Embed Size (px)

Citation preview

Tax Amnesty A Breakthrough in Indonesia Current Budget

1

Presented by: Kurnia Chairi Deputy of Macroeconomic and State Revenue Anaysis, DG Budget

2

Recent Macroeconomic dan Budget Posture

Tax Amnesty as A Breakthrough

3

Recent Macroeconomic dan Budget Posture

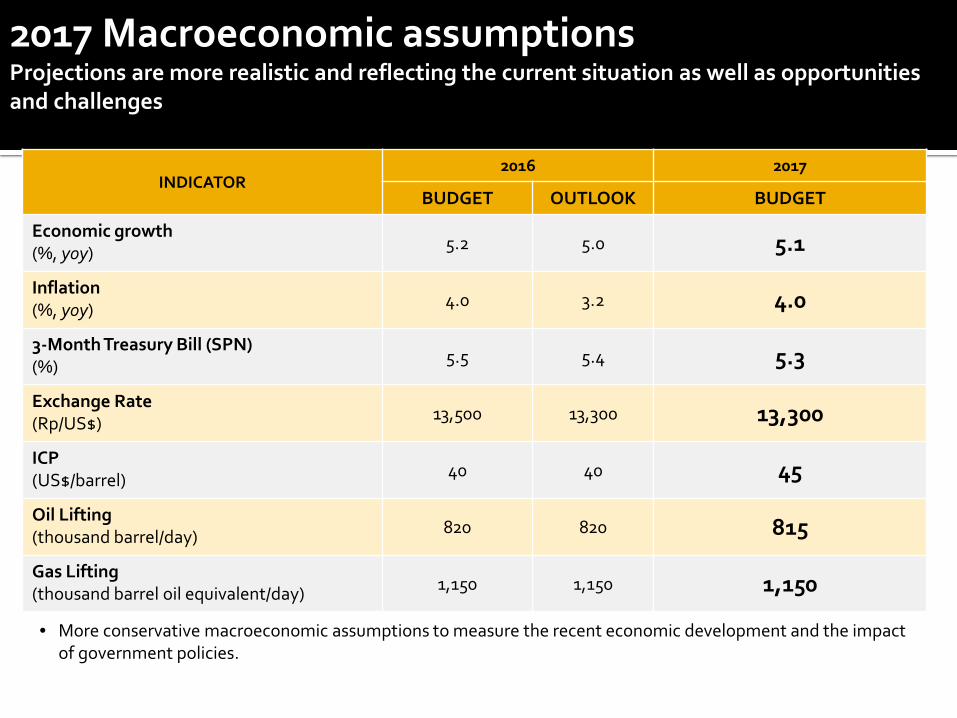

2017 Macroeconomic assumptions Projections are more realistic and reflecting the current situation as well as opportunities and challenges

Sumber: Kementerian Keuangan

INDICATOR 2016 2017

BUDGET OUTLOOK BUDGET

Economic growth (%, yoy) 5.2 5.0 5.1

Inflation (%, yoy) 4.0 3.2 4.0

3-Month Treasury Bill (SPN) (%) 5.5 5.4 5.3

Exchange Rate (Rp/US$) 13,500 13,300 13,300

ICP (US$/barrel) 40 40 45

Oil Lifting (thousand barrel/day) 820 820 815

Gas Lifting (thousand barrel oil equivalent/day) 1,150 1,150 1,150

• More conservative macroeconomic assumptions to measure the recent economic development and the impact of government policies.

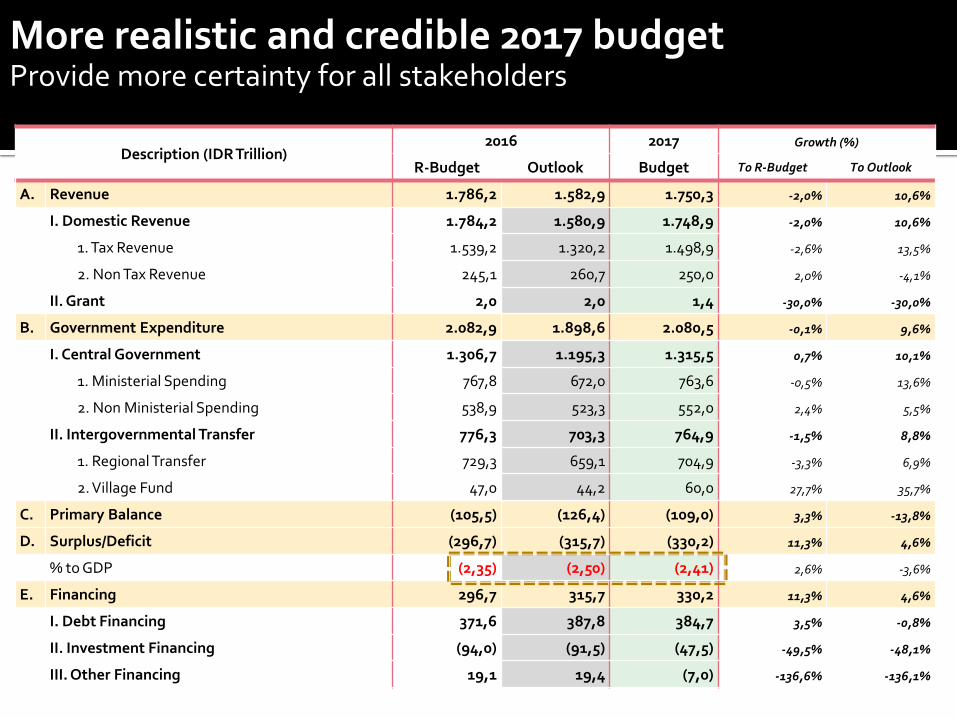

More realistic and credible 2017 budget Provide more certainty for all stakeholders

