jul-

11

ene

-12

jul-

12

ene

-13

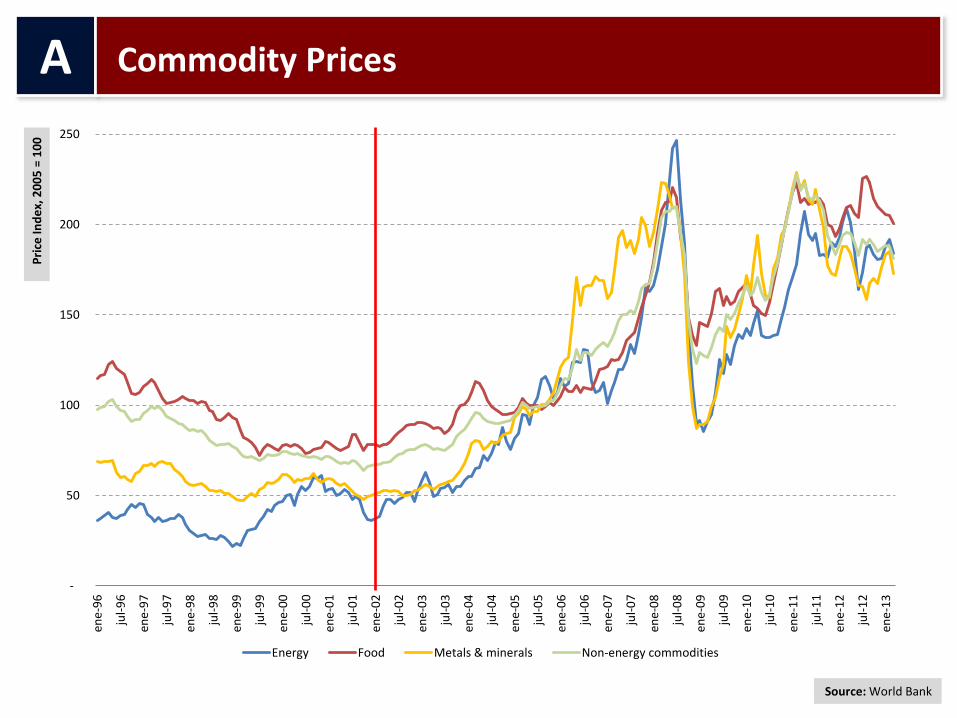

Energy Food Metals & minerals Non-energy commodities

Pri

ce In

de

x, 2

00

5 =

10

0

A

Commodity Prices

Source: World Bank

1. Oil prices increased threefold in nominal terms and twofold in real terms in the years after 2002 compared to very stable prices prevailing in the seventeen years after 1984.

2. This price behavior is not exclusive of oil / energy but is replicated by other commodities and food prices.

3. The increase in the price of all commodities as from 2002 is due to a demand push from the non-OECD countries, particularly Asian.

4. For the specific case of oil the structural factors behind the price increase are the demand push from the Non-OECD coupled with a shift towards more expensive production in the OECD countries as will be described next.

A

Commodity Prices: Observations

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

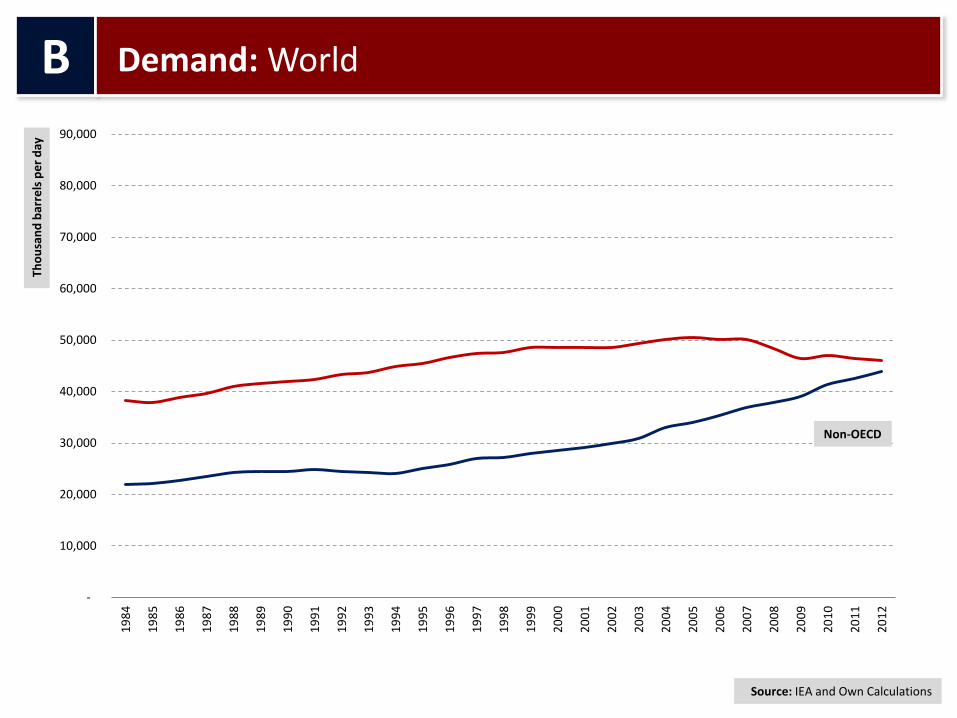

B

Demand: World Th

ou

san

d b

arre

ls p

er

day

OECD

Source: IEA and Own Calculations

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

B

Demand: World Th

ou

san

d b

arre

ls p

er

day

Non-OECD

Source: IEA and Own Calculations

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

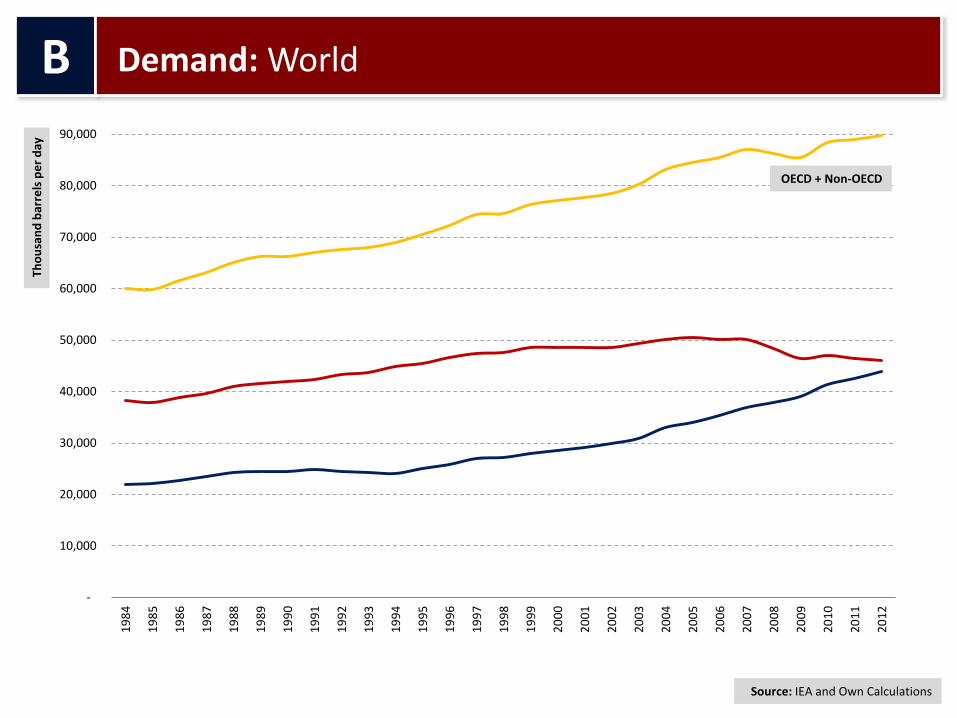

B

Demand: World Th

ou

san

d b

arre

ls p

er

day

OECD + Non-OECD

Source: IEA and Own Calculations

(3,000)

-

3,000

6,000

9,000

12,000

15,000

18,000

21,000

24,000

27,000

30,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Tho

usa

nd

bar

rels

pe

r d

ay

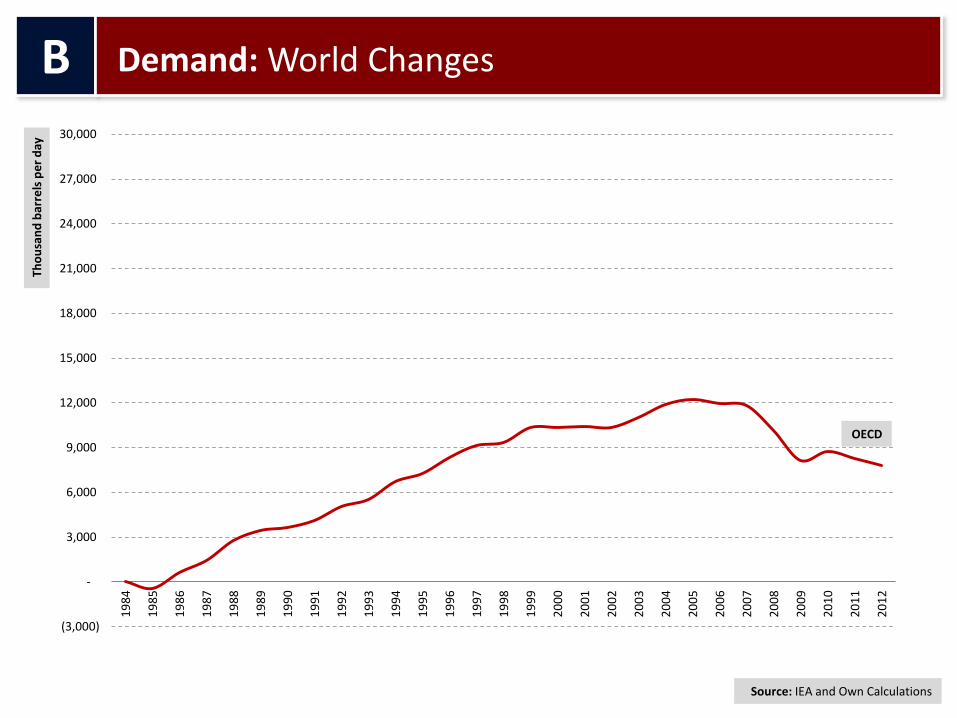

B

Demand: World Changes

OECD

Source: IEA and Own Calculations

(3,000)

-

3,000

6,000

9,000

12,000

15,000

18,000

21,000

24,000

27,000

30,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Tho

usa

nd

bar

rels

pe

r d

ay

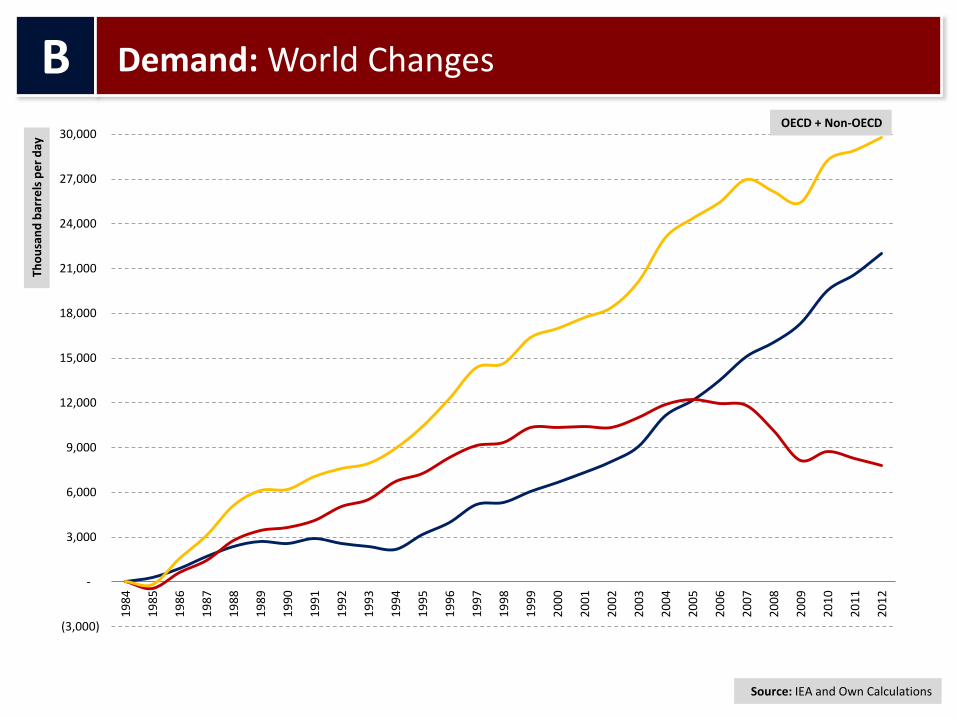

B

Demand: World Changes

Non-OECD

Source: IEA and Own Calculations

(3,000)

-

3,000

6,000

9,000

12,000

15,000

18,000

21,000

24,000

27,000

30,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Tho

usa

nd

bar

rels

pe

r d

ay

B

Demand: World Changes

OECD + Non-OECD

Source: IEA and Own Calculations

-

5,000

10,000

15,000

20,000

25,000

30,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

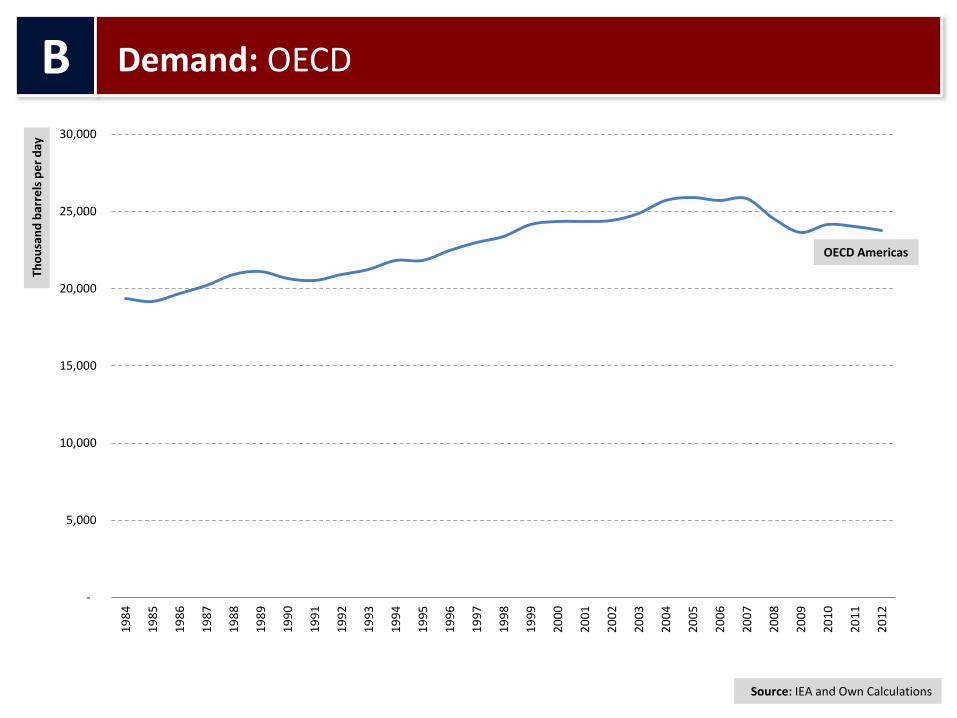

B

Demand: OECD Th

ou

san

d b

arre

ls p

er

day

OECD Americas

Source: IEA and Own Calculations

-

5,000

10,000

15,000

20,000

25,000

30,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

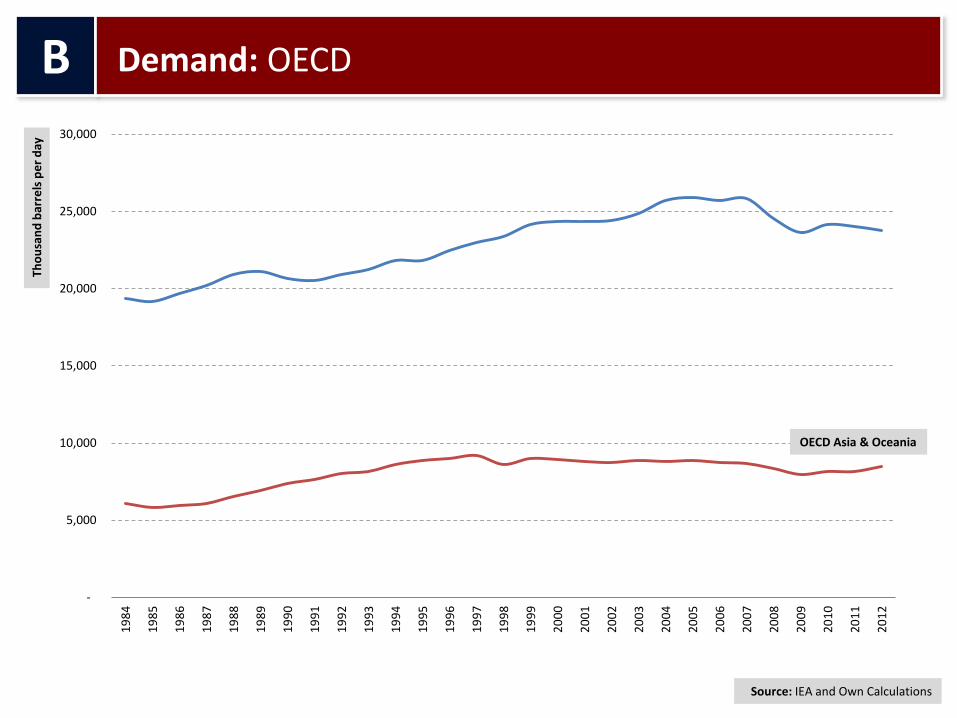

B

Demand: OECD Th

ou

san

d b

arre

ls p

er

day

OECD Asia & Oceania

Source: IEA and Own Calculations

-

5,000

10,000

15,000

20,000

25,000

30,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

B

Demand: OECD Th

ou

san

d b

arre

ls p

er

day

OECD Europe

Source: IEA and Own Calculations

(1,000)

-

1,000

2,000

3,000

4,000

5,000

6,000

7,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

B

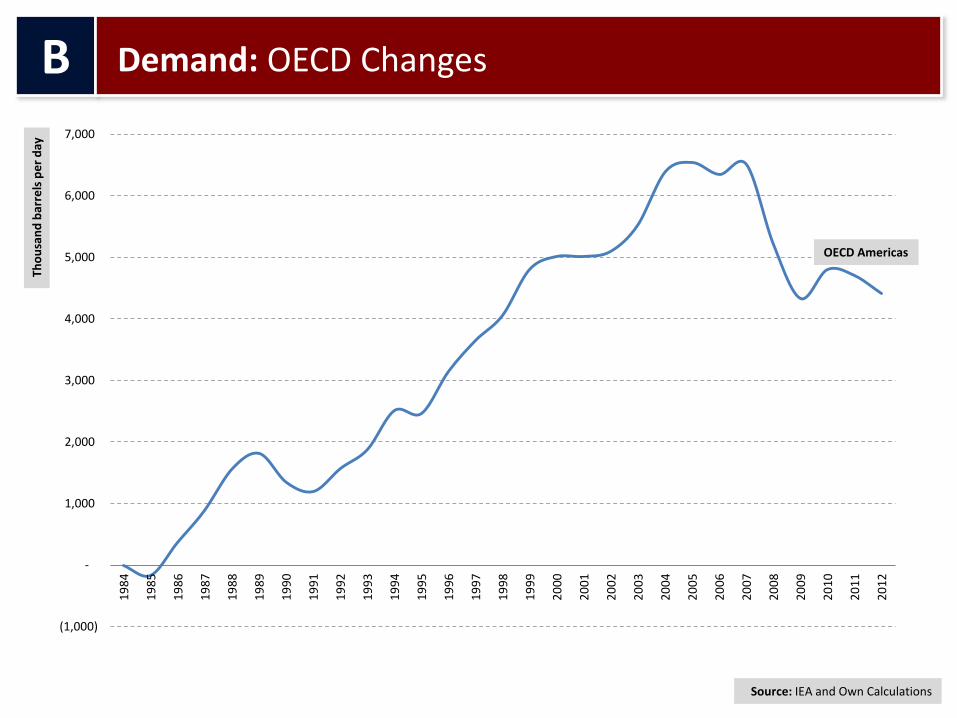

Demand: OECD Changes Th

ou

san

d b

arre

ls p

er

day

OECD Americas

Source: IEA and Own Calculations

(1,000)

-

1,000

2,000

3,000

4,000

5,000

6,000

7,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

B

Demand: OECD Changes Th

ou

san

d b

arre

ls p

er

day

OECD Asia & Oceania

Source: IEA and Own Calculations

(1,000)

