Embed Size (px)

Citation preview

Spike Choo

Country Director, Indonesia

INDONESIA DIGITAL TRANSFORMATION OUTLOOK BRIEFING 2016

ASEAN & Indonesia e-Commerce Outlook

1

2

Year in Review: Global Key Highlights of 2015

• Asia E-Commerce flexes its muscle • Alibaba Singles’ Day sales reached USD 14.3Bn• India’s e-Commerce grew ~40% in 2015 to USD 7.5Bn• SEA e-Commerce to double to $15Bn by 2019 from $6.5Bn

22

• Wearables goes mainstream• Apple Watch debut; mainstream watchmakers join the fray• Activity trackers make it to top 10 X’mas shopping lists• More niche wearables (kids , elderly , etc) emerges

33

• Cross industry disruption will continue to accelerate• More disruptive services from Uber and the likes; UberCargo in

HK, GoJek’s Food Delivery, WeChat’s WePay, etc• Fintech continues to evolve, ie Crowd-finance, Digital Banking

44

• Startup investment is cooling down• Number of mega deals (100Mn & above) drop to <20• Several tech IPO perform badly despite lowering their IPO

price or shares (eg Square, Etsy, Shopify, First Data etc)

11

3

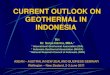

ASEAN e-Commerce Market Overview

• Robust growth (~25% YoY) but market still small compare to China and US

• Positive factors driving e-Commerce growth in APAC such as sizable and youthful population, robust economic growth from and higher domestic spending