Description (IDR Trillion) 2016 2017 Growth (%)

R-Budget Outlook Budget To R-Budget To Outlook

A. Revenue 1.786,2 1.582,9 1.750,3 -2,0% 10,6%

I. Domestic Revenue 1.784,2 1.580,9 1.748,9 -2,0% 10,6%

1. Tax Revenue 1.539,2 1.320,2 1.498,9 -2,6% 13,5%

2. Non Tax Revenue 245,1 260,7 250,0 2,0% -4,1%

II. Grant 2,0 2,0 1,4 -30,0% -30,0%

B. Government Expenditure 2.082,9 1.898,6 2.080,5 -0,1% 9,6%

I. Central Government 1.306,7 1.195,3 1.315,5 0,7% 10,1%

1. Ministerial Spending 767,8 672,0 763,6 -0,5% 13,6%

2. Non Ministerial Spending 538,9 523,3 552,0 2,4% 5,5%

II. Intergovernmental Transfer 776,3 703,3 764,9 -1,5% 8,8%

1. Regional Transfer 729,3 659,1 704,9 -3,3% 6,9%

2. Village Fund 47,0 44,2 60,0 27,7% 35,7%

C. Primary Balance (105,5) (126,4) (109,0) 3,3% -13,8%

D. Surplus/Deficit (296,7) (315,7) (330,2) 11,3% 4,6%

% to GDP (2,35) (2,50) (2,41) 2,6% -3,6%

E. Financing 296,7 315,7 330,2 11,3% 4,6%

I. Debt Financing 371,6 387,8 384,7 3,5% -0,8%

II. Investment Financing (94,0) (91,5) (47,5) -49,5% -48,1%

III. Other Financing 19,1 19,4 (7,0) -136,6% -136,1%

416.1

104.0

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

450.0

2011 2012 2013 2014 2015 2016 2017

6

Major current Budget Reform … effective and sustainable budget

Pendidikan

Infrastruktur

Subsidi Energi

Kesehatan

Rp. Triliun

77,3

387,7

Subsidy Reform : Tax Reform :

•More realistic target •Increase tax base by Tax Amnesty

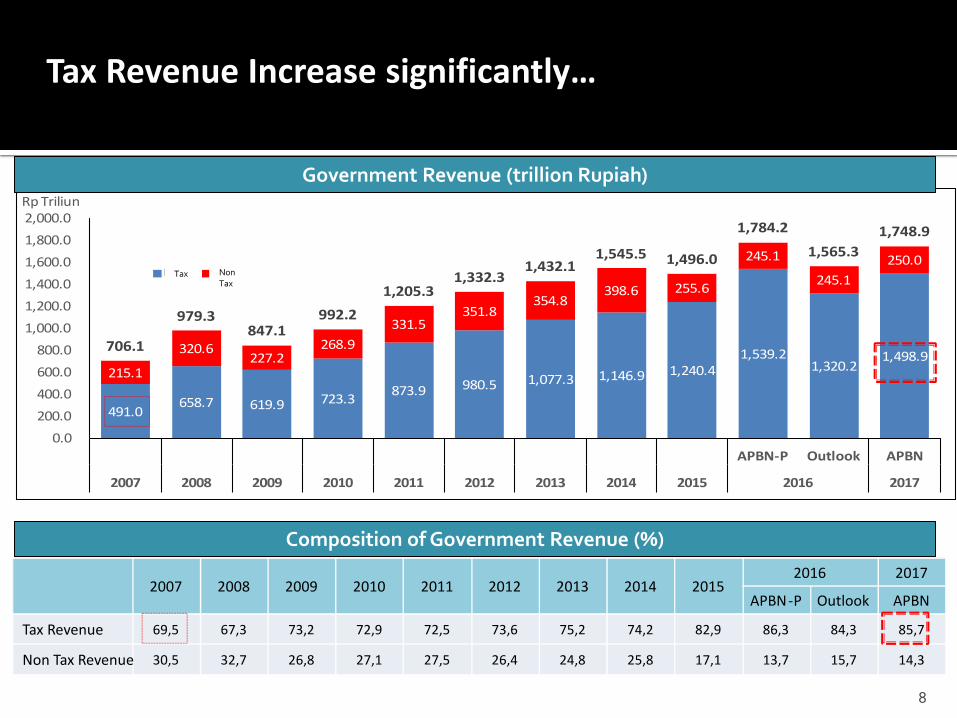

Tax Revenue increases 13.5% from 2016 Outlook

7

Tax Amnesty as A Breakthrough

491.0 658.7 619.9 723.3 873.9 980.5 1,077.3 1,146.9 1,240.4

1,539.2 1,320.2

1,498.9 215.1

320.6 227.2

268.9 331.5

351.8 354.8

398.6 255.6

245.1

245.1 250.0

706.1

979.3847.1

992.21,205.3

1,332.31,432.1

1,545.5 1,496.0

1,784.2

1,565.31,748.9

0.0 200.0 400.0 600.0 800.0

1,000.0 1,200.0 1,400.0 1,600.0 1,800.0 2,000.0

APBN-P Outlook APBN

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Rp Triliun

Pajak PNBP Series3

Composition of Government Revenue (%)

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

APBN - P Outlook APBN

Tax Revenue 69,5 67,3 73,2 72,9 72,5 73,6 75,2 74,2 82,9 86,3 84,3 85,7

Non Tax Revenue 30,5 32,7 26,8 27,1 27,5 26,4 24,8 25,8 17,1 13,7 15,7 14,3

Government Revenue (trillion Rupiah)