-

1,000

2,000

3,000

4,000

5,000

6,000

7,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

B

Demand: OECD Changes Th

ou

san

d b

arre

ls p

er

day

OECD Europe

Source: IEA and Own Calculations

-

2,000

4,000

6,000

8,000

10,000

12,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

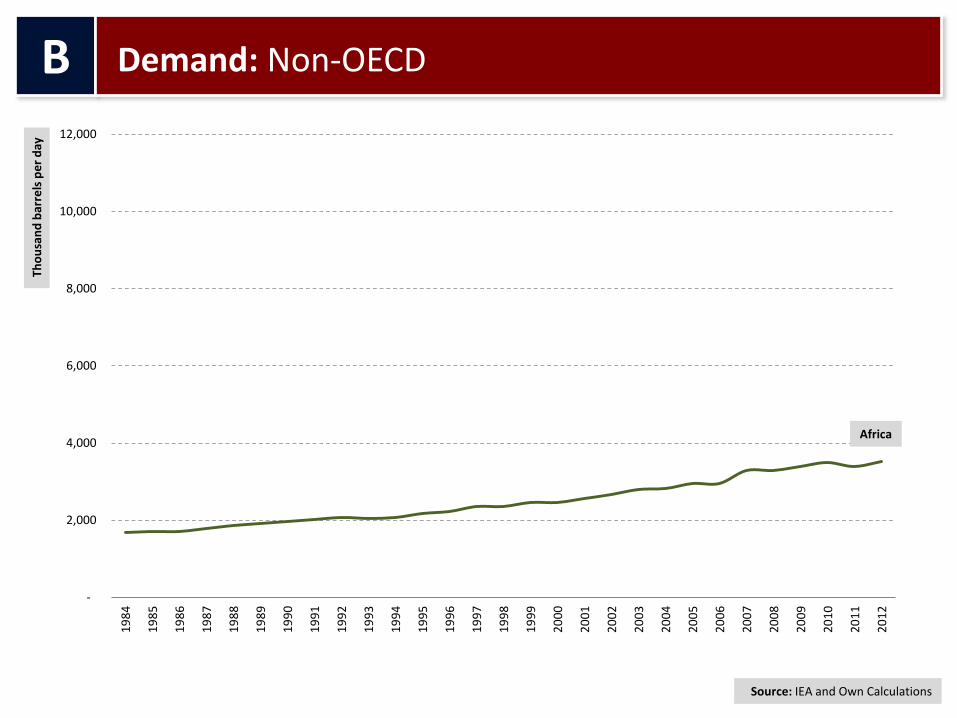

B

Demand: Non-OECD Th

ou

san

d b

arre

ls p

er

day

Africa

Source: IEA and Own Calculations

-

2,000

4,000

6,000

8,000

10,000

12,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

B

Demand: Non-OECD Th

ou

san

d b

arre

ls p

er

day

China

Source: IEA and Own Calculations

-

2,000

4,000

6,000

8,000

10,000

12,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

B

Demand: Non-OECD Th

ou

san

d b

arre

ls p

er

day

Former USSR

Source: IEA and Own Calculations

-

2,000

4,000

6,000

8,000

10,000

12,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

B

Demand: Non-OECD Th

ou

san

d b

arre

ls p

er

day

Middle East

Source: IEA and Own Calculations

-

2,000

4,000

6,000

8,000

10,000

12,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

B

Demand: Non-OECD Th

ou

san

d b

arre

ls p

er

day

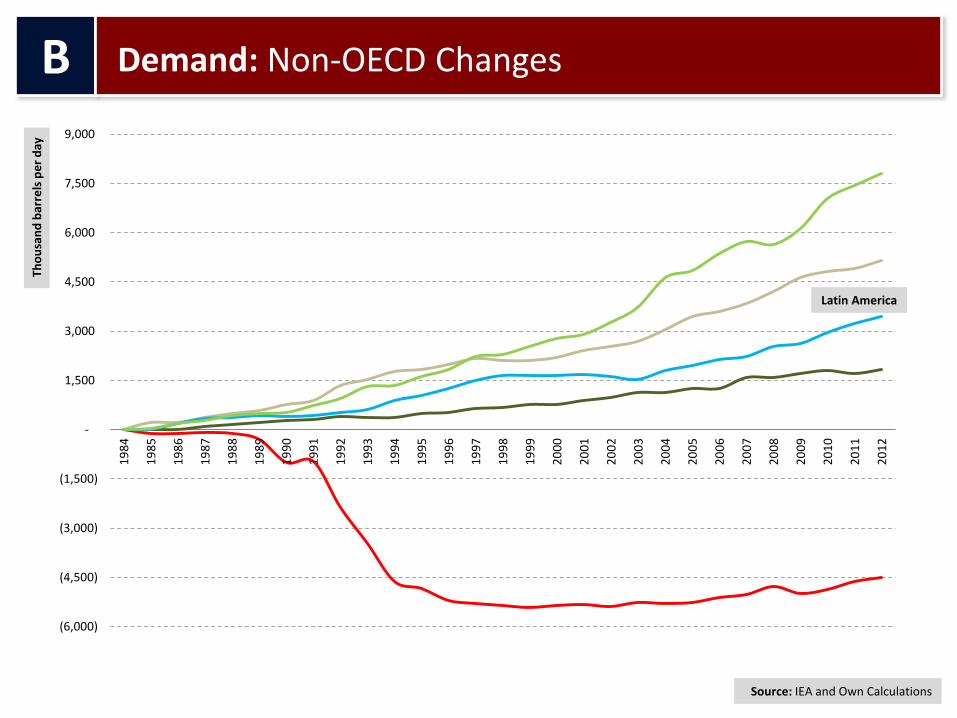

Latin America

Source: IEA and Own Calculations

-

2,000

4,000

6,000

8,000

10,000

12,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

B

Demand: Non-OECD Th

ou

san

d b

arre

ls p

er

day

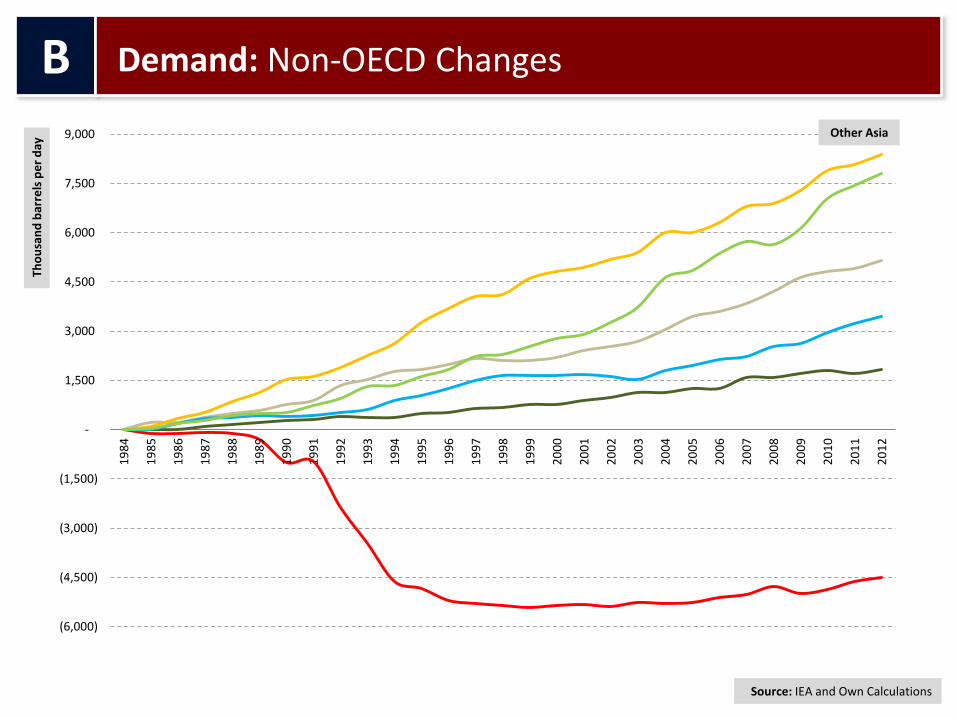

Other Asia

Source: IEA and Own Calculations

(6,000)

(4,500)

(3,000)

(1,500)

-

1,500

3,000

4,500

6,000

7,500

9,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

B

Demand: Non-OECD Changes Th

ou

san

d b

arre

ls p

er

day

Africa

Source: IEA and Own Calculations

(6,000)

(4,500)

(3,000)

(1,500)

-

1,500

3,000

4,500

6,000

7,500

9,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

B

Demand: Non-OECD Changes Th

ou

san

d b

arre

ls p

er

day

China

Source: IEA and Own Calculations

(6,000)

(4,500)

(3,000)

(1,500)

-

1,500

3,000

4,500

6,000

7,500

9,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

B

Demand: Non-OECD Changes Th

ou

san

d b

arre

ls p

er

day

Former USSR

Source: IEA and Own Calculations

(6,000)

(4,500)

(3,000)

(1,500)

-

1,500

3,000

4,500

6,000

7,500

9,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

B

Demand: Non-OECD Changes Th

ou

san

d b

arre

ls p

er

day

Middle East

Source: IEA and Own Calculations

(6,000)

(4,500)

(3,000)

(1,500)

-

1,500

3,000

4,500

6,000

7,500

9,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

B

Demand: Non-OECD Changes Th

ou

san

d b

arre

ls p

er

day

Latin America

Source: IEA and Own Calculations

(6,000)

(4,500)

(3,000)

(1,500)

-

1,500

3,000

4,500

6,000

7,500

9,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

B

Demand: Non-OECD Changes Th

ou

san

d b

arre

ls p

er

day

Other Asia

Source: IEA and Own Calculations

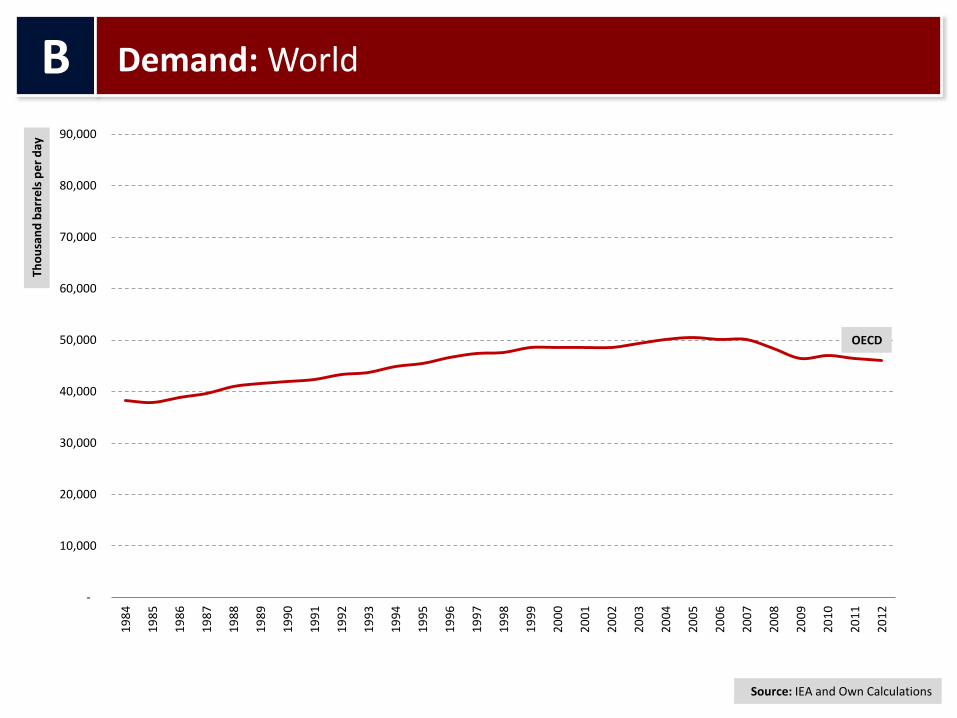

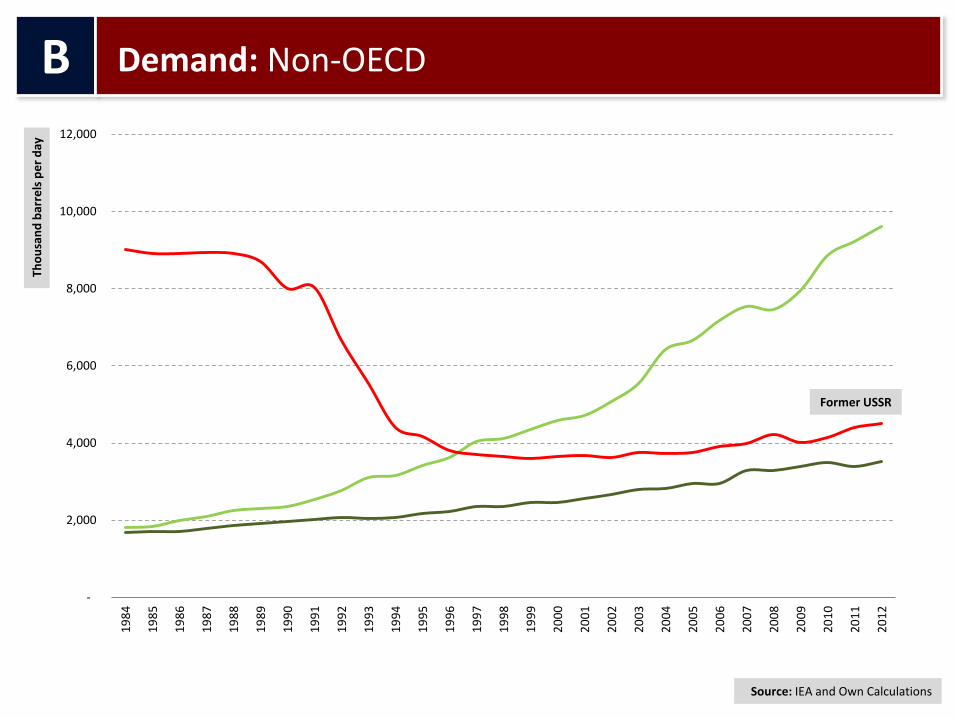

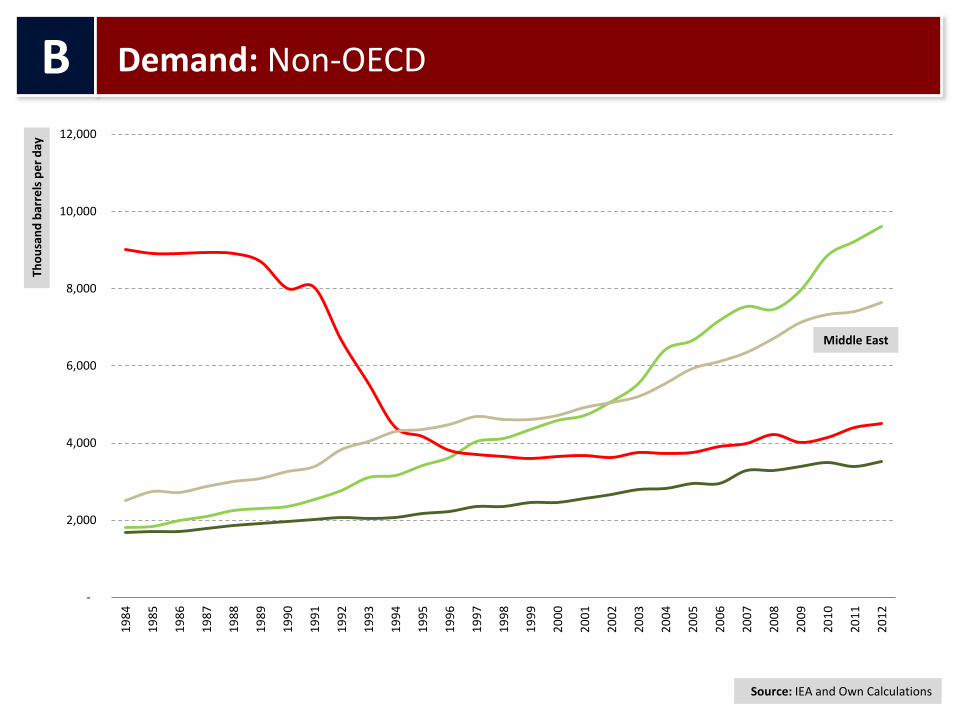

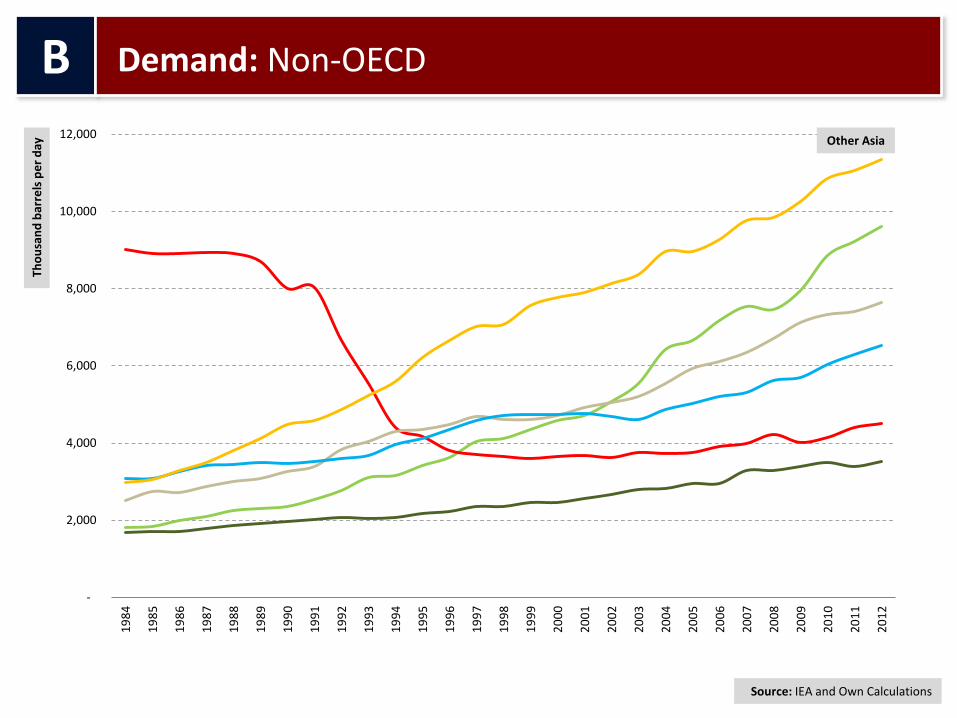

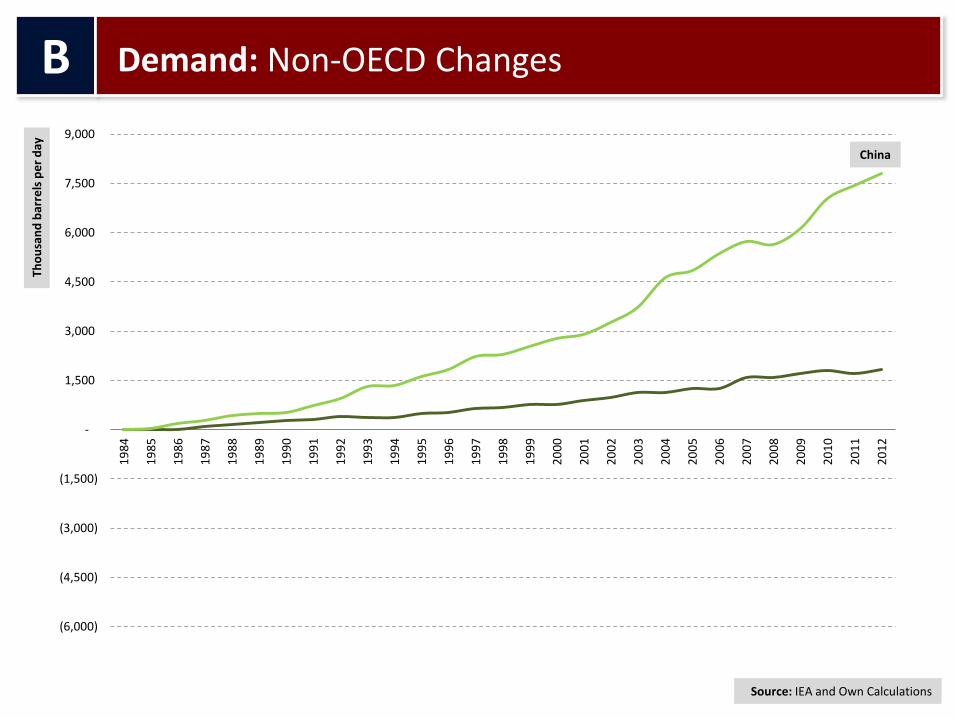

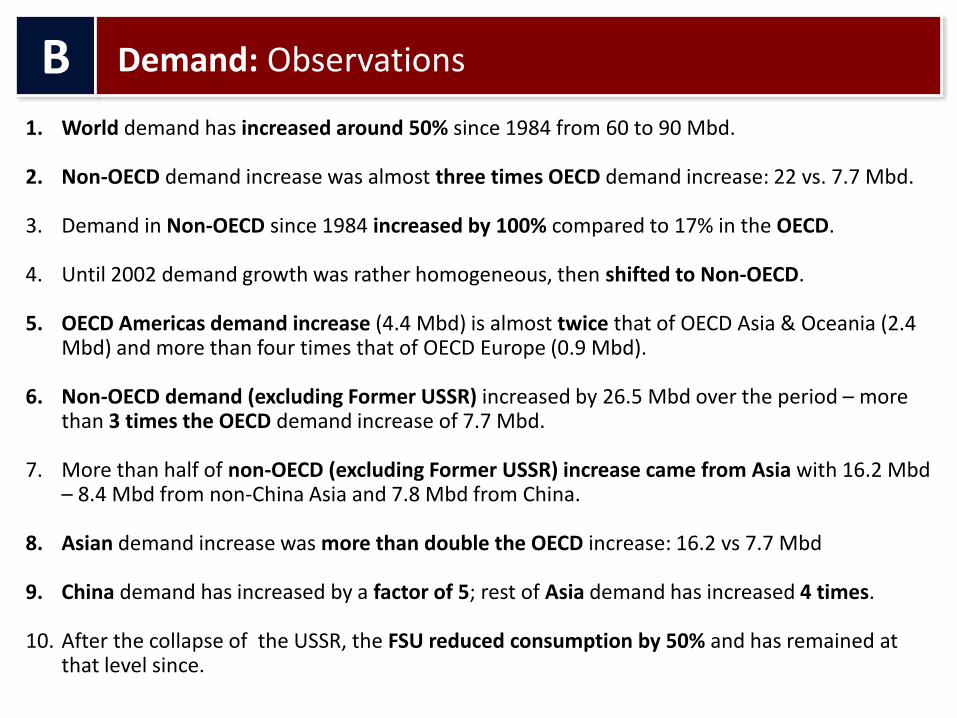

1. World demand has increased around 50% since 1984 from 60 to 90 Mbd. 2. Non-OECD demand increase was almost three times OECD demand increase: 22 vs. 7.7 Mbd.