ASEAN 6, China & US e-Commerce

Market Size, 2015-2019, USD Billions

Source: Frost Analysis ASEAN 6 refers to SG, MY, ID, TH, PH, VT

6.5

217.3277.0

14.8

411.6 430.0

ASEAN 6 China US

24.9%

24.1%

11.6%

ASEAN 6, China & US Population,

2015E, Millions

553.2

1,375.0

321.2ASEAN 6,

China,

US,

2015

2019

CAGR

4

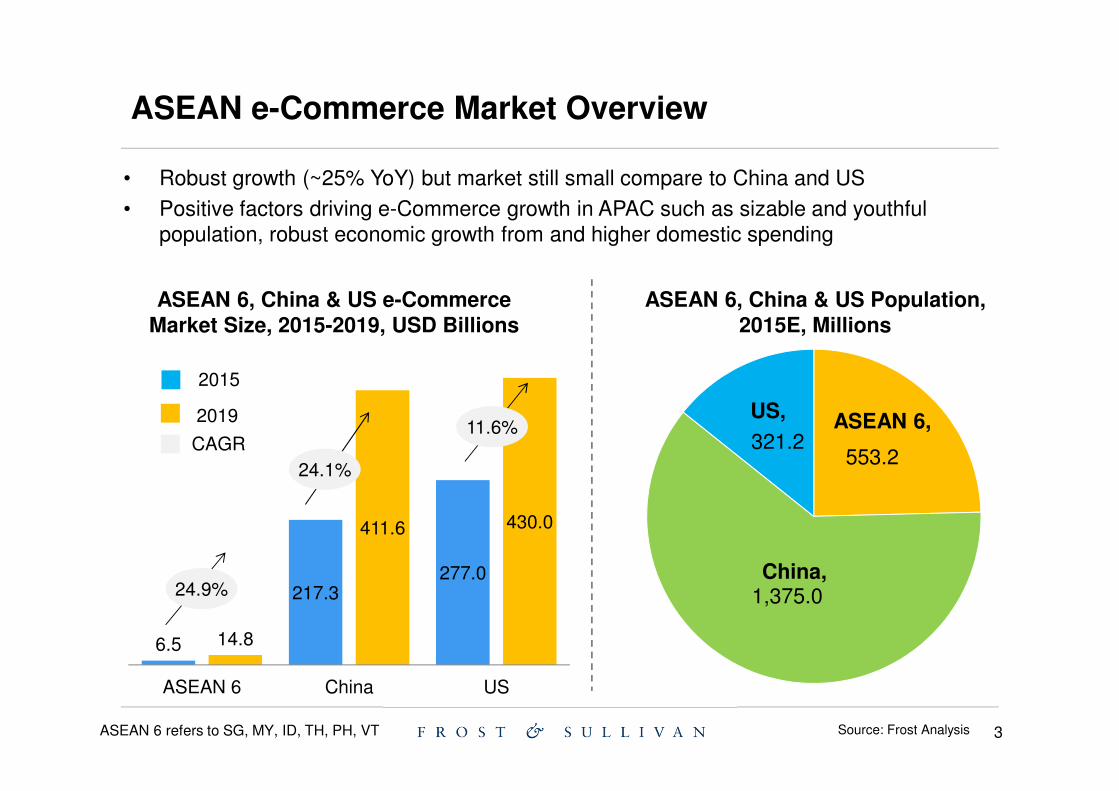

Indonesia e-Commerce Market Snapshot

7501,100

1,350

1,850

2,400

2,950

3,800

2013 2014 2015 2016 2017 2018 2019

31.1%

Indonesia e-Commerce Market Size, 2015-2019, USD Millions

1. Positive demographics profile2. Robust economic growth3. High ICT adoption4. Large number of local players

GROWTH DRIVERS KEY RESTRAINTS

1. Poor logistics infrastructure2. Large unbanked population3. Low adoption of cashless payment4. Limited ICT competency

5

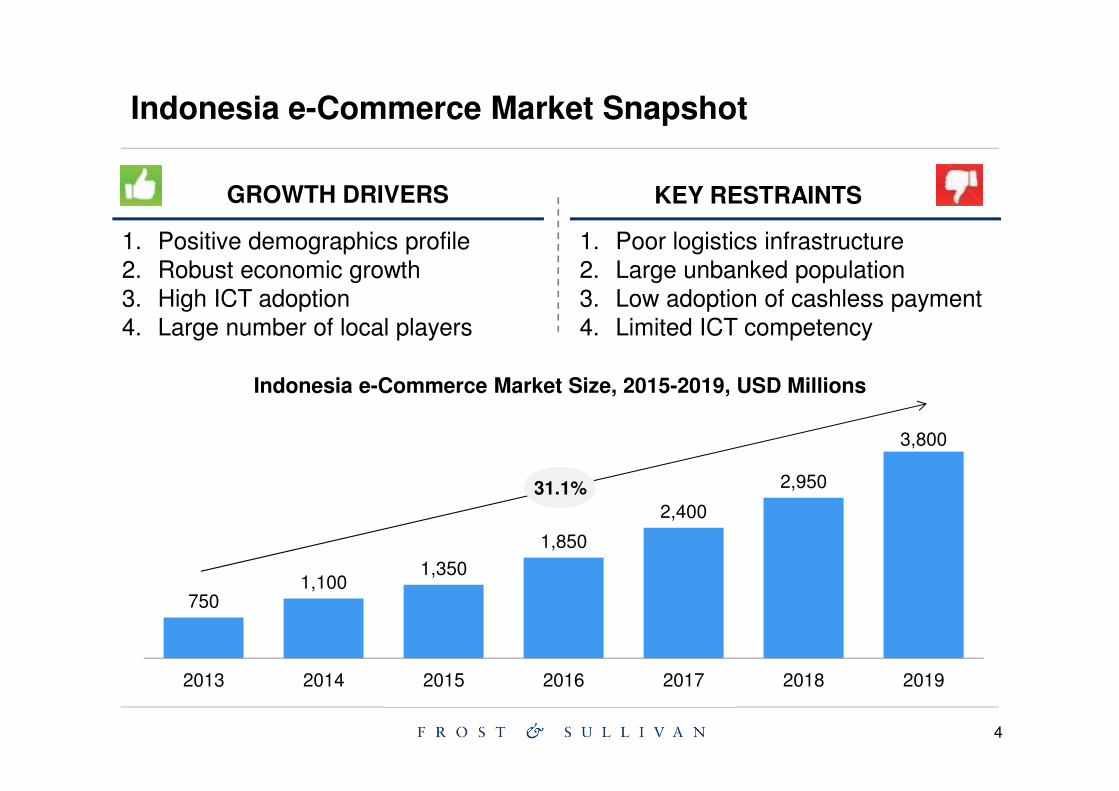

Growth Drivers of EcommerceA fast growing economy with a young population and increasing income

Real GDP & Disposable Income Level

$896 $1,207

$2,148$2,464

2015 2019

Real GDP(USD, BN)