Tax Non Tax

Tax Revenue Increase significantly…

8

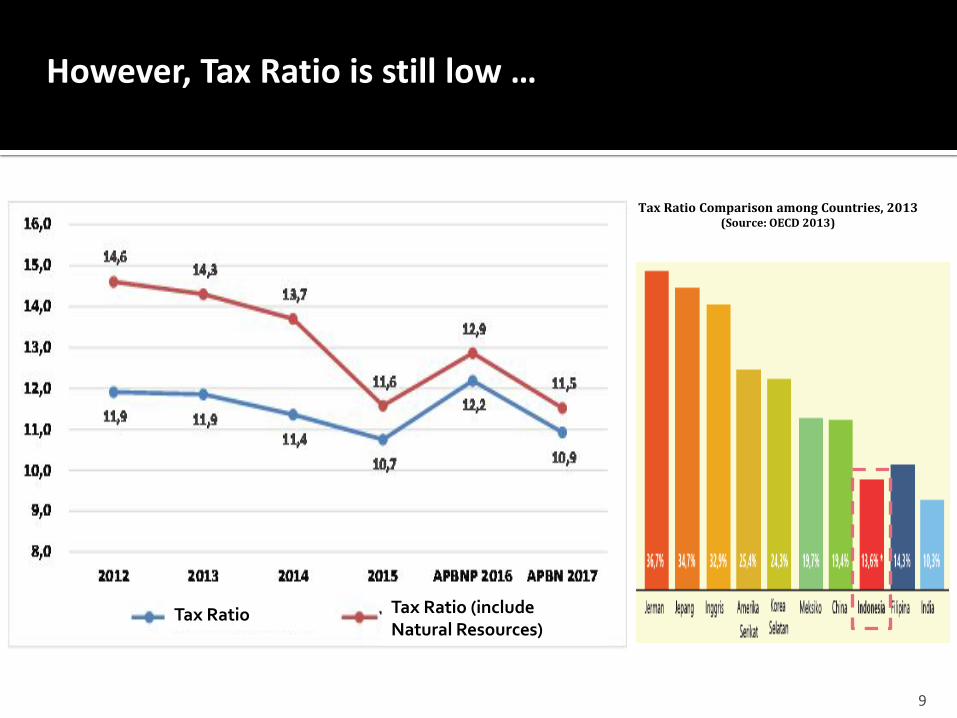

However, Tax Ratio is still low …

Tax Ratio Tax Ratio (include Natural Resources)

9

Tax Ratio Comparison among Countries, 2013 (Source: OECD 2013)

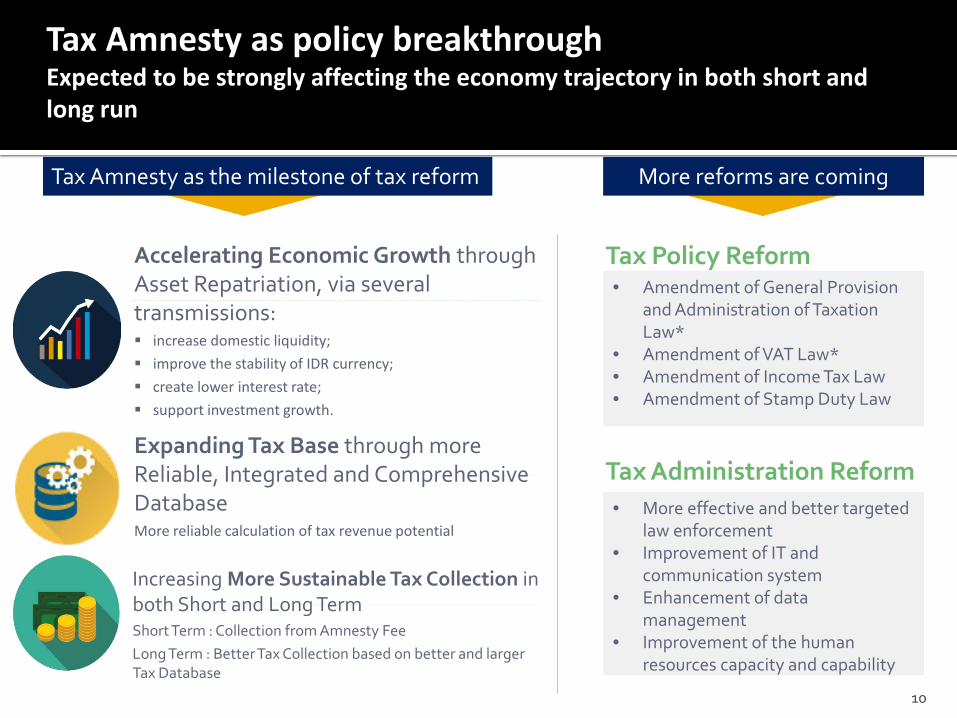

Tax Amnesty as policy breakthrough Expected to be strongly affecting the economy trajectory in both short and long run

Accelerating Economic Growth through Asset Repatriation, via several transmissions: increase domestic liquidity; improve the stability of IDR currency; create lower interest rate; support investment growth.

Expanding Tax Base through more Reliable, Integrated and Comprehensive Database More reliable calculation of tax revenue potential

Increasing More Sustainable Tax Collection in both Short and Long Term Short Term : Collection from Amnesty Fee Long Term : Better Tax Collection based on better and larger Tax Database

Tax Policy Reform

Tax Administration Reform • More effective and better targeted

law enforcement • Improvement of IT and

communication system • Enhancement of data

management • Improvement of the human

resources capacity and capability

• Amendment of General Provision and Administration of Taxation Law*

• Amendment of VAT Law* • Amendment of Income Tax Law • Amendment of Stamp Duty Law