3. Demand in Non-OECD since 1984 increased by 100% compared to 17% in the OECD.

4. Until 2002 demand growth was rather homogeneous, then shifted to Non-OECD.

5. OECD Americas demand increase (4.4 Mbd) is almost twice that of OECD Asia & Oceania (2.4

Mbd) and more than four times that of OECD Europe (0.9 Mbd).

6. Non-OECD demand (excluding Former USSR) increased by 26.5 Mbd over the period – more than 3 times the OECD demand increase of 7.7 Mbd.

7. More than half of non-OECD (excluding Former USSR) increase came from Asia with 16.2 Mbd – 8.4 Mbd from non-China Asia and 7.8 Mbd from China.

8. Asian demand increase was more than double the OECD increase: 16.2 vs 7.7 Mbd

9. China demand has increased by a factor of 5; rest of Asia demand has increased 4 times.

10. After the collapse of the USSR, the FSU reduced consumption by 50% and has remained at that level since.

B

Demand: Observations

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: World Th

ou

san

d b

arre

ls p

er

day

OECD

Source: IEA and Own Calculations

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: World Th

ou

san

d b

arre

ls p

er

day

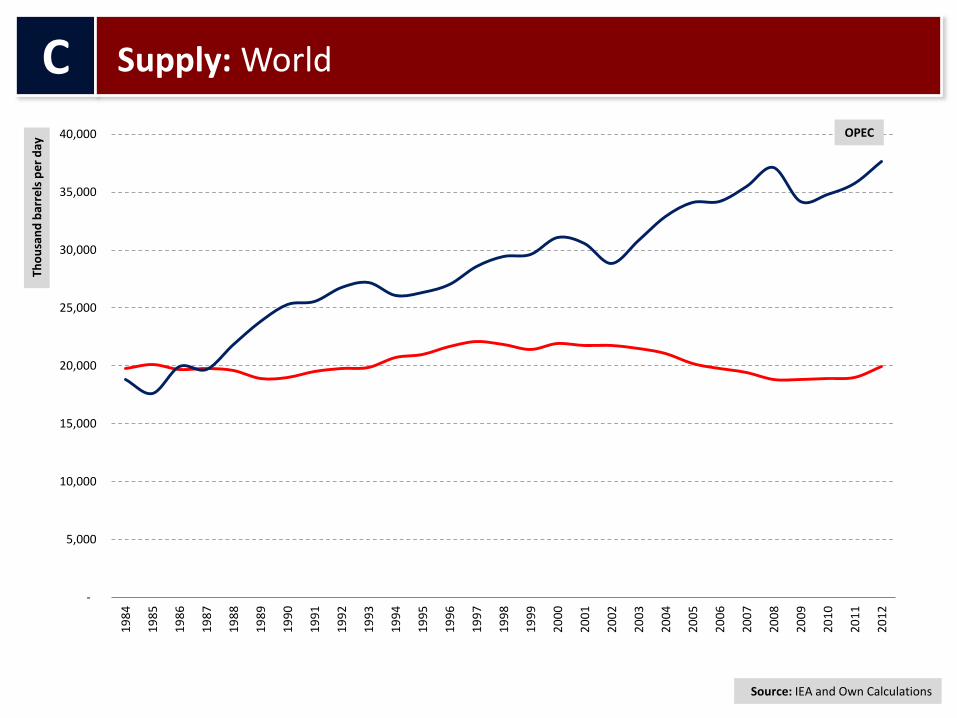

OPEC

Source: IEA and Own Calculations

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: World Th

ou

san

d b

arre

ls p

er

day

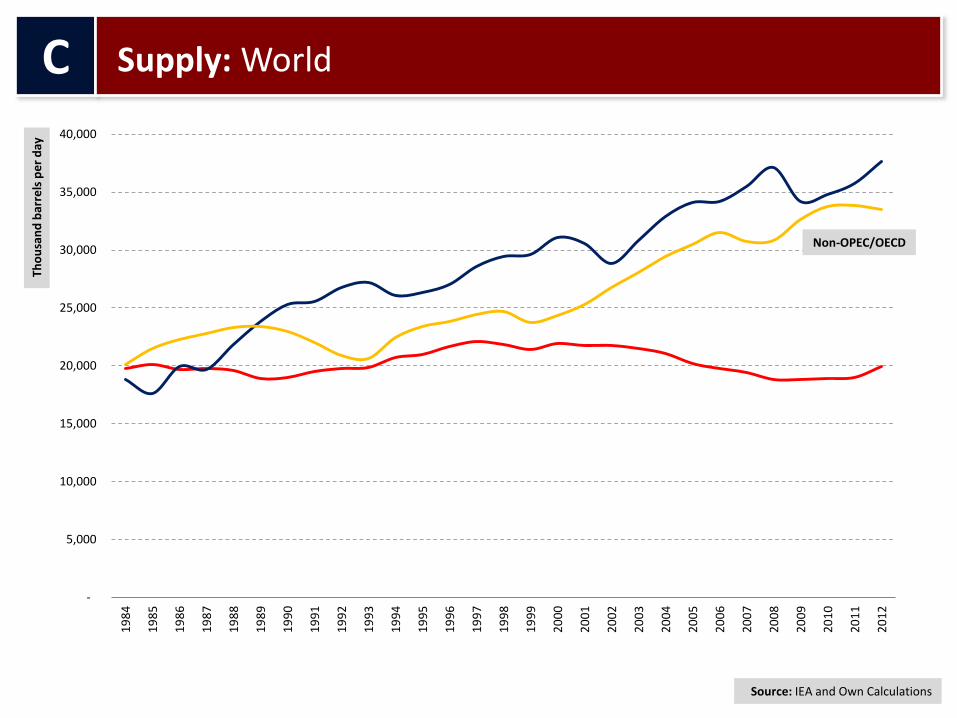

Non-OPEC/OECD

Source: IEA and Own Calculations

(2,500)

-

2,500

5,000

7,500

10,000

12,500

15,000

17,500

20,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

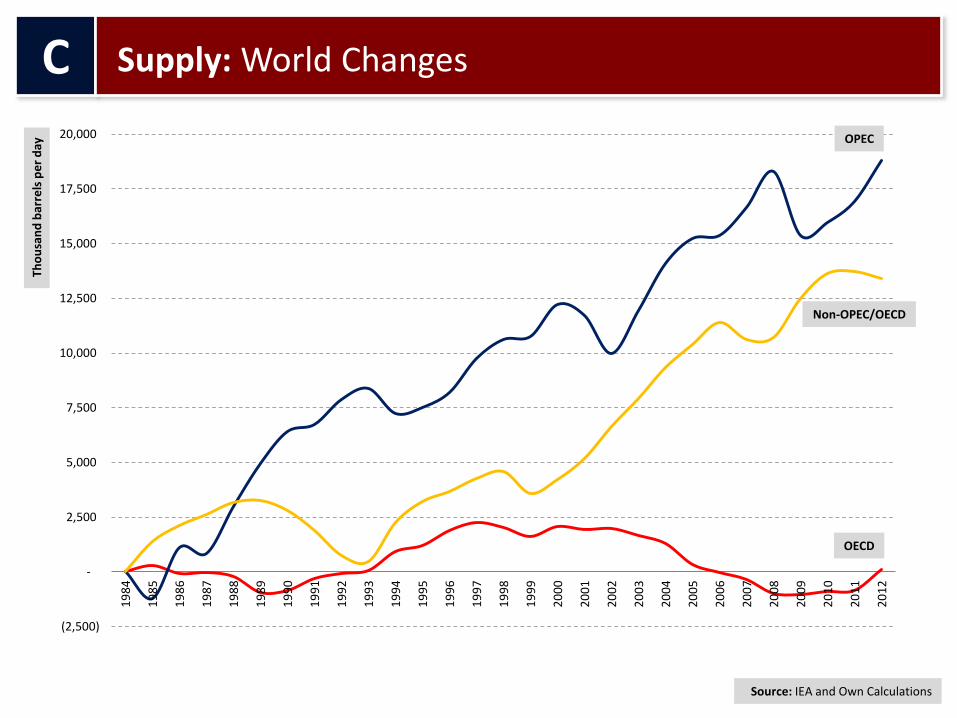

Supply: World Changes Th

ou

san

d b

arre

ls p

er

day

OECD

Source: IEA and Own Calculations

(2,500)

-

2,500

5,000

7,500

10,000

12,500

15,000

17,500

20,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: World Changes Th

ou

san

d b

arre

ls p

er

day

OPEC

OECD

Source: IEA and Own Calculations

(2,500)

-

2,500

5,000

7,500

10,000

12,500

15,000

17,500

20,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: World Changes Th

ou

san

d b

arre

ls p

er

day

OPEC

Non-OPEC/OECD

OECD

Source: IEA and Own Calculations

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

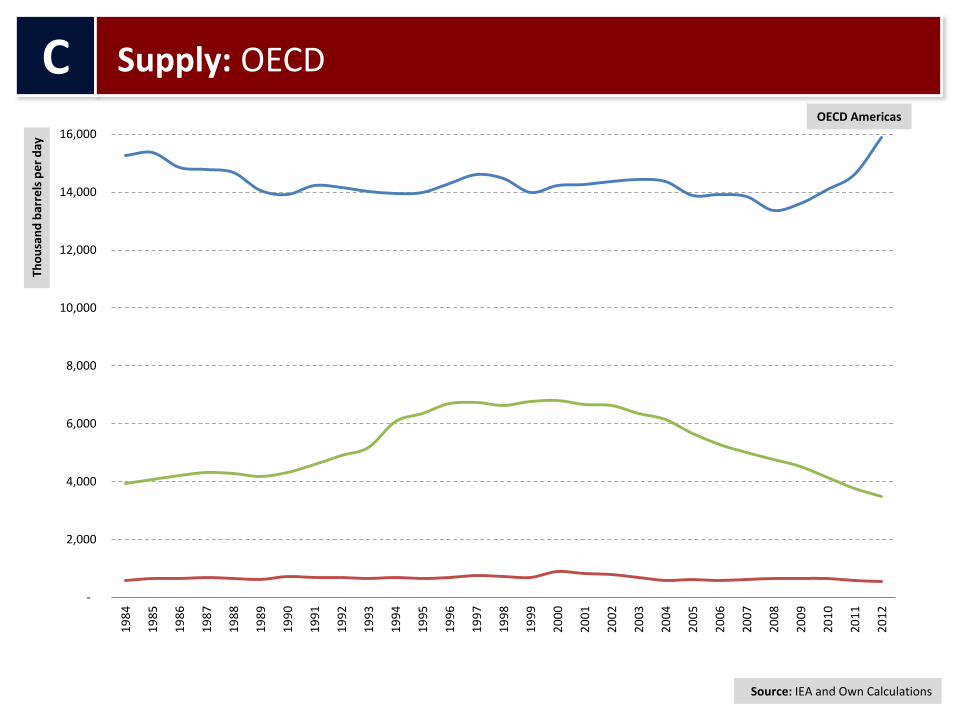

C

Supply: OECD

Tho

usa

nd

bar

rels

pe

r d

ay

OECD Asia & Oceania

Source: IEA and Own Calculations

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: OECD

Tho

usa

nd

bar

rels

pe

r d

ay

OECD Europe

Source: IEA and Own Calculations

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: OECD

Tho

usa

nd

bar

rels

pe

r d

ay

OECD Americas

Source: IEA and Own Calculations

(2,000)

(1,500)

(1,000)

(500)

-

500

1,000

1,500

2,000

2,500

3,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

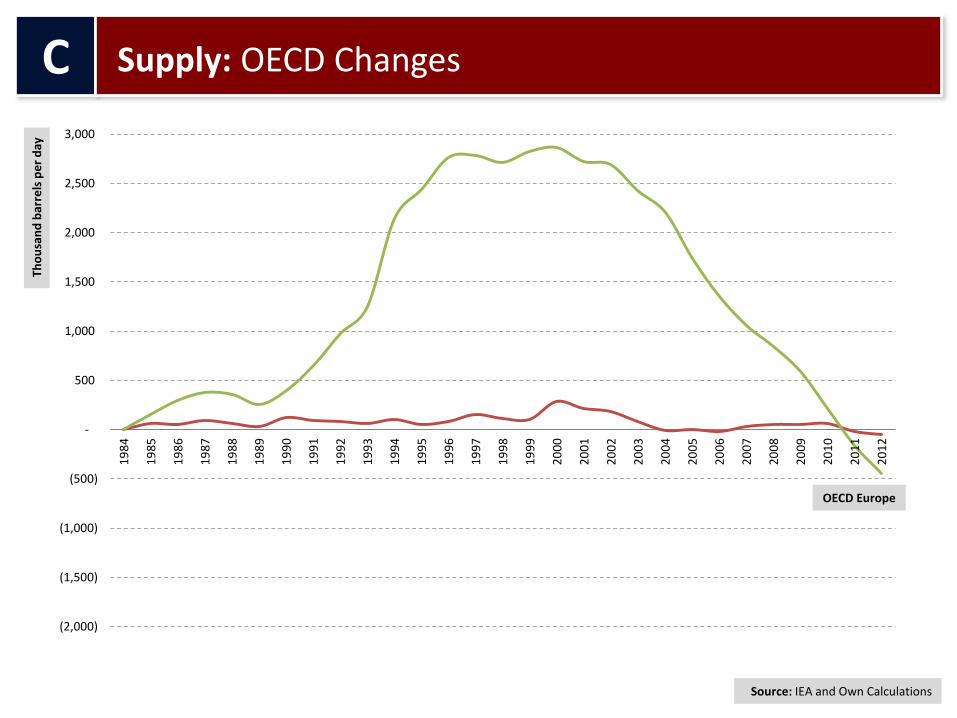

Supply: OECD Changes Th

ou

san

d b

arre

ls p

er

day

OECD Asia & Oceania

Source: IEA and Own Calculations

(2,000)

(1,500)

(1,000)

(500)

-

500

1,000

1,500

2,000

2,500

3,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: OECD Changes Th

ou

san

d b

arre

ls p

er

day

OECD Europe

Source: IEA and Own Calculations

(2,000)

(1,500)

(1,000)

(500)

-

500

1,000

1,500

2,000

2,500

3,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: OECD Changes Th

ou

san

d b

arre

ls p

er

day

OECD Americas

Source: IEA and Own Calculations

-

2,500

5,000

7,500

10,000

12,500

15,000

17,500

20,000

22,500

25,000

27,5001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: OPEC Th

ou

san

d b

arre

ls p

er

day

OPEC Latin America

Source: IEA and Own Calculations

-

2,500

5,000

7,500

10,000

12,500

15,000

17,500

20,000

22,500

25,000

27,5001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: OPEC Th

ou

san

d b

arre

ls p

er

day

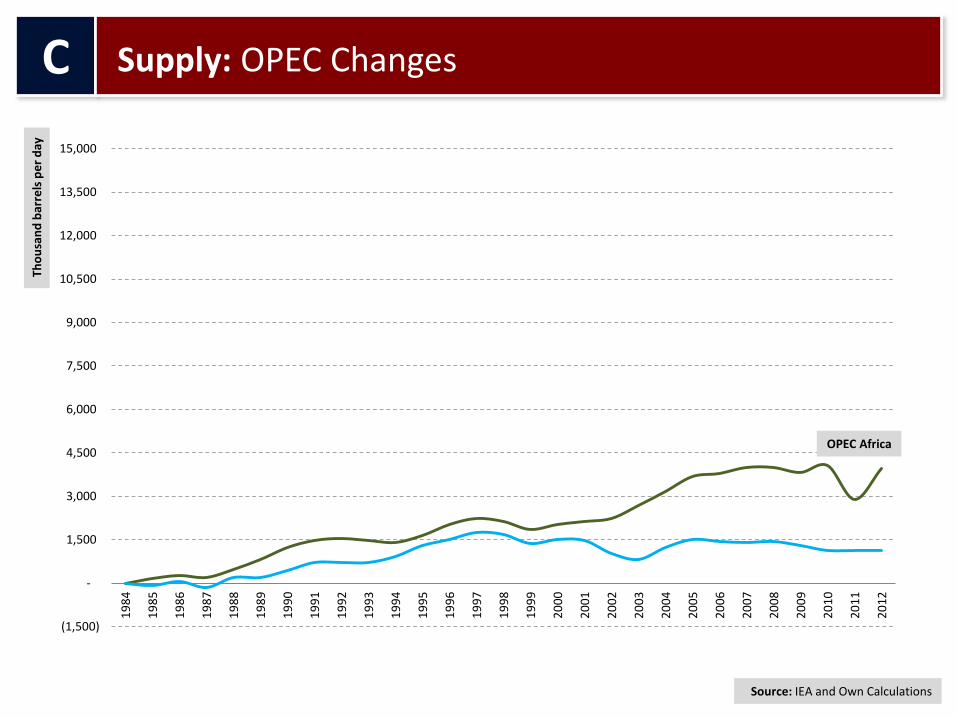

OPEC Africa

Source: IEA and Own Calculations

-

2,500

5,000

7,500

10,000

12,500

15,000

17,500

20,000

22,500

25,000

27,5001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: OPEC Th

ou

san

d b

arre

ls p

er

day

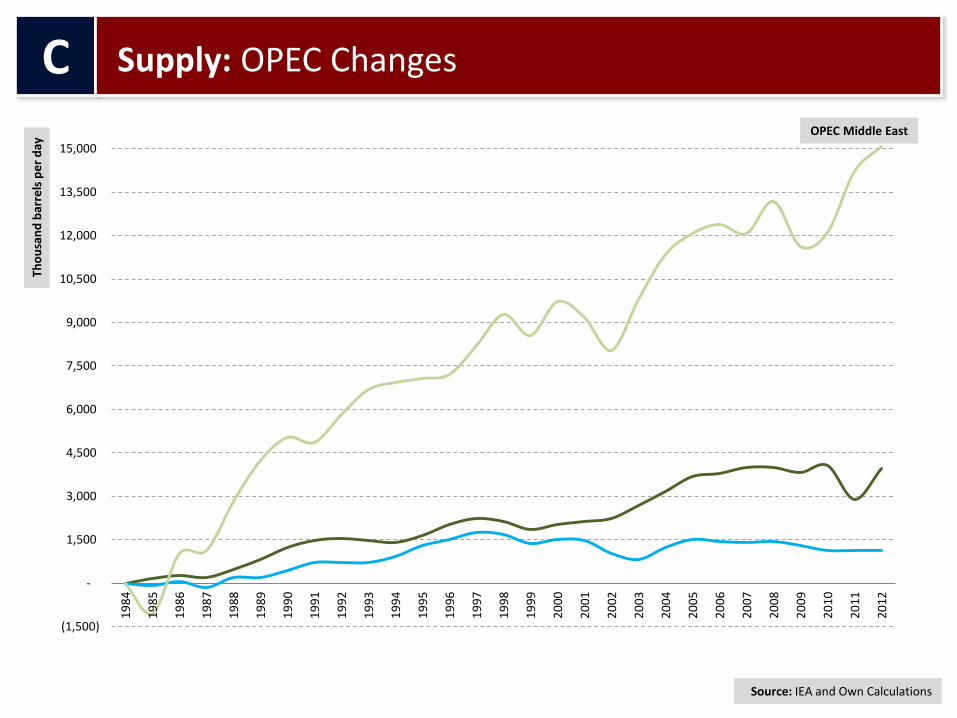

OPEC Middle East

Source: IEA and Own Calculations

(1,500)

-

1,500

3,000

4,500

6,000

7,500

9,000

10,500

12,000

13,500

15,000

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: OPEC Changes Th

ou

san

d b

arre

ls p

er

day

OPEC Latin America

Source: IEA and Own Calculations

(1,500)

-

1,500

3,000

4,500

6,000

7,500

9,000

10,500

12,000

13,500

15,000

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: OPEC Changes Th

ou

san

d b

arre

ls p

er

day

OPEC Africa

Source: IEA and Own Calculations

(1,500)