DisposableIncome (USD)

3.5%

7.8%

28%

64%

8%0-14

15-59

60 andabove

Indonesia Population by Age Group, 2013

Indonesia Internet User Forecast

73.0 88.5 104.0 119.5 135.0

0%

10%

20%

30%

40%

50%

60%

0

50

100

150

2015 2016 2017 2018 2019

Internet Users (million)

% population

CAGR = 16.6%

6

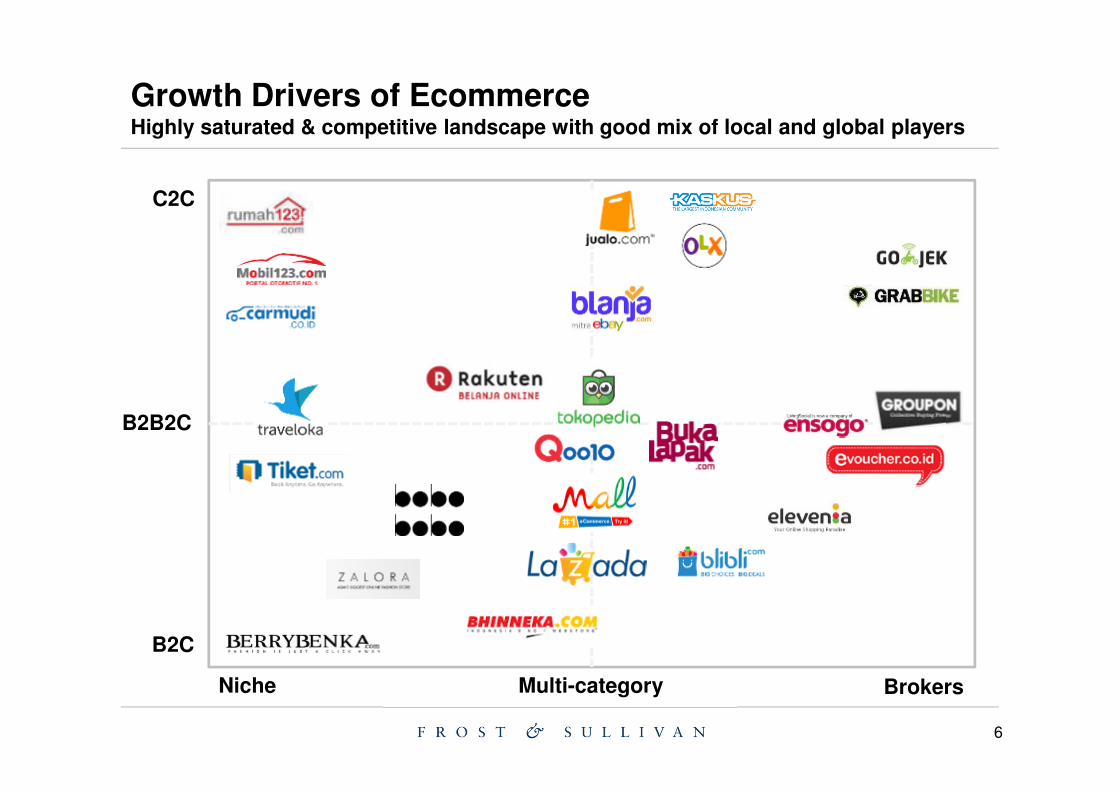

Growth Drivers of EcommerceHighly saturated & competitive landscape with good mix of local and global players