Tax Amnesty as the milestone of tax reform More reforms are coming

10

11

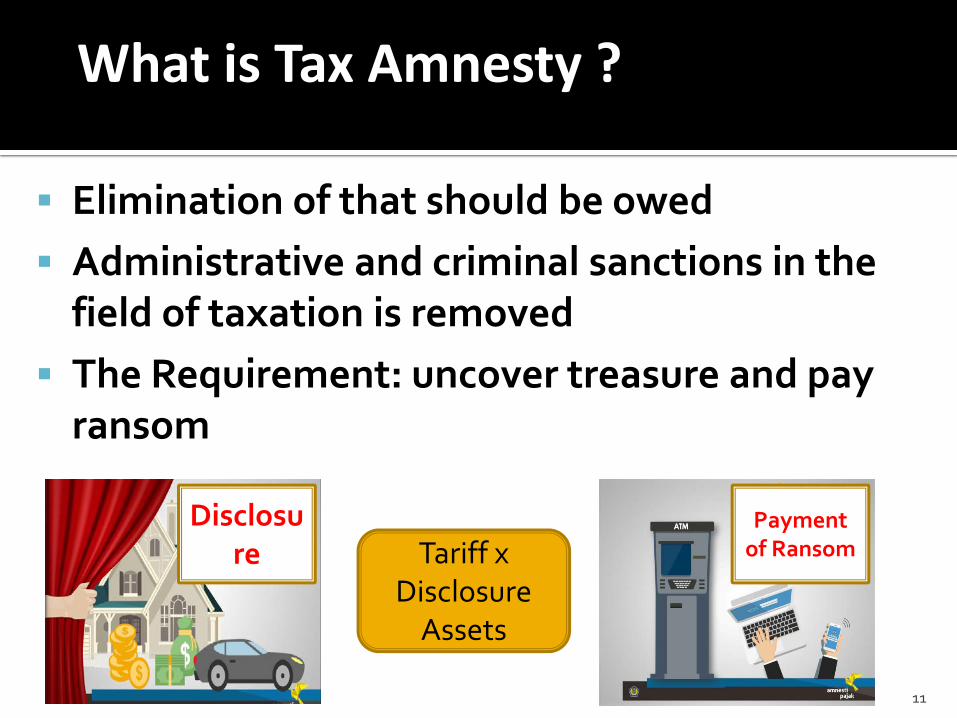

Elimination of that should be owed Administrative and criminal sanctions in the

field of taxation is removed The Requirement: uncover treasure and pay

ransom

What is Tax Amnesty ?

Disclosure

Payment of Ransom Tariff x

Disclosure Assets

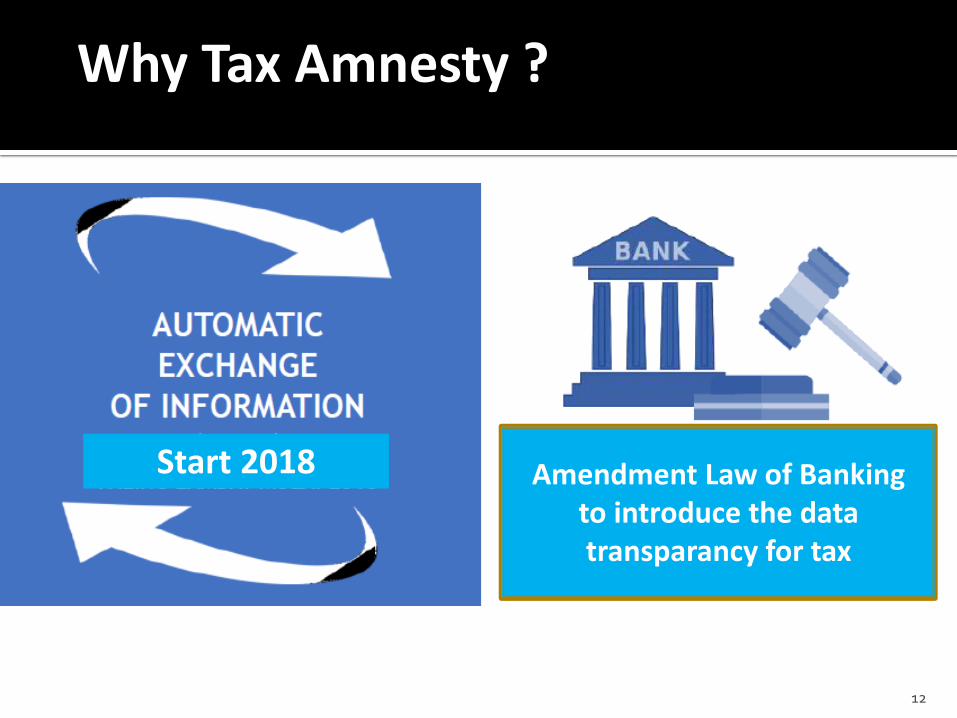

Why Tax Amnesty ?