-

1,500

3,000

4,500

6,000

7,500

9,000

10,500

12,000

13,500

15,000

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: OPEC Changes Th

ou

san

d b

arre

ls p

er

day

OPEC Middle East

Source: IEA and Own Calculations

-

2,000

4,000

6,000

8,000

10,000

12,000

14,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: Non-OPEC/OECD Th

ou

san

d b

arre

ls p

er

day

Non-OECD Europe

Source: IEA and Own Calculations

-

2,000

4,000

6,000

8,000

10,000

12,000

14,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: Non-OPEC/OECD Th

ou

san

d b

arre

ls p

er

day

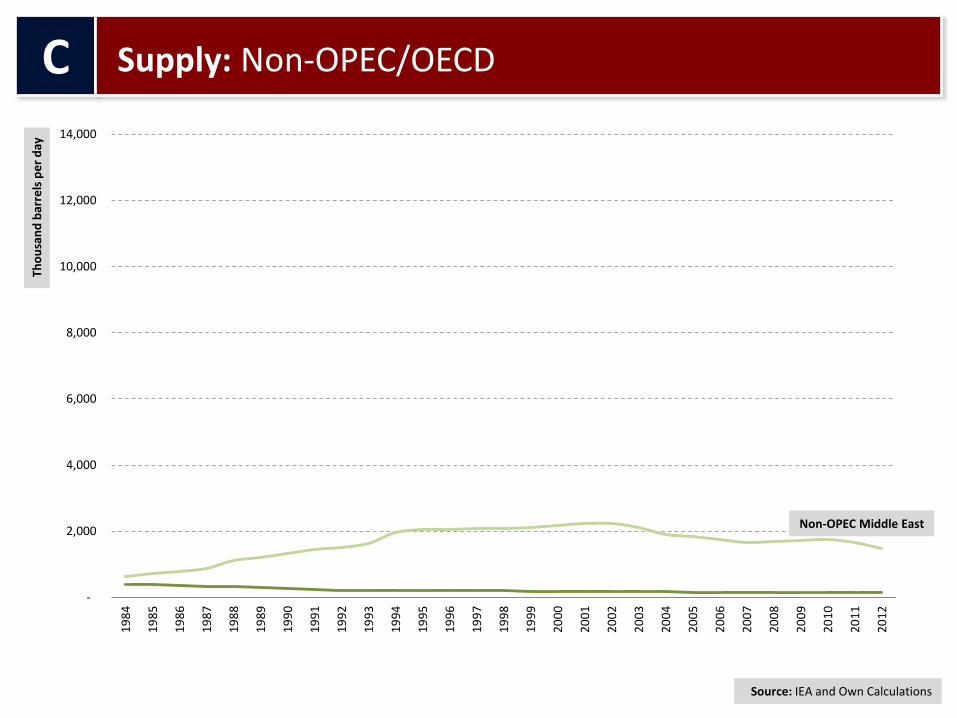

Non-OPEC Middle East

Source: IEA and Own Calculations

-

2,000

4,000

6,000

8,000

10,000

12,000

14,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: Non-OPEC/OECD Th

ou

san

d b

arre

ls p

er

day

Non-OPEC Africa

Source: IEA and Own Calculations

-

2,000

4,000

6,000

8,000

10,000

12,000

14,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: Non-OPEC/OECD Th

ou

san

d b

arre

ls p

er

day

Non-OPEC Latin America

Source: IEA and Own Calculations

-

2,000

4,000

6,000

8,000

10,000

12,000

14,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: Non-OPEC/OECD Th

ou

san

d b

arre

ls p

er

day

Non-OPEC Asia

Source: IEA and Own Calculations

-

2,000

4,000

6,000

8,000

10,000

12,000

14,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: Non-OPEC/OECD Th

ou

san

d b

arre

ls p

er

day

Former USSR

Source: IEA and Own Calculations

(5,000)

(4,000)

(3,000)

(2,000)

(1,000)

-

1,000

2,000

3,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: Non-OPEC/OECD Changes Th

ou

san

d b

arre

ls p

er

day

Non-OECD Europe

Source: IEA and Own Calculations

(5,000)

(4,000)

(3,000)

(2,000)

(1,000)

-

1,000

2,000

3,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: Non-OPEC/OECD Changes Th

ou

san

d b

arre

ls p

er

day

Non-OPEC Middle East

Source: IEA and Own Calculations

(5,000)

(4,000)

(3,000)

(2,000)

(1,000)

-

1,000

2,000

3,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: Non-OPEC/OECD Changes Th

ou

san

d b

arre

ls p

er

day

Non-OPEC Africa

Source: IEA and Own Calculations

(5,000)

(4,000)

(3,000)

(2,000)

(1,000)

-

1,000

2,000

3,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: Non-OPEC/OECD Changes Th

ou

san

d b

arre

ls p

er

day

Former USSR

Source: IEA and Own Calculations

(5,000)

(4,000)

(3,000)

(2,000)

(1,000)

-

1,000

2,000

3,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: Non-OPEC/OECD Changes Th

ou

san

d b

arre

ls p

er

day

Non-OPEC Latin America

Source: IEA and Own Calculations

(5,000)

(4,000)

(3,000)

(2,000)

(1,000)

-

1,000

2,000

3,0001

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

C

Supply: Non-OPEC/OECD Changes Th

ou

san

d b

arre

ls p

er

day

Non-OPEC Asia

Source: IEA and Own Calculations

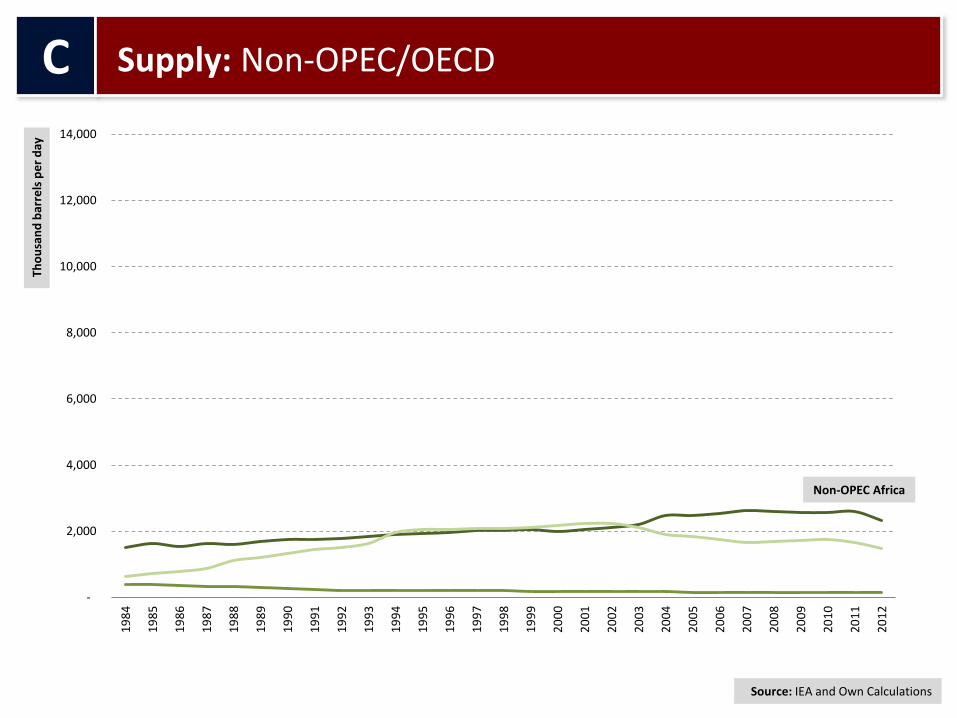

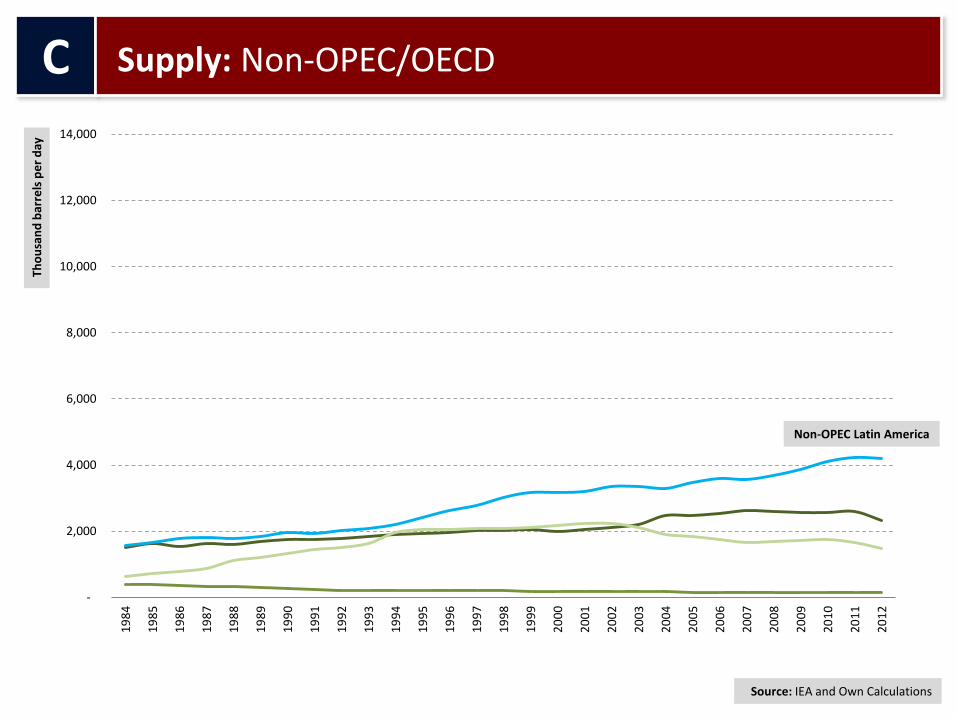

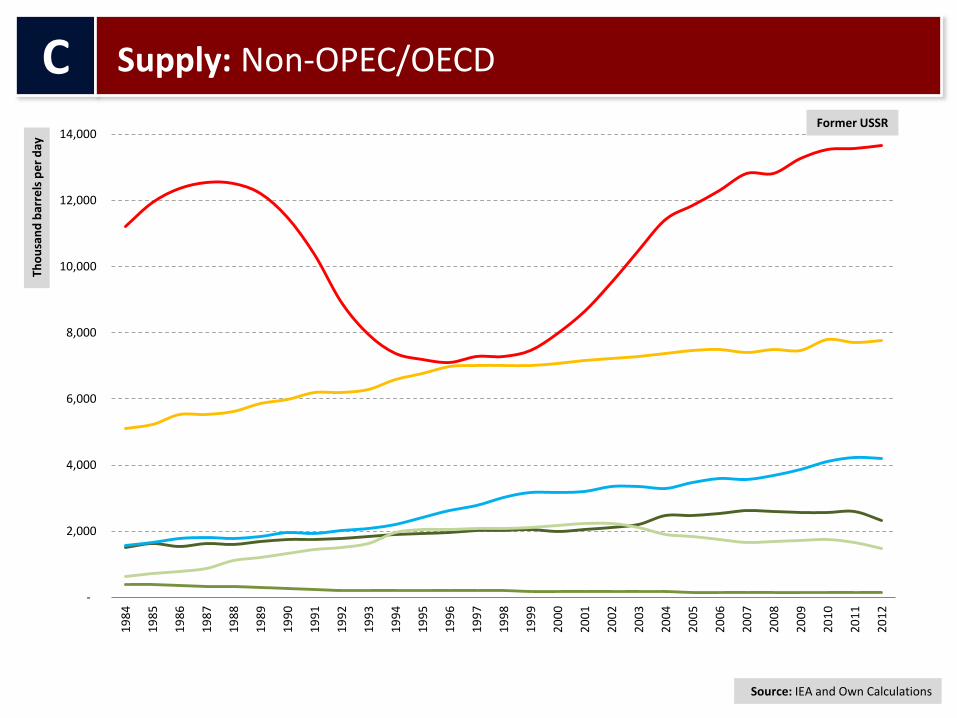

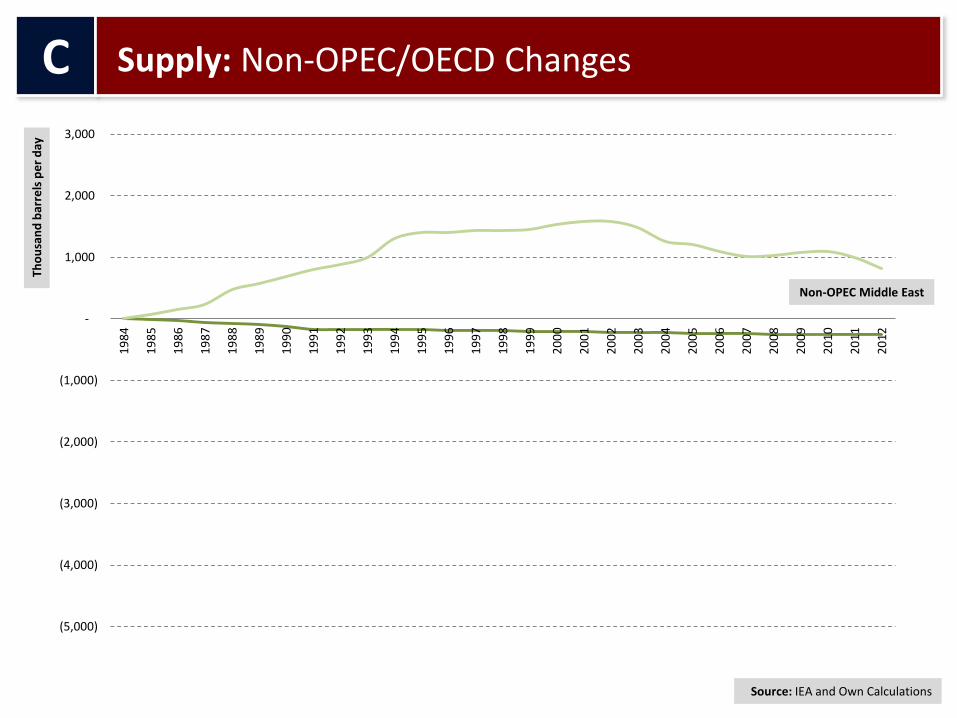

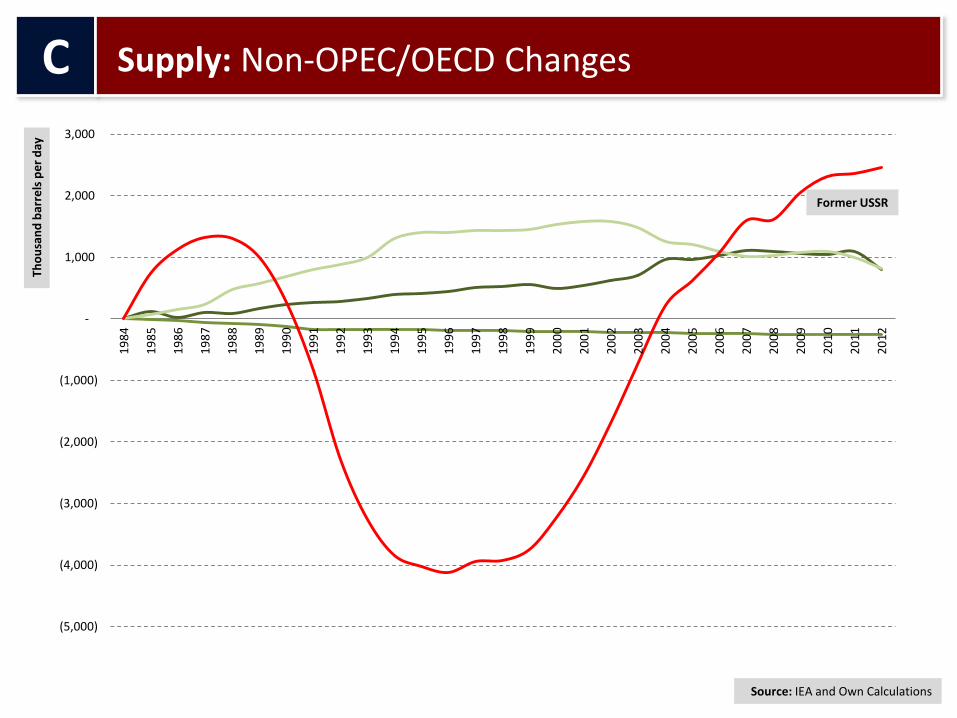

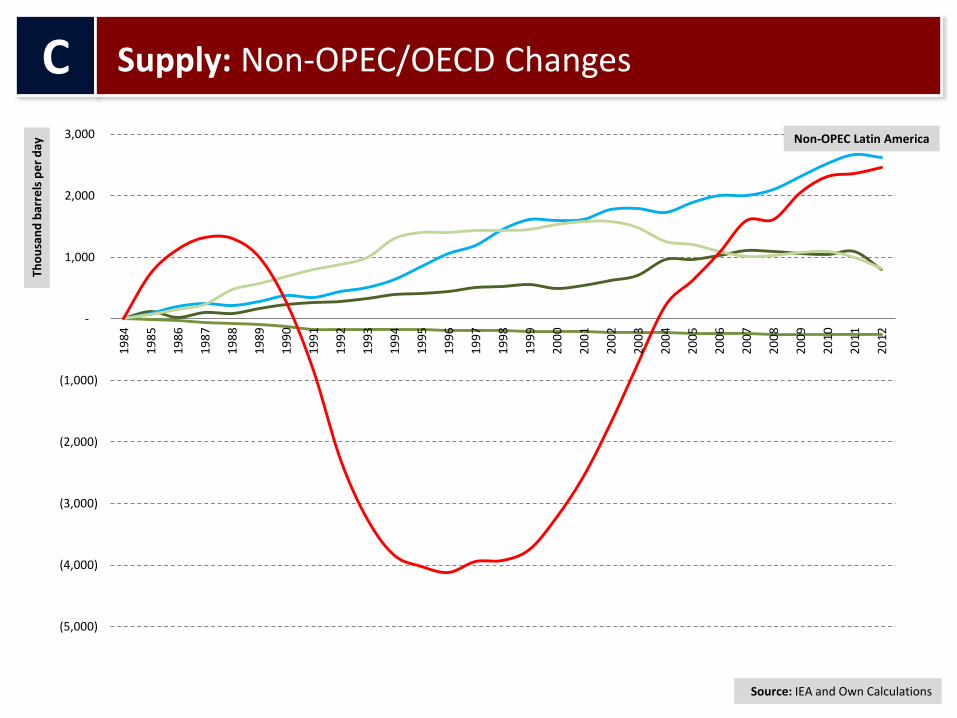

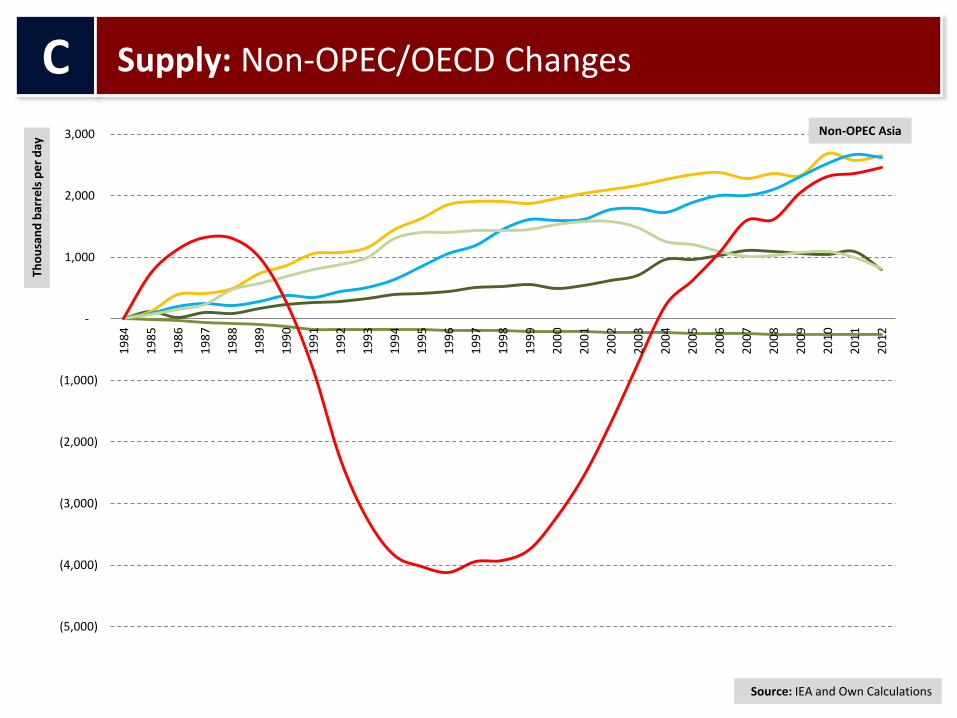

1. Non-OPEC/OECD supply increase has more than compensated the decline in OEDC supply.

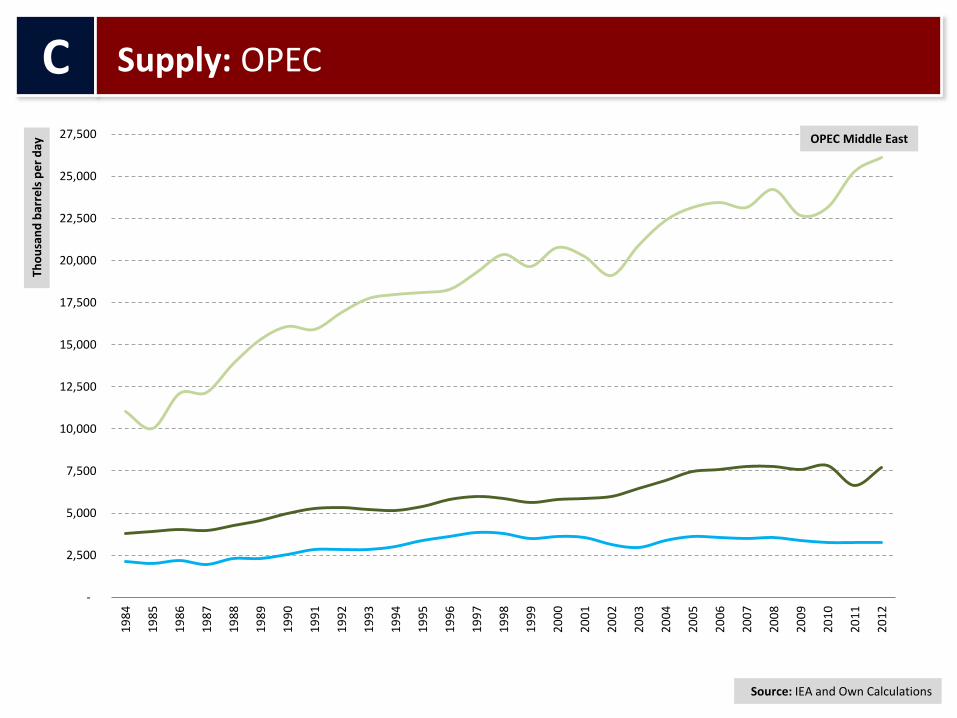

2. The bulk of the net supply increase has come from OPEC production out of spare capacity since 1985. It increased twofold from 18 to 38 Mbd.