Niche

B2C

Multi-category

C2C

B2B2C

Brokers

7

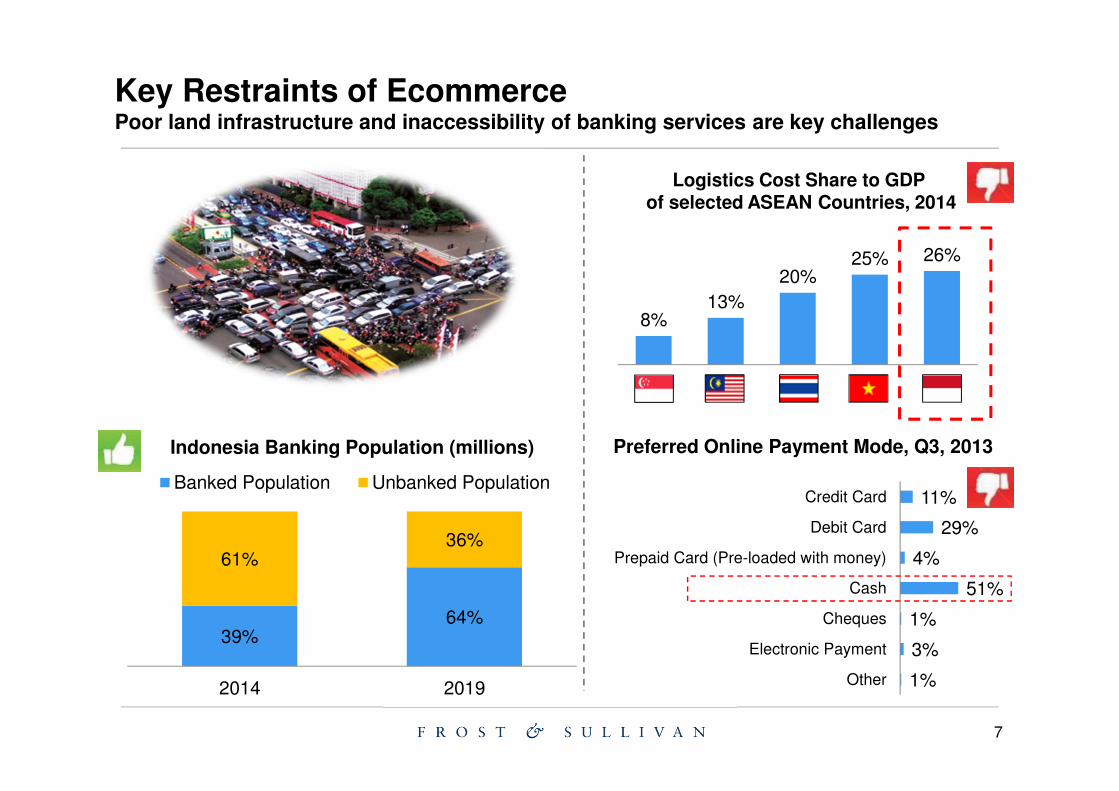

Key Restraints of EcommercePoor land infrastructure and inaccessibility of banking services are key challenges

Indonesia Banking Population (millions)

39%64%

61%36%

2014 2019

Banked Population Unbanked Population

8%13%

20%25% 26%

Logistics Cost Share to GDP of selected ASEAN Countries, 2014

1%

3%

1%

51%

4%

29%

11%

Other

Electronic Payment

Cheques

Cash

Prepaid Card (Pre-loaded with money)