Start 2018 Amendment Law of Banking to introduce the data transparancy for tax

12

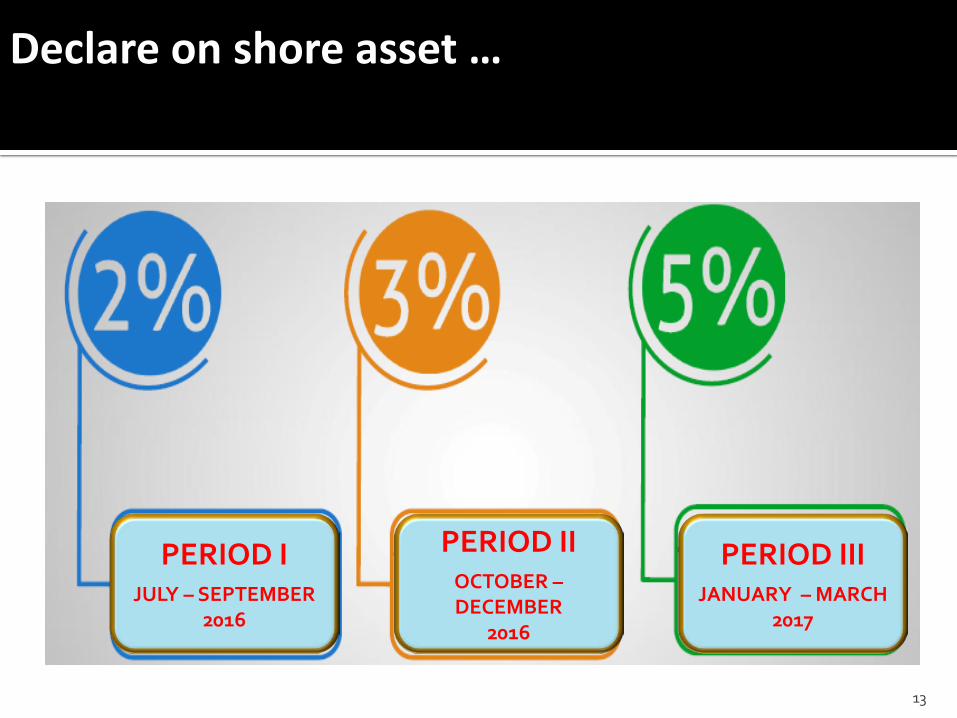

Declare on shore asset …

13

PERIOD I JULY – SEPTEMBER

2016

PERIOD II OCTOBER – DECEMBER

2016

PERIOD III JANUARY – MARCH

2017

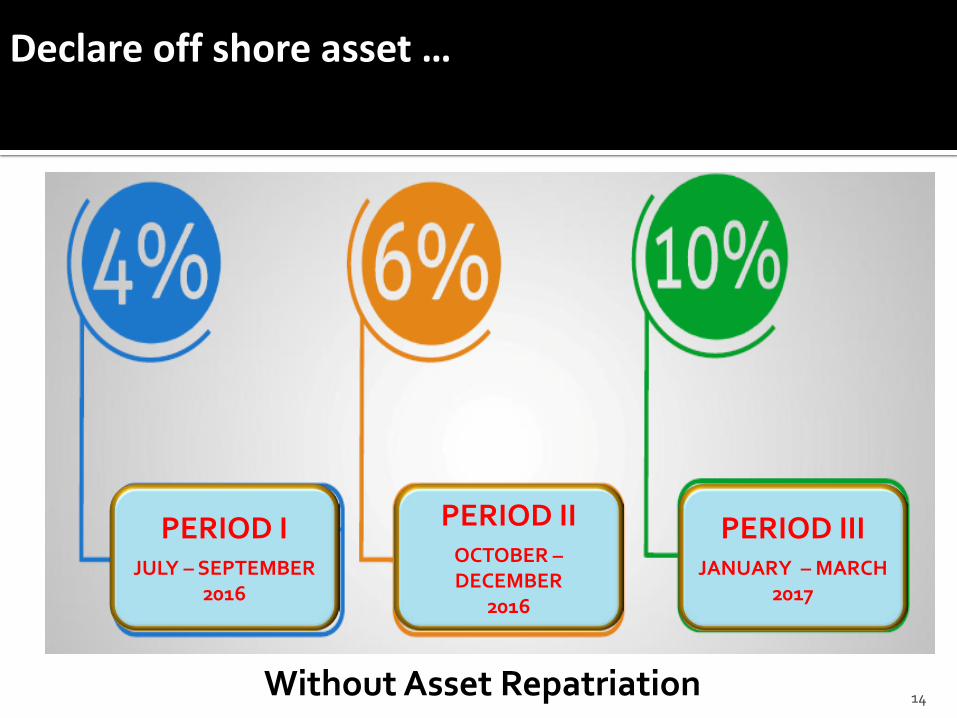

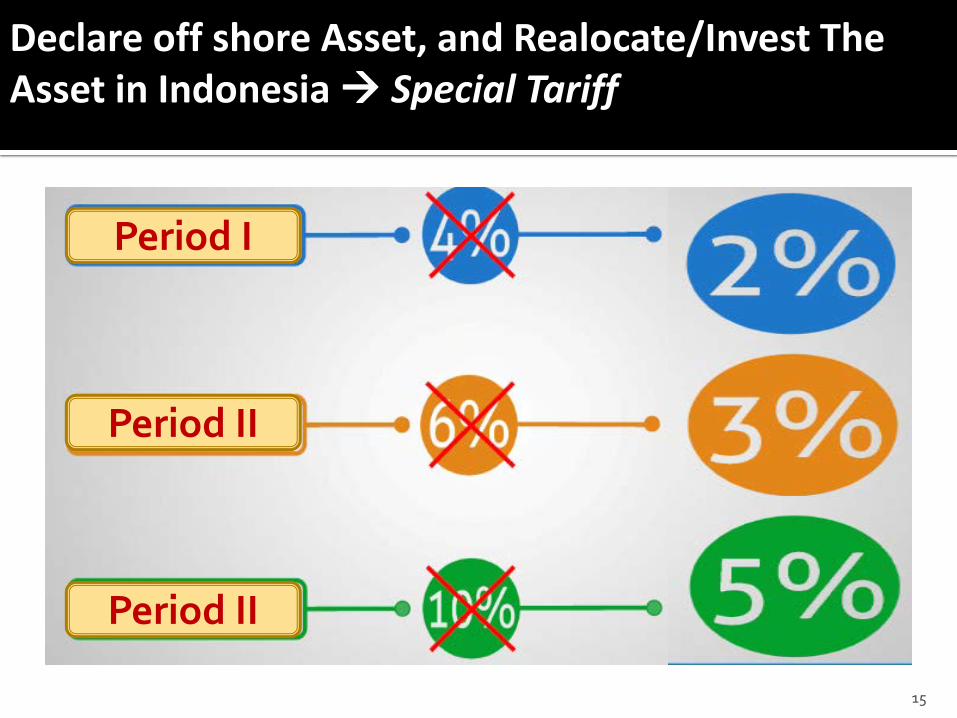

Declare off shore asset …

Without Asset Repatriation 14

PERIOD I JULY – SEPTEMBER

2016

PERIOD II OCTOBER – DECEMBER

2016

PERIOD III JANUARY – MARCH

2017

Declare off shore Asset, and Realocate/Invest The Asset in Indonesia Special Tariff