3. OECD essentially flat behavior has coincided with oil price increase since 2002.

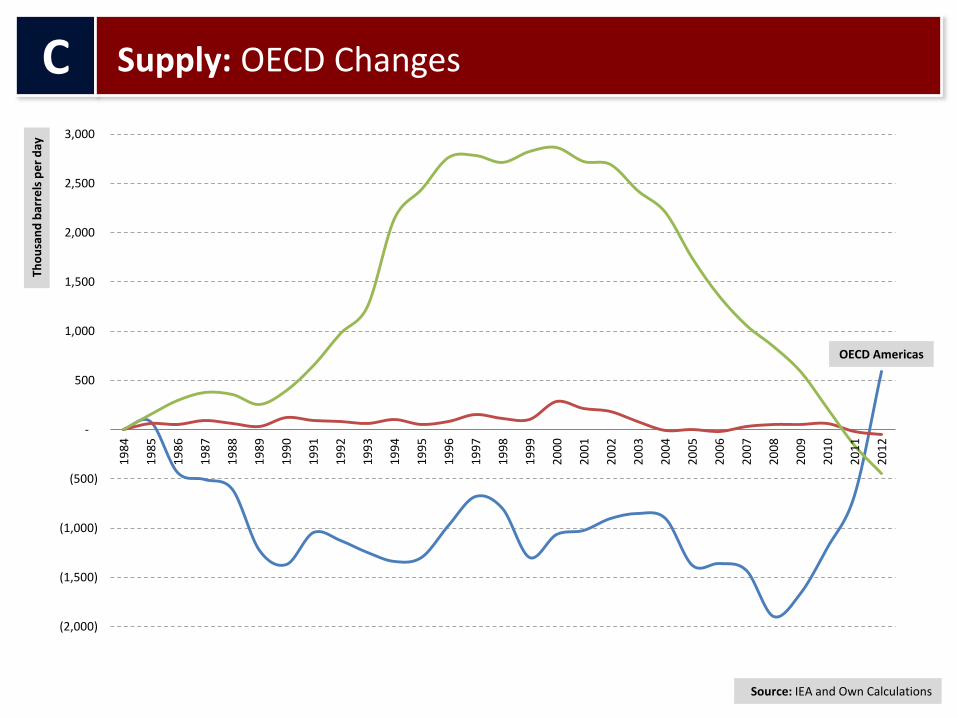

4. OECD Americas has recovered slightly from its decline in production since 1985; OECD Europe peaked in production and has been declining since 2000 and is below 1985 level.

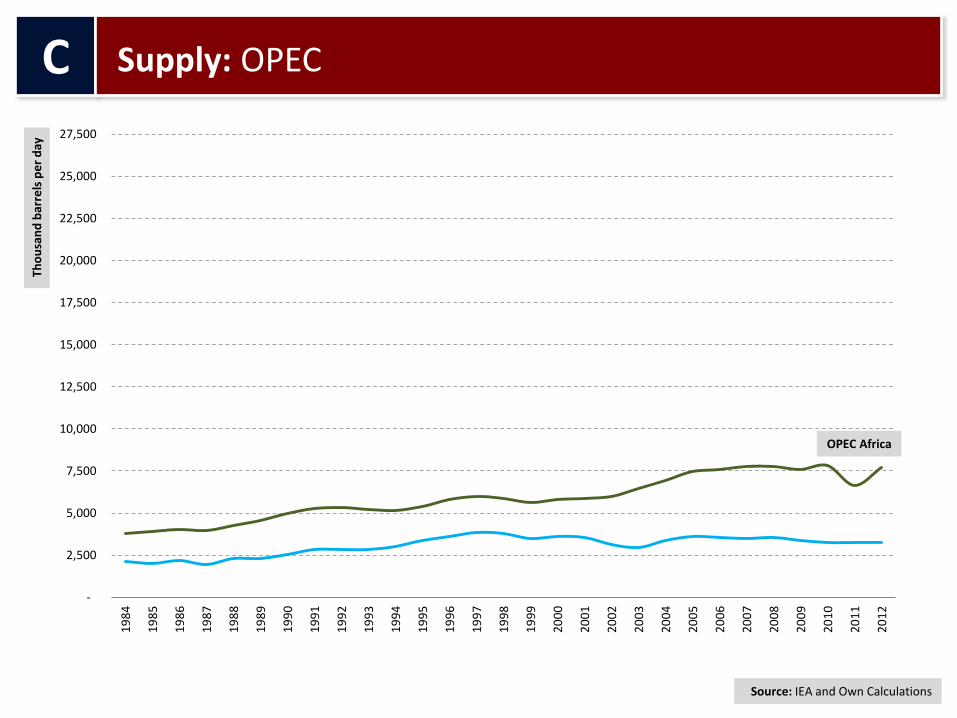

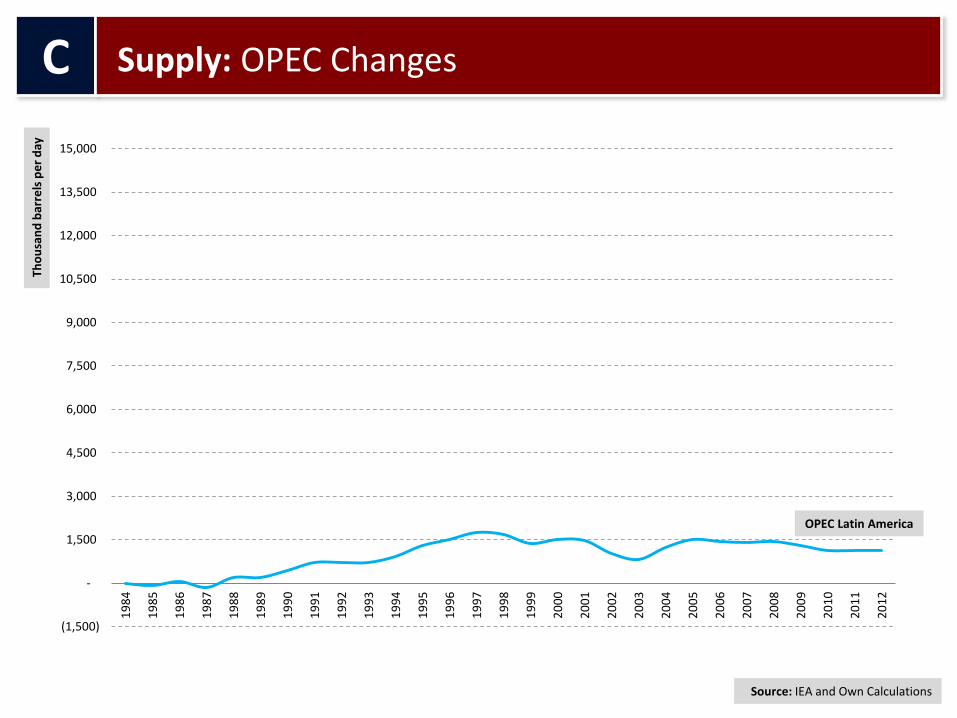

5. OPEC Latin America is slightly above 1985; OPEC Africa increased almost twofold; OPEC Middle East increase more than doubles the rest of OPEC.

6. The FSU is back to where it was in 1985 with export capacity around 9 Mbd.

7. Latin America is the Non OPEC/OECD region with the fastest and largest growth.

C

Supply: Observations

2 A New Energy Paradigm

Price Scenarios

New Sources of Crude

A

B

D

C

Changes in Demand

New Oil Balances

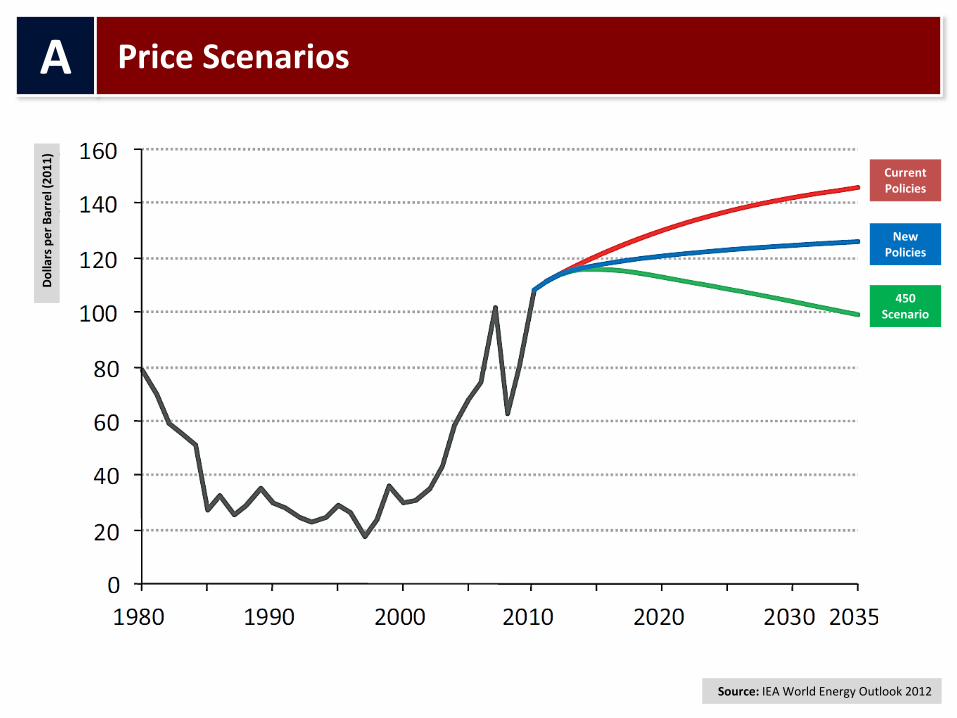

A Price Scenarios

Source: IEA World Energy Outlook 2012

Current Policies

New Policies

450 Scenario

Do

llars

pe

r B

arre

l (2

01

1)

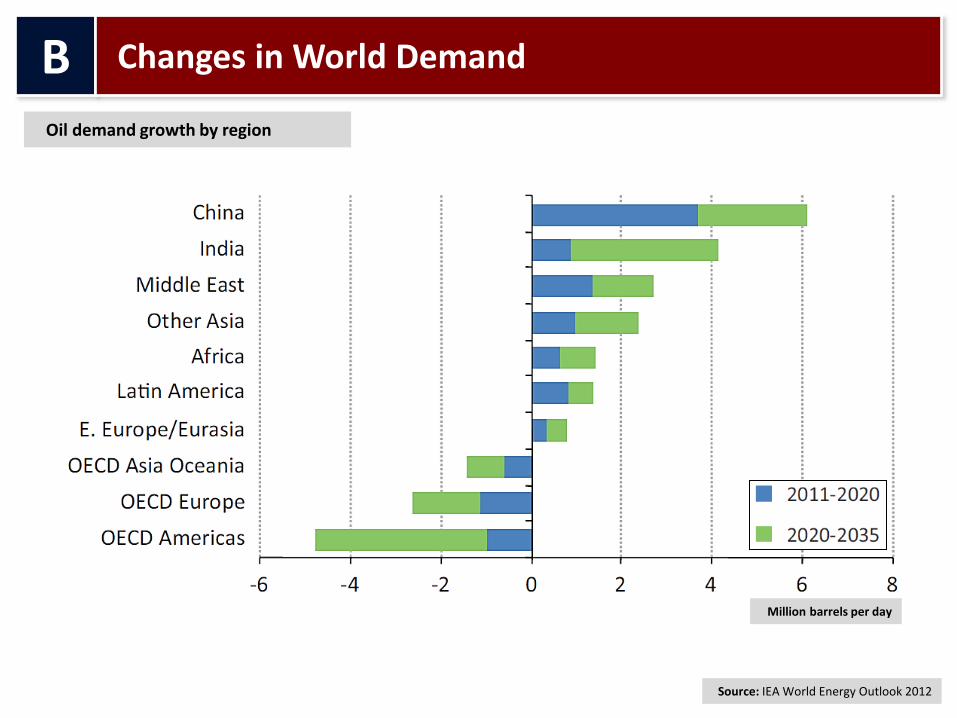

B Changes in World Demand M

illio

n b

arre

ls p

er

day

Source: IEA World Energy Outlook 2012

Do

llars

pe

r b

arre

l (2

01

1)

Current Policies

New Policies

450 Scenario

Source: IEA World Energy Outlook 2012

B Changes in World Demand

Oil demand growth by region

Million barrels per day

Source: IEA World Energy Outlook 2012

B Changes in Demand B

illio

n t

on

ne

-Km

Incremental road freight growth by region since 2000

Source: IEA World Energy Outlook 2012

C New Sources of Crude

World oil supply by type

Mill

ion

bar

rels

pe

r d

ay

Processing Gains Light tight oil Other unconventional oil

NGLs Fields yet-to-be found Fields yet-to-be developed Currently producing

Source: IEA World Energy Outlook 2012

C New Sources of Crude

US oil production by type

Mill

ion

bar

rels

pe

r d

ay

Light tight oil Other unconventional oil

Fields yet-to-be found Fields yet-to-be developed Currently producing

NGLs

0

2

4

6

8

10

12

14

China European Union India United States Japan

2005 2011 2020 2035

Source: IEA World Energy Outlook 2012

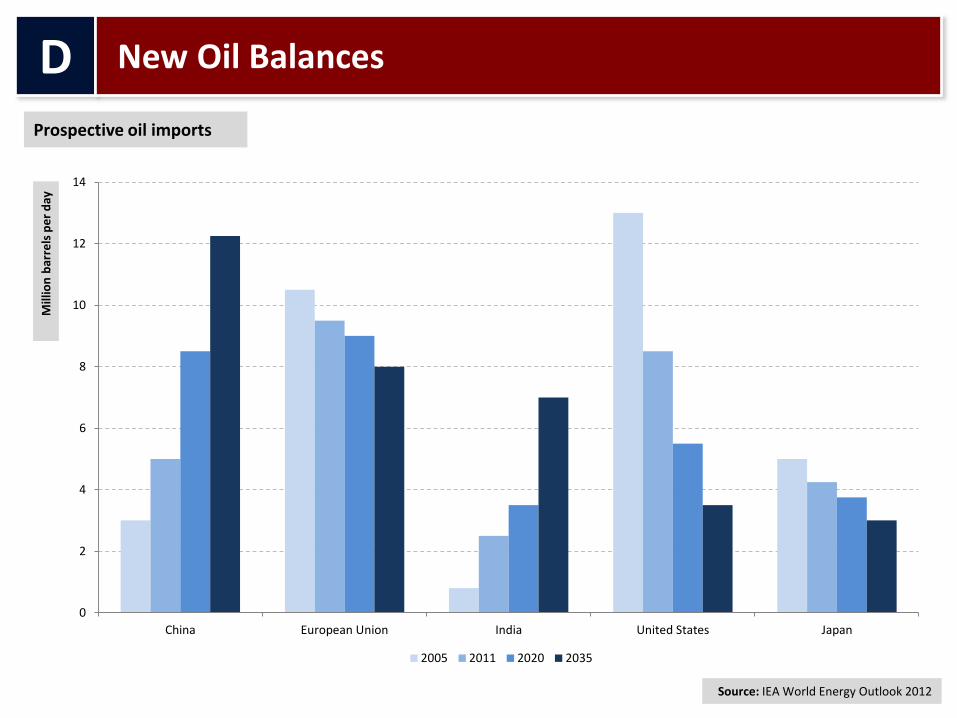

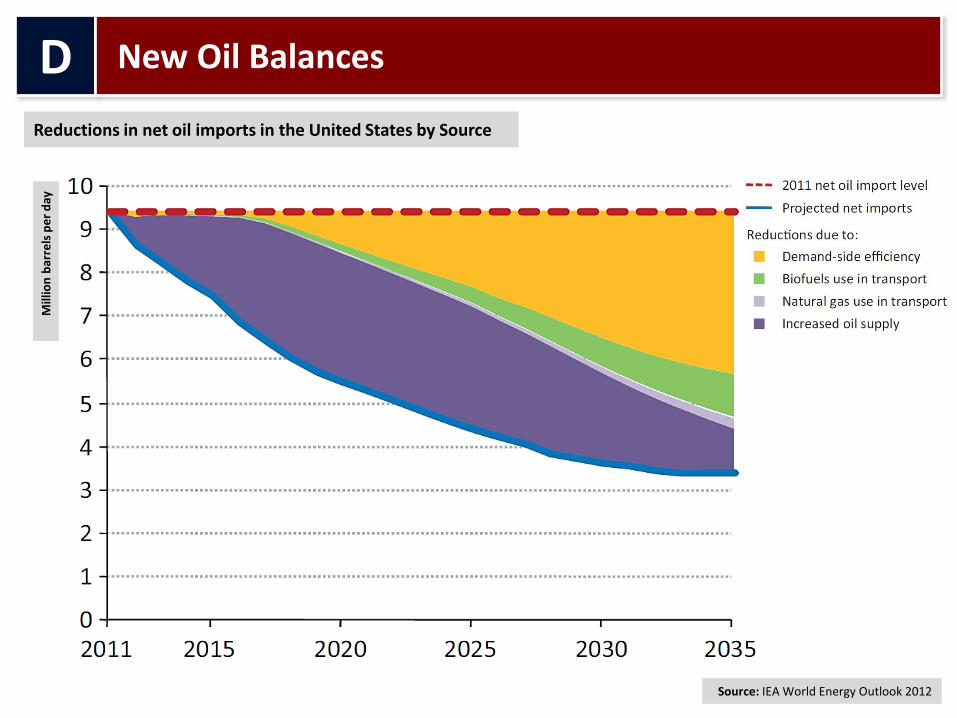

D New Oil Balances

Prospective oil imports

Mill

ion

bar

rels

pe

r d

ay

D New Oil Balances

Reductions in net oil imports in the United States by Source

Source: IEA World Energy Outlook 2012

Mill

ion

bar

rels

pe

r d

ay

3

Oil Sector Performance & Institutional Frameworks

Price Dynamics

Contracting for Oil Production

A

B

D

C

Response to Price Signals

Institutional Features & Consequences

Response process to price signals:

Price Investment Supply

3

Oil Sector Performance & Institutional Frameworks

Response process to price signals:

Price Investment

Active Drilling Rigs

3

Oil Sector Performance & Institutional Frameworks

050

100

150

$/b

bl

1995m1 2000m1 2005m1 2010m1Period

Data Source: IEA, U.S. BLS and own calculations

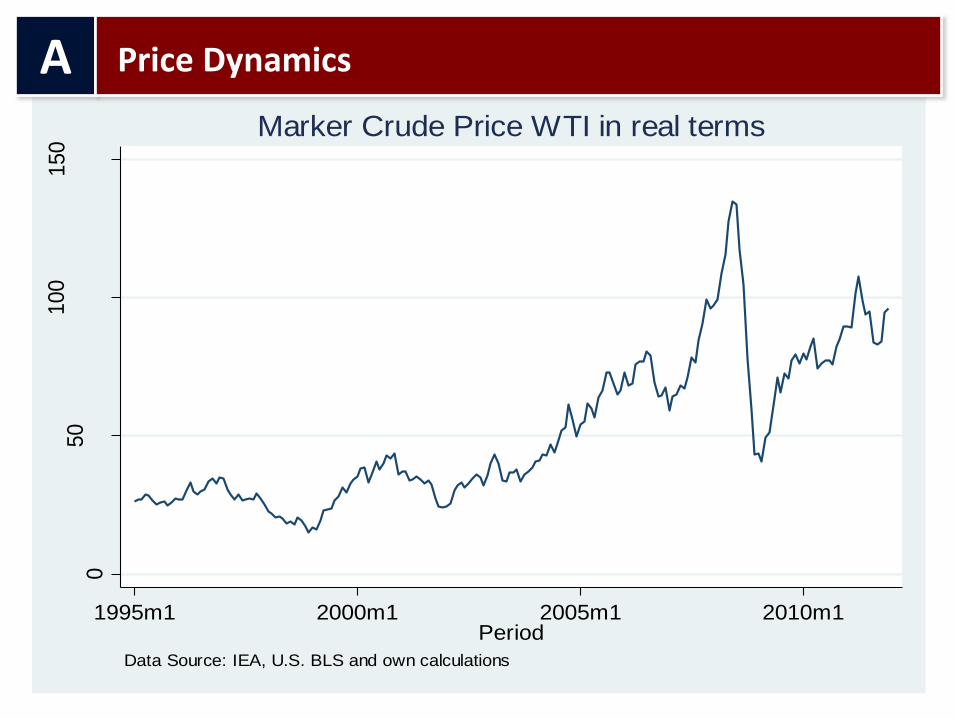

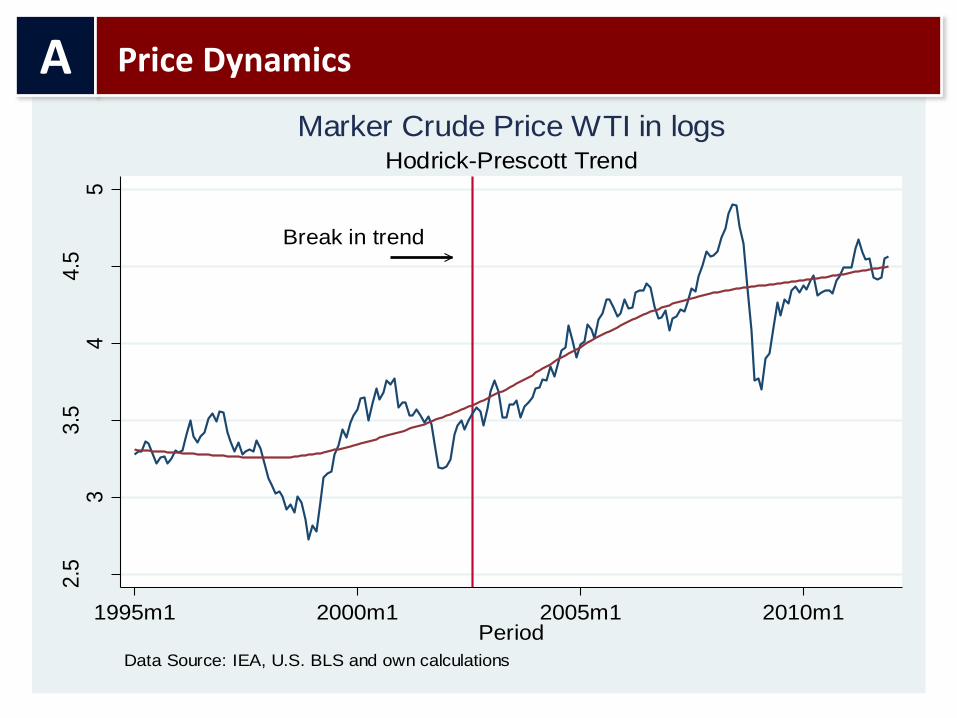

Marker Crude Price WTI in real terms

A

Price Dynamics

Break in trend

2.5

33.5

44.5

5

WT

I in

logs

1995m1 2000m1 2005m1 2010m1Period

Data Source: IEA, U.S. BLS and own calculations

Hodrick-Prescott Trend

Marker Crude Price WTI in logs

A

Price Dynamics

Based on experiences of the last 15 years, we can sort the Latin American oil producers into 2 groups, depending on their responses to price signals:

Group 1 Group 2

Argentina Ecuador Mexico

Venezuela

Brazil Colombia

Peru

B

Response to Price Signals

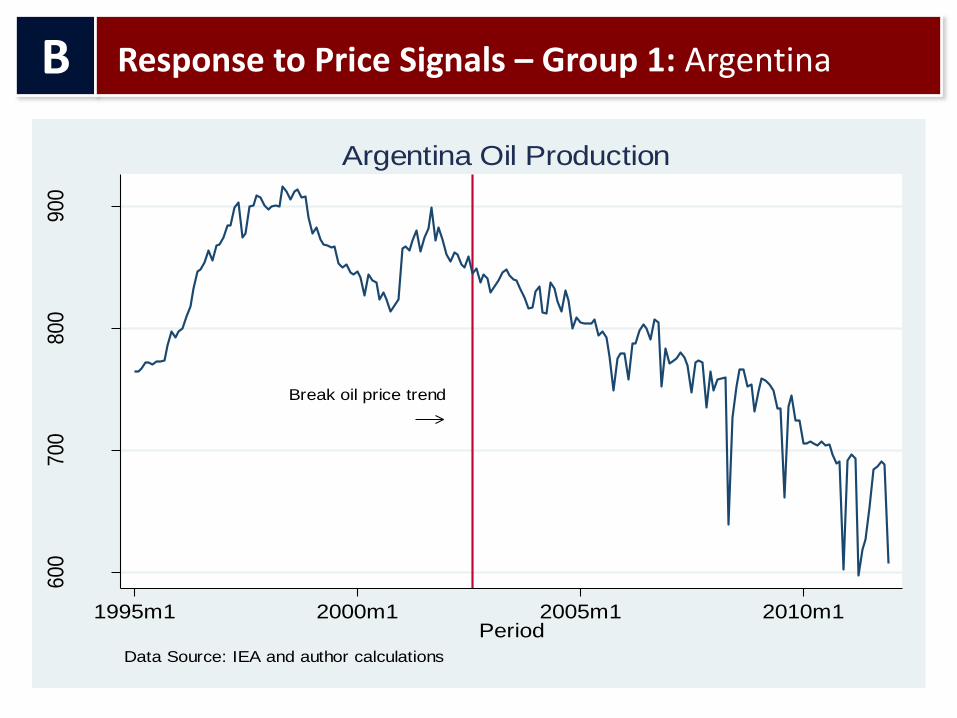

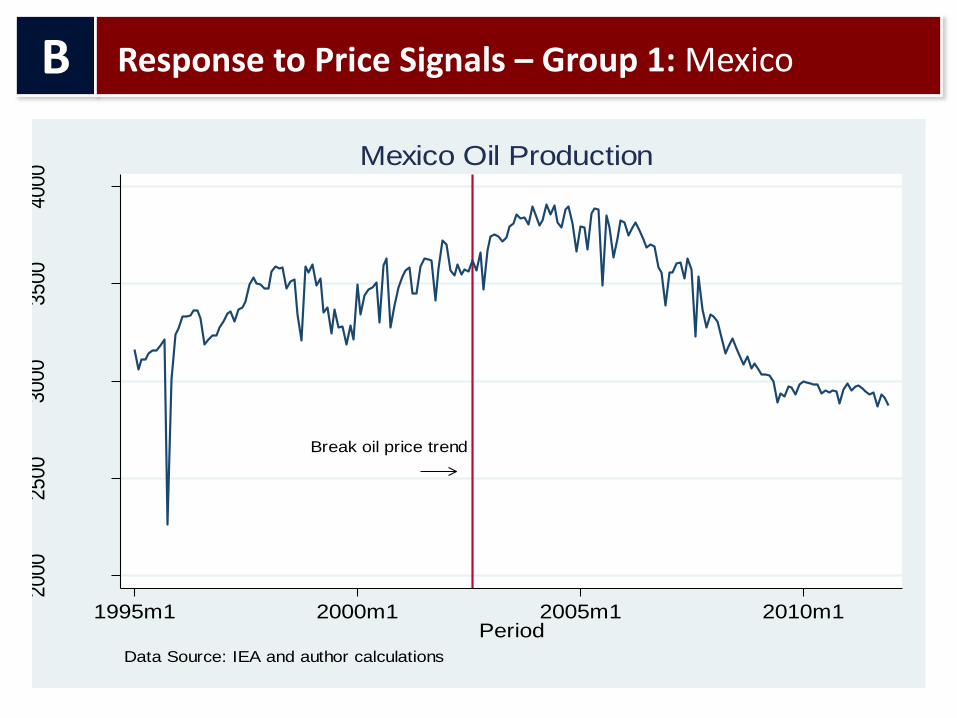

Despite oil price increases, oil production has fallen in:

Group 1

Argentina Ecuador Mexico

Venezuela

B

Response to Price Signals: Supply

Break oil price trend

600

700

800

900

supply

(th

b/d

)

1995m1 2000m1 2005m1 2010m1Period

Data Source: IEA and author calculations

Argentina Oil Production

B

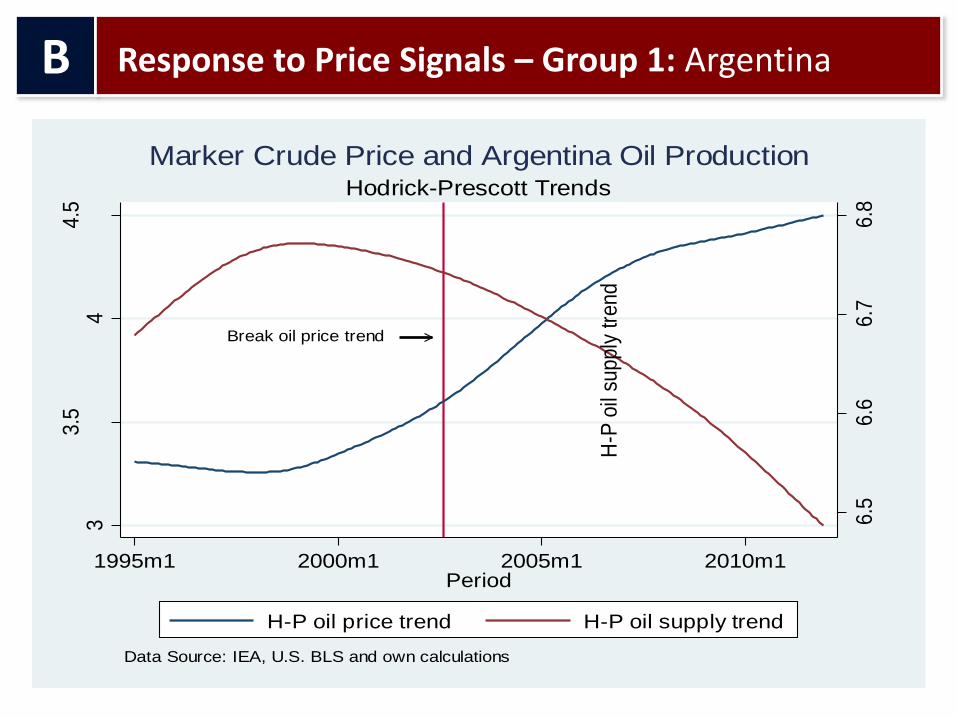

Response to Price Signals – Group 1: Argentina

Break oil price trend

6.5

6.6

6.7

6.8

H-P

oil

supply

tre

nd

33.5

44.5

H-P

oil

pri

ce tre

nd

1995m1 2000m1 2005m1 2010m1Period

H-P oil price trend H-P oil supply trend

Data Source: IEA, U.S. BLS and own calculations

Hodrick-Prescott Trends

Marker Crude Price and Argentina Oil Production

B

Response to Price Signals – Group 1: Argentina

Break oil price trend

300

350

400

450

500

550

supply

(th

b/d

)

1995m1 2000m1 2005m1 2010m1Period

Data Source: IEA and author calculations

Ecuador Oil Production

B

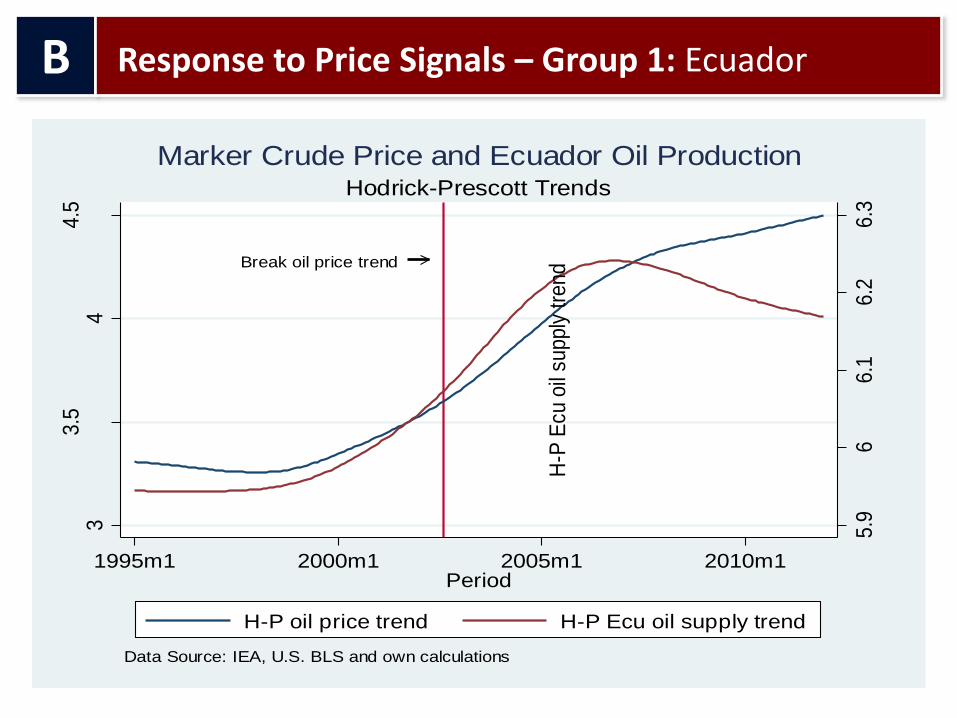

Response to Price Signals – Group 1: Ecuador

Break oil price trend

5.9

66.1

6.2

6.3

H-P

Ecu

oil

supply

tre

nd

33.5

44.5

H-P

oil

pri

ce tre

nd

1995m1 2000m1 2005m1 2010m1Period

H-P oil price trend H-P Ecu oil supply trend

Data Source: IEA, U.S. BLS and own calculations

Hodrick-Prescott Trends

Marker Crude Price and Ecuador Oil Production

B

Response to Price Signals – Group 1: Ecuador

Break oil price trend

2000

2500

3000

3500

4000

supply

(th

b/d

)

1995m1 2000m1 2005m1 2010m1Period

Data Source: IEA and author calculations

Mexico Oil Production

B

Response to Price Signals – Group 1: Mexico

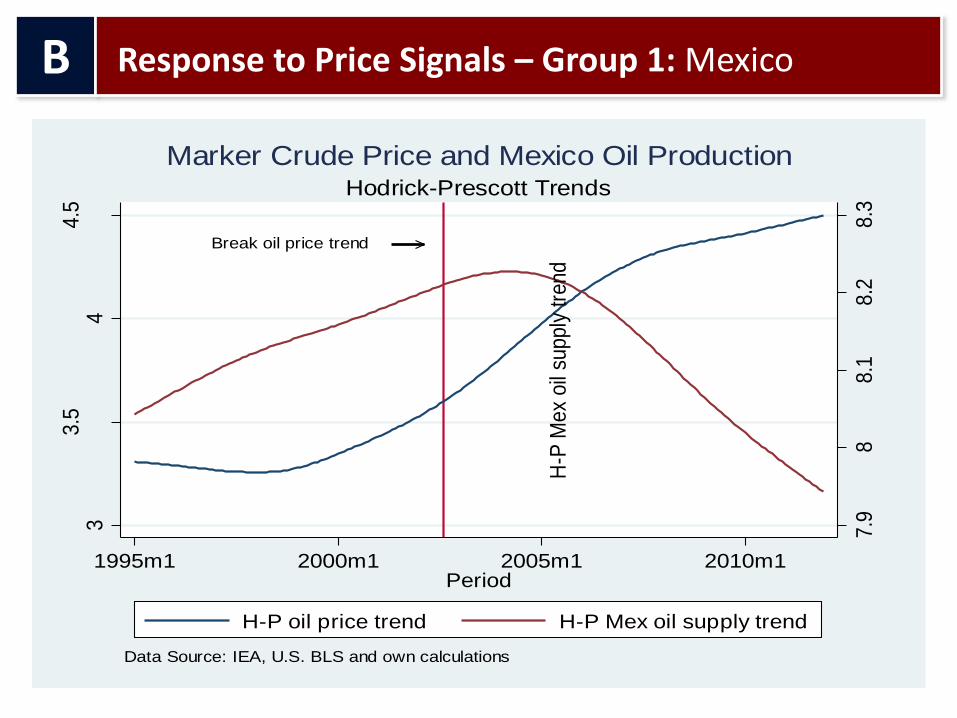

Break oil price trend

7.9

88.1

8.2

8.3

H-P

Mex

oil

supply

tre

nd

33.5

44.5

H-P

oil

pri

ce tre

nd

1995m1 2000m1 2005m1 2010m1Period

H-P oil price trend H-P Mex oil supply trend

Data Source: IEA, U.S. BLS and own calculations

Hodrick-Prescott Trends

Marker Crude Price and Mexico Oil Production

B

Response to Price Signals – Group 1: Mexico

Break oil price trend

1500

2000

2500

3000

3500

supply

(th

b/d

)

1995m1 2000m1 2005m1 2010m1Period

Data Source: IEA and author calculations

Venezuela Oil Production

B

Response to Price Signals – Group 1: Venezuela

Break oil price trend

7.9

7.9

58

8.0

58.1

H-P

Vzl

a o

il su

pply

tre

nd

33.5

44.5

H-P

oil

pri

ce tre

nd

1995m1 2000m1 2005m1 2010m1Period

H-P oil price trend H-P Vzla oil supply trend

Data Source: IEA, U.S. BLS and own calculations

Hodrick-Prescott Trends

Marker Crude Price and Venezuela Oil Production

B

Response to Price Signals – Group 1: Venezuela

Following oil price increases, oil production has sharply increased in:

Group 2

Brazil Colombia

Peru

B

Response to Price Signals: Supply

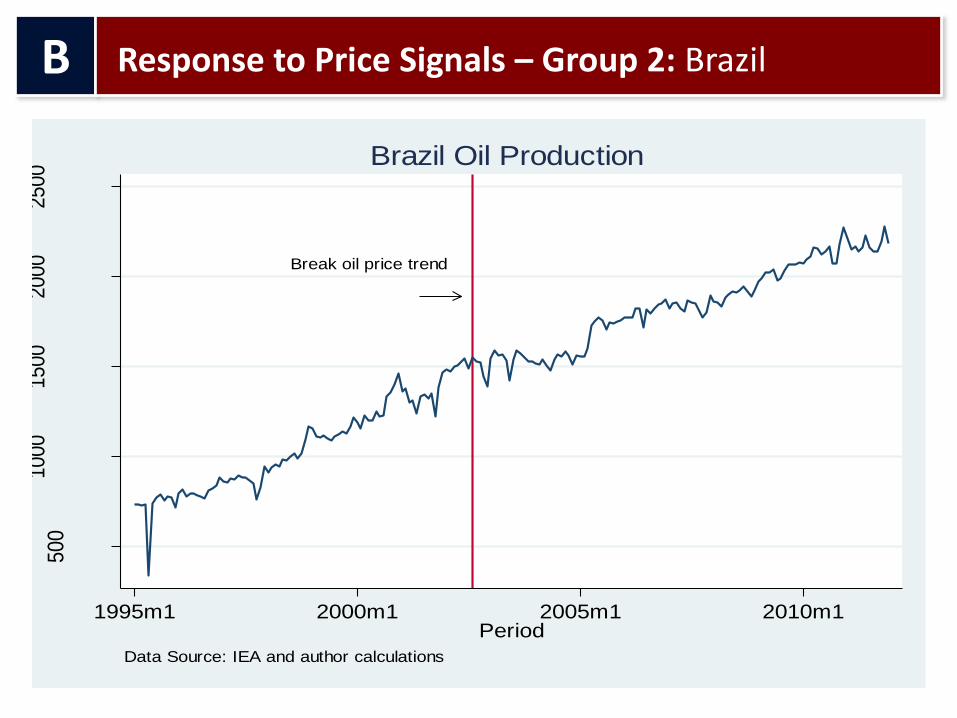

Break oil price trend

500

1000

1500

2000

2500

supply

(th

b/d

)

1995m1 2000m1 2005m1 2010m1Period

Data Source: IEA and author calculations

Brazil Oil Production

B

Response to Price Signals – Group 2: Brazil

Break oil price trend

6.5

77.5

8

H-P

Bra

oil

supply

tre

nd

33.5

44.5

H-P

oil

pri

ce tre

nd

1995m1 2000m1 2005m1 2010m1Period

H-P oil price trend H-P Bra oil supply trend

Data Source: IEA, U.S. BLS and own calculations

Hodrick-Prescott Trends

Marker Crude Price and Brazil Oil Production

B

Response to Price Signals – Group 2: Brazil

Break oil price trend

500

600

700

800

900

1000

supply

(th

b/d

)

1995m1 2000m1 2005m1 2010m1Period

Data Source: IEA and author calculations

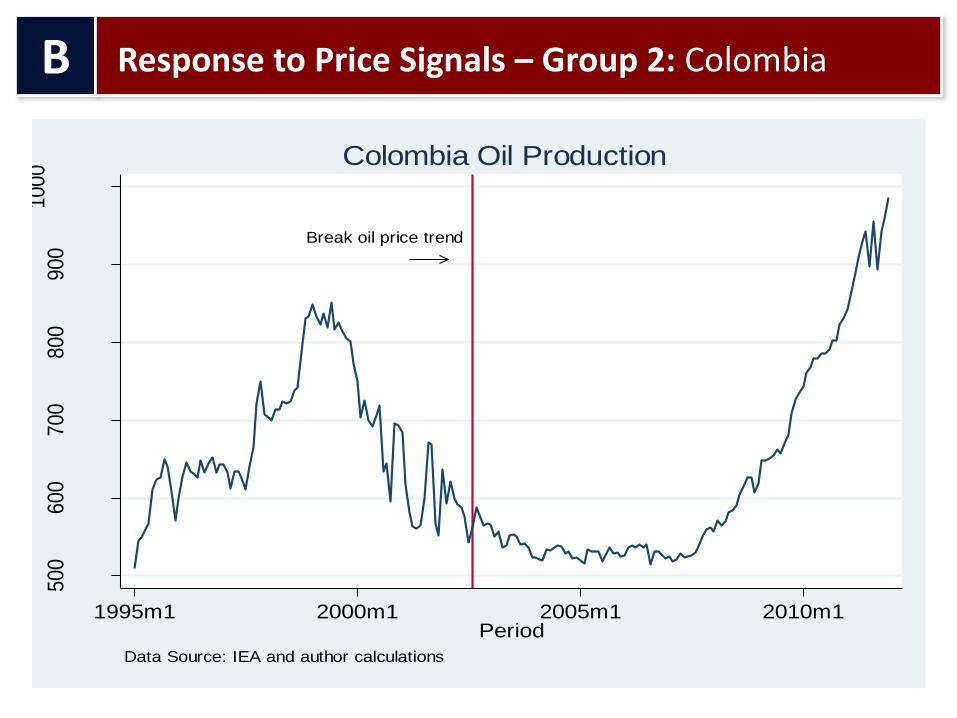

Colombia Oil Production

B

Response to Price Signals – Group 2: Colombia

Break oil price trend

6.3

6.4

6.5

6.6

6.7

6.8

H-P

Col o

il su

pply

tre

nd

33.5

44.5

H-P

oil

pri

ce tre

nd

1995m1 2000m1 2005m1 2010m1Period

H-P oil price trend H-P Col oil supply trend

Data Source: IEA, U.S. BLS and own calculations

Hodrick-Prescott Trends

Marker Crude Price and Colombia Oil Production

B

Response to Price Signals – Group 2: Colombia

Break oil price trend

80

100

120

140

160

supply

(th

b/d

)