Debit Card

Credit Card

Preferred Online Payment Mode, Q3, 2013

8

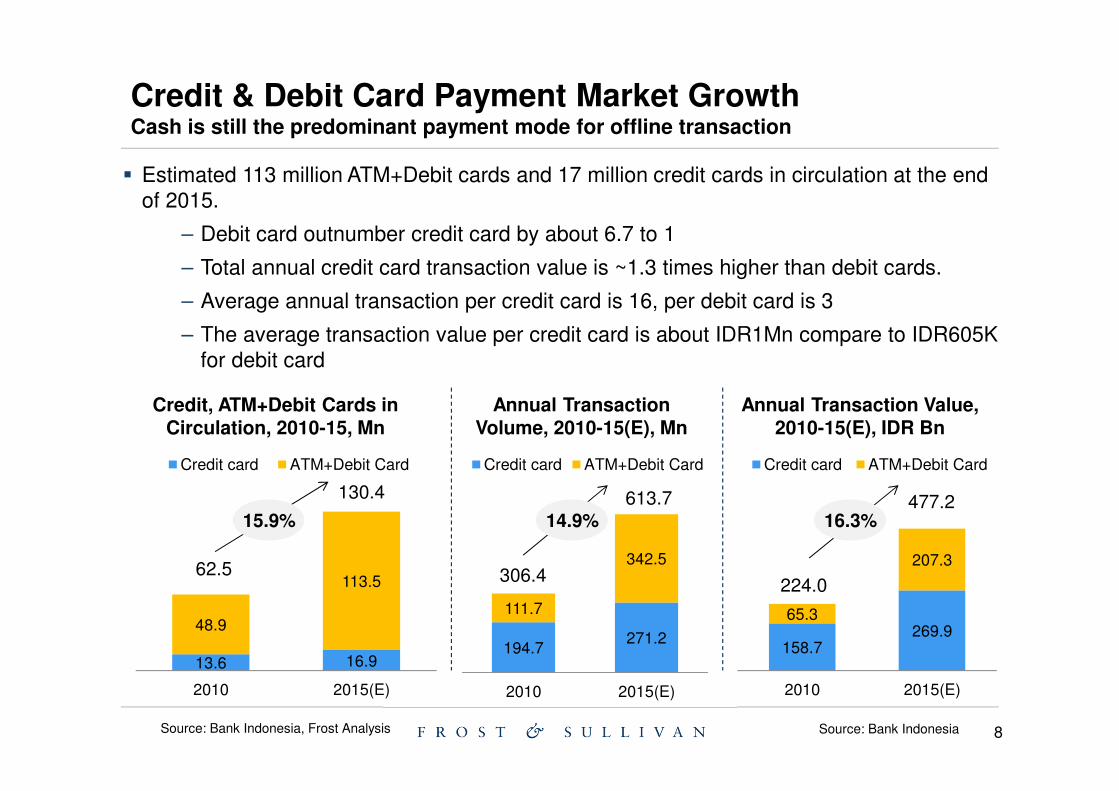

Credit & Debit Card Payment Market GrowthCash is still the predominant payment mode for offline transaction

� Estimated 113 million ATM+Debit cards and 17 million credit cards in circulation at the end of 2015.

– Debit card outnumber credit card by about 6.7 to 1

– Total annual credit card transaction value is ~1.3 times higher than debit cards.

– Average annual transaction per credit card is 16, per debit card is 3

– The average transaction value per credit card is about IDR1Mn compare to IDR605K for debit card

Source: Bank Indonesia, Frost Analysis

Annual Transaction Value, 2010-15(E), IDR Bn

Annual Transaction Volume, 2010-15(E), Mn

194.7271.2

111.7

342.5

2010 2015(E)

Credit card ATM+Debit Card

158.7269.9

65.3

207.3

2010 2015(E)

Credit card ATM+Debit Card

224.0

477.216.3%

306.4

613.714.9%

13.6 16.9

48.9

113.5

2010 2015(E)

Credit card ATM+Debit Card

Credit, ATM+Debit Cards in Circulation, 2010-15, Mn

62.5

130.4

15.9%

Source: Bank Indonesia

9

2010 2015(E)2010 2015(E)2010 2015(E)