15

Period I

Period II

Period II

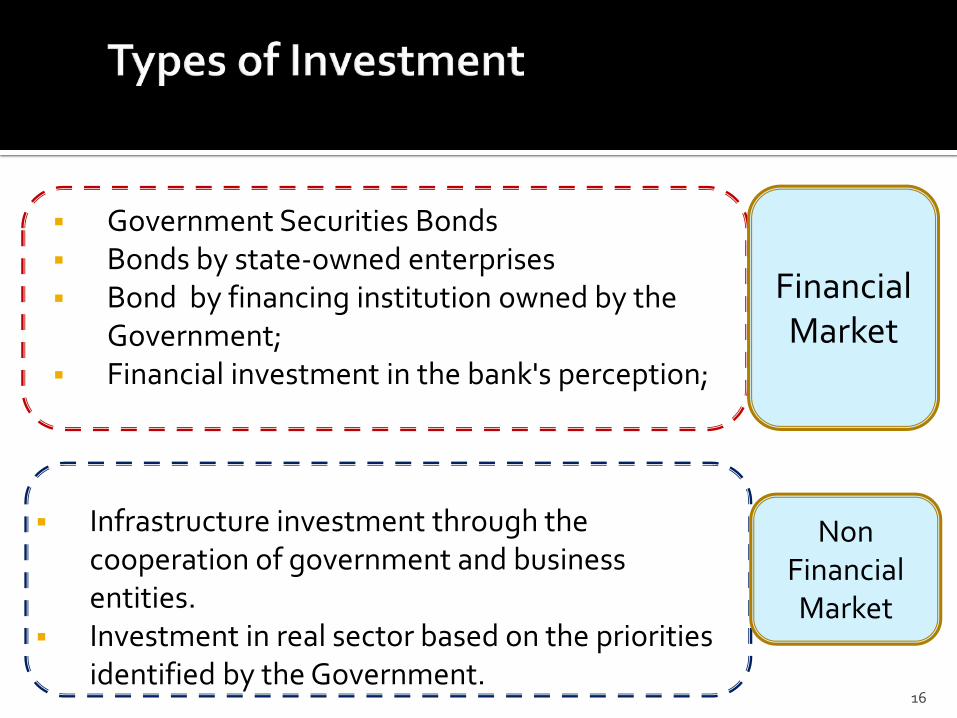

Government Securities Bonds Bonds by state-owned enterprises Bond by financing institution owned by the

Government; Financial investment in the bank's perception;

16

Financial Market

Non Financial Market

Infrastructure investment through the cooperation of government and business entities.

Investment in real sector based on the priorities identified by the Government.

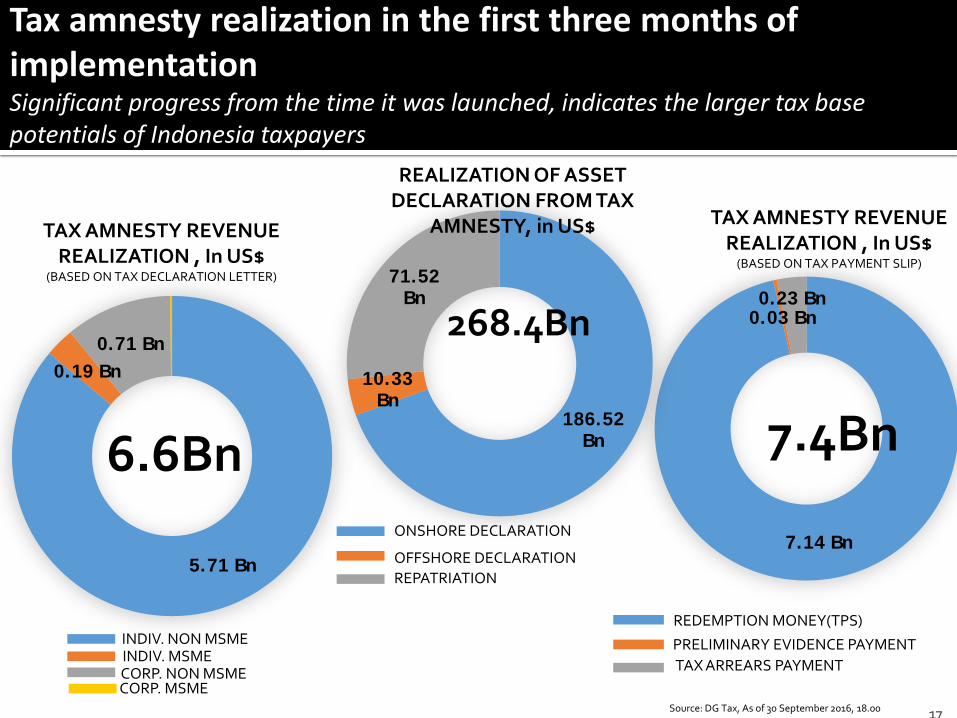

Tax amnesty realization in the first three months of implementation Significant progress from the time it was launched, indicates the larger tax base potentials of Indonesia taxpayers

17

TAX AMNESTY REVENUE REALIZATION , In US$

(BASED ON TAX PAYMENT SLIP)

TAX AMNESTY REVENUE REALIZATION , In US$

(BASED ON TAX DECLARATION LETTER)