1995m1 2000m1 2005m1 2010m1Period

Data Source: IEA and author calculations

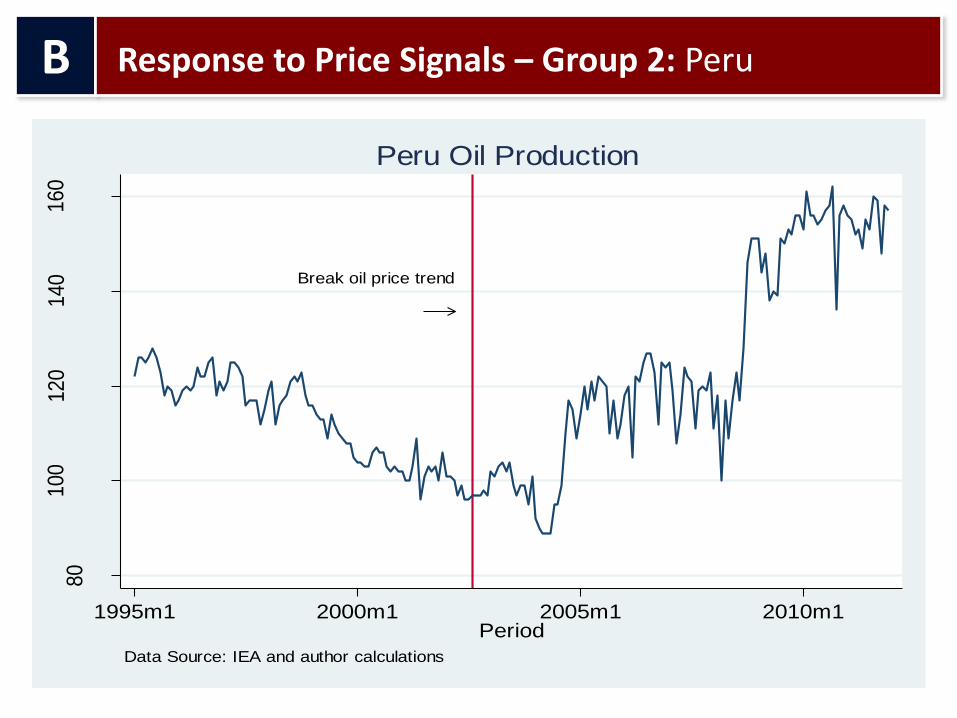

Peru Oil Production

B

Response to Price Signals – Group 2: Peru

Break oil price trend

4.6

4.7

4.8

4.9

55.1

H-P

Per

oil s

upply

tre

nd

33.5

44.5

H-P

oil

pri

ce tre

nd

1995m1 2000m1 2005m1 2010m1Period

H-P oil price trend H-P Per oil supply trend

Data Source: IEA, U.S. BLS and own calculations

Hodrick-Prescott Trends

Marker Crude Price and Peru Oil Production

B

Response to Price Signals – Group 2: Peru

Break oil price trend

100

200

300

400

500

1995m1 2000m1 2005m1 2010m1period

Group 1 supply index Group 2 supply index

Oil price index

Data Source: IEA, U.S. BLS, Baker Hughes Inc and own calculations

Price and Supply Performance

Group 1 vs. Group 2

B

Response to Price Signals – Group 1 vs. Group 2

Over the last 15 years, oil prices increased almost fourfold – in real terms – from $26 / barrel to $96 / barrel

LAC oil producers reacted differently:

Group 1 Group 2

Drilling activity has remained stagnant and oil supply has

fallen

Drilling activity has increased 2.8 x Oil output has

increased 150%

B

Response to Price Signals

Therefore, the situation is: Same price signals Different reactions Why?

Institutional Framework

B

Response to Price Signals

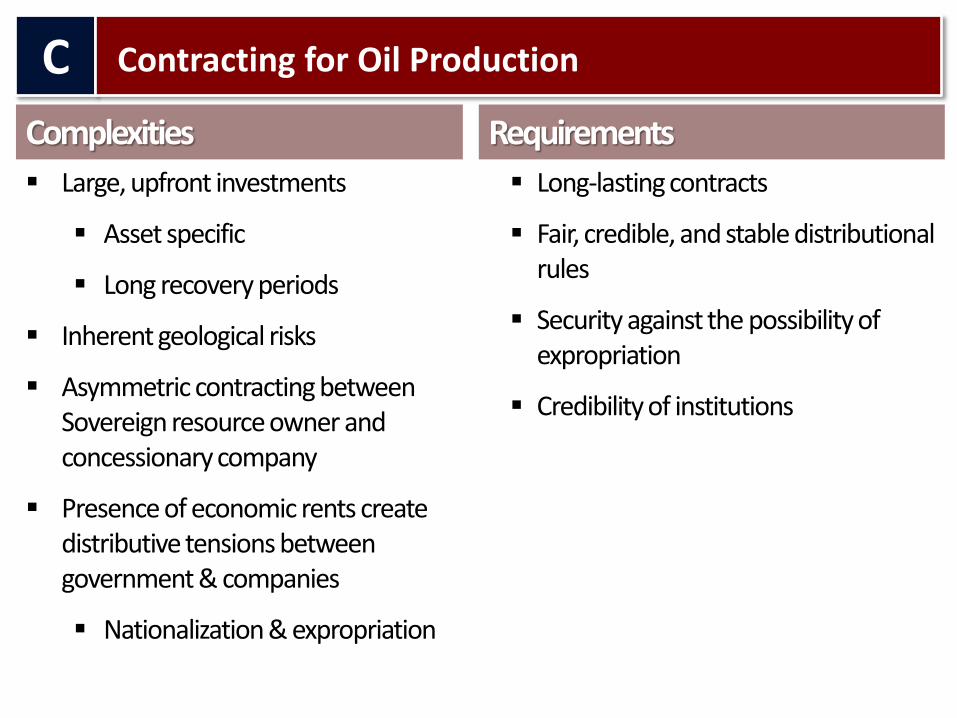

Large, upfront investments

Asset specific

Long recovery periods

Inherent geological risks

Asymmetric contracting between Sovereign resource owner and concessionary company

Presence of economic rents create distributive tensions between government & companies

Nationalization & expropriation

Complexities Requirements

Long-lasting contracts

Fair, credible, and stable distributional rules

Security against the possibility of expropriation

Credibility of institutions

C

Contracting for Oil Production

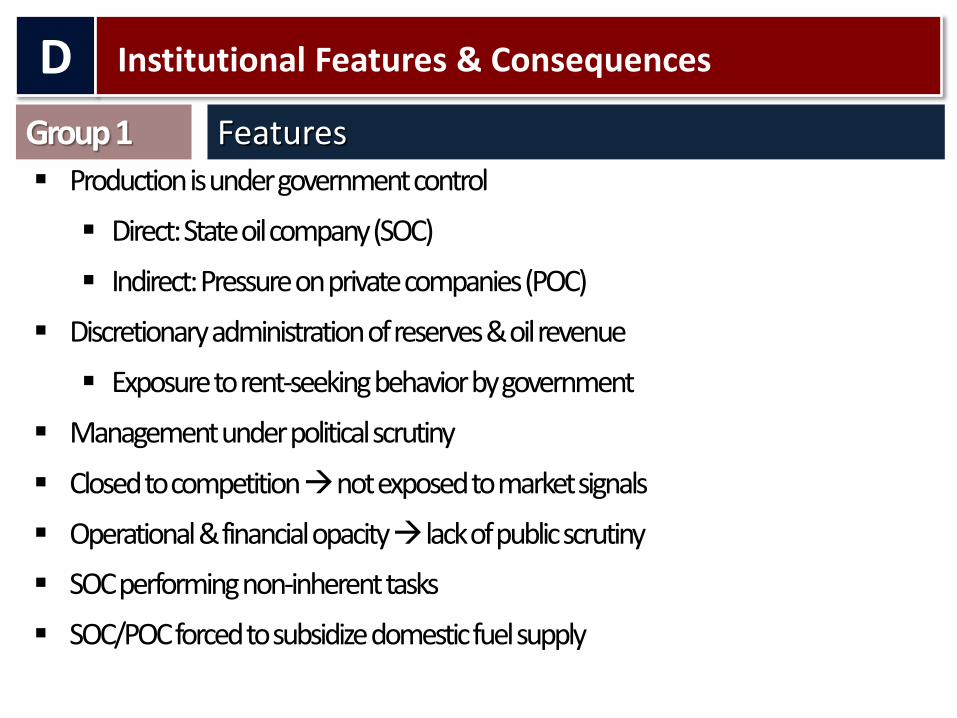

Production is under government control

Direct: State oil company (SOC)

Indirect: Pressure on private companies (POC)

Discretionary administration of reserves & oil revenue

Exposure to rent-seeking behavior by government

Management under political scrutiny

Closed to competition not exposed to market signals

Operational & financial opacity lack of public scrutiny

SOC performing non-inherent tasks

SOC/POC forced to subsidize domestic fuel supply

Group 1 Features

D

Institutional Features & Consequences

Permanent expropriation of revenues

Subsidies, non-oil related activities, and discretionary distribution

Uncertainty regarding revenues & savings

Difficult to undertake large projects

No response to market signals

No behavior as a commercial firm

Lack of competition Leads to inefficiency

Limited access to

Technology, financing , and engineering capacity

Group 1 Consequences

D

Institutional Features & Consequences

6.5

6.6

6.7

6.8

Hodri

ck-P

resc

ott T

rend

1995m1 2000m1 2005m1 2010m1Period

Data Source: IEA and own calculations

Hodrick-Prescott Trend

Argentina Oil Production and Institutional Break

Swearing in Néstor Kischner 05/03

D

Institutional Features – Group 1: Argentina

5.9

66.1

6.2

6.3

Hodri

ck-P

resc

ott T

rend

1995m1 2000m1 2005m1 2010m1Period

Data Source: IEA and own calculations

Hodrick-Prescott Trend

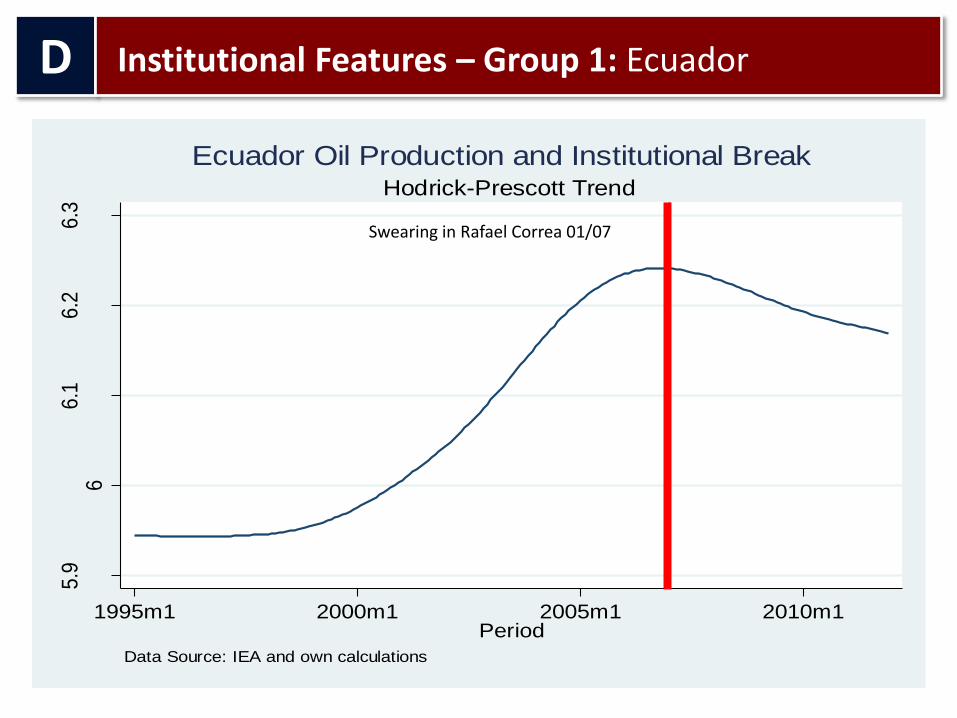

Ecuador Oil Production and Institutional Break

Swearing in Rafael Correa 01/07

D

Institutional Features – Group 1: Ecuador

7.9

88.1

8.2

8.3

Hodri

ck-P

resc

ott T

rend

1995m1 2000m1 2005m1 2010m1Period

Data Source: IEA and own calculations

Hodrick-Prescott Trend

Mexico Oil Production and Institutional Break

Swearing in Felipe Calderón 12/06

D

Institutional Features – Group 1: Mexico

7.9

7.9

5

8

8.0

58.1

Hodri

ck-P

resc

ott T

rend

1995m1 2000m1 2005m1 2010m1Period

Data Source: IEA and own calculations

Hodrick-Prescott Trend

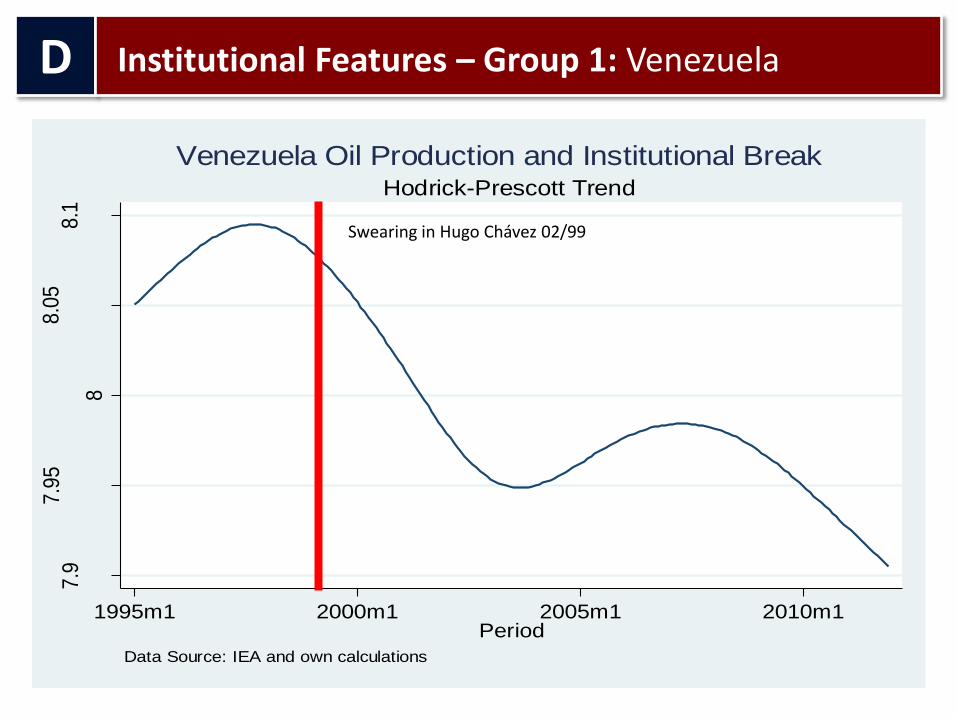

Venezuela Oil Production and Institutional Break

Swearing in Hugo Chávez 02/99

D

Institutional Features – Group 1: Venezuela

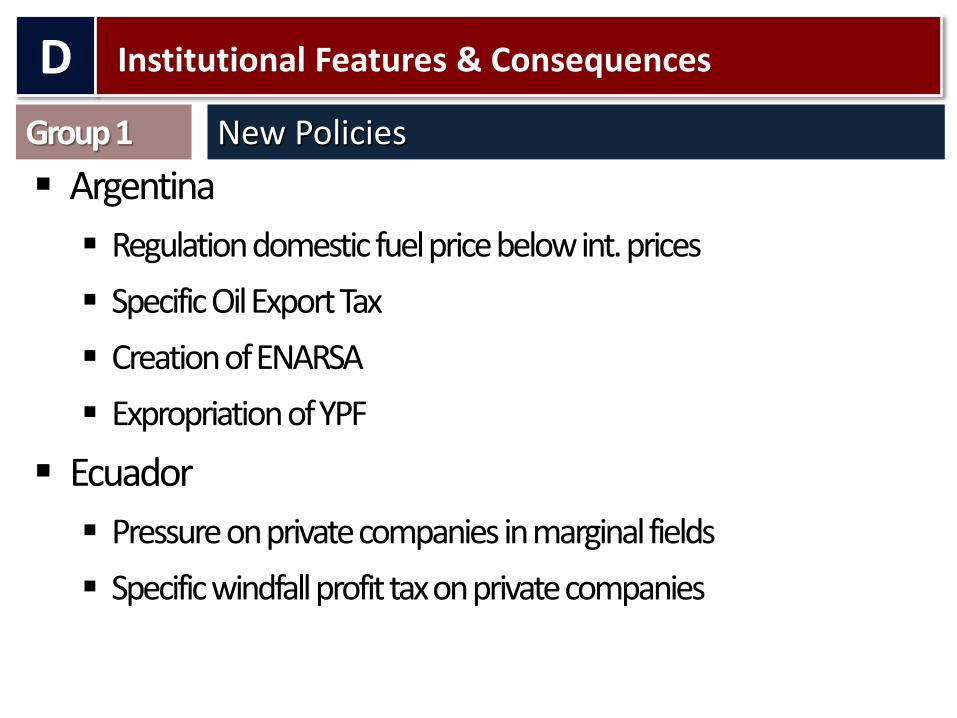

Argentina

Regulation domestic fuel price below int. prices

Specific Oil Export Tax

Creation of ENARSA

Expropriation of YPF

Ecuador

Pressure on private companies in marginal fields

Specific windfall profit tax on private companies

Group 1 New Policies

D

Institutional Features & Consequences

Mexico

Pressure on PEMEX spending in favor of transfers to government

Ceiling on PIDIREGAS debt

Venezuela

Interference on PDVSA professional management

New 2002 Hydrocarbons Law increasing government intervention power

Expropriation of private companies both national and international, core and non-core

Group 1 New Policies

D

Institutional Features & Consequences

Government administers national oil reserves

By a non-operating hydrocarbon agency (NHA)