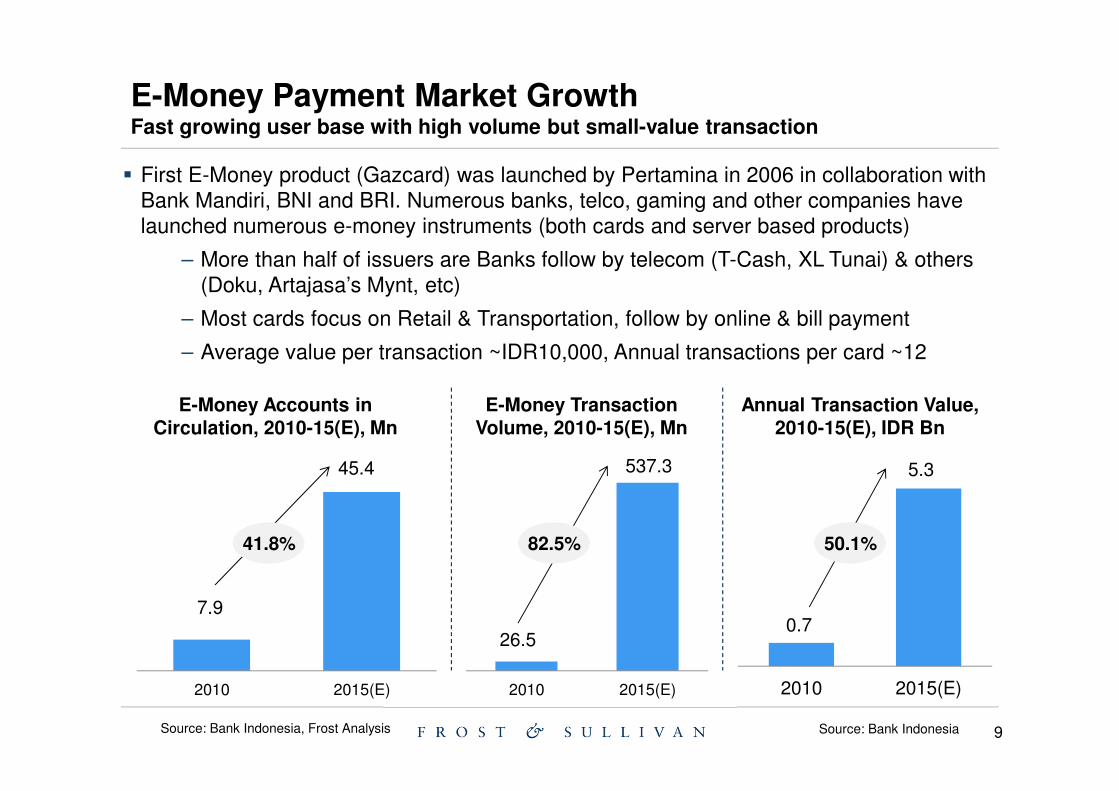

E-Money Payment Market GrowthFast growing user base with high volume but small-value transaction

� First E-Money product (Gazcard) was launched by Pertamina in 2006 in collaboration with Bank Mandiri, BNI and BRI. Numerous banks, telco, gaming and other companies have launched numerous e-money instruments (both cards and server based products)

– More than half of issuers are Banks follow by telecom (T-Cash, XL Tunai) & others (Doku, Artajasa’s Mynt, etc)