7.14 Bn

0.03 Bn 0.23 Bn

7.4Bn

REDEMPTION MONEY(TPS)

PRELIMINARY EVIDENCE PAYMENT TAX ARREARS PAYMENT

186.52 Bn

10.33 Bn

71.52 Bn

268.4Bn

ONSHORE DECLARATION

OFFSHORE DECLARATION REPATRIATION

5.71 Bn

0.19 Bn 0.71 Bn

6.6Bn

INDIV. NON MSME INDIV. MSME CORP. NON MSME CORP. MSME

REALIZATION OF ASSET DECLARATION FROM TAX

AMNESTY, in US$

Source: DG Tax, As of 30 September 2016, 18.00

18

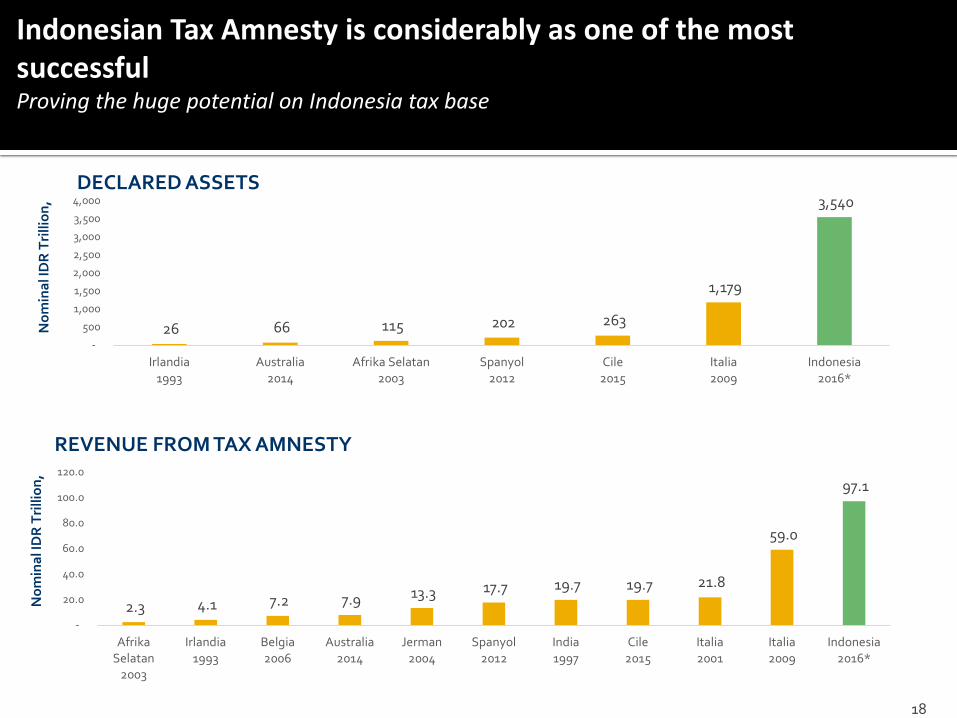

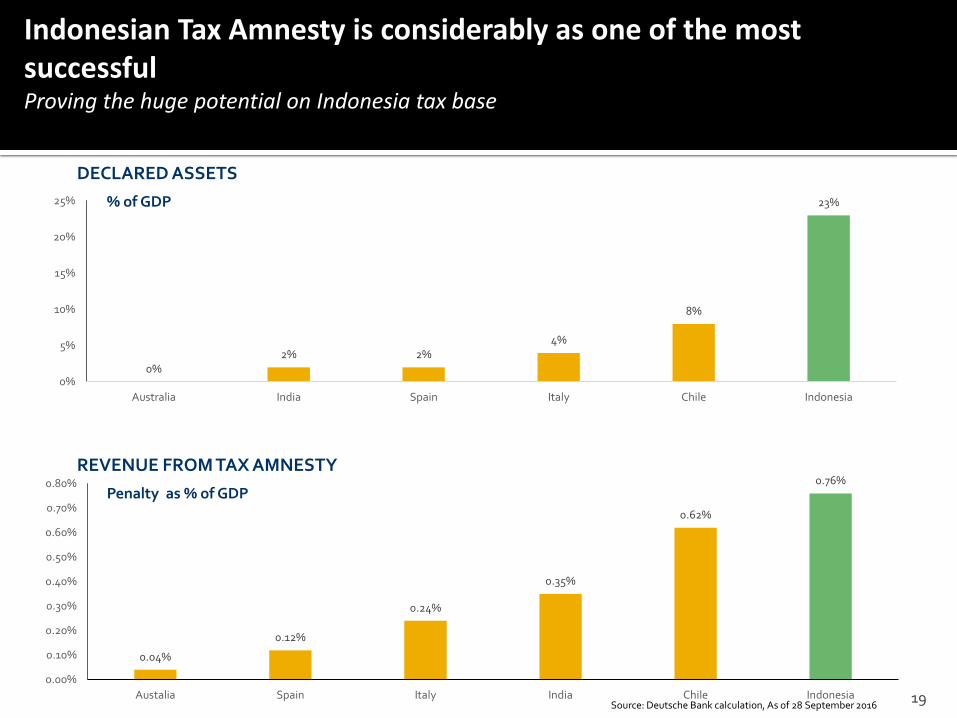

Indonesian Tax Amnesty is considerably as one of the most successful Proving the huge potential on Indonesia tax base