NHA opens oil bearing lands to competition

National & foreign

Private & state owned

Exposed to market signals

Contractually set rules: distribution & operation

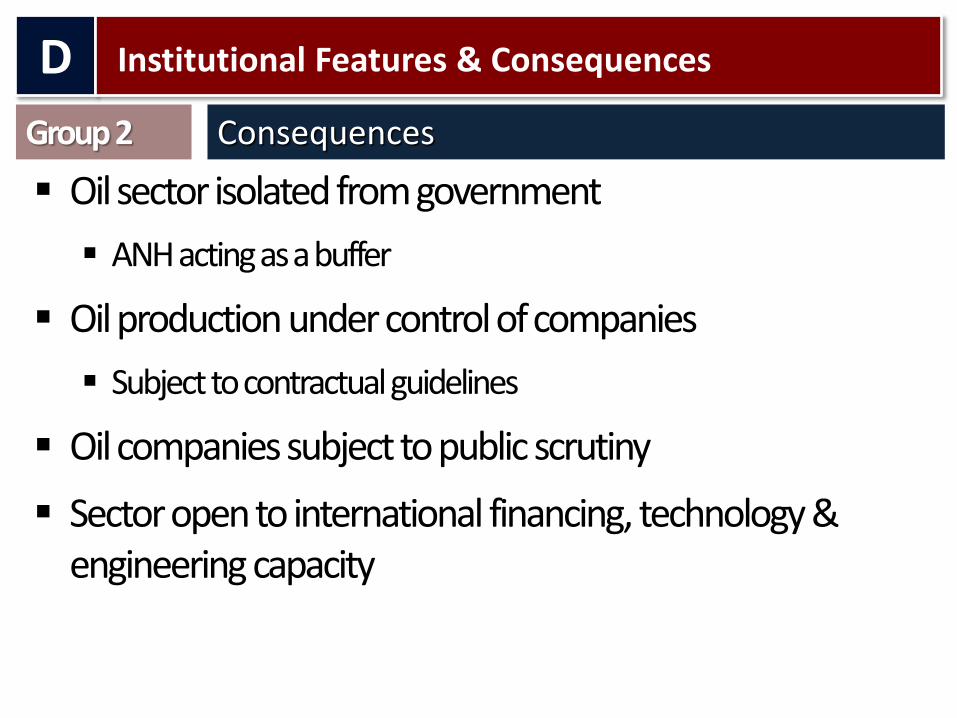

Group 2 Features

D

Institutional Features & Consequences

SOC under same rules as POC

Not subject to discretionary government intervention

SOC focused on industry related activities

Subject to competition & public scrutiny

Subsidy to domestic market

Explicit and assumed by the government

Reserves not in jeopardy

SOC can be partially privatized

Group 2 Features

D

Institutional Features & Consequences

Oil sector isolated from government

ANH acting as a buffer

Oil production under control of companies

Subject to contractual guidelines

Oil companies subject to public scrutiny

Sector open to international financing, technology & engineering capacity

Group 2 Consequences

D

Institutional Features & Consequences

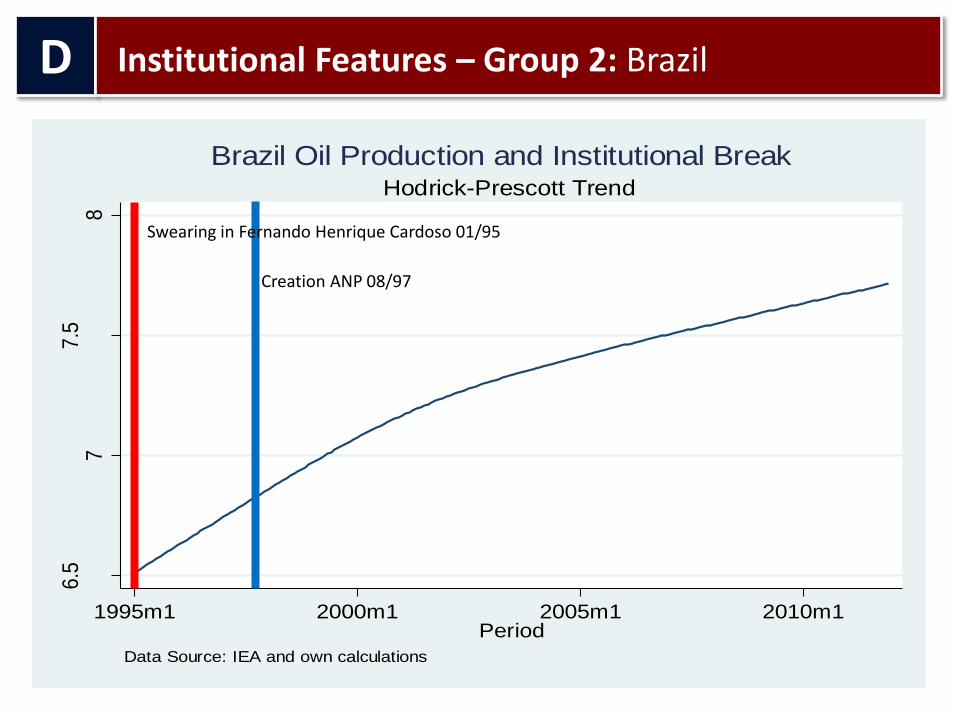

6.5

77.5

8

Hodri

ck-P

resc

ott T

rend

1995m1 2000m1 2005m1 2010m1Period

Data Source: IEA and own calculations

Hodrick-Prescott Trend

Brazil Oil Production and Institutional Break

Swearing in Fernando Henrique Cardoso 01/95

Creation ANP 08/97

D

Institutional Features – Group 2: Brazil

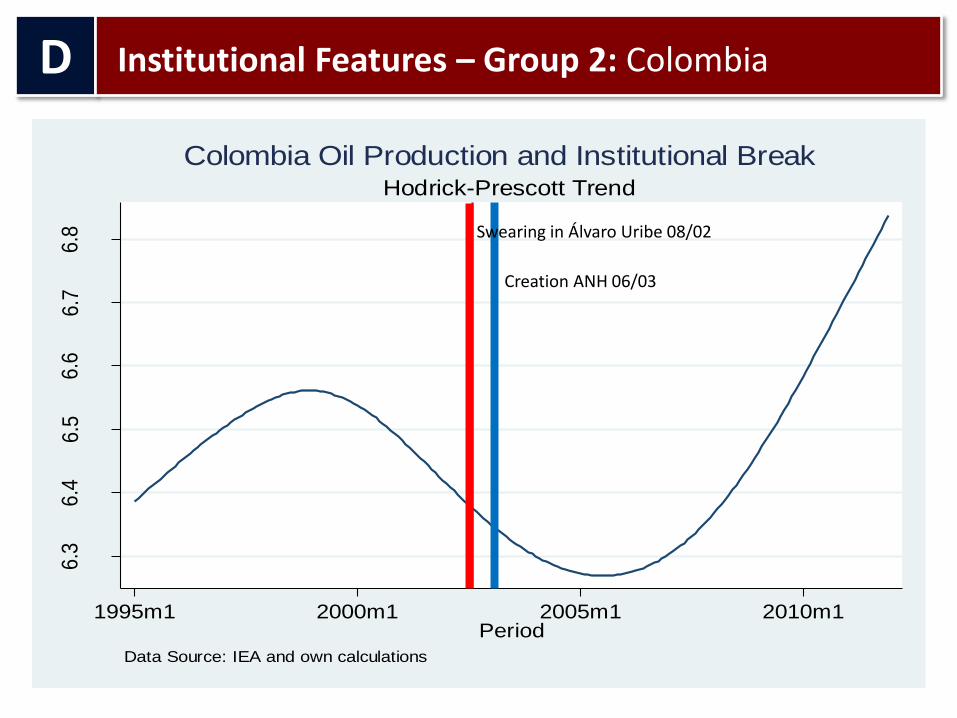

6.3

6.4

6.5

6.6

6.7

6.8

Hodri

ck-P

resc

ott T

rend

1995m1 2000m1 2005m1 2010m1Period

Data Source: IEA and own calculations

Hodrick-Prescott Trend

Colombia Oil Production and Institutional Break

Swearing in Álvaro Uribe 08/02

Creation ANH 06/03

D

Institutional Features – Group 2: Colombia

4.6

4.7

4.8

4.9

55.1

Hodri

ck-P

resc

ott T

rend

1995m1 2000m1 2005m1 2010m1Period

Data Source: IEA and own calculations

Hodrick-Prescott Trend

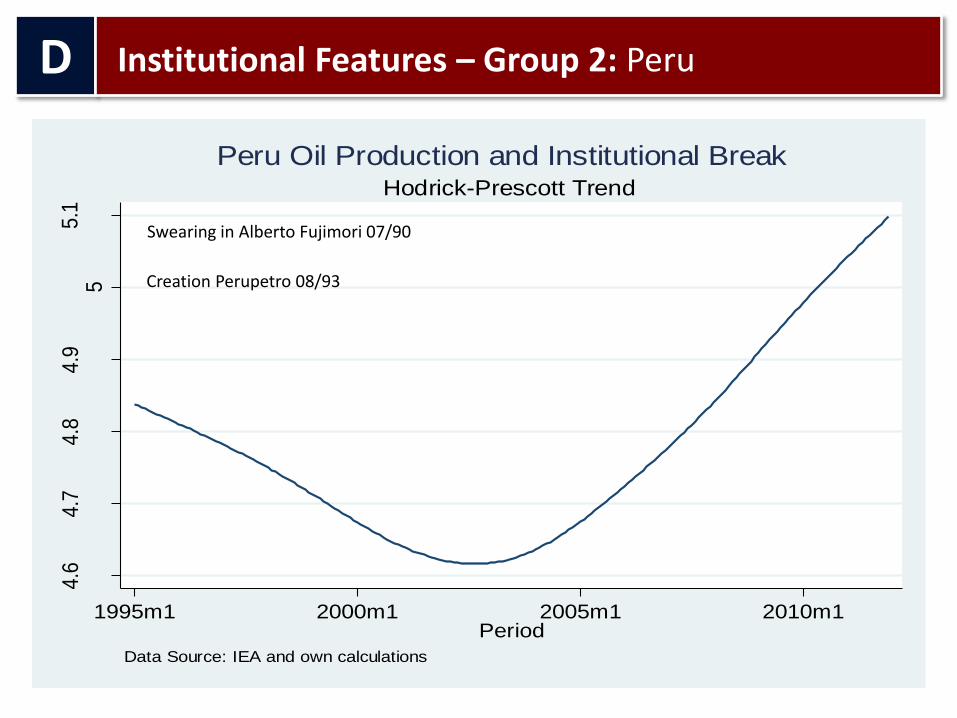

Peru Oil Production and Institutional Break

Swearing in Alberto Fujimori 07/90

Creation Perupetro 08/93

D

Institutional Features – Group 2: Peru

Brazil

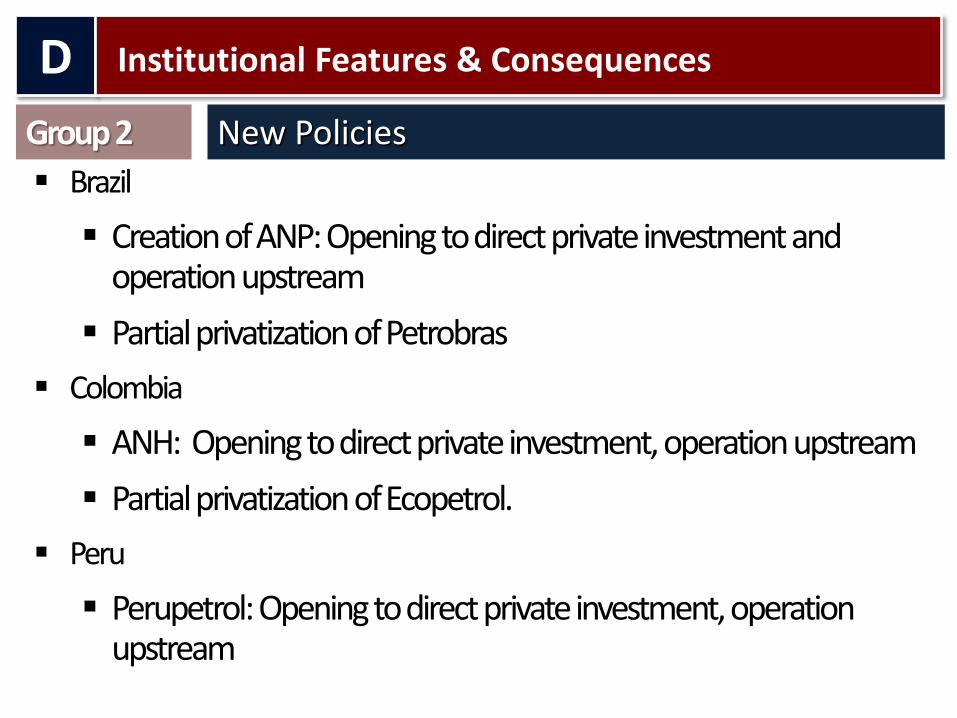

Creation of ANP: Opening to direct private investment and operation upstream

Partial privatization of Petrobras

Colombia

ANH: Opening to direct private investment, operation upstream

Partial privatization of Ecopetrol.

Peru

Perupetrol: Opening to direct private investment, operation upstream

Group 2 New Policies

D

Institutional Features & Consequences

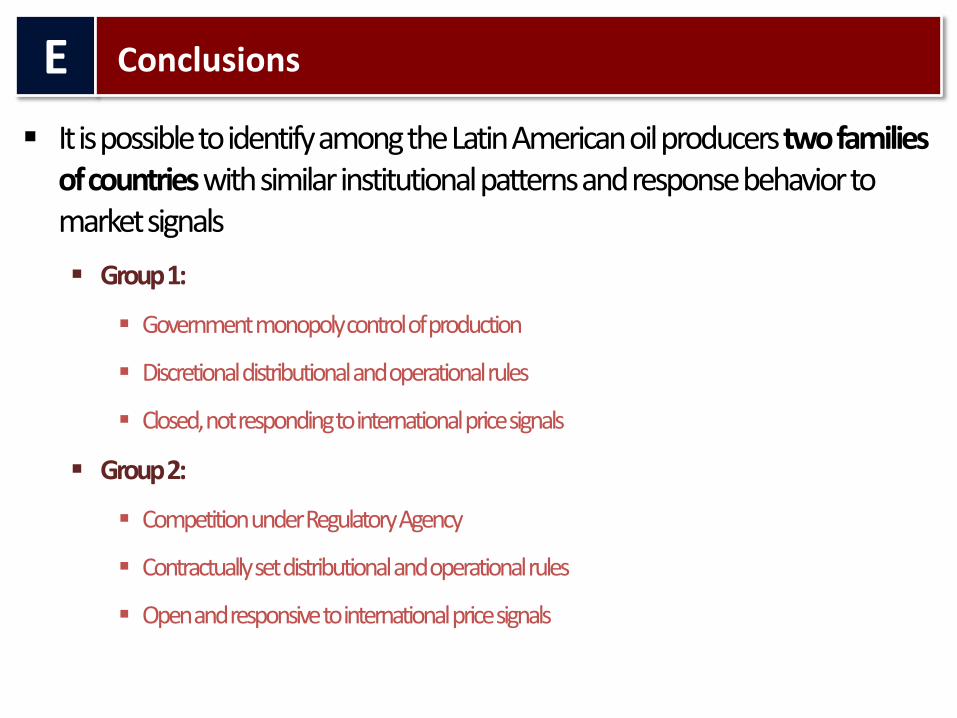

It is possible to identify among the Latin American oil producers two families of countries with similar institutional patterns and response behavior to market signals

Group 1:

Government monopoly control of production

Discretional distributional and operational rules

Closed, not responding to international price signals

Group 2:

Competition under Regulatory Agency

Contractually set distributional and operational rules

Open and responsive to international price signals

E

Conclusions

4

The Peruvian Case

The Oil Market in Peru

Drilling Activity

A

B

C

Natural Gas Growth

Closing Considerations D

A

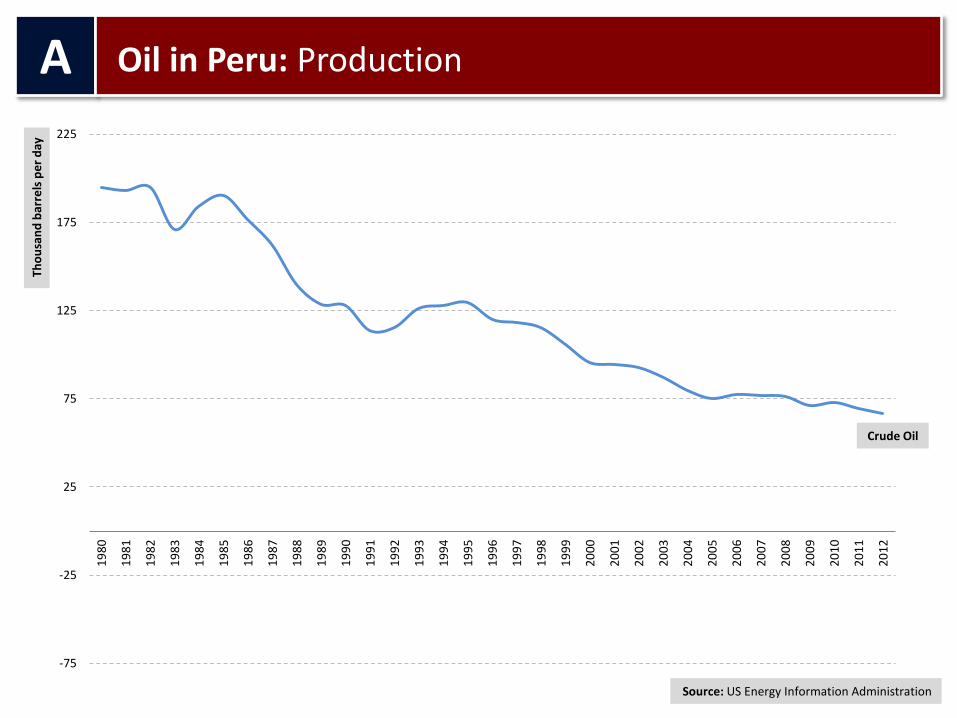

Oil in Peru: Production

Source: US Energy Information Administration

Tho

usa

nd

bar

rels

pe

r d

ay

Crude Oil

-75

-25

25

75

125

175

225

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

A

Oil in Peru: Production

Source: US Energy Information Administration

Tho

usa

nd

bar

rels

pe

r d

ay

Non-Crude Oil

-75

-25

25

75

125

175

225

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

A

Oil in Peru: Production

Source: US Energy Information Administration

Tho

usa

nd

bar

rels

pe

r d

ay

Total Oil

-75

-25

25

75

125

175

225

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

A

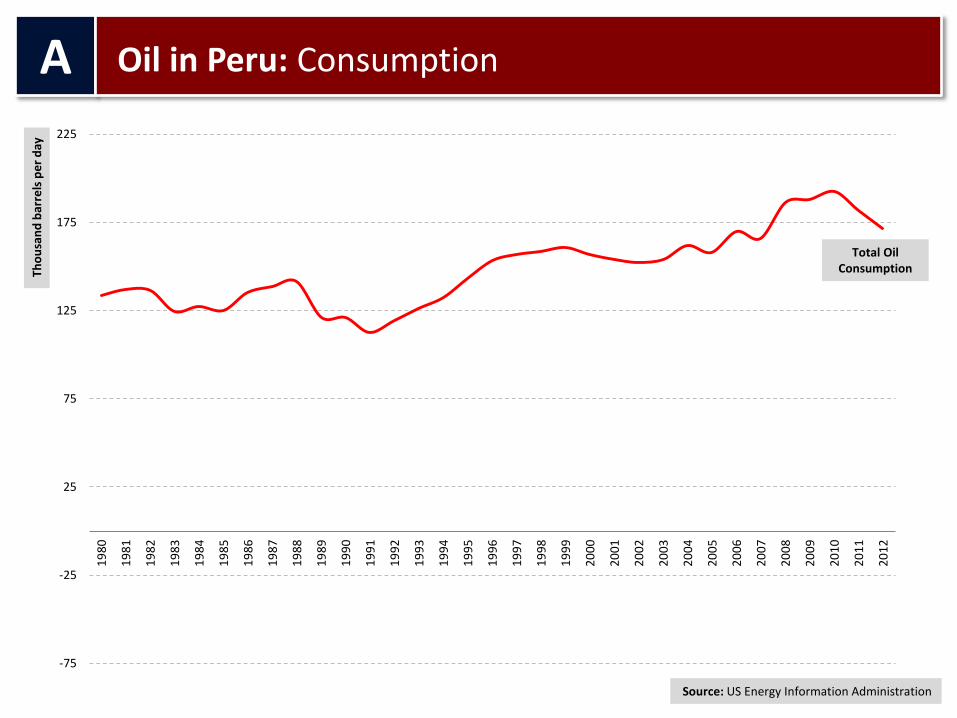

Oil in Peru: Consumption

Source: US Energy Information Administration

Tho

usa

nd

bar

rels

pe

r d

ay

Total Oil Consumption

-75

-25

25

75

125

175

225

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

A

Oil in Peru: Balance

Source: US Energy Information Administration

Tho

usa

nd

bar

rels

pe

r d

ay

Oil Balance

-75

-25

25

75

125

175

225

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

B

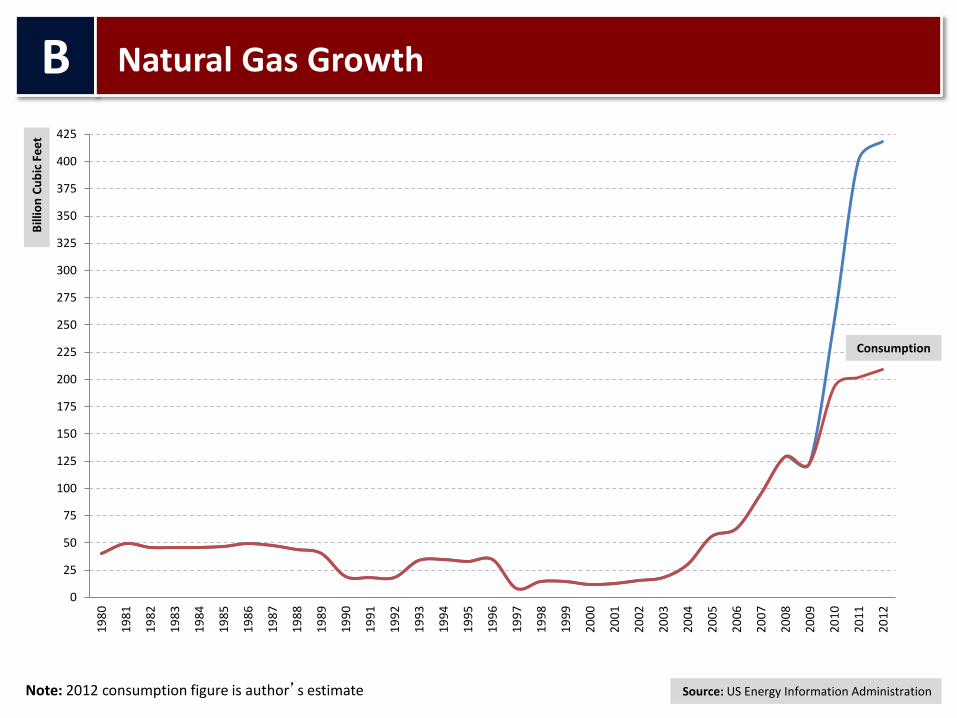

Natural Gas Growth

Source: US Energy Information Administration

Bill

ion

Cu

bic

Fe

et

0

25

50

75

100

125

150

175

200

225

250

275

300

325

350

375

400

425

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Production