– Most cards focus on Retail & Transportation, follow by online & bill payment

– Average value per transaction ~IDR10,000, Annual transactions per card ~12

Source: Bank Indonesia, Frost Analysis

Annual Transaction Value, 2010-15(E), IDR Bn

E-Money Transaction Volume, 2010-15(E), Mn

0.7

5.3

50.1%

26.5

537.3

82.5%

E-Money Accounts in Circulation, 2010-15(E), Mn

7.9

45.4

41.8%

Source: Bank Indonesia

10

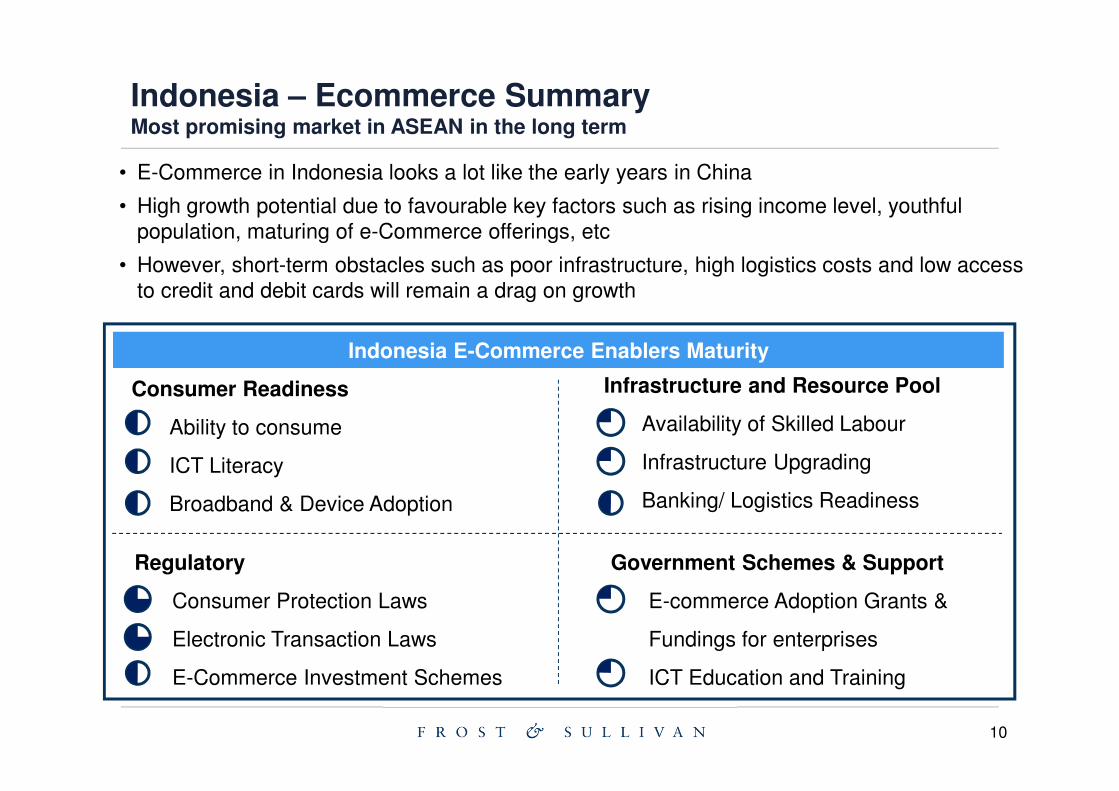

Indonesia – Ecommerce Summary Most promising market in ASEAN in the long term

• E-Commerce in Indonesia looks a lot like the early years in China

• High growth potential due to favourable key factors such as rising income level, youthful population, maturing of e-Commerce offerings, etc

• However, short-term obstacles such as poor infrastructure, high logistics costs and low access to credit and debit cards will remain a drag on growth