DECLARED ASSETS

REVENUE FROM TAX AMNESTY

26 66 115 202 263

1,179

3,540

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Irlandia1993

Australia2014

Afrika Selatan2003

Spanyol2012

Cile2015

Italia2009

Indonesia2016*

2.3 4.1 7.2 7.9 13.3 17.7 19.7 19.7 21.8

59.0

97.1

-

20.0

40.0

60.0

80.0

100.0

120.0

AfrikaSelatan

2003

Irlandia1993

Belgia2006

Australia2014

Jerman2004

Spanyol2012

India1997

Cile2015

Italia2001

Italia2009

Indonesia2016*

Nom

inal

IDR

Tri

llion

, N

omin

al ID

R T

rilli

on,

0.04%

0.12%

0.24%

0.35%

0.62%

0.76%

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

0.60%

0.70%

0.80%

Austalia Spain Italy India Chile Indonesia

0% 2% 2%

4%

8%

23%

0%

5%

10%

15%

20%

25%

Australia India Spain Italy Chile Indonesia

DECLARED ASSETS

REVENUE FROM TAX AMNESTY

Indonesian Tax Amnesty is considerably as one of the most successful Proving the huge potential on Indonesia tax base

Source: Deutsche Bank calculation, As of 28 September 2016

% of GDP

Penalty as % of GDP

19

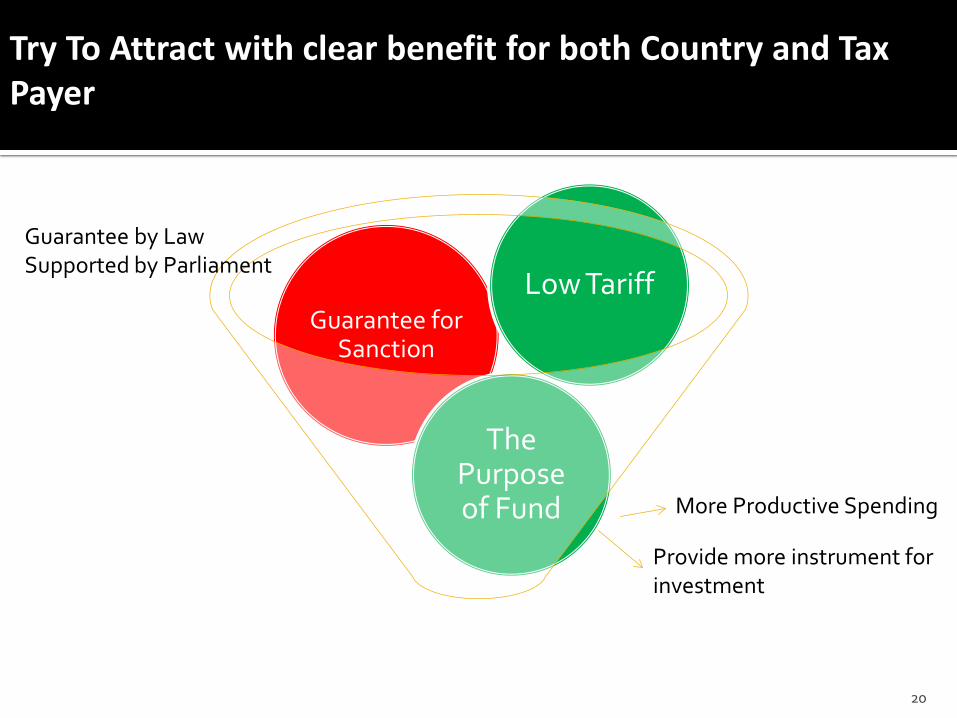

Guarantee for Sanction

Try To Attract with clear benefit for both Country and Tax Payer

Low Tariff

The Purpose of Fund

20

More Productive Spending

Guarantee by Law Supported by Parliament

Provide more instrument for investment

21

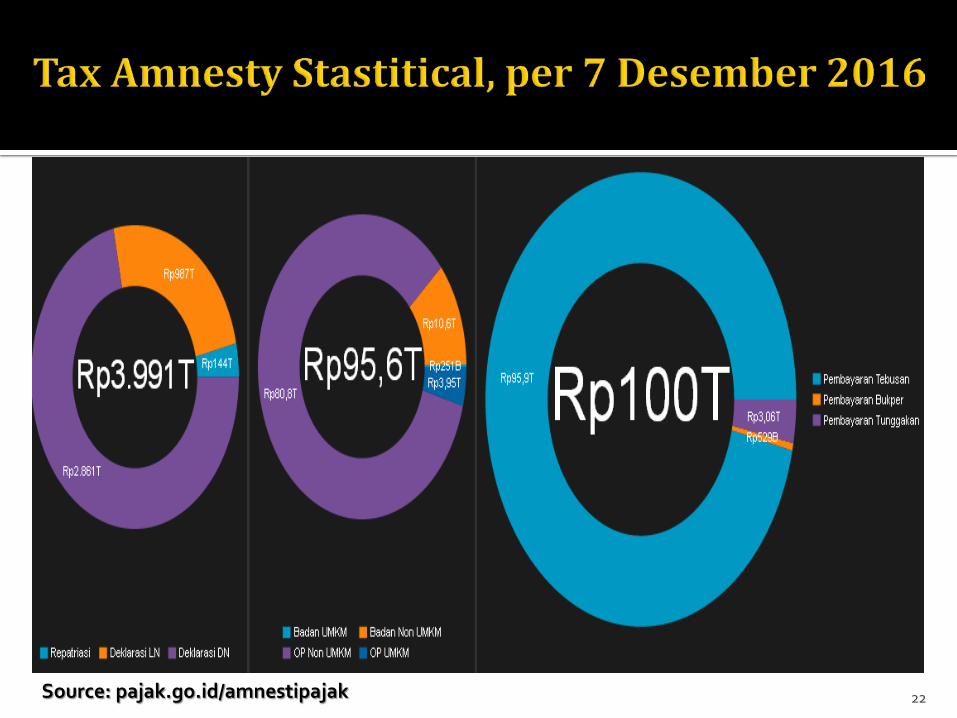

Source: pajak.go.id/amnestipajak 22