Indonesia E-Commerce Enablers Maturity

Infrastructure and Resource Pool

� Availability of Skilled Labour

� Infrastructure Upgrading

� Banking/ Logistics Readiness

Regulatory

� Consumer Protection Laws

� Electronic Transaction Laws

� E-Commerce Investment Schemes

Consumer Readiness

� Ability to consume

� ICT Literacy

� Broadband & Device Adoption

Government Schemes & Support

� E-commerce Adoption Grants &

Fundings for enterprises

� ICT Education and Training

11

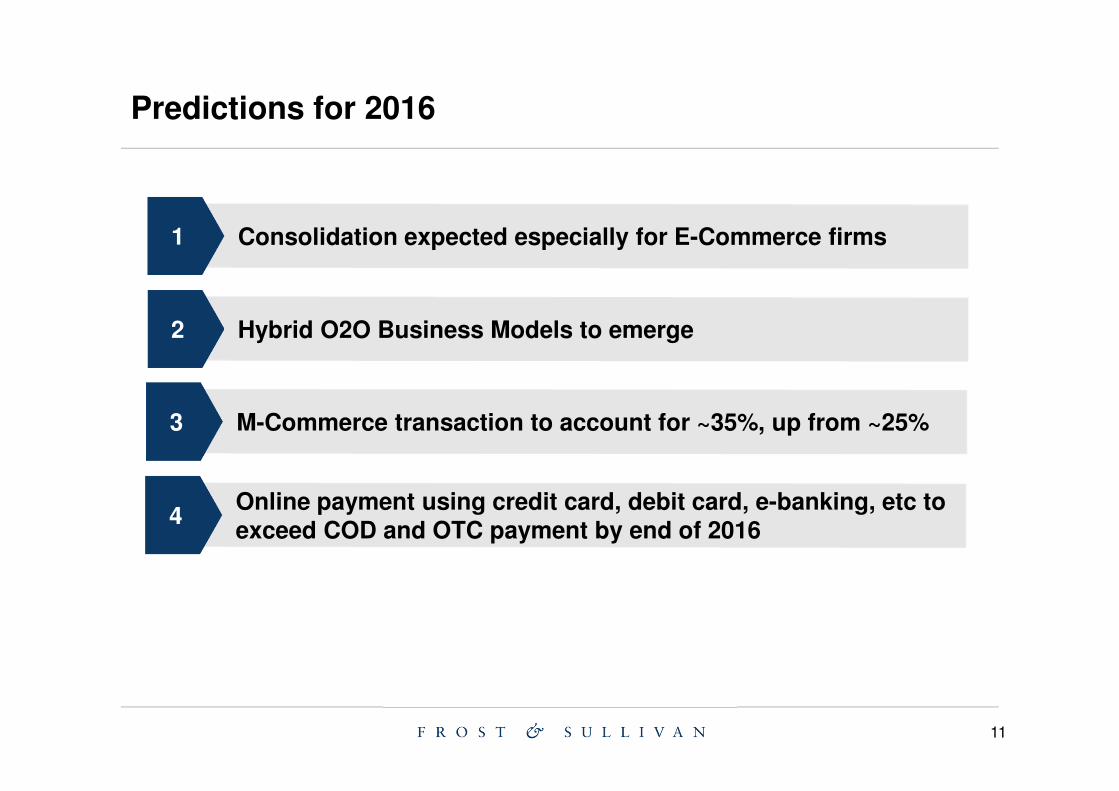

Predictions for 2016

Consolidation expected especially for E-Commerce firms1

Hybrid O2O Business Models to emerge2

M-Commerce transaction to account for ~35%, up from ~25% 3

Online payment using credit card, debit card, e-banking, etc to exceed COD and OTC payment by end of 2016

4

12

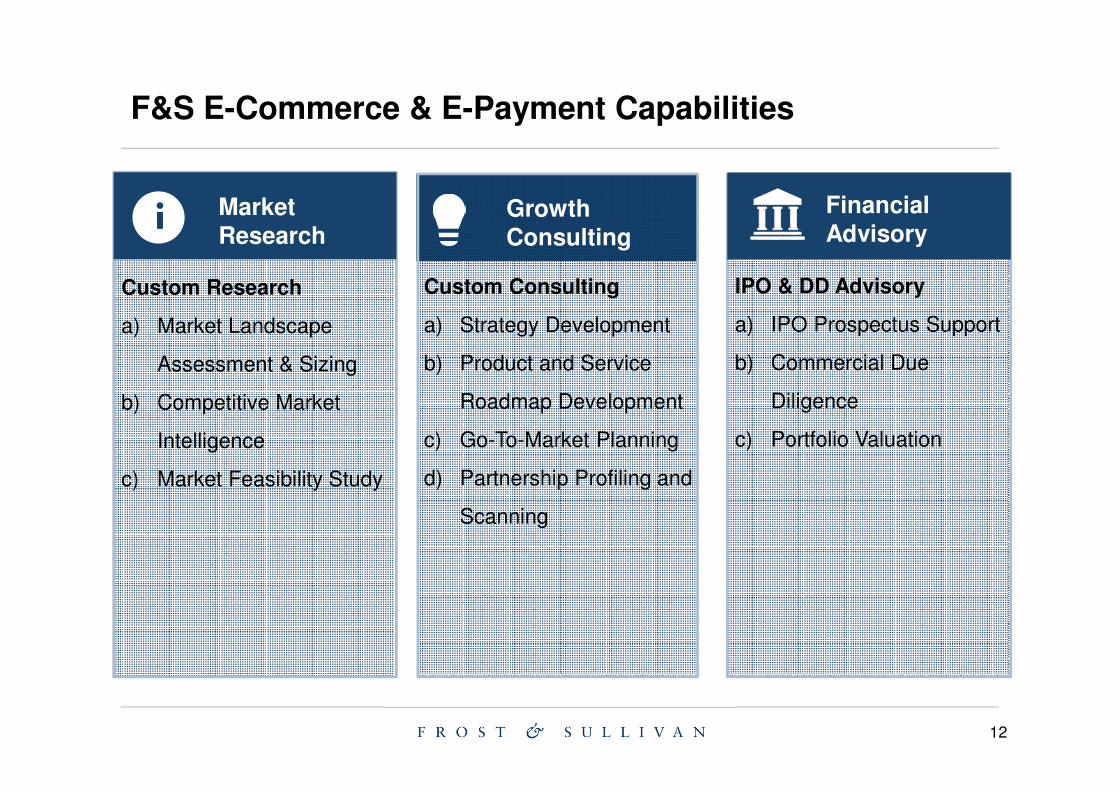

F&S E-Commerce & E-Payment Capabilities

Custom Research

a) Market Landscape

Assessment & Sizing

b) Competitive Market

Intelligence

c) Market Feasibility Study

i

IPO & DD Advisory

a) IPO Prospectus Support

b) Commercial Due

Diligence

c) Portfolio Valuation

Custom Consulting

a) Strategy Development

b) Product and Service

Roadmap Development

c) Go-To-Market Planning

d) Partnership Profiling and

Scanning

Market Research

Growth Consulting

Financial Advisory

13

Thank You

All Rights Reserved, Copyright